Subawards and Indirect Costs: A Speedy Overview

|

|

|

- Allyson Butler

- 6 years ago

- Views:

Transcription

1 Subawards and Indirect Costs: A Speedy Overview Theresa Saunders-Landreth Subaward Specialist Sponsored Projects Office RAC Forum May 10, 2017

2 The Questions: The Subaward Team has been getting questions from PIs and RAs regarding confusion about: UCB s vs. a Subrecipient s indirect costs UCB indirect costs charged against Subawards UCB indirect costs charged against Multi-Campus Award UCB indirect costs charged against Subrecipients vs. Vendors NIH s practice of excluding Subrecipient F&A when determining modular and prior-approval budget requirements?

3 UCB s Payment of Subrecipient Indirect Costs A Subrecipient s total costs (direct + indirect) are part of UCB s direct costs. UCB s Direct Costs IDC Sub s Total Costs UC Berkeley pays Subrecipients for their total incurred costs, including both their direct and indirect costs. Subrecipient s Personnel Subrecipient s Consultants Subrecipient s Materials/Supplies Subrecipient s Travel Subrecipient s Project Equipment Subrecipient s Other Direct Costs Subrecipient s Indirect Costs

4 UCB s Indirect vs. Subrecipient s Indirect UCB s Direct Costs Sub s Direct Costs UCB s Indirect Costs Sub s Indirect Costs

5 When Indirect Costs are Charged: UCB s Direct Costs UCB s Indirect Costs EXCEPT. Sub s Direct Costs Sub s Indirect Costs

")

6 When Indirect Costs are not Charged: Modified Total Direct Costs (MTDC) Exclusions: Project Equipment/Fabrication Capital Expenditures Patient Care Costs Student Tuition Remission UCB s Direct Costs Rent for Off-Site Facilities Scholarships and Fellowships Subaward Costs > $25,000 and all Subaward Costs to other UC Campuses MTDC exclusions are direct costs that would create inequity in the distribution of indirect costs.

AHF $10,000 57.00% $5,700 $5,700 Stanford $25,000 57.")

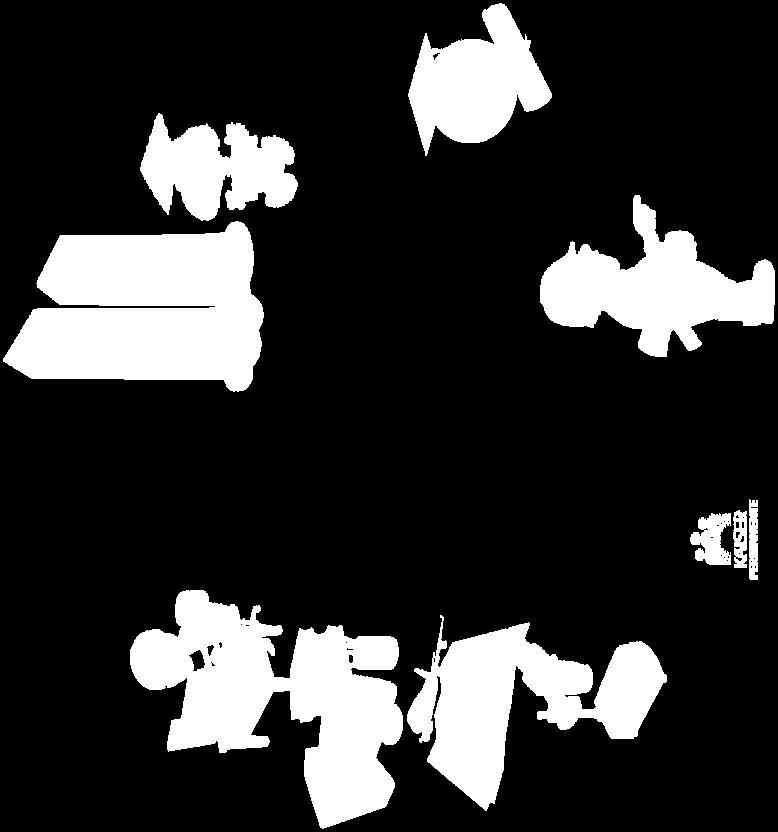

7 When Indirect Costs are not Charged: MTDC excluded costs would incur disproportionately high indirect costs, if we were to apply our indirect rate against their full direct cost. Example: Subaward Costs > $25,000 and all Subaward costs to other UCs Subaward Cost Indirect Rate Indirect Cost (Without Exclusion) Indirect Cost (With Exclusion) AHF $10, % $5,700 $5,700 Stanford $25, % $14,250 $14,250 UCSF $100, % $57,000 $0 Kaiser $500, % $285,000 $14,250 Northrup $1,000, % $570,000 $14,250 Administering an expensive Subaward, should not cost UC Berkeley more than administering a cheap Subaward.

8 Subrecipient vs. Vendor Indirect Costs Because UCB only charges indirect on the first $25,000 of each Subrecipient s total costs, it is very important to make sure that Vendors are not budgeted as Subrecipients, at the proposal stage. Example: Entity Vendor Cost Indirect Rate Budgeted as a. Indirect Cost to Project Budgeted as SSI Survey Research $75, % Vendor $42,750 (Correct) Subrecipient $14,250 (Incorrect) Ouch Factor = $28,500 Quest Diagnostics $500, % Vendor $285,000 (Correct) Subrecipient $14,250 (Incorrect) Ouch Factor = $270,750

9 Subrecipient vs. Vendor Indirect Costs Why is it important to distinguish between a Subrecipient and a Vendor? Subaward: Subrecipients are partners in our research and are involved in programmatic decision making. Subrecipients must conduct their portions of research projects in compliance with all applicable terms and conditions of the Prime Award. Subrecipient costs must be reasonable and allowable. Subrecipients retain ownership rights to patentable or copyrightable products. Vendor: Vendors are simply a for-hire entity. Vendors are not bound to the full set terms and conditions of the Prime Award. Vendors are subject to competitive bid, to assure payments do not exceed fair market value.

