THE ANNUAL FINANCIAL REPORTING WEEK Theme : Reliance on Enhanced Financial Reporting for Economic Growth and Development

|

|

|

- Ronald Gilbert

- 5 years ago

- Views:

Transcription

1 THE ANNUAL FINANCIAL REPORTING WEEK Theme : Reliance on Enhanced Financial Reporting for Economic Growth and Development FCPA Erastus Kwaka Omolo Crowe Erastus & Co. Date : 13 th September, 2018 Venue : Hilton Hotel, Nairobi horwatherastus@crowehorwath.co.ke Uphold public interest Smart Decisions. Lasting Value 1

2 Contents IAS 8, IPSAS 3 / SECTION 10 OF IFRS FOR SMEs ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS IAS 10 : EVENTS AFTER THE REPORTING PERIOD 2

3 1. Objective of the Standard IAS 8 1. Prescribe the criteria for selecting and changing accounting policies, together with the accounting treatment and disclosure of changes in accounting policies, changes in accounting estimates and correction of errors. 2. Disclosure requirements for accounting policies, except those for changes in accounting policies are set out in IPSAS 1, IAS 1 3

4 2. Scope of the Standard IAS 8 Application 1. selecting and applying accounting policies, 2. accounting for changes in accounting policies, changes in accounting estimates, and 3. corrections of prior period errors. 4

5 3. Selections and Application of Accounting Policies When an IPSAS / IFRS specifically applies to a transaction, other event or condition, the accounting policy or policies applied to that item shall be determined by applying the Standard and considering any relevant Implementation Guidance issued by the IPSASB for the Standard [IPSAS 3 IAS 8 para 9] 5

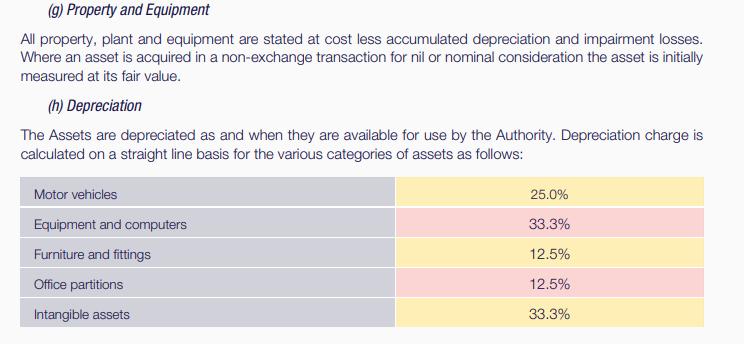

6 4. An example of an accounting policy of an entity based on IPSAS Competition Authority of Kenya cs/cak_annual_report%20_2014_1 5_final.pdf 6

7 4. An example of an accounting policy of an entity based on IPSAS 7

8 5. PPOA Example of accounting Policy 8

9 Where no IPSAS / IFRS that specifically applies to a transaction, other event or condition, management shall use its judgment in developing and applying an accounting policy that results in information that is relevant to the decisionmaking needs of users; and faithfully represents the financial position, financial performance and cash flows of the entity, neutral, prudent and complete [IPSAS 3 (12), IAS 8 (10) and IFRS SME 10.4] 9

10 When making judgment management to observe: - 1. requirements in IPSASs / IFRS in dealing with similar and related issues 2. definition, recognition and measurement criteria for assets, liabilities, income and expenses described in IPSAS - Conceptual Framework for General Purpose Financial Reporting for Public Sector Entities 10

11 When making judgment management to observe: - IFRS for SMEs Concepts and Pervasive principles in Section 2 or Full IFRS 3. most recent pronouncements of other standard setting bodies e.g. IASB, IFRIC, former SIC, IFRS 4. accepted public sector practices IPSAS 11

12 Consistency, Changes and Retrospective Application Accounting policies shall be applied consistently. Changes in accounting policy shall be applied retrospectively and to comparative information for prior periods as far back as practicable. Retrospective application requires adjustment of opening balance of each affected component of equity for the earliest period presented and comparative information. Impractical? Apply from the earliest date practicable 12

13 Disclosure Requirements Example To test IAS 8 Paragraph 17 An entity shall disclose when:- 1. Initial application of an IPSAS / IFRS 2. Voluntary application of IPSAS / IFRS 3. Newly issued IPSAS / IFRS that is not yet effective and has not been applied 13

14 CHANGES IN ACCOUNTING ESTIMATES [IPSAS 37-45, IAS , SME ] a) Estimates result from uncertainties in measuring items in financial statements with precision. Such items can only be estimated based on latest available and reliable information b) Examples are warranty obligations, bad debts, inventory obsolescence etc. c) An estimate may need revision if changes occur in the circumstances on which the estimate was based or as a result of new information or more experience. By its nature, the revision of an estimate does not relate to prior periods and is not the correction of an error. 14

15 CHANGES IN ACCOUNTING ESTIMATES [IPSAS 37-45, IAS , SME ] d) A change in the measurement basis applied is a change in an accounting policy, and is not a change in an accounting estimate. When it is difficult to distinguish a change in an accounting policy from a change in an accounting estimate, the change is treated as a change in an accounting estimate. e) A change in an accounting estimate that gives rise to changes in assets and liabilities, or relates to an item of net assets/equity, is recognized by adjusting the carrying amount of the related asset, liability or net assets/equity item in the period of change. 15

