Berneta L. Haynes Director of Equity and Access Georgia Watch

|

|

|

- Kristopher Walker

- 6 years ago

- Views:

Transcription

1 Berneta L. Haynes Director of Equity and Access Georgia Watch

2 Our organization Founded in 2002 Statewide advocacy organization Non-profit and non- partisan Our work Ensure consumers get a fair shake Trusted resource for elected officials, the public, and the media Empower consumers through outreach and education Offer a toll-free Consumer Hotline Our issues Health Access Program Financial Literacy Consumer Energy Program Access to Civil Justice

3 Georgia Watch focuses on a wide range of healthcare access issues, including: Advocates for equitable access to healthcare» Providing practical information for managing medical bills (e.g. dealing with surprise medical bills, navigating health insurance, and seeking financial assistance)» Promoting hospital accountability» Engaging in policy work to minimize surprise medical bills Designs educational programs and workshops on medical billing and debt Works with partners to support legislation and efforts that would ensure healthcare access to Georgians

4 1) Introduction 2) Before You Make a Doctor s Appointment 3) Explanation of Benefits (EOB) Statements 4) Reading Your Medical Bill 5) Medical Debt and Your Credit Report 6) Filing an Appeal with Your Insurer 7) Paying Your Medical Bills 8) Filing for Bankruptcy 9) Debt Collection and Your Rights 10) Conclusion

5 The information provided is not a substitute for legal advice. Georgia Watch encourages anyone in need of help on these matters to seek legal counsel.

6 » Bad news Healthcare costs are higher than they have been in 50 years Consumers are paying higher and higher health insurance premiums and out-of-pocket medical expenses Healthcare costs are a struggle for both uninsured and insured consumers Increased healthcare costs medical debt Healthcare costs are the #1 reason people file bankruptcy

7 » Good News Medical debt is not beyond your control You can learn to manage and minimize your medical debt The Georgia Consumer Guide for Medical Bills and Debt helps consumers find answers to some of the most complex questions associated with medical billing and debt

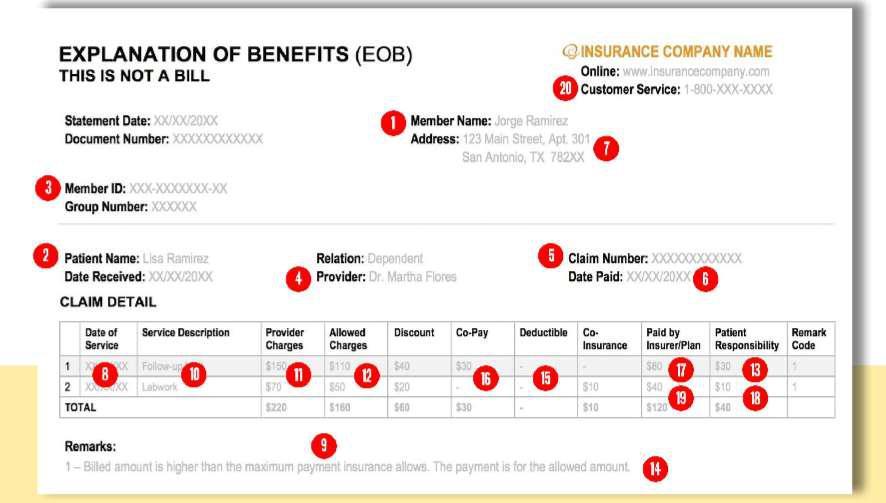

8 » You have a right to get clear, simple financial information about your healthcare services and bills.» Ask questions and get answers!

9 Before you schedule a doctor s appointment, you should ask your insurer which of the following? a. Is the healthcare service free? b. Is there a co-pay or deductible? c. Both a and b.

10 » Is the healthcare service free? Preventive» Free services : screenings, check-ups, and patient counseling to prevent illnesses, disease, or other health problems.» Is there a co-pay or deductible?

before your health insurance begins to pay.")

11 Deductible How much you owe for services (that your insurance covers) before your health insurance begins to pay. Co-Pay A fixed amount that you pay for covered healthcare services or prescriptions, usually when you receive the service. Ex. If your deductible is $500, then your plan won't pay until you've met the $500 deductible. Many plans have separate in-network and out-of-network deductibles. Ex. $25 for a visit to doctor's office. This amount can vary by the type of covered healthcare service.

rates.")

12 In-Network Out-of- Network The healthcare provider has contracted with your insurance company to accept certain negotiated (i.e. discounted) rates. The healthcare provider has not contracted with your insurance company to accept certain negotiated (i.e. discounted) rates. You may be responsible for additional costs.

13 Ask how much the service will cost. You have the right to ask about healthcare charges before you visit a doctor. This is particularly important if you don't have insurance. If the service will involve outside labs or doctors, be sure to find out whether those providers are innetwork with your insurance plan. Compare costs. Use trustworthy websites like HealthcareBluebook.com and FairHealthConsumer.org to compare costs. Ask about the rate for insured patients. Patients with insurance are charged less. If you are uninsured, ask for the rate that insured in-network patients pay for the same care, and ask to have your rate lowered.

14 After your appointment, your doctor mails you an Explanation of Benefits (EOB) statement. True False

15 » EOB statement is NOT a bill» FAQs about EOBs Insurance company mails it to you Explains how much your healthcare provider is charging your insurer Explains how much the insurer will pay Explains how much you have paid or may have to pay (usually your co-pay, deductible, or any other balance due)

16 » Patient name» Enrollee name» Patient number» Claim number» Date of service» Place of service» Customer Service» CPT codes» Reason codes» Date of process» Charge amount» Allowed amount» Payment amount» Due from patient

17

18 » Compare the EOB statement to your bill (if you receive a bill later). There should be no differences or duplicate charges If you see differences or errors, you will need to contact your insurance and perhaps your provider» Keep your EOB statement. Store and file it for at least a year» Shred old ones to protect your personal information

