Investment and Financing of the ICT sector. Arab Conference on Industrial Information and Networks Tunis - May 23, 2005

|

|

|

- Dana Leonard

- 5 years ago

- Views:

Transcription

1 Investment and Financing of the ICT sector Arab Conference on Industrial Information and Networks Tunis - May 23, 2005

2 GICT Structure IFC Activities World Bank Units Global Communications Investment Portfolio & Technology Investment Policy InfoDev Provides long-term debt & equity financing for telecom infrastructure, broadband connectivity, IT, broadcast/media & satellite sectors Provides debt, equity & quasiequity financing to technology companies; manages IFC s ICT portfolio & provides credit review function Provides policy & regulatory advisory services to governments on telecom, postal, broadcasting & e- governance. Finances investments where market gaps exist. Grant-based facility for innovative applications of ICT with social impact

3 The Three Core Pillars of GICT s Strategic Vision Catalyzing Market Growth - Liberalization - Regulation - Finance private infrastructure - Finance Media Addressing Market Failures - Rural access - Broadband/Internet - National & regional backbones - State-owned incumbents Driving Demand Through Innovation - Finance ICT applications - Support ICT in non-ict sectors - Support convergence technologies

4 Map of GICT Activities ( ) CITPO IFC Both CITPO and IFC Not active

5 WBG Worldwide Activities IBRD/IDA, IFC (including syndications) and MIGA commitments in ICT by region ( ), in million USD Other, $54, 2% SA, $439, 14% SSA, $682, 22% MENA, $655, 21% EAP, $200, 6% ECA, $424, 13% LAC, $693, 22%

6 ICT in 1990 Fixed penetration: 46% in developed and 3% in emerging markets Mobile penetration: 12% in developed and 0% in emerging markets Outgoing international traffic per subscriber (voice): 99 m/s in developed and 108 m/s in emerging markets Investment in the Sector : US$13.7 bn total incl. US$4.6 bn private Technologies deployed Circuit switched fixed Analog mobile

7 ICT in 2005 Fixed penetration: 56% in developed and 11% in emerging markets Mobile penetration: 71% in developed and 14% in emerging markets Outgoing international traffic per subscriber (voice): 214 m/s in developed and 104 m/s in emerging markets Investment in the Sector : US$40.7 bn total incl. US$28.5 bn private Technologies deployed digital cellular fixed and wireless broadband IP switching

8 1. Global Village Impact on business models Impacts Global supply chain global competition New businesses through off-shoring (call-centers, data centers, accounting, etc.) 2. Backbones & Regional Connectivity Unequal development/lack of backbone on a regional, national & subnational level What business models could stimulate demand & attract new investments? PPP Cost of communications / leased lines 3. Internet Access Unequal internet access and prices around the globe and locally Local content Policy and regulatory reform to promote internet access

9 Close to One Trillion dollars of Investment in Developing Country Telecommunications Telecommunications Investment % GDP SSA EAP ECA LAC MENA SAR

10 A Growing Share Private By 2003, among all 164 countries with available data, 130 had three or more competing digital mobile operators. Since 1988, 76 developing countries have privatized their public telecommunication operators (PTOs), raising over US$ 70 billion Over the period, developing countries attracted $331 billion of private investment into telecommunications (dramatic slowdown post 2000) 88 countries have attracted private participation in infrastructure worth more than 1% of their GDP over the period, including 26 countries in Africa

11 7.0% With High Returns In Rollout Fixed line growth % 6.0% 5.0% 4.6% 5.4% 5% 4.0% No separate regulator Separate regulator No separate regulator Separate regulator Not liberalized Liberalized

12 With High Returns In Prices and Efficiency 20% drop in fixed prices where there is fixed competition 36% drop in international prices moving from public monopoly to competitive provision involving FDI Countries with PPI in Telecoms > 1% GDP see 5% productivity gain (lines/employee)

13 Percentage of Businesses Labeling Telecommunications A Significant Business Constraint No Involvement Involvement Extent of Private Involvement in Fixed Provision

14 Continuing Investment Demand Estimates that developing countries need $100 billion a year in new investment to continue rollout. SSA alone will need nearly $4 billion (0.8% GDP) in new investment annually, plus an additional $3 billion in maintenance.

15 1.2 Attracting PPI PPI (% GDP) LDC Average Independent Regulator......And Fixed and Mobile Competition

16 Attracting PPI, Cont d Six additional telecoms commitments to the WTO are associated with a 31 percent increase in private participation perhaps because of the stability and certainty such commitments bring. A survey of restrictions to telecoms FDI in fifteen Asian economies found fourteen of them have restrictions, ranging from 30 to 49 percent of total equity The top four constraints to investment rated by surveyed companies across 53 countries were policy uncertainty, macro instability, tax rates and corruption.

17 But growth outside mobile communications is constrained by political and institutional problems Incumbent fixed line operators are not privatized and are mostly inefficient In 14 MNA countries, 10 incumbents are state-owned, 4 are partially privatized. Morocco has now a majority private investor (CITPO followed the reform in Morocco). Limited effective independence for regulatory agencies Marginal or no competition in most ICT market segments (outside mobile) THIS IS THE CORE ISSUE

18

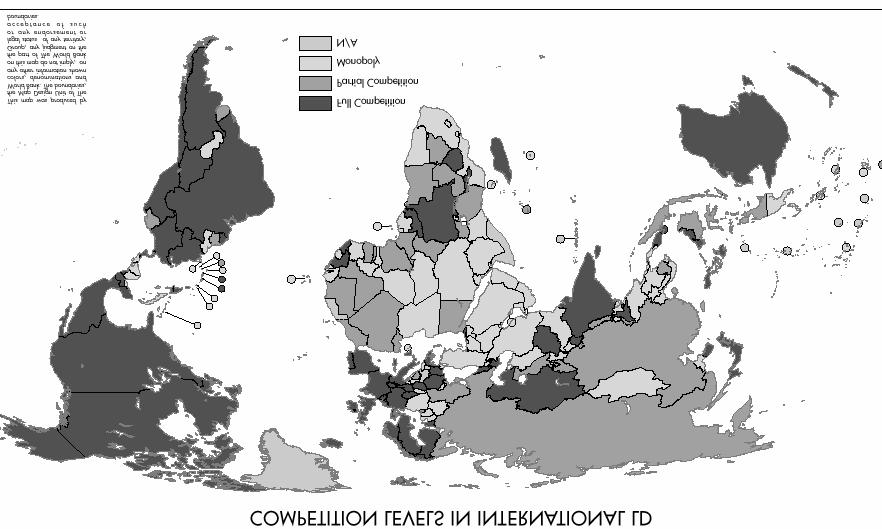

19 Competition is a global phenomenon, but many countries are left behind All developed countries and selected developing countries have competition in international communications. affordable calls for domestic users facilitates global integration facilitates contacts with overseas communities Many developing countries have restrictions to competition in international communications. most domestic users cannot afford the service 10% increase in communications cost means 8% trade economic and social isolation from the rest of the world

20 MNA Lags Behind Monopoly Partial competition Full competition Data not available

21 Prices are high and they are not decreasing fast enough Saudi Arabia Bahrain Iran Oman Chile Prices are decreasing relatively slowly, compared with e.g. Chile, Estonia. Large gap between MNA prices and those of fully competitive countries Price of a 1 min. call to the US

22 Only 1.6% of the Arab population has Internet access UNDP Arab Human Development Report

23 Broadband and backbone

24 The Role of Donors/IFIs: Policy and Regulation Bilaterals very active FY02-03 USAID funding approx. 115 ICT Sector projects Many multilateral players UNDP, MDBs World Bank has a major role Active in approx. 80 countries

25 The Role of Donors/IFIs: Investment Bilateral support for telecommunications: averages over $1 billion early 1990s, now under $100m. Only 14% of the projects listed in the PPI database involved an IFI IFIs Account for Approx. 1/60 th of Investment Evidence of Counter-Cyclical Role IFC Grows After 2000, Especially to Africa Growing role in access programs IT in demand, yet often included in other sectors investment

