Revision of macroeconomic forecasts - November Dimitar Bogov Governor

|

|

|

- Megan Greer

- 5 years ago

- Views:

Transcription

1 Revision of macroeconomic forecasts - November Dimitar Bogov Governor 2 November 2017

2 Contents : Change in risks between the two forecasts External assumptions Macroeconomic scenario for

3 Change in risks between the two forecasts Unfavorable risks estimated to be lower than in the April forecasts......particularly risks arising from the domestic environment whose effects are assessed to be completely exhausted in the period ahead......external risks associated with the global economy are balanced in the short term, but still assessed as unfavorable in the medium term - uncertainty associated with the new US policies, increased protectionism, worsened conditions in the global financial markets, effects of the Brexit, as well as geopolitical turbulences However, in this scenario, there are favorable risks that are mainly associated with the possible larger positive effects of the operations of the new export-oriented companies 3

4 Key assumptions underlying October forecasts Assumption about stable environment and exhausted effects of the domestic political crisis for 2018 and 2019 Maintaining the assessments of sound economic fundamentals of the domestic economy Fundamental factors similar to the April forecasts - gradual improvement of the external environment, further contribution of foreign export-oriented facilities, expectations for continuation and acceleration of public infrastructure investments and increase of foreign investments, increased confidence of domestic entities and acceleration of credit growth Assumption about gradual fiscal consolidation, same as in the April forecast, in line with the budget revision for 2017 and the fiscal strategy for

5 Downward correction of the foreign effective inflation for 2017 and 2018 to 1.8% and 1.4% (April forecast: 1.9% and 1.6%, respectively), and in 2019, expectations for accelerated price growth in our major trading partners and forecasts for foreign inflation of 1.7% Analyzing primary commodities, slower increase in oil price in 2017 and stabilization in the next two years, divergent movements in food and metal prices Foreign effective inflation (annual rates in %) changes in p.p. (right axis) CF March 2017 CF September Q1 Q Q1 Q Q1 Q Q1 Q Q1 Q Q1 Q

, mainly reflecting the expectations for faster growth of Germany For 2019, there are expectations for slight slowdown in the economic activity of our trading partners and forecasts")

6 Upward revision of foreign demand for 2017 and growth of 2.2% and 2.1%, respectively (April: 1.8% and 1.9%, respectively), mainly reflecting the expectations for faster growth of Germany For 2019, there are expectations for slight slowdown in the economic activity of our trading partners and forecasts for foreign demand growth of 1.8% Foreign effective demand (annual changes in %) changes in p.p. (right axis) CF March 2017 CF September Q Q3 Q Q3 Q Q3 Q Q3 Q Q3 Q Q

Private consumption Investment Government consumption Imports Exports GDP (in %) 0.")

