One way to pump up ROE: Use more debt

|

|

|

- Sharyl Heath

- 5 years ago

- Views:

Transcription

1 One way to pump up ROE: Use more debt 175 ROE = ROC + D/E (ROC - i (1-t)) where, ROC = EBIT t (1 - tax rate) / Book value of Capital t-1 D/E = BV of Debt/ BV of Equity i = Interest Expense on Debt / BV of Debt t = Tax rate on ordinary income Note that Book value of capital = Book Value of Debt + Book value of Equity- Cash. 175

2 Decomposing ROE: Brahma in Brahma (now Ambev) had an extremely high return on equity, partly because it borrowed money at a rate well below its return on capital Return on Capital = 19.91% Debt/Equity Ratio = 77% After-tax Cost of Debt = 5.61% Return on Equity = ROC + D/E (ROC - i(1-t)) = 19.91% (19.91% %) = 30.92% This seems like an easy way to deliver higher growth in earnings per share. What (if any) is the downside? 176

3 Decomposing ROE: Titan Watches (India) 177 in 2000 Return on Capital = 9.54% Debt/Equity Ratio = 191% (book value terms) After-tax Cost of Debt = % Return on Equity = ROC + D/E (ROC - i(1-t)) = 9.54% (9.54% %) = 8.42% 177

4 178 II. Expected Growth in Net Income from noncash assets The limitation of the EPS fundamental growth equation is that it focuses on per share earnings and assumes that reinvested earnings are invested in projects earning the return on equity. To the extent that companies retain money in cash balances, the effect on net income can be muted. A more general version of expected growth in earnings can be obtained by substituting in the equity reinvestment into real investments (net capital expenditures and working capital) and modifying the return on equity definition to exclude cash: Net Income from non-cash assets = Net income Interest income from cash (1- t) Equity Reinvestment Rate = (Net Capital Expenditures + Change in Working Capital) (1 - Debt Ratio)/ Net Income from non-cash assets Non-cash ROE = Net Income from non-cash assets/ (BV of Equity Cash) Expected Growth Net Income = Equity Reinvestment Rate * Non-cash ROE 178

5 179 Estimating expected growth in net income from non-cash assets: Coca Cola in 2010 In 2010, Coca Cola reported net income of $11,809 million. It had a total book value of equity of $25,346 million at the end of Coca Cola had a cash balance of $7,021 million at the end of 2009, on which it earned income of $105 million in Coca Cola had capital expenditures of $2,215 million, depreciation of $1,443 million and reported an increase in working capital of $335 million. Coca Cola s total debt increased by $150 million during Equity Reinvestment = = $957 million Non-cash Net Income = $11,809 - $105 = $ 11,704 million Non-cash book equity = $25,346 - $7021 = $18,325 million Reinvestment Rate = $957 million/ $11,704 million= 8.18% Non-cash ROE = $11,704 million/ $18,325 million = 63.87% Expected growth rate = 8.18% * 63.87% = 5.22% 179

6 180 III. Expected Growth in EBIT And Fundamentals: Stable ROC and Reinvestment Rate When looking at growth in operating income, the definitions are Reinvestment Rate = (Net Capital Expenditures + Change in WC)/EBIT(1-t) Return on Investment = ROC = EBIT(1-t)/(BV of Debt + BV of Equity-Cash) Reinvestment Rate and Return on Capital Expected Growth rate in Operating Income = (Net Capital Expenditures + Change in WC)/EBIT(1-t) * ROC = Reinvestment Rate * ROC Proposition: The net capital expenditure needs of a firm, for a given growth rate, should be inversely proportional to the quality of its investments. 180

7 181 Estimating Growth in Operating Income, if fundamentals stay unchanged Cisco s Fundamentals Reinvestment Rate = % Return on Capital =34.07% Expected Growth in EBIT =(1.0681)(.3407) = 36.39% Motorola s Fundamentals Reinvestment Rate = 52.99% Return on Capital = 12.18% Expected Growth in EBIT = (.5299)(.1218) = 6.45% Cisco s expected growth rate is clearly much higher than Motorola s sustainable growth rate. As a potential investor in Cisco, what would worry you the most about this forecast? a. That Cisco s return on capital may be overstated (why?) b. That Cisco s reinvestment comes mostly from acquisitions (why?) c. That Cisco is getting bigger as a firm (why?) d. That Cisco is viewed as a star (why?) e. All of the above 181

and its limits")

8 182 The Magical Number: ROIC (or any accounting return) and its limits 182

9 183 IV. Operating Income Growth when Return on Capital is Changing When the return on capital is changing, there will be a second component to growth, positive if the return on capital is increasing and negative if the return on capital is decreasing. If ROC t is the return on capital in period t and ROC t+1 is the return on capital in period t+1, the expected growth rate in operating income will be: Expected Growth Rate = ROC t+1 * Reinvestment rate +(ROC t+1 ROC t ) / ROC t If the change is over multiple periods, the second component should be spread out over each period. 183

10 Motorola s Growth Rate 184 Motorola s current return on capital is 12.18% and its reinvestment rate is 52.99%. We expect Motorola s return on capital to rise to 17.22% over the next 5 years (which is half way towards the industry average) Expected Growth Rate = ROC New Investments *Reinvestment Rate Current + {[1+(ROC In 5 years -ROC Current )/ROC Current] 1/5-1} =.1722* { [1+( )/.1218]1/5-1} =.1629 or 16.29% One way to think about this is to decompose Motorola s expected growth into Growth from new investments:.1722*5299= 9.12% Growth from more efficiently using existing investments: 16.29%-9.12%= 7.17% Note that I am assuming that the new investments start making 17.22% immediately, while allowing for existing assets to improve returns gradually 184

11 The Value of Growth 185 Expected growth = Growth from new investments + Efficiency growth = Reinv Rate * ROC + (ROC t -ROC t-1 )/ROC t-1 Assume that your cost of capital is 10%. As an investor, rank these firms in the order of most value growth to least value growth. 185

12 186 Growth IV Top Down Growth

13 187 Estimating Growth when Operating Income is Negative or Margins are changing All of the fundamental growth equations assume that the firm has a return on equity or return on capital it can sustain in the long term. When operating income is negative or margins are expected to change over time, we use a three step process to estimate growth: Estimate growth rates in revenues over time n Determine the total market (given your business model) and estimate the market share that you think your company will earn. n Decrease the growth rate as the firm becomes larger n Keep track of absolute revenues to make sure that the growth is feasible Estimate expected operating margins each year n Set a target margin that the firm will move towards n Adjust the current margin towards the target margin Estimate the capital that needs to be invested to generate revenue growth and expected margins n Estimate a sales to capital ratio that you will use to generate reinvestment needs each year. 187