26 Examples of WB/IFC activities Tunisia: WB lending for an ICT Sector Development Project ICT Strategy, Licensing, Regulation E-Government strategy, applications (e-justice, e-disabled, e-culture, ICT library, e- learning, Arabic DNS ) E-security training, National Back-up and recovery center, CERT Support to WSIS and Sector monitoring Morocco: IFC co-led Medi Telecom s US$1.1 billion Debt Restructuring In 2000, IFC approved a financial package for Medi Telecom to build and operate a nationwide GSM network in Morocco; One of the largest telecom project financings ever in Africa (US$1.6 billion). Awarded African Telecom Deal of the Year by Global Finance Magazine in IFC acted as Advisor and Joint Lead Arranger of Medi Telecom s debt restructuring that was successfully closed in July The original debt would mature in 2008 (B Loan; US$340 million) and 2009 (A Loan; US$66m and C Loan; US$22m). The loans had their maturities extended for three years (including one year grace period), until 2011 for the B Loan and 2012 for the A and C Loans; Sponsors committed US$50 million in additional contingent equity

27 Major IFI Investors Number of Projects Listed in PPI Database IFC EBRD EIB Others

28 Conclusion Massive Rollout of ICT in the 1990 s, yet Mixed picture for Broadband and Internet (coverage and price) limiting the potential use of IT Growing share of private investment, yet Competitive and well regulated private investment climate is key to attract investors Considerable investment needs, yet Difficult to attract private financing : FDI reforms, WTO commitments, regulatory stability Pro-investment policy and regulation Leveraging government as a consumer, Public Private Partnerships Government-supported access initiatives

29 THANK YOU Michel Maechler, GICT References (available on-line) Financing Information and Communication Infrastructure Needs in the Developing World: Public and Private Roles, The World Bank, February Competition in International Voice Communications, Rossoto C.M., Wellenius B., Lewin A. and Gomez C.R., World Bank Working Paper No 42, 2004.

30 The Three Core Pillars of GICT s Strategic Vision Catalyzing Market Growth - Liberalization - Regulation - Finance private infrastructure - Finance Media Addressing Market Failures - Rural access - Broadband/Internet - National & regional backbones - State-owned incumbents Driving Demand Through Innovation - Finance ICT applications - Support ICT in non-ict sectors - Support convergence technologies

31 Catalyzing Market Growth I. Policy Work Competition & regulatory reform, regulatory capacity building From segment focused policy & regulation to converged policy and regulation Spectrum policy Unprivatized incumbents Capacity-building & analytical work on policy & regulatory issues (regulatory toolkit, etc) II. Investments Infrastructure Support traditional players with full product range/new products Explore investing in broadband/alternative providers Finance regional players ( South South ) Explore working with emerging equipment suppliers Media Focus on large & rapidly growing media markets Finance non-controversial entertainment & advertising-based media Explore investing in media with news & editorial components

32 Addressing Market Failures I. Policy Work Universal/Rural Access Increased focus on broadband, ICT training, content National & regional backbones Analytical work & policy toolkits for extending access (open access study, etc.) II. Investments Increase public-private partnerships Develop SME & microfinance products to support the next billion Innovative financing schemes for universal/rural access Pre-privatization investments in incumbents Piloting on options for extending access (support for last mile pilots)

II.")

33 Driving Demand Through Innovation I. Policy Work e-legislation Regulation for e-government, e-commerce, security, etc. Analytical work & scalability experiments on ICT use in core sectors (education, health) II. Investments E-Government & IT Services: selectively expand into new markets IT Enabled Services/Business Process Outsourcing: emerging portfolio in a few key markets IP/Technology Products (software & IT hardware): focus on India and China Convergence: Applications & Services that emerge from the convergence of telecom and computing Financing for connectivity and ICT applications for governments and other sectors Financing the global network of ICT incubators, leading to broader innovation-support program

34 WBG Worldwide Activities IBRD/IDA, IFC (including syndications) and MIGA commitments in ICT by region ( ), in million USD Other, $54, 2% SA, $439, 14% SSA, $682, 22% MENA, $655, 21% EAP, $200, 6% ECA, $424, 13% LAC, $693, 22%

35 WBG Activities IFC, IBRD/IDA and MIGA commitments and syndications for ICT sector, (excl AAA) USD millions TFs (w/ PPIAF & InfoDev), $70.55, 2% MIGA, $666, 21% IFC (excl B- loans), $1,156, 36% IBRD/IDA, $851, 26% IFC B-loans, $474, 15%

36 WBG- A Continuing Commitment IFC, IBRD/IDA, MIGA commitments and syndications for ICI sector (excl AAA) $1,000 USD millions $800 $600 $400 $200 MIGA TFs (w/ PPIAF & InfoDev) IBRD/IDA IFC B-loans IFC (excl B-loans) $ FY approved

37 IFC ICT Portfolio 8% 1% Cable and Broadband 26% Computer Systems Design and Related Services Content Fixed Telephony 45% 1% 3% Internet Access Providers (Including ISPs) Mobile Telephony 1% 15% Other (Satellite, Radio and Television Broadcasting, etc.) Private Equity/Venture Cap Fund - Regional

38 South Asia 13% MENA 11% IFC ICT Portfolio SECA 10% AFRICA 10% ECA 8% EAP 14% LAC 34%

39 Investment Focus in IT IT Services IT Enabled Services Software Development Software Products IC Design e-commerce e-government

Financing Information and Communication Infrastructure Needs in the Developing World: Public and Private Roles

Financing Information and Communication Infrastructure Needs in the Developing World: Public and Private Roles DRAFT FOR DISCUSSION February 2005 The World Bank Global Information and Communication Technologies

Financing Information and Communication Infrastructure Needs in the Developing World: Public and Private Roles DRAFT FOR DISCUSSION February 2005 The World Bank Global Information and Communication Technologies

Digital Infrastructure Initiative. Carlos A. Toshiharu Katsuya Chief Investment Officer Head Telecom, Media & Technology Asia, Europe & MENA

Digital Infrastructure Initiative Carlos A. Toshiharu Katsuya Chief Investment Officer Head Telecom, Media & Technology Asia, Europe & MENA IFC S OVERVIEW Providing Development Solutions! Provides investment,

Digital Infrastructure Initiative Carlos A. Toshiharu Katsuya Chief Investment Officer Head Telecom, Media & Technology Asia, Europe & MENA IFC S OVERVIEW Providing Development Solutions! Provides investment,

Investors/Analysts Meet. October 25 th, 2005

Investors/Analysts Meet October 25 th, 2005 Safe Harbor Statement Some of the statements herein constitute forwardlooking statements that do not directly or exclusively relate to historical facts. These

Investors/Analysts Meet October 25 th, 2005 Safe Harbor Statement Some of the statements herein constitute forwardlooking statements that do not directly or exclusively relate to historical facts. These

Infrastructure Financing in APEC Emerging Economies

2017/FDM1/007 Session: 3 Infrastructure Financing in APEC Emerging Economies Purpose: Information Submitted by: World Bank Group Finance and Central Bank Deputies Meeting Nha Trang, Viet Nam 23-24 February

2017/FDM1/007 Session: 3 Infrastructure Financing in APEC Emerging Economies Purpose: Information Submitted by: World Bank Group Finance and Central Bank Deputies Meeting Nha Trang, Viet Nam 23-24 February

TABLE OF CONTENTS. Chapter 3. Telecommunication Market Size Market Drivers... 45

TABLE OF CONTENTS Chapter 1. Introduction... 11 The Road to Regulatory Reform... 11 Communication Markets in the OECD Area... 15 Leading PTOs in OECD Area... 16 Chapter 2. Recent Communication Policy Developments...

TABLE OF CONTENTS Chapter 1. Introduction... 11 The Road to Regulatory Reform... 11 Communication Markets in the OECD Area... 15 Leading PTOs in OECD Area... 16 Chapter 2. Recent Communication Policy Developments...

