Vice President and Chief Actuary CLHIA

|

|

|

- Hillary Hall

- 5 years ago

- Views:

Transcription

1 1

2 TITLE Presentation Points Steve Additional Easson, Points FCIA, FSA, CFA Additional Points Vice President and Chief Actuary CLHIA 2

3 TITLE AGENDA Presentation Points 1. Regulatory Additional (and Points Supervisory) Convergence Why and How? Additional Points 2. Global Regulatory Convergence Themes Global Supervision, Solvency Standards, ORSA, Economic Balance Sheet, Eligible Capital 3. Canadian Implications and Views Selected Issues Balanced approach adopting International Standards Supervision, Solvency Standards, Reinsurance 3

4 Regulatory Convergence Why? International Financial Crisis G20 / Finance Ministers / Financial Stability Board (FSB) Canada Member of G20 and FSB Global comparability IAIS Adherence/Cooperation Trend to more risk-based/ principles based standards Advances in actuarial and capital theory; increased complexity and globalization of products Convergence among Sectors Consistency: insurers and banks 5

5 Regulatory Convergence How? International IAIS Insurance Core Principles, Standards, Guidance Supervision IAIS, Solvency II Solvency Standards IAIS, Solvency II, NAIC Reinsurance IAIS, Solvency II, NAIC Canada Acts and Regulations, Guidelines, Advisories, Application Guides, Consultations, Supervisory Practices, Industry Notices OSFI s Feb 2011 revision to Supervisory Framework Life Insurer Solvency Assessment Framework (Standard and Advanced Approaches) Reinsurance Response Paper ; Guideline B-3; Guidance on RSAs

6 Regulatory Convergence How? IAIS Insurance Core Principles (ICP s) Feb pages! Introduction ICP 1 Objectives, powers and responsibilities of the supervisor ICP 2 Supervisor ICP 3 Information exchange ICP 4 Licensing ICP 5 Suitability of Persons. ICP 6 Changes in control and portfolio transfers ICP 7 Corporate Governance ICP 8 Risk Management and Internal Controls ICP 9 Supervisory review and reporting ICP 10 Preventive and corrective measures ICP 11 Enforcement ICP 12 Winding-up and exit from the market ICP 13 Reinsurance and Other Forms of Risk Transfer ICP 14 Valuation ICP 15 Investment Solvency Standards ICP 16 Enterprise Risk Management for solvency purposes ICP 17 Capital Adequacy ICP 18 Intermediaries ICP 19 Conduct of Business ICP 20 Public Disclosure ICP 21 Countering fraud in insurance ICP 22 Anti-money laundering and combating the financing of terrorism (AML/CFT) ICP 23 Group-wide supervision ICP 24 Macroprudential supervision and market analysis ICP 25 Supervisory cooperation and coordination ICP 26 Cross-border cooperation and coordination on crisis management Assessment methodology Reinsurance Supervision (excerpts)

7 Regulatory Convergence How? IAIS Insurance Core Principles (ICP), Standards and Guidance * ICP 17 Capital Adequacy** - the (Insurance Core) Principle The supervisor establishes capital adequacy requirements for solvency purposes so that insurers can absorb significant unforeseen losses and to provide for degrees of supervisory intervention. * ICP s and Standards are mandatory, Guidance is not ** Supported by 18 Standards and within each of these 18 Standards many Guidelines

8 Regulatory Convergence How? ICP 17 Standard (#4) 17.4 In the context of insurance legal entity capital adequacy assessment, the regulatory capital requirements establish: (i) a solvency control level above which the supervisor does not intervene on capital adequacy grounds. This is referred to as the Prescribed Capital Requirement (PCR). The PCR is defined such that assets will exceed technical provisions and other liabilities with a specified level of safety over a defined time horizon. (ii) a solvency control level at which, if breached, the supervisor would invoke its strongest actions, in the absence of appropriate corrective action by the insurance legal entity. This is referred to as the Minimum Capital Requirement (MCR). The MCR is subject to a minimum bound below which no insurer is regarded to be viable to operate effectively

9 Regulatory Convergence How? ICP 17 Guideline (#2) to support Standard (#4) In broad terms, the highest regulatory capital requirement, the Prescribed Capital Requirement (PCR), will be set at the level at which the supervisor would not require action to increase the capital resources held or reduce the risks undertaken by the insurer. However if the insurer s capital resources were to fall below the level at which the PCR is set, the supervisor would require some action by the insurer to either restore capital resources to at least the PCR level or reduce the level of risk undertaken (and hence the required capital level).

10 Global Regulatory Convergence Themes Global Supervision ICP 23 (Group wide supervision) ICP 3 (refers to Supervisory Colleges) IAIS s Com Frame for Internationally Active Insurance Groups Solvency II (e.g. Equivalence) OSFI (revised Supervisory Framework)

11 Global Regulatory Convergence Themes Solvency Standards ICP 14 (Valuation) and ICP 17 (Capital Adequacy) Solvency II (Pillar 1) NAIC s Solvency Modernization Initiative OSFI transition to Life Insurer Solvency Assessment

12 Global Regulatory Convergence Themes Own Risk and Solvency Assessment (ORSA) ICP 8 Risk Management and Internal Controls ICP 16 Enterprise Risk Management Primary purpose of ORSA is to assess whether insurer s risk management and solvency position is currently adequate and is likely to remain so in the future Solvency II (Pillar 2) OSFI s Supervisory Framework

13 Global Regulatory Convergence Themes Economic Balance Sheet ICP 14 Valuation Reflect total balance sheet approach on an economic basis Solvency II Assets: exchanged between knowledgable, willing parties Liabilities: amount they can be transferred ( exit value ) OSFI s transition from MCCSR to Life Insurer Solvency Assessment (Standard and Advanced Approaches)

14 Global Regulatory Convergence Themes Eligible Capital Capital Targets ICP 17, Capital Adequacy OSFI s (Draft) Guideline A-4 Basel III OSFI Guidelines for Deposit Taking Institutions (DTIs) Importation to insurers discussions will start soon

15 Global Regulatory Convergence Themes Reinsurance ICP 13 Reinsurance and other forms of risk transfer NAIC Reinsurance Modernization Act OSFI Response Paper, Guideline B-3, Guidance on RSAs

16 Canadian Implications and Views Balanced Approach adopting International Standards 1. Level of adoption Avoid adopting only the more onerous international guidance a more onerous version of other international guidance 2. Pace of adoption Overall neither lead implementing the more onerous international guidance follow implementing the more onerous international guidance

17 Canadian Implications and Views Supervision Group-wide supervision Multiple IAIS sources Establish an effective and efficient framework ICP 23.6 Reliance on foreign regulators to supervise foreign subsidiaries Reliance on the group supervisor of foreign parent to properly supervise group

18 Canadian Implications and Views Solvency Standards Capital adequacy and establishing regulatory capital - ICP 17.1 and 17.2 Total balance sheet approach ICP 17.1 Meet obligations under adversity ICP 17.2 Confidence levels; Diversification credits Solvency control levels/triggers of intervention - ICP 17.3 and 17.4 Solvency Control Levels ICP 17.3 Various considerations PCR; MCR ICP 17.4 Below MCR/PCR, supervisor invokes strongest action/requires action

19 Canadian Implications and Views Reinsurance Strategies and Transparency ICP 13.1, 13.2 Supervisor requires cedant to have strategies appropriate to nature, scale and complexity (plus systems and procedures) ICP 13.1 OSFI s Guideline B-3: Risk management policy (Key Principle #1) OSFI s Guidance on Reinsurance Security Agreements Supervisor requires that cedants are transparent ICP 13.2 OSFI s Response Paper : Adopted View 2 (comprehensive regulation) instead of View 1 (little, if any regulation) OSFI s Guideline B-3: Due diligence of reinsurers (Key Principle #2)