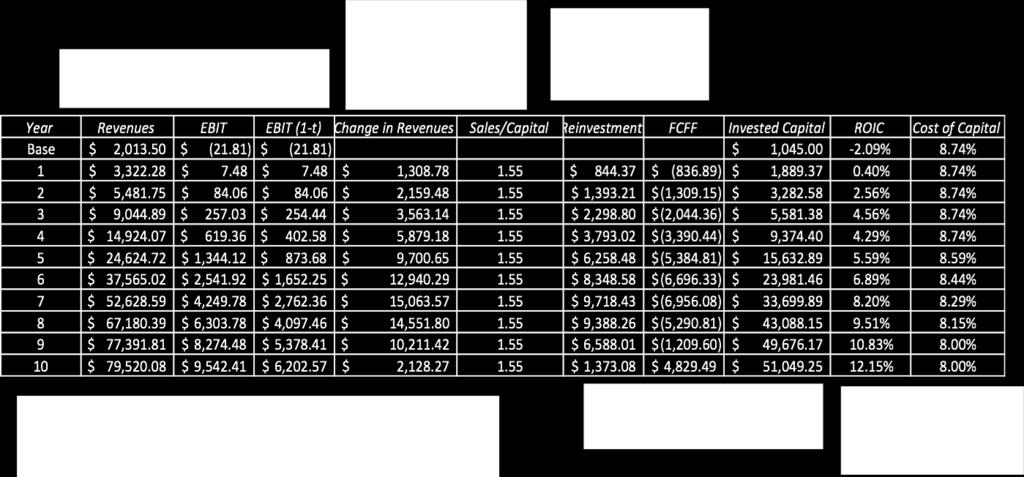

14 Tesla in July 2015: Growth and Profitability

15 Tesla: Reinvestment and Profitability

16 Expected Growth Rate Equity Earnings Operating Income Analysts Fundamentals Historical Fundamentals Historical Stable ROC Changing ROC Negative Earnings ROC * Reinvestment Rate ROCt+1*Reinvestment Rate + (ROCt+1-ROCt)/ROCt Earnings per share Net Income 1. Revenue Growth 2. Operating Margins 3. Reinvestment Needs Stable ROE Changing ROE Stable ROE Changing ROE ROE * Retention Ratio 190 ROEt+1*Retention Ratio + (ROEt+1-ROEt)/ROEt ROE * Equity Reinvestment Ratio ROEt+1*Eq. Reinv Ratio + (ROEt+1-ROEt)/ROEt

17 191 CLOSURE IN VALUATION The Big Enchilada

18 Getting Closure in Valuation 192 A publicly traded firm potentially has an infinite life. The value is therefore the present value of cash flows forever. Value = t= CF t t=1 (1+r) t Since we cannot estimate cash flows forever, we estimate cash flows for a growth period and then estimate a terminal value, to capture the value at the end of the period: Value = t=n t=1 CF t Terminal Value + (1+r) t (1+r) N 192

19 Ways of Estimating Terminal Value 193 Terminal Value Liquidation Value Multiple Approach Stable Growth Model Most useful when assets are separable and marketable Easiest approach but makes the valuation a relative valuation Technically soundest, but requires that you make judgments about when the firm will grow at a stable rate which it can sustain forever, and the excess returns (if any) that it will earn during the period. 193

20 1. Obey the growth cap 194 When a firm s cash flows grow at a constant rate forever, the present value of those cash flows can be written as: Value = Expected Cash Flow Next Period / (r - g) where, r = Discount rate (Cost of Equity or Cost of Capital) g = Expected growth rate The stable growth rate cannot exceed the growth rate of the economy but it can be set lower. If you assume that the economy is composed of high growth and stable growth firms, the growth rate of the latter will probably be lower than the growth rate of the economy. The stable growth rate can be negative. The terminal value will be lower and you are assuming that your firm will disappear over time. If you use nominal cashflows and discount rates, the growth rate should be nominal in the currency in which the valuation is denominated. One simple proxy for the nominal growth rate of the economy is the riskfree rate. 194

21 Risk free Rates and Nominal GDP Growth Risk free Rate = Expected Inflation + Expected Real Interest Rate The real interest rate is what borrowers agree to return to lenders in real goods/services. Nominal GDP Growth = Expected Inflation + Expected Real Growth The real growth rate in the economy measures the expected growth in the production of goods and services. The argument for Risk free rate = Nominal GDP growth 1. In the long term, the real growth rate cannot be lower than the real interest rate, since you have the growth in goods/services has to be enough to cover the promised rate. 2. In the long term, the real growth rate can be higher than the real interest rate, to compensate risk taking. However, as economies mature, the difference should get smaller and since there will be growth companies in the economy, it is prudent to assume that the extra growth comes from these companies. Period 10-Year T.Bond Rate Inflation Rate Real GDP Growth Nominal GDP growth rate Nominal GDP - T.Bond Rate % 3.61% 3.06% 6.67% 0.74% % 4.49% 3.50% 7.98% 2.15% % 3.26% 3.04% 6.30% -0.58% % 1.66% 1.47% 3.14% 0.57%

22 196 A Practical Reason for using the Risk free Rate Cap Preserve Consistency You are implicitly making assumptions about nominal growth in the economy, with your risk free rate. Thus, with a low risk free rate, you are assuming low nominal growth in the economy (with low inflation and low real growth) and with a high risk free rate, a high nominal growth rate in the economy. If you make an explicit assumption about nominal growth in cash flows that is at odds with your implicit growth assumption in the denominator, you are being inconsistent and bias your valuations: If you assume high nominal growth in the economy, with a low risk free rate, you will over value businesses. If you assume low nominal growth rate in the economy, with a high risk free rate, you will under value businesses. 196

23 2. Don t wait too long 197 Assume that you are valuing a young, high growth firm with great potential, just after its initial public offering. How long would you set your high growth period? a. < 5 years b. 5 years c. 10 years d. >10 years While analysts routinely assume very long high growth periods (with substantial excess returns during the periods), the evidence suggests that they are much too optimistic. Most growth firms have difficulty sustaining their growth for long periods, especially while earning excess returns. 197