Third quarter report 2009

Third quarter report 2009 Henry sténson Senior Vice President Communications Third quarter report 2009 This presentation contains forward looking statements. Such statements are based on our current expectations

Third quarter report 2009 Henry sténson Senior Vice President Communications Third quarter report 2009 This presentation contains forward looking statements. Such statements are based on our current expectations

Water Supply & Sanitation Hydropower

The Role of the World Bank in a Changing Water World Water Supply & Sanitation Hydropower Jamal Saghir Director, Energy and Water World Bank Water Week 2003 4 March 2003 Outline of the presentation A changing

The Role of the World Bank in a Changing Water World Water Supply & Sanitation Hydropower Jamal Saghir Director, Energy and Water World Bank Water Week 2003 4 March 2003 Outline of the presentation A changing

The Sustainable Development Commitments Mobilizing Resources for Implementing the SDGs Anne Bakilana Program Leader World Bank Group

The Sustainable Development Commitments Mobilizing Resources for Implementing the SDGs Anne Bakilana Program Leader World Bank Group @wbg2030 worldbank.org/sdgs Symposium on Governance for Implementing

The Sustainable Development Commitments Mobilizing Resources for Implementing the SDGs Anne Bakilana Program Leader World Bank Group @wbg2030 worldbank.org/sdgs Symposium on Governance for Implementing

FROM COMMITMENT TO DELIVERY. Catalyzing Resources for Development

FROM COMMITMENT TO DELIVERY Catalyzing Resources for Development UNITAR Learning Conference 2 March, 2017 GLOBAL FRAMEWORKS FOR DEVELOPMENT: FROM MDGS TO SDGS MDGs (2000-2015) SDGs (2016-2030) Goals 8

FROM COMMITMENT TO DELIVERY Catalyzing Resources for Development UNITAR Learning Conference 2 March, 2017 GLOBAL FRAMEWORKS FOR DEVELOPMENT: FROM MDGS TO SDGS MDGs (2000-2015) SDGs (2016-2030) Goals 8

2017 ICT Backbone Sector. Private Participation in Infrastructure (PPI)

") 2017 ICT Backbone Sector Private Participation in Infrastructure (PPI) Acknowledgement & Disclaimer This report was written by a team comprising Deblina Saha (Task Team Leader), Alex Shao and Iuliia Zemlytska,

2017 ICT Backbone Sector Private Participation in Infrastructure (PPI) Acknowledgement & Disclaimer This report was written by a team comprising Deblina Saha (Task Team Leader), Alex Shao and Iuliia Zemlytska,

Financing Asia s infrastructure gap: New ideas for the public and private sectors

Financing Asia s infrastructure gap: New ideas for the public and private sectors Dr. Kevin Lu Regional Director, Asia Pacific Multilateral Investment Guarantee Agency World Bank Group Distinguished Fellow

Financing Asia s infrastructure gap: New ideas for the public and private sectors Dr. Kevin Lu Regional Director, Asia Pacific Multilateral Investment Guarantee Agency World Bank Group Distinguished Fellow

Bridging the Digital Divide: through access to finance

Bridging the Digital Divide: through access to finance Chijioke Egejuru, Investment Officer, TMT Africa Contents 1. What we do 2. A Case for TMT Investments 3. Key Focus Sectors 4. Targeted Funding for

Bridging the Digital Divide: through access to finance Chijioke Egejuru, Investment Officer, TMT Africa Contents 1. What we do 2. A Case for TMT Investments 3. Key Focus Sectors 4. Targeted Funding for

PPI data update note 21 March 2009

PPI data update note 21 March 29 New private infrastructure projects in developing countries continue to take place but projects are being affected by the financial crisis 1 Summary: Throughout the financial

PPI data update note 21 March 29 New private infrastructure projects in developing countries continue to take place but projects are being affected by the financial crisis 1 Summary: Throughout the financial

RELIANCE COMMUNICATIONS (RCOM) ANNOUNCES ITS FINANCIAL RESULTS FOR THE QUARTER ENDED JUNE 30, 2007

ANNOUNCES ITS FINANCIAL RESULTS FOR THE QUARTER ENDED JUNE 30, 2007") RELIANCE COMMUNICATIONS (RCOM) ANNOUNCES ITS FINANCIAL RESULTS FOR THE QUARTER ENDED JUNE 30, 2007 NET PROFIT INCREASES BY 138% T0 RS. 1,221 CRORE (US$ 301 MILLION) REVENUES AT RS. 4,304 CRORE (US$ 1,061

RELIANCE COMMUNICATIONS (RCOM) ANNOUNCES ITS FINANCIAL RESULTS FOR THE QUARTER ENDED JUNE 30, 2007 NET PROFIT INCREASES BY 138% T0 RS. 1,221 CRORE (US$ 301 MILLION) REVENUES AT RS. 4,304 CRORE (US$ 1,061

Mapping of Development Partners Support to Leverage Investment to Africa s infrastructure

Mapping of Development Partners Support to Leverage Investment to Africa s infrastructure Dambudzo Muzenda, OECD Directorate for Finance and Enterprise Affairs Investment Division AfI Project Background

Mapping of Development Partners Support to Leverage Investment to Africa s infrastructure Dambudzo Muzenda, OECD Directorate for Finance and Enterprise Affairs Investment Division AfI Project Background

IFC: PROMOTING INCLUSIVE GREEN GROWTH IN THE MIDDLE EAST & NORTH AFRICA (MENA)

") IFC: PROMOTING INCLUSIVE GREEN GROWTH IN THE MIDDLE EAST & NORTH AFRICA (MENA) Thomas Jacobs, MENA Climate Anchor & Resident Representative, Lebanon & Syria IFC: Largest development bank focused solely

IFC: PROMOTING INCLUSIVE GREEN GROWTH IN THE MIDDLE EAST & NORTH AFRICA (MENA) Thomas Jacobs, MENA Climate Anchor & Resident Representative, Lebanon & Syria IFC: Largest development bank focused solely

Economic Importance of Cross-border Trade in Services- Recent Developments

Symposium on Cross-Border Supply of Services World Trade Organization 28-29 April 2005 Economic Importance of Cross-border Trade in Services- Recent Developments WTO Economic Research and Statistics Division

Symposium on Cross-Border Supply of Services World Trade Organization 28-29 April 2005 Economic Importance of Cross-border Trade in Services- Recent Developments WTO Economic Research and Statistics Division

IFC STRATEGY AND CAPITAL INCREASE. June 26, 2018

IFC STRATEGY AND CAPITAL INCREASE June 26, 2018 Global Context: Meeting Development Goals Requires Increased Financing and Managing Global Risks in a Changing Landscape More than 3 million new jobs are

IFC STRATEGY AND CAPITAL INCREASE June 26, 2018 Global Context: Meeting Development Goals Requires Increased Financing and Managing Global Risks in a Changing Landscape More than 3 million new jobs are

The WB Clean Technology Fund MENA Renewable Energy Program

The WB Clean Technology Fund MENA Renewable Energy Program Mohab Hallouda Sr. Energy Specialist MENA Energy and Transport Unit World Bank RCREEE/MED EMIP Joint Event Regional Challenges to Green the Power

The WB Clean Technology Fund MENA Renewable Energy Program Mohab Hallouda Sr. Energy Specialist MENA Energy and Transport Unit World Bank RCREEE/MED EMIP Joint Event Regional Challenges to Green the Power

Arab Financing Facility for Infrastructure Developing infrastructure for growth and regional integration in Arab countries

AFFI Brochure Arab Financing Facility for Infrastructure Developing infrastructure for growth and regional integration in Arab countries What is AFFI? The Arab Financing Facility for Infrastructure (AFFI)

AFFI Brochure Arab Financing Facility for Infrastructure Developing infrastructure for growth and regional integration in Arab countries What is AFFI? The Arab Financing Facility for Infrastructure (AFFI)