20 Canadian Implications and Views Reinsurance (continued) Supervisory Recognition and Binding Documentation ICP 13.3, 13.4 Supervisor takes into account nature of supervision of reinsurers (unilateral, bilateral, multilateral) ICP 13.3 OSFI s Response Paper : Premature to consider mutual recognition Supervisor requires prompt documentation of principal economic and coverage terms and conditions in a timely fashion ICP 13.4 OSFI s Guideline B-3: binding summary agreements, reinsurance contracts, clarity and certainty of terms (Key Principles #3 and #4)

21 Regulatory Convergence: Some International Themes Canadian Reinsurance Conference Session 6 Michael Bean Director, Capital Division April 7, 2011

22 Focus of this Presentation Consider three themes in insurance regulation and their implications for Canadian companies: Greater expectation for companies to assess and manage their own risks Use of internal models for risk measurement, risk management and the determination of regulatory requirements Movement toward the use of more market-based methods of valuation and capital determination 2

23 Company-Specific Risk Measurement Greater expectation for companies to: assess the risks they actually have on their balance sheets hold appropriate amounts of capital for those risks actively manage those risks versus: relying solely on regulatory capital as a measure of risk using regulatory capital to manage their businesses 3

24 Company Specific Risk Measurement Catalysts: More sophisticated products (e.g., variable annuities with complex guarantees) More sophisticated risk management techniques (e.g., dynamic hedging) Rationale: Companies better placed than regulators to understand all the risks in their business One size fits all risk measurement not sufficiently granular to capture all the risks in sophisticated products 4

25 Company Specific Risk Measurement Canadian context: OSFI has always encouraged companies to conduct their own analyses and develop appropriate risk and capital management plans Recent developments: Guideline A4 Capital Targets Guideline B3 Sound Reinsurance Practices & Procedures Future developments: Own Risk and Solvency Assessment (ORSA) 5

26 Use of Internal Models Context: Company-specific risk measurement requires the use of company-specific models Internal models have the potential to better capture the risks in sophisticated products than standardized models Applications: Regulatory capital Economic capital 6

27 Use of Internal Models Economic capital models: Intended to allocate a company s capital commensurate with risk to enhance shareholder value, subject to the constraints posed by regulators and rating agencies Regulatory capital models: Intended to protect policyholders / depositors, but not necessarily shareholders Capital needed to continue to write new business not considered 7

28 Use of Internal Models Canadian context: Internal models used to calculate regulatory capital requirements for segregated fund guarantees since 2002 (subject to OSFI approval) Recent developments: Comprehensive review of capital requirements for segregated fund guarantees Future developments: Project to expand the use of internal models for regulatory capital (both life and P&C) 8

29 Market-Based Methods of Valuation & Capital Determination Move toward the use of more market based methods for market risks versus Use of methods based primarily on historical experience 9

30 Market-Based Methods of Valuation & Capital Determination Market-based methods can mean: methods based on arbitrage-free principles risk neutral calculation techniques methods based on replication methods based on financial economics methods in which parameters are market observed values 10

31 Market-Based Methods of Valuation & Capital Determination Rationale: Market risk has non-diversifiable components Law of large numbers doesn t hold Traditional actuarial techniques insufficient Market risk has become a more material component of the risk on insurance company balance sheets Products with embedded guarantees (e.g., variable annuities) 11

32 Market-Based Methods of Valuation & Capital Determination Rationale: Market-based methods enable companies to better capture the economics of the risk in products such as variable annuities Companies are using more market-based techniques to manage market risk Accounting (IFRS) 12

33 Market-Based Methods of Valuation & Capital Determination Canadian context: Development of market consistent approach to determining regulatory capital requirements for segregated fund guarantees ( ) Increased use of financial instruments and/or dynamic strategies to manage risk in segregated fund guarantee products Financial instruments have a market value Desirability of having consistency between asset and liability valuations Potential for the use of more market-based approaches to market risk in other products 13

34 Questions? 14

35

36 TITLE Presentation Points Additional Points Additional Points Dan Doyle FSA, FCIA Partner, Actuarial Services PricewaterhouseCoopers

37 Lessons Learned QIS 5 Background, Results, Impact PwC Solvency II Survey Preparedness, Critical Success Factors Impact of Solvency II Lessons for Canada

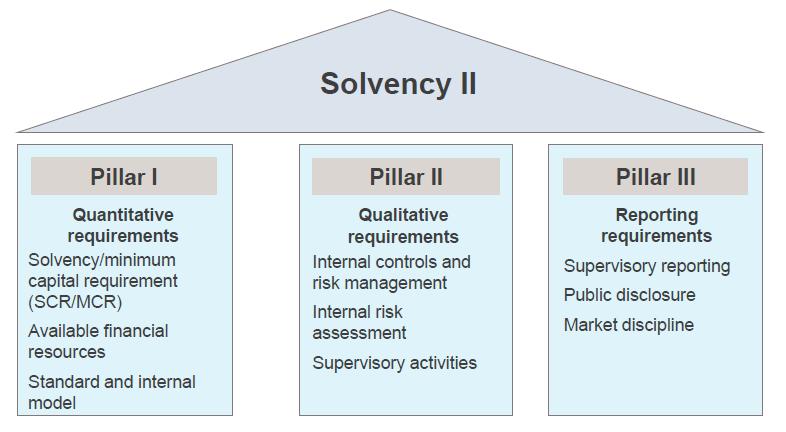

38 Pillars

39 QIS 5 - Background Fifth (and last) quantitative impact study for European insurers Dry-run for Solvency II (SII) Measure solvency standards using standard formula for SCR EIOPA (formerly CEIOPS) requested information on model results Over 2500 insurers 70% participated (QIS 4 ~ 30%)

40 QIS 5 - Results Mixed German Insurers blast SII as complex (especially for smaller insurers) Denmark Six failed SCR, push for simplification Italy/Austria Most better off than prior regime 15% fail SCR across Europe (20% within U.K.) Overall results show industry is healthy Highlight some weaknesses (both in measures and preparedness)

Sharing (- 314 bn/ -23.7%) SCR ( 547 bn / 41.2%) 00% 25% 0.1 50% 0.2 75% 0.3 100% 125% 0.4 150% 0.5 175% 0.6200% 225% 0.")

41 QIS 5 Results Impact of Diversification and Loss-absorbing Capacity Risks ( 1328bn) Diversification ( -466bn/ -35.1%) Sharing (- 314 bn/ -23.7%) SCR ( 547 bn / 41.2%) 00% 25% % % % 125% % % % 225% %

42 QIS 5 Next Steps Found areas of weakness (QIS 6?) SII framework in place in 2011 Models not a panacea 1-2 year transition period

43 PwC Survey What level of convergence do you hope to achieve with other significant initiatives? Enterprise Risk Management Strong Convergence Basic Convergence International Financial Reporting Standards No convergence Not Applicable Economic Capital Market Consistent Embedded Value 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

44 PwC Survey Rank the top three factors you believe are the critical success factors for successful implementation of the Solvency II program Rank 3 60% 50% 40% 30% 20% 10% 0% Rank 2 Rank 1

45 PwC Survey 80% 70% 60% 50% 40% 30% 20% 10% 0% Rank the top three elements which present significant challenges to the implementation of the Solvency II program ORSA Internal Model Approval Use Test Actuarial function Risk management function Compliance function Pillar 3 (reporting to and dialogue with supervisors) Rank 3 Rank 2 Rank 1 Other

46 SII Impact/Comments Solvency II will create an illusion that crisis will be avoided Small/med. size insurers overwhelmed by Pillar II requirements Complexity of standard model Impact on those who have limited access to capital and those who operate with a minimal capital base (captives)

47 SII Impact/Comments Monoline Insurers (no diversification) Cost of SII carried by policyholders Innovative tailored reinsurance solutions and corporate structures Benefits: Common platform State of the art ERM Documentation/transparency

48 Lessons for Canada For Regulators: Too much and too fast can cause significant market disruption issues For Insurance Companies: Convergence will happen in time Convergence has benefits but regulatory overhead will not decrease any time soon European issues illustrate our potential future challenges

