ASIA POLY HOLDINGS BERHAD (Company No. No A) (Incorporated in in Malaysia under under the the Companies Act Act 2016) 2016)

|

|

|

- Willis Dawson

- 5 years ago

- Views:

Transcription

1 THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the course of action to be taken, you should consult your stockbroker, bank manager, solicitor, accountant or other professional advisers immediately. THIS THIS CIRCULAR IS IS IMPORTANT AND AND REQUIRES YOUR IMMEDIATE ATTENTION. Bursa Malaysia Securities Berhad ( Bursa Securities ) has not perused the contents of this Circular in relation to the Proposed If Amendments you If you are are in in any (as any doubt defined doubt as herein) as to to the the prior course to its of of action issuance action to pursuant to be be taken, taken, to you Guidance you should Note consult 22 of your the your ACE stockbroker, Market Listing bank bank Requirements manager, solicitor, of Bursa accountant Securities. or Bursa or other other Securities professional takes advisers no responsibility immediately. for the contents of this Circular, makes no representation as to its accuracy or Bursa completeness Bursa Malaysia and Securities expressly Berhad disclaims ( Bursa any Securities ) liability whatsoever has has not not for perused any loss the the howsoever contents of arising of this this Circular from or in in in reliance relation upon to to the the the Proposed whole or Amendments any part of the (as (as contents defined herein) of this Circular. prior prior to its to its issuance pursuant to Guidance to Note Note of of the the ACE ACE Market Listing Requirements of of Bursa Bursa Securities. This Circular Bursa Bursa has Securities been reviewed takes takes no by no TA responsibility Securities Holdings for for the the contents Berhad, of who of this this Circular, the Adviser makes makes to Asia no no Poly representation Holdings Berhad as as to to its ( Asia its accuracy Poly or or completeness Company ) and for and expressly the Proposed disclaims Rights any Issue any liability of ICPS whatsoever with Warrants for for any any (as loss defined loss howsoever herein), arising Proposed from from Acquisition or or in in reliance (as upon defined upon the the whole herein) whole or and or any Proposed any part part of of the Diversification the contents of of this (as this Circular. defined herein). This This Circular has has been been reviewed by by TA TA Securities Holdings Berhad, who who is the is the Adviser to Asia to Asia Poly Poly Holdings Berhad ( Asia Poly Poly or or Company ) for for the the Proposed Rights Rights Issue Issue of of ICPS ICPS with with Warrants (as (as defined herein), Proposed Acquisition (as (as defined herein) and and Proposed Diversification (as (as defined herein). ASIA POLY HOLDINGS BERHAD (Company No. No A) (Incorporated in in Malaysia under under the the Companies Act Act 2016) 2016) CIRCULAR TO TO SHAREHOLDERS IN IN RELATION TO TO THE THE PART A A (I) (I) (II) (II) (III) (III) (IV) (IV) (V) (V) PROPOSED RIGHTS ISSUE OF OF ICPS WITH WARRANTS; PROPOSED ACQUISITION; PROPOSED VARIATION; PROPOSED DIVERSIFICATION; AND AND PROPOSED AMENDMENTS PART B B INDEPENDENT ADVICE LETTER FROM INTER-PACIFIC SECURITIES SDN SDN BHD BHD TO TO THE THE NON- INTERESTED SHAREHOLDERS OF OF ASIA POLY IN IN RELATION TO TO THE THE PROPOSED ACQUISITION AND AND NOTICE OF OF EXTRAORDINARY GENERAL MEETING Adviser for Part A (I), (II) and (IV) Independent Adviser for for Part B B (14948-M) (A Participating Organisation of Bursa Malaysia Securities Berhad) The Notice of Extraordinary General Meeting ( EGM ) of our Company, to be held at Conference Room of Asia Poly Industrial Sdn Bhd, Lot 758, Jalan Haji Sirat, Mukim Kapar, Klang, Selangor Darul Ehsan on Friday, 25 August 2017 at p.m. or any The adjournment Notice of Extraordinary thereof, together General with Meeting the Proxy ( EGM ) Form are of enclosed our Company, in this to Circular. be held at Conference Room of Asia Poly Industrial Sdn Bhd, Lot 758, Jalan Haji Sirat, Mukim Kapar, Klang, Selangor Darul Ehsan on Friday, 25 August 2017 at p.m. A shareholder or any adjournment entitled thereof, to attend together and vote with at the the EGM Proxy is Form entitled are to enclosed appoint in up this to Circular. 2 proxies to attend and vote instead of him/her. The Proxy Form must be lodged at the Registered Office of our Company at 308, Block A (3 rd Floor), Kelana Business Centre, 97, Jalan SS A 7/2, shareholder Kelana Jaya, entitled to attend Petaling and Jaya, vote Selangor at the EGM Darul is entitled Ehsan not to appoint later than up 48 to 2 hours proxies before to attend the time and set vote for instead the EGM of him/her. or at any The adjournment Proxy Form thereof. must be The lodged lodgement at the of Registered the Proxy Office Form will of our not Company preclude at you 308, from Block attending A (3 rd and Floor), voting Kelana in person Business at the Centre, EGM should 97, Jalan you SS subsequently 7/2, Kelana wish Jaya, to do so. Petaling Jaya, Selangor Darul Ehsan not later than 48 hours before the time set for the EGM or at any adjournment thereof. The lodgement of the Proxy Form will not preclude you from attending and voting in person at the EGM should Last you day, subsequently date and time wish for to lodging do so. the Proxy Form Day, date and time of the EGM Last day, date and time for lodging the Proxy Form : : : Wednesday, 23 August 2017 at p.m. Friday, 25 August 2017 at p.m. Wednesday, 23 August 2017 at p.m. Day, date and time of the EGM This This Circular is is dated dated : July Friday, July August 2017 at p.m. This Circular is dated 27 July 2017

2 CIRCULAR TO SHAREHOLDERS IN RELATION TO THE: (I) PROPOSED RENOUNCEABLE RIGHTS ISSUE OF UP TO 390,023,853 NEW IRREDEEMABLE CONVERTIBLE PREFERENCE SHARES IN ASIA POLY ( ICPS ) ON THE BASIS OF 1 ICPS FOR EVERY 1 EXISTING ORDINARY SHARE IN ASIA POLY ( ASIA POLY SHARE OR SHARE ) HELD AT AN ENTITLEMENT DATE TO BE DETERMINED LATER, TOGETHER WITH UP TO 97,505,963 FREE DETACHABLE WARRANTS ( WARRANTS ) ON THE BASIS OF 1 WARRANT FOR EVERY 4 ICPS SUBSCRIBED FOR ( PROPOSED RIGHTS ISSUE OF ICPS WITH WARRANTS ); (II) (III) (IV) (V) PROPOSED ACQUISITION OF 500,000 ORDINARY SHARES IN HIGH RESERVE LAND SDN BHD ( HRLSB ), REPRESENTING THE ENTIRE EQUITY INTEREST IN HRLSB FOR A PURCHASE CONSIDERATION OF RM14,800,000 ( PURCHASE CONSIDERATION ) TO BE SATISFIED VIA A COMBINATION OF RM8,000,000 IN CASH AND THE ISSUANCE OF 42,027,194 NEW ASIA POLY SHARES AT AN ISSUE PRICE OF RM EACH ( PROPOSED ACQUISITION ); PROPOSED VARIATION OF THE UTILISATION OF PROCEEDS RAISED FROM THE TWO- CALL RIGHTS ISSUE OF SHARES WITH WARRANTS OF ASIA POLY WHICH WAS COMPLETED ON 21 DECEMBER 2015 ( PROPOSED VARIATION ); PROPOSED DIVERSIFICATION OF THE EXISTING BUSINESS OF ASIA POLY AND ITS SUBSIDIARIES TO INCLUDE PROPERTY DEVELOPMENT ( PROPOSED DIVERSIFICATION ); AND PROPOSED AMENDMENTS TO THE CONSTITUTION (MEMORANDUM AND ARTICLES OF ASSOCIATION) OF ASIA POLY ( PROPOSED AMENDMENTS )

3 DEFINITIONS Unless otherwise indicated, the following words and abbreviations shall have the following meaning in this Circular and the accompanying appendices: 5D-VWAP : 5-day volume weighted average market price ACE Market : ACE Market of Bursa Securities Act : Companies Act 2016 Adjustment Warrants : Up to 8,237,661 additional Warrants 2015/2020 to be issued pursuant to the Proposed Rights Issue of ICPS with Warrants Advances by DYBL : The total advances of RM6,019, and RM7,017, made by DYBL to HRLSB as at the date of the SSA and the LPD, respectively Ambank : Ambank (M) Berhad Announcements : Announcements in relation to the Proposals dated 25 January 2017 and 21 February 2017 Announcement LPD : 24 January 2017, being the latest practicable date prior to the Announcements Asia Poly or Company : Asia Poly Holdings Berhad Asia Poly Group or Group : Asia Poly and our subsidiaries Asia Poly Shares or Shares : Ordinary shares in Asia Poly Board : Board of Directors of our Company Bursa Securities : Bursa Malaysia Securities Berhad CAGR : Compound annual growth rate Cash Consideration : Cash payment of RM8,000,000 being part payment for the Purchase Consideration Circular : This circular to our shareholders dated 27 July 2017 Code : Malaysian Code on Take-overs and Mergers 2016 Consideration Shares : 42,027,194 new Asia Poly Shares to be issued at an issue price of RM each to the Vendors to partly satisfy (i.e., RM6,800,000) the Purchase Consideration for the Proposed Acquisition Conversion Ratio and Conversion Price : Conversion ratio and conversion price of the ICPS which have been fixed at either 2 ICPS to be converted into 1 Asia Poly Share or a combination of 1 ICPS and RM0.05 in cash for 1 Asia Poly Share Deed Poll : The document constituting the Warrants to be executed by our Company Director : A natural person who holds a directorship in our Company, whether in an executive or non-executive capacity, and shall have the meaning given in Section 2 of the Act and Section 2(1) of the Capital Markets and Services Act 2007 DYBL or Undertaking Shareholder : Dato Yeo Boon Leong, a major shareholder and Executive Chairman of our Company as well as a director and the controlling shareholder of HRLSB i

