1Q18 M&A AND CORPORATE AFINANCE OVERVIEW: Merger & Acquisition Corporate Finance Advisory Strategic Consulting

|

|

|

- Katrina Casey

- 5 years ago

- Views:

Transcription

1 M&A AND CORPORATE AFINANCE OVERVIEW: 1Q18 Merger & Acquisition Corporate Finance Advisory Strategic Consulting 400 Southpointe Boulevard, Plaza I, Suite 440 Canonsburg, PA Tel Fax Securities and investment advisory services are offered through BPU Investment Management, Inc. 301 Grant Street, Suite 3300 / Pittsburgh, PA Telephone: / Website: Member FINRA/SIPC, and an SEC registered investment advisor

in the United States. The number of total private equity (PE) deals tracked by Pitchbook was down 4.")

2 Bringing Efficiency to Inefficient Markets Executive Summary Clear Skies But Muddy Waters: Deal Volume Mixed In 1Q18 But Expected to Recover 1Q18 saw mixed deal and funding activity for PE and the middle market (MM) in the United States. The number of total private equity (PE) deals tracked by Pitchbook was down 4.0% in 1Q18 compared to 4Q17 but was far better than the typical first quarter 25% decline in deal count. However, deal activity for sub $500.0m transactions as measured by Baird actually increased 4.3% year over year through February. Add on acquisitions continued to gain in popularity, comprising 70% of buy out activity in 1Q18. US PE Fundraising also declined in 1Q18 compared to 4Q17. Median fund size followed suit, declining slightly in 1Q18 to $252.5m compared to $275.0m in Questions on price and quality continue to dog deal flow, but these concerns are counter balanced by strong investor demand and a friendly financing environment. Average valuations in the lower MM (deals of $250.0m or less) declined slightly to 6.9x Total Enterprise Value (TEV) to EBITDA in 1Q18 from 7.4x in This compares to the aggregate median valuation of all U.S. PE deals (deals of $25.0m to $1.0bn+) of 10.5x in Since the recession, valuations have been benefiting from intense deal competition driven by bulge bracket PE firms shopping down market from non traditional participants such as family offices, insurance companies, and institutional pension funds. A competitive financing environment and a glut of available capital have kept deal terms friendly. This supported higher leverage multiples across all deal levels, albeit with an increase in rep and warranty insurance. Leverage as measured by total debt to EBITDA was 4.2x for the lower MM in 1Q18 (down from 4.3x in 4Q17) and 5.7x for all US PE deals in Despite a mixed start to 2018, the outlook for the year remains supportive of a strong PE and MM M&A environment reflecting small and MM business optimism and positive views from PE industry participants. Nonetheless, an increased chance of recession looms, which is continuing to increase downside risk to this outlook. Recession will likely be driven by changes to inflation (and the resulting Federal Reserve policy), the strength of the dollar, and trade policy.

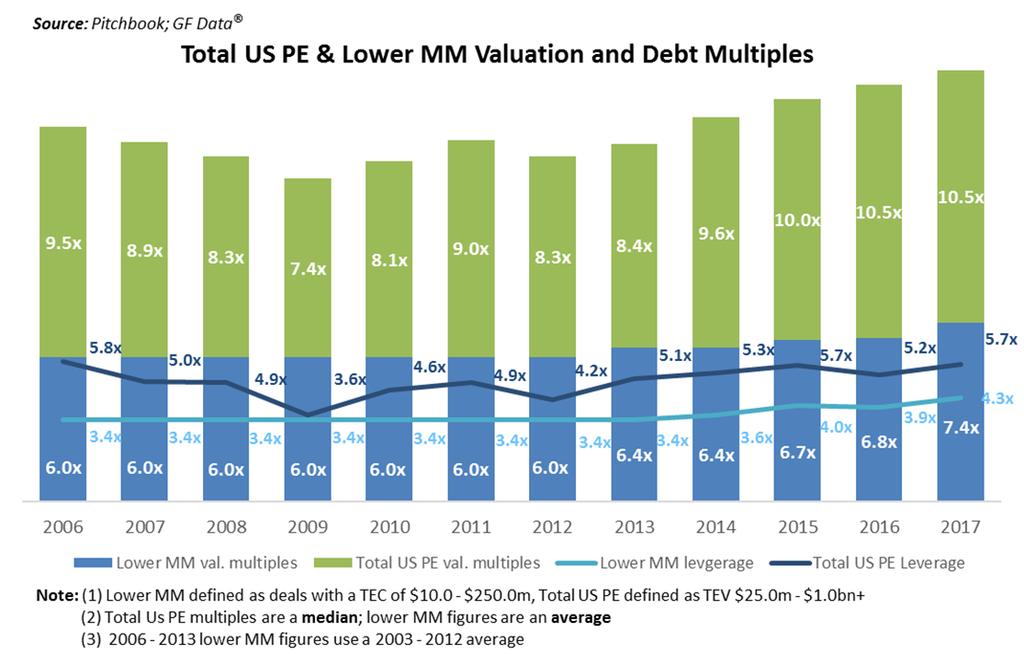

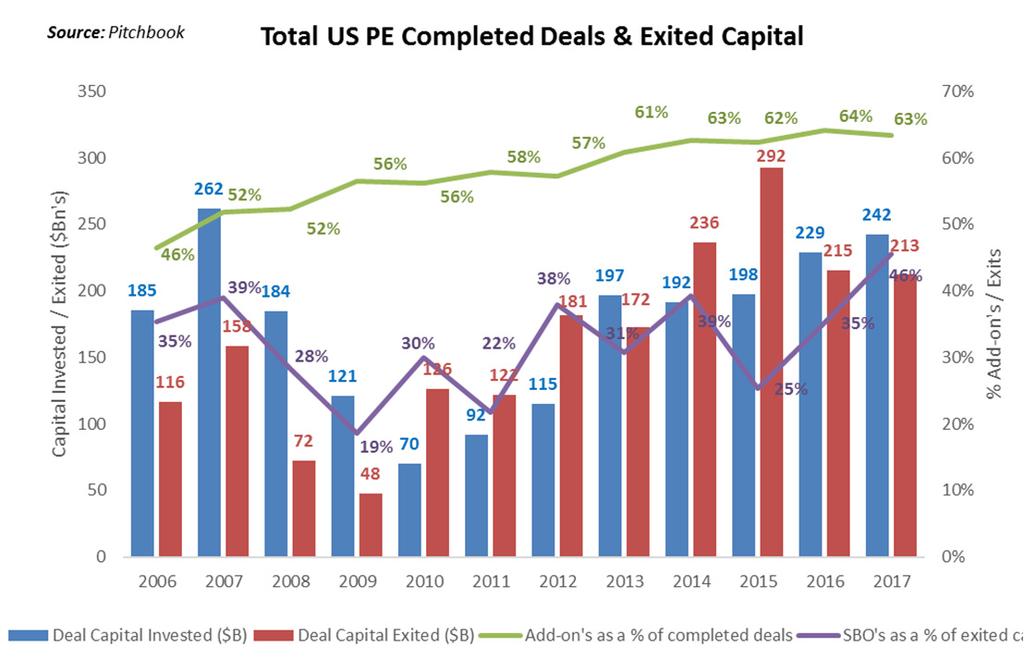

3 The View From Above 1Q18: A Rocky But Not Unexpected Start to 2018 Add on acquisitions continued to represent the majority of buy out activity (70%) in 1Q18. The grab for add on acquisitions will likely diminish the investible universe of these assets and support high multiples across lower tier EBITDA thresholds. High valuations and aggressive financing terms remained the norm through 1Q18. However, deal count, fundraising, and valuations experienced mixed results for the quarter. This is in contrast to overall US and Canadian M&A activity, which according to Mergermarket was up 17.4% to $412.2bn year over year in 1Q18. According to Pitchbook s US PE Breakdown 1Q 2018 report, 881 deals were completed across the U.S. in 1Q18 with an aggregate deal value of $76.6bn. When factoring in estimated deals closed, these figures rise to 1,101 deals with a value of $88.8bn for a year over year decline of 4.0% and 32.8%, respectively. Partially mitigating deal flow concerns are the 124 deals worth $94.3bn, which have been announced but have yet to close in Despite sitting on just over a trillion in dry powder globally, the number of completed PE deals declined due to price and target quality concerns. In terms of split, MM deals contributed 530 (60%) of completed deals and $324.0bn (59%) of total capital. Although the pace of completed deals has continued to decelerate compared to , competition has sustained high median valuation multiples mutiples for all PE transactions were 10.5x Total Enterprise Value (TEV) to EBITDA and 10.4x for the MM. Multiples for the lower MM (TEV of $10.0m to $250m) declined slightly during 1Q18 to 6.9x but were within the range of previous quarters. Despite this, robust valuations have been noted by the Lincoln Middle Market Index (MMI) over 1Q18, which saw a growth rate in enterprise values of 2.9% compared to 0.9% for the S&P 500. This index measures quarterly changes in enterprise values for 350 MM companies, primarily owned by PE groups. Since 1Q14 the MMI has appreciated by 28.2%. The technology segment led the index over the last year, increasing 16.4%, followed by industrials at 10%. Deal exit volume dropped 27% in 1Q18 to 196 exits worth $36.6bn (compared to 269 exits worth $64.2bn in 4Q17). Of total US PE exits, 84% of exited deals and 33% of exited capital was attributed to the MM. The decline in the number of exited deals was largely due to the continued decline in Secondary Buyouts (SBO s), which were down from 46% of exited capital in 2017 to 25% in 1Q18. SBO s are transactions where a PE owned portfolio company sells to another PE fund. Corporate acquisitions accounted for 61% of exited capital in 1Q 2018, comprised of 505 deals worth $85.1bn. SBO s have until 1Q18 trended as an increasingly popular exit opportunity. SBO s will likely rebound in the coming quarters given that many PE funds are maturing (more than a third of portfolio companies are more than five years old) in an environment flush with dry powder, thereby making other PE firms the most likely buyers in an exit. Median buyout size continued to increase through 1Q18 to $175.0m (up 17% over FY 2017) due to the aforementioned increase in deal multiples. From a sector standpoint, healthcare PE deals fell the most over the last quarter as a percentage of deal value in dollars (from 16% to 14%), whereas IT, financial services, and B2B *Strategic Advisors defines the Lower Middle Market as deals having a TEV of between $10.0m and $250.0m