Capital Adequacy and Supervisory Assessment of Solvency Position

Capital Adequacy and Supervisory Assessment of Solvency Position Jeffery Yong IAIS Secretariat Regional Seminar for Supervisors in Africa on Risk-based Solvency and Supervision, 14 September 2010 Agenda

Capital Adequacy and Supervisory Assessment of Solvency Position Jeffery Yong IAIS Secretariat Regional Seminar for Supervisors in Africa on Risk-based Solvency and Supervision, 14 September 2010 Agenda

Gregg Clifton. CFO Aurigen Reinsurance

Gregg Clifton CFO Aurigen Reinsurance Regulatory Capital When it comes to regulatory capital, is there a discernable clicking sound of a ratchet? More onerous Canadian capital requirements and the inherent

Gregg Clifton CFO Aurigen Reinsurance Regulatory Capital When it comes to regulatory capital, is there a discernable clicking sound of a ratchet? More onerous Canadian capital requirements and the inherent

The Solvency II project and the work of CEIOPS

Thomas Steffen CEIOPS Chairman Budapest, 16 May 07 The Solvency II project and the work of CEIOPS Outline Reasons for a change in the insurance EU regulatory framework The Solvency II project Drivers Process

Thomas Steffen CEIOPS Chairman Budapest, 16 May 07 The Solvency II project and the work of CEIOPS Outline Reasons for a change in the insurance EU regulatory framework The Solvency II project Drivers Process

International Regulatory Developments

International Regulatory Developments An Introduction to Solvency II Simone Brathwaite, FSA, FCIA, CERA Principal Oliver Wyman December 2, 2010 Many bodies driving global regulatory change A simplification

International Regulatory Developments An Introduction to Solvency II Simone Brathwaite, FSA, FCIA, CERA Principal Oliver Wyman December 2, 2010 Many bodies driving global regulatory change A simplification

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar 1 Sub Committee Capital Requirements Task Group Discussion Document 74 (v 3) Minimum Capital Requirement (MCR) EXECUTIVE SUMMARY Having compared the IAIS ICPs

Solvency Assessment and Management: Pillar 1 Sub Committee Capital Requirements Task Group Discussion Document 74 (v 3) Minimum Capital Requirement (MCR) EXECUTIVE SUMMARY Having compared the IAIS ICPs

Solvency II Update. Latest developments and industry challenges (Session 10) Réjean Besner

Réjean Besner") Solvency II Update Latest developments and industry challenges (Session 10) Canadian Institute of Actuaries - Annual Meeting, 29 June 2011 Réjean Besner Content Solvency II framework Solvency II equivalence

Solvency II Update Latest developments and industry challenges (Session 10) Canadian Institute of Actuaries - Annual Meeting, 29 June 2011 Réjean Besner Content Solvency II framework Solvency II equivalence

Karel VAN HULLE. Head of Unit, Insurance and Pensions, DG Markt, European Commission

Solvency II: State of Play Guernsey, 18th December 2009 Karel VAN HULLE Head of Unit, Insurance and Pensions, DG Markt, European Commission 1 Why do we need Solvency II? Lack of risk sensitivity in existing

Solvency II: State of Play Guernsey, 18th December 2009 Karel VAN HULLE Head of Unit, Insurance and Pensions, DG Markt, European Commission 1 Why do we need Solvency II? Lack of risk sensitivity in existing

Framework for a New Standard Approach to Setting Capital Requirements. Joint Committee of OSFI, AMF, and Assuris

Framework for a New Standard Approach to Setting Capital Requirements Joint Committee of OSFI, AMF, and Assuris Table of Contents Background... 3 Minimum Continuing Capital and Surplus Requirements (MCCSR)...

Framework for a New Standard Approach to Setting Capital Requirements Joint Committee of OSFI, AMF, and Assuris Table of Contents Background... 3 Minimum Continuing Capital and Surplus Requirements (MCCSR)...

Actuaries and the Regulatory Environment. Role of the Actuary in the Solvency II framework

Actuaries and the Regulatory Environment Role of the Actuary in the Solvency II framework IAA Fund Southeast Europe Actuarial Seminar, Zagreb, 3 October 2011 1 Solvency II primary objectives fundamental

Actuaries and the Regulatory Environment Role of the Actuary in the Solvency II framework IAA Fund Southeast Europe Actuarial Seminar, Zagreb, 3 October 2011 1 Solvency II primary objectives fundamental

Solvency II. Insurance and Pensions Unit, European Commission

Solvency II Insurance and Pensions Unit, European Commission Introduction Solvency II Deepened integration of the EU insurance market 14 existing Directives on insurance and reinsurance supervision, insurance

Solvency II Insurance and Pensions Unit, European Commission Introduction Solvency II Deepened integration of the EU insurance market 14 existing Directives on insurance and reinsurance supervision, insurance

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

Questions and Answers

ReImagine Regulation Overview of Session Steve Easson Regulatory Landscape Overview Paul Savage LICAT (Direct Writer) Focus Chris Piper IFRS17 (Reinsurance) Focus Questions and Answers Regulatory Landscape

ReImagine Regulation Overview of Session Steve Easson Regulatory Landscape Overview Paul Savage LICAT (Direct Writer) Focus Chris Piper IFRS17 (Reinsurance) Focus Questions and Answers Regulatory Landscape

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar I - Sub Committee Capital Requirements Task Group Discussion Document 61 (v 1) SCR standard formula: Operational Risk EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar I - Sub Committee Capital Requirements Task Group Discussion Document 61 (v 1) SCR standard formula: Operational Risk EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Steering Committee Position Paper 73 1 (v 3) Treatment of new business in SCR

Treatment of new business in SCR") Solvency Assessment and Management: Steering Committee Position Paper 73 1 (v 3) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework Directive and IAIS guidance, the risk

Solvency Assessment and Management: Steering Committee Position Paper 73 1 (v 3) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework Directive and IAIS guidance, the risk

Solvency II overview

Solvency II overview David Payne, FIA Casualty Loss Reserve Seminar 21 September 2010 INTNL-2: Solvency II - Update and Current Events Antitrust Notice The Casualty Actuarial Society is committed to adhering

Solvency II overview David Payne, FIA Casualty Loss Reserve Seminar 21 September 2010 INTNL-2: Solvency II - Update and Current Events Antitrust Notice The Casualty Actuarial Society is committed to adhering

SOLVENCY ASSESSMENT AND MANAGEMENT (SAM) FRAMEWORK

FRAMEWORK") SOLVENCY ASSESSMENT AND MANAGEMENT (SAM) FRAMEWORK Hantie van Heerden Head: Actuarial Insurance Department 5 October 2010 High-level summary of Solvency II Background to SAM Agenda Current Structures Progress

SOLVENCY ASSESSMENT AND MANAGEMENT (SAM) FRAMEWORK Hantie van Heerden Head: Actuarial Insurance Department 5 October 2010 High-level summary of Solvency II Background to SAM Agenda Current Structures Progress

Solvency Assessment and Management (SAM)

") Solvency Assessment and Management (SAM) 1. Solvency Assessment and Management (SAM) The FSB is in the process of developing a new risk-based solvency regime for South African shortterm and long-term insurers,

Solvency Assessment and Management (SAM) 1. Solvency Assessment and Management (SAM) The FSB is in the process of developing a new risk-based solvency regime for South African shortterm and long-term insurers,

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 2.2.6 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES OCTOBER 2007 This document was prepared

Guidance Paper No. 2.2.6 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES OCTOBER 2007 This document was prepared

SOLVENCY ADVISORY COMMITTEE QUÉBEC CHARTERED LIFE INSURERS

SOLVENCY ADVISORY COMMITTEE QUÉBEC CHARTERED LIFE INSURERS March 2008 volume 4 FRAMEWORK FOR A NEW STANDARD APPROACH TO SETTING CAPITAL REQUIREMENTS AUTORITÉ DES MARCHÉS FINANCIERS SOLVENCY ADVISORY COMMITTEE

