Filing: Florida Department of Financial Services

|

|

|

- Ralph Charles

- 5 years ago

- Views:

Transcription

1 Filing: Florida Department of Financial Services

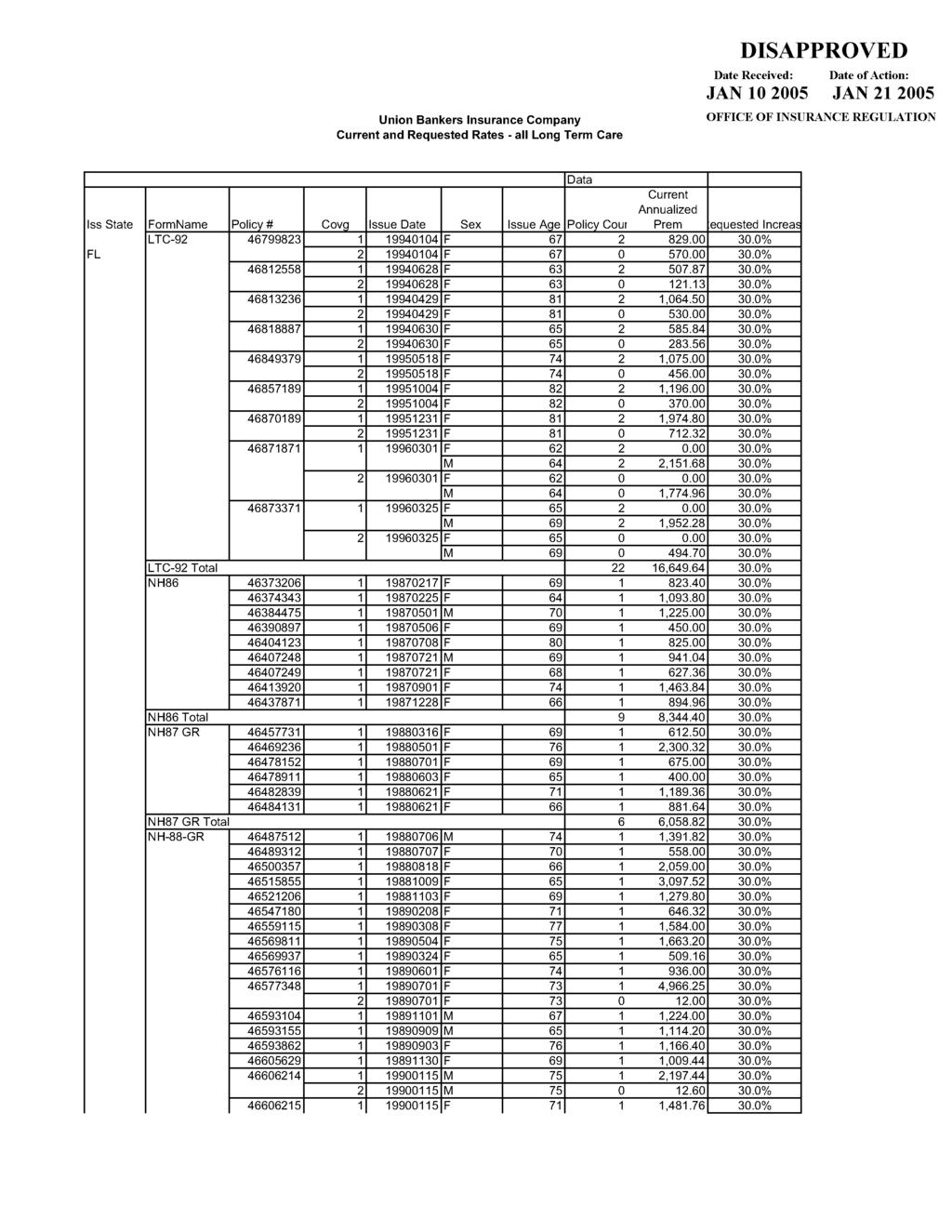

2 I. Scope and Purpose Union Bankers Insurance Company Actuarial Memorandum Individual Comprehensive Long-Term Care Business The purpose of this filing is to request a rate increase on our entire block of comprehensive longterm care business (the forms are listed below) and to demonstrate that, after the requested increase, the expected lifetime loss ratio meets the minimum requirements of your state. This filing is not intended to be used for other purposes. FL Form Title LTC-92 Long-Term Care Policy NH86 w/rider UB-NH86GR Nursing Home Policy w/policy Amendment Rider (the rider makes the policy guaranteed renewable) NH87 GR Nursing Home Policy NH-88-GR Long-Term Care Policy UB-8801 Home Convalescent Care Benefit Rider Non-FL Form Title H Nursing Home Policy (Integrity National Life Insurance Company form assumed by Union Bankers Insurance Company) H-716 Long-Term Care Policy (Integrity National Life Insurance Company form assumed by Union Bankers Insurance Company) LTC-CV Long-Term Care Policy II. Benefit Description These forms are individual policies providing daily benefits for nursing home care. Benefits for home care are included in forms NH86, NH87, and H and were optional in forms LTC- 92 and H-716. Forms LTC-CV and NH-88-GR were sold with optional rider UB-8801 (which provides home care benefits). III. Renewability Clause The forms are guaranteed renewable. IV. Applicability This rate increase will apply to existing policies only, as this is a closed block of business. V. Morbidity Pricing claim costs were based on the experience of Bankers Life and Casualty as well as the 1985 National Nursing Home Survey and Medicare Program Statistics of 1982 (published by HCFA). VI. Mortality The mortality table used in the projections is the 1983 Group Annuity Mortality Table. FL Page 1 of 6

3 VII. Persistency The projections assume a lapse rate of 6.7%, based on the difference between the actual total decrement rate from 12/31/02 to 12/31/03 and the mortality rate. VIII. Expenses LTC-92 Renewal Commission 10% (add 5% for issues ages 55-75) Fixed - $1.282/policy/month Overhead 2.62% of premium earned Premium and DAC Tax 3.40% of premium earned Claims Administration 4.33% of claims paid NH86 and NH87 GR Renewal Commission 15% Fixed - $1.25/individual/month Overhead 6.00% of premium earned Premium and DAC Tax 2.40% of premium earned Claims Administration 1.00% of claims paid UB-8801 Renewal Commission 15%, decreasing to 2% in the 11 th year Overhead 3.0% of premium earned Premium and DAC Tax 2.0% of premium earned Claims Administration 6.9% of claims paid IX. Marketing Method These policies were marketed through brokers. X. Underwriting These forms were medically underwritten. XI. Premium Classes Premiums vary by issue age, premium mode, benefit period/maximum, elimination period/deductible, and optional benefits selected. XII. Issue Age Range The issue age range was for LTC-92 and NH-88-GR. For NH86 and NH87 GR, it was All premiums are on an issue age basis. XIII. Area Factors The premiums do not differ by area within a state. FL Page 2 of 6

4 XIV. Average Annual Premium Nationwide Florida Policy Annualized Average Prem Average Prem Policy Annualized Average Prem Average Prem Form Count Premium Before Inc After Inc Count Premium Before Inc After Inc H N/A N/A H , , N/A N/A LTC , , , , , , LTC-CV 11 7, N/A N/A NH , , , , , NH87 GR , , , , , , NH-88-GR ,489, , , , , , UB-8801* 73 16, Total ,266, , , , , , *Riders not included in total policy count XV. Premium Modalization Rules The modal factors are as follows: Mode Schedule Annual Semi-Annual Quarterly Monthly Monthly PAC LTC-92 3-yr max, 90-day elim, level Schedule 31 other Schedule 32 NH86 1-yr max, all elims Schedule 25 3 or 5-yr max, 100-day elim Schedule 23 other Schedule 20 NH87 GR 5-yr max Schedule 20 other Schedule 25 NH-88-GR 3-yr max, 20-day elim, increasing Schedule 31 level, sold after 7/89 Schedule 21 level, sold prior to 8/89 Schedule 23 other Schedule 32 UB-8801 all - Schedule 32 XVI. Claim Liability and Reserves The claim liabilities were calculated using a continuance table provided by Milliman USA. The nationwide claim reserve as of 12/31/03 is $6,591,654. FL Page 3 of 6

5 XVII. Active Life Reserves The active life reserve is calculated using Southwestern Life Insurance Company s reserve factor file. XVIII. Trend Assumption Medical and Insurance A. Medical Trend Due to the indemnity nature of the benefits provided by these policies, we have assumed no medical trend. B. Insurance Trend The aging factor is based on the ultimate trend of the expected durational loss ratios. Shock lapses are estimated as half of the rate increase in excess of 15%. Antiselection is calculated as one minus the shock lapse. XIX. Minimum Loss Ratio The minimum required loss ratio is 60.0%. XX. Anticipated Loss Ratio Exhibit B shows the nationwide experience by duration and compares the actual to the expected experience. This shows that the actual experience for the years for which we have data ( ) is 227% of expected. Adding in the experience (modeled at 100% of expected see Section XXIII) brings the number to 139%. We are filing for an increase of 30.0%. Exhibit C takes the experience from Exhibit B and projects it 20 years at 5.00% interest, with and without the requested increase effective 8/1/2004 (the nationwide effective date). Since this increase will not bring the future loss ratio to the target loss ratio, we will continue to monitor the experience closely, but we are not projecting future rate increases at this time. The projected durational loss ratios (from the original filings) are as follows: Pol Yr LTC-92 NH86 NH87GR NHST XXI. Distribution of Business Please see Exhibit A for the distribution of business by premium class. XXII. Contingency & Risk Margins NH86 and NH87 GR 10% FL Page 4 of 6

6 XXIII. Experience Past & Future The experience of these forms has been combined due to the lack of credibility of the individual forms, and rider experience has been included with the experience of the base policy. Claims are shown on a restated basis. For example, the 2001 incurred claims consist of claims paid on any date for all claimants with a 2001 original incurred date, plus the estimated remaining claim liability for 2001 incurred claims as of 12/31/03. Due to the lack of availability of data, we have estimated the actual incurred claims prior to 2000 as 100% of expected claims. Expected claims are based on the originally filed durational loss ratios for forms LTC-92, NH86, and NH87 GR. For the remaining forms, we used the originally filed durational loss ratios for the most similar form from the previous list. Earned premiums prior to 1998 (except NH86, NH87 GR, and LTC- 92 which are based on information from previous rate filings) were modeled from the 1998 premiums, with the same mortality and lapse assumptions as the projections. Historical premiums adjusted to the current rate level are shown in Exhibit D. XXIV. Lifetime Loss Ratio The projection shows the following loss ratios: Earned Incurred Loss Premium Claims Ratio Historical 138,700,031 75,837, % Future without Increase 13,532,702 34,698, % Lifetime without Increase 152,232, ,536, % Future with Increase 15,537,229 31,947, % Lifetime with Increase 154,237, ,785, % XXV. History of Previous Rate Revisions The only previous rate revision in FL was a 15% decrease on LTC-92, approved 9/16/1993. XXVI. Number of Policyholders Please see section XIV for both nationwide and Florida policy counts. XXVII. Proposed Effective Date The proposed effective date is 3/1/2005 (8/1/2004 on a nationwide basis), following 45 days advance notice and Department approval. FL Page 5 of 6