Infrastructure Policy Unit 2012 Global PPI Data Update

Note 85 July 213 Infrastructure Policy Unit Global PPI Data Update Private investment commitments to infrastructure in the developing world rise by 4 percent in Private investment commitments (hereafter,

Note 85 July 213 Infrastructure Policy Unit Global PPI Data Update Private investment commitments to infrastructure in the developing world rise by 4 percent in Private investment commitments (hereafter,

AIIB S ROLE IN FINANCING ASIA S INFRASTRUCTURE GAP OPPORTUNITIES FOR EUROPEAN CONTRACTORS

AIIB S ROLE IN FINANCING ASIA S INFRASTRUCTURE GAP OPPORTUNITIES FOR EUROPEAN CONTRACTORS Ian Nightingale - AIIB Procurement Advisor WHAT IS THE ASIAN INFRASTRUCTURE INVESTMENT BANK? A new multilateral

AIIB S ROLE IN FINANCING ASIA S INFRASTRUCTURE GAP OPPORTUNITIES FOR EUROPEAN CONTRACTORS Ian Nightingale - AIIB Procurement Advisor WHAT IS THE ASIAN INFRASTRUCTURE INVESTMENT BANK? A new multilateral

Investment Development Authority of Lebanon Arab Spanish Investment Forum 2011

Investment Development Authority of Lebanon Arab Spanish Investment Forum 2011 Wednesday October 26 th Headlines 1. ABOUT LEBANON 2. CURRENT TRENDS IN SPANISH LEBANESE TRADE 3. SPANISH COMPANIES AND LEBANON

Investment Development Authority of Lebanon Arab Spanish Investment Forum 2011 Wednesday October 26 th Headlines 1. ABOUT LEBANON 2. CURRENT TRENDS IN SPANISH LEBANESE TRADE 3. SPANISH COMPANIES AND LEBANON

OPIC and the Information & Communications Technology (ICT) Sector

Sector") OPIC and the Information & Communications Technology (ICT) Sector May 3, 2018 OPIC Policy Standards Investors and project proposals must satisfy certain policy criteria. OPIC s Unique Position Eligibility

OPIC and the Information & Communications Technology (ICT) Sector May 3, 2018 OPIC Policy Standards Investors and project proposals must satisfy certain policy criteria. OPIC s Unique Position Eligibility

Meeting the Infrastructure Challenge: The Case for a New Development Bank

Washington DC, 21 st March 2013 Meeting the Infrastructure Challenge: The Case for a New Development Bank Prepared for the G-24 Technical Group Meeting Amar Bhattacharya & Mattia Romani C O N F I D E N

Washington DC, 21 st March 2013 Meeting the Infrastructure Challenge: The Case for a New Development Bank Prepared for the G-24 Technical Group Meeting Amar Bhattacharya & Mattia Romani C O N F I D E N

Partnering with IFC. Anita Bhatia and Urkaly Isaev October 2014 THE POWER OF PARTNERSHIPS

Partnering with IFC Anita Bhatia and Urkaly Isaev October 2014 THE POWER OF PARTNERSHIPS 1 World Bank Group 2 Twin Goals of the World Bank Group 3 4 The private sector in development 5 IFC s Three Businesses

Partnering with IFC Anita Bhatia and Urkaly Isaev October 2014 THE POWER OF PARTNERSHIPS 1 World Bank Group 2 Twin Goals of the World Bank Group 3 4 The private sector in development 5 IFC s Three Businesses

MENA Infrastructure: Opportunities and Challenges. DIFC Economics Workshop Adil Marghub December 2009

MENA Infrastructure: Opportunities and Challenges DIFC Economics Workshop Adil Marghub December 2009 IFC: Background 2 IFC is a Member of the World Bank Group IBRD International Bank for Reconstruction

MENA Infrastructure: Opportunities and Challenges DIFC Economics Workshop Adil Marghub December 2009 IFC: Background 2 IFC is a Member of the World Bank Group IBRD International Bank for Reconstruction

How the Arab World Can Benefit from Low Oil Prices. Shanta Devarajan World Bank

How the Arab World Can Benefit from Low Oil Prices Shanta Devarajan World Bank www.brookings.edu/futuredevelopment Current problems in the Arab World Unemployment 30 Unemployment rate (latest available),

How the Arab World Can Benefit from Low Oil Prices Shanta Devarajan World Bank www.brookings.edu/futuredevelopment Current problems in the Arab World Unemployment 30 Unemployment rate (latest available),

Joint MDB Statement of Ambitions for Crowding in Private Finance 1

Joint MDB Statement of Ambitions for Crowding in Private Finance 1 Background These Ambitions build on the recently approved Principles for MDBs Strategy Crowding in Private Sector Finance for Growth and

Joint MDB Statement of Ambitions for Crowding in Private Finance 1 Background These Ambitions build on the recently approved Principles for MDBs Strategy Crowding in Private Sector Finance for Growth and

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PPI data update note 22 June 29 Assessment of the impact of the crisis on new PPI projects

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PPI data update note 22 June 29 Assessment of the impact of the crisis on new PPI projects

MOBILIZATION OF PRIVATE FINANCE BY MULTILATERAL DEVELOPMENT BANKS

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized MOBILIZATION OF PRIVATE FINANCE BY MULTILATERAL DEVELOPMENT BANKS 2016 Joint Report Report

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized MOBILIZATION OF PRIVATE FINANCE BY MULTILATERAL DEVELOPMENT BANKS 2016 Joint Report Report

BEZEQ (TASE: BEZQ) Investor Presentation Results

Investor Presentation Results") BEZEQ (TASE: BEZQ) Investor Presentation 2016 Results Forward-Looking Information and Statement This presentation contains general data and information as well as forward looking statements about Bezeq

BEZEQ (TASE: BEZQ) Investor Presentation 2016 Results Forward-Looking Information and Statement This presentation contains general data and information as well as forward looking statements about Bezeq

MENA Transition Fund

Financial Report Prepared by the Trustee As of December 31, 2016 1 Table of Contents Table of Contents Introduction... 3 Financial Summary as of December 31, 2016... 4 1. Summary Inception through December

Financial Report Prepared by the Trustee As of December 31, 2016 1 Table of Contents Table of Contents Introduction... 3 Financial Summary as of December 31, 2016... 4 1. Summary Inception through December

Promoting investment in the digital economy

APRIL 2017 SPECIAL ISSUE Promoting investment in the digital economy H I G H L I G H T S The development of the digital economy is a key objective for almost all countries. Many countries and economies

APRIL 2017 SPECIAL ISSUE Promoting investment in the digital economy H I G H L I G H T S The development of the digital economy is a key objective for almost all countries. Many countries and economies

WBG Infrastructure Response to the Crisis

WBG Infrastructure Response to the Crisis BA April 2009 BANK FOR INTERNATIONAL WORLD BANK 1 DEVELOPMENT RECONSTRUCTION AND Outline I. Context and Background II. Infrastructure and the Crisis III.WBG Response

WBG Infrastructure Response to the Crisis BA April 2009 BANK FOR INTERNATIONAL WORLD BANK 1 DEVELOPMENT RECONSTRUCTION AND Outline I. Context and Background II. Infrastructure and the Crisis III.WBG Response

OPIC and the Information & Communications Technology (ICT) Sector

Sector") OPIC and the Information & Communications Technology (ICT) Sector Dynamic Spectrum Alliance, April 28, 2016 OPIC Development Priorities ICTs support OPIC s development strategy. OPIC s Unique Position

OPIC and the Information & Communications Technology (ICT) Sector Dynamic Spectrum Alliance, April 28, 2016 OPIC Development Priorities ICTs support OPIC s development strategy. OPIC s Unique Position