SOLVENCY ADVISORY COMMITTEE QUÉBEC CHARTERED LIFE INSURERS March 2008 volume 4 FRAMEWORK FOR A NEW STANDARD APPROACH TO SETTING CAPITAL REQUIREMENTS AUTORITÉ DES MARCHÉS FINANCIERS SOLVENCY ADVISORY COMMITTEE

Sharing insights on key industry issues*

Insurance This article is from a PricewaterhouseCoopers publication entitled Insurancedigest Sharing insights on key industry issues* Americas edition February 2009 Solvency II: A competitive advantage

Insurance This article is from a PricewaterhouseCoopers publication entitled Insurancedigest Sharing insights on key industry issues* Americas edition February 2009 Solvency II: A competitive advantage

The Review of Solvency II. 01/02/2018 Hans De Cuyper, President of Assuralia

The Review of Solvency II 01/02/2018 Hans De Cuyper, President of Assuralia 1 Implementation of Solvency II Belgian insurance companies early adopters with first dry runs in 2014 2 From Solvency I to Solvency

The Review of Solvency II 01/02/2018 Hans De Cuyper, President of Assuralia 1 Implementation of Solvency II Belgian insurance companies early adopters with first dry runs in 2014 2 From Solvency I to Solvency

'SOLVENCY II': Frequently Asked Questions (FAQs)

") MEMO/07/286 Brussels, 10 July 2007 'SOLVENCY II': Frequently Asked Questions (FAQs) (see also IP/07/1060) 1. Why does the EU need harmonised solvency rules? The aim of a solvency regime is to ensure the

MEMO/07/286 Brussels, 10 July 2007 'SOLVENCY II': Frequently Asked Questions (FAQs) (see also IP/07/1060) 1. Why does the EU need harmonised solvency rules? The aim of a solvency regime is to ensure the

An Introduction to Solvency II

An Introduction to Solvency II Peter Withey KPMG Agenda 1. Background to Solvency II 2. Pillar 1: Quantitative Pillar Basic building blocks Assets Technical Reserves Solvency Capital Requirement Internal

An Introduction to Solvency II Peter Withey KPMG Agenda 1. Background to Solvency II 2. Pillar 1: Quantitative Pillar Basic building blocks Assets Technical Reserves Solvency Capital Requirement Internal

2013 Conference Risk, Recovery & Real Growth" 23rd Annual CAA Conference Secrets Wild Orchid Montego Bay, Jamaica. 4 th to 6 th December 2013

2013 Conference Risk, Recovery & Real Growth" 23rd Annual CAA Conference Secrets Wild Orchid Montego Bay, Jamaica. 4 th to 6 th December 2013 Regulatory developments in life assurance Nick Dumbreck Milliman

2013 Conference Risk, Recovery & Real Growth" 23rd Annual CAA Conference Secrets Wild Orchid Montego Bay, Jamaica. 4 th to 6 th December 2013 Regulatory developments in life assurance Nick Dumbreck Milliman

International Insurance Regulation 101: International Association of Insurance Supervisors

The Academy Capitol Forum: Meet the Experts International Insurance Regulation 101: International Association of Insurance Supervisors George Brady, Deputy Secretary General, IAIS Moderator: Jeffrey S.

The Academy Capitol Forum: Meet the Experts International Insurance Regulation 101: International Association of Insurance Supervisors George Brady, Deputy Secretary General, IAIS Moderator: Jeffrey S.

The road to Solvency II: The Regulatory View

The road to Solvency II: The Regulatory View Rob Curtis Director, KPMG 1 June 2011 Background to developments The Global Financial Crisis (GFC) highlighted: Regulatory focus at individual firm level and

The road to Solvency II: The Regulatory View Rob Curtis Director, KPMG 1 June 2011 Background to developments The Global Financial Crisis (GFC) highlighted: Regulatory focus at individual firm level and

CEA proposed amendments, April 2008

CEA proposed amendments, April 2008 Amendment 1: Recital 14 a (new) The supervision of reinsurance activity shall take account of the special characteristics of reinsurance business, notably its global

CEA proposed amendments, April 2008 Amendment 1: Recital 14 a (new) The supervision of reinsurance activity shall take account of the special characteristics of reinsurance business, notably its global

Solvency Assessment and Management: Steering Committee Position Paper (v 4) Life SCR - Retrenchment Risk

Life SCR - Retrenchment Risk") Solvency Assessment and Management: Steering Committee Position Paper 108 1 (v 4) Life SCR - Retrenchment Risk EXECUTIVE SUMMARY This document discusses the structure and calibration of the proposed Retrenchment

Solvency Assessment and Management: Steering Committee Position Paper 108 1 (v 4) Life SCR - Retrenchment Risk EXECUTIVE SUMMARY This document discusses the structure and calibration of the proposed Retrenchment

Solvency II Insights for North American Insurers. CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

Solvency II Insights for North American Insurers CAS Centennial Meeting Damon Paisley Bill VonSeggern November 10, 2014 Agenda 1 Introduction to Solvency II 2 Pillar I 3 Pillar II and Governance 4 North

A (personal) view. Philip Whittingham, European Chief Enterprise Risk Officer. 22 March 2010

view. Philip Whittingham, European Chief Enterprise Risk Officer. 22 March 2010") The role of the risk profession in a Solvency II world A (personal) view Philip Whittingham, European Chief Enterprise Risk Officer XL Group plc 22 March 2010 Session Aims Successful Solvency II implementation

The role of the risk profession in a Solvency II world A (personal) view Philip Whittingham, European Chief Enterprise Risk Officer XL Group plc 22 March 2010 Session Aims Successful Solvency II implementation

Past and Future of Corporate Governance

Past and Future of Corporate Governance Sónia Camacho 13 th November 2017 Insurance Financial Planning Retirement Investments Wealth Brief History of Corporate Governance Cadbury Greenbury Hampel UK Combined

Past and Future of Corporate Governance Sónia Camacho 13 th November 2017 Insurance Financial Planning Retirement Investments Wealth Brief History of Corporate Governance Cadbury Greenbury Hampel UK Combined

The Omnibus II Directive

The Omnibus II Directive Presentation to Gibraltar Insurance Association Michael Oliver Head of Insurance Supervision 9 March 2011 1 The Omnibus II Directive Timeline Contents EIOPA and its powers Transitional

The Omnibus II Directive Presentation to Gibraltar Insurance Association Michael Oliver Head of Insurance Supervision 9 March 2011 1 The Omnibus II Directive Timeline Contents EIOPA and its powers Transitional

Solvency Assessment and Management: Steering Committee Position Paper 34 1 (v 5) Own Risk and Solvency Assessment

Own Risk and Solvency Assessment") Solvency Assessment and Management: Steering Committee Position Paper 34 1 (v 5) Own Risk and Solvency Assessment EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document is to present

Solvency Assessment and Management: Steering Committee Position Paper 34 1 (v 5) Own Risk and Solvency Assessment EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document is to present

IAIS Standards Setting Activities

London 3 Secretary General International Association of Insurance Supervisors (IAIS) Website: www.iaisweb.org Overview 1. IAIS structure and process 2. Insurance Core Principles 3. IAIS views on IASB standards

London 3 Secretary General International Association of Insurance Supervisors (IAIS) Website: www.iaisweb.org Overview 1. IAIS structure and process 2. Insurance Core Principles 3. IAIS views on IASB standards

Solvency II The Global Insurance Financial Trojan Horse. Les Boughner EVP & Managing Director Willis Captive & Consulting Practice

Solvency II The Global Insurance Financial Trojan Horse Les Boughner EVP & Managing Director Willis Captive & Consulting Practice 1 Solvency II What is it Why is it important to you What is the US Impact

Solvency II The Global Insurance Financial Trojan Horse Les Boughner EVP & Managing Director Willis Captive & Consulting Practice 1 Solvency II What is it Why is it important to you What is the US Impact

Global Capital Standards: laying down the future for global insurance supervision

KEYNOTE SPEECH Gabriel Bernardino Chairman of EIOPA Global Capital Standards: laying down the future for global insurance supervision Seminar of the Actuarial Association of Europe Brussels, 3 March 2014