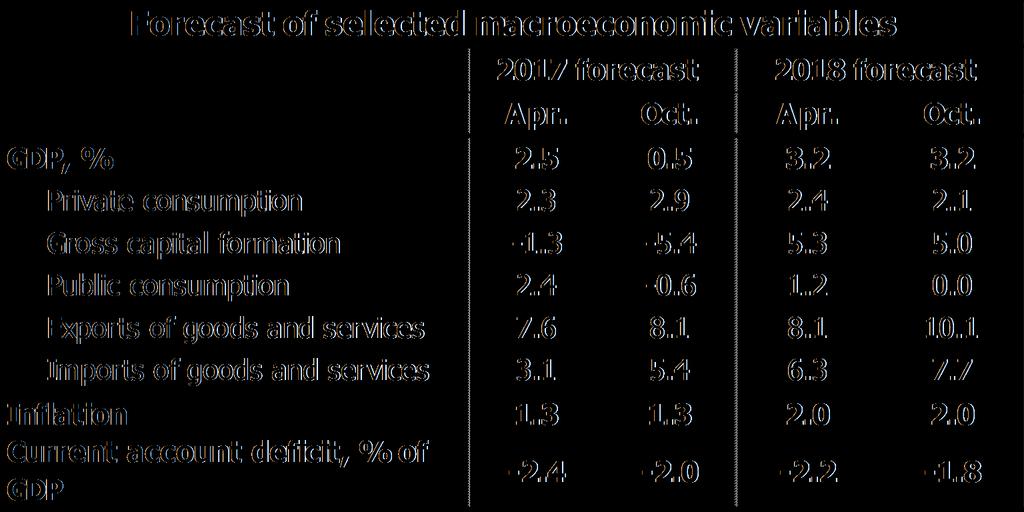

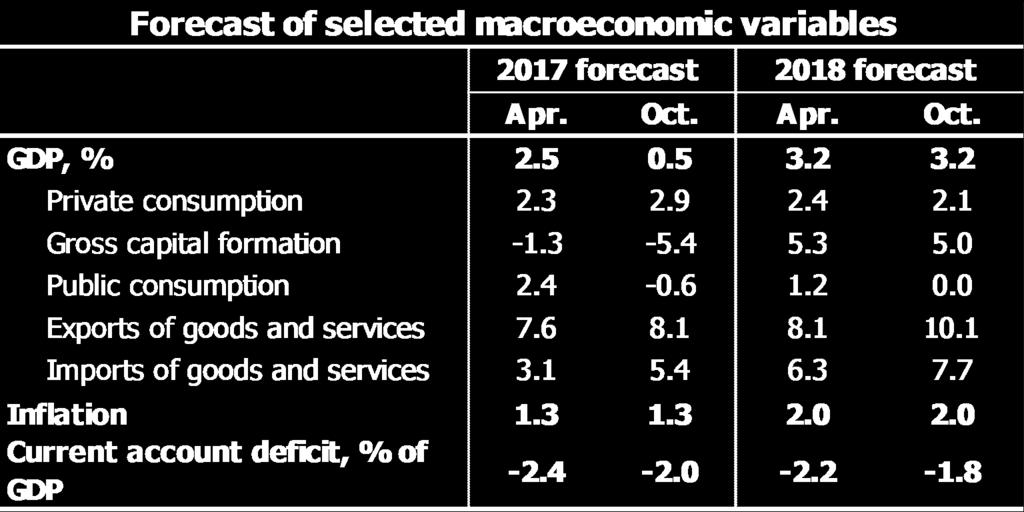

7 Macroeconomic scenario GDP forecast Downward correction of the forecast for economic growth for 2017, and retained estimates for growth in 2018, same as in April After the modest movement of 0.5% in 2017, there are expectations for reversal to the previous growth path for 2018 and 2019, at expected rates of 3.2% and 3.5%, respectively In , the economic growth is expected to be export driven, with additional impetus from investment and private consumption GDP (annual growth rates, in %) Growth decomposition (contributions to annual growth rate, in p.p.) Private consumption Investment Government consumption Imports Exports GDP (in %) Apr.17 Oct

8 GDP forecast Fundamental growth factors same as before - exports as generator of growth, with additional impetus from private consumption and investment: Exhaustion of the adverse effects of the political crisis and GDP growth in the second half of 2017, driven particularly by the solid growth of exports and private consumption, amid gradual recovery of investment On average for the three years, exports are expected to be the generator, driven by the new production facilities, as well as recovery of some of the traditional sectors and continued growth of the global economy Positive contribution of the private consumption, given the favorable developments in the disposable income and solid credit support Growth stimulated by investment - following the decrease in 2017, assessments for their growth supported by public and foreign investment, as well as improved investment environment for domestic investors Regarding the growth structure, in the medium term, domestic demand is expected to continue to make the greatest contribution to the growth, with the exception of 2017, when growth will be driven primarily by net exports GDP Private consumption Gross capital formation Exports of goods and services Imports of goods and services Public consumption Domestic demand Net exports % % p.p. % p.p. % p.p. % p.p. % p.p. contrib. in p.p

9 Inflation forecast The current pace of inflation generally follows the April forecasts Unchanged expectations about the price movement compared to April - expectations for normalization of inflation from 1.3% in 2017 to around 2% in 2018 and 2019, amid mild positive output gap, upward movements of some import prices and higher foreign inflation Risks to the forecast inflation trajectory mainly attributed to the uncertainty about import prices revisions (in p.p.) October 2017 April 2017 Inflation rate (in %) Q Q3 Q Q3 Q Q3 Q Q2 Q Q2 Q Q2 9

Reduction of the deficit in trade in goods")

10 Moderate current account deficit in the period , averaging about 2% (somewhat lower than the April forecast) Reduction of the deficit in trade in goods and services, with assessments for further improvement of the performance of the new export facilities, recovery of some traditional export sectors and improved balance of trade in services (similar to April) Slight decrease in the secondary income and assessments for further widening of the primary income deficit (slightly lower than in April)

and assessments for")

11 Inflows in the financial account in averaged 2.1% of GDP (slightly lower than expected in April) and assessments for financial inflows of 2.9% of GDP in 2019 Main inflows in the financial account during the forecast horizon: net inflows of foreign direct investment and long-term public sector borrowing During the entire forecast horizon, foreign reserves adequacy indicators are maintained in a safe zone

12 Forecast of deposit and credit growth In 2017, amid weaker performances, deposit growth is estimated at 3.6% (4.2% in the April forecast), and with the further stabilization of the expectations and increased economic activity, the growth of deposits is expected to accelerate to around 6 % in 2018 and 2019 For 2017, according to the previous performances, the credit growth was slightly corrected downward to 4.6% (5.2% in the April forecasts), and in 2018 and 2019, credit growth is expected to accelerate to around 7% The banking system remains stable, liquid and highly capitalized Credit and deposit growth Total credit, y-o-y changes, in % Total deposits, y-o-y changes, in % Total credit share in GDP, in % (RHS) 12

13 Summary Risks to the latest macroeconomic scenario have been reduced compared to the April forecasts......whereas the October forecast incorporates expectations for stable domestic environment and exhaustion of the effects of previous adverse political developments These projections show the potential for solid economic growth, stable prices, moderate external position, solid deposit and credit growth in With stable fundamentals, yet present risks at certain points, the NBRM did not make changes in the monetary policy in the third quarter The NBRM will continue to monitor the developments closely and if necessary, will make appropriate changes in the monetary policy 13