SECOND REPORT TO THE G20 ON THE MDB ACTION PLAN TO OPTIMIZE BALANCE SHEETS JUNE 2017

SECOND REPORT TO THE G20 ON THE MDB ACTION PLAN TO OPTIMIZE BALANCE SHEETS JUNE 2017 The G20 Leaders endorsed the MDB Action Plan to Optimize Balance Sheets at the 2015 November Antalya meeting. The Plan

SECOND REPORT TO THE G20 ON THE MDB ACTION PLAN TO OPTIMIZE BALANCE SHEETS JUNE 2017 The G20 Leaders endorsed the MDB Action Plan to Optimize Balance Sheets at the 2015 November Antalya meeting. The Plan

India s Growth Story. Is It Sustainable? Parag Saxena May 30, 2008

India s Growth Story Is It Sustainable? Parag Saxena May 30, 2008 Widely Acknowledged to be the Architect of Indian Reforms In 1991, Manmohan Singh, as Finance Minister in Narasimha Rao s government, embarked

India s Growth Story Is It Sustainable? Parag Saxena May 30, 2008 Widely Acknowledged to be the Architect of Indian Reforms In 1991, Manmohan Singh, as Finance Minister in Narasimha Rao s government, embarked

FROM BILLIONS TO TRILLIONS:

98023 FROM BILLIONS TO TRILLIONS: MDB Contributions to Financing for Development In 2015, the international community is due to agree on a new set of comprehensive and universal sustainable development

98023 FROM BILLIONS TO TRILLIONS: MDB Contributions to Financing for Development In 2015, the international community is due to agree on a new set of comprehensive and universal sustainable development

GENERAL MEETING 3 MAY Arnaud Lagardère General and Managing Partner

GENERAL MEETING 3 MAY 2018 Arnaud Lagardère General and Managing Partner CONTENTS 1 OUR MARKETS AND THEIR TRENDS 2 OUR GROUP TODAY 3 OUR STRATEGIC VISION AND AMBITION 2 OUR MARKETS AND OUR GROUP TODAY

GENERAL MEETING 3 MAY 2018 Arnaud Lagardère General and Managing Partner CONTENTS 1 OUR MARKETS AND THEIR TRENDS 2 OUR GROUP TODAY 3 OUR STRATEGIC VISION AND AMBITION 2 OUR MARKETS AND OUR GROUP TODAY

WEST AFRICA REGIONAL MINING FORUM, CONAKRY, GUINEA

WEST AFRICA REGIONAL MINING FORUM, CONAKRY, GUINEA Creating Enabling Environment for Infrastructure Development For Large-scale Mining William Bulmer, Associate Director, Head of Mining Division, IFC February

WEST AFRICA REGIONAL MINING FORUM, CONAKRY, GUINEA Creating Enabling Environment for Infrastructure Development For Large-scale Mining William Bulmer, Associate Director, Head of Mining Division, IFC February

Telecom Egypt At A Glance

FY 2010 Disclaimer This document has been prepared by Telecom Egypt (the Company ) solely for the use at the analyst/investor presentation, held in connection with the Company. The information contained

FY 2010 Disclaimer This document has been prepared by Telecom Egypt (the Company ) solely for the use at the analyst/investor presentation, held in connection with the Company. The information contained

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro and Small Enterprise Finance Financial Institutions

The goals to Access / Financial Inclusion 2020 Briefing for World Bank Group President Dr. Jim Yong Kim Terence Gallagher Senior Specialist in Micro and Small Enterprise Finance Financial Institutions

How would you characterize the telecom market in Bangladesh?

How would you characterize the telecom market in Bangladesh? In 1971, Bangladesh Telegraph and Telephone Department was set up under the Ministry of Posts and Telecommunications to run telecommunication

How would you characterize the telecom market in Bangladesh? In 1971, Bangladesh Telegraph and Telephone Department was set up under the Ministry of Posts and Telecommunications to run telecommunication

OVERVIEW OF CONVERGENCE BLENDED FINANCE INFORMATION SESSION & NETWORKING BREAKFAST ZÜRICH, 28 TH AUGUST, 2018

OVERVIEW OF BLENDED FINANCE INFORMATION SESSION & NETWORKING BREAKFAST ZÜRICH, 28 TH AUGUST, 2018 WHAT IS? Convergence is the global network for blended finance. We generate blended finance data, intelligence,

OVERVIEW OF BLENDED FINANCE INFORMATION SESSION & NETWORKING BREAKFAST ZÜRICH, 28 TH AUGUST, 2018 WHAT IS? Convergence is the global network for blended finance. We generate blended finance data, intelligence,

Key Activities of the WB/IFC Securities Markets Group. Global Capital Markets Development Department

Key Activities of the WB/IFC Securities Markets Group Global Capital Markets Development Department WB-IFC Securities Market Group (GCMSM) WBG Global Product Group for local securities market development

Key Activities of the WB/IFC Securities Markets Group Global Capital Markets Development Department WB-IFC Securities Market Group (GCMSM) WBG Global Product Group for local securities market development

Private Participation in Infrastructure 1 Database (PPIDB) Half Year Update (January June 2016)

Half Year Update (January June 2016)") Private Participation in Infrastructure 1 Database (PPIDB) Half Year Update (January June 216) Investment 2 in infrastructure 3 with private participation in developing countries totaled US$29.5 billion

Private Participation in Infrastructure 1 Database (PPIDB) Half Year Update (January June 216) Investment 2 in infrastructure 3 with private participation in developing countries totaled US$29.5 billion

FDI and the Arab World. OECD Meeting in Istanbul February 11 th, 2004 Dr. Martin Berlin Chief Strategy Officer

FDI and the Arab World OECD Meeting in Istanbul February 11 th, 2004 Dr. Martin Berlin Chief Strategy Officer Why Investment Promotion Current status of FDI While Global FDI flows have increased at a dramatic

FDI and the Arab World OECD Meeting in Istanbul February 11 th, 2004 Dr. Martin Berlin Chief Strategy Officer Why Investment Promotion Current status of FDI While Global FDI flows have increased at a dramatic

SECOND QUARTER REPORT 2009

SECOND QUARTER REPORT 2009 1 HENRY STÉNSON Senior Vice President Communications 2 SECOND QUARTER REPORT 2009 This presentation contains forward looking statements. Such statements are based on our current

SECOND QUARTER REPORT 2009 1 HENRY STÉNSON Senior Vice President Communications 2 SECOND QUARTER REPORT 2009 This presentation contains forward looking statements. Such statements are based on our current

The Sustainable Development Goals

The Sustainable Development Goals Reality & Prospects Mahmoud Mohieldin, Senior Vice President World Bank Group Mahmoud Mohieldin March 13 th, 2017 Global Context Global Economy GDP Growth (Percent) 5

The Sustainable Development Goals Reality & Prospects Mahmoud Mohieldin, Senior Vice President World Bank Group Mahmoud Mohieldin March 13 th, 2017 Global Context Global Economy GDP Growth (Percent) 5

IFC Operational Highlights

IFC Operational Highlights Dollars in millions, for the years ended June 30 2017 2016 2015 2014 2013 Long-Term Investment Commitments FOR IFC S OWN ACCOUNT $11,854 $11,117 $10,539 $ 9,967 $11,008 Number

IFC Operational Highlights Dollars in millions, for the years ended June 30 2017 2016 2015 2014 2013 Long-Term Investment Commitments FOR IFC S OWN ACCOUNT $11,854 $11,117 $10,539 $ 9,967 $11,008 Number

NDC IMPLEMENTATION SUPPORT. Dr. Ana Bucher Sr. Climate Change Specialist Climate Analytics and Advisory Services

NDC IMPLEMENTATION SUPPORT Dr. Ana Bucher Sr. Climate Change Specialist Climate Analytics and Advisory Services abucher@worldbank.org WBG Climate Change Action Plan explicitly points to NDC implementation

NDC IMPLEMENTATION SUPPORT Dr. Ana Bucher Sr. Climate Change Specialist Climate Analytics and Advisory Services abucher@worldbank.org WBG Climate Change Action Plan explicitly points to NDC implementation

