29th Indian Fellowship Seminar 1-2 June 2018

|

|

|

- Gregory Phillips

- 5 years ago

- Views:

Transcription

1 29th Indian Fellowship Seminar 1-2 June 2018 Current Issues with Health Insurance Under Guidance Mr R. ARUNACHALAM Presented By Kunal Bansal, S Sabareesh, Shreya Bagrodia

2 Agenda Health Insurance - Overview Current issues in Health Insurance Resolutions Way Forward

3 Health Insurance - Overview During , Health Insurance Companies collected INR crore as Health Insurance Premium, registering a growth of 24.3 % Classification of Health Insurance Business Number of person covered Share of different classes of Business Share of states in Health Insurance Premium

4 Current Issues Health Ins. Frauds Current Issues Health Ins. High Claims Ratio Low level of consumer awareness

5 Fraud Introduction An act or omission intended to gain dishonest or unlawful advantage for a party committing the fraud or for other related parties (as per International Association of Insurance Supervisors, IAIS) According to a recent survey by Insurance Institute of India, false claims account for 10%- 15% of total claims. Healthcare industry in India loses approx. INR crores on fraudulent claims annually.

6 Types of Fraud Hard Fraud deliberate attempt either to stage or invent an accident, injury or other type of loss that would be covered under an insurance policy Soft Fraud also called opportunity fraud; more common and includes exaggeration of legitimate claims by policyholder

7 Parties Involved Policyholder Fraud and/or Claims Fraud Fraud against the insurer in the purchase and/or execution of an insurance product, including fraud at the time of making a claim. Intermediary Fraud Fraud perpetuated by an intermediary against the insurer and/or policyholders. Internal Fraud Fraud/mis-appropriation against the insurer by a staff member.

8 Common Frauds Customers Concealing pre-existing diseases (PED) Manipulating pre-policy health check-up findings Fake/fabricated documents to meet policy terms conditions Duplicate and inflated bills Impersonation Purchasing multiple policies Participating fraud rings Staged accidents & fake disability claims

9 Common Frauds Agents & Brokers Providing fake policy to customer and collecting premium Manipulating pre-policy health check-up records Guiding customer to hide PED/material fact to obtain cover or to file a claim Facilitating policies in fictitious names Channelizing customers to rogue providers Fudging data in group health covers

10 Common Frauds Providers Overcharging, inflated billing Billing for services not provided Unwarranted procedures, excessive investigations Unbundling and upcoding Overutilization, extended length of stay Fudging records, patient history Billing for services to family members or other individuals accompanying the patient

11 Fraud Indicator Examples Claims made shortly after policy inception Multiple claims with repeated hospitalization, multiple claims towards end of policy period Claims made immediately after policy sum insured enhancement Young policyholders between years getting admitted for acute medical illness Claims from hospital located far away from insured s residence Reimbursement claim from a network hospital Claims with a relatively high proportion of pharmacy costs Claims from members creating abnormal pressure to settle claims

12 Current Action against Fraud Action limited to: Rejection of claims for serious fraud all the cases Cancelation of policy in serious fraud cases and not abuse or mis-declaration Most companies do not have an underwriting loop for cases of mis-declaration and nondeclaration Action against agents limited Legal action against fraud not very common Recoveries are rare

13 IRDA Guidelines on Fraud Corporate Governance guidelines mandate insurance companies to set-up a Risk Management Committee. Anti-Fraud Policy duly approved by the Board Fraud Monitoring Department (FMD) Reports to IRDA on an annual basis

14 Managing Fraud Tele-underwriting/proposal verification call helps minimizing agent-led fraud and use of recorded calls help substantiate evidence of fraud at claims stage Pre-authorization Internal audits and post payment claim audits Automated red flag systems Data analytics processes for predictive modelling

15 Managing Fraud (Contd.) Comprehensive fraud and abuse management policy including documentation of definition of types of fraud and abuse; policies, procedures, controls; company s action and review mechanism Health claims forum may be constituted Sharing of knowledge and data including fraud patterns and case studies, fraud customer list and intermediaries, fraudulent providers and investigators etc. Reporting to external bodies such as MCI, IRDA can be looked at

16 Managing Fraud Tele-underwriting/proposal verification call Pre-authorization Internal audits and post payment claim audits Automated red flag systems Data analytics processes for predictive modelling

17 Managing Fraud (Contd.) Comprehensive fraud and abuse management policy Health claims forum may be constituted Sharing of knowledge and data Reporting to external bodies

18 Claim Ratio? Claim Ratio (CR) = (Incurred Claims + Reinsurance payments + Reinsurance recoveries) / (Earned Contributions) For every Rs.100 company collect as premium, they are paying more than Rs.100 as a claim for a year. Instead of profit, they are into loss For every Rs.100 company collect as premium, they are paying less than Rs.100 as a claim for a year. Such companies are making a profit

19 High Claim Ratio - Issues Higher claim than expected High premium Non Competitive Higher Reserve requirements Fluctuation in profits Lower profits

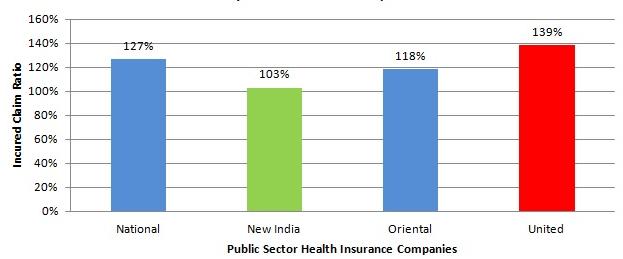

20 Claim Ratio Comparison Public/ Private

21 High Claim Ratio Trend Analysis Net ICR is high for Group Business (>100%) for each of the preceding five years and also consistently increasing over the same period. Net ICR increased for Government Sponsored Health Insurance from 87 percent during to 122 percent in Improvement in Net ICR of individual business - gradual decline from 83 percent in to 76 percent in

22 Claim Ratio Precepts of standards Standard claim definition across industry. Such as definition of critical illness, family floater, ADL s Sensible comparison of data and analysis of claims ratios Generic terms used e.g. exclusions, deferment period

23 Managing High Claim Ratio Alternatives Create Large pools of similar risks Increased Participation Reduce anti selection Premium levels - Stable over time Underwriting Adequate Improve premium rating rules - health status, age, gender, geography, tobacco use, industry/occupation, and family size Reinsurance-Adequate Standardisation of medical treatment across service provider treatment Standardisation of tariffs for procedures across all medical service providers

24 Customer Awareness? The Business Dictionary defines it as The understanding by an individual of their rights as a consumer concerning available products being sold. The concept includes Choice Availability of products Information Able to understand Terms and Conditions Right to be heard Grievance redressal mechanism

25 Customer Awareness- Low?

26 Customer Awareness- Low?

27 Customer Awareness -Low? A Study on Customer Awareness towards Health Insurance With Special Reference to Coimbatore City Analysis of Distribution of the Respondents On The Basis Of Problems Faced By Policy Holders Problems Faced By Policy Holders RANK Terms & Conditions Stated By The Company 1 More Formalities While Claiming 2 Less No Of Hospitals 3 Poor Service 4 Rate Of Premium 5 Poor Response From Agents At The Time Of Claiming 6 Mis-Statement Given By The Agents 7 Expected Amount Not Sanctioned 8 Delay In Claim Statements 9 Source::iosrjournals.org/iosr-jbm/papers/Vol17-issue7/Version- 3/I pdf

28 Low Customer Awareness - Effect In a recent survey conducted by Aviva Life Insurance Company it was found that Indians dream big but are weak at financial planning. Plan index 24% shows how Indians plan financially towards achieving their life goals. Dream Index 61% which explains how aware Indians are of their life goals While 61% of Indian s in the survey had big dreams only 24% of the people had a financial plan to reach there. One of the reasons is unexpected out-of-pocket medical expense due to lack of health insurance.