7 XXVIII. Actuarial Certification To the best of my knowledge and judgment, this filing is in compliance with the applicable laws of the State of Florida and with the rules of the Department of Insurance, and complies with Actuarial Standard of Practice No. 8, Regulatory Filings for Rates and Financial Projections for Health Plans, as adopted by the Actuarial Standards Board, January, 1989, which standard is hereby adopted and incorporated by reference, and that the benefits provided are reasonable in relation to the proposed premiums. Garry R. Reed, ASA, MAAA Vice President and Actuary May 25, 2006 FL Page 6 of 6

8 1001 Heahtrow Park Lane Lake Mary, FL Mailing Address: PO Box 3509 Orlando, FL , x , x Fax January 10, 2005 Mr. Frank Dino Florida Department of Financial Service Office of Insurance Regulation 200 East Gaines Street Tallahassee, FL RE: Union Bankers Insurance Company NAIC #69701 Request for Rate Revision Long Term Care Form(s): LTC-92, et al Dear Mr. Dino: Enclosed for your review and approval is a rate revision request for the above referenced filing. Union Bankers is requesting a 30% increase. If you have any questions, please direct them to my attention at , ext. 8319, by e mail at cboyd@uafc.com or by fax at Sincerely, Carmen Boyd AVP, Actuarial Compliance Tempdoc.DOC Subsidiaries: American Exchange American Pioneer American Progressive Constitution Life Marquette National Peninsular Life Pennsylvania Life Penn Corp. Canada Union Bankers

9

10

11

12

13 Union Bankers Insurance Company Individual Comprehensive Long-Term Care Business Nationwide Distribution by Premium Class Exhibit A Issue Age All Forms Mode All Forms % Annual 45.7% % SemiAnnual 10.6% % Quarterly 10.9% % Monthly 32.8% % Total 100.0% % % Benefit % Period/Max FL Forms % 1 Year 5.2% % 2 Years 9.4% % 3 Years 31.7% % 5 Years 35.5% % Lifetime 18.1% % Total 100.0% % % Elimination/ % Deductible FL Forms % 0 Day 27.2% % 20 Day 32.6% % 30 Day 5.6% % 90 Day 13.6% % 100 Day 18.5% % 150 Day 2.6% % Total 100.0% % % % % % % % % % % % % % Total 100.0% FL

14 Union Bankers Insurance Company Individual Comprehensive Long-Term Care Business Projected Nationwide Experience Exhibit C NW Rate Increase: 30.0% NW Eff Date: 8/1/2004 Int Rate: 5.00% Projection Date: 12/31/03 WITHOUT INTEREST WITH 5% INTEREST ASSUMPTIONS Premium Factors Claim Factors Persistency Factors Interest Factors Cal Earned Incurred Loss Earned Incurred Loss Rate Effective- Rate Medical Mortality Shock Adverse Policy Claim Interest Year Premium Claims* Ratio Premium Claims* Ratio Increase ness Effect Aging Combined Trend Aging Combined & Lapses Lapses Selection Persistency Persistency Years Factor (B) (C) (D) (E) (F) (G) (H) (I) (J) (K) (L) (M) (N) (O) (P) (Q) (R) (S) (T) (U) (V) (W) (C)(-1)*(M)*(T) (D)(-1)*(P)*(U) (D)/(C) (C)*(W) (D)*(W) (G)/(F) (K)*(L) (N)*(O) 1-(R) 1-(Q)-(R) 1-(Q)-(R)*(S) Past ,464 33, % 541,272 79, % Experience ,665, , % 5,961, , % ,648,025 1,022, % 12,031,803 2,178, % ,105,780 1,286, % 12,387,566 2,610, % ,436,573 1,546, % 12,436,846 2,988, % ,409,494 1,785, % 11,794,783 3,284, % ,207,154 2,018, % 10,878,510 3,537, % ,861,973 2,234, % 9,784,338 3,729, % ,083,022 2,560, % 9,669,806 4,070, % ,250,905 2,920, % 9,463,503 4,421, % ,839,948 3,160, % 8,420,322 4,557, % ,499,780 3,491, % 7,552,239 4,794, % ,259,758 3,877, % 6,878,709 5,071, % ,566,766 3,859, % 5,688,013 4,807, % ,109,226 6,278, % 4,874,416 7,448, % ,463,569 6,979, % 3,912,885 7,885, % ,994,614 7,788, % 3,221,994 8,380, % ,124,341 4,901, % 3,201,497 5,022, % ,734,412 4,718, % 2,668,513 4,605, % 0.0% ,377,835 4,513, % 2,210,028 4,195, % 0.0% Projected ,053,759 4,288, % 1,817,926 3,796, % 0.0% Future ,761,192 4,045, % 1,484,719 3,410, % 0.0% Experience ,498,961 3,787, % 1,203,479 3,040, % 0.0% w/o Requested ,265,415 3,516, % 967,591 2,689, % 0.0% Increase ,058,869 3,237, % 771,102 2,357, % 0.0% ,506 2,950, % 608,597 2,046, % 0.0% ,151 2,660, % 475,019 1,757, % 0.0% ,140 2,368, % 366,209 1,490, % 0.0% ,903 2,080, % 278,532 1,246, % 0.0% ,735 1,800, % 208,684 1,027, % 0.0% ,916 1,532, % 153, , % 0.0% ,634 1,278, % 111, , % 0.0% ,261 1,043, % 78, , % 0.0% , , % 54, , % 0.0% , , % 36, , % 0.0% , , % 23, , % 0.0% , , % 14, , % 0.0% Past 86,756,617 56,181, % 138,700,031 75,837, % Future (w/o Rate Inc) 16,705,484 46,136, % 13,532,702 34,698, % Lifetime 103,462, ,317, % 152,232, ,536, % ,688,895 4,344, % 2,624,093 4,240, % 30.0% ,826,286 4,155, % 2,626,831 3,862, % 0.0% Projected ,441,090 3,948, % 2,160,780 3,495, % 0.0% Future ,093,346 3,724, % 1,764,731 3,139, % 0.0% Experience ,781,660 3,487, % 1,430,451 2,799, % 0.0% After 30% ,504,067 3,238, % 1,150,075 2,476, % 0.0% (Nationwide ,258,568 2,980, % 916,529 2,170, % 0.0% composite) ,043,000 2,717, % 723,377 1,884, % 0.0% Increase ,780 2,449, % 564,606 1,617, % 0.0% ,929 2,181, % 435,275 1,372, % 0.0% ,583 1,915, % 331,062 1,147, % 0.0% ,711 1,658, % 248, , % 0.0% ,273 1,410, % 182, , % 0.0% ,113 1,177, % 132, , % 0.0% , , % 93, , % 0.0% , , % 64, , % 0.0% , , % 43, , % 0.0% , , % 28, , % 0.0% , , % 17, , % 0.0% Past 86,756,617 56,181, % 138,700,031 75,837, % Future (After 30% Increase) 19,294,862 42,479, % 15,537,229 31,947, % Lifetime 106,051,479 98,660, % 154,237, ,785, % * Incurred claims do not include the policy reserve FL

15 Calendar Issue Year Year Earned Premium at Original Rate Level Claim by Incurral Year Actual Incurred Claims*,** Expected Incurred Claims Ratio of Actual to Expected Claims Union Bankers Insurance Company Individual Comprehensive Long-Term Care Business Nationwide Actual to Expected Claims Number on by Incurral Year Earned Premium at Original Rate Level Earned Actual Loss Expected Calendar Issue Earned IBNR+ICOS Actual Loss Expected Premium Ratio Loss Ratio Year Year Ratio Loss Ratio , , , , N/A N/A Total 230, , , , % N/A N/A , , , , , , ,702,343 1,702, , , , , ,668 67, , , , , , , , , , , , Total 2,665,227 2,665, , , % , , , , , , , ,728 32, , , ,375,331 2,375, , , , , , , , ,606,925 2,606, , , , , , ,929 1,342, , , , , , , , , , , , Total 5,648,025 5,648, ,022, ,022, % , ,819 1,114, ,279 1,230, , , , , , , , ,571,482 1,571, , , ,274 98, , , , ,337,736 2,337, , , Total 4,109,226 3,481,127 5,285, ,641 6,278, ,268, % ,739,270 1,739, , , , , , , N/A N/A Total 6,105,780 6,105, ,286, ,286, % N/A N/A , ,330 97, , , ,441,377 1,441, , , , , ,623 74, , , ,469,634 1,469, , , , , ,790 94, , , ,879,655 1,879, , , , , , , , , ,293,472 1,293, , , , , , , , , , , , , , , , , , Total 6,436,573 6,436, ,546, ,546, % , ,606 1,144, ,204 1,320, , , , ,942 98, , , , , , , , ,331 1,053, ,307 1,173, , ,351,747 1,351, , , , , , ,526 1,151, , ,345,588 1,345, , , ,163 71, ,764 60, , , ,627,195 1,627, , , Total 3,463,569 2,698,903 5,890,004 1,089,916 6,979, ,847, % ,048,624 1,048, , , , , , , N/A N/A Total 6,409,494 6,409, ,785, ,785, % N/A N/A , , ,858 87, , , , , , , , , ,341 55, , , , , , , , , , , , , ,232,045 1,232, , , ,751 90, , , , , ,229,579 1,229, , , ,917 99, ,441 72, , , ,434,975 1,434, , , , , ,882 67, , , , , , , , , , ,387 1,080, , , , , , , , , ,071 1,342, , Total 6,207,154 6,207, ,018, ,018, % , , , ,749 1,170, , , , , ,617 1,366, , , , , , ,697 69, , , , , , , , Total 2,994,614 2,211,905 5,780,130 2,008,682 7,788, ,593, % , , , , ,126,911 1,129, , , N/A N/A ,125,824 1,126, , , N/A N/A ,284,069 1,308, , , , ,445 32, ,652 70, , , , , , , ,800 74, ,789 62, , , , , , , , ,993 89, ,333 82, , , Total 5,861,973 5,934, ,234, ,270,601 98% , ,046 82,189 78,016 53, , , ,489 78, , , , , , , , , , , , ,639 72, , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,028,836 1,033, , , , , , , , , , ,030,403 1,031, , , ,457 40, ,679 99,019 31, , , ,146,483 1,196, , , Total 3,124,341 2,195,551 1,862,764 2,067, ,844 4,901, ,699, % , , , , , , , , Total 13,691,750 10,587,486 18,818,067 6,160, ,844 25,949, ,408, % Total 6,083,022 6,234, ,560, ,648,862 97% 0 Grand Total 86,756,617 82,215,612 48,619,071 6,591, ,844 56,181, ,438, % , , , ,788 0 ** Incurred Claims do not include the Active Life Reserve , , , , , ,984 92, , , , , , , , , , , , , , , , , , , ,048,770 1,094, , , , , , , , , , , Total 6,250,905 6,386,007 92,500 2,920, ,012,995 97% , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , Total 5,839,948 5,816, ,160, ,170, % N/A N/A , , , , , , , , , , , , , , , , , , , , , , , , , , , , , ,256 58, , , , , , , , , , , , , , , Total 5,499,780 5,216,154 58,375 3,491, ,321, % N/A N/A N/A N/A , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , , Total 5,259,758 4,460, ,785 3,877, ,241, % N/A N/A N/A N/A , , , , , ,504 16, , , , ,845 15, , , , , , , , ,753 62, , , , , , , , ,982 1, , , , , , , , ,640 73, , , , , , , , , , , Total 4,566,766 3,877, ,826 3,859, ,236, % 9 * Paid Claims by Incurral Year are not available prior to 2000 Paid Claims by Incurral Year Claim by Incurral Year Actual Incurred Claims** Expected Incurred Claims Exhibit B Ratio of Actual to Expected Claims Number on by Incurral Year FL