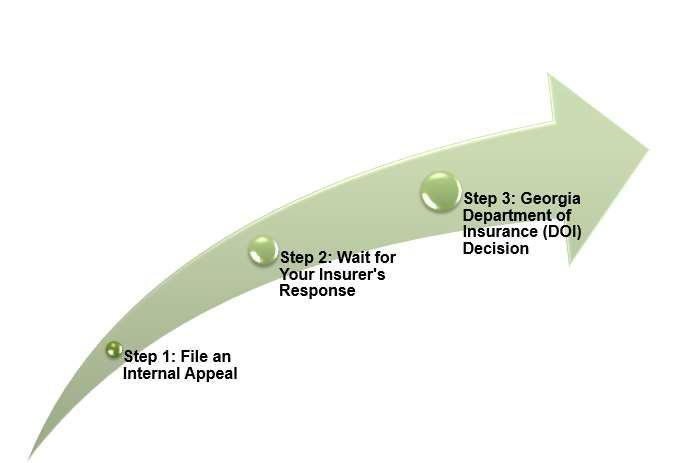

19 Is there an error in your statement? Call your insurance company's customer service number (listed on the EOB). Tell them your concerns. Did your insurer tell you to follow up with your provider? Follow your insurer's advice and call your provider's billing department. Do you suspect fraud? (e.g. upcoding, unbundled fees, billing for unnecessary services or services you did not receive, etc.)* Contact your insurance company's antifraud department.

20 » You may receive a medical bill in the mail after you receive the EOB» Typical terms on your medical bill: Charge: amount the healthcare provider has decided to charge for the service(s) Amount Paid by Insurance: what your insurer paid to provider Balance Due: amount you now owe the provider Adjustment: amount the healthcare provider has agreed not to charge

21

22 » Who sent the bill? One care visit can lead to many different bills» Is the bill overdue? Take action as soon as possible» What is the bill for? If you don t know, call and ask for an explanation of the charge» What are the details of the bill? If unclear, ask for an itemized bill with CPT codes

23 » Are there errors in the bill? CPT codes in bill should be the same as the CPT codes in EOB statement» Look for common errors in the bill: Marked up supplies: gowns, gloves, etc Operating room overcharges: compare anesthesia record with your bill Unbundled fees and upcoding

24 » If I find a medical bill error Contact your medical provider s office Contact insurer Request corrected/adjusted bill Take detailed notes and keep records of phone calls (get a reference number for each call) Pay part of bill that s correct Check your credit report

25 Credit reporting agencies have to wait 60 days from the date a medical bill is past due before adding the debt to your credit report? True False

26 » Medical debt can appear on your credit report» Credit report: record of loan-paying history, credit cards, debt collections, etc» Lenders use these reports to make lending decisions

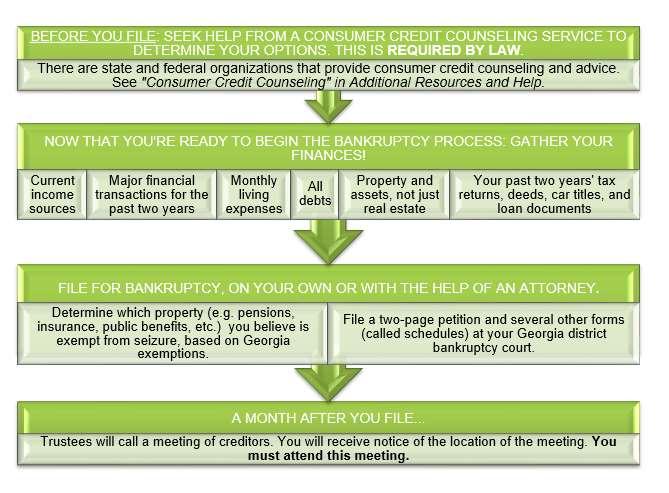

27 » Annual Credit Report online» Check your personal information Name, SS#, address, etc.» Unpaid medical debt is added to your credit report 180 days from the date a medical bill is past due This gives you time to receive and pay the bill» Debt should be removed after it s paid» You can file credit bureau dispute if there are errors

28 » You have the right to appeal a charge with your insurer if you think your insurer should have covered a service or item» Appeal: asking your insurer to reconsider its decision to not pay for a certain portion of your care» There are two levels of appeal

to file this appeal.")

29 1: Internal Appeal 2: External Appeal Your insurer reviews its payment decision in a full and fair way. You have 180 days (from the time you find out your claim been denied) to file this appeal. If the insurer still decides they will not pay for the service, then you can ask the Georgia Department of Insurance review your claim. You have 60 days from the results of the internal appeal to file this appeal.

30

31

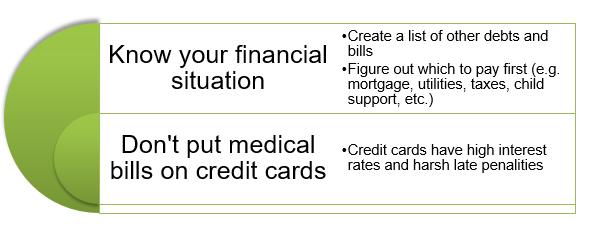

32 If you can t afford to pay the bill, call your provider and negotiate to pay a lower amount. Keep these things in mind:

33 Nonprofit hospitals have financial assistance policies to help you pay your medical bills. True False

34

35 Getting help paying your bill:» Indigent Care Trust Fund (ICTF)» Department of Community Health» Retroactive Medicaid Eligibility» Hospital s bill assistance webpage» Legal services consumer assistance programs Remember» You have rights!

36 » Bankruptcy: federal court process to help consumers eliminate their debts or repay them» Types of bankruptcy: Chapter 7 and Chapter 13 Chapter 7 No minimum amount of debt you must have in order to file. You have to file in court. The court erases almost all of your debts, and on the day you file. But not so fast! You might still have to sell some property and assets to pay creditors. Chapter 13 Designed for people with stable incomes who believe they can repay all their debts eventually. You have to file in court. The court does not erase your debts. Instead, the court creates a repayment plan to help you pay off your debts.

37

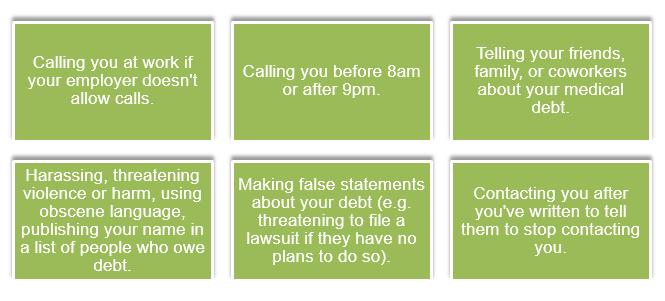

38 » Debt collector: A person or a company that regularly collects debts owed to others, usually when those debts are past due.» Federal and state laws exist to protect you from unfair, deceptive, or abusive debt collection practices.

