Risk Management in Islamic Financial Institutions

|

|

|

- Shanna Freeman

- 6 years ago

- Views:

Transcription

1 1 Risk Management in Islamic Financial Institutions Rifki Ismal Fakultas Ekonomi UI dan IQTISHAD consulting Training on Risk Management Depok, 23 November 2013

and PhD in Islamic economics and Finance from Durham")

2 SHORT BIO Rifki Ismal is both central banker and lecturer. He earned bachelor degree in economics from University of Indonesia, master degree in economics from University of Michigan, Ann Arbor (USA) and PhD in Islamic economics and Finance from Durham University (England). An Associate Professor in Islamic Banking and Finance is from the Australian Government (Australian Center for Islamic Financial Studies). He has published more thirty papers in international journals and a book titling Islamic Banking in Indonesia: New Perspective in Monetary and Finance (John Wiley and Sons, March 2013)

3 3 Risk in Sharia Jurisprudence and Sharia Mechanism in Risk Management

4 RISK IN SHARIA JURISPRUDENCE Risk is close to definition of gharar in sharia. Gharar is any uncertainty or ambiguity created by the lack of information or control in contract. By size, there are gharar fahish (big gharar) and gharar yasir (small gharar). The former should be controlled and minimized while the latter has characteristics of (i) Negligible (ii) Inevitable (iii) Unintentional; and could be borne or ignored.

5 RISK IN SHARIA JURISPRUDENCE In gharar fahish, by behavior, there are natural gharar and created gharar. Natural gharar happens without any intervention of any party like business loss, natural disaster, asset destruction, etc. Islamic banks may or may not avoid this risk but can not transfer it to other parties.

6 RISK IN SHARIA JURISPRUDENCE Created gharar occurs because of human interventional like gambling, impermissible contracts, fake contracts, invalid contracts, etc. Types of intervention are taghrir al fi li (fraudulent acts); taghrir al qawli (fraudulent statement); taghrir kithman (fraudulent concealment). Islamic banks may not do and must avoid this created gharar because created gharar means creating problem of uncertainty or playing with uncertainty condition.

7 RISK IN SHARIA JURISPRUDENCE Risk management in Islamic banking deals with minimizing lack of information and maximizing control through sharia approaches such as profit and loss sharing, al ghunmu billa ghurmi, al kharaj bid daman, positive or negative sum game, cooperation and coordination and sharia compliance business activities, etc.

8 8 Types and Characteristics of Risks in Banking Operations

9 RISK MANAGEMENT IN FINANCIAL INSTITUTIONS Risk management determines the successfulness of financial institutions in managing funds and providing wellexpected return to stakeholders. It prevents a bank from financial failure, insolvency, liquidity distress, etc and build a good communication/coordination with stakeholders. It measures and explains every type of risk which will allow a bank to take necessary actions to anticipate and mitigate any risk.

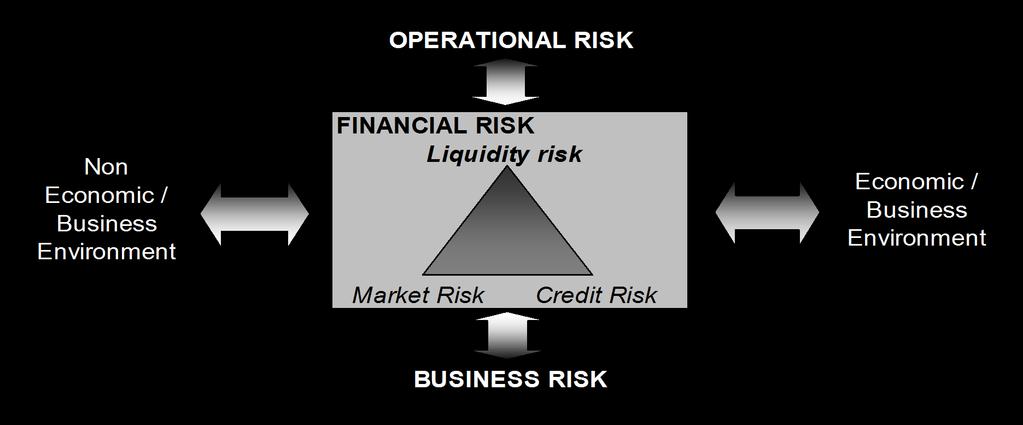

10 RISK MANAGEMENT IN FINANCIAL INSTITUTIONS In general it is necessity for the robustness of the overall financial system and economic stability at the end. Risk management unexceptionally becomes part of Islamic banking institution with its unique characteristics and operations. Risk in financial terms is usually defined as the probability that the actual return may differ from the expected return (Howells and Bain, 1999:30). There are in fact three broad categories of risk namely (1) Financial risk, (2) Business risk and lastly (3) Operational risk.

11 TYPES OF RISKS IN BANKING FINANCIAL AND BUSINESS RISK Financial Risk Business Risk Operational Risk Credit Risk Management Risk People Risk Default Risk Planning Risk Relationship Risk Down Grade Risk Organization Risk Ethics Risk Counter party Risk Reporting Risk Processes Risk Settlement Risk Monitoring Risk Legal Risk Market Risk Strategic Risk Compliance Risk Commodity Price Risk R & D Risk Control Risk Equity Price Risk Product Design Risk Interest Rate Risk Market Dynamic Risk System Risk Exchange Rate Risk Economic Risk Hardware Risk Reputation Risk Software Risk Liquidity Risk Models ICT Risk Asset-Liability Imbalance Maturity Mismatch Risk Followed by External Risk Insolvency Risk Event Risk Gov't Taken Over Risk Client Risk Reputation Risk Legal Risk Security Risk Supervisory Risk System Risk Source : Tariqullah Khan, 2006 (modified) Equity Investment Risk

12 TYPES OF RISKS IN BANKING Risk can be expressed within a casual and interactive system, as the impact of each risk can t be seen isolated, since they correlate and influence each other. Financial risk is the exposures that result in a direct financial loss to the assets or liabilities of a bank. Besides credit, market risk and liquidity risk, Islamic banks face equity investment risk. Credit risk relates to the performance of entrepreneurs: failure to fulfill their payment obligations, settlement, clearing, etc.

13 TYPES OF RISKS IN BANKING Market risk happens due to unfavorable price movement or economic/financial condition such as RoR risk, exchange rate, inflation, etc. Unlike conventional one, Islamic banks bear risk of tradable, marketable, leaseable asset and mark up risk. Liquidity risk consists of 2 part: (i) Liquidity of financial instruments in financial market and; (ii) Liquidity related to solvency.

14 TYPES OF RISKS IN BANKING Business risk links with the performance of bank s business and internal action such as business policy, infrastructure, payment system, etc. Thus business risk deals with (i) management risk which asks how is bank s planning, organizing, monitoring, reporting, etc and (ii) strategic risk is like R&D, product design, etc.

15 TYPES OF RISKS IN BANKING Operational risk occurs if a bank fails to manage people, system, legal, external risk and equity investment. It is internal process risk which brings together harmonization of : People (relationship, ethics, process, etc); Legal (compliance and control risk); System (hardware, software, etc) and; External risk (event, clients, security, supervisory, etc). Equity investment (asset, pricing, valuation).

16 TYPES OF RISKS IN BANKING Mark up risk is risk because of fluctuation of benchmark rate or inaccurate/unfavorable mark up determination. Commodity price risk happens due to the fluctuation of price of a commodity. Legal risk is because of improper regulation, lack of regulation, etc.