16 Union Bankers Insurance Company Exhibit D Individual Long-Term Care Policy Forms H ,H-716,LTC-92,LTC-CV,NH86,NH87 GR,NH-88-GR Nationwide Earned Premium Restated to Current Rate Level H H-716 Current Yr Cumulative Premium at Current Yr Cumulative Premium at Calendar Avg Avg Portion Premium 12/31/03 Calendar Avg Avg Portion Premium 12/31/03 Year Rate Inc Eff Date Remaining Trend Rate Level Year Rate Inc Eff Date Remaining Trend Rate Level % N/A 0.0% ,445 #### % N/A 0.0% ,030 #### % N/A 0.0% , % N/A 0.0% ,129 #### % N/A 0.0% , % N/A 0.0% ,178 #### % N/A 0.0% , % N/A 0.0% ,287 #### % N/A 0.0% , % N/A 0.0% ,451 #### % N/A 0.0% , % N/A 0.0% ,668 #### % N/A 0.0% , % N/A 0.0% ,933 #### % N/A 0.0% , % N/A 0.0% ,244 #### % N/A 0.0% , % N/A 0.0% ,599 #### % N/A 0.0% , % N/A 0.0% ,993 #### % N/A 0.0% , % N/A 0.0% ,426 #### % N/A 0.0% , % N/A 0.0% ,471 #### % N/A 0.0% , % N/A 0.0% ,359 #### % N/A 0.0% , % N/A 0.0% ,813 #### % N/A 0.0% , % N/A 0.0% ,699 #### % 01/10/ % , % N/A 0.0% #### % N/A 2.8% ,071 LTC-92 LTC-CV Current Yr Cumulative Premium at Current Yr Cumulative Premium at Calendar Avg Avg Portion Premium 12/31/03 Calendar Avg Avg Portion Premium 12/31/03 Year Rate Inc Eff Date Remaining Trend Rate Level Year Rate Inc Eff Date Remaining Trend Rate Level #### #### #### % N/A 0.0% ,024 #### % N/A 0.0% ,768 #### % N/A 0.0% , #### % N/A 0.0% , % 10/01/ % ,750 #### % N/A 0.0% , % N/A 0.0% ,530,924 #### % N/A 0.0% , % N/A 0.0% ,509,910 #### % N/A 0.0% , % N/A 0.0% ,518,567 #### % N/A 0.0% , % 08/19/ % ,362,514 #### % N/A 0.0% , % N/A 0.0% ,097,033 #### % N/A 0.0% , % N/A 0.0% ,762,453 #### % N/A 0.0% , % N/A 0.0% ,571,147 #### % N/A 0.0% , % 03/22/ % ,270 #### % N/A 0.0% , % 01/04/ % ,350 #### % N/A 0.0% , % N/A 1.2% ,322 #### % N/A 0.0% ,426 NH86 and NH87 GR NH-88-GR Current Yr Cumulative Premium at Current Yr Cumulative Premium at Calendar Avg Avg Portion Premium 12/31/03 Calendar Avg Avg Portion Premium 12/31/03 Year Rate Inc Eff Date Remaining Trend Rate Level Year Rate Inc Eff Date Remaining Trend Rate Level % N/A 0.0% ,265 #### % N/A 0.0% ,619,459 #### % N/A 0.0% ,851,903 #### % N/A 0.0% ,308, % N/A 0.0% ,088,543 #### % N/A 0.0% ,076, % N/A 0.0% ,613,580 #### % N/A 0.0% ,498, % N/A 0.0% ,784,196 #### % N/A 0.0% ,054, % N/A 0.0% ,249,045 #### % N/A 0.0% ,197, % N/A 0.0% ,849,210 #### % N/A 0.0% ,787, % N/A 0.0% ,466,984 #### % N/A 0.0% ,381, % N/A 0.0% ,206,485 #### % N/A 0.0% ,001, % 09/07/ % ,924,987 #### % N/A 0.0% ,644, % 09/13/ % ,618,648 #### % N/A 0.0% ,310, % N/A 0.0% ,511,169 #### % N/A 0.0% ,996, % N/A 0.0% ,435,480 #### % N/A 0.0% ,528, % N/A 0.0% ,267,522 #### % N/A 0.0% ,320, % 06/23/ % ,054,901 #### % 06/24/ % ,052, % 10/24/ % ,350 #### % 01/03/ % ,704, % N/A 0.0% ,440 #### % N/A 1.1% ,430,318 FL Page 4 of 7

17 Union Bankers Insurance Company Exhibit D Individual Long-Term Care Policy Forms H ,H-716,LTC-92,LTC-CV,NH86,NH87 GR,NH-88-GR Nationwide Earned Premium Restated to Current Rate Level All Forms Cumulative Premium at Calendar Premium 12/31/03 Year Trend Rate Level , ,624, ,266, ,355, ,368, ,108, ,708, ,186, ,613, ,931, ,282, ,468, ,765, ,871, ,283, ,136, ,384, ,128,127 FL Page 5 of 7

18 Union Bankers Insurance Company Individual Comprehensive Long-Term Care Business Projected Florida Experience Exhibit C-FL NW Rate Increase: 30.0% FL Eff Date: 2/1/2005 Int Rate: 5.00% Projection Date: 12/31/03 WITHOUT INTEREST WITH 5% INTEREST ASSUMPTIONS Premium Factors Claim Factors Persistency Factors Interest Factors Cal Earned Incurred Loss Earned Incurred Loss Rate Effective- Rate Medical Mortality Shock Adverse Policy Claim Interest Year Premium Claims* Ratio Premium Claims* Ratio Increase ness Effect Aging Combined Trend Aging Combined & Lapses Lapses Selection Persistency Persistency Years Factor (B) (C) (D) (E) (F) (G) (H) (I) (J) (K) (L) (M) (N) (O) (P) (Q) (R) (S) (T) (U) (V) (W) (C)(-1)*(M)*(T) (D)(-1)*(P)*(U) (D)/(C) (C)*(W) (D)*(W) (G)/(F) (K)*(L) (N)*(O) 1-(R) 1-(Q)-(R) 1-(Q)-(R)*(S) Past , % 8,760 1, % Experience ,809 21, % 321,669 47, % ,389 42, % 546,178 91, % ,182 51, % 515, , % ,262 56, % 452, , % ,747 64, % 431, , % ,550 73, % 397, , % ,834 82, % 437, , % ,320 87, % 375, , % ,299 91, % 319, , % ,093 98, % 279, , % , , % 242, , % , , % 208, , % , , % 179, , % ,366 89, % 153, , % , , % 121, , % ,127 64, % 85,135 69, % , , % 82, , % ,650 97, % 68,947 95, % 0.0% ,437 93, % 57,101 86, % 0.0% Projected ,063 88, % 46,970 78, % 0.0% Future ,504 83, % 38,361 70, % 0.0% Experience ,729 78, % 31,095 62, % 0.0% w/o Requested ,695 72, % 25,000 55, % 0.0% Increase ,358 66, % 19,923 48, % 0.0% ,672 60, % 15,724 42, % 0.0% ,581 54, % 12,273 36, % 0.0% ,041 48, % 9,462 30, % 0.0% ,012 42, % 7,196 25, % 0.0% ,450 37, % 5,392 21, % 0.0% ,310 31, % 3,972 17, % 0.0% ,546 26, % 2,870 13, % 0.0% ,115 21, % 2,028 10, % 0.0% ,979 17, % 1,398 8, % 0.0% ,099 13, % 938 5, % 0.0% ,436 10, % 611 4, % 0.0% , % 385 2, % 0.0% Past 3,133,501 1,393, % 5,158,964 2,022, % Future (w/o Rate Inc) 431, , % 349, , % Lifetime 3,565,124 2,346, % 5,508,611 2,739, % ,650 97, % 68,947 95, % 0.0% ,395 85, % 62,639 79, % 30.0% Projected ,033 81, % 55,795 72, % 0.0% Future ,054 76, % 45,568 64, % 0.0% Experience ,005 71, % 36,937 57, % 0.0% After 30% ,837 66, % 29,697 51, % 0.0% (Nationwide ,498 61, % 23,666 44, % 0.0% composite) ,932 56, % 18,679 38, % 0.0% Increase ,072 50, % 14,579 33, % 0.0% ,867 45, % 11,239 28, % 0.0% ,269 39, % 8,549 23, % 0.0% ,225 34, % 6,405 19, % 0.0% ,683 29, % 4,719 15, % 0.0% ,587 24, % 3,409 12, % 0.0% ,888 19, % 2,409 9, % 0.0% ,538 15, % 1,661 7, % 0.0% ,494 12, % 1,115 5, % 0.0% ,705 9, % 726 3, % 0.0% ,126 6, % 457 2, % 0.0% Past 3,133,501 1,393, % 5,158,964 2,022, % Future (After 30% Increase) 493, , % 397, , % Lifetime 3,627,359 2,278, % 5,556,158 2,689, % * Incurred claims do not include the policy reserve FL Not Credible