Ziggo Q Results. October 14, 2011

Ziggo Q3 2011 Results October 14, 2011 Disclaimer Various statements contained in this document constitute forward-looking statements as that term is defined by U.S. federal securities laws. Words like

Ziggo Q3 2011 Results October 14, 2011 Disclaimer Various statements contained in this document constitute forward-looking statements as that term is defined by U.S. federal securities laws. Words like

technicolor.com 7 JUNE 2018

technicolor.com 7 JUNE 2018 COUNTRIES SITES REVENUES Connected Home 57% 57% 2017 2016 16% 1% 26% Production Services 18% DVD Services 24% North America 53% 2017 2016 25% 16% 52% 7% Europe, Middle-East

technicolor.com 7 JUNE 2018 COUNTRIES SITES REVENUES Connected Home 57% 57% 2017 2016 16% 1% 26% Production Services 18% DVD Services 24% North America 53% 2017 2016 25% 16% 52% 7% Europe, Middle-East

Millicom International Cellular Rating: Buy

SATELLITE, CABLE & BROADCASTING David B. Kestenbaum 212-218-3851 dkestenbaum@morganjoseph.com Heather Hou 212-218-3713 hhou@morganjoseph.com Company Update October 7, 2008 Key Metrics MICC - NASDAQ $58.45

SATELLITE, CABLE & BROADCASTING David B. Kestenbaum 212-218-3851 dkestenbaum@morganjoseph.com Heather Hou 212-218-3713 hhou@morganjoseph.com Company Update October 7, 2008 Key Metrics MICC - NASDAQ $58.45

Acquisition and Amalgamation of Suntel by Dialog Broadband

... Enriching Sri Lankan Lives an axiata company Dialog Axiata PLC Up-Scaling Enterprise & Broadband Play via Fixed Sector Consolidation Acquisition and Amalgamation of Suntel by Dialog Broadband Dialog

... Enriching Sri Lankan Lives an axiata company Dialog Axiata PLC Up-Scaling Enterprise & Broadband Play via Fixed Sector Consolidation Acquisition and Amalgamation of Suntel by Dialog Broadband Dialog

Assessment of the impact of the crisis on new PPI projects Update 4 (09/28/09)

") Assessment of the impact of the crisis on new PPI projects Update 4 (/28/) New private infrastructure activity in developing countries recovered in the first half of thanks to the electricity sector, but

Assessment of the impact of the crisis on new PPI projects Update 4 (/28/) New private infrastructure activity in developing countries recovered in the first half of thanks to the electricity sector, but

2017 Transport Sector. Private Participation in Infrastructure (PPI)

") 2017 Transport Sector Private Participation in Infrastructure (PPI) Acknowledgement & Disclaimer This report was written by a team comprising Deblina Saha (Task Team Leader), Akhilesh Modi and Iuliia Zemlytska,

2017 Transport Sector Private Participation in Infrastructure (PPI) Acknowledgement & Disclaimer This report was written by a team comprising Deblina Saha (Task Team Leader), Akhilesh Modi and Iuliia Zemlytska,

IFC INVESTMENT OVERVIEW. Darlington Akaiso

IFC INVESTMENT OVERVIEW Darlington Akaiso IFC OVERVIEW IFC is the member of the World Bank Group focused on the private sector Founded in 1956 with 184 member countries Largest multilateral source of loan/equity

IFC INVESTMENT OVERVIEW Darlington Akaiso IFC OVERVIEW IFC is the member of the World Bank Group focused on the private sector Founded in 1956 with 184 member countries Largest multilateral source of loan/equity

Deutsche Bank 25th Annual Media and Telecom Conference March 6, 2017

Deutsche Bank 25th Annual Media and Telecom Conference March 6, 2017 Safe Harbor Statement All information set forth in this presentation, except historical and factual information, represents forward-looking

Deutsche Bank 25th Annual Media and Telecom Conference March 6, 2017 Safe Harbor Statement All information set forth in this presentation, except historical and factual information, represents forward-looking

Importance of financial infrastructure to increase Access to Finance

Building a high performance SME business in the MENA Region Arab Monetary Fund & International Finance Corporation Dubai, 7-8 May 2013 Importance of financial infrastructure to increase Access to Finance

Building a high performance SME business in the MENA Region Arab Monetary Fund & International Finance Corporation Dubai, 7-8 May 2013 Importance of financial infrastructure to increase Access to Finance

Bezeq Group. Third Quarter 2008 Results. Investor Presentation

Bezeq Group Third Quarter 2008 Results Investor Presentation 1 Disclaimer Forward-Looking Information and Statement This presentation contains general data and information as well as forward looking statements

Bezeq Group Third Quarter 2008 Results Investor Presentation 1 Disclaimer Forward-Looking Information and Statement This presentation contains general data and information as well as forward looking statements

A Review of the Post and Telecommunications Market 2008/09

A Review of the Post and Telecommunications Market 2008/09 Introduction It is that time of the year that the UCC takes time to review the industry performance, key developments and challenges for the previous

A Review of the Post and Telecommunications Market 2008/09 Introduction It is that time of the year that the UCC takes time to review the industry performance, key developments and challenges for the previous

Enhancing legal conditions for infrastructure investment in the Mediterranean raising awareness of risk mitigation instruments

Enhancing legal conditions for infrastructure investment in the Mediterranean raising awareness of risk mitigation instruments the investment security in the mediterranean support programme The Organisation

Enhancing legal conditions for infrastructure investment in the Mediterranean raising awareness of risk mitigation instruments the investment security in the mediterranean support programme The Organisation

ECONOMIC ANALYSIS. A. Introduction

North Pacific Regional Connectivity Investment Project (RRP PAL 46382) ECONOMIC ANALYSIS A. Introduction 1. Project summary. The Asian Development Bank (ADB) will support Palau to develop a fiber optic

North Pacific Regional Connectivity Investment Project (RRP PAL 46382) ECONOMIC ANALYSIS A. Introduction 1. Project summary. The Asian Development Bank (ADB) will support Palau to develop a fiber optic

a Saudi Joint Stock Company

a Saudi Joint Stock Company Consolidated Financial Statements for the Year Ended December 31, 2013 Index to the Consolidated Financial Statements for the Year Ended December 31, 2013 Page Auditors Report.

a Saudi Joint Stock Company Consolidated Financial Statements for the Year Ended December 31, 2013 Index to the Consolidated Financial Statements for the Year Ended December 31, 2013 Page Auditors Report.

The Water Sector and Development. Public Spending and Development Assistance in the Sector

Water for Life: Implications for Developing Countries Danny M. Leipziger Vice President and Head of Network Poverty Reduction and Economic Management The World Bank Zaragoza, Spain June 30, 2008 Outline

Water for Life: Implications for Developing Countries Danny M. Leipziger Vice President and Head of Network Poverty Reduction and Economic Management The World Bank Zaragoza, Spain June 30, 2008 Outline

IFC in Nigeria: Review. Amitava Banerjee, Manager Miguel Rebolledo Dellepiane, Senior Evaluation Officer

IFC in Nigeria: An Independent Country Impact Review. Amitava Banerjee, Manager Miguel Rebolledo Dellepiane, Senior Evaluation Officer Independent Evaluation Group IEG Independent we report to World Bank/MIGA/IFC

IFC in Nigeria: An Independent Country Impact Review. Amitava Banerjee, Manager Miguel Rebolledo Dellepiane, Senior Evaluation Officer Independent Evaluation Group IEG Independent we report to World Bank/MIGA/IFC

OTE GROUP REPORTS 2018 FIRST QUARTER RESULTS

OTE GROUP REPORTS 2018 FIRST QUARTER RESULTS Group EBITDA up 3.6% on robust performance in Greece Greece progress fueled by successful investments: o Accelerating take-up of fiber broadband o Growth in

OTE GROUP REPORTS 2018 FIRST QUARTER RESULTS Group EBITDA up 3.6% on robust performance in Greece Greece progress fueled by successful investments: o Accelerating take-up of fiber broadband o Growth in

