Shariah Guidelines for Sukuk. Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014

|

|

|

- Maximilian Tyler

- 6 years ago

- Views:

Transcription

1 Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October

2 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail Ebrahim [3] Shari ah Advisory Services Mufti Ismail Ebrahim [5] Introduction to Sukuk Introduction to Sukuk [7] General and Specific Shariah Guidelines [8] Sukuk Vs. Conventional Bond Instruments (10) Sukuk Structures and Examples Musharakah [13] Ijarah [16] Wakalah [20] Shariah Compliance: Contemporary Issues (23) 1

3 Credentials Mufti Ismail Ebrahim Shariah Advisor: Ethica Institute of Islamic Finance, Dubai (Shariah Education and Advisory) Infinity Consultants, India (Shariah Consultancy Practice) Al-Mabroor Investments, RSA (Shariah Compliant Investment Vehicle) Jenuard AG, Austria (Shariah Investment Vehicle) IFSCAR, Trinidad and Tobago (Shariah Advisory) PSG Investment Bank, RSA (Shariah Wealth Management) Centre for Advanced Islamic Economics, Pakistan (Shariah Education and Advisory) Shariah Review Bureaux, Bahrain (Shariah Advisory) Lishui Prefecture Municipality, Peoples Republic of China (Shariah Advisory) Advisor to Governments and Central Banks on Islamic Finance Executive Director and Shariah Advisor, Russian Islamic Finance Council (Shariah Advisory and Fatawa) 2

4 Islamic Financial Services Products Mufti Ismail Ebrahim 1.Advised and developed several Shariah Compliant Real Estate and Asset Management Funds Worldwide 2.Developed first Domestic Shariah Compliant Sukuk for South African Market 3.Issued hundreds of Fatawa (Islamic Legal Edicts) on Islamic Finance and Economics 4.Developed Shariah Wealth Management Products for leading investment bank in South Africa 5.Conducted Shariah training for hundreds of bankers and financial professionals in the GCC and beyond 6.Advising the Chinese Government on Shariah Compliant Energy Project worth $150 Million 7.Advising South American Government on Sukuk 8.Conducted annual Shariah Compliance review and audit for leading Shariah Compliant Investment Firm in South Africa 3

5 Islamic Financial Services Products Mufti Ismail Ebrahim 9.Advised Government and central Banks on Shariah Regulations and Guidelines for Islamic Finance 10.Advised and executed Shariah Compliant Trade Finance transactions worth more than $300 Million 11.Advising leading Turkish Bank on setting up Shariah Compliant Window 12.Developed first ever Shariah Compliant asset management company in Austria 13.Advising major European religious agency on Islamic Finance 4

6 Shari ah Auditing and Advisory Services Mufti Ismail Ebrahim Shariah Product Development Fatāwā and Certification. Sharīàh Review Sharīàh Audit and Assurance Shariah Mediation and Arbitration Islamic Private Wealth Management Shariah Board Development Islamic Finance Training and Human Capital Development Central Bank Regulatory Assistance Sukuk and Islamic Fund Structuring Islamic Finance Knowledge and Research 5

7 Embracing Islamic Finance through Shariah Compliance, achieving new heights in expansion and growth 6

8 Introduction to Sukuk Sukuk are certificated Shariah Compliant financial instruments. Sukuk always linked to underlying assets representing partial ownership in the asset. Usually translated as Islamic bond and is the most active Islamic debt market instruments. Derived from the Arabic word Sakk (Plural: Sukuk) Islamic Financial Services Board (IFSB-2) definition: Certificates that represent the holder s proportionate ownership in an undivided part of the underlying asset, where the holder assumes all rights and obligations to such asset. Benefits and objectives of Sukuk: Expansion of investor base, liquidity for secondary capital market, raising Shariah Compliant funding, Shariah Compliant investment opportunities, Shariah balance sheet management and tradability Sukuk Holders are exposed to asset level risks and the Sukuk income is based on asset ownership and not revenue rights 7

9 General Shariah Guidelines 1.All transactions must conform with Islamic Law (Shari ah) 2.Prohibition of interest (riba) but 3.trading between parties is acceptable 4.Prohibition of speculation (maysir) 5.Avoidance of uncertain or excessively risky transactions (gharar) 6.Prohibition of investment in unlawful goods and services (e.g. pork, alcohol, gambling) 7.Sharing of risk between parties 8

10 Specific Sukuk Shariah Guidelines 1. Funds raised must be used for Shariah compliant activities. 2. All funds raised may be used to finance tangible assets. Specificity of assets is important, since Sukuk unlike conventional bonds cannot be used for general financial needs of the issuer. Non-tangible assets may be used based on Urf and Aaadah subject to Shariah Board approval. 3. Income received by sukuk holders (investors) must be derived from the direct cash flows generated by the underlying assets. 4. Sukuk holders have a right to the ownership of the underlying asset and its cash-flows. 5. Clear and transparent specification of rights and obligations of all parties to the transaction, in particular the originator (customer) and sukuk holders. 6. No fixity in returns and no financial guarantees. 7. Generic Shariah Compliant screening. 9

11 Specific Sukuk Shariah Guidelines 8. All the rules of original contract on the basis of which Sukuk are created should be applied. 9. The issuer cannot guarantee the face value of the certificate for the holder except in case of negligence/misconduct. 10. In Sukuk based on sale and lease back, the issuer can unilaterally undertake that he will purchase the asset after one year for a pre-agreed price. 11. Different types of reserves (e.g. profit equalization reserve) or takaful pool can be created. 12. Only those Sukuk can be traded that represent proportionate ownership of tangible assets, usufructs or services. 13. In Sukuk of Musharakah/Mudarabah, the issuer can redeem the certificates on the market price. Purchase undertaking is allowed however the purchase price should be market value of the underlying assets. 10

12 Sukuk Vs. Conventional Bond Instruments Sukuk: Conventional Debt Instruments: Each Sukuk unit represents an ownership of the underlying asset; Maturity of the Sukuk corresponds to the term of the underlying project or activity; The Sukuk prospectus contains all the Shariah rules related to the issue; The underlying asset / project / business has to be Shariah complaint (i.e. not dealing with pork related items, gambling, tobacco, institutions that deal with Riba (interest) etc.); and The Sukuk manager is required to abide by Shariah rules The Sukuk holders have the rights to profits but also bear losses Bonds represent pure debt obligations due from the issuer; The core relationship is a loan of money, which implies a contract whose subject is purely earning money on money; The issue prospectus does not include Shariah constraints; and The underlying asset / project / business can belong to any sector / industry Can be issued to finance almost any purpose which is legal in its jurisdiction. Bond holders are not exposed to losses on the asset although they might bear losses in the event of insolvency by the issuer. 11

