Boom or gloom? Examining the Dutch disease in two-speed economies

|

|

|

- Brandon Gray

- 5 years ago

- Views:

Transcription

1 Boom or gloom? Examining the Dutch disease in two-speed economies Hilde C. Bjørnland Leif Anders Thorsrud Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CAMP Workshop on Commodity Price Dynamics and Financialization Oslo, June Bjørnland and Thorsrud Resource boom CAMP, June / 21

2 Background Much theoretical work has been carried out analysing the benefits and costs of energy discoveries, but relatively few empirical studies. Traditional Dutch Disease (DD): Inverse long run relationship between increased exploitation of natural resources and growth in the manufacturing sector. Resource Movement Effect Spending Effect Real appreciation that will hurt some sectors and benefit others. Does it fit the data? Since the early 1990s Australia and Norway, two commodity exporters, have experienced aggregate growth rates up to 0.5 percentage points higher than comparable countries The average growth in the manufacturing sector has not been significantly lower than in comparable countries. But... Bjørnland and Thorsrud Resource boom CAMP, June / 21

3 Boom or gloom? Stylized facts Australia Norway Prices Employment Bjørnland and Thorsrud Resource boom CAMP, June / 21

4 What we do and how we contribute Extend the traditional Dutch Disease theory: Standard Dutch Disease models do not account for productivity spillovers between the resource rich sector and the rest of the economy. We assume learning by doing (LBD) in the traded and non-traded sectors, as well as learning spillovers between these sectors and from the resource rich sector, i.e., augment Torvik (2001). E.g., Norway: Offshore oil extraction demands complicated technical solutions which could in itself generate positive knowledge externalities that benefit other sectors. Develop a structural Bayesian Dynamic Factor Model that: Explicitly distinguishes between a resource gift that is due to commodity price disturbances and a boom in the resource sector itself. Potentially takes into account all the direct and indirect spillovers among the sectors in the economy. Control for global activity and (non-resource) domestic activity. Study applied to Australia and Norway. Bjørnland and Thorsrud Resource boom CAMP, June / 21

5 Questions and answers Do resource gifts contribute to a boom in the domestic economy? Resource sector has large (productivity) spillovers on non-resource sectors in Australia and Norway. Effects not captured in previous analysis. Value added and employment increases in the non-traded relative to the traded sectors, contributing to a two-speed transmission phase. Bjørnland and Thorsrud Resource boom CAMP, June / 21

6 Questions and answers How does the domestic economy respond to commodity price changes? Norway: Value added and employment in the technologically intense service sectors and the government sector increase temporarily. But, substantial real exchange rate appreciation and reduced cost competitiveness. Gloom: For Australia there is evidence of crowding out and an eventual decline in tradeable sectors, i.e., more classical Dutch Disease effects. But, if commodity price increases are caused by positive disturbances to global demand, the commodity exporting countries are positively affected. Bjørnland and Thorsrud Resource boom CAMP, June / 21

7 The theory model New mechanism: Allow for direct technology spillovers from the resource boom (R t ) to the non-resource sectors. Following Corden (1984):R t is exogenous (measured in terms of traded sector productivity units) and is happening in one of two ways: 1 An (unpredicted) technical improvement in the booming sector, represented by a favourable shift in the production function. 2 A windfall discovery of new resources. Augment Torvik (2001): Assume both the traded and the non-traded sector can contribute to learning and that there are spillovers between these sectors, in addition to the direct productivity spillovers from resource sector. Control for an exogenous rise in the world price of the resource that is exported in the empirical analysis. Bjørnland and Thorsrud Resource boom CAMP, June / 21

8 Key equations Productivity (output) growth and LBD: Ḣ Nt H Nt = uη(λ t, R t ) + vδ T (1 η(λ t, R t )) + δ R R t, 0 δ T 1 (1) Ḣ Tt H Tt = uδ N η(λ t, R t ) + v(1 η(λ t, R t )) + δ R R t, 0 δ N 1 (2) Steady state (aggregate) output g = δ R R + v(1 δ T ) u(1 δ N ) + v(1 δ T ) (3) In traditional DD models with LBD: u = δ T = δ N = δ R = 0, i.e., no spillovers and learning happening in the traded sector only, or, u = δ N = δ R = 0, i.e., spillovers from the traded sector. We extend Torvik (2001) by having δ R = 0. Bjørnland and Thorsrud Resource boom CAMP, June / 21

9 Theory meets data Goal: Analyse business cycle variation. Distinguish between transitory R t and commodity price shocks. Allow for spending and resource movement effects, and spillover between sectors. Bjørnland and Thorsrud Resource boom CAMP, June / 21

10 Theory meets data cont d Include a broad range of sectoral employment and production series, plus productivity, the real exchange rate, wage and investment series, the terms of trade, stock prices, consumer and producer prices, and the short term interest rate. In Norway, the real commodity price is the real price of oil. In Australia we use the Reserve Bank of Australia (RBA) Index of Commodity Prices (US dollars). Both commodity prices are deflated using the US CPI. Global activity reflect important trading partners and the largest economies in the world. Transformed to be stationary (year on year growth). Sample: 1991.Q1/1996.Q Q4. Bjørnland and Thorsrud Resource boom CAMP, June / 21

11 Theory meets empirical model: Bayesian dynamic factor model (BDFM) Observation equation: Transition equation: y t = λ 0 f t + + λ s f t s + ɛ t (4) f t = φ 1 f t φ h f t h + u t (5) with [ ] ( [0 ] [ ] ) ɛt R 0 i.i.d.n, (6) u t 0 0 Q and autoregressive errors: ɛ t,i = ρ 1,i ɛ t 1,i + + ρ l,i ɛ t l,i + ω t,i (7) Restricting (see Bai and Wang (2012): [ ] λ0,1 λ 0 = λ 0,2 λ 0,1 = I 4 (8) Bjørnland and Thorsrud Resource boom CAMP, June / 21

12 The model: Identification of shocks Identify four structural shocks: Global activity shock (e gact t ) Commodity price shock (e comp t ) Resource activity shock/resource booms (e ract t ) Non-resource (domestic) activity shock (e dact t ). The mapping between the reduced form residuals u t and structural disturbances e t, u t = A 0 e t, is given by (recursive ordering): u gact t a e gact ut comp t ut ract = a 21 a e comp t a 31 a 32 a 33 0 e ract (9) ut dact t a 41 a 42 a 43 a 44 et dact Bjørnland and Thorsrud Resource boom CAMP, June / 21

