IAS 1R- Presentation of Financial Statements. Introduction to IFRS / Ind AS

|

|

|

- Tamsin Martin

- 5 years ago

- Views:

Transcription

1 IAS 1R- Presentation of Financial Statements Introduction to IFRS / Ind AS

2 IAS 1R- Presentation of financial statements

3 Objective The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure comparability both with the entity's financial statements of previous periods and with the financial statements of other entities. To achieve this objective, this Standard sets out overall requirements for the presentation of financial statements, guidelines for their structure and minimum requirements for their content. Slide 3

4 Fair presentation and compliance An entity whose financial statements comply with IFRSs shall make an explicit and unreserved statement of such compliance in the notes. An entity shall not describe financial statements as complying with IFRSs unless they comply with all the requirements of IFRSs. An entity cannot rectify inappropriate accounting policies either by disclosure of the accounting policies used or by notes or explanatory material. In the extremely rare circumstances in which management concludes that compliance with a requirement in an IFRS would be so misleading that it would conflict with the objective of financial statements set out in the Framework, the entity shall depart from that requirement. However the entity is required to make specific disclosures prescribed under IAS 1R Slide 4

5 Comparative information Comparatives required for all numerical information Comparatives required for narrative and descriptive information when it is relevant to an understanding of the current period s financial statement Additional statement of financial position When an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements, the entity is required to disclose a statement of financial position as at the beginning of the earliest comparative period. Slide 5

6 Components of financial statements A complete set of financial statements comprises The primary statements - Statement of financial position for the period end - Statement of comprehensive income for the period - Statement of changes in equity for the period - Statement of cash flows for the period Notes, including summary of accounting policies and other explanatory information An entity may use titles for the statements other than those prescribed in IAS 1R, however the titles used shall not be misleading. All primary statements of equal prominence Slide 6

7 Statement of Financial Position Basis of presentation Classified Balance sheet An entity shall present current and non-current asset, and current and noncurrent liability as separate classification on the face of the statement of financial position Exception to above rule When a presentation based on liquidity provides information that is reliable and more relevant. All assets and liabilities are required to be presented in the order of liquidity. Choice driven by type of business Manufacturers and retailers current/non-current basis Financial institutions, banks and real estate companies liquidity basis Slide 7

8 Statement of Financial Position Current vs. Non-current Classification Current asset Expected to be realised, sold or consumed within entity s normal operating cycle Held primarily for trading purposes Expected to be realised within 12 months after balance sheet date Unrestricted cash or cash equivalent Current liability Expected to be settled within entity s normal operating cycle Held primarily for trading purposes Expected to be settled within 12 months after balance sheet date No unconditional right to defer settlement for at least 12 months after balance sheet date An entity shall classify all other assets as non-current. An entity shall classify all other liabilities as non-current. Slide 8

9 Statement of Financial Position Operating cycle Definition the operating cycle of an entity is the time between the acquisition of assets for processing and their realisation in cash or cash equivalents Items realised, sold or consumed within operating cycle are current items Operating cycle may be more than 12 months Slide 9

10 Statement of Financial Position Minimum line items Property, plant and equipment Investment property Intangible assets Financial assets (other than those shown on other line items) Investments accounted for using the equity method Biological assets Inventories Trade and other receivables Cash and cash equivalents Held for sale assets and assets included in disposal groups Trade and other payables Provisions Financial liabilities (other than those shown on other line items) Current tax assets and liabilities Deferred tax assets and liabilities Liabilities included in disposal groups Minority interest Issued capital and reserves attributable to owners of the parent An entity shall present additional line items, headings and subtotals in the statement of financial position when such presentation is relevant to an understanding of the entity's financial position. Slide 10

11 Statement of Financial Position Slide 11

12 Statement of Comprehensive Income Basis of presentation An entity shall present all items of income and expense recognised in a period in a single statement of comprehensive income, or in two statements: a statement displaying components of profit or loss (separate income statement) and a second statement beginning with profit or loss and displaying components of other comprehensive income (statement of comprehensive income). Slide 12

13 Statement of Comprehensive Income Application of the requirement to analyse expenses Choose most relevant presentation analysis method by: - Function - usually used by manufacturers, retailers, etc. - Nature - usually used by financial institutions, etc. If analysis by function is provided, additional note disclosures analysing the nature of expenses is required Slide 13

14 Statement of Comprehensive Income Minimum line items Revenue Finance costs Share of profit or loss of associates and joint ventures Tax expense Discontinued operations Profit or loss Profit or loss attributable to: - Minority interest - Owners of the parent Each component of other comprehensive income by nature Share of other comprehensive income of associates and joint ventures Total comprehensive income attributable to: - Minority interest - Owners of the parent An entity shall not present any items of income or expense as extraordinary items Slide 14

15 Statement of Comprehensive Income Additional line items, headings and sub-totals Required when relevant to an understanding of performance Description and order of line items amended where necessary to explain elements of performance Framework qualitative characteristics of financial statements - Understandability - Relevance - Reliability - Comparability Undefined terms may be used where relevant to an understanding (subject to meeting qualitative characteristics) Slide 15

