Indian Accounting Standards (Ind AS)

|

|

|

- Ashlynn Black

- 5 years ago

- Views:

Transcription

1 Indian Accounting Standards (Ind AS)

2 Applicability to Companies Phase I Phase II Voluntary adoption Year of adoption FY FY FY or thereafter Comparative year FY FY FY or thereafter Covered Companies (a) Listed companies (b) Unlisted companies (c) Group Companies All companies with net worth of >= 500 crores All companies with net worth of >= 500 crores All companies listed or in the process of being listed All companies with net worh of >= 250 crores All companies could voluntarily adopt Applicable to holding, subsidiaries, joint ventures, or associates of Companies covered in (a) and (b) above The net worth, for this purpose, shall be calculated based on stand-alone financial statements of the Company as on March 31, 2014 or the first audited financial statements for the accounting period ending subsequently.

3

4 Key areas of difference Topic IFRS Indian GAAP Ind AS Statement of changes in equity Restatement Single entity Vs Consolidated view Breach of covenants Extraordinary items A separate statement showing total comprehensive income, showing separately the amounts attributable to parent and controlling interests. When a change in accounting policy is applied retrospectively or items of financial statements have been reclassified, a statement of financial position is required as at the beginning of the earliest period presented No such separate statement is required No such requirement Required as part of balance sheet. Consolidated view Single entity view Single entity view Non current if the lender has agreed to provide grace period before the end of the reporting period. Presentation of extraordinary items is prohibited Under Indian context, generally continued to be disclosed as non-current (Revised Sch VI) Disclosed separately in a statement of profit and loss. Classification based only on the nature of expense

5 Key areas of difference Topic IFRS Indian GAAP Ind AS Statement of cash flows Bank overdrafts Cash flows Interest dividends Cash flows - Changes in ownership interests Cash flows investing activities Changes in accounting policies and errors Errors New accounting pronouncements Included as part of cash and cash equivalents if they form an integral part of the entity s cash management Classified as operating, investing financing activities in a consistent manner Considered as financing activities Guidance for financial enterprises and other enterprises Financing activities No specific guidance Only expenditures resulting in a recognised asset is considered as investing activities Retrospective application with presentation of third balance sheet Requires retrospective application; Third balance sheet Specific requirement to disclose the impact of newly issued accounting pronouncements not yet adopted by the Company No specific guidance No such requirement for third balance sheet Only disclosure shall be made in the financial statements No need to disclose Absence of literature Similar to the framework of IASB No specific guidance IASB, then others

6 Key areas of difference Topic IFRS Indian GAAP Ind AS Presentation of critical judgements Inventories Inventories Deferred income taxes Deferred tax on unrealised intra-group profits Deferred tax assets Deferred tax impact on business combinations Requires disclosure of critical accounting judgements Measurement exception for inventories held by commodity traders Write-down of inventory is reversed if circumstances that previously caused write-down no longer exist. No specific requirement under AS 1 No scope exclusion under Indian GAAP Non specific guidance in AS-2 for reversal of write-down. Balance sheet approach Income statement approach Deferred tax is recognised using buyer s rate. To the extent there is a virtual certainty supported by convincing evidence that there will be a future income. Recognised except on the goodwill No deferred tax is recognised. It is probable that the future taxable profits will be available against which the unused tax losses and tax credits can be utilised No specific guidance.

7 Key areas of difference Topic IFRS Indian GAAP Ind AS Deferred taxes disclosures Requires disclosure of rate reconciliation, tax holidays and expiry, unrecognised deferred tax liability on undistributed tax earnings Not required to be disclosed PPE depreciation Componentised and depreciated separately No requirement to componentise Property, plant and equipment Cost of major inspections and replacements Cost of major inspections and overhauls is recognised in the carrying amount of the asset Generally expensed when incurred PPE- residual value Estimates of residual value are to be updated at every reporting date Not required to be updates PPE - change in method of depreciation Considered prospectively Requires retrospective recomputation and adjustment in the current period PPE presentation of capital advances Usually included in the capitalwork-in-progress Disclosed as part of long-term advances

8 Key areas of difference Topic IFRS Indian GAAP Ind AS Leases lease of land Recorded as operating lease or finance lease as per criteria. Generally, operating. Generally recorded as fixed asset. Leases determining whether an arrangement contains lease Arrangements that do not take the form of lease but fulfillment of which is dependent on use of specific asset which convey the right to use are accounted as lease No specific guidance. Payments under such arrangements are recognised in accordance with nature of expenses incurred Lease- operating lease incentives Recognised as reduction from rental income or expense over the lease term No specific guidanace Revenue principal vs agent IAS 18 provides guidance to determine whether an entity is acting as a principal or as an agent No specific guidance

9 Key areas of difference Topic IFRS Indian GAAP Ind AS Revenue consideration Revenue exchange transactions Revenue interest income Multiple deliverables Unit of accounting Customer loyalty programmes Government grants government loans below the market rate of interest Recognised at the fair value of the consideration receivable To be recognised at fair value if the transaction has commercial substance Recognised using effective interest rate method No specific guidance (IFRS 15 has incorporated sufficient guidance) Fair value of the credit points is deferred and recognised when redeemed or lapsed Recognised at the nominal value of the consideration receivable No specific guidance Recognised on time proportion basis No specific guidance No specific guidance No specific guidance as of now. Recorded as government grant No specific guidance

10 Key areas of difference Topic IFRS Indian GAAP Ind AS Effects of changes in foreign currency rates Concept of functional currency Integral and non-integral approach Effects of changes in foreign currency ratesderivatives IAS 39 / IFRS 9 requires entity to apply mark to market accounting AS 11 is applied for forwards; AS 1 is applied for other derivatives requires the entity to recognised only loss (if AS 30 is not early adopted) Consolidated financial statements Mandatory requirement on entities to prepare consolidated financial statements No specific mandate. Governed by the statutes in India Similar to the existing Indian GAAP Consolidated financial statements Control Control exists when the entity is exposed to, or has the ability to affect the returns through power over other entity. Primarily ownership driven either by equity share holding or through composition of the Board

11 Key areas of difference Topic IFRS Indian GAAP Ind AS Consolidated financial statements potential voting rights Considered if they are currently exercisable Not considered in assessing the control Minority interest / Non-controlling interest Presented in the statement of financial position with in equity, separately from equity of owners Presented separately from liabilities a d o e s equity. Joint ventures Equity method of accounting Shall be presented using the proportionate consolidation method (Accounting for KRRP would be impacted) Financial instruments IFRS 9 provides a detailed guidance As 30, 31 and 32 are not yet notified by the Companies (Accounting Standards) rules, Can be adopted to the extent they do not contradict with other existing standards