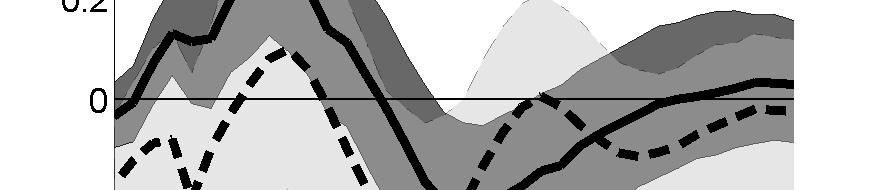

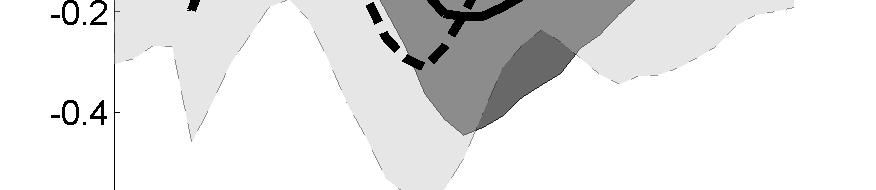

13 Note in the figures below... Norway: Solid lines and dark shaded probability bands Australia: Dotted lines and lighter shaded probability bands Bjørnland and Thorsrud Resource boom CAMP, June / 21

14 Resource gifts and domestic impulse responses GDP Productivity Employment Real exchange rate Bjørnland and Thorsrud Resource boom CAMP, June / 21

15 Sectoral responses - Norway Value added Employment Resource activity shock Bjørnland and Thorsrud Resource boom CAMP, June / 21

16 Sectoral responses - Australia Value added Employment Resource activity shock Bjørnland and Thorsrud Resource boom CAMP, June / 21

17 Global activity shocks and commodity prices If commodity price increases are caused by positive disturbances to global demand, the commodity exporting countries are positively affected. GDP CPI But... Bjørnland and Thorsrud Resource boom CAMP, June / 21

18 Commodity price shocks (not related to global activity) and domestic impulse responses GDP Productivity Employment Real exchange rate Bjørnland and Thorsrud Resource boom CAMP, June / 21

19 Sectoral responses - Norway Value added Employment Commodity price shock Bjørnland and Thorsrud Resource boom CAMP, June / 21

20 Sectoral responses - Australia Value added Employment Commodity price shock Bjørnland and Thorsrud Resource boom CAMP, June / 21

21 Conclusion Propose theory model that allows for learning by doing (LBD) in the traded and non-traded sectors, as well as learning spillovers between these sectors and from the resource rich sector. We develop a structural BDFM that potentially accounts for direct and indirect spillovers between the sectors in the economy and that explicitly distinguishes between a resource gift that is due to commodity price disturbances and a boom in the resource sector itself. We find that: Booms in the resource sector have productivity and growth spillovers on the non-resource sectors, effects that have not been captured in previous analysis. For both Australia and Norway, resource gifts have contributed to the observed two-speed patterns in these economies. It is important to separate between resource gifts happening either as unexpected price movements or favourable shifts in the production function. Bjørnland and Thorsrud Resource boom CAMP, June / 21

Oil and macroeconomic (in)stability

stability") Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

Oil and macroeconomic (in)stability Hilde C. Bjørnland Vegard H. Larsen Centre for Applied Macro- and Petroleum Economics (CAMP) BI Norwegian Business School CFE-ERCIM December 07, 2014 Bjørnland and Larsen

What drives oil prices? Emerging versus developed economies

Crawford School of Public Policy CAMA Centre for Applied Macroeconomic Analysis What drives oil prices? Emerging versus developed economies CAMA Working Paper /23 February 23 Knut Are Aastveit Norges Bank

Crawford School of Public Policy CAMA Centre for Applied Macroeconomic Analysis What drives oil prices? Emerging versus developed economies CAMA Working Paper /23 February 23 Knut Are Aastveit Norges Bank

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Shocked by the world! Introducing the three block open economy FAVAR

Shocked by the world! Introducing the three block open economy FAVAR Özer Karagedikli Leif Anders Thorsrud November 5, 2 Abstract We estimate a three block FAVAR with separate world, regional and domestic

Shocked by the world! Introducing the three block open economy FAVAR Özer Karagedikli Leif Anders Thorsrud November 5, 2 Abstract We estimate a three block FAVAR with separate world, regional and domestic

The world is not enough! Monetary policy and regional dependence

The world is not enough! Monetary policy and regional dependence Knut Are Aastveit Hilde C. Bjørnland Leif Anders Thorsrud May 9, 211 Abstract A long standing literature has investigated the patterns of

The world is not enough! Monetary policy and regional dependence Knut Are Aastveit Hilde C. Bjørnland Leif Anders Thorsrud May 9, 211 Abstract A long standing literature has investigated the patterns of

The Effects of Monetary Policy on Asset Price Bubbles: Some Evidence

The Effects of Monetary Policy on Asset Price Bubbles: Some Evidence Jordi Galí Luca Gambetti September 2013 Jordi Galí, Luca Gambetti () Monetary Policy and Bubbles September 2013 1 / 17 Monetary Policy

The Effects of Monetary Policy on Asset Price Bubbles: Some Evidence Jordi Galí Luca Gambetti September 2013 Jordi Galí, Luca Gambetti () Monetary Policy and Bubbles September 2013 1 / 17 Monetary Policy

Gernot Müller (University of Bonn, CEPR, and Ifo)

") Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Housing Prices and Growth

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

Housing Prices and Growth James A. Kahn June 2007 Motivation Housing market boom-bust has prompted talk of bubbles. But what are fundamentals? What is the right benchmark? Motivation Housing market boom-bust

ECONOMIC GROWTH 1. THE ACCUMULATION OF CAPITAL

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy Iklaga, Fred Ogli University of Surrey f.iklaga@surrey.ac.uk Presented at the 33rd USAEE/IAEE North American Conference, October 25-28,

A Small Open Economy DSGE Model for an Oil Exporting Emerging Economy Iklaga, Fred Ogli University of Surrey f.iklaga@surrey.ac.uk Presented at the 33rd USAEE/IAEE North American Conference, October 25-28,

Global shocks, economic fluctuations and timeliness of monetary policy.