16 Other Comprehensive Income ( OCI ) Components of Other Comprehensive Income Changes in revaluation surplus (on account of PPE and intangibles) Actuarial gains and losses on defined benefit plans recognised in full in equity, if the entity elects the option available under IAS 19 Gains and losses arising from translation of a foreign operation Gains and losses on re-measuring available-for-sale financial assets Effective portion of gains and losses on hedging instruments in a cash flow hedge. All non-owners change in equity are recognised in OCI Components of OCI shall be presented either net of related taxes or at gross of related tax with one amount representing aggregate amount of income tax relating to those components. Items of income and expense are recognised in profit or loss unless standards prescribe or permit otherwise. Slide 16

17 Other Comprehensive Income ( OCI ) Recycling of other comprehensive income Reclassifications ( recycling ) - as required by standards items previously recognised in OCI shall be transferred to Statement of Comprehensive Income Items Revaluation of PPE and intangible assets Actuarial gains/losses on defined benefit plans (optional) FX gains/losses from the translation of foreign operations Gain/losses on revaluation of available-for-sale financial assets Effective portion of gains/losses from cash flow hedges Recycled under IFRS? No No Yes Yes Yes Remarks Decrease can only be recognised in OCI if they reverse previous increments for the same asset Immediate recognition in retained earnings Transfer to P&L required Transfer to P&L required Transfer to P&L or include in cost/carrying amount of non-financial asset or liability (basis adjustment) Slide 17

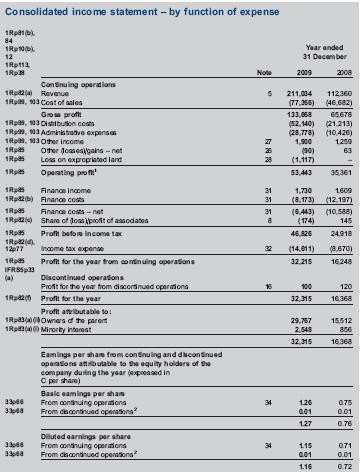

18 Two statement, by function of expense Slide 18

19 Statement of changes in shareholders equity This statement shows movements/ transactions during the reporting period that have affected the shareholders equity. It is generally tabular in approach with the various categories of equity across the top common shares, additional paid-in capital, retained earnings, other reserves. The transactions are listed line by line and include amongst others net income for the year, cumulative translation adjustments (if applicable), issue of shares, dividends paid, other movements in shares. The outcome is a reconciliation in the movement of each category of shareholder s equity from one period to the next. Slide 19

20 Statement of changes in shareholders equity Slide 20

21 Notes to financial statements Notes to financial statements comprise of: Background of the Company Significant accounting policies Accounting estimates Changes in accounting policies Concentration of risks Schedule of individual material items on B/s, I/s, CF and Sh Equity Explanation of material transaction e.g., acquisition, disposal. Recently issued pronouncements and their implications Slide 21

22 Significant differences between IFRS and IND AS Single statement of profit and loss Statement of changes in equity Classification of expenses recognized in profit and loss Slide 22

23 IAS 1R- Presentation of financial statements IAS 7 Cash flow statements

24 Cash flow statements Statement of cash flows Cash and cash equivalents Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and so near their maturity that they present insignificant risk of changes in value because of changes in interest rates. Generally, only investments with original maturities of three months or less qualify as cash equivalents. They may also include bank overdrafts. Under Indian GAAP bank overdrafts are excluded from cash and cash equivalents Examples: fixed deposits, Treasury bills, commercial paper etc. Requires disclosure of policy used for determining items treated as cash equivalents Slide 24

25 Cash flow statements Statement of cash flows Direct versus Indirect Method Enterprise may choose to report the cash flow from operating activity by using either the direct or the indirect method Reconciliation of net income and net cash flow from operating activity is required to be provided if the direct method is used Net Cash provided by or used in: Operating activities Investing activities Financing activities Net increase (decrease) in cash and cash equivalent Slide 25

26 Cash flow statements Significant differences between IFRS and IND AS Classification of interest and dividend Other additional disclosures Slide 26

27 IAS 1R- Presentation of financial statements IAS 8 Accounting policies, changes in accounting estimates & errors

28 Accounting policies, changes in accounting estimates & errors Introduction IFRS IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors Indian GAAP AS 5 Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies Slide 28

29 Accounting policies, changes in accounting estimates & errors Selection of Accounting Policy - Hierarchy Prescribed Standard or Interpretation IFRS, IAS, IFRIC, SIC Any relevant Implementation Guidance issued by the IASB for the Standard or Interpretation (technically not a part of the standards) Guidance for similar or related issue Framework of IFRS Most recent pronouncements of other standard-setting bodies Other accounting literature and accepted industry practices Onus on management - select policy to make financials relevant & reliable Slide 29

30 Accounting policies, changes in accounting estimates & errors What s the big change? Accounting policies change: retrospective application Accounting estimate change: Prospective application Change in depreciation method = prospective Correction of errors: retrospective application Management cannot assert compliance with IFRS if financial statements does not comply with all prescribed accounting standards Slide 30

31 Accounting policies, changes in accounting estimates & errors Change in Accounting Policy - Change in inventory valuation method (i.e., from LIFO to FIFO) - Change in method of amortizing actuarial gains and losses - Change in method of presenting the statement of cash flows (i.e., direct vs. indirect) Following are not changes in accounting policies: Accounting policy for transactions that differ in substance from those previously occurring; and Application of a new accounting policy for transactions that did not occur previously or were immaterial. Retrospective application to all prior periods unless impracticable Slide 31

