Financial Intermediaries in India. Samir K Mahajan

|

|

|

- Donald Gordon

- 5 years ago

- Views:

Transcription

1 Financial Intermediaries in India

2 Financial Institutions are intermediaries that mobilizes saving and channelize the funds to the productive investment. These are responsible for efficient allocation and distribution of saving among those who demands it. Finical institutions are classified as: Financial Intermediaries /Institutions o Banking financial institutions (creators and purveyors of credit) o Non-banking financial institutions (purveyors of credit)

3 Financial Institutions contd.

4 Development FIs/ Non-Bank Non-Intermediary FIs Development Financial Institutions ( FIs) were set up during the planning period to meet the needs of industrial economy mostly through legislation which would provide term finances to the public sector industrial economy of the country. ü They are not financial intermediaries because till recently they did not mobilize saving from the ultimate surplus spending units and instead obtain funds from Government or RBI. ü They can not be classed as banks though some of them include the terms bank.

5 Development FIs/ Non-Bank Non-Intermediary FIs contd. ü Some of them have turned into companies, and private participation in ownership and functioning has been allowed after new economic reforms in 1990s. ü Some of them entered in commercial banking and diversified their activities in financial sector of the country.

6 Non-Bank Non-Intermediary FIs contd

7 Development FIs contd Classification of Development Financial Institutions qall-india Development FIs Development Banks (mainly confined to over all capital good sector industrial finances) such as : o Industrial Finance Corporation of India (IFCI )1948 o Industrial Credit and Investment Corporation of India (ICICI )1955 o Industrial Development Bank of India( IDBI )1964

8 Classification of Development Financial Institutions contd. Development FIs contd qall-india Development Fis contd. Specialized FIs ( provides finance certain specific areas industrial and productive activities ) such as o Industrial Reconstruction Corporation of India IRCI 1985 now Industrial Investment Bank of India (IIBI )1997 o Export Import Bank of India (EXIM )bank1982 o Tourism Finance Corporation of India (TFCI )1990 o Infrastructure Development Finance Companies ( IDFC)1990

9 Development FIs contd Classification of Development FIs contd. Refinance Institution (extends refinance to banks as well as non-banking financial intermediaries for lending to agricultures. Small scale industries, and housing finance companies. o National Bank For Agriculture And Rural Development (NABARD) 1982 o Small Industries Development Bank of India (SIDBI) 1990 o National Housing Bank (NHB)

10 Classification of Development FIs contd. Development FIs contd Other financial Institutions includes o Deposit Insurance and Credit Guarantee Corporation (DICGC) 1962 o Export Credit Guarantee Corporation of India Limited (ECGC ) 1985 qstate level development financial institution includes o State Finance Corporations (18 nos.) o State Industrial Development Corporations (28 nos.)

11 History of Banking in India In modern times, the first bank was set up in 1683 in Madras by members of East India Company. The first joint stock bank was Bank of Hindustan in Calcutta which was established in Three presidency banks: Banking FIs qbank of Bengal established in Calcutta Presidency in qbank of Bombay in Bombay Presidency set up in 1840 qbank of Madras in Madras Presidency set up in 1843

12 Banking Institutions History of Banking contd. Three presidency banks were merged to form Imperial Bank of India in The role of Imperial Bank was that of commercial bank, a banker s bank and a banker to the government. The Imperial Bank eventually became the State Bank of India.

13 History of Banking contd. Reserve Bank of India was set up in 1935 to check bank failures and to cater to the requirement of agriculture. However, the RBI did not have enough power to regulate or control the commercial banks which were regulated by the Company Law. The RBI was entirely owned by private shareholders. It was nationalized on 1 January In order to enlarge the reach of banking services, the government nationalized Imperial Bank of India by converting it into State bank of India in This step is the first bank nationalization in India.

14 History of Banking contd. By the late 1960s, there had been significant rise in the number of banks and bank branches in the country but banking services did not extend to rural and agriculture sector of the country. In 1969, 14 private sector joint stock banks were nationalized to promote objectives of economic growth and regional balance. This was the second phase of bank nationalization. Further, 6 commercial banks in private sector were nationalized in This is the third phase of bank nationalization. At present there are 27 nationalized bank in the country.

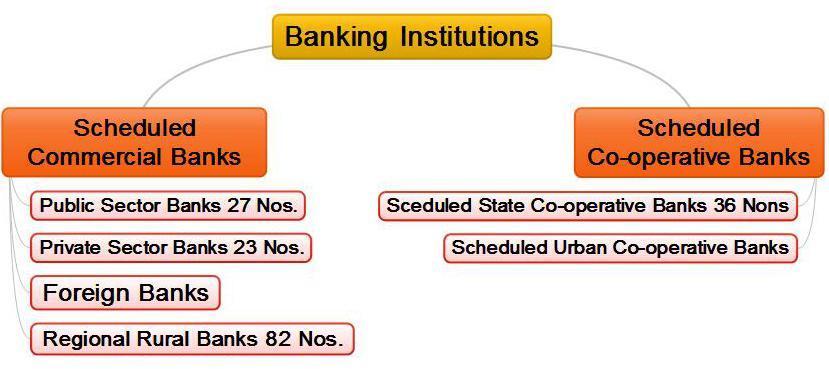

15 History of Banking contd. Banking Instituions Scheduled Commercial Banks Public Sectors Banks Private Sector Banks Scheduled Coperative Banks Schduled State Co-operative Banks Schedule Urban Co-operative Banks Freign Banks Reginal Rural Banks

16 Banking Institutions

17 Scheduled Commercial Banks Commercial banks are governed by Banking Regulation Act. Scheduled Commercial Banks are those which are included in the Second schedule of Reserve Bank of India Act RBI in turn includes only those banks in this schedule which satisfy the criteria laid down vide section 42 (6) (a) of the Act. Scheduled Commercial Banks includes o 21 Public Sector Banks (banks in which government has major holding) o 38 Private Sector Banks o 45 Foreign banks o 82 Regional Rural Banks Note: Bank data (number of banks may change)

18 Scheduled Commercial Banks Public Sector Banks : Public sector banks have State Bank of India and its associates, 19 nationalized banks. State bank of India and its five associates (SB of Patiala, SB of Travancore, SB of Bikaner and Jaipur, SB of Hyderabad, SB of Mysore ) is the largest banking institution in the country with more than bank branches and largest number of ATM network and around 17 percent market share.

19 Scheduled Commercial Banks contd. Private Sector Banks : During bank nationalisation of 14 banks in 1969, no banks were allowed to be set up private sector. In the pre-reformed period there were 19 private sectors banks. However after economic reforms and guidelines of Narasimhan Committee, new private sector banks are allowed to operate in India. Today there are all together 38 private sector banks in the banking sector. Theses banks includes Private - Indian Banks, Local Area Banks (LABs), Small Finance Banks (SFBs), Payments Banks (PBs).

20 Scheduled Commercial Banks contd. Foreign Banks : Foreign banks have been operating in India for decades. A few banks have been operating in India for centuries. ANZ Grindlays had been operating in India for more than hundred years, while Standard Chartered Bank has been around since Many foreign banks from different countries set their branches in India during the 1991 the liberalization period. A total of 27 new foreign banks open branches after economic reforms. Altogether there are 84 foreign banks in India.

21 Scheduled Commercial Banks contd. Regional Rural Banks: Regional Rural Banks were established under the provisions of an Ordinance passed on 26 September 1975 and the RRB Act 1976 to provide sufficient banking and credit facility rural economy of India and to supplement cooperative credits structure. The Government of India, the concerned State Government and the sponsoring bank, contributed to the share capital of RRBs in the proportion of 50%, 15% and 35%, respectively. At present, the sources of funds of RRBs comprise of owned fund, deposits, borrowings from NABARD, Sponsor Banks and other sources including SIDBI and National Housing Bank.

22 Scheduled Commercial Banks contd. The area of operation of the RRBs is limited to notified few districts in a State. However, RRBs may have branches set up for urban operations and their area of operation may include urban areas too. The main purpose of RRB's is to mobilize financial resources from rural / semiurban areas, and grant loans and advances mostly to small and marginal farmers, agricultural labourers and rural artisans. RRBs also carry out government operations like disbursement of wages of MGNREGA workers, distribution of pensions, providing Para-Banking facilities like locker facilities, debit and credit cards etc. There are 82 RRBs in the country.