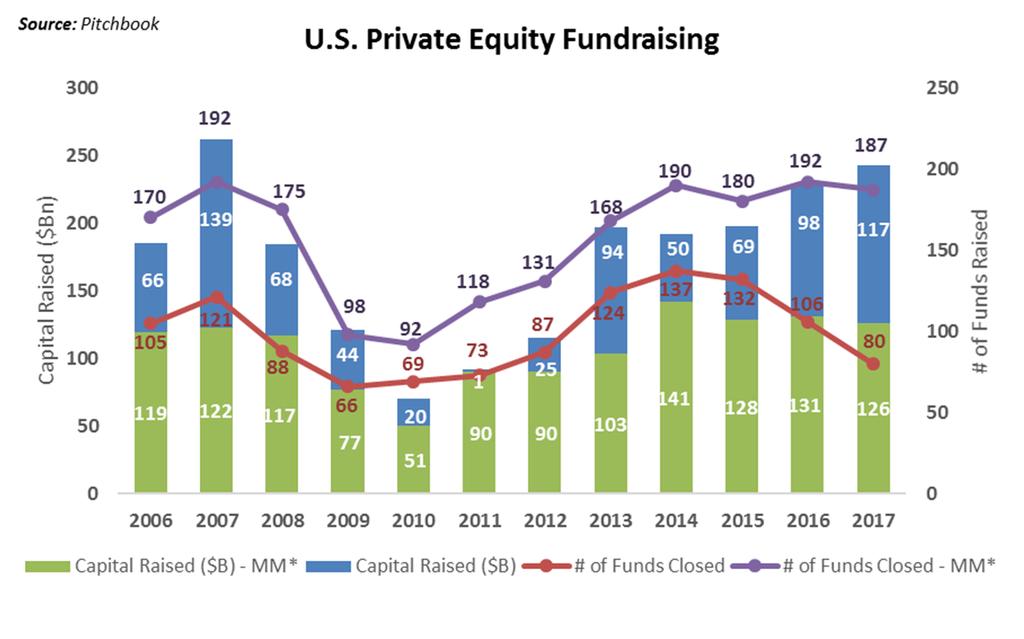

4 *Pitchbook defines the Middle Market (MM) as deals having a TEV of $25.0m - $1.0bn; all other deals are > $1.0bn had the largest increase at 1% each. All other sectors remained flat or decreased slightly. Capital raised by PE funds in 1Q18 totaled $36.6bn committed across 55 funds, compared to $63.9bn in capital raised across 83 funds in 4Q had been the strongest fundraising year in a decade, which likely took some steam out of early 1Q18. Breaking down the figures, the MM accounted for 79% of capital raised across 65% of funds raised. Larger funds (over $1.0bn) continue to raise a large portion of funds, taking in over half of raised capital in 1Q18. GF Data CEO Andrew Greenberg believes that continued high valuations could be frothy market conditions extending to businesses that are more pedestrian and may signal a peak in market valuations. GF Data co founder, Mr. Graeme Frazier, noted that another reason for high multiples may be the continued trend favoring add on acquisitions. Yet another reason is likely due to strong MM earnings, which according to a Golub Capital MM report grew 6.22% year over year through 1Q18 and 12.77% in FY Median US PE size of raised funds declined slightly in 1Q18 from $275.0m in 2017 to $252.5m in 1Q18. Approximately 19% of these investments are concentrated in mega funds with more than $5.0bn at closing, a decrease from 47% of all capital raised in Despite continued consolidation into mega funds, the number of first time funds, as a percentage of all funds raised, has remained above the historical trough seen in There is a continued re assertion of the quality premium, which GF Data refers to as the valuation reward offered for above average financial performance (defined as those with both EBITDA margins and revenue growth rates at or above 10%, or with one factor above 12% and the other metric at 8% or above). In 1Q18, this premium was at 21% (flat since 2016) and was in line with 2015 and 2016 figures. Middle Market Deal Structure & Terms Leverage Declines Slightly; Still Near Record Highs The average total debt multiple on MM deals with a TEV of up to $250.0m declined slightly in 1Q18 to 4.2x (comprised of 3.4x senior debt & 0.8x sub debt) compared to 4.4x in 4Q17. Debt multiples ranged from 3.3x for deals with a TEV of $10.0m $25.0m to 4.9x for deals with a TEV of $100.0m $250.0m. The median leverage in 2017 was 5.7x for the entire US PE MM. Lower MM average debt multiples have been on the rise since , when they averaged x. Lower Middle Market Close-up Valuations Decline Slightly But Remain Healthy According to data reported to GF Data from 52 transactions of $250.0m or less, the average valuation multiple in the lower MM in 1Q18 was 6.9x. This was down from 7.4x in Further, MM valuation multiples ranged from 5.7x for deals with a TEV of $10.0 $25.0m to 9.2x for deals with a TEV of $50.0 $100.0m

5 Leverage has remained elevated due in part to the competitive financing environment. Banks are continuing to loosen underwriting standards in order to put abundant capital to work in a low yield environment. As a result, highyield credit spreads remain low, and debt continues to increase as a component of the capital structure in order to boost returns. According to Pitchbook, in 2017 the median debt percentage for all US PE deals increased to 53% of enterprise value (compared to 59% for MM deals of $250.0m and less in 1Q18). Although sustainable in the current environment, should a recession occur or interest rates rise too quickly, companies purchased in highly leveraged deals will unlikely be able to service their debt. The prevalence of cheap debt financing has lowered the average equity contribution as a percentage of a deal s capital structure. According to the Spring 2018 GF Data Key Deal Terms report, this figure averaged 44% in 2017, which is down from the 2009 high of 53%. In response to the lower equity requirement in the capital structure, there has been a substantial increase in the utilization of rep and warranty insurance (7.7% of reported deals in 2016 compared to 42% in 2017). Deals utilizing rep and warranty insurance have closed at half a turn of leverage higher than deals without (7.7x versus 7.1x). In addition, indemnification cap levels, the maximum liability for a seller as a percentage of the purchase price, declined to 12% in 2017 from 16% in Outlook Key Message Remains Cautious Optimism 2018 is set to be another promising year of deal activity driven by small and MM business optimism, continued economic growth, and favorable views from PE industry participants. This is despite Intralinks and FACTSET data, which suggest an alternative view of the next six months and last three months, respectively. Intralinks Q2 Deal Flow Predictor forecasts M&A activity based on the number of M&A transactions that are being planned or have begun early stage due diligence. This suggests that although global M&A volume will increase between 6% and 10% in the first half of 2018, North American volume will decrease by 5%. This is in line with data from FACTSET that noted US M&A activity dropped 5.7% in terms of aggregate transaction value in the three months ending in April It is important to mention, however, that this is in comparison to a remarkably strong first half for 2017 as well as the overall M&A market, which is having its own challenges surrounding mega deals. Turning to factors that support 2018 PE and MM deal activity; according to NFIB s Small Business Economic Trends, the Index of Small Business Optimism remained robust but declined slightly in April to from near Reagan era highs of in February Given the removal of uncertainty from the passage of recent tax legislation and the current deregulatory environment, this index will likely continue to remain elevated. Nonetheless, remaining uncertainty on healthcare reform, the stalled pace of deregulation, and a smorgasbord of geopolitical issues could cap the upper bounds of this index for the time being. Additional metrics that highlight business optimism include data from the Q RSM US Middle Market Index (which surveyed 700 MM executives) and the SunTrust 2018 Business Pulse Survey (which surveyed 264 businesses with $2.0m $9.99m in revenues and 250 with revenues of $10.0m to $250.0m). According to the RSM data, its index is at an alltime high of (> 100 notes expansion) supported by the strong economy, a robust labor market, and changes to the aforementioned tax legislation. SunTrust echoed this by noting that 80% of its surveyed participants viewed their firms as strong, and 70% thought their business conditions would improve over the next 6 months. Capital spending (as measured by the NFIB) signaled further business owner optimism with 61% of respondents making capital expenditures (capex) in the last six months. The majority of capex was used to purchase new equipment and vehicles. PE firms were equally as optimistic as business owners about their 2018 outlook. In a recent Pitchbook survey 75%+ to 90%+ of PE firms surveyed were optimistic about their portfolios performance. In addition, they had a similar outlook for the performance of all industry sectors within their portfolios. Three other factors conducive to deal making and sustaining high valuations in the short to intermediate term concerned dry powder, the availability of debt, and taxes. First, a large amount of dry powder remains that needs to be invested, and PE firms have a glut of aged inventory they will need to liquidate in the near term. As mentioned earlier, global PE dry powder is sitting at just over $1.0 trillion. This concentration