19 Calendar Issue Year Year Earned Premium at Original Rate Level Claim by Incurral Year Actual Incurred Claims*,** Expected Incurred Claims Ratio of Actual to Expected Claims Union Bankers Insurance Company Individual Comprehensive Long-Term Care Business Florida Actual to Expected Claims Number on by Incurral Year Earned Premium at Original Rate Level Earned Actual Loss Expected Calendar Issue Earned IBNR+ICOS Actual Loss Expected Premium Ratio Loss Ratio Year Year Ratio Loss Ratio ,730 3, N/A N/A Total 3,730 3, % N/A N/A ,356 6, , , ,809 21, , ,884 8, , N/A N/A ,886 9, , Total 143, , , , % ,739 4, , ,989 5, , , ,235 19, , ,614 14, , , ,154 23, , ,723 14, , N/A N/A ,970 24, , Total 256, , , , % ,709 24, , ,496 10, , ,860 68,860 10, , N/A N/A , ,471 19, , Total 129, ,407 89, , ,653 77% ,851 81,851 21, , N/A N/A N/A N/A Total 254, , , , % N/A N/A ,130 4, , ,419 37,419 5, , ,459 3, , ,462 63,462 12, , ,709 5, , ,800 79,800 21, , N/A N/A ,580 53,580 17, , ,142 6, , N/A N/A ,856 13, , Total 234, , , , % ,096 15, , ,583 23, , ,181 34,181 5, , ,547 18, , ,436 34,436 6, , ,670 7, , ,403 58,403 15, , N/A N/A ,191 67,191 21, , Total 107,192 99, ,099 20, , , % ,536 40,536 15, , N/A N/A N/A N/A Total 234, , , , % N/A N/A ,131 4, , ,870 12,870 1, , ,012 3, , ,405 31,405 6, , ,912 3, , ,639 31,639 8, , N/A N/A ,659 53,659 17, , ,293 6, , ,902 60,902 23, , ,392 9, , ,075 36,075 16, , ,073 12, , N/A N/A ,041 19, , Total 226, , , , % ,426 7, , ,847 6, , ,340 9,751 1, , N/A N/A ,803 11,803 2, , Total 79,127 72,312 64, , ,097 77% ,802 28,802 7, , ,016 29,016 9, , N/A N/A ,211 49,211 19, , N/A N/A ,499 55,499 25, , ,373 4, , ,586 32,586 17, , ,553 4, , N/A N/A ,131 6, , Total 261, , , , % N/A N/A ,294 6, , N/A N/A ,578 9, , ,548 10,057 2, , ,015 12, , ,803 10,803 2, , ,398 13, , ,360 26,360 8, , ,389 11, , ,557 26,557 10, , ,994 3, , ,040 45,040 20, , N/A N/A ,413 49,413 26, , Total 80,724 71,362 37,954 42,741 20, , , % ,884 27,884 17, , N/A N/A Total 396, , ,998 62,861 20, , , % Total 236, , , , % 0 Grand Total 3,133,501 2,841,348 1,310,269 62,861 20,532 1,393, ,362, % N/A N/A 0 ** Incurred Claims do not include the Active Life Reserve N/A N/A ,806 9,183 2, , ,865 9,865 3, , ,072 24,072 9, , ,251 24,251 10, , ,130 41,130 21, , ,251 43,251 26, , ,833 22,833 16, , N/A N/A Total 211, , , ,574 99% N/A N/A N/A N/A N/A N/A ,110 8,365 3, , ,986 8,986 3, , ,926 21,926 9, , ,089 22,089 11, , ,463 37,463 23, , ,073 39,481 28, , ,749 20,918 18, , N/A N/A Total 194, , , , % N/A N/A N/A N/A N/A N/A N/A N/A ,458 7,220 3, , ,161 8,161 3, , ,915 19,915 10, , ,063 20,063 12, , ,027 34,027 24, , ,397 34,107 30, , ,754 16,538 18, , N/A N/A Total 176, , , , % N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A ,847 5,945 3, , ,389 7,389 3, , ,030 18,030 11, , ,165 18,165 13, , ,807 30,807 25, , ,952 29,655 30, , ,884 13,253 18, , N/A N/A Total 159, , , , % N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A ,274 5,363 4, , ,666 6,666 4, , ,265 16,265 11, , ,386 16,386 13, , ,791 27,791 26, , ,727 26,752 30, , ,134 11,956 18, , N/A N/A Total 143, , , , % 0 * Paid Claims by Incurral Year are not available prior to 2000 Paid Claims by Incurral Year Claim by Incurral Year Actual Incurred Claims** Expected Incurred Claims Exhibit B-FL Ratio of Actual to Expected Claims Number on by Incurral Year FL Not Credible

20 Filing Details Work Unit Number: W Filing Purpose: Rates Only Line of Business: Non-Fraternal Accident and Health Products Date Created: 1/10/ :56:02 PM Filing Name: UBIC 2005 LTC FL Company Details Company Name FEIN NAIC CC NAIC GC UNION BANKERS INSURANCE COMPANY Filing Originator Information Company Contact Name: Ms. Carmen Boyd Contact Title: AVP, Actuarial Compliance Professional Designation: Contact Street Address: 1001 Heathrow Park Lane Suite/Room #: 5001 P.O. Box Mailing Address: Department: City: Lake Mary State: FL Zip Code: Country: Non US Postal Code: Phone Number: Ext 8319 Fax Number: Toll Free Number: Ext 8319 Non US Phone Number:

21 Company Contact Information Company Contact Name: Ms. Carmen Boyd Contact Title: AVP, Actuarial Compliance Professional Designation: Contact Street Address: 1001 Heathrow Park Lane Suite/Room #: 5001 P.O. Box Mailing Address: Department: City: Lake Mary State: FL Zip Code: Country: Non US Postal Code: Phone Number: Ext 8319 Fax Number: Toll Free Number: Ext 8319 Non US Phone Number: General Information A. Do you currently have in force business on this plan of insurance in Florida? Yes B. Are you selling new business on this plan of insurance in Florida? No If no, date discontinued: 1 / 1 / 1996 C. Are you currently selling this plan of insurance in other states? No D. What market restrictions (such as available to military persons only), do you have on this form? Life & Health Insurance A. Your policy or coverage is (Bold one) Health Life Variable Life Annuity Variable Annuity B. Your policy or coverage is (Bold one) Fraternal Individual Group D. Individual Policy Characteristics(Bold One)

22 1. Optional Renewable 2. Conditionally Renewable 3. Guaranteed Renewable 4. Non-Cancelable 5. Non-Renewable 6. Other(Specify) E. Is your policy or Coverage primarily for individuals over 65? YES F. Check the type(s) of benefit your policy or coverage provides:(bold One) 1. Disability Income 2. Major Medical 3. Long Term Care 4. Prepaid Limited Health Service Organization 5. Medicare Supplement 6. Small Employer Group Coverage (see section , F.S.) 7. Health Maintenance Organization 8. Other (specify)

23 Rate Filing History - Including Annual Rate Certifications (This section is for Florida experience only) (1) (2) (3) (4) (5) (6) (7) Rate Change Requested Total Annualized Premium Volume # of Certificates / Subscribers or Individual Policies Average Rate Change Maximum Rate Change Date Changed Approved or Acknowledged Florida Filing Number Current Filing 30 $ % 30 % % 1st Prior Filing 0 % $ % 0 % 2nd Prior Filing 0 % $ % 0 % Rate Request By Form (To be completed for all filings which include pooled blocks - Florida experience only) Primary Form Form Number Rate Change Requested Total Annualized Premium Volume # of Certificates or Policies LTC % $ Additional Form(s) NH86 30 % $ NH87 G 30 % $ NH88-G 30 % $ UB % $ Additional Data For New Form & Rate Filings (Provide current data for the form(s) submitted) Florida Only Nationwide A. Number of Certificates or Individual Policies Affected: B. If Group, Average Number of Certificates Per Policy/ Participating Unit (e.g. Employer Unit) 0 0 C. Annualized Premium Volume $ $ D. Average Annual Premium (current / proposed or new form) $ $ $ $ E. Anticipated Loss Ratio (Current / Proposed Premium) % % % % F. Lifetime Loss Ratio (Current / Proposed Premium) 49.7 % 48.4 % 72.6 % 69.9 % G. Loss Ratio Standard for The Form (or pooled group/forms) 60 % 60 % H. Total Past Incurred Loss Ratio Without Active Life Reserve Increases 39.2 % 54.7 % I. Current Year Loss Ratio for Policies 3 Years & Older (For Med. Supp.) Without Policy Reserves:

24 0 % 0 %

25 Uploaded Documents Document Type Filenet Number Form Number Title Actuarial Memorandum 0 Actuarial Memorandum Cover Letter 0 Cover Letter Manual/Rate Pages 0 Rate Pages Miscellaneous 0 Exhibits Rate Filing Certification gfedcb I certify that I and am authorized to make this Rate Filing on behalf of the company, further that the information contained in related transmittals and the filing is true, complete, correct, and in compliance with all applicable state laws. I certify that the proposed premiums are reasonable in relationship to the benefits provided. (Check one) nmlkj nmlkji I am an actuary I am not an actuary Name: Carmen Boyd Title: AVP, Actuarial Compliance

26 1001 Heathrow Park Lane Lake Mary, FL Fax Mailing Address: PO Box Lake Mary, FL January 20, 2005 Daniel J. Keating Bureau of Life & Health Forms & Rates Department of Financial Services Office of Insurance Regulation 200 East Gaines Street Tallahassee, FL Re: Union Bankers Insurance Company NAIC #69701 Long-Term Care Rate Increase Filing Forms: H , et al Your Filing Number Your of 1/18/05 to Carmen Boyd Dear Mr. Keating: I am writing in response to the above-referenced . Unfortunately, I have neither the total number of claims incurred in any year nor any open claim counts prior to 9/2001. The following are the number of open claims as of year end for each of the last 4 years: Nationwide Florida Please continue to direct any questions or requests for additional information to Carmen Boyd. She can be reached at , ext I look forward to the receipt of your formal approval. Sincerely, Eva L. W. Gaber, ASA, MAAA Assistant Actuary

27 Filing Details Work Unit Number: W Filing Purpose: Rates Only Line of Business: Non-Fraternal Accident and Health Products Date Created: 1/20/ :31:49 PM Filing Name: UBIC 2005 LTC FL Company Details Company Name FEIN NAIC CC NAIC GC UNION BANKERS INSURANCE COMPANY

28 Uploaded Documents Document Type Filenet Number Form Number Title Cover Letter 0 Cover Letter

29 KEVIN M. MCCARTY COMMISSIONER DEPARTMENT OF FINANCIAL SERVICES OFFICE OF INSURANCE REGULATION FINANCIAL SERVICES COMMISSION JEB BUSH GOVERNOR TOM GALLAGHER CHIEF FINANCIAL OFFICER CHARLIE CRIST ATTORNEY GENERAL CHARLES BRONSON COMMISSIONER OF AGRICULTURE via & telecopier: (407) January 21, 2005 Ms. Carmen Boyd AVP, Actuarial Compliance Union Bankers Insurance Company 1001 Heathrow Park Lane Suite 5001 Lake Mary, FL RE: UNION BANKERS INSURANCE COMPANY FORM NUMBER(S): LTC-92, ET AL FILE LOG NUMBER: FLR PLEASE REFER TO THIS FILE NUMBER WHEN CORRESPONDING Dear Ms. Boyd: The review of the above referenced filing is complete. This letter serves as notification that the filing is DISAPPROVED under Section , F.S., and for the following: 1 The company has not provided a count of incurred claims for each of the past five years, needed to determine the credibility of the experience data provided. 2 The company has not provided expected claim and expected loss ratio data for all forms included in the filing. 3 Experience and projected data was not provided in the format required by Rule 69O (3)(b)23 F.A.C. Consequently, the Office is unable to determine if the proposed rates are reasonable in relation to the benefits provided. The Office of Insurance Regulation s disapproval of this filing is a decision that affects the substantial interests of your company and, as such, your company may be entitled to a hearing to contest this decision. You have the right to contest this action pursuant to Section , F.S. An outline of your rights and procedures to follow is attached. Feel free to contact me if you have any questions. BUREAU OF LIFE & HEALTH FORMS & RATES 200 EAST GAINES STREET TALLAHASSEE, FLORIDA (850) FAX (850) Affirmative Action / Equal Opportunity Employer