10 Subrecipient vs. Vendor Indirect Costs Questions to ask before including a Subrecipient, in a proposal: Do they commonly provide goods/services as their normal business? Do they provide similar goods/services to other purchasers? Are the goods/services being provided secondary to the central purpose of the project? Is their work carried out according to the UCB specifications using standard operating procedures? If yes to any of these, the entity fits the profile of a VENDOR

11 Subrecipient vs. Vendor Indirect Costs By contrast, a Subrecipient will: Conduct substantive, programmatic work, or an important or significant portion of the research. Participate in a creative way in designing and/or conducting the research. Retain some element of programmatic control and discretion over how the work is carried out. Make independent decisions regarding how to implement the requested activities. Have a PI who has been identified and functions as a Co-Investigator. Expect to retain ownership rights for patents or copyrights. Expect to co-author papers.

, or determining whether prior approval is needed to submit an application (direct costs > $500K/year). https://grants.nih.")

12 NIH and Subrecipient F&A For NIH proposals, Subrecipient F&A costs are NOT included as part of the direct cost base when determining whether an application can use the modular format (direct costs < $250K/year), or determining whether prior approval is needed to submit an application (direct costs > $500K/year). Once funding is awarded: The Sponsor will provide funding to cover the Subrecipient s indirect costs as budgeted in the proposal; and UCB is responsible for paying the Subrecipient s indirect costs, as part of UCB s direct cost line item. SPO requires a detailed Subrecipient budget for Modular grants: To check for correct F&A cost calculations; and For use as the Subaward budget, at the time of award.

13 Take-Home Summary: Direct costs are those that are completely attributable to the research. Indirect costs are those needed to provide the infrastructure for the research. Both UCB and Subrecipients have indirect costs that support the research. UCB only collects indirect costs when a researcher spends direct costs. Subrecipient indirect costs are part of UCB Direct costs, and are paid in full. UCB only collects its own indirect costs on the first $25,000 of each Subaward. UCB collects none of its own indirect costs on Subawards to other UCs. Be very careful not to budget a Vendor as a Subrecipient. SPO has fantastic resources related to indirect costs on its website:

14 Questions: Q: If a Sponsor Award allows for budgeting of indirect costs with a base of Total Direct Costs (as opposed to Modified Total Direct Costs), does UCB get to collect indirect costs on the total cost of Subawards? A: Yes. If a base of Total Direct Costs is approved by the Sponsor, then UCB and is be able to collect indirect costs on the total cost of a Subaward, not just the first $25,000. The Total Direct Cost (TDC) base includes all of the direct costs being charged to the Sponsor. Nothing is excluded from the base prior to calculating the indirect costs (F&A). This base is typically used when a Sponsor declines to pay Berkeley s federally approved indirect cost/f&a rate and an F&A waiver is granted by the University..?

The Basics of Budget Preparation. Janet Boyles Pre-Award Services Office of Sponsored Programs

The Basics of Budget Preparation Janet Boyles Pre-Award Services Office of Sponsored Programs What is a Budget? A budget is a financial proposal A budget reflects the work proposed A budget is a detailed

The Basics of Budget Preparation Janet Boyles Pre-Award Services Office of Sponsored Programs What is a Budget? A budget is a financial proposal A budget reflects the work proposed A budget is a detailed

Proposal Budget Basics

Proposal Budget Basics Include both direct and F&A costs Should be detailed Include only allowable costs If required, include matching or cost-sharing (cost sharing should only be included if required

Proposal Budget Basics Include both direct and F&A costs Should be detailed Include only allowable costs If required, include matching or cost-sharing (cost sharing should only be included if required

BASIC BUDGETING ERA ELECTIVE

BASIC BUDGETING ERA ELECTIVE Presented by: Judy Brown, Director, Office of Research Support, College of Natural Science Denise Lator, Sponsored Programs Administrator, Office of Sponsored Programs 1 AGENDA

BASIC BUDGETING ERA ELECTIVE Presented by: Judy Brown, Director, Office of Research Support, College of Natural Science Denise Lator, Sponsored Programs Administrator, Office of Sponsored Programs 1 AGENDA

Indirect Costs (Facilities and Administrative Costs or F&A)

") East Tennessee State University Policy Title: Sponsored Program Costs Issued: 4/30/14 Responsible Official: Vice Provost for Research and Sponsored Programs Responsible Office: Office of Research and Sponsored

East Tennessee State University Policy Title: Sponsored Program Costs Issued: 4/30/14 Responsible Official: Vice Provost for Research and Sponsored Programs Responsible Office: Office of Research and Sponsored

Proposal Preparation and Submission. Module 3B Facilities and Administrative Costs

Proposal Preparation and Submission Module 3B Facilities and Administrative Costs Copyright UC Regents 2008 - All Rights Reserved Welcome to Module 3B Facilities and Administrative Costs. F&A is probably

Proposal Preparation and Submission Module 3B Facilities and Administrative Costs Copyright UC Regents 2008 - All Rights Reserved Welcome to Module 3B Facilities and Administrative Costs. F&A is probably

RESEARCH ADMINISTRATORS ROUND TABLE. June 7, 2016 Health Sciences Center June 8, 2016 Brooks Hall

RESEARCH ADMINISTRATORS ROUND TABLE June 7, 2016 Health Sciences Center June 8, 2016 Brooks Hall Round Table Menu Budgeting Overview Janet Boyles Recharge Centers Jaime Bunner Sub-award Management John

RESEARCH ADMINISTRATORS ROUND TABLE June 7, 2016 Health Sciences Center June 8, 2016 Brooks Hall Round Table Menu Budgeting Overview Janet Boyles Recharge Centers Jaime Bunner Sub-award Management John

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

BUDGET BUILDING. Christy Bischoff Justin Stidham Grants & Contracts Administrators Office of Sponsored Projects

BUDGET BUILDING Christy Bischoff Justin Stidham Grants & Contracts Administrators Office of Sponsored Projects Topics Budget components: Direct vs. Indirect costs Costing principles from the Uniform Guidance

BUDGET BUILDING Christy Bischoff Justin Stidham Grants & Contracts Administrators Office of Sponsored Projects Topics Budget components: Direct vs. Indirect costs Costing principles from the Uniform Guidance

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

HOW TO PREPARE A GRANT PROPOSAL BUDGET TAMARA FRANKLIN, ASSISTANT CONTROLLER GRANTS AND CONTRACTS ACCOUNTING JANUARY 10, 2018

HOW TO PREPARE A GRANT PROPOSAL BUDGET TAMARA FRANKLIN, ASSISTANT CONTROLLER GRANTS AND CONTRACTS ACCOUNTING JANUARY 10, 2018 Gathering the information Put all of the relevant costs down on paper What