23 Co-operative Banks Co-operative banks are registered with Registrar of Co-operative Societies (Co-operative Societies Act 1904). These banks are organised and managed on the principles of co-operation, self help and mutual help. They mobilises savings, supply credit and provide remittance facilities but range of services offered by them are narrower, degree of product differentiation in service is much less compared to commercial banks. Co-operative banks are structured in into Urban Co-operative Banks (both Scheduled and Non-scheduled) and Rural Credit Institutions offering short term and long-term loans.

24 Co-operative Banks contd. State Co-operative Bank is the apex of the rural co-operative credit structure (short term ). These banks gets financial and other help NABARD, central and state governments which they disburse to District Central Cooperative Banks and Primary Agricultural Credit Societies. District Central Cooperative banks are the federation of Primary Agricultural Credit Societies. Primary Agricultural Credit Societies are formed at grass root level.

25

26 NABARD (NATIONAL BANK FOR AGRICULTURE AND RURAL DEVELOPMENT) 1982 NABARD is the apex institution for financing agriculture and rural sectors. It co-ordinates the rural financing activities of all institutions engaged in developmental work at the field level and maintains liaison with Government of India, State Governments, Reserve Bank of India (RBI) and other national level institutions concerned with policy formulation. NABARD is a refinancing agency to financial institutions such as state cooperative banks, regional rural banks, and commercial banks for promotion of both farm and non-farm sector in rural areas. It promotes credit for development of agriculture and allied activities (such as: minor irrigation, farm mechanization, land development, soil conservation, dairy, sheep rearing, poultry, piggery, plantation and agriculture, forestry, storage, biogas), small scale industries, cottage and village industries, handicrafts and other rural crafts and allied economics activities in rural areas. It oversees entire rural credit system and to that extent, it has taken over the role of RBI such as refinancing role of RBI relating to state cooperative banks and regionals and rural banks.

27 Non-Bank Financial Intermediaries Non-Banking Financial Intermediaries mobilize savings from the ultimate lenders i.e. the households and supply the same to borrowers i.e. corporate and government sectors. These are business organizations that act as mobilisers and depositories of savings, and purveyors of credit or finance.

28 Non-Bank Financial Intermediaries contd.

29 q Non-Banking Financial Companies (NBFCs) A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 engaged in the business of finance. NBFCs lend and make investments and hence their activities are akin to that of banks; however there are a few differences. NBFC cannot accept demand deposits and cannot form part of payment and settlement system and cannot issue cheque drawn on itself. As per RBI Act 1934, no NBFC can commence or carry on business without a) obtaining a certificate of registration from the RBI and without having a Net Owned Funds of Rs. 25 lakhs (Rs two crore since April 1999). However, NBFCs regulated by other regulators are exempted from the requirement of registration with RBI.

30 qnon-banking Financial Companies (NBFCs) contd. Various types of NBFCs : o Loan Companies (RBI) o Investment Companies (RBI) o Asset Finance Companies (RBI) o Infrastructure Finance Company (RBI) o Microfinance Companies (RBI) o Factors (RBI) o Merchant Banking (SEBI) o Investment Banks (SEBI) o Venture Capital Fund (SEBI) o Stock Broking Companies (SEBI) o Depositories and Custodial Services(SEBI) o Housing Finance Companies o Credit Rating Agencies (SEBI) o Hire-Purchase Companies o Lease Finance Companies o Miscellaneous Non-Banking Financial Companies such as Chit Fund (Chit Funds Act, 1982) o R e s i d u a l N o n - B a n k i n g Financial Companies such as: Nidhis etc. (Companies Act 1956)

31 Non-Bank Financial Intermediaries contd qsmall Savings /Small Saving Organizations Next to commercial banks, Small Saving Organizations mobilize the largest volumes of savings, followed by co-operative banks, UTI. Among these, post office branches play a dominant role. Small Savings constitute nonmarketable debt of public authorities. Though, technically, these saving go to Central Government, these mostly shared with state governments to meet their budgetary obligations. Various Types of Small Savings Instruments are o Post Office Saving Deposits o Post Office Recurring Deposits o Post office Time Deposits o National Savings Certificates o Kisan Vikas Patra o National Savings Schemes

32 Non-Banking Financial Intermediaries contd. qprovident Funds Provident Funds are maintained by salaried people to provide for old age security after superannuation or relief to the family after the income earner s death during the tenure of the job. However, with the introduction of Public Provident Fund Schemes, it is possible for non-salaried earner to save in provident fund. Funds mobilized through provident fund, should be invested wholly or substantially in central and state government securities, and securities guaranteed by these public authorities; securities of public sector financial institutions including banks, and bonds of public sector enterprises, certificates of deposits issued by public sector banks.

33 qprovident Funds contd. Non-Banking Financial Intermediaries contd. Various Types of Provident Funds Instruments are o Employees Provident Funds o Coal Mine Provident Funds o Assam Tea plantations Provident Funds o Public Provident Funds in Post Office or Banks

34 Non-Banking Financial Intermediaries contd. qmutual Funds Mutual Funds /Unit Trusts Mutual Funds Mutual Funds /Unit Trusts mobilise savings from the public by selling units/share, and invests the mobilised funds/resources in large diversified and sound portfolios of equity shares, bonds and money market instruments. It is a pure intermediaries which performs a basic functions of buying and selling of securities on behalf of its unit-holders.

35 Non-Banking Financial Intermediaries contd. qmutual Funds Mutual Funds /Unit Trusts contd. Mutual Fund was introduced in India with the setting up of Unit Trust of India (UTI) in the country in UTI maintained its monopoly and experienced a consistent growth in till The second phase witnessed the entry of mutual fund companies sponsored by nationalised banks and insurance companies since then. The third phase marked a turning point in the history of mutual finds when Securities Exchange Board of India issued Mutual Funds Regulations in January 1993.

36 Non-Banking Financial Intermediaries contd. qinsurance Companies Insurance may be described as a social device to reduce or eliminate risk of life and property. Insurance is a collective bearing of risk. Insurance spreads the loss of the risks and losses of few people among large number of people who as whole subscribe to a common pool or fund which is collected by the insurers. Insurance cannot prevent the occurrence of risks but provides for the losses of risks. Insurance is also a means of savings and investment. The risks can be insured against loss of life/premature death, ailments, loss or theft of property, fire accidents and so on.

37 qinsurance Companies contd. Non-Banking Financial Intermediaries contd. The major players are qlife Insurance Corporation of India (dealing with life/public sector) qgeneral Insurance Corporation of India (dealing with property/public sector) o Oriental Insurance Companies o New India Insurance Company o National Insurance Company o United India Insurance Company q Private Insurers in Life and Property

An Overview of Financial Services Sector in India: A Huge Untapped Potential in the Market. Manendra Singh*

Article 222 KNOWLEDGE RESOURCE [Vol. 38 An Overview of Financial Services Sector in India: A Huge Untapped Potential in the Market Manendra Singh* The growth of financial sector in India at present is

Article 222 KNOWLEDGE RESOURCE [Vol. 38 An Overview of Financial Services Sector in India: A Huge Untapped Potential in the Market Manendra Singh* The growth of financial sector in India at present is

STATUS OF RURAL AND AGRICULTURAL FINANCE IN INDIA

STATUS OF RURAL AND AGRICULTURAL FINANCE IN INDIA Dr. K. K. Tripathy The public capital formation in the agricultural sector is on the decline and the traditional concern about accessibility of agricultural

STATUS OF RURAL AND AGRICULTURAL FINANCE IN INDIA Dr. K. K. Tripathy The public capital formation in the agricultural sector is on the decline and the traditional concern about accessibility of agricultural

INDIAN BANKING SYSTEM (UNIT-4) REGIONAL RURAL BANKS IN INDIA (PART-1)

REGIONAL RURAL BANKS IN INDIA (PART-1)") INDIAN BANKING SYSTEM (UNIT-4) REGIONAL RURAL BANKS IN INDIA (PART-1) 1. INTRODUCTION Hello viewers welcome to the lecture series on Indian Banking System. Today we shall take up unit 4 and we shall discuss

INDIAN BANKING SYSTEM (UNIT-4) REGIONAL RURAL BANKS IN INDIA (PART-1) 1. INTRODUCTION Hello viewers welcome to the lecture series on Indian Banking System. Today we shall take up unit 4 and we shall discuss

ANSWER KEY C F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C Indian Financial System

(CHOICE BASE) SEMESTER - I / C Indian Financial System") ANSWER KEY-00135 C0921 - F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C0584 - Indian Financial System Q1) a) Answer whether the below statements are True or False: (Attempt any 8) (8

