Claims: A Consumer s Perspective

|

|

|

- Jessie Barker

- 5 years ago

- Views:

Transcription

1 Claims: A Consumer s Perspective Pacific Life Re 2018 Irish consumer research

2

3 When does a consumer think about protection insurance claims? The most likely answer is: very rarely; when they are in the unfortunate position of having to make one. Alternatively, they might have seen headlines like these: Devastated widower in tears as he reveals family may lose home after beloved wife s death Insurers doctors deny ANOTHER life insurance claim from a dying customer Scales of injustice? The wrong weight on a form meant one grieving widow received NOTHING from her insurer When protection insurers, and more specifically, the work of the claims department, comes to public attention, it s often when the media are shining the spotlight on a dissatisfied customer; typically an individual who feels let down or cheated by their insurer. With this in mind, and to understand a little more about consumer perceptions of protection cover, we wanted to know what consumers really think about insurers. Do they think that claims are routinely declined? Do they have any idea why some claims are declined? How do they think an insurer should respond when a customer has provided them with inaccurate or incorrect information? In February this year, we commissioned a survey of 1,000 adults in the Republic of Ireland to find out. 03

4 04 Do Consumers Trust Insurers to Pay Claims? Besides the cost of cover, it s safe to assume that this is one of the most important factors for consumers. When it comes to the moment of truth, how likely is it that their claim will get paid? We asked: What percentage of life insurance claims do you think are paid? 25% 20% 15% 5% 0% 22% 16% 13% 14% 7% 1% 4% 5% 4% 5% It probably comes as no surprise that consumers in general have very little insight into how many claims are actually paid by the life insurance industry. The perception falls a long way short of the true figures. 83% of consumers believe that no more than 80% of life claims are paid Nearly a quarter of our respondents think that only 70%-80% of claims are paid out In reality, most insurers report that well in excess of 90% of their life claims are paid. Only 7% of our respondents believed that this is the case.

5 Why Are Protection Claims Declined? It s disappointing that consumers think so many claims are declined, so we wanted to know if they have any concept of why this does sometimes happen. We asked: Why do you think insurers sometimes decline life insurance claims? 25% 20% 15% 25% 17% 16% 5% 0% 9% 8% 7% 6% 6% 5% 2% We might have expected that small print or loopholes would feature heavily here, however our findings show consumers perceptions of why claims are declined in a slightly better light. In fact, 42% think that claims are declined due to some form of misrepresentation by the customer, either lying on forms or not disclosing relevant information. Whilst this is promising, there is still more that could be done to promote positive claims stories; for example, insurers could publish case studies or client testimonials on their website from satisfied customers. 05

6 06 Do Insurers Treat Misrepresentation Fairly? Having established that consumers understand that misrepresentation occurs, and that this might result in a declined claim, we wanted to know whether or not they think that insurers are fair in the way they treat misrepresentation. We described the following scenario: A person who applies for life insurance doesn t tell the insurer they are a smoker. Had they done so, they would have had to pay twice as much for their life insurance cover. A year after they bought the insurance, they make a claim. We asked: For each of the following causes of death, how much, if anything, do you think it would be reasonable for the insurer to pay? 100% 90% 80% 70% 60% 50% 40% 20% 0% 9% 16% 18% 14% 39% 31% 37% 26% 77% 40% 53% 45% 43% 21% Car crash Skin cancer Heart attack Suicide Lung cancer Shouldn't have to pay any of the claim Should pay a part of the claim Should pay the whole of the claim

7 It s reasonable to make a couple of assumptions about how consumers expect misrepresentation to be treated: 1. Most of the consumers in our sample would expect a penalty to be imposed where the claim is for lung cancer. This suggests that where there s a clearly established link between the information that was not disclosed (smoking) and the cause of death, the penalty for the misrepresentation is more easily understood. 2. Where that link is not so clearly established, consumers typically expect insurers to respond more favourably. The responses recorded where the death was the result of a car crash are not at all surprising. Most consumers would expect the claim to be paid in full. Based on our market experience both in the UK and Ireland, most insurers would limit their claims investigation in these circumstances and a full payment is the most likely outcome. It s a little more difficult to interpret the response where the cause of death is a heart attack. We know that smoking is a risk factor for heart disease, so why does more than twice the number of consumers expect a full payment when the cause of death is a heart attack as opposed to lung cancer? Perhaps there is less public awareness of the risks of smoking in relation to heart attacks, than there is of the link between smoking and lung cancer, in spite of numerous public health awareness campaigns highlighting the effect smoking has on the general health of the population. Suicide is something of an outlier, as many consumers believe that insurers simply do not pay out in these circumstances. 07