17 TYPES OF RISKS IN BANKING Withdrawal risk is when depositors take out their money for regular or irregular reasons. Fiduciary risk, when Islamic bank operates unislamically (violating sharia principles). Displaced commercial risk occurs when depositors switch their deposit into conventional one which offers more profitable/attractive return.

18 18 Islamic Banking Principles and Internal/External Factors Leading to Risks

19 ISLAMIC BANKING PRINCIPLES & RISK MANAGEMENT Islamic contracts require depositors to fully understand consequence of dealing with Islamic bank particularly: no guarantee/fixed return on deposit, no return on demand deposit, periodical withdrawal on long term time deposit and risk/return sharing. Islamic bank mitigates its risk through risk sharing with depositors and entrepreneurs particularly profit and loss sharing (PLS) or return sharing scheme.

20 ISLAMIC BANKING PRINCIPLES & RISK MANAGEMENT Economic / financial market risks are pure risk that can not be hindered by all parties but have to be minimized, avoided and handled properly. Islamic bank does not eliminate risk (interest based) but sharing/handling risk. Regulator coordinates and designs proper legal and regulatory standard to control and manage performance of Islamic banking as well as preventing any unfavorable economic/business condition.

21 INTERNAL/EXTERNAL FACTORS & RISK MANAGEMENT

22 ISLAMIC WAY OF MITIGATING RISK IN BANKS DEPOSIT/ SOURCE OF FUNDING Withdrawal risk, Displaced commercial risk, Liquidity Risk Risk Sharing BANKING AUTHORITY ISLAMIC BANK People risk, Legal risk, Reputation risk, External risk, Equity investment risk Risk Sharing ECONOMIC & FINANCIAL MARKET REAL SECTOR FINANCING Credit risk, Default risk, Counterparty risk, Settlement risk, etc Legal risk, Supervisory risk, Systemic risk, Monitoring risk Coordination and Regulation Exchange rate risk, RoR risk, Inflation risk, Price risk Pure Risk

23 PROBLEMS IN HANDLING RISK IN ISLAMIC BANKS Every Sharia contract connects/relates with performance of real sector. Interest rate disconnects financial sector with real sector. Market risk applies directly or indirectly in every Islamic contract.

24 PROBLEMS IN HANDLING RISK IN ISLAMIC BANKS Due to its early stage of development, Islamic banking industry faces lack of infrastructure, technology, regulation, lack of eligible human resources, lack of product innovation, etc. All of them might invite risk into the operation of Islamic bank. Islamic banks are free from interest rate risk but indirectly impacted by it.

25 25 Islamic Financial Services Board (IFSB) Guides on Risk Management in Islamic Financial Institutions

26 IFSB GUIDES ON RISK MANAGEMENT IFSB Principles of Risk Management: Islamic financial institution (IFI) shall have a sound process for executing all elements of risk management. IFI shall ensure an adequate system of controls with appropriate checks and balances. IFI shall ensure the quality and timeliness of risk reporting available to regulatory authorities. IFI shall make appropriate and timely disclosure of information.

27 IFSB GUIDES ON RISK MANAGEMENT IFSB Principles of Credit risk: Principle 2.1: Islamic financial institutions (IFI) shall have in place a strategy for financing using the various Islamic instruments in compliance with sharia, whereby it recognizes the potential credit exposures that may arise at different stages of the various financing agreement. Principle 2.2: IFI shall carry out a due diligence review in respect of counterparties prior to deciding on the choice of an appropriate Islamic financing instruments.

28 IFSB GUIDES ON RISK MANAGEMENT IFSB Principles of Credit risk: Principle 2.3 : IFI shall have in place appropriate methodologies for measuring and reporting the credit risk exposures arising under each Islamic financing instruments. Principle 2.4: IFI shall have in place sharia compliant credit risk mitigating techniques appropriate for each Islamic financing instruments.

29 IFSB GUIDES ON RISK MANAGEMENT IFSB Principles of Market risk: Principle 4.1: IFI shall have in place an appropriate framework for market risk management in respect of all assets held, including those that do not have a ready market and/or are exposed to high price volatility. IFSB Principles of Liquidity risk: Principle 5.1: IFI shall have in place a liquidity management framework taking into account separately and on an overall basis their liquidity exposure in respect of each category of current accounts, unrestricted and restricted investment accounts. Principle 5.2: IFI shall undertake liquidity risk commensurate with their ability to have sufficient recourse to sharia compliant funds to mitigate such risk.

30 30 Sharia Approaches on Liquidity Risk Management

31 Challenges Related to Liquidity Risk Management From liability side: the requirement to maintain adequate liquidity as a standby reserve. It contains two modes of reserves, namely cash reserve requirement in the central bank and statutory liquidity requirement in the bank itself Another type of liquidity reserved for such purpose is placement in money market instrument essentially the very short-term basis. Usually, the instruments take form of debt based such as Murabahah inter bank or equity based such as Musharakah and Mudarabah inter bank and ready to be liquidated whenever the bank needs.

32 Challenges Related to Liquidity Risk Management From asset side: Islamic bank tends to allocate fund in just short-term investment basis (Gafoor, 1995:8). Even, in the short investment period, Islamic bank prefers debt based Islamic financing to equity based. The necessary challenge appears in the case of default by business partners because Islamic bank is prohibited from charging any accrued interest or imposing any penalty. The other challenges are lack of easily liquidated long-term investment, immature financial market, etc.

33 IFSB Guide on Liquidity Risk Management IIFS shall have in place a liquidity management framework (including reporting) taking into account separately and on an overall basis their liquidity exposures in respect of each category of current accounts, unrestricted and restricted investment accounts (Principle 5.1). IIFS shall assume liquidity risk commensurate with their ability to have sufficient recourse to sharia compliant funds to mitigate such risk (Principle 5.2). Best practices in many IB identify involvement of investors, Islamic bank, business partners and their stakeholders in dealing with liquidity risk mitigation.

34 Best Practices in ISLAMIC BANKS

35 Investors Involvement in Liquidity Risk Management Sharia ties investors of the bank to be responsible and aware of liquidity risk. Their engagements are ultimately in forms of their deep understanding of Islamic banking principles, operations and business consequences. The most important one is their unwillingness to entail in the prohibited business activities such as: speculation, interest rate return seeking, etc besides their willingness to share the risk and responsibility with the bank.

36 Investors Involvement in Liquidity Risk Management The mature investors will be ready to accept: risk sharing, no periodic return in certain types of the banks products, and all other following consequences. Meanwhile, for business partners, the understood investors will indirectly guarantee the availability of fund for business.

37 IB Roles in Liquidity Risk Management IB develops internal sharia approaches facing liquidity risk problem : Liquidity risk management policy that includes policy related to liability and asset side. It is established by Board of Director and followed up by special task body and continued by senior management in a very technical level. Measuring and monitoring liquidity risk. Islamic bank is obliged to maintain adequate liquidity as its standby reserve and regularly review its limit. Prudential and sharia compliance banking operation that deals with the bank s financing decisions, business partners selection, and possibility of join operation with other Islamic banks.

38 IB Roles in Liquidity Risk Management Sharia based liability management. IB follows three approaches: Adjusting types of deposit products into projects to be financed; Balancing of financing needed and amount to be collected and; Managing maturity date of both deposit products and projects financing.