16 CHANGES IN ACCOUNTING ESTIMATES [IPSAS 37-45, IAS , SME ] f) The effect of a change in an accounting estimate, other than a change to which (d) above applies, shall be recognized prospectively by including it in surplus or deficit in the period of the change, if the change affects the period only; or the period of the change and future periods, if the change affects both. g) Disclosure requirements - Disclose the nature and amount of a change in an accounting estimate or the fact if its impractical to estimate [Illustration Change in useful life of assets PPOA] 16

17 ERRORS [IPSAS , IAS , SME ] a) An error is a discrepancy, mathematical mistake, mistake in applying GAAP, misrepresentation of an existing fact during recognition, measurement, presentation or disclosure of elements of financial statements. b) Material errors or intentional immaterial errors when discovered must be corrected before authorization of financial statements for issue. c) Material errors discovered in subsequent periods are corrected in comparative information in that subsequent period 17

18 ERRORS [IPSAS , IAS , SME ] d) Retrospective correction Correction of comparative information presented, if earlier, restate the opening balances of assets and liabilities, net assets/equity of earliest period presented. e) Limitation to retrospective restatement if impractical to determine the period specific effects or cumulative effect of the error f) Correction of prior period error is excluded from the surplus or deficit of the period in which the error is discovered 18

19 ERRORS [IPSAS , IAS , SME ] g) Disclosure Requirements i. The nature of the prior period error; ii. For each prior period presented, to the extent practicable, the amount of the correction for each financial statement line item affected; iii. The amount of the correction at the beginning of the earliest prior period presented; and iv. If retrospective restatement is impracticable for a particular prior period, the circumstances that led to the existence of that condition and a description of how and from when the error has been corrected. 19

20 DO NOT FORGET THE TAX ANGLE! Remember that for tax purposes, the tax effect must be given by a note to the accounts. You may also have to visit the KRA i-tax System to make adjustments!! 20

21 IAS 8, IPSAS 3 / SECTION 10 OF IFRS FOR SMEs IAS 10; EVENTS AFTER THE REPORTING PERIOD 21

22 OBJECTIVE : IAS 10 Effective date annual periods beginning 1 January, Give guidance on 1. When financial statements should be adjusted for events after the reporting period 2. Disclosures to be given about the date FS were authorized for issue and events after the reporting period. 22

23 SCOPE : IAS 10 Accounting for and disclosure of events after the reporting period. 23

24 KEY TERMS: IAS 10 Reporting period span of time covered by a set of financial statements. Events after period end matters which occur after the reporting period but before the financial statements are authorized for issue. The events may be favorable or unfavorable. 24

25 KEY TERMS : IAS 10 Events after period end are classified as: Those that provide evidence of conditions that existed at the end of the reporting period (adjusting events after period end) Those that are indicative of conditions that arose after the reporting period (nonadjusting events after the reporting period) 25

26 KEY TERMS : IAS 10 Date of authorization of issue of financial statements may vary from one entity to the other depending on the management structure or statutory requirements. In most instances it is the date the FS are issued either by the management or the board for approval by a supervisory board or shareholders. 26

27 RECOGNITION AND MEASUREMENT IAS 10 ADJUSTING EVENTS Financial statements are adjusted to recognize adjusting events after the period end. Examples include: A liability arising from the settlement of a court case after the period end the provisions are adjusted to include the liability. Discovery of fraud or error indicating that the financial statements are incorrect. 27

28 RECOGNITION AND MEASUREMENT IAS 10 NON-ADJUSTING EVENTS Financial statements are not adjusted to reflect non-adjusting events after the period end. Examples include: Decline of the fair value of investments after year end before the financial statements are authorized for issue quoted equity. The decline is not related to the condition of the investments at the reporting period end but indicate circumstances that arose after the period end. 28

29 RECOGNITION AND MEASUREMENT IAS 10 DIVIDENDS Dividends declared to equity holders after the reporting period are not recognized as a liability at the end of the reporting period. They are discosed in the notes indicating the total amount of dividends proposed and the related amount per share. 29

30 NON-ADJUSTING EVENTS THAT NEED DISCLOSURE Material events that if not disclosed would affect the economic decisions that users make on the basis of the financial statements. Disclose: Nature of the event. An estimate of its financial effect or a statement that such an estimate cannot be made. 30

31 NON-ADJUSTING EVENTS THAT NEED DISCLOSURE Examples: Announcing a plan to discontinue an operation. Major purchase of assets or destruction of a major production plant by fire after the reporting period. Major share transactions Abnormally large changes in asset prices or foreign exchange rates. 31

32 NON-ADJUSTING EVENTS THAT NEED DISCLOSURE Examples: Changes in tax rates or tax laws that have a major impact on an operation from a tax point of view Entering into significant commitments or contingent liabilities. Commencing major litigation arising out of events that occurred solely after the reporting period 32

33 GOING CONCERN If management determines after year end before FS are authorized for issue its intention to liquidate the entity or to cease trading, the financial statements shall not be prepared on a going concern basis. In this case the amounts recognized may not require adjusting but the basis of accounting (going concern) shall change. 33

34 DISCLOSURE Date of authorization for issue. Who gave the authorization. Conditions relating to events that existed at the end of the reporting period which are brought to the attention of Management after the reporting period end. Update disclosures previously reported with details of new information received after the reporting period end e.g. contingent liabilities. 34

35 Answers Solution Case 1 Per paragraph 9 (a) of IAS 10, this is an adjusting event. The event took place during the reporting period and the settlement after the reporting period of the court case confirms that Maisha Limited had a present obligation at the end of the reporting period. The entity adjusts any previously recognized provision related to this court case in accordance with IAS 37 Provisions, Contingent Liabilities and Contingent Assets or recognises a new provision. 35