HOW TO PREPARE A GRANT PROPOSAL BUDGET TAMARA FRANKLIN, ASSISTANT CONTROLLER GRANTS AND CONTRACTS ACCOUNTING JANUARY 10, 2018 Gathering the information Put all of the relevant costs down on paper What

Facilities and Administrative Cost

Georgia Regents University Policy Library Facilities and Administrative Cost Policy Owner: Sponsored Program Administration POLICY STATEMENT This policy establishes the principles for the appropriate allowable

Georgia Regents University Policy Library Facilities and Administrative Cost Policy Owner: Sponsored Program Administration POLICY STATEMENT This policy establishes the principles for the appropriate allowable

Budgeting. Certificate Program 03/09/2016

Budgeting Certificate Program 03/09/2016 Presenters: Gaye Bugenhagen Director of Admin Services, Sociology X54840 gbugenha@umd.edu Muriel Averilla-Chin Senior Contract Administrator, ORA x55465 maverill@umd.edu

Budgeting Certificate Program 03/09/2016 Presenters: Gaye Bugenhagen Director of Admin Services, Sociology X54840 gbugenha@umd.edu Muriel Averilla-Chin Senior Contract Administrator, ORA x55465 maverill@umd.edu

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1316000989A1 ORGANIZATION: University of Cincinnati P.O. Box 210225 Cincinnati, OH 45221-0225 DATE:03/15/2017 FILING REF.: The preceding agreement was dated

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1316000989A1 ORGANIZATION: University of Cincinnati P.O. Box 210225 Cincinnati, OH 45221-0225 DATE:03/15/2017 FILING REF.: The preceding agreement was dated

Overview: Note: To add subrecipient information in all places needed in a proposal record, a user needs full edit access.

Overview: Subrecipients perform a portion of the project s scope of work, subject to review and oversight by CSU s lead PI. Note: To add subrecipient information in all places needed in a proposal record,

Overview: Subrecipients perform a portion of the project s scope of work, subject to review and oversight by CSU s lead PI. Note: To add subrecipient information in all places needed in a proposal record,

Introduction to Indirect Costs

Introduction to Indirect Costs Questions to be Answered What are indirect costs? How are they documented? How are they recovered? Points to Keep in Mind Indirect costs tend to be support costs (e.g., telephone,

Introduction to Indirect Costs Questions to be Answered What are indirect costs? How are they documented? How are they recovered? Points to Keep in Mind Indirect costs tend to be support costs (e.g., telephone,

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1150532082A4 ORGANIZATION: Cornell University 341 Pine Tree Road Ithaca, NY 14850-2820 DATE:07/10/2017 FILING REF.: The preceding agreement was dated 01/20/2017

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1150532082A4 ORGANIZATION: Cornell University 341 Pine Tree Road Ithaca, NY 14850-2820 DATE:07/10/2017 FILING REF.: The preceding agreement was dated 01/20/2017

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs Kimberly Read, PhD, CRA Assistant Director Florida Center for Inclusive Communities University of South Florida

Facilities & Administrative Costs: Balancing Sponsor Requirements and Institutional Needs Kimberly Read, PhD, CRA Assistant Director Florida Center for Inclusive Communities University of South Florida

Proposal & Budget Development. Jordan Brown, Kiley Compton & Stacey Wade

Proposal & Budget Development Jordan Brown, Kiley Compton & Stacey Wade Training Credit Effective August 2017, employees must use k@te to submit training credit forms hr.tennessee.edu/training Choose:

Proposal & Budget Development Jordan Brown, Kiley Compton & Stacey Wade Training Credit Effective August 2017, employees must use k@te to submit training credit forms hr.tennessee.edu/training Choose:

ELEMENTS FOR CREATING A SUCCESSFUL RESEARCH BUDGET

ELEMENTS FOR CREATING A SUCCESSFUL RESEARCH BUDGET Office of Sponsored Programs Al Marks, Presenter Presentation Objectives 2 Discuss the basic foundations for a successful budget Examination of the key

ELEMENTS FOR CREATING A SUCCESSFUL RESEARCH BUDGET Office of Sponsored Programs Al Marks, Presenter Presentation Objectives 2 Discuss the basic foundations for a successful budget Examination of the key

Office of Sponsored Research

Budget Revision Form Instructions and Field Definitions Table of Contents Example Form 1 Part 1 General Information 2 Project Specific Information Submitter Information Part 2 Indirect Costs 2 Identifying

Budget Revision Form Instructions and Field Definitions Table of Contents Example Form 1 Part 1 General Information 2 Project Specific Information Submitter Information Part 2 Indirect Costs 2 Identifying

An Introduction to Facilities & Administrative Rates

An Introduction to Facilities & Administrative Rates F&A Costs What are they? What are they not? Developing a rate Components of a rate Negotiated rates Standard Distributions Special Considerations 1

An Introduction to Facilities & Administrative Rates F&A Costs What are they? What are they not? Developing a rate Components of a rate Negotiated rates Standard Distributions Special Considerations 1

December Facilities and Administrative Costs Primer The Research Foundation for The State University of New York

December 2014 Facilities and Administrative Costs Primer The Research Foundation for The State University of New York Table of Contents Introduction... 3 Direct vs. Facilities and Administrative (F&A)...

December 2014 Facilities and Administrative Costs Primer The Research Foundation for The State University of New York Table of Contents Introduction... 3 Direct vs. Facilities and Administrative (F&A)...

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.85 Policy Name: Subrecipient Monitoring Procedures General Policy and Procedure Overview: The University of Missouri

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.85 Policy Name: Subrecipient Monitoring Procedures General Policy and Procedure Overview: The University of Missouri

Advanced Budgeting September 8 th, 2015

Advanced Budgeting September 8 th, 2015 Maria Skinner Office of Sponsored Programs, Proposal Team 1 517-884-7431 skinne51@osp.msu.edu MaryJo Banasik College of Veterinary Medicine, Research Administration

Advanced Budgeting September 8 th, 2015 Maria Skinner Office of Sponsored Programs, Proposal Team 1 517-884-7431 skinne51@osp.msu.edu MaryJo Banasik College of Veterinary Medicine, Research Administration

COST ISSUES PART 2: INDIRECT COST RATES, WHAT THEY ARE & WHAT YOU NEED TO KNOW

COST ISSUES PART 2: INDIRECT COST RATES, WHAT THEY ARE & WHAT YOU NEED TO KNOW Edward (Ted) Waters, Esq. Scott Sheffler, Esq. August 4, 2016 1 AGENDA Cost Allocation and Indirect Costs Direct Costs vs

COST ISSUES PART 2: INDIRECT COST RATES, WHAT THEY ARE & WHAT YOU NEED TO KNOW Edward (Ted) Waters, Esq. Scott Sheffler, Esq. August 4, 2016 1 AGENDA Cost Allocation and Indirect Costs Direct Costs vs

Two main Goals. Budgeting for Sponsored Projects 2/21/2018 WASHINGTON STATE UNIVERSITY. Template-WSU Hrz 201.ppt 1.