13 Sukuk Structures Musharakah Sukuk: Issued with the aim of using the mobilized funds for establishing a new project, developing an existing project or financing a business activity on the basis of any of partnership contracts. Participation Certificates represent projects or activities managed on the basis of Musharaka. Mudaraba Sukuk represent projects or activities managed on the basis of Mudaraba. Investment Agency Sukuk represent projects or activities managed on the basis of an investment agency by appointing an agent to manage the operation. Murabaha Sukuk: Issued for the purpose of financing the purchase of goods through Murabaha so that Sukuk holders become the owners of Murabaha Commodity 12

14 Sukuk Structures Salam Sukuk Issued for the purpose of mobilizing funds so that the goods to be delivered on the basis of salam come to be owned by the Sukuk holders Istisna Sukuk Issued for the purpose of mobilizing funds to be employed for the production of goods so that the goods produced come to be owned by the Sukuk holders Muzara ah (sharecropping) / Musaqa (irrigation) Sukuk Issued for the purpose of using the mobilized funds for financing a project so that Sukuk holders become entitled to a share in the crop as per the agreement. Mugharasa (agricultural) Sukuk Issued for the purpose of mobilizing funds so that Sukuk holders become entitled to a share in the land and plantation. 13

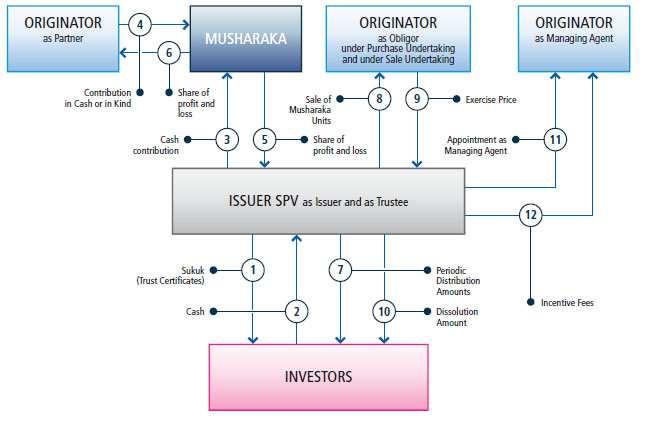

15 Sukuk Examples and Shariah Guidelines: Musharakah Musharakah is a mode of financing which can be securitized easily especially in the case of large projects where huge amounts are required. An SPV is formed to collect funds from the Islamic investors, acquire assets and serve as partner in the Musharakah agreement on behalf of the Islamic investors. The obligor serves as Musharik and is typically appointed the management agent of the Musharakah project. Every subscriber is given a Musharakah certificate, which represents his proportionate ownership in the assets of the Musharakah. After the project is started, these Musharakah certificates can be treated as negotiable instruments. Certificates can be bought and sold in the secondary capital market. Securitization of Musharakah can be used for: Construction of projects and factories, expansion Projects, working capital finance 14

16 Musharakah Sukuk 15

17 Musharakah Sukuk Shariah Guidelines Profit earned by the Musharakah is shared according to an agreed ratio. Loss is shared on pro rata basis. All the assets of the Musharakah should not be in liquid form. Portfolio of Musharakah should consist of non-liquid assets valuing more than 33% of its total worth. However, if the Hanafi view is adopted, trading will be allowed even if the non-liquid assets are less than 33% but the size of the non-liquid assets should not be negligible. Whenever there is a combination of liquid and non-liquid assets, it can be sold and purchased for an amount greater than the amount of liquid assets in combination. Bilateral undertaking (Wa d Mulzim) is not permissible in Shariah. However unilateral undertaking (Wa d Ghair Mulzim) is permitted. Guaranteed fixed returns are not permitted as this constitutes Riba (interest). 16

18 Sukuk Ijarah Sukuk Ijarah are title deeds of equal shares in a leasing project giving their holders the right to hold shares, receive rental payments and dispose of their assets/properties. Ijarah certificates are tradable on the secondary markets. The lessor (owner) can sell the leased asset wholly or partly either to one party or to a number of individuals to recover his cost of purchase of the asset with a profit thereon. This purchase of a proportion of the asset by each individual may be evidenced by a certificate, which may be called 'Ijarah certificate. The Ijarah certificate represents the holder's proportionate ownership in the leased asset. The holder will assume the rights and obligations of the owner/lessor to the extent of his ownership. The holder will have the right to enjoy a part of the rent according to his proportion of ownership in the asset. In the case of total destruction of the asset, he will suffer the loss to the extent of his ownership. These certificates can be negotiated and traded freely in the market and can serve as an instrument easily convertible into cash. 17

19 Sukuk Ijarah 18

20 Shariah Guidelines: Sukuk Ijarah The rental payments maybe structured such that it comprises of (i) profits on the rental and (ii) redemption amount on the principal. Rental payments cannot be guaranteed. Sukuk Ijarah does not represent debts; but undivided proportionate ownership of the leased asset (participatory certificates). Because the Sukuk Ijarah are not debts nor monetary, the issue of sale of monetary-debts with a discount do not arise. Hence Sukuk Ijarah may be traded in the secondary market freely. It is essential that the Ijarah certificates are designed to represent real ownership of the leased assets, and not only a right to receive rental payments. The Sukuk holders are responsible for major asset maintenance whereas the obligor (lessee) is responsible for ordinary maintenance. All contractual agreements should be separated and individualized. For example, sale and lease agreements should be separated. Conversion should be well defined. 19

21 Sukuk Wakalah Wakalah is an agreement whereby one party entrusts another to act on its behalf. Wakalah is akin to an agency agreement. A principal (the investor) appoints an agent (wakeel) to invest funds provided by the principal into a pool of investments or assets and the wakeel lends it expertise and manages those investments on behalf of the principal for a particular duration, in order to generate an agreed upon profit return. The Wakalah agreement will govern the scope of the services provided, remuneration and appointment term. There should be no ambiguity. The Wakalah portfolio assets should be Shariah Compliant and approved by the Shariah Supervisory Board. 20

22 Sukuk Wakalah 1/2.SPV/Issuer issues Sukuk to raise funds from investors. 3.SPV enters into a Wakala agreement with the Wakeel. 4/5.The Wakeel on behalf of the issuer will invest in assets. 6. Generation of profit and kept by Wakeel on behalf of the SPV. 7.Company makes periodic payments. 8.SPV distributes payments to investors 9.Obligor buys the assets from the Wakeel 10. SPV, in its capacity as Trustee, will pay the Dissolution Amount to investors 21

23 Sukuk Wakalah: Shariah Guidelines The scope of the wakala arrangement must be within the boundaries of Shari a i.e. the principal cannot require the wakeel to perform tasks that would not otherwise be Shari a compliant. The Wakalah Agreement must be clear and well defined. The scope of services provided, appointment term, duties, terms and conditions and fees payable should be well defined. Any ambiguity will render the agreement voidable. All portfolio assets should be screened and endorsed by the Shariah Supervisory Board. 22