8

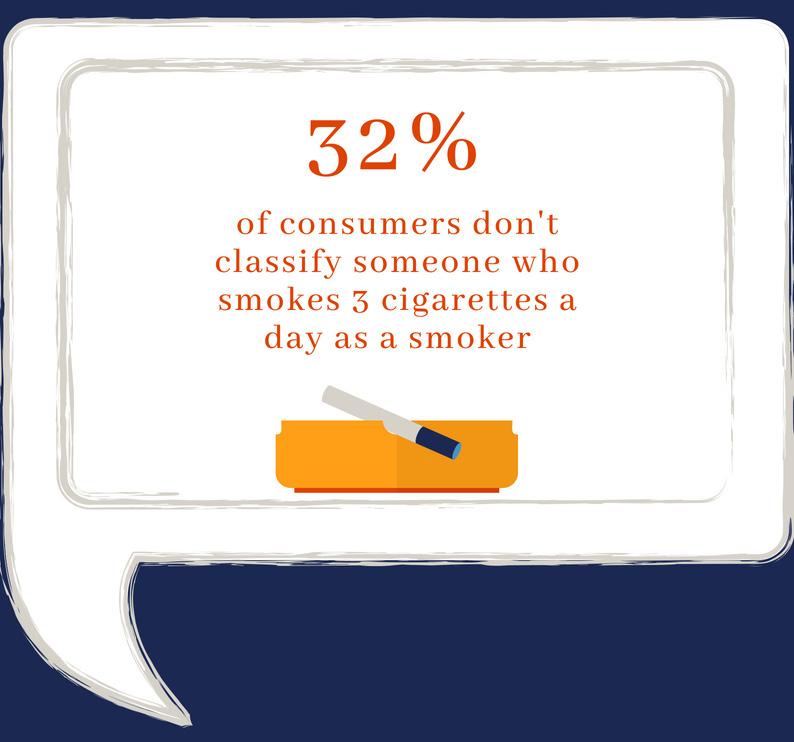

9 When is a Smoker Not a Smoker? We ve looked at attitudes towards misrepresentation where an individual fails to disclose that they are a smoker, but what is a smoker? It seems a very obvious question, with a yes or no answer. Life insurance applications always include a very clearly worded question on this and there s rarely any ambiguity. Our consumer research suggests that people have very different ideas about what makes someone a smoker, driven by how many cigarettes, and how often, a person smokes. We asked: Which of the following would you class as a smoker? 100% 90% 100% 80% 70% 60% 68% 50% 40% 20% 29% 0% Daily - more than 3 cigarettes Daily - up to 3 cigarettes Occasional cigarette or cigar when out socially (e.g. 5 a week) 11% Used to smoke cigarettes, but now using an e- cigarette only There are some surprising results here, perhaps the most unexpected being that 32% thought a person who smokes 3 cigarettes every day is a nonsmoker. 09

10 10 We looked into this in greater depth, to see if there was any difference between how people think, depending on whether they themselves are a smoker, exsmoker or non-smoker. 100% 90% 80% 70% 60% 100% 67% 80% Current smoker Ex-smoker Have never smoked 50% 40% 20% 0% Daily - more than 3 cigarettes 37% Daily - up to 3 cigarettes 31% 35% 6% 1% Occasional cigarette or cigar when out socially (e.g. 5 a week) 13% 11% Used to smoke cigarettes, but now using an e-cigarette only Smokers appear to have a much higher benchmark in terms of how many cigarettes you have to smoke every day to be classified as a smoker. Might this attitude influence how a person interprets and answers a question about smoking on a life insurance application?