39 IB Roles in Liquidity Risk Management Sharia based asset management. IB approaches are, Fitting characteristics of deposit and projects financing; Matching the flow of projects return with the due date of PLS payment; Selecting business partners through due diligence; Employing joint financing with other Islamic banks to share the risk and; Monitoring and conducting cooperative business

40 40 End

Risk Management in Islamic Banking (lecture 1)

") Risk Management in Islamic Banking (lecture 1) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4 th, 2009 Rifki Ismal Durham University

Risk Management in Islamic Banking (lecture 1) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4 th, 2009 Rifki Ismal Durham University

Liquidity Risk Management in Islamic Banking

Liquidity Risk Management in Islamic Banking Executive Development Program Islamic Treasury & Liquidity Management March 26 th 27 th, 2012 Sampoerna Business School and BNI Syariah Dr. Rifki Ismal Bank

Liquidity Risk Management in Islamic Banking Executive Development Program Islamic Treasury & Liquidity Management March 26 th 27 th, 2012 Sampoerna Business School and BNI Syariah Dr. Rifki Ismal Bank

Risk Management in Islamic Financial Institutions

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY THREE Sharia Approaches on Liquidity Risk Management Challenges Related to Liquidity

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY THREE Sharia Approaches on Liquidity Risk Management Challenges Related to Liquidity

Risk Management in Islamic Financial Institutions

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY TWO Risk in Sharia Jurisprudence and Sharia Mechanism in Risk Management RISK IN SHARIA

1 Risk Management in Islamic Financial Institutions Rifki Ismal Sesric Training Program Turkey, 3-5th June 2013 2 DAY TWO Risk in Sharia Jurisprudence and Sharia Mechanism in Risk Management RISK IN SHARIA

Sharia Issues in Liquidity Risk Management

Sharia Issues in Liquidity Risk Management Paper Presented in Colloque International Banque et Finance Islamiques Universite Robert Schuman, Strasbourg (France) January, 11 th, 2008 Rifki Ismal Doctoral

Sharia Issues in Liquidity Risk Management Paper Presented in Colloque International Banque et Finance Islamiques Universite Robert Schuman, Strasbourg (France) January, 11 th, 2008 Rifki Ismal Doctoral

Risk Management in Islamic Banking (lecture 3)

") Risk Management in Islamic Banking (lecture 3) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4th, 2009 Rifki Ismal Durham University

Risk Management in Islamic Banking (lecture 3) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4th, 2009 Rifki Ismal Durham University

Sharia Issues in Liquidity Risk Management

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

Seminar on Islamic Finance. Challenges in Developing Islamic Financial Services in Europe. 11 November 2009, Rome, Italy.

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

THE INDONESIAN ISLAMIC BANKING Theory and Practices

Rifki Ismal, PhD THE INDONESIAN ISLAMIC BANKING Theory and Practices ^ d publishing TABLE OF CONTENT FOREWORDS..., vii TABLE OF CONTENT xi LIST OF FIGURES,.. '. xvii LIST OF TABLES... '. xxi Chapter 1

Rifki Ismal, PhD THE INDONESIAN ISLAMIC BANKING Theory and Practices ^ d publishing TABLE OF CONTENT FOREWORDS..., vii TABLE OF CONTENT xi LIST OF FIGURES,.. '. xvii LIST OF TABLES... '. xxi Chapter 1

Liquidity Risk Problem in Islamic Banking Industry (Case of Indonesia)

") Liquidity Risk Problem in Islamic Banking Industry (Case of Indonesia) Paper Presented in Ustinov College Finance Seminar Durham University, May 3 rd, 2008 Rifki Ismal PhD Student School of Government

Liquidity Risk Problem in Islamic Banking Industry (Case of Indonesia) Paper Presented in Ustinov College Finance Seminar Durham University, May 3 rd, 2008 Rifki Ismal PhD Student School of Government

Indonesian Islamic Banking: Facing Liquidity Risk?

Indonesian Islamic Banking: Facing Liquidity Risk? Paper Presented in Summer School Program in Islamic Finance and Banking Durham University, July 2007 Rifki Ismal PhD Student Durham University Outline

Indonesian Islamic Banking: Facing Liquidity Risk? Paper Presented in Summer School Program in Islamic Finance and Banking Durham University, July 2007 Rifki Ismal PhD Student Durham University Outline

Asset & Liability Management : challenges facing Islamic financial institutions! Majdi Chaabouni!

Asset & Liability Management : challenges facing Islamic financial institutions! Majdi Chaabouni! Presented at the Durham Islamic Finance Autumn School 21 jointly organised by Durham Centre for Islamic

Asset & Liability Management : challenges facing Islamic financial institutions! Majdi Chaabouni! Presented at the Durham Islamic Finance Autumn School 21 jointly organised by Durham Centre for Islamic

RISK MANAGEMENT MODULE

RISK MANAGEMENT MODULE MODULE: RM (Risk Management) Table of Contents RM-A RM-B RM-1 RM-2 RM-3 RM-4 RM-5 RM-6 RM-7 Date Last Changed Introduction RM-A.1 Purpose 01/2013 RM-A.2 Module History 04/2013 Scope

RISK MANAGEMENT MODULE MODULE: RM (Risk Management) Table of Contents RM-A RM-B RM-1 RM-2 RM-3 RM-4 RM-5 RM-6 RM-7 Date Last Changed Introduction RM-A.1 Purpose 01/2013 RM-A.2 Module History 04/2013 Scope

The Certified Islamic Specialist in Risk Management

1 The Certified Islamic Specialist in Risk Management Introduction: Due to the sheer nature of their varied and complex activities, banks are often exposed to an array of risks such as credit risks, market

1 The Certified Islamic Specialist in Risk Management Introduction: Due to the sheer nature of their varied and complex activities, banks are often exposed to an array of risks such as credit risks, market

Indonesian Islamic Banking: Current Development, Policies and Prospect

Indonesian Islamic Banking: Current Development, Policies and Prospect Paper Presented in Summer School Program in Islamic Finance and Banking Durham University, 28 July 2006 Rifki Ismal Bank Indonesia

Indonesian Islamic Banking: Current Development, Policies and Prospect Paper Presented in Summer School Program in Islamic Finance and Banking Durham University, 28 July 2006 Rifki Ismal Bank Indonesia

Mr. D.A.N. EKE DEPUTY DIRECTOR

AN OVER-VIEW OF CBN NON-INTEREST (ISLAMIC) BANKING FRAMEWORK Mr. D.A.N. EKE DEPUTY DIRECTOR BANKING SUPERVISION DEPARTMENT 29 TH JULY, 2009 Central Bank of Nigeria 1 Outline Central Bank of Nigeria 1.

AN OVER-VIEW OF CBN NON-INTEREST (ISLAMIC) BANKING FRAMEWORK Mr. D.A.N. EKE DEPUTY DIRECTOR BANKING SUPERVISION DEPARTMENT 29 TH JULY, 2009 Central Bank of Nigeria 1 Outline Central Bank of Nigeria 1.