29 Low Customer Awareness Effect Cntd.. Lower awareness of health products Lower Sales Field force needs to toil more Higher commission Lack of innovative products Lower awareness about Terms and Conditions Possibility of misselling Dissatisfied customers Lower Persistency Regulatory Interventions

30 Low Customer Awareness Possible solutions Some common approaches Educating consumers - by a public authority, non-profit or community body Sales force can also undertake education as part of their marketing strategy. Recommendation from influential individuals - Trusted members of the community such as health workers, are engaged to explain and demonstrate the product. Bundling with more familiar products - with other familiar complementary products and therefore get to experience the new product. Initial discount - The product is subsidized so that there are incentives for enterprises to invest in raising awareness until there is a demand for it.

31 Low Customer Awareness Possible Solutions Awareness programs eg. phone in program, press release, radio jingles, Awareness materials Tax incentives Reduce GST on premium Compulsory insurance (eg. Motor) beyond certain income level Leverage of Social media to increase awareness. Any compulsory "rural obligation" for health companies so that there will be push to increase the size of volume from Rural and Semi urban Companies to file and sell different policies to cater to the needs of population residing in different cities (e.g. A class, B Class, C class and deep rural etc) such as budget plans to meet the needs of economically backward population.

32 Low Customer Awareness Possible Solutions A Study on Customer Awareness towards Health Insurance With Special Reference to Coimbatore City Source of Awareness about Health Insurance SOURCE PERCENTAGE Advertisement 27.4 Agents 45.5 Friends & Relatives 19.1 Doctors /Hospitals 7.4 Employees 0.6 Source:iosrjournals.org/iosr-jbm/papers/Vol17-issue7/Version-3/I pdf

33 Low Customer Awareness Possible Solutions Simplified products Minimal documents at Point of Sales Quicker Issuance Training to agents Collective advertisement across industry Family insurance Develop a deeper base of customers by insuring entire family Using technologies linking health insurance programs to smart phone applications etc Creating networks eg. Create a network of diagnostic labs and hospitals to help prospective customers by setting up a call center.

34 Low Customer Awareness Possible Solutions Enhancing the scope AYUSH Treatment broadened to improve access and affordability Health plus Life Combi-products are allowed - Increasing Penetration Group Credit Linked Health Insurance Policies Lobby for Increased Government funding National Health protection scheme Facilitate the provision of wellness and preventive features as part of Health Insurance Policies

35 Customer Awareness Right to be heard Improving Grievance redressal cells within insurers Collective redressal mechanism for the entire industry eg. Easy accessible 3 digit phone number. Separate cell for senior citizen.

36 Thank You! Any Questions?

29 th India Fellowship Seminar

29 th India Fellowship Seminar 1 st & 2 nd June 2018 Guide: Liyaquat Khan Presenters: Lakshmi Ramaswamy Som Kamal Chatterjee Ashok KR Singh Kushwaha Pradhan Mantri Health Insurance Scheme: 1)Understanding

29 th India Fellowship Seminar 1 st & 2 nd June 2018 Guide: Liyaquat Khan Presenters: Lakshmi Ramaswamy Som Kamal Chatterjee Ashok KR Singh Kushwaha Pradhan Mantri Health Insurance Scheme: 1)Understanding

CLAIM MANAGEMENT CASHLESS REIMBURSEMENT

Presented by Dr. Abhijeet K. Chattoraj, MBA( Marketing ), PGDHRM,FIII, Dip.CIIUK) Certificate in Health Insurance Fraud from North American Training Group and Helpmate services, PhD,University of Pune

Presented by Dr. Abhijeet K. Chattoraj, MBA( Marketing ), PGDHRM,FIII, Dip.CIIUK) Certificate in Health Insurance Fraud from North American Training Group and Helpmate services, PhD,University of Pune

IC38 CORPORATE AGENTS SECTION I COMMON SECTION

IC38 CORPORATE AGENTS SECTION I COMMON SECTION CHAPTER 1: INTRODUCTION TO INSURANCE: Life insurance History and evolution - History of insurance - Insurance through the ages - Modern concepts of insurance

IC38 CORPORATE AGENTS SECTION I COMMON SECTION CHAPTER 1: INTRODUCTION TO INSURANCE: Life insurance History and evolution - History of insurance - Insurance through the ages - Modern concepts of insurance

I3: The Emergence of Healthcare as a Global Issue

I3: The Emergence of Healthcare as a Global Issue Chris Burns Agenda Key Global Trends Centralization of Purchasing War For Talent Trends In Global Healthcare Financing, Data and Analytics 2 1 Key Global

I3: The Emergence of Healthcare as a Global Issue Chris Burns Agenda Key Global Trends Centralization of Purchasing War For Talent Trends In Global Healthcare Financing, Data and Analytics 2 1 Key Global

MAKE OR BUY Role of Private Sector in Health. Alaa Hamed MNA Health Policy Forum, November 12,

MAKE OR BUY Role of Private Sector in Health Alaa Hamed MNA Health Policy Forum, November 12, 13 2017 Based on the chapter: Political Economy of Strategic Purchasing The Question Is it possible to know

MAKE OR BUY Role of Private Sector in Health Alaa Hamed MNA Health Policy Forum, November 12, 13 2017 Based on the chapter: Political Economy of Strategic Purchasing The Question Is it possible to know

Life Insurance in the United Kingdom, Key Trends and Opportunities to 2017

Life Insurance in the United Kingdom, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0362MR Published: August 2013 www.timetric.com Timetric John Carpenter House 7 Carmelite

Life Insurance in the United Kingdom, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0362MR Published: August 2013 www.timetric.com Timetric John Carpenter House 7 Carmelite

An Overview of Insurance Services in Nepal

An Overview of Insurance Services in Nepal Prof. Dr. Puspa Raj Sharma The present scenario of micro (finance and insurance) seems a lot of uncertainty. Naturally uncertainty gives birth to risk. Therefore,

An Overview of Insurance Services in Nepal Prof. Dr. Puspa Raj Sharma The present scenario of micro (finance and insurance) seems a lot of uncertainty. Naturally uncertainty gives birth to risk. Therefore,

Fraud Red Flags for Life Insurance

Fraud Red Flags for Life Insurance December 2017 Underwriting/New Business Signatures on application and paramed exam are not consistent. Inconsistencies in height, weight, physical descriptions, license

Fraud Red Flags for Life Insurance December 2017 Underwriting/New Business Signatures on application and paramed exam are not consistent. Inconsistencies in height, weight, physical descriptions, license