24 Shariah Compliance: Contemporary Issues 1. Shariah Supervisory Boards should ensure the underlying structure, all financial documentation including prospectus and implementation of the transaction is Shariah Compliant. 2. The prospectus must mention the obligation to comply with all the guidelines and principles of Shariah as advised by the Shariah Supervisory Board. 3. All transactions should be separated and individualized. No bilateral agreements permitted in Shariah. 4. External Shariah Oversight Committee should be established to ensure optimal Shariah Governance. 5. Regular Shariah Audits should be conducted by external oversight committee. 23

25 Shariah Non- Compliance Shariah non-compliance risk very high due to several reasons including: Ambiguity in conversion process Conventional options Organized Tawarruq structures Commercial guarantees of cash flows and capital funds Conventional insurance Bilateral sale-lease back agreements Tradability of debt-receivable instruments Improper Shariah oversight and implementation Conventional funding placement No genuine risk sharing 24

26 What we do today will determine the success of the Islamic Finance Industry in the future. The sustainability of this industry is our responsibility. 25

27 Shukran And May God Bless! 26

28 Contact Details: Mufti Ismail Ebrahim Presenter s contact details: Mufti Ismail Ebahim Desai Executive Director : Russian Islamic Finance Council and Global Islamic Financial Services Firm +27 (31) (72) ismailebrahim7861@gmail.com/mufti@gifs.co.za/ceo@rifc.su The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. We will be pleased to provide definitive advice on request and following written acceptance of our standard terms and conditions. 27

Fixed Income Securities Shari a Perspective

SBP Research Bulletin Volume 3, Number 1, 2007 Fixed Income Securities Shari a Perspective Muhammad Imran Usmani 1. Introduction Fixed income securities have been popular around the world in raising finance

SBP Research Bulletin Volume 3, Number 1, 2007 Fixed Income Securities Shari a Perspective Muhammad Imran Usmani 1. Introduction Fixed income securities have been popular around the world in raising finance

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

J. P. M O R G A N I S L A M I C F I N A N C E

Islamic Finance Overview May 2014 S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L English_General 2013 JPMorgan Chase & Co. All rights reserved. These materials herein are provided for informational

Islamic Finance Overview May 2014 S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L English_General 2013 JPMorgan Chase & Co. All rights reserved. These materials herein are provided for informational

SUKUK Islamic Bonds. by Mr. Hamad Rasool.

SUKUK Islamic Bonds by Mr. Hamad Rasool 1 2 Sukuk is the Arabic name for a financial certificate, Islamic alternative to conventional bonds, Sukuk is a Trust certificate in which investor returns are derived

SUKUK Islamic Bonds by Mr. Hamad Rasool 1 2 Sukuk is the Arabic name for a financial certificate, Islamic alternative to conventional bonds, Sukuk is a Trust certificate in which investor returns are derived

Primer on Shariah Finance

INTERNATIONAL INSOLVENCY INSTITUTE 7 th Annual Conference Primer on Shariah Finance New York, NY June 11-12, 2007 Jonathan D. Strum, Esq. Primer on Shariah Finance Shariah is the legal framework that regulates

INTERNATIONAL INSOLVENCY INSTITUTE 7 th Annual Conference Primer on Shariah Finance New York, NY June 11-12, 2007 Jonathan D. Strum, Esq. Primer on Shariah Finance Shariah is the legal framework that regulates

Luxembourg A prime location for Sukuk issuance

Luxembourg A prime location for issuance Contents Islamic finance in Luxembourg listed in Luxembourg 5 Structuring transactions 6 al-ijara 8 Mixed-asset 9 al-musharaka 0 al-murabaha al-istisna al-salam

Luxembourg A prime location for issuance Contents Islamic finance in Luxembourg listed in Luxembourg 5 Structuring transactions 6 al-ijara 8 Mixed-asset 9 al-musharaka 0 al-murabaha al-istisna al-salam

Securitization and Structuring Sukuk

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Fatwa and DFM Shari a Standard Supervisory For Board. DFM Standard For Issuing, Acquiring and Trading Sukuk

Fatwa and DFM Shari a Standard Supervisory For Board The Board Issuing, Secretariat Acquiring and Trading Sukuk DFM Standard For 1 Contents INTRODUCTION... 4 1. THE SCOPE OF THE STANDARD... 6 2. TYPES

Fatwa and DFM Shari a Standard Supervisory For Board The Board Issuing, Secretariat Acquiring and Trading Sukuk DFM Standard For 1 Contents INTRODUCTION... 4 1. THE SCOPE OF THE STANDARD... 6 2. TYPES

Islamic Financing Products and Concepts, Current Market Trends and Opportunities. Nadim Khan, Partner, Herbert Smith LLP July 2010

Islamic Financing Products and Concepts, Current Market Trends and Opportunities Nadim Khan, Partner, Herbert Smith LLP July 2010 1 Overview Introduction to Islamic Finance The Key Products The Compliance

Islamic Financing Products and Concepts, Current Market Trends and Opportunities Nadim Khan, Partner, Herbert Smith LLP July 2010 1 Overview Introduction to Islamic Finance The Key Products The Compliance

Appendix A: Securities Commission

Appendix A: Securities Commission Malaysia Guidelines on Sukuk 1 In order for the market players to issue a Sukuk under Ijarah sukuk or otherwise, they have to comply with the Securities Commission Malaysia

Appendix A: Securities Commission Malaysia Guidelines on Sukuk 1 In order for the market players to issue a Sukuk under Ijarah sukuk or otherwise, they have to comply with the Securities Commission Malaysia

Analysis of the Sukuk Market. Dubai, April 25, 2007

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

Sukuks. Bin Shabib & Associates (BSA) LLP. 1. Legal and Regulatory Issues: a. Introduction. Overview of the Sukuk Market

LLP. 1. Legal and Regulatory Issues: a. Introduction. Overview of the Sukuk Market") Bin Shabib & Associates (BSA) LLP Sukuks 1. Legal and Regulatory Issues: a. Introduction Overview of the Sukuk Market In a growing Islamic Finance market, it is essential to continually strengthen the

Bin Shabib & Associates (BSA) LLP Sukuks 1. Legal and Regulatory Issues: a. Introduction Overview of the Sukuk Market In a growing Islamic Finance market, it is essential to continually strengthen the

Sukuk An Alternative to Bonds & A Viable Liquidity Management Tool for Financial Institutions. ISMAIL IDLE Chief Executive Officer

Sukuk An Alternative to Bonds & A Viable Liquidity Management Tool for Financial Institutions by ISMAIL IDLE Chief Executive Officer (1) Sukuk as a viable alternative to Conventional Bonds: DEFINING Sukuk

Sukuk An Alternative to Bonds & A Viable Liquidity Management Tool for Financial Institutions by ISMAIL IDLE Chief Executive Officer (1) Sukuk as a viable alternative to Conventional Bonds: DEFINING Sukuk

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

Islamic Instruments for Asset Management

Islamic Instruments for Asset Management Professor Rodney Wilson IRTI 15th Distance Learning Programme Intermediate Level Course Tuesday, March 20, 2012 Contents Islamic asset management vehicles Advantages

Islamic Instruments for Asset Management Professor Rodney Wilson IRTI 15th Distance Learning Programme Intermediate Level Course Tuesday, March 20, 2012 Contents Islamic asset management vehicles Advantages

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SNA/M1.18/6.a. 12 th Meeting of the Advisory Expert Group on National Accounts, November 2018, Luxembourg. Agenda item: 6.a.