Budgeting for Sponsored Projects Presented by: Matt Michener Grant and Contract Coordinator Lead Office of Research Support and Operations Erin-Kae Rice Director of Operations International Programs Kim

Budgeting for Sponsored Projects Presented by: Matt Michener Grant and Contract Coordinator Lead Office of Research Support and Operations Erin-Kae Rice Director of Operations International Programs Kim

Basics of F&A: A University Perspective. Alex Weekes Principal ML Weekes & Company, PC

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Budget. ASC Time Saver Alert! Excerpt - [ ] 15. Budget Tab on InfoEd: Would you like to data enter less budget information?

![Budget. ASC Time Saver Alert! Excerpt - [ ] 15. Budget Tab on InfoEd: Would you like to data enter less budget information?](/thumbs/89/98879616.jpg "Budget. ASC Time Saver Alert! Excerpt - [ ] 15. Budget Tab on InfoEd: Would you like to data enter less budget information?") Creating a Budget Do not complete the InfoEd budget tab for the following projects: ISMMS (i.e., internally) funded Projects in which the extramural funding agency provides funding by milestone (i.e.,

Creating a Budget Do not complete the InfoEd budget tab for the following projects: ISMMS (i.e., internally) funded Projects in which the extramural funding agency provides funding by milestone (i.e.,

Indirect Cost Rates A Non-Profit Perspective. Alex Weekes Principal ML Weekes & Company, PC

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

Creating a high-level budget in Kuali Research Non-personnel Budget Entry Method non-modular Budgets

Creating a high-level budget in Kuali Research Non-personnel Budget Entry Method non-modular Budgets A high-level budget has annual direct and indirect (F&A) costs for a proposal with little to no budget

Creating a high-level budget in Kuali Research Non-personnel Budget Entry Method non-modular Budgets A high-level budget has annual direct and indirect (F&A) costs for a proposal with little to no budget

Scope: X Medical Center X Beckman Research X Philanthropy/External Relations

Policy and Procedure Manual Administrative Manual Administrative Institutional Department: Basic Research Operations Written: 02/10/13 Reviewed: 10/01/14 Revised: 04/25/13; 09/09/14 Page: 1 of 4 (Attachments)

Policy and Procedure Manual Administrative Manual Administrative Institutional Department: Basic Research Operations Written: 02/10/13 Reviewed: 10/01/14 Revised: 04/25/13; 09/09/14 Page: 1 of 4 (Attachments)

Frequently Requested Information

SBS Grants and Contracts Frequently Requested Information Resource information from the gathered sources of NAU OGCS and College of SBS Grants and Contracts Office Stacy Wyman, Grants and Contract Administrator,

SBS Grants and Contracts Frequently Requested Information Resource information from the gathered sources of NAU OGCS and College of SBS Grants and Contracts Office Stacy Wyman, Grants and Contract Administrator,

The University Maryland Baltimore County

The University Maryland Baltimore County Office of Sponsored Programs Subaward Policies and Procedures Purpose The purpose of the University Maryland Baltimore County Subaward Policies and Procedures is

The University Maryland Baltimore County Office of Sponsored Programs Subaward Policies and Procedures Purpose The purpose of the University Maryland Baltimore County Subaward Policies and Procedures is

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1020222111A3 ORGANIZATION: Dartmouth College Office of Sponsored Projects 11 Rope Ferry Road #6210 Hanover, NH 03755-1404 DATE:11/30/2017 FILING REF: The preceding

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1020222111A3 ORGANIZATION: Dartmouth College Office of Sponsored Projects 11 Rope Ferry Road #6210 Hanover, NH 03755-1404 DATE:11/30/2017 FILING REF: The preceding

OMB Super Circular Proposed Uniform Guidance. RAC Forum April 10, 2013

OMB Super Circular Proposed Uniform Guidance RAC Forum April 10, 2013 Change is Coming Good news A-21 is gone! Bad news It s back and bigger than ever Circular Consolidation Super Storm? Extreme Makeover:

OMB Super Circular Proposed Uniform Guidance RAC Forum April 10, 2013 Change is Coming Good news A-21 is gone! Bad news It s back and bigger than ever Circular Consolidation Super Storm? Extreme Makeover:

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Regulations (Current and New) Rate Types

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Regulations (Current and New) Rate Types

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1586002050A1 ORGANIZATION: Georgia State University and Georgia State University Foundation University Services & Administration P.O. Box 3999 Atlanta, GA

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1586002050A1 ORGANIZATION: Georgia State University and Georgia State University Foundation University Services & Administration P.O. Box 3999 Atlanta, GA

10 Frequently Asked Questions on Indirect Costs

1 10 Frequently Asked Questions on Indirect Costs Bonnie Graham, Esq. bgraham@bruman.com (202) 965-3652 www.bruman.com First, some background 2 Total Cost of Federal Awards Indirect 10% Direct Indirect

1 10 Frequently Asked Questions on Indirect Costs Bonnie Graham, Esq. bgraham@bruman.com (202) 965-3652 www.bruman.com First, some background 2 Total Cost of Federal Awards Indirect 10% Direct Indirect

WHAT THE PI NEEDS TO KNOW

The UC Uniform Guidance Workgroup would like to acknowledge and thank the Council on Governmental Relations, the University of Minnesota, and Columbia University for their resources on which much of this

The UC Uniform Guidance Workgroup would like to acknowledge and thank the Council on Governmental Relations, the University of Minnesota, and Columbia University for their resources on which much of this

State and University Proposal & Administration Manual

State and University Proposal & Administration Manual December 1, 2015 DRAFT State and University Proposal & Administration Manual For use with AB20 Model State Agreement w/uc and CSU for Research, Training

State and University Proposal & Administration Manual December 1, 2015 DRAFT State and University Proposal & Administration Manual For use with AB20 Model State Agreement w/uc and CSU for Research, Training

CAYUSE (S2S) NIH SUBAWARD CHECKLIST Revised September 7, 2012

NIH SUBAWARD CHECKLIST Revised September 7, 2012") CAYUSE (S2S) NIH SUBAWARD CHECKLIST Revised September 7, 2012 Other Project Information Section 6.a. Does this project involve activities outside the U.S. or partnership with International Collaborators?