32 Accounting policies, changes in accounting estimates & errors Correction of Error in previously Issued Financial Statements Errors discovered subsequent to issuance of financial statement reported as a priorperiod adjustment by restating previously issued financial statements. Example Corrections of mistakes in the application of IFRS Corrections of mathematical mistakes Oversight or misuse of facts that existed at the time the financial statements were prepared. Slide 32

33 Thank You

IAS 1 Presentation of Financial Statement

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 1 Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 1 Presentation of Financial Statements

Presentation of Financial Statements

Presentation of Financial Statements 2016 Deloitte & Touche 1 2015 Deloitte Touche Limited Index 1. Objective 2. Scope 3. Objective of Financial Statements 4. Components of Financial Statements 5. Fair

Presentation of Financial Statements 2016 Deloitte & Touche 1 2015 Deloitte Touche Limited Index 1. Objective 2. Scope 3. Objective of Financial Statements 4. Components of Financial Statements 5. Fair

IFRS Training. IAS 1 Presentation of Financial Statements. Professional Training Services

IFRS Training IAS 1 Presentation of Financial Statements Table of Contents Section 1 Overview 2 Objectives 3 Scope 4 Purpose of Financial Statements 5 Frequency of Reporting and Period Covered 6 Components

IFRS Training IAS 1 Presentation of Financial Statements Table of Contents Section 1 Overview 2 Objectives 3 Scope 4 Purpose of Financial Statements 5 Frequency of Reporting and Period Covered 6 Components

International GAAP Disclosure Checklist

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

Preparation and Presentation of Financial Statements Part 1 17 September 2013

Preparation and Presentation of Financial Statements Part 1 17 September 2013 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2008-13 Nelson Consulting

Preparation and Presentation of Financial Statements Part 1 17 September 2013 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2008-13 Nelson Consulting

Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (IASB) adopted Presentation of Financial Statements, which had originally

International Accounting Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (IASB) adopted Presentation of Financial Statements, which had originally

ICPAK Financial Reporting Workshop IAS 1- PRESENTATION OF FINANCIAL STATEMENTS December 2011 Presented by: Simon Fisher

ICPAK Financial Reporting Workshop IAS 1- PRESENTATION OF FINANCIAL STATEMENTS December 2011 Presented by: Simon Fisher This slide presentation has been prepared for general guidance only, and does not

ICPAK Financial Reporting Workshop IAS 1- PRESENTATION OF FINANCIAL STATEMENTS December 2011 Presented by: Simon Fisher This slide presentation has been prepared for general guidance only, and does not

Presentation on Indian Accounting Standards

Presentation on Indian Accounting Standards By Bharat K Shetty Associate Director Walker, Chandiok & Co 1 Agenda Ind AS 1 Presentation of Financial Statements Ind AS 2 Inventories Ind AS 3 Statement of

Presentation on Indian Accounting Standards By Bharat K Shetty Associate Director Walker, Chandiok & Co 1 Agenda Ind AS 1 Presentation of Financial Statements Ind AS 2 Inventories Ind AS 3 Statement of

International GAAP Disclosure Checklist

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

Amendments to IFRS for SMEs

A C C O U N T I N G U P D A T E ( I F R S f o r S M E s ) s to IFRS for SMEs Introduction The International Accounting Standards Board (IASB) has published amendments to its 'International Financial Reporting

A C C O U N T I N G U P D A T E ( I F R S f o r S M E s ) s to IFRS for SMEs Introduction The International Accounting Standards Board (IASB) has published amendments to its 'International Financial Reporting

IAS 1 Presentation of Financial Statements - A Closer Look

MPRA Munich Personal RePEc Archive IAS 1 Presentation of Financial Statements - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 19 May 2008 Online at https://mpra.ub.uni-muenchen.de/41617/

MPRA Munich Personal RePEc Archive IAS 1 Presentation of Financial Statements - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 19 May 2008 Online at https://mpra.ub.uni-muenchen.de/41617/

International GAAP Disclosure Checklist

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 31 August 2015 International GAAP Disclosure Checklist Updated: August 2015 For

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 31 August 2015 International GAAP Disclosure Checklist Updated: August 2015 For

International GAAP Disclosure Checklist

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any

Presentation of Financial Statements

IAS 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (Board) adopted IAS 1 Presentation of Financial Statements, which had originally been issued by the

IAS 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (Board) adopted IAS 1 Presentation of Financial Statements, which had originally been issued by the

Presentation of Financial Statements

IAS Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 1 Presentation of Financial Statements, which had originally been

IAS Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 1 Presentation of Financial Statements, which had originally been

Presentation of Financial Statements

Indian Accounting Standard (Ind AS) 1 Presentation of Financial Statements (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in

Indian Accounting Standard (Ind AS) 1 Presentation of Financial Statements (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in

IFRS disclosure checklist

IFRS disclosure checklist 2017 IFRS disclosure checklist 2017 Introduction The IFRS disclosure checklist has been updated to outline the disclosures required for December 2017 year ends. It also contains

IFRS disclosure checklist 2017 IFRS disclosure checklist 2017 Introduction The IFRS disclosure checklist has been updated to outline the disclosures required for December 2017 year ends. It also contains

International Financial Reporting Standards Disclosure Checklist 2004

International Financial Reporting Standards Disclosure Checklist 2004 Meeting all IFRS requirements www.pwc.com/ifrs PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation.

International Financial Reporting Standards Disclosure Checklist 2004 Meeting all IFRS requirements www.pwc.com/ifrs PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation.