4 DEFINITIONS (CONT D) EGM : Extraordinary general meeting Entitled Shareholders : The shareholders of our Company whose names appear in our Company s Record of Depositors on the Entitlement Date Entitlement Date : The date (to be determined by our Board and announced later by our Company) as at the close of business on which the names of our shareholders must appear in the Record of Depositors in order to be entitled to the Proposed Rights Issue of ICPS with Warrants EPS : Earnings per Share Existing business : Our group s principal business of investment holding and the manufacture and sale of cast acrylic products FPE : Financial period ended/ending, as the case may be FYE : Financial year ended/ending, as the case may be GDC : Gross development cost GDV : Gross development value HRLSB : High Reserve Land Sdn Bhd HRLSB Shares : Ordinary shares in HRLSB IAL : Independent Advice Letter ICPS : Up to 390,023,853 new irredeemable convertible preference shares in Asia Poly to be issued pursuant to the Proposed Rights Issue of ICPS with Warrants IMR Report : Independent market research report on the cast acrylic sheet industry in Malaysia dated 17 July 2017 prepared by Infobusiness Infobusiness : Infobusiness Research & Consulting Sdn Bhd, the independent market researcher Interested Person : DYBL, an interested Director and interested major shareholder of our Company Inter-Pacific Securities or Independent Adviser : Inter-Pacific Securities Sdn Bhd Land or Subject Property : A parcel of commercial land with approved Planning Permission located at Mukim of Semenyih, District of Ulu Langat, Selangor Darul Ehsan LAT : Loss after tax LBT : Loss before tax Listing Requirements : ACE Market Listing Requirements of Bursa Securities LPD : 30 June 2017, being the latest practicable date prior to the printing of this Circular M&A : Memorandum and Articles of Association ii

5 DEFINITIONS (CONT D) Master Layout Plan : Master Layout Plan dated 25 October 2016 (Reference No.: MPKJ.JPP/BPB/ (PD)) Maximum Scenario : Assuming all shareholders will subscribe for their entitlements in full. The ICPS are converted at 1 ICPS and cash of RM0.05 for 1 Asia Poly Share MFRS : Malaysian Financial Reporting Standards Minimum Scenario or Minimum Subscription Level : Assuming only the Undertaking Shareholder subscribes to his entitlement pursuant to the Undertaking and subscription by the underwriters pursuant to the underwriting arrangements of the ICPS. The ICPS are converted at 2 ICPS for 1 Asia Poly Share NA : Net assets Planning Permission : Planning Permission letter dated 1 February 2017 (Reference No.: (32) dlm. MPKj.JPP/BPB/KM3/ ) Private Placement : 30,319,000 Asia Poly Shares placed out at an issue price of RM0.16 per Asia Poly Share pursuant to a private placement which was completed on 8 March 2017 Proposals : Proposed Rights Issue of ICPS with Warrants, Proposed Acquisition, Proposed Variation, Proposed Diversification and Proposed Amendments, collectively Proposed Acquisition : Proposed acquisition of 500,000 HRLSB Shares, representing the entire equity interest in HRLSB for the Purchase Consideration, to be satisfied via a combination of the Cash Consideration and the issuance of the Consideration Shares at an issue price of RM each Proposed Amendments : Proposed amendments to the Constitution (M&A) of our Company Proposed Development : Proposed development of the Land which was approved as per the approved Master Layout Plan and approved Planning Permission Proposed Diversification : Proposed diversification of the existing business of our Group to include property development Proposed Rights Issue of ICPS with Warrants : Proposed renounceable rights issue of up to 390,023,853 new ICPS on the basis of 1 ICPS for every 1 existing Asia Poly Share held at the Entitlement Date, together with up to 97,505,963 Warrants on the basis of 1 Warrant for every 4 ICPS subscribed for Proposed Variation : Proposed variation of the utilisation of proceeds raised from the Two- Call Rights Issue of Shares with Warrants Purchase Consideration : Purchase consideration of RM14,800,000 pursuant to the Proposed Acquisition R&D : Research and development Rights Circular : Circular to our shareholders dated 6 October 2015 in relation to, among others, the Two-Call Rights Issue of Shares with Warrants Rights Proceeds : Proceeds raised of approximately RM8.79 million from the Two-Call Rights Issue of Shares with Warrants iii

6 DEFINITIONS (CONT D) RM and sen : Ringgit Malaysia and sen, respectively Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions Sale Shares : 500,000 HRLSB Shares, comprising the entire equity interest in HRLSB as at the Completion Date, which are to be sold by the Vendors to Asia Poly on the terms and subject to the conditions of the SSA SC : Securities Commission Malaysia SIS : Share issuance scheme sq. m. : Square metre SSA : Share sale agreement for the Proposed Acquisition dated 25 January 2017 and supplemented by the Supplemental SSA as well as letter of extension dated 4 July 2017, collectively Supplemental SSA : Supplemental share sale agreement for the Proposed Acquisition dated 21 February 2017 TA Securities : TA Securities Holdings Berhad TEAP : Theoretical ex-all price TERP : Theoretical ex-rights price Two-Call Rights Issue of Shares with Warrants : Two-call rights issue of 175,829,920 Asia Poly Shares together with 58,609,973 Warrants 2015/2020 which was completed on 21 December 2015 Undertaking : Unconditional and irrevocable undertaking from the Undertaking Shareholder that he will subscribe for his entitlement of 48,649,800 ICPS together with 12,162,450 Warrants Underwriting : Underwriting arrangements for 51,350,200 ICPS together with 12,837,550 Warrants so that the Minimum Subscription Level will be achieved USD : United States Dollar Valuation : Market value of the Land of RM17,000,000 as at 3 February 2017 (being the material date of valuation) Valuation Report : Valuation report of the Land dated 2 June 2017 Valuer : Weise International Property Consultants Sdn Bhd Vendors : DYBL, YBH and YBT, collectively Warrants : Up to 97,505,963 free detachable warrants to be issued pursuant to the Proposed Rights Issue of ICPS with Warrants Warrants 2015/2020 : 56,463,973 outstanding warrants 2015/2020 in Asia Poly that have yet to be exercised as at the LPD YBH : Yeo Boon Ho YBT : Yeo Boon Thai iv

7 DEFINITIONS (CONT D) All references to our Company in this Circular are to Asia Poly, references to our Group are to our Company and our subsidiaries. All references to we, us, our and ourselves are to our Company, or where the context requires, our Group. All references to you in this Circular are references to the shareholders of our Company. Words incorporating the singular shall, where applicable, include the plural and vice versa. Words incorporating the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. Any reference to persons shall include a corporation, unless otherwise specified. Any reference in this Circular to any enactment is a reference to that enactment as for the time being amended or re-enacted. Any reference to a time of day in this Circular shall be a reference to Malaysian time, unless otherwise specified. [The rest of this page has been intentionally left blank] v

8 TECHNICAL GLOSSARY To facilitate better understanding of the business of our Company, the following glossary contains the definition, explanation and/or description of certain terms used in this Circular in relation to the cast acrylic industry. The terms and their meanings may not correspond to standard industry meanings or usage of these terms. Except where the context otherwise requires, the following technical terms shall apply throughout this Circular and the accompanying appendices: abrasion : Refers to frictional rubbing DMMA : Refers to the breakdown and depolymerisation of scrap/strips from polymer units to monomer units ex-factory sales : Refers to sales registered by the manufacturers, and not the distributors and/or fabricators micron : A millionth of a metre MMA : Refers to methyl methacrylate, a type of monomer monomers : Derived from either naphtha or natural gas, they are the basic building blocks of polymers nanometre : A thousand millionth of a metre nanoparticle(s) : Refers to a microscopic particle of matter between 1 nanometre and 100 nanometres in size naphtha : It is a type of hydrocarbon derived from the refining of crude oil PMMA : Refers to polymethyl methacrylate, a type of polymer. It is also known as acrylics polymers : They are formed by the union or polymerisation of monomers. Also known as synthetic resins or plastic resin polymerisation : Chemical reaction that links monomers to form polymers sol-gels : Solid nanoparticles which are dispersed in a liquid medium to form a network extending throughout the liquid medium substrate : It is the underlying material to which another substance is applied and to which that second substance adheres to [The rest of this page has been intentionally left blank] vi