36 Answers Solution Case 2 Per paragraph 11 of IAS 10, this is a non-adjusting event. The decline in fair value does not normally relate to the condition of the investments at the end of the reporting period, but reflects circumstances that have arisen subsequently. Similarly, the entity does not update the amounts disclosed for the investments as at the end of the reporting period, although it may need to give additional disclosure. 36

37 Answers Solution Case 3 Per paragraph 9 (b ii) of IAS 10, this is an adjusting event. The sale of inventories after the reporting period can give evidence about the net realizable value of the inventory at the end of the reporting period. The inventory s net realizable value in early January 2018 is Kshs 120,000/= whereas the cost of the inventories at 31 December 2017 was Kshs 500,000/=. Using the IAS 2 Inventories rule that inventory is to be valued at the lower of cost and net realizable value, the inventory at the year-end should be included at Kshs 120,000 in the financial statements and therefore, the financial statements have to be adjusted to reflect this change. 37

38 Answers Solution Case 4 Per paragraph 12 of IAS 10 if an entity declares dividends to holders of equity instruments after the reporting period, the entity shall not recognize those dividends as a liability at the end of the reporting period. Therefore, the accounting treatment is incorrect and the accountant should reverse the transaction and include the dividend in the financial statements for the year-ended 31 December For 2017 it should be disclosed in a note and shown as a distribution in the statement of changes in equity. 38

39 Questions THANK YOU FOR SUPPORTING OUR INSTITUTE, horwatherastus@crowehorwath.co.ke Smart Decisions. Lasting Value 39

EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS

execution EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN execution Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Policies... 5 4.1 Selection and Application

execution EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN execution Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Policies... 5 4.1 Selection and Application

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors Objective 1 The objective of this Standard is to prescribe the criteria for selecting and changing accounting

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors Objective 1 The objective of this Standard is to prescribe the criteria for selecting and changing accounting

IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look

MPRA Munich Personal RePEc Archive IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September

MPRA Munich Personal RePEc Archive IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September

Accounting Policies, Changes in Accounting Estimates and Errors. Jalis Ahmad & Co. Chartered Accountants

International Accounting Standard (IAS-8) Accounting Policies, Changes in Accounting Estimates and Errors Objective Of IAS 8 O O O O O O it prescribes the criteria for: selection of accounting policies;

International Accounting Standard (IAS-8) Accounting Policies, Changes in Accounting Estimates and Errors Objective Of IAS 8 O O O O O O it prescribes the criteria for: selection of accounting policies;

International Accounting Standard 10 Events after the Reporting Period

International Accounting Standard 10 Events after the Reporting Period Objective 1 The objective of this Standard is to prescribe: when an entity should adjust its financial statements for events after

International Accounting Standard 10 Events after the Reporting Period Objective 1 The objective of this Standard is to prescribe: when an entity should adjust its financial statements for events after

IPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors

IPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors IPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors Objective To prescribe the criteria for selecting and changing

IPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors IPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors Objective To prescribe the criteria for selecting and changing

Events after the Reporting Period

IAS Standard 10 Events after the Reporting Period In April 2001 the International Accounting Standards Board (the Board) adopted IAS 10 Events After the Balance Sheet Date, which had originally been issued

IAS Standard 10 Events after the Reporting Period In April 2001 the International Accounting Standards Board (the Board) adopted IAS 10 Events After the Balance Sheet Date, which had originally been issued

Accounting Policies, Changes in Accounting Estimates and Errors

Indian Accounting Standard (Ind AS) 8 Accounting Policies, Changes in Accounting Estimates and Errors (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal

Indian Accounting Standard (Ind AS) 8 Accounting Policies, Changes in Accounting Estimates and Errors (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal

Financial Management for the Higher Education Sector Regulatory And Reporting Requirements

Financial Management for the Higher Education Sector Regulatory And Reporting Requirements CPA Anthony M. Njiru August 2018 Uphold public interest 1 Regulatory Background IFRSs International financial

Financial Management for the Higher Education Sector Regulatory And Reporting Requirements CPA Anthony M. Njiru August 2018 Uphold public interest 1 Regulatory Background IFRSs International financial

Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors In April 2001 the International Accounting Standards Board (IASB) adopted IAS 8 Net Profit or Loss for

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors In April 2001 the International Accounting Standards Board (IASB) adopted IAS 8 Net Profit or Loss for

Events after the Reporting Period

International Accounting Standard 10 Events after the Reporting Period This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 10 Events After the Balance Sheet Date was

International Accounting Standard 10 Events after the Reporting Period This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 10 Events After the Balance Sheet Date was

Accounting Policies, Changes in Accounting Estimates and Errors

Accounting Policies, Changes in Accounting Estimates and Errors SCOPE 1. Selection and application of accounting policies 2. Accounting for changes in accounting policies 3. Accounting for changes in accounting

Accounting Policies, Changes in Accounting Estimates and Errors SCOPE 1. Selection and application of accounting policies 2. Accounting for changes in accounting policies 3. Accounting for changes in accounting

RECOGNITION AND MEASUREMENT

Indian Accounting Standard ( Ind AS) 10 Events after the Reporting Period Contents Paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 3-7 RECOGNITION AND MEASUREMENT 8-13 Adjusting events after the reporting period