6 is likely to spur continued mega fund raises, platform add on acquisitions, and continued investment into less traditional PE sectors such as technology. Second, investors will continue to seek debt financing while rates remain low and creditors are willing to lend. Third, lower corporate taxes will likely boost portfolio returns and corporate spending. These three factors and strong optimism on both the part of businesses and PE firms suggests a strong 2018 M&A environment. Additional trends that are likely to help sustain the current M&A environment include efficiencies gained from AI and the trend of aqui hiring, whereby companies are seeking to grow their workforce through acquisitions. The caveat to the above outlook, however, is that high valuation multiples are forcing industry participants to alter their strategies by focusing more on operational efficiencies, SBO s, and add on acquisitions. Further, these participants are doing so during a period of increasing recession risk. The US is in its longest ever economic recovery and concerns regarding inflation, the strength of the dollar, and economic policies are causing respected market participants such as KKR to state that the odds of a recession occurring within the next two years is 100% (compared to JP Morgan, which recently forecast the odds of a recession at >75% during the same time frame).

7 APPENDIX HISTORICAL CHARTS

8 About Strategic Advisors Strategic Advisors is a middle market investment banking firm that helps clients achieve financial and business goals by providing merger and acquisition advisory, corporate finance advisory and strategic consulting services. Along with many years of experience in advising middle market clients, our Managing Directors have experience investing in and managing portfolio companies. As a result, Strategic Advisors not only has expertise in advisory services but also firsthand knowledge of what stakeholders, investors, and lenders expect and desire. When considering a sale of your business, the acquisition of a business, or the restructuring or recapitalization of your balance sheet, the best pathway for achieving your expectations is a well run process that addresses all your business and personal goals. Strategic Advisors is accustomed to working with business owners to determine the best pathway to achieve their goals and objectives. Give us a call to discuss your possibilities. Strategic Advisors works with clients across diverse industries. Selected recent transactions include:

9 Author: Richard Wilusz, Investment Banking MBA Intern Sources: Pitchbook US PE Middle Market 2017 Annual, US PE Breakdown 2017 Annual, 2018 Crystal Ball Report, 2018 PE Outlook, Private Market Playbook; GF Data Key Deal Terms, Spring 2018; NFIB Small Business Economic Trends, February 2018; MERGERS&ACQUISITIONS, S&P Global Market Intelligence M&A Trends; Lincoln International Middle Market Index; Merrill Corporation M&A Deal Forecaster, Mergermarket FY 2017 Monthly M&A Insider; RSM (and U.S. Chamber of Commerce) US Middle Market Business Index; SunTrust 2018 Business Pulse Survey; FACTSET Flashwire US Monthly; Intralinks Deal Flow Predictor Important Information: Securities and investment advisory services are offered through BPU Investment Management, Inc. 301 Grant Street, Suite 3300 Pittsburgh PA Member FINRA/SIPC An SEC Registered Investment Advisor Please be advised that the accuracy and completeness of this information are not guaranteed. The opinions expressed are those of the author(s) and are not necessarily those of Strategic Advisors or BPU Investment Management, Inc. The material is distributed solely for informational purposes and is not a solicitation of an offer to buy any security or instrument or to participate in any trading strategy. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. For more information, please contact any of the professionals listed below or visit our website at: Name Title Phone Andy Bianco Managing Director ajbianco@strategicad.com Anthony Ventura Managing Director ajventura@strategicad.com Eric Wissinger Managing Director eawissinger@strategicad.com Richard Wilusz MBA Intern rwilusz@tepper.cmu.edu Viktoriia Koshelieva MBA Intern viktoriia@strategicad.com Marcia McCracken Office Manager mjm@strategicad.com

10 Bringing Efficiency to Inefficient Markets

M&A AND CORPORATE FINANCE OVERVIEW

Bringing Efficiency to an Inefficient Market 2017 Merger & Acquisition Corporate Finance Advisory Strategic Consulting 400 Southpointe Boulevard, Plaza I, Suite 440 Canonsburg, PA 15317 Tel. 724-743-5800

Bringing Efficiency to an Inefficient Market 2017 Merger & Acquisition Corporate Finance Advisory Strategic Consulting 400 Southpointe Boulevard, Plaza I, Suite 440 Canonsburg, PA 15317 Tel. 724-743-5800

M&A AND CORPORATE FINANCE OVERVIEW

Bringing Efficiency to an Inefficient Market 216 Merger & Acquisition Corporate Finance Advisory Strategic Consulting 4 Southpointe Boulevard, Plaza I, Suite 44 Canonsburg, PA 15317 Tel. 724-743-58 Fax

Bringing Efficiency to an Inefficient Market 216 Merger & Acquisition Corporate Finance Advisory Strategic Consulting 4 Southpointe Boulevard, Plaza I, Suite 44 Canonsburg, PA 15317 Tel. 724-743-58 Fax

Overall M&A Market Commentary

Overall M&A Market Commentary The U.S. economy continues to show strong momentum with 2Q18 GDP growth recorded at 4.2%. The Blue Chip consensus estimate for 3Q18 GDP growth of 3.3% and the Atlanta Fed

Overall M&A Market Commentary The U.S. economy continues to show strong momentum with 2Q18 GDP growth recorded at 4.2%. The Blue Chip consensus estimate for 3Q18 GDP growth of 3.3% and the Atlanta Fed

Overall M&A Market Commentary

Overall M&A Market Commentary At 115 months and counting, the current U.S. economic expansion is in record territory. After eight years of fed policy induced stock market tranquility, stock market volatility

Overall M&A Market Commentary At 115 months and counting, the current U.S. economic expansion is in record territory. After eight years of fed policy induced stock market tranquility, stock market volatility

Perspectives JAN Market Preview: Private Equity

Perspectives JAN 2018 2018 Market Preview: Private Equity RELATIVE OPPORTUNITY FUELING GROWTH Private equity investors in 2017 benefited from strong overall industry performance, with U.S. funds up 12%

Perspectives JAN 2018 2018 Market Preview: Private Equity RELATIVE OPPORTUNITY FUELING GROWTH Private equity investors in 2017 benefited from strong overall industry performance, with U.S. funds up 12%

Quarterly Asset Class Report Private Equity

Quarterly Asset Class Report canterburyconsulting.com Canterbury Consulting ( CCI ) is an SEC registered Investment Adviser. Information pertaining to CCI's advisory operations, services, and fees is set

Quarterly Asset Class Report canterburyconsulting.com Canterbury Consulting ( CCI ) is an SEC registered Investment Adviser. Information pertaining to CCI's advisory operations, services, and fees is set

Perspectives JAN Market Preview: Private Equity

Perspectives JAN 2019 2019 Market Preview: Private Equity POISED FOR ROBUST DEPLOYMENT Private equity investors in 2018 benefited from strong overall industry performance, with U.S. funds up 8.3% YTD.

Perspectives JAN 2019 2019 Market Preview: Private Equity POISED FOR ROBUST DEPLOYMENT Private equity investors in 2018 benefited from strong overall industry performance, with U.S. funds up 8.3% YTD.

Quarterly Asset Class Report Private Equity

Quarterly Asset Class Report canterburyconsulting.com Canterbury Consulting ( CCI ) is an SEC registered Investment Adviser. Information pertaining to CCI's advisory operations, services, and fees is set

Quarterly Asset Class Report canterburyconsulting.com Canterbury Consulting ( CCI ) is an SEC registered Investment Adviser. Information pertaining to CCI's advisory operations, services, and fees is set

The Strategic Alternatives Review

Bringing Efficiency to Inefficient Markets The Strategic Alternatives Review Create, Build and Realize Wealth. 400 400 Southpointe Southpointe Boulevard, Boulevard, Plaza Plaza I, I, Suite Suite 440 440

Bringing Efficiency to Inefficient Markets The Strategic Alternatives Review Create, Build and Realize Wealth. 400 400 Southpointe Southpointe Boulevard, Boulevard, Plaza Plaza I, I, Suite Suite 440 440

M&A, Private Equity and Capital Markets Update

M&A, Private Equity and Capital Markets Update April 211 DRAFT M&A Market Drivers DRAFT Macroeconomic Conditions Favorable For M&A GDP growth expected to continue The second half of 29 exhibited the first

M&A, Private Equity and Capital Markets Update April 211 DRAFT M&A Market Drivers DRAFT Macroeconomic Conditions Favorable For M&A GDP growth expected to continue The second half of 29 exhibited the first

Perspectives. Private Equity TEV / EBITDA* Multiples by Transaction Size. 6.3x. 4.0x $10M - $25M $25M - $50M $50M - $100M $100M - $250M

M A Y 2 0 1 7 Perspectives SPOTLIGHT ON PRIV ATE EQUITY V I E W S O N I N D U S T R Y T R E N D S A N D N E W S Private Equity in the Mid-Market Only when the tide goes out do you discover who s been swimming

M A Y 2 0 1 7 Perspectives SPOTLIGHT ON PRIV ATE EQUITY V I E W S O N I N D U S T R Y T R E N D S A N D N E W S Private Equity in the Mid-Market Only when the tide goes out do you discover who s been swimming

Create, Build and Realize Wealth.