12 Key areas of difference Topic IFRS Indian GAAP Ind AS Allocation of losses to noncontrolling interest holders Special purpose entities Amortisation of goodwill Impairment loss on goodwill Reversal Provisions, contingent liabilities discounting Can be allocated even if the amount becomes negative Separate guidance is available under IFRS 10 Cannot be amortised. Shall be tested for impairment on at least on an annual basis Minority interest cannot be negative. It can at the most be zero No separate guidance is available under Indian GAAP Can be amortised. Cannot be reversed Can be reversed Discounted to present value of the effect of time value is material No concept of discounting. Provisions and liabilities are carried at full values

13 Key areas of difference Topic IFRS Indian GAAP Ind AS Business combinations IFRS 3 provides detailed guidance No specific guidance. AS 21 or AS 14 is used appropriately. Both the standards, require the acquirer to consider book values of acquiree. Consequently goodwill amount would be significantly high. Segment reporting Identified based on financial information regularly reviewed by CODM Requires an enterprise to identify two segments Business and geographical Intangibles No guidance on acquisition of In process R&D Acquisition of in process R&D shall be capitalised on the date of acquisition at its acquisition value Proposed dividend Recognised in the period in which it is approved by shareholders Recognised in the period in which it is proposed by the Board. Employee benefits Actuarial gains or losses Recognised immediately in OCI Recognised immediately in profit and loss Recognised immediately in OCI

14 Challenges associated with Ind AS 115 Areas where significant changes in accounting are expected Su sidized se i es/p odu ts; Li e ses; Milesto e pay e ts; Multiple ele e t a a ge e ts Key requirements of the standard: Ne si gle fi e step e e ue e og itio odel; Ti i g of e og itio of e e ue Point in time Vs over the period; Fai alue Vs sta dalo e alue; Multiple ele e t a a ge e ts Fair value of each component Revenue recognition TODAY AS 9/IAS 18 Associated challenges: Transition related Full retrospective Vs modified retrospective approach; Increased management judgement; Gathering of data and analysis of transactions; Disclosure modifications; Stake holder communications and Training and education to the controllers and Ongoing monitoring Revenue recognition TOMORROW (Ind AS 115)

15 Challenges associated with Ind AS 109 Areas where significant changes in accounting are expected Investments in mutual funds; Provisions for bad and doubtful debts; Hedging; Key requirements of the standard: Categories of Investments - FVTPL/FVTOCI and Amortized cost ; All investments are generally measured at fair value; Impairment of financial assets Expected loss model; Increased disclosures Financial Instruments TODAY AS 11 and AS 30/IAS 39 Associated challenges: Increased management judgement (hedge accounting); Strengthening of documentation due to expected credit loss model; Disclosure modifications; Stake holder communications and Training and education to the controllers and ongoing monitoring Financial Instruments TOMORROW (Ind AS 109)

16 Impact on first time adoption Comparatives It is optional for entities to present comparative information under Ind AS in the first year. In other words, the first time adopter shall present latest corresponding previous period s financial statements prepared as per previous GAAP (existing Indian GAAP). However, such previous GAAP financial statements shall be reclassified to the extent possible and practicable, when presenting the first Ind AS financial statements. Optional exemptions from retrospective application of Ind AS Exemption Business Combination Share based payments Fair value as deemed cost Cumulative transition differences Investments in subsidiaries, jointly controlled entities Implication of exemption Option to apply business combination accounting for all combinations after the transition date or from a date before the transition date Share based payments which are not vested at the date of transition will be accounted in accordance with Ind AS 102 An entity can use fair value as the deemed cost on transition date for PPE and intangible assets Entities can set FCTR to zero for all subsidiaries Entities can choose to fair value as per Ind AS 39 or carrying amount under the previous GAAP

17 Impact on first time adoption Optional exemptions from retrospective application of Ind AS Exemption Designation of previously recognised financial instruments Use of fair value on the transition date for financial instruments Non-current assets held for sale Implication of exemption Option to designate financial assets as AFS of FVTPL provided the asset meets the criteria for designation on the transition date. Choice to apply fair value on transition date as the new amortised cost instead of retrospective application of effective interest rate method Entities can measure non-current assets held for sale and discontinued operations at lower of carrying amount and fair value as on transition date. Mandatory exception Retrospective application of some aspects of Ind AS is prohibited Exemption Estimates Hedge accounting Non controlling interests Implication of exemption Estimates in the previous GAAP can be changed only if erroneous If a hedge does not meet the conditions for hedge under Ind AS 39, the entity shall discontinue hedge accounting. Provisions relating to NCI have to be applied prospectively

18 Ind AS 101 Objective of Ind-AS 101 This standard provides the principles of accounting for an Indian company while adopting Ind-AS for the first time. This standard ensures that: A o pa y s fi st Ind-AS financial statements, and its interim financial reports contained within the period covered by those Financial Statements, comprises high quality information; The information so used: is transparent and comparable over all periods presented; caters as an appropriate initial point for accounting as per Ind-ASs; and can be produced at a cost that does not exceed the paybacks. Use of Ind-AS A company is required to use Ind-AS for the following: Fi st Ind-AS compliant Financial Statements; and Ea h i te i fi a ial epo t fo pa t of the pe iod o e ed y its fi st Ind-AS Financial Statements. The sta da d la ifies that a e tity's fi st fi a ial state e t a e the fi st a ual fi a ial statements in which the entity adopts Ind-AS in accordance with Ind-ASs notified under the Companies Act, 2013, by an explicit and unreserved statement in those financial statements of compliance with Ind-AS.