LAICO REGENCY HOTEL ANNUAL INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) WEEK PRESENTATION OF FINANCIAL STATEMENTS - IAS 1

WEEK PRESENTATION OF FINANCIAL STATEMENTS - IAS 1") ANNUAL INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) WEEK 24 th 28 th August 2015 LAICO REGENCY HOTEL PRESENTATION OF FINANCIAL STATEMENTS - IAS 1 BY, CPA NEBART AVUTSWA NAIROBI Credibility. Professionalism.

ANNUAL INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) WEEK 24 th 28 th August 2015 LAICO REGENCY HOTEL PRESENTATION OF FINANCIAL STATEMENTS - IAS 1 BY, CPA NEBART AVUTSWA NAIROBI Credibility. Professionalism.

International GAAP Disclosure Checklist

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2015 Effective for entities with a year-end of 30 June 2015 or thereafter

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2015 Effective for entities with a year-end of 30 June 2015 or thereafter

Indian Accounting Standard 1 Presentation of Financial Statements

Indian Accounting Standard 1 Presentation of Financial Statements Objective This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability - both with

Indian Accounting Standard 1 Presentation of Financial Statements Objective This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability - both with

Presentation of Financial Statements

HKAS 1 (Revised) Revised JanuaryAugust 2017 Effective for annual periods beginning on or after 1 January 2009 Hong Kong Accounting Standard 1 (Revised) Presentation of Financial Statements COPYRIGHT Copyright

HKAS 1 (Revised) Revised JanuaryAugust 2017 Effective for annual periods beginning on or after 1 January 2009 Hong Kong Accounting Standard 1 (Revised) Presentation of Financial Statements COPYRIGHT Copyright

IMPORTANT TAKEAWAYS ON IFRS

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

IFRS disclosure checklist 2011

www.pwc.com/ifrs IFRS disclosure checklist 2011 IFRS disclosure checklist 2011 Introduction The IFRS disclosure checklist has been updated to take into account standards and interpretations effective

www.pwc.com/ifrs IFRS disclosure checklist 2011 IFRS disclosure checklist 2011 Introduction The IFRS disclosure checklist has been updated to take into account standards and interpretations effective

Click to edit Master title style. Presentation of Financial Statements ( LKAS 1)

") 1 Click to edit Master title style Presentation of Financial Statements ( LKAS 1) 2 1 LKAS 1 Presentation of Financial Statements 3 LKAS 1: Overview Objective Scope Components of financial statements Overall

1 Click to edit Master title style Presentation of Financial Statements ( LKAS 1) 2 1 LKAS 1 Presentation of Financial Statements 3 LKAS 1: Overview Objective Scope Components of financial statements Overall

IFRS 1 First-time Adoption of International Financial Reporting Standards

IFRS 1 First-time Adoption of International Financial Reporting Standards Scope An entity is required to apply IFRS 1 in: Its first IFRS financial statements; and Each interim financial report, if any,

IFRS 1 First-time Adoption of International Financial Reporting Standards Scope An entity is required to apply IFRS 1 in: Its first IFRS financial statements; and Each interim financial report, if any,

IFRS 1 First-time Adoption of International. Standards*

Wrestling with First-time Adoption of IFRS IFRS 1 First-time Adoption of International Financial Reporting Standards* Session Objective and Key Take aways Session Objective: The objective of this session

Wrestling with First-time Adoption of IFRS IFRS 1 First-time Adoption of International Financial Reporting Standards* Session Objective and Key Take aways Session Objective: The objective of this session

IFRS disclosure checklist 2008

IFRS disclosure checklist 2008 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2008 IFRS technical publications IFRS Manual of Accounting 2008 Provides expert practical guidance

IFRS disclosure checklist 2008 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2008 IFRS technical publications IFRS Manual of Accounting 2008 Provides expert practical guidance

A New Era of Financial Reporting

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

IFRS pocket guide inform.pwc.com

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

IFRS 1 - First-Time Adoption of IFRS

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

NZ International Accounting Standard 1 (PBE) Presentation of Financial Statements (NZ IAS 1 (PBE))

Presentation of Financial Statements (NZ IAS 1 (PBE))") NZ International Accounting Standard 1 (PBE) Presentation of Financial Statements () Issued November 2012 excluding consequential amendments resulting from early adoption of NZ IFRS 9 (2009) (PBE) Financial

NZ International Accounting Standard 1 (PBE) Presentation of Financial Statements () Issued November 2012 excluding consequential amendments resulting from early adoption of NZ IFRS 9 (2009) (PBE) Financial

New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1)

") New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1) Issued November 2007 and incorporates amendments to 31 December 2016 other than consequential

New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1) Issued November 2007 and incorporates amendments to 31 December 2016 other than consequential

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2012 International Financial Reporting Standards

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2012 International Financial Reporting Standards A Layout (International) Group Plc Annual report and financial statements For the year ended 31

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2012 International Financial Reporting Standards A Layout (International) Group Plc Annual report and financial statements For the year ended 31

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities

for Small and Medium-sized Entities") International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

Framework and IAS 1 March 2007

Framework and IAS 1 March 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) 2005-07 Nelson 1 Today s Agenda Introduction Framework Simple but Comprehensive Contentious and

Framework and IAS 1 March 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) 2005-07 Nelson 1 Today s Agenda Introduction Framework Simple but Comprehensive Contentious and

April Grant Thornton LLP All rights reserved U.S. member firm of Grant Thornton International Ltd