Bringing Efficiency to Inefficient Markets Create, Build and Realize Wealth. Overview of the Divestiture Alternative 400 400 Southpointe Southpointe Boulevard, Boulevard, Plaza Plaza I, I, Suite Suite

Bringing Efficiency to Inefficient Markets Create, Build and Realize Wealth. Overview of the Divestiture Alternative 400 400 Southpointe Southpointe Boulevard, Boulevard, Plaza Plaza I, I, Suite Suite

Business Products and Services: McGladrey Quarterly Private Equity Deal

Business Products and Services: McGladrey Quarterly Private Equity Deal Insight Analysis Experience the power of being understood. SM Q3 213 Powered by McGladrey announces the Q3 213 Private Equity Deal

Business Products and Services: McGladrey Quarterly Private Equity Deal Insight Analysis Experience the power of being understood. SM Q3 213 Powered by McGladrey announces the Q3 213 Private Equity Deal

M&A AND CAPITAL MARKETS OUTLOOK SUMMER 2014

M&A AND CAPITAL MARKETS OUTLOOK SUMMER 2014 Inside this Issue: M&A Market Overview M&A Market Activity Middle Market Deal Valuations Private Equity vs Strategic Valuations Middle Market Leveraged Buy Out

M&A AND CAPITAL MARKETS OUTLOOK SUMMER 2014 Inside this Issue: M&A Market Overview M&A Market Activity Middle Market Deal Valuations Private Equity vs Strategic Valuations Middle Market Leveraged Buy Out

Private Equity. Panel Detail: Monday, May 2, :30 AM - 10:45 AM

Private Equity Panel Detail: Monday, May 2, 211 9:3 AM - 1:45 AM Speakers: Leon Black, Founding Partner, Apollo Management, LP David Bonderman, Founding Partner, TPG Capital Jonathan Nelson, CEO and Founder,

Private Equity Panel Detail: Monday, May 2, 211 9:3 AM - 1:45 AM Speakers: Leon Black, Founding Partner, Apollo Management, LP David Bonderman, Founding Partner, TPG Capital Jonathan Nelson, CEO and Founder,

2019 ANTARES COMPASS REPORT

2019 ANTARES COMPASS REPORT A unique, triangulated perspective on the middle market from our portfolio companies, private equity sponsors and loan investors. Resilient Optimism in U.S. Economy Drives Continued

2019 ANTARES COMPASS REPORT A unique, triangulated perspective on the middle market from our portfolio companies, private equity sponsors and loan investors. Resilient Optimism in U.S. Economy Drives Continued

Mergers & Acquisitions Update: The Middle Market Year End Preview

Mergers & Acquisitions Update: The Middle Market Year End Preview The Mufson Howe Hunter Middle Market M&A Update is designed to provide business owners, managers, private equity investors and M&A professionals

Mergers & Acquisitions Update: The Middle Market Year End Preview The Mufson Howe Hunter Middle Market M&A Update is designed to provide business owners, managers, private equity investors and M&A professionals

PitchBook s Private Equity Outlook: Assessing 2018 Themes and Beyond

W E B I N A R PitchBook s Private Equity Outlook: Assessing 2018 Themes and Beyond Dylan Cox, Senior Analyst Dylan.Cox@pitchbook.com Wylie Fernyhough, Analyst Wylie.Fernyhough@pitchbook.com Private Equity

W E B I N A R PitchBook s Private Equity Outlook: Assessing 2018 Themes and Beyond Dylan Cox, Senior Analyst Dylan.Cox@pitchbook.com Wylie Fernyhough, Analyst Wylie.Fernyhough@pitchbook.com Private Equity

The evolution of U.S. buyouts from a cottage investment business into a

U.S. Small Buyouts: Private Equity s Best Kept Little Secret FEBRUARY 2017 The evolution of U.S. buyouts from a cottage investment business into a multi-trillion-dollar industry has created what we believe

U.S. Small Buyouts: Private Equity s Best Kept Little Secret FEBRUARY 2017 The evolution of U.S. buyouts from a cottage investment business into a multi-trillion-dollar industry has created what we believe

news from the middle deal perspectives for middle market companies and their advisors

B O S T O N C H I C A G O L O S A N G E L E S P H I L A D E L P H I A news from the middle deal perspectives for middle market companies and their advisors Q1 212 MERGERS & ACQUISITIONS PRIVATE PLACEMENTS

B O S T O N C H I C A G O L O S A N G E L E S P H I L A D E L P H I A news from the middle deal perspectives for middle market companies and their advisors Q1 212 MERGERS & ACQUISITIONS PRIVATE PLACEMENTS

Increasing Shareholder Value Through Transaction Preparation

Increasing Shareholder Value Through Transaction Preparation PRESENTED BY: CHRIS DALTON, NATIONAL TRANSACTION SERVICES LEADER & KEN HIRSCH, MANAGING DIRECTOR, BKD CORPORATE FINANCE TO RECEIVE CPE CREDIT

Increasing Shareholder Value Through Transaction Preparation PRESENTED BY: CHRIS DALTON, NATIONAL TRANSACTION SERVICES LEADER & KEN HIRSCH, MANAGING DIRECTOR, BKD CORPORATE FINANCE TO RECEIVE CPE CREDIT

Leveraged Finance Q Leveraged Finance Market Resurgence Continues. In This Report Issuer-friendly conditions continue

Q3 2016 Leveraged Finance Market Resurgence Continues In This Report Issuer-friendly conditions continue Institutional market surges Leveraged Finance Rise of the unitranche Active high-yield market amid

Q3 2016 Leveraged Finance Market Resurgence Continues In This Report Issuer-friendly conditions continue Institutional market surges Leveraged Finance Rise of the unitranche Active high-yield market amid

Overall M&A Market Commentary

Overall M&A Market Commentary Middle market M&A activity continued its decline in 3Q17, recording another quarter of lower deal volume and lower dollar value. While on the surface this is disconcerting,

Overall M&A Market Commentary Middle market M&A activity continued its decline in 3Q17, recording another quarter of lower deal volume and lower dollar value. While on the surface this is disconcerting,

Uncorking M&A: The 2013 Vintage

DECEMBER 2012 Uncorking M&A: The 2013 Vintage Investors increasingly reward synergistic transactions Published by Corporate Finance Advisory & Mergers and Acquisitions For questions or further information,

DECEMBER 2012 Uncorking M&A: The 2013 Vintage Investors increasingly reward synergistic transactions Published by Corporate Finance Advisory & Mergers and Acquisitions For questions or further information,

THE U.S. MIDDLE MARKET

THE U.S. MIDDLE MARKET An alternative source of income, growth and diversification ALTERNATIVE THINKING FS Investment Solutions, LLC (member FINRA/SIPC) is an affiliated broker-dealer that serves as the

THE U.S. MIDDLE MARKET An alternative source of income, growth and diversification ALTERNATIVE THINKING FS Investment Solutions, LLC (member FINRA/SIPC) is an affiliated broker-dealer that serves as the

Private Equity Overview

Private Equity Overview June 10, 2010 State Universities Retirement System Rob Parkinson, Associate Agenda Asset Class Overview Market Update SURS Private Equity Portfolio Asset Class Overview Benefits

Private Equity Overview June 10, 2010 State Universities Retirement System Rob Parkinson, Associate Agenda Asset Class Overview Market Update SURS Private Equity Portfolio Asset Class Overview Benefits

Presentation Global private equity trends

Presentation Global private equity trends Alex Scott Partner Pantheon Ventures Global Private Equity Trends Alex Scott July 2018 Hitting the headlines IPOS ARE DWINDLING, SO IS THE NUMBER OF PUBLIC COMPANIES

Presentation Global private equity trends Alex Scott Partner Pantheon Ventures Global Private Equity Trends Alex Scott July 2018 Hitting the headlines IPOS ARE DWINDLING, SO IS THE NUMBER OF PUBLIC COMPANIES

PitchBook. Bet ter Data. Bet ter Decisions. The Private Equity. Company Inventory. Report 2012 Edition

PitchBook The Private Equity Company Inventory Report 2012 Edition TABLE OF CONTENTS Introduction... ii Overview...1 Company Inventory by Age Bucket...2 2009-2012... 2 2005-2008... 3 2000-2004... 3 Company