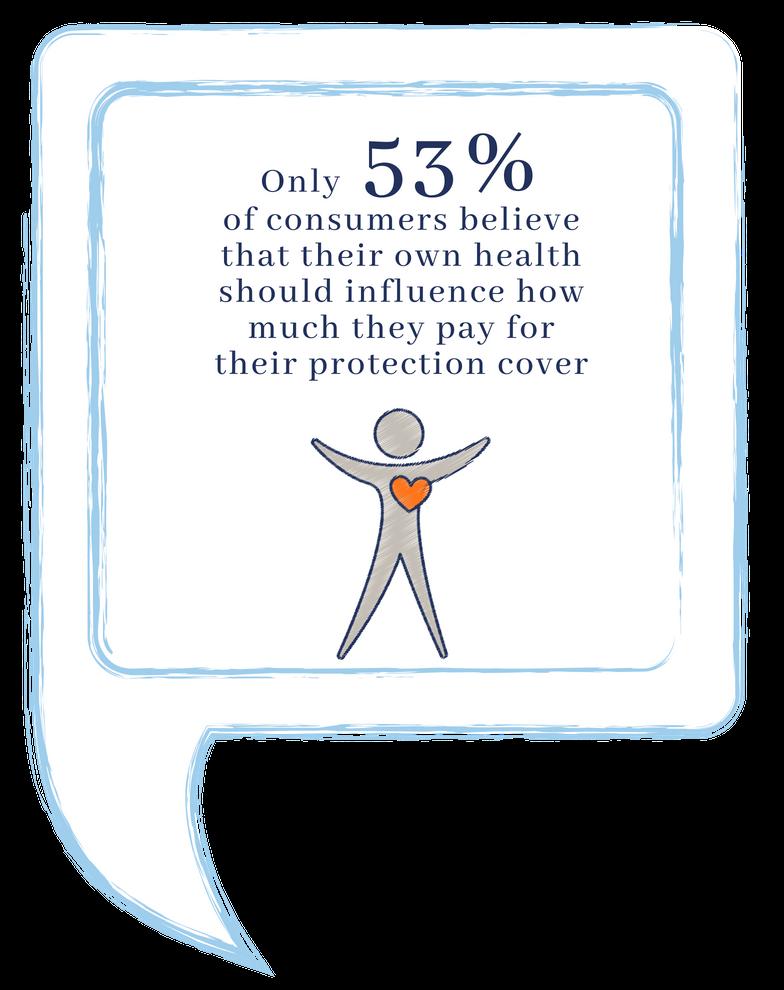

11 What Factors Drive the Cost of Cover? We ve seen that consumers have some expectation of a financial penalty if certain facts are not disclosed. We wanted to know if they understand how their own disclosures affect how much they pay for life cover. We asked: Do you think life insurers should be able to charge different amounts depending on any of the following...? 80% 70% 60% Smoking habits 50% Lifestyle Personal health 40% 69% 55% 53% Age Family health Salary Postcode Gender 20% 42% 0% 22% 12% 3% It s interesting to note that nearly 70% would expect to pay more for their life cover if they were a smoker, when compared to those who would still expect the insurer to pay a claim in full if a person fails to disclose that they are a smoker. It s perhaps a little more worrying that only around half of those surveyed felt that their own medical history and alcohol consumption should be taken into consideration. Only 22% appear to appreciate the relevance of their own family history and the impact this might have on their own health and long-term risk. 11

12 12 When do we Pay Life Claims Early? Assessing claims based on a predicted outcome is vastly different to assessing claims where the insured event has already taken place. When you also consider the emotive nature of many Terminal Illness claims, it s easy to see that these can be very challenging cases for claims assessors. The industry definition of Terminal Illness is based on a 12 month life expectancy but this has no relevance to any medical definition or clinical practice. We wanted to know what consumers understand the word terminal to mean, in terms of life expectancy. We asked: What length of time do you consider as being terminally ill? 35% 25% 20% 15% 28% 29% 5% 19% 14% 11% 0% Up to 3 months to live More than 3 months but less than 6 months to live More than 6 months but less than 12 months to live More than 12 months but less than 24 months to live Longer than 24 months to live We had a broad range of responses to this question, suggesting that terminal means different things to different people. The Terminal Illness definition was introduced to provide peace of mind for Terminal Illness policyholders with a very short life expectancy, and to allow them time to ensure that their financial affairs are in order before they die.