Indian Accounting Standard ( Ind AS) 10 Events after the Reporting Period Contents Paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 3-7 RECOGNITION AND MEASUREMENT 8-13 Adjusting events after the reporting period

NZ International Accounting Standard 8 (PBE) Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE))

Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE))") NZ International Accounting Standard 8 (PBE) Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE)) Issued November 2012 excluding consequential amendments resulting from early

NZ International Accounting Standard 8 (PBE) Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE)) Issued November 2012 excluding consequential amendments resulting from early

Sri Lanka Accounting Standard-LKAS 10. Events after the Reporting Period

Sri Lanka Accounting Standard-LKAS 10 Events after the Reporting Period CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 10 EVENTS AFTER THE REPORTING PERIOD paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 3 7 RECOGNITION

Sri Lanka Accounting Standard-LKAS 10 Events after the Reporting Period CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 10 EVENTS AFTER THE REPORTING PERIOD paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 3 7 RECOGNITION

Opinion n of 18 October 2012 on Central Government Accounting Standard 14, renamed Changes in accounting policies,

Opinion n 2012-06 of 18 October 2012 on Central Government Accounting Standard 14, renamed Changes in accounting policies, changes in accounting estimates, and corrections of errors The purpose of this

Opinion n 2012-06 of 18 October 2012 on Central Government Accounting Standard 14, renamed Changes in accounting policies, changes in accounting estimates, and corrections of errors The purpose of this

Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 8 Net Profit

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 8 Net Profit

New Zealand Equivalent to International Accounting Standard 10 Events after the Reporting Period (NZ IAS 10)

") New Zealand Equivalent to International Accounting Standard 10 Events after the Reporting Period (NZ IAS 10) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than

New Zealand Equivalent to International Accounting Standard 10 Events after the Reporting Period (NZ IAS 10) Issued November 2004 and incorporates amendments up to and including 30 June 2011 other than

Exposure Draft. Accounting Standard (AS) 5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors

5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors") Exposure Draft Accounting Standard (AS) 5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors (Last date for Comments: April 07, 2010) Issued by Accounting

Exposure Draft Accounting Standard (AS) 5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors (Last date for Comments: April 07, 2010) Issued by Accounting

CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1.

CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1 Presentation by: CPA Donald Omengo Manager, Audit, KPMG Kenya Monday, 4 th September

CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1 Presentation by: CPA Donald Omengo Manager, Audit, KPMG Kenya Monday, 4 th September

Opinion n of 18 October 2012 relating to changes in accounting policies, changes in accounting estimates, and corrections of errors

Opinion n 2012-05 of 18 October 2012 relating to changes in accounting policies, changes in accounting estimates, and corrections of errors Contents 1. SCOPE... 2 2. CHANGES IN ACCOUNTING POLICIES... 2

Opinion n 2012-05 of 18 October 2012 relating to changes in accounting policies, changes in accounting estimates, and corrections of errors Contents 1. SCOPE... 2 2. CHANGES IN ACCOUNTING POLICIES... 2

Exposure Draft. Accounting Standard (AS) 4 (Revised 20XX) (Corresponding to IAS 10) Events after the Reporting Period

4 (Revised 20XX) (Corresponding to IAS 10) Events after the Reporting Period") Exposure Draft Accounting Standard (AS) 4 (Revised 20XX) (Corresponding to IAS 10) Events after the Reporting Period (Last date for Comments: February 01, 2010) Issued by Accounting Standards Board The

Exposure Draft Accounting Standard (AS) 4 (Revised 20XX) (Corresponding to IAS 10) Events after the Reporting Period (Last date for Comments: February 01, 2010) Issued by Accounting Standards Board The

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 14 EVENTS AFTER THE REPORTING DATE (PBE IPSAS 14)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 14 EVENTS AFTER THE REPORTING DATE (PBE IPSAS 14) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 14 EVENTS AFTER THE REPORTING DATE (PBE IPSAS 14) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

Separate Financial Statements

IAS Standard 27 Separate Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 27 Consolidated Financial Statements and Accounting for Investments in Subsidiaries,

IAS Standard 27 Separate Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 27 Consolidated Financial Statements and Accounting for Investments in Subsidiaries,

Table 1 IPSAS and Equivalent IFRS Summary 2

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

Understanding ASPE. Section 1506, Accounting Changes

Understanding ASPE Section 1506, Accounting Changes Seven questions for private business owners: Accounting Changes A better working world begins with better questions. Asking better questions leads to

Understanding ASPE Section 1506, Accounting Changes Seven questions for private business owners: Accounting Changes A better working world begins with better questions. Asking better questions leads to

IAS 10 Events after the Reporting Period

IAS 10 Events after the Reporting Period By Mr. Conor Foley, B. Comm., MAcc., FCA, Dip IFR Examiner: Formation 2 Financial Accounting This article provides information and application in relation to IAS

IAS 10 Events after the Reporting Period By Mr. Conor Foley, B. Comm., MAcc., FCA, Dip IFR Examiner: Formation 2 Financial Accounting This article provides information and application in relation to IAS

Table 1 IPSAS and Equivalent IFRS Summary 2

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

International Accounting Standard 27 Separate Financial Statements. Objective. Scope. Definitions

International Accounting Standard 27 Separate Financial Statements Objective 1 The objective of this Standard is to prescribe the accounting and disclosure requirements for investments in subsidiaries,

International Accounting Standard 27 Separate Financial Statements Objective 1 The objective of this Standard is to prescribe the accounting and disclosure requirements for investments in subsidiaries,