Stakeholder protection Under Company Law and Insurance Law

Stakeholder protection Under Company Law and Insurance Law 26 th April 2014 Stakeholders The Insurance Regulatory and Development Authority (IRDA) considers a stakeholder to be any person, group or organization

Stakeholder protection Under Company Law and Insurance Law 26 th April 2014 Stakeholders The Insurance Regulatory and Development Authority (IRDA) considers a stakeholder to be any person, group or organization

Personal Accident and Health Insurance in India, Key Trends and Opportunities to 2018

Personal Accident and Health Insurance in India, Key Trends and Opportunities to 2018 Market Intelligence Report Reference code: IS0706MR Published: October 2014 www.timetric.com Timetric John Carpenter

Personal Accident and Health Insurance in India, Key Trends and Opportunities to 2018 Market Intelligence Report Reference code: IS0706MR Published: October 2014 www.timetric.com Timetric John Carpenter

FLORIDA TECH EMPLOYEE ACCIDENT/ INJURY REPORT

FLORIDA TECH EMPLOYEE ACCIDENT/ INJURY REPORT Contact Financial Affairs @ 674-7297 OR 8885 IMMEDIATELY regarding an Employee's Injury. Employee AND Supervisor must complete this report. EMPLOYEE INFORMATION

FLORIDA TECH EMPLOYEE ACCIDENT/ INJURY REPORT Contact Financial Affairs @ 674-7297 OR 8885 IMMEDIATELY regarding an Employee's Injury. Employee AND Supervisor must complete this report. EMPLOYEE INFORMATION

Personal Accident and Health Insurance in Romania, Key Trends and Opportunities to 2017

Personal Accident and Health Insurance in Romania, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0587MR Published: May 2014 www.timetric.com Timetric John Carpenter

Personal Accident and Health Insurance in Romania, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0587MR Published: May 2014 www.timetric.com Timetric John Carpenter

Schemes Targeting Healthcare Affordability in India

www.swaniti.in Schemes Targeting Healthcare Affordability in India 1. Rashtriya Swasthya Bima Yojana (RSBY) Background Public Expenditure on healthcare is only 1.2% of GDP as compared to 7.7% in USA Out

www.swaniti.in Schemes Targeting Healthcare Affordability in India 1. Rashtriya Swasthya Bima Yojana (RSBY) Background Public Expenditure on healthcare is only 1.2% of GDP as compared to 7.7% in USA Out

POLICY DOCUMENT. Bajaj Allianz Life Insurance Co. Ltd. Policy Document Ver.2(032013) Page 1 of 9

Page 1 of 9") POLICY DOCUMENT This Policy is issued on the basis of the information given and declaration made by the Policyholder in the Proposal Form, which is incorporated herein and forms the basis of this Policy.

POLICY DOCUMENT This Policy is issued on the basis of the information given and declaration made by the Policyholder in the Proposal Form, which is incorporated herein and forms the basis of this Policy.

Insurance fraud Problem definition and overview of approaches across Europe

Insurance fraud Problem definition and overview of approaches across Europe XIII International Conference about Insurance Crime 11 March 2010 Sandrine Noël Head of Non-life insurance The CEA Fraud problem

Insurance fraud Problem definition and overview of approaches across Europe XIII International Conference about Insurance Crime 11 March 2010 Sandrine Noël Head of Non-life insurance The CEA Fraud problem

A promise of compensation for specific potential future losses in exchange for a periodic payment. Insurance is designed to protect the financial

INSURANCE OMBUDSMAN A promise of compensation for specific potential future losses in exchange for a periodic payment. Insurance is designed to protect the financial well-being of an individual, company

INSURANCE OMBUDSMAN A promise of compensation for specific potential future losses in exchange for a periodic payment. Insurance is designed to protect the financial well-being of an individual, company

EXECUTIVE SUMMARY. A systematic approach for combating enrollment fraud

EXECUTIVE SUMMARY A systematic approach for combating enrollment fraud OCTOBER 2017 Enrollment fraud is a serious and growing problem The proliferation of identity fraud and new ways of enrolling in health

EXECUTIVE SUMMARY A systematic approach for combating enrollment fraud OCTOBER 2017 Enrollment fraud is a serious and growing problem The proliferation of identity fraud and new ways of enrolling in health

Nothing in this Guide may be reproduced without the approval of LIA. YGTHI May 2016

2016 This Guide is an initiative of the MoneySENSE national financial education programme. The MoneySENSE programme brings together industry and public sector initiatives to enhance the basic financial

2016 This Guide is an initiative of the MoneySENSE national financial education programme. The MoneySENSE programme brings together industry and public sector initiatives to enhance the basic financial

Mainstreaming Micro-Insurance Schemes: Role of Insurance Companies in Nepal

Economic Literature, Vol. XI (4046), June 203 Mainstreaming MicroInsurance Schemes: Role of Insurance Companies in Nepal Puspa Raj Sharma, Ph. D * ABSTRACT Microinsurance refers to the relatively short

Economic Literature, Vol. XI (4046), June 203 Mainstreaming MicroInsurance Schemes: Role of Insurance Companies in Nepal Puspa Raj Sharma, Ph. D * ABSTRACT Microinsurance refers to the relatively short

Health Insurance Glossary of Terms

1 Health Insurance Glossary of Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

1 Health Insurance Glossary of Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Pre Insurance. Medical Examination Portal Operational Manual. Area Doctor Login

Pre Insurance Medical Examination Portal Operational Manual Area Doctor Login Copyright Information used in this document is subject to change without notice. Companies, names, and the data used in the

Pre Insurance Medical Examination Portal Operational Manual Area Doctor Login Copyright Information used in this document is subject to change without notice. Companies, names, and the data used in the

Personal Accident and Health Insurance in Malaysia, Key Trends and Opportunities to 2017

Personal Accident and Health Insurance in Malaysia, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0414MR Published: October 2013 www.timetric.com Timetric John Carpenter

Personal Accident and Health Insurance in Malaysia, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0414MR Published: October 2013 www.timetric.com Timetric John Carpenter

Introduction to the US Health Care System. What the Business Development Professional Should Know

Introduction to the US Health Care System What the Business Development Professional Should Know November 2006 1 Understanding of the US Health Care System Evolution of the US health care system to its

Introduction to the US Health Care System What the Business Development Professional Should Know November 2006 1 Understanding of the US Health Care System Evolution of the US health care system to its

Berneta L. Haynes Director of Equity and Access Georgia Watch

Berneta L. Haynes Director of Equity and Access Georgia Watch www.georgiawatch.org Our organization Founded in 2002 Statewide advocacy organization Non-profit and non- partisan Our work Ensure consumers

Berneta L. Haynes Director of Equity and Access Georgia Watch www.georgiawatch.org Our organization Founded in 2002 Statewide advocacy organization Non-profit and non- partisan Our work Ensure consumers

Medicare supplement (Medigap) plan application

plan application") Medicare supplement (Medigap) plan application SECTION 1 Personal information Last name First name Middle initial Social Security number - - Primary street address City State ZIP code Mailing street address

Medicare supplement (Medigap) plan application SECTION 1 Personal information Last name First name Middle initial Social Security number - - Primary street address City State ZIP code Mailing street address