9 TABLE OF CONTENTS PART A PAGE LETTER TO OUR SHAREHOLDERS CONTAINING: 1. INTRODUCTION DETAILS OF THE PROPOSALS UTILISATION OF PROCEEDS RATIONALE FOR THE PROPOSALS INDUSTRY OUTLOOK AND FUTURE PROSPECTS OF OUR GROUP RISK FACTORS EFFECTS OF THE PROPOSALS HISTORICAL SHARE PRICES APPROVALS REQUIRED CORPORATE EXERCISES ANNOUNCED BUT PENDING COMPLETION INTER-CONDITIONALITY OF THE PROPOSALS INTERESTS OF DIRECTORS, MAJOR SHAREHOLDERS AND/OR PERSONS CONNECTED WITH THEM TRANSACTION WITH THE SAME RELATED PARTY INDEPENDENT ADVISER DIRECTORS STATEMENT AND RECOMMENDATION AUDIT COMMITTEE S STATEMENT ESTIMATED TIME FRAME FOR COMPLETION EGM FURTHER INFORMATION PART B INDEPENDENT ADVICE LETTER FROM INTER-PACIFIC SECURITIES TO OUR NON- INTERESTED SHAREHOLDERS IN RELATION TO THE PROPOSED ACQUISITION 59 APPENDICES I PRO FORMA CONSOLIDATED STATEMENTS OF FINANCIAL POSITION OF ASIA POLY AS AT 31 DECEMBER 2016 TOGETHER WITH THE REPORTING ACCOUNTANTS LETTER THEREON 92 II INFORMATION ON HRLSB 115 III AUDITED FINANCIAL STATEMENTS OF HRLSB FOR THE FYE 31 DECEMBER IV VALUATION CERTIFICATE BY VALUER 149 V FULL DETAILS OF THE PROPOSED AMENDMENTS 157 VI SALIENT TERMS, RIGHTS AND PRIVILEGES OF THE ICPS 158 VII FURTHER INFORMATION 163 NOTICE OF EGM PROXY FORM ENCLOSED ENCLOSED vii

10 PART A LETTER TO OUR SHAREHOLDERS IN RELATION TO THE PROPOSALS

11 ASIA POLY HOLDINGS BERHAD (Company No A) (Incorporated in Malaysia under the Companies Act 2016) Registered Office: 308, Block A (3 rd Floor), Kelana Business Centre, 97, Jalan SS 7/2, Kelana Jaya, Petaling Jaya, Selangor Darul Ehsan 27 July 2017 Board of Directors Dato Yeo Boon Leong (Executive Chairman) Tan Ban Tatt (Independent Non-Executive Director) Thoo Soon Huat (Independent Non-Executive Director) Lim Teck Seng (Non-Independent Non-Executive Director) To: Our shareholders Dear Sir/Madam, (I) PROPOSED RIGHTS ISSUE OF ICPS WITH WARRANTS; (II) PROPOSED ACQUISITION; (III) PROPOSED VARIATION; (IV) PROPOSED DIVERSIFICATION; AND (V) PROPOSED AMENDMENTS 1. INTRODUCTION On 25 January 2017, TA Securities announced on behalf of our Board that our Company proposes to undertake the following proposals: (i) (ii) (iii) (iv) (v) proposed renounceable rights issue of up to 395,675,253 new ICPS on the basis of 1 ICPS for every 1 existing Asia Poly Share held, together with up to 98,918,813 Warrants on the basis of 1 Warrant for every 4 ICPS subscribed for; proposed acquisition of 500,000 HRLSB Shares, representing the entire equity interest in HRLSB for a purchase consideration of RM16,000,000 to be satisfied via a combination of RM8,000,000 in cash and the issuance of 49,443,758 new Asia Poly Shares at an issue price of RM each; Proposed Variation; Proposed Diversification; proposed increase in the authorised share capital of our Company from RM50,000,000 comprising 500,000,000 Asia Poly Shares to RM125,000,000 comprising 1,000,000,000 Asia Poly Shares and 500,000,000 ICPS ( Proposed Increase in Authorised Share Capital ); and 1

12 (vi) proposed amendments to the M&A of our Company to facilitate the issuance of the ICPS pursuant to the Proposed Rights Issue of ICPS with Warrants and the Proposed Increase in Authorised Share Capital. On 21 February 2017, TA Securities announced on behalf of our Board the following: (i) (ii) Our Company and the Vendors had on 21 February 2017 entered into the Supplemental SSA to vary certain terms and conditions of the share sale agreement for the Proposed Acquisition dated 25 January 2017 in view of the recognition of provision for deferred tax liability at 24% on the revaluation surplus arising from the revaluation of the Land in HRLSB subsequent to the said share sale agreement. Please refer to Section 2.2 of this Circular for further details on the variation of terms and conditions of the share sale agreement for the Proposed Acquisition dated 25 January 2017; and In view of the Act which was gazetted on 15 September 2016 and came into effect on 31 January 2017 (with the exception of Section 241 and Division 8, Part III), the Proposed Increase in Authorised Share Capital is no longer necessary pursuant to the Act. As announced on 25 January 2017, the proposed rights issue of ICPS with Warrants entailed the issuance of up to 395,675,253 ICPS together with up to 98,918,813 Warrants under a maximum scenario which had assumed that the private placement was implemented after the full exercise of Warrants 2015/2020. On 8 March 2017, our Company completed the Private Placement prior to the full exercise of Warrants 2015/2020. As such, the number of ICPS and Warrants to be issued pursuant to the Proposed Rights Issue of Shares with Warrants have been revised downwards to 390,023,853 ICPS and 97,505,963 Warrants. Bursa Securities had vide its letter dated 6 July 2017 approved the following: (a) (b) (c) admission to the Official List and the listing of and quotation for up to 390,023,853 ICPS, up to 97,505,963 Warrants and up to 8,244,956* Adjustment Warrants to be issued pursuant to the Proposed Rights Issue of ICPS with Warrants; listing of and quotation for up to 390,023,853 new Asia Poly Shares, up to 97,505,963 new Asia Poly Shares and up to 8,244,956* new Asia Poly Shares to be issued pursuant to the conversion of the ICPS, exercise of the Warrants and Adjustment Warrants, respectively; and listing of and quotation for 42,027,194 Consideration Shares to be issued pursuant to the Proposed Acquisition, Note: * The number of Adjustment Warrants to be issued has decreased to up to 8,237,661 due to the exercise of 50,000 Warrants 2015/2020 as announced on 25 May on the ACE Market, subject to the conditions as stated in Section 9 of Part A of this Circular. THE PURPOSE OF THIS CIRCULAR IS TO PROVIDE YOU WITH THE RELEVANT INFORMATION ON THE PROPOSALS, TO SET OUT OUR BOARD S RECOMMENDATION AND TO SEEK YOUR APPROVAL FOR THE RESOLUTIONS PERTAINING TO THE PROPOSALS TO BE TABLED AT OUR FORTHCOMING EGM. THE NOTICE OF EGM TOGETHER WITH THE PROXY FORM ARE ENCLOSED IN THIS CIRCULAR. YOU ARE ADVISED TO READ AND CONSIDER THE CONTENTS OF THIS CIRCULAR TOGETHER WITH THE APPENDICES CONTAINED HEREIN CAREFULLY BEFORE VOTING ON THE RESOLUTIONS PERTAINING TO THE PROPOSALS TO BE TABLED AT OUR FORTHCOMING EGM. 2

13 2. DETAILS OF THE PROPOSALS 2.1 Proposed Rights Issue of ICPS with Warrants Our Company is proposing to issue up to 390,023,853 ICPS on the basis of 1 ICPS for every 1 existing Asia Poly Share held, together with up to 97,505,963 Warrants on the basis of 1 Warrant for every 4 ICPS subscribed for by the Entitled Shareholders. For illustrative purposes only, the maximum number of 390,023,853 ICPS and 97,505,963 Warrants were arrived at, after taking into consideration of the following: (i) (ii) the existing issued share capital of our Company as at the LPD of RM35,175,128 comprising 333,559,880 Asia Poly Shares; and assuming 56,463,973 outstanding Warrants 2015/2020 are exercised into 56,463,973 new Asia Poly Shares on or prior to the Entitlement Date. The actual number of ICPS to be offered will only be determined on the Entitlement Date. The entitlements for the ICPS with Warrants are renounceable in full or in part. However, the ICPS and the Warrants cannot be renounced separately. Should the Entitled Shareholders renounce all of their ICPS entitlements under the Proposed Rights Issue of ICPS with Warrants, they will not be entitled to the Warrants. However, if the Entitled Shareholders accept only part of their ICPS entitlements under the Proposed Rights Issue of ICPS with Warrants, they shall be entitled to the Warrants in proportion of their acceptances of the ICPS entitlements. In determining shareholders entitlements to the Warrants under the Proposed Rights Issue of ICPS with Warrants, fractional entitlements, if any, shall be disregarded, and dealt with by our Board in such manner at its absolute discretion as it may deem fit or expedient and in the best interest of our Company. The ICPS with Warrants which are not taken up or validly taken up shall be made available for excess applications by the Entitled Shareholders and/or their renouncee(s) (if applicable). It is the intention of our Board to allocate the excess ICPS in a fair and equitable manner on a basis to be determined by our Board and announced later by our Company. The Warrants will be immediately detached from the ICPS upon issuance and separately traded from the ICPS on the ACE Market of Bursa Securities. The Warrants will be issued in registered form and constituted by the Deed Poll Basis of determining and justification for the issue price of the ICPS and the exercise price of the Warrants (a) ICPS Our Board has fixed the issue price of the ICPS at RM0.05 each after taking into consideration, among others, the following: (i) (ii) (iii) (iv) the TEAP of RM per Asia Poly Share, calculated based on the 5D-VWAP of Asia Poly Shares up to and including the Announcement LPD of RM per Asia Poly Share; the issued share capital of each Asia Poly Share of RM0.10 then; the issued share capital of each ICPS of RM0.05 then, the Conversion Ratio and Conversion Price of the ICPS which have been fixed at either 2 ICPS to be converted into 1 Asia Poly Share or a combination of 1 ICPS and RM0.05 in cash for 1 Asia Poly Share; the rationale for the Proposed Rights Issue of ICPS with Warrants as set out in Section 4 of Part A of this Circular; and 3