30 Sincerely, Daniel J. Keating, FSA, MAAA Actuary (850) Enclosures

31 NOTICE OF RIGHTS Pursuant to Sections and , Florida Statutes and Rule Chapters and , Florida Administrative Code (F.A.C.), you have a right to request a proceeding to contest this action by the Office of Insurance Regulation (hereinafter the Office ). You may request a proceeding by filing a Petition. Your Petition for a proceeding must be in writing and must be filed with the General Counsel acting as the Agency Clerk, Office of Insurance Regulation. If served by U.S. Mail the Petition should be addressed to the Florida Office of Insurance Regulation at 612 Larson Building, Tallahassee, Florida If Express Mail or hand-delivery is utilized, the Petition should be delivered to 612 Larson Building, 200 East Gaines Street, Tallahassee, Florida The written Petition must be received by, and filed in the Office no later than 5:00 p.m. on the twenty-first (21) day after your receipt of this notice. Unless your Petition challenging this action is received by the Office within twenty-one (21) days from the date of the receipt of this notice, the right to a proceeding shall be deemed waived. Mailing the response on the twenty-first day will not preserve your right to a hearing. If a proceeding is requested and there is no dispute of material fact the provisions of Section (2), Florida Statutes would apply. In this regard you may submit oral or written evidence in opposition to the action taken by this agency or a written statement challenging the grounds upon which the agency has relied. While a hearing is normally not required in the absence of a dispute of fact, if you feel that a hearing is necessary one will be conducted in Tallahassee, Florida or by telephonic conference call upon your request. If you dispute material facts which are the basis for this agency's action you may request a formal adversarial proceeding pursuant to Sections and (1), Florida Statutes. If you request this type of proceeding, the request must comply with all of the requirements of Rule Chapter , F.A.C., must demonstrate that your substantial interests have been affected by this agency s action, and contain: a) A statement of all disputed issues of material fact. If there are none, the petition must so indicate; b) A concise statement of the ultimate facts alleged, including the specific facts the petitioner contends warrant reversal or modification of the agency s proposed action; c) A statement of the specific rules or statutes the petitioner contends require reversal or modification of the agency s proposed action; and d) A statement of the relief sought by the petitioner, stating precisely the action petitioner wishes the agency to take with respect to the agency s proposed action. These proceedings are held before a State Administrative Law Judge of the Division of Administrative Hearings. Unless the majority of witnesses are located elsewhere, the Office will request that the hearing be conducted in Tallahassee. In some instances you may have additional statutory rights than the ones described herein. Failure to follow the procedure outlined with regard to your response to this notice may result in the request being denied. Any request for an administrative proceeding received prior to the date of this notice shall be deemed abandoned unless timely renewed in compliance with the guidelines as set out above.

32 To: Sent: 1/18/2005 4:52:18 PM From: Cc: Bcc: Subject: Florida Office of Insurance Regulation [RE: Filing Number ] Attachment(s): Please provide the number of incurred claims for each of the last 5 calendar years, for both Florida and Nationwide business. Please provide this information by close of business Thursday, January 20, 2005 Sincerely, Daniel J. Keating, FSA, MAAA Actuary (850)

33 To: Sent: 1/21/2005 1:43:32 PM From: Cc: Bcc: Subject: Florida Office of Insurance Regulation [RE: Filing Number ] Attachment(s): FLR-Dis-Union-Bankers-Ins-Co.rtf Click the link below to view the documents for this filing: Please see the attached letter. A signed copy of the letter will be faxed and mailed. Electronic copies of the stamped documents may be viewed using the link provided. If you have any questions, please do not hesitate to contact me. Sincerely, Daniel J. Keating, FSA, MAAA Actuary (850)

34

35

36

STATE FARM MUTUAL AUTOMOBILE INSURANCE COMPANY BLOOMINGTON, ILLINOIS ACTUARIAL MEMORANDUM RATE INCREASE

STATE FARM MUTUAL AUTOMOBILE INSURANCE COMPANY BLOOMINGTON, ILLINOIS 61710 ACTUARIAL MEMORANDUM RATE INCREASE STATE FARM TAX QUALIFIED LONG TERM CARE INSURANCE POLICY FORM 97059MD SIMPLE AUTOMATIC INCREASE

STATE FARM MUTUAL AUTOMOBILE INSURANCE COMPANY BLOOMINGTON, ILLINOIS 61710 ACTUARIAL MEMORANDUM RATE INCREASE STATE FARM TAX QUALIFIED LONG TERM CARE INSURANCE POLICY FORM 97059MD SIMPLE AUTOMATIC INCREASE

MEDAMERICA INSURANCE COMPANY. Address: 165 Court Street, Rochester, New York Simplicity ii Actuarial Memorandum.

Simplicity ii Product Tax Qualified Long Term Care Policy Form Number SPL2 336 MD This policy form was issued in Maryland by (MedAmerica) from June 2008 through April 2014 and is no longer being marketed

Simplicity ii Product Tax Qualified Long Term Care Policy Form Number SPL2 336 MD This policy form was issued in Maryland by (MedAmerica) from June 2008 through April 2014 and is no longer being marketed

Lifetime Loss Ratio ( LLR ) Without/with proposed rate increase of 32.25% (actuarially equivalent to two 15% increases) Nationwide experience

Without/with proposed rate increase of 32.25% (actuarially equivalent to two 15% increases) Nationwide experience") June 13, 2018 Re: LTC-FAC, LTC-VAL, LTC-IDEAL and LTC-PREM Issued by Metropolitan Life Insurance Company (MetLife) Attached is the filing for the captioned forms. This letter provides an overview of the

June 13, 2018 Re: LTC-FAC, LTC-VAL, LTC-IDEAL and LTC-PREM Issued by Metropolitan Life Insurance Company (MetLife) Attached is the filing for the captioned forms. This letter provides an overview of the

Lifetime Loss Ratio ( LLR ) Without/with proposed rate increase of 32.25% (actuarially equivalent to two 15% increases) Nationwide experience

Without/with proposed rate increase of 32.25% (actuarially equivalent to two 15% increases) Nationwide experience") June 12, 2018 Re: 1LTC-97-MD-1, 1LTC-97-MD-2, 2LTC-97-MD-1, 2LTC-97-MD-2 Issued by Metropolitan Life Insurance Company (MetLife) Attached is the filing for the captioned forms. This letter provides an

June 12, 2018 Re: 1LTC-97-MD-1, 1LTC-97-MD-2, 2LTC-97-MD-1, 2LTC-97-MD-2 Issued by Metropolitan Life Insurance Company (MetLife) Attached is the filing for the captioned forms. This letter provides an

MEDAMERICA INSURANCE COMPANY Address: 165 Court Street, Rochester, New York Series 11 and Prior Actuarial Memorandum.

MEDAMERICA INSURANCE COMPANY Address: 165 Court Street, Rochester, New York 14647 Series 11 and Prior Actuarial Memorandum August 27, 2018 Product Prior to Series 11 Facility Only Form Comprehensive Form

MEDAMERICA INSURANCE COMPANY Address: 165 Court Street, Rochester, New York 14647 Series 11 and Prior Actuarial Memorandum August 27, 2018 Product Prior to Series 11 Facility Only Form Comprehensive Form

Lincoln National Life Insurance Company

Page 1 of 10 1. PURPOSE AND SCOPE OF FILING This is a rate increase filing for Lincoln National Life Insurance existing Long Term Care policy forms. The purpose of this filing is to demonstrate that the

Page 1 of 10 1. PURPOSE AND SCOPE OF FILING This is a rate increase filing for Lincoln National Life Insurance existing Long Term Care policy forms. The purpose of this filing is to demonstrate that the

CURRICULUM MAPPING FORM

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

TOI: LTC03I Individual Long Term Care Sub-TOI: LTC03I.001 Qualified

SERFF Tracking Number: MULF-126856968 State: Oregon Filing Company: John Hancock Life Insurance Company (USA) State Tracking Number: HL 0047 08, HL 0086 09, HL 0647 01, HL 0169 03, Company Tracking Number:

SERFF Tracking Number: MULF-126856968 State: Oregon Filing Company: John Hancock Life Insurance Company (USA) State Tracking Number: HL 0047 08, HL 0086 09, HL 0647 01, HL 0169 03, Company Tracking Number:

Investment Symposium March I7: Impact of Economic Crisis on OTC Derivatives Markets for Insurers. Moderator Frank Zhang

Investment Symposium March 2010 I7: Impact of Economic Crisis on OTC Derivatives Markets for Insurers Naveed Choudri Sean Huang John Wiesner Moderator Frank Zhang UFS Economic Crisis Impact on Derivative

Investment Symposium March 2010 I7: Impact of Economic Crisis on OTC Derivatives Markets for Insurers Naveed Choudri Sean Huang John Wiesner Moderator Frank Zhang UFS Economic Crisis Impact on Derivative

MEDAMERICA INSURANCE COMPANY. Address: 165 Court Street, Rochester, New York Series 11 Group Actuarial Memorandum.

MEDAMERICA INSURANCE COMPANY Address: 165 Court Street, Rochester, New York 14647 Series 11 Group Actuarial Memorandum April 27, 2017 Product Comprehensive Form Comprehensive Certificate Number GRP11-341-MA-MD-601

MEDAMERICA INSURANCE COMPANY Address: 165 Court Street, Rochester, New York 14647 Series 11 Group Actuarial Memorandum April 27, 2017 Product Comprehensive Form Comprehensive Certificate Number GRP11-341-MA-MD-601

Overhead 2018 EA-2F Seminar outline Page # Revised July 25, 2018

01 13 CM-01 CM- CM- CM-16 CM-17 CM-24 CM-25 CM-31 CM-32 CM-33 CM-34 CM-35 CM-36 CM-38 I. INTRODUCTION A. General information B. Summary of past exams C. Summary of Overhead sections II. COST METHODS A.

01 13 CM-01 CM- CM- CM-16 CM-17 CM-24 CM-25 CM-31 CM-32 CM-33 CM-34 CM-35 CM-36 CM-38 I. INTRODUCTION A. General information B. Summary of past exams C. Summary of Overhead sections II. COST METHODS A.

CUSTOMERS. PEOPLE. PARTNERS.

THIRD-QUARTER 2017 FINANCIAL REVIEW October 24, 2017 CUSTOMERS. PEOPLE. PARTNERS. FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events

THIRD-QUARTER 2017 FINANCIAL REVIEW October 24, 2017 CUSTOMERS. PEOPLE. PARTNERS. FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events

Group long-term policy G.LTC1697 (including GCLTCAARP-04-OP in Maryland) Issued by Metropolitan Life Insurance Company (MetLife)

Issued by Metropolitan Life Insurance Company (MetLife)") April 16, 2018 Re: Group long-term policy G.LTC1697 (including GCLTCAARP-04-OP in Maryland) Issued by (MetLife) Attached is the filing for the captioned forms. This letter provides an overview of the filing

April 16, 2018 Re: Group long-term policy G.LTC1697 (including GCLTCAARP-04-OP in Maryland) Issued by (MetLife) Attached is the filing for the captioned forms. This letter provides an overview of the filing

PART I INSURANCE COMPANIES

ISSN 19957165 TABLE OF CONTENTS 1. REPORT OF THE CENTRAL BANK OF TRINIDAD.01 1.05 AND TOBAGO FOR THE YEAR ENDED DECEMBER 31, 2006. 2. OVERVIEW OF THE INSURANCE INDUSTRY 2.01 2.06 FIGURES. Gross Premium

ISSN 19957165 TABLE OF CONTENTS 1. REPORT OF THE CENTRAL BANK OF TRINIDAD.01 1.05 AND TOBAGO FOR THE YEAR ENDED DECEMBER 31, 2006. 2. OVERVIEW OF THE INSURANCE INDUSTRY 2.01 2.06 FIGURES. Gross Premium

SERFF Tracking #: MULF State Tracking #: Company Tracking #: CT RERATE FILING, GROUP LONG-TERM CARE I...