PitchBook The Private Equity Company Inventory Report 2012 Edition TABLE OF CONTENTS Introduction... ii Overview...1 Company Inventory by Age Bucket...2 2009-2012... 2 2005-2008... 3 2000-2004... 3 Company

Presentation to KCAP Investors

Presentation to KCAP Investors January 2, 2019 BCP Important Information Forward-Looking Statements Statements contained in this Presentation (including those relating to the proposed transaction, the

Presentation to KCAP Investors January 2, 2019 BCP Important Information Forward-Looking Statements Statements contained in this Presentation (including those relating to the proposed transaction, the

Middle-Market M&A Review

A Quarterly Corporate Investment Banking Division Publication 1st Quarter 214 Middle-Market M&A Overview and Trends In this Issue Despite a soft first quarter of 214, barring any major fiscal or systematic

A Quarterly Corporate Investment Banking Division Publication 1st Quarter 214 Middle-Market M&A Overview and Trends In this Issue Despite a soft first quarter of 214, barring any major fiscal or systematic

M&A and Financing Trends in the Car Wash Industry Today. A presentation by Commercial Plus Group

M&A and Financing Trends in the Car Wash Industry Today A presentation by Commercial Plus Group Agenda About Commercial Plus Group 2017 Scorecard Current Car Wash M&A Environment Sale Considerations Types

M&A and Financing Trends in the Car Wash Industry Today A presentation by Commercial Plus Group Agenda About Commercial Plus Group 2017 Scorecard Current Car Wash M&A Environment Sale Considerations Types

Corporate Capital Trust, Inc. Quarterly Earnings Presentation. Quarter Ended December 31, 2017

Corporate Capital Trust, Inc. Quarterly Earnings Presentation Quarter Ended December 31, 2017 CCT Overview CCT The Basics CCT is a business development company focused on making originated, senior secured

Corporate Capital Trust, Inc. Quarterly Earnings Presentation Quarter Ended December 31, 2017 CCT Overview CCT The Basics CCT is a business development company focused on making originated, senior secured

LEADING WITH OPTIMISM IN TIMES OF UNCERTAINTY How companies, sponsors and investors view the middle market landscape post-election.

ANTARES COMPASS: LEADING WITH OPTIMISM IN TIMES OF UNCERTAINTY How companies, sponsors and investors view the middle market landscape post-election. Optimism is the prevailing sentiment within the middle

ANTARES COMPASS: LEADING WITH OPTIMISM IN TIMES OF UNCERTAINTY How companies, sponsors and investors view the middle market landscape post-election. Optimism is the prevailing sentiment within the middle

WHITE PAPER VENUE MARKET SPOTLIGHT. M&A Financing Edition. DFINsolutions.com

WHITE PAPER VENUE MARKET SPOTLIGHT M&A Financing 2018 Edition DFINsolutions.com FOREWORD...3 SURVEY...4 Methodology Mergermarket interviewed 25 global dealmakers from across the corporate, private equity

WHITE PAPER VENUE MARKET SPOTLIGHT M&A Financing 2018 Edition DFINsolutions.com FOREWORD...3 SURVEY...4 Methodology Mergermarket interviewed 25 global dealmakers from across the corporate, private equity

Materials for Discussion May 26, 2011 Eliot Kerlin, Bud Moore

Private Equity: Current Environment, Trends and Expectations Private Equity: Current Environment, Trends and Expectations Materials for Discussion May 26, 2011 Eliot Kerlin, Bud Moore AGENDA I. Current

Private Equity: Current Environment, Trends and Expectations Private Equity: Current Environment, Trends and Expectations Materials for Discussion May 26, 2011 Eliot Kerlin, Bud Moore AGENDA I. Current

SOFTWARE MIDDLE-MARKET UPDATE 3Q2018

SOFTWARE MIDDLE-MARKET UPDATE 3Q218 3Q 218 OVERALL MARKET UPDATE AND ECONOMIC REVIEW Middle-market M&A activity declined for the third consecutive quarter, continuing the same trend experienced over the

SOFTWARE MIDDLE-MARKET UPDATE 3Q218 3Q 218 OVERALL MARKET UPDATE AND ECONOMIC REVIEW Middle-market M&A activity declined for the third consecutive quarter, continuing the same trend experienced over the

Breaking Down PE s Push into the Lower Middle Market

Breaking Down PE s Push into the Lower Middle Market 1Q 219 A Review of Key Dynamics in the Lower Middle Market Data provided by: As alternative investments in general have grown in allure throughout the

Breaking Down PE s Push into the Lower Middle Market 1Q 219 A Review of Key Dynamics in the Lower Middle Market Data provided by: As alternative investments in general have grown in allure throughout the

Asset Allocation Model March Update

The month of February was marked by a sell-off in global equity markets and a sudden increase in market volatility with the CBOE Volatility Index reaching its highest level since August 2015. The rout

The month of February was marked by a sell-off in global equity markets and a sudden increase in market volatility with the CBOE Volatility Index reaching its highest level since August 2015. The rout

M&A Market Snapshot Q4 2015

Market Report M&A Market Snapshot Q4 2015 New York Chicago Boston Hartford Orlando Princeton www.mpival.com Table of Contents Total U.S. Market Activity Overview... 3 Transaction Multiples... 4 Private

Market Report M&A Market Snapshot Q4 2015 New York Chicago Boston Hartford Orlando Princeton www.mpival.com Table of Contents Total U.S. Market Activity Overview... 3 Transaction Multiples... 4 Private

SMALL BUSINESS INVESTOR ALLIANCE Lower Middle Market Investment Insights

Small Business Investor Alliance Lower Middle Market Investment Insights Volume 1, Issue 1 1 SMALL BUSINESS INVESTOR ALLIANCE Lower Middle Market Investment Insights 2H 2013 Volume 1, Issue 1 March 17,

Small Business Investor Alliance Lower Middle Market Investment Insights Volume 1, Issue 1 1 SMALL BUSINESS INVESTOR ALLIANCE Lower Middle Market Investment Insights 2H 2013 Volume 1, Issue 1 March 17,

Ownership Succession / Transition Strategies

ship Succession / Transition Strategies Maner Costerian Solutions Conference November 2017 Tom Ziemba, PhD BDO USA, LLP tziemba@bdo.com BDO USA, LLP, a Delaware limited liability partnership, is the U.S.

ship Succession / Transition Strategies Maner Costerian Solutions Conference November 2017 Tom Ziemba, PhD BDO USA, LLP tziemba@bdo.com BDO USA, LLP, a Delaware limited liability partnership, is the U.S.

JOB SITUATION INCOME. 3 rd Quarter 2015 PITTSBURGH

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

3 rd Quarter PITTSBURGH JOB SITUATION The Pittsburgh market area will continue to experience slow and steady economic growth through the remainder of and into next year. The market area s employment is

Alternative Investments in a Changing World

NORTHERN TRUST 2010 PROGRAM SOLUTIONS CONFERENCE Investment Solutions in an Uncertain World: WHAT S NEXT? Alternative Investments in a Changing World Andrew C Smith, CFA, Chief Investment Officer, NTGA

NORTHERN TRUST 2010 PROGRAM SOLUTIONS CONFERENCE Investment Solutions in an Uncertain World: WHAT S NEXT? Alternative Investments in a Changing World Andrew C Smith, CFA, Chief Investment Officer, NTGA

Merger Tracker. December 2018 Investment Banking. Speed and Certainty Become Powerful Differentiators. In This Issue

December 2018 Investment Banking Speed and Certainty Become Powerful Differentiators In This Issue Merger Tracker Tactics used by buyers to accelerate dealmaking processes Sellers prepare to run fast Recent

December 2018 Investment Banking Speed and Certainty Become Powerful Differentiators In This Issue Merger Tracker Tactics used by buyers to accelerate dealmaking processes Sellers prepare to run fast Recent

November Deal Metrics Survey. A survey of Australian VC and PE deal activity in FY2012. In association with

November Deal Metrics Survey A survey of Australian VC and PE deal activity in FY In association with AVCAL Deal Metrics Report Message from the Chief Executive Welcome to the AVCAL and Pacific Strategy

November Deal Metrics Survey A survey of Australian VC and PE deal activity in FY In association with AVCAL Deal Metrics Report Message from the Chief Executive Welcome to the AVCAL and Pacific Strategy

Corporate Capital Trust, Inc. Quarterly Earnings Presentation. Quarter Ended March 31, 2018

Corporate Capital Trust, Inc. Quarterly Earnings Presentation Quarter Ended March 31, 2018 CCT Overview CCT The Basics CCT is a business development company focused on making originated, senior secured

Corporate Capital Trust, Inc. Quarterly Earnings Presentation Quarter Ended March 31, 2018 CCT Overview CCT The Basics CCT is a business development company focused on making originated, senior secured

Volume Report H1 2017

Volume Report H1 2017 First in the Secondary Market. Setter Capital Volume Report 1 Highlights The Setter Capital Volume Report analyzes global secondary market activity in H1 2017 and covers the following