CAYUSE (S2S) NIH SUBAWARD CHECKLIST Revised September 7, 2012 Other Project Information Section 6.a. Does this project involve activities outside the U.S. or partnership with International Collaborators?

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 846000545 ORGANIZATION: Colorado State University Business and Financial 202 Johnson Hall Fort Collins, CO 80523 DATE:04/15/2015 FILING REF.: The preceding

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 846000545 ORGANIZATION: Colorado State University Business and Financial 202 Johnson Hall Fort Collins, CO 80523 DATE:04/15/2015 FILING REF.: The preceding

PACS Portal Grants Module Create a Funding Proposal

PACS Portal Grants Module Create a Funding Proposal 1 Table of Contents What is the PACS Portal?... 4 Getting a PACS Account... 4 Logging into the PACS Portal... 5 Grants Tab... 6 Workflow... 7 Additional

PACS Portal Grants Module Create a Funding Proposal 1 Table of Contents What is the PACS Portal?... 4 Getting a PACS Account... 4 Logging into the PACS Portal... 5 Grants Tab... 6 Workflow... 7 Additional

Procedures for the Administration of Sponsored Projects Subcontracts

Procedures for the Administration of Sponsored Projects Subcontracts Office of Research Administration University of Maryland, College Park (Updated August 6, 2015) 1 TABLE OF CONTENTS INTRODUCTION...

Procedures for the Administration of Sponsored Projects Subcontracts Office of Research Administration University of Maryland, College Park (Updated August 6, 2015) 1 TABLE OF CONTENTS INTRODUCTION...

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1591961248A3 ORGANIZATION: Florida State University Office - Sr. V.P. for Fin. & Admin. 214 Westcott Building Tallahassee, FL 32306-1320 DATE:07/09/2018 FILING

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1591961248A3 ORGANIZATION: Florida State University Office - Sr. V.P. for Fin. & Admin. 214 Westcott Building Tallahassee, FL 32306-1320 DATE:07/09/2018 FILING

Indirect costs, on the other hand, are expenses that cannot be specifically identified with a particular project or activity.

II. Other Direct Costs A. Overview A project budget is comprised of direct costs, i.e. salaries and other direct costs, and indirect costs. Other direct costs refer to expenditures that are allowed as

II. Other Direct Costs A. Overview A project budget is comprised of direct costs, i.e. salaries and other direct costs, and indirect costs. Other direct costs refer to expenditures that are allowed as

2 CFR Part 200 Series #2 New Definitions

This is the second of a series dedicated to the topic of new citations found in 2 CFR Part 200 Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Grants. The following

This is the second of a series dedicated to the topic of new citations found in 2 CFR Part 200 Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Grants. The following

Hot Topics In Research Administration

General Session (8:30-9:20): Research Update STEW 302 Breakout Sessions (9:30-10:40 & 10:50-12:00) Subrecipient Monitoring STEW 202 Effective Communication in Research Administration STEW 310 Facility

General Session (8:30-9:20): Research Update STEW 302 Breakout Sessions (9:30-10:40 & 10:50-12:00) Subrecipient Monitoring STEW 202 Effective Communication in Research Administration STEW 310 Facility

Illinois Coalition Against Domestic Violence. Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016

Illinois Coalition Against Domestic Violence Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016 1 Understanding the Uniform Guidance and Indirect Cost Rate Presented by: Teri L. Taylor,

Illinois Coalition Against Domestic Violence Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016 1 Understanding the Uniform Guidance and Indirect Cost Rate Presented by: Teri L. Taylor,

Office of Sponsored Research Budget Revision Form Instructions and Field Definitions

Budget Revision Form Instructions and Field Definitions Table of Contents Example Form 1 Part 1 General Information 2 Project Specific Information Submitter Information Part 2 Indirect Costs 2 Identifying

Budget Revision Form Instructions and Field Definitions Table of Contents Example Form 1 Part 1 General Information 2 Project Specific Information Submitter Information Part 2 Indirect Costs 2 Identifying

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers October 18, 2018 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers October 18, 2018 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 5929796169 ORGANIZATION: University of North Florida 1 UNF Drive Jacksonville, FL 32224-2645 DATE:07/13/2017 FILING REF.: The preceding agreement was dated

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 5929796169 ORGANIZATION: University of North Florida 1 UNF Drive Jacksonville, FL 32224-2645 DATE:07/13/2017 FILING REF.: The preceding agreement was dated

Everything You ve Always Wanted to Know. About Indirect Costs. But Were Too Confused to Ask.

Everything You ve Always Wanted to Know About Indirect Costs But Were Too Confused to Ask. Presentation to RADG Harry W. Orf, PhD 10 June 2014 Page 1 2 What We Will Cover Federal Statutes That Govern Indirect

Everything You ve Always Wanted to Know About Indirect Costs But Were Too Confused to Ask. Presentation to RADG Harry W. Orf, PhD 10 June 2014 Page 1 2 What We Will Cover Federal Statutes That Govern Indirect

Medical School NIH Research Proposal Review Checklist

Medical School This checklist serves as a reference guide for Medical School departments/units when reviewing NIH research grants prior to routing for approval. This document provides a quick reference

Medical School This checklist serves as a reference guide for Medical School departments/units when reviewing NIH research grants prior to routing for approval. This document provides a quick reference

Today s Topics. Cost Principles. Federal Guidance. Guidance Resources. Purpose of Cost Principles. Cost Principles Overview 5/7/2015

Cost Principles Presented by: Contracts and Grants Accounting James Ringo Today s Topics Making good decisions about costs Allowable Allocable Reasonable, necessary Consistent Distinguishing direct vs.

Cost Principles Presented by: Contracts and Grants Accounting James Ringo Today s Topics Making good decisions about costs Allowable Allocable Reasonable, necessary Consistent Distinguishing direct vs.