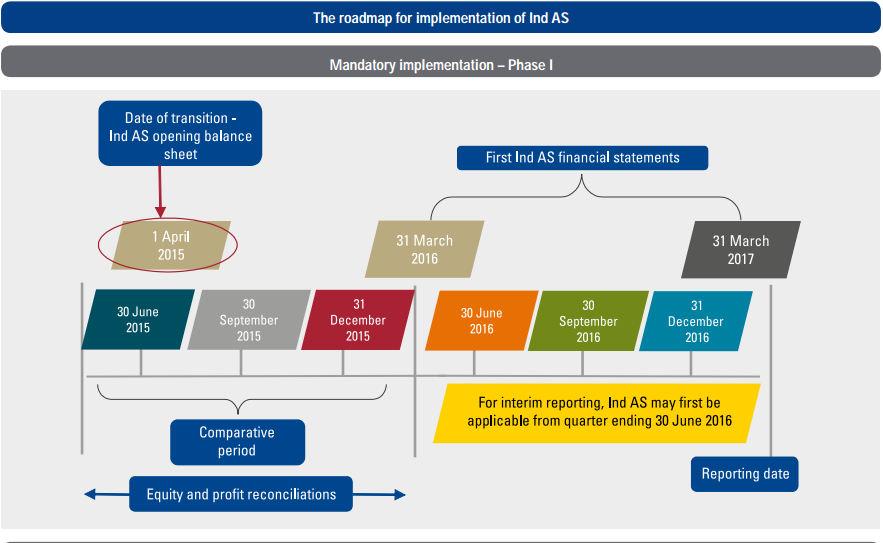

19 Ind AS 101 Opening Ind-AS Balance Sheet On adoption of Ind-AS, a company is required to prepare and present an opening Ind-AS Balance Sheet BS at the t a sitio date. Transition date is defined as the beginning of the earliest comparative period presented on the basis of Ind-AS.. This is the sta ti g poi t fo a o pa y s a ou ti g i a o da e ith Ind-AS and all adjustments arising from the transition to Ind-AS are be recorded in the retained earnings as at the transition date (i.e. on 1 April 2015 for the companies covered under Phase-I) An entity shall also explain how the transition from previous GAAP to Ind ASs affected its reported BS, financial performance and cash flows. Opening reconciliation Ind-AS 101 also requires that a detailed quantitative reconciliation is to be included in the first Ind-AS financial statements. With respect to the financial statements for the year , the companies covered under phase-i shall explain the reason for the difference between the net equity as at 1 April 2015 and 31 March 2016, prepared under the existing Indian GAAP and under Ind-AS. In addition, these companies shall also provide reconciliation for its total comprehensive income for the FY to explain the impact of the transition.

20 Ind AS 101 Comparatives for first Ind-AS BS A o pa y s fi st Ind AS Financial Statements shall have at least 3 Balance Sheets, 2 Statements of profit and loss, 2 Statements of cash flows and 2 Statements of changes in equity and related notes, including comparative information for all statements presented. For companies covered under phase-i, the first reportable period is the year Therefore, their transition date is 1 April Such companies will present its Financial Statements as per existing Indian GAAP upto 31 March Thereafter these companies are required to apply the Ind ASs effective for periods ending on 31 March 2017 in: p epa i g a d p ese ti g its ope i g Ind AS-BS at 1 April 2015; p epa i g a d p ese ti g its BS fo Ma h ith o pa ati es fo the yea e ded Ma h 2016); state e t of p ofit a d loss, state e t of ha ges i e uity a d state e t of ash flo s fo the yea to 31 March 2017 (with comparatives for the year ended 31 March 2016); and dis losu es i ludi g o pa ati e i fo atio fo the yea e ded Ma h. A company which wishes to additionally provide any Financial Statements containing historical summaries or comparative information in accordance with existing Indian GAAP, then it shall: a k these i fo atio as ot ei g p epa ed i a o da e ith Ind-ASs; and dis lose the atu e of the o e adjust e ts that ould ake it o ply ith Ind ASs. However, there is no necessity to quantify these adjustments.

21 Ind AS 101 Accounting Policies A company preparing the Ind-AS Financial Statements for the first time: shall hoose the a ou ti g poli ies o plia t ith Ind-AS, effective at its first annual Ind-AS reporting date with certain exceptions; shall ge e ally apply these a ou ti g poli ies et ospe ti ely hile p epa i g the ope i g BS sheet and for all periods presented in the first Ind-AS BS; shall ot apply diffe e t e sio s of Ind-ASs that were effective at earlier dates; and ay apply a e ised Ind-AS which is non-mandatory, if that Ind-AS permits early adoption Recognition and de-recognition With certain exceptions, a company while preparing its opening Ind-AS BS shall: e og ise all assets a d lia ilities hose e og itio is e ui ed i a o da e ith Ind-ASs; de-recognize all assets or liabilities in case Ind-ASs prohibit such recognition; e lassify asset, lia ility o o po e t of e uity i a o da e ith Ind-ASs; and apply Ind-ASs for the purpose of measuring all recognised assets and liabilities. Presentation and Disclosure IND-AS-101 does not provide any exemption from the presentation and disclosure requirements of other Ind-ASs.

First-time Adoption of Indian Accounting Standards

Indian Accounting Standard (Ind-AS) 101 First-time Adoption of Indian Accounting Standards CONTENTS Paragraph OBJECTIVE 1 SCOPE 2 5 RECOGNITION AND MEASUREMENT 6 19 Opening Ind-AS Balance Sheet 6 Accounting

Indian Accounting Standard (Ind-AS) 101 First-time Adoption of Indian Accounting Standards CONTENTS Paragraph OBJECTIVE 1 SCOPE 2 5 RECOGNITION AND MEASUREMENT 6 19 Opening Ind-AS Balance Sheet 6 Accounting

First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards This version was issued in November 2008. Its effective date is 1 July 2009. It includes

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards This version was issued in November 2008. Its effective date is 1 July 2009. It includes

Introduction to Ind-AS By Neeraj Sharma

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

Impact of Ind AS adoption on Industry Applying it in simple way

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

Overview of Transition to IND-AS. CA Sanjeev Maheshwari

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

BlueScope Financial Report 2013/14

BlueScope Financial Report /14 ABN 16 000 011 058 Annual Financial Report - Page Financial statements Statement of comprehensive income 2 Statement of financial position 4 Statement of changes in equity

BlueScope Financial Report /14 ABN 16 000 011 058 Annual Financial Report - Page Financial statements Statement of comprehensive income 2 Statement of financial position 4 Statement of changes in equity

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell 2 PwC Introduction This pocket guide provides a brief summary of the recognition, measurement, presentation and disclosure requirements

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell 2 PwC Introduction This pocket guide provides a brief summary of the recognition, measurement, presentation and disclosure requirements

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

2009 International Financial Reporting Standards update

2009 International Financial Reporting Standards update Contents Introduction 3 Section 1: New and amended standards and interpretations applicable to December 2009 year-end 5 IFRS 1 First-time Adoption

2009 International Financial Reporting Standards update Contents Introduction 3 Section 1: New and amended standards and interpretations applicable to December 2009 year-end 5 IFRS 1 First-time Adoption

IFRS 1 - First-Time Adoption of IFRS

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD in India Consistently ranked amongst India s top six accounting

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD in India Consistently ranked amongst India s top six accounting

IAS 1 Presentation of Financial Statement

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

Opening balance sheet 1 April Opening balance sheet 1 April Unlisted companies whose net worth is >= INR 250 crores but < INR 500 crores