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

Examination of the AAOIFI pronouncement on Sukuk issuance and its implication on the future Sukuk structure in the Islamic Capital Market

Examination of the AAOIFI pronouncement on Sukuk issuance and its implication on the future Sukuk structure in the Islamic Capital Market Dr. Ahcene Lahsasna Shariah & Legal Studies Department INCEIF,

Examination of the AAOIFI pronouncement on Sukuk issuance and its implication on the future Sukuk structure in the Islamic Capital Market Dr. Ahcene Lahsasna Shariah & Legal Studies Department INCEIF,

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

The Guide to Islamic Economics, Banking, and Finance

MPRA Munich Personal RePEc Archive The Guide to Islamic Economics, Banking, and Finance Nidal Alsayyed INCEIF the Global University in Islamic Finance, International Islamic University Malaysia 11. December

MPRA Munich Personal RePEc Archive The Guide to Islamic Economics, Banking, and Finance Nidal Alsayyed INCEIF the Global University in Islamic Finance, International Islamic University Malaysia 11. December

Islamic Finance More Than Window Dressing?

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Islamic Transactions September 2008

Islamic Transactions September 2008 TABLE OF CONTENTS TABLE OF CONTENTS 2 INTRODUCTION 3 BASIC PRINCIPLES 5 FINANCE STRUCTURES 7 Partnership Structures 7 Sale and Purchase Structures 8 Leasing Structures

Islamic Transactions September 2008 TABLE OF CONTENTS TABLE OF CONTENTS 2 INTRODUCTION 3 BASIC PRINCIPLES 5 FINANCE STRUCTURES 7 Partnership Structures 7 Sale and Purchase Structures 8 Leasing Structures

Shari ah Standard No. (44) Obtaining and Deploying Liquidity

Obtaining and Deploying Liquidity") Shari ah Standard No. (44) Obtaining and Deploying Liquidity Contents Subject Page Preface... 1087 Statement of the Standard... 1088 1. Scope of the Standard... 1088... 1088 3. Need to Utilise Liquidity

Shari ah Standard No. (44) Obtaining and Deploying Liquidity Contents Subject Page Preface... 1087 Statement of the Standard... 1088 1. Scope of the Standard... 1088... 1088 3. Need to Utilise Liquidity

SUKUK, an Emerging Asset Class

SUKUK, an Emerging Asset Class Ibrahim Mardam-Bey CEO, Siraj Capital Ltd November, 2007 DEFINITION AAOIFI Standard 17: investment Sukuk are certificates of equal value representing undivided shares in

SUKUK, an Emerging Asset Class Ibrahim Mardam-Bey CEO, Siraj Capital Ltd November, 2007 DEFINITION AAOIFI Standard 17: investment Sukuk are certificates of equal value representing undivided shares in

Sharia Issues in Liquidity Risk Management

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

SUKUK. A Fixed Income Opportunity

SUKUK A Fixed Income Opportunity WHAT ARE SUKUK Tradable Shariah-compliant Fixed Income Securities Sukuk, a shariah compliant fixed income instrument, represents an undivided share in the ownership of

SUKUK A Fixed Income Opportunity WHAT ARE SUKUK Tradable Shariah-compliant Fixed Income Securities Sukuk, a shariah compliant fixed income instrument, represents an undivided share in the ownership of

EXPLANATORY NOTE ON ISSUANCE AND SUBSCRIPTION OF SUKUK IN LABUAN INTERNATIONAL BUSINESS AND FINANCIAL CENTRE

EXPLANATORY NOTE ON ISSUANCE AND SUBSCRIPTION OF SUKUK IN LABUAN INTERNATIONAL BUSINESS AND FINANCIAL CENTRE 1.0 Introduction 1.1 As part of the efforts to facilitate and promote the development of the

EXPLANATORY NOTE ON ISSUANCE AND SUBSCRIPTION OF SUKUK IN LABUAN INTERNATIONAL BUSINESS AND FINANCIAL CENTRE 1.0 Introduction 1.1 As part of the efforts to facilitate and promote the development of the

Islamic Finance and Capital Markets: Sukuk Structure and Trading. Power point and Assessments

Islamic Finance and Capital Markets: Sukuk Structure and Trading Power point and Assessments Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work

Islamic Finance and Capital Markets: Sukuk Structure and Trading Power point and Assessments Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work

Mawarid Finance P.J.S.C. Consolidated Financial Statements

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-7 Consolidated statement of financial position 8 Consolidated statement of

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-7 Consolidated statement of financial position 8 Consolidated statement of

Mawarid Finance P.J.S.C. Consolidated Financial Statements for the year ended 31 December 2015

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-4 Consolidated statement of financial position 5 Consolidated statement of

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-4 Consolidated statement of financial position 5 Consolidated statement of

Making Finance Work for Africa Islamic Capital Markets

Making Finance Work for Africa Islamic Capital Markets 12 June 2014 HANI IBRAHIM Head of Debt Capital Markets - QInvest Islamic Finance Market 2 Global Islamic Finance Assets Defined as a financial service

Making Finance Work for Africa Islamic Capital Markets 12 June 2014 HANI IBRAHIM Head of Debt Capital Markets - QInvest Islamic Finance Market 2 Global Islamic Finance Assets Defined as a financial service

The DFSA Rulebook. Islamic Finance Rules (IFR) IFR/VER12/01-18

IFR/VER12/01-18") The DFSA Rulebook Islamic Finance Rules (IFR) IFR/VER12/01-18 Contents The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 1.1 Application...

The DFSA Rulebook Islamic Finance Rules (IFR) IFR/VER12/01-18 Contents The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 1.1 Application...

SUKUK MARKET AND REGULATIONS IN PAKISTAN

SUKUK MARKET AND REGULATIONS IN PAKISTAN Introduction There has been a concerted push by regulatory authorities in Pakistan in the last few years to promote the Islamic finance industry. Recently, the

SUKUK MARKET AND REGULATIONS IN PAKISTAN Introduction There has been a concerted push by regulatory authorities in Pakistan in the last few years to promote the Islamic finance industry. Recently, the

Q: What types of Financial Institutions and transactions are involved in Islamic finance?