14 14

15 Appendix 2: Comparison of GDP and inflation forecasts for Macedonia 15

Latest Macroeconomic Projections - May Vice-Governor Anita Angelovska-Bezhoska

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

Macroeconomic projections for Assumptions from the external surrounding. Baseline macroeconomic scenario for

Dimitar Bogov Governor November, Macroeconomic projections for -4 Assumptions from the external surrounding Baseline macroeconomic scenario for -4 Comparison with the previous projection In the period

Dimitar Bogov Governor November, Macroeconomic projections for -4 Assumptions from the external surrounding Baseline macroeconomic scenario for -4 Comparison with the previous projection In the period

Macroeconomic Projections for 2014 and 2015

Macroeconomic Projections for 2014 and 2015 Anita Angelovska-Bezovska Vice-Governor March 2014 CONTENTS Process of macroeconomic projections and monetary policy decision-making Macroeconomic projections

Macroeconomic Projections for 2014 and 2015 Anita Angelovska-Bezovska Vice-Governor March 2014 CONTENTS Process of macroeconomic projections and monetary policy decision-making Macroeconomic projections

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT. Recent Macroeconomic Indicators Review of the Current Situation

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation February 216 Recent Macroeconomic Indicators Review of

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation February 216 Recent Macroeconomic Indicators Review of

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 This issue of Economic Review includes the of key macroeconomic indicators for the 2018 2020 period. It is based on information

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT. Recent Macroeconomic Indicators Review of the Current Situation

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation October 216 Recent Macroeconomic Indicators Review of

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation October 216 Recent Macroeconomic Indicators Review of

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2016 2018 The BNB forecast of key macroeconomic indicators is based on the information published as of 17 June 2016. ECB, EC and

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2016 2018 The BNB forecast of key macroeconomic indicators is based on the information published as of 17 June 2016. ECB, EC and

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT. Recent Macroeconomic Indicators Review of the Current Situation

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation January 216 Recent Macroeconomic Indicators Review of

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation January 216 Recent Macroeconomic Indicators Review of

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 The BNB forecast of key macroeconomic indicators is based on data published as of 15 June 2018. ECB, EC and IMF assumptions

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 The BNB forecast of key macroeconomic indicators is based on data published as of 15 June 2018. ECB, EC and IMF assumptions

MACROECONOMIC FORECAST

MACROECONOMIC FORECAST Spring 17 Ministry of Finance of the Republic of Bulgaria Bulgarian economy is expected to expand by 3% in 17 driven by domestic demand. As compared to 16, the external sector will

MACROECONOMIC FORECAST Spring 17 Ministry of Finance of the Republic of Bulgaria Bulgarian economy is expected to expand by 3% in 17 driven by domestic demand. As compared to 16, the external sector will

MACROECONOMIC FORECAST

MACROECONOMIC FORECAST Autumn 2017 Ministry of Finance of the Republic of Bulgaria The Autumn macroeconomic forecast of the Ministry of Finance takes into account better performance of the Bulgarian economy

MACROECONOMIC FORECAST Autumn 2017 Ministry of Finance of the Republic of Bulgaria The Autumn macroeconomic forecast of the Ministry of Finance takes into account better performance of the Bulgarian economy

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT. Recent Macroeconomic Indicators Review of the Current Situation

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation September 17 Recent Macroeconomic Indicators Review of

National Bank of the Republic of Macedonia MONETARY POLICY AND RESEARCH DEPARTMENT Recent Macroeconomic Indicators Review of the Current Situation September 17 Recent Macroeconomic Indicators Review of

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Slovak Macroeconomic Outlook

Slovak Macroeconomic Outlook CFA society 29 March 2017 Jan Toth Deputy Governor National Bank of Slovakia Summary Acceleration of GDP growth in the medium-term due to start of the new productions in the

Slovak Macroeconomic Outlook CFA society 29 March 2017 Jan Toth Deputy Governor National Bank of Slovakia Summary Acceleration of GDP growth in the medium-term due to start of the new productions in the

Meeting with Analysts

CNB s New Forecast (Inflation Report I/2018) Meeting with Analysts Tomáš Holub Prague, 2 February 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report I/2018) Meeting with Analysts Tomáš Holub Prague, 2 February 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

Economic growth prospects in the Czech Republic

Economic growth prospects in the 1st century in CEE Economic growth prospects in the Czech Republic Petr Král Deputy Executive Director, Monetary Department Czech National Bank 1 September 18 Krakow Economic

Economic growth prospects in the 1st century in CEE Economic growth prospects in the Czech Republic Petr Král Deputy Executive Director, Monetary Department Czech National Bank 1 September 18 Krakow Economic

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE GLOBAL TRENDS Accelerating growth in advanced economies (US, UK, Eurozone) vs. Slowdown in almost all emerging markets Downward revisions

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE GLOBAL TRENDS Accelerating growth in advanced economies (US, UK, Eurozone) vs. Slowdown in almost all emerging markets Downward revisions

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2018) Meeting with Analysts Petr Král Prague, 4 May 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report II/2018) Meeting with Analysts Petr Král Prague, 4 May 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

Economic Projections :2

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2018-2020 2018:2 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Macedonian economy during the global crisis and challenges ahead

Macedonian economy during the global crisis and challenges ahead Aneta Krstevska Chief Economist Skopje, January 13 Content: The impacts of the crisis on Macedonian economy and latest macroeconomic forecasts