Article information: Access to this document was granted through an Emerald subscription provided by Emerald Author Access

International Journal of Islamic and Middle Eastern Finance and Management Emerald Article: Formulating withdrawal risk and bankruptcy risk in Islamic banking Rifki Ismal Article information: To cite this

International Journal of Islamic and Middle Eastern Finance and Management Emerald Article: Formulating withdrawal risk and bankruptcy risk in Islamic banking Rifki Ismal Article information: To cite this

MUDARABAH Mudarabah: Investment Financing How does Mudarabah work as an Islamic mode of financing? A Mudarabah agreement creates a partnership business whereby an investing partner (rab al maal) brings

MUDARABAH Mudarabah: Investment Financing How does Mudarabah work as an Islamic mode of financing? A Mudarabah agreement creates a partnership business whereby an investing partner (rab al maal) brings

IFSB Standards for Institution Offering Islamic Financial Services (IIFS)

") Islamic Financial Services Board IFSB Standards for Institution Offering Islamic Financial Services (IIFS) Lecture in the IRTI DL Course 26 April 2011 Abdullah Haron Assistant Secretary General 1 About

Islamic Financial Services Board IFSB Standards for Institution Offering Islamic Financial Services (IIFS) Lecture in the IRTI DL Course 26 April 2011 Abdullah Haron Assistant Secretary General 1 About

Humanomics An optimal risk return portfolio of Islamic banks Rifki Ismal

Humanomics An optimal risk return portfolio of Islamic banks Rifki Ismal Article information: To cite this document: Rifki Ismal, (2014),"An optimal risk return portfolio of Islamic banks", Humanomics,

Humanomics An optimal risk return portfolio of Islamic banks Rifki Ismal Article information: To cite this document: Rifki Ismal, (2014),"An optimal risk return portfolio of Islamic banks", Humanomics,

IMPORTANT/DISCLAIMER THIS IS AN INVESTMENT ACCOUNT PRODUCT THAT IS TIED TO THE PERFORMANCE OF THE UNDERLYING ASSETS, AND IS NOT A DEPOSIT PRODUCT

IMPORTANT/DISCLAIMER THIS IS AN INVESTMENT ACCOUNT PRODUCT THAT IS TIED TO THE PERFORMANCE OF THE UNDERLYING ASSETS, AND IS NOT A DEPOSIT PRODUCT PRODUCT DISCLOSURE SHEET (Please read and understand this

IMPORTANT/DISCLAIMER THIS IS AN INVESTMENT ACCOUNT PRODUCT THAT IS TIED TO THE PERFORMANCE OF THE UNDERLYING ASSETS, AND IS NOT A DEPOSIT PRODUCT PRODUCT DISCLOSURE SHEET (Please read and understand this

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

FINANCIAL INSTITUTIONS

FINANCIAL INSTITUTIONS OVERVIEW 1. Islamic banking is not a negligible or merely transient phenomenon. Islamic financial institutions are here to stay and there are signs that they will continue to grow

FINANCIAL INSTITUTIONS OVERVIEW 1. Islamic banking is not a negligible or merely transient phenomenon. Islamic financial institutions are here to stay and there are signs that they will continue to grow

Capital Adequacy, Liquidity, and Risk: Is Islamic Banking Too Expensive? Camille Paldi 1

Journal of Finance and Bank Management June 2014, Vol. 2, No. 2, pp. 173-177 ISSN: 2333-6064 (Print) 2333-6072 (Online) Copyright The Author(s). 2014. All Rights Reserved. Published by American Research

Journal of Finance and Bank Management June 2014, Vol. 2, No. 2, pp. 173-177 ISSN: 2333-6064 (Print) 2333-6072 (Online) Copyright The Author(s). 2014. All Rights Reserved. Published by American Research

Dr. Mohamed Damak Senior Director Global Head of Islamic Finance Copyright 2017 by S&P Global. All rights reserved.

Sharia Compliance and Fiduciary Ratings Dr. Mohamed Damak Senior Director Global Head of Islamic Finance Copyright 2017 by S&P Global. All rights reserved. Agenda 1- S&P Credit Ratings 2- Fiduciary Ratings:

Sharia Compliance and Fiduciary Ratings Dr. Mohamed Damak Senior Director Global Head of Islamic Finance Copyright 2017 by S&P Global. All rights reserved. Agenda 1- S&P Credit Ratings 2- Fiduciary Ratings:

Investment Account. Issued on: 10 October 2017 BNM/RH/PD

Investment Account Applicable to: 1. Licensed Islamic banks 2. Licensed banks and licensed investment banks approved to carry on Islamic banking business 3. Prescribed institutions approved to carry on

Investment Account Applicable to: 1. Licensed Islamic banks 2. Licensed banks and licensed investment banks approved to carry on Islamic banking business 3. Prescribed institutions approved to carry on

Title Guidelines on the Recognition and Measurement of Profit Sharing Investment Account as Risk Absorbent

Title Guidelines on the Recognition and Investment Account as Risk Effective Date The framework was first issued and came into effect on 1 January 2008. The revised framework becomes effective on financial

Title Guidelines on the Recognition and Investment Account as Risk Effective Date The framework was first issued and came into effect on 1 January 2008. The revised framework becomes effective on financial

Islamic Financial Services Board (IFSB)

") Islamic Financial Services Board (IFSB) Mutual Insurance and Takāful in a Changing World 12-13 November 2012 27-28 Zulhijjah 1433 Ceylan Intercontinental Hotel Istanbul, Turkey www.ifsb.org AGENDA About

Islamic Financial Services Board (IFSB) Mutual Insurance and Takāful in a Changing World 12-13 November 2012 27-28 Zulhijjah 1433 Ceylan Intercontinental Hotel Istanbul, Turkey www.ifsb.org AGENDA About

Building an Effective Islamic Financial System

Building an Effective Islamic Financial System Dr. Shamshad Akhtar Governor, State Bank of Pakistan Global Islamic Financial Forum Governor s: Financial Regulators Forum in Islamic Finance Kuala Lumpur,

Building an Effective Islamic Financial System Dr. Shamshad Akhtar Governor, State Bank of Pakistan Global Islamic Financial Forum Governor s: Financial Regulators Forum in Islamic Finance Kuala Lumpur,

There has been large-scale growth in Islamic finance and banking in the last twenty five years.

RISK MANAGEMENT IN MUDHARABAH AND MUSHARAKAH FINANCING OF ISLAMIC BANKS 1 Irawan Febianto Lecturer and Researcher Laboratory Management Faculty of Economics (LMFE), University of Padjadjaran E-mail: i_febianto@yahoo.com

RISK MANAGEMENT IN MUDHARABAH AND MUSHARAKAH FINANCING OF ISLAMIC BANKS 1 Irawan Febianto Lecturer and Researcher Laboratory Management Faculty of Economics (LMFE), University of Padjadjaran E-mail: i_febianto@yahoo.com

Shariah Guidelines for Sukuk. Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010 Risk Management and Disclosure in Takaful Practices Dawood Y Taylor Senior Regional Executive-Takaful, Middle East Prudential Corporation

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010 Risk Management and Disclosure in Takaful Practices Dawood Y Taylor Senior Regional Executive-Takaful, Middle East Prudential Corporation

Preamble. The purpose of this Policy is to protect NIB s reputation and promote a transparent business practice.