ANSWER KEY-00135 C0921 - F.Y.B. Com. (FINANCIAL MANAGEMENT) (CHOICE BASE) SEMESTER - I / C0584 - Indian Financial System Q1) a) Answer whether the below statements are True or False: (Attempt any 8) (8

Development Financial Institutions

CHAPTER 10 Development Financial Institutions LEARNING OBJECTIVES: After studying the chapter you should be able to understand: overview of development financial institutions in india Role of DFis in indian

CHAPTER 10 Development Financial Institutions LEARNING OBJECTIVES: After studying the chapter you should be able to understand: overview of development financial institutions in india Role of DFis in indian

Money and Banking, Commercial Banks. General Economics

Money and Banking, Commercial Banks General Economics Money Money is an important and indispensable element of modern civilization. In ordinary usage, what we use to pay for things is called money. To

Money and Banking, Commercial Banks General Economics Money Money is an important and indispensable element of modern civilization. In ordinary usage, what we use to pay for things is called money. To

ROLE OF RRB IN RURAL DEVELOPMENT. G.K.Lavanya, Assistant Professor, St.Joseph scollege

ROLE OF RRB IN RURAL DEVELOPMENT G.K.Lavanya, Assistant Professor, St.Joseph scollege ABSTRACT: The importance of the rural banking in the economic development of a country cannot be overlooked. The objective

ROLE OF RRB IN RURAL DEVELOPMENT G.K.Lavanya, Assistant Professor, St.Joseph scollege ABSTRACT: The importance of the rural banking in the economic development of a country cannot be overlooked. The objective

FUNCTIONAL PROGRESS OF REGIONAL RURAL BANKS IN PRIORITY SECTOR LENDING: A CASE STUDY OF PUNJAB STATE

I.J.E.M.S., VOL.6 (4) 2015: 197-210 ISSN 2229-600X FUNCTIONAL PROGRESS OF REGIONAL RURAL BANKS IN PRIORITY SECTOR LENDING: A CASE STUDY OF PUNJAB STATE Kaushal Meetu Vivek High School Chandigarh, Union

I.J.E.M.S., VOL.6 (4) 2015: 197-210 ISSN 2229-600X FUNCTIONAL PROGRESS OF REGIONAL RURAL BANKS IN PRIORITY SECTOR LENDING: A CASE STUDY OF PUNJAB STATE Kaushal Meetu Vivek High School Chandigarh, Union

Research Outline on A Study of Financial Performance of Selected Co- Operative Banks in Karnataka

Research Outline on A Study of Financial Performance of Selected Co- Operative Banks in Karnataka Submitted by Nagaraja, R. C, M.Com., M.Phil., S/o Sri. R. Channabasappa, Kakkaragola (at Post) 577 589,

Research Outline on A Study of Financial Performance of Selected Co- Operative Banks in Karnataka Submitted by Nagaraja, R. C, M.Com., M.Phil., S/o Sri. R. Channabasappa, Kakkaragola (at Post) 577 589,

PRIORITY SECTOR LENDING - RRB

PRIORITY SECTOR LENDING - RRB Priority Sector lending includes lending to those sectors that impact large sections of the population, the weaker sections and the sectors which are employment-intensive

PRIORITY SECTOR LENDING - RRB Priority Sector lending includes lending to those sectors that impact large sections of the population, the weaker sections and the sectors which are employment-intensive

REGIONAL RURAL BANKS The need for evolving a hybrid type of credit agency which combines the resource orientation of the commercial banks and the

REGIONAL RURAL BANKS The need for evolving a hybrid type of credit agency which combines the resource orientation of the commercial banks and the rural orientation of the co-operatives has been expressed

REGIONAL RURAL BANKS The need for evolving a hybrid type of credit agency which combines the resource orientation of the commercial banks and the rural orientation of the co-operatives has been expressed

OSN ACADEMY. LUCKNOW

OSN ACADEMY www.osnacademy.com LUCKNOW 0522-4006074 SUBJECT COMMERCE SUBJECT CODE 08 UNIT - IX 9935977317 0522-4006074 [2] S.No. Contents Pages 1 Indian Banking and Industry 3-25 2 Financial System 1-6

OSN ACADEMY www.osnacademy.com LUCKNOW 0522-4006074 SUBJECT COMMERCE SUBJECT CODE 08 UNIT - IX 9935977317 0522-4006074 [2] S.No. Contents Pages 1 Indian Banking and Industry 3-25 2 Financial System 1-6

Mathematical Analysis on the Role of S. B. I. in Indian Economy

http://ijopaar.com; 2016 Vol. 1(1); pp. 57-69 Mathematical Analysis on the Role of S. B. I. in Indian Economy Dr. Shujat Husain Assistant Professor, Department of Commerce Shia P. G. College, Lucknow-226020.

http://ijopaar.com; 2016 Vol. 1(1); pp. 57-69 Mathematical Analysis on the Role of S. B. I. in Indian Economy Dr. Shujat Husain Assistant Professor, Department of Commerce Shia P. G. College, Lucknow-226020.

BANKING AWARENESS MATERIALS PART-I

BANKING AWARENESS MATERIALS PART-I ALL THE BEST... P r e p a r e d b y S H I N E S C H O O L O F B A N K I N G Page 1 TYPES OF BANKS:- 1. Nationalized banks (PSB s) 2. Scheduled banks (Private SB s) 3.

BANKING AWARENESS MATERIALS PART-I ALL THE BEST... P r e p a r e d b y S H I N E S C H O O L O F B A N K I N G Page 1 TYPES OF BANKS:- 1. Nationalized banks (PSB s) 2. Scheduled banks (Private SB s) 3.

In the previous lesson you learnt about the various methods of raising long-term

16 SOURCES OF LONG-TERM FINANCE In the previous lesson you learnt about the various methods of raising long-term finance. Normally the methods of raising finance are also termed as the sources of finance.

16 SOURCES OF LONG-TERM FINANCE In the previous lesson you learnt about the various methods of raising long-term finance. Normally the methods of raising finance are also termed as the sources of finance.

Financial Inclusion & Postal Banking The India Story

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

Nationalised bank./ NABARD. Central Government. Central Government. State Government and the Sponsoring Commercial Reserve Bank of India.

1. The Regional Rural Banks are sponsored by Reserve Bank of India./ NABARD. Any scheduled commercial bank./ All of these. Any scheduled commercial bank. 2. A Regional Rural Bank has an authorized capital

1. The Regional Rural Banks are sponsored by Reserve Bank of India./ NABARD. Any scheduled commercial bank./ All of these. Any scheduled commercial bank. 2. A Regional Rural Bank has an authorized capital

Contents MODULE I : EVOLUTION OF BANKING

Contents MODULE I : EVOLUTION OF BANKING UNIT- 1 Evolution of Bank and Banking Systems Ancient Banking Pre-historic Age Barter system Bronze Age The money needs banks The first bank in the world- Piggy

Contents MODULE I : EVOLUTION OF BANKING UNIT- 1 Evolution of Bank and Banking Systems Ancient Banking Pre-historic Age Barter system Bronze Age The money needs banks The first bank in the world- Piggy

Banking Awareness Question Bank

Banking Awareness Question Bank 1. Accounts are allowed to be operator by cheques in respect of (a) Both savings bank accounts and fixed deposit accounts (b) Savings bank accounts and current accounts

Banking Awareness Question Bank 1. Accounts are allowed to be operator by cheques in respect of (a) Both savings bank accounts and fixed deposit accounts (b) Savings bank accounts and current accounts

International Research Journal of Business and Management IRJBM

A STUDY ON CONSUMER ATTITUDE TOWARDS RETAIL BANKING WITH RESPECT TO STATE BANK OF INDIA Mrs.B.Chitra Assistant Professor, Department of Commerce (UA-DAY), PSG College of Arts and Science, Coimbatore -14

A STUDY ON CONSUMER ATTITUDE TOWARDS RETAIL BANKING WITH RESPECT TO STATE BANK OF INDIA Mrs.B.Chitra Assistant Professor, Department of Commerce (UA-DAY), PSG College of Arts and Science, Coimbatore -14

IJMSS Vol.03 Issue-01, (January 2015) ISSN: Impact Factor

ISSN: Impact Factor") Indian Financial System- Structure and Function Dr Ritu Chandna Associate Professor in Commerce Sant Mohan Singh Khalsa Labana Girls College Barara Introduction Financial System is a set of institutional

Indian Financial System- Structure and Function Dr Ritu Chandna Associate Professor in Commerce Sant Mohan Singh Khalsa Labana Girls College Barara Introduction Financial System is a set of institutional

DOMESTIC SAVING. National Accounts Statistics Sources & Methods, 2007 CHAPTER 24. quasi government bodies and nondepartmental

DOMESTIC SAVING Introduction 24.1 Saving represents the excess of current income over current expenditure and is the balancing item of: the income and outlay accounts (as per 1968 SNA) and use of disposable

DOMESTIC SAVING Introduction 24.1 Saving represents the excess of current income over current expenditure and is the balancing item of: the income and outlay accounts (as per 1968 SNA) and use of disposable

Question Bank. 4. Define the term size transformation of the business of banking. 5. What is meant by risk transformation of thebusiness of banking?