Step up to Ind AS Ind AS an overview India made a commitment towards the convergence of Indian accounting standards with IFRS at the G20 summit in 2009. In line with this, the Ministry of Corporate Affairs,

Step up to Ind AS Ind AS an overview India made a commitment towards the convergence of Indian accounting standards with IFRS at the G20 summit in 2009. In line with this, the Ministry of Corporate Affairs,

Introduction Consolidated statement of comprehensive income for the year ended 31 December 20XX... 6

PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF International Limited is not responsible for the acts or omissions

PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF International Limited is not responsible for the acts or omissions

IAS 1R- Presentation of Financial Statements. Introduction to IFRS / Ind AS

IAS 1R- Presentation of Financial Statements Introduction to IFRS / Ind AS IAS 1R- Presentation of financial statements Objective The objective of this Standard is to prescribe the basis for presentation

IAS 1R- Presentation of Financial Statements Introduction to IFRS / Ind AS IAS 1R- Presentation of financial statements Objective The objective of this Standard is to prescribe the basis for presentation

OVERVIEW OF IND AS INCLUDING CARVE OUTS. C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

Indian Accounting Standards (Ind AS) AT A GLANCE

AT A GLANCE") Indian Accounting Standards (Ind AS) AT A GLANCE Indian Accounting Standards (Ind AS) An Introduction The Hon'ble Finance Minister in the presentation of the Union Budget for 2014-15, proposed the adoption

Indian Accounting Standards (Ind AS) AT A GLANCE Indian Accounting Standards (Ind AS) An Introduction The Hon'ble Finance Minister in the presentation of the Union Budget for 2014-15, proposed the adoption

Good First-time Adopter (International) Limited

Limited") Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

Consolidated financial statements and independent auditor s report BORETS INTERNATIONAL LIMITED 31 December 2017

Consolidated financial statements and independent auditor s report BORETS INTERNATIONAL LIMITED 31 December 2017 Contents Independent Auditor s Report Consolidated Statement of Financial Position 1 Consolidated

Consolidated financial statements and independent auditor s report BORETS INTERNATIONAL LIMITED 31 December 2017 Contents Independent Auditor s Report Consolidated Statement of Financial Position 1 Consolidated

Pearson plc IFRS Technical Analysis

Pearson plc IFRS Technical Analysis Contents A. Introduction B. Basis of presentation C. UK GAAP to IFRS adjustments D. Performance measures Schedules 1. Income statement Reconciliation UK GAAP to IFRS

Pearson plc IFRS Technical Analysis Contents A. Introduction B. Basis of presentation C. UK GAAP to IFRS adjustments D. Performance measures Schedules 1. Income statement Reconciliation UK GAAP to IFRS

Exposure Draft. Indian Accounting Standard (Ind AS) 101, First-time Adoption of Indian Accounting Standards

101, First-time Adoption of Indian Accounting Standards") Exposure Draft Indian Accounting Standard (Ind AS) 101, First-time Adoption of Indian Accounting Standards (Last date for Comments: November 17, 2014) Issued by Accounting Standards Board The Institute

Exposure Draft Indian Accounting Standard (Ind AS) 101, First-time Adoption of Indian Accounting Standards (Last date for Comments: November 17, 2014) Issued by Accounting Standards Board The Institute

International GAAP Disclosure Checklist

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any

International GAAP Disclosure Checklist

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2015 Effective for entities with a year-end of 30 June 2015 or thereafter

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2015 Effective for entities with a year-end of 30 June 2015 or thereafter

New IFRS standards and interpretations. Warsaw, December 2012

New IFRS standards and interpretations Warsaw, December 2012 Agenda Pronouncements Effective First annual year of application* IFRS 1 First-time Adoption of International Financial Reporting Standards

New IFRS standards and interpretations Warsaw, December 2012 Agenda Pronouncements Effective First annual year of application* IFRS 1 First-time Adoption of International Financial Reporting Standards

Ind-AS 101. First Time adoption of Ind-AS

Ind-AS 101 First Time adoption of Ind-AS 1 Ind-AS 101 : First Time Adoption of Ind-AS 1 04 2016 2 3 Ind-AS 101 : Snap Shot Appendices forming integral part of the Standard A = Defined terms. B = Mandatory

Ind-AS 101 First Time adoption of Ind-AS 1 Ind-AS 101 : First Time Adoption of Ind-AS 1 04 2016 2 3 Ind-AS 101 : Snap Shot Appendices forming integral part of the Standard A = Defined terms. B = Mandatory

First-Time Adoption of International Financial Reporting Standards

Audit and Assurance First-Time Adoption of International Financial Reporting Standards Discussion Paper December 2003 Contents Contents 1. Executive Summary 3 2. Harmonisation in New Zealand 4 3. Application

Audit and Assurance First-Time Adoption of International Financial Reporting Standards Discussion Paper December 2003 Contents Contents 1. Executive Summary 3 2. Harmonisation in New Zealand 4 3. Application

March 2018 IFRS and Austrian GAAP Similarities and Differences

www.pwc.com/at March 2018 IFRS and Austrian GAAP Similarities and Differences IFRS and Austrian GAAP: Similarities and Differences March 2018 Table of Contents Introduction... 3 Accounting Framework...

www.pwc.com/at March 2018 IFRS and Austrian GAAP Similarities and Differences IFRS and Austrian GAAP: Similarities and Differences March 2018 Table of Contents Introduction... 3 Accounting Framework...

Statement by Directors. Independent Audit Report. Consolidated statement of comprehensive income. Consolidated statement of financial position

CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER Contents Di e to s epo t 2 4 Statement by Directors 5 Independent Audit Report 6 Consolidated statement of comprehensive income 7 Consolidated statement

CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER Contents Di e to s epo t 2 4 Statement by Directors 5 Independent Audit Report 6 Consolidated statement of comprehensive income 7 Consolidated statement

International GAAP Disclosure Checklist

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

International GAAP Disclosure Checklist

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 31 August 2015 International GAAP Disclosure Checklist Updated: August 2015 For

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 31 August 2015 International GAAP Disclosure Checklist Updated: August 2015 For

Ind AS 1 st Time Adoption Challenges. Compiled By Ca Yagnesh Desai ,

Ind AS 1 st Time Adoption Challenges Compiled By Ca Yagnesh Desai. ymdesaiandco@gmail.com +09820133227,0932244770 1 Ind AS 1 : First Time Adoption of Ind AS 1 04? 2 3 Ind-AS 101 : Snap Shot Total Clauses