Global shocks, economic fluctuations and timeliness of monetary policy. Hilde C. Bjørnland Leif Anders Thorsrud Sepideh Khayati Zahiri December 6, 215 PRELIMINARY VERSION. Abstract Do central banks respond

Global shocks, economic fluctuations and timeliness of monetary policy. Hilde C. Bjørnland Leif Anders Thorsrud Sepideh Khayati Zahiri December 6, 215 PRELIMINARY VERSION. Abstract Do central banks respond

5. STRUCTURAL VAR: APPLICATIONS

5. STRUCTURAL VAR: APPLICATIONS 1 1 Monetary Policy Shocks (Christiano Eichenbaum and Evans, 1998) Monetary policy shocks is the unexpected part of the equation for the monetary policy instrument (S t

5. STRUCTURAL VAR: APPLICATIONS 1 1 Monetary Policy Shocks (Christiano Eichenbaum and Evans, 1998) Monetary policy shocks is the unexpected part of the equation for the monetary policy instrument (S t

WORKING PAPER SERIES

ISSN 1503-299X WORKING PAPER SERIES No. 8/2006 RESOURCE BOOM, PRODUCTIVITY GROWTH AND REAL EXCHANGE RATE DYNAMICS - A dynamic general equilibrium analysis of South Africa HILDEGUNN EKROLL STOKKE Department

ISSN 1503-299X WORKING PAPER SERIES No. 8/2006 RESOURCE BOOM, PRODUCTIVITY GROWTH AND REAL EXCHANGE RATE DYNAMICS - A dynamic general equilibrium analysis of South Africa HILDEGUNN EKROLL STOKKE Department

Country Spreads as Credit Constraints in Emerging Economy Business Cycles

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

Modeling fiscal policy in a small, open, resourcerich

Modeling fiscal policy in a small, open, resourcerich economy Norwegian experiences Ådne Cappelen Statistics Norway 1 MMU, Dec.2017 Outline Resource richness and fiscal policies Implications for private

Modeling fiscal policy in a small, open, resourcerich economy Norwegian experiences Ådne Cappelen Statistics Norway 1 MMU, Dec.2017 Outline Resource richness and fiscal policies Implications for private

BUSI 101 Capital Markets and Real Estate

BUSI 101 Capital Markets and Real Estate PURPOSE AND SCOPE The Capital Markets and Real Estate course (BUSI 101) is intended to acquaint the student with the basic principles of macroeconomics and to give

BUSI 101 Capital Markets and Real Estate PURPOSE AND SCOPE The Capital Markets and Real Estate course (BUSI 101) is intended to acquaint the student with the basic principles of macroeconomics and to give

The Chinese impact on GDP growth and inflation in the industrial countries

The Chinese impact on GDP growth and inflation in the industrial countries Christian Dreger German Institute for Economic Research (DIW Berlin) Yanqun Zhang Chinese Academy of Social Sciences (CASS) 1

The Chinese impact on GDP growth and inflation in the industrial countries Christian Dreger German Institute for Economic Research (DIW Berlin) Yanqun Zhang Chinese Academy of Social Sciences (CASS) 1

For students electing Macro (8702/Prof. Smith) & Macro (8701/Prof. Roe) option

& Macro (8701/Prof. Roe) option") WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics June. - 2011 Trade, Development and Growth For students electing Macro (8702/Prof. Smith) & Macro (8701/Prof. Roe) option Instructions

WRITTEN PRELIMINARY Ph.D EXAMINATION Department of Applied Economics June. - 2011 Trade, Development and Growth For students electing Macro (8702/Prof. Smith) & Macro (8701/Prof. Roe) option Instructions

Monetary policy, leaning and concern for financial stability

Monetary policy, leaning and concern for financial stability Hilde C. Bjørnland 1,2 Leif Brubakk 2 Junior Maih 2,1 1 BI Norwegian Business School 2 Norges Bank The 8th International Conference on Computational

Monetary policy, leaning and concern for financial stability Hilde C. Bjørnland 1,2 Leif Brubakk 2 Junior Maih 2,1 1 BI Norwegian Business School 2 Norges Bank The 8th International Conference on Computational

Oil Booms, Dutch Disease and Manufacturing Growth

Oil Booms, Dutch Disease and Manufacturing Growth Nouf N. Alsharif 1 Abstract This paper estimates the causal effect of two commodity shocks suggested by the Dutch Disease hypothesis on the tradable manufacturing

Oil Booms, Dutch Disease and Manufacturing Growth Nouf N. Alsharif 1 Abstract This paper estimates the causal effect of two commodity shocks suggested by the Dutch Disease hypothesis on the tradable manufacturing

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account LAMES November 21, 2008 Intertemporal Approach to the Current Account Intertemporal Approach to the Current Account Dynamic,

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account LAMES November 21, 2008 Intertemporal Approach to the Current Account Intertemporal Approach to the Current Account Dynamic,

Learning About Commodity Cycles and Saving-Investment Dynamics in a Commodity-Exporting Economy

Learning About Commodity Cycles and Saving-Investment Dynamics in a Commodity-Exporting Economy Jorge Fornero Markus Kirchner Central Bank of Chile, Macroeconomic Analysis Division Fifth BIS CCA Research

Learning About Commodity Cycles and Saving-Investment Dynamics in a Commodity-Exporting Economy Jorge Fornero Markus Kirchner Central Bank of Chile, Macroeconomic Analysis Division Fifth BIS CCA Research

Sustainable Financial Obligations and Crisis Cycles

Sustainable Financial Obligations and Crisis Cycles Mikael Juselius and Moshe Kim 220 200 180 160 140 120 (a) U.S. household sector total debt to income. 10 8 6 4 2 0 2 (b) Nominal (solid line) and real

Sustainable Financial Obligations and Crisis Cycles Mikael Juselius and Moshe Kim 220 200 180 160 140 120 (a) U.S. household sector total debt to income. 10 8 6 4 2 0 2 (b) Nominal (solid line) and real