Macedonian economy during the global crisis and challenges ahead Aneta Krstevska Chief Economist Skopje, January 13 Content: The impacts of the crisis on Macedonian economy and latest macroeconomic forecasts

2 Macroeconomic Scenario

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

The macroeconomic scenario was conceived as realistic and conservative with an effort to balance out the positive and negative risks of economic development..1 The World Economy and Technical Assumptions

Economic Projections :3

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Economic Projections 2018-2020 2018:3 Outlook for the Maltese economy Economic projections 2018-2020 The Central Bank s latest projections foresee economic growth over the coming three years to remain

Meeting with Analysts

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

CNB s New Forecast (Inflation Report III/2018) Meeting with Analysts Karel Musil Prague, 3 August 2018 Outline 1. Assumptions of the forecast 2. The new macroeconomic forecast 3. Comparison with the previous

Macroeconomic and financial market developments. March 2014

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

Macroeconomic and financial market developments March 2014 Background material to the abridged minutes of the Monetary Council meeting 25 March 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013 on

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Projections for the Portuguese Economy:

Projections for the Portuguese Economy: 2018-2020 March 2018 BANCO DE PORTUGAL E U R O S Y S T E M BANCO DE EUROSYSTEM PORTUGAL Projections for the portuguese economy: 2018-20 Continued expansion of economic

Projections for the Portuguese Economy: 2018-2020 March 2018 BANCO DE PORTUGAL E U R O S Y S T E M BANCO DE EUROSYSTEM PORTUGAL Projections for the portuguese economy: 2018-20 Continued expansion of economic

Introduction and summary

MACROECONOMIC PROJECTIONS FOR THE SPANISH ECONOMY (2018-2021): THE BANCO DE ESPAÑA S CONTRIBUTION TO THE EUROSYSTEM S DECEMBER 2018 JOINT FORECASTING EXERCISE Introduction and summary This report describes

MACROECONOMIC PROJECTIONS FOR THE SPANISH ECONOMY (2018-2021): THE BANCO DE ESPAÑA S CONTRIBUTION TO THE EUROSYSTEM S DECEMBER 2018 JOINT FORECASTING EXERCISE Introduction and summary This report describes

The ECB Survey of Professional Forecasters. Fourth quarter of 2016

The ECB Survey of Professional Forecasters Fourth quarter of 16 October 16 Contents 1 Inflation expectations for 16-18 broadly unchanged 3 2 Longer-term inflation expectations unchanged at 1.8% 4 3 Real

The ECB Survey of Professional Forecasters Fourth quarter of 16 October 16 Contents 1 Inflation expectations for 16-18 broadly unchanged 3 2 Longer-term inflation expectations unchanged at 1.8% 4 3 Real

Economic Projections For 2014 And 2015

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

Economic Projections For 2014 And 2015 Article published in the Quarterly Review 2014:3, pp. 77-81 7. ECONOMIC PROJECTIONS FOR 2014 AND 2015 Outlook for the Maltese economy 1 The Bank s latest macroeconomic

Outlook for Economic Activity and Prices (April 2010)

") April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

Developments in inflation and its determinants

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

INFLATION REPORT February 2018 Summary Developments in inflation and its determinants The annual CPI inflation rate strengthened its upward trend in the course of 2017 Q4, standing at 3.32 percent in December,

Economic projections

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Economic projections 2017-2020 December 2017 Outlook for the Maltese economy Economic projections 2017-2020 The pace of economic activity in Malta has picked up in 2017. The Central Bank s latest economic

Latvia's Macro Profile January 2019

Latvia's Macro Profile January 2019 Incl. macro comparison of LV, EE and LT. Latvia's Economic Developments and Outlook Last year's growth robust and balanced Latvia's economic growth was robust and balanced

Latvia's Macro Profile January 2019 Incl. macro comparison of LV, EE and LT. Latvia's Economic Developments and Outlook Last year's growth robust and balanced Latvia's economic growth was robust and balanced

Latin America Outlook. 1st QUARTER 2018

Latin America Outlook 1st QUARTER Main messages 1. Strong global growth continues. Forecasts revised up in in most areas. Growth stabilizing in. 2. Growth recovers in Latin America, reaching close to potential

Latin America Outlook 1st QUARTER Main messages 1. Strong global growth continues. Forecasts revised up in in most areas. Growth stabilizing in. 2. Growth recovers in Latin America, reaching close to potential

China Economic Outlook 2013

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

Erdem Başçi: Recent economic and financial developments in Turkey

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Erdem Başçi: Recent economic and financial developments in Turkey Speech by Mr Erdem Başçi, Governor of the Central Bank of the Republic of Turkey, at the press conference for the presentation of the April

Czech Monetary Policy and Economic Outlook

IMF/WB Annual Meetings 17 Czech Monetary Policy and Economic Outlook Vladimir TOMSIK Vice-Governor Czech National Bank Bank of America Merril Lynch Symposium and JPMorgan Investor Seminar 13 1 October

IMF/WB Annual Meetings 17 Czech Monetary Policy and Economic Outlook Vladimir TOMSIK Vice-Governor Czech National Bank Bank of America Merril Lynch Symposium and JPMorgan Investor Seminar 13 1 October