SERFF Tracking #: MULF-129019410 State Tracking #: 201396350 Company Tracking #: CT RERATE FILING, GROUP LONG-TERM CARE I... State: Connecticut Filing Company: John Hancock Life Insurance Company (USA)

SERFF Tracking #: MULF-129019410 State Tracking #: 201396350 Company Tracking #: CT RERATE FILING, GROUP LONG-TERM CARE I... State: Connecticut Filing Company: John Hancock Life Insurance Company (USA)

SECURITIES AND EXCHANGE COMMISSION Consolidated quarterly report QSr 1 / 2005

SECURITIES AND EXCHANGE COMMISSION Consolidated quarterly report QSr 1 / 2005 Pursuant to 93 section 2 and 94 section 1 of the Regulation of the Council of Ministers of March 21, 2005 (Journal of Laws

SECURITIES AND EXCHANGE COMMISSION Consolidated quarterly report QSr 1 / 2005 Pursuant to 93 section 2 and 94 section 1 of the Regulation of the Council of Ministers of March 21, 2005 (Journal of Laws

Physicians Mutual Insurance Company 2600 Dodge Street Omaha, Nebraska 68131

2600 Dodge Street Omaha, Nebraska 68131 Actuarial Rate Memorandum Long-Term Care Policies December 15, 2016 Maryland 1. Purpose of Filing This is a rate increase filing for individual Long-Term Care policy

2600 Dodge Street Omaha, Nebraska 68131 Actuarial Rate Memorandum Long-Term Care Policies December 15, 2016 Maryland 1. Purpose of Filing This is a rate increase filing for individual Long-Term Care policy

COMPOSITION OF COMMITTEES OF ANJANI SYNTHETICS LIMITED

COMPOSITION OF COMMITTEES OF ANJANI SYNTHETICS LIMITED AUDIT COMMITTEES: 1) Audit s : Section 177 of the Companies Act, 2013 provides that every listed company shall constitute an Audit comprising of a

COMPOSITION OF COMMITTEES OF ANJANI SYNTHETICS LIMITED AUDIT COMMITTEES: 1) Audit s : Section 177 of the Companies Act, 2013 provides that every listed company shall constitute an Audit comprising of a

GASB 74 RSI Exhibits. Financial Statement Disclosure (Liabilities as of June 30, 2017)

") GASB 74 RSI Exhibits 1. EFFECT OF 1% CHANGE IN HEALTHCARE TREND In the event that healthcare trend rates were 1% higher than forecast and employee contributions were to increase at the forecast rates,

GASB 74 RSI Exhibits 1. EFFECT OF 1% CHANGE IN HEALTHCARE TREND In the event that healthcare trend rates were 1% higher than forecast and employee contributions were to increase at the forecast rates,

Overall, the oil and gas companies are not using a significant percentage of the federal lands that they have leased, but we all own.

Sitting Pretty: The numbers show that the oil and gas industry is flourishing on our federal lands, while sitting on thousands of unused drilling permits and tens of millions of acres of idle federal leases.

Sitting Pretty: The numbers show that the oil and gas industry is flourishing on our federal lands, while sitting on thousands of unused drilling permits and tens of millions of acres of idle federal leases.

Third Quarter 2018 Financial Review. October 23, 2018

Third Quarter 2018 Financial Review October 23, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

Third Quarter 2018 Financial Review October 23, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

CNO reports second quarter 2011 net income of $59.5 million, or 21 cents per share

Contact: (News Media) Tony Zehnder +1.312.396.7086 (Investors) Scott Galovic +1.317.817.3228 CNO reports second quarter 2011 net income of $59.5 million, or 21 cents per share Carmel, Ind. - CNO Financial

Contact: (News Media) Tony Zehnder +1.312.396.7086 (Investors) Scott Galovic +1.317.817.3228 CNO reports second quarter 2011 net income of $59.5 million, or 21 cents per share Carmel, Ind. - CNO Financial

SECOND-QUARTER 2017 FINANCIAL REVIEW. July 25, 2017

SECOND-QUARTER 2017 FINANCIAL REVIEW July 25, 2017 FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

SECOND-QUARTER 2017 FINANCIAL REVIEW July 25, 2017 FORWARD-LOOKING STATEMENTS Forward-looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

3Q18 Supplemental Slides. John McCallion Chief Financial Officer

3Q18 Supplemental Slides John McCallion Chief Financial Officer Table of Contents Explanatory Note on Non-GAAP Financial Information and Reconciliations... Page 3 Net Income (Loss) to Adjusted Earnings........

3Q18 Supplemental Slides John McCallion Chief Financial Officer Table of Contents Explanatory Note on Non-GAAP Financial Information and Reconciliations... Page 3 Net Income (Loss) to Adjusted Earnings........

SECURITIES AND EXCHANGE COMMISSION Washington, DC FORM 8-K. MOOG INC. (Exact name of registrant as specified in its charter)

") SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported):

SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported):

September 12, PreferredOne Insurance Company. Individual Comprehensive Medical Business. Rate Filing Justification

September 12, 2018 Individual Comprehensive Medical Business Rate Filing Justification Part Ill Actuarial Memorandum and Certification OVERVIEW This document contains the Part III Actuarial Memorandum

September 12, 2018 Individual Comprehensive Medical Business Rate Filing Justification Part Ill Actuarial Memorandum and Certification OVERVIEW This document contains the Part III Actuarial Memorandum

It is intended to be a Qualified Long-Term Care Insurance contract under the Federal Internal Revenue Code.

John Hancock Life Insurance Company (U.S.A.) Product Name Form Number Issue Date Range Group Long Term Care GPB-SPR-0007.02 June 1998 - October 2012 1. Scope & Purpose This memorandum consists of materials

John Hancock Life Insurance Company (U.S.A.) Product Name Form Number Issue Date Range Group Long Term Care GPB-SPR-0007.02 June 1998 - October 2012 1. Scope & Purpose This memorandum consists of materials

Proposed Revisions to Model 641 July 18, 2013 Draft (as discussed by Senior Issues (B) Task Force at Interim Meeting on June 11, 2013)

Task Force at Interim Meeting on June 11, 2013)") LONG-TERM CARE INSURANCE MODEL REGULATION Table of Contents Section 10. Section [XX] Section 20. Section 28. ***** Initial Filing Requirements ***** Annual Rate Certification Requirements ***** Premium

LONG-TERM CARE INSURANCE MODEL REGULATION Table of Contents Section 10. Section [XX] Section 20. Section 28. ***** Initial Filing Requirements ***** Annual Rate Certification Requirements ***** Premium

Fourth-Quarter and Year-End 2017 Financial Review. January 25, 2018

Fourth-Quarter and Year-End 2017 Financial Review January 25, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

Fourth-Quarter and Year-End 2017 Financial Review January 25, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

DAC Accounting Change Impact of Implementing ASU

DAC Accounting Change Impact of Implementing ASU 2010-26 on 2011 and Prior Periods April 25, 2012 Forward-Looking Statements Cautionary Statement Regarding Forward-Looking Statements. Our statements, trend

DAC Accounting Change Impact of Implementing ASU 2010-26 on 2011 and Prior Periods April 25, 2012 Forward-Looking Statements Cautionary Statement Regarding Forward-Looking Statements. Our statements, trend

NEIGHBOURHOOD CONCEPT PLAN (NCP) AREAS REQUIRE AMENITY CONTRIBUTIONS

AREAS REQUIRE AMENITY CONTRIBUTIONS") 13450 104 Ave Surrey, BC, V3T 1V8 March, 2018 PLANNING & DEVELOPMENT DEPARTMENT NEIGHBOURHOOD CONCEPT PLAN (NCP) AREAS REQUIRE AMENITY CONTRIBUTIONS The Surrey Official Community Plan encourages orderly

13450 104 Ave Surrey, BC, V3T 1V8 March, 2018 PLANNING & DEVELOPMENT DEPARTMENT NEIGHBOURHOOD CONCEPT PLAN (NCP) AREAS REQUIRE AMENITY CONTRIBUTIONS The Surrey Official Community Plan encourages orderly

Caterpillar Resource Industries. Denise Johnson, Group President

Caterpillar Resource Industries Denise Johnson, Group President Forward-Looking Statements Certain statements in this presentation relate to future events and expectations and are forward-looking statements

Caterpillar Resource Industries Denise Johnson, Group President Forward-Looking Statements Certain statements in this presentation relate to future events and expectations and are forward-looking statements

Homeowners Insurance Coverages

Homeowners Insurance Coverages An Actuarial Study of the Frequency and Cost of Claims for the State of Michigan by EPIC Consulting, LLC Principal Authors: Michael J. Miller, FCAS, MAAA Klayton N. Southwood,

Homeowners Insurance Coverages An Actuarial Study of the Frequency and Cost of Claims for the State of Michigan by EPIC Consulting, LLC Principal Authors: Michael J. Miller, FCAS, MAAA Klayton N. Southwood,

Actuarial Memorandum Supporting Rate Revision for Senior Health Insurance Company of Pennsylvania Long-Term Care Insurance Plan

April 2, 2018 Actuarial Memorandum Supporting Rate Revision for Long-Term Care Insurance Plan 1. PURPOSE OF FILING This is a rate increase filing for s (SHIP) policy forms outlined below. SHIP is requesting

April 2, 2018 Actuarial Memorandum Supporting Rate Revision for Long-Term Care Insurance Plan 1. PURPOSE OF FILING This is a rate increase filing for s (SHIP) policy forms outlined below. SHIP is requesting

Actuarial Memorandum Supporting Rate Revision for Senior Health Insurance Company of Pennsylvania Long-Term Care Insurance Plan

March 16, 2018 Actuarial Memorandum Supporting Rate Revision for Long-Term Care Insurance Plan 1. PURPOSE OF FILING This is a rate increase filing for s (SHIP) policy forms outlined below. SHIP is requesting

March 16, 2018 Actuarial Memorandum Supporting Rate Revision for Long-Term Care Insurance Plan 1. PURPOSE OF FILING This is a rate increase filing for s (SHIP) policy forms outlined below. SHIP is requesting

Philippine Case Study. Exploration and Investment Strategies In the frontier Basins. Mr. Lim Vatha Mr. Kimty Phally

Philippine Case Study Exploration and Investment Strategies In the frontier s Mr. Lim Vatha Mr. Kimty Phally Cambodian National Petroleum Authority Waterfront Hotel, Cebu City, Philippines March 14-18,