24 And tie to competitive advantages 198 Recapping a key lesson about growth, it is not growth per se that creates value but growth with excess returns. For growth firms to continue to generate value creating growth, they have to be able to keep the competition at bay. Proposition 1: The stronger and more sustainable the competitive advantages, the longer a growth company can sustain value creating growth. Proposition 2: Growth companies with strong and sustainable competitive advantages are rare. 198

25 3. Don t forget that growth has to be earned In the section on expected growth, we laid out the fundamental equation for growth: Growth rate = Reinvestment Rate * Return on invested capital + Growth rate from improved efficiency In stable growth, you cannot count on efficiency delivering growth and you have to reinvest to deliver the growth rate that you have forecast. Consequently, your reinvestment rate in stable growth will be a function of your stable growth rate and what you believe the firm will earn as a return on capital in perpetuity: Reinvestment Rate = Stable growth rate/ Stable period ROC = g/ ROC Your terminal value equation can then be rewritten as: Terminal Value in year n =./ (56 9 :;< ) (>?@7?A >BCD7BE6F) 199

26 The Big Assumption 200 Growth rate forever Return on capital in perpetuity 6% 8% 10% 12% 14% 0.0% $1,000 $1,000 $1,000 $1,000 $1, % $965 $987 $1,000 $1,009 $1, % $926 $972 $1,000 $1,019 $1, % $882 $956 $1,000 $1,029 $1, % $833 $938 $1,000 $1,042 $1, % $778 $917 $1,000 $1,056 $1, % $714 $893 $1,000 $1,071 $1,122 Terminal value for a firm with expected after-tax operating income of $100 million in year n+1 and a cost of capital of 10%. 200

who argue that the return on capital should always be equal to cost of")

27 Excess Returns to Zero? 201 There are some (McKinsey, for instance) who argue that the return on capital should always be equal to cost of capital in stable growth. But excess returns seem to persist for very long time periods. 201

28 And don t fall for sleight of hand 202 A typical assumption in many DCF valuations, when it comes to stable growth, is that capital expenditures offset depreciation and there are no working capital needs. Stable growth firms, we are told, just have to make maintenance cap ex (replacing existing assets ) to deliver growth. If you make this assumption, what expected growth rate can you use in your terminal value computation? What if the stable growth rate = inflation rate? Is it okay to make this assumption then? 202

29 4. Be internally consistent 203 Risk and costs of equity and capital: Stable growth firms tend to Have betas closer to one Have debt ratios closer to industry averages (or mature company averages) Country risk premiums (especially in emerging markets should evolve over time) The excess returns at stable growth firms should approach (or become) zero. ROC -> Cost of capital and ROE -> Cost of equity The reinvestment needs and dividend payout ratios should reflect the lower growth and excess returns: Stable period payout ratio = 1 - g/ ROE Stable period reinvestment rate = g/ ROC 203

A Test. a. -600% b. +600% c. +120% d. Cannot be estimated. Aswath Damodaran

A Test 159 You are trying to estimate the growth rate in earnings per share at Time Warner from 1996 to 1997. In 1996, the earnings per share was a deficit of $0.05. In 1997, the expected earnings per

A Test 159 You are trying to estimate the growth rate in earnings per share at Time Warner from 1996 to 1997. In 1996, the earnings per share was a deficit of $0.05. In 1997, the expected earnings per

CHAPTER 6 ESTIMATING FIRM VALUE

1 CHAPTER 6 ESTIMATING FIRM VALUE In the last chapter, you examined the determinants of expected growth. Firms that reinvest substantial portions of their earnings and earn high returns on these investments

1 CHAPTER 6 ESTIMATING FIRM VALUE In the last chapter, you examined the determinants of expected growth. Firms that reinvest substantial portions of their earnings and earn high returns on these investments

II. Analyst Forecasts of Growth

II. Analyst Forecasts of Growth 149 While the job of an analyst is to find under and over valued stocks in the sectors that they follow, a significant propor@on of an analyst s @me (outside of selling)

II. Analyst Forecasts of Growth 149 While the job of an analyst is to find under and over valued stocks in the sectors that they follow, a significant propor@on of an analyst s @me (outside of selling)

Valuation. Aswath Damodaran. Aswath Damodaran 186

Valuation Aswath Damodaran Aswath Damodaran 186 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects

Valuation Aswath Damodaran Aswath Damodaran 186 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde. Aswath Damodaran! 1!

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde Aswath Damodaran! 1! First Principles! Aswath Damodaran! 2! Three approaches to valuation! Intrinsic

Valuation! Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde Aswath Damodaran! 1! First Principles! Aswath Damodaran! 2! Three approaches to valuation! Intrinsic

Valuation Inferno: Dante meets

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

Estimating growth in EPS: Deutsche Bank in January 2008

238 Estimating growth in EPS: Deutsche Bank in January 2008 In 2007, Deutsche Bank reported net income of 6.51 billion Euros on a book value of equity of 33.475 billion Euros at the start of the year (end

238 Estimating growth in EPS: Deutsche Bank in January 2008 In 2007, Deutsche Bank reported net income of 6.51 billion Euros on a book value of equity of 33.475 billion Euros at the start of the year (end

DCF Choices: Equity Valuation versus Firm Valuation

5 DCF Choices: Equity Valuation versus Firm Valuation Firm Valuation: Value the entire business Assets Liabilities Existing Investments Generate cashflows today Includes long lived (fixed) and short-lived(working

5 DCF Choices: Equity Valuation versus Firm Valuation Firm Valuation: Value the entire business Assets Liabilities Existing Investments Generate cashflows today Includes long lived (fixed) and short-lived(working

CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION

1 CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION In the last chapter, you were introduced to the notion that the value of an asset is determined by its expected cash flows

1 CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION In the last chapter, you were introduced to the notion that the value of an asset is determined by its expected cash flows

Aswath Damodaran 1. Intrinsic Valuation

1 Valuation: Lecture Note Packet 1 Intrinsic Valuation Updated: September 2016 The essence of intrinsic value 2 In intrinsic valuation, you value an asset based upon its fundamentals (or intrinsic characteristics).

1 Valuation: Lecture Note Packet 1 Intrinsic Valuation Updated: September 2016 The essence of intrinsic value 2 In intrinsic valuation, you value an asset based upon its fundamentals (or intrinsic characteristics).