Budget Workbook Instructions for Proof of Concept Proposals

Budget Workbook Instructions for Proof of Concept Proposals FY2012-2013 (1) Fill out forms. Provide requested information (indicated in yellow) on each form worksheet. Skip subcontract worksheet if not

Budget Workbook Instructions for Proof of Concept Proposals FY2012-2013 (1) Fill out forms. Provide requested information (indicated in yellow) on each form worksheet. Skip subcontract worksheet if not

Understanding F&A Rates. OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

Uniform Guidance Super Circular 2 CFR Part 200

Uniform Guidance Super Circular 2 CFR Part 200 MSU First Looks and Future Plans May 27, 2014 Dan Evon, Contract & Grant Administration The Rules Contracts Federal Acquisition Regulations (FAR) Grants and

Uniform Guidance Super Circular 2 CFR Part 200 MSU First Looks and Future Plans May 27, 2014 Dan Evon, Contract & Grant Administration The Rules Contracts Federal Acquisition Regulations (FAR) Grants and

Coeus Proposal Hierarchy

Coeus Proposal Hierarchy Last Updated: May 9, 2018 Table of Contents Proposal Hierarchy... 3 What is a proposal hierarchy?... 3 Why create a proposal hierarchy?... 3 A Basic Understanding of Coeus and

Coeus Proposal Hierarchy Last Updated: May 9, 2018 Table of Contents Proposal Hierarchy... 3 What is a proposal hierarchy?... 3 Why create a proposal hierarchy?... 3 A Basic Understanding of Coeus and

NOVA SOUTHEASTERN UNIVERSITY OFFICE OF SPONSORED PROGRAMS POLICIES AND PROCEDURES

PAGE 1 OF 5 PURPOSE: To establish the policy and procedures when the university will engage a third party in performing a substantive programmatic role under a sponsored award to the university. This policy

PAGE 1 OF 5 PURPOSE: To establish the policy and procedures when the university will engage a third party in performing a substantive programmatic role under a sponsored award to the university. This policy

Frequently Asked Questions

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Subcontract Request Form

960 Renaissance Park www.northeastern.edu/raf oraf@neu.edu Subcontract Request Form Please provide the information requested below and attach the following: 1. Subcontractors Statement of Work 2. Subcontractors

960 Renaissance Park www.northeastern.edu/raf oraf@neu.edu Subcontract Request Form Please provide the information requested below and attach the following: 1. Subcontractors Statement of Work 2. Subcontractors

Cost Accounting Standards & Disclosure Statement

Cost Accounting Standards & Disclosure Statement Ginger Baker, Manager SW Systems Office Cost Analysis and Sponsored Program Administration Ginger.Baker@alaska.edu (907) 474-6496 Today s Topics Overview

Cost Accounting Standards & Disclosure Statement Ginger Baker, Manager SW Systems Office Cost Analysis and Sponsored Program Administration Ginger.Baker@alaska.edu (907) 474-6496 Today s Topics Overview

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1350868188Al ORGANIZATION: University of Notre Dame 804 Grace Hall Notre Dame, IN 46556-5612 DATE:03/20/2017 FILING REF.: The preceding agreement was dated

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 1350868188Al ORGANIZATION: University of Notre Dame 804 Grace Hall Notre Dame, IN 46556-5612 DATE:03/20/2017 FILING REF.: The preceding agreement was dated

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 46-2354111 ORGANIZATION: Rutgers School of Biomedical & Health Sciences 3 Rutgers Plaza,Admin.Sv.Blg.3,2 Fl New Brunswick, NJ 08901-3325 DATE:02/15/2019 FILING

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: 46-2354111 ORGANIZATION: Rutgers School of Biomedical & Health Sciences 3 Rutgers Plaza,Admin.Sv.Blg.3,2 Fl New Brunswick, NJ 08901-3325 DATE:02/15/2019 FILING

January 16, DATES: Effective date: This interim final rule is effective on December 26, 2014

COGR Summary of Background and Technical Corrections to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards January 16, 2015 The interim joint final

COGR Summary of Background and Technical Corrections to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards January 16, 2015 The interim joint final

Uniform Guidance vs. OMB Circulars

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

STANDARD ADMINISTRATIVE PROCEDURE

STANDARD ADMINISTRATIVE PROCEDURE 15.01.01.M1.02 Residual Balances from Fixed Price Sponsored Agreements Approved March 6, 2000 Revised April 1, 2004 Revised July 5, 2010 Revised July 30, 2013 Revised

STANDARD ADMINISTRATIVE PROCEDURE 15.01.01.M1.02 Residual Balances from Fixed Price Sponsored Agreements Approved March 6, 2000 Revised April 1, 2004 Revised July 5, 2010 Revised July 30, 2013 Revised

The Subaward Process Part One A Research Administrator s Guide

The Subaward Process Part One A Research Administrator s Guide Anne Lesky, SPARCS Amy Herman, SPARCS With Assistance from Allison Nelson, C&G Brad Priser, C&G Learning Objectives After attending this session,

The Subaward Process Part One A Research Administrator s Guide Anne Lesky, SPARCS Amy Herman, SPARCS With Assistance from Allison Nelson, C&G Brad Priser, C&G Learning Objectives After attending this session,

Policy on Cost Allocation, Cost Recovery, and Cost Sharing

Page 1 of 13 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting,

Page 1 of 13 PURPOSE: Provide guidance and structure when allocating and documenting costs (direct and indirect) for extramurally funded awards. Serves to provide direction for budgeting,

PHS Financial Disclosure Form

This form is to be completed by all investigators who have responded yes to the PHS Financial Interest Screening Questions. Submit this form when requested for pending awards/jit requests from the Public

This form is to be completed by all investigators who have responded yes to the PHS Financial Interest Screening Questions. Submit this form when requested for pending awards/jit requests from the Public

The Texas A&M University System Uniform Guidance Cost Principles Reference Guide. Selected Items of Cost

The The Uniform Guidance issued by the White House Office of Management and Budget includes revised cost principles for federal awards made on or after December 26, 2014. This Cost Principles Reference

The The Uniform Guidance issued by the White House Office of Management and Budget includes revised cost principles for federal awards made on or after December 26, 2014. This Cost Principles Reference

UACES Subrecipient Monitoring Policy Statement

UACES Subrecipient Monitoring Policy Statement UACES monitors the financial and programmatic performance of Subrecipients, and evaluates their capacity to effectively manage a Subaward. The university