Uncertainty and Economic Activity: A Global Perspective

Uncertainty and Economic Activity: A Global Perspective Ambrogio Cesa-Bianchi 1 M. Hashem Pesaran 2 Alessandro Rebucci 3 IV International Conference in memory of Carlo Giannini 26 March 2014 1 Bank of

Uncertainty and Economic Activity: A Global Perspective Ambrogio Cesa-Bianchi 1 M. Hashem Pesaran 2 Alessandro Rebucci 3 IV International Conference in memory of Carlo Giannini 26 March 2014 1 Bank of

Explaining the Last Consumption Boom-Bust Cycle in Ireland

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 6525 Explaining the Last Consumption Boom-Bust Cycle in

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Policy Research Working Paper 6525 Explaining the Last Consumption Boom-Bust Cycle in

Volume 38, Issue 1. The dynamic effects of aggregate supply and demand shocks in the Mexican economy

Volume 38, Issue 1 The dynamic effects of aggregate supply and demand shocks in the Mexican economy Ivan Mendieta-Muñoz Department of Economics, University of Utah Abstract This paper studies if the supply

Volume 38, Issue 1 The dynamic effects of aggregate supply and demand shocks in the Mexican economy Ivan Mendieta-Muñoz Department of Economics, University of Utah Abstract This paper studies if the supply

THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH

South-Eastern Europe Journal of Economics 1 (2015) 75-84 THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH IOANA BOICIUC * Bucharest University of Economics, Romania Abstract This

South-Eastern Europe Journal of Economics 1 (2015) 75-84 THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH IOANA BOICIUC * Bucharest University of Economics, Romania Abstract This

PRIVATE AND GOVERNMENT INVESTMENT: A STUDY OF THREE OECD COUNTRIES. MEHDI S. MONADJEMI AND HYEONSEUNG HUH* University of New South Wales

INTERNATIONAL ECONOMIC JOURNAL 93 Volume 12, Number 2, Summer 1998 PRIVATE AND GOVERNMENT INVESTMENT: A STUDY OF THREE OECD COUNTRIES MEHDI S. MONADJEMI AND HYEONSEUNG HUH* University of New South Wales

INTERNATIONAL ECONOMIC JOURNAL 93 Volume 12, Number 2, Summer 1998 PRIVATE AND GOVERNMENT INVESTMENT: A STUDY OF THREE OECD COUNTRIES MEHDI S. MONADJEMI AND HYEONSEUNG HUH* University of New South Wales

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Do central banks respond timely to developments in the global economy?

CENTRE FOR APPLIED MACRO AND PETROLEUM ECONOMICS (CAMP) CAMP Working Paper Series No 8/2016 Do central banks respond timely to developments in the global economy? Hilde C. Bjørnland, Leif Anders Thorsrud

CENTRE FOR APPLIED MACRO AND PETROLEUM ECONOMICS (CAMP) CAMP Working Paper Series No 8/2016 Do central banks respond timely to developments in the global economy? Hilde C. Bjørnland, Leif Anders Thorsrud

Fiscal Multipliers in Recessions

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

Adjustment Costs and Incentives to Work: Evidence from a Disability Insurance Program

Adjustment Costs and Incentives to Work: Evidence from a Disability Insurance Program Arezou Zaresani Research Fellow Melbourne Institute of Applied Economics and Social Research University of Melbourne

Adjustment Costs and Incentives to Work: Evidence from a Disability Insurance Program Arezou Zaresani Research Fellow Melbourne Institute of Applied Economics and Social Research University of Melbourne

FETP/MPP8/Macroeconomics/Riedel. General Equilibrium in the Short Run II The IS-LM model

FETP/MPP8/Macroeconomics/iedel General Equilibrium in the Short un II The -LM model The -LM Model Like the AA-DD model, the -LM model is a general equilibrium model, which derives the conditions for simultaneous

FETP/MPP8/Macroeconomics/iedel General Equilibrium in the Short un II The -LM model The -LM Model Like the AA-DD model, the -LM model is a general equilibrium model, which derives the conditions for simultaneous

Hotelling Under Pressure. Soren Anderson (Michigan State) Ryan Kellogg (Michigan) Stephen Salant (Maryland)

Ryan Kellogg (Michigan) Stephen Salant (Maryland)") Hotelling Under Pressure Soren Anderson (Michigan State) Ryan Kellogg (Michigan) Stephen Salant (Maryland) October 2015 Hotelling has conceptually underpinned most of the resource extraction literature

Hotelling Under Pressure Soren Anderson (Michigan State) Ryan Kellogg (Michigan) Stephen Salant (Maryland) October 2015 Hotelling has conceptually underpinned most of the resource extraction literature

The Model: Tradables, Non-tradables, and Semi-tradables in Trade Models. Shantayanan Devarajan Jeffrey D. Lewis Jaime de Melo Sherman Robinson

The 1-2-3 Model: Tradables, Non-tradables, and Semi-tradables in Trade Models Shantayanan Devarajan Jeffrey D. Lewis Jaime de Melo Sherman Robinson Macroeconomic Adjustment GDP = C + I + G + E - M GDP

The 1-2-3 Model: Tradables, Non-tradables, and Semi-tradables in Trade Models Shantayanan Devarajan Jeffrey D. Lewis Jaime de Melo Sherman Robinson Macroeconomic Adjustment GDP = C + I + G + E - M GDP

Traded and non-traded goods

Traded and non-traded goods ECON4330 Spring 2013 Lecture 12A Asbjørn Rødseth University of Oslo April 22, 2013 Traded and non-traded goods April 22, 2013 1 / 16 Different market structures Mundell-Fleming

Traded and non-traded goods ECON4330 Spring 2013 Lecture 12A Asbjørn Rødseth University of Oslo April 22, 2013 Traded and non-traded goods April 22, 2013 1 / 16 Different market structures Mundell-Fleming

Monetary policy and the asset risk-taking channel

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

Øystein Olsen: Monetary policy and wealth management in a small petroleum economy

Øystein Olsen: Monetary policy and wealth management in a small petroleum economy Speech by Mr Øystein Olsen, Governor of the Norges Bank (Central Bank of Norway), at the Harvard Kennedy School, Cambridge,

Øystein Olsen: Monetary policy and wealth management in a small petroleum economy Speech by Mr Øystein Olsen, Governor of the Norges Bank (Central Bank of Norway), at the Harvard Kennedy School, Cambridge,

What determines government spending multipliers?