CHAPTER 4 SHOW ME THE MONEY: THE BASICS OF VALUATION

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

Valuation. Aswath Damodaran For the valuations in this presentation, go to Seminars/ Presentations. Aswath Damodaran 1

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

Valuation. Aswath Damodaran For the valuations in this presentation, go to Seminars/ Presentations. Aswath Damodaran 1

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

Valuation Aswath Damodaran http://www.damodaran.com For the valuations in this presentation, go to Seminars/ Presentations Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot

Aswath Damodaran 217 VALUATION. Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde

217 VALUATION Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde First Principles 218 218 Three approaches to valuaeon 219 Intrinsic valuaeon: The value of an asset

217 VALUATION Cynic: A person who knows the price of everything but the value of nothing.. Oscar Wilde First Principles 218 218 Three approaches to valuaeon 219 Intrinsic valuaeon: The value of an asset

In the previous chapter, we examined the determinants of expected growth. Firms

ch12_p304-322.qxd 12/5/11 2:14 PM Page 304 CHAPTER 12 Closure in Valuation: Estimating Terminal Value In the previous chapter, we examined the determinants of expected growth. Firms that reinvest substantial

ch12_p304-322.qxd 12/5/11 2:14 PM Page 304 CHAPTER 12 Closure in Valuation: Estimating Terminal Value In the previous chapter, we examined the determinants of expected growth. Firms that reinvest substantial

Twelve Myths in Valuation

Twelve Myths in Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Why do valuation? " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 1. Valuation is a science

Twelve Myths in Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Why do valuation? " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 1. Valuation is a science

III. One-Time and Non-recurring Charges

III. One-Time and Non-recurring Charges 130 Assume that you are valuing a firm that is reporting a loss of $ 500 million, due to a one-time charge of $ 1 billion. What is the earnings you would use in

III. One-Time and Non-recurring Charges 130 Assume that you are valuing a firm that is reporting a loss of $ 500 million, due to a one-time charge of $ 1 billion. What is the earnings you would use in

Step 6: Be ready to modify narrative as events unfold

266 Step 6: Be ready to modify narrative as events unfold Narrative Break/End Narrative Shift Narrative Change (Expansionor Contraction) Events, external (legal, political or economic) or internal (management,

266 Step 6: Be ready to modify narrative as events unfold Narrative Break/End Narrative Shift Narrative Change (Expansionor Contraction) Events, external (legal, political or economic) or internal (management,

Valuation Inferno: Dante meets

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here www.damodaran.com 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business by discounting cash flow to the firm

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here www.damodaran.com 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business by discounting cash flow to the firm

The Dark Side of Valuation Valuing young, high growth companies

The Dark Side of Valuation Valuing young, high growth companies Aswath Damodaran Aswath Damodaran 1 Risk Adjusted Value: Three Basic Propositions The value of an asset is the present value of the expected

The Dark Side of Valuation Valuing young, high growth companies Aswath Damodaran Aswath Damodaran 1 Risk Adjusted Value: Three Basic Propositions The value of an asset is the present value of the expected

Return on Capital (ROC), Return on Invested Capital (ROIC) and Return on Equity (ROE): Measurement and Implications

, Return on Invested Capital (ROIC) and Return on Equity (ROE): Measurement and Implications") 1 Return on Capital (ROC), Return on Invested Capital (ROIC) and Return on Equity (ROE): Measurement and Implications Aswath Damodaran Stern School of Business July 2007 2 ROC, ROIC and ROE: Measurement

1 Return on Capital (ROC), Return on Invested Capital (ROIC) and Return on Equity (ROE): Measurement and Implications Aswath Damodaran Stern School of Business July 2007 2 ROC, ROIC and ROE: Measurement

Measuring Investment Returns

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle

Measuring Investment Returns Aswath Damodaran Stern School of Business Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle

Aswath Damodaran. Value Trade Off. Cash flow benefits - Tax benefits - Better project choices. What is the cost to the firm of hedging this risk?

Value Trade Off Negligible What is the cost to the firm of hedging this risk? High Cash flow benefits - Tax benefits - Better project choices Is there a significant benefit in terms of higher cash flows

Value Trade Off Negligible What is the cost to the firm of hedging this risk? High Cash flow benefits - Tax benefits - Better project choices Is there a significant benefit in terms of higher cash flows

Aswath Damodaran. ROE = 16.03% Retention Ratio = 12.42% g = Riskfree rate = 2.17% Assume that earnings on the index will grow at same rate as economy.

Valuing the S&P 500: Augmented Dividends and Fundamental Growth January 2015 Rationale for model Why augmented dividends? Because companies are increasing returning cash in the form of stock buybacks Why

Valuing the S&P 500: Augmented Dividends and Fundamental Growth January 2015 Rationale for model Why augmented dividends? Because companies are increasing returning cash in the form of stock buybacks Why

Valuation: Closing Thoughts

Valuation: Closing Thoughts Spring 2012 It ain t over till its over Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately)

Valuation: Closing Thoughts Spring 2012 It ain t over till its over Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately)

Relative vs. fundamental valuation

Relative Valuation Relative vs. fundamental valuation The DCF model is a method of fundamental valuation. Value of equity is the present value of future cash flows. Ignores the current level of the stock

Relative Valuation Relative vs. fundamental valuation The DCF model is a method of fundamental valuation. Value of equity is the present value of future cash flows. Ignores the current level of the stock

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. You have been asked to assess the impact of a proposed acquisition

Value Enhancement: Back to Basics

Value Enhancement: Back to Basics Aswath Damodaran NACVA Conference Aswath Damodaran 1 Price Enhancement versus Value Enhancement Aswath Damodaran 2 DISCOUNTED CASHFLOW VALUATION Cashflow to Firm EBIT

Value Enhancement: Back to Basics Aswath Damodaran NACVA Conference Aswath Damodaran 1 Price Enhancement versus Value Enhancement Aswath Damodaran 2 DISCOUNTED CASHFLOW VALUATION Cashflow to Firm EBIT

Valuation. Aswath Damodaran Aswath Damodaran 1

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

The Dark Side of Valuation Dante meets DCF

The Dark Side of Valuation Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran! 1! DCF Choices: Equity versus Firm Firm Valuation: Value the entire

The Dark Side of Valuation Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran! 1! DCF Choices: Equity versus Firm Firm Valuation: Value the entire

CHAPTER 10 FROM EARNINGS TO CASH FLOWS

1 CHAPTER 10 FROM EARNINGS TO CASH FLOWS The value of an asset comes from its capacity to generate cash flows. When valuing a firm, these cash flows should be after taxes, prior to debt payments and after

1 CHAPTER 10 FROM EARNINGS TO CASH FLOWS The value of an asset comes from its capacity to generate cash flows. When valuing a firm, these cash flows should be after taxes, prior to debt payments and after

Valuation. Aswath Damodaran Aswath Damodaran 1

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 A philosophical basis

LET THE GAMES BEGIN TIME TO VALUE COMPANIES..