13 out before death if the policyholder has a very short life expectancy (to get their affairs in order). In this situation, at what point is it reasonable for an insurer to make the payment? 40% 35% 25% With this in mind, we asked consumers: Life insurance policies can pay 20% 15% 35% 21% 5% 0% 8% Up to 3 months More than 3 monthsmore than 6 months but less than 6 but less than 12 More than 12 months but less than 24 5% Longer than 24 months We found that 87% of those surveyed felt that an accelerated life claim payment would be reasonable where life expectancy is less than 12 months; 66% indicated less than 6 months. In the UK, Terminal Illness claims have increased to the point where, for some insurers, Terminal Illness accounts for more than of all life claims. The vast majority of Terminal Illness claims are for cancer, where for many diagnoses, outcomes are improving and published data is quickly becoming outdated. Outcomes for incurable neurological conditions like Motor Neurone Disease and Parkinson s are even more difficult to predict. Many specialists acknowledge that it s very difficult to predict life expectancy beyond 6 months. A reasonable case can be made for a review of the current Terminal Illness definition that would reduce the life expectancy requirement to 6 months. From our research, it appears that this would be more in-line with consumer expectations. 13

14 14 Some Final Thoughts... We ve seen that consumers understand some of the concepts that influence our claims decisions and broadly, would expect there to be a penalty where misrepresentation has been discovered. We asked: If a policyholder has been found to have not disclosed important information at the point of claim, what should the insurer do? 22% Reduce the amount paid Pay claim in full 78% We ve also seen that there is a gap between how they expect insurers to deal with misrepresentation and what happens in practice. Consumers trust is vital to our industry, but do we build more trust by simply paying more claims? We regularly meet with claims teams from insurers accross the industry in Ireland and it s very clear that they strive to treat claimants fairly. However, they also recognise that they have a responsibility to all of their customers. In a previous survey we commissioned, consumers were asked whether they would be prepared to pay more for their own life insurance to cover the cost of some claims being paid out to people who did not provide important facts when their policy was taken out... 76% said no. Declined claims are statistically rare and insurers typically only apply penalties where significant and material misrepresentation is identified. Bridging the gap between consumer perceptions and the reality of how many claims are paid remains a challenge. It s perhaps unrealistic to expect much press attention when it comes to positive claim outcomes but insurers might find benefit in highlighting their claims experience during the sales and application process.

15

16 For more information about Pacific Life Re please visit our website follow us on LinkedIn or contact James Tait Head of Protection Pacific Life Re Europe T: +44 (0) E: Ian Rowe Director, Claims Pacific Life Re Europe T: +44 (0) E: Pacific Life Re Limited (No ) is registered in England and Wales and has its registered office at Tower Bridge House, St Katharine s Way, London, E1W 1BA. Pacific Life Re Limited is authorised and regulated by the Financial Conduct Authority and Prudential Regulatory Authority in the United Kingdom (Reference Number ). The material contained in this booklet is for information purposes only. Pacific Life Re gives no assurance as to the completeness or accuracy of such material and accepts no responsibility for loss occasioned to any person acting or refraining from acting on the basis of such material Pacific Life Re Limited. All rights reserved. PLRECCR0918

Claims: A Consumer s Perspective. Pacific Life Re 2018 UK consumer research

Claims: A Consumer s Perspective Pacific Life Re 2018 UK consumer research When does a consumer think about protection insurance claims? Typically, the answer is: very rarely; except perhaps, when they

Claims: A Consumer s Perspective Pacific Life Re 2018 UK consumer research When does a consumer think about protection insurance claims? Typically, the answer is: very rarely; except perhaps, when they

THE MOMENT OF TRUTH: A consumer s perspective

EUROPE May 2017 In 2016, we commissioned a survey of 2,000 people in the UK to try to gain some insight into their views of protection claims management, what they consider the chance is of getting a claim

EUROPE May 2017 In 2016, we commissioned a survey of 2,000 people in the UK to try to gain some insight into their views of protection claims management, what they consider the chance is of getting a claim

35 Years of CI. Pacific Life Re Re:think. Introduction. August September 2018

35 Years of CI Pacific Life Re Re:think August 2018 September 2018 Introduction This year marks 35 years since the first Critical Illness (CI) insurance policy was launched. It was the inspiration of a

35 Years of CI Pacific Life Re Re:think August 2018 September 2018 Introduction This year marks 35 years since the first Critical Illness (CI) insurance policy was launched. It was the inspiration of a

60 is the New 50. Pacific Life Re Re:think. Introduction. August October 2018

60 is the New 50 Pacific Life Re Re:think August 2018 October 2018 Introduction The whole of life over 50s plan in one shape or other has been a feature of the UK protection market for a number of years.