Integrity Due Diligence Policy Approved by the Board of Directors on 8 March 2018 with entry into force on 1 May 2018 Preamble NIB follows international standards and good practices regarding know-your-customer

Integrity Due Diligence Policy Approved by the Board of Directors on 8 March 2018 with entry into force on 1 May 2018 Preamble NIB follows international standards and good practices regarding know-your-customer

Operational Guidance Memorandum For International Islamic Financial Market (IIFM) Interbank Unrestricted Master Investment Wakalah Agreement

Interbank Unrestricted Master Investment Wakalah Agreement") Operational Guidance Memorandum For International Islamic Financial Market (IIFM) Interbank Unrestricted Master Investment Wakalah Agreement Disclaimer The contents of these Guidelines do not constitute

Operational Guidance Memorandum For International Islamic Financial Market (IIFM) Interbank Unrestricted Master Investment Wakalah Agreement Disclaimer The contents of these Guidelines do not constitute

PART B: PROFIT EQUALISATION RESERVE FRAMEWORK...4

Takaful Department PART A: INTRODUCTION...1 OVERVIEW...1 Purpose...1 Applicability...3 Effective Date/Implementation Date...3 PART B: PROFIT EQUALISATION RESERVE FRAMEWORK...4 POLICY REQUIREMENTS...4 Operating

Takaful Department PART A: INTRODUCTION...1 OVERVIEW...1 Purpose...1 Applicability...3 Effective Date/Implementation Date...3 PART B: PROFIT EQUALISATION RESERVE FRAMEWORK...4 POLICY REQUIREMENTS...4 Operating

DEBT POLICY Last Revised October 11, 2013 Last Reviewed October 7, 2016

INTRODUCTION AND PURPOSE This Debt Policy Statement serves to articulate Puget Sound s philosophy regarding debt and to establish a framework to help guide decisions regarding the use and management of

INTRODUCTION AND PURPOSE This Debt Policy Statement serves to articulate Puget Sound s philosophy regarding debt and to establish a framework to help guide decisions regarding the use and management of

Islamic Banking and Shock Absorbers

Islamic Banking and Shock Absorbers Prepared by Faisal Alqahtani PhD Seminar, Oyster Inn, Waiheke Island 1. Introduction In recent years especially after the Global Financial Crisis (GFC), the need for

Islamic Banking and Shock Absorbers Prepared by Faisal Alqahtani PhD Seminar, Oyster Inn, Waiheke Island 1. Introduction In recent years especially after the Global Financial Crisis (GFC), the need for

REGULATORY APPROACHES TO MONITORING LIQUIDITY MANAGEMENT IN ISLAMIC FINANCIAL SERVICES INDUSTRY

REGULATORY APPROACHES TO MONITORING LIQUIDITY MANAGEMENT IN ISLAMIC FINANCIAL SERVICES INDUSTRY PRESENTED AT: Conrad Istanbul Hotel, Istanbul, Turkey 6-7 April 2011 Seminar on Managing Liquidity in the

REGULATORY APPROACHES TO MONITORING LIQUIDITY MANAGEMENT IN ISLAMIC FINANCIAL SERVICES INDUSTRY PRESENTED AT: Conrad Istanbul Hotel, Istanbul, Turkey 6-7 April 2011 Seminar on Managing Liquidity in the

MCMA Enhancing Liquidity Management

IIFM Seminar on Islamic Financial Markets Monday, 1 st December 2014, Manama Ismail Dadabhoy Advisor - IIFM MCMA Enhancing Liquidity Management Murabahah transaction with the benefit of : 1 1 Purpose of

IIFM Seminar on Islamic Financial Markets Monday, 1 st December 2014, Manama Ismail Dadabhoy Advisor - IIFM MCMA Enhancing Liquidity Management Murabahah transaction with the benefit of : 1 1 Purpose of

Risk Concentrations Principles

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Risk Concentrations Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS Basel December

Profit-sharing investment accounts in Islamic banks: Regulatory problems and possible solutions

Original Article Profit-sharing investment accounts in Islamic banks: Regulatory problems and possible solutions Simon Archer is Visiting Professor at the ICMA Centre, Henley Business School, University

Original Article Profit-sharing investment accounts in Islamic banks: Regulatory problems and possible solutions Simon Archer is Visiting Professor at the ICMA Centre, Henley Business School, University

The Recent Turmoil and Monetary Policy in a Dual Financial System with Islamic Perspective

The Recent Turmoil and Monetary Policy in a Dual Financial System with Islamic Perspective Prof. Dr. Zubair Hasan The financial turmoil that the 2007 subprime debacle of the US set into motion has raised

The Recent Turmoil and Monetary Policy in a Dual Financial System with Islamic Perspective Prof. Dr. Zubair Hasan The financial turmoil that the 2007 subprime debacle of the US set into motion has raised

THE PRACTICAL MODEL OF HEDGING IN ISLAMIC FINANCIAL MARKETS

International Journal of Economics, Commerce and Management United Kingdom Vol. VI, Issue 6, June 2018 http://ijecm.co.uk/ ISSN 2348 0386 THE PRACTICAL MODEL OF HEDGING IN ISLAMIC FINANCIAL MARKETS Ehab

International Journal of Economics, Commerce and Management United Kingdom Vol. VI, Issue 6, June 2018 http://ijecm.co.uk/ ISSN 2348 0386 THE PRACTICAL MODEL OF HEDGING IN ISLAMIC FINANCIAL MARKETS Ehab

Diversity of Islamic financial instruments

ISWGNA Task Force on Islamic Banking Classification of property income associated with Islamic financial services Russell Krueger Economic and Social Commission for Western Asia (ESCWA) Beirut October

ISWGNA Task Force on Islamic Banking Classification of property income associated with Islamic financial services Russell Krueger Economic and Social Commission for Western Asia (ESCWA) Beirut October

MURABAHA Definition Of Murabaha What is a Murabaha? A Murabaha is a sale transaction where the cost of acquiring the asset and the profit to be added are disclosed to the client. The buying client typically

MURABAHA Definition Of Murabaha What is a Murabaha? A Murabaha is a sale transaction where the cost of acquiring the asset and the profit to be added are disclosed to the client. The buying client typically

Islamic Repo & Collateralization Possibilities and the Role of Sukuk

Islamic Repo & Collateralization Possibilities and the Role of Sukuk Euroclear Treasury & Collateral Management Conference Thursday, 11 th February 2010 Emirates Palace, Abu Dhabi Mr. Ijlal Ahmed Alvi

Islamic Repo & Collateralization Possibilities and the Role of Sukuk Euroclear Treasury & Collateral Management Conference Thursday, 11 th February 2010 Emirates Palace, Abu Dhabi Mr. Ijlal Ahmed Alvi

IFSB Standards Comparison to Basel II: Capital Adequacy

IFSB Standards Comparison to Basel II: Capital Adequacy IFSB Forum The European Challenge Frankfurt-am-Main 5-6 December 2007 Simon Archer Consultant, IFSB Session Outline Common features of Basel II Pillar

IFSB Standards Comparison to Basel II: Capital Adequacy IFSB Forum The European Challenge Frankfurt-am-Main 5-6 December 2007 Simon Archer Consultant, IFSB Session Outline Common features of Basel II Pillar

BERMUDA MONETARY AUTHORITY THE INSURANCE CODE OF CONDUCT FEBRUARY 2010

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

MURABAHAH TAX TREATMENT IN THE INDONESIAN ISLAMIC FINANCE

MURABAHAH TAX TREATMENT IN THE INDONESIAN ISLAMIC FINANCE Associate Professor Rifki Ismal & Dece Kurniadi, MM Central Bank of Indonesia International Center for Development in Islamic Finance Lembaga Pengembangan

MURABAHAH TAX TREATMENT IN THE INDONESIAN ISLAMIC FINANCE Associate Professor Rifki Ismal & Dece Kurniadi, MM Central Bank of Indonesia International Center for Development in Islamic Finance Lembaga Pengembangan

Frequently Asked Question (FAQ) on Investment Account Last updated: 14 July 2016

on Investment Account Last updated: 14 July 2016") Frequently Asked Question (FAQ) on Investment Account Last updated: 14 July 2016 This document supplements the policy document on Investment Account (IAF) by addressing common and potential implementation

Frequently Asked Question (FAQ) on Investment Account Last updated: 14 July 2016 This document supplements the policy document on Investment Account (IAF) by addressing common and potential implementation

The impact of the financial crisis on Islamic finance Clare College, Cambridge

The impact of the financial crisis on Islamic finance Clare College, Cambridge Simon Gray Director, Supervision 31 st August 2010 Agenda Whirlwind tour of world developments Developments in international

The impact of the financial crisis on Islamic finance Clare College, Cambridge Simon Gray Director, Supervision 31 st August 2010 Agenda Whirlwind tour of world developments Developments in international

Securitization. Management exercises authority that should rest with the board or engages in activities that expose the institution to excessive risk.