Philippine Case Study Exploration and Investment Strategies In the frontier s Mr. Lim Vatha Mr. Kimty Phally Cambodian National Petroleum Authority Waterfront Hotel, Cebu City, Philippines March 14-18,

ACTUARIAL VALUATION OF CITY OF LAUDERHILL POLICE OFFICERS RETIREMENT SYSTEM AS OF OCTOBER 1, July, 2013

ACTUARIAL VALUATION OF CITY OF LAUDERHILL POLICE OFFICERS RETIREMENT SYSTEM AS OF OCTOBER 1, 2012 July, 2013 Determination of Contribution for the Plan Year ending September 30, 2013 Contribution to be

ACTUARIAL VALUATION OF CITY OF LAUDERHILL POLICE OFFICERS RETIREMENT SYSTEM AS OF OCTOBER 1, 2012 July, 2013 Determination of Contribution for the Plan Year ending September 30, 2013 Contribution to be

First Quarter 2018 Financial Review. April 24, 2018

First Quarter 2018 Financial Review April 24, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

First Quarter 2018 Financial Review April 24, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

A statement that the policy design and coverage provided have been reviewed and taken into consideration;

LONG-TERM CARE INSURANCE MODEL REGULATION Table of Contents Section 10. Section [XX] Section 15. Section 20. Section 28. ***** Initial Filing Requirements ***** Annual Rate Certification Requirements *****

LONG-TERM CARE INSURANCE MODEL REGULATION Table of Contents Section 10. Section [XX] Section 15. Section 20. Section 28. ***** Initial Filing Requirements ***** Annual Rate Certification Requirements *****

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN The Government of Canada and the Government of Sweden, Resolved to continue their co-operation in the field of

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN The Government of Canada and the Government of Sweden, Resolved to continue their co-operation in the field of

SHARED RISK PLAN FOR CUPE EMPLOYEES OF NEW BRUNSWICK HOSPITALS. Amended and Revised as at

SHARED RISK PLAN FOR CUPE EMPLOYEES OF NEW BRUNSWICK HOSPITALS Amended and Revised as at October 20, 2017 TABLE OF CONTENTS Article I BACKGROUND AND PURPOSE OF THE PLAN...1 Article II DEFINITIONS...2 Article

SHARED RISK PLAN FOR CUPE EMPLOYEES OF NEW BRUNSWICK HOSPITALS Amended and Revised as at October 20, 2017 TABLE OF CONTENTS Article I BACKGROUND AND PURPOSE OF THE PLAN...1 Article II DEFINITIONS...2 Article

METLIFE ANNOUNCES FOURTH QUARTER AND FULL YEAR 2008 RESULTS

Public Relations MetLife, Inc. 1095 Avenue of the Americas New York, NY 10036 Contacts: For Media: For Investors: John Calagna Conor Murphy (212) 578-6252 (212) 578-7788 METLIFE ANNOUNCES FOURTH QUARTER

Public Relations MetLife, Inc. 1095 Avenue of the Americas New York, NY 10036 Contacts: For Media: For Investors: John Calagna Conor Murphy (212) 578-6252 (212) 578-7788 METLIFE ANNOUNCES FOURTH QUARTER

Second Quarter 2018 Financial Review. July 30, 2018

Second Quarter 2018 Financial Review July 30, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

Second Quarter 2018 Financial Review July 30, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

ACTUARIAL VALUATION OF TOWN OF DAVIE POLICE PENSION PLAN AS OF OCTOBER 1, February, 2014

ACTUARIAL VALUATION OF TOWN OF DAVIE POLICE PENSION PLAN AS OF OCTOBER 1, 2013 February, 2014 Determination of Contribution for the Plan Year ending September 30, 2014 Contribution to be Paid in Fiscal

ACTUARIAL VALUATION OF TOWN OF DAVIE POLICE PENSION PLAN AS OF OCTOBER 1, 2013 February, 2014 Determination of Contribution for the Plan Year ending September 30, 2014 Contribution to be Paid in Fiscal

CNO reports third quarter 2011 net income of $196.0 million, or 66 cents per share

Contact: (News Media) Tony Zehnder +1.312.396.7086 (Investors) Scott Galovic +1.317.817.3228 CNO reports third quarter 2011 net income of $196.0 million, or 66 cents per share Carmel, Ind. - CNO Financial

Contact: (News Media) Tony Zehnder +1.312.396.7086 (Investors) Scott Galovic +1.317.817.3228 CNO reports third quarter 2011 net income of $196.0 million, or 66 cents per share Carmel, Ind. - CNO Financial

Malvern Borough Zoning Ordinance TABLE OF CONTENTS

TABLE OF CONTENTS Article I: Title, Purpose, Objectives, and Interpretation Page Section 100. Title...I-1 Section 101. Purposes...I-1 Section 102. Statement of Community Development Objectives...I-1 Section

TABLE OF CONTENTS Article I: Title, Purpose, Objectives, and Interpretation Page Section 100. Title...I-1 Section 101. Purposes...I-1 Section 102. Statement of Community Development Objectives...I-1 Section

1998 Semi-annual Report

1998 Semi-annual Report Profit Net profit for the first six months of 1998 was PLN 8.6 million, with an end-of-year net profit forecast of PLN 18 million. The bank can contribute results to efficient allocation

1998 Semi-annual Report Profit Net profit for the first six months of 1998 was PLN 8.6 million, with an end-of-year net profit forecast of PLN 18 million. The bank can contribute results to efficient allocation

SEMI-ANNUAL SERVICER S CERTIFICATE

SEMI-ANNUAL SERVICER S CERTIFICATE TXU ELECTRIC DELIVERY TRANSITION BOND COMPANY LLC, $789,777,000 Transition Bonds, Series 2004-1 TXU Electric Delivery Company, as Servicer. Pursuant to Section 4.01(c)(ii)

SEMI-ANNUAL SERVICER S CERTIFICATE TXU ELECTRIC DELIVERY TRANSITION BOND COMPANY LLC, $789,777,000 Transition Bonds, Series 2004-1 TXU Electric Delivery Company, as Servicer. Pursuant to Section 4.01(c)(ii)

The Permanent University Fund and Available University Fund

The Permanent University Fund and Available University Fund This issue brief describes the Permanent University Fund (PUF) and the Available University Fund (AUF), particularly as used and administered

The Permanent University Fund and Available University Fund This issue brief describes the Permanent University Fund (PUF) and the Available University Fund (AUF), particularly as used and administered

The accompanying notes are an integral part of these unconsolidated financial statements.

UNCONSOLIDATED BALANCE SHEET AS OF 31 MARCH 2016 I. BALANCE SHEET (STATEMENT OF FINANCIAL POSITION) Audited 31 March 2017 31 December 2016 ASSETS Note TRY FC Total TRY FC Total I. CASH AND BALANCES WITH

UNCONSOLIDATED BALANCE SHEET AS OF 31 MARCH 2016 I. BALANCE SHEET (STATEMENT OF FINANCIAL POSITION) Audited 31 March 2017 31 December 2016 ASSETS Note TRY FC Total TRY FC Total I. CASH AND BALANCES WITH

CITY OF WINTER SPRINGS DEFINED BENEFIT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2008

CITY OF WINTER SPRINGS DEFINED BENEFIT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2008 This Valuation Determines the Annual Contribution for the Plan Year October 1, 2008 through September 30, 2009 with

CITY OF WINTER SPRINGS DEFINED BENEFIT PLAN ACTUARIAL VALUATION AS OF OCTOBER 1, 2008 This Valuation Determines the Annual Contribution for the Plan Year October 1, 2008 through September 30, 2009 with

SEMI-ANNUAL SERVICER S CERTIFICATE

SEMI-ANNUAL SERVICER S CERTIFICATE TXU ELECTRIC DELIVERY TRANSITION BOND COMPANY LLC, $789,777,000 Transition Bonds, Series 2004-1 TXU Electric Delivery Company, as Servicer. Pursuant to Section 4.01(c)(ii)

SEMI-ANNUAL SERVICER S CERTIFICATE TXU ELECTRIC DELIVERY TRANSITION BOND COMPANY LLC, $789,777,000 Transition Bonds, Series 2004-1 TXU Electric Delivery Company, as Servicer. Pursuant to Section 4.01(c)(ii)

AVIVA GROUP GRATUITY ADVANTAGE [UIN : 122L090V01] Non Participating Linked Plan STANDARD TERMS & CONDITIONS

![AVIVA GROUP GRATUITY ADVANTAGE [UIN : 122L090V01] Non Participating Linked Plan STANDARD TERMS & CONDITIONS](/thumbs/92/108015691.jpg "AVIVA GROUP GRATUITY ADVANTAGE [UIN : 122L090V01] Non Participating Linked Plan STANDARD TERMS & CONDITIONS") AVIVA GROUP GRATUITY ADVANTAGE [UIN : 122L090V01] Non Participating Linked Plan STANDARD TERMS & CONDITIONS Note: In this Master Policy, the investment risk in the investment portfolio is borne by You

AVIVA GROUP GRATUITY ADVANTAGE [UIN : 122L090V01] Non Participating Linked Plan STANDARD TERMS & CONDITIONS Note: In this Master Policy, the investment risk in the investment portfolio is borne by You

Holding(s) in Company - London Stock Exchange

in Company - London Stock Exchange") Page 1 of 5 Regulatory Story Go to market news section Company TIDM Headline Released HUM Holding(s) in Company 16:03 16-Dec-2010 1281Y16 RNS : 1281Y 16 December 2010 TR-1: NOTIFICATION OF MAJOR INTEREST

Page 1 of 5 Regulatory Story Go to market news section Company TIDM Headline Released HUM Holding(s) in Company 16:03 16-Dec-2010 1281Y16 RNS : 1281Y 16 December 2010 TR-1: NOTIFICATION OF MAJOR INTEREST

BES FINANCE LTD. [50,000,000] BES PORTUGAL OUTUBRO NOTES Guaranteed by Banco Espirito Santo S.A. (acting through its London branch)

![BES FINANCE LTD. [50,000,000] BES PORTUGAL OUTUBRO NOTES Guaranteed by Banco Espirito Santo S.A. (acting through its London branch)](/thumbs/93/114466678.jpg "BES FINANCE LTD. [50,000,000] BES PORTUGAL OUTUBRO NOTES Guaranteed by Banco Espirito Santo S.A. (acting through its London branch)") 27 September 2011 BES FINANCE LTD. [50,000,000] BES PORTUGAL OUTUBRO 2011-2014 NOTES Guaranteed by Banco Espirito Santo S.A. (acting through its London branch) Issued under the 20,000,000,000 Euro Medium

27 September 2011 BES FINANCE LTD. [50,000,000] BES PORTUGAL OUTUBRO 2011-2014 NOTES Guaranteed by Banco Espirito Santo S.A. (acting through its London branch) Issued under the 20,000,000,000 Euro Medium

(CONVENIENCE TRANSLATION OF FINANCIAL STATEMENTS)

") BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.245.952 27.373.211 53.619.163 1.1 Cash and cash equivalents 2.125.340

BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.245.952 27.373.211 53.619.163 1.1 Cash and cash equivalents 2.125.340

(CONVENIENCE TRANSLATION OF FINANCIAL STATEMENTS)