60 is the New 50 Pacific Life Re Re:think August 2018 October 2018 Introduction The whole of life over 50s plan in one shape or other has been a feature of the UK protection market for a number of years.

Protecting Families. Getting the conversation started. Retirement Investments Insurance Health

Retirement Investments Insurance Health Protecting Families Getting the conversation started For financial adviser use only. Not approved for use with customers. Unearthing opportunities in an ever-changing

Retirement Investments Insurance Health Protecting Families Getting the conversation started For financial adviser use only. Not approved for use with customers. Unearthing opportunities in an ever-changing

THE IMPORTANCE OFPERSONAL PROTECTION

THE IMPORTANCE OFPERSONAL PROTECTION THE IMPORTANCE OF PERSONAL PROTECTION You re reading this leaflet because your Financial Adviser has identified you have a protection need. They ll help you understand

THE IMPORTANCE OFPERSONAL PROTECTION THE IMPORTANCE OF PERSONAL PROTECTION You re reading this leaflet because your Financial Adviser has identified you have a protection need. They ll help you understand

Legal & General Critical Illness Cover

1 Contents Critical Illness Cover Page 3 What is a critical illness? Page 4 Could it happen to me? Page 5 How can Critical Illness Cover help? Page 6-7 Legal & General Nurse Support Services Page 8-9 Legal

1 Contents Critical Illness Cover Page 3 What is a critical illness? Page 4 Could it happen to me? Page 5 How can Critical Illness Cover help? Page 6-7 Legal & General Nurse Support Services Page 8-9 Legal

Life and protection insurance explained

protection? illness Life and protection explained A guide to personal and family protection This guide explains the types of life and protection available and how they can offer you valuable peace of mind.

protection? illness Life and protection explained A guide to personal and family protection This guide explains the types of life and protection available and how they can offer you valuable peace of mind.

Life and protection insurance explained

illness Life and protection explained A guide to personal and family protection This guide explains the types of life and protection available and how they can offer you valuable peace of mind. If you

illness Life and protection explained A guide to personal and family protection This guide explains the types of life and protection available and how they can offer you valuable peace of mind. If you

SCOTTISH WIDOWS ENHANCED ANNUITY HOW COULD YOU MAKE MORE OF YOUR RETIREMENT INCOME?

SCOTTISH WIDOWS ENHANCED ANNUITY HOW COULD YOU MAKE MORE OF YOUR RETIREMENT INCOME? PAGE 1 HOW COULD YOU MAKE MORE OF YOUR RETIREMENT INCOME? PAGE 2 CAN YOU GET MORE INCOME FROM YOUR ANNUITY? PAGE 3 ARE

SCOTTISH WIDOWS ENHANCED ANNUITY HOW COULD YOU MAKE MORE OF YOUR RETIREMENT INCOME? PAGE 1 HOW COULD YOU MAKE MORE OF YOUR RETIREMENT INCOME? PAGE 2 CAN YOU GET MORE INCOME FROM YOUR ANNUITY? PAGE 3 ARE

Income Protection Benefit. How would you cope without an income?

Income Protection Benefit How would you cope without an income? Contents 3 Ensure you re ready 4 The plan - your questions answered 5 Being there for Michael when he needed us most 6 Income protection.

Income Protection Benefit How would you cope without an income? Contents 3 Ensure you re ready 4 The plan - your questions answered 5 Being there for Michael when he needed us most 6 Income protection.