14 (v) the funding requirements of our Group, the details of which are set out in Section 3 of Part A of this Circular. The Conversion Price of RM0.10 is at a discount of approximately RM or 26.09% to the TEAP of RM per Asia Poly Share, calculated based on the 5D-VWAP of Asia Poly Shares up to and including the Announcement LPD of RM per Asia Poly Share. The Conversion Price is fixed at RM0.10 and was arrived at holistically, after taking into consideration, among others, the issue price of the ICPS and the exercise price of the Warrants, and is at a discount (as set out above) to encourage the ICPS holders to convert their ICPS and further increase their equity participation in our Company at a predetermined price. (b) Warrants The Warrants will be issued at no cost to the Entitled Shareholders who successfully subscribed for the ICPS. Our Board has fixed the exercise price of the Warrants at RM0.10 each after taking into consideration, among others, the following: (i) (ii) the TERP of RM per Asia Poly Share, calculated based on the 5D-VWAP of Asia Poly Shares up to and including the Announcement LPD of RM per Asia Poly Share; and the issued share capital of each Asia Poly Share of RM0.10 then. The exercise price of RM0.10 per Warrant represents a discount of RM or 29.18% to the TERP of RM per Asia Poly Share, calculated based on the 5D-VWAP of Asia Poly Shares up to and including the Announcement LPD of RM per Asia Poly Share. The exercise price of the Warrants of RM0.10 which is at a discount (as set out above) to provide further incentive to the Entitled Shareholders to subscribe for the Proposed Rights Issue of ICPS with Warrants, and to encourage the Warrant holders to exercise their Warrants and increase their equity participation in our Company at a predetermined price Salient terms of the ICPS The salient terms of the ICPS are as follows: Terms Details Issue size : Up to 390,023,853 ICPS. Issue price : RM0.05 per ICPS. Dividend rate : Our Company has full discretion over the declaration of dividends, if any. Dividends declared and payable annually in arrears are non-cumulative and shall be in priority over the ordinary shares of our Company. Tenure : 5 years commencing from and inclusive of the date of issue of the ICPS. 4

15 Maturity date : The day immediately preceding the 5 th anniversary from the date of issue of the ICPS unless the tenure of the ICPS, if permitted by law, is extended by our Company and the ICPS holders. If such day falls on a day which is not a market day, then on the preceding market day. Redemption : Not redeemable for cash. Board lot : For the purpose of trading on Bursa Securities, 1 board lot of ICPS shall comprise 100 ICPS, or such other denomination as determined by Bursa Securities from time to time. Form and denomination : The ICPS will be issued in registered form and will be constituted by our Company s Constitution (M&A). Conversion rights : (a) Each ICPS carries the entitlement to convert into new Asia Poly Shares at the Conversion Ratio through the surrender of the ICPS. (b) (c) No adjustment to the Conversion Price shall be made for any declared and unpaid dividends on the ICPS surrendered for conversion. If the conversion results in a fractional entitlement to ordinary shares of our Company, such fractional entitlement shall be disregarded and no refund or credit, whether in the form of the ICPS, cash or otherwise, shall be given in respect of the disregarded fractional entitlement. Conversion period : (a) The ICPS may be converted at any time within 5 years commencing on and including the date of issue of the ICPS up to and including the maturity date, as determined by the Conversion Ratio and Conversion Price. (b) Any remaining ICPS that are not converted by the maturity date shall be automatically converted into new Asia Poly Shares at the conversion ratio of 2 ICPS to be converted into 1 Asia Poly Share. Conversion Ratio and Conversion Price Ranking of the ICPS and liquidation preference : The Conversion Ratio and Conversion Price have been fixed at either 2 ICPS to be converted into 1 new Asia Poly Share or a combination of 1 ICPS and RM0.05 in cash for 1 new Asia Poly Share. : The ICPS shall rank pari passu amongst themselves and shall rank in priority to any other class of shares in the capital of our Company. In the event of liquidation, dissolution, winding-up, reduction of capital or other repayment of capital: 5

16 (a) (b) The ICPS shall confer on the holders the right to receive in priority to the holders of ordinary shares in Asia Poly, cash repayment in full of the amount of any non-cumulative preferential dividend that has been declared and remaining in arrears. After the payment of any dividends to the holders of ICPS, the remaining assets shall be distributed first to the holders of ICPS in full of the amount which is equal to the issue price for each ICPS, provided that there shall be no further right to participate in any surplus capital or surplus profits of our Company. In the event that our Company has insufficient assets to permit payment of the full issue price to the ICPS holders, the assets of our Company shall be distributed pro rata on an equal priority, to the ICPS holders in proportion to the amount that each ICPS holder would otherwise be entitled to receive. Ranking of new Asia Poly Shares to be issued pursuant to the conversion of the ICPS : All new Asia Poly Shares to be issued pursuant to the conversion of the ICPS shall, upon allotment and issuance, rank pari passu in all respects with the existing Asia Poly Shares except that such new Asia Poly Shares shall not be entitled to any dividends, rights, allotments and/or other distribution, the entitlement date of which is prior to the date of allotment and issuance of the new Asia Poly Shares arising from the conversion of the ICPS. Adjustment to Conversion Price and Conversion Ratio : The Conversion Price and/or Conversion Ratio will be adjusted at the determination of our Company, in all or any of the following cases: (a) (b) (c) (d) (e) an alteration to the number of Asia Poly Shares by reason of consolidation or subdivision; or a bonus issue of fully paid-up ordinary shares by our Company or any other capitalisation issue for accounting purposes; or a capital distribution to shareholders made by our Company whether on a reduction of capital or otherwise, but excluding any cancellation of capital which is loss or unrepresented by assets; or a rights issue of ordinary shares by our Company; or any other circumstances that our Board deems necessary, provided that any adjustment to the Conversion Price will be rounded down to the nearest one sen (RM0.01). No adjustment to the Conversion Price and/or Conversion Ratio will be made unless the computation has been certified by the external auditors of our Company. 6

17 Rights of the ICPS holders : The ICPS holders are not entitled to any voting right or participation in any rights, allotments and/or other distribution in our Company except in the following circumstances: (a) (b) (c) (d) (e) (f) when the dividend or part of the dividend on the ICPS is in arrears for more than 6 months; on a proposal to reduce our Company s share capital; on a proposal for the disposal of the whole of our Company s property, business and undertaking; on a proposal that affects their rights and privileges attached to the ICPS; on a proposal to wind-up our Company; and during the winding-up of our Company. Listing : The ICPS will be listed and traded on the ACE Market of Bursa Securities. Approval has been obtained from Bursa Securities for the admission of the ICPS to the Official List of the ACE Market of Bursa Securities and the listing of and quotation for the ICPS and the new Asia Poly Shares to be issued pursuant to the conversion of the ICPS on the ACE Market of Bursa Securities. Transfer : The ICPS will be transferable only by instrument in writing in the usual or common form or such other form as the Directors of our Company and the relevant authorities may approve. As the ICPS will be listed on and traded on the ACE Market of Bursa Securities, they will be deposited in a central depository system and may be subject to the rules of such system. Modification of rights : Our Company may from time to time with the consent or sanction of all the holders of the ICPS make modifications to the terms of which in the opinion of our Company are not materially prejudicial to the interest of the holders of the ICPS or are to correct a manifest error or to comply with mandatory provisions of the laws of Malaysia and the relevant regulations. Governing law : The laws of Malaysia Salient terms of the Warrants The indicative salient terms of the Warrants are as follows: Terms Details Issue size : Up to 97,505,963 Warrants. Form and denomination : The Warrants which are free will be issued in registered form and will be constituted by the Deed Poll. Exercise price : The exercise price of the Warrants is fixed at RM0.10 each. 7