") BALANCE SHEET AS OF SEPTEMBER 30, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 30.09.2018 I. FINANCIAL ASSETS (Net) 36.351.297 34.145.223 70.496.520 1.1 Cash and cash equivalents 2.216.435

BALANCE SHEET AS OF SEPTEMBER 30, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 30.09.2018 I. FINANCIAL ASSETS (Net) 36.351.297 34.145.223 70.496.520 1.1 Cash and cash equivalents 2.216.435

(CONVENIENCE TRANSLATION OF FINANCIAL STATEMENTS)

") BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.600.080 27.411.488 54.011.568 1.1 Cash and cash equivalents 2.537.892

BALANCE SHEET AS OF DECEMBER 31, 2018 (STATEMENT OF FINANCIAL POSITION) I. BALANCE SHEET ASSETS 31.12.2018 I. FINANCIAL ASSETS (Net) 26.600.080 27.411.488 54.011.568 1.1 Cash and cash equivalents 2.537.892

Southern California Contractors Association, Inc E. Washington Blvd., Suite 200 Los Angeles, CA / Fax 323/

Southern California Contractors Association, Inc. 6055 E. Washington Blvd., Suite 200 Los Angeles, CA 90040 323/726-3511 Fax 323/726-2366 LABOR BULLETIN 11/13 TO: SUBJECT: SCCA CONTRACTOR & ALLIED MEMBERS

Southern California Contractors Association, Inc. 6055 E. Washington Blvd., Suite 200 Los Angeles, CA 90040 323/726-3511 Fax 323/726-2366 LABOR BULLETIN 11/13 TO: SUBJECT: SCCA CONTRACTOR & ALLIED MEMBERS

9/6/13 Long-Term Care Pricing Subgroup Call Discussion Document

9/6/13 Long-Term Care Pricing Subgroup Call Discussion Document Below is the set of recommendations for modifications to the Long-Term Care Insurance Model Regulation as discussed on the 8/16 LTC Pricing

9/6/13 Long-Term Care Pricing Subgroup Call Discussion Document Below is the set of recommendations for modifications to the Long-Term Care Insurance Model Regulation as discussed on the 8/16 LTC Pricing

Allianz Bajaj Life Insurance Company Limited. Group Master Policy No. Allianz Bajaj Group Gratuity Care. for the employees of

Allianz Bajaj Life Insurance Company Limited Group Master Policy No. Allianz Bajaj Group Gratuity Care for the employees of GROUP GRATUITY CARE MASTER POLICY SCHEDULE Schedule Date: Schedule No: [x] This

Allianz Bajaj Life Insurance Company Limited Group Master Policy No. Allianz Bajaj Group Gratuity Care for the employees of GROUP GRATUITY CARE MASTER POLICY SCHEDULE Schedule Date: Schedule No: [x] This

Guide to completing W-8BEN-E entity US tax forms. Applicable to Companies, Trusts, Self Managed Superannuation Funds and Deceased Estates

Guide to completing W-8BEN-E entity US tax forms Applicable to Companies, Trusts, Self Managed Superannuation Funds and Deceased Estates Contents 1 General information 01 1.1 Who is this guide intended

Guide to completing W-8BEN-E entity US tax forms Applicable to Companies, Trusts, Self Managed Superannuation Funds and Deceased Estates Contents 1 General information 01 1.1 Who is this guide intended

METLIFE ANNOUNCES STRONG SECOND QUARTER 2010 RESULTS

Public Relations MetLife, Inc. 1095 Avenue of the Americas New York, NY 10036 Contacts: For Media: John Calagna (212) 578-6252 For Investors: Conor Murphy (212) 578-7788 METLIFE ANNOUNCES STRONG SECOND

Public Relations MetLife, Inc. 1095 Avenue of the Americas New York, NY 10036 Contacts: For Media: John Calagna (212) 578-6252 For Investors: Conor Murphy (212) 578-7788 METLIFE ANNOUNCES STRONG SECOND

Prospectus Rules. Chapter 2. Drawing up the prospectus

Prospectus Rules Chapter Drawing up the PR : Drawing up the included in a.3 Minimum information to be included in a.3.1 EU Minimum information... Articles 3 to 3 of the PD Regulation provide for the minimum

Prospectus Rules Chapter Drawing up the PR : Drawing up the included in a.3 Minimum information to be included in a.3.1 EU Minimum information... Articles 3 to 3 of the PD Regulation provide for the minimum

Wells Fargo Industrials Conference. May 8, 2018

Wells Fargo Industrials Conference May 8, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

Wells Fargo Industrials Conference May 8, 2018 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking statements within

MetLife, Inc. Acquisition of ALICO. March 8, 2010

MetLife, Inc. Acquisition of ALICO March 8, 2010 ALICO: A Unique and Compelling Transaction Significantly Accelerates the Execution of MetLife s Global Growth Strategy Diversifies revenue and earnings

MetLife, Inc. Acquisition of ALICO March 8, 2010 ALICO: A Unique and Compelling Transaction Significantly Accelerates the Execution of MetLife s Global Growth Strategy Diversifies revenue and earnings

PRICING SUPPLEMENT FOR CREDIT-LINKED NOTES

PRICING SUPPLEMENT FOR CREDIT-LINKED NOTES The terms and conditions of Credit-Linked Notes shall consist of the "Terms and Conditions of the Notes" set out in "Part B Information relating to the Notes

PRICING SUPPLEMENT FOR CREDIT-LINKED NOTES The terms and conditions of Credit-Linked Notes shall consist of the "Terms and Conditions of the Notes" set out in "Part B Information relating to the Notes

Finance (No. 2) Bill 2014

Bill 2014") Finance (No. 2) Bill 2014 Proposed Income Tax Amendments Mr. R.N. LAKHOTIA Leading Income Tax Consultant & Author The Finance Minister presented the Finance (No.2) Bill 2014 along with the Union Budget

Finance (No. 2) Bill 2014 Proposed Income Tax Amendments Mr. R.N. LAKHOTIA Leading Income Tax Consultant & Author The Finance Minister presented the Finance (No.2) Bill 2014 along with the Union Budget

Important Disclosure Information Health Savings Account Custodial Agreement

Important Disclosure Information Health Savings Account Custodial Agreement Under section 223(a) of the Internal Revenue Code I. Agreement PayFlex Systems USA, Inc. ( PayFlex, Custodian, "us" or "we")

Important Disclosure Information Health Savings Account Custodial Agreement Under section 223(a) of the Internal Revenue Code I. Agreement PayFlex Systems USA, Inc. ( PayFlex, Custodian, "us" or "we")

Assurant, Inc. (Exact Name of Registrant as Specified in Charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event

bulletin For distribution to relevant parties within your firm Jane Tan Information Analyst BULLETIN #3362 (416) December 17, 2004

December 17, 2004") bulletin Contact: For distribution to relevant parties within your firm Jane Tan Information Analyst BULLETIN #3362 (416) 943-6979 December 17, 2004 By-laws and Regulations Amendments to Regulation 100.9

bulletin Contact: For distribution to relevant parties within your firm Jane Tan Information Analyst BULLETIN #3362 (416) 943-6979 December 17, 2004 By-laws and Regulations Amendments to Regulation 100.9

Prospectus. Alcoa Corporation. Common Stock. Alcoa Corporation 2016 Stock Incentive Plan (As Amended and Restated)

") Prospectus Alcoa Corporation Common Stock Alcoa Corporation 2016 Stock Incentive Plan (As Amended and Restated) This prospectus relates to shares of common stock, par value $0.01 per share (the Common

Prospectus Alcoa Corporation Common Stock Alcoa Corporation 2016 Stock Incentive Plan (As Amended and Restated) This prospectus relates to shares of common stock, par value $0.01 per share (the Common

Fourth Quarter and Full Year 2018 Financial Review. January 28, 2019

Fourth Quarter and Full Year 2018 Financial Review January 28, 2019 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

Fourth Quarter and Full Year 2018 Financial Review January 28, 2019 Forward-Looking Statements Certain statements in this financial review relate to future events and expectations and are forward-looking

GOVERNMENT OF ANDHRA PRADESH ABSTRACT

GOVERNMENT OF ANDHRA PRADESH ABSTRACT PUBLIC SERVICES Revised Pay Scales 2015 Orders Issued. --------------------------------------------------------------------------------------------------------------------------------

GOVERNMENT OF ANDHRA PRADESH ABSTRACT PUBLIC SERVICES Revised Pay Scales 2015 Orders Issued. --------------------------------------------------------------------------------------------------------------------------------

As you are aware, a copy of the Report should be filed with the State at the following address upon approval by the Board.

April 27, 2015 Mr. Ricky Thompson City Clerk City of Starke General Employees P.O. Box C 209 N. Thompson Street Starke, Florida 32091-1278 Re: Actuarial Valuation General Employees Dear Ricky: As requested,

April 27, 2015 Mr. Ricky Thompson City Clerk City of Starke General Employees P.O. Box C 209 N. Thompson Street Starke, Florida 32091-1278 Re: Actuarial Valuation General Employees Dear Ricky: As requested,

City of Winter Springs Defined Benefit Plan Actuarial Valuation

February 28, 2011 Mr. Shawn Boyle Finance and Administrative Services Director City of Winter Springs 1126 East State Road 434 Winter Springs, Florida 32708 Re: City of Winter Springs Actuarial Valuation

February 28, 2011 Mr. Shawn Boyle Finance and Administrative Services Director City of Winter Springs 1126 East State Road 434 Winter Springs, Florida 32708 Re: City of Winter Springs Actuarial Valuation

ALCOA INC Alcoa Stock Incentive Plan, as Amended and Restated

ALCOA INC. 2013 Alcoa Stock Incentive Plan, as Amended and Restated SECTION 1. PURPOSE. The purpose of the 2013 Alcoa Stock Incentive Plan is to encourage selected Directors and Employees to acquire a

ALCOA INC. 2013 Alcoa Stock Incentive Plan, as Amended and Restated SECTION 1. PURPOSE. The purpose of the 2013 Alcoa Stock Incentive Plan is to encourage selected Directors and Employees to acquire a

Honda Auto Receivables Owner Trust. American Honda Receivables LLC, American Honda Finance Corporation

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-D ASSET-BACKED ISSUER DISTRIBUTION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-D ASSET-BACKED ISSUER DISTRIBUTION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-D

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-D ASSET-BACKED ISSUER DISTRIBUTION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-D ASSET-BACKED ISSUER DISTRIBUTION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the

Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements

Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements (Ordinance of the Ministry of Finance No. 28 of October 30, 1976) Pursuant to the provisions of Article 193

Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements (Ordinance of the Ministry of Finance No. 28 of October 30, 1976) Pursuant to the provisions of Article 193

NORWEGIAN CRUISE LINE HOLDINGS LTD. Reported by AIF VI MANAGEMENT, LLC

NORWEGIAN CRUISE LINE HOLDINGS LTD. Reported by AIF VI MANAGEMENT, LLC FORM 4 (Statement of Changes in Beneficial Ownership) Filed 11/21/14 for the Period Ending 11/19/14 Address 7665 CORPORATE DRIVE MIAMI,