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE EVENTS AFTER THE REPORTING DATE () Issued by the Accounting Standards Board February 2010 Acknowledgement The Standard of

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE EVENTS AFTER THE REPORTING DATE () Issued by the Accounting Standards Board February 2010 Acknowledgement The Standard of

THE FINANCIAL REPORTING WORKSHOP- A FOCUS ON SMEs. IFRS for SMEs Section 10 Accounting Policies, estimates & Errors

THE FINANCIAL REPORTING WORKSHOP- A FOCUS ON SMEs 17th 18th NOVEMBER SIRIKWA HOTEL, ELDORET IFRS for SMEs Section 10 Accounting Policies, estimates & Errors Credibility Professionalism Accountability 1

THE FINANCIAL REPORTING WORKSHOP- A FOCUS ON SMEs 17th 18th NOVEMBER SIRIKWA HOTEL, ELDORET IFRS for SMEs Section 10 Accounting Policies, estimates & Errors Credibility Professionalism Accountability 1

Events after the Reporting Period

HKAS 10 Revised February 2014September 2018 Hong Kong Accounting Standard 10 Events after the Reporting Period HKAS 10 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This

HKAS 10 Revised February 2014September 2018 Hong Kong Accounting Standard 10 Events after the Reporting Period HKAS 10 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2018 sued but not yet effective Introduction This document is applicable for Tier

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2018 sued but not yet effective Introduction This document is applicable for Tier

Events After the Reporting Date

IFAC Public Sector Committee Issued December 2001 IPSAS 14 Events After the Reporting Date International Public Sector Accounting Standard Issued by the International Federation of Accountants This Standard

IFAC Public Sector Committee Issued December 2001 IPSAS 14 Events After the Reporting Date International Public Sector Accounting Standard Issued by the International Federation of Accountants This Standard

IAS 8 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS

1 IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors IAS 8 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS FACT SHEET 2 IAS 8 Accounting Policies, Changes in Accounting

1 IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors IAS 8 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS FACT SHEET 2 IAS 8 Accounting Policies, Changes in Accounting

Presentation of Financial Statements

Presentation of Financial Statements 2016 Deloitte & Touche 1 2015 Deloitte Touche Limited Index 1. Objective 2. Scope 3. Objective of Financial Statements 4. Components of Financial Statements 5. Fair

Presentation of Financial Statements 2016 Deloitte & Touche 1 2015 Deloitte Touche Limited Index 1. Objective 2. Scope 3. Objective of Financial Statements 4. Components of Financial Statements 5. Fair

Table 1 IPSAS and Equivalent IFRS Summary 1

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

FUNDAMENTALS OF IFRS

FUNDAMENTALS OF IFRS 15.1 FUNDAMENTALS OF IFRS CHAPTER 15 Accounting Policies, Changes in Accounting Estimates and Errors (IAS 8) 15.2 CHAPTER FIFTEEN Introduction Accounting Policies, Changes in Accounting

FUNDAMENTALS OF IFRS 15.1 FUNDAMENTALS OF IFRS CHAPTER 15 Accounting Policies, Changes in Accounting Estimates and Errors (IAS 8) 15.2 CHAPTER FIFTEEN Introduction Accounting Policies, Changes in Accounting

IAS 10 Events After the Reporting Period - A Closer Look

MPRA Munich Personal RePEc Archive IAS 10 Events After the Reporting Period - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. October 2008 Online at https://mpra.ub.uni-muenchen.de/36783/

MPRA Munich Personal RePEc Archive IAS 10 Events After the Reporting Period - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. October 2008 Online at https://mpra.ub.uni-muenchen.de/36783/

International Public Sector Accounting Standard 32 Service Concession Arrangements: Grantor IPSASB Basis for Conclusions

International Public Sector Accounting Standard 32 Service Concession Arrangements: Grantor IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts, Consultation

International Public Sector Accounting Standard 32 Service Concession Arrangements: Grantor IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts, Consultation

Click to edit Master title style

Click to edit Master title style Accounting policies, estimates and errors (LKAS 8) Tishan Subasinghe Partner BDO Partners LKAS 8: Overview Objective Scope Definitions Accounting policies Impracticability

Click to edit Master title style Accounting policies, estimates and errors (LKAS 8) Tishan Subasinghe Partner BDO Partners LKAS 8: Overview Objective Scope Definitions Accounting policies Impracticability

IAS 1R- Presentation of Financial Statements. Introduction to IFRS / Ind AS

IAS 1R- Presentation of Financial Statements Introduction to IFRS / Ind AS IAS 1R- Presentation of financial statements Objective The objective of this Standard is to prescribe the basis for presentation

IAS 1R- Presentation of Financial Statements Introduction to IFRS / Ind AS IAS 1R- Presentation of financial statements Objective The objective of this Standard is to prescribe the basis for presentation

SLAS 10. Sri Lanka Accounting Standard SLAS 10. Net Profit or Loss for the Period, Fundamental Errors and Changes in Accounting Policies

Sri Lanka Accounting Standard SLAS 10 Net Profit or Loss for the Period, Fundamental Errors and Changes in Accounting Policies 138 Contents Sri Lanka Accounting Standard SLAS 10 Net Profit or Loss for

Sri Lanka Accounting Standard SLAS 10 Net Profit or Loss for the Period, Fundamental Errors and Changes in Accounting Policies 138 Contents Sri Lanka Accounting Standard SLAS 10 Net Profit or Loss for

IAS 34 Interim Financial Reporting

// Shreeji // IAS 34 Interim Financial Reporting 1. Introduction IAS 34 Interim Financial Reporting was issued by the International Accounting Standards Committee in February 1998. A limited amendment

// Shreeji // IAS 34 Interim Financial Reporting 1. Introduction IAS 34 Interim Financial Reporting was issued by the International Accounting Standards Committee in February 1998. A limited amendment

This article discusses the selection of and changes in accounting policies, changes in accounting estimates and corrections of errors.