Unit-1 Introduction to Banking 1 Mark Questions 1. List the categories of commercial banks. 2. What is meant by the non-scheduled bank? 3. What is meant by the business of banking? 4. Define the term size

Unit-1 Introduction to Banking 1 Mark Questions 1. List the categories of commercial banks. 2. What is meant by the non-scheduled bank? 3. What is meant by the business of banking? 4. Define the term size

A STUDY OF TOP PRIVATE AND PUBLIC SECTOR BANKS IN INDIA: A COMPARATIVE ANALYSIS OF THEIR FINANCIAL PERFORMANCE

International Journal of Management, IT & Engineering Vol. 8 Issue 1, January 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

International Journal of Management, IT & Engineering Vol. 8 Issue 1, January 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

Contents Evolution and Functions of Money Role of Money Flow of Funds Accounts The Circular Flow of Money Monetary Standards

Contents 1. Evolution and Functions of Money The Barter System; The Evolution of Money; Classification of Money; Money and Near Money; Nature and Definition of Money; Theoretical and Empirical Definitions

Contents 1. Evolution and Functions of Money The Barter System; The Evolution of Money; Classification of Money; Money and Near Money; Nature and Definition of Money; Theoretical and Empirical Definitions

CONCLUSIONS AND SUGGESTIONS

CHAPTER - VIII CONCLUSIONS AND SUGGESTIONS The main function of IDBI, as its name suggests, is to finance industrial enterprises such as manufacturing, mining, processing, shipping and other transport

CHAPTER - VIII CONCLUSIONS AND SUGGESTIONS The main function of IDBI, as its name suggests, is to finance industrial enterprises such as manufacturing, mining, processing, shipping and other transport

Entrepreneurship: Financial Engineering

Entrepreneurship: Financial Engineering Who is an entrepreneur? Personal traits Vision Willingness to take Risk Decision making Leadership Passionate Creative Committed Independent Majority of entrepreneurs

Entrepreneurship: Financial Engineering Who is an entrepreneur? Personal traits Vision Willingness to take Risk Decision making Leadership Passionate Creative Committed Independent Majority of entrepreneurs

E- ISSN X ISSN MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

Dr. Najmi Shabbir Lecturer Shia P.G. College, Lucknow

Banking Development after Nationalization and Social Control in India (1967 To 1991) Dr. Najmi Shabbir Lecturer Shia P.G. College, Lucknow Abstract: This paper mainly analyses the impact of Nationalisation

Banking Development after Nationalization and Social Control in India (1967 To 1991) Dr. Najmi Shabbir Lecturer Shia P.G. College, Lucknow Abstract: This paper mainly analyses the impact of Nationalisation

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur.

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture 39 What I am going to start today is the cooperative banks its amazing

Money and Banking Prof. Dr. Surajit Sinha Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture 39 What I am going to start today is the cooperative banks its amazing

CHAPTER II THE KARNATAKA STATE CO-OPERATIVE AGRICULTURE AND RURAL DEVELOPMENT BANK LTD

CHAPTER II THE KARNATAKA STATE CO-OPERATIVE AGRICULTURE AND RURAL DEVELOPMENT BANK LTD INTRODUCTION In the year 1929 on 25 th November the Mysore State Co-operative Land Mortgage Bank was established in

CHAPTER II THE KARNATAKA STATE CO-OPERATIVE AGRICULTURE AND RURAL DEVELOPMENT BANK LTD INTRODUCTION In the year 1929 on 25 th November the Mysore State Co-operative Land Mortgage Bank was established in

1.7 TOP TEN INDIAN BANKING COMPANIES DURING

1.1 INTRODUCTION 1.2 ORIGIN OF BANKS 1.3 MEANING AND DEFINITIONS OF BANK 1.4 FUNCTIONS OF BANKS 1.5 IMPORTANCE OF BANKS 1.6 STRUCTURE OF INDIAN BANKING SYSTEM 1.6.1 Reserve Bank of India (RBI) 1.6.2 Scheduled

1.1 INTRODUCTION 1.2 ORIGIN OF BANKS 1.3 MEANING AND DEFINITIONS OF BANK 1.4 FUNCTIONS OF BANKS 1.5 IMPORTANCE OF BANKS 1.6 STRUCTURE OF INDIAN BANKING SYSTEM 1.6.1 Reserve Bank of India (RBI) 1.6.2 Scheduled

Banking of India in 2000

Banking of India in 2000 Although some form of banking, mainly of the moneylending type, has been in existence in India since ancient times, it was only over a century ago that proper banking began. The

Banking of India in 2000 Although some form of banking, mainly of the moneylending type, has been in existence in India since ancient times, it was only over a century ago that proper banking began. The

IBPS Clerk Mains (Banking Awareness-Assignment) Banking Awareness. IBPS Clerk (Mains) Exam 2017

Banking Awareness. IBPS Clerk (Mains) Exam 2017") Banking Awareness IBPS Clerk (Mains) Exam 2017 BANKING AWARENESS 1) A NBFC is prohibited to offer or undertake? (A) Accept demand deposits (B) Accept time deposits (C) Lend long term loans (D) Pay a higher

Banking Awareness IBPS Clerk (Mains) Exam 2017 BANKING AWARENESS 1) A NBFC is prohibited to offer or undertake? (A) Accept demand deposits (B) Accept time deposits (C) Lend long term loans (D) Pay a higher

Structure of Indian Banking System

Structure of Indian Banking System Banking - Definition Section 5 of BR Act defines Banking as Accepting deposit from public For the purpose of lending and investment Repayable on demand or otherwise Withdrawable

Structure of Indian Banking System Banking - Definition Section 5 of BR Act defines Banking as Accepting deposit from public For the purpose of lending and investment Repayable on demand or otherwise Withdrawable

Seat No. Total No. of Questions : 6] [Total No. of Printed Pages : 2 [4185]-101

![Seat No. Total No. of Questions : 6] [Total No. of Printed Pages : 2 [4185]-101](/thumbs/95/124619348.jpg "Seat No. Total No. of Questions : 6] [Total No. of Printed Pages : 2 [4185]-101") Total of Questions : 6] [Total of Printed Pages : 2 [4185]-101 P. G. D. F. S. (Semester - I) Examination - 2012 FINANCIAL AND COST ACCOUNTING (2008 Pattern) Time : 3 Hours] [Max. Marks : 70 (1) Answer

Total of Questions : 6] [Total of Printed Pages : 2 [4185]-101 P. G. D. F. S. (Semester - I) Examination - 2012 FINANCIAL AND COST ACCOUNTING (2008 Pattern) Time : 3 Hours] [Max. Marks : 70 (1) Answer

CHAPTER 1 INTRODUCTION

CHAPTER 1 INTRODUCTION Contents 1.1 Genesis of Statement 1.1.1 1 st Phase from the year 1786 to 1947 1.1.2 2 nd Phase from the year 1947 to 1969 1.1.3 3 rd Phase from the year 1969 till beginning of 1990

CHAPTER 1 INTRODUCTION Contents 1.1 Genesis of Statement 1.1.1 1 st Phase from the year 1786 to 1947 1.1.2 2 nd Phase from the year 1947 to 1969 1.1.3 3 rd Phase from the year 1969 till beginning of 1990

LOANS AND ADVANCES OF TNSC BANK

CHAPTER V LOANS AND ADVANCES OF TNSC BANK 5.1 INTRODUCTION 5.2 LOANS AND ADVANCES 5.3 LENDING RATES 5.4 GOVERNMENT OF INDIA INTEREST SUBVENTION 5.5 GOVERNMENT OF TAMIL NADU INTEREST SUBSIDY 5.6 NUMBER

CHAPTER V LOANS AND ADVANCES OF TNSC BANK 5.1 INTRODUCTION 5.2 LOANS AND ADVANCES 5.3 LENDING RATES 5.4 GOVERNMENT OF INDIA INTEREST SUBVENTION 5.5 GOVERNMENT OF TAMIL NADU INTEREST SUBSIDY 5.6 NUMBER