Securitization Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

Securitization Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

METHODOLOGY FOR FIDUCIARY RATINGS

METHODOLOGY FOR FIDUCIARY RATINGS Fiduciary Rating Methodology METHODOLOGY FOR FIDUCIARY RATINGS Preamble The evolution of Islamic Finance as a parallel to conventional finance has gained significant

METHODOLOGY FOR FIDUCIARY RATINGS Fiduciary Rating Methodology METHODOLOGY FOR FIDUCIARY RATINGS Preamble The evolution of Islamic Finance as a parallel to conventional finance has gained significant

RISK AND CAPITAL MANAGEMENT DISCLOSURES (BASEL II - PILLAR III) RISK AND CAPITAL MANAGEMENT DISCLOSURES (BASEL II - PILLAR III) Contents

RISK AND CAPITAL MANAGEMENT DISCLOSURES (BASEL II - PILLAR III) Contents") RISK AND CAPITAL MANAGEMENT DISCLOSURES Contents 1 Introduction 78 2 Executive summary 78 3 Group Structure 78 4 Risk management framework 79 4.1 Risks In Pillar I 79 4.1.1 Credit Risk 80 4.1.2 Market

RISK AND CAPITAL MANAGEMENT DISCLOSURES Contents 1 Introduction 78 2 Executive summary 78 3 Group Structure 78 4 Risk management framework 79 4.1 Risks In Pillar I 79 4.1.1 Credit Risk 80 4.1.2 Market

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017 Significance of Capital Adequacy Capital is the foundation of any business.

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017 Significance of Capital Adequacy Capital is the foundation of any business.

SNA/M1.18/6.a. 12 th Meeting of the Advisory Expert Group on National Accounts, November 2018, Luxembourg. Agenda item: 6.a.

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

The DFSA Rulebook. Islamic Finance Rules (IFR) IFR/VER3/

IFR/VER3/") The DFSA Rulebook Islamic Finance Rules (IFR) IFR/VER3/02-11 060 Contents The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION...1 1.1 Application...

The DFSA Rulebook Islamic Finance Rules (IFR) IFR/VER3/02-11 060 Contents The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION...1 1.1 Application...

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

Sukuk: Definition, Structure and Accounting Issues

MPRA Munich Personal RePEc Archive Sukuk: Definition, Structure and Accounting Issues Khalil Ahmed USIM 2011 Online at http://mpra.ub.uni-muenchen.de/33675/ MPRA Paper No. 33675, posted 25. September 2011

MPRA Munich Personal RePEc Archive Sukuk: Definition, Structure and Accounting Issues Khalil Ahmed USIM 2011 Online at http://mpra.ub.uni-muenchen.de/33675/ MPRA Paper No. 33675, posted 25. September 2011

A cross sectoral approach to the supervision of Islamic Financial Services: the IOSCO view

A cross sectoral approach to the supervision of Islamic Financial Services: the IOSCO view Philippe Richard, IOSCO Secretary General Introduction IOSCO is the global standard setter for securities regulation,

A cross sectoral approach to the supervision of Islamic Financial Services: the IOSCO view Philippe Richard, IOSCO Secretary General Introduction IOSCO is the global standard setter for securities regulation,

Statement of Investment Policy. Amended December 4, 2017

Statement of Investment Policy Amended December 4, 2017 Table of Contents 1. Introduction... 1 2. Purposes of the Statement of Investment Policy... 1 3. Mission Statement... 2 4. Roles and Responsibilities...

Statement of Investment Policy Amended December 4, 2017 Table of Contents 1. Introduction... 1 2. Purposes of the Statement of Investment Policy... 1 3. Mission Statement... 2 4. Roles and Responsibilities...

CBK-IIFM Seminar on Islamic Hedging, Liquidity Management and Sukūk

CBK-IIFM Seminar on Islamic Hedging, Liquidity Management and Sukūk RISK MANAGEMENT IN ISLAMIC BANKS: THE CBK S REGULATORY APPROACH FOR ISLAMIC HEDGING, LIQUIDITY MANAGEMENT AND SUKŪK Session 1: Risk Management

CBK-IIFM Seminar on Islamic Hedging, Liquidity Management and Sukūk RISK MANAGEMENT IN ISLAMIC BANKS: THE CBK S REGULATORY APPROACH FOR ISLAMIC HEDGING, LIQUIDITY MANAGEMENT AND SUKŪK Session 1: Risk Management

Summary Enterprise Risk Management Framework

Summary Enterprise Risk Management Framework Last Updated: September 26, 2016 CONTENTS I. Overview II. III. Risk Management Philosophy General Risk Management Activities Board of Directors Risk Management

Summary Enterprise Risk Management Framework Last Updated: September 26, 2016 CONTENTS I. Overview II. III. Risk Management Philosophy General Risk Management Activities Board of Directors Risk Management

REGULATION. on Internal Governance Arrangements, the Management body and the Internal Capital Adequacy Assessment Process for Banks and Savings banks

Pursuant to point 1 of Article 58 and points 1, 2 and 3 of Article 135 of the Banking Act (Official Gazette of the Republic of Slovenia, No. 25/15; hereinafter: the ZBan-2) and the second paragraph of

Pursuant to point 1 of Article 58 and points 1, 2 and 3 of Article 135 of the Banking Act (Official Gazette of the Republic of Slovenia, No. 25/15; hereinafter: the ZBan-2) and the second paragraph of

RISK MANAGEMENT ASSESSMENT SYSTEMS: AN APPLICATION TO ISLAMIC BANKS

RISK MANAGEMENT ASSESSMENT SYSTEMS: AN APPLICATION TO ISLAMIC BANKS Abstract HABIB AHMED Risk management is central in operations of financial institutions, both from business and regulatory perspectives.

RISK MANAGEMENT ASSESSMENT SYSTEMS: AN APPLICATION TO ISLAMIC BANKS Abstract HABIB AHMED Risk management is central in operations of financial institutions, both from business and regulatory perspectives.

Kenya Gazette Supplement No. 42 3rd April, (Legislative Supplement No. 19)

") SPECIAL ISSUE 169 Kenya Gazette Supplement No. 42 3rd April, 2017 LEGAL NOTICE NO. 45 (Legislative Supplement No. 19) THE INSURANCE ACT (Cap. 487) THE INSURANCE (INVESTMENTS MANAGEMENT) GUIDELINES, 2017

SPECIAL ISSUE 169 Kenya Gazette Supplement No. 42 3rd April, 2017 LEGAL NOTICE NO. 45 (Legislative Supplement No. 19) THE INSURANCE ACT (Cap. 487) THE INSURANCE (INVESTMENTS MANAGEMENT) GUIDELINES, 2017

Chapter 5: Summary and Conclusion

Chapter 5: Summary and Conclusion 5.1 Introduction This chapter comprises of five sections. A summary of findings is provided under-section 5.2. It highlights the issues and challenges in introducing Islamic

Chapter 5: Summary and Conclusion 5.1 Introduction This chapter comprises of five sections. A summary of findings is provided under-section 5.2. It highlights the issues and challenges in introducing Islamic