239 LET THE GAMES BEGIN TIME TO VALUE COMPANIES.. Let s have some fun! Equity Risk Premiums in ValuaHon 240 The equity risk premiums that I have used in the valuahons that follow reflect my thinking (and

239 LET THE GAMES BEGIN TIME TO VALUE COMPANIES.. Let s have some fun! Equity Risk Premiums in ValuaHon 240 The equity risk premiums that I have used in the valuahons that follow reflect my thinking (and

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Aswath Damodaran Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach Value = t=n CF t t=1(1+ r) t where CF t is the cash flow in period t, r is the discount

Discounted Cash Flow Valuation Aswath Damodaran Aswath Damodaran 1 Discounted Cashflow Valuation: Basis for Approach Value = t=n CF t t=1(1+ r) t where CF t is the cash flow in period t, r is the discount

Relative vs. fundamental valuation

Relative Valuation Relative vs. fundamental valuation The DCF model is a method of fundamental valuation. Value of equity is the present value of future cash flows. Ignores the current level of the stock

Relative Valuation Relative vs. fundamental valuation The DCF model is a method of fundamental valuation. Value of equity is the present value of future cash flows. Ignores the current level of the stock

Netflix Studio : My Analysis, Not necessarily the analysis. Aswath Damodaran

Netflix Studio : My Analysis, Not necessarily the analysis Aswath Damodaran Executive Summary The cost of capital for the cash flows from the studio, reflecting its risk (content production) and its focus

Netflix Studio : My Analysis, Not necessarily the analysis Aswath Damodaran Executive Summary The cost of capital for the cash flows from the studio, reflecting its risk (content production) and its focus

PE Ratios. Aswath Damodaran. Aswath Damodaran 1

PE Ratios Aswath Damodaran Aswath Damodaran 1 Price Earnings Ratio: Definition PE = Market Price per Share / Earnings per Share There are a number of variants on the basic PE ratio in use. They are based

PE Ratios Aswath Damodaran Aswath Damodaran 1 Price Earnings Ratio: Definition PE = Market Price per Share / Earnings per Share There are a number of variants on the basic PE ratio in use. They are based

Valuing Equity in Firms in Distress!

Valuing Equity in Firms in Distress! Aswath Damodaran http://www.damodaran.com Aswath Damodaran! 1! The Going Concern Assumption! Traditional valuation techniques are built on the assumption of a going

Valuing Equity in Firms in Distress! Aswath Damodaran http://www.damodaran.com Aswath Damodaran! 1! The Going Concern Assumption! Traditional valuation techniques are built on the assumption of a going

VALUATION: FUTURE GROWTH AND CASH FLOWS. You will be wrong 100% of the Eme and it is okay.

1 VALUATION: FUTURE GROWTH AND CASH FLOWS You will be wrong 100% of the Eme and it is okay. Set Up and Objective 1: What is corporate finance 2: The Objective: Utopia and Let Down 3: The Objective: Reality

1 VALUATION: FUTURE GROWTH AND CASH FLOWS You will be wrong 100% of the Eme and it is okay. Set Up and Objective 1: What is corporate finance 2: The Objective: Utopia and Let Down 3: The Objective: Reality

Valuation: Closing Thoughts

Valuation: Closing Thoughts Fall 2012 It ain t over till its over Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately)

Valuation: Closing Thoughts Fall 2012 It ain t over till its over Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately)

The value of an asset comes from its capacity to generate cash flows. When valuing

ch10_p249-269.qxd 12/2/11 2:04 PM Page 249 CHAPTER 10 From Earnings to Cash Flows The value of an asset comes from its capacity to generate cash flows. When valuing a firm, these cash flows should be after

ch10_p249-269.qxd 12/2/11 2:04 PM Page 249 CHAPTER 10 From Earnings to Cash Flows The value of an asset comes from its capacity to generate cash flows. When valuing a firm, these cash flows should be after

Case 3: BP: Summary of Dividend Policy:

208 Case 3: BP: Summary of Dividend Policy: 1982-1991 Summary of calculations Average Standard Deviation Maximum Minimum Free CF to Equity $571.10 $1,382.29 $3,764.00 ($612.50) Dividends $1,496.30 $448.77

208 Case 3: BP: Summary of Dividend Policy: 1982-1991 Summary of calculations Average Standard Deviation Maximum Minimum Free CF to Equity $571.10 $1,382.29 $3,764.00 ($612.50) Dividends $1,496.30 $448.77

Mandated Dividend Payouts

Mandated Dividend Payouts 207 Assume now that the government decides to mandate a minimum dividend payout for all companies. Given our discussion of FCFE, what types of companies will be hurt the most

Mandated Dividend Payouts 207 Assume now that the government decides to mandate a minimum dividend payout for all companies. Given our discussion of FCFE, what types of companies will be hurt the most

1. Mul'ples have skewed distribu'ons

1. Mul'ples have skewed distribu'ons 14 PE Ra&os for US stocks: January 2015 700. 600. 500. 400. 300. Current Trailing Forward 200. 100. 0. 0.01 To 4 4 To 8 8 To 12 12 To 16 16 To 20 20 To 24 24 To 28

1. Mul'ples have skewed distribu'ons 14 PE Ra&os for US stocks: January 2015 700. 600. 500. 400. 300. Current Trailing Forward 200. 100. 0. 0.01 To 4 4 To 8 8 To 12 12 To 16 16 To 20 20 To 24 24 To 28

Value Enhancement: Back to Basics. Aswath Damodaran

Value Enhancement: Back to Basics 86 Price Enhancement versus Value Enhancement 87 The Paths to Value Creation Using the DCF framework, there are four basic ways in which the value of a firm can be enhanced:

Value Enhancement: Back to Basics 86 Price Enhancement versus Value Enhancement 87 The Paths to Value Creation Using the DCF framework, there are four basic ways in which the value of a firm can be enhanced:

Week 6 Equity Valuation 1

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Three views of the gap

Three views of the gap The Efficient Marketer The value extremist The pricing extremist View of the gap The gaps between price and value, if they do occur, are random. You view pricers as dilettantes who

Three views of the gap The Efficient Marketer The value extremist The pricing extremist View of the gap The gaps between price and value, if they do occur, are random. You view pricers as dilettantes who

65.98% 6.59% 4.35% % 19.92% 9.18%

10 Illustration 32.2: An EVA Valuation of Boeing - 1998 The equivalence of traditional DCF valuation and EVA valuation can be illustrated for Boeing. We begin with a discounted cash flow valuation of Boeing

10 Illustration 32.2: An EVA Valuation of Boeing - 1998 The equivalence of traditional DCF valuation and EVA valuation can be illustrated for Boeing. We begin with a discounted cash flow valuation of Boeing

Breaking out G&A Costs into fixed and variable components: A simple example

230 Breaking out G&A Costs into fixed and variable components: A simple example Assume that you have a time series of revenues and G&A costs for a company. What percentage of the G&A cost is variable?

230 Breaking out G&A Costs into fixed and variable components: A simple example Assume that you have a time series of revenues and G&A costs for a company. What percentage of the G&A cost is variable?

FINAL EXAM SOLUTIONS

FINAL EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Wednesday, December 14, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

FINAL EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Wednesday, December 14, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

DIVERSIFICATION, CONTROL & LIQUIDITY: THE DISCOUNT TRIFECTA. Aswath Damodaran

DIVERSIFICATION, CONTROL & LIQUIDITY: THE DISCOUNT TRIFECTA Aswath Damodaran www.damodran.com Fundamental Assumptions The Diversified Investor: Investors are rational and attempt to maximize expected returns,

DIVERSIFICATION, CONTROL & LIQUIDITY: THE DISCOUNT TRIFECTA Aswath Damodaran www.damodran.com Fundamental Assumptions The Diversified Investor: Investors are rational and attempt to maximize expected returns,

PowerPoint. to accompany. Chapter 9. Valuing Shares

PowerPoint to accompany Chapter 9 Valuing Shares 9.1 Share Basics Ordinary share: a share of ownership in the corporation, which gives its owner rights to vote on the election of directors, mergers or

PowerPoint to accompany Chapter 9 Valuing Shares 9.1 Share Basics Ordinary share: a share of ownership in the corporation, which gives its owner rights to vote on the election of directors, mergers or

Discount Rates: III. Relative Risk Measures. Aswath Damodaran

79 Discount Rates: III Relative Risk Measures 80 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

79 Discount Rates: III Relative Risk Measures 80 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

The Dark Side of Valuation

The Dark Side of Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 The Lemming Effect... Aswath Damodaran 2 To make our estimates, we draw our information from.. The firm

The Dark Side of Valuation Aswath Damodaran http://www.stern.nyu.edu/~adamodar Aswath Damodaran 1 The Lemming Effect... Aswath Damodaran 2 To make our estimates, we draw our information from.. The firm

THE FINANCING DECISION

1 THE FINANCING DECISION You can have too much debt or too little.. Debt Ratios across Companies 2 2 Debt Ratios across Sectors 3 3 The Financial Balance Sheet 4 Assets Liabilities Existing Investments

1 THE FINANCING DECISION You can have too much debt or too little.. Debt Ratios across Companies 2 2 Debt Ratios across Sectors 3 3 The Financial Balance Sheet 4 Assets Liabilities Existing Investments

Valuation: Closing Thoughts

Valuation: Closing Thoughts Spring 2010 Aswath Damodaran Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately) to

Valuation: Closing Thoughts Spring 2010 Aswath Damodaran Aswath Damodaran! 1! Back to the very beginning: Approaches to Valuation Discounted cashflow valuation, where we try (sometimes desperately) to

Valuation and Tax Policy

Valuation and Tax Policy Lakehead University Winter 2005 Formula Approach for Valuing Companies Let EBIT t Earnings before interest and taxes at time t T Corporate tax rate I t Firm s investments at time

Valuation and Tax Policy Lakehead University Winter 2005 Formula Approach for Valuing Companies Let EBIT t Earnings before interest and taxes at time t T Corporate tax rate I t Firm s investments at time

Earnings per Share Payout Ratio 10% 20% 30% 40% 45%

Money & Capital Markets Fall 2011 Homework #3 Due: Friday, Nov. 11 th 1. An analyst has made the following forecasts for a corporation s earnings and payout ratio. The analyst believes that after 2016,

Money & Capital Markets Fall 2011 Homework #3 Due: Friday, Nov. 11 th 1. An analyst has made the following forecasts for a corporation s earnings and payout ratio. The analyst believes that after 2016,

Valuation. Aswath Damodaran. Aswath Damodaran 1

Valuation Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects

Valuation Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should be higher for riskier projects

chapter, you look at valuation from the perspective of the managers of the firms. Unlike

1 VALUE ENHANCEMENT CHAPTER 12 In all the valuations so far in this book, you have taken the perspective of an investor valuing a firm from the outside. Given how Cisco, Motorola, Amazon, Ariba and Rediff

1 VALUE ENHANCEMENT CHAPTER 12 In all the valuations so far in this book, you have taken the perspective of an investor valuing a firm from the outside. Given how Cisco, Motorola, Amazon, Ariba and Rediff

FINAL EXAM SOLUTIONS

FINAL EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Module 2 Wednesday, December 7, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

FINAL EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Module 2 Wednesday, December 7, 2005 INSTRUCTIONS: 1. You have 2 hours to complete

CHAPTER 15 COST OF CAPITAL

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

Valuation. Aswath Damodaran Aswath Damodaran 1

Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 Misconceptions about Valuation

Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 Misconceptions about Valuation

CORPORATE FINANCE FINAL EXAM: FALL 1992

Practice finals CORPORATE FINANCE FINAL EXAM: FALL 1992 1. You have been asked to analyze the capital structure of DASA Inc, and make recommendations on a future course of action. DASA Inc. has 40 million

Practice finals CORPORATE FINANCE FINAL EXAM: FALL 1992 1. You have been asked to analyze the capital structure of DASA Inc, and make recommendations on a future course of action. DASA Inc. has 40 million

The Dark Side of Valuation: Firms with no Earnings, no History and no. Comparables. Can Amazon.com be valued? Aswath Damodaran