DIVINE IAS ACADEMY [INDIAN ECONOMY NOTES INDIAN BANKING SYSTEM]

![DIVINE IAS ACADEMY [INDIAN ECONOMY NOTES INDIAN BANKING SYSTEM]](/thumbs/77/76147457.jpg "DIVINE IAS ACADEMY [INDIAN ECONOMY NOTES INDIAN BANKING SYSTEM]") Indian Banking System Nationalization and development of banking India Nationalization of RBI in 1949. RBI was established in 1935 according to RBI Act 1934 on the basis of recommendation of Hilton Young

Indian Banking System Nationalization and development of banking India Nationalization of RBI in 1949. RBI was established in 1935 according to RBI Act 1934 on the basis of recommendation of Hilton Young

5. AGRICULTURAL CREDIT MANAGEMENT

Agricultural Credit Management 100 5. AGRICULTURAL CREDIT MANAGEMENT Capital accumulation plays a pivotal role in almost all the models of growth and development because it raises the productive capacity

Agricultural Credit Management 100 5. AGRICULTURAL CREDIT MANAGEMENT Capital accumulation plays a pivotal role in almost all the models of growth and development because it raises the productive capacity

Shabd Braham E ISSN

A Comparative Study of Financial Performance of & Bank Dr.Anjana Gorani (Asst. Prof) R.P.L Maheshwari College CA Omprakash Maheshwari Dr. Hema Mishra (Asst.Prof.) Shree Cloth Market Girls College Indore,

A Comparative Study of Financial Performance of & Bank Dr.Anjana Gorani (Asst. Prof) R.P.L Maheshwari College CA Omprakash Maheshwari Dr. Hema Mishra (Asst.Prof.) Shree Cloth Market Girls College Indore,

BANK EXAMS GENERAL AWARENESS Kinds of Banks in India

BANK EXAMS GENERAL AWARENESS Kinds of s in India The Financial Requirements in a modern economy are of a diverse nature, distinctive variety and large magnitude. These banks satisfy the various needs of

BANK EXAMS GENERAL AWARENESS Kinds of s in India The Financial Requirements in a modern economy are of a diverse nature, distinctive variety and large magnitude. These banks satisfy the various needs of

A study of financial performance of Banks with special reference (ICICI and SBI)

") International Journal of Science, Technology and Humanities 1 (2014) 99-104 Available online at www.svmcugi.com International Journal of Science, Technology and Humanities A study of financial performance

International Journal of Science, Technology and Humanities 1 (2014) 99-104 Available online at www.svmcugi.com International Journal of Science, Technology and Humanities A study of financial performance

Question Answers with Explanation SEBI and other Institutions

Question Answers with Explanation SEBI and other Institutions 1. Which is distributary agency of Kisan Credit Card Scheme? a) NABARD b) SBI c) Rural Development Bank d) Regional Rural Bank and Commercial

Question Answers with Explanation SEBI and other Institutions 1. Which is distributary agency of Kisan Credit Card Scheme? a) NABARD b) SBI c) Rural Development Bank d) Regional Rural Bank and Commercial

CO:RURAL BANKING DEPARTMENT. Revised Kisan Credit Card (KCC) Scheme

Scheme") a MAIN : ADV - 29/2012-13 DT. 14-05-2012 SUB : Rural Lending - 04 CO:RURAL BANKING DEPARTMENT FILE M-2 S-201 Revised Kisan Credit Card (KCC) Scheme Our Bank issued Master circular on Indian Bank Kisan

a MAIN : ADV - 29/2012-13 DT. 14-05-2012 SUB : Rural Lending - 04 CO:RURAL BANKING DEPARTMENT FILE M-2 S-201 Revised Kisan Credit Card (KCC) Scheme Our Bank issued Master circular on Indian Bank Kisan

Financial Regulatory Framework. Multiple Choice Questions

Financial Regulatory Framework Multiple Choice Questions 1. The performance of which scheme does the National Housing Bank monitor? a) Liberalized Finance Scheme b) Golden Jubilee Rural Housing Finance

Financial Regulatory Framework Multiple Choice Questions 1. The performance of which scheme does the National Housing Bank monitor? a) Liberalized Finance Scheme b) Golden Jubilee Rural Housing Finance

CPW2A THEORY OF MONEY AND BANKING. Unit : I

THEORY OF MONEY AND BANKING Unit : I Unit: I Introduction to money Kinds functions and significance Demand for and supply of Money Monetary standards Gold standard Bimetallism and paper currency systems

THEORY OF MONEY AND BANKING Unit : I Unit: I Introduction to money Kinds functions and significance Demand for and supply of Money Monetary standards Gold standard Bimetallism and paper currency systems

PERFORMANCE DIFFERENCE BETWEEN PUBLIC SECTOR BANK AND PRIVATE SECTOR BANK: COMPARATIVE STUDY BETWEEN SBI AND ICICI BANK IN INDIA

PERFORMANCE DIFFERENCE BETWEEN PUBLIC SECTOR BANK AND PRIVATE SECTOR BANK: COMPARATIVE STUDY BETWEEN SBI AND ICICI BANK IN INDIA DR. GARGI SRIVASTAVA Vidya Jyoti Eduversity,Derabassi. PUNYO YARING Vidya

PERFORMANCE DIFFERENCE BETWEEN PUBLIC SECTOR BANK AND PRIVATE SECTOR BANK: COMPARATIVE STUDY BETWEEN SBI AND ICICI BANK IN INDIA DR. GARGI SRIVASTAVA Vidya Jyoti Eduversity,Derabassi. PUNYO YARING Vidya

A Study on Indian Rural Banking Industry - Issues and Challenges

A Study on Indian Rural Banking Industry - Issues and Challenges Monika Bansal *, Sneha Department of Human Resource, BLS Institute of Technology Management, GGSIPU, New Delhi, India Article Info Article

A Study on Indian Rural Banking Industry - Issues and Challenges Monika Bansal *, Sneha Department of Human Resource, BLS Institute of Technology Management, GGSIPU, New Delhi, India Article Info Article

Monetary, Banking and Financial Developments in India

Monetary, Banking and Financial Developments in India 1947-48 to 2009-10 Incorporating A Comprehensive Description and Review, of the Post-Independence Evolution and Present Structure of India's Monetary

Monetary, Banking and Financial Developments in India 1947-48 to 2009-10 Incorporating A Comprehensive Description and Review, of the Post-Independence Evolution and Present Structure of India's Monetary

FINANCIAL MARKETS AND SERVICES. Finance-Specialization. BCom-VI Semester-CUCBCSS-2014 onwards.

FINANCIAL MARKETS AND SERVICES Finance-Specialization BCom-VI Semester-CUCBCSS-2014 onwards. MULTIPLE CHOICE QUESTION BANK WITH ANSWER KEYS 1) ---------- is a set of complex or closely connected or intermixed

FINANCIAL MARKETS AND SERVICES Finance-Specialization BCom-VI Semester-CUCBCSS-2014 onwards. MULTIPLE CHOICE QUESTION BANK WITH ANSWER KEYS 1) ---------- is a set of complex or closely connected or intermixed

Chapter-VII Data Analysis and Interpretation

Chapter-VII Data Analysis and Interpretation 16 CHAPTER-VII DATA ANALYSIS AND INTERPRETATION In order to arrive at a logical and constructive analysis of micro financing by commercial banks in Rajasthan

Chapter-VII Data Analysis and Interpretation 16 CHAPTER-VII DATA ANALYSIS AND INTERPRETATION In order to arrive at a logical and constructive analysis of micro financing by commercial banks in Rajasthan

RoleofPrimaryAgriculturalCoOperativeSocietyPacsinAgriculturalDevelopmentinIndia

Global Journal of Management and Business Research: C Finance Volume 17 Issue 3 Version 1.0 Year 2017 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA)

Global Journal of Management and Business Research: C Finance Volume 17 Issue 3 Version 1.0 Year 2017 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA)

Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012

Bill, 2012") Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012 The Bill was introduced in the Lok Sabha by the Minister of Finance on May 22, 2012. The Bill was referred to the

Legislative Brief The Micro Finance Institutions (Development and Regulation) Bill, 2012 The Bill was introduced in the Lok Sabha by the Minister of Finance on May 22, 2012. The Bill was referred to the