HKU Announced 2013 Q3 HK Macroeconomic Forecast

COMMUNICATIONS & PUBLIC AFFAIRS OFFICE THE UNIVERSITY OF HONG KONG Enquiry: 2859 1106 Website: http://www.hku.hk/cpao For Immediate Release HKU Announced 2013 Q3 HK Macroeconomic Forecast Hong Kong Economic

COMMUNICATIONS & PUBLIC AFFAIRS OFFICE THE UNIVERSITY OF HONG KONG Enquiry: 2859 1106 Website: http://www.hku.hk/cpao For Immediate Release HKU Announced 2013 Q3 HK Macroeconomic Forecast Hong Kong Economic

Main Economic & Financial Indicators Poland

Main Economic & Financial Indicators Poland. 6 OCTOBER 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Main Economic & Financial Indicators Poland. 6 OCTOBER 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Peru: Revised Multiannual Macroeconomic Framework

Peru: Revised Multiannual Macroeconomic Framework 2017-2019 Executive Summary The Revised Multiannual Macroeconomic Framework (Revised MMF) presents the government s official projections, and was approved

Peru: Revised Multiannual Macroeconomic Framework 2017-2019 Executive Summary The Revised Multiannual Macroeconomic Framework (Revised MMF) presents the government s official projections, and was approved

The ECB Survey of Professional Forecasters (SPF) Third quarter of 2016

Third quarter of 2016") The ECB Survey of Professional Forecasters (SPF) Third quarter of 2016 July 2016 Contents 1 Inflation expectations revised slightly down for 2017 and 2018 3 2 Longer-term inflation expectations unchanged

The ECB Survey of Professional Forecasters (SPF) Third quarter of 2016 July 2016 Contents 1 Inflation expectations revised slightly down for 2017 and 2018 3 2 Longer-term inflation expectations unchanged

Economic Projections for

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

NATIONAL BANK OF SERBIA. Speech at the presentation of the Inflation Report November 2017

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November Dr Ana Ivković, General Manager Directorate for Economic Research and Statistics Belgrade, November Ladies and gentlemen,

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November Dr Ana Ivković, General Manager Directorate for Economic Research and Statistics Belgrade, November Ladies and gentlemen,

Czech monetary policy: On a way to neutral interest rates

Czech monetary policy: On a way to neutral interest rates Petr Král Deputy Executive Director Monetary Department Czech & Hungary Investor Day London, 14 November 2018 Current economic situation 2 Structure

Czech monetary policy: On a way to neutral interest rates Petr Král Deputy Executive Director Monetary Department Czech & Hungary Investor Day London, 14 November 2018 Current economic situation 2 Structure

MEDIUM-TERM FORECAST

MEDIUM-TERM FORECAST Q2 2010 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: Monetary Policy Department +421 2 5787 2611 +421

MEDIUM-TERM FORECAST Q2 2010 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: Monetary Policy Department +421 2 5787 2611 +421

Eurozone Economic Watch

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

BBVA Research Eurozone Economic Watch November 2018 / 1 Eurozone Economic Watch November 2018 Eurozone: Growth to recover in 4Q18, but concerns about the slowdown next year are growing Eurozone GDP growth

The ECB Survey of Professional Forecasters (SPF) First quarter of 2016

First quarter of 2016") The ECB Survey of Professional Forecasters (SPF) First quarter of 16 January 16 Content 1 Inflation expectations maintain upward profile but have been revised down for 16 and 17 3 2 Longer-term inflation

The ECB Survey of Professional Forecasters (SPF) First quarter of 16 January 16 Content 1 Inflation expectations maintain upward profile but have been revised down for 16 and 17 3 2 Longer-term inflation

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

Minutes of the Monetary Policy Council decision-making meeting held on 2 September 2015 Members of the Monetary Policy Council discussed monetary policy against the background of the current and expected

2. International developments

2. International developments (6) During the period, global economic developments were generally positive. The economy grew faster in the second quarter, mainly driven by the favourable financing conditions

2. International developments (6) During the period, global economic developments were generally positive. The economy grew faster in the second quarter, mainly driven by the favourable financing conditions

Economic Projections :1

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Projections 2017-2020 2018:1 Outlook for the Maltese economy Economic projections 2017-2020 The Central Bank s latest economic projections foresee economic growth over the coming three years to

Economic Outlook for FY2010 and FY2011

Economic Outlook for FY2010 and FY2011 (revised to reflect the Second Preliminary Quarterly Estimates of GDP for the Jan-Mar quarter of 2010) June 2010 Key points of Mizuho Research Institute s (MHRI)

Economic Outlook for FY2010 and FY2011 (revised to reflect the Second Preliminary Quarterly Estimates of GDP for the Jan-Mar quarter of 2010) June 2010 Key points of Mizuho Research Institute s (MHRI)

I N F L A T I O N R E P O R T

I N F L A T I O N R E P O R T M A R C H 1 ... wise is the man who can put purpose to his desires. Miklós Zrínyi: The Life of Matthias Corvinus I N F L A T I O N R E P O R T M A R C H 1 Published by the