18 Exercise rights : Each Warrant entitles the registered holder to subscribe for 1 new Asia Poly Share at any time during the exercise period at the exercise price (subject to adjustments in accordance with the provisions of the Deed Poll). Expiry date : The day immediately preceding the 5 th anniversary date of the issuance of the Warrants, provided that if such day falls on a day which is not a market day, then on the preceding market day. Exercise period : The Warrants may be exercised at any time within 5 years commencing on and including the date of issuance of the Warrants until 5.00 p.m. on the expiry date. Warrants not exercised during the exercise period will thereafter lapse and cease to be valid. Mode of exercise : The registered holder of the Warrants is required to lodge an exercise form, as set out in the Deed Poll, with our Company s registrar, duly completed, signed and stamped together with payment of the exercise price for the new Asia Poly Shares subscribed for by banker s draft or cashier s order or money order or postal order in Ringgit Malaysia drawn on a bank or post office operating in Malaysia. Board lot : For the purpose of trading on Bursa Securities, 1 board lot of Warrant shall comprise 100 Warrants carrying the right to subscribe for 100 new Asia Poly Shares at any time during the exercise period, or such other denomination as determined by Bursa Securities from time to time. Adjustments in the exercise price and/or number of the Warrants : Subject to the provisions in the Deed Poll, the exercise price and the number of Warrants held by each Warrant holder shall be adjusted by our Board in consultation with the approved adviser and certified by the auditors of our Company, in the event of alteration to the share capital of our Company. Rights of the Warrants : The Warrant holders are not entitled to any dividends, rights, allotments and/or other distributions that may be declared, made or paid where the entitlement date precedes the date of allotment and issuance of the new Asia Poly Shares upon the exercise of the Warrants. The Warrant holders are not entitled to any voting rights or participation in any form of distribution and/or offer of securities in our Company until and unless such Warrant holders exercise their Warrants into new Asia Poly Shares. Provision for changes in the terms of the Warrants : Any modification to the Deed Poll (including the form and content of the warrant certificate) may be effected only by Deed Poll, executed by our Company and expressed to be supplemental to the Deed Poll, and only if the requirement of Condition 7 of the Deed Poll has been complied with. Any modification shall however be subject to the approval of Bursa Securities (if so required). A memorandum of every such supplemental deed shall be endorsed on the Deed Poll. 8

19 Rights in the event of winding-up, liquidation, compromise and/or arrangement : If a resolution is passed for a members voluntary winding-up of our Company or there is a compromise or arrangement, whether or not for the purpose of or in connection with a scheme for the reconstruction of our Company or the amalgamation of our Company with one or more companies, then: (i) (ii) for the purposes of such winding-up, compromise or arrangement (other than a consolidation, amalgamation or merger in which our Company is the continuing corporation) to which the Warrant holder (or some person designated by them for such purpose by special resolution) shall be a party, the terms of such winding-up, compromise and arrangement shall be binding on all the Warrant holders; and in any other case, every Warrant holder shall be entitled upon and subject to the conditions at any time within 6 weeks after the passing of such resolution for a members voluntary winding-up of our Company or the granting of the court order approving the compromise or arrangement (as the case may be), to exercise their Warrants by submitting the exercise form duly completed authorising the debiting of his Warrants together with payment of the relevant exercise price to elect to be treated as if he had immediately prior to the commencement of such winding-up exercised the exercise rights to the extent specified in the exercise form(s) and had on such date been the holder of the new Shares to which he would have become entitled pursuant to such exercise and the liquidator of our Company shall give effect to such election accordingly. Listing status : The Warrants will be listed and traded on the ACE Market of Bursa Securities. Approval has been obtained from Bursa Securities for the admission of Warrants to the Official List of the ACE Market of Bursa Securities and the listing of and quotation for the Warrants and the new Asia Poly Shares to be issued pursuant to the exercise of the Warrants on the ACE Market of Bursa Securities. Governing law : The laws of Malaysia Ranking of the new Asia Poly Shares to be issued pursuant to the conversion of the ICPS and/or the exercise of the Warrants and/or Adjustment Warrants The new Asia Poly Shares to be issued arising from the conversion of the ICPS and/or exercise of the Warrants and/or Adjustment Warrants shall, upon allotment and issuance, rank pari passu in all respects with the existing Asia Poly Shares, save and except that the new Asia Poly Shares shall not be entitled to any dividends, rights, allotments and/or other distributions, the entitlement date of which is prior to the date of allotment and issuance of the new Asia Poly Shares arising from the conversion of the ICPS and/or exercise of the Warrants and/or Adjustment Warrants. 9

20 2.1.5 Minimum subscription level, major shareholder s undertaking and underwriting arrangement The Proposed Rights Issue of ICPS with Warrants will be implemented on the Minimum Subscription Level. Based on the issue price of RM0.05 per ICPS, our Company will raise minimum gross proceeds of RM5.00 million from the Proposed Rights Issue of ICPS with Warrants. The Minimum Subscription Level was determined by our Board after taking into consideration, inter-alia, the funding requirements of our Group as set out in Section 3 of Part A of this Circular. To meet the Minimum Subscription Level, our Company has procured the Undertaking from the Undertaking Shareholder and that he will not dispose any of his Asia Poly Shares following the announcement dated 25 January 2017 up to the Entitlement Date. In addition to the Undertaking, Asia Poly will also procure the Underwriting so that the Minimum Subscription Level will be achieved. The underwriting commission payable to underwriters and all other costs in relation to the Underwriting will be fully borne by our Company. The Underwriting will be finalised at a later date prior to the implementation of the Proposed Rights Issue of ICPS with Warrants. The terms of the Underwriting have therefore not been finalised and no underwriting agreement has been entered into at this juncture. In view of the Undertaking and Underwriting, the Minimum Subscription Level will be achieved. Details of the Undertaking (at the time the Undertaking was entered into) and Underwriting based on the Minimum Subscription Level are as summarised below: ICPS entitled and undertaken/ to be underwritten As at 23 January 2017 (2) No. of Asia Poly Shares held % No. of ICPS % (1) Undertaking Shareholder DYBL 48,649, ,649, Underwriters ,350, Total 48,649, ,000, Notes: (1) Percentages are calculated based on 100,000,000 ICPS available for subscription under the Minimum Subscription Level. (2) Based on our Company s Record of Depositors as at 23 January 2017 (i.e., at the time the Undertaking was entered into). DYBL holds 29,700 Warrants 2015/2020 based on our Company s Record of Depositors as at 23 January The above assumes that DYBL will not exercise the said Warrants 2015/2020 held. In the event DYBL exercises the 29,700 Warrants 2015/2020 into 29,700 Asia Poly Shares prior to the Entitlement Date, the ICPS undertaken to be subscribed by DYBL will increase by 29,700. [The rest of this page has been intentionally left blank] 10

21 Details of the Undertakings and Underwriting based on the Minimum Subscription Level as at the LPD are as follows: ICPS entitlement (1) ICPS undertaken (2) / underwritten As at the LPD (5) No. of Asia Poly Shares held % No. of ICPS No. of ICPS % (3) Undertaking Shareholder DYBL 48,802,300 (4) ,802,300 48,649, Underwriters ,350, Total 48,802, ,802, ,000, Notes: (1) Entitlement based on DYBL s shareholding in our Record of Depositors as at the LPD. (2) Subscription of ICPS pursuant to the Undertaking. (3) Percentages are calculated based on 100,000,000 ICPS available for subscription under the Minimum Subscription Level. (4) The shareholding of DYBL has increased subsequent to the Undertaking. (5) Based on our Company s Record of Depositors as at the LPD. DYBL holds 29,700 Warrants 2015/2020 based on our Company s Record of Depositors as at the LPD. The above assumes that DYBL will not exercise the said Warrants 2015/2020 held. In the event DYBL exercises the 29,700 Warrants 2015/2020 into 29,700 Asia Poly Shares prior to the Entitlement Date, the ICPS undertaken to be subscribed by DYBL will increase by 29,700. The Undertaking Shareholder has confirmed that he has sufficient financial resources to subscribe for his entitlement of 48,649,800 ICPS together with 12,162,450 Warrants as well as his additional entitlement of 29,700 ICPS with 7,425 Warrants arising from the exercise of his 29,700 Warrants 2015/2020 pursuant to the Undertaking (being his full entitlement at the time the Undertaking was entered into). As the Adviser for the Proposed Rights Issue of ICPS with Warrants, TA Securities has verified that the Undertaking Shareholder has sufficient resources to fulfil his commitment pursuant to the Undertaking. After taking into consideration the Undertaking and Underwriting, the subscription of the ICPS by the Undertaking Shareholder will not give rise to any consequences of mandatory general offer obligations pursuant to the Code and the Rules. The Undertaking Shareholder has undertaken to observe and comply at all times with the provisions of the Code and the Rules. [The rest of this page has been intentionally left blank] 11

22 2.2 Proposed Acquisition On 25 January 2017 and 21 February 2017, our Company entered into the share sale agreement and Supplemental SSA, respectively with the Vendors for the Proposed Acquisition, to be satisfied via the Cash Consideration and Consideration Shares. Subsequently, our Company and the Vendors had via a letter of extension dated 4 July 2017 mutually agreed to the extension of the Stipulated Period (as defined in Section (a) of this Circular) until 24 November Pursuant to the terms of the SSA, our Company shall acquire 500,000 HRLSB Shares from the Vendors, free from all liens, charges and encumbrances and with all rights attaching to them, and all dividends and distributions declared, paid or made in respect thereof as from the Completion Date (as defined in Section of Part A of this Circular) at the Purchase Consideration, upon the terms and conditions of the SSA. With effect from 21 February 2017 (being the date of the Supplemental SSA), the SSA shall be amended and varied in the manner set out below in view of the recognition of provision for deferred tax liability at 24% on the revaluation surplus arising from the revaluation of the Land in HRLSB, subsequent to the share sale agreement dated 25 January 2017: (i) (ii) (iii) (iv) the Purchase Consideration in the share sale agreement dated 25 January 2017 shall be amended to RM14,800,000 only and shall be paid by the Purchaser to the Vendors, in the proportions set out in Section of Part A of this Circular, in accordance with the terms of the SSA; the Consideration Shares in the share sale agreement dated 25 January 2017 shall be amended to 42,027,194 new Asia Poly Shares to be issued at an issue price of RM0.1618, the aggregate value which amounts to RM6,800,000 only, by the Purchaser to part satisfy the Purchase Consideration; the Deposit in the share sale agreement dated 25 January 2017 shall be amended to RM1,480,000 only; and the Balance Purchase Price in the share sale agreement dated 25 January 2017 shall be amended to RM10,120,000 only, being the difference between the Purchase Consideration (of RM14,800,000) and the Deposit (of RM1,480,000) and Redemption Sum* (of RM3,200,000). Please also refer to Sections and of this Circular for the breakdown of the Purchase Consideration. * Being the redemption sum for the redemption of the Land by the Vendors from Ambank as set out in Section (ii) of this Circular. Save for the above, all other terms of the share sale agreement dated 25 January 2017 remain unchanged. Upon completion of the Proposed Acquisition, HRLSB will become a wholly-owned subsidiary of Asia Poly. The Proposed Acquisition is a related party transaction pursuant to Rule of the Listing Requirements in view of the interest the Interested Person as set out in Section 12 of Part A of this Circular. [The rest of this page has been intentionally left blank] 12