ANTI-FRAUD PLAN INTRODUCTION

ANTI-FRAUD PLAN INTRODUCTION We recognize the importance of preventing, detecting and investigating fraud, abuse and waste, and are committed to protecting and preserving the integrity and availability

ANTI-FRAUD PLAN INTRODUCTION We recognize the importance of preventing, detecting and investigating fraud, abuse and waste, and are committed to protecting and preserving the integrity and availability

INDIA FELLOWSHIP SEMINAR 01/06/18-02/06/18

INDIA FELLOWSHIP SEMINAR 01/06/18-02/06/18 General insurance companies - Understanding key performance measures, Benefits and limitations in listing GI companies. Shubhanjali Gupta, Richa Gupta, Rohit

INDIA FELLOWSHIP SEMINAR 01/06/18-02/06/18 General insurance companies - Understanding key performance measures, Benefits and limitations in listing GI companies. Shubhanjali Gupta, Richa Gupta, Rohit

A Specialist Health Insurer in India

Presents Personal Accident plan combined with overseas family medical insurance in india for NRI s in UAE & their dependants residing anywhere Claims Adminstrator A Specialist Health Insurer in India MY

Presents Personal Accident plan combined with overseas family medical insurance in india for NRI s in UAE & their dependants residing anywhere Claims Adminstrator A Specialist Health Insurer in India MY

Sun Life Assurance Company of Canada

Short Term Disability Claim Packet Instructions Send in ALL signed statements, which we require to properly review the claim. Failure to provide complete and accurate information could result in the need

Short Term Disability Claim Packet Instructions Send in ALL signed statements, which we require to properly review the claim. Failure to provide complete and accurate information could result in the need

Experience of Deregulation of Insurance Sector in India

Experience of Deregulation of Insurance Sector in India BY Sriram Taranikanti, Executive Director INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY 17 th April, 2013 1 FRAMEWORK OF PRESENTATION Evolution

Experience of Deregulation of Insurance Sector in India BY Sriram Taranikanti, Executive Director INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY 17 th April, 2013 1 FRAMEWORK OF PRESENTATION Evolution

Request for Proposal (RFP) for Corporate Agency Arrangement for Life Insurance, General Insurance & Standalone Health Insurance Business

for Corporate Agency Arrangement for Life Insurance, General Insurance & Standalone Health Insurance Business") Registered Office IFCI Tower, 61, Nehru Place, New Delhi 110019 Corporate Office Continental Chambers, 3 rd Floor, 142, M.G. Road, Numgambakkam, Chennai 600034 Regional Office West Mafatlal Chambers B,

Registered Office IFCI Tower, 61, Nehru Place, New Delhi 110019 Corporate Office Continental Chambers, 3 rd Floor, 142, M.G. Road, Numgambakkam, Chennai 600034 Regional Office West Mafatlal Chambers B,

Access to Medicines in Low and Middle Income Countries: Goals and Challenges. Andreas Seiter The World Bank August 2013

Access to Medicines in Low and Middle Income Countries: Goals and Challenges Andreas Seiter The World Bank August 2013 1 The World Bank and its clients Financing (IDA, subsidized) Low-Income Countries

Access to Medicines in Low and Middle Income Countries: Goals and Challenges Andreas Seiter The World Bank August 2013 1 The World Bank and its clients Financing (IDA, subsidized) Low-Income Countries

THE F FILES. Group benefits fraud what you need to know to fight fraud GET #FRAUDSMART

THE F FILES Group benefits fraud what you need to know to fight fraud GET #FRAUDSMART SPRING 2018 LOOKING INTO THE FUTURE OF FRAUD WITH PREDICTIVE ANALYTICS Big data it is fundamental in the fight against

THE F FILES Group benefits fraud what you need to know to fight fraud GET #FRAUDSMART SPRING 2018 LOOKING INTO THE FUTURE OF FRAUD WITH PREDICTIVE ANALYTICS Big data it is fundamental in the fight against

INSURED STATEMENT OF CLAIM

INSURED STATEMENT OF CLAIM Last Name First MI Address Apt No. City State Zip Telephone No. - - Home Cell Work E-Mail Address: Birth Date / / Soc. Sec. No. Policy Number Gender: M F Height Weight Spouse

INSURED STATEMENT OF CLAIM Last Name First MI Address Apt No. City State Zip Telephone No. - - Home Cell Work E-Mail Address: Birth Date / / Soc. Sec. No. Policy Number Gender: M F Height Weight Spouse

(3) 20,000 policies in the 5th year are to be made from sector

20,000 policies in the 5th year are to be made from sector") IRDA Agent Licensing Question paper (1) Potential purchaser of product is called Prospect Consumer Customer Client (2) If policyholder is in grievance, will solve Grievance officer Court order Ombudsman

IRDA Agent Licensing Question paper (1) Potential purchaser of product is called Prospect Consumer Customer Client (2) If policyholder is in grievance, will solve Grievance officer Court order Ombudsman

(1) Potential purchaser of product is called (a) Prospect (b) Consumer (c) Customer (d) Client

Potential purchaser of product is called (a) Prospect (b) Consumer (c) Customer (d) Client") (1) Potential purchaser of product is called (a) Prospect (b) Consumer (c) Customer (d) Client (2) If policyholder is in grievance, will solve (a) Grievance officer (b) Court order (c) Ombudsman (d) All

(1) Potential purchaser of product is called (a) Prospect (b) Consumer (c) Customer (d) Client (2) If policyholder is in grievance, will solve (a) Grievance officer (b) Court order (c) Ombudsman (d) All

Washington State Enrollment Form for Medical and/or Prescription Insurance for Individuals and Families

Washington State Enrollment Form for Medical and/or Prescription Insurance for Individuals and Families PLEASE PRINT IN BLACK INK AGENT/AGENCY INFORMATION Agent Name: Agent Number: Key Agency Contact:

Washington State Enrollment Form for Medical and/or Prescription Insurance for Individuals and Families PLEASE PRINT IN BLACK INK AGENT/AGENCY INFORMATION Agent Name: Agent Number: Key Agency Contact:

The Risk of Economic Crime

The Risk of Economic Crime 0 ACFE European Fraud Conference London, March 7, 0 GROUP SECURITY HERE TO PROTECT OUR WORLD Torsten Wolf Group Head of Crime and Fraud Prevention Agenda Introduction Economic

The Risk of Economic Crime 0 ACFE European Fraud Conference London, March 7, 0 GROUP SECURITY HERE TO PROTECT OUR WORLD Torsten Wolf Group Head of Crime and Fraud Prevention Agenda Introduction Economic

Regulation of Micro-insurance

Regulation of Micro-insurance insurance T. K. Banerjee Member 1 Outline Bridging the Demand-Supply gap - response of IRDA. Proposed Micro-insurance insurance regulation - idea and objective. Proposed mechanism

Regulation of Micro-insurance insurance T. K. Banerjee Member 1 Outline Bridging the Demand-Supply gap - response of IRDA. Proposed Micro-insurance insurance regulation - idea and objective. Proposed mechanism