Airo International Research Journal ISSN: March, 2017 Volume IX

1 Impact of Demonetization on Financial inclusion D. VENKAIAH M.Com;M.B.A;M.Phil; (PhD) Research Scholar G.Pulla Reddy Degree & P.G College Abstract Demonetization causes inconvenience for initial few

1 Impact of Demonetization on Financial inclusion D. VENKAIAH M.Com;M.B.A;M.Phil; (PhD) Research Scholar G.Pulla Reddy Degree & P.G College Abstract Demonetization causes inconvenience for initial few

RBI FINANCING GIIDELINES FOR ROOFTOP GRID CONNECTED SOLAR PV SYSTEMS, 2015

RBI FINANCING GIIDELINES FOR ROOFTOP GRID CONNECTED SOLAR PV SYSTEMS, 2015 Sl. No. Description Summary 1. Categories under priority sector Agriculture Micro, Small and Medium Export Credit Education Housing

RBI FINANCING GIIDELINES FOR ROOFTOP GRID CONNECTED SOLAR PV SYSTEMS, 2015 Sl. No. Description Summary 1. Categories under priority sector Agriculture Micro, Small and Medium Export Credit Education Housing

Financial Framework in India

Financial Framework in India For Finance related courses and CSE Main Optional Paper on Finance 10x10 Learning TM 1 10x10 Learning TM 2 Laws applicable to the Financial Sector : Act = 15. Rules = 10. Regulations

Financial Framework in India For Finance related courses and CSE Main Optional Paper on Finance 10x10 Learning TM 1 10x10 Learning TM 2 Laws applicable to the Financial Sector : Act = 15. Rules = 10. Regulations

OPERATIONAL EFFICIENCY OF REGIONAL RURAL BANKS AND OTHER COMMERCIAL BANKS OF ODISHA INDIA: A COMPARATIVE STUDY

OPERATIONAL EFFICIENCY OF REGIONAL RURAL BANKS AND OTHER COMMERCIAL BANKS OF ODISHA INDIA: A COMPARATIVE STUDY Prof. RN Subudhi & Jitendra K. Ram School of Management, KIIT University Bhubaneswar, India

OPERATIONAL EFFICIENCY OF REGIONAL RURAL BANKS AND OTHER COMMERCIAL BANKS OF ODISHA INDIA: A COMPARATIVE STUDY Prof. RN Subudhi & Jitendra K. Ram School of Management, KIIT University Bhubaneswar, India

Non performing assets of NBFI S in India

Non performing of NBFI S in India Journal of Social Welfare and Management 103 Volume 4 Number 2, April - June 2012 S. Kamalaveni*, R. Anitha** Abstract This paper focuses on the non-performing of NBFI

Non performing of NBFI S in India Journal of Social Welfare and Management 103 Volume 4 Number 2, April - June 2012 S. Kamalaveni*, R. Anitha** Abstract This paper focuses on the non-performing of NBFI

Orientation Programme on Credit linked Capital Subsidy Scheme

Orientation Programme on Credit linked Capital Subsidy Scheme Presentation by Shri N.K.Narula,Dy General Manager SIDBI, HYDERABAD MISSION of SIDBI To empower the Micro, Small and Medium Enterprises (MSME)

Orientation Programme on Credit linked Capital Subsidy Scheme Presentation by Shri N.K.Narula,Dy General Manager SIDBI, HYDERABAD MISSION of SIDBI To empower the Micro, Small and Medium Enterprises (MSME)

PERFORMANCE OF LEAD BANK SCHEME IN VIRUDHUNAGAR DISTRICT OF TAMILNADU

PERFORMANCE OF LEAD BANK SCHEME IN VIRUDHUNAGAR DISTRICT OF TAMILNADU A.Surendran 1 and Dr. B.Manoharan 2 1 Assistant Professor in Commerce, Rajapalayam Rajus College, Rajapalayam Email: surendran.ayyan@gmail.com

PERFORMANCE OF LEAD BANK SCHEME IN VIRUDHUNAGAR DISTRICT OF TAMILNADU A.Surendran 1 and Dr. B.Manoharan 2 1 Assistant Professor in Commerce, Rajapalayam Rajus College, Rajapalayam Email: surendran.ayyan@gmail.com

Review of Literature:

Review of Literature: Agriculture sector is vital for India in view of the food and nutritional security of the nation as well as the fact that the sector remains the principal source of livelihood for

Review of Literature: Agriculture sector is vital for India in view of the food and nutritional security of the nation as well as the fact that the sector remains the principal source of livelihood for

In the words of Charles T Horngren, Capital budgeting is a long term planning for making and financing proposed capital outlays.

Capital budgeting I) Meaning of Capital Budgeting: Capital budgeting can be defined as the planning, evaluation and selection of capital expenditure proposals. Capital budgeting is important for firms

Capital budgeting I) Meaning of Capital Budgeting: Capital budgeting can be defined as the planning, evaluation and selection of capital expenditure proposals. Capital budgeting is important for firms

SUCCESSFUL COOPERATIVE SYSTEMS IN GUJARAT, MAHARASHTRA, PUNJAB

SUCCESSFUL COOPERATIVE SYSTEMS IN GUJARAT, MAHARASHTRA, PUNJAB Co-operative credit System in Maharashtra Maharashtra has all along been a leader in cooperative movement. Cooperative has become a way of

SUCCESSFUL COOPERATIVE SYSTEMS IN GUJARAT, MAHARASHTRA, PUNJAB Co-operative credit System in Maharashtra Maharashtra has all along been a leader in cooperative movement. Cooperative has become a way of

INSTITUTIONS. After reading this unit, you should be able to: 2.1 Introduction 2.2 Participants in Money Markets

Markets and Services UNIT 2 FINANCIAL MARKETS AND INSTITUTIONS Objectives After reading this unit, you should be able to: r recognise the various instruments of Financial Market; and r identify various

Markets and Services UNIT 2 FINANCIAL MARKETS AND INSTITUTIONS Objectives After reading this unit, you should be able to: r recognise the various instruments of Financial Market; and r identify various

New Banking Awareness Edition 2015

New Banking Awareness Edition 2015 Study Material For Banking Awareness Aptitude Regd. Office :- A-202, Shanti Enclave, Opp.Railway Station, Mira Road(E), Mumbai. www.bankpo.laqshya.in bankpo@laqshya.in

New Banking Awareness Edition 2015 Study Material For Banking Awareness Aptitude Regd. Office :- A-202, Shanti Enclave, Opp.Railway Station, Mira Road(E), Mumbai. www.bankpo.laqshya.in bankpo@laqshya.in

ECONOMICS WBCS (Mains) 2015

2015") ECONOMICS WBCS (Mains) 2015 5 year plan 121) Consider the following: 1. Growing public sector was emphasized in first eighth plans 2. Planning in India derives its objectives and social premises from the

ECONOMICS WBCS (Mains) 2015 5 year plan 121) Consider the following: 1. Growing public sector was emphasized in first eighth plans 2. Planning in India derives its objectives and social premises from the

Presents The Power of 30!

Presents The Power of 30! A web series of 30 episodes covering different areas of corporate, securities and financial laws for the corporate professionals across the country. COPYRIGHT The presentation

Presents The Power of 30! A web series of 30 episodes covering different areas of corporate, securities and financial laws for the corporate professionals across the country. COPYRIGHT The presentation

MICROFINANCE: ITS EVOLUTION AND VARIOUS MODELS FOR ENPOWERMENT OF RURAL POOR IN INDIA

MICROFINANCE: ITS EVOLUTION AND VARIOUS MODELS FOR ENPOWERMENT OF RURAL POOR IN INDIA * Mrs. Ghousia Shameen, Assistant Prof., Millennium Institute of Management, Aurangabad. INTRODUCTION: The major concern

MICROFINANCE: ITS EVOLUTION AND VARIOUS MODELS FOR ENPOWERMENT OF RURAL POOR IN INDIA * Mrs. Ghousia Shameen, Assistant Prof., Millennium Institute of Management, Aurangabad. INTRODUCTION: The major concern

IJEMR April Vol 8 Issue 04 - Online - ISSN Print - ISSN

Functioning of Kscard Bank in the Economic Development of Farming Community (A Study with reference to Karnataka) Mr. Gopalakrishna K. Dr. Pramod Gonchikar Assistant Professor and Research Scholar, Department

Functioning of Kscard Bank in the Economic Development of Farming Community (A Study with reference to Karnataka) Mr. Gopalakrishna K. Dr. Pramod Gonchikar Assistant Professor and Research Scholar, Department

Indian Microfinance can be chronologically classified into four phases. The four stages are:

Background Note: 03 Microfinance in India: An Overview Indian Microfinance can be chronologically classified into four phases. The four stages are: Phase I: 1900s 1969 Cooperative Movement Phase II: 1969-1991

Background Note: 03 Microfinance in India: An Overview Indian Microfinance can be chronologically classified into four phases. The four stages are: Phase I: 1900s 1969 Cooperative Movement Phase II: 1969-1991

1. Why do you want to join banking sector?

1. Why do you want to join banking sector? Banking is one of the fastest growing sectors in India with more stable and high growth and more over providing wide range of career opportunities for graduates.