LV= Flexible Guarantee Bond Series 3. Bond Conditions

LV= Flexible Guarantee Bond Series 3 Bond Conditions LV= Flexible Guarantee Bond Series 3 Bond Conditions Welcome to LV=, and to our Flexible Guarantee Bond Series 3 These Bond Conditions, together with

LV= Flexible Guarantee Bond Series 3 Bond Conditions LV= Flexible Guarantee Bond Series 3 Bond Conditions Welcome to LV=, and to our Flexible Guarantee Bond Series 3 These Bond Conditions, together with

Life insurance. Serious and critical illness insurance

protection? Life illness Life and protection explained A guide to personal and family protection his guide explains the types of life and p rotection available and how t hey can offer you valuable peace

protection? Life illness Life and protection explained A guide to personal and family protection his guide explains the types of life and p rotection available and how t hey can offer you valuable peace

100% 36.6 MILLION 152, % PAID 100% PAID 10.5 MILLION 12.3 MILLION PAID LIFE COVER 104, ,920

CLAIMS IN 2017 We regularly update our literature. You or your financial adviser can confirm that this March 2018 version is the latest by checking the literature library on our website, www.oldmutualwealth.co.uk

CLAIMS IN 2017 We regularly update our literature. You or your financial adviser can confirm that this March 2018 version is the latest by checking the literature library on our website, www.oldmutualwealth.co.uk

BUYING A PENSION ANNUITY

PENSION ANNUITIES BUYING A PENSION ANNUITY BUYING A PENSION ANNUITY 1 This is an important, once and for all, decision. We want you to be confident that you have the information you need to make the right

PENSION ANNUITIES BUYING A PENSION ANNUITY BUYING A PENSION ANNUITY 1 This is an important, once and for all, decision. We want you to be confident that you have the information you need to make the right

FREE Parent Life Cover

Free Life Cover FREE Parent Life Cover A helping hand to protect your family Free Parent Life Cover Aim Cost of cover Time period Jargonfree To kick start protecting your family by giving each parent 25,000

Free Life Cover FREE Parent Life Cover A helping hand to protect your family Free Parent Life Cover Aim Cost of cover Time period Jargonfree To kick start protecting your family by giving each parent 25,000

Protecting Families. Getting the conversation started. For financial adviser use only. Not approved for use with customers.

Retirement Investments Insurance Health Protecting Families Getting the conversation started For financial adviser use only. Not approved for use with customers. Unearthing opportunities in an ever-changing

Retirement Investments Insurance Health Protecting Families Getting the conversation started For financial adviser use only. Not approved for use with customers. Unearthing opportunities in an ever-changing

PENSIONS INVESTMENTS LIFE INSURANCE FREE LIFE INSURANCE A HELPING HAND TO PROTECT YOUR LOVED-ONES

PENSIONS INVESTMENTS LIFE INSURANCE FREE LIFE INSURANCE A HELPING HAND TO PROTECT YOUR LOVED-ONES FREE LIFE INSURANCE Aim To give you a head start with your life insurance needs. Cost of cover Absolutely

PENSIONS INVESTMENTS LIFE INSURANCE FREE LIFE INSURANCE A HELPING HAND TO PROTECT YOUR LOVED-ONES FREE LIFE INSURANCE Aim To give you a head start with your life insurance needs. Cost of cover Absolutely

GUIDE TO OUR PROTECTION SERVICES. Protecting the things that matter the most

GUIDE TO OUR PROTECTION SERVICES Protecting the things that matter the most 02 GUIDE TO INVESTING Contents Intrinsic shares our values and beliefs about being clear and transparent with our clients. This

GUIDE TO OUR PROTECTION SERVICES Protecting the things that matter the most 02 GUIDE TO INVESTING Contents Intrinsic shares our values and beliefs about being clear and transparent with our clients. This

LEVEL TERM ASSURANCE KEY FEATURES

CELEBRATING seeing retirement differently YEARS sin ce 1 9 9 5 The Financial Conduct Authority is a financial service regulator. It requires us, Partnership, to give you this important information to help

CELEBRATING seeing retirement differently YEARS sin ce 1 9 9 5 The Financial Conduct Authority is a financial service regulator. It requires us, Partnership, to give you this important information to help

Providing financial and emotional support

Providing financial and emotional support WHAT IS Group Critical Illness policies pay out a cash lump-sum if you suffer one of the agreed list of illnesses and surgical procedures as set out in our policy

Providing financial and emotional support WHAT IS Group Critical Illness policies pay out a cash lump-sum if you suffer one of the agreed list of illnesses and surgical procedures as set out in our policy