Group Long Term Disability

Group Long Term Disability Life Insurance Company of rth America Connecticut General Life Insurance Company Cigna Life Insurance Company of New York Great-West Healthcare Administered by Cigna Group Long

Group Long Term Disability Life Insurance Company of rth America Connecticut General Life Insurance Company Cigna Life Insurance Company of New York Great-West Healthcare Administered by Cigna Group Long

Edelweiss Tokio Life Insurance Company Limited ANTI FRAUD POLICY

Edelweiss Tokio Life Insurance Company Limited ANTI FRAUD POLICY Anti Fraud Policy_Ver 2.3 Page 1 of 7 TABLE OF CONTENTS Sr. Particulars Page No. No. 1 Background and Purpose 3 2 Scope 3 3 Fraud Risk Governance

Edelweiss Tokio Life Insurance Company Limited ANTI FRAUD POLICY Anti Fraud Policy_Ver 2.3 Page 1 of 7 TABLE OF CONTENTS Sr. Particulars Page No. No. 1 Background and Purpose 3 2 Scope 3 3 Fraud Risk Governance

Annual Report of Insurance Fraud and Abuse for 2016

Annual Report of Insurance Fraud and Abuse for 2016 Prepared by the Maine Bureau of Insurance June 2017 Paul R. LePage Governor Anne L. Head Commissioner Eric A. Cioppa Superintendent Table of Contents

Annual Report of Insurance Fraud and Abuse for 2016 Prepared by the Maine Bureau of Insurance June 2017 Paul R. LePage Governor Anne L. Head Commissioner Eric A. Cioppa Superintendent Table of Contents

Shaping a Partnership in Voluntary Benefits ACA Solutions

Shaping a Partnership in Voluntary Benefits ACA Solutions Annual Survey of Americans' Views on Health Care and the ACA Finds Nearly Half of Remaining Uninsured are Unaware of the Individual Mandate or

Shaping a Partnership in Voluntary Benefits ACA Solutions Annual Survey of Americans' Views on Health Care and the ACA Finds Nearly Half of Remaining Uninsured are Unaware of the Individual Mandate or

Non-Life Insurance in Taiwan, Key Trends and Opportunities to 2017

Non-Life Insurance in Taiwan, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0481MR Published: January 2014 www.timetric.com Timetric John Carpenter House 7 Carmelite

Non-Life Insurance in Taiwan, Key Trends and Opportunities to 2017 Market Intelligence Report Reference code: IS0481MR Published: January 2014 www.timetric.com Timetric John Carpenter House 7 Carmelite

Disability Claim Form Instructions

Documentation required upon submitting a Disability Claim: Disability Claim Form Instructions To substantiate a claim for disability benefits covered by the Policy terms, the following documents must be

Documentation required upon submitting a Disability Claim: Disability Claim Form Instructions To substantiate a claim for disability benefits covered by the Policy terms, the following documents must be

INSURED STATEMENT OF CLAIM

INSURED STATEMENT OF CLAIM Last Name First MI Policy Number Address Apt No. City State Zip Telephone No. - - Home Cell Work E-Mail Address: Birth Date / / Soc. Sec. No. Gender: M F Height Weight Spouse

INSURED STATEMENT OF CLAIM Last Name First MI Policy Number Address Apt No. City State Zip Telephone No. - - Home Cell Work E-Mail Address: Birth Date / / Soc. Sec. No. Gender: M F Height Weight Spouse

Pricing Health Insurance Products

Pricing Health Insurance Products Anuradha Sriram -- Appointed Actuary - Aditya Birla Health Insurance Co. Ltd Anshul Mittal Apollo Munich Health Insurance Co. Ltd Ankit Kedia Aditya Birla Health Insurance

Pricing Health Insurance Products Anuradha Sriram -- Appointed Actuary - Aditya Birla Health Insurance Co. Ltd Anshul Mittal Apollo Munich Health Insurance Co. Ltd Ankit Kedia Aditya Birla Health Insurance

Receive 90% of the surplus generated as bonus. Simplified product structure for easy understanding. Enhance your benefits by adding various riders

Reasons Edelweiss Tokio Life Save n Grow Plan (WA) An Endowment Assurance Plan (with profits) 2 3 4 5 6 7 1 Increasing protection over the policy term Receive 90% of the surplus generated as bonus Simplified

Reasons Edelweiss Tokio Life Save n Grow Plan (WA) An Endowment Assurance Plan (with profits) 2 3 4 5 6 7 1 Increasing protection over the policy term Receive 90% of the surplus generated as bonus Simplified

SECTION A SECTION 8 SECTION C SECTION D SECTION E SECTION F SECTION G

CLAIM FORM - PART A TO 8E FILLED IN 8Y THE INSURED The issue of this Form is not to be taken as an admission of liability (To be filled in block letters) DETAILS OF PRIMARY INSURED: a) Policy No: b) Sl.

CLAIM FORM - PART A TO 8E FILLED IN 8Y THE INSURED The issue of this Form is not to be taken as an admission of liability (To be filled in block letters) DETAILS OF PRIMARY INSURED: a) Policy No: b) Sl.

Chapter 15. Agenda. Health Care Problems in the US. Individual Health Insurance Coverages. Problem 1: Rising Health Care Expenditures

Chapter 15 Individual Health Insurance Coverages Agenda 2 Health Care Problems in the US Individual Health Insurance Coverages Hospital-Surgical Insurance Major Medical Insurance Health Savings Accounts

Chapter 15 Individual Health Insurance Coverages Agenda 2 Health Care Problems in the US Individual Health Insurance Coverages Hospital-Surgical Insurance Major Medical Insurance Health Savings Accounts

Corporate Presentation

Corporate Presentation Agenda Industry Overview Operating Performance Financial Performance 2 Agenda Industry Overview Operating Performance Financial Performance 3 Industry has witnessed steady growth

Corporate Presentation Agenda Industry Overview Operating Performance Financial Performance 2 Agenda Industry Overview Operating Performance Financial Performance 3 Industry has witnessed steady growth

INSURANCE LAW OF THE KINGDOM OF CAMBODIA

INSURANCE LAW OF THE KINGDOM OF CAMBODIA (Adopted by the National Assembly of The Kingdom of Cambodia on 20th June,2000 at the 4 th Session, 2 nd Legislation) UNOFFICIAL TRANSLATION Prepared by RE. Dept

INSURANCE LAW OF THE KINGDOM OF CAMBODIA (Adopted by the National Assembly of The Kingdom of Cambodia on 20th June,2000 at the 4 th Session, 2 nd Legislation) UNOFFICIAL TRANSLATION Prepared by RE. Dept

Sun Life Assurance Company of Canada

Sun Life Assurance Company of Canada Short Term Disability Claim Packet Instructions Send in ALL signed statements, which we require to properly review the claim. Failure to provide complete and accurate

Sun Life Assurance Company of Canada Short Term Disability Claim Packet Instructions Send in ALL signed statements, which we require to properly review the claim. Failure to provide complete and accurate

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future.