Ind AS 1 st Time Adoption Challenges Compiled By Ca Yagnesh Desai. ymdesaiandco@gmail.com +09820133227,0932244770 1 Ind AS 1 : First Time Adoption of Ind AS 1 04? 2 3 Ind-AS 101 : Snap Shot Total Clauses

Global vision backed by local knowledge. IND AS - APPLICATION, ANALYSIS & MAT Financial Year ended 31 March 2017 THE POWER OF BEING UNDERSTOOD

Global vision backed by local knowledge IND AS - APPLICATION, ANALYSIS & MAT Financial Year ended 31 March 2017 THE POWER OF BEING UNDERSTOOD IN INDIA India (comprising of Astute Consulting Group and affiliates)

Global vision backed by local knowledge IND AS - APPLICATION, ANALYSIS & MAT Financial Year ended 31 March 2017 THE POWER OF BEING UNDERSTOOD IN INDIA India (comprising of Astute Consulting Group and affiliates)

IMPORTANT TAKEAWAYS ON IFRS

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

International GAAP Disclosure Checklist

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

IND AS IMPLEMENTATION PRELIMINARY IMPACT ASSESSMENT ON SASKEN FINANCIAL STATEMENTS

IND AS IMPLEMENTATION PRELIMINARY IMPACT ASSESSMENT ON SASKEN FINANCIAL STATEMENTS 1 Contents 1. Context 2. Scope of the Presentation 3. Key Standards with an Impact 4. Draft Opening Balance Sheet 5. Draft

IND AS IMPLEMENTATION PRELIMINARY IMPACT ASSESSMENT ON SASKEN FINANCIAL STATEMENTS 1 Contents 1. Context 2. Scope of the Presentation 3. Key Standards with an Impact 4. Draft Opening Balance Sheet 5. Draft

Investment Corporation of Dubai and its subsidiaries

Investment Corporation of Dubai and its subsidiaries CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 Investment Corporation of Dubai and its subsidiaries CONSOLIDATED INCOME STATEMENT Year ended 31

Investment Corporation of Dubai and its subsidiaries CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 Investment Corporation of Dubai and its subsidiaries CONSOLIDATED INCOME STATEMENT Year ended 31

1 Good Company FTA (India) Limited

Limited") 1 Good Company FTA (India) Limited 2 Good Company FTA (India) Limited & Young LLP Contents Introduction... 6 Objective... 6 Consolidated Balance Sheet... 10 Consolidated Statement of Profit & Loss... 13

1 Good Company FTA (India) Limited 2 Good Company FTA (India) Limited & Young LLP Contents Introduction... 6 Objective... 6 Consolidated Balance Sheet... 10 Consolidated Statement of Profit & Loss... 13

Interim Financial Reporting

Indian Accounting Standard (Ind AS) 34 Interim Financial Reporting (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type

Indian Accounting Standard (Ind AS) 34 Interim Financial Reporting (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type

Financial statements. Consolidated financial statements. Company financial statements

73 Consolidated financial statements 74 CONSOLIDATED INCOME STATEMENT 74 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 75 CONSOLIDATED BALANCE SHEET 76 CONSOLIDATED CASH FLOW STATEMENT 78 CONSOLIDATED

73 Consolidated financial statements 74 CONSOLIDATED INCOME STATEMENT 74 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 75 CONSOLIDATED BALANCE SHEET 76 CONSOLIDATED CASH FLOW STATEMENT 78 CONSOLIDATED

Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ]

![Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ]](/thumbs/74/70304882.jpg "Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ]") Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ] Applicability of Ind AS (India s convergence with International Financial Reporting Standards) On February 16, 2015, the Ministry

Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ] Applicability of Ind AS (India s convergence with International Financial Reporting Standards) On February 16, 2015, the Ministry

MB Petroleum Services LLC and its subsidiaries FINANCIAL REVIEW

MB Petroleum Services LLC and its subsidiaries FINANCIAL REVIEW 30 June 2011 Review Report and financial information for 6 months period ended 30 June 2011 Pages 1. Summary of Financial Data 1-2 2. Financial

MB Petroleum Services LLC and its subsidiaries FINANCIAL REVIEW 30 June 2011 Review Report and financial information for 6 months period ended 30 June 2011 Pages 1. Summary of Financial Data 1-2 2. Financial

Unaudited consolidated interim financial statements and independent auditor s review report BORETS INTERNATIONAL LIMITED 30 June 2015

Unaudited consolidated interim financial statements and independent auditor s review report BORETS INTERNATIONAL LIMITED 30 June 2015 Contents Independent Auditor s Review Report Unaudited Consolidated

Unaudited consolidated interim financial statements and independent auditor s review report BORETS INTERNATIONAL LIMITED 30 June 2015 Contents Independent Auditor s Review Report Unaudited Consolidated

Sri Lanka Accounting Standard SLFRS 1. First-time Adoption of Sri Lanka Accounting Standards (SLFRSs)

") Sri Lanka Accounting Standard SLFRS 1 First-time Adoption of Sri Lanka Accounting Standards (SLFRSs) CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD SLFRS 1 FIRST-TIME ADOPTION OF SRI LANKA ACCOUNTING

Sri Lanka Accounting Standard SLFRS 1 First-time Adoption of Sri Lanka Accounting Standards (SLFRSs) CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD SLFRS 1 FIRST-TIME ADOPTION OF SRI LANKA ACCOUNTING

Stay informed. Visit IFRS pocket guide 2012

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

Ind-AS Implementation Issues. Himanshu Kishnadwala

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Example Consolidated Financial Statements. International Financial Reporting Standards (IFRS) Illustrative Corporation Group 31 December 2010

Illustrative Corporation Group 31 December 2010") Example Consolidated Financial Statements International Financial Reporting Standards (IFRS) Illustrative Corporation Group 1 Introduction 2010 The preparation of financial statements in accordance with

Example Consolidated Financial Statements International Financial Reporting Standards (IFRS) Illustrative Corporation Group 1 Introduction 2010 The preparation of financial statements in accordance with

IFRS for SMEs IFRS Foundation-World Bank

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

BLUESCOPE STEEL LIMITED FINANCIAL REPORT 2011/2012

BLUESCOPE STEEL LIMITED FINANCIAL REPORT / ABN 16 000 011 058 Annual Financial Report - Page Financial statements Statement of comprehensive income 2 Statement of financial position 3 Statement of changes

BLUESCOPE STEEL LIMITED FINANCIAL REPORT / ABN 16 000 011 058 Annual Financial Report - Page Financial statements Statement of comprehensive income 2 Statement of financial position 3 Statement of changes

A Comparative Analysis of PERS, MPERS and MFRS Frameworks

A Comparative Analysis of PERS, MPERS and MFRS Frameworks By Tan Liong Tong 1. Introduction In February 2014, the MASB issued Malaysian Private Entities Reporting Standard (MPERS) and this sets a new milestone