THE FAMILY PROTECTION CONVERSATION

THE FAMILY PROTECTION CONVERSATION CONVERSATION STARTERS This information is for UK financial adviser use only and should not be distributed to, or relied upon by, any other person. As you know, people

THE FAMILY PROTECTION CONVERSATION CONVERSATION STARTERS This information is for UK financial adviser use only and should not be distributed to, or relied upon by, any other person. As you know, people

STATE OF THE PROTECTION NATION. March 2017

STATE OF THE March 2017 INTRODUCTION Royal London commissioned this research to find out how people felt about their own protection needs and the industry as a whole. And to answer questions such as: does

STATE OF THE March 2017 INTRODUCTION Royal London commissioned this research to find out how people felt about their own protection needs and the industry as a whole. And to answer questions such as: does

Act today, protect what matters

Why you need protection Act today, protect what matters Life changes. Be prepared. Be protected. Say Yes to Life and Critical illness cover If someone is likely to suffer financially if you fall seriously

Why you need protection Act today, protect what matters Life changes. Be prepared. Be protected. Say Yes to Life and Critical illness cover If someone is likely to suffer financially if you fall seriously

pension annuity customer guide guaranteed income for life

pension annuity customer guide guaranteed income for life 2 pension annuity If you re thinking... I want a secure income that is guaranteed to be paid for life. How can I be sure I ll get the most out

pension annuity customer guide guaranteed income for life 2 pension annuity If you re thinking... I want a secure income that is guaranteed to be paid for life. How can I be sure I ll get the most out

SHEDDING LIGHT ON LIFE INSURANCE

SHEDDING LIGHT ON LIFE INSURANCE A practical guide LEARN MORE ABOUT Safeguarding your loved ones Protecting your future Ensuring your dreams live on Life s brighter under the sun About this guide We ve

SHEDDING LIGHT ON LIFE INSURANCE A practical guide LEARN MORE ABOUT Safeguarding your loved ones Protecting your future Ensuring your dreams live on Life s brighter under the sun About this guide We ve

Aviva Personal Pension

Retirement Investments Insurance Aviva Personal Pension Customer Booklet Contents 10 good reasons to start a pension 3 Introducing the Aviva Personal Pension 4 Aviva Online 5 Is the Aviva Personal Pension

Retirement Investments Insurance Aviva Personal Pension Customer Booklet Contents 10 good reasons to start a pension 3 Introducing the Aviva Personal Pension 4 Aviva Online 5 Is the Aviva Personal Pension

Please read this document carefully as it contains important information about this plan VITALITYLIFE ESSENTIALS PLAN SUMMARY

Please read this document carefully as it contains important information about this plan VITALITYLIFE ESSENTIALS PLAN SUMMARY About this booklet This booklet gives you an overview of the cover you have

Please read this document carefully as it contains important information about this plan VITALITYLIFE ESSENTIALS PLAN SUMMARY About this booklet This booklet gives you an overview of the cover you have

GUARDIAN LIFE PROTECTION

A CUSTOMER GUIDE GUARDIAN LIFE PROTECTION BECAUSE LIFE CHANGES The life insurance you need today won t necessarily be the life insurance you need tomorrow. As we all know, life has a habit of changing.

A CUSTOMER GUIDE GUARDIAN LIFE PROTECTION BECAUSE LIFE CHANGES The life insurance you need today won t necessarily be the life insurance you need tomorrow. As we all know, life has a habit of changing.

Protection. Free Life Insurance A HELPING HAND TO PROTECT YOUR LOVED-ONES FREE LIFE INSURANCE IS PROVIDED BY IRISH LIFE ASSURANCE PLC.