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

ENHANCED DUE DILIGENCE TO CURB INSURANCE FRAUD

ENHANCED DUE DILIGENCE TO CURB INSURANCE FRAUD Paul Cochrane STATEMENT OF INTENT Driven by tightened regulatory restriction in the financial sector and boosted by the recent recession, insurance fraud

ENHANCED DUE DILIGENCE TO CURB INSURANCE FRAUD Paul Cochrane STATEMENT OF INTENT Driven by tightened regulatory restriction in the financial sector and boosted by the recent recession, insurance fraud

MICRO INSURANCE IN INDIA PERSPECTIVES AND CHALLENGES. M Kalyanasundaram Chief Executive INAFI-INDIA

MICRO INSURANCE IN INDIA PERSPECTIVES AND CHALLENGES M Kalyanasundaram Chief Executive INAFI-INDIA E-mail: indiainafi@touchtelindia.net Poverty & Micro Finance Poverty A state of deprivation A state of

MICRO INSURANCE IN INDIA PERSPECTIVES AND CHALLENGES M Kalyanasundaram Chief Executive INAFI-INDIA E-mail: indiainafi@touchtelindia.net Poverty & Micro Finance Poverty A state of deprivation A state of

Module II (Exam 1) - Risk Analysis and Insurance Planning (RAIP)

- Risk Analysis and Insurance Planning (RAIP)") Marks Category Module II (Exam 1) - Risk Analysis and Insurance Planning (RAIP) Exam 1 Topic List to the extent of 80% of Total Marks (150) i.e. 120 marks (30 marks reserved for the Module I Introduction

Marks Category Module II (Exam 1) - Risk Analysis and Insurance Planning (RAIP) Exam 1 Topic List to the extent of 80% of Total Marks (150) i.e. 120 marks (30 marks reserved for the Module I Introduction

CEU INSTITUTE Medical Fraud and Abuse: Strategies for the Claim Professional

CEU INSTITUTE Medical Fraud and Abuse: Strategies for the Claim Professional March 22, 2011 Ted Colquett Wilson & Berryhill, P.C. Birmingham Alabama Section 1 Summary Fraud costs the insurance industry

CEU INSTITUTE Medical Fraud and Abuse: Strategies for the Claim Professional March 22, 2011 Ted Colquett Wilson & Berryhill, P.C. Birmingham Alabama Section 1 Summary Fraud costs the insurance industry

Total Health Care USA, Inc.: Total Saver Complete Summary of Benefits and Coverage: What this Plan Covers & What it Costs

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the policy or plan document at www.thcmi.com or by calling 1-800-826-2862 Important Questions

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the policy or plan document at www.thcmi.com or by calling 1-800-826-2862 Important Questions

Health Information Technology and Management

Health Information Technology and Management CHAPTER 9 Healthcare Coding and Reimbursement Pretest (True/False) CPT-4 codes are used to bill for disease and illness. Medicare Part B provides medical insurance

Health Information Technology and Management CHAPTER 9 Healthcare Coding and Reimbursement Pretest (True/False) CPT-4 codes are used to bill for disease and illness. Medicare Part B provides medical insurance

POLICY FOR PROTECTION OF INTERESTS OF POLICYHOLDERS. TATA AIG General Insurance Co. Ltd. POLICY FOR PROTECTION OF INTERESTS OF POLICYHOLDERS

POLICY FOR PROTECTION OF INTERESTS OF POLICYHOLDERS Page 1 of 6 Abbreviations Tata AIG IRDAI PPC PPI TAT Tata AIG General Insurance Company Ltd Insurance Regulatory and Development Authority of India Policyholders

POLICY FOR PROTECTION OF INTERESTS OF POLICYHOLDERS Page 1 of 6 Abbreviations Tata AIG IRDAI PPC PPI TAT Tata AIG General Insurance Company Ltd Insurance Regulatory and Development Authority of India Policyholders

Salaried Team Total Benefits Summary

Salaried Team 2018 Total Benefits Summary Compensation Gentex total compensation is engineered specifically for those of us wired with an ownership mentality mindset. Take a minute to study up it is innovative,

Salaried Team 2018 Total Benefits Summary Compensation Gentex total compensation is engineered specifically for those of us wired with an ownership mentality mindset. Take a minute to study up it is innovative,

AMENDED ANTI-FRAUD PLAN FOR AVMED, INC. Amended November 2014

AMENDED ANTI-FRAUD PLAN FOR AVMED, INC. Amended November 2014 AvMed, Inc. hereby amends the Anti-Fraud Plan of its Special Investigations Unit ("SIU") which was created to identify, investigate, and rectify

AMENDED ANTI-FRAUD PLAN FOR AVMED, INC. Amended November 2014 AvMed, Inc. hereby amends the Anti-Fraud Plan of its Special Investigations Unit ("SIU") which was created to identify, investigate, and rectify

Health System and Policies of China

of China Yang Cao, PhD Associate Professor China Pharmaceutical University Nanjing, China Transformation of Healthcare Delivery in China Medical insurance 1 The timeline of the medical and health system

of China Yang Cao, PhD Associate Professor China Pharmaceutical University Nanjing, China Transformation of Healthcare Delivery in China Medical insurance 1 The timeline of the medical and health system

Total Health Care USA, Inc.: Total Gold Premier Summary of Benefits and Coverage: What this Plan Covers & What it Costs

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the policy or plan document at www.thcmi.com or by calling 1-800-826-2862 Important Questions

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the policy or plan document at www.thcmi.com or by calling 1-800-826-2862 Important Questions

SHORT WALKS. BIG BENEFITS.

SHORT WALKS. BIG BENEFITS. Optima Restore with Stay Active benefit. SAVE 2% SAVE 5% SAVE 8% Introducing Optima Restore Health Insurance Plan The Optima Restore isn`t just a regular health insurance plan.

SHORT WALKS. BIG BENEFITS. Optima Restore with Stay Active benefit. SAVE 2% SAVE 5% SAVE 8% Introducing Optima Restore Health Insurance Plan The Optima Restore isn`t just a regular health insurance plan.

Standard Bank Unity Hospital Cash Plan

Standard Bank Unity Hospital Cash Plan Standard Insurance Limited Registration number: 1993/007593/06 Between Standard Insurance Limited (Us) and the Policyholder (You) 1 Important information about the

Standard Bank Unity Hospital Cash Plan Standard Insurance Limited Registration number: 1993/007593/06 Between Standard Insurance Limited (Us) and the Policyholder (You) 1 Important information about the

Summary of Benefits and Coverage for Assurant Health individual major medical Bronze plans

Assurant Health Time Insurance Company Summary of Benefits and Coverage for Assurant Health individual major medical Bronze plans View Summary of Benefits and Coverage for an individual plan View Summary

Assurant Health Time Insurance Company Summary of Benefits and Coverage for Assurant Health individual major medical Bronze plans View Summary of Benefits and Coverage for an individual plan View Summary

ACCESS TO THE HIGHEST QUALITY PRIMARY HEALTHCARE AT AFFORDABLE PRICES

ACCESS TO THE HIGHEST QUALITY PRIMARY HEALTHCARE AT AFFORDABLE PRICES WELCOME TO ELIXI MEDICAL INSURANCE PURPLE PLAN - PRIMARY AND HOSPITAL CARE Elixi Medical Insurance aims to make private healthcare