What determines government spending multipliers? Paper by Giancarlo Corsetti, André Meier and Gernot J. Müller Presented by Michele Andreolli 12 May 2014 Outline Overview Empirical strategy Results Remarks

What determines government spending multipliers? Paper by Giancarlo Corsetti, André Meier and Gernot J. Müller Presented by Michele Andreolli 12 May 2014 Outline Overview Empirical strategy Results Remarks

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

The impacts of cereal, soybean and rapeseed meal price shocks on pig and poultry feed prices

The impacts of cereal, soybean and rapeseed meal price shocks on pig and poultry feed prices Abstract The goal of this paper was to estimate how changes in the market prices of protein-rich and energy-rich

The impacts of cereal, soybean and rapeseed meal price shocks on pig and poultry feed prices Abstract The goal of this paper was to estimate how changes in the market prices of protein-rich and energy-rich

Working Paper. The world is not enough! Small open economies and regional dependence. Economics Department

2 6 Working Paper Economics Department The world is not enough! Small open economies and regional dependence Knut Are Aastveit, Hilde C. Bjørnland and Leif Anders Thorsrud Working papers fra Norges Bank,

2 6 Working Paper Economics Department The world is not enough! Small open economies and regional dependence Knut Are Aastveit, Hilde C. Bjørnland and Leif Anders Thorsrud Working papers fra Norges Bank,

Why so low for so long? A long-term view of real interest rates

Why so low for so long? A long-term view of real interest rates Claudio Borio, Piti Disyatat, and Phurichai Rungcharoenkitkul Bank of Finland/CEPR Conference, Demographics and the Macroeconomy, Helsinki,

Why so low for so long? A long-term view of real interest rates Claudio Borio, Piti Disyatat, and Phurichai Rungcharoenkitkul Bank of Finland/CEPR Conference, Demographics and the Macroeconomy, Helsinki,

Exchange Rate Pass-through in India

Exchange Rate Pass-through in India Rudrani Bhattacharya, Ila Patnaik and Ajay Shah National Institute of Public Finance and Policy, New Delhi March 27, 2008 udrani Bhattacharya, Ila Patnaik and Ajay Shah

Exchange Rate Pass-through in India Rudrani Bhattacharya, Ila Patnaik and Ajay Shah National Institute of Public Finance and Policy, New Delhi March 27, 2008 udrani Bhattacharya, Ila Patnaik and Ajay Shah

Identifying of the fiscal policy shocks

The Academy of Economic Studies Bucharest Doctoral School of Finance and Banking Identifying of the fiscal policy shocks Coordinator LEC. UNIV. DR. BOGDAN COZMÂNCĂ MSC Student Andreea Alina Matache Dissertation

The Academy of Economic Studies Bucharest Doctoral School of Finance and Banking Identifying of the fiscal policy shocks Coordinator LEC. UNIV. DR. BOGDAN COZMÂNCĂ MSC Student Andreea Alina Matache Dissertation

Estimating Bivariate GARCH-Jump Model Based on High Frequency Data : the case of revaluation of Chinese Yuan in July 2005

Estimating Bivariate GARCH-Jump Model Based on High Frequency Data : the case of revaluation of Chinese Yuan in July 2005 Xinhong Lu, Koichi Maekawa, Ken-ichi Kawai July 2006 Abstract This paper attempts

Estimating Bivariate GARCH-Jump Model Based on High Frequency Data : the case of revaluation of Chinese Yuan in July 2005 Xinhong Lu, Koichi Maekawa, Ken-ichi Kawai July 2006 Abstract This paper attempts

Christina Zauner. June 8 th, Department of Economics, University of Vienna. The Goods Market of an Open Economy. Christina Zauner.

Department of Economics, University of Vienna June 8 th, 2011 The for In the final chapter we analyse the equilibrium in the goods market in an open economy Changes in domestic as well as foreign demand

Department of Economics, University of Vienna June 8 th, 2011 The for In the final chapter we analyse the equilibrium in the goods market in an open economy Changes in domestic as well as foreign demand

Terms of Trade Shocks and Investment in Commodity-Exporting Economies 1

Terms of Trade Shocks and Investment in Commodity-Exporting Economies Jorge Fornero Markus Kirchner Andrés Yany Research Division Central Bank of Chile XXXII Economist Meeting of the Central Bank of Peru

Terms of Trade Shocks and Investment in Commodity-Exporting Economies Jorge Fornero Markus Kirchner Andrés Yany Research Division Central Bank of Chile XXXII Economist Meeting of the Central Bank of Peru

Online Appendix: Asymmetric Effects of Exogenous Tax Changes

Online Appendix: Asymmetric Effects of Exogenous Tax Changes Syed M. Hussain Samreen Malik May 9,. Online Appendix.. Anticipated versus Unanticipated Tax changes Comparing our estimates with the estimates

Online Appendix: Asymmetric Effects of Exogenous Tax Changes Syed M. Hussain Samreen Malik May 9,. Online Appendix.. Anticipated versus Unanticipated Tax changes Comparing our estimates with the estimates

Lecture 22. Aggregate demand and aggregate supply

Lecture 22 Aggregate demand and aggregate supply By the end of this lecture, you should understand: three key facts about short-run economic fluctuations how the economy in the short run differs from the

Lecture 22 Aggregate demand and aggregate supply By the end of this lecture, you should understand: three key facts about short-run economic fluctuations how the economy in the short run differs from the

Beyond the Basic Solow Growth Model, Part 1 Agenda. The Basic Solow Growth Model. The Basic Solow Growth Model. The Basic Solow Growth Model

Beyond the Basic Solow Growth Model, Part genda The. Shortcomings The Growth ccounting Formula. The The : depends on v, n-dot, δ, and. Changes in v, δ, and lead to changes in the level of but they affect