KEYNOTE SPEECH Gabriel Bernardino Chairman of EIOPA Global Capital Standards: laying down the future for global insurance supervision Seminar of the Actuarial Association of Europe Brussels, 3 March 2014

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 75 (v 4) Treatment of risk-mitigation techniques in the SCR EXECUTIVE SUMMARY As per Solvency

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 75 (v 4) Treatment of risk-mitigation techniques in the SCR EXECUTIVE SUMMARY As per Solvency

CONSULTATION PAPER ON A RISK- BASED CAPITAL FRAMEWORK FOR THE INSURANCE INDUSTRY IN HONG KONG

CONSULTATION PAPER ON A RISK- BASED CAPITAL FRAMEWORK FOR THE INSURANCE INDUSTRY IN HONG KONG On 16 September 2014, the Office of the Commissioner of Insurance ("OCI") announced the publication by the

CONSULTATION PAPER ON A RISK- BASED CAPITAL FRAMEWORK FOR THE INSURANCE INDUSTRY IN HONG KONG On 16 September 2014, the Office of the Commissioner of Insurance ("OCI") announced the publication by the

EVOLVING INSURANCE REGULATION

EVOLVING INSURANCE REGULATION A CONSULTATION PAPER ON THE REVISION OF THE REGULATIONS, RULES AND CODES FOR LICENSED INSURERS 24 September 2013 1 P age The Guernsey Financial Services Commission invites

EVOLVING INSURANCE REGULATION A CONSULTATION PAPER ON THE REVISION OF THE REGULATIONS, RULES AND CODES FOR LICENSED INSURERS 24 September 2013 1 P age The Guernsey Financial Services Commission invites

SAM Reporting for Insurance Groups with Participations in Non-equivalent Jurisdictions

SAM Reporting for Insurance Groups with Participations in Non-equivalent Jurisdictions In November 2016 the FSB published the proposed Financial Soundness Standards (FS) for initial public comment. These

SAM Reporting for Insurance Groups with Participations in Non-equivalent Jurisdictions In November 2016 the FSB published the proposed Financial Soundness Standards (FS) for initial public comment. These

Frequently Asked Questions for The global risk-based Insurance Capital Standard (ICS) Updated 21 July 2017

Updated 21 July 2017") Updated 21 July 2017 Frequently Asked Questions for The global risk-based Insurance Capital Standard (ICS) Updated 21 July 2017 Questions 1. What is the risk-based global insurance capital standard (ICS)?...

Updated 21 July 2017 Frequently Asked Questions for The global risk-based Insurance Capital Standard (ICS) Updated 21 July 2017 Questions 1. What is the risk-based global insurance capital standard (ICS)?...

WHITE PAPER. Solvency II Compliance and beyond: Title The essential steps for insurance firms

WHITE PAPER Solvency II Compliance and beyond: Title The essential steps for insurance firms ii Contents Introduction... 1 Step 1 Data Management... 1 Step 2 Risk Calculations... 3 Solvency Capital Requirement

WHITE PAPER Solvency II Compliance and beyond: Title The essential steps for insurance firms ii Contents Introduction... 1 Step 1 Data Management... 1 Step 2 Risk Calculations... 3 Solvency Capital Requirement

INSURANCE REGULATION OMNIBUS CONSULTATION A CONSULTATION PAPER ON REVISION OF THE RULES AND GUIDANCE FOR LICENSED INSURERS

INSURANCE REGULATION OMNIBUS CONSULTATION A CONSULTATION PAPER ON REVISION OF THE RULES AND GUIDANCE FOR LICENSED INSURERS Issued 17 April 2018 This Consultation Paper makes proposals in respect of the

INSURANCE REGULATION OMNIBUS CONSULTATION A CONSULTATION PAPER ON REVISION OF THE RULES AND GUIDANCE FOR LICENSED INSURERS Issued 17 April 2018 This Consultation Paper makes proposals in respect of the

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar 1 - Sub Committee Technical Provisions Task Group Discussion Document 87 (v 6) Future Management Actions in Technical Provisions EXECUTIVE SUMMARY 1. INTRODUCTION

Solvency Assessment and Management: Pillar 1 - Sub Committee Technical Provisions Task Group Discussion Document 87 (v 6) Future Management Actions in Technical Provisions EXECUTIVE SUMMARY 1. INTRODUCTION

17/06/2012. Solvency II: Implementation Challenges & Opportunities. What is Solvency II about?

What is Solvency II about? Solvency II: Implementation Challenges & Opportunities The Solvency II Directive is a regulatory framework for the European insurance industry that adopts a more dynamic and

What is Solvency II about? Solvency II: Implementation Challenges & Opportunities The Solvency II Directive is a regulatory framework for the European insurance industry that adopts a more dynamic and

September 28, Overview of Submission

September 28, 2017 Director Financial Institutions Division Financial Sector Branch Department of Finance Canada James Michael Flaherty Building 90 Elgin Street Ottawa ON K1A 0G5 Email: fin.legislativereview-examenlegislatif.fin@canada.ca

September 28, 2017 Director Financial Institutions Division Financial Sector Branch Department of Finance Canada James Michael Flaherty Building 90 Elgin Street Ottawa ON K1A 0G5 Email: fin.legislativereview-examenlegislatif.fin@canada.ca

Own Risk and Solvency Assessment (ORSA)

") Own Risk and Solvency Assessment (ORSA) Presentations to OCCA (Nov. 19, 2014) and AAIARD (Nov. 21, 2014) Jacqueline Friedland, FCIA, FCAS, FSA, MAAA Chief Actuary, RSA Canada Presentation Outline What

Own Risk and Solvency Assessment (ORSA) Presentations to OCCA (Nov. 19, 2014) and AAIARD (Nov. 21, 2014) Jacqueline Friedland, FCIA, FCAS, FSA, MAAA Chief Actuary, RSA Canada Presentation Outline What

Solvency II. New Rules in Europe for the Insurance Industry. Lecture at UConn Law, January 28, 2013

Solvency II New Rules in Europe for the Insurance Industry Lecture at UConn Law, January 28, 2013 Christian Armbrüster Freie Universität Berlin c.armbruester@fu-berlin.de Main institutions of the European

Solvency II New Rules in Europe for the Insurance Industry Lecture at UConn Law, January 28, 2013 Christian Armbrüster Freie Universität Berlin c.armbruester@fu-berlin.de Main institutions of the European

BERMUDA MONETARY AUTHORITY INSURANCE DEPARTMENT GUIDANCE NOTE #14 INSURANCE ACTIVITY

BERMUDA MONETARY AUTHORITY INSURANCE DEPARTMENT GUIDANCE NOTE #14 INSURANCE ACTIVITY MARCH 2005 March, 2005 Page 1 of 5 GUIDANCE NOTE: INSURANCE ACTIVITY Introduction 1 The prime responsibility for the

BERMUDA MONETARY AUTHORITY INSURANCE DEPARTMENT GUIDANCE NOTE #14 INSURANCE ACTIVITY MARCH 2005 March, 2005 Page 1 of 5 GUIDANCE NOTE: INSURANCE ACTIVITY Introduction 1 The prime responsibility for the

Webinar. The Gibraltar Financial Services Commission. Solvency II Implications for Non-Executive Directors (NEDs) 28 th May 2015

28 th May 2015") Webinar Solvency II Implications for Non-Executive Directors (NEDs) 28 th May 2015 Kathryn Morgan, Director or Regulatory Operations Ken Hogg, Solvency II Project Manager Webinar 28 th May 2015 Agenda

Webinar Solvency II Implications for Non-Executive Directors (NEDs) 28 th May 2015 Kathryn Morgan, Director or Regulatory Operations Ken Hogg, Solvency II Project Manager Webinar 28 th May 2015 Agenda

Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test

Use Test") Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document

Solvency Assessment and Management: Pillar 2 - Sub Committee ORSA and Use Test Task Group Discussion Document 35 (v 3) Use Test EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose of this document