HKAS 8 Accounting policies, changes in accounting estimates and errors (Relevant to AAT Examination Paper 7 Financial Accounting) Dr. M H Ho, School of Continuing & Professional Studies, The Chinese University

HKAS 8 Accounting policies, changes in accounting estimates and errors (Relevant to AAT Examination Paper 7 Financial Accounting) Dr. M H Ho, School of Continuing & Professional Studies, The Chinese University

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures Presentation by: By Mr. Abdullatif Essajee Wednesday, 18 th October 2017 Uphold public interest IPSAS 1: Presentation

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures Presentation by: By Mr. Abdullatif Essajee Wednesday, 18 th October 2017 Uphold public interest IPSAS 1: Presentation

FIRST TIME ADOPTION OF ACCRUAL BASIS IPSASS

Meeting Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 17 20, 2013 Agenda Item 6 For: Approval Discussion Information FIRST TIME ADOPTION OF

Meeting Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 17 20, 2013 Agenda Item 6 For: Approval Discussion Information FIRST TIME ADOPTION OF

Improvements to IPSAS, 2018

Exposure Draft 65 April 2018 Comments due: July 15, 2018 Proposed International Public Sector Accounting Standard Improvements to IPSAS, 2018 This document was developed and approved by the International

Exposure Draft 65 April 2018 Comments due: July 15, 2018 Proposed International Public Sector Accounting Standard Improvements to IPSAS, 2018 This document was developed and approved by the International

ES IIAS 8 -ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS

ES IIAS 8 -ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS Presentation by: CPA Polycarp.O. Obara Accountant Management information at KPA- Mombasa Uphold public interest 2/24/2017 1 OVERVIEW

ES IIAS 8 -ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS Presentation by: CPA Polycarp.O. Obara Accountant Management information at KPA- Mombasa Uphold public interest 2/24/2017 1 OVERVIEW

Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies

Accounting Standard (AS) 5 (revised 1997) Net Profit or Loss for the Period 89 Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies Contents OBJECTIVE SCOPE Paragraphs

Accounting Standard (AS) 5 (revised 1997) Net Profit or Loss for the Period 89 Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies Contents OBJECTIVE SCOPE Paragraphs

IFRS pocket guide inform.pwc.com

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

Table 1 IPSAS and Equivalent IFRS Summary*

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Financial Reporting in Hyperinflationary Economies

International Accounting Standard 29 Financial Reporting in Hyperinflationary Economies This version includes amendments resulting from IFRSs issued up to 31 December 2010. IAS 29 Financial Reporting in

International Accounting Standard 29 Financial Reporting in Hyperinflationary Economies This version includes amendments resulting from IFRSs issued up to 31 December 2010. IAS 29 Financial Reporting in

Amendments to IFRS for SMEs

A C C O U N T I N G U P D A T E ( I F R S f o r S M E s ) s to IFRS for SMEs Introduction The International Accounting Standards Board (IASB) has published amendments to its 'International Financial Reporting

A C C O U N T I N G U P D A T E ( I F R S f o r S M E s ) s to IFRS for SMEs Introduction The International Accounting Standards Board (IASB) has published amendments to its 'International Financial Reporting

Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (IASB) adopted Presentation of Financial Statements, which had originally

International Accounting Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (IASB) adopted Presentation of Financial Statements, which had originally

First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

Presentation of Financial Statements

IAS Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 1 Presentation of Financial Statements, which had originally been

IAS Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 1 Presentation of Financial Statements, which had originally been

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

1 IAS 10 Events after the Reporting Period IAS 10 EVENTS AFTER THE REPORTING PERIOD FACT SHEET

1 IAS 10 Events after the Reporting Period IAS 10 EVENTS AFTER THE REPORTING PERIOD FACT SHEET 2 IAS 10 Events after the Reporting Period This fact sheet is based on existing requirements as at 31 December

1 IAS 10 Events after the Reporting Period IAS 10 EVENTS AFTER THE REPORTING PERIOD FACT SHEET 2 IAS 10 Events after the Reporting Period This fact sheet is based on existing requirements as at 31 December

ASPE at a Glance. Standards Included in Topic

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

New Accounting Standards and Interpretations for Tier 1 Public Sector and Notfor-Profit. Entities. 31 December 2016

New Accounting Standards and Interpretations for Tier 1 Public Sector and Notfor-Profit Public Benefit Entities 31 December Introduction This document is applicable for Tier 1 Public Benefit Entities (PBEs)

New Accounting Standards and Interpretations for Tier 1 Public Sector and Notfor-Profit Public Benefit Entities 31 December Introduction This document is applicable for Tier 1 Public Benefit Entities (PBEs)

International GAAP Disclosure Checklist

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

The Effects of Changes in Foreign Exchange Rates

International Public Sector Accounting Standards Board IPSAS 4 Issued January 2007 International Public Sector Accounting Standard The Effects of Changes in Foreign Exchange Rates International Public

International Public Sector Accounting Standards Board IPSAS 4 Issued January 2007 International Public Sector Accounting Standard The Effects of Changes in Foreign Exchange Rates International Public

CHAPTER 2 UPDATE. alternative method is preferable to the method replaced. IAS 8 states that the change must result in more relevant information.