ACCESS TO THE HIGHEST QUALITY PRIMARY HEALTHCARE AT AFFORDABLE PRICES WELCOME TO ELIXI MEDICAL INSURANCE PURPLE PLAN - PRIMARY AND HOSPITAL CARE Elixi Medical Insurance aims to make private healthcare

ASHK Healthcare Seminar 2015

ASHK Healthcare Seminar 2015 Latest Development on Voluntary Health Insurance Scheme 17 April 2015 Mr Chris SUN Head (Healthcare Planning and Development Office) Food & Health Bureau Hong Kong SAR Government

ASHK Healthcare Seminar 2015 Latest Development on Voluntary Health Insurance Scheme 17 April 2015 Mr Chris SUN Head (Healthcare Planning and Development Office) Food & Health Bureau Hong Kong SAR Government

GUIDANCE NOTE ON DETERING, PREVENTING, DETECTING, REPORTING AND REMEDYING INSURANCE FRAUD

GUERNSEY FINANCIAL SERVICES COMMISSION GUIDANCE NOTE ON DETERING, PREVENTING, DETECTING, REPORTING AND REMEDYING INSURANCE FRAUD Introduction Fraud is a serious risk to the insurance sector and can have

GUERNSEY FINANCIAL SERVICES COMMISSION GUIDANCE NOTE ON DETERING, PREVENTING, DETECTING, REPORTING AND REMEDYING INSURANCE FRAUD Introduction Fraud is a serious risk to the insurance sector and can have

Summary of Benefits and Coverage for Assurant Health individual major medical Bronze plans

Assurant Health Time Insurance Company Summary of Benefits and Coverage for Assurant Health individual major medical Bronze plans View Summary of Benefits and Coverage for an individual plan View Summary

Assurant Health Time Insurance Company Summary of Benefits and Coverage for Assurant Health individual major medical Bronze plans View Summary of Benefits and Coverage for an individual plan View Summary

Investor Presentation. November 2016

Investor Presentation November 2016 Agenda Industry overview Company overview & strategy ICICI Lombard performance 2 Agenda Industry overview Company overview & strategy ICICI Lombard performance 3 Industry

Investor Presentation November 2016 Agenda Industry overview Company overview & strategy ICICI Lombard performance 2 Agenda Industry overview Company overview & strategy ICICI Lombard performance 3 Industry

Why worry about future expenses?

Why worry about future expenses? DOUBLE YOUR DREAMS BHARTI AXA LIFE SUPER ENDOWMENT PLAN A Non Linked Non-Participating Limited Pay Endowment Life Insurance Plan Bharti AXA Life Super Endowment Plan A

Why worry about future expenses? DOUBLE YOUR DREAMS BHARTI AXA LIFE SUPER ENDOWMENT PLAN A Non Linked Non-Participating Limited Pay Endowment Life Insurance Plan Bharti AXA Life Super Endowment Plan A

A Study on Policy Holder s Satisfaction towards Life Insurance Corporation of India (LIC) with Special Reference to Coimbatore City

with Special Reference to Coimbatore City") DOI : 10.18843/ijms/v5iS5/08 DOIURL :http://dx.doi.org/10.18843/ijms/v5is5/08 A Study on Policy Holder s Satisfaction towards Life Insurance Corporation of India (LIC) with Special Reference to Coimbatore

DOI : 10.18843/ijms/v5iS5/08 DOIURL :http://dx.doi.org/10.18843/ijms/v5is5/08 A Study on Policy Holder s Satisfaction towards Life Insurance Corporation of India (LIC) with Special Reference to Coimbatore

Predictive Analytics in the People s Republic of China

Predictive Analytics in the People s Republic of China Rong Yi, PhD Senior Consultant Rong.Yi@milliman.com Tel: 781.213.6200 4 th National Predictive Modeling Summit Arlington, VA September 15-16, 2010

Predictive Analytics in the People s Republic of China Rong Yi, PhD Senior Consultant Rong.Yi@milliman.com Tel: 781.213.6200 4 th National Predictive Modeling Summit Arlington, VA September 15-16, 2010

OJK SUPERVISION RELATED TO FRAUD

OJK SUPERVISION RELATED TO FRAUD Ahmad Nasrullah Director Of Insurance and BPJS Kesehatan Supervision Bali, 13 Oktober 2017 FRAUD IN INSURANCE Fraud means a deviating act or purposeful neglect undertaken

OJK SUPERVISION RELATED TO FRAUD Ahmad Nasrullah Director Of Insurance and BPJS Kesehatan Supervision Bali, 13 Oktober 2017 FRAUD IN INSURANCE Fraud means a deviating act or purposeful neglect undertaken

Maine Association of Health Underwriters 2010 Health Care Reform Position Paper

Maine Association of Health Underwriters 2010 Health Care Reform Position Paper The Maine Association of Health Underwriters (MAHU) represents health insurance brokers and consultants advising thousands

Maine Association of Health Underwriters 2010 Health Care Reform Position Paper The Maine Association of Health Underwriters (MAHU) represents health insurance brokers and consultants advising thousands

Important Questions Answers Why this Matters: What is the overall deductible? Are there other deductibles for specific services?

Exclusive Care: Plan Coverage Period: 01/01/2019 12/31/2019 This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the Summary Plan Document at

Exclusive Care: Plan Coverage Period: 01/01/2019 12/31/2019 This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the Summary Plan Document at

Health Basics. 8.1 General Definitions LEARNING OBJECTIVES OVERVIEW

8 Health Basics LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify the definitions of accident, sickness, peril, and pre-existing conditions 2. Understand the principal

8 Health Basics LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify the definitions of accident, sickness, peril, and pre-existing conditions 2. Understand the principal

Financial Planning. Patient Education. For a liver transplant

Patient Education Financial Planning For a liver transplant Liver transplants are expensive. Planning your finances, both your income and insurance, will be a key part of planning for transplant. The planning

Patient Education Financial Planning For a liver transplant Liver transplants are expensive. Planning your finances, both your income and insurance, will be a key part of planning for transplant. The planning

Help NYSIF Fight Fraud

NEW YORK STATE INSURANCE FUND Help NYSIF Fight Fraud Red Flags of Claims Fraud About Policy and Provider Fraud Reporting Fraud to NYSIF nysif.com THE NEW YORK STATE INSURANCE FUND Workers Compensation

NEW YORK STATE INSURANCE FUND Help NYSIF Fight Fraud Red Flags of Claims Fraud About Policy and Provider Fraud Reporting Fraud to NYSIF nysif.com THE NEW YORK STATE INSURANCE FUND Workers Compensation

CLAIM FORM FOR MEDICAL EXPENSES AND OTHER EXPENSES

CLAIM FORM FOR MEDICAL EXPENSES AND OTHER EXPENSES Please note that we have to ensure that our claim form covers all types of claim. If you do not consider a question to be relevant to your circumstances

CLAIM FORM FOR MEDICAL EXPENSES AND OTHER EXPENSES Please note that we have to ensure that our claim form covers all types of claim. If you do not consider a question to be relevant to your circumstances

Workers Compensation. Workers Compensation

Federal and State Administration Qualifications for coverage Classifications of cases Physician reimbursement Billing and claims processing 2 1 Federal and State Laws Employers required to provide workers

