The EY Life Insurance Index. 1 st quarter 2016

|

|

|

- Shauna Fleming

- 5 years ago

- Views:

Transcription

1 The EY Life Insurance Index 1 st quarter 2016

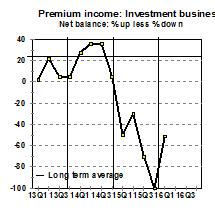

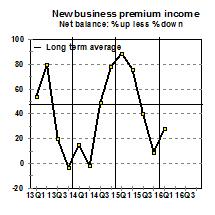

2 Executive Summary Life insurance confidence recovers marginally According to the BER s survey, growth in premium income was minimal in 16Q1. Premium income from both risk and investment business contracted again, even more so than in 15Q4. Continued declines in new business premiums and rising lapses lead to a weak premium income outlook. After moving broadly sideways during 2015, growth in investment income fell in 16Q1. Growth in administrative and marketing expenses edged lower during 16Q1. In 16Q1, net profits after tax increased in line with 15Q4 levels. The Financial Services Index 1 st quarter 2016 EY 2

3 Life insurance Slow economic growth and weak investor confidence in emerging markets across the globe has resulted in a slowdown for life insurers from both their main revenue earnings streams, namely premium income and investment earnings. With equity markets falling across most of the globe, and asset prices weakening, this has inevitably slowed investment income growth. Added to that, weak economic growth has seen a considerable slowdown in both corporate and individual premiums. Life insurer confidence increased from 74 index points in 15Q4 to 79 in 16Q1, with life insurers returning to being the most confident of all financial services segments (this after investment banker confidence fell sharply in the first quarter). Life insurers are only marginally below their long-term average confidence level (82). The stronger confidence is in line with marginally stronger profits growth, and a sharp recovery in new business value. By historical measures, confidence levels are weak, although much stronger than the other financial services segments. According to data from the SA Reserve Bank s March 2016 Quarterly Bulletin, slow growth in premiums is ascribed to both weak group and individual premiums (see the charts below). According to the BER s survey, there was close to zero growth in premiums in 16Q1, with both risk and investment business contracting, albeit at an improved pace since 15Q4. Continued declining new business premiums, coupled with rising lapses do not bode well for future premium income flows. With the exception of the High Net Worth segment of the retail market, strong pressures are impacting household finances, with rising prices and higher interest rates, coupled with limited job prospects all playing a role. After moving broadly sideways during 2015, investment income growth shrank sharply in 16Q1. Benefit pay-outs picked up noticeably in the third quarter and further in the fourth quarter of 2015 after a long period of sedate growth between the middle of 2013 and the middle of Pay-outs slowed noticeably in 16Q1, but respondents expect a rebound in 16Q2. Life insurers reported lower administrative and marketing expenses growth in 16Q1. Lower costs were in line with considerably lower headcount numbers, with both the sales force and administrative employee numbers declining. Life insurers have been cutting back on the administrative headcount for a full year now, whilst the first quarter was the first to see sales force numbers shrinking. Net profits after tax increased again in the quarter, in line with 15Q4 levels. The Financial Services Index 1 st quarter 2016 EY 3

4 Survey data: Life Insurance Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2* 1 Business confidence Inflow a) total inflow 3, b) total premium income 3, i) risk business / no of new contracts ii) investment business (only individual business) c) new business premium income d) lapses / no of contracts terminated e) investment income 3, Outflow a) total outflow 3, b) benefits c) value of surrenders d) sales remuneration 3, e) administration and marketing expenses f) number of full-time admin employees 3, g) number of in-house agents Profitability a) net profit after tax b) profitability of risk business c) administration expenses as % of premium income d) value of new business * Expected 1. Individual life and retirement annuities business plus group life and employee benefit business. 2. % satisfactory, weighted according to firm size 3. Net balance (see Technical Note at the end of the report), weighted according to firm size 4. Weighted net balance (80% total premium income + 20% investment income) 5. The total reflects the responses of participants. It is therefore not calculated as the average of the responses to the components. Each data series has to be considered on its own. Deviations between the total and components occur when participants reply the same given that the net balance statistic does not take the same responses into account. The fact that respondents only answer questions applicable to them and that missing items are not imputed also have an effect. 6. Investment income refers to all income from investments and not the investment return. It includes dividend, interest, rental and other non-capital investment income, as well as realised and unrealised capital gains and losses on investments. 7. Weighted net balance (90% benefits + 10% administration and marketing expenses) 8. Distribution costs and commissions. 9. Excluding field staff The Financial Services Index 1 st quarter 2016 EY 4

5 The Financial Services Index 1 st quarter 2016 EY 5

6 The Financial Services Index 1 st quarter 2016 EY 6

7 Technical note A document with more information on the survey method is available on Click the button named Services and then select Surveys and finally Financial Services. Alternatively, click on EY Financial Survey on the home page and then on Financial Services under Quick Links. Survey method The BER started conducting surveys amongst retail and investment banks in The scope of the survey was expanded to asset managers and life insurers in EY, the international accounting and business advisory firm, not only supports the financial sector survey financially, but also made valuable inputs to the design and makes the overall results public. However, the BER conducts the survey and interprets the results. The BER treats the identities of participants and individual responses as confidential and does not reveal this information to any third party, including the sponsoring firm. The division heads of all the major retail banks, investment banks, asset managers and life insurers operating in South Africa participate in the survey. The survey results reveal current and expected changes in income, expenses and profitability for these firms South Africa operations only. Industry specific issues, such as banks credit standards and the demand for various products of asset managers, are covered during the first and third quarter surveys. The surveys are conducted during March, June, September and December. The results reflect developments per calendar quarter, i.e. the first quarter reflect developments during January, February and March; the second quarter reflects April, May and June etc. On occasion questionnaires reach us after the date on which the results of the current quarter are processed. Small revisions of the survey results of the previous quarter could occur when we process such questionnaires at a later stage. The need for the financial sector survey South Africa has one of the most advanced financial sectors of all emerging market economies and its development is in many respects on par with those of industrialised countries and yet its performance is not measured regularly and consistently. There is a general consensus on the need for a regular, consistent and impartial financial services survey, from managers in the financial sector to financial analysts. The contribution of the financial sector to GDP has in-creased over the past decade and stood at 9.7% during The contribution of for example real estate (6.0%), transport (6.6%) and retail trade (7.2%) are all lower compared to that of the financial sector. However, the general government (16.5%), manufacturing (12.8%) and mining (10.2%) are bigger. Despite its importance, current information on the performance of the financial sector lags behind: Statistics SA publishes GDP and employment figures for the sector covering financial intermediation, insurance, real estate and business services with a lag of one quarter and no details about the sector s financial performance. The compulsory monthly BA 120 (DI 200 until 2007) returns of banks to and the Annual Report of the Bank Supervision Department of the Reserve Bank, the Quarterly Financial Stability Review of the Financial Stability Department of the Reserve Bank and the Annual Report of the Financial Services Board (FSB) provide detailed information about the performance of banks and other financial institutions, but the information is made public with a lag in time except for the BA 120 returns. The interim and annual reports of listed financial companies provide information about their performance, but these reports appear at irregular intervals (their release dates depend on the financial year-ends of the different companies) and the results are not always comparable. The periodic Price Waterhouse Coopers (PWC) Survey, although entirely relevant in relation to its intended target market and ultimate aim, differs fundamentally from the EY financial services survey. The EY survey measures the same performance criteria of financial institutions over time, appears quarterly and the results are obtained by means of short questionnaires. The Financial Services Index 1 st quarter 2016 EY 7

8 The quarterly unit trust and bi-annual life insurance reviews of the Association for Savings and Investment SA (ASISA) are useful. However, the unit trust review does not provide information on the financial performance of management companies and the life insurance review is only published twice a year. The investment performance and strategy of asset managers are measured regularly (e.g. Alexander Forbes and Plexus), but no regular, consistent measure of income and expenditure of asset managers exist. The Financial Services Index 1 st quarter 2016 EY 8

9 The international standing of the financial sector survey The UK, Poland and Switzerland have the longest experience in conducting financial services surveys. In the UK, the Confederation of British Industries (CBI) in London has been conducting comprehensive quarterly financial services surveys in partnership with Price Waterhouse Coopers (PWC) since December In Poland, the Research Institute for Economic Development (RIED) at the Warsaw School of Economics has been conducting a banking survey since The Swiss Business Cycle Institute (KOF) in Zurich has been conducting a quarterly banking and insurance survey since the beginning of In the USA, the Federal Reserve Bank has been conducting a Senior Loan Officer Opinion Survey on Bank Lending Practices for many years, but unlike the UK, Polish and Swiss banking surveys, it focuses on bank lending practices and not the financial performance of the bank sector. The South African financial services survey is modelled on those of the UK and Switzerland. However, the questionnaire has been adapted for South African conditions and needs. Furthermore, it also includes the questions on credit standards for approving applications for loans and credit lines out of the US Senior Loan Officer Opinion Survey. Ensuring the reliability and accuracy of the financial sector survey The questionnaire has been designed for maximum efficiency and minimum input time. Only multiple-answer type ticks are required. No figures are requested. For example, participants only have to tick if a particular activity (such as total income or number of people employed) is up, the same or down compared to the same period a year ago and with respect to their South African operations only. Respondents are carefully selected and approached on the basis of their position in the financial world. The head of retail banking or the head of group life insurance is quizzed and not the chairperson of the board of directors of the group or holding company. Divisional heads tend to be best informed about their business units. The confidentiality of the responses adds to the honesty and candour of participants. Furthermore, respondent quality is monitored. The same group of participants is surveyed from one quarter to the next. Changes in the results from one quarter to the next can therefore be attributed to an actual change in the performance yardstick in question and not because of the participation or not of particular banks, asset managers or life insurers. South Africa has relatively few banks, asset managers and life insurers. For example, four banks dominate the retail and six the merchant and investment banking sector. Likewise, two companies dominate the life insurance industry. The number of potential participants in a financial sector survey is therefore relatively low in South Africa. The degree of presentation of the panel of participants has an important impact on the reliability of a quantitative survey, i.e. when respondents have to indicate actual amounts for each activity and the rand value of the level and change are calculated. In contrast, the financial sector survey is a qualitative survey, i.e. the majority view of respondents on a particular activity is taken as an indication of the direction and strength of the trend in that activity. The degree of presentation of the panel of participants is less of a concern in the case of qualitative surveys. Furthermore, the participation or not of a particular respondent has less of an impact on the overall results in the case of qualitative surveys compared to quantitative ones, as the view of the majority is established and not the actual size. The participating retail and investment banks accounted for 95% of total assets of registered banks in December The value of the total funds under management of the participating asset managers accounted for 63% of the total during the second quarter of For reasons of focus, the following financial institutions are not covered, namely short-term insurers, public financial institutions (e.g. the Reserve Bank, Land Bank, Post Bank and official pension and provident funds), medical insurance savings schemes, the informal micro-lending and savings industry, retailers providing credit and individual insurance brokers/agents. The survey also only focuses on the supply of financial services and not on the demand for such services, which stems from government, businesses, households and the rest of the world. The survey results reveal trends and not actual figures. The net balance statistic is used to interpret the survey results. (See next section for more details on the interpretation of the net balance statistic.) The net balance statistic is the percentage of respondents replying up less the percentage replying down. The percentage of respondents replying the same is ignored. Over the years, the net balance statistic has proved to be the most reliable indicator of the direction and size of change in the trend The Financial Services Index 1 st quarter 2016 EY 9

10 of the respective activities surveyed. The net balance statistic is a qualitative yardstick of the direction and size of the year-on-year growth rate of a particular activity. A positive net balance implies positive year-on-year growth and vice versa. The higher the value of the net balance (positive / negative), the larger the rate of increase / decrease of the activity in question. To aggregate the sector performance, individual responses are weighted according to their relative size. It makes sense that the response of a small participant has to count less compared to that of a large participant. Results are published according to type of activity (e.g. retail banking, investment banking, life insurance and asset management) and not per institution (e.g. ABSA, Investec, Sanlam or Coronation). How to interpret the net balance statistic We base our interpretation of the survey results on the net balance statistic. Over the years, the net balance statistic has proved to be the most reliable indicator of the direction and size of change in the trend of the respective activities surveyed. The net balance statistic is the percentage of respondents replying up less the percentage replying down. The percentage of respondents replying the same is ignored. For example, if the percentage of respondents rating the volume of business higher / the same / lower compared to the same period a year ago is as follows: Higher Same Lower Net balance 70% 10% 20% 50% Then we can conclude that the majority of participants experienced higher business volumes. A net majority (i.e. the percentage of respondents rating the volume of business higher less the percentage rating the volume lower) of 50% is registered in the above example. The net balance statistic is an advanced qualitative yardstick / indicator of the direction (up, same or down) and size (small or large) of the year-on-year percentage change of the corresponding quantitative data (if available) of a particular activity. A net balance of zero tends to indicate no growth (marked A on the accompanying chart), between 0 and 100 a contraction (marked B ) and between 0 and 100 an expansion (marked C ) compared to the same quarter a year ago. A positive net balance, therefore, implies positive year-on-year growth and vice versa. The higher the value of the net balance (positive / negative), the larger the rate of increase / decrease of the activity in question tend to be. Note that a net balance of 50%, for instance, is therefore not equivalent to a 50% decline (calculated year-on-year) in the quantitative data series. A net balance of 50% may correspond to 10% in the case of one set of quantitative data and 3% in another case. The net balance and corresponding percentage change in the quantitative data vary from one data set to the next and this relationship could only be established if many data points are available. The Financial Services Index 1 st quarter 2016 EY 10

11 Published March 2016 Warning This material has been prepared for general information purposes only and may not be relied upon as accounting, tax, or other professional advice. EY specifically renounces any liability for reliance on this material by either you or any third party to whom this material may be distributed. Please refer to your advisors for specific advice. EY Assurance Tax Transactions Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com EYGM Limited. All Rights Reserved.

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for Stronger

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for Stronger

Cyprus. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Renewed external funding to support growth, but is a worry Published in collaboration with Highlights The ending of capital controls and the approval

EY Forecast June 215 rebalancing recovery Outlook for Renewed external funding to support growth, but is a worry Published in collaboration with Highlights The ending of capital controls and the approval

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Eurozone. EY Eurozone Forecast March 2014

Eurozone EY Eurozone Forecast March 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

Eurozone EY Eurozone Forecast March 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

Slovenia. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Activity to remain solid this year, after growing 2.4% in 214 Published in collaboration with Highlights n GDP grew by 2.4% in 214 and 3% in Q1 215,

EY Forecast June 215 rebalancing recovery Outlook for Activity to remain solid this year, after growing 2.4% in 214 Published in collaboration with Highlights n GDP grew by 2.4% in 214 and 3% in Q1 215,

Eurozone. EY Eurozone Forecast December 2013

Eurozone EY Eurozone Forecast December 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany Strong

Eurozone EY Eurozone Forecast December 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany Strong

Ireland. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

Morningstar Rating Analysis of South African Domiciled Asset Managers

Morningstar South Africa Q3 2017 Morningstar Rating Analysis of South African Domiciled Asset Managers 30 September 2017 Authors: Matthew Mellors Matthew Vass Content Morningstar Rating Analysis of South

Morningstar South Africa Q3 2017 Morningstar Rating Analysis of South African Domiciled Asset Managers 30 September 2017 Authors: Matthew Mellors Matthew Vass Content Morningstar Rating Analysis of South

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Inward investment after Brexit

EY s UK Attractiveness Survey Inward investment after Brexit March 2018 Contents Executive summary 1 Investor perspectives on FDI 2 Methodology 11 About EY s Attractiveness Program 12 Executive summary

EY s UK Attractiveness Survey Inward investment after Brexit March 2018 Contents Executive summary 1 Investor perspectives on FDI 2 Methodology 11 About EY s Attractiveness Program 12 Executive summary

European Banking Barometer 2H13

A brighter outlook? Autumn/Winter 2013 Belgium Focus Introduction As part of EY s commitment to building a better working world, we have developed the European Banking Barometer to provide our clients

A brighter outlook? Autumn/Winter 2013 Belgium Focus Introduction As part of EY s commitment to building a better working world, we have developed the European Banking Barometer to provide our clients

Applying IFRS. ITG discusses IFRS 9 impairment issues at December 2015 ITG meeting. December 2015

Applying IFRS ITG discusses IFRS 9 impairment issues at December 2015 ITG meeting December 2015 Contents Introduction... 3 Paper 1 - Incorporation of forward-looking information... 4 Paper 2 - Scope of

Applying IFRS ITG discusses IFRS 9 impairment issues at December 2015 ITG meeting December 2015 Contents Introduction... 3 Paper 1 - Incorporation of forward-looking information... 4 Paper 2 - Scope of

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for exits bailout,

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for exits bailout,

Can today s operational challenges create tomorrow s opportunities?

Can today s operational challenges create tomorrow s opportunities? A review of South Africa s banking sector financials 2017 13 March 2018 Analysis of South Africa s six largest banks, based on 12 month

Can today s operational challenges create tomorrow s opportunities? A review of South Africa s banking sector financials 2017 13 March 2018 Analysis of South Africa s six largest banks, based on 12 month

The Basel Committee Guidance on credit risk and accounting for expected credit losses. January 2016

The Basel Committee Guidance on credit risk and accounting for expected credit losses January 2016 What you need to know The G-CRAECL applies to ECLs calculated under both US GAAP and IFRS. However, as

The Basel Committee Guidance on credit risk and accounting for expected credit losses January 2016 What you need to know The G-CRAECL applies to ECLs calculated under both US GAAP and IFRS. However, as

Eurozone. EY Eurozone Forecast December 2014

Eurozone EY Eurozone Forecast December 2014 Outlook for Road to recovery remains strewn with obstacles Published in collaboration with Highlights GDP growth With the Finnish economy still struggling to

Eurozone EY Eurozone Forecast December 2014 Outlook for Road to recovery remains strewn with obstacles Published in collaboration with Highlights GDP growth With the Finnish economy still struggling to

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Malta

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Malta

IFRS adopted by the European Union

IFRS adopted by the European Union Status of the endorsement process for IFRS standards, interpretations and amendments issued by the IASB as at 31 December 2017 February 2018 1. Published International

IFRS adopted by the European Union Status of the endorsement process for IFRS standards, interpretations and amendments issued by the IASB as at 31 December 2017 February 2018 1. Published International

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for Modest

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Slovakia Slovenia Spain Outlook for Modest

Business Expectations Survey March 2014 Summary Review

Business Expectations Survey March 2014 Summary Review 1. Introduction The BES reports on current confidence levels among local businesses as well as their expectations of movements in key economic indicators.

Business Expectations Survey March 2014 Summary Review 1. Introduction The BES reports on current confidence levels among local businesses as well as their expectations of movements in key economic indicators.

Investec Services PMI Ireland

Embargoed until: 06:00 (Dublin) July 4th 18 Investec Services PMI Ireland Sharpest rise in activity since January Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

Embargoed until: 06:00 (Dublin) July 4th 18 Investec Services PMI Ireland Sharpest rise in activity since January Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Ireland

Eurozone EY Eurozone Forecast September 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Ireland

Can consumer goods companies benefit from the expected uptick? Consumer Products analysis February 2018

Can consumer goods companies benefit from the expected uptick? Consumer Products analysis February 2018 A sombre but improving economic outlook South Africa s 2017 growth recovered, but remains weak Weak

Can consumer goods companies benefit from the expected uptick? Consumer Products analysis February 2018 A sombre but improving economic outlook South Africa s 2017 growth recovered, but remains weak Weak

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Slovenia

Eurozone EY Eurozone Forecast June 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Slovenia

District Economic. Structurally Deficient Bridges, 2001 (Percent)

") District Economic BY ROBERT LACY Apprehension about terrorism and political developments regarding Iraq cast a pall over the Fifth District economy in the last three months of. Many businesses continued

District Economic BY ROBERT LACY Apprehension about terrorism and political developments regarding Iraq cast a pall over the Fifth District economy in the last three months of. Many businesses continued

Investec Services PMI Ireland

Embargoed until: 06:00 (Dublin) September 5th 18 Investec Services PMI Ireland Activity rises at sharper pace in August Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

Embargoed until: 06:00 (Dublin) September 5th 18 Investec Services PMI Ireland Activity rises at sharper pace in August Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec

Eurozone. EY Eurozone Forecast March 2014

Eurozone EY Eurozone Forecast March 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Belgium

Eurozone EY Eurozone Forecast March 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Belgium

Greece. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

EY Forecast June 215 rebalancing recovery Outlook for Delay in agreeing reform agenda has undermined the recovery Published in collaboration with Highlights The immediate economic outlook for continues

18. Real gross domestic product

18. Real gross domestic product 6 Percentage change from quarter to quarter 4 2-2 6 4 2-2 1997 1998 1999 2 21 22 Total Non-agricultural sectors Seasonally adjusted and annualised rates South Africa s real

18. Real gross domestic product 6 Percentage change from quarter to quarter 4 2-2 6 4 2-2 1997 1998 1999 2 21 22 Total Non-agricultural sectors Seasonally adjusted and annualised rates South Africa s real

The BEPS project is the beginning, but is the end in sight?

The BEPS project is the beginning, but is the end in sight? Panel Moderator Panel Michael Hewson Annet Oguttu Oliver Wehnert Ryaad Owodally Africa Transfer Pricing Leader EY Africa Professor of Tax Law

The BEPS project is the beginning, but is the end in sight? Panel Moderator Panel Michael Hewson Annet Oguttu Oliver Wehnert Ryaad Owodally Africa Transfer Pricing Leader EY Africa Professor of Tax Law

Investec Services PMI Ireland

Embargoed until: 06:00 (Dublin) June 6th 18 Investec Services PMI Ireland Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec in Ireland, a member of the Investec Group,

Embargoed until: 06:00 (Dublin) June 6th 18 Investec Services PMI Ireland Investec T: +3-1-421-0496 E: Investec.Economics@investec.ie W: www.investec.ie Investec in Ireland, a member of the Investec Group,

Eurozone. EY Eurozone Forecast December 2013

Eurozone EY Eurozone Forecast December 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Cyprus Severe

Eurozone EY Eurozone Forecast December 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Cyprus Severe

Staying the course. EY s attractiveness program Africa 2016

Staying the course EY s attractiveness program Africa 2016 Africa attractiveness program 2011 2012 2013 2014 2015 It s time for Africa Building bridges Getting down to business Executing growth Making

Staying the course EY s attractiveness program Africa 2016 Africa attractiveness program 2011 2012 2013 2014 2015 It s time for Africa Building bridges Getting down to business Executing growth Making

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2013

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Eurozone Ernst & Young Eurozone Forecast Spring edition March 2013 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain

Financial Services Act (FIDLEG)

") Financial Services Act (FIDLEG) Impact on the value chain and strategic implications September 2017 1 Financial Services Act (FIDLEG) Table of content Editorial... 03 FIDLEG At a glance... 04 Core processes

Financial Services Act (FIDLEG) Impact on the value chain and strategic implications September 2017 1 Financial Services Act (FIDLEG) Table of content Editorial... 03 FIDLEG At a glance... 04 Core processes

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Slovenia

Eurozone EY Eurozone Forecast September 214 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Slovenia

Record to report. Are you audit ready?

Record to report Are you audit ready? Panel Moderator Panel Cleedon Botha Anselme Patipewe Njiakin Stephen Ntsoane EY South Africa Director EY Cameroon Associate Director EY South Africa Director Sean

Record to report Are you audit ready? Panel Moderator Panel Cleedon Botha Anselme Patipewe Njiakin Stephen Ntsoane EY South Africa Director EY Cameroon Associate Director EY South Africa Director Sean

Global analysis of health insurance in The Gulf Region

Global analysis of health insurance in The Gulf Region The prospects for health care insurance in the GCC states The sharp sell-off in global oil prices that began in mid-214 triggered an economic slowdown

Global analysis of health insurance in The Gulf Region The prospects for health care insurance in the GCC states The sharp sell-off in global oil prices that began in mid-214 triggered an economic slowdown

European attractiveness survey 2016 Russia findings

European attractiveness survey 2016 Russia findings European context: Western Europe continues to be the most appealing FDI destination in Europe Despite a number of geopolitical risks, investors continue

European attractiveness survey 2016 Russia findings European context: Western Europe continues to be the most appealing FDI destination in Europe Despite a number of geopolitical risks, investors continue

EXPERIAN BUSINESS DEBT INDEX (BDI) RESULTS FOR Q2 2017

RESULTS FOR Q2 2017") EXPERIAN BUSINESS DEBT INDEX (BDI) RESULTS FOR Q2 2017 Business debt conditions still holding up despite recession The Experian Business Debt Index (BDI) rose moderately in the second quarter of 2017 compared

EXPERIAN BUSINESS DEBT INDEX (BDI) RESULTS FOR Q2 2017 Business debt conditions still holding up despite recession The Experian Business Debt Index (BDI) rose moderately in the second quarter of 2017 compared

IFRS 12. Disclosure of Interests in Other Entities

IFRS 12 Disclosure of Interests in Other Entities Agenda Background and objectives Main changes to disclosure requirements Summarised financial information Other disclosure requirements for subsidiaries,

IFRS 12 Disclosure of Interests in Other Entities Agenda Background and objectives Main changes to disclosure requirements Summarised financial information Other disclosure requirements for subsidiaries,

Joint Transition Resource Group for Revenue Recognition discusses more implementation issues

Applying IFRS Joint Transition Resource Group for Revenue Recognition discusses more implementation issues April 2015 Contents 1. Overview... 2 2. Issues that may require further evaluation by the Boards...

Applying IFRS Joint Transition Resource Group for Revenue Recognition discusses more implementation issues April 2015 Contents 1. Overview... 2 2. Issues that may require further evaluation by the Boards...

Driving integrated ÕfYf[aYd Yf\ kg[ayd j]lmjfk

![Driving integrated ÕfYf[aYd Yf\ kg[ayd j]lmjfk](/thumbs/85/92943938.jpg "Driving integrated ÕfYf[aYd Yf\ kg[ayd j]lmjfk") Driving integrated An integrated measurement approach The global business landscape is undergoing a perceptible shift. regulation (on one hand) and social and environmental impacts (on the other hand)

Driving integrated An integrated measurement approach The global business landscape is undergoing a perceptible shift. regulation (on one hand) and social and environmental impacts (on the other hand)

Business Expectations Survey September 2017 Summary Review

Business Expectations Survey September 2017 Summary Review 1. Introduction The BES summarises views of the business community regarding their perceptions about the current and future state of the economy.

Business Expectations Survey September 2017 Summary Review 1. Introduction The BES summarises views of the business community regarding their perceptions about the current and future state of the economy.

IFRS outlook. In this issue... Insights on International GAAP. SEC Roadmap

September 2008 Insights on International GAAP IFRS outlook In this issue... SEC Roadmap Feature 2 SEC roadmap Technical focus 4 Post-employment benefits views on proposed amendments Guidance on the fair

September 2008 Insights on International GAAP IFRS outlook In this issue... SEC Roadmap Feature 2 SEC roadmap Technical focus 4 Post-employment benefits views on proposed amendments Guidance on the fair

Fund Information. Fund Name. Fund Category. Fund Investment Objective. Fund Performance Benchmark. Fund Distribution Policy

Fund Information Fund Name (PBFI) Fund Category Bond Fund Investment Objective To provide a steady stream of annual income through its investment in private debt securities (bonds) and money market instruments.

Fund Information Fund Name (PBFI) Fund Category Bond Fund Investment Objective To provide a steady stream of annual income through its investment in private debt securities (bonds) and money market instruments.

STELLENBOSCH UNIVERSITY RETIREMENT FUND (USRF) OVERVIEW OF THE INVESTMENT FRAMEWORK OF USRF

OVERVIEW OF THE INVESTMENT FRAMEWORK OF USRF") 1 STELLENBOSCH UNIVERSITY RETIREMENT FUND (USRF) OVERVIEW OF THE INVESTMENT FRAMEWORK OF USRF November 2016 1. BRIEF SUMMARY... 2 2. INTRODUCTION... 3 3. INVESTMENT OBJECTIVES... 4 4. INVESTMENT STRATEGIES...

1 STELLENBOSCH UNIVERSITY RETIREMENT FUND (USRF) OVERVIEW OF THE INVESTMENT FRAMEWORK OF USRF November 2016 1. BRIEF SUMMARY... 2 2. INTRODUCTION... 3 3. INVESTMENT OBJECTIVES... 4 4. INVESTMENT STRATEGIES...

Financing the U.S. Trade Deficit

James K. Jackson Specialist in International Trade and Finance November 16, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov

James K. Jackson Specialist in International Trade and Finance November 16, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov

Second Quarter 2017 Report to Shareholders

Second Quarter 2017 Report to Shareholders BMO Financial Group Reports Net Income of $1.25 Billion for Second Quarter of 2017 Financial Results Highlights: Second Quarter 2017 Compared with Second Quarter

Second Quarter 2017 Report to Shareholders BMO Financial Group Reports Net Income of $1.25 Billion for Second Quarter of 2017 Financial Results Highlights: Second Quarter 2017 Compared with Second Quarter

SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 6-K REPORT OF FOREIGN ISSUER

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 OF THE SECURITIES EXCHANGE ACT OF 1934 Date: September 29, 2005 UBS AG (Registrant

SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 OF THE SECURITIES EXCHANGE ACT OF 1934 Date: September 29, 2005 UBS AG (Registrant

Reporting climate change risk

Reporting climate change risk A step-by-step guide to implementing the Financial Stability Board Task Force Recommendations for disclosing climate change risk Contents The Financial Stability Board Task

Reporting climate change risk A step-by-step guide to implementing the Financial Stability Board Task Force Recommendations for disclosing climate change risk Contents The Financial Stability Board Task

Svein Gjedrem: The outlook for the Norwegian economy

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

SOUTH AFRICAN BANKING SECTOR OVERVIEW

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

1 SOUTH AFRICAN BANKING SECTOR OVERVIEW TABLE OF CONTENTS Sections Page 1 Background 1 2. Total Assets 1 3. Total liabilities 3 4. Credit extension 4 5. Branches and ATMs 5 6. Usage of payment systems

A Decomposition of Equity Returns in South Africa: By Daniel R Wessels. May 2006

A Decomposition of Equity Returns in South Africa: By Daniel R Wessels May 2006 Available at: www.indexinvestor.co.za 1. Introduction Equity investments are perplexing and unpredictable. When you least

A Decomposition of Equity Returns in South Africa: By Daniel R Wessels May 2006 Available at: www.indexinvestor.co.za 1. Introduction Equity investments are perplexing and unpredictable. When you least

Industries Financial Services. Survey on Effective Management of South African Retirement Funds* March PwC. *connectedthinking

Industries Financial Services Survey on Effective Management of South African Retirement Funds* March 2007 PwC *connectedthinking PricewaterhouseCoopers has exercised reasonable professional care and diligence

Industries Financial Services Survey on Effective Management of South African Retirement Funds* March 2007 PwC *connectedthinking PricewaterhouseCoopers has exercised reasonable professional care and diligence

Capital Confidence Barometer

Financial Services Capital Confidence Barometer April 2014 ey.com/ccb Measured approach to growth M&A Focus on quality over quantity Economic outlook Moving beyond a recovery mindset, anticipating future

Financial Services Capital Confidence Barometer April 2014 ey.com/ccb Measured approach to growth M&A Focus on quality over quantity Economic outlook Moving beyond a recovery mindset, anticipating future

EYGS UK tax strategy. Financial year ending 30 June 2017

EYGS UK tax strategy Financial year ending 30 June 2017 EY s values and our commitment to building a better working world drive our tax strategy Scope This tax strategy applies to EYGS LLP and all its

EYGS UK tax strategy Financial year ending 30 June 2017 EY s values and our commitment to building a better working world drive our tax strategy Scope This tax strategy applies to EYGS LLP and all its

Are your climate disclosures revealing the true risks of your business?

Are your climate disclosures revealing the true risks of your business? Insights for the CFO on the release of Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures.

Are your climate disclosures revealing the true risks of your business? Insights for the CFO on the release of Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures.

Mergers, acquisitions and capital-raising in mining and metals trends, 2014 outlook: changing gear. The CFO perspective at a glance

Mergers, acquisitions and capital-raising in mining and metals 2013 trends, 2014 outlook: changing gear The CFO perspective at a glance The CFO perspective at a glance We want to help you get to the insight

Mergers, acquisitions and capital-raising in mining and metals 2013 trends, 2014 outlook: changing gear The CFO perspective at a glance The CFO perspective at a glance We want to help you get to the insight

Indonesia. Real Sector. The economy grew 3.7% in the first three quarters.

Indonesia Real Sector The economy grew 3.7% in the first three quarters. The economy grew in a 3.5-4% range in each of the first three quarters, in spite of adverse effects from the 22 Bali bombing, the

Indonesia Real Sector The economy grew 3.7% in the first three quarters. The economy grew in a 3.5-4% range in each of the first three quarters, in spite of adverse effects from the 22 Bali bombing, the

Banking Sector Dynamics

April 2015 Banking Sector Dynamics Issue 2 In this issue At a glance 1 Capital adequacy 2 Key banking sector indicators 3 Total assets 4 Total deposits and liabilities 6 Recent developments 8 Key events

April 2015 Banking Sector Dynamics Issue 2 In this issue At a glance 1 Capital adequacy 2 Key banking sector indicators 3 Total assets 4 Total deposits and liabilities 6 Recent developments 8 Key events

IFRS adopted by the European Union

IFRS adopted by the European Union IFRS standards and amendments issued by the IASB and endorsed by the as at 31 December 2016 January 2017 1. Published International Financial Reporting Standards The

IFRS adopted by the European Union IFRS standards and amendments issued by the IASB and endorsed by the as at 31 December 2016 January 2017 1. Published International Financial Reporting Standards The

IPO destination guide. Find the right market strategy to maximize value for your IPO or secondary listing

IPO destination guide Find the right market strategy to maximize value for your IPO or secondary listing IPO destination guide You've decided to go public and now you need to map out all the necessary

IPO destination guide Find the right market strategy to maximize value for your IPO or secondary listing IPO destination guide You've decided to go public and now you need to map out all the necessary

RESEARCH PAPER Benchmarking New Zealand s payment systems

RESEARCH PAPER Benchmarking New Zealand s payment systems May 2016 Payments NZ has relied on publically available information and information provided to it by third parties in the production of this report.

RESEARCH PAPER Benchmarking New Zealand s payment systems May 2016 Payments NZ has relied on publically available information and information provided to it by third parties in the production of this report.

EUROPEAN EXPORT INDEX Q4 2017

EUROPEAN EXPORT INDEX Q4 2017 BDO EXPORT INDEX KEY FIGURES The BDO Export Indices are composite indicators which provide snapshots of the export markets in Europe s five largest economies Germany, UK,

EUROPEAN EXPORT INDEX Q4 2017 BDO EXPORT INDEX KEY FIGURES The BDO Export Indices are composite indicators which provide snapshots of the export markets in Europe s five largest economies Germany, UK,

T T Mboweni: Recent developments in South Africa s financial markets

T T Mboweni: Recent developments in South Africa s financial markets Address by Mr T T Mboweni, Governor of the South African Reserve Bank, at the Beeld/Investec Guinness Flight Economist of the Year Banquet,

T T Mboweni: Recent developments in South Africa s financial markets Address by Mr T T Mboweni, Governor of the South African Reserve Bank, at the Beeld/Investec Guinness Flight Economist of the Year Banquet,

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 20 November 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 20 November 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 24 May 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank In recent weeks,

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 24 May 2018 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank In recent weeks,

What if SA is downgraded?

Home / What if SA is downgraded? What if SA is downgraded? By Sanlam Investments 1 September 2016 Previous Next Bookmark By Melville du Plessis Portfolio manager, Fixed Interest Six ways it could impact

Home / What if SA is downgraded? What if SA is downgraded? By Sanlam Investments 1 September 2016 Previous Next Bookmark By Melville du Plessis Portfolio manager, Fixed Interest Six ways it could impact

Budget Connect Pre-Budget Survey

Budget Connect 2017 Pre-Budget Survey The industry anticipates a delay in GST implementation: the Budget would not see any big ticket announcement in indirect taxes 2 Q1 Do you expect the postponement

Budget Connect 2017 Pre-Budget Survey The industry anticipates a delay in GST implementation: the Budget would not see any big ticket announcement in indirect taxes 2 Q1 Do you expect the postponement

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Germany

DECEMBER 2017/JANUARY 2018

MONEY MONEY AND AND BANKING BANKING STATISTICS STATISTICS DECEMBER 2017/JANUARY 2018 FEBRUARY 2017/MARCH 2017 HIGHLIGHTS ON MAJOR MONETARY AGGREGATES MONTHLY % CHANGE VARIABLE ANNUAL % MONTHLY CHANGE PERCENTAGE

MONEY MONEY AND AND BANKING BANKING STATISTICS STATISTICS DECEMBER 2017/JANUARY 2018 FEBRUARY 2017/MARCH 2017 HIGHLIGHTS ON MAJOR MONETARY AGGREGATES MONTHLY % CHANGE VARIABLE ANNUAL % MONTHLY CHANGE PERCENTAGE

Investor pre-close briefing. 16 March 2018

Investor pre-close briefing 16 March 2018 Proviso Please note that matters discussed in today s presentation may contain forward looking statements which are subject to various risks and uncertainties

Investor pre-close briefing 16 March 2018 Proviso Please note that matters discussed in today s presentation may contain forward looking statements which are subject to various risks and uncertainties

Macroeconomic and financial market developments. February 2014

Macroeconomic and financial market developments February 2014 Background material to the abridged minutes of the Monetary Council meeting 18 February 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013

Macroeconomic and financial market developments February 2014 Background material to the abridged minutes of the Monetary Council meeting 18 February 2014 Article 3 (1) of the MNB Act (Act CXXXIX of 2013

Morningstar Investment Services. Investing for You. Managed portfolios created to put your needs front and center where they belong.

Morningstar Investment Services Investing for You Managed portfolios created to put your needs front and center where they belong. Morningstar Investment Services Portfolios Designed To Put You First At

Morningstar Investment Services Investing for You Managed portfolios created to put your needs front and center where they belong. Morningstar Investment Services Portfolios Designed To Put You First At

1. Published International Financial Reporting Standards

1. Published International Financial Reporting Standards The table below provides an overview of the status of the European Union () endorsement process of IFRS standards and amendments issued by the International

1. Published International Financial Reporting Standards The table below provides an overview of the status of the European Union () endorsement process of IFRS standards and amendments issued by the International

Monitoring the Performance

Monitoring the Performance of the South African Labour Market An overview of the Sector from 2014 Quarter 1 to 2017 Quarter 1 Factsheet 19 November 2017 South Africa s Sector Government broadly defined

Monitoring the Performance of the South African Labour Market An overview of the Sector from 2014 Quarter 1 to 2017 Quarter 1 Factsheet 19 November 2017 South Africa s Sector Government broadly defined

abcdefg Introductory remarks by Jean-Pierre Roth News Conference

abcdefg News Conference Zurich, 14 December 2006 Introductory remarks by As stated in our press release, the Swiss National Bank is raising its target range for the three-month Libor with immediate effect

abcdefg News Conference Zurich, 14 December 2006 Introductory remarks by As stated in our press release, the Swiss National Bank is raising its target range for the three-month Libor with immediate effect

Ulster Bank Northern Ireland PMI

Embargoed until 0101 UK (0001 UTC) 10 September 2018 Ulster Bank Northern Ireland PMI New orders rise at weakest pace in four months Key Findings Weaker growth of output and new orders Further increase

Embargoed until 0101 UK (0001 UTC) 10 September 2018 Ulster Bank Northern Ireland PMI New orders rise at weakest pace in four months Key Findings Weaker growth of output and new orders Further increase

Making choices. EY s attractiveness survey Africa 2015

Making choices EY s attractiveness survey Africa 2015 Africa attractiveness surveys Background Fifth annual Africa attractiveness survey Analysis of greenfield and brownfield foreign direct investment

Making choices EY s attractiveness survey Africa 2015 Africa attractiveness surveys Background Fifth annual Africa attractiveness survey Analysis of greenfield and brownfield foreign direct investment

Monitoring the Performance of the South African Labour Market

Monitoring the Performance of the South African Labour Market An overview of the South African labour market for the Year Ending 2016 14 July 2016 Contents Recent labour market trends... 2 A labour market

Monitoring the Performance of the South African Labour Market An overview of the South African labour market for the Year Ending 2016 14 July 2016 Contents Recent labour market trends... 2 A labour market

UAE RESIDENTIAL MARKET REVIEW Q3 2017

RESEARCH MARKET REVIEW ABU DHABI AND DUBAI S RESIDENTIAL MARKET PERFORMANCE DIVERGES RESIDENTIAL RESEARCH MARKET REVIEW Key findings In Dubai s mainstream market sales prices fell by 2% in the year to

RESEARCH MARKET REVIEW ABU DHABI AND DUBAI S RESIDENTIAL MARKET PERFORMANCE DIVERGES RESIDENTIAL RESEARCH MARKET REVIEW Key findings In Dubai s mainstream market sales prices fell by 2% in the year to

Characteristics of the euro area business cycle in the 1990s

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

UK construction: margin pressure

UK construction: margin pressure Contents 3 5 Part 1 Strong headwind Part 2 Anticipating the storm 1 Research methodology EY analysed available accounts of the top 100 private and public UK construction

UK construction: margin pressure Contents 3 5 Part 1 Strong headwind Part 2 Anticipating the storm 1 Research methodology EY analysed available accounts of the top 100 private and public UK construction

Markit Global Business Outlook

News Release Markit Global Business Outlook EMBARGOED UNTIL: 00:01, 16 March 2015 Global business confidence and hiring intentions slip to post-crisis low Expectations regarding activity and employment

News Release Markit Global Business Outlook EMBARGOED UNTIL: 00:01, 16 March 2015 Global business confidence and hiring intentions slip to post-crisis low Expectations regarding activity and employment

Automotive transactions and trends 1H16

Automotive transactions and trends 1H16 Global automotive mergers and acquisitions review Produced by Global Markets EY Knowledge Contents Executive summary 01 Analysis by deal sizes Cross-border deals

Automotive transactions and trends 1H16 Global automotive mergers and acquisitions review Produced by Global Markets EY Knowledge Contents Executive summary 01 Analysis by deal sizes Cross-border deals

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Outlook for Economic Activity and Prices (April 2010)

") April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

April 30, 2010 Bank of Japan Outlook for Economic Activity and Prices (April 2010) The Bank's View 1 The global economy has emerged from the sharp deterioration triggered by the financial crisis and has

8 June Issue No. 12. New practice note explains how IRD will interpret the new law exempting PE funds from tax

Hong Kong Tax Alert 8 June 2016 2016 Issue No. 12 New practice note explains how IRD will interpret the new law exempting PE funds from tax Useful guidance provided, but certain issues e.g., the permitted

Hong Kong Tax Alert 8 June 2016 2016 Issue No. 12 New practice note explains how IRD will interpret the new law exempting PE funds from tax Useful guidance provided, but certain issues e.g., the permitted

Understanding ASPE. Section 3840, Related Party Transactions

Understanding ASPE Section 3840, Related Party Transactions Four questions for private business owners: Related Party Transactions A better working world begins with asking better questions. Better questions

Understanding ASPE Section 3840, Related Party Transactions Four questions for private business owners: Related Party Transactions A better working world begins with asking better questions. Better questions

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 2013

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 213 JULY 213 European Central Bank, 213 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

THE EURO AREA BANK LENDING SURVEY 2ND QUARTER OF 213 JULY 213 European Central Bank, 213 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

Budget 2012: The Minister tries really hard to get infrastructure going

Budget 2012: The Minister tries really hard to get infrastructure going Minister hits richer savers with tax increase. Agenda. Background to the Budget 2012. World South Africa. The Budget in a nutshell.

Budget 2012: The Minister tries really hard to get infrastructure going Minister hits richer savers with tax increase. Agenda. Background to the Budget 2012. World South Africa. The Budget in a nutshell.

The Weekly Focus. A Market and Economic Update 25 June 2018

The Weekly Focus A Market and Economic Update 25 June 2018 Contents Newsflash...3 Economic Update...3 Rates...7 STANLIB Money Market Fund... 7 STANLIB Enhanced Yield Fund... 7 STANLIB Income Fund... 7

The Weekly Focus A Market and Economic Update 25 June 2018 Contents Newsflash...3 Economic Update...3 Rates...7 STANLIB Money Market Fund... 7 STANLIB Enhanced Yield Fund... 7 STANLIB Income Fund... 7

MID-TERM REVIEW OF THE 2013 MONETARY POLICY STATEMENT

MID-TERM REVIEW OF THE MONETARY POLICY STATEMENT. INTRODUCTION. The Mid-Term Review (MTR) of the Monetary Policy Statement (MPS) evaluates progress in achieving the percent medium-term inflation objective.

MID-TERM REVIEW OF THE MONETARY POLICY STATEMENT. INTRODUCTION. The Mid-Term Review (MTR) of the Monetary Policy Statement (MPS) evaluates progress in achieving the percent medium-term inflation objective.

The quest for profitable growth

Global banking outlook 2015: transforming banking for the next generation The quest for profitable growth We estimate that if the average global bank grew revenues by 17% from FY13 levels, it would be

Global banking outlook 2015: transforming banking for the next generation The quest for profitable growth We estimate that if the average global bank grew revenues by 17% from FY13 levels, it would be

Investment. Insights. Emerging Markets. Invesco Global Equity. A 2012 outlook

Investment Insights Invesco Global Equity Emerging Markets A 2012 outlook Ingrid Baker Portfolio Manager Invesco Global Equity Many investors have watched from the sidelines as emerging market equities

Investment Insights Invesco Global Equity Emerging Markets A 2012 outlook Ingrid Baker Portfolio Manager Invesco Global Equity Many investors have watched from the sidelines as emerging market equities

Applying IFRS Goodwill Hunting

Applying IFRS Goodwill Hunting Looking for property investors missing cash flows February 2016 Contents 1. Introduction 2 2. An illustration 3 3. Goodwill acquired with investment property businesses 4

Applying IFRS Goodwill Hunting Looking for property investors missing cash flows February 2016 Contents 1. Introduction 2 2. An illustration 3 3. Goodwill acquired with investment property businesses 4