The Impact of International Issues on Insurance Compliance in the United States

The Impact of International Issues on Insurance Compliance in the United States Fred E. Karlinsky Rubén N. Gely Rodríguez AICP Gulf States Chapter E-Day Atlanta, Georgia June 13, 2014 www.cftlaw.com Disclaimer

The Impact of International Issues on Insurance Compliance in the United States Fred E. Karlinsky Rubén N. Gely Rodríguez AICP Gulf States Chapter E-Day Atlanta, Georgia June 13, 2014 www.cftlaw.com Disclaimer

The Society of Actuaries in Ireland

The Society of Actuaries in Ireland The Solvency II Actuary Kathryn Morgan Annette Olesen 8 Content Overview of Solvency II and latest developments The Actuarial Function Impact on the role of the actuary

The Society of Actuaries in Ireland The Solvency II Actuary Kathryn Morgan Annette Olesen 8 Content Overview of Solvency II and latest developments The Actuarial Function Impact on the role of the actuary

Solvency II. Yannis Pitaras IACPM Brussels, 15 May 2009

Solvency II Yannis Pitaras IACPM Brussels, 15 May 2009 CEA s Member Associations 33 national member associations: 27 EU Member States + 6 Non EU Markets Switzerland, Iceland, Norway, Turkey, Liechtenstein,

Solvency II Yannis Pitaras IACPM Brussels, 15 May 2009 CEA s Member Associations 33 national member associations: 27 EU Member States + 6 Non EU Markets Switzerland, Iceland, Norway, Turkey, Liechtenstein,

Southeastern Actuaries Conference 2012 Annual Meeting. Jeffrey S. Schlinsog, CFA, FSA, MAAA

www.pwc.com November 15, 2012 ERM Topics Southeastern Actuaries Conference 2012 Annual Meeting Jeffrey S. Schlinsog, CFA, FSA, MAAA ERM Topics 1. The development and implementation of the ORSA 2. The contents

www.pwc.com November 15, 2012 ERM Topics Southeastern Actuaries Conference 2012 Annual Meeting Jeffrey S. Schlinsog, CFA, FSA, MAAA ERM Topics 1. The development and implementation of the ORSA 2. The contents

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Principles No. 3.4 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS PRINCIPLES ON GROUP-WIDE SUPERVISION OCTOBER 2008 This document has been prepared by the Financial Conglomerates Subcommittee (renamed

Principles No. 3.4 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS PRINCIPLES ON GROUP-WIDE SUPERVISION OCTOBER 2008 This document has been prepared by the Financial Conglomerates Subcommittee (renamed

Solvency Monitoring and

Solvency Monitoring and Reporting Venkatasubramanian A CILA2006/AV 1 Intro No amount of capital can substitute for the capacity to understand, measure and manage risk and no formula or model can capture

Solvency Monitoring and Reporting Venkatasubramanian A CILA2006/AV 1 Intro No amount of capital can substitute for the capacity to understand, measure and manage risk and no formula or model can capture

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES PAPER ON GROUP-WIDE SOLVENCY ASSESSMENT AND SUPERVISION 5 MARCH 2009 This document was prepared jointly by the Solvency and Actuarial Issues Subcommittee

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES PAPER ON GROUP-WIDE SOLVENCY ASSESSMENT AND SUPERVISION 5 MARCH 2009 This document was prepared jointly by the Solvency and Actuarial Issues Subcommittee

ORSA An International Development

ORSA An International Development 25.02.14 Agenda What is an ORSA? Global reach Comparison of requirements Common challenges Potential solutions Origin of ORSA FSA ICAS Solvency II IAIS ICP16 What is an

ORSA An International Development 25.02.14 Agenda What is an ORSA? Global reach Comparison of requirements Common challenges Potential solutions Origin of ORSA FSA ICAS Solvency II IAIS ICP16 What is an

P/C Risk-Based Capital: State and International Solvency Regulation

P/C Risk-Based Capital: State and International Solvency Regulation May 31, 2011 Presented by the Property and Casualty Risk-Based Capital Committee 1 Presenters Moderator and speaker: Alex Krutov, FCAS,

P/C Risk-Based Capital: State and International Solvency Regulation May 31, 2011 Presented by the Property and Casualty Risk-Based Capital Committee 1 Presenters Moderator and speaker: Alex Krutov, FCAS,

CEIOPS-DOC-06/06. November 2006

CEIOPS-DOC-06/06 Advice to the European Commission in the framework of the Solvency II project on insurance undertakings Internal Risk and Capital Assessment requirements, supervisors evaluation procedures

CEIOPS-DOC-06/06 Advice to the European Commission in the framework of the Solvency II project on insurance undertakings Internal Risk and Capital Assessment requirements, supervisors evaluation procedures

Advanced Methods in Insurance Capital Requirements

Advanced Methods in Insurance Capital Requirements Allan Brender Special Advisor, Capital Division Mexico City, 19 April 2007 Declare Solvency! If only it were that simple! 2 Canadian Financial System

Advanced Methods in Insurance Capital Requirements Allan Brender Special Advisor, Capital Division Mexico City, 19 April 2007 Declare Solvency! If only it were that simple! 2 Canadian Financial System

Overview of IAIS Activities

Stockholm Lonny McPherson Member of Secretariat International Association of Insurance Supervisors (IAIS) Website: www.iaisweb.org 1. IAIS mandate, structure and process 2. Revised Insurance Core Principles

Stockholm Lonny McPherson Member of Secretariat International Association of Insurance Supervisors (IAIS) Website: www.iaisweb.org 1. IAIS mandate, structure and process 2. Revised Insurance Core Principles

Session 032 PD - Life Insurance Capital Framework in Canada. Moderator: Benjamin L. Marshall, FSA, CERA, FCIA, MAAA

Session 032 PD - Life Insurance Capital Framework in Canada Moderator: Benjamin L. Marshall, FSA, CERA, FCIA, MAAA Presenters: Henri Boudreau Lisa Marie Peterson, FSA, FCIA SOA Antitrust Compliance Guidelines

Session 032 PD - Life Insurance Capital Framework in Canada Moderator: Benjamin L. Marshall, FSA, CERA, FCIA, MAAA Presenters: Henri Boudreau Lisa Marie Peterson, FSA, FCIA SOA Antitrust Compliance Guidelines

OSFI Supervisory Model

OSFI Supervisory Model IAIS-ASSAL Regional Seminar 2003 Unclassified Agenda Achieving OSFI s Mission Key Supervisory Framework Principles Development of Rating Sharing of Supervisory Ratings Composite

OSFI Supervisory Model IAIS-ASSAL Regional Seminar 2003 Unclassified Agenda Achieving OSFI s Mission Key Supervisory Framework Principles Development of Rating Sharing of Supervisory Ratings Composite

Guidance paper on the use of internal models for risk and capital management purposes by insurers

Guidance paper on the use of internal models for risk and capital management purposes by insurers October 1, 2008 Stuart Wason Chair, IAA Solvency Sub-Committee Agenda Introduction Global need for guidance

Guidance paper on the use of internal models for risk and capital management purposes by insurers October 1, 2008 Stuart Wason Chair, IAA Solvency Sub-Committee Agenda Introduction Global need for guidance

Introductory Speech. The Solvency II Review: What happens next? Conference on "The review of Solvency II organised by the National Bank of Belgium

Introductory Speech Gabriel Bernardino Chairman of the European Insurance and Occupational Pensions Authority (EIOPA) The Solvency II Review: What happens next? Conference on "The review of Solvency II

Introductory Speech Gabriel Bernardino Chairman of the European Insurance and Occupational Pensions Authority (EIOPA) The Solvency II Review: What happens next? Conference on "The review of Solvency II

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords Basel Committee on Banking Supervision ( BCBS ) (www.bis.org: bcbs230 September 2012) Basel Committee on Banking

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords Basel Committee on Banking Supervision ( BCBS ) (www.bis.org: bcbs230 September 2012) Basel Committee on Banking