CHAPTER 2 UPDATE In May 2005, the FASB adopted Statement of Financial Accounting Standards (SFAS) No. 154, Accounting Changes and Error Corrections, a replacement of APB Opinion No. 20, Accounting Changes

CHAPTER 2 UPDATE In May 2005, the FASB adopted Statement of Financial Accounting Standards (SFAS) No. 154, Accounting Changes and Error Corrections, a replacement of APB Opinion No. 20, Accounting Changes

IFRS for SMEs (proposals) Pocket Guide 2007

Pocket Guide 2007") IFRS for SMEs (proposals) Pocket Guide 2007 PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation. Drawing on the knowledge and skills of 125,000 people in 142

IFRS for SMEs (proposals) Pocket Guide 2007 PricewaterhouseCoopers (www.pwc.com) is the world s largest professional services organisation. Drawing on the knowledge and skills of 125,000 people in 142

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 8 INTERESTS IN JOINT VENTURES (PBE IPSAS 8)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 8 INTERESTS IN JOINT VENTURES (PBE IPSAS 8) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 8 INTERESTS IN JOINT VENTURES (PBE IPSAS 8) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential

Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies

90 Accounting Standard (AS) 5 (revised 1997) Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies Contents OBJECTIVE SCOPE Paragraphs 1-3 DEFINITIONS 4 NET PROFIT OR

90 Accounting Standard (AS) 5 (revised 1997) Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies Contents OBJECTIVE SCOPE Paragraphs 1-3 DEFINITIONS 4 NET PROFIT OR

International Accounting Standard 34 Interim Financial Reporting. Objective. Scope. Definitions. Content of an interim financial report IAS 34

International Accounting Standard 34 Interim Financial Reporting Objective The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles

International Accounting Standard 34 Interim Financial Reporting Objective The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2017 New Accounting Standards and Interpretations for Tier 1 Public Benefit Entities

New Accounting Standards and Interpretations for Tier 1 Public Sector and Not-for-Profit Public Benefit Entities 31 March 2017 New Accounting Standards and Interpretations for Tier 1 Public Benefit Entities

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International GAAP Disclosure Checklist

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 1 Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 1 Presentation of Financial Statements

FOR THE ACCOMPANYING DOCUMENT LISTED BELOW, SEE PART B OF THIS EDITION BASIS FOR CONCLUSIONS

NIIF-IFRS International Financial Report... Part A International Accounting Stand... IFRS 2014- IAS 29 FINANCIAL REPORTING IN HYPERINFLATIONARY ECONOMIES IAS 29 Financial Reporting in Hyperinflationary

NIIF-IFRS International Financial Report... Part A International Accounting Stand... IFRS 2014- IAS 29 FINANCIAL REPORTING IN HYPERINFLATIONARY ECONOMIES IAS 29 Financial Reporting in Hyperinflationary

IFRS vs Prudential Guidelines. Interest revenue recognition on non-performing loans in IFRS financial statements

IFRS vs Prudential Guidelines Interest revenue recognition on non-performing loans in IFRS financial statements Preamble There is currently a divergence between IFRS requirements and the Prudential Guidelines

IFRS vs Prudential Guidelines Interest revenue recognition on non-performing loans in IFRS financial statements Preamble There is currently a divergence between IFRS requirements and the Prudential Guidelines

Exposure Draft 66 August 2018 Comments due: October 22, Proposed International Public Sector Accounting Standard

Exposure Draft 66 August 2018 Comments due: October 22, 2018 Proposed International Public Sector Accounting Standard Long-term Interests in Associates and Joint Ventures (Amendments to IPSAS 36) and Prepayment

Exposure Draft 66 August 2018 Comments due: October 22, 2018 Proposed International Public Sector Accounting Standard Long-term Interests in Associates and Joint Ventures (Amendments to IPSAS 36) and Prepayment

International Public Sector Accounting Standard 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) IPSASB Basis for Conclusions

IPSASB Basis for Conclusions") International Public Sector Accounting Standard 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts,

International Public Sector Accounting Standard 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts,

Interim Financial Reporting

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

Stay informed. Visit IFRS pocket guide 2012

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

PUBLIC BENEFIT ENTITY INTERNATIONAL FINANCIAL REPORTING STANDARD 5 NON-CURRENT ASSETS HELD FOR SALE AND DISCONTINUED OPERATIONS (PBE IFRS 5)

") PUBLIC BENEFIT ENTITY INTERNATIONAL FINANCIAL REPORTING STANDARD 5 NON-CURRENT ASSETS HELD FOR SALE AND DISCONTINUED OPERATIONS (PBE IFRS 5) Issued May 2013 This Standard was issued by the New Zealand

PUBLIC BENEFIT ENTITY INTERNATIONAL FINANCIAL REPORTING STANDARD 5 NON-CURRENT ASSETS HELD FOR SALE AND DISCONTINUED OPERATIONS (PBE IFRS 5) Issued May 2013 This Standard was issued by the New Zealand

Click to edit Master title style. Presentation of Financial Statements ( LKAS 1)

") 1 Click to edit Master title style Presentation of Financial Statements ( LKAS 1) 2 1 LKAS 1 Presentation of Financial Statements 3 LKAS 1: Overview Objective Scope Components of financial statements Overall