I N F L A T I O N R E P O R T M A R C H 1 ... wise is the man who can put purpose to his desires. Miklós Zrínyi: The Life of Matthias Corvinus I N F L A T I O N R E P O R T M A R C H 1 Published by the

The Economic Outlook of Taiwan

The Economic Outlook of Taiwan by Ray Yeutien Chou and An-Chi Wu The Institute of Economics, Academia Sinica, Taipei October 2017 1 Prepared for Project LINK 2017 Fall Meeting, Geneva, Oct. 3-5, 2017 2

The Economic Outlook of Taiwan by Ray Yeutien Chou and An-Chi Wu The Institute of Economics, Academia Sinica, Taipei October 2017 1 Prepared for Project LINK 2017 Fall Meeting, Geneva, Oct. 3-5, 2017 2

NATIONAL BANK OF SERBIA. Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor Belgrade, May Ladies and gentlemen, representatives of the press, dear colleagues, Welcome

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report May Dr Jorgovanka Tabaković, Governor Belgrade, May Ladies and gentlemen, representatives of the press, dear colleagues, Welcome

The ECB Survey of Professional Forecasters. First quarter of 2017

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

The ECB Survey of Professional Forecasters First quarter of 217 January 217 Contents 1 Near-term inflation expectations a little higher, due to oil price rises 3 2 Longer-term inflation expectations unchanged

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Minutes of the Monetary Policy Council decision-making meeting held on 6 July 2016 At the meeting, members of the Monetary Policy Council discussed monetary policy against the background of macroeconomic

Foreign Direct Investments in the RM. Anita Angelovska Bezhoska Vice Governor National Bank of the Republic of Macedonia October 2014

Foreign Direct Investments in the RM Anita Angelovska Bezhoska Vice Governor National Bank of the Republic of Macedonia October 2014 Foreign Direct Investments and Economic Growth FDIs are considered an

Foreign Direct Investments in the RM Anita Angelovska Bezhoska Vice Governor National Bank of the Republic of Macedonia October 2014 Foreign Direct Investments and Economic Growth FDIs are considered an

JUNE 2015 EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA 1

JUNE 2015 EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA 1 1. EURO AREA OUTLOOK: OVERVIEW AND KEY FEATURES The June projections confirm the outlook for a recovery in the euro area. According

JUNE 2015 EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA 1 1. EURO AREA OUTLOOK: OVERVIEW AND KEY FEATURES The June projections confirm the outlook for a recovery in the euro area. According

NATIONAL BANK OF ROMANIA

1 The annual inflation rate dropped below the mid-point of the ±1pp variation band around the 3% target set by the NBR for 212 12 annual percentage change 1 8 Target 2 5. 2 Target 27. Target 28 3.8 Target

1 The annual inflation rate dropped below the mid-point of the ±1pp variation band around the 3% target set by the NBR for 212 12 annual percentage change 1 8 Target 2 5. 2 Target 27. Target 28 3.8 Target

Austria s economy set to grow by close to 3% in 2018

Austria s economy set to grow by close to 3% in 218 Gerhard Fenz, Friedrich Fritzer, Fabio Rumler, Martin Schneider 1 Economic growth in Austria peaked at the end of 217. The first half of 218 saw a gradual

Austria s economy set to grow by close to 3% in 218 Gerhard Fenz, Friedrich Fritzer, Fabio Rumler, Martin Schneider 1 Economic growth in Austria peaked at the end of 217. The first half of 218 saw a gradual

Russia Monthly Economic Developments June 2018

Russia Monthly Economic Developments June 2018 The global economy experienced divergent growth in the second quarter of 2018 characterized by a rebounding in advanced economies, continued moderation in

Russia Monthly Economic Developments June 2018 The global economy experienced divergent growth in the second quarter of 2018 characterized by a rebounding in advanced economies, continued moderation in

Economic Bulletin December 2018

Economic Bulletin December 218 Economic Bulletin December 218 BANCO DE PORTUGAL EUROSYSTEM Lisbon, 218 www.bportugal.pt Economic Bulletin December 218 Banco de Portugal Av. Almirante Reis, 71 115-12 Lisboa

Economic Bulletin December 218 Economic Bulletin December 218 BANCO DE PORTUGAL EUROSYSTEM Lisbon, 218 www.bportugal.pt Economic Bulletin December 218 Banco de Portugal Av. Almirante Reis, 71 115-12 Lisboa

PBO Economic and Fiscal Outlook. Ottawa, Canada November 1,

PBO Economic and Fiscal Outlook Ottawa, Canada November 1, 11 www.parl.gc.ca/pbo-dpb PBO Economic and Fiscal Outlook The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis

PBO Economic and Fiscal Outlook Ottawa, Canada November 1, 11 www.parl.gc.ca/pbo-dpb PBO Economic and Fiscal Outlook The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis

Consensus Forecast 2010 and 2011

Consensus Forecast 2010 and 2011 Seventeenth Annual Automotive Outlook Symposium Detroit, Michigan June 4, 2010 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Review

Consensus Forecast 2010 and 2011 Seventeenth Annual Automotive Outlook Symposium Detroit, Michigan June 4, 2010 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Review

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 19 July 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 19 July 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