Volume Report H1 2017 First in the Secondary Market. Setter Capital Volume Report 1 Highlights The Setter Capital Volume Report analyzes global secondary market activity in H1 2017 and covers the following

Piper Jaffray Middle Market Mergers & Acquisitions M&A Monitor: Analyzing M&A Activity February 8, 2006

M&A Monitor: Analyzing M&A Activity February 8, 2006 Sections: Feature Article Feature Transaction Domestic M&A Transactions LTM Transaction Multiples Public Company Premiums Deal Financing Buyout Fund

M&A Monitor: Analyzing M&A Activity February 8, 2006 Sections: Feature Article Feature Transaction Domestic M&A Transactions LTM Transaction Multiples Public Company Premiums Deal Financing Buyout Fund

MMI LINCOLN LINCOLN MIDDLE MARKET INDEX INSIDE THIS ISSUE

INSIDE THIS ISSUE Quarterly Overview Private Middle Market Company Value Results Performance by Industry: Sector Breakdown Examining the LMMI: EBITDA Multiples vs. Earnings Summary of the LMMI Methodology:

INSIDE THIS ISSUE Quarterly Overview Private Middle Market Company Value Results Performance by Industry: Sector Breakdown Examining the LMMI: EBITDA Multiples vs. Earnings Summary of the LMMI Methodology:

DEBT CAPITAL MARKETS EXECUTIVE SUMMARY MIDDLE MARKET

MARKET INSIGHTS 2Q 2018 DEBT CAPITAL MARKETS EXECUTIVE SUMMARY Middle market clients have a unique borrowing opportunity, with banks competing to originate new loans for clients. In the leveraged loan

MARKET INSIGHTS 2Q 2018 DEBT CAPITAL MARKETS EXECUTIVE SUMMARY Middle market clients have a unique borrowing opportunity, with banks competing to originate new loans for clients. In the leveraged loan

Industry Consolidations Financing Alternatives for Acquisition-Driven Companies

Financing Alternatives for Acquisition-Driven Companies Charles A Sheffield President, Sheffield Capital Advisors This article focuses on the trends and financing opportunities for clients who are pursuing

Financing Alternatives for Acquisition-Driven Companies Charles A Sheffield President, Sheffield Capital Advisors This article focuses on the trends and financing opportunities for clients who are pursuing

Secondary Market Update Q All securities transacted through Sixpoint Partners, member FINRA/SIPC

Secondary Market Update Q3 2014 All securities transacted through Sixpoint Partners, member FINRA/SIPC Secondary Market Environment 2 Executive Summary 2014 is shaping up to be a banner year for the private

Secondary Market Update Q3 2014 All securities transacted through Sixpoint Partners, member FINRA/SIPC Secondary Market Environment 2 Executive Summary 2014 is shaping up to be a banner year for the private

Canadian M&A Insights. W i n t e r

Canadian M&A Insights W i n t e r 2 0 1 9 Implied Enterprise Value (CA$ in millions) Canadian M&A Insights Winter 2019 Canadian M&A Update Canadian M&A Transactions (CA$ in millions) In 2018, Canadian

Canadian M&A Insights W i n t e r 2 0 1 9 Implied Enterprise Value (CA$ in millions) Canadian M&A Insights Winter 2019 Canadian M&A Update Canadian M&A Transactions (CA$ in millions) In 2018, Canadian

The PitchBook Platform. Credits & Contact. 3 Overview. Introduction 4-6. Spotlight: Target Company Characteristics

2017 3Q M&A Report Credits & Contact PitchBook Data, Inc. JOHN GABBERT Founder, CEO ADLEY BOWDEN Vice President, Contents Market Development & Analysis Content DYL AN E. COX Analyst II BRYAN HANSON Data

2017 3Q M&A Report Credits & Contact PitchBook Data, Inc. JOHN GABBERT Founder, CEO ADLEY BOWDEN Vice President, Contents Market Development & Analysis Content DYL AN E. COX Analyst II BRYAN HANSON Data

The Business Environment Facing Emerging Companies Today

A Report Presented By: Foley & Lardner LLP December 13, 2007 Page 2 EXECUTIVE SUMMARY Emerging company executives, investors and advisors have expressed greater uncertainty in the current market, however

A Report Presented By: Foley & Lardner LLP December 13, 2007 Page 2 EXECUTIVE SUMMARY Emerging company executives, investors and advisors have expressed greater uncertainty in the current market, however

State of the Middle Market M&A Private Equity Financing

State of the Middle Market M&A Private Equity Financing Webcast: May 10, 2011 DEBT ADVISORY GROUP The Capital Markets Desk for the Middle Market State of the Middle Market Agenda Agenda Update on Market

State of the Middle Market M&A Private Equity Financing Webcast: May 10, 2011 DEBT ADVISORY GROUP The Capital Markets Desk for the Middle Market State of the Middle Market Agenda Agenda Update on Market

Alphabet Inc. GOOGL - NASDAQ Neutral -1

COMPANY UPDATE / ESTIMATE CHANGE / TARGET CHANGE Key Metrics GOOGL - NASDAQ - as of 10/30/17 $1,033.13 Price Target $1,100 52-Week Range $743.59 - $1,063.62 Diluted Shares Outstanding (mil) 703.5 Market

COMPANY UPDATE / ESTIMATE CHANGE / TARGET CHANGE Key Metrics GOOGL - NASDAQ - as of 10/30/17 $1,033.13 Price Target $1,100 52-Week Range $743.59 - $1,063.62 Diluted Shares Outstanding (mil) 703.5 Market

Outsourced Investment Management

Outsourced Investment Management Quarterly Commentary Second Quarter 2017 The first half of 2017 was a goldilocks environment for investments. United States GDP growth was steady in the first quarter,

Outsourced Investment Management Quarterly Commentary Second Quarter 2017 The first half of 2017 was a goldilocks environment for investments. United States GDP growth was steady in the first quarter,

Note Important Disclosures on Pages 6-7 Note Analyst Certification on Page 6

COMPANY UPDATE / ESTIMATE CHANGE Key Metrics GOOGL - NASDAQ - as 4/23/18 $1,073.81 Price Target $1,100 52-Week Range $866.11 - $1,198.00 Diluted Shares Outstanding (mil) 703.5 Market Cap. ($mil) 1-Mo.

COMPANY UPDATE / ESTIMATE CHANGE Key Metrics GOOGL - NASDAQ - as 4/23/18 $1,073.81 Price Target $1,100 52-Week Range $866.11 - $1,198.00 Diluted Shares Outstanding (mil) 703.5 Market Cap. ($mil) 1-Mo.

MPI. M&A Market Snapshot Q Valuation Opinions & Transaction Advisory.

Valuation Opinions & Transaction Advisory M&A Market Snapshot Q2 2014 www.mpival.com Contents 02 Total U.S. Market Activity Increasing volume and ripe deal conditions 03 Capital Market Performance Growth

Valuation Opinions & Transaction Advisory M&A Market Snapshot Q2 2014 www.mpival.com Contents 02 Total U.S. Market Activity Increasing volume and ripe deal conditions 03 Capital Market Performance Growth

M&A AND CAPITAL MARKETS OUTLOOK SPRING 2015

M&A AND CAPITAL MARKETS OUTLOOK SPRING 2015 Inside this Issue: M&A Market Overview M&A Market Activity Middle Market Deal Valuations Private Equity vs Strategic Valuations Middle Market Leveraged Buy Out

M&A AND CAPITAL MARKETS OUTLOOK SPRING 2015 Inside this Issue: M&A Market Overview M&A Market Activity Middle Market Deal Valuations Private Equity vs Strategic Valuations Middle Market Leveraged Buy Out

The infrastructure equity cycle

UBS Asset Management The infrastructure equity cycle Infrastructure white paper series Part 3 Institutional investor interest in the infrastructure sector is at record highs. This paper takes a closer

UBS Asset Management The infrastructure equity cycle Infrastructure white paper series Part 3 Institutional investor interest in the infrastructure sector is at record highs. This paper takes a closer

Evaluating Debt Structures and Interest Rate Risk. July 17, 2018

Evaluating Debt Structures and Interest Rate Risk July 17, 2018 Table of Contents Section Page I. CCCA Overview 3 II. Capital Markets Update 7 III. Debt Portfolio Considerations 16 IV. Summary & Conclusions

Evaluating Debt Structures and Interest Rate Risk July 17, 2018 Table of Contents Section Page I. CCCA Overview 3 II. Capital Markets Update 7 III. Debt Portfolio Considerations 16 IV. Summary & Conclusions

AND COMPANY INVENTORY

AND COMPANY INVENTORY 2015 Annual IN PAST TWO YEARS, PE-BACKED EXIT VALUE TOTALS $1.07T PAG E 4» CORPORATE ACQUISITIONS SURGE IN TOTAL VALUE, HITTING $360B IN 2015 PAG E 7» PE-BACKED IPO VALUATION SLIDES