Q: What is Islamic Finance Islamic finance is an interest free finance system. There is therefore, no charge for its use. Islamic finance is asset based as opposed to being currency based. A deal is structured

Q: What is Islamic Finance Islamic finance is an interest free finance system. There is therefore, no charge for its use. Islamic finance is asset based as opposed to being currency based. A deal is structured

Islamic Instruments for Asset Management IDB/IRTI DL Program April 12th, 2011 Tehran, Iran

بسم االله الر حمن الر حيم 13th Distance Learning Course: Spring 2011 An Intermediate Course in Islamic Finance Islamic Instruments for Asset Management IDB/IRTI DL Program April 12th, 2011 Tehran, Iran

بسم االله الر حمن الر حيم 13th Distance Learning Course: Spring 2011 An Intermediate Course in Islamic Finance Islamic Instruments for Asset Management IDB/IRTI DL Program April 12th, 2011 Tehran, Iran

There are fundamental differences between these. The diagrams set out below explain the mechanics of how each sukuk operates.

ISLAMIC FINANCE From 2013, Islamic finance becomes part of the Paper P4 syllabus, following its introduction to Paper F9 two years ago. This article looks at Islamic finance as a growing and important

ISLAMIC FINANCE From 2013, Islamic finance becomes part of the Paper P4 syllabus, following its introduction to Paper F9 two years ago. This article looks at Islamic finance as a growing and important

CIFE STUDY NOTES

CIFE STUDY NOTES ABOUT ETHICA DOWNLOAD BROCHURE HERE >> About Ethica Institute of Islamic Finance About Ethica Institute of Islamic Finance About the Certified Islamic Finance Executive (CIFE ) About

CIFE STUDY NOTES ABOUT ETHICA DOWNLOAD BROCHURE HERE >> About Ethica Institute of Islamic Finance About Ethica Institute of Islamic Finance About the Certified Islamic Finance Executive (CIFE ) About

Glossary Of Islamic Finance Terms

January 7, 2008 Glossary Of Islamic Finance Terms Primary Credit Analyst: Mohamed Damak, Paris (33) 1-4420-7322; mohamed_damak@standardandpoors.com Table Of Contents The Five Pillars Of Islamic Finance

January 7, 2008 Glossary Of Islamic Finance Terms Primary Credit Analyst: Mohamed Damak, Paris (33) 1-4420-7322; mohamed_damak@standardandpoors.com Table Of Contents The Five Pillars Of Islamic Finance

Tax Treatment of Islamic Financial Transactions

Tax Treatment of Islamic Financial Transactions This document should be read in conjunction with Part 8A Taxes Consolidation Act 1997 Document created November 2018. 1 Table of Contents 1 Introduction

Tax Treatment of Islamic Financial Transactions This document should be read in conjunction with Part 8A Taxes Consolidation Act 1997 Document created November 2018. 1 Table of Contents 1 Introduction

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

Islamic Financial Markets: Stocks and Sukuk. Professor Habib Ahmed Durham University Business School

Islamic Financial Markets: Stocks and Sukuk Professor Habib Ahmed Durham University Business School Outline Stock Markets Islamic Perspectives Sukuk Structures and Evolution Sukuk Issues and Controversies

Islamic Financial Markets: Stocks and Sukuk Professor Habib Ahmed Durham University Business School Outline Stock Markets Islamic Perspectives Sukuk Structures and Evolution Sukuk Issues and Controversies

Presentation Outline Copyright Bank Nizwa. All Rights Reserved. 2

Presentation Outline Real Economy VS Capitalism PREAMBLE Overview of Islamic Finance Section 1 Islamic Banks VS Conventional Banks Section 2 A Glimpse Into Islamic Finance Products and Services Section

Presentation Outline Real Economy VS Capitalism PREAMBLE Overview of Islamic Finance Section 1 Islamic Banks VS Conventional Banks Section 2 A Glimpse Into Islamic Finance Products and Services Section

Diversification of Islamic Financial Instruments in Turkey

Republic of Turkey Undersecretariat of Treasury Diversification of Islamic Financial Instruments in Turkey Utku ŞEN Treasury Expert 9 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October

Republic of Turkey Undersecretariat of Treasury Diversification of Islamic Financial Instruments in Turkey Utku ŞEN Treasury Expert 9 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October

AIFC ISLAMIC FINANCE RULES (IFR)

") ---------------------------------------------------------------------------------------------- AIFC ISLAMIC FINANCE RULES (IFR) AIFC RULES NO. FR0013 OF 2017 ----------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------- AIFC ISLAMIC FINANCE RULES (IFR) AIFC RULES NO. FR0013 OF 2017 ----------------------------------------------------------------------------------------------

Sukuk: Definition, Structure and Accounting Issues

MPRA Munich Personal RePEc Archive Sukuk: Definition, Structure and Accounting Issues Khalil Ahmed USIM 2011 Online at http://mpra.ub.uni-muenchen.de/33675/ MPRA Paper No. 33675, posted 25. September 2011

MPRA Munich Personal RePEc Archive Sukuk: Definition, Structure and Accounting Issues Khalil Ahmed USIM 2011 Online at http://mpra.ub.uni-muenchen.de/33675/ MPRA Paper No. 33675, posted 25. September 2011

8BURSA 12 SUKUK. c ontents SUQ AL-SILA SHARI AH COMPLIANT LISTED EQUITIES. ISLAMIC REAL ESTATE INVESTMENT TRUSTS (ireits)

") c ontents 8BURSA SUQ AL-SILA 10 SHARI AH COMPLIANT LISTED EQUITIES 2 THE MALAYSIA INTERNATIONAL ISLAMIC FINANCIAL CENTRE (MIFC) INITIATIVE 4 BURSA MALAYSIA 6 ISLAMIC MARKETS 12 SUKUK 14 ISLAMIC REAL ESTATE

c ontents 8BURSA SUQ AL-SILA 10 SHARI AH COMPLIANT LISTED EQUITIES 2 THE MALAYSIA INTERNATIONAL ISLAMIC FINANCIAL CENTRE (MIFC) INITIATIVE 4 BURSA MALAYSIA 6 ISLAMIC MARKETS 12 SUKUK 14 ISLAMIC REAL ESTATE

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2010 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2010 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2010 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

Dubai Islamic Bank P.J.S.C. Consolidated financial statements for the year ended 31 December 2015

Consolidated financial statements These audited financial statements are subject to the Central Bank of the UAE approval and adoption by shareholders at the annual general meeting. Report and consolidated

Consolidated financial statements These audited financial statements are subject to the Central Bank of the UAE approval and adoption by shareholders at the annual general meeting. Report and consolidated

Sharing of Risks in Islamic Finance

IBSU Scientific Journal, 5(2): 13-20, 2011 ISSN: 1512-3731 print / 2233-3002 online Sharing of Risks in Islamic Finance Ahmet SEKRETER Abstract For most of the people the prohibition on interest is the