A Comparative Analysis of PERS, MPERS and MFRS Frameworks By Tan Liong Tong 1. Introduction In February 2014, the MASB issued Malaysian Private Entities Reporting Standard (MPERS) and this sets a new milestone

Disclosure on transition to IFRS

- 13 - Disclosure on transition to The Company adopted in preparing its consolidated financial statements for the fiscal year ended March 31, 2017. The date of transition to is April 1, 2015. (1) First-time

- 13 - Disclosure on transition to The Company adopted in preparing its consolidated financial statements for the fiscal year ended March 31, 2017. The date of transition to is April 1, 2015. (1) First-time

11 Consolidated Statement of Profit or Loss and Other Comprehensive Income Year ended Notes 2017 2016 $ 000 $ 000 Revenue 19 16,513,084 15,780,756 Earnings before interest, depreciation, amortisation,

11 Consolidated Statement of Profit or Loss and Other Comprehensive Income Year ended Notes 2017 2016 $ 000 $ 000 Revenue 19 16,513,084 15,780,756 Earnings before interest, depreciation, amortisation,

ACCOUNTING POLICIES 1 PRESENTATION OF FINANCIAL STATEMENTS MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 17

20 ACCOUNTING POLICIES FOR THE YEAR ENDED 30 JUNE 2017 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 Basis of preparation These consolidated and separate financial statements have been prepared under the

20 ACCOUNTING POLICIES FOR THE YEAR ENDED 30 JUNE 2017 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 Basis of preparation These consolidated and separate financial statements have been prepared under the

IFRS compared to US GAAP: An overview

compared to GAAP: An overview November 2014 kpmg.com/ifrs KPMG s Global Institute KPMG s Global Institute provides information and resources to help board and audit committee members gain insight and access

compared to GAAP: An overview November 2014 kpmg.com/ifrs KPMG s Global Institute KPMG s Global Institute provides information and resources to help board and audit committee members gain insight and access

Consolidated income statement for for the year ended 31 January 2017

Consolidated income statement for for the year ended 31 January Revenue 3 871.3 963.2 Cost of sales 3 (422.7) (544.2) Gross profit 448.6 419.0 Administrative and selling expenses 4 (251.6) (227.3) Investment

Consolidated income statement for for the year ended 31 January Revenue 3 871.3 963.2 Cost of sales 3 (422.7) (544.2) Gross profit 448.6 419.0 Administrative and selling expenses 4 (251.6) (227.3) Investment

Comparative statement on Indian GAAP and IFRS

Comparative statement on Indian GAAP and IFRS (As on 1 January 2010) 2010 edition Contents i ii 6 Basic standards 7 First-time adoption 7 Small and medium sized entities (SMEs)/Small and medium sized companies

Comparative statement on Indian GAAP and IFRS (As on 1 January 2010) 2010 edition Contents i ii 6 Basic standards 7 First-time adoption 7 Small and medium sized entities (SMEs)/Small and medium sized companies

IFRS 1 First-time Adoption of International Financial Reporting Standards

IFRS 1 First-time Adoption of International Financial Reporting Standards Scope An entity is required to apply IFRS 1 in: Its first IFRS financial statements; and Each interim financial report, if any,

IFRS 1 First-time Adoption of International Financial Reporting Standards Scope An entity is required to apply IFRS 1 in: Its first IFRS financial statements; and Each interim financial report, if any,

IFRS illustrative consolidated financial statements

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

Ind AS presentation and disclosure checklist 2018

Ind AS presentation and disclosure checklist 2018 Introduction This publication presents a checklist of presentation and disclosure requirements applicable to entities preparing financial statements in

Ind AS presentation and disclosure checklist 2018 Introduction This publication presents a checklist of presentation and disclosure requirements applicable to entities preparing financial statements in

November Changes To The Financial Reporting Framework In Singapore

November 2009 Changes To The Financial Reporting Framework In Singapore The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

November 2009 Changes To The Financial Reporting Framework In Singapore The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

ACCOUNTING POLICIES. for the year ended 30 June MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

ACCOUNTING POLICIES 1 PRESENTATION OF FINANCIAL STATEMENTS. for the year ended 30 June BASIS OF PREPARATION 1.2 STATEMENT OF COMPLIANCE

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

Example Consolidated Financial Statements. International Financial Reporting Standards (IFRS) Granthor Corporation Group 31 December 2008

Granthor Corporation Group 31 December 2008") Example Consolidated Financial Statements International Financial Reporting Standards (IFRS) Granthor Corporation Group 1 Introduction 2008 The preparation of financial statements in accordance with IFRS

Example Consolidated Financial Statements International Financial Reporting Standards (IFRS) Granthor Corporation Group 1 Introduction 2008 The preparation of financial statements in accordance with IFRS

IFRS 1 First-time Adoption of International. Standards*

Wrestling with First-time Adoption of IFRS IFRS 1 First-time Adoption of International Financial Reporting Standards* Session Objective and Key Take aways Session Objective: The objective of this session

Wrestling with First-time Adoption of IFRS IFRS 1 First-time Adoption of International Financial Reporting Standards* Session Objective and Key Take aways Session Objective: The objective of this session

84 Macquarie Group Limited and its subsidiaries 2017 Annual Report macquarie.com FINANCIAL REPORT

84 Macquarie Group Limited and its subsidiaries Annual Report macquarie.com FINANCIAL REPORT ABOUT GOVERNANCE DIRECTORS REPORT FINANCIAL REPORT FURTHER INFORMATION 85 Income Statements Statements of comprehensive

84 Macquarie Group Limited and its subsidiaries Annual Report macquarie.com FINANCIAL REPORT ABOUT GOVERNANCE DIRECTORS REPORT FINANCIAL REPORT FURTHER INFORMATION 85 Income Statements Statements of comprehensive

First-time Adoption of International Financial Reporting Standards

IFRS Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (the Board) adopted SIC-8 First-time Application of IASs as

IFRS Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (the Board) adopted SIC-8 First-time Application of IASs as

Pearson plc IFRS Technical Analysis

Pearson plc IFRS Technical Analysis Contents A. Introduction B. Basis of presentation C. Accounting Policies D. Critical Accounting Assumptions and Judgements Schedules 1. Income statement Reconciliation

Pearson plc IFRS Technical Analysis Contents A. Introduction B. Basis of presentation C. Accounting Policies D. Critical Accounting Assumptions and Judgements Schedules 1. Income statement Reconciliation