39

40 » Other applicable laws Truth in Lending Act (TILA) Fair Credit Reporting Act (FCRA)» Helpful resources National Consumer Law Center: Disputing Errors in a Credit Report Consumer Financial Protection Bureau (CFPB) Federal Trade Commission (FTC) Atlanta Legal Aid

41 » Medical debt is not beyond your control» You can learn to manage and minimize your medical debt» You have rights! Georgia Watch s medical debt guide is available on our website at Contact Berneta L. Haynes (bhaynes@georgiawatch.org) for more information or if you would like to receive hard copies of the guide.

42

Understanding Your Medical Bill

Understanding Your Medical Bill After you visit a provider, you ll typically receive a bill telling you how much you have to pay. Providers can include healthcare professionals, hospitals and other types

Understanding Your Medical Bill After you visit a provider, you ll typically receive a bill telling you how much you have to pay. Providers can include healthcare professionals, hospitals and other types

Financial Literacy Course. East High School Module 9

Financial Literacy Course East High School Module 9 What will you learn about? Identity Theft and Consumer Fraud Protecting Against and Identity Theft and Consumer Fraud Fair Debt Collection Practices

Financial Literacy Course East High School Module 9 What will you learn about? Identity Theft and Consumer Fraud Protecting Against and Identity Theft and Consumer Fraud Fair Debt Collection Practices

Managing Medical Debt

Managing Medical Debt Foundation Communities Financial Coaching Program July 28, 2017 Many clients have unpaid medical bills and medical collections. Today we will discuss how to help clients with outstanding

Managing Medical Debt Foundation Communities Financial Coaching Program July 28, 2017 Many clients have unpaid medical bills and medical collections. Today we will discuss how to help clients with outstanding

Volume 2 Your Credit Report and Your Rights

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

The Missouri SMP. Empowering Seniors to Prevent Healthcare Fraud

The Missouri SMP Empowering Seniors to Prevent Healthcare Fraud SMP s Department of Health and Human Services Administration for Community Living/Administration on Aging Mission of the Missouri SMP Empower

The Missouri SMP Empowering Seniors to Prevent Healthcare Fraud SMP s Department of Health and Human Services Administration for Community Living/Administration on Aging Mission of the Missouri SMP Empower

Consumer Finance Protection Bureau. About this presentation. The CFPB 1/26/2012

Consumer Finance Protection Bureau Annual Conference Coalition of Higher Education Assistance Organizations John Dean Washington Partners, LLC January 2012 About this presentation This presentation is

Consumer Finance Protection Bureau Annual Conference Coalition of Higher Education Assistance Organizations John Dean Washington Partners, LLC January 2012 About this presentation This presentation is

Do yourself a favor and save some money, too. Don t believe these statements.

CREDIT REPAIR: Help Yourself You see the advertisements in newspapers, on TV, and on the Internet. You hear them on the radio. You get fliers in the mail. You may even get calls from telemarketers offering

CREDIT REPAIR: Help Yourself You see the advertisements in newspapers, on TV, and on the Internet. You hear them on the radio. You get fliers in the mail. You may even get calls from telemarketers offering

lesson nine in trouble overheads

lesson nine in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

lesson nine in trouble overheads why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies Materialism

Presentation Slides. Lesson Nine. In Trouble 04/09

Presentation Slides $ Lesson Nine In Trouble 04/09 why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies

Presentation Slides $ Lesson Nine In Trouble 04/09 why consumers don t pay loss of income (48%) Unemployment (24%) Illness (16%) Other (divorce, death) (8%) overextension (25%) Poor money management Emergencies

ACA Implementation: Status Update

ACA Implementation: Status Update National Academy of Sciences Roundtable on Health Literacy July 21, 2016 Karen Pollitz, Senior Fellow Kaiser Family Foundation Figure 1 Eligibility Status of 32.9 million

ACA Implementation: Status Update National Academy of Sciences Roundtable on Health Literacy July 21, 2016 Karen Pollitz, Senior Fellow Kaiser Family Foundation Figure 1 Eligibility Status of 32.9 million

Your Money, Your Goals Spotlight Series. Understanding credit reports and scores: An in-depth look

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

Essential Standard Understand business credit and risk management.

Essential Standard 5.00 Understand business credit and risk management. 1 Objective 5.01 Understand credit management 2 3 Topics Main types of credit Common advantages and disadvantages of businesses using

Essential Standard 5.00 Understand business credit and risk management. 1 Objective 5.01 Understand credit management 2 3 Topics Main types of credit Common advantages and disadvantages of businesses using

Maximizing Purchasing Power: Make the Most of Your Credit Score

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

Is There Such a Thing as Legal Credit Repair?

Is There Such a Thing as Legal Credit Repair? Not only does the legal credit repair process work for errors but can also help remove "unverifiable" negative, yet accurate, information. Credit Laws Fair

Is There Such a Thing as Legal Credit Repair? Not only does the legal credit repair process work for errors but can also help remove "unverifiable" negative, yet accurate, information. Credit Laws Fair

Billing and Collections Knowledge Assessment

Billing and Collections Knowledge Assessment Message to the manager who may use this assessment tool: All or portions of the following questions can be used for interviewing/assessing candidates for open

Billing and Collections Knowledge Assessment Message to the manager who may use this assessment tool: All or portions of the following questions can be used for interviewing/assessing candidates for open

List of Insurance Terms and Definitions for Uniform Translation

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

How to Dispute Credit Report Errors

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 www.ftc.gov 1-877-ftc-help How to Dispute Credit Report Errors Y our credit report contains information about where you live,

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 www.ftc.gov 1-877-ftc-help How to Dispute Credit Report Errors Y our credit report contains information about where you live,

CLARIFYING INSURANCE CLAIMS What is an Insurance Claim?