Comparison between and International Financial Reporting Standards April 2016 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 5 International standards

Comparison between and International Financial Reporting Standards April 2016 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 5 International standards

IFRS for SMEs (proposals) Pocket Guide 2007

Pocket Guide 2007") IFRS for SMEs (proposals) Pocket Guide 2007 PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation. Drawing on the knowledge and skills of 125,000 people in 142

IFRS for SMEs (proposals) Pocket Guide 2007 PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation. Drawing on the knowledge and skills of 125,000 people in 142

IFRS for SMEs IFRS Foundation-World Bank

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

Comparison between U.S. GAAP and International Financial Reporting Standards

Comparison between and International Financial Reporting Standards April 2014 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 6 International standards

Comparison between and International Financial Reporting Standards April 2014 Comparison between and International Financial Reporting Standards 2 Contents 1. Introduction... 6 International standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

Stay informed. Visit IFRS pocket guide 2012

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

5 5BC G877?H> JKLMNOPQO S TUOVWO S XVNYO

.!# /01/.!# /2& 3'**$!"#$ &'( )#$$'*&*!' +,$- * 5851 5 789:;;?@?A 5BC DE 012345678 45678 44 1851 8 8 458 5 56214 JKLMNOPQO S TUOVWO S XVNYO SFRS FOR SMALL ENTITIES DISCLOSURE AND

.!# /01/.!# /2& 3'**$!"#$ &'( )#$$'*&*!' +,$- * 5851 5 789:;;?@?A 5BC DE 012345678 45678 44 1851 8 8 458 5 56214 JKLMNOPQO S TUOVWO S XVNYO SFRS FOR SMALL ENTITIES DISCLOSURE AND

SESSION 36 IFRS 1 FIRST-TIME ADOPTION

SESSION 36 IFRS 1 FIRST-TIME ADOPTION Overview Objective To explain how an entity s first-time IFRS financial statements should be prepared and presented in accordance with IFRS 1 First-Time Adoption of

SESSION 36 IFRS 1 FIRST-TIME ADOPTION Overview Objective To explain how an entity s first-time IFRS financial statements should be prepared and presented in accordance with IFRS 1 First-Time Adoption of

Introduction Consolidated statement of comprehensive income for the year ended 31 December 20XX... 6

PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF International Limited is not responsible for the acts or omissions

PKF International Limited administers a network of legally independent member firms which carry on separate businesses under the PKF Name. PKF International Limited is not responsible for the acts or omissions

The Effects of Changes in Foreign Exchange Rates

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 21 The Effects of Changes

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 21 The Effects of Changes

First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards This version was issued in November 2008. Its effective date is 1 July 2009. It includes

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards This version was issued in November 2008. Its effective date is 1 July 2009. It includes

Hong Kong Financial Reporting Standards Presentation and Disclosure Checklist 2008

Hong Kong Financial Reporting Standards Presentation and Disclosure Checklist 2008 Audit Presentation and Disclosure Checklist 2008 Hong Kong Financial Reporting Standards Presentation and disclosure

Hong Kong Financial Reporting Standards Presentation and Disclosure Checklist 2008 Audit Presentation and Disclosure Checklist 2008 Hong Kong Financial Reporting Standards Presentation and disclosure

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

PSAK Pocket guide 2018

PSAK Pocket guide 2018 www.pwc.com/id Introduction This pocket guide provides a summary of the recognition, measurement and presentation requirements of Indonesia financial accounting standards (PSAK)

PSAK Pocket guide 2018 www.pwc.com/id Introduction This pocket guide provides a summary of the recognition, measurement and presentation requirements of Indonesia financial accounting standards (PSAK)

Introduction to International Financial Reporting Standards

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors Objective 1 The objective of this Standard is to prescribe the criteria for selecting and changing accounting

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors Objective 1 The objective of this Standard is to prescribe the criteria for selecting and changing accounting

IFRS illustrative consolidated financial statements

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

CAMBODIAN ACCOUNTING STANDARDS (CAS)

") CAMBODIAN ACCOUNTING STANDARDS (CAS) 1 - CAS 1 : Presentation of Financial Statements an Audit of Financial Statements 2 - CAS 2 : Inventories 3 - CAS 7 : Cash Flow Statements 4 - CAS 8 : Net profit or

CAMBODIAN ACCOUNTING STANDARDS (CAS) 1 - CAS 1 : Presentation of Financial Statements an Audit of Financial Statements 2 - CAS 2 : Inventories 3 - CAS 7 : Cash Flow Statements 4 - CAS 8 : Net profit or

SRI LANKA ACCOUNTING STANDARD

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL STATEMENTS THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL STATEMENTS THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL

Entity B's management has agreed to change the accounting for the complex financial instrument for the year ending 31 December 20X7.

First time adoption of IFRS Case Study 1 Entity B prepares financial statements that contain an explicit and unreserved statement of compliance with IFRS. The auditors' report on the financial statements

First time adoption of IFRS Case Study 1 Entity B prepares financial statements that contain an explicit and unreserved statement of compliance with IFRS. The auditors' report on the financial statements

IAS 1. Presentation of financial statements.