Interpretations effective in the year ended 28 February 2009 Standards and interpretations not yet effective

Accounting Policies Interpretations effective in the year ended 28 February 2009 IFRS 7 Financial instruments: disclosures. This amendment introduces new disclosures relating to financial instruments and

Accounting Policies Interpretations effective in the year ended 28 February 2009 IFRS 7 Financial instruments: disclosures. This amendment introduces new disclosures relating to financial instruments and

Adviser alert Example Consolidated Financial Statements 2013

Adviser alert Example Consolidated Financial Statements 2013 September 2013 Overview The Grant Thornton International IFRS team has published the 2013 version of Reporting under IFRS: Example Consolidated

Adviser alert Example Consolidated Financial Statements 2013 September 2013 Overview The Grant Thornton International IFRS team has published the 2013 version of Reporting under IFRS: Example Consolidated

SESSION 36 IFRS 1 FIRST-TIME ADOPTION

SESSION 36 IFRS 1 FIRST-TIME ADOPTION Overview Objective To explain how an entity s first-time IFRS financial statements should be prepared and presented in accordance with IFRS 1 First-Time Adoption of

SESSION 36 IFRS 1 FIRST-TIME ADOPTION Overview Objective To explain how an entity s first-time IFRS financial statements should be prepared and presented in accordance with IFRS 1 First-Time Adoption of

IFRS for small and medium-sized entities ( IFRS for SMEs) 1. Basics 1.1 Development of an IFRS for SMEs. 1. Basics 1.2 Definition of SMEs. 1.

1. Basics 1.1 Development of an IFRS for SMEs. 1. Basics 1.2 Definition of SMEs. 1.") IFRS for small and medium-sized entities ( IFRS for SMEs) 1. Basics 2. Components of a complete set of financial statements 3. Pecularities in the accounting policy for SMEs 4. Transition to IFRS for SMEs

IFRS for small and medium-sized entities ( IFRS for SMEs) 1. Basics 2. Components of a complete set of financial statements 3. Pecularities in the accounting policy for SMEs 4. Transition to IFRS for SMEs

ASPE at a Glance. Standards Included in Topic

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

Good First-time Adopter (International) Limited

Limited") Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2012 Based on International Financial Reporting

Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2012 Based on International Financial Reporting

PJSC LUKOIL CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS 31 December 2017 Consolidated Statement of Financial Position (Millions of Russian rubles) Assets 31 December 31 December Note Current assets Cash and cash equivalents

CONSOLIDATED FINANCIAL STATEMENTS 31 December 2017 Consolidated Statement of Financial Position (Millions of Russian rubles) Assets 31 December 31 December Note Current assets Cash and cash equivalents

KUWAIT FINANCE HOUSE K.S.C.P. AND SUBSIDIARIES

KUWAIT FINANCE HOUSE K.S.C.P. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 CONSOLIDATED STATEMENT OF INCOME Year ended 31 December 2015 Notes INCOME Financing income 663,423 645,801

KUWAIT FINANCE HOUSE K.S.C.P. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 CONSOLIDATED STATEMENT OF INCOME Year ended 31 December 2015 Notes INCOME Financing income 663,423 645,801

Interim Financial Reporting

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

NOTES TO THE FINANCIAL STATEMENTS

NOTES TO THE FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES 1.1 Nature of business Super Group Limited (Registration number 1943/016107/06), the holding Company (the Company) of the Group, is a Company listed

NOTES TO THE FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES 1.1 Nature of business Super Group Limited (Registration number 1943/016107/06), the holding Company (the Company) of the Group, is a Company listed

November Changes to the financial reporting framework in Singapore.

November 2008 Changes to the financial reporting framework in Singapore. The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

November 2008 Changes to the financial reporting framework in Singapore. The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

MALAYSIAN PRIVATE ENTITIES REPORTING STANDARD (MPERS)

") BT NEWS BRIEF AUGUST 2016 MALAYSIAN PRIVATE ENTITIES REPORTING STANDARD (MPERS) THE NEW FINANCIAL REPORTING FRAMEWORK FOR PRIVATE ENTITIES HIGHLIGHTS WHAT SHOULD WE KNOW? 1 January 2016 marked an important

BT NEWS BRIEF AUGUST 2016 MALAYSIAN PRIVATE ENTITIES REPORTING STANDARD (MPERS) THE NEW FINANCIAL REPORTING FRAMEWORK FOR PRIVATE ENTITIES HIGHLIGHTS WHAT SHOULD WE KNOW? 1 January 2016 marked an important

Impact of Ind AS on Cost computations & audit By CMA Milind Date M Com, FCMA, CMA (USA), Dip IFRS (ACCA UK)

, Dip IFRS (ACCA UK)") Impact of Ind AS on Cost computations & audit By CMA Milind Date M Com, FCMA, CMA (USA), Dip IFRS (ACCA UK) 13-03-2018 CMA Milind Date 1 Merging of two pillars Financial & Cost Accounting..we all are accountants

Impact of Ind AS on Cost computations & audit By CMA Milind Date M Com, FCMA, CMA (USA), Dip IFRS (ACCA UK) 13-03-2018 CMA Milind Date 1 Merging of two pillars Financial & Cost Accounting..we all are accountants

International Financial Reporting Standards Disclosure Checklist 2004

International Financial Reporting Standards Disclosure Checklist 2004 Meeting all IFRS requirements www.pwc.com/ifrs PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation.

International Financial Reporting Standards Disclosure Checklist 2004 Meeting all IFRS requirements www.pwc.com/ifrs PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation.

PwC Alert. Malaysian Private Entities Reporting Standards (MPERS) A new reporting framework for Private Entities

A new reporting framework for Private Entities") Issue 124 November 2015 PP 9741/10/2012 (031262) PwC Alert Malaysian Private Entities Reporting Standards (MPERS) A new reporting framework for Private Entities Page 3 MPERS at a glance Page 5 Comparing

Issue 124 November 2015 PP 9741/10/2012 (031262) PwC Alert Malaysian Private Entities Reporting Standards (MPERS) A new reporting framework for Private Entities Page 3 MPERS at a glance Page 5 Comparing

Good Construction Group (International) Limited

Limited") Good Construction Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2012 Based on International Financial Reporting Standards in issue at

Good Construction Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2012 Based on International Financial Reporting Standards in issue at

Notes to the financial statements

11 1. Accounting policies 1.1 Nature of business Super Group Limited (Registration number 1943/016107/06), the holding Company of the Group (the Company), is a Company listed on the Main Board of the JSE

11 1. Accounting policies 1.1 Nature of business Super Group Limited (Registration number 1943/016107/06), the holding Company of the Group (the Company), is a Company listed on the Main Board of the JSE