The Dark Side of Valuation: Firms with no Earnings, no History and no Comparables Can Amazon.com be valued? Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 adamodar@stern.nyu.edu

The Dark Side of Valuation: Firms with no Earnings, no History and no Comparables Can Amazon.com be valued? Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 adamodar@stern.nyu.edu

Key Expense Assumptions

Key Expense Assumptions 204 The operating expenses are assumed to be 60% of the revenues at the parks, and 75% of revenues at the resort properties. Disney will also allocate corporate general and administrative

Key Expense Assumptions 204 The operating expenses are assumed to be 60% of the revenues at the parks, and 75% of revenues at the resort properties. Disney will also allocate corporate general and administrative

Aswath Damodaran! 1! SESSION 8: ESTIMATING GROWTH

1! SESSION 8: ESTIMATING GROWTH Growth in Earnings 2! Look at the past The historical growth in earnings per share is usually a good starcng point for growth escmacon Look at what others are escmacng Analysts

1! SESSION 8: ESTIMATING GROWTH Growth in Earnings 2! Look at the past The historical growth in earnings per share is usually a good starcng point for growth escmacon Look at what others are escmacng Analysts

Closure on Cash Flows

Closure on Cash Flows In a project with a finite and short life, you would need to compute a salvage value, which is the expected proceeds from selling all of the investment in the project at the end of

Closure on Cash Flows In a project with a finite and short life, you would need to compute a salvage value, which is the expected proceeds from selling all of the investment in the project at the end of

Measuring Investment Returns

Measuring Investment Returns Stern School of Business Aswath Damodaran 158 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should

Measuring Investment Returns Stern School of Business Aswath Damodaran 158 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate should

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Price or Value? What s your game?

1 Price or Value? What s your game? March 2016 Test 1: Are you pricing or valuing? 2 2 Test 2: Are you pricing or valuing? 3 3 Test 3: Are you pricing or valuing? 4 4 Price versus Value: The Set up 5 Drivers

1 Price or Value? What s your game? March 2016 Test 1: Are you pricing or valuing? 2 2 Test 2: Are you pricing or valuing? 3 3 Test 3: Are you pricing or valuing? 4 4 Price versus Value: The Set up 5 Drivers

Problem 2 Reinvestment Rate = 5/12.5 = 40% Firm Value = (150 *.6-36)*1.05 / ( ) = $ 1,134.00

*1.05 / ( ) = $ 1,134.00") Fall 1997 Problem 1 1 2 3 4 Terminal Year EPS $ 1.50 $ 1.80 $ 2.16 $ 2.59 $ 2.75 FCFE $ (2.00) $ (1.20) $ 0.34 $ 0.09 $ 1.50 Net Cap Ex $ 3.50 $ 3.00 $ 1.82 $ 2.50 $ 1.25 a. Terminal Value of Equity =

Fall 1997 Problem 1 1 2 3 4 Terminal Year EPS $ 1.50 $ 1.80 $ 2.16 $ 2.59 $ 2.75 FCFE $ (2.00) $ (1.20) $ 0.34 $ 0.09 $ 1.50 Net Cap Ex $ 3.50 $ 3.00 $ 1.82 $ 2.50 $ 1.25 a. Terminal Value of Equity =

CHAPTER 18: EQUITY VALUATION MODELS

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Absolute and relative security valuation

Absolute and relative security valuation Bertrand Groslambert bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio

Absolute and relative security valuation Bertrand Groslambert bertrand.groslambert@skema.edu Skema Business School Portfolio Management 1 Course Outline Introduction (lecture 1) Presentation of portfolio

Do you live in a mean-variance world?

Do you live in a mean-variance world? 76 Assume that you had to pick between two investments. They have the same expected return of 15% and the same standard deviation of 25%; however, investment A offers

Do you live in a mean-variance world? 76 Assume that you had to pick between two investments. They have the same expected return of 15% and the same standard deviation of 25%; however, investment A offers

ESTIMATING CASH FLOWS

113 ESTIMATING CASH FLOWS Cash is king Steps in Cash Flow Estimation 114 Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses - i.e. net

113 ESTIMATING CASH FLOWS Cash is king Steps in Cash Flow Estimation 114 Estimate the current earnings of the firm If looking at cash flows to equity, look at earnings after interest expenses - i.e. net

Slouching towards Financial Honesty: Ten Truths I learned along the way

1 Slouching towards Financial Honesty: Ten Truths I learned along the way October 2016 1. Valuation is simple 2 What are the cashflows from existing assets? - Equity: Cashflows after debt payments - Firm:

1 Slouching towards Financial Honesty: Ten Truths I learned along the way October 2016 1. Valuation is simple 2 What are the cashflows from existing assets? - Equity: Cashflows after debt payments - Firm:

Choosing Between the Multiples

Choosing Between the Multiples 100 As presented in this section, there are dozens of multiples that can be potentially used to value an individual firm. In addition, relative valuation can be relative

Choosing Between the Multiples 100 As presented in this section, there are dozens of multiples that can be potentially used to value an individual firm. In addition, relative valuation can be relative

Discount Rates: III. Relative Risk Measures. Aswath Damodaran

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

80 Discount Rates: III Relative Risk Measures 81 The CAPM Beta: The Most Used (and Misused) Risk Measure The standard procedure for estimating betas is to regress stock returns (Rj) against market returns

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Acquirers Anonymous: Seven Steps back to Sobriety

84 Acquirers Anonymous: Seven Steps back to Sobriety Acquisitions are great for target companies but not always for acquiring company stockholders 85 85 86 And the long-term follow up is not positive either..

84 Acquirers Anonymous: Seven Steps back to Sobriety Acquisitions are great for target companies but not always for acquiring company stockholders 85 85 86 And the long-term follow up is not positive either..

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Two problems with these approaches..

Two problems with these approaches.. 57 Focus just on revenues: To the extent that revenues are the only variable that you consider, when weighting risk exposure across markets, you may be missing other

Two problems with these approaches.. 57 Focus just on revenues: To the extent that revenues are the only variable that you consider, when weighting risk exposure across markets, you may be missing other

Valuation. Aswath Damodaran Aswath Damodaran 1

Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 Misconceptions about Valuation

Valuation Aswath Damodaran http://www.damodaran.com Aswath Damodaran 1 Some Initial Thoughts " One hundred thousand lemmings cannot be wrong" Graffiti Aswath Damodaran 2 Misconceptions about Valuation

Let s now stretch our consideration to the real world.