CLARIFYING INSURANCE CLAIMS What is an Insurance Claim? Often those in the scleroderma community find themselves frequenting health care providers and being left with mounds of invoices and bills. Medical

CLARIFYING INSURANCE CLAIMS What is an Insurance Claim? Often those in the scleroderma community find themselves frequenting health care providers and being left with mounds of invoices and bills. Medical

Glossary of Terms. Adjudication: The way a health plan decides how much it will pay for certain expenses.

Page 1 Glossary of Terms Adjudication: The way a health plan decides how much it will pay for certain expenses. Affordable Care Act (ACA): The comprehensive health care reform law enacted in March 2010.

Page 1 Glossary of Terms Adjudication: The way a health plan decides how much it will pay for certain expenses. Affordable Care Act (ACA): The comprehensive health care reform law enacted in March 2010.

Insurance Rights for Cancer Survivors. Bobbi Meins, M.S. Director UBC Cancer Rehab Centers

Insurance Rights for Cancer Survivors Bobbi Meins, M.S. Director UBC Cancer Rehab Centers 800-562-6900 Over the last 12 months Regardless of what you think about Obamacare, there are some good things

Insurance Rights for Cancer Survivors Bobbi Meins, M.S. Director UBC Cancer Rehab Centers 800-562-6900 Over the last 12 months Regardless of what you think about Obamacare, there are some good things

MODULE 7: Borrowing Basics PARTICIPANT GUIDE

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

Billing and Collections Knowledge Assessment

Billing and Collections Knowledge Assessment Message to the manager who may use this assessment tool: All or portions of the following questions can be used for interviewing/assessing candidates for open

Billing and Collections Knowledge Assessment Message to the manager who may use this assessment tool: All or portions of the following questions can be used for interviewing/assessing candidates for open

Financial Assistance & Debt Crisis Intervention

Financial Assistance & Debt Crisis Intervention Patient Advocate Foundation 700 Thimble Shoals Blvd. Suite 200 Newport News, VA 23606 (800) 532-5274 EMAIL: info@patientadvocate.org INTERNET: www.patientadvocate.org

Financial Assistance & Debt Crisis Intervention Patient Advocate Foundation 700 Thimble Shoals Blvd. Suite 200 Newport News, VA 23606 (800) 532-5274 EMAIL: info@patientadvocate.org INTERNET: www.patientadvocate.org

Teacher's Guide. Lesson Nine. In Trouble 04/09

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Teacher's Guide $ Lesson Nine In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Assurant Clarity SM. Questions about your plan? Benefits Guide. Time Insurance Company John Alden Life Insurance Company. Finally, Original Thinking

Assurant Clarity SM Benefits Guide Finally, Original Thinking Questions about your plan? Call your Front Desk team at 888.345.6007 Time Insurance Company John Alden Life Insurance Company Assurant Health

Assurant Clarity SM Benefits Guide Finally, Original Thinking Questions about your plan? Call your Front Desk team at 888.345.6007 Time Insurance Company John Alden Life Insurance Company Assurant Health

Coverage Determinations, Appeals and Grievances

Coverage Determinations, Appeals and Grievances Filing a grievance (making a complaint) about your prescription coverage Asking for a coverage determination (coverage decision) 60-day formulary change

Coverage Determinations, Appeals and Grievances Filing a grievance (making a complaint) about your prescription coverage Asking for a coverage determination (coverage decision) 60-day formulary change

Teacher's Guide. Lesson Thirteen. In Trouble 04/09

Teacher's Guide $ Lesson Thirteen In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Teacher's Guide $ Lesson Thirteen In Trouble 04/09 in trouble websites It's hard to admit and deal with debt or financial trouble. It can be a painful time, but students need to learn practical, beneficial

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Brought to you by the Missouri Association of Area Agencies on Aging (ma4).

.") Brought to you by the Missouri Association of Area Agencies on Aging (ma4). www.ma4web.org July/August 2014 1 The Missouri Association of Area Agencies on Aging (ma4) was founded in 1973 to serve as a

Brought to you by the Missouri Association of Area Agencies on Aging (ma4). www.ma4web.org July/August 2014 1 The Missouri Association of Area Agencies on Aging (ma4) was founded in 1973 to serve as a

Helping Older Americans Cope with Medical Debt

Helping Older Americans Cope with Medical Debt Cheryl Fish-Parcham, Families USA Chi Chi Wu, National Consumer Law Center Odette Williamson & Jessica Hiemenz National Consumer Law Center National Elder

Helping Older Americans Cope with Medical Debt Cheryl Fish-Parcham, Families USA Chi Chi Wu, National Consumer Law Center Odette Williamson & Jessica Hiemenz National Consumer Law Center National Elder

A Guide for Credit Grantors:

: Extending Credit, Managing your Company s Delinquent Accounts and When to Hire a Third-Party Debt Collector Consumer Credit The extension of credit to consumers and the resulting debt has steadily increased

: Extending Credit, Managing your Company s Delinquent Accounts and When to Hire a Third-Party Debt Collector Consumer Credit The extension of credit to consumers and the resulting debt has steadily increased

Subject HHS Commentary From Preamble Regulatory Provision Agent Specific Provisions Definition of Agent/Broker

National Association of Health Underwriters Overview of Provisions in the Proposed Federal Rule on the Establishment of Exchanges and Qualified Health Plans (Released on July 11, 2011) of Specific Interest

National Association of Health Underwriters Overview of Provisions in the Proposed Federal Rule on the Establishment of Exchanges and Qualified Health Plans (Released on July 11, 2011) of Specific Interest

Your Money, Your Goals too. Financial empowerment toolkit

Your Money, Your Goals too Financial empowerment toolkit DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It does not constitute

Your Money, Your Goals too Financial empowerment toolkit DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It does not constitute

SECTION SUMMARY EFFECTIVE DATE Section 101. Minimum Standards for Residential Mortgage Loans

SECTION SUMMARY EFFECTIVE DATE Section 101. Minimum Standards for Residential Mortgage Loans Section 103. Access to Affordable Mortgages. Section 104. Home Mortgage Disclosure Act Adjustment and Study