Beyond the Basic Solow Growth Model, Part genda The. Shortcomings The Growth ccounting Formula. The The : depends on v, n-dot, δ, and. Changes in v, δ, and lead to changes in the level of but they affect

slides chapter 6 Interest Rate Shocks

slides chapter 6 Interest Rate Shocks Princeton University Press, 217 Motivation Interest-rate shocks are generally believed to be a major source of fluctuations for emerging countries. The next slide

slides chapter 6 Interest Rate Shocks Princeton University Press, 217 Motivation Interest-rate shocks are generally believed to be a major source of fluctuations for emerging countries. The next slide

Effects of U.S. Quantitative Easing on Emerging Market Economies

Effects of U.S. Quantitative Easing on Emerging Market Economies Saroj Bhattarai Arpita Chatterjee Woong Yong Park 3 University of Texas at Austin University of New South Wales 3 University of Illinois

Effects of U.S. Quantitative Easing on Emerging Market Economies Saroj Bhattarai Arpita Chatterjee Woong Yong Park 3 University of Texas at Austin University of New South Wales 3 University of Illinois

Supplementary Appendix. July 22, 2016

For Online Publication Supplementary Appendix News Shocks In Open Economies: Evidence From Giant Oil Discoveries July 22, 2016 1 Supplementary Appendix C: Model Graphs -.06-.04-.02 0.02.04 Sector 1 Output

For Online Publication Supplementary Appendix News Shocks In Open Economies: Evidence From Giant Oil Discoveries July 22, 2016 1 Supplementary Appendix C: Model Graphs -.06-.04-.02 0.02.04 Sector 1 Output

Report ISBN: (PDF)

") Report ISBN: 978-0-478-38248-8 (PDF) NZIER is a specialist consulting firm that uses applied economic research and analysis to provide a wide range of strategic advice to clients in the public and private

Report ISBN: 978-0-478-38248-8 (PDF) NZIER is a specialist consulting firm that uses applied economic research and analysis to provide a wide range of strategic advice to clients in the public and private

Balance Sheet Recessions

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

Lecture 23 The New Keynesian Model Labor Flows and Unemployment. Noah Williams

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Lecture 23 The New Keynesian Model Labor Flows and Unemployment Noah Williams University of Wisconsin - Madison Economics 312/702 Basic New Keynesian Model of Transmission Can be derived from primitives:

Macroeconomic Modelling at the Central Bank of Brazil. Angelo M. Fasolo Research Department

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

1 Dynamic programming

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

Uncertainty and the Transmission of Fiscal Policy

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 32 ( 2015 ) 769 776 Emerging Markets Queries in Finance and Business EMQFB2014 Uncertainty and the Transmission of

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 32 ( 2015 ) 769 776 Emerging Markets Queries in Finance and Business EMQFB2014 Uncertainty and the Transmission of

MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

Bank Contagion in Europe

Bank Contagion in Europe Reint Gropp and Jukka Vesala Workshop on Banking, Financial Stability and the Business Cycle, Sveriges Riksbank, 26-28 August 2004 The views expressed in this paper are those of

Bank Contagion in Europe Reint Gropp and Jukka Vesala Workshop on Banking, Financial Stability and the Business Cycle, Sveriges Riksbank, 26-28 August 2004 The views expressed in this paper are those of

MA Advanced Macroeconomics 3. Examples of VAR Studies

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

Monetary Policy and Exchange Rate Stabilization in Norway and Sweden

Discussion of Monetary Policy and Exchange Rate Stabilization in Norway and Sweden By Hilde C. Bjørnland and Junior Maih Reform Capacity and Macroeconomic Performance in the Nordic Countries Copenhagen

Discussion of Monetary Policy and Exchange Rate Stabilization in Norway and Sweden By Hilde C. Bjørnland and Junior Maih Reform Capacity and Macroeconomic Performance in the Nordic Countries Copenhagen

Monetary Policy Shock Analysis Using Structural Vector Autoregression

Monetary Policy Shock Analysis Using Structural Vector Autoregression (Digital Signal Processing Project Report) Rushil Agarwal (72018) Ishaan Arora (72350) Abstract A wide variety of theoretical and empirical

Monetary Policy Shock Analysis Using Structural Vector Autoregression (Digital Signal Processing Project Report) Rushil Agarwal (72018) Ishaan Arora (72350) Abstract A wide variety of theoretical and empirical

Exchange Rate Valuation and its Impact on the Real Economy. Enzo Cassino and David Oxley

Exchange Rate Valuation and its Impact on the Real Economy Enzo Cassino and David Oxley We try to understand the relationship between New Zealand s exchange rate and the wider economy......and review the

Exchange Rate Valuation and its Impact on the Real Economy Enzo Cassino and David Oxley We try to understand the relationship between New Zealand s exchange rate and the wider economy......and review the

Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 2006)

") Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 26) Country Interest Rates and Output in Seven Emerging Countries Argentina Brazil.5.5...5.5.5. 94 95 96 97 98

Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 26) Country Interest Rates and Output in Seven Emerging Countries Argentina Brazil.5.5...5.5.5. 94 95 96 97 98

Mark Scheme (Results) Summer 2007

Summer 2007") Mark Scheme (Results) Summer 2007 GCE GCE Economic (6353) Paper 1 Edexcel Limited. Registered in England and Wales No. 4496750 Registered Office: One90 High Holborn, London WC1V 7BH 6353 Mark Scheme Summer

Mark Scheme (Results) Summer 2007 GCE GCE Economic (6353) Paper 1 Edexcel Limited. Registered in England and Wales No. 4496750 Registered Office: One90 High Holborn, London WC1V 7BH 6353 Mark Scheme Summer

Part I (45 points; Mark your answers in a SCANTRON)

") Final Examination Name: ECON 4020/ SPRING 2005 Instructor: Dr. M. Nirei 1:30 3:20 pm, April 28, 2005 Part I (45 points; Mark your answers in a SCANTRON) (1) The GDP deflator is equal to: a. the ratio of

Final Examination Name: ECON 4020/ SPRING 2005 Instructor: Dr. M. Nirei 1:30 3:20 pm, April 28, 2005 Part I (45 points; Mark your answers in a SCANTRON) (1) The GDP deflator is equal to: a. the ratio of

Charles University Faculty of Social Sciences Institute of Economic Studies

Charles University Faculty of Social Sciences Institute of Economic Studies MASTER'S THESIS The Impact of Oil Prices in Norway on Macroeconomic Indicators Author: Bc. Peter Bogren Supervisor: prof. Roman