Portfolio123 Virtual Strategy Design Class By Marc Gerstein Topic 1B Valuation Theory, Moving Form Dividends to EPS In Topic 1A, we started, where else, at the beginning, the foundational idea that a stock

Portfolio123 Virtual Strategy Design Class By Marc Gerstein Topic 1B Valuation Theory, Moving Form Dividends to EPS In Topic 1A, we started, where else, at the beginning, the foundational idea that a stock

Lecture 6 Cost of Capital

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Valuation: Lecture Note Packet 1 Intrinsic Valuation

Valuation: Lecture Note Packet 1 Intrinsic Valuation Aswath Damodaran Updated: September 2012 Aswath Damodaran 1 The essence of intrinsic value In intrinsic valuation, you value an asset based upon its

Valuation: Lecture Note Packet 1 Intrinsic Valuation Aswath Damodaran Updated: September 2012 Aswath Damodaran 1 The essence of intrinsic value In intrinsic valuation, you value an asset based upon its

Islamic University of Gaza Advanced Financial Management Dr. Fares Abu Mouamer Final Exam Sat.30/1/ pm

Islamic University of Gaza Advanced Financial Management Dr. Fares Abu Mouamer Final Exam Sat.30/1/2008 3 pm 1. Which of the following statements is most correct? a. A risk averse investor will seek to

Islamic University of Gaza Advanced Financial Management Dr. Fares Abu Mouamer Final Exam Sat.30/1/2008 3 pm 1. Which of the following statements is most correct? a. A risk averse investor will seek to

COPYRIGHTED MATERIAL. The Very Basics of Value. Discounted Cash Flow and the Gordon Model: CHAPTER 1 INTRODUCTION COMMON QUESTIONS

INTRODUCTION CHAPTER 1 Discounted Cash Flow and the Gordon Model: The Very Basics of Value We begin by focusing on The Very Basics of Value. This subtitle is intentional because our purpose here is to

INTRODUCTION CHAPTER 1 Discounted Cash Flow and the Gordon Model: The Very Basics of Value We begin by focusing on The Very Basics of Value. This subtitle is intentional because our purpose here is to

Should there be a risk premium for foreign projects?

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

More Tutorial at Corporate Finance

[Type text] More Tutorial at Corporate Finance Question 1. Hardwood Factories, Inc. Hardwood Factories (HF) expects earnings this year of $6/share, and it plans to pay a $4 dividend to shareholders this

[Type text] More Tutorial at Corporate Finance Question 1. Hardwood Factories, Inc. Hardwood Factories (HF) expects earnings this year of $6/share, and it plans to pay a $4 dividend to shareholders this

Information Transparency: Can you value what you cannot see?

Information Transparency: Can you value what you cannot see? Aswath Damodaran Aswath Damodaran 1 An Experiment Company A Company B Operating Income $ 1 billion $ 1 billion Tax rate 40% 40% ROIC 10% 10%

Information Transparency: Can you value what you cannot see? Aswath Damodaran Aswath Damodaran 1 An Experiment Company A Company B Operating Income $ 1 billion $ 1 billion Tax rate 40% 40% ROIC 10% 10%

Discounted Cashflow Valuation: Equity and Firm Models. Aswath Damodaran 1

Discounted Cashflow Valuation: Equity and Firm Models 1 Summarizing the Inputs In summary, at this stage in the process, we should have an estimate of the the current cash flows on the investment, either

Discounted Cashflow Valuation: Equity and Firm Models 1 Summarizing the Inputs In summary, at this stage in the process, we should have an estimate of the the current cash flows on the investment, either

Many of the firms that we have valued in this book are publicly traded firms with

ch23_p643_666.qxd 12/7/11 2:28 PM Page 643 CHAPTER 23 Valuing Young or Start-Up Firms Many of the firms that we have valued in this book are publicly traded firms with established operations. But what

ch23_p643_666.qxd 12/7/11 2:28 PM Page 643 CHAPTER 23 Valuing Young or Start-Up Firms Many of the firms that we have valued in this book are publicly traded firms with established operations. But what

Key Concepts and Skills

Chapter 14 Dividends and Dividend Policy Key Concepts and Skills Understand dividend types and how they are paid Understand the issues surrounding dividend policy decisions Understand the difference between

Chapter 14 Dividends and Dividend Policy Key Concepts and Skills Understand dividend types and how they are paid Understand the issues surrounding dividend policy decisions Understand the difference between

Financial Statement Analysis

Financial Statement Analysis MSc. in Financial Analysis for xecutives Department of Banking & Financial Management University of Piraeus Dr. Georgios A. Papanastasopoulos 4- 4-2 4-3 Simple (and Cheap)

Financial Statement Analysis MSc. in Financial Analysis for xecutives Department of Banking & Financial Management University of Piraeus Dr. Georgios A. Papanastasopoulos 4- 4-2 4-3 Simple (and Cheap)

Midterm Review. P resent value = P V =

JEM034 Corporate Finance Winter Semester 2018/2019 Instructor: Olga Bychkova Midterm Review F uture value of $100 = $100 (1 + r) t Suppose that you will receive a cash flow of C t dollars at the end of

JEM034 Corporate Finance Winter Semester 2018/2019 Instructor: Olga Bychkova Midterm Review F uture value of $100 = $100 (1 + r) t Suppose that you will receive a cash flow of C t dollars at the end of

Choice of comparable firms for multiple valuation. A paper by Jens Overgaard Knudsen, Simon Vesterby Kold and Thomas Plenborg

Choice of comparable firms for multiple valuation A paper by Jens Overgaard Knudsen, Simon Vesterby Kold and Thomas Plenborg 1 Agenda 1 Comparable firm selection for multiple valuation 2 Our idea 3 How

Choice of comparable firms for multiple valuation A paper by Jens Overgaard Knudsen, Simon Vesterby Kold and Thomas Plenborg 1 Agenda 1 Comparable firm selection for multiple valuation 2 Our idea 3 How

Bank & Financial Institution Questions & Answers

Bank & Financial Institution Questions & Answers I created this section of the interview guide because I kept getting questions on what to expect when interviewing for specific industry groups. This chapter

Bank & Financial Institution Questions & Answers I created this section of the interview guide because I kept getting questions on what to expect when interviewing for specific industry groups. This chapter