Solvency Assessment and Management: Steering Committee Position Paper (v 3) Loss-absorbing capacity of deferred taxes

Loss-absorbing capacity of deferred taxes") Solvency Assessment and Management: Steering Committee Position Paper 112 1 (v 3) Loss-absorbing capacity of deferred taxes EXECUTIVE SUMMARY SAM introduces a valuation basis of technical provisions that

Solvency Assessment and Management: Steering Committee Position Paper 112 1 (v 3) Loss-absorbing capacity of deferred taxes EXECUTIVE SUMMARY SAM introduces a valuation basis of technical provisions that

IRSG Opinion on Potential Harmonisation of Recovery and Resolution Frameworks for Insurers

IRSG OPINION ON DISCUSSION PAPER (EIOPA-CP-16-009) ON POTENTIAL HARMONISATION OF RECOVERY AND RESOLUTION FRAMEWORKS FOR INSURERS EIOPA-IRSG-17-03 28 February 2017 IRSG Opinion on Potential Harmonisation

IRSG OPINION ON DISCUSSION PAPER (EIOPA-CP-16-009) ON POTENTIAL HARMONISATION OF RECOVERY AND RESOLUTION FRAMEWORKS FOR INSURERS EIOPA-IRSG-17-03 28 February 2017 IRSG Opinion on Potential Harmonisation

Solvency Control Levels

International Association of Insurance Supervisors Solvency, Solvency Assessments and Actuarial Issues Subcommittee Draft Guidance Paper Solvency Control Levels Contents I. Introduction...1 II. Minimum

International Association of Insurance Supervisors Solvency, Solvency Assessments and Actuarial Issues Subcommittee Draft Guidance Paper Solvency Control Levels Contents I. Introduction...1 II. Minimum

MAS reviews Risk-Based Capital framework

www.pwc.com MAS reviews Risk-Based Capital framework 29 June 2012 In the light of evolving market practices and global regulatory developments, MAS is reviewing the risk-based capital framework for insurers

www.pwc.com MAS reviews Risk-Based Capital framework 29 June 2012 In the light of evolving market practices and global regulatory developments, MAS is reviewing the risk-based capital framework for insurers

GUERNSEY NEW RISK BASED INSURANCE SOLVENCY REQUIREMENTS

GUERNSEY NEW RISK BASED INSURANCE SOLVENCY REQUIREMENTS Introduction The Guernsey Financial Services Commission has published a consultation paper entitled Evolving Insurance Regulation. The paper proposes

GUERNSEY NEW RISK BASED INSURANCE SOLVENCY REQUIREMENTS Introduction The Guernsey Financial Services Commission has published a consultation paper entitled Evolving Insurance Regulation. The paper proposes

Developments & Insights in Singapore RBC 2 and Overview of ORSA across Regions

Developments & Insights in Singapore RBC 2 and Overview of ORSA across Regions 1 Agenda RBC 2 Developments in Singapore Comparison of ORSA Across Jurisdictions RBC2 Developments in Singapore In 2004, the

Developments & Insights in Singapore RBC 2 and Overview of ORSA across Regions 1 Agenda RBC 2 Developments in Singapore Comparison of ORSA Across Jurisdictions RBC2 Developments in Singapore In 2004, the

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes. George Brady. IAIS Deputy Secretary General

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

IAIS: Enterprise Risk Management for Capital Adequacy & Solvency Purposes George Brady IAIS Deputy Secretary General Table of Contents 1. Introduction 2. Governance and an Enterprise Risk Management (ERM)

Defining the Internal Model for Risk & Capital Management under the Solvency II Directive

14 Defining the Internal Model for Risk & Capital Management under the Solvency II Directive Mark Dougherty is an international Senior Corporate Governance and Risk Management professional and Chartered

14 Defining the Internal Model for Risk & Capital Management under the Solvency II Directive Mark Dougherty is an international Senior Corporate Governance and Risk Management professional and Chartered

Regulation and risk The strategic response to insurance regulatory developments Alex Thomson, May 2013

Regulation and risk The strategic response to insurance regulatory developments Alex Thomson, May 2013!@# Agenda 1. Strategic priorities and regulation 2. Global insurance regulatory developments 3. East

Regulation and risk The strategic response to insurance regulatory developments Alex Thomson, May 2013!@# Agenda 1. Strategic priorities and regulation 2. Global insurance regulatory developments 3. East

Proposal for a Directive on Reinsurance Supervision Frequently Asked Questions (see also IP/04/513)

") MEMO/04/90 Brussels, 21 April 2004 Proposal for a Directive on Reinsurance Supervision Frequently Asked Questions (see also IP/04/513) What are the main objectives of the proposal? The proposed Directive

MEMO/04/90 Brussels, 21 April 2004 Proposal for a Directive on Reinsurance Supervision Frequently Asked Questions (see also IP/04/513) What are the main objectives of the proposal? The proposed Directive

Emerging from the Crisis Building a Stronger International Financial System

Secrétariat général de la Commission bancaire Emerging from the Crisis Building a Stronger International Financial System Session 4: Issues Highlighted by the Crisis: Expanding the Regulatory Perimeter

Secrétariat général de la Commission bancaire Emerging from the Crisis Building a Stronger International Financial System Session 4: Issues Highlighted by the Crisis: Expanding the Regulatory Perimeter

Risk management framework Under Solvency II

Risk management framework Under Solvency II ICISA WORKING GROUP / 09 06 EH GRC Jean-Francois DECROOCQ Risk management under SII- PASA 09/2006 JF DECROOCQ 1 SOLVENCY II ENVIRONMENT The evolution of regulation

Risk management framework Under Solvency II ICISA WORKING GROUP / 09 06 EH GRC Jean-Francois DECROOCQ Risk management under SII- PASA 09/2006 JF DECROOCQ 1 SOLVENCY II ENVIRONMENT The evolution of regulation

Draft Application Paper on Group Corporate Governance

Public Draft Application Paper on Group Corporate Governance Draft, 3 March 2017 3 March 2017 Page 1 of 33 About the IAIS The International Association of Insurance Supervisors (IAIS) is a voluntary membership

Public Draft Application Paper on Group Corporate Governance Draft, 3 March 2017 3 March 2017 Page 1 of 33 About the IAIS The International Association of Insurance Supervisors (IAIS) is a voluntary membership

TABLE OF CONTENTS. Lombardi, Chapter 1, Overview of Valuation Requirements. A- 22 to A- 26

iii TABLE OF CONTENTS FINANCIAL REPORTING PriceWaterhouseCoopers, Chapter 3, Liability for Income Tax. A- 1 to A- 2 PriceWaterhouseCoopers, Chapter 4, Income for Tax Purposes. A- 3 to A- 6 PriceWaterhouseCoopers,

iii TABLE OF CONTENTS FINANCIAL REPORTING PriceWaterhouseCoopers, Chapter 3, Liability for Income Tax. A- 1 to A- 2 PriceWaterhouseCoopers, Chapter 4, Income for Tax Purposes. A- 3 to A- 6 PriceWaterhouseCoopers,

IFRS 4 Phase 2 Insurance contracts Update on the industry s response. December 2, 2010

IFRS 4 Phase 2 Insurance contracts Update on the industry s response December 2, 2010 Contents Introduction Jacques Tremblay 3 Goal of IFRS Phase 2 Timeline Overview building blocks of the measurement

IFRS 4 Phase 2 Insurance contracts Update on the industry s response December 2, 2010 Contents Introduction Jacques Tremblay 3 Goal of IFRS Phase 2 Timeline Overview building blocks of the measurement

Risk-based Global Insurance Capital Standard Version 1.0 for Extended Field Testing

Public Risk-based Global Insurance Capital Standard Version 1.0 for Extended Field Testing 21 July 2017 21 July 2017 Page 1 of 124 About the IAIS The International Association of Insurance Supervisors

Public Risk-based Global Insurance Capital Standard Version 1.0 for Extended Field Testing 21 July 2017 21 July 2017 Page 1 of 124 About the IAIS The International Association of Insurance Supervisors