UACES Subrecipient Monitoring Policy Statement UACES monitors the financial and programmatic performance of Subrecipients, and evaluates their capacity to effectively manage a Subaward. The university

UNDERSTANDING FACILITIES & ADMINISTRATIVE (INDIRECT) COSTS AT GEORGIA STATE UNIVERSITY

COSTS AT GEORGIA STATE UNIVERSITY") UNDERSTANDING FACILITIES & ADMINISTRATIVE (INDIRECT) COSTS AT GEORGIA STATE UNIVERSITY I. What is the difference between Direct Costs, and Facilities & Administrative (Indirect) Costs? Georgia State University

UNDERSTANDING FACILITIES & ADMINISTRATIVE (INDIRECT) COSTS AT GEORGIA STATE UNIVERSITY I. What is the difference between Direct Costs, and Facilities & Administrative (Indirect) Costs? Georgia State University

DoD Appropriations Act, 2008 (PL ) Indirect Cost Recovery Limitation on DoD Basic Research

Indirect Cost Recovery Limitation on DoD Basic Research") DoD Appropriations Act, 2008 (PL110-116) Indirect Cost Recovery Limitation on DoD Basic Research January 10, 2008 Federal Demonstration Partnership Presented by: University Business Affairs, Indirect Cost

DoD Appropriations Act, 2008 (PL110-116) Indirect Cost Recovery Limitation on DoD Basic Research January 10, 2008 Federal Demonstration Partnership Presented by: University Business Affairs, Indirect Cost

Module 8 Setting up the Project Outline

Module 8 Setting up the Project Outline Key concepts in this module are: Financial Accounting System (FAS) structure and FAS account create process Setting up Payroll and other recurring expenses Setting

Module 8 Setting up the Project Outline Key concepts in this module are: Financial Accounting System (FAS) structure and FAS account create process Setting up Payroll and other recurring expenses Setting

Guide to the Budget Worksheet for Pre-ERA Planning

Guide to the Budget Worksheet for Pre-ERA Planning Contents: Introduction to the Worksheet Pages 2-8 Creating a budget with the Worksheet Pages 9-22 Modifying F&A rates in the Worksheet Pages 23-24 Adding

Guide to the Budget Worksheet for Pre-ERA Planning Contents: Introduction to the Worksheet Pages 2-8 Creating a budget with the Worksheet Pages 9-22 Modifying F&A rates in the Worksheet Pages 23-24 Adding

FACILITATED BY: Robin Booth, CPA

U.S. Department of Housing and Urban Development Office of Housing Counseling Applying and Computing the 10% De Minimis Rate November 22, 2016 2:00 PM (EST) Facilitated by Booth Management Consulting,

U.S. Department of Housing and Urban Development Office of Housing Counseling Applying and Computing the 10% De Minimis Rate November 22, 2016 2:00 PM (EST) Facilitated by Booth Management Consulting,

Subrecipient Monitoring Guide

Office of Research Subrecipient Monitoring Guide The purpose of this document is to communicate the University of Florida s guidelines pertaining to the programmatic and financial monitoring of its sponsored

Office of Research Subrecipient Monitoring Guide The purpose of this document is to communicate the University of Florida s guidelines pertaining to the programmatic and financial monitoring of its sponsored

Training Exercise Guide Fall 2018

Coeus Lite Proposal Development Training Exercise Guide Fall 2018 Contents EXERCISE 1: CREATE A NEW PROPOSAL... 6 EXERCISE 2: REVIEW ORGANIZATION TAB... 8 EXERCISE 3: ADD KEY PERSONNEL... 9 Modify Person

Coeus Lite Proposal Development Training Exercise Guide Fall 2018 Contents EXERCISE 1: CREATE A NEW PROPOSAL... 6 EXERCISE 2: REVIEW ORGANIZATION TAB... 8 EXERCISE 3: ADD KEY PERSONNEL... 9 Modify Person

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers October 12, 2017 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers October 12, 2017 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

OFFICE OF RESEARCH AND PROJECT ADMINISTRATION Updated December 2014 UNIVERSITY OF ROCHESTER

OFFICE OF RESEARCH AND PROJECT ADMINISTRATION Updated December 2014 POLICIES AND PROCEDURES FOR THE ADMINISTRATION OF SUBAGREEMENTS ISSUED TO A THIRD PARTY UNIVERSITY OF ROCHESTER December 2014 TABLE OF

OFFICE OF RESEARCH AND PROJECT ADMINISTRATION Updated December 2014 POLICIES AND PROCEDURES FOR THE ADMINISTRATION OF SUBAGREEMENTS ISSUED TO A THIRD PARTY UNIVERSITY OF ROCHESTER December 2014 TABLE OF

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN : 1376005961Al ORGANIZATION : Southern Illinois University at Carbondale Mail Code 4344 Carbondale, IL 62901-4716 DATE:08/19/2016 FILING REF.: The preceding

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN : 1376005961Al ORGANIZATION : Southern Illinois University at Carbondale Mail Code 4344 Carbondale, IL 62901-4716 DATE:08/19/2016 FILING REF.: The preceding

Subrecipient Assessment and Monitoring - It Takes a Village!

Subrecipient Assessment and Monitoring - It Takes a Village! Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor for Research, Director of OSR The

Subrecipient Assessment and Monitoring - It Takes a Village! Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor for Research, Director of OSR The

Downstate Medical Center. Office of Research Administration Sharon Levine-Sealy, Pre-Award Director Elliot Feder, Post-Award Director.