54 ECB RESULTS OF THE ECB SURVEY OF PROFESSIONAL FORECASTERS FOR THE FOURTH QUARTER OF 2009

Box 7 RESULTS OF THE ECB SURVEY OF PROFESSIONAL FORECASTERS FOR THE FOURTH QUARTER OF 9 This box reports the results of the ECB Survey of Professional Forecasters (SPF) for the fourth quarter of 9. The

Box 7 RESULTS OF THE ECB SURVEY OF PROFESSIONAL FORECASTERS FOR THE FOURTH QUARTER OF 9 This box reports the results of the ECB Survey of Professional Forecasters (SPF) for the fourth quarter of 9. The

BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

Europe Outlook. Third Quarter 2015

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

Europe Outlook Third Quarter 2015 Main messages 1 2 3 4 5 Moderation of global growth and slowdown in emerging economies, with downside risks The recovery continues in the eurozone, but still marked by

The Future of Mexican Monetary Policy

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

Medium-term. forecast

Medium-term forecast Q1 2018 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: +421 2 5787 2146 http://www.nbs.sk Discussed by

Medium-term forecast Q1 2018 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: +421 2 5787 2146 http://www.nbs.sk Discussed by

Monetary Policy Report

Monetary Policy Report 219/I The report refers to s Monetary Policy statement for 218 H2, Approved by the Supervisory Council, Decision No. 5, Dated 6.2.219 Data from this publication may be used, provided

Monetary Policy Report 219/I The report refers to s Monetary Policy statement for 218 H2, Approved by the Supervisory Council, Decision No. 5, Dated 6.2.219 Data from this publication may be used, provided

September 2017 ECB staff macroeconomic projections for the euro area 1

September 2017 ECB staff macroeconomic projections for the euro area 1 The economic expansion in the euro area is projected to continue over the projection horizon at growth rates well above potential.

September 2017 ECB staff macroeconomic projections for the euro area 1 The economic expansion in the euro area is projected to continue over the projection horizon at growth rates well above potential.

CNB Monetary Policy on its Way Back to Normal

CNB Monetary Policy on its Way Back to Normal Luboš KOMÁREK Czech National Bank Spring Meetings 2018 Washington, D.C. Exit from FX commitment % CZK/EUR FX commitment was abandoned on 6 April 2017 as conditions

CNB Monetary Policy on its Way Back to Normal Luboš KOMÁREK Czech National Bank Spring Meetings 2018 Washington, D.C. Exit from FX commitment % CZK/EUR FX commitment was abandoned on 6 April 2017 as conditions

The ECB Survey of Professional Forecasters. Second quarter of 2017

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

The ECB Survey of Professional Forecasters Second quarter of 17 April 17 Contents 1 Near-term headline inflation expectations revised up, expectations for HICP inflation excluding food and energy broadly

National Bank of the Republic of Macedonia Research Department. Monthly Information 10/2012

National Bank of the Republic of Macedonia Research Department Monthly Information 1/212 November, 212 Summary During October 212, the National Bank kept the key interest rate at the level of 3.75%, assessing

National Bank of the Republic of Macedonia Research Department Monthly Information 1/212 November, 212 Summary During October 212, the National Bank kept the key interest rate at the level of 3.75%, assessing

In fiscal year 2016, for the first time since 2009, the

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

Summary In fiscal year 216, for the first time since 29, the federal budget deficit increased in relation to the nation s economic output. The Congressional Budget Office projects that over the next decade,

RESULTS OF THE ECB SURVEY OF PROFESSIONAL FORECASTERS FOR THE SECOND QUARTER OF 2012

Box 7 RESULTS OF THE SURVEY OF PROFESSIONAL FORECASTERS FOR THE SECOND QUARTER OF 212 This box reports the results of the Survey of Professional Forecasters (SPF) for the second quarter of 212. The survey

Box 7 RESULTS OF THE SURVEY OF PROFESSIONAL FORECASTERS FOR THE SECOND QUARTER OF 212 This box reports the results of the Survey of Professional Forecasters (SPF) for the second quarter of 212. The survey

INFLATION REPORT / III

INFLATION REPORT / III 11 INFLATION REPORT / III FOREWORD 3 In 1998, the Czech National Bank switched to inflation targeting. In the inflation targeting regime, the central bank s communication with

INFLATION REPORT / III 11 INFLATION REPORT / III FOREWORD 3 In 1998, the Czech National Bank switched to inflation targeting. In the inflation targeting regime, the central bank s communication with

Assessment of the 2018 Stability Programme for. Portugal

EUROPEAN COMMISSION DIRECTORATE GENERAL ECONOMIC AND FINANCIAL AFFAIRS Brussels, 23 May 2018 Assessment of the 2018 Stability Programme for Portugal (Note prepared by DG ECFIN staff) 1 CONTENTS 1. INTRODUCTION...

EUROPEAN COMMISSION DIRECTORATE GENERAL ECONOMIC AND FINANCIAL AFFAIRS Brussels, 23 May 2018 Assessment of the 2018 Stability Programme for Portugal (Note prepared by DG ECFIN staff) 1 CONTENTS 1. INTRODUCTION...