Legal Aspects of Islamic Finance LCA4592 DR. ZULKIFLI HASAN

Legal Aspects of Islamic Finance LCA4592 DR. ZULKIFLI HASAN 1 Legal Systems CONTENTS Rationale for regulations Legal framework Regulatory and Supervisory Authorities International Standard Setting Agencies

Legal Aspects of Islamic Finance LCA4592 DR. ZULKIFLI HASAN 1 Legal Systems CONTENTS Rationale for regulations Legal framework Regulatory and Supervisory Authorities International Standard Setting Agencies

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment Keynote address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the State Street Islamic

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment Keynote address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the State Street Islamic

Shariah Governance and Regulatory Aspects of Takaful

1 Shariah Governance and Regulatory Aspects of Takaful Introduction Kazi Md. Mortuza Ali Chief Consultant to the Board Prime Islami Life Insurance Ltd Every takaful scheme is and intended to be a legally

1 Shariah Governance and Regulatory Aspects of Takaful Introduction Kazi Md. Mortuza Ali Chief Consultant to the Board Prime Islami Life Insurance Ltd Every takaful scheme is and intended to be a legally

APPENDIX A SAMPLE. (name of organization) STATEMENT OF INVESTMENT POLICY, OBJECTIVES, AND GUIDELINES. ADOPTED: (date)

STATEMENT OF INVESTMENT POLICY, OBJECTIVES, AND GUIDELINES. ADOPTED: (date)") APPENDIX A SAMPLE (name of organization) STATEMENT OF INVESTMENT POLICY, OBJECTIVES, AND GUIDELINES ADOPTED: (date) THEOLOGICAL STATEMENT The biblical imperative of the stewardship of all that God has

APPENDIX A SAMPLE (name of organization) STATEMENT OF INVESTMENT POLICY, OBJECTIVES, AND GUIDELINES ADOPTED: (date) THEOLOGICAL STATEMENT The biblical imperative of the stewardship of all that God has

Risk Management Practices in the Republic of Yemen: Are Islamic banks different?

Risk Management Practices in the Republic of Yemen: Are Islamic banks different? Hussein A. Abdou 1 Omar A. Muslem 2 Rifki Ismal 3 Abstract The main aims of this paper are, firstly, to investigate the

Risk Management Practices in the Republic of Yemen: Are Islamic banks different? Hussein A. Abdou 1 Omar A. Muslem 2 Rifki Ismal 3 Abstract The main aims of this paper are, firstly, to investigate the

Note on the Strategic Development of an Enhanced Bank Resolution Framework for Ukraine in Alignment with the EU Acquis March 2019

Note on the Strategic Development of an Enhanced Bank Resolution Framework for Ukraine in Alignment with the EU Acquis March 2019 Disclaimer: This summary is based on discussions held in a Working Group

Note on the Strategic Development of an Enhanced Bank Resolution Framework for Ukraine in Alignment with the EU Acquis March 2019 Disclaimer: This summary is based on discussions held in a Working Group

International Islamic Liquidity Management Corporation

International Islamic Liquidity Management Corporation An Overview of Liquidity Management Issues for Institutions Offering Islamic Financial Services March 9 th, 2016/ Jumada Al- Awwal 29, 1437 IRTI Eminent

International Islamic Liquidity Management Corporation An Overview of Liquidity Management Issues for Institutions Offering Islamic Financial Services March 9 th, 2016/ Jumada Al- Awwal 29, 1437 IRTI Eminent

DEPOSITOR S BEHAVIOR AND ECONOMIC CONDITION LEADING TO LIQUIDITY RISK PROBLEM IN ISLAMIC BANKING INDUSTRY

1 DEPOSITOR S BEHAVIOR AND ECONOMIC CONDITION LEADING TO LIQUIDITY RISK PROBLEM IN ISLAMIC BANKING INDUSTRY (Indonesian Case : 2001 2007) Rifki Ismal Durham University School of Government and International

1 DEPOSITOR S BEHAVIOR AND ECONOMIC CONDITION LEADING TO LIQUIDITY RISK PROBLEM IN ISLAMIC BANKING INDUSTRY (Indonesian Case : 2001 2007) Rifki Ismal Durham University School of Government and International

Investment Policy Statement For Montana Community Foundation MCF Investment Portfolio

Statement For Montana Community Foundation MCF Investment Portfolio Revised: October 2007 Revised: March 2011 Revised: November 2015 Table of Contents I. Introduction...2 PURPOSE OF THIS POLICY STATEMENT...

Statement For Montana Community Foundation MCF Investment Portfolio Revised: October 2007 Revised: March 2011 Revised: November 2015 Table of Contents I. Introduction...2 PURPOSE OF THIS POLICY STATEMENT...

RISK MANAGEMENT RISK MANAGEMENT GOVERNANCE

39 RISK MANAGEMENT The Bank has been guided by its risk management principles in managing its business risk, which outline a basis for an integrated risk management effort and good corporate governance.

39 RISK MANAGEMENT The Bank has been guided by its risk management principles in managing its business risk, which outline a basis for an integrated risk management effort and good corporate governance.

Derivatives Sound Practices for Federally Regulated Private Pension Plans

Guideline Subject: for Federally Regulated Private Pension Plans Date: Introduction This Guideline outlines the factors that the Office of the Superintendent of Financial Institutions (OSFI) expects administrators

Guideline Subject: for Federally Regulated Private Pension Plans Date: Introduction This Guideline outlines the factors that the Office of the Superintendent of Financial Institutions (OSFI) expects administrators

SFAS 28 SFAS 28 Statement of Statement of Financial Accounting Standards No.28 Financial Accounting Standards No. 28

Statement of Financial Accounting Standards No. 28 Statement of Financial Accounting Standards No.28 Disclosures in the Financial Statements of Banks Revised on 22 September 2005 Translated by Robert K.

Statement of Financial Accounting Standards No. 28 Statement of Financial Accounting Standards No.28 Disclosures in the Financial Statements of Banks Revised on 22 September 2005 Translated by Robert K.

REGULATION ON THE LIQUIDITY RISK MANAGEMENT CHAPTER I GENERAL PROVISION. Article 1 Purpose and Scope

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010), and Articles 19 and 85 of the

Pursuant to Article 35, paragraph 1.1 of the Law No. 03/L-209 on Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No.77 / 16 August 2010), and Articles 19 and 85 of the

BANK INDONESIA REGULATION NUMBER 11/33/PBI/2009 CONCERNING

REGULATION NUMBER 11/33/PBI/2009 CONCERNING THE IMPLEMENTATION OF GOOD CORPORATE GOVERNANCE BY ISLAMIC COMMERCIAL BANKS AND ISLAMIC BUSINESS UNITS BY THE GRACE OF THE ALMIGHTY GOD, THE GOVERNOR OF, Considering:

REGULATION NUMBER 11/33/PBI/2009 CONCERNING THE IMPLEMENTATION OF GOOD CORPORATE GOVERNANCE BY ISLAMIC COMMERCIAL BANKS AND ISLAMIC BUSINESS UNITS BY THE GRACE OF THE ALMIGHTY GOD, THE GOVERNOR OF, Considering:

Financial Services Agency

Guideline for Financial Conglomerates Supervision March 2007 Financial Services Agency Guideline for Financial Conglomerates Supervision I Basic Concepts concerning Financial

Guideline for Financial Conglomerates Supervision March 2007 Financial Services Agency Guideline for Financial Conglomerates Supervision I Basic Concepts concerning Financial

Swap Markets CHAPTER OBJECTIVES. The specific objectives of this chapter are to: describe the types of interest rate swaps that are available,