Charles University Faculty of Social Sciences Institute of Economic Studies MASTER'S THESIS The Impact of Oil Prices in Norway on Macroeconomic Indicators Author: Bc. Peter Bogren Supervisor: prof. Roman

Exchange Rates and Fundamentals: A General Equilibrium Exploration

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Innovations in Macroeconomics

Paul JJ. Welfens Innovations in Macroeconomics Third Edition 4y Springer Contents A. Globalization, Specialization and Innovation Dynamics 1 A. 1 Introduction 1 A.2 Approaches in Modern Macroeconomics

Paul JJ. Welfens Innovations in Macroeconomics Third Edition 4y Springer Contents A. Globalization, Specialization and Innovation Dynamics 1 A. 1 Introduction 1 A.2 Approaches in Modern Macroeconomics

The Balassa-Samuelson Effect and The MEVA G10 FX Model

The Balassa-Samuelson Effect and The MEVA G10 FX Model Abstract: In this study, we introduce Danske s Medium Term FX Evaluation model (MEVA G10 FX), a framework that falls within the class of the Behavioural

The Balassa-Samuelson Effect and The MEVA G10 FX Model Abstract: In this study, we introduce Danske s Medium Term FX Evaluation model (MEVA G10 FX), a framework that falls within the class of the Behavioural

The Economy Wide Benefits of Increasing the Proportion of Students Achieving Year 12 Equivalent Education

January 2003 A Report prepared for the Business Council of Australia by The Economy Wide Benefits of Increasing the Proportion of Students Achieving Year 12 Equivalent Education Modelling Results The

January 2003 A Report prepared for the Business Council of Australia by The Economy Wide Benefits of Increasing the Proportion of Students Achieving Year 12 Equivalent Education Modelling Results The

Øystein Olsen: Monetary policy and interrelationships in the Norwegian economy

Øystein Olsen: Monetary policy and interrelationships in the Norwegian economy Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI

Øystein Olsen: Monetary policy and interrelationships in the Norwegian economy Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), at the Centre for Monetary Economics (CME)/BI

Financial Factors in Business Cycles

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Information from "nancial markets and VAR measures of monetary policy

European Economic Review 43 (1999) 825}837 Information from "nancial markets and VAR measures of monetary policy Fabio C. Bagliano*, Carlo A. Favero Dipartimento di Scienze Economiche e Finanziarie, Universita%

European Economic Review 43 (1999) 825}837 Information from "nancial markets and VAR measures of monetary policy Fabio C. Bagliano*, Carlo A. Favero Dipartimento di Scienze Economiche e Finanziarie, Universita%

Aggregate Supply. Reading. On real wages, also see Basu and Taylor (1999), Journal of Economic. Mankiw, Macroeconomics: Chapters 9.4 and 13.1 and.

, Journal of Economic. Mankiw, Macroeconomics: Chapters 9.4 and 13.1 and.") Aggregate Supply Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Aggregate Supply 1/38 Reading Mankiw, Macroeconomics: Chapters 9.4 and 13.1 and.2 On real wages, also see Basu

Aggregate Supply Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Aggregate Supply 1/38 Reading Mankiw, Macroeconomics: Chapters 9.4 and 13.1 and.2 On real wages, also see Basu

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers?

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers? Michael Woodford Columbia University Federal Reserve Bank of New York June 3, 2010 Woodford (Columbia) Corsetti

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers? Michael Woodford Columbia University Federal Reserve Bank of New York June 3, 2010 Woodford (Columbia) Corsetti

ECON 815. A Basic New Keynesian Model II

ECON 815 A Basic New Keynesian Model II Winter 2015 Queen s University ECON 815 1 Unemployment vs. Inflation 12 10 Unemployment 8 6 4 2 0 1 1.5 2 2.5 3 3.5 4 4.5 5 Core Inflation 14 12 10 Unemployment

ECON 815 A Basic New Keynesian Model II Winter 2015 Queen s University ECON 815 1 Unemployment vs. Inflation 12 10 Unemployment 8 6 4 2 0 1 1.5 2 2.5 3 3.5 4 4.5 5 Core Inflation 14 12 10 Unemployment

ECON 3560/5040 Week 3

ECON 3560/5040 Week 3 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology

ECON 3560/5040 Week 3 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology

Inflation Targeting: A New Monetary Policy Framework in Korea. October Junggun Oh The Bank of Korea

Inflation Targeting: A New Monetary Policy Framework in Korea October 2000 Junggun Oh The Bank of Korea Inflation Targeting Framework Korean Experiences in Inflation Targeting Inflation Targeting Framework

Inflation Targeting: A New Monetary Policy Framework in Korea October 2000 Junggun Oh The Bank of Korea Inflation Targeting Framework Korean Experiences in Inflation Targeting Inflation Targeting Framework

What Drives Commodity Price Booms and Busts?

What Drives Commodity Price Booms and Busts? David Jacks Simon Fraser University Martin Stuermer Federal Reserve Bank of Dallas August 10, 2017 J.P. Morgan Center for Commodities The views expressed here

What Drives Commodity Price Booms and Busts? David Jacks Simon Fraser University Martin Stuermer Federal Reserve Bank of Dallas August 10, 2017 J.P. Morgan Center for Commodities The views expressed here

Interpreting sterling exchange rate movements

By Mark S Astley and Anthony Garratt of the Bank s Monetary Assessment and Strategy Division. This article considers the analysis and interpretation of exchange rate fluctuations. It stresses the importance

By Mark S Astley and Anthony Garratt of the Bank s Monetary Assessment and Strategy Division. This article considers the analysis and interpretation of exchange rate fluctuations. It stresses the importance

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program. Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

UNIVERSITY OF TOKYO 1 st Finance Junior Workshop Program Monetary Policy and Welfare Issues in the Economy with Shifting Trend Inflation Le Thanh Ha (GRIPS) (30 th March 2017) 1. Introduction Exercises

Aggregate Supply. Dudley Cooke. Trinity College Dublin. Dudley Cooke (Trinity College Dublin) Aggregate Supply 1 / 38