Projections for the Portuguese economy in 2017

Projections for the Portuguese economy in 2017 85 Projections for the Portuguese economy in 2017 Continued recovery process of the Portuguese economy According to the projections prepared by Banco de Portugal,

Projections for the Portuguese economy in 2017 85 Projections for the Portuguese economy in 2017 Continued recovery process of the Portuguese economy According to the projections prepared by Banco de Portugal,

Eurozone Economic Watch. May 2018

Eurozone Economic Watch May 2018 BBVA Research - Eurozone Economic Watch / 2 Eurozone: more moderate growth with higher uncertainty The eurozone GDP growth slowed in more than expected. Beyond temporary

Eurozone Economic Watch May 2018 BBVA Research - Eurozone Economic Watch / 2 Eurozone: more moderate growth with higher uncertainty The eurozone GDP growth slowed in more than expected. Beyond temporary

Projections for the Portuguese economy:

Projections for the Portuguese economy: 217-19 7 Projections for the Portuguese economy: 217-19 1. Introduction The projections for the Portuguese economy point to a continued economic activity recovery

Projections for the Portuguese economy: 217-19 7 Projections for the Portuguese economy: 217-19 1. Introduction The projections for the Portuguese economy point to a continued economic activity recovery

Medium-term. forecast

Medium-term forecast Q2 217 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: +421 2 5787 2146 http://www.nbs.sk Discussed by

Medium-term forecast Q2 217 Published by: Národná banka Slovenska Address: Národná banka Slovenska Imricha Karvaša 1 813 25 Bratislava Slovakia Contact: +421 2 5787 2146 http://www.nbs.sk Discussed by

Recent developments. Note: The author of this section is Yoki Okawa. Research assistance was provided by Ishita Dugar. 1

Growth in the Europe and Central Asia region is anticipated to ease to 3.2 percent in 2018, down from 4.0 percent in 2017, as one-off supporting factors wane in some of the region s largest economies.

Growth in the Europe and Central Asia region is anticipated to ease to 3.2 percent in 2018, down from 4.0 percent in 2017, as one-off supporting factors wane in some of the region s largest economies.

Outlook for Economic Activity and Prices (April 2018)

") Outlook for Economic Activity and Prices (April 2018) The Bank's View 1 Summary April 27, 2018 Bank of Japan Japan's economy is likely to continue growing at a pace above its potential in fiscal 2018,

Outlook for Economic Activity and Prices (April 2018) The Bank's View 1 Summary April 27, 2018 Bank of Japan Japan's economy is likely to continue growing at a pace above its potential in fiscal 2018,

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Main Economic & Financial Indicators The Czech Republic

Main Economic & Financial Indicators The Czech Republic 15 OCTOBER 215 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-()2-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi

Main Economic & Financial Indicators The Czech Republic 15 OCTOBER 215 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-()2-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 23 November 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 23 November 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

NATIONAL BANK OF SERBIA. Speech at the presentation of the Inflation Report November 2018

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November 8 Savo Jakovljević, Acting General Manager of the Economic Research and Statistics Department Belgrade, November 8 Ladies

NATIONAL BANK OF SERBIA Speech at the presentation of the Inflation Report November 8 Savo Jakovljević, Acting General Manager of the Economic Research and Statistics Department Belgrade, November 8 Ladies

Meeting with Analysts

CNB s New Forecast (Inflation Report III/3) Meeting with Analysts Tibor Hlédik Prague, 9 August, 3 Summary of the Inflation Forecast (i) The recovery of GDP in the effective euro area is postponed again

CNB s New Forecast (Inflation Report III/3) Meeting with Analysts Tibor Hlédik Prague, 9 August, 3 Summary of the Inflation Forecast (i) The recovery of GDP in the effective euro area is postponed again

MONETARY POLICY REPORT. June 2018

MONETARY POLICY REPORT June MONETARY POLICY REPORT * / JUNE */ This is a translation of a document originally written in Spanish. In case of discrepancy or difference in interpretation the Spanish original

MONETARY POLICY REPORT June MONETARY POLICY REPORT * / JUNE */ This is a translation of a document originally written in Spanish. In case of discrepancy or difference in interpretation the Spanish original

World Economic outlook

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Frontier s Strategy Note: 01/23/2014 World Economic outlook IMF has just released the World Economic Update on the 21st January 2015 and we are displaying the main points here. Even with the sharp oil

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2016 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS Fourth Quarter 2016 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Econ 102 Exam 2 Name ID Section Number

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

Econ 102 Exam 2 Name ID Section Number 1. Suppose investment spending increases by $50 billion and as a result the equilibrium income increases by $200 billion. The investment multiplier is: A) 10. B)

SUMMARY OF MACROECONOMIC DEVELOPMENTS

SUMMARY OF MACROECONOMIC DEVELOPMENTS FEBRUARY 2018 2 Summary of macroeconomic developments, February 2018 Forecasts for global economic developments over the medium term are optimistic. In its January

SUMMARY OF MACROECONOMIC DEVELOPMENTS FEBRUARY 2018 2 Summary of macroeconomic developments, February 2018 Forecasts for global economic developments over the medium term are optimistic. In its January

Svein Gjedrem: The outlook for the Norwegian economy

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Short-term indicators and Updated Forecasts. Eurozone NOVEMBER 2016

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the