SECTION SUMMARY EFFECTIVE DATE Section 101. Minimum Standards for Residential Mortgage Loans Section 103. Access to Affordable Mortgages. Section 104. Home Mortgage Disclosure Act Adjustment and Study

More Than Just a DIGITAL SPRING Band-Aid CLEANING. Connie Alarcon

More Than Just a DIGITAL SPRING Band-Aid CLEANING Connie Alarcon Agenda BBB Services Complaints Check BBB Scams Health Care Fraud & Abuse Medical Identity Theft Phone Scams Better Business Bureau BBB Serving

More Than Just a DIGITAL SPRING Band-Aid CLEANING Connie Alarcon Agenda BBB Services Complaints Check BBB Scams Health Care Fraud & Abuse Medical Identity Theft Phone Scams Better Business Bureau BBB Serving

USAACE & Fort Rucker Preventative Law Program. Debt Collection

USAACE & Fort Rucker Preventative Law Program Debt Collection THIS PAMPHLET contains basic information on this particular legal topic for your general information. If you have specific questions, contact

USAACE & Fort Rucker Preventative Law Program Debt Collection THIS PAMPHLET contains basic information on this particular legal topic for your general information. If you have specific questions, contact

Eligibility and Point of Service Collection Practices that Work

Eligibility and Point of Service Collection Practices that Work Douglas Turek Senior VP of Regulatory and Governmental Affairs MedData (formerly Cardon Outreach and Alegis) TAHFA Roadshow Dallas, Texas

Eligibility and Point of Service Collection Practices that Work Douglas Turek Senior VP of Regulatory and Governmental Affairs MedData (formerly Cardon Outreach and Alegis) TAHFA Roadshow Dallas, Texas

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Amy Bingham, Compliance Director Reviewed Only Date: 6/05,1/31/2011, 1/24/2012 Supersedes and replaces: "CC-02 - Anti-

MOLINA HEALTHCARE Polic:y and Procedure No. C 08 of Utah Effective Date: November 2003 Reviewed and Revised Ollie: 2/6/08; 2/25/0S; 11 /5/0S; II/ IS/OS, 3/4/09, 6/9/09, S/31 / 1O Amy Bingham, Compliance

MOLINA HEALTHCARE Polic:y and Procedure No. C 08 of Utah Effective Date: November 2003 Reviewed and Revised Ollie: 2/6/08; 2/25/0S; 11 /5/0S; II/ IS/OS, 3/4/09, 6/9/09, S/31 / 1O Amy Bingham, Compliance

Understanding the Insurance Process

Understanding the Insurance Process This summary provides an overview of the health insurance process. Health insurance falls into two major categories: commercial insurance and government insurance. Commercial

Understanding the Insurance Process This summary provides an overview of the health insurance process. Health insurance falls into two major categories: commercial insurance and government insurance. Commercial

Having a Problem with a Debt Collector? You Also Have Protections

DEALING WITH DEBT Having a Problem with a Debt Collector? You Also Have Protections Debt collection problems are among the most common complaints received by the FDIC and the Consumer Financial Protection

DEALING WITH DEBT Having a Problem with a Debt Collector? You Also Have Protections Debt collection problems are among the most common complaints received by the FDIC and the Consumer Financial Protection

Chapter 8. Your rights and responsibilities

Chapter 8: Your rights and responsibilities 1 Chapter 8. Your rights and responsibilities SECTION 1 Our plan must honor your rights as a member of the plan... 1 Section 1.1 We must provide information

Chapter 8: Your rights and responsibilities 1 Chapter 8. Your rights and responsibilities SECTION 1 Our plan must honor your rights as a member of the plan... 1 Section 1.1 We must provide information

Private Loan Guide. Apply for free, federal and state financial aid programs:

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

A Guide to Health Insurance

A Guide to Health Insurance Your health matters. A healthier you makes a healthier Cleveland! Healthy Cleveland Insurance Guide Dial Dial Acknowledgements On behalf of the City of Cleveland Department

A Guide to Health Insurance Your health matters. A healthier you makes a healthier Cleveland! Healthy Cleveland Insurance Guide Dial Dial Acknowledgements On behalf of the City of Cleveland Department

THE AFFORDABLE CARE ACT & TAXES. A resource for VITA & AARP tax preparers in Georgia

THE AFFORDABLE CARE ACT & TAXES A resource for VITA & AARP tax preparers in Georgia Empowering Navigators and Tax Preparers to Serve Consumers in GA Atlanta Debrief Savannah Debrief Goals for Today 1)

THE AFFORDABLE CARE ACT & TAXES A resource for VITA & AARP tax preparers in Georgia Empowering Navigators and Tax Preparers to Serve Consumers in GA Atlanta Debrief Savannah Debrief Goals for Today 1)

RE: Billing and Collection Policy and Procedure. PREPARED BY: Linda Fausett REVISION DATE: 06/14/2018

Page 1 of 6 The online (server) version of this policy is official. Therefore, all printed versions of this document are unofficial copies. APPLING HEALTHCARE SYSTEM 163 EAST TOLLISON STREET BAXLEY, GEORGIA

Page 1 of 6 The online (server) version of this policy is official. Therefore, all printed versions of this document are unofficial copies. APPLING HEALTHCARE SYSTEM 163 EAST TOLLISON STREET BAXLEY, GEORGIA

One to One Newsletter

One to One Newsletter DENTAL SUMMER EDITION Blue Cross of Idaho has been busy since the beginning of the year. Much of the information this quarter is important for appropriate coding, getting good information

One to One Newsletter DENTAL SUMMER EDITION Blue Cross of Idaho has been busy since the beginning of the year. Much of the information this quarter is important for appropriate coding, getting good information

Product User Guide It s Your Credit. Keep It That Way with 5LINX Safe Score.