23 2.2.1 Background information on HRLSB HRLSB is a private limited company incorporated in Malaysia on 26 November 2012 under the Act. The principal activity of HRLSB is to carry on business in land or property development. HRLSB is the registered owner of the Land located at Mukim of Semenyih, District of Ulu Langat, Selangor Darul Ehsan. Further details of the Land are set out in Section of Part A of this Circular. As at the LPD, the share capital of HRLSB is RM500,000 comprising 500,000 issued HRLSB Shares. As at the LPD, the directors and shareholders of HRLSB and their respective shareholdings in HRLSB are as follows: Name No. of HRLSB Shares % of issued share capital of HRLSB Directors and shareholders DYBL 400, YBH 50, Shareholder YBT 50, Total 500, As at the LPD, HRLSB does not have any subsidiary and/ or associate company Background information on the Vendors (i) DYBL DYBL, age 51, is a director and the controlling shareholder of HRLSB who currently owns 80% equity interest in HRLSB. He is also the Executive Chairman and major shareholder of our Company. (ii) YBH YBH, age 46, is a director and shareholder of HRLSB who currently owns 10% equity interest in HRLSB. He is not a Director of our Company and does not hold any Asia Poly Shares as at the LPD. (iii) YBT YBT, age 35, is a shareholder of HRLSB who currently owns 10% equity interest in HRLSB. He is not a Director of our Company and held 70,000 Asia Poly Shares (i.e., 0.02% equity interest) as at the LPD. The Vendors are brothers. [The rest of this page has been intentionally left blank] 13

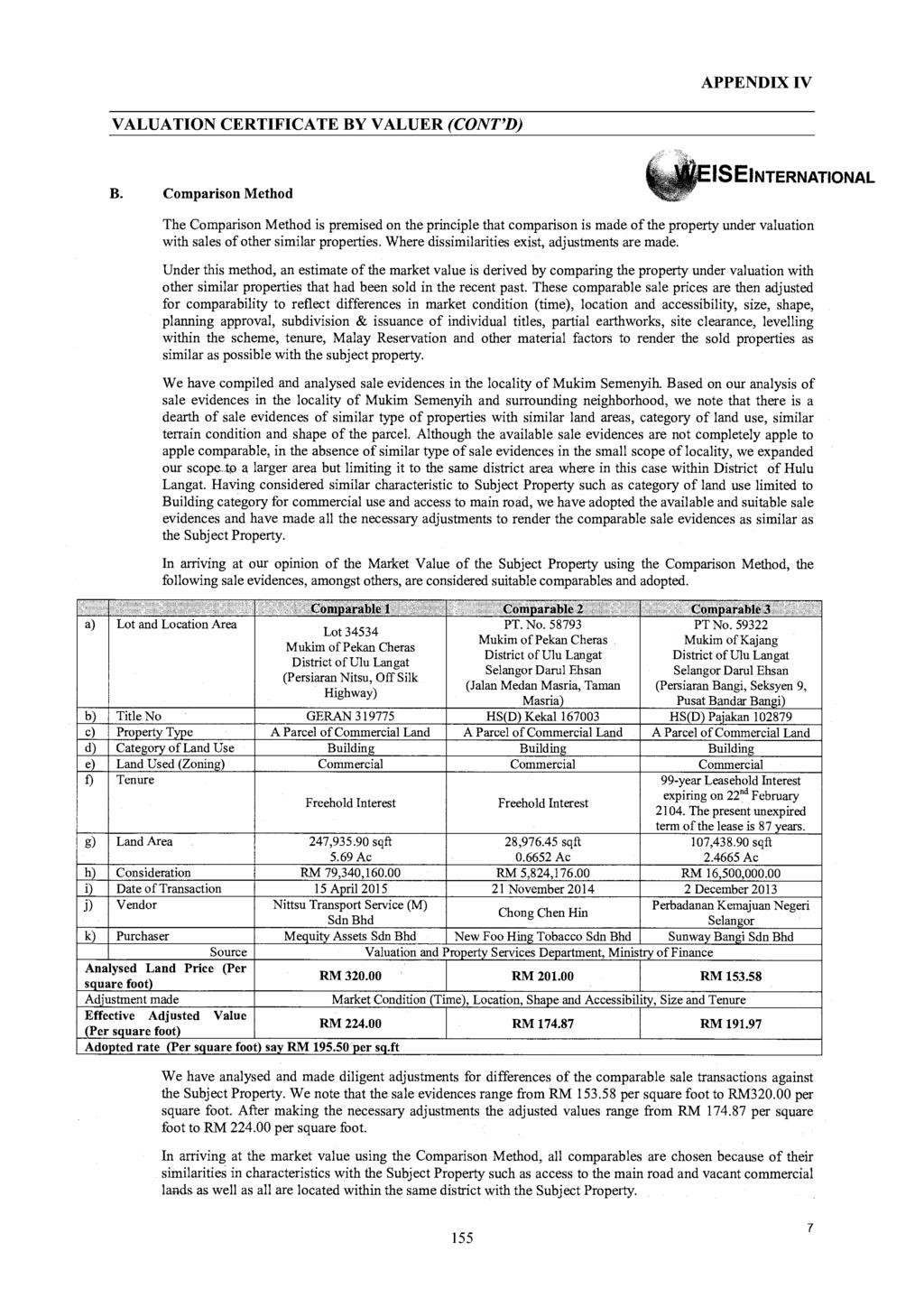

24 2.2.3 Details of the Land Postal address and identification : Lot 1894, held under Title No. Geran 47916, Mukim of Semenyih, District of Ulu Langat, State of Selangor Darul Ehsan Title land area : Measuring approximately acres (8, sq. m. or 86, square feet) Land tenure : Freehold interest Audited net book value as at 31 December 2016 : RM8,026,271 Category of land use : Building Express condition : Construction of buildings according to the specifications of the Selangor Town and Country Planning Department Restriction in interests : Nil Encumbrance / Charge : As at the Announcement LPD, the Land was charged to Ambank since 6 June 2013 as collateral for a term loan and overdraft facility. The term loan and overdraft outstanding then were RM2.88 million and RM0.28 million, respectively. Existing use : Vacant Proposed use : Commercial Independent valuation on the Land As at the LPD, the term loan and overdraft outstanding were RM2.07 million and RM0.20 million, respectively. The Land shall be redeemed by the Vendors and shall be free from any liens, charges and encumbrances prior to the completion of the Proposed Acquisition. Please refer to Section of Part A of this Circular for further details. The Valuer has been appointed to conduct an independent valuation on the Land for submission to Bursa Securities. In arriving at the Valuation of RM17,000,000 (being the market value of the Land), the Valuer adopted the residual method as the primary valuation method as the Subject Property is yet to be subdivided and issued with individual titles into specific land uses and the site clearance, earthwork and levelling of this land has yet to be carried out. The Valuer also adopted the comparison method as a check. [The rest of this page has been intentionally left blank] 14

25 2.2.5 Proposed development on the Land The Proposed Development was approved by the Kajang Municipal Council as per the approved Master Layout Plan dated 25 October 2016 and approved Planning Permission dated 1 February The Planning Permission is valid for a period of 1 year. The details on the Proposed Development are as follows: Type of development : Commercial which will comprise: (i) (ii) 12 units of three-storey terrace shop offices (24 x 70 ); 1 unit of four-storey terrace shop office (24 x 70 ); and (iii) 1 unit of three-storey terrace shop office (35 x 70 ); all with basement level for car park bays RM GDV (A) : 39,969, (Source: Valuation Report) Total cost (B) : 25,882, Comprising the following: - Cost of investment in HRLSB 14,800, Net GDC* 11,082, * The net GDC was arrived at as follows: GDC (excluding land cost) 19,875, Less: Developer s profit to be earned (8,793,235.54) Net GDC 11,082, (Source: Valuation Report) Expected gross development profit (A) (B) 14,086, Less: Tax payable on the profit at 24% (3,380,780.56) Expected net development profit 10,705, Expected commencement date of the Proposed Development Expected completion date of the Proposed Development : Our enlarged Group will undertake the Proposed Development after the completion of the Proposed Acquisition (i.e., the said commencement is expected to be in the 4 th quarter of 2017). : 2 years from the commencement of the Proposed Development. Stage of the Proposed Development : As at the LPD, HRLSB has not commenced any work on the Land and Proposed Development. Category of Proposed Development use : For sale 15