IAS 1 Presentation of financial statements. Objectives and Scope of IAS 1 Usefulness of financial statements General features Components To prescribe the basis for presentation of general purpose financial

IAS 1 Presentation of financial statements. Objectives and Scope of IAS 1 Usefulness of financial statements General features Components To prescribe the basis for presentation of general purpose financial

IFRS Institute Webcast. presentation and related-party disclosures

IFRS Institute Webcast Financial statement presentation and related-party disclosures June 13, 2012 1 Administrative CPE regulations require online participants take part in online questions. Participants

IFRS Institute Webcast Financial statement presentation and related-party disclosures June 13, 2012 1 Administrative CPE regulations require online participants take part in online questions. Participants

Topic 1: The International Accounting Environment and Financial Reporting

Topic 1: The International Accounting Environment and Financial Reporting USERS OF FINANCIAL STATEMENTS - Internal Users involves Management Accounting communicating to those within entity looking for

Topic 1: The International Accounting Environment and Financial Reporting USERS OF FINANCIAL STATEMENTS - Internal Users involves Management Accounting communicating to those within entity looking for

March 2018 IFRS and Austrian GAAP Similarities and Differences

www.pwc.com/at March 2018 IFRS and Austrian GAAP Similarities and Differences IFRS and Austrian GAAP: Similarities and Differences March 2018 Table of Contents Introduction... 3 Accounting Framework...

www.pwc.com/at March 2018 IFRS and Austrian GAAP Similarities and Differences IFRS and Austrian GAAP: Similarities and Differences March 2018 Table of Contents Introduction... 3 Accounting Framework...

Good First-time Adopter (International) Limited

Limited") Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

International Financial Reporting Standards (IFRS)

") FACT SHEET February 2010 IFRS 1 First-time Adoption of International Financial Reporting Standards (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based

FACT SHEET February 2010 IFRS 1 First-time Adoption of International Financial Reporting Standards (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based

Similarities and Differences A comparison of IFRS and US GAAP

Similarities and Differences A comparison of and October 2007 Contents Page Preface 2 How to use this publication 3 Summary of similarities and differences 4 Accounting framework 12 Financial statements

Similarities and Differences A comparison of and October 2007 Contents Page Preface 2 How to use this publication 3 Summary of similarities and differences 4 Accounting framework 12 Financial statements

Indian Accounting Standards (Ind AS) AT A GLANCE

AT A GLANCE") Indian Accounting Standards (Ind AS) AT A GLANCE Indian Accounting Standards (Ind AS) An Introduction The Hon'ble Finance Minister in the presentation of the Union Budget for 2014-15, proposed the adoption

Indian Accounting Standards (Ind AS) AT A GLANCE Indian Accounting Standards (Ind AS) An Introduction The Hon'ble Finance Minister in the presentation of the Union Budget for 2014-15, proposed the adoption

Annual Improvements Cycle

Annual Improvements 2009 2011 Cycle 1 Copyright ANNUAL IMPROVEMENTS 2009 2011 CYCLE INTRODUCTION NZ IFRS 1 NZ IAS 1 NZ IAS 16 NZ IAS 32 NZ IAS 34 First-time Adoption of New Zealand Equivalents to International

Annual Improvements 2009 2011 Cycle 1 Copyright ANNUAL IMPROVEMENTS 2009 2011 CYCLE INTRODUCTION NZ IFRS 1 NZ IAS 1 NZ IAS 16 NZ IAS 32 NZ IAS 34 First-time Adoption of New Zealand Equivalents to International

2. Reconciliation between Japanese GAAP and IFRS

2. Reconciliation between Japanese GAAP and IFRS Reconciliation of assets, liabilities, and equity as of March 31, 2016 and 2017, and reconciliation of net profit for the fiscal years ended March 31, 2016

2. Reconciliation between Japanese GAAP and IFRS Reconciliation of assets, liabilities, and equity as of March 31, 2016 and 2017, and reconciliation of net profit for the fiscal years ended March 31, 2016

MALAYSIAN PRIVATE ENTITIES REPORTING STANDARD (MPERS)

") BT NEWS BRIEF AUGUST 2016 MALAYSIAN PRIVATE ENTITIES REPORTING STANDARD (MPERS) THE NEW FINANCIAL REPORTING FRAMEWORK FOR PRIVATE ENTITIES HIGHLIGHTS WHAT SHOULD WE KNOW? 1 January 2016 marked an important

BT NEWS BRIEF AUGUST 2016 MALAYSIAN PRIVATE ENTITIES REPORTING STANDARD (MPERS) THE NEW FINANCIAL REPORTING FRAMEWORK FOR PRIVATE ENTITIES HIGHLIGHTS WHAT SHOULD WE KNOW? 1 January 2016 marked an important

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell 2 PwC Introduction This pocket guide provides a brief summary of the recognition, measurement, presentation and disclosure requirements

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell 2 PwC Introduction This pocket guide provides a brief summary of the recognition, measurement, presentation and disclosure requirements

IFAS Disclosure Checklist 2014 For non listed entities

www.pwc.com/id July 2014 IFAS Disclosure Checklist 2014 For non listed entities Introduction The Indonesian Financial Accounting Standards (IFAS) disclosure checklist for non listed entities is designed

www.pwc.com/id July 2014 IFAS Disclosure Checklist 2014 For non listed entities Introduction The Indonesian Financial Accounting Standards (IFAS) disclosure checklist for non listed entities is designed

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

IFRS for SMEs World Bank REPARIS FR CoP

!International Financial Reporting Standards International Financial Reporting Standards 1 IFRS for SMEs World Bank REPARIS FR CoP 14 September 2010 Vienna, Austria Copyright 2010 IFRS Foundation. All