1 Click to edit Master title style Presentation of Financial Statements ( LKAS 1) 2 1 LKAS 1 Presentation of Financial Statements 3 LKAS 1: Overview Objective Scope Components of financial statements Overall

Sri Lanka Accounting Standard LKAS 27. Separate Financial Statements

Sri Lanka Accounting Standard LKAS 27 Separate Financial Statements CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 27 SEPARATE FINANCIAL STATEMENTS paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 PREPARATION

Sri Lanka Accounting Standard LKAS 27 Separate Financial Statements CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 27 SEPARATE FINANCIAL STATEMENTS paragraphs OBJECTIVE 1 SCOPE 2 DEFINITIONS 4 PREPARATION

Consolidated and Separate Financial Statements

International Accounting Standard 27 Consolidated and Separate Financial Statements This version was issued in January 2008 with an effective date of 1 July 2009. It includes subsequent amendments resulting

International Accounting Standard 27 Consolidated and Separate Financial Statements This version was issued in January 2008 with an effective date of 1 July 2009. It includes subsequent amendments resulting

Presentation of Financial Statements

IAS 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (Board) adopted IAS 1 Presentation of Financial Statements, which had originally been issued by the

IAS 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (Board) adopted IAS 1 Presentation of Financial Statements, which had originally been issued by the

REVENUE APPROACH TO IFRS 15

Meeting: Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 19 22, 2018 Agenda Item 8 For: Approval Discussion Information From: Amon Dhliwayo REVENUE

Meeting: Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 19 22, 2018 Agenda Item 8 For: Approval Discussion Information From: Amon Dhliwayo REVENUE

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

IFRIC DRAFT INTERPRETATION D13

IFRIC International Financial Reporting Interpretations Committee International Accounting Standards Board IFRIC DRAFT INTERPRETATION D13 Service Concession Arrangements The Financial Asset Model Comments

IFRIC International Financial Reporting Interpretations Committee International Accounting Standards Board IFRIC DRAFT INTERPRETATION D13 Service Concession Arrangements The Financial Asset Model Comments

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

Non-current Assets Held for Sale and Discontinued Operations

International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations In April 2001 the International Accounting Standards Board (IASB) adopted IAS 35 Discontinuing

International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations In April 2001 the International Accounting Standards Board (IASB) adopted IAS 35 Discontinuing

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

First-time Adoption of International Financial Reporting Standards

IFRS Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (the Board) adopted SIC-8 First-time Application of IASs as

IFRS Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (the Board) adopted SIC-8 First-time Application of IASs as

Interim Financial Reporting

International Accounting Standard 34 Interim Financial Reporting This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 34 Interim Financial Reporting was issued by the

International Accounting Standard 34 Interim Financial Reporting This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 34 Interim Financial Reporting was issued by the

IMPORTANT TAKEAWAYS ON IFRS

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

FIRE AWARD 2017 EVALUATION TOOL

FIRE AWARD 2017 EVALUATION TOOL CPA Cliff Nyandoro FiRe Awards Secretariat Hilton Hotel, Nairobi Wednesday, 13 September 2017 1 Introduction The evaluation tool updates focused on amendments to the existing

FIRE AWARD 2017 EVALUATION TOOL CPA Cliff Nyandoro FiRe Awards Secretariat Hilton Hotel, Nairobi Wednesday, 13 September 2017 1 Introduction The evaluation tool updates focused on amendments to the existing

Sri Lanka Accounting Standard SLFRS 1. First-time Adoption of Sri Lanka Accounting Standards (SLFRSs)

") Sri Lanka Accounting Standard SLFRS 1 First-time Adoption of Sri Lanka Accounting Standards (SLFRSs) CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD SLFRS 1 FIRST-TIME ADOPTION OF SRI LANKA ACCOUNTING

Sri Lanka Accounting Standard SLFRS 1 First-time Adoption of Sri Lanka Accounting Standards (SLFRSs) CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD SLFRS 1 FIRST-TIME ADOPTION OF SRI LANKA ACCOUNTING

PUBLIC BENEFIT ENTITY STANDARDS. IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs

PUBLIC BENEFIT ENTITY STANDARDS IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs Prepared June 2012 Issued November 2013 This document contains assessments of the impact for public sector PBEs of transitioning

PUBLIC BENEFIT ENTITY STANDARDS IMPACT ASSESSMENT FOR PUBLIC SECTOR PBEs Prepared June 2012 Issued November 2013 This document contains assessments of the impact for public sector PBEs of transitioning

Good Group (International) Limited

Limited") IFRS Core Tools Good Group (International) Limited Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key... 2 Introduction...

IFRS Core Tools Good Group (International) Limited Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key... 2 Introduction...

NZ IFRS 1 COPYRIGHT. External Reporting Board ( XRB ) 2011

2011") New Zealand Equivalent to International Financial Reporting Standard 1 First-time Adoption of New Zealand Equivalents to International Financial Reporting Standards (NZ IFRS 1) Issued December 2008 and

New Zealand Equivalent to International Financial Reporting Standard 1 First-time Adoption of New Zealand Equivalents to International Financial Reporting Standards (NZ IFRS 1) Issued December 2008 and

Non-current Assets Held for Sale and Discontinued Operations

International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations In April 2001 the International Accounting Standards Board (IASB) adopted IAS 35 Discontinuing

International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations In April 2001 the International Accounting Standards Board (IASB) adopted IAS 35 Discontinuing

International GAAP Disclosure Checklist

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any