AND COMPANY INVENTORY 2015 Annual IN PAST TWO YEARS, PE-BACKED EXIT VALUE TOTALS $1.07T PAG E 4» CORPORATE ACQUISITIONS SURGE IN TOTAL VALUE, HITTING $360B IN 2015 PAG E 7» PE-BACKED IPO VALUATION SLIDES

M&A and Private Equity Update

M&A and Private Equity Update For Further Information Contact: Martin G. Burkett Ph: 305.982.5578 Email: martin.burkett@akerman.com Carl D. Roston Ph: 305.982.5628 Email: carl.roston@akerman.com Shannon

M&A and Private Equity Update For Further Information Contact: Martin G. Burkett Ph: 305.982.5578 Email: martin.burkett@akerman.com Carl D. Roston Ph: 305.982.5628 Email: carl.roston@akerman.com Shannon

The Northern Trust Experience

The Northern Trust Experience ACCESS. EXPERTISE. SERVICE. Are Alternatives Still Alternative? November 4, 2010 Robert P. Morgan SVP, Director of Private Equity 2010 Northern Trust Corporation northerntrust.com

The Northern Trust Experience ACCESS. EXPERTISE. SERVICE. Are Alternatives Still Alternative? November 4, 2010 Robert P. Morgan SVP, Director of Private Equity 2010 Northern Trust Corporation northerntrust.com

CFO OUTLOOK 2018 MIDDLE MARKET

CFO OUTLOOK 2018 MIDDLE MARKET TABLE OF CONTENTS Summary and Key Findings...1 Growth in the Current Environment...2 Emerging Trends...6 An Increasingly Evolving Role...10 SUMMARY AND KEY FINDINGS We are

CFO OUTLOOK 2018 MIDDLE MARKET TABLE OF CONTENTS Summary and Key Findings...1 Growth in the Current Environment...2 Emerging Trends...6 An Increasingly Evolving Role...10 SUMMARY AND KEY FINDINGS We are

PRIVATE CAPITAL: RECORD- SETTING PACE IN 2017 At the end of September, Preqin

Q4 217 Fundraising Update PRIVATE CAPITAL: RECORD- SETTING PACE IN 217 At the end of September, Preqin asked whether a dip in quarterly fundraising might represent a slowdown in overall activity, or simply

Q4 217 Fundraising Update PRIVATE CAPITAL: RECORD- SETTING PACE IN 217 At the end of September, Preqin asked whether a dip in quarterly fundraising might represent a slowdown in overall activity, or simply

Madison Capital Funding Market Overview

Communicate. Commit. Deliver. Third Quarter 2014 Table of Contents Loan Volume 2 CLO Issuance, Investors 3 Madison Capital Funding Market Overview Yields, Debt and Equity Multiples 4 Madison Capital Overview

Communicate. Commit. Deliver. Third Quarter 2014 Table of Contents Loan Volume 2 CLO Issuance, Investors 3 Madison Capital Funding Market Overview Yields, Debt and Equity Multiples 4 Madison Capital Overview

Creating value for corporate America

Creating value for corporate America The Rise of M&A is likely to continue..in the U.S., non- financial companies in the S&P s 500 sit on a record of USD 1.4 trillion cash. Meanwhile borrowing is cheap.

Creating value for corporate America The Rise of M&A is likely to continue..in the U.S., non- financial companies in the S&P s 500 sit on a record of USD 1.4 trillion cash. Meanwhile borrowing is cheap.

STOCK BUYBACKS HIGHLIGHTS DRIVING THE STOCK MARKET THE MECHANICS OF A BUYBACK PROGRAM WHERE DO BUYBACKS COME FROM?

OCTOBER 2014 STOCK BUYBACKS DAVID KREIN Head of Research NASDAQ OMX Global Indexes CAMERON LILJA Sr. Product Developer NASDAQ OMX Global Indexes HIGHLIGHTS Among the biggest buyers in today s stock market

OCTOBER 2014 STOCK BUYBACKS DAVID KREIN Head of Research NASDAQ OMX Global Indexes CAMERON LILJA Sr. Product Developer NASDAQ OMX Global Indexes HIGHLIGHTS Among the biggest buyers in today s stock market

Private Enterprise. Behind the curtain: What mid-sized private companies need to know about what drives Private-Equity investments

Behind the curtain: What mid-sized private companies need to know about what drives Private-Equity investments Deloitte s Commitment to Private Enterprise Deloitte has a large group of professionals committed

Behind the curtain: What mid-sized private companies need to know about what drives Private-Equity investments Deloitte s Commitment to Private Enterprise Deloitte has a large group of professionals committed

9/1/ /1/1977 9/1/ /1/ /1/1963

CAPITAL IDEAS It Pays to Collect Dividends Executive Summary Dividend income makes up a significant portion of total return over long time periods. 18.0% 16.0% 14.0% 12.0% 10.0% Figure 1: Dividend Yield

CAPITAL IDEAS It Pays to Collect Dividends Executive Summary Dividend income makes up a significant portion of total return over long time periods. 18.0% 16.0% 14.0% 12.0% 10.0% Figure 1: Dividend Yield

Industry Consolidations Recognizing Banking Opportunities in Acquisition- Driven Companies

Industry Consolidations Recognizing Banking Opportunities in Acquisition- Driven Companies Business strategy is a key driver of client needs and customized banking solutions. There are many tools and techniques

Industry Consolidations Recognizing Banking Opportunities in Acquisition- Driven Companies Business strategy is a key driver of client needs and customized banking solutions. There are many tools and techniques

Madison Capital Funding Market Overview

Communicate. Commit. Deliver. Third Quarter 2013 Table of Contents Loan Volume 2 Yields and Debt and Equity Multiples 3 Madison Capital Funding Market Overview Investors, CLO Issuance and 4 Default Rate

Communicate. Commit. Deliver. Third Quarter 2013 Table of Contents Loan Volume 2 Yields and Debt and Equity Multiples 3 Madison Capital Funding Market Overview Investors, CLO Issuance and 4 Default Rate

TRANSACTION ADVISORY SERVICES. Customized, value-added solutions every step of the way

TRANSACTION ADVISORY SERVICES Customized, value-added solutions every step of the way TRANSACTION ADVISORY SERVICES 3 TABLE OF CONTENTS THE REHMANN EXPERIENCE TRANSACTION ADVISORY SERVICE OFFERINGS YOUR

TRANSACTION ADVISORY SERVICES Customized, value-added solutions every step of the way TRANSACTION ADVISORY SERVICES 3 TABLE OF CONTENTS THE REHMANN EXPERIENCE TRANSACTION ADVISORY SERVICE OFFERINGS YOUR

How the Global Credit Meltdown Has Changed the World of Private Equity For The Better

How the Global Credit Meltdown Has Changed the World of Private Equity For The Better David M. Rubenstein Co-Founder and Managing Director February 4, 2009 1 At The Peak! 2007 commitments to new funds

How the Global Credit Meltdown Has Changed the World of Private Equity For The Better David M. Rubenstein Co-Founder and Managing Director February 4, 2009 1 At The Peak! 2007 commitments to new funds

U.S. Commercial Real Estate Valuation Trends

The NAIC s Capital Markets Bureau monitors developments in the capital markets globally and analyzes their potential impact on the investment portfolios of U.S. insurance companies. A list of archived

The NAIC s Capital Markets Bureau monitors developments in the capital markets globally and analyzes their potential impact on the investment portfolios of U.S. insurance companies. A list of archived

BMO Sponsor Finance Q Economic Review and Forward Outlook

BMO Sponsor Finance Q3 2017 Transaction Trends This issue of Transaction Trends includes data and commentary on relevant and interesting developments affecting middle-market leveraged finance and private

BMO Sponsor Finance Q3 2017 Transaction Trends This issue of Transaction Trends includes data and commentary on relevant and interesting developments affecting middle-market leveraged finance and private

DEBT CAPITAL MARKETS EXECUTIVE SUMMARY MIDDLE MARKET

MARKET INSIGHTS 4Q 2017 DEBT CAPITAL MARKETS EXECUTIVE SUMMARY In the middle market, bank loan capital is available at attractive levels. For leveraged middle market companies, non-bank lenders are driving

MARKET INSIGHTS 4Q 2017 DEBT CAPITAL MARKETS EXECUTIVE SUMMARY In the middle market, bank loan capital is available at attractive levels. For leveraged middle market companies, non-bank lenders are driving

M&A Deal Report. May Partner and Head of Corporate Sparke Helmore Lawyers tel

M&A Deal Report May 2015 Contact: Nick Humphrey Partner and Head of Corporate Sparke Helmore Lawyers tel + 61 2 9260 2747 nick.humphrey@sparke.com.au 1 Global activity in 2014 Australian activity in 2014

M&A Deal Report May 2015 Contact: Nick Humphrey Partner and Head of Corporate Sparke Helmore Lawyers tel + 61 2 9260 2747 nick.humphrey@sparke.com.au 1 Global activity in 2014 Australian activity in 2014

A PATH FORWARD. Insights from the 2010 RIA Benchmarking Study from Charles Schwab

A PATH FORWARD Insights from the 2010 RIA Benchmarking Study from Charles Schwab The year 2009 marked a turning point for registered investment advisors. As an era of rapid growth came to an end, advisors

A PATH FORWARD Insights from the 2010 RIA Benchmarking Study from Charles Schwab The year 2009 marked a turning point for registered investment advisors. As an era of rapid growth came to an end, advisors

Fourth Quarter Market Outlook. Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Fourth Quarter 2018 Market Outlook Jason Bulinski, CFA Donald A. Powell, CFA Joseph Styrna, CFA Economic Outlook Growth: Strong 2018, But Expecting Slowdown in 2019 Growth & Jobs 2018 2017 2016 2015 2014

Venture Capital 4% Strategy. Mega/Large Buyout 29% Highlights from the 2016 GP Dashboard include:

GP Dashboard We are pleased to present Hamilton Lane s GP Dashboard, which captures the opinions and expectations of general partners from around the world and offers insight into where the GP community

GP Dashboard We are pleased to present Hamilton Lane s GP Dashboard, which captures the opinions and expectations of general partners from around the world and offers insight into where the GP community

Alphabet Inc. GOOGL - NASDAQ Neutral -1

COMPANY UPDATE / TARGET CHANGE ESTIMATE CHANGE Key Metrics GOOGL - NASDAQ - as of 5/1/17 $932.82 Price Target $1,000.00 52-Week Range $672.66 - $935.82 Diluted Shares Outstanding (mil) 702.0 Market Cap.