Mobiles for Development: the case of Banking Poverty and Access in Latin America

Mobiles for Development: the case of Banking Poverty and Access in Latin America Judith Mariscal 1 CONTENTS 1. Underserved Population in Latin America. 2. Mobile opportunities Survey: Key Results 3. M

Mobiles for Development: the case of Banking Poverty and Access in Latin America Judith Mariscal 1 CONTENTS 1. Underserved Population in Latin America. 2. Mobile opportunities Survey: Key Results 3. M

O)FFICAL 130CUNIENTS 'IFC ADMINISTRATION ARRANGEMENT AMONG AND INTERNATIONAL FINANCE CORPORATION FOR THE FINANCIAL SUPPORT

FFICAL 130CUNIENTS 'IFC ADMINISTRATION ARRANGEMENT AMONG AND INTERNATIONAL FINANCE CORPORATION FOR THE FINANCIAL SUPPORT") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized O)FFICAL 130CUNIENTS 'IFC ADMINISTRATION ARRANGEMENT AMONG TF071837 IBRD/IDA TFO71823

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized O)FFICAL 130CUNIENTS 'IFC ADMINISTRATION ARRANGEMENT AMONG TF071837 IBRD/IDA TFO71823

Introduction to IFC &

Introduction to IFC & Prospects for Cooperation Ashgabat, Turkmenistan August 6, 2012 IFC s Structure Owned by 183 member countries IFC is the main driver of private sector development in the World Bank

Introduction to IFC & Prospects for Cooperation Ashgabat, Turkmenistan August 6, 2012 IFC s Structure Owned by 183 member countries IFC is the main driver of private sector development in the World Bank

Mobilizing Resources for Climate Finance

Mobilizing Resources for Climate Finance Dr Mattia Romani Deputy Director General Global Green Growth Institute - Seoul Senior Visiting Fellow Grantham Research Institute on Climate Change London School

Mobilizing Resources for Climate Finance Dr Mattia Romani Deputy Director General Global Green Growth Institute - Seoul Senior Visiting Fellow Grantham Research Institute on Climate Change London School

The impact of regulation and public policy on telecom sector performance Dr. Raúl L. Katz Adjunct Professor, Division of Finance and Economics

The impact of regulation and public policy on telecom sector performance Dr. Raúl L. Katz Adjunct Professor, Division of Finance and Economics Director, Business Strategy Research Columbia Institute of

The impact of regulation and public policy on telecom sector performance Dr. Raúl L. Katz Adjunct Professor, Division of Finance and Economics Director, Business Strategy Research Columbia Institute of

Rogers Reports Third Quarter 2009 Financial and Operating Results

Rogers Reports Third Quarter 2009 Financial and Operating Results Third Quarter Adjusted Operating Profit up 15% as Revenue Grows to Over $3 Billion; Wireless Network and Cable Operations Revenue Both

Rogers Reports Third Quarter 2009 Financial and Operating Results Third Quarter Adjusted Operating Profit up 15% as Revenue Grows to Over $3 Billion; Wireless Network and Cable Operations Revenue Both

José Chembeze (Dr. Charles E. Schlumberger) Transport Specialist

Transport Specialist") Joint ICAO/AFCAC Regional Symposium for African States on Airport and Air Navigation Services Infrastructure Financing Financing of Air Transport Projects x José Chembeze (Dr. Charles E. Schlumberger)

Joint ICAO/AFCAC Regional Symposium for African States on Airport and Air Navigation Services Infrastructure Financing Financing of Air Transport Projects x José Chembeze (Dr. Charles E. Schlumberger)

IFC s Approach to Risk

IFC s Approach to Risk INTERNATIONAL BANKING FORUM 2011 Brescia, 16-17 June 2011 Vittorio Di Bello Chief Credit Officer IFC World Bank Group Agenda IFC: Who we are, What we do IFC and Sustainability IFC

IFC s Approach to Risk INTERNATIONAL BANKING FORUM 2011 Brescia, 16-17 June 2011 Vittorio Di Bello Chief Credit Officer IFC World Bank Group Agenda IFC: Who we are, What we do IFC and Sustainability IFC

Infosys Technologies Limited Financial Release December 31, 2003

Infosys increases guidance for revenue and EPS for fiscal 2004 Bangalore, India January 9, 2004 Highlights Results for the quarter ended December 31, 2003 Income from software development services and

Infosys increases guidance for revenue and EPS for fiscal 2004 Bangalore, India January 9, 2004 Highlights Results for the quarter ended December 31, 2003 Income from software development services and

Telenor Group. Jon Fredrik Baksaas, CEO DNB Nordic TMT Conference

Telenor Group Jon Fredrik Baksaas, CEO DNB Nordic TMT Conference Disclaimer The following presentation is being made only to, and is only directed at, persons to whom such presentation may lawfully be

Telenor Group Jon Fredrik Baksaas, CEO DNB Nordic TMT Conference Disclaimer The following presentation is being made only to, and is only directed at, persons to whom such presentation may lawfully be

William Blair Growth Stock Conference. June 13, 2012

NLSN @ William Blair Growth Stock Conference June 13, 2012 Forward Looking Statements The following discussion contains forward-looking statements, including those about Nielsen s outlook and prospects,

NLSN @ William Blair Growth Stock Conference June 13, 2012 Forward Looking Statements The following discussion contains forward-looking statements, including those about Nielsen s outlook and prospects,

FDI linkages with innovation & technology-related benefits for SMEs

FDI linkages with innovation & technology-related benefits for SMEs David Brown Chief Operating Officer WWW.CZECH-INVENT.ORG Beirut June 21 2011 CzechINVENT Mission Not-for profit technology agency established

FDI linkages with innovation & technology-related benefits for SMEs David Brown Chief Operating Officer WWW.CZECH-INVENT.ORG Beirut June 21 2011 CzechINVENT Mission Not-for profit technology agency established

EBRD Communications Sector Assessment Conference. Activities of the TMT Team. 29 May 2009 Tbilisi

EBRD Communications Sector Assessment Conference Activities of the TMT Team 29 May 2009 Tbilisi Outline I. The European Bank for Reconstruction and Development (EBRD) II. III. EBRD regional presence Telecoms,

EBRD Communications Sector Assessment Conference Activities of the TMT Team 29 May 2009 Tbilisi Outline I. The European Bank for Reconstruction and Development (EBRD) II. III. EBRD regional presence Telecoms,

USCIB Trade and Investment Agenda 2018

USCIB Trade and Investment Agenda 2018 The United States Council for International Business (USCIB) corporate members represent $5 trillion in revenues and employ 11.5 million people worldwide across a

USCIB Trade and Investment Agenda 2018 The United States Council for International Business (USCIB) corporate members represent $5 trillion in revenues and employ 11.5 million people worldwide across a

Earnings Results for the Fiscal Year Ended March 31, 2008 (FY2007) Analyst Meeting. May 9, 2008 SOFTBANK CORP.

Analyst Meeting. May 9, 2008 SOFTBANK CORP.") Earnings Results for the Fiscal Year Ended March 31, 28 (FY27) Analyst Meeting May 9, 28 SOFTBANK CORP. 2 Content Accounting Finance Operations Items Page Consolidated P/L Analysis 4 Consolidated B/S Analysis

Earnings Results for the Fiscal Year Ended March 31, 28 (FY27) Analyst Meeting May 9, 28 SOFTBANK CORP. 2 Content Accounting Finance Operations Items Page Consolidated P/L Analysis 4 Consolidated B/S Analysis

The Imperative of Competitiveness in a Multilateral Trading System: What s s an LDC to Do?