FINANCIAL STATEMENTS UNDER IND AS: OVER ALL CONSIDERATIONS

FINANCIAL STATEMENTS UNDER IND AS: OVER ALL CONSIDERATIONS October 2016 1 Titre de la présentation CONSTITUENTS OF FINANCIAL STATEMENTS Balance sheet Statement of profit and loss (title not entirely representative

FINANCIAL STATEMENTS UNDER IND AS: OVER ALL CONSIDERATIONS October 2016 1 Titre de la présentation CONSTITUENTS OF FINANCIAL STATEMENTS Balance sheet Statement of profit and loss (title not entirely representative

Slides IAS 12 Income Taxes. BDO Atrio. IAS 12 (revised 2000) Income Taxes. BDO Atrio

Income Taxes. BDO Atrio") (revised 2000) 1 Authoritive pronouncements (revised 2000) SIC 21: Income taxes; Recovery of revalued Non-depreciable assets SIC 25: Income taxes; Changes in the tax status of an enterprise or its shareholders

(revised 2000) 1 Authoritive pronouncements (revised 2000) SIC 21: Income taxes; Recovery of revalued Non-depreciable assets SIC 25: Income taxes; Changes in the tax status of an enterprise or its shareholders

International Petroleum Investment Company PJSC and its subsidiaries CHAIRMAN S REPORT AND CONSOLIDATED FINANCIAL STATEMENTS

International Petroleum Investment Company PJSC and its subsidiaries CHAIRMAN S REPORT AND CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2011 International Petroleum Investment Company PJSC and its subsidiaries

International Petroleum Investment Company PJSC and its subsidiaries CHAIRMAN S REPORT AND CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2011 International Petroleum Investment Company PJSC and its subsidiaries

Consolidated financial statements for the year ended December 31 st, In accordance with International Financial Reporting Standards («IFRS»)

") INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2008 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2008 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

(All numbers in $ 000 unless otherwise stated) Marks

Marks") Answers Diploma in International Financial Reporting December 200 Answers (All numbers in $ 000 unless otherwise stated) (a) Consolidated statement of financial position of Alpha at 30 September 200 ASSETS

Answers Diploma in International Financial Reporting December 200 Answers (All numbers in $ 000 unless otherwise stated) (a) Consolidated statement of financial position of Alpha at 30 September 200 ASSETS

IFRS disclosure checklist 2008

IFRS disclosure checklist 2008 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2008 IFRS technical publications IFRS Manual of Accounting 2008 Provides expert practical guidance

IFRS disclosure checklist 2008 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2008 IFRS technical publications IFRS Manual of Accounting 2008 Provides expert practical guidance

International Accounting Standard 34 Interim Financial Reporting. Objective. Scope. Definitions. Content of an interim financial report IAS 34

International Accounting Standard 34 Interim Financial Reporting Objective The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles

International Accounting Standard 34 Interim Financial Reporting Objective The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles

Consolidated Financial Statements for the year ended December 31 st, 2007 In accordance with International Financial Reporting Standards («IFRS»)

") INFO-QUEST S.A. Consolidated Financial Statements for the year ended December 31 st, 2007 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

INFO-QUEST S.A. Consolidated Financial Statements for the year ended December 31 st, 2007 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

Similarities and Differences A comparison of IFRS and US GAAP

Similarities and Differences A comparison of and October 2007 Contents Page Preface 2 How to use this publication 3 Summary of similarities and differences 4 Accounting framework 12 Financial statements

Similarities and Differences A comparison of and October 2007 Contents Page Preface 2 How to use this publication 3 Summary of similarities and differences 4 Accounting framework 12 Financial statements

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 15)

") International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 15) Appendix 2: Early application of IFRS 15 Revenue from Contracts with

International GAAP Holdings Limited Model financial statements for the year ended 31 December 2017 (With early adoption of IFRS 15) Appendix 2: Early application of IFRS 15 Revenue from Contracts with

Continuing operations Revenue 3(a) 464, ,991. Revenue 464, ,991

464, ,991. Revenue 464, ,991") STATEMENT OF PROFIT OR LOSS For the year ended 30 June 2017 Consolidated Consolidated Note Continuing operations Revenue 3(a) 464,411 323,991 Revenue 464,411 323,991 Other Income 3(b) 4,937 5,457 Share

STATEMENT OF PROFIT OR LOSS For the year ended 30 June 2017 Consolidated Consolidated Note Continuing operations Revenue 3(a) 464,411 323,991 Revenue 464,411 323,991 Other Income 3(b) 4,937 5,457 Share

A New Era of Financial Reporting

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

FINANCIAL PRUDENCE WORKSHOP FOR SMALL MEDIUM SIZE ENTITIES. 8th -10th December 2014, SAFARI PARK NAIROBI.

FINANCIAL PRUDENCE WORKSHOP FOR SMALL MEDIUM SIZE ENTITIES 8th -10th December 2014, SAFARI PARK NAIROBI. FINANCIAL REPORTING FOR SMEs By: CPA JOSEPHAT NJOROGE WAITITU. CONTACTS:JOSEPHAT WAITITU & ASSOCIATES

FINANCIAL PRUDENCE WORKSHOP FOR SMALL MEDIUM SIZE ENTITIES 8th -10th December 2014, SAFARI PARK NAIROBI. FINANCIAL REPORTING FOR SMEs By: CPA JOSEPHAT NJOROGE WAITITU. CONTACTS:JOSEPHAT WAITITU & ASSOCIATES

A n n u a l f i n a n c i a l r e s u l t s

A n n u a l f i n a n c i a l r e s u l t s DIRECTORS STATEMENT The directors of Air New Zealand Limited are pleased to present to shareholders the Annual Report* and financial statements for Air New

A n n u a l f i n a n c i a l r e s u l t s DIRECTORS STATEMENT The directors of Air New Zealand Limited are pleased to present to shareholders the Annual Report* and financial statements for Air New

HKFRSs / IFRSs UPDATE 2011/02

28 FEBRUARY 2011 WWW.BDO.COM.HK HKFRSs / IFRSs UPDATE 2011/02 NEW AND REVISED HKFRSs 2010 YEAR ENDS REPORTING (A) New and revised HKFRSs that are mandatory for the first time for 2010 year ends 1. HKFRS

28 FEBRUARY 2011 WWW.BDO.COM.HK HKFRSs / IFRSs UPDATE 2011/02 NEW AND REVISED HKFRSs 2010 YEAR ENDS REPORTING (A) New and revised HKFRSs that are mandatory for the first time for 2010 year ends 1. HKFRS