The valuation of insurance liabilities under Solvency 2

The valuation of insurance liabilities under Solvency 2 Introduction Insurance liabilities being the core part of an insurer s balance sheet, the reliability of their valuation is the very basis to assess

The valuation of insurance liabilities under Solvency 2 Introduction Insurance liabilities being the core part of an insurer s balance sheet, the reliability of their valuation is the very basis to assess

A. General comments. October 27, 2012

AEGON N.V./Transamerica comments on Comparing Certain Aspects of the Insurance Supervisory and Regulatory Regimes in the European Union and the United States October 27, 2012 AEGON appreciates the opportunity

AEGON N.V./Transamerica comments on Comparing Certain Aspects of the Insurance Supervisory and Regulatory Regimes in the European Union and the United States October 27, 2012 AEGON appreciates the opportunity

January CNB opinion on Commission consultation document on Solvency II implementing measures

NA PŘÍKOPĚ 28 115 03 PRAHA 1 CZECH REPUBLIC January 2011 CNB opinion on Commission consultation document on Solvency II implementing measures General observations We generally agree with the Commission

NA PŘÍKOPĚ 28 115 03 PRAHA 1 CZECH REPUBLIC January 2011 CNB opinion on Commission consultation document on Solvency II implementing measures General observations We generally agree with the Commission

Actuarial Roles under the Solvency II Framework Dr. Huijuan Liu

Actuarial Roles under the Solvency II Framework Dr. Huijuan Liu Actuarial conference for supervisors 4 June 2014 Setting the scene Solvency II where do the actuaries fit? 2 Agenda The actuaries and the

Actuarial Roles under the Solvency II Framework Dr. Huijuan Liu Actuarial conference for supervisors 4 June 2014 Setting the scene Solvency II where do the actuaries fit? 2 Agenda The actuaries and the

ORSA An international requirement

Prepared by: Padraic O'Malley, Principal, Dublin Eamonn Phelan, Principal, Dublin December 2013 ORSA An international requirement Title Author a [Footer - regular] Month YYYY Title Author b [Footer - regular]

Prepared by: Padraic O'Malley, Principal, Dublin Eamonn Phelan, Principal, Dublin December 2013 ORSA An international requirement Title Author a [Footer - regular] Month YYYY Title Author b [Footer - regular]

CEA response to CEIOPS request on the calculation of the group SCR

Position CEA response to CEIOPS request on the calculation of the group SCR CEA reference: ECO-SLV-09-060 Date: 27 February 2009 Referring to: Related CEA documents: CEIOPS request on the calculation of

Position CEA response to CEIOPS request on the calculation of the group SCR CEA reference: ECO-SLV-09-060 Date: 27 February 2009 Referring to: Related CEA documents: CEIOPS request on the calculation of

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar I - Sub Committee Capital Resources and Capital Requirements Task Groups Discussion Document 53 (v 10) Treatment of participations in the solo entity submission

Solvency Assessment and Management: Pillar I - Sub Committee Capital Resources and Capital Requirements Task Groups Discussion Document 53 (v 10) Treatment of participations in the solo entity submission

LONGEVITY SWAPS. Impact of Solvency II AN EFFECTIVE, INNOVATIVE WAY TO MANAGE THE LONGEVITY RISK. Presenter: Tom O Sullivan, F.S.A, F.C.I.A, M.A.A.A.

LONGEVITY SWAPS AN EFFECTIVE, INNOVATIVE WAY TO MANAGE THE LONGEVITY RISK Impact of Solvency II Presenter: Tom O Sullivan, F.S.A, F.C.I.A, M.A.A.A. Date: December 3, 2010 AGENDA 1. Solvency II - Background

LONGEVITY SWAPS AN EFFECTIVE, INNOVATIVE WAY TO MANAGE THE LONGEVITY RISK Impact of Solvency II Presenter: Tom O Sullivan, F.S.A, F.C.I.A, M.A.A.A. Date: December 3, 2010 AGENDA 1. Solvency II - Background

EIOPA: recent developments in insurance and pensions. EVCA Investors' Forum Geneva, 14 March 2012

EIOPA: recent developments in insurance and pensions EVCA Investors' Forum Geneva, 14 March 2012 Content What is EIOPA? Recent developments on Solvency II EIOPA s advice on pensions 2 EIOPA: Background

EIOPA: recent developments in insurance and pensions EVCA Investors' Forum Geneva, 14 March 2012 Content What is EIOPA? Recent developments on Solvency II EIOPA s advice on pensions 2 EIOPA: Background

Session 31PD: Life Insurance Capital Framework in Canada. Moderator: Presenters: Ritchie Hok FSA Lisa Marie Peterson FSA,FCIA

Session 31PD: Life Insurance Capital Framework in Canada Moderator: Presenters: Ritchie Hok FSA Lisa Marie Peterson FSA,FCIA SOA Antitrust Disclaimer SOA Presentation Disclaimer A New Chapter in Capital

Session 31PD: Life Insurance Capital Framework in Canada Moderator: Presenters: Ritchie Hok FSA Lisa Marie Peterson FSA,FCIA SOA Antitrust Disclaimer SOA Presentation Disclaimer A New Chapter in Capital

SAIA SAM PSO. Issue 3 / ORSA: meeting the challenge and seeking the value

SAIA SAM PSO Issue 3 / 2011 ORSA: meeting the challenge and seeking the value Insurers preparing for Solvency II are finding that meeting the requirements for the Own Risk and Solvency Assessment (ORSA)

SAIA SAM PSO Issue 3 / 2011 ORSA: meeting the challenge and seeking the value Insurers preparing for Solvency II are finding that meeting the requirements for the Own Risk and Solvency Assessment (ORSA)

Solvency II Update. Craig McCulloch

Solvency II Update Craig McCulloch Agenda SII overview Latest Developments Legislative timetable Current regulatory progress Implementation measures QIS4 results & implications Australian Implications

Solvency II Update Craig McCulloch Agenda SII overview Latest Developments Legislative timetable Current regulatory progress Implementation measures QIS4 results & implications Australian Implications

Essential adjustments for the success of Solvency II for groups

Position Paper Essential adjustments for the success of Solvency II for groups (based on the findings from QIS5 for groups and the current discussion on implementing measures) CEA reference: ECO-SLV-11-729

Position Paper Essential adjustments for the success of Solvency II for groups (based on the findings from QIS5 for groups and the current discussion on implementing measures) CEA reference: ECO-SLV-11-729

Current status of Solvency II and challenges down the line. Matthew Edwards 11 October 2011

Current status of Solvency II and challenges down the line Matthew Edwards 11 October 2011 Solvency II Timeline Page 2 15 September 2011 UK Life Solvency II Discussion Forum Regulatory timelines Level

Current status of Solvency II and challenges down the line Matthew Edwards 11 October 2011 Solvency II Timeline Page 2 15 September 2011 UK Life Solvency II Discussion Forum Regulatory timelines Level

LICAT Overview. December 1 st, Jacques Tremblay, FCIA, FSA, MAAA

LICAT Overview December 1 st, 2017 Jacques Tremblay, FCIA, FSA, MAAA 1. Introduction Choosing a risk based capital framework Will the new LICAT fit the bill for Caribbean regulators? Versions of MCCSR

LICAT Overview December 1 st, 2017 Jacques Tremblay, FCIA, FSA, MAAA 1. Introduction Choosing a risk based capital framework Will the new LICAT fit the bill for Caribbean regulators? Versions of MCCSR

Insurance Summit Mr Raymond Tam Executive Director (Policy and Development) Insurance Authority 21 September 2017

Insurance Authority 21 September 2017") Insurance Summit 2017 Mr Raymond Tam Executive Director (Policy and Development) Insurance Authority 21 September 2017 Priority of Policy Initiatives Development of risk-based capital regime Facilitation

Insurance Summit 2017 Mr Raymond Tam Executive Director (Policy and Development) Insurance Authority 21 September 2017 Priority of Policy Initiatives Development of risk-based capital regime Facilitation