26 The developer s profit is the expected profit to be realised by HRLSB (as provided by the Valuer in the Valuation Report) whom will be undertaking the development and sale of the Proposed Development assuming HRLSB acquires the Land at the current market value of RM17,000,000. The expected gross development profit is the expected profit to be realised by our Company from the Proposed Acquisition (i.e., acquisition of HRLSB which owns the Land, as per the computation set out above) as our enlarged Group will undertake the Proposed Development after the completion of the Proposed Acquisition. The Proposed Development is expected to be funded through a combination of internally generated funds of our enlarged Group (i.e., after the Proposed Acquisition), progressive collections from sales billings, bank borrowings and/or fund raising exercise (if necessary), the proportion of which has yet to be determined at this juncture. The actual proportion of the sources of funding for the Proposed Development will depend on, among others, the demand/take-up rate of the properties Salient terms of the SSA The salient terms and conditions of the SSA include, inter alia, the following: Purchase Consideration The purchase consideration for the Sale Shares was initially RM16,000,000 based on the share sale agreement for the Proposed Acquisition dated 25 January Subsequently, our Company and the Vendors entered into the Supplemental SSA to revise the Purchase Consideration* to RM14,800,000 and to vary certain terms and conditions of the share sale agreement dated 25 January 2017 in relation to the said revision. Note: * The Purchase Consideration was revised in view of the recognition of provision for deferred tax liability at 24% on the revaluation surplus arising from the revaluation of the Land in HRLSB, subsequent to the share sale agreement dated 25 January Thus, the Purchase Consideration for the Sale Shares shall be RM14,800,000 only and shall be paid by our Company to the Vendors in the proportions set out in Section of Part A of this Circular. The Purchase Consideration shall be satisfied by part cash (54.05%) of RM8,000,000 and part by the issuance of 42,027,194 new Asia Poly Shares (45.95%) at the issue price of RM (being the 5D-VWAP of Asia Poly Shares up to and including 24 January 2017, being the latest practicable date prior to entering into the SSA of RM0.1618) amounting to RM6,800,000 in the following manner: (i) the deposit amounting to 10% of the Purchase Consideration (i.e., RM1,480,000) ( Deposit )^ shall be paid upon the signing of the SSA; Note: ^ As at the LPD, our Company has paid the Deposit. 16

27 (ii) a redemption sum amounting to 21.62% of the Purchase Consideration (i.e., RM3,200,000) ( Redemption Sum ) shall be paid within 14 days from the day HRLSB obtains the redemption statement (for the redemption of the Land by the Vendors) from Ambank; and The Vendors confirmed in the SSA that the amount owing to Ambank^ as at the date of the SSA does not exceed the Redemption Sum. Note: ^ As at the Announcement LPD, the term loan and overdraft outstanding were RM2.88 million and RM0.28 million, respectively. As at the LPD, the term loan and overdraft outstanding were RM2.07 million and RM0.20 million, respectively. The Land shall be redeemed by the Vendors and shall be free from any liens, charges and encumbrances prior to the completion of the Proposed Acquisition. (iii) the balance of the Purchase Consideration (i.e., RM10,120,000 out of which RM6,800,000 is to be paid via the issuance of the Consideration Shares) shall be paid on the completion date which is a date falling within 45 market days from the date the last of the conditions precedent ( Conditions Precedent ) is fulfilled ( Completion Date ) Conditions Precedent (a) The sale and purchase of the Sale Shares shall be conditional upon the fulfilment of the following within 5 months ( Stipulated Period )* of the date of the SSA or such other period as the parties may mutually agree in writing: (i) (ii) (iii) (iv) (v) (vi) our Company obtaining the approval of our shareholders in a general meeting for the acquisition of the Sale Shares and the issue of the Consideration Shares; our Company obtaining the approval of our shareholders in a general meeting for the proposed diversification of its business as a result of the acquisition of the Sale Shares; our Company obtaining the approval of our board of directors for the acquisition of the Sale Shares respectively; our Company obtaining the approval of Bursa Securities for the listing and quotation of the Consideration Shares; the charge on the Land to Ambank being discharged and the Land being free from any liens, charges and encumbrances; and the parties obtaining such other approvals as shall be necessary under the laws or from the regulatory authority for the completion of the sale of the Sale Shares herein. Note: * The Stipulated Period has been extended until 24 November 2017 via a letter of extension dated 4 July

28 (b) In the event that the Conditions Precedent are not fulfilled and/or waived by our Company within the Stipulated Period, the following shall take place on or before the expiry of 14 days from the day next following the expiry of the Stipulated Period: (i) (ii) the Vendors shall refund our Company, together with accrued interest, the Deposit and the Redemption Sum (if applicable); our Company shall return or cause to be returned to the Vendors, all documents and things (whether original or copies) forwarded to our Company by the Vendors hereunder (including all documents provided to or obtained by our Company in the course of its due diligence review on HRLSB), if any; and thereafter, the SSA shall be mutually terminated and shall have no further force and effect with neither party having any rights and obligations against the other save and except for any antecedent breaches. (c) The Vendors and our Company shall use their respective best endeavours to ensure that the SSA becomes unconditional on or before the expiry of the Stipulated Period Completion On the Completion Date, the Vendors shall complete the sale of the Sale Shares at a place to be mutually agreed by the parties, failing which, it shall be held at the office of our Company by the delivery of: (i) (ii) (iii) (iv) (v) (vii) the original share certificates to the Sale Shares; the valid and registrable memoranda of transfer of the Sale Shares duly executed by the Vendors in favour of our Company together with the relevant stamping pro forma; the resolution of the directors of HRLSB approving the transfer of the Sale Shares in favour of our Company; if required, all the statutory and account books of HRLSB, invoices, common seal and all other documents relating to HRLSB; all documents of title, if any, pertaining to the assets of HRLSB and all the necessary authorisations as shall be necessary so as to enable our Company to obtain physical possession of the assets of HRLSB; and such waivers, consents or other documents as may be required to give a good title to the Sale Shares and to enable our Company or its nominee(s) to become the registered owner(s) of the Sale Shares. [The rest of this page has been intentionally left blank] 18

29 Default (a) In the event that any party being either our Company or the Vendors shall: (i) (ii) neglect or by wilful default, fail or refuse or be unable to complete this transaction in accordance with the provisions herein; or breach any of the material provisions of the SSA; the party not in breach of the SSA shall be entitled at its absolute discretion to elect either to: (aa) (bb) give notice in writing ( Termination Notice ) to the party in default ( Defaulting Party ) specifying the breach(es) complained of, and if the Defaulting Party fails to remedy the breach(es) within 14 days of receipt of the Termination Notice, the party not in default may without further reference to the Defaulting Party terminate the SSA, in which event the provisions as prescribed in Section (b) of Part A of this Circular shall apply and thereafter the SSA shall be terminated and the Vendors and our Company shall have no further claims against each other save and except for any antecedent breaches; or alternatively complete the SSA, in which case the remedy of specific performance of the SSA shall be available to the party not in default, and thereafter the party not in default may claim for such damages, losses (excluding loss of profits, goodwill and reputation), costs, expenses or outgoings which remain outstanding despite having obtained specific performance. (b) In the event that the SSA is terminated in accordance with Section (a)(aa) of Part A of this Circular, then: (i) if the Defaulting Party are the Vendors, the Vendors shall, within 14 days from the day after the expiration of the 14 day period referred to in Section (a)(aa) of Part A of this Circular, (aa) (bb) duly refund and/or authorise to be refunded to our Company, the Deposit and the Redemption Sum (if applicable), together with accrued interest of 3.50% per annum, and all other monies paid by our Company to the Vendors hereunder (if any); and pay to our Company a sum amounting to 10% of the total Purchase Consideration being the agreed liquidated damages, and in exchange thereof, our Company shall return all documents and things forwarded by the Vendors in relation to the SSA, save and except where our Company requires the same for application for refund of any stamp duty paid pursuant hereto, in which case the documents and things shall be returned as soon as is reasonably possible; and (ii) if the Defaulting Party is our Company, the Vendors shall refund the Deposit and the Redemption Sum (if applicable), together with accrued interest of 3.50% per annum, to our Company. 19