IBSU Scientific Journal, 5(2): 13-20, 2011 ISSN: 1512-3731 print / 2233-3002 online Sharing of Risks in Islamic Finance Ahmet SEKRETER Abstract For most of the people the prohibition on interest is the

Islamic Bonds (Sukuk) M. Kabir Hassan, Rasem N. Kayed, and Umar A. Oseni

M. Kabir Hassan, Rasem N. Kayed, and Umar A. Oseni") Islamic Bonds (Sukuk) M. Kabir Hassan, Rasem N. Kayed, and Umar A. Oseni Learning Objectives Upon the completion of this chapter, the reader should be able to: 1. Understand what sukuk is, its historical

Islamic Bonds (Sukuk) M. Kabir Hassan, Rasem N. Kayed, and Umar A. Oseni Learning Objectives Upon the completion of this chapter, the reader should be able to: 1. Understand what sukuk is, its historical

Global Sukuk Market Trends

Global Sukuk Market Trends Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development Center

Global Sukuk Market Trends Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development Center

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

Dubai Islamic Bank P.J.S.C. Review report and condensed consolidated interim financial information for the nine-month period ended 30 September 2017

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

Dubai Islamic Bank P.J.S.C. Consolidated financial statements for the year ended 31 December 2016

Consolidated financial statements Report and consolidated financial statements Pages Independent auditors report 1-8 Consolidated statement of financial position 9 Consolidated statement of profit or loss

Consolidated financial statements Report and consolidated financial statements Pages Independent auditors report 1-8 Consolidated statement of financial position 9 Consolidated statement of profit or loss

Dubai Islamic Bank P.J.S.C. Review report and condensed consolidated interim financial information for the three-month period ended 31 March 2016

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

PROPOSED ESTABLISHMENT OF A PERPETUAL SUKUK PROGRAMME OF UP TO RM5.0 BILLION IN NOMINAL VALUE ( SUKUK PROGRAMME ) SUKUK DIAGRAM

SUKUK DIAGRAM") Sukuk Wakalah transaction structure SUKUK DIAGRAM 7. Purchase Undertaking Sukuk Trustee (acting on behalf of Sukukholders) 1. Appoint as Wakeel 2 (a). Issue Sukuk Wakalah 2 (b). Proceeds 8. Sale Undertaking

Sukuk Wakalah transaction structure SUKUK DIAGRAM 7. Purchase Undertaking Sukuk Trustee (acting on behalf of Sukukholders) 1. Appoint as Wakeel 2 (a). Issue Sukuk Wakalah 2 (b). Proceeds 8. Sale Undertaking

Islamic Finance and Capital Markets: Structure and Trading of Sukuk. Khalifa M Ali Hassanain

Islamic Finance and Capital Markets: Structure and Trading of Sukuk Khalifa M Ali Hassanain Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work are

Islamic Finance and Capital Markets: Structure and Trading of Sukuk Khalifa M Ali Hassanain Copy Rights Notice Islamic research and Training Institute 2016 All rights reserved. All parts of this work are

THE SUKUK HANDBOOK. A Guide To Structuring Sukuk. Second Edition

THE SUKUK HANDBOOK A Guide To Structuring Sukuk Second Edition CONTENTS THE HISTORY AND DEVELOPMENT OF SUKUK... 1 SUMMARY OF SUKUK STRUCTURES... 6 SUKUK AL-IJARA... 9 CASE STUDY: GOVERNMENT OF DUBAI US$5

THE SUKUK HANDBOOK A Guide To Structuring Sukuk Second Edition CONTENTS THE HISTORY AND DEVELOPMENT OF SUKUK... 1 SUMMARY OF SUKUK STRUCTURES... 6 SUKUK AL-IJARA... 9 CASE STUDY: GOVERNMENT OF DUBAI US$5

Abu Dhabi Islamic Bank PJSC

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2015 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2015 (unaudited) Contents Page Review report of interim

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2015 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2015 (unaudited) Contents Page Review report of interim

Islamic Project Finance and Infrastructure Funding in Thailand Key Concepts and Structures. Stephen Jaggs 23 November 2012

Islamic Project Finance and Infrastructure Funding in Thailand Key Concepts and Structures Stephen Jaggs 23 November 2012 Allen & Overy 2012 BN:1932301.1 1 Religious Principles and Background Body of Islamic

Islamic Project Finance and Infrastructure Funding in Thailand Key Concepts and Structures Stephen Jaggs 23 November 2012 Allen & Overy 2012 BN:1932301.1 1 Religious Principles and Background Body of Islamic

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 31 MARCH 2008 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 31 MARCH 2008 (UNAUDITED) INTERIM CONSOLIDATED BALANCE SHEET At 31 March 2008 (Unaudited) Three months Three months ended 31 March ended 31 March 2008

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 31 MARCH 2008 (UNAUDITED) INTERIM CONSOLIDATED BALANCE SHEET At 31 March 2008 (Unaudited) Three months Three months ended 31 March ended 31 March 2008

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

[Exposure Draft (ver. 1.6) of] Financial Accounting Standard No. 29. Sukuk Issuance

![[Exposure Draft (ver. 1.6) of] Financial Accounting Standard No. 29. Sukuk Issuance](/thumbs/75/72194154.jpg "[Exposure Draft (ver. 1.6) of] Financial Accounting Standard No. 29. Sukuk Issuance") [Exposure Draft (ver. 1.6) of] Financial Accounting Standard No. 29 Sukuk Issuance 1 Contents Preface... 5 Introduction... 6 Overview... 6 Reasons for issuing this standard... 6 Main features... 6 Objective

[Exposure Draft (ver. 1.6) of] Financial Accounting Standard No. 29 Sukuk Issuance 1 Contents Preface... 5 Introduction... 6 Overview... 6 Reasons for issuing this standard... 6 Main features... 6 Objective

Use of Sukuk/Islamic Securities as Collateral

Use of Sukuk/Islamic Securities as Collateral 11 th Meeting of the Organisation of Islamic Cooperation (OIC) Member Staters Stock Exchanges Forum Tuesday, 31 st October 2017, Le Meridien Etiler Hotel,

Use of Sukuk/Islamic Securities as Collateral 11 th Meeting of the Organisation of Islamic Cooperation (OIC) Member Staters Stock Exchanges Forum Tuesday, 31 st October 2017, Le Meridien Etiler Hotel,

Sharia Issues in Liquidity Risk Management

Sharia Issues in Liquidity Risk Management Paper Presented in Colloque International Banque et Finance Islamiques Universite Robert Schuman, Strasbourg (France) January, 11 th, 2008 Rifki Ismal Doctoral

Sharia Issues in Liquidity Risk Management Paper Presented in Colloque International Banque et Finance Islamiques Universite Robert Schuman, Strasbourg (France) January, 11 th, 2008 Rifki Ismal Doctoral

Risk Management in Islamic Banking (lecture 3)

") Risk Management in Islamic Banking (lecture 3) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4th, 2009 Rifki Ismal Durham University