1. Why do you want to join banking sector? Banking is one of the fastest growing sectors in India with more stable and high growth and more over providing wide range of career opportunities for graduates.

FINANCIAL INCLUSION USING PRADHAN MANTRI JAN-DHAN YOJANA A CONCEPTUAL STUDY

FINANCIAL INCLUSION USING PRADHAN MANTRI JAN-DHAN YOJANA A CONCEPTUAL STUDY Mr. Divyesh Kumar, Research Scholar, Assistant Professor, Dayananda Sagar Academy of Technology and Management, Udayapura, Kanakapura

FINANCIAL INCLUSION USING PRADHAN MANTRI JAN-DHAN YOJANA A CONCEPTUAL STUDY Mr. Divyesh Kumar, Research Scholar, Assistant Professor, Dayananda Sagar Academy of Technology and Management, Udayapura, Kanakapura

ECONOMIC POLICIES, GROWTH AND STRUCTURAL CHANGE OF INDIA B. A. PRAKASH

ECONOMIC POLICIES, GROWTH AND STRUCTURAL CHANGE OF INDIA B. A. PRAKASH Chairman, Fifth State Finance Commission December 6, 2017 Objectives Examine the economic policies prior and after liberalisation

ECONOMIC POLICIES, GROWTH AND STRUCTURAL CHANGE OF INDIA B. A. PRAKASH Chairman, Fifth State Finance Commission December 6, 2017 Objectives Examine the economic policies prior and after liberalisation

AN ANALYSIS OF IMPACT ON BANKING SECTOR REFORMS IN THE PERFORMANCE OF DEPOSITS AND LOANS AND ADVANCES OF PANDYAN GRAMA BANK IN NADU

AN ANALYSIS OF IMPACT ON BANKING SECTOR REFORMS IN THE PERFORMANCE OF DEPOSITS AND LOANS AND ADVANCES OF PANDYAN GRAMA BANK IN TAMIL NADU V. Alwarnayaki Assistant Professor of Commerce, SRNM College, Sattur

AN ANALYSIS OF IMPACT ON BANKING SECTOR REFORMS IN THE PERFORMANCE OF DEPOSITS AND LOANS AND ADVANCES OF PANDYAN GRAMA BANK IN TAMIL NADU V. Alwarnayaki Assistant Professor of Commerce, SRNM College, Sattur

COMMERCIAL BANKING INTRODUCTION

1 COMMERCIAL BANKING INTRODUCTION Banking occupies one of the most important positions in the modern economic world. It is necessary for trade and industry. Hence it is one of the great agencies of commerce.

1 COMMERCIAL BANKING INTRODUCTION Banking occupies one of the most important positions in the modern economic world. It is necessary for trade and industry. Hence it is one of the great agencies of commerce.

Annual Results FY 08. May 02, 2008

Annual Results May 02, 2008 1 BUSINESS HIGHLIGHTS SBI Group net profit crosses USD 2.24 Billion (Rs 8,960 crore) SBI Stand-alone Net Profit crosses Rs 6,700 crore Net Profit for at Rs 6,729 crore, up by

Annual Results May 02, 2008 1 BUSINESS HIGHLIGHTS SBI Group net profit crosses USD 2.24 Billion (Rs 8,960 crore) SBI Stand-alone Net Profit crosses Rs 6,700 crore Net Profit for at Rs 6,729 crore, up by

A STUDY OF FINANCIAL PERFORMANCE: A COMPARATIVE ANALYSIS OF STATE BANK OF INDIA AND ICICI BANK

A STUDY OF FINANCIAL PERFORMANCE: A COMPARATIVE ANALYSIS OF STATE BANK OF INDIA AND BANK Chahat Gupta, Assistant Professor, G.G.S. College for Women, Chandigarh, India Amandeep Kaur, Assistant Professor,

A STUDY OF FINANCIAL PERFORMANCE: A COMPARATIVE ANALYSIS OF STATE BANK OF INDIA AND BANK Chahat Gupta, Assistant Professor, G.G.S. College for Women, Chandigarh, India Amandeep Kaur, Assistant Professor,

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT 17,62,51,48,07, ,54,51,43,51, ,87,67,92,03,000.

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF NOV/218 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF NOV/218 GENERAL STATEMENT OF ACCOUNT TAMILNADU

CIVIL ACCOUNT FOR THE GOVERNMENT OF GENERAL STATEMENT OF ACCOUNT 17,62,51,48,07, ,14,37,60,32, ,34,23,85,29,000.

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF FEB/219 GENERAL STATEMENT OF ACCOUNT TAMILNADU

REPORT ID: PRINTED BY: PRINTED ON: CIVIL ACCOUNT FOR THE GOVERNMENT OF FOR THE MONTH OF FEB/219 GENERAL STATEMENT OF ACCOUNT TAMILNADU

A Study on Non Performing Assets of Select Public and Private Sector Banks Challenges, Innovations & Strategies

A Study on Non Performing Assets of Select Public and Private Sector Banks Challenges, Innovations & Strategies Prof I.Babu Rathinam, Associate Professor and Head, Department of Corporate Secretaryship,

A Study on Non Performing Assets of Select Public and Private Sector Banks Challenges, Innovations & Strategies Prof I.Babu Rathinam, Associate Professor and Head, Department of Corporate Secretaryship,

Total No. of Questions : 7] [Total No. of Printed Pages : 2 [3885]-101

![Total No. of Questions : 7] [Total No. of Printed Pages : 2 [3885]-101](/thumbs/96/128932629.jpg "Total No. of Questions : 7] [Total No. of Printed Pages : 2 [3885]-101") Total No. of Questions : 7] [Total No. of Printed Pages : 2 [3885]-101 P. G. D. F. S. (Semester - I) Examination - 2010 FINANCIAL AND COST ACCOUNTING (2008 Pattern) Time : 3 Hours] [Max. Marks : 70 (1)

Total No. of Questions : 7] [Total No. of Printed Pages : 2 [3885]-101 P. G. D. F. S. (Semester - I) Examination - 2010 FINANCIAL AND COST ACCOUNTING (2008 Pattern) Time : 3 Hours] [Max. Marks : 70 (1)

Ref.No.: FIDC/ 136/ 0405 June 17, SUB:PRE-BUDGET MEMORANDUM ISSUES RELATING TO NON-BANKING FIN ANCIAL COMPANIES (NBFCs)

") Ref.No.: FIDC/ 136/ 0405 June 17, 2004 To, Mr. P. Chidambaram, Finance Minister, Government of India, North Block, New Delhi - 110 001. Hon ble Finance Minister Sir, SUB:PRE-BUDGET MEMORANDUM 2004-05 -

Ref.No.: FIDC/ 136/ 0405 June 17, 2004 To, Mr. P. Chidambaram, Finance Minister, Government of India, North Block, New Delhi - 110 001. Hon ble Finance Minister Sir, SUB:PRE-BUDGET MEMORANDUM 2004-05 -

AN IMPACT OF TECHNOLOGY IN BANKING SECTOR IN INDIA

AN IMPACT OF TECHNOLOGY IN BANKING SECTOR IN INDIA DR. K. MALA, M.COM. M.PHIL., PH.D., ASSISTANT PROFESSOR IN COMMERCE, BON SECOURS COLLEGE OF ARTS AND SCIENCE (FOR WOMEN.) VILAR ROAD, THANJAVUR. Abstract:

AN IMPACT OF TECHNOLOGY IN BANKING SECTOR IN INDIA DR. K. MALA, M.COM. M.PHIL., PH.D., ASSISTANT PROFESSOR IN COMMERCE, BON SECOURS COLLEGE OF ARTS AND SCIENCE (FOR WOMEN.) VILAR ROAD, THANJAVUR. Abstract:

NBFCs in India s Financial Landscape. - Manisha Sachdeva (Associate Economist) - Darshini Kansara (Research Analyst)

- Darshini Kansara (Research Analyst)") NBFCs in India s Financial Landscape - Manisha Sachdeva (Associate Economist) - Darshini Kansara (Research Analyst) This presentation is based on the Reserve Bank of India (RBI) study and we, at CARE Ratings

NBFCs in India s Financial Landscape - Manisha Sachdeva (Associate Economist) - Darshini Kansara (Research Analyst) This presentation is based on the Reserve Bank of India (RBI) study and we, at CARE Ratings

Chapter 3 INDIAN BANKING STRUCTURE AN OVERVIEW

Chapter 3 INDIAN BANKING STRUCTURE AN OVERVIEW 3.1 Introduction The existing banking structure in India, evolved over several decades, is elaborate and has been serving the credit and banking services

Chapter 3 INDIAN BANKING STRUCTURE AN OVERVIEW 3.1 Introduction The existing banking structure in India, evolved over several decades, is elaborate and has been serving the credit and banking services

19 th Year of Publication. A monthly publication from South Indian Bank.