Product User Guide It s Your Credit. Keep It That Way with 5LINX Safe Score. Features & Benefits Identity Verification Credit Monitoring Score Simulator Full Access to Credit Reports Score Tracker Resource

Product User Guide It s Your Credit. Keep It That Way with 5LINX Safe Score. Features & Benefits Identity Verification Credit Monitoring Score Simulator Full Access to Credit Reports Score Tracker Resource

Getting Delinquent Accounts to Pay Up. Presented by Larry Holmes

Getting Delinquent Accounts to Pay Up Presented by Larry Holmes Overview 1. Writing a good collection policy 2. Elements of a collection call 3. Handling the no money excuse 4. 5 techniques for collection

Getting Delinquent Accounts to Pay Up Presented by Larry Holmes Overview 1. Writing a good collection policy 2. Elements of a collection call 3. Handling the no money excuse 4. 5 techniques for collection

A Guide for Credit Grantors

A Guide for Credit Grantors Extending Credit, Managing Your Company s Delinquent Accounts and When to Hire a Third-Party Debt Collector Consumer Credit The extension of credit to consumers and the resulting

A Guide for Credit Grantors Extending Credit, Managing Your Company s Delinquent Accounts and When to Hire a Third-Party Debt Collector Consumer Credit The extension of credit to consumers and the resulting

My Medicare Options Workbook

My Medicare Options Workbook This workbook will walk you through the process of deciding what steps you need to take now that you are eligible for Medicare. Table of Contents Introduction... 3 Where do

My Medicare Options Workbook This workbook will walk you through the process of deciding what steps you need to take now that you are eligible for Medicare. Table of Contents Introduction... 3 Where do

2. To earn as much interest as possible, you should open a savings account that earns () interest Hide answers

interest Hide answers") 1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

Personal Finance Unit 2 Chapter Glencoe/McGraw-Hill

0 Chapter 6 Consumer Credit What You ll Learn Section 6.1 Explain the meaning of consumer credit. Differentiate between closed-end credit and openend credit. Section 6.2 Name the five C s of credit. Identify

0 Chapter 6 Consumer Credit What You ll Learn Section 6.1 Explain the meaning of consumer credit. Differentiate between closed-end credit and openend credit. Section 6.2 Name the five C s of credit. Identify

Chapter 27. Your Credit and the Law pp

Your Credit and the Law pp. 434-447 Learning Objectives After completing this chapter, you ll be able to: 1. Explain how government protects credit rights. 2. Name federal laws that protect consumers.

Your Credit and the Law pp. 434-447 Learning Objectives After completing this chapter, you ll be able to: 1. Explain how government protects credit rights. 2. Name federal laws that protect consumers.

Fair Debt Collection Practices

Fair Debt Collection Practices Scott Daugherty, President/General Counsel A UBA Company Introduction Wouldn t it be great if every loan we ever made was paid on time, as agreed, through maturity? Unfortunately,

Fair Debt Collection Practices Scott Daugherty, President/General Counsel A UBA Company Introduction Wouldn t it be great if every loan we ever made was paid on time, as agreed, through maturity? Unfortunately,

It is determined that a patient does not have adequate financial resources to pay for services rendered at MGH.

POLICY: As part of the mission of Monongalia General Hospital (MGH), promotion of health, relief of burdens of government, and volunteer and community services shall be implemented in a reasonable manner

POLICY: As part of the mission of Monongalia General Hospital (MGH), promotion of health, relief of burdens of government, and volunteer and community services shall be implemented in a reasonable manner

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

YOUR MONEY, YOUR GOALS. A financial empowerment toolkit

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

YOUR MONEY, YOUR GOALS A financial empowerment toolkit Consumer Financial Protection Bureau December 2016 About the Consumer Financial Protection Bureau The Consumer Financial Protection Bureau (CFPB)

Your guide to your health plan

Health Plan, Inc. Your guide to your health plan Welcome to Presbyterian. We are glad to have you as a member, and we look forward to being your partner in good health. In this booklet you will find essential

Health Plan, Inc. Your guide to your health plan Welcome to Presbyterian. We are glad to have you as a member, and we look forward to being your partner in good health. In this booklet you will find essential

Chapter 07. Sources of Consumer Credit. Chapter 7 Learning Objectives. Choosing a Source of Credit: The of Credit Alternatives

Chapter 07 Choosing a Source of Credit: The of Credit Alternatives McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 7-1 Chapter 7 Learning Objectives 1. Analyze

Chapter 07 Choosing a Source of Credit: The of Credit Alternatives McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 7-1 Chapter 7 Learning Objectives 1. Analyze

INSTALLATION AND USE OF CREDIT-AID SOFTWARE

1 TABLE OF CONTENTS INSTALLATION AND USE OF CREDIT-AID SOFTWARE... 3 INTRODUCTION FROM THE CREDIT DOCTOR... 4 YOUR CREDIT REPORTS... 7 CREDIT SCORING... 8 ORDERING COPIES OF YOUR CREDIT REPORTS... 9 REVIEWING

1 TABLE OF CONTENTS INSTALLATION AND USE OF CREDIT-AID SOFTWARE... 3 INTRODUCTION FROM THE CREDIT DOCTOR... 4 YOUR CREDIT REPORTS... 7 CREDIT SCORING... 8 ORDERING COPIES OF YOUR CREDIT REPORTS... 9 REVIEWING

Debt getting in your way? Get a handle on it.

Debt getting in your way? Get a handle on it. Bureau of Consumer Financial Protection Your Money, Your Goals About the Bureau The Bureau of Consumer Financial Protection regulates the offering and provision

Debt getting in your way? Get a handle on it. Bureau of Consumer Financial Protection Your Money, Your Goals About the Bureau The Bureau of Consumer Financial Protection regulates the offering and provision

c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:](/thumbs/76/73531259.jpg "c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:") The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

FAQ: Federal Regulations and Coding Compliance

Question 1: Why is coding compliance important? Answer 1: Coding compliance is part of the overall effort of medical practices to comply with regulations in the coding area. Compliant claims are an indication

Question 1: Why is coding compliance important? Answer 1: Coding compliance is part of the overall effort of medical practices to comply with regulations in the coding area. Compliant claims are an indication

A CONSUMER S GUIDE TO CANCER INSURANCE

A CONSUMER S GUIDE TO CANCER INSURANCE WHAT IS CANCER INSURANCE? Cancer insurance provides benefits only if you are diagnosed with cancer, as defined by the terms of the policy contract. These policies

A CONSUMER S GUIDE TO CANCER INSURANCE WHAT IS CANCER INSURANCE? Cancer insurance provides benefits only if you are diagnosed with cancer, as defined by the terms of the policy contract. These policies