COMPANY UPDATE / TARGET CHANGE ESTIMATE CHANGE Key Metrics GOOGL - NASDAQ - as of 5/1/17 $932.82 Price Target $1,000.00 52-Week Range $672.66 - $935.82 Diluted Shares Outstanding (mil) 702.0 Market Cap.

M&A Financing. Presentation to: FEI NE WI Chapter. April 19, 2016

M&A Financing Presentation to: FEI NE WI Chapter April 19, 2016 Agenda Characteristics of Attractive M&A Targets Key Financial and Tax Considerations Typical M&A Financing Participants Typical Buyout Capital

M&A Financing Presentation to: FEI NE WI Chapter April 19, 2016 Agenda Characteristics of Attractive M&A Targets Key Financial and Tax Considerations Typical M&A Financing Participants Typical Buyout Capital

Middle-Market M&A Review

A Quarterly Corporate Investment Banking Division Publication Middle-Market M&A Overview and Trends Robust transaction volumes in the first nine months confirm predictions that 2014 will be a big year

A Quarterly Corporate Investment Banking Division Publication Middle-Market M&A Overview and Trends Robust transaction volumes in the first nine months confirm predictions that 2014 will be a big year

Global PE & VC Fund Performance Report. Data through 2Q 2017

Global PE & VC Fund Performance Report Data through 2Q 2017 Contents Key Takeaways 2 IRR by Fund Type 3 PE Fund Performance 4 VC Fund Performance 6 Spotlight: Going with the Flows 8 Credits & Contact PitchBook

Global PE & VC Fund Performance Report Data through 2Q 2017 Contents Key Takeaways 2 IRR by Fund Type 3 PE Fund Performance 4 VC Fund Performance 6 Spotlight: Going with the Flows 8 Credits & Contact PitchBook

M&A AND CAPITAL MARKETS OUTLOOK SUMMER 2016

M&A AND CAPITAL MARKETS OUTLOOK SUMMER 2016 Inside this Issue: M&A Market Overview M&A Market Activity Middle Market Deal Valuations Private Equity vs Strategic Valuations Middle Market Leveraged Buy Out

M&A AND CAPITAL MARKETS OUTLOOK SUMMER 2016 Inside this Issue: M&A Market Overview M&A Market Activity Middle Market Deal Valuations Private Equity vs Strategic Valuations Middle Market Leveraged Buy Out

SEPTEMBER 2017 Private Equity Outlook

SEPTEMBER 2017 Table of contents VERU.S.INVESTMENTS.COM SEATTLE 206 622 3700 LOS ANGELES 310 297 1777 SAN FRANCISCO 415 362 3484 Executive summary 3 Market update: Other 19 Fund finance: Subscription credit

SEPTEMBER 2017 Table of contents VERU.S.INVESTMENTS.COM SEATTLE 206 622 3700 LOS ANGELES 310 297 1777 SAN FRANCISCO 415 362 3484 Executive summary 3 Market update: Other 19 Fund finance: Subscription credit

ASSUMPTION vs REALITY AT BARINGS, WE BELIEVE THAT IDENTIFYING HIGH-QUALITY PRIVATE EQUITY MANAGERS

January 2019 DON T JUDGE A PRIVATE EQUITY FUND BY ITS NUMBER ASSUMPTION vs REALITY AT BARINGS, WE BELIEVE THAT IDENTIFYING HIGH-QUALITY PRIVATE EQUITY MANAGERS EARLY IN THEIR FIRM LIFECYCLE CAN DELIVER

January 2019 DON T JUDGE A PRIVATE EQUITY FUND BY ITS NUMBER ASSUMPTION vs REALITY AT BARINGS, WE BELIEVE THAT IDENTIFYING HIGH-QUALITY PRIVATE EQUITY MANAGERS EARLY IN THEIR FIRM LIFECYCLE CAN DELIVER

ICI RESEARCH PERSPECTIVE

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG APRIL 2018 VOL. 24, NO. 3 WHAT S INSIDE 2 Mutual Fund Expense Ratios Have Declined Substantially over

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG APRIL 2018 VOL. 24, NO. 3 WHAT S INSIDE 2 Mutual Fund Expense Ratios Have Declined Substantially over

Volume Report FY 2017

Volume Report FY 2017 Setter Capital Volume Report 1 Highlights The Setter Capital Volume Report analyzes global secondary market activity in FY 2017 and covers the following topics: Total Volume of Secondary

Volume Report FY 2017 Setter Capital Volume Report 1 Highlights The Setter Capital Volume Report analyzes global secondary market activity in FY 2017 and covers the following topics: Total Volume of Secondary

Manufacturing Barometer

Special topic: Year 2016 major challenges Manufacturing Barometer Business outlook report January 2016 Contents 1 Quarterly highlights 1.1 Key indicators for the business outlook 7 1.2 PwC global manufacturing

Special topic: Year 2016 major challenges Manufacturing Barometer Business outlook report January 2016 Contents 1 Quarterly highlights 1.1 Key indicators for the business outlook 7 1.2 PwC global manufacturing

Midwest M&A Quarterly Update. First Quarter 2016

Bridgepoint Merchant Banking is a division of Bridgepoint Holdings, LLC. Securities offered through an unaffiliated entity, M&A Securities Group, Inc., member FINRA/SIPC. This entity is not affiliated

Bridgepoint Merchant Banking is a division of Bridgepoint Holdings, LLC. Securities offered through an unaffiliated entity, M&A Securities Group, Inc., member FINRA/SIPC. This entity is not affiliated

European Private Equity Outlook Frankfurt am Main, February 2015

European Private Equity Outlook 2015 Frankfurt am Main, February 2015 Preliminary remarks Our sixth European Private Equity ("PE") Outlook reveals how experts view the market and its development in 2015

European Private Equity Outlook 2015 Frankfurt am Main, February 2015 Preliminary remarks Our sixth European Private Equity ("PE") Outlook reveals how experts view the market and its development in 2015

M&A DEVELOPMENTS IN THE FIRST HALF OF 2017 NORTH AMERICA & EUROPE

M&A DEVELOPMENTS IN THE FIRST HALF OF 217 NORTH AMERICA & EUROPE INTRODUCTION What happened in the first half of 217 in M&A after the announcement of Brexit and the election of President Trump in 216 and

M&A DEVELOPMENTS IN THE FIRST HALF OF 217 NORTH AMERICA & EUROPE INTRODUCTION What happened in the first half of 217 in M&A after the announcement of Brexit and the election of President Trump in 216 and

2017 2Q. US PE Middle Market Report

2017 2Q US PE Middle Market Report In partnership with Co-sponsored by Credits & Contact PitchBook Data, Inc. JOHN GABBERT Founder, CEO ADLEY BOWDEN Vice President, Market Development & Analysis Content

2017 2Q US PE Middle Market Report In partnership with Co-sponsored by Credits & Contact PitchBook Data, Inc. JOHN GABBERT Founder, CEO ADLEY BOWDEN Vice President, Market Development & Analysis Content

2Q Middle Market Indicator

2Q 2014 Middle Market Indicator Middle Market Indicator from The National Center for the Middle Market The Middle Market Indicator (MMI) from The National Center for the Middle Market is a quarterly business

2Q 2014 Middle Market Indicator Middle Market Indicator from The National Center for the Middle Market The Middle Market Indicator (MMI) from The National Center for the Middle Market is a quarterly business

2017 2Q. US PE Middle Market Report

2017 2Q US PE Middle Market Report In partnership with Co-sponsored by For more than 16 years, 271 private equity sponsors have relied on our industry expertise, stable capital reliable deal execution

2017 2Q US PE Middle Market Report In partnership with Co-sponsored by For more than 16 years, 271 private equity sponsors have relied on our industry expertise, stable capital reliable deal execution