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 19 th Year of Publication SIB STUDENTS

To kindle interest in economic affairs... To empower the student community... Open YAccess www.sib.co.in ho2099@sib.co.in A monthly publication from South Indian Bank 19 th Year of Publication SIB STUDENTS

ROLE OF GOVERNMENT IN FINANCIAL INCLUSION

Continuous issue-14 May - August 2015 ROLE OF GOVERNMENT IN FINANCIAL INCLUSION INTRODUCTION: Providing financial access to the poor by connecting them with banks has always been an important priority

Continuous issue-14 May - August 2015 ROLE OF GOVERNMENT IN FINANCIAL INCLUSION INTRODUCTION: Providing financial access to the poor by connecting them with banks has always been an important priority

Non-Performing Assets - Status And Impact

Non-Performing Assets - Status And Impact Ms. Laveena Mehta Assistant Professor, Chitkara University, Research Scholar, Punjab Technical University Avneet Singh Student, Chitkara University, Punjab Abstract:

Non-Performing Assets - Status And Impact Ms. Laveena Mehta Assistant Professor, Chitkara University, Research Scholar, Punjab Technical University Avneet Singh Student, Chitkara University, Punjab Abstract:

NBFC Prudential Norms & Compliances Important Aspects

NBFC Prudential Norms & Compliances Important Aspects Bombay Chartered Accountants Society CA Bhavesh Vora Coverage Existence of NBFCs Last Decade of NBFC Banks Vs. Non-Banks Meaning of NBFCs Major Changes

NBFC Prudential Norms & Compliances Important Aspects Bombay Chartered Accountants Society CA Bhavesh Vora Coverage Existence of NBFCs Last Decade of NBFC Banks Vs. Non-Banks Meaning of NBFCs Major Changes

Price Band : Rs per share December 10, 2010 IPO open during : December 13-16, 2010 (for QIBs issue closes on Dec.

Punjab & Sind Bank Ltd. I P O N O T E Price Band : Rs 113-120 per share December 10, 2010 IPO open during : December 13-16, 2010 (for QIBs issue closes on Dec. 15, 2010) Book Running Lead Manager To list

Punjab & Sind Bank Ltd. I P O N O T E Price Band : Rs 113-120 per share December 10, 2010 IPO open during : December 13-16, 2010 (for QIBs issue closes on Dec. 15, 2010) Book Running Lead Manager To list

Management s Discussion & Analysis

Management s Discussion & Analysis FINANCIALS AS PER INDIAN GAAP The effective date of the merger of ICICI, ICICI PFS and ICICI Capital with ICICI Bank ( the merger ) was May 3, 2002. However, the Appointed

Management s Discussion & Analysis FINANCIALS AS PER INDIAN GAAP The effective date of the merger of ICICI, ICICI PFS and ICICI Capital with ICICI Bank ( the merger ) was May 3, 2002. However, the Appointed

FUNDS MANAGEMENT OR FUNCTIONAL AREAS OF ICICI BANK

FUNDS MANAGEMENT OR FUNCTIONAL AREAS OF ICICI BANK Anjali Gupta Assistant Professor in Commerce CCAS Jains Girls College, Ganaur Sonepat (Haryana), India The ICICI Bank total business Rs. 48421 crores,

FUNDS MANAGEMENT OR FUNCTIONAL AREAS OF ICICI BANK Anjali Gupta Assistant Professor in Commerce CCAS Jains Girls College, Ganaur Sonepat (Haryana), India The ICICI Bank total business Rs. 48421 crores,

Bonanza Portfolio Ltd

Public Issue of Tax Free Secured Redeemable Non-Convertible Bonds issued by HIGHLIGHTS OF TAX BENEFITS In exercise of the powers conferred by item (h) of sub-clause (iv) of clause (15) of Section 10 of

Public Issue of Tax Free Secured Redeemable Non-Convertible Bonds issued by HIGHLIGHTS OF TAX BENEFITS In exercise of the powers conferred by item (h) of sub-clause (iv) of clause (15) of Section 10 of

Banking in India- A Success Story

Banking in India- A Success Story ANURAG SHARMA M.Com, B.Com (H), CA, CS MOHD. SAJID M.Com, B.Com (H) HASHIR MAIRAJ M.Com, B.Com (H) Abstract: Indian Banking system by and large has shown a very positive

Banking in India- A Success Story ANURAG SHARMA M.Com, B.Com (H), CA, CS MOHD. SAJID M.Com, B.Com (H) HASHIR MAIRAJ M.Com, B.Com (H) Abstract: Indian Banking system by and large has shown a very positive

Efficacy of Andhra Pragathi Grameena Bank (APGB) in Andhra Pradesh: A Conventional Analysis

in Andhra Pradesh: A Conventional Analysis") Efficacy of Andhra Pragathi Grameena Bank (APGB) in Andhra Pradesh: A Conventional Analysis Rajashekar 1, Dr. Sudarsana Murthy 2 1 Research Scholar, Dept. Of Management Studies, JNTUA, Ananthapuramu, A.P.,

Efficacy of Andhra Pragathi Grameena Bank (APGB) in Andhra Pradesh: A Conventional Analysis Rajashekar 1, Dr. Sudarsana Murthy 2 1 Research Scholar, Dept. Of Management Studies, JNTUA, Ananthapuramu, A.P.,

Chapter-2 History and development of DFIs

Chapter-2 History and development of DFIs Chapter-2 History and development of DFIs 2.1 A brief history of DFIs Development financial institutions (DFIs) are financial institutions that were established

Chapter-2 History and development of DFIs Chapter-2 History and development of DFIs 2.1 A brief history of DFIs Development financial institutions (DFIs) are financial institutions that were established

Regional Rural Banks- Sustainability through Outreach. Amarendra Sahoo Chief General Manager RBI, Mumbai

Regional Rural Banks- Sustainability through Outreach Amarendra Sahoo Chief General Manager RBI, Mumbai Scheme of Presentation I. RRBs mandate and to what extent fulfilled II. Perceived tension between

Regional Rural Banks- Sustainability through Outreach Amarendra Sahoo Chief General Manager RBI, Mumbai Scheme of Presentation I. RRBs mandate and to what extent fulfilled II. Perceived tension between

INDIAN FINANCIAL SYSTEM OPPORTUNITIES AND CHALLENGES FOR BANKING SECTOR: AN ASSESSMENT

INDIAN FINANCIAL SYSTEM OPPORTUNITIES AND CHALLENGES FOR BANKING SECTOR: AN ASSESSMENT Prof. Vaishali Doshi Assistant Professor Modern College Of Arts Science &Commerce (Wing of Computer and Business Studies)

INDIAN FINANCIAL SYSTEM OPPORTUNITIES AND CHALLENGES FOR BANKING SECTOR: AN ASSESSMENT Prof. Vaishali Doshi Assistant Professor Modern College Of Arts Science &Commerce (Wing of Computer and Business Studies)

ABHINAV NATIONAL MONTHLY REFEREED JOURNAL OF RESEARCH IN COMMERCE & MANAGEMENT

FINANCIAL SECTOR REFORMS IN INDIA A DESCRIPTIVE ANALYSIS Bhargab Kumar Kalita Research Scholar, Department of Economics, Gauhati University, Assam, India Email: bhargabk@yahoo.com ABSTRACT Financial sector

FINANCIAL SECTOR REFORMS IN INDIA A DESCRIPTIVE ANALYSIS Bhargab Kumar Kalita Research Scholar, Department of Economics, Gauhati University, Assam, India Email: bhargabk@yahoo.com ABSTRACT Financial sector