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

Islamic Finance as a Means of Shaping the Future of Sustainable Finance

Islamic Finance as a Means of Shaping the Future of Sustainable Finance Can Mehmet International University of Sarajevo Hrasnička Cesta 1, 71210 Ilidža/Sarajevo,Bosnia and Herzegovina mcan@ius.edu.ba Abstract

Islamic Finance as a Means of Shaping the Future of Sustainable Finance Can Mehmet International University of Sarajevo Hrasnička Cesta 1, 71210 Ilidža/Sarajevo,Bosnia and Herzegovina mcan@ius.edu.ba Abstract

Prudential sourcebook for Banks, Building Societies and Investment Firms. Chapter 5. Credit risk mitigation

Prudential sourcebook for Banks, Building Societies and Investment Firms Chapter Credit risk mitigation BIPU : Credit risk mitigation Section.1 : Application and purpose.1 Application and purpose.1.1 Application

Prudential sourcebook for Banks, Building Societies and Investment Firms Chapter Credit risk mitigation BIPU : Credit risk mitigation Section.1 : Application and purpose.1 Application and purpose.1.1 Application

INVESTMENT MANAGEMENT GUIDELINE

INVESTMENT MANAGEMENT GUIDELINE August 2010 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Sound and prudent investment management... 7 2. General

INVESTMENT MANAGEMENT GUIDELINE August 2010 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Sound and prudent investment management... 7 2. General

Developing Islamic Finance Secondary Markets

Developing Islamic Finance Secondary Markets By Ahmed Ali Siddiqui Vice President & Manager, Product Development & Shariah Compliance (PDSC) Meezan Bank Limited 2 nd IIFM Conference - June 18, 2007 Islamic

Developing Islamic Finance Secondary Markets By Ahmed Ali Siddiqui Vice President & Manager, Product Development & Shariah Compliance (PDSC) Meezan Bank Limited 2 nd IIFM Conference - June 18, 2007 Islamic

OECD guidelines for pension fund governance

DIRECTORATE FOR FINANCIAL AND ENTERPRISE AFFAIRS OECD guidelines for pension fund governance RECOMMENDATION OF THE COUNCIL These guidelines, prepared by the OECD Insurance and Private Pensions Committee

DIRECTORATE FOR FINANCIAL AND ENTERPRISE AFFAIRS OECD guidelines for pension fund governance RECOMMENDATION OF THE COUNCIL These guidelines, prepared by the OECD Insurance and Private Pensions Committee

Wakala Treasury Deposit Account. Special conditions. alrayanbank.co.uk

Wakala Treasury Deposit Account Special conditions alrayanbank.co.uk Contents Sections A Words with special meanings 3 Section B The Wakala Treasury Deposit Account 6 Operation of your account 6 Procedures

Wakala Treasury Deposit Account Special conditions alrayanbank.co.uk Contents Sections A Words with special meanings 3 Section B The Wakala Treasury Deposit Account 6 Operation of your account 6 Procedures

Corporate Governance Guideline

Office of the Superintendent of Financial Institutions Canada Bureau du surintendant des institutions financières Canada Corporate Governance Guideline January 2003 EFFECTIVE CORPORATE GOVERNANCE IN FEDERALLY

Office of the Superintendent of Financial Institutions Canada Bureau du surintendant des institutions financières Canada Corporate Governance Guideline January 2003 EFFECTIVE CORPORATE GOVERNANCE IN FEDERALLY

GUIDELINE ON ENTERPRISE RISK MANAGEMENT

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

Gotham Absolute Return Fund. Institutional Class GARIX. Gotham Enhanced Return Fund. Institutional Class GENIX. Gotham Neutral Fund

Gotham Absolute Return Fund Institutional Class GARIX Gotham Enhanced Return Fund Institutional Class GENIX Gotham Neutral Fund Institutional Class GONIX Gotham Index Plus Fund Institutional Class GINDX

Gotham Absolute Return Fund Institutional Class GARIX Gotham Enhanced Return Fund Institutional Class GENIX Gotham Neutral Fund Institutional Class GONIX Gotham Index Plus Fund Institutional Class GINDX

Financial Risk Management

132ANNALS OF THE UNIVERSITY OF CRAIOVA ECONOMIC SCIENCES Year XXXXI No. 39 2011 Financial Risk Management Catalin-Florinel Stanescu Ph.D. Student University of Craiova Faculty of Economics and Business

132ANNALS OF THE UNIVERSITY OF CRAIOVA ECONOMIC SCIENCES Year XXXXI No. 39 2011 Financial Risk Management Catalin-Florinel Stanescu Ph.D. Student University of Craiova Faculty of Economics and Business

Intra-Group Transactions and Exposures Principles

Intra-Group Transactions and Exposures Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Intra-Group Transactions and Exposures Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Ajman Bank PJSC and its Subsidiaries. Consolidated financial statements For the year ended 31 December 2014

Consolidated financial statements For the year ended 31 December 2014 Consolidated financial statements For the year ended 31 December 2014 Contents Page Directors report 1 Independent auditors report

Consolidated financial statements For the year ended 31 December 2014 Consolidated financial statements For the year ended 31 December 2014 Contents Page Directors report 1 Independent auditors report

Basel Committee on Banking Supervision. Consultative Document. Pillar 2 (Supervisory Review Process)

") Basel Committee on Banking Supervision Consultative Document Pillar 2 (Supervisory Review Process) Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Table

Basel Committee on Banking Supervision Consultative Document Pillar 2 (Supervisory Review Process) Supporting Document to the New Basel Capital Accord Issued for comment by 31 May 2001 January 2001 Table

SNA Treatment of Islamic Windows of Conventional Banks

SNA Treatment of Islamic Windows of Conventional Banks 2 August 2017 Windows - UNSD A significant complication in the SNA treatment of Islamic finance is the treatment of Islamic windows, which are Islamic

SNA Treatment of Islamic Windows of Conventional Banks 2 August 2017 Windows - UNSD A significant complication in the SNA treatment of Islamic finance is the treatment of Islamic windows, which are Islamic

M.S. HOWELLS & CO. NOTES TO FINANCIAL STATEMENTS

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Organization and Business M.S. Howells & Co. (the Company ) was incorporated in Delaware on April 11, 2000, and is a securities broker-dealer serving primarily

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Organization and Business M.S. Howells & Co. (the Company ) was incorporated in Delaware on April 11, 2000, and is a securities broker-dealer serving primarily

INTEGRATED RISK MANAGEMENT GUIDELINE

INTEGRATED RISK MANAGEMENT GUIDELINE Initial publication: April 2009 Updated: May 2015 TABLE OF CONTENTS Preamble... ii Scope... iii Coming into effect and updating... iv Introduction... v 1. Integrated

INTEGRATED RISK MANAGEMENT GUIDELINE Initial publication: April 2009 Updated: May 2015 TABLE OF CONTENTS Preamble... ii Scope... iii Coming into effect and updating... iv Introduction... v 1. Integrated

Islamic Instruments for Asset Management IDB/IRTI DL Program April 12th, 2011 Tehran, Iran

بسم االله الر حمن الر حيم 13th Distance Learning Course: Spring 2011 An Intermediate Course in Islamic Finance Islamic Instruments for Asset Management IDB/IRTI DL Program April 12th, 2011 Tehran, Iran

بسم االله الر حمن الر حيم 13th Distance Learning Course: Spring 2011 An Intermediate Course in Islamic Finance Islamic Instruments for Asset Management IDB/IRTI DL Program April 12th, 2011 Tehran, Iran