!International Financial Reporting Standards International Financial Reporting Standards 1 IFRS for SMEs World Bank REPARIS FR CoP 14 September 2010 Vienna, Austria Copyright 2010 IFRS Foundation. All

IFRS disclosure checklist 2009

IFRS disclosure checklist 2009 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2009 IFRS technical publications Manual of accounting IFRS 2010 Global guide to IFRS providing

IFRS disclosure checklist 2009 PricewaterhouseCoopers IFRS and corporate governance publications and tools 2009 IFRS technical publications Manual of accounting IFRS 2010 Global guide to IFRS providing

First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS

execution EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN execution Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Policies... 5 4.1 Selection and Application

execution EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN execution Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Policies... 5 4.1 Selection and Application

Good Group (International) Limited

Limited") IFRS Core Tools Good Group (International) Limited Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key... 2 Introduction...

IFRS Core Tools Good Group (International) Limited Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key... 2 Introduction...

Ind AS 1 st Time Adoption Challenges. Compiled By Ca Yagnesh Desai ,

Ind AS 1 st Time Adoption Challenges Compiled By Ca Yagnesh Desai. ymdesaiandco@gmail.com +09820133227,0932244770 1 Ind AS 1 : First Time Adoption of Ind AS 1 04? 2 3 Ind-AS 101 : Snap Shot Total Clauses

Ind AS 1 st Time Adoption Challenges Compiled By Ca Yagnesh Desai. ymdesaiandco@gmail.com +09820133227,0932244770 1 Ind AS 1 : First Time Adoption of Ind AS 1 04? 2 3 Ind-AS 101 : Snap Shot Total Clauses

(Entity that already applies the International Financial Reporting Standards)... II-1

... II-1") CONSOLIDATED FINANCIAL STATEMENTS December 31, 2016 (Entity that already applies the International Financial Reporting Standards)... I-1 Independent auditor's report... I-3 Consolidated statements of financial

CONSOLIDATED FINANCIAL STATEMENTS December 31, 2016 (Entity that already applies the International Financial Reporting Standards)... I-1 Independent auditor's report... I-3 Consolidated statements of financial

Wrestling with the First-Time Adoption of IFRS. PwC

Wrestling with the First-Time Adoption of IFRS PwC First time adoption Session outline Exemptions and Preparation of the first IFRS financial statements IFRS 1 General principles Replaces SIC-8 Application

Wrestling with the First-Time Adoption of IFRS PwC First time adoption Session outline Exemptions and Preparation of the first IFRS financial statements IFRS 1 General principles Replaces SIC-8 Application

Alternative format. Illustrative consolidated financial statements for the year ended 31 December International GAAP

IFRS Core Tools Good Group (International) Limited Alternative format Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key...

IFRS Core Tools Good Group (International) Limited Alternative format Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key...

Similarities and Differences

Similarities and Differences A comparison of IFRS and February 2006 www.pwc.com/ifrs PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation. Drawing on the knowledge

Similarities and Differences A comparison of IFRS and February 2006 www.pwc.com/ifrs PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation. Drawing on the knowledge

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD in India Consistently ranked amongst India s top six accounting

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD in India Consistently ranked amongst India s top six accounting

Contents. About this publication 3 Roadmap to the models for Australian entities 5 Model financial statements for the year ended 31 December 2017

International GAAP Holdings Limited Model financial statements for the year 31 December 2017 1 Contents Contents About this publication 3 Roadmap to the models for Australian entities 5 Model financial

International GAAP Holdings Limited Model financial statements for the year 31 December 2017 1 Contents Contents About this publication 3 Roadmap to the models for Australian entities 5 Model financial

3. Financial statements should present information in a manner that:

ATTACHMENT E Exhibit 1 FINANCIAL STATEMENT PRESENTATION PROJECT Phase B: Summary of Tentative Preliminary Views and Illustrative Sample Financial Statements Reflective of Meetings through May 16, 2007

ATTACHMENT E Exhibit 1 FINANCIAL STATEMENT PRESENTATION PROJECT Phase B: Summary of Tentative Preliminary Views and Illustrative Sample Financial Statements Reflective of Meetings through May 16, 2007

Tier 2 For-Profit Reporters

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS REDUCED DISCLOSURE REGIME Tier 2 For-Profit Reporters RDR Layout (New

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS REDUCED DISCLOSURE REGIME Tier 2 For-Profit Reporters RDR Layout (New

Ind AS 1 Presentation of Financial Statements

Ind AS 1 Presentation of Financial Statements CA Rajkumar S Adukia B.Com (Hons), FCA, ACS, ACWA, LLB, DIPR, DLL &LP, IFRS(UK), MBA email id: rajkumarradukia@caaa.in Mob: 09820061049/09323061049 To receive

Ind AS 1 Presentation of Financial Statements CA Rajkumar S Adukia B.Com (Hons), FCA, ACS, ACWA, LLB, DIPR, DLL &LP, IFRS(UK), MBA email id: rajkumarradukia@caaa.in Mob: 09820061049/09323061049 To receive

Disclosure on transition to IFRS

- 13 - Disclosure on transition to The Company adopted in preparing its consolidated financial statements for the fiscal year ended March 31, 2017. The date of transition to is April 1, 2015. (1) First-time