The Imperative of Competitiveness in a Multilateral Trading System: What s s an LDC to Do? Preeti Arora World Bank National Dialogue on Aid for Trade January 17, 2008 Main points The global economy is

The Imperative of Competitiveness in a Multilateral Trading System: What s s an LDC to Do? Preeti Arora World Bank National Dialogue on Aid for Trade January 17, 2008 Main points The global economy is

OPERATING AND FINANCIAL REVIEW MANAGEMENT DISCUSSION AND ANALYSIS GROUP REVIEW. Operating revenue 18,825 18,

GROUP REVIEW GROUP (S$ million) (S$ million) Change (%) Operating revenue 18,825 18,071 4.2 EBITDA 5,219 5,119 1.9 EBITDA margin 27.7% 28.3% Share of associates pre-tax profits 2,005 2,141-6.4 EBITDA and

GROUP REVIEW GROUP (S$ million) (S$ million) Change (%) Operating revenue 18,825 18,071 4.2 EBITDA 5,219 5,119 1.9 EBITDA margin 27.7% 28.3% Share of associates pre-tax profits 2,005 2,141-6.4 EBITDA and

COMPANY REPORT TO THE GENERAL MEETING OF SHAREHOLDERS OF FORTHNET S.A. ON THE SHARE CAPITAL INCREASE OF FORTHNET S.A.

COMPANY REPORT TO THE GENERAL MEETING OF SHAREHOLDERS OF FORTHNET S.A. ON THE SHARE CAPITAL INCREASE OF FORTHNET S.A. INTRODUCTION At its meeting of 22 April 2008, the Board of Directors of FORTHNET S.A.

COMPANY REPORT TO THE GENERAL MEETING OF SHAREHOLDERS OF FORTHNET S.A. ON THE SHARE CAPITAL INCREASE OF FORTHNET S.A. INTRODUCTION At its meeting of 22 April 2008, the Board of Directors of FORTHNET S.A.

Globalization and the Developing Countries (for MABE Program Students)

") Globalization and the Developing Countries (for MABE Program Students) Prof. Shigeru T. OTSUBO GSID, Nagoya University August 2003 1 What is Globalization? --a traditional definition-- Globalization, defined

Globalization and the Developing Countries (for MABE Program Students) Prof. Shigeru T. OTSUBO GSID, Nagoya University August 2003 1 What is Globalization? --a traditional definition-- Globalization, defined

Measuring Payment System Development

Measuring Payment System Development Cape Town, April 7th, 2009 Jose Antonio Garcia Payment Systems Development Group Background, Rationale and Purpose for obtaining Payment Systems Indicators Requested

Measuring Payment System Development Cape Town, April 7th, 2009 Jose Antonio Garcia Payment Systems Development Group Background, Rationale and Purpose for obtaining Payment Systems Indicators Requested

EPORTING FROM NOVEMBER

EPORTING FROM NOVEMBER Context Case Studies Matching expectations, Looking ahead / / / / İSTANBUL, 5 NOVEMBER 2012 2 INTERACTIVE: Where do you live? 1. Asia 2. Middle East and North Africa 3. Europe 4.

EPORTING FROM NOVEMBER Context Case Studies Matching expectations, Looking ahead / / / / İSTANBUL, 5 NOVEMBER 2012 2 INTERACTIVE: Where do you live? 1. Asia 2. Middle East and North Africa 3. Europe 4.

INSTITUTIONAL INVESTORS + INFRASTRUCTURE FINANCING

INSTITUTIONAL INVESTORS + INFRASTRUCTURE FINANCING Fiona Stewart Oxford Infrastructure Conference July 2, 2015 ENHANCING INSTITUTIONAL INVESTORS ROLE IN INFRASTRUCTURE KEY BARRIERS Country selection and

INSTITUTIONAL INVESTORS + INFRASTRUCTURE FINANCING Fiona Stewart Oxford Infrastructure Conference July 2, 2015 ENHANCING INSTITUTIONAL INVESTORS ROLE IN INFRASTRUCTURE KEY BARRIERS Country selection and

Delivering mobile connectivity in MENA: A review of mobile sector taxation and licence extension. May 2017

Delivering mobile connectivity in MENA: A review of mobile sector taxation and licence extension May 2017 Executive Summary The report provides an overview of the tax and fee regime applied to mobile services

Delivering mobile connectivity in MENA: A review of mobile sector taxation and licence extension May 2017 Executive Summary The report provides an overview of the tax and fee regime applied to mobile services

Bahk Byongwon. Board Member, Korea API and Former Senior Economic Advisor to the President of Korea. Tokyo, Japan 11 May 2011

Bahk Byongwon Board Member, Korea API and Former Senior Economic Advisor to the President of Korea Tokyo, Japan 11 May 2011 Contents 1. European Bank for Reconstruction and Development (EBRD) 2. Black

Bahk Byongwon Board Member, Korea API and Former Senior Economic Advisor to the President of Korea Tokyo, Japan 11 May 2011 Contents 1. European Bank for Reconstruction and Development (EBRD) 2. Black

Hellas Group 3nd Quarter 2007 Results. November 15, 2007

Hellas Group 3nd Quarter 2007 Results November 15, 2007 Forward looking statement This presentation includes forward-looking statements. These forward-looking statements include all matters that are not

Hellas Group 3nd Quarter 2007 Results November 15, 2007 Forward looking statement This presentation includes forward-looking statements. These forward-looking statements include all matters that are not

PPI data update note 28 November Private activity in infrastructure down, but still around peak levels

PPI data update note 28 November 29 Private activity in infrastructure down, but still around peak levels Private activity in infrastructure showed mixed results in 28, according to just-released data

PPI data update note 28 November 29 Private activity in infrastructure down, but still around peak levels Private activity in infrastructure showed mixed results in 28, according to just-released data

Rethinking mobile taxation to improve connectivity

Rethinking mobile taxation to improve connectivity Summary Copyright 2019 GSM Association The GSMA represents the interests of mobile operators worldwide, uniting more than 750 operators with over 350

Rethinking mobile taxation to improve connectivity Summary Copyright 2019 GSM Association The GSMA represents the interests of mobile operators worldwide, uniting more than 750 operators with over 350

Risk Mitigation Strategy for Infrastructure Projects

2008/SOM3/IEG/SEM2/012 Risk Mitigation Strategy for Infrastructure Projects Submitted by: Peru Seminar on Recent Trends on Investment Liberalization and Facilitation in Transport and Telecommunication

2008/SOM3/IEG/SEM2/012 Risk Mitigation Strategy for Infrastructure Projects Submitted by: Peru Seminar on Recent Trends on Investment Liberalization and Facilitation in Transport and Telecommunication

Mobile segment revenues increased by 24.9% mainly driven by a substantial increase in traffic and enhanced service revenues.

Contact: Szabolcs Czenthe, Matáv IR +36-1-458-0437 Tamás Dancsecs, Matáv IR +36-1-457-6084 Zsolt Kerti, Matáv IR +36-1-458-0403 investor.relations@ln.matav.hu Belinda Bishop, Taylor Rafferty +44-(0)207-936-0400

Contact: Szabolcs Czenthe, Matáv IR +36-1-458-0437 Tamás Dancsecs, Matáv IR +36-1-457-6084 Zsolt Kerti, Matáv IR +36-1-458-0403 investor.relations@ln.matav.hu Belinda Bishop, Taylor Rafferty +44-(0)207-936-0400

Private activity in telecommunications twenty percent down in 2011

1990 1990 PPI data update note 77 September 2012 Private activity in telecommunications twenty percent down in In, ten new telecom projects with private participation reached financial or contractual closure.

1990 1990 PPI data update note 77 September 2012 Private activity in telecommunications twenty percent down in In, ten new telecom projects with private participation reached financial or contractual closure.

AT&T Inc. Financial Review 2012

AT&T Inc. Financial Review 2012 Selected Financial and Operating Data 30 Management s Discussion and Analysis of Financial Condition and Results of Operations 31 Consolidated Financial Statements 59 Notes

AT&T Inc. Financial Review 2012 Selected Financial and Operating Data 30 Management s Discussion and Analysis of Financial Condition and Results of Operations 31 Consolidated Financial Statements 59 Notes