Risk Management in Islamic Banking (lecture 3) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4th, 2009 Rifki Ismal Durham University

Basic Islamic Finance and Islamic Contracts

BASIC ISLAMIC FINANCE AND ISLAMIC CONTRACTS Basic Islamic Finance and Islamic Contracts PUBLISHED BY: AL ALAWI & CO., ADVOCATES & LEGAL CONSULTANTS BANKING & FINANCE GROUP In today s day and age, banking

BASIC ISLAMIC FINANCE AND ISLAMIC CONTRACTS Basic Islamic Finance and Islamic Contracts PUBLISHED BY: AL ALAWI & CO., ADVOCATES & LEGAL CONSULTANTS BANKING & FINANCE GROUP In today s day and age, banking

Dubai Islamic Bank P.J.S.C. Review report and condensed consolidated interim financial information for the nine-month period ended 30 September 2015

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

Alternative financing structures for the aviation industry

Alternative financing structures for the aviation industry Gregory Man Partner and Head of Debt Capital Markets (Middle East) Norton Rose Fulbright (Middle East) LLP October 4, 2016 Agenda Introduction

Alternative financing structures for the aviation industry Gregory Man Partner and Head of Debt Capital Markets (Middle East) Norton Rose Fulbright (Middle East) LLP October 4, 2016 Agenda Introduction

Qatar International Islamic Bank (Q.P.S.C)

") CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONSOLIDATED STATEMENT OF INCOME For the year ended 31 December 2017 Notes Income from financing activities 24 1,418,995 1,261,932 Net income from

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONSOLIDATED STATEMENT OF INCOME For the year ended 31 December 2017 Notes Income from financing activities 24 1,418,995 1,261,932 Net income from

Role of Sukuk in Islamic capital market: experience of Iran ( )

") Role of Sukuk in Islamic capital market: experience of Iran (1994-2011) Majid karimzadeh, Department of Economics, Aligarh Muslim University. Abstract Recent innovations in Islamic finance have changed

Role of Sukuk in Islamic capital market: experience of Iran (1994-2011) Majid karimzadeh, Department of Economics, Aligarh Muslim University. Abstract Recent innovations in Islamic finance have changed

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view 1 O M A R M U S T A F A A N S A R I A S S I S T A N T S E C R E T A R Y G E N E R A L A C C O U N T I N

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view 1 O M A R M U S T A F A A N S A R I A S S I S T A N T S E C R E T A R Y G E N E R A L A C C O U N T I N

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2011 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2011 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2011 (Unaudited) Contents Page Report on review of interim

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2011 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2011 (Unaudited) Contents Page Report on review of interim

Islamic Finance Rules (IFR)

") Islamic Finance Rules (IFR) IFR VER02.150617 TABLE OF CONTENTS The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 2. ISLAMIC FINANCE... 2

Islamic Finance Rules (IFR) IFR VER02.150617 TABLE OF CONTENTS The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 2. ISLAMIC FINANCE... 2

The asset side of Takaful and implications on product design

building value together 13 November 2012 The asset side of Takaful and implications on product design Hassan Scott Odierno, FSA Istanbul www.actuarialpartners.com Conventional bonds Bonds are the backbone

building value together 13 November 2012 The asset side of Takaful and implications on product design Hassan Scott Odierno, FSA Istanbul www.actuarialpartners.com Conventional bonds Bonds are the backbone

SABA ISLAMIC BANK (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN

SANA A, REPUBLIC OF YEMEN") (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS

(Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS

Introduction to Islamic Investing. For professional clients only

Introduction to Islamic Investing For professional clients only 2 Overview Assets of Islamic financial institutions have grown by an average of 15% per annum* over the past five years to reach over $1trillion

Introduction to Islamic Investing For professional clients only 2 Overview Assets of Islamic financial institutions have grown by an average of 15% per annum* over the past five years to reach over $1trillion

Introduction to Islamic Finance & Banking

Introduction to Islamic Finance & Banking World Bank BRSA - TKBB Joint Workshop on Innovative Product Development in Islamic Banks Istanbul, Turkey March 2, 2017 Zamir Iqbal, PhD. Lead Financial Sector

Introduction to Islamic Finance & Banking World Bank BRSA - TKBB Joint Workshop on Innovative Product Development in Islamic Banks Istanbul, Turkey March 2, 2017 Zamir Iqbal, PhD. Lead Financial Sector

The DFSA Rulebook. Prudential Investment, Insurance Intermediation and Banking Module (PIB) Appendix 5

Appendix 5") Appendix 5 All provisions shown as struck through in this appendix have been moved to the Islamic Finance Rules Module of the DFSA Rulebook. Please see the destination table for further information. The

Appendix 5 All provisions shown as struck through in this appendix have been moved to the Islamic Finance Rules Module of the DFSA Rulebook. Please see the destination table for further information. The

IIFM-BAFT Master Participation Agreements - Key legal aspects

IIFM-BAFT Master Participation Agreements - Key legal aspects M. Delwar Hossain Senior Associate - Bahrain office What is a Participation? An arrangement between two banks/financial institutions whereby:

IIFM-BAFT Master Participation Agreements - Key legal aspects M. Delwar Hossain Senior Associate - Bahrain office What is a Participation? An arrangement between two banks/financial institutions whereby:

Mr. D.A.N. EKE DEPUTY DIRECTOR

AN OVER-VIEW OF CBN NON-INTEREST (ISLAMIC) BANKING FRAMEWORK Mr. D.A.N. EKE DEPUTY DIRECTOR BANKING SUPERVISION DEPARTMENT 29 TH JULY, 2009 Central Bank of Nigeria 1 Outline Central Bank of Nigeria 1.

AN OVER-VIEW OF CBN NON-INTEREST (ISLAMIC) BANKING FRAMEWORK Mr. D.A.N. EKE DEPUTY DIRECTOR BANKING SUPERVISION DEPARTMENT 29 TH JULY, 2009 Central Bank of Nigeria 1 Outline Central Bank of Nigeria 1.