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Written by Credit Doctor, author of Credit-Aid Software the Award-winning Credit Repair Software Kit. Table of Contents (Click to view)

") Boost your FICO Score in 7 Easy Steps! Tricks of the trade the Pro s use to Boost your Credit Score FAST! These are the Credit Repair Secrets the banks don t want you to know Written by Credit Doctor,

Boost your FICO Score in 7 Easy Steps! Tricks of the trade the Pro s use to Boost your Credit Score FAST! These are the Credit Repair Secrets the banks don t want you to know Written by Credit Doctor,

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

Chapter 9 Credit Problems and Laws. Copyright 2007 Thomson South-Western

Chapter 9 Credit Problems and Laws Copyright 2007 Thomson South-Western Errors and Fraud Recourse is a remedy for unfair treatment Credit to your account Replacement for damaged goods Disputing charges

Chapter 9 Credit Problems and Laws Copyright 2007 Thomson South-Western Errors and Fraud Recourse is a remedy for unfair treatment Credit to your account Replacement for damaged goods Disputing charges

Legal Aid Society of Hawai`i. What You Need To Know About Student Loans

Legal Aid Society of Hawai`i What You Need To Know About Student Loans This brochure provides basic information about student loans. It provides information on: C defaulted student loans, C delinquent

Legal Aid Society of Hawai`i What You Need To Know About Student Loans This brochure provides basic information about student loans. It provides information on: C defaulted student loans, C delinquent

You must pay all the costs up to the deductible amount before this plan. covered services after you meet the deductible.

Secure Choice Health Savings Account Partner Coverage Period: Beginning on or after 01-01-2016 Summary of Benefits and Coverage: What this Plan covers & What it Costs Coverage for: S, S+1, and Family coverage

Secure Choice Health Savings Account Partner Coverage Period: Beginning on or after 01-01-2016 Summary of Benefits and Coverage: What this Plan covers & What it Costs Coverage for: S, S+1, and Family coverage

COUNTRYTELL FINANCIAL HARDSHIP POLICY

(annexing Summary of Financial Hardship Policy see Schedule B) 1. INTRODUCTION This is Countrytell s Financial Hardship Policy. We understand that financial hardship can make it difficult for some customers

(annexing Summary of Financial Hardship Policy see Schedule B) 1. INTRODUCTION This is Countrytell s Financial Hardship Policy. We understand that financial hardship can make it difficult for some customers

U.S. Railroad Retirement Board MEDICARE. For Railroad Workers and Their Families

U.S. Railroad Retirement Board www.rrb.gov MEDICARE For Railroad Workers and Their Families U.S. Railroad Retirement Board Mission Statement The Railroad Retirement Board s mission is to administer retirement/survivor

U.S. Railroad Retirement Board www.rrb.gov MEDICARE For Railroad Workers and Their Families U.S. Railroad Retirement Board Mission Statement The Railroad Retirement Board s mission is to administer retirement/survivor

CREDIT COUNSELING REQUIREMENT

CREDIT COUNSELING REQUIREMENT In order to file bankruptcy, an individual must receive from an approved nonprofit budget and credit counseling agency... an individual or group briefing... that outlines

CREDIT COUNSELING REQUIREMENT In order to file bankruptcy, an individual must receive from an approved nonprofit budget and credit counseling agency... an individual or group briefing... that outlines

SIP Connect Financial Hardship Policy

SIP Connect Financial Hardship Policy 1) Introduction This is SIP Connects Financial Hardship Policy. We understand that financial hardship can make it difficult for some customers to pay their bills.

SIP Connect Financial Hardship Policy 1) Introduction This is SIP Connects Financial Hardship Policy. We understand that financial hardship can make it difficult for some customers to pay their bills.

Take control of your auto loan

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

Choosing a Medigap Policy:

C E N T E R S F O R M E D I C A R E & M E D I C A I D S E R V I C E S 2016 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information

C E N T E R S F O R M E D I C A R E & M E D I C A I D S E R V I C E S 2016 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information

Rebuilding YOUR CREDIT. Leader s Guide

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

October is Credit Month at Taylor Financial Group

Taylor Financial Group s Monthly Planning Letter October 017 Are you turning 65? The Medicare open enrollment period runs from October 15, 017 through December 7, 017. Learn more in this month s planning

Taylor Financial Group s Monthly Planning Letter October 017 Are you turning 65? The Medicare open enrollment period runs from October 15, 017 through December 7, 017. Learn more in this month s planning

Billing Guidelines Manual for Contracted Professional HMO Claims Submission

Billing Guidelines Manual for Contracted Professional HMO Claims Submission The Centers for Medicare and Medicaid Services (CMS) 1500 claim form is the acceptable standard for paper billing of professional

Billing Guidelines Manual for Contracted Professional HMO Claims Submission The Centers for Medicare and Medicaid Services (CMS) 1500 claim form is the acceptable standard for paper billing of professional

Get to know your benefits. State of Florida 2018 Benefits Guide. welcometouhc.com/florida

Get to know your benefits. State of Florida 2018 Benefits Guide welcometouhc.com/florida Knowing your benefits helps you make more informed choices. By understanding your benefits, you can select the coverage

Get to know your benefits. State of Florida 2018 Benefits Guide welcometouhc.com/florida Knowing your benefits helps you make more informed choices. By understanding your benefits, you can select the coverage

INDUSTRIAL COMMISSION OF ARIZONA

INDUSTRIAL COMMISSION OF ARIZONA WORKERS COMPENSATION INFORMATION FOR THE INJURED WORKER Phoenix Office: Industrial Commission of Arizona 800 W. Washington Street Phoenix, Arizona 85007-2922 Claims Phone:

INDUSTRIAL COMMISSION OF ARIZONA WORKERS COMPENSATION INFORMATION FOR THE INJURED WORKER Phoenix Office: Industrial Commission of Arizona 800 W. Washington Street Phoenix, Arizona 85007-2922 Claims Phone:

Fixing Bad Credit and Solving Credit Problems 1

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

FCS 5049 Fixing Bad Credit and Solving Credit Problems 1 Mary N. Harrison 2 When you want to buy a car, a house, or other expensive items you probably expect to use credit. For smaller purchases, your