Aggregate Supply 1 / 38") Aggregate Supply Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Aggregate Supply 1 / 38 Reading Mankiw, Macroeconomics: Chapters 9.4 and 13.1 and.2 On real wages, also see Basu

Aggregate Supply Dudley Cooke Trinity College Dublin Dudley Cooke (Trinity College Dublin) Aggregate Supply 1 / 38 Reading Mankiw, Macroeconomics: Chapters 9.4 and 13.1 and.2 On real wages, also see Basu

202: Dynamic Macroeconomics

202: Dynamic Macroeconomics Solow Model Mausumi Das Delhi School of Economics January 14-15, 2015 Das (Delhi School of Economics) Dynamic Macro January 14-15, 2015 1 / 28 Economic Growth In this course

202: Dynamic Macroeconomics Solow Model Mausumi Das Delhi School of Economics January 14-15, 2015 Das (Delhi School of Economics) Dynamic Macro January 14-15, 2015 1 / 28 Economic Growth In this course

INCOME DISTRIBUTION, DUTCH DISEASE AND REAL EXCHANGE RATE MOVEMENTS

ICOE DISRIBUIO DUCH DISEASE AD REA ECHAGE RAE OVEES arzosa Valdivia Fernando Enrique University of Antwerp Belgium ational University of Córdoba Argentina zarfer@hotmail.com fernando.zarzosavaldivia@student.ua.ac.be

ICOE DISRIBUIO DUCH DISEASE AD REA ECHAGE RAE OVEES arzosa Valdivia Fernando Enrique University of Antwerp Belgium ational University of Córdoba Argentina zarfer@hotmail.com fernando.zarzosavaldivia@student.ua.ac.be

Components of Economic Growth

Components of Economic Growth Components of Economic Growth 1. Capital Accumulation: savings from present income invested to increase future output and income New factories, equipment, etc., increase the

Components of Economic Growth Components of Economic Growth 1. Capital Accumulation: savings from present income invested to increase future output and income New factories, equipment, etc., increase the

Enrique Martínez-García. University of Texas at Austin and Federal Reserve Bank of Dallas

Discussion: International Recessions, by Fabrizio Perri (University of Minnesota and FRB of Minneapolis) and Vincenzo Quadrini (University of Southern California) Enrique Martínez-García University of

Discussion: International Recessions, by Fabrizio Perri (University of Minnesota and FRB of Minneapolis) and Vincenzo Quadrini (University of Southern California) Enrique Martínez-García University of

The Effects of Portfolio Capital Flows and Domestic Credit on the Australian Economy

The Effects of Portfolio Capital Flows and Domestic Credit on the Australian Economy Mala Raghavan*, Amy Churchill and Jing Tian Tasmanian School of Business and Economics University of Tasmania 1 This

The Effects of Portfolio Capital Flows and Domestic Credit on the Australian Economy Mala Raghavan*, Amy Churchill and Jing Tian Tasmanian School of Business and Economics University of Tasmania 1 This

Are we there yet? Adjustment paths in response to Tariff shocks: a CGE Analysis.

Are we there yet? Adjustment paths in response to Tariff shocks: a CGE Analysis. This paper takes the mini USAGE model developed by Dixon and Rimmer (2005) and modifies it in order to better mimic the

Are we there yet? Adjustment paths in response to Tariff shocks: a CGE Analysis. This paper takes the mini USAGE model developed by Dixon and Rimmer (2005) and modifies it in order to better mimic the

NORWEGIAN SCHOOL OF ECONOMICS

A"Critical"Readjustment" Analyzing)the)Regional)Employment)Composition)in)Norway During'Times'of'Change NorwegianSchoolofEconomics Bergen,Spring2016 Emma Hartland Gramstad & Katrine Willumsen Wærness Supervisor:

A"Critical"Readjustment" Analyzing)the)Regional)Employment)Composition)in)Norway During'Times'of'Change NorwegianSchoolofEconomics Bergen,Spring2016 Emma Hartland Gramstad & Katrine Willumsen Wærness Supervisor:

Credit Channel of Monetary Policy between Australia and New. Zealand: an Empirical Note

Credit Channel of Monetary Policy between Australia and New Zealand: an Empirical Note Tomoya Suzuki Faculty of Economics Ryukoku University 67 Tsukamoto-cho Fukakusa Fushimi-ku Kyoto 612-8577 JAPAN E-mail:

Credit Channel of Monetary Policy between Australia and New Zealand: an Empirical Note Tomoya Suzuki Faculty of Economics Ryukoku University 67 Tsukamoto-cho Fukakusa Fushimi-ku Kyoto 612-8577 JAPAN E-mail:

Taxing Firms Facing Financial Frictions

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Effi cient monetary policy frontier for Iceland

Effi cient monetary policy frontier for Iceland A report to taskforce on reviewing Iceland s monetary and currency policies Marías Halldór Gestsson May 2018 1 Introduction A central bank conducting monetary

Effi cient monetary policy frontier for Iceland A report to taskforce on reviewing Iceland s monetary and currency policies Marías Halldór Gestsson May 2018 1 Introduction A central bank conducting monetary

Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence.

Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence. Jorge Miranda-Pinto 1, Daniel Murphy 2, Kieran Walsh 2, Eric Young 1 1 UVA, 2 UVA Darden School of Business

Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence. Jorge Miranda-Pinto 1, Daniel Murphy 2, Kieran Walsh 2, Eric Young 1 1 UVA, 2 UVA Darden School of Business

Workshop on resilience

Workshop on resilience Paris 14 June 2007 SVAR analysis of short-term resilience: A summary of the methodological issues and the results for the US and Germany Alain de Serres OECD Economics Department

Workshop on resilience Paris 14 June 2007 SVAR analysis of short-term resilience: A summary of the methodological issues and the results for the US and Germany Alain de Serres OECD Economics Department

Volume 29, Issue 3. Application of the monetary policy function to output fluctuations in Bangladesh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Petroleum s impact on the national economy. Martin Skancke Director General

Petroleum s impact on the national economy Dili, May 2010 Martin Skancke Director General Asset Management Department Overview Part 1 Key challenges in managing petroleum revenues Important governance

Petroleum s impact on the national economy Dili, May 2010 Martin Skancke Director General Asset Management Department Overview Part 1 Key challenges in managing petroleum revenues Important governance