Downstate Medical Center Office of Research Administration Sharon Levine-Sealy, Pre-Award Director Elliot Feder, Post-Award Director September 2015 Identify the different funding opportunities Interpret

Downstate Medical Center Office of Research Administration Sharon Levine-Sealy, Pre-Award Director Elliot Feder, Post-Award Director September 2015 Identify the different funding opportunities Interpret

Allowable Costs. Exception to Direct or Indirect Cost Category. Item of Cost Description Normally Direct or Indirect Cost

Allowable Costs The Federal Office of Budget and Management (OMB) 2 CFR Part 200 provides principles to be applied to determine the allowability of certain items of cost on Federal Awards. The principles

Allowable Costs The Federal Office of Budget and Management (OMB) 2 CFR Part 200 provides principles to be applied to determine the allowability of certain items of cost on Federal Awards. The principles

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.07 Policy Name: Allowable Costs and Cost Principles General Policy and Procedure Overview This policy outlines the

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.07 Policy Name: Allowable Costs and Cost Principles General Policy and Procedure Overview This policy outlines the

Research Administration Start to Finish. (GC1000) Complete Course

Complete Course") Part II Research Administration Start to Finish (GC1000) Complete Course Award Administration (Module 2.00) In this module Project Start-Up Expenditures Expense Monitoring Compliance Spending Awards Personnel

Part II Research Administration Start to Finish (GC1000) Complete Course Award Administration (Module 2.00) In this module Project Start-Up Expenditures Expense Monitoring Compliance Spending Awards Personnel

PROPOSAL BUDGET BUDGETING OVERVIEW E.1.1. NAVIGATE TO BUDGET E.1.2. NAVIGATE FROM BUDGET TO PROPOSAL HOW TO START A BUDGET

E. PROPOSAL BUDGET E. E. E. BUDGETING OVERVIEW E. NAVIGATE TO BUDGET E. NAVIGATE FROM BUDGET TO PROPOSAL HOW TO START A BUDGET PERSONNEL E. E.2 E. E. F. E. E. E. E.7. E.8. E.9. E.10. E.1 E.1 E.1 E.1 E.1

E. PROPOSAL BUDGET E. E. E. BUDGETING OVERVIEW E. NAVIGATE TO BUDGET E. NAVIGATE FROM BUDGET TO PROPOSAL HOW TO START A BUDGET PERSONNEL E. E.2 E. E. F. E. E. E. E.7. E.8. E.9. E.10. E.1 E.1 E.1 E.1 E.1

María M. Santiago Morales Budget Director University of Puerto Rico at Cayey October 19, 2018

María M. Santiago Morales Budget Director University of Puerto Rico at Cayey October 19, 2018 Budget Definition Why is a budget important? Budget Phases Preparing the budget Approving the budget Executing

María M. Santiago Morales Budget Director University of Puerto Rico at Cayey October 19, 2018 Budget Definition Why is a budget important? Budget Phases Preparing the budget Approving the budget Executing

Processing Research Participant Costs

Processing Research Participant Costs Support, Patient Care and Compensation Principle: Many research studies rely on participants in various ways to fulfill the desired outcome of the project. Varying

Processing Research Participant Costs Support, Patient Care and Compensation Principle: Many research studies rely on participants in various ways to fulfill the desired outcome of the project. Varying

Working with F&A at UVA. Caroline Beeman

Caroline Beeman By the end of this session you should be able to solve this problem: Your PI is writing a proposal for an $800,000 grant. This is the total amount the sponsor is willing to pay for both

Caroline Beeman By the end of this session you should be able to solve this problem: Your PI is writing a proposal for an $800,000 grant. This is the total amount the sponsor is willing to pay for both

PURDUE UNIVERSITY SPONSORED PROGRAM SERVICES. July 9, (Supersedes Memorandum dated September 19, 2012)

") PURDUE UNIVERSITY SPONSORED PROGRAM SERVICES July 9, 2015 (Supersedes Memorandum dated September 19, 2012) TO: SUBJECT: David Wesse, Vice Chancellor for Financial Affairs IPFW Campus Facilities and Administrative

PURDUE UNIVERSITY SPONSORED PROGRAM SERVICES July 9, 2015 (Supersedes Memorandum dated September 19, 2012) TO: SUBJECT: David Wesse, Vice Chancellor for Financial Affairs IPFW Campus Facilities and Administrative

Project Modification Request (PMR) Justification Checklist Reference Guide

Justification Checklist Reference Guide") Project Modification Request (PMR) Justification Checklist No Cost Extension 1. Is agency approval needed? 2. Do we have a deadline to request extension? Is this a RUSH? 3. Is this a first NCE request?

Project Modification Request (PMR) Justification Checklist No Cost Extension 1. Is agency approval needed? 2. Do we have a deadline to request extension? Is this a RUSH? 3. Is this a first NCE request?

Disclosure of Financial Interests & Management of Conflicts of Interest, Public Health Service Research Awards

Disclosure of Financial Interests & Management of Conflicts of Interest, Public Health Service Research Responsible Officer: VP - Research & Graduate Studies Responsible Office: RG - Research & Graduate

Disclosure of Financial Interests & Management of Conflicts of Interest, Public Health Service Research Responsible Officer: VP - Research & Graduate Studies Responsible Office: RG - Research & Graduate

Procedures for the Administration of Subcontracts

Procedures for the Administration of Subcontracts The purpose of this document is to assist Rensselaer faculty and staff in the preparation and administration of subawards and subcontracts issued under

Procedures for the Administration of Subcontracts The purpose of this document is to assist Rensselaer faculty and staff in the preparation and administration of subawards and subcontracts issued under

SPA and Outgoing Subawards. Molly Epstein, Karin Bourassa, Kathy McConnell, Erin Fitzgerald 12/8/2017

SPA and Outgoing Subawards Molly Epstein, Karin Bourassa, Kathy McConnell, Erin Fitzgerald 12/8/2017 This presentation will cover The difference between a subaward and a contract Roles and responsibilities

SPA and Outgoing Subawards Molly Epstein, Karin Bourassa, Kathy McConnell, Erin Fitzgerald 12/8/2017 This presentation will cover The difference between a subaward and a contract Roles and responsibilities

COLLEGES AND UNIVERSITIES RATE AGREEMENT

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: ORGANIZATION: San Jose State University and the Foundation 210 North 4th Street San Jose, CA 95112 DATE:07/16/2018 FILING REF.: The preceding agreement was

COLLEGES AND UNIVERSITIES RATE AGREEMENT EIN: ORGANIZATION: San Jose State University and the Foundation 210 North 4th Street San Jose, CA 95112 DATE:07/16/2018 FILING REF.: The preceding agreement was

Budget Preparation under Uniform Guidance 2 CFR 200

Budget Preparation under Uniform Guidance 2 CFR 200 Kim C. Carter Associate Director, Office of Sponsored Programs The Ohio State University carter.552@osu.edu Florida Research Administration Conference

Budget Preparation under Uniform Guidance 2 CFR 200 Kim C. Carter Associate Director, Office of Sponsored Programs The Ohio State University carter.552@osu.edu Florida Research Administration Conference