What s New for Stage 1 in 2014

The problem Your Accounting for a New Economy What s New for Stage 1 in 2014 Medical identity is now the fastest-growing type of identity theft in the world and Texas has become the fourth highest identity

The problem Your Accounting for a New Economy What s New for Stage 1 in 2014 Medical identity is now the fastest-growing type of identity theft in the world and Texas has become the fourth highest identity

Your Money, Your Goals Spotlight Series. Dealing with debt: A closer look

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

Patient Billing and Financial Services

Patient Billing and Financial Services UNDERSTANDING YOUR OBLIGATIONS BAYHEALTH.ORG We realize this can be a stressful time for you and your family. We particularly understand how frustrating it can be

Patient Billing and Financial Services UNDERSTANDING YOUR OBLIGATIONS BAYHEALTH.ORG We realize this can be a stressful time for you and your family. We particularly understand how frustrating it can be

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

Laura Mackie Mortgages. A Guide to Understanding and Rebuilding Your Credit Score

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

Laura Mackie Mortgages Your Credit Report A Guide to Understanding and Rebuilding Your Credit Score Introduction This guide is intended to help you improve your credit score and provide you with information

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

Your HIPnation Primary Care Physician is truly a concierge service.

Patient Education How to Use HIPnation + New Era Indemnity Plan* HIPnation is a membership program that provides 24/7 access to your personal HIPnation Primary Care Physician. Your HIPnation Primary Care

Patient Education How to Use HIPnation + New Era Indemnity Plan* HIPnation is a membership program that provides 24/7 access to your personal HIPnation Primary Care Physician. Your HIPnation Primary Care

Student Activities. Lesson Nine. In Trouble 04/09

Student Activities $ Lesson Nine In Trouble 04/09 name: date: test your knowledge of trouble The following questions are designed to test what you ve just learned about dealing with financial woes. directions

Student Activities $ Lesson Nine In Trouble 04/09 name: date: test your knowledge of trouble The following questions are designed to test what you ve just learned about dealing with financial woes. directions

20 Steps to Financial Health:

20 Steps to Financial Health: Achieving Lifelong Financial Fitness American Consumer Credit Counseling 130 Rumford Avenue Auburndale, MA 02466 1.800.769.3571 ConsumerCredit.com On behalf of American Consumer

20 Steps to Financial Health: Achieving Lifelong Financial Fitness American Consumer Credit Counseling 130 Rumford Avenue Auburndale, MA 02466 1.800.769.3571 ConsumerCredit.com On behalf of American Consumer

POLICY: FINANCIAL ASSISTANCE, BILLING AND COLLECTIONS

SUBJECT: Financial Assistance, Billing and Collections ORIGINATED BY: Finance Department APPROVED BY: Administrative Staff LEGAL REVIEW: POLICY NO: DATE OF ORIGIN: 12/29/15 REVIEW DATES: 11/18/15 LATEST

SUBJECT: Financial Assistance, Billing and Collections ORIGINATED BY: Finance Department APPROVED BY: Administrative Staff LEGAL REVIEW: POLICY NO: DATE OF ORIGIN: 12/29/15 REVIEW DATES: 11/18/15 LATEST

Learning Series. Health Connector and MassHealth: Year-end tax filing process. Massachusetts HealthCare Training Forum (MTF) January 2018

January 2018") Learning Series Massachusetts HealthCare Training Forum (MTF) Health Connector and MassHealth: Year-end tax filing process January 2018 Agenda During this presentation, the following information will be

Learning Series Massachusetts HealthCare Training Forum (MTF) Health Connector and MassHealth: Year-end tax filing process January 2018 Agenda During this presentation, the following information will be

Your Rights and Responsibilities

Your Rights and Responsibilities 1-877-633-7943 24 hours a day/365 days a year TTY users dial 711 MGRX_18_WEBSITERIGHTSRESP SECTION 1 Our plan must honor your rights as a member of the plan ec 1.1 e must

Your Rights and Responsibilities 1-877-633-7943 24 hours a day/365 days a year TTY users dial 711 MGRX_18_WEBSITERIGHTSRESP SECTION 1 Our plan must honor your rights as a member of the plan ec 1.1 e must

CRCE Exam Study Manual Update for 2018

CRCE Exam Study Manual Update for 2018 This document reflects updates made to the instructional content from the Certified Revenue Cycle Executive (CRCE-I, CRCE-P) Exam Study Manual - 2017 to the 2018

CRCE Exam Study Manual Update for 2018 This document reflects updates made to the instructional content from the Certified Revenue Cycle Executive (CRCE-I, CRCE-P) Exam Study Manual - 2017 to the 2018

FTC Facts. For Consumers Federal Trade Commission. Credit Scoring Ever wonder how a creditor decides

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

Contractor Disclosure, Authorization & Consent for the Procurement of Consumer Reports

Contractor Disclosure, Authorization & Consent for the Procurement of Consumer Reports Section I: Disclosure (the Company ) may request background information about you from a consumer reporting agency

Contractor Disclosure, Authorization & Consent for the Procurement of Consumer Reports Section I: Disclosure (the Company ) may request background information about you from a consumer reporting agency

Your AARP Personal Guide to Buying Health Insurance. What you should know. BA9802 (3/06)

") Your AARP Personal Guide to Buying Health Insurance What you should know. BA9802 (3/06) A word from AARP Health Care Options AARP Health Care Options is happy to offer you this personal guide to buying

Your AARP Personal Guide to Buying Health Insurance What you should know. BA9802 (3/06) A word from AARP Health Care Options AARP Health Care Options is happy to offer you this personal guide to buying

Get to know your benefits. Bristol-Myers Squibb 2018 Benefits Guide. Annual Enrollment is OCTOBER 23RD NOVEMBER 10TH, 2017 welcometouhc.

Get to know your benefits. Bristol-Myers Squibb 2018 Benefits Guide Annual Enrollment is OCTOBER 23RD NOVEMBER 10TH, 2017 welcometouhc.com/bms Knowing your benefits helps you make more informed choices.

Get to know your benefits. Bristol-Myers Squibb 2018 Benefits Guide Annual Enrollment is OCTOBER 23RD NOVEMBER 10TH, 2017 welcometouhc.com/bms Knowing your benefits helps you make more informed choices.