Protection Free Life Insurance A HELPING HAND TO PROTECT YOUR LOVED-ONES FREE LIFE INSURANCE IS PROVIDED BY IRISH LIFE ASSURANCE PLC. FREE LIFE INSURANCE Aim To give you a head start with your life insurance

Protection Free Life Insurance A HELPING HAND TO PROTECT YOUR LOVED-ONES FREE LIFE INSURANCE IS PROVIDED BY IRISH LIFE ASSURANCE PLC. FREE LIFE INSURANCE Aim To give you a head start with your life insurance

pension annuity customer guide guaranteed income for life

pension annuity customer guide guaranteed income for life 2 pension annuity If you re thinking... I want a secure income that is guaranteed to be paid for life. How can I be sure I ll get the most out

pension annuity customer guide guaranteed income for life 2 pension annuity If you re thinking... I want a secure income that is guaranteed to be paid for life. How can I be sure I ll get the most out

Buying an annuity Legal & General s Pension Annuity

Buying an annuity Legal & General s Pension Annuity This is an important, once and for all, decision. We want you to be confident that you have the information you need to make the right decision. Contents

Buying an annuity Legal & General s Pension Annuity This is an important, once and for all, decision. We want you to be confident that you have the information you need to make the right decision. Contents

important information

Key Features of the Relevant Life Cover policy The Financial Conduct Authority is a financial services regulator. It requires us, LV= to give you this important information to help you decide whether our

Key Features of the Relevant Life Cover policy The Financial Conduct Authority is a financial services regulator. It requires us, LV= to give you this important information to help you decide whether our

Over 50s Life Cover Terms and Conditions

Over 50s Life Cover Terms and Conditions Contents How does my Over 50s Life Cover work?... page 4 How to make a claim... page 6 Making changes... page 8 How to complain... page 10 Cancelling your policy...

Over 50s Life Cover Terms and Conditions Contents How does my Over 50s Life Cover work?... page 4 How to make a claim... page 6 Making changes... page 8 How to complain... page 10 Cancelling your policy...

Guide to buying an annuity

Guide to buying an annuity 2 Welcome to our guide to buying an annuity You now have more choice than ever before when it comes to using your pension savings. Of course having more options can make it difficult

Guide to buying an annuity 2 Welcome to our guide to buying an annuity You now have more choice than ever before when it comes to using your pension savings. Of course having more options can make it difficult

Protection Report. protecting your home

Protection Report protecting your home May 2014 A home is rarely justfour walls It represents the way we engage with almost every element of family, community, business and, indeed, life in general. The

Protection Report protecting your home May 2014 A home is rarely justfour walls It represents the way we engage with almost every element of family, community, business and, indeed, life in general. The

Aviva Retirement Bond

Retirement Investments Insurance Aviva Retirement Bond Customer Booklet Contents 5 good reasons to start a Retirement Bond 3 Introducing the Aviva Retirement Bond 4 Aviva Online 5 Is the Aviva Retirement

Retirement Investments Insurance Aviva Retirement Bond Customer Booklet Contents 5 good reasons to start a Retirement Bond 3 Introducing the Aviva Retirement Bond 4 Aviva Online 5 Is the Aviva Retirement

HELPING CLIENTS WITH EXPERT ADVICE

INCOME PROTECTION ADVISER GUIDE HELPING CLIENTS WITH EXPERT ADVICE People are well aware of what could happen if they were unable to work, so they also understand the value of a protection product. However,

INCOME PROTECTION ADVISER GUIDE HELPING CLIENTS WITH EXPERT ADVICE People are well aware of what could happen if they were unable to work, so they also understand the value of a protection product. However,

Key Features of the Group Stakeholder Pension Scheme. This is an important document which you should keep in a safe place.

Key Features of the Group Stakeholder Pension Scheme This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

Key Features of the Group Stakeholder Pension Scheme This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

RIGHT UP YOUR STREET.

BUY TO LET LANDLORDS GUIDE RIGHT UP YOUR STREET. More and more people are renting. As a landlord you ve got enough to think about, without worrying if you ve made the right financial choices. Our advisers

BUY TO LET LANDLORDS GUIDE RIGHT UP YOUR STREET. More and more people are renting. As a landlord you ve got enough to think about, without worrying if you ve made the right financial choices. Our advisers

Reaching out to renters

For financial adviser use only. Not approved for use with customers. Reaching out to renters How to write effective letters and emails to renters about the need for protection With renting on the rise,

For financial adviser use only. Not approved for use with customers. Reaching out to renters How to write effective letters and emails to renters about the need for protection With renting on the rise,

THE skandia plan. A unit-linked life assurance plan that can provide cover throughout your life. for information only.

Key features of THE skandia plