Integrating Risk & Finance using SAS

|

|

|

- Cody Washington

- 5 years ago

- Views:

Transcription

1 Integrating Risk & Finance using SAS Jiri Kubalek, senior consultant SAS Czech Republic

2 Why solutions integration...?

Controlling, Planning &")

Tax Optimization")

3 List of typical requirements within financial industry Legal Consolidation (convergence of IFRS and regulatory standards) Controlling, Planning & Budgeting (refinement of controlling and planning processes) Tax Optimization (optimal income tax & VAT repartition) Regulatory Reporting (mixed conglomerates - Basel2/Solvency) Risk Management (consistent framework for credit, market, operational and insurance risks) Performance Measurement

4 Financial Consolidation, Controlling & Regulatory Reporting Financial Management 4.2 Credit Risk Management for Banking 4.2 Provides real-time consolidations, flexible budgeting, planning and fully supports all controlling and internal audit processes Faciliate reporting according to GAAP/IFRS, Basel2/Solvency and supplementary supervision of banking/insurance groups and mixed financial holding companies in terms of Capital adequacy Risk concentration Intragroup transactions

5 Overlaps between IFRS and Basel II It s crucial to have one, and only one, centralised set of fully reconciled data from which all risk and financial disclosures emanate.

6 Solution architecture FM Studio Portal... Data entry... Administration... Reporting Solution Datamart (SDM) FM4 CRMS FM Detailed Data Store (DDS) Regulatory Capital Engine (CRMS) Data Structures Mapping tables Trial B/S, I/S, CF/S DB of entities Portfolio data

.")

7 Major IFRS & Regulatory enhancements Account Segment Currency Source Analysis Time Trader Organization Evidence Regulatory Business line Customer country Customer industry Maturity (Absolute, Remaining, etc.). Transferable regulatory capital Non-transferable regulatory capital Requirement (A,B,Op,Solvency) Regulatory capital limits. Balance at the beginning of fiscal period (+) Additions (-) Disposals (-) Amortization & impairment losses Balance at the end of fiscal period

8 Legal consolidation in FM Data Entry Part Data entry and Validation forms Consolidation Rules Reports Consolidiation and reporting part Composite Result Model Composite Result Model: Combination of different RM s for combined reporting Result Model 1 Conso Rules 1 Result Model 2 Conso Rules 2 Result Model 3 Conso Rules 3 Solution Data Mart Data Entry &Reporting Cycle Result Model: logical data container, defined by a subset of the dimensions in the cycle & owning an own set of consolidation rules Cycle: Physical data container defined by a selection of dimensions Central FM Data Base DDS

9 Controlling, Planning & Budgeting tasks 1) Controlling, Planning & Budgeting performed by SAS Financial Management (same cycle, separate Result Models) can be based on consolidation or different chart of accounts usually different level of aggregation, segmentation and evidence provides organization annual business and financial plan on a monthly or quarterly basis tactical (2 and 3 years) business and financial plan on an annual basis strategic plan with a longer time horizon 2) Tax Optimization data collection (in local GAAPs) plan and simulate tax position of the group (scenario analysis)

10 Regulatory reporting requirements 1) Process pre-calculated capital requirements ( Aggregation ) performed by SAS Financial Management aggregate results at conglomerate level set, distribute and review exposure limits plan and simulate RWA and capital and aggregate results produce reports required by the regulator and reports for management 2) Calculate RWA and capital requirement for individually unregulated companies ( RWA Calculation ) performed by SAS Credit Risk Management Solution (CRMS) report results (more detailed) export results into FMS (less detailed)

11 Regulatory Reporting (financial conglomerates) Insurance companies Investment companies Local banks Brokers Foreign banks Individualy non-regulated financial companies CRMS Engine configured for STD/IRB Method Summary data in FM IFRS & Solvency I. Reports Basel II (CP04) Reports

12 SAS Financial Management Example: Regulatory dimension details

13 Financial Consolidation & Risk Management Financial Management 4.2 Credit Risk Management 4.2 SAS Forecast Server 1.2 Model each risk in terms of (earnings or value) volatility and target debt rating Look at the capital consumption and define limits Portfolio optimization (Buy/Sell/Hedge decisions) Alignment of regulatory requirements with best practice risk management (Pillar II) Development of robust Economic Capital/Solvency Framework

14 Simple EC calculation framework Defaults Hist. DB Recovery Hist. DB Contracts Hist. DB Regulatory Capital UL i = f( PD, LGD, EAD ) Economic Capital ULP= ( UL * ρ ij * UL T ) Time Series Default Correlations

15 Trading Book Banking Book Basel II / CAD Defaults Hist. DB Ratingsystem LGD System Recovery Hist. DB Collateral Retail Pool Builder EAD (t) Probability of Defaults PD 1 Year Capital Requirement K = f (PD, LGD) Probability of Default Vectors PD=f(t) Riskmitigation Reporting System Regulatory Capital RC = RWA * 8% Expected Loss EL= f (PD(t), LGD) Default Time Series Sector/Country Correlations ρ i,j Unexpected Loss Transaction UL i =f (EL, ρ PD, ρ LGD ) Unexpected Loss Portfolio ULP, RC i Capital Planning Economic Capital Securitisation MIS System Shareholder Value Added Accounting

16 SAS Risk Dimensions

17 SAS Portal

18 SAS Portal

19 Integrating Risk Management into Decision Making More risky asset mix and if yes, equities, credit or should the company strive for more conservative investment policy and try to invest the capital for more growth? or New development in product design; Insurance savings & packaging of capital market commodities

20 Setting limits based on 4CAP approach REGULATORY CAPITAL AGENCY DRIVEN CAPITAL ECONOMIC CAPITAL ACTUAL CAPITAL Amount of capital required to protect the Group against statutory insolvency over a one-year time-frame Amount of capital the rating agencies expect in order to feel comfortable giving certain rating Amount of capital required to protect the Group against economic insolvency (over a one-year time-frame) Amount of equity capital or Embedded Value actually held to protect the Group against economic and statutoryinsolvency over a one-year time-frame Based on undifferentiated rules of thumb that do not reflect the real economic risks of the business and usually based on (relatively) public information Designed to protect policy holders and creditors Acts as a floor, which triggers takeover by the regulators Based on relatively undifferentiated rules of thumb (bank), and/or simple models (insurance) Not formulaic other factors such as quality of management and likelihood of Government bail-out are also considered Reflects real risks taken in the sense of unexpected movements in the value of assets and liabilities and on the confidence interval management wishes to tolerate Designed to be a tool for management Accounting result; expanded definition includes hidden reserves BARE MINIMUM CAPITAL YOU MUST HAVE CAPITAL YOU ARE EXPECTED TO HAVE CAPITAL YOU OUGHT TO HAVE CAPITAL YOU ACTUALLY HAVE

21 Setting limits based on 4CAP approach MM Available Financial Resources (Fair value) Required Capital (Economic Capital) Regulatory Capital (Statutory Reserves and Basel requirements) Actual capital Fair Value Economic Capital Amount of equity capital held to protect against economic and statutory insolvency Actual <- capital Regulatory capital --> Amount of capital required to protect the company against statutory insolvency. Acts as a floor, which triggers takeover by the regulators. - Based on rules of thumb that do not reflect real economic risk of the business.

22 Solution architecture FM Studio Portal... Data entry... Administration... Reporting Solution Datamart (SDM) FM4 CRMS + FS Business Intelligence &Analytical tools... FM Detailed Data Store (DDS) Regulatory Capital Engine (CRMS) Risk Dimensions Data Structures Mapping tables Trial B/S, I/S, CF/S DB of entities Portfolio data Risk factors Condor+ Reuters

23 Finance, Risk, Analytics and Performance Measurement Financial Management 4.2 Credit Risk Management 4.2 SAS Forecast Server 1.2 Strategic Performance Mgmt 2.2 Determining Risk-Return & RAPM profiles (lines of business) Risk-based pricing (products) Internal Transfer based pricing (banking-trading book)

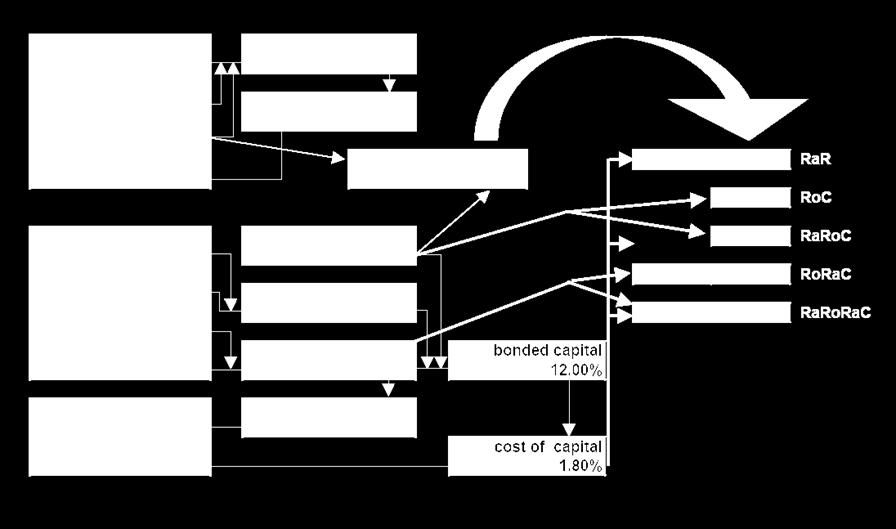

24 SPM: Linking financial, regulatory and risk perspective Accounting view RoA (Return on Assets) RoE (Return on Equity) RoC (Return on Capital) Regulatory view RoRE (Return on Required Equity) Economic view RaRoC (Risk Adjusted Return on Capital) RoRaC (Return on Risk Adjusted Capital) RaRoRaC (Risk Adjusted Return on Risk Adjusted Capital)

25 Risk Adjusted Performance Measures (RAPM)

26 SAS Strategic Performance

27 Solution architecture FM Studio Portal SPM Solution Datamart (SDM) FM4 + SPM CRMS + FS Business Intelligence &Analytical tools... FM Detailed Data Store (DDS) Regulatory Capital Engine (CRMS) Risk Dimensions Data Structures Mapping tables Trial B/S, I/S, CF/S DB of entities Portfolio data Risk factors Condor+ Reuters

28 Copyright 2004, 2003, SAS Institute Inc. All rights reserved. 28

2004 ELA Equipment Management Conference

2004 ELA Equipment Management Conference February 23, 2004 The Basel II Accord and Risk-Based Pricing Impact on Leasing and Asset Management C O N F I D E N T I A L Contents 1. Introduction 2. What Is

2004 ELA Equipment Management Conference February 23, 2004 The Basel II Accord and Risk-Based Pricing Impact on Leasing and Asset Management C O N F I D E N T I A L Contents 1. Introduction 2. What Is

Risk & Capital Management Under Basel III and IFRS 9 This course is presented in London on: May 2018

Risk & Capital Management Under Basel III and IFRS 9 This course is presented in London on: 14-17 May 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants Will: Understand

Risk & Capital Management Under Basel III and IFRS 9 This course is presented in London on: 14-17 May 2018 The Banking and Corporate Finance Training Specialist Course Objectives Participants Will: Understand

Risk & Capital Management Under Basel III and IFRS 9 This course can also be presented in-house for your company or via live on-line webinar

Risk & Capital Management Under Basel III and IFRS 9 This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course

Risk & Capital Management Under Basel III and IFRS 9 This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course

Index. Managing Risks in Commercial and Retail Banking By Amalendu Ghosh Copyright 2012 John Wiley & Sons Singapore Pte. Ltd.

Index A absence of control criteria, as cause of operational risk, 395 accountability, 493 495 additional exposure, incremental loss from, 115 advances and loans, ratio of core deposits to, 308 309 advances,

Index A absence of control criteria, as cause of operational risk, 395 accountability, 493 495 additional exposure, incremental loss from, 115 advances and loans, ratio of core deposits to, 308 309 advances,

IFRS 9. Challenges and solutions. May 2016

IFRS 9 Challenges and solutions May 2016 REGULATORY CONTEXT and objectives of the document Additional document on Impairment Nov 2009 Mar 2013 IFRS 9 Final Standard BIS Guidelines Guidance on accounting

IFRS 9 Challenges and solutions May 2016 REGULATORY CONTEXT and objectives of the document Additional document on Impairment Nov 2009 Mar 2013 IFRS 9 Final Standard BIS Guidelines Guidance on accounting

Implementing IFRS 9 Impairment Key Challenges and Observable Trends in Europe

Implementing IFRS 9 Impairment Key Challenges and Observable Trends in Europe Armando Capone 30 November 2016 Experian and the marks used herein are service marks or registered trademarks of Experian Limited.

Implementing IFRS 9 Impairment Key Challenges and Observable Trends in Europe Armando Capone 30 November 2016 Experian and the marks used herein are service marks or registered trademarks of Experian Limited.

INTRODUCTION. This document is not audited and should be read in conjunction with our Q Quarterly Report to Shareholders and 2017 Annual Report.

INTRODUCTION This document is not audited and should be read in conjunction with our Q3 2018 Quarterly Report to Shareholders and 2017 Annual Report. Effective November 1, 2012, Canadian banks are subject

INTRODUCTION This document is not audited and should be read in conjunction with our Q3 2018 Quarterly Report to Shareholders and 2017 Annual Report. Effective November 1, 2012, Canadian banks are subject

Risk Based Capital in Banking (Basel II) APRIA Conference

APRIA Conference") Risk Based Capital in Banking (Basel II) APRIA Conference Dirk McLiesh General Manager Group Risk, Westpac July 7 th, 2008 Contents What is Basel II? What Basel II means for risk based capital at Westpac

Risk Based Capital in Banking (Basel II) APRIA Conference Dirk McLiesh General Manager Group Risk, Westpac July 7 th, 2008 Contents What is Basel II? What Basel II means for risk based capital at Westpac

BCBS Discussion Paper: Regulatory treatment of accounting provisions

12 January 2017 EBF_024875 BCBS Discussion Paper: Regulatory treatment of accounting provisions Key points: The regulatory framework must ensure that the same potential losses are not covered both by capital

12 January 2017 EBF_024875 BCBS Discussion Paper: Regulatory treatment of accounting provisions Key points: The regulatory framework must ensure that the same potential losses are not covered both by capital

Capital Management in commercial and investment banking Back to the drawing board? Rolf van den Heever. ABSA Capital

Capital Management in commercial and investment banking Back to the drawing board? Rolf van den Heever ABSA Capital Contents Objectives Background Existing regulatory and internal dispensation to meet

Capital Management in commercial and investment banking Back to the drawing board? Rolf van den Heever ABSA Capital Contents Objectives Background Existing regulatory and internal dispensation to meet

UNAUDITED SUPPLEMENTARY FINANCIAL INFORMATION

1. Capital charge for credit, market and operational risks The bases of regulatory capital calculation for credit risk, market risk and operational risk are described in Note 4.5 to the Financial Statements

1. Capital charge for credit, market and operational risks The bases of regulatory capital calculation for credit risk, market risk and operational risk are described in Note 4.5 to the Financial Statements

COPYRIGHTED MATERIAL. Bank executives are in a difficult position. On the one hand their shareholders require an attractive

chapter 1 Bank executives are in a difficult position. On the one hand their shareholders require an attractive return on their investment. On the other hand, banking supervisors require these entities

chapter 1 Bank executives are in a difficult position. On the one hand their shareholders require an attractive return on their investment. On the other hand, banking supervisors require these entities

What will Basel II mean for community banks? This

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

Credit Risk. Lecture 5 Risk Modeling and Bank Steering. Loïc BRIN

Credit Risk Lecture 5 Risk Modeling and Bank Steering École Nationale des Ponts et Chaussées Département Ingénieurie Mathématique et Informatique (IMI) Master II Credit Risk - Lecture 5 1/20 1 Credit risk

Credit Risk Lecture 5 Risk Modeling and Bank Steering École Nationale des Ponts et Chaussées Département Ingénieurie Mathématique et Informatique (IMI) Master II Credit Risk - Lecture 5 1/20 1 Credit risk

Basel II to Basel III The Way forward

White Paper Basel II to Basel III The Way forward - Rohit VM, Sudarsan Kumar, Jitendra Kumar Abstract Basel III guidelines are the response of BCBS (Basel Committee on Banking Supervision) to the 2008

White Paper Basel II to Basel III The Way forward - Rohit VM, Sudarsan Kumar, Jitendra Kumar Abstract Basel III guidelines are the response of BCBS (Basel Committee on Banking Supervision) to the 2008

Basel II Pillar 3 disclosures

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

RISK REPORT PILLAR

A French corporation with share capital of EUR 1,009,897,137.75 Registered office: 29 boulevard Haussmann - 75009 PARIS 552 120 222 R.C.S. PARIS RISK REPORT PILLAR 3 30.09.2018 CONTENTS 1 CAPITAL MANAGEMENT

A French corporation with share capital of EUR 1,009,897,137.75 Registered office: 29 boulevard Haussmann - 75009 PARIS 552 120 222 R.C.S. PARIS RISK REPORT PILLAR 3 30.09.2018 CONTENTS 1 CAPITAL MANAGEMENT

Santander UK plc Additional Capital and Risk Management Disclosures

Santander UK plc Additional Capital and Risk Management Disclosures 1 Introduction Santander UK plc s Additional Capital and Risk Management Disclosures for the year ended should be read in conjunction

Santander UK plc Additional Capital and Risk Management Disclosures 1 Introduction Santander UK plc s Additional Capital and Risk Management Disclosures for the year ended should be read in conjunction

Superseded document. Basel Committee on Banking Supervision. Consultative Document. The New Basel Capital Accord. Issued for comment by 31 July 2003

Basel Committee on Banking Supervision Consultative Document The New Basel Capital Accord Issued for comment by 31 July 2003 April 2003 Table of Contents Part 1: Scope of Application... 1 A. Introduction...

Basel Committee on Banking Supervision Consultative Document The New Basel Capital Accord Issued for comment by 31 July 2003 April 2003 Table of Contents Part 1: Scope of Application... 1 A. Introduction...

Capital Buffer under Stress Scenarios in Multi-Period Setting

Capital Buffer under Stress Scenarios in Multi-Period Setting 0 Disclaimer The views and materials presented together with omissions and/or errors are solely attributable to the authors / presenters. These

Capital Buffer under Stress Scenarios in Multi-Period Setting 0 Disclaimer The views and materials presented together with omissions and/or errors are solely attributable to the authors / presenters. These

Basel II Pillar 3 disclosures 6M 09

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

Basel II Pillar 3 disclosures 6M 09 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse

Basel II Implementation Update

Basel II Implementation Update World Bank/IMF/Federal Reserve System Seminar for Senior Bank Supervisors from Emerging Economies 15-26 October 2007 Elizabeth Roberts Director, Financial Stability Institute

Basel II Implementation Update World Bank/IMF/Federal Reserve System Seminar for Senior Bank Supervisors from Emerging Economies 15-26 October 2007 Elizabeth Roberts Director, Financial Stability Institute

PILLAR 3 DISCLOSURES

. The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended December 31, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure

. The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended December 31, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Supplementary Regulatory Capital Disclosure and Pillar 3 Report

Supplementary Regulatory Capital Disclosure and Pillar 3 Report For the period ended October 31, 2018 For further information, please contact: Amy South, Senior Vice-President, Investor Relations (416)

Supplementary Regulatory Capital Disclosure and Pillar 3 Report For the period ended October 31, 2018 For further information, please contact: Amy South, Senior Vice-President, Investor Relations (416)

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

25 / 06 / 2008 APPLICATION OF THE BASEL II REFORM

25 / 06 / 2008 APPLICATION OF THE BASEL II REFORM Disclaimer The following presentation contains a number of forward-looking statements relating to Societe Generale s targets and strategy. These forecasts

25 / 06 / 2008 APPLICATION OF THE BASEL II REFORM Disclaimer The following presentation contains a number of forward-looking statements relating to Societe Generale s targets and strategy. These forecasts

Pillar 3 Disclosure (UK)

") MORGAN STANLEY INTERNATIONAL LIMITED Pillar 3 Disclosure (UK) As at 31 December 2009 1. Basel II accord 2 2. Background to PIllar 3 disclosures 2 3. application of the PIllar 3 framework 2 4. morgan stanley

MORGAN STANLEY INTERNATIONAL LIMITED Pillar 3 Disclosure (UK) As at 31 December 2009 1. Basel II accord 2 2. Background to PIllar 3 disclosures 2 3. application of the PIllar 3 framework 2 4. morgan stanley

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended December 31, 2015

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

African Bank Holdings Limited and African Bank Limited. Annual Public Pillar III Disclosures

African Bank Holdings Limited and African Bank Limited Annual Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 30 September 2016 1 African Bank Holdings Limited and African

African Bank Holdings Limited and African Bank Limited Annual Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 30 September 2016 1 African Bank Holdings Limited and African

The Internal Capital Adequacy Assessment Process ICAAP a New Challenge for the Romanian Banking System

The Internal Capital Adequacy Assessment Process ICAAP a New Challenge for the Romanian Banking System Arion Negrilã The Bucharest Academy of Economic Studies Abstract. In the near future, Romanian banks

The Internal Capital Adequacy Assessment Process ICAAP a New Challenge for the Romanian Banking System Arion Negrilã The Bucharest Academy of Economic Studies Abstract. In the near future, Romanian banks

GUIDELINES ON SIGNIFICANT RISK TRANSFER FOR SECURITISATION EBA/GL/2014/05. 7 July Guidelines

EBA/GL/2014/05 7 July 2014 Guidelines on Significant Credit Risk Transfer relating to Articles 243 and Article 244 of Regulation 575/2013 Contents 1. Executive Summary 3 Scope and content of the Guidelines

EBA/GL/2014/05 7 July 2014 Guidelines on Significant Credit Risk Transfer relating to Articles 243 and Article 244 of Regulation 575/2013 Contents 1. Executive Summary 3 Scope and content of the Guidelines

2 Modeling Credit Risk

2 Modeling Credit Risk In this chapter we present some simple approaches to measure credit risk. We start in Section 2.1 with a short overview of the standardized approach of the Basel framework for banking

2 Modeling Credit Risk In this chapter we present some simple approaches to measure credit risk. We start in Section 2.1 with a short overview of the standardized approach of the Basel framework for banking

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 9 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 9 3. Supplementary

2017 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at September 30, 2017

217 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at September 3, 217 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets

217 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at September 3, 217 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets

2017 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at June 30, 2017

217 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at June 3, 217 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets Exposure

217 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at June 3, 217 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets Exposure

2017 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at March 31, 2017

217 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at March 31, 217 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets Exposure

217 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at March 31, 217 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets Exposure

Frequently asked questions on the comprehensive quantitative impact study - EU specific annex

CEBS QIS FAQs 22 April 2010 Frequently asked questions on the comprehensive quantitative impact study - EU specific annex This document provides answers to technical and interpretive questions raised by

CEBS QIS FAQs 22 April 2010 Frequently asked questions on the comprehensive quantitative impact study - EU specific annex This document provides answers to technical and interpretive questions raised by

Pillar 3 Disclosure Report

Pillar 3 Disclosure Report 31 March 2018 United Overseas Bank Limited Incorporated in the Republic of Singapore Contents 1 INTRODUCTION... 3 2 KEY METRICS... 4 3 LEVERAGE RATIO... 5 4 OVERVIEW OF RWA...

Pillar 3 Disclosure Report 31 March 2018 United Overseas Bank Limited Incorporated in the Republic of Singapore Contents 1 INTRODUCTION... 3 2 KEY METRICS... 4 3 LEVERAGE RATIO... 5 4 OVERVIEW OF RWA...

OPTIMISTIC. Operational Review. Sub Contents. 148 Risk Management 234 Human Resources 244 Information Technology 249 Operations

Danamon s Highlights Reports Company Profile Discussion & Analysis OPTIMISTIC Operational Sub Contents 148 Risk 234 Human Resources 244 Information Technology 249 Operations 146 PT Bank Danamon Indonesia,

Danamon s Highlights Reports Company Profile Discussion & Analysis OPTIMISTIC Operational Sub Contents 148 Risk 234 Human Resources 244 Information Technology 249 Operations 146 PT Bank Danamon Indonesia,

ZAG BANK BASEL PILLAR 3 DISCLOSURES. December 31, 2015

ZAG BANK BASEL PILLAR 3 DISCLOSURES December 31, 2015 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of Desjardins Group (

ZAG BANK BASEL PILLAR 3 DISCLOSURES December 31, 2015 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of Desjardins Group (

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Goldman Sachs Group UK (GSGUK) Pillar 3 Disclosures

Pillar 3 Disclosures") Goldman Sachs Group UK (GSGUK) Pillar 3 Disclosures For the year ended December 31, 2013 TABLE OF CONTENTS Page No. Introduction... 3 Regulatory Capital... 6 Risk-Weighted Assets... 7 Credit Risk... 7

Goldman Sachs Group UK (GSGUK) Pillar 3 Disclosures For the year ended December 31, 2013 TABLE OF CONTENTS Page No. Introduction... 3 Regulatory Capital... 6 Risk-Weighted Assets... 7 Credit Risk... 7

Pillar 3 report. Table of Contents. Introduction 1. Scope of Application 2. Capital 3. Credit Risk Exposures 4. Credit Provision and Losses 6

Pillar 3 report Table of Contents Section 1 Introduction 1 Section 2 Scope of Application 2 Section 3 Capital 3 Section 4 Credit Risk Exposures 4 Section 5 Credit Provision and Losses 6 Section 6 Securitisation

Pillar 3 report Table of Contents Section 1 Introduction 1 Section 2 Scope of Application 2 Section 3 Capital 3 Section 4 Credit Risk Exposures 4 Section 5 Credit Provision and Losses 6 Section 6 Securitisation

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2017 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2017 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

ZAG BANK BASEL PILLAR 3 AND OTHER REGULATORY DISCLOSURES. December 31, 2017

ZAG BANK BASEL PILLAR 3 AND OTHER REGULATORY DISCLOSURES December 31, 2017 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of

ZAG BANK BASEL PILLAR 3 AND OTHER REGULATORY DISCLOSURES December 31, 2017 1. OVERVIEW OF ZAG BANK Zag Bank (the Bank ) is a Schedule I federally chartered Canadian bank and a wholly-owned subsidiary of

Supplementary Notes on the Financial Statements (continued)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2014 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2014 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

Estimating Economic Capital for Private Equity Portfolios

Estimating Economic Capital for Private Equity Portfolios Mark Johnston, Macquarie Group 22 September, 2008 Today s presentation What is private equity and how is it different to public equity and credit?

Estimating Economic Capital for Private Equity Portfolios Mark Johnston, Macquarie Group 22 September, 2008 Today s presentation What is private equity and how is it different to public equity and credit?

Boaz Galinson,VP -Credit Risk Modeling and Measurement, Leumi, Israel

Paper 1320- SGF14 Internal Credit Ratings Industry Norms and How to Get There with SAS Boaz Galinson,VP -Credit Risk Modeling and Measurement, Leumi, Israel My presentation addresses two main topics: The

Paper 1320- SGF14 Internal Credit Ratings Industry Norms and How to Get There with SAS Boaz Galinson,VP -Credit Risk Modeling and Measurement, Leumi, Israel My presentation addresses two main topics: The

12. Main change directions and types of risk of the mbank Group s activities

Retail Risk Department 12. Main change directions and types of risk of the mbank Group s activities 12.1. Main directions of change in the management of risk area The Group manages risks on the basis of

Retail Risk Department 12. Main change directions and types of risk of the mbank Group s activities 12.1. Main directions of change in the management of risk area The Group manages risks on the basis of

Pillar III Disclosures. Al Rajhi Bank

Pillar III Disclosures Al Rajhi Bank June 30, 2018 Summary Semi Annually Reports Section Part 2 Overview of risk management and RWA Part 4 Credit risk Part 5 Counterparty credit risk Part 6 Securitisation

Pillar III Disclosures Al Rajhi Bank June 30, 2018 Summary Semi Annually Reports Section Part 2 Overview of risk management and RWA Part 4 Credit risk Part 5 Counterparty credit risk Part 6 Securitisation

Pillar III Disclosures. Al Rajhi Bank

Pillar III Disclosures Al Rajhi Bank June 30, 201 Summary Semi Annually Reports Section Part 2 Overview of risk management and RWA Part 4 Credit risk Part 5 Counterparty credit risk Part 6 Securitisation

Pillar III Disclosures Al Rajhi Bank June 30, 201 Summary Semi Annually Reports Section Part 2 Overview of risk management and RWA Part 4 Credit risk Part 5 Counterparty credit risk Part 6 Securitisation

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended June 30, 2016

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2016 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy... 2

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended June 30, 2016 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy... 2

Disclosure Report as at 30 June. in accordance with the Capital Requirements Regulation (CRR)

") Disclosure Report as at 30 June 2018 in accordance with the Capital Requirements Regulation (CRR) Contents 3 Introduction 4 Equity capital, capital requirement and RWA 4 Capital structure 8 Connection

Disclosure Report as at 30 June 2018 in accordance with the Capital Requirements Regulation (CRR) Contents 3 Introduction 4 Equity capital, capital requirement and RWA 4 Capital structure 8 Connection

As of September 30, 2013 (Basel III) Risk weighted assets 58, ,790.1

Risk weighted assets 58, ,790.1") Exhibit 1 Corrections to Status of Capital Adequacy furnished on Form 6-K on January 30, 2014 Capital adequacy ratio highlights Page 2 Capital adequacy ratio highlights Mizuho Financial Group (Consolidated)

Exhibit 1 Corrections to Status of Capital Adequacy furnished on Form 6-K on January 30, 2014 Capital adequacy ratio highlights Page 2 Capital adequacy ratio highlights Mizuho Financial Group (Consolidated)

2015 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at September 30, 2015

215 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at September 3, 215 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets

215 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at September 3, 215 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets

Q4 18. Supplementary Regulatory Capital Information. For the Quarter Ended October 31, For further information, contact:

Supplementary Regulatory Capital Information For the Quarter Ended October 31, 2018 For further information, contact: JILL HOMENUK CHRISTINE VIAU Head, Investor Relations Director, Investor Relations 416.867.4770

Supplementary Regulatory Capital Information For the Quarter Ended October 31, 2018 For further information, contact: JILL HOMENUK CHRISTINE VIAU Head, Investor Relations Director, Investor Relations 416.867.4770

FSAP stress testing: Denmarks experience. Jakob W Lund (Danmarks Nationalbank) Presentation on 8 November 2007 to Bank of Canada Economic Conference

Presentation on 8 November 2007 to Bank of Canada Economic Conference") FSAP stress testing: Denmarks experience Jakob W Lund (Danmarks Nationalbank) Presentation on 8 November 2007 to Bank of Canada Economic Conference 16-09-2010 DANMARKS NATIONALBANK 2 FSAP Stress test experience

FSAP stress testing: Denmarks experience Jakob W Lund (Danmarks Nationalbank) Presentation on 8 November 2007 to Bank of Canada Economic Conference 16-09-2010 DANMARKS NATIONALBANK 2 FSAP Stress test experience

Market Risk Capital Disclosures Report. For the Quarterly Period Ended June 30, 2014

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarterly period ended June 30, 2014 Table of Contents Page Part I Overview 1 Morgan Stanley... 1 Part II Market Risk Capital Disclosures 1 Risk-based Capital

MARKET RISK CAPITAL DISCLOSURES REPORT For the quarterly period ended June 30, 2014 Table of Contents Page Part I Overview 1 Morgan Stanley... 1 Part II Market Risk Capital Disclosures 1 Risk-based Capital

Internal Rating Based (IRB) Approach Regulatory Expectations and Challenges. B. Mahapatra Reserve Bank of India July 11, 2013

Approach Regulatory Expectations and Challenges. B. Mahapatra Reserve Bank of India July 11, 2013") Internal Rating Based (IRB) Approach Regulatory Expectations and Challenges B. Mahapatra Reserve Bank of India July 11, 2013 Contents Introduction Concepts Variation in Credit RWAs Recent Study Regulatory

Internal Rating Based (IRB) Approach Regulatory Expectations and Challenges B. Mahapatra Reserve Bank of India July 11, 2013 Contents Introduction Concepts Variation in Credit RWAs Recent Study Regulatory

Loan Portfolio Management

Loan Portfolio Management Michael Wear 2016 1 2 ALLL Activity - Summary ($000) 2013 2014 2015 6/2016 Beginning 2,456 3,471 4,343 6,513 Balance Provisions 2,000 2,000 8,000 6,000 Net Charge-offs Ending

Loan Portfolio Management Michael Wear 2016 1 2 ALLL Activity - Summary ($000) 2013 2014 2015 6/2016 Beginning 2,456 3,471 4,343 6,513 Balance Provisions 2,000 2,000 8,000 6,000 Net Charge-offs Ending

Basel III Pillar 3. Capital Adequacy and Risks Disclosures as at 31 December 2016

Basel III Pillar 3 Capital Adequacy and Risks Disclosures as at 31 December 2016 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 15 FEBRUARY 2017 This page has been intentionally left blank Table of Contents

Basel III Pillar 3 Capital Adequacy and Risks Disclosures as at 31 December 2016 COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 15 FEBRUARY 2017 This page has been intentionally left blank Table of Contents

Basel Committee on Banking Supervision. Basel III counterparty credit risk - Frequently asked questions

Basel Committee on Banking Supervision Basel III counterparty credit risk - Frequently asked questions November 2011 Copies of publications are available from: Bank for International Settlements Communications

Basel Committee on Banking Supervision Basel III counterparty credit risk - Frequently asked questions November 2011 Copies of publications are available from: Bank for International Settlements Communications

AXA Bank Europe. Risk Disclosure Report 2012

AXA Bank Europe Disclosure Report 2012 Table of contents disclosure policy... 3 List of acronyms used in this report... 3 Executive summary... 4 1 Governance... 5 2 Appetite Framework... 7 3 Capital adequacy...

AXA Bank Europe Disclosure Report 2012 Table of contents disclosure policy... 3 List of acronyms used in this report... 3 Executive summary... 4 1 Governance... 5 2 Appetite Framework... 7 3 Capital adequacy...

Integrating Economic Capital, Regulatory Capital and Regulatory Stress Testing in Decision Making

Complimentary Webinar: Integrating Economic Capital, Regulatory Capital and Regulatory Stress Testing in Decision Making Amnon Levy, Managing Director, Head of Portfolio Research Co-Sponsored by: Originally

Complimentary Webinar: Integrating Economic Capital, Regulatory Capital and Regulatory Stress Testing in Decision Making Amnon Levy, Managing Director, Head of Portfolio Research Co-Sponsored by: Originally

Exhibit 1. Corrections to Status of Capital Adequacy furnished on Form 6-K on July 30, Capital adequacy ratio highlights

Exhibit 1 Corrections to Status of Capital Adequacy furnished on Form 6-K on July 30, 2013 Capital adequacy ratio highlights Page 2 Capital adequacy ratio highlights Mizuho Financial Group (Consolidated)

Exhibit 1 Corrections to Status of Capital Adequacy furnished on Form 6-K on July 30, 2013 Capital adequacy ratio highlights Page 2 Capital adequacy ratio highlights Mizuho Financial Group (Consolidated)

Risk Modeling and Bank Steering

Tutorial 5 Risk Modeling and Bank Steering École Nationale des Ponts et Chausées Département Ingénieurie Mathématique et Informatique Master II An Excel version of the correction is available here: http://defaultrisk.free.fr/pdf/td5.xlsx.

Tutorial 5 Risk Modeling and Bank Steering École Nationale des Ponts et Chausées Département Ingénieurie Mathématique et Informatique Master II An Excel version of the correction is available here: http://defaultrisk.free.fr/pdf/td5.xlsx.

Oracle Financial Services Pricing Management, Capital Charge Component. User Guide. Release 6.0. March 2012

Oracle Financial Services Pricing Management, Capital Charge Component User Guide Release March 2012 Contents LIST OF FIGURES... IV LIST OF TABLES... VI ABOUT THE GUIDE... 7 SCOPE OF THE GUIDE... 7 AUDIENCE...

Oracle Financial Services Pricing Management, Capital Charge Component User Guide Release March 2012 Contents LIST OF FIGURES... IV LIST OF TABLES... VI ABOUT THE GUIDE... 7 SCOPE OF THE GUIDE... 7 AUDIENCE...

Panel 3: Implementation issues model complexity and supervisory capacity

Panel 3: Implementation issues model complexity and supervisory capacity Banco de España CEMFI FSI High-Level Conference The new bank provisioning standards: Implementation challenges and financial stability

Panel 3: Implementation issues model complexity and supervisory capacity Banco de España CEMFI FSI High-Level Conference The new bank provisioning standards: Implementation challenges and financial stability

Supplementary Notes on the Financial Statements (continued)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2013 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2013 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

2016 PILLAR 3 REPORT. Incorporating the requirements of APS 330 Third Quarter Update as at 30 June 2016

PILLAR 3 REPORT Incorporating the requirements of APS 330 Third Quarter Update as at 30 June This page has been left blank intentionally third quarter pillar 3 report 1. Introduction third quarter pillar

PILLAR 3 REPORT Incorporating the requirements of APS 330 Third Quarter Update as at 30 June This page has been left blank intentionally third quarter pillar 3 report 1. Introduction third quarter pillar

Pillar 3 Disclosure Report

Pillar 3 Disclosure Report 30 September 2018 United Overseas Bank Limited Incorporated in the Republic of Singapore Contents 1 INTRODUCTION... 3 2 KEY METRICS... 4 3 LEVERAGE RATIO... 5 4 OVERVIEW OF RWA...

Pillar 3 Disclosure Report 30 September 2018 United Overseas Bank Limited Incorporated in the Republic of Singapore Contents 1 INTRODUCTION... 3 2 KEY METRICS... 4 3 LEVERAGE RATIO... 5 4 OVERVIEW OF RWA...

Effective Computation & Allocation of Enterprise Credit Capital for Large Retail and SME portfolios

Effective Computation & Allocation of Enterprise Credit Capital for Large Retail and SME portfolios RiskLab Madrid, December 1 st 2003 Dan Rosen Vice President, Strategy, Algorithmics Inc. drosen@algorithmics.com

Effective Computation & Allocation of Enterprise Credit Capital for Large Retail and SME portfolios RiskLab Madrid, December 1 st 2003 Dan Rosen Vice President, Strategy, Algorithmics Inc. drosen@algorithmics.com

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

Agenda on-site pre-application meeting INSTITUTION NAME Address (including city) DATE, start time / finish time

DATE, start time / finish time") Agenda on-site pre-application meeting INSTITUTION NAME Address (including city) DATE, start time / finish time The ECB would like to discuss with INSTITUTION NAME the pre-application process and the main

Agenda on-site pre-application meeting INSTITUTION NAME Address (including city) DATE, start time / finish time The ECB would like to discuss with INSTITUTION NAME the pre-application process and the main

Basel II Pillar 3 Disclosures Year ended 31 December 2009

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

Basel III - Pillar 3. Semiannual Disclosures

138943.4 Basel III - Pillar 3 Semiannual Disclosures As at 30th June 2017 Table of Contents Item Part 2 Overview of risk management and RWA Tables and templates* Template ref. # Page No. OV1 Overview of

138943.4 Basel III - Pillar 3 Semiannual Disclosures As at 30th June 2017 Table of Contents Item Part 2 Overview of risk management and RWA Tables and templates* Template ref. # Page No. OV1 Overview of

Supervisory Views on Bank Economic Capital Systems: What are Regulators Looking For?

Supervisory Views on Bank Economic Capital Systems: What are Regulators Looking For? Prepared By: David M Wright Group, Vice President Federal Reserve Bank of San Francisco July, 2007 Any views expressed

Supervisory Views on Bank Economic Capital Systems: What are Regulators Looking For? Prepared By: David M Wright Group, Vice President Federal Reserve Bank of San Francisco July, 2007 Any views expressed

Guideline. Capital Adequacy Requirements (CAR) Chapter 8 Operational Risk. Effective Date: November 2016 / January

Chapter 8 Operational Risk. Effective Date: November 2016 / January") Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 8 Effective Date: November 2016 / January 2017 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 8 Effective Date: November 2016 / January 2017 1 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank

Introduction. Regulatory environment in Legal Context

P. 15 Introduction Regulatory environment in 2017 Legal Context As a Spanish credit institution, BBVA is subject to Directive 2013/36/EU of the European Parliament and of the Council dated June 26, 2013,

P. 15 Introduction Regulatory environment in 2017 Legal Context As a Spanish credit institution, BBVA is subject to Directive 2013/36/EU of the European Parliament and of the Council dated June 26, 2013,

PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended June 30, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure 8

The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended June 30, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure 8

Basel Committee on Banking Supervision. Frequently asked questions on Basel III monitoring ad hoc exercise

Basel Committee on Banking Supervision Frequently asked questions on Basel III monitoring ad hoc exercise 31 May 2016 This publication is available on the BIS website (www.bis.org/bcbs/qis/). Grey underlined

Basel Committee on Banking Supervision Frequently asked questions on Basel III monitoring ad hoc exercise 31 May 2016 This publication is available on the BIS website (www.bis.org/bcbs/qis/). Grey underlined

For personal use only

2013 BASEL III PILLAR 3 DISCLOSURE YEAR ENDED 30 SEPTEMBER 2013 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet

2013 BASEL III PILLAR 3 DISCLOSURE YEAR ENDED 30 SEPTEMBER 2013 APS 330: PUBLIC DISCLOSURE Important notice This document has been prepared by Australia and New Zealand Banking Group Limited (ANZ) to meet

Basel III Pillar 3. Capital Adequacy and Risks Disclosures as at 31 December 2017

Basel III Pillar 3 Capital Adequacy and Risks Disclosures as at 31 December 2017 Commonwealth Bank of Australia ACN 123 123 124 7 February 2018 Images Mastercard is a registered trademark and the circles

Basel III Pillar 3 Capital Adequacy and Risks Disclosures as at 31 December 2017 Commonwealth Bank of Australia ACN 123 123 124 7 February 2018 Images Mastercard is a registered trademark and the circles

Counterparty Credit Risk under Basel III

Counterparty Credit Risk under Basel III Application on simple portfolios Mabelle SAYAH European Actuarial Journal Conference September 8 th, 2016 Recent crisis and Basel III After recent crisis, and the

Counterparty Credit Risk under Basel III Application on simple portfolios Mabelle SAYAH European Actuarial Journal Conference September 8 th, 2016 Recent crisis and Basel III After recent crisis, and the

Pillar 3 Disclosures. Quantitative Disclosures As at 31 December 2015

Pillar 3 Disclosures Quantitative Disclosures As at 31 December 2015 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 199901152M Content Page Introduction...

Pillar 3 Disclosures Quantitative Disclosures As at 31 December 2015 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 199901152M Content Page Introduction...

Beyond Basel II: Leveraging Economic Capital to Achieve Strategic Objectives

Enterprise Risk Management Symposium Beyond Basel II: Leveraging Economic Capital to Achieve Strategic Objectives March 2007 Ashish Dev adev@promontory.com Broader Concept of ERM with EC as the cornerstone

Enterprise Risk Management Symposium Beyond Basel II: Leveraging Economic Capital to Achieve Strategic Objectives March 2007 Ashish Dev adev@promontory.com Broader Concept of ERM with EC as the cornerstone

Solvency II. Building an internal model in the Solvency II context. Montreal September 2010

Solvency II Building an internal model in the Solvency II context Montreal September 2010 Agenda 1 Putting figures on insurance risks (Pillar I) 2 Embedding the internal model into Solvency II framework

Solvency II Building an internal model in the Solvency II context Montreal September 2010 Agenda 1 Putting figures on insurance risks (Pillar I) 2 Embedding the internal model into Solvency II framework

the DZ BANK Banking Regulatory Risk Report Risk of Report the DZ BANK Banking Group December 31, 2007

Member of the cooperative financial services network Regulatory Risk Report Risk of Report the DZ BANK Banking Group the DZ BANK Banking December 31, 2007 December 31, 2007 II Regulatory Risk Report of

Member of the cooperative financial services network Regulatory Risk Report Risk of Report the DZ BANK Banking Group the DZ BANK Banking December 31, 2007 December 31, 2007 II Regulatory Risk Report of

Basel II Pillar 3 disclosures

Basel II Pillar 3 disclosures 6M12 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Basel II Pillar 3 disclosures 6M12 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

2018 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at March 31, 2018

218 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at March 31, 218 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets Exposure

218 HSBC Bank Canada Regulatory Capital and Risk Management Pillar 3 Supplemental Disclosures as at March 31, 218 Index & Notes to Users Index Page Index Page Regulatory Capital Risk-Weighted Assets Exposure

Citigroup Global Markets Limited Pillar 3 Disclosures

Citigroup Global Markets Limited Pillar 3 Disclosures 30 September 2018 1 Table Of Contents 1. Overview... 3 2. Own Funds and Capital Adequacy... 5 3. Counterparty Credit Risk... 6 4. Market Risk... 7

Citigroup Global Markets Limited Pillar 3 Disclosures 30 September 2018 1 Table Of Contents 1. Overview... 3 2. Own Funds and Capital Adequacy... 5 3. Counterparty Credit Risk... 6 4. Market Risk... 7

Managing Capital Adequacy and Capital Utilization

Managing Capital Adequacy and Capital Utilization ERM Symposium Chicago, March 14, 2011 Bogie Ozdemir, Vice President Sun Life Financial Disclaimer and References Managing Capital Buffers in the Pillar

Managing Capital Adequacy and Capital Utilization ERM Symposium Chicago, March 14, 2011 Bogie Ozdemir, Vice President Sun Life Financial Disclaimer and References Managing Capital Buffers in the Pillar

Wells Fargo & Company. Basel III Pillar 3 Regulatory Capital Disclosures

Wells Fargo & Company Basel III Pillar 3 Regulatory Capital Disclosures For the quarter ended June 30, 2018 1 Table of Contents Disclosure Map.. 3 Introduction... 6 Executive Summary... 6 Company Overview

Wells Fargo & Company Basel III Pillar 3 Regulatory Capital Disclosures For the quarter ended June 30, 2018 1 Table of Contents Disclosure Map.. 3 Introduction... 6 Executive Summary... 6 Company Overview

Wells Fargo & Company. Basel III Pillar 3 Regulatory Capital Disclosures

Wells Fargo & Company Basel III Pillar 3 Regulatory Capital Disclosures For the quarter ended September 30, 2018 1 Table of Contents Disclosure Map.. 3 Introduction... 6 Executive Summary... 6 Company

Wells Fargo & Company Basel III Pillar 3 Regulatory Capital Disclosures For the quarter ended September 30, 2018 1 Table of Contents Disclosure Map.. 3 Introduction... 6 Executive Summary... 6 Company

BASEL II PILLAR 3 DISCLOSURE

2012 BASEL II PILLAR 3 DISCLOSURE HALF YEAR ENDED 31 MARCH 2012 APS 330: CAPITAL ADEQUACY & RISK MANAGEMENT IN ANZ Important notice This document has been prepared by Australia and New Zealand Banking

2012 BASEL II PILLAR 3 DISCLOSURE HALF YEAR ENDED 31 MARCH 2012 APS 330: CAPITAL ADEQUACY & RISK MANAGEMENT IN ANZ Important notice This document has been prepared by Australia and New Zealand Banking