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

Amana Participation Fund

Investor Shares AMAPX Amana Participation Fund Institutional Shares: AMIPX Halal Capital Preservation and Current Income About Amana Mutual Funds Trust At the Amana Mutual Funds Trust and Saturna Capital,

Investor Shares AMAPX Amana Participation Fund Institutional Shares: AMIPX Halal Capital Preservation and Current Income About Amana Mutual Funds Trust At the Amana Mutual Funds Trust and Saturna Capital,

Chapter 3. Islamic Finance and Investment- An Overview. outlining Shariah principles, features of the investment, key components of Shariah

Chapter 3 Islamic Finance and Investment- An Overview Introduction This chapter gives an overview about the concept of Shariah Finance by outlining Shariah principles, features of the investment, key components

Chapter 3 Islamic Finance and Investment- An Overview Introduction This chapter gives an overview about the concept of Shariah Finance by outlining Shariah principles, features of the investment, key components

Content. n Why? n Objectives. n Shariah Standards issued by BNM. n AAOIFI Shariah Standards

Shariah Standards 1 Content n Why? n Objectives n Shariah Standards issued by BNM n AAOIFI Shariah Standards Why? n Differences in interpreting Shari ah has led to a diverse legal and regulatory landscape

Shariah Standards 1 Content n Why? n Objectives n Shariah Standards issued by BNM n AAOIFI Shariah Standards Why? n Differences in interpreting Shari ah has led to a diverse legal and regulatory landscape

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES. MEHOL K. SADAIN Commissioner NCMF February 9, 2015

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES MEHOL K. SADAIN Commissioner NCMF February 9, 2015 Definition of Terms Finance is the science or study of management of funds; the system that includes

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES MEHOL K. SADAIN Commissioner NCMF February 9, 2015 Definition of Terms Finance is the science or study of management of funds; the system that includes

Wealth Creation and Wealth Management in an Islamic Economy

Wealth Creation and Wealth Management in an Islamic Economy Professor Rodney Wilson IRTI Distance Learning Programme Islamic Development Bank, April 2011 Outline Material wealth, spiritual fulfilment and

Wealth Creation and Wealth Management in an Islamic Economy Professor Rodney Wilson IRTI Distance Learning Programme Islamic Development Bank, April 2011 Outline Material wealth, spiritual fulfilment and

Islamic Risk Management. Instruments. First International Islamic Finance Conference Labuan - Malaysia. (6-7 July 2004)

") First International Islamic Finance Conference Labuan - Malaysia (6-7 July 2004) Islamic Risk Management Corporate and Investment Banking Instruments Table of contents SECTION 1 The FX & Debt/Deposit issues

First International Islamic Finance Conference Labuan - Malaysia (6-7 July 2004) Islamic Risk Management Corporate and Investment Banking Instruments Table of contents SECTION 1 The FX & Debt/Deposit issues

Glossary of Islamic Capital Market Terms

Glossary of Islamic Capital Market Terms Terms Definition Bai` Bithaman Ajil (BBA) Bai` al-`inah Bai` al-istijrar A contract that refers to the sale and purchase transaction for the financing of assets

Glossary of Islamic Capital Market Terms Terms Definition Bai` Bithaman Ajil (BBA) Bai` al-`inah Bai` al-istijrar A contract that refers to the sale and purchase transaction for the financing of assets

Operational models for Ijarah, Istisna, and Murabaha sukuk from Islamic point of view 1 Syed abbas musavian 2

Operational models for Ijarah, Istisna, and Murabaha sukuk from Islamic point of view 1 Syed abbas musavian 2 Mostafa Zehtabian 3 Abstract The absence of bonds in the capital market and the capability

Operational models for Ijarah, Istisna, and Murabaha sukuk from Islamic point of view 1 Syed abbas musavian 2 Mostafa Zehtabian 3 Abstract The absence of bonds in the capital market and the capability

From PLI s Course Handbook Islamic Financing: A Comparative Analysis of Sukuk and Conventional Bonds and Securitizations #15105

From PLI s Course Handbook Islamic Financing: A Comparative Analysis of Sukuk and Conventional Bonds and Securitizations #15105 14 SECURITIZATION GLOSSARY Submitted by: Mark Adelson Nomura Securities International,

From PLI s Course Handbook Islamic Financing: A Comparative Analysis of Sukuk and Conventional Bonds and Securitizations #15105 14 SECURITIZATION GLOSSARY Submitted by: Mark Adelson Nomura Securities International,

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE MARCH 2019 VERSION 1.0 Contents Contents 1. Introduction... 5 1.1. Purpose of this Guide... 5 1.2. About the National Bureau for Revenue (NBR)... 5 1.3.

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE MARCH 2019 VERSION 1.0 Contents Contents 1. Introduction... 5 1.1. Purpose of this Guide... 5 1.2. About the National Bureau for Revenue (NBR)... 5 1.3.

Al Salam Bank-Bahrain B.S.C.

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2014 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note BD '000 BD '000 ASSETS Cash and balances with banks and Central Bank of Bahrain 5 277,751 86,097 Central

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2014 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note BD '000 BD '000 ASSETS Cash and balances with banks and Central Bank of Bahrain 5 277,751 86,097 Central

GROUP CONSOLIDATED FINANCIAL STATEMENTS

In the Name of Allah The most Gracious and Merciful Emirates Islamic Bank (Public Joint Stock Company) Head Office 3rd Floor, Building 16, Dubai Health Care City, Dubai Tel.: +97 1 4 3160336 Fax: +97 1

In the Name of Allah The most Gracious and Merciful Emirates Islamic Bank (Public Joint Stock Company) Head Office 3rd Floor, Building 16, Dubai Health Care City, Dubai Tel.: +97 1 4 3160336 Fax: +97 1

Al Salam Bank-Bahrain B.S.C.

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2016 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note BD '000 BD '000 ASSETS Cash and balances with banks and Central Bank 5 131,990 152,572 Sovereign Sukuk

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2016 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note BD '000 BD '000 ASSETS Cash and balances with banks and Central Bank 5 131,990 152,572 Sovereign Sukuk

Taxation of Islamic financial products in Ireland

Chapter 25 Taxation of Islamic financial products in Ireland 25.1 Introduction During 2010, the Republic of Ireland amended its taxation laws to accommodate Islamic finance more favourably. These amendments

Chapter 25 Taxation of Islamic financial products in Ireland 25.1 Introduction During 2010, the Republic of Ireland amended its taxation laws to accommodate Islamic finance more favourably. These amendments

Session 5 Interest Scheme Act in Need of Reformation:

Session 5 Interest Scheme Act in Need of Reformation: By: Prof. Dr. Ashraf bin Md. Hashim* CEO ISRA Consultancy Sdn. Bhd. * Prof. Dr. Ashraf Md. Hashim is the CEO, ISRA Consultancy Sdn. Bhd. He is also

Session 5 Interest Scheme Act in Need of Reformation: By: Prof. Dr. Ashraf bin Md. Hashim* CEO ISRA Consultancy Sdn. Bhd. * Prof. Dr. Ashraf Md. Hashim is the CEO, ISRA Consultancy Sdn. Bhd. He is also

Risk Management in Islamic Financial Institutions

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY THREE Sharia Approaches on Liquidity Risk Management Challenges Related to Liquidity

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY THREE Sharia Approaches on Liquidity Risk Management Challenges Related to Liquidity

Sharia-Compliant Structured Products

News Bulletin April 15, 2010 Volume 1, Issue 7 Structured Thoughts News for the financial services community. Sharia-Compliant Structured Products The same features that continue to attract investors to

News Bulletin April 15, 2010 Volume 1, Issue 7 Structured Thoughts News for the financial services community. Sharia-Compliant Structured Products The same features that continue to attract investors to