- 13 - Disclosure on transition to The Company adopted in preparing its consolidated financial statements for the fiscal year ended March 31, 2017. The date of transition to is April 1, 2015. (1) First-time

Accounting and auditing research at your fingertips inform.pwc.com

inform.pwc.com March 2017 IFRS pocket guide pwc.com/ifrs Inform Accounting and auditing research at your fingertips inform.pwc.com Online resource for finance professionals worldwide. Use Inform to access

inform.pwc.com March 2017 IFRS pocket guide pwc.com/ifrs Inform Accounting and auditing research at your fingertips inform.pwc.com Online resource for finance professionals worldwide. Use Inform to access

IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look

MPRA Munich Personal RePEc Archive IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September

MPRA Munich Personal RePEc Archive IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September

FINANCIAL PRUDENCE WORKSHOP FOR SMALL MEDIUM SIZE ENTITIES. 8th -10th December 2014, SAFARI PARK NAIROBI.

FINANCIAL PRUDENCE WORKSHOP FOR SMALL MEDIUM SIZE ENTITIES 8th -10th December 2014, SAFARI PARK NAIROBI. FINANCIAL REPORTING FOR SMEs By: CPA JOSEPHAT NJOROGE WAITITU. CONTACTS:JOSEPHAT WAITITU & ASSOCIATES

FINANCIAL PRUDENCE WORKSHOP FOR SMALL MEDIUM SIZE ENTITIES 8th -10th December 2014, SAFARI PARK NAIROBI. FINANCIAL REPORTING FOR SMEs By: CPA JOSEPHAT NJOROGE WAITITU. CONTACTS:JOSEPHAT WAITITU & ASSOCIATES

IFRS for SMEs IFRS Foundation-World Bank

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 9 13 January 2011 Almaty, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 9 13 January 2011 Almaty, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

Insights into IFRS An overview

Insights into IFRS An overview Audit Committee Institute September 2018 kpmg.com/ifrs About the Audit Committee Institute Sponsored by more than 40 member firms around the world, KPMG s Audit Committee

Insights into IFRS An overview Audit Committee Institute September 2018 kpmg.com/ifrs About the Audit Committee Institute Sponsored by more than 40 member firms around the world, KPMG s Audit Committee

PwC Alert. Malaysian Private Entities Reporting Standards (MPERS) A new reporting framework for Private Entities

A new reporting framework for Private Entities") Issue 124 November 2015 PP 9741/10/2012 (031262) PwC Alert Malaysian Private Entities Reporting Standards (MPERS) A new reporting framework for Private Entities Page 3 MPERS at a glance Page 5 Comparing

Issue 124 November 2015 PP 9741/10/2012 (031262) PwC Alert Malaysian Private Entities Reporting Standards (MPERS) A new reporting framework for Private Entities Page 3 MPERS at a glance Page 5 Comparing

Good Group (International) Limited

Limited") Ernst & Young IFRS Core Tools Good Group (International) Limited International GAAP Illustrative interim condensed consolidated financial statements for the period ended 30 June 2013 Based on International

Ernst & Young IFRS Core Tools Good Group (International) Limited International GAAP Illustrative interim condensed consolidated financial statements for the period ended 30 June 2013 Based on International

OVERVIEW OF IND AS INCLUDING CARVE OUTS. C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

New IFRS standards and interpretations. Warsaw, December 2012

New IFRS standards and interpretations Warsaw, December 2012 Agenda Pronouncements Effective First annual year of application* IFRS 1 First-time Adoption of International Financial Reporting Standards

New IFRS standards and interpretations Warsaw, December 2012 Agenda Pronouncements Effective First annual year of application* IFRS 1 First-time Adoption of International Financial Reporting Standards

REPORT OF INDEPENDENT AUDITORS. ABC Manufacturing Company Future Village, Makati City 1 (A Wholly Owned Subsidiary of XYZ Holdings Corporation)

") REPORT OF INDEPENDENT AUDITORS The Board of Directors 123 Maganda Street ABC Manufacturing Company Future Village, Makati City 1 (A Wholly Owned Subsidiary of XYZ Holdings Corporation) We have audited

REPORT OF INDEPENDENT AUDITORS The Board of Directors 123 Maganda Street ABC Manufacturing Company Future Village, Makati City 1 (A Wholly Owned Subsidiary of XYZ Holdings Corporation) We have audited

IFRS AND IND AS Preface

IFRS AND IND AS CA. Rajkumar S. Adukia http://www.carajkumarradukia.com rajkumarfca@gmail.com +91 98200 61049/09323061049 Preface India, one of the fastest growing global economies is on the verge of converging

IFRS AND IND AS CA. Rajkumar S. Adukia http://www.carajkumarradukia.com rajkumarfca@gmail.com +91 98200 61049/09323061049 Preface India, one of the fastest growing global economies is on the verge of converging

Presentation of Financial Statements

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD MASB Standard 1 Presentation of Financial Statements Any correspondence regarding this Standard should be addressed to: The Chairman

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD MASB Standard 1 Presentation of Financial Statements Any correspondence regarding this Standard should be addressed to: The Chairman

Backing Precision. Audit Tax Advisory.

Backing Precision ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2015 New Zealand Equivalents to International Financial Reporting Standards Tier 1 For-Profit Reporters Audit Tax Advisory www.bdo.co.nz

Backing Precision ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2015 New Zealand Equivalents to International Financial Reporting Standards Tier 1 For-Profit Reporters Audit Tax Advisory www.bdo.co.nz