Federal and State Administration Qualifications for coverage Classifications of cases Physician reimbursement Billing and claims processing 2 1 Federal and State Laws Employers required to provide workers

Personal Finance, 6e (Madura) Chapter 12 Health and Disability Insurance Background on Health Insurance

Chapter 12 Health and Disability Insurance Background on Health Insurance") Personal Finance, 6e (Madura) Chapter 12 Health and Disability Insurance 12.1 Background on Health Insurance 1) Health insurance protects net worth by minimizing the chance that you will have to reduce

Personal Finance, 6e (Madura) Chapter 12 Health and Disability Insurance 12.1 Background on Health Insurance 1) Health insurance protects net worth by minimizing the chance that you will have to reduce

Sun Life Assurance Company of Canada

Long Term Disability Claim Packet - Claimant Instructions for the Claimant Please mail all documents 4-6 weeks before the end of your elimination period. Please make sure to initiate the Long Term Disability

Long Term Disability Claim Packet - Claimant Instructions for the Claimant Please mail all documents 4-6 weeks before the end of your elimination period. Please make sure to initiate the Long Term Disability

Sun Life Assurance Company of Canada

Long Term Disability Claim Packet - Claimant Instructions for the Claimant Please mail all documents 4-6 weeks before the end of your elimination period. Please make sure to initiate the Long Term Disability

Long Term Disability Claim Packet - Claimant Instructions for the Claimant Please mail all documents 4-6 weeks before the end of your elimination period. Please make sure to initiate the Long Term Disability

General Insurance Industry in India

General Insurance Industry in India 2009 Casualty Loss Reserve Seminar September 14, 2009 Anita Sathe FCAS, FSA, MAAA ansathe@deloitte.com Contents History State of the market Removal of tariffs Key lines

General Insurance Industry in India 2009 Casualty Loss Reserve Seminar September 14, 2009 Anita Sathe FCAS, FSA, MAAA ansathe@deloitte.com Contents History State of the market Removal of tariffs Key lines

Easy Travel Insurance CLAIM FORM

Easy Travel Insurance Apollo Munich Health Insurance Co. Ltd. 10th Floor, Tower-B, Building No. 10, CLAIM FORM Issuance of this form does not amount to admission of any liability or a waiver of any of

Easy Travel Insurance Apollo Munich Health Insurance Co. Ltd. 10th Floor, Tower-B, Building No. 10, CLAIM FORM Issuance of this form does not amount to admission of any liability or a waiver of any of

Claim form for health insurance policies other than travel and personal accident - PART A

M M Claim form for health insurance policies other than travel and personal accident - PART A TO BE FILLED IN BY THE INSURED (TO BE FILLED IN BLOCK LETTERS) The issue of this Form is not to be taken as

M M Claim form for health insurance policies other than travel and personal accident - PART A TO BE FILLED IN BY THE INSURED (TO BE FILLED IN BLOCK LETTERS) The issue of this Form is not to be taken as

Toll-free: Fax: Call toll-free Monday through Friday, 8 a.m. to 8 p.m. Eastern Time.

For use with policies issued by the following Unum Group [ Unum ] subsidiaries: Unum Life Insurance Company of America Provident Life and Accident Insurance Company OUR COMMITMENT TO YOU We understand

For use with policies issued by the following Unum Group [ Unum ] subsidiaries: Unum Life Insurance Company of America Provident Life and Accident Insurance Company OUR COMMITMENT TO YOU We understand

WHO IS RESPONSIBLE FOR LOOKING AFTER YOUR PERSONAL DATA?

OVERVIEW of this Policy and Commitments to Privacy within Dual At Dual ("we", "us", "our"), we regularly collect and use information which may identify individuals ("personal data"), including insured

OVERVIEW of this Policy and Commitments to Privacy within Dual At Dual ("we", "us", "our"), we regularly collect and use information which may identify individuals ("personal data"), including insured

FY2018 Performance Review. April 25, 2018

FY2018 Performance Review April 25, 2018 Agenda Company Strategy Financial Performance Industry Overview 2 Agenda Company Strategy Financial Performance Industry Overview 3 Strategy: Market leadership

FY2018 Performance Review April 25, 2018 Agenda Company Strategy Financial Performance Industry Overview 2 Agenda Company Strategy Financial Performance Industry Overview 3 Strategy: Market leadership

$ 200 family deductible per benefit year for Major Medical benefits. Only applies to out-ofnetwork. $ No

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the policy or plan document at www.njcf.org or by calling 1-800-624-3096. Important Questions

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the policy or plan document at www.njcf.org or by calling 1-800-624-3096. Important Questions

Aadhaar Enabled Administration of Health Insurance in Sikkim, India. Pompy Sridhar 12 th International Microinsurance Conference 2016

Aadhaar Enabled Administration of Health Insurance in Sikkim, India Pompy Sridhar 12 th International Microinsurance Conference 2016 Agenda The following will be discussed What is Aadhaar Rationale for

Aadhaar Enabled Administration of Health Insurance in Sikkim, India Pompy Sridhar 12 th International Microinsurance Conference 2016 Agenda The following will be discussed What is Aadhaar Rationale for

Exposure Draft. 1. Short title and commencement

Exposure Draft IRDA (Issuance of Capital by General Insurance Companies) Regulations, 2012 In exercise of powers conferred under section 14 of the Insurance Regulatory and Development Authority Act, 1999

Exposure Draft IRDA (Issuance of Capital by General Insurance Companies) Regulations, 2012 In exercise of powers conferred under section 14 of the Insurance Regulatory and Development Authority Act, 1999

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain RISK MANAGEMENT CA. Pramod Jain Risks are potential events that

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain RISK MANAGEMENT CA. Pramod Jain Risks are potential events that

SIMPLIFIED INDEX INSURANCE LAW AND PRACTICE - DEC 2017 BASED ON LATEST ICSI MAT Professional Express Solutions CS RAHUL HARSH

CS PROFESSIONAL OPEN BOOK EXAM COMPLETE LIST OF ALL TOPICS SAVE TIME & GET ANSWERS QUICKLY! Full ICSI MAT available on this link:https://goo.gl/5l2h8e) This Simplified Index will be updated as and when

CS PROFESSIONAL OPEN BOOK EXAM COMPLETE LIST OF ALL TOPICS SAVE TIME & GET ANSWERS QUICKLY! Full ICSI MAT available on this link:https://goo.gl/5l2h8e) This Simplified Index will be updated as and when

ASSEMBLY BANKING AND INSURANCE COMMITTEE STATEMENT TO SENATE COMMITTEE SUBSTITUTE FOR. SENATE, No. 63 STATE OF NEW JERSEY DATED: MAY 5, 2003

ASSEMBLY BANKING AND INSURANCE COMMITTEE STATEMENT TO SENATE COMMITTEE SUBSTITUTE FOR SENATE, No. 63 STATE OF NEW JERSEY DATED: MAY 5, 2003 The Assembly Banking and Insurance Committee reports favorably

ASSEMBLY BANKING AND INSURANCE COMMITTEE STATEMENT TO SENATE COMMITTEE SUBSTITUTE FOR SENATE, No. 63 STATE OF NEW JERSEY DATED: MAY 5, 2003 The Assembly Banking and Insurance Committee reports favorably