30 Shareholder s advances (a) (b) DYBL in his capacity as a shareholder of HRLSB has been making monetary advances to HRLSB for working capital purposes. As at the date of the SSA the total Advances by DYBL to HRLSB is RM6,019, only. In consideration of our Company agreeing to enter into the SSA, DYBL expressly and irrevocably forgives the Advances by DYBL and waives all his rights to claim for the Advances by DYBL from HRLSB. The Advances by DYBL shall de deemed duly settled by HRLSB to DYBL upon the completion of the SSA on the Completion Date. Further to Section (a) of Part A of this Circular, the Vendors hereby irrevocably waive any and all claims which they may have against HRLSB as at the Completion Date Basis and justification in arriving at the Purchase Consideration The Purchase Consideration was arrived at on a willing-buyer-willing-seller basis, after taking into consideration of, amongst others, the following: RM The unaudited net liabilities of HRLSB as at 31 December 2016 (1,192,678) Add: Net revaluation surplus 6,844,035 (i) Add: Waiver of Advances by DYBL as at 31 December ,823,217 (ii) 11,474,574 Add: Settlement of the bank borrowings as at 31 December ,329,344 (iii) Adjusted unaudited NA of HRLSB 14,803,918 # Less: Discount mutually agreed between the Vendors and Asia (3,918) # Poly Total Purchase Consideration 14,800,000 # Based on the audited financial statements of HRLSB for the FYE 31 December 2016 as disclosed in Appendix III of this Circular, the impact to the adjusted audited NA of HRLSB and the discount would be as follows: RM The audited net liabilities of HRLSB as at 31 December 2016 (1,170,552) # Add: Net revaluation surplus 6,820,034 (i) Add: Waiver of Advances by DYBL as at 31 December ,823,217 (ii) 11,472,699 Add: Settlement of the bank borrowings as at 31 December ,329,344 (iii) Adjusted unaudited NA of HRLSB 14,802,043 Less: Discount mutually agreed between the Vendors and Asia (2,043) # Poly Total Purchase Consideration 14,800,000 The breakdown of the Purchase Consideration (as detailed in Section of Part A of this Circular) is as follows: Deposit 1,480,000 Balance Purchase Price - Cash 3,320,000 - Issuance of Consideration Shares 6,800,000 Purchase consideration for the Sale Shares payable to the Vendors 11,600,000 Add: Redemption Sum 3,200,000 Total Purchase Consideration 14,800,000 20

31 Notes: (i) ^ The net revaluation surplus was arrived at as follows: RM Market value of the Land 17,000,000 Less: Unaudited net book value of the Land as at 31 December 2016 (7,994,691) # Revaluation surplus 9,005,309 Less: Deferred tax liabilities at 24%^ (2,161,274) Net revaluation surplus 6,844,035 Pursuant to the MFRS 112 para 51, the measurement of the deferred tax liabilities would follow the manner in which the management expects to recover the carrying amounts of its assets. As it is the management of Asia Poly s intention is to develop the Land, it will be subject to corporate tax in the future and thus deferred tax liabilities is computed at 24%. The adjustment for the provision of deferred tax liabilities will not result in cash outflow by HRLSB. # The audited net book value of the Land as at 31 December 2016 was RM8,026,271 due to professional fees incurred for the applications of the Master Layout Plan and the Planning Permission of RM31,580 which was not taken up earlier. In view of the said difference, the impact to the net revaluation surplus would be as follows: The net revaluation surplus was arrived at as follows: RM Market value of the Land 17,000,000 Less: Audited net book value of the Land as at 31 December 2016 (8,026,271) Revaluation surplus 8,973,729 Less: Deferred tax liabilities at 24% (2,153,695) Net revaluation surplus 6,820,034 (ii) The Advances by DYBL has increased to RM6,019,217 as at the date of the SSA and to RM7,017, as at the LPD. DYBL in his capacity as a shareholder of HRLSB has been making monetary advances to HRLSB for working capital purposes. In consideration of our Company agreeing to enter into the SSA, DYBL agreed to waive all his rights to claim for the said advances from HRLSB. The Advances by DYBL shall de deemed dully settled by HRLSB to DYBL upon the completion of the SSA on the Completion Date. As such, the waiver of the Advances by DYBL will be treated as a capital contribution reserve (by a shareholder) of HRLSB. (iii) Bank borrowings was RM3,329,344* as at 31 December 2016 comprising the following: RM - Overdraft 297,896 # - Term loan with Ambank 3,031,448 # 3,329,344 * The balance bank borrowings (after excluding the Redemption Sum) is RM129,344. Any amounts in excess of the Redemption Sum at the time the Land is redeemed from Ambank will be assumed by DYBL. As at the LPD, the term loan and overdraft outstanding were RM2.07 million and RM0.20 million, respectively. The Land shall be redeemed by the Vendors and shall be free from any liens, charges and encumbrances prior to the completion of the Proposed Acquisition. # The unaudited and audited values as at 31 December 2016 are the same. 21

32 Premised on the above, our Board (save for DYBL being the Interested Person) is of the view that the Purchase Consideration is justifiable Basis and justification of the issue price of the Consideration Shares The issue price of RM per Consideration Share was arrived at after taking into consideration the 5D-VWAP of Asia Poly Shares up to and including 24 January 2017, being the latest practicable date prior to entering into the SSA of RM The basis of determining the issue price of the Consideration Shares was in accordance with marketbased principles and the 5D-VWAP represents the current weighted average trading price of Asia Poly Shares up to the said latest practicable date. The Purchase Consideration of RM14,800,000 will be satisfied via a combination of the Cash Consideration and issuance of the Consideration Shares. The part settlement via the Consideration Shares will ease the strain on our Group s cash flow as the Cash Consideration is expected to be financed via our Group s internally generated funds. Premised on the above, our Board (save for DYBL being the Interested Person) is of the view that the issue price and the part settlement of the Purchase Consideration via the issuance of the Consideration Shares is justifiable Mode of satisfaction of Purchase Consideration The mode of satisfaction of the Purchase Consideration to the Vendors is as follows: Equity interest in HRLSB to be acquired from the Vendors DYBL YBH YBT Total 80.00% 10.00% 10.00% % RM RM RM RM Apportionment of the Deposit payable to Vendors 1,184, , ,000 1,480,000 Apportionment of balance cash payable to Vendors 2,656, , ,000 3,320,000 Apportionment of Redemption Sum 2,560, , ,000 3,200,000 Cash Consideration 6,400, , ,000 8,000,000 Settlement of part Purchase Consideration via the issuance of Consideration Shares 5,440, , ,000 6,800,000 Total Purchase Consideration 11,840,000 1,480,000 1,480,000 14,800,000 Number of Consideration Shares to be issued at the issue price of RM ,621,756 4,202,719 4,202,719 42,027, Ranking of the Consideration Shares The Consideration Shares shall, upon allotment and issuance, rank pari passu in all respects with the existing Asia Poly Shares, save and except that they shall not be entitled to any dividends, rights, allotments and/or other distributions that are declared, made or paid to the shareholders of our Company, the entitlement date of which is prior to the date of allotment and issuance of the Consideration Shares Liabilities to be assumed There are no liabilities, including contingent liabilities or guarantees to be assumed by our Company arising from the Proposed Acquisition. 22

33 Additional financial commitment required Save for the future development costs to be incurred for the Proposed Development (as set out in Section of Part A of this Circular), there is no other additional financial commitment required by our Company arising from the Proposed Acquisition Sources of funding The Purchase Consideration of RM14,800,000 will be satisfied via a combination of the Cash Consideration and issuance of the Consideration Shares. The Cash Consideration is expected to be satisfied via our Group s internally generated funds Original cost of investment The Vendors original cost of investment in HRLSB is as follows: Vendor Date of investment No. of HRLSB Shares Cost of investment (RM) DYBL 26 December June , , January , ,000 * YBH 15 January ,000 50,000 * YBT 15 January ,000 50,000 * Total 500, ,000 Note: * Purchased from an original shareholder who is an independent third party. Based on the above, the total original cost of investment of the Vendors in HRLSB is RM500,000. In addition, pursuant to the SSA DYBL has agreed to waive all his rights to claim for the Advances by DYBL of RM7,017, as at the LPD which shall be treated as a capital contribution reserve (by a shareholder) of HRLSB, subject to the completion of the SSA. As such, the total original cost of investment of the Vendors in HRLSB will increase to RM7,517, [The rest of this page has been intentionally left blank] 23

34 2.3 Proposed Variation Our Company raised the Rights Proceeds from the Two-Call Rights Issue of Shares with Warrants. Our Company wishes to undertake the Proposed Variation as follows: Description Actual proceeds raised and proposed utilisation (1) (RM 000) Amount utilised as at the LPD (RM 000) Amount unutilised as at the LPD (RM 000) Proposed Variation (RM 000) After Proposed Variation (RM 000) Expected timeframe for the utilisation from the date of receipt on 21 December 2015 Repayment of bank borrowings 3,162 3, Within 12 months Setting up of a waste management 3,000-3,000 (3,000) - Within 18 months plant (2) Working capital 2,000 2,000-3,000 3,000 Within 18 months (3) Estimated expenses in relation to the previous corporate exercises Within 2 weeks Total 8,792 5,792 3,000-3,000 Notes: (1) As disclosed in the Rights Circular. (2) As disclosed in the Rights Circular, our Group intended to utilise RM3.00 million of the proceeds to fund the entire estimated cost to set up a waste management plant (a separate building with a built-up area of approximately 2,400 sq. m. beside our Group s current production factory on our existing land in Klang, Selangor) to recover the scrap/strip (i.e., waste) from its current business. The scrap/strip arises mainly from the manufacturing process as the acrylic sheets manufactured would be slightly larger than the customers order. The acrylic sheets would then be cut to the actual size as per the customers order thus resulting in scrap/strip pieces of acrylic sheets. By setting up the waste management plant, this will enable our Group to breakdown and depolymerise the scraps/strips from polymer units to monomer units which are known as DMMA. The DMMA will have an average purity of 96% to 98% and can be used in our Group s own production of cast acrylic sheets, where the DMMA can be mixed with MMA to produce new cast acrylic sheets. (3) The intended timeframe for utilisation (from 21 December 2015) is proposed to be revised from 18 months to 30 months (i.e., from 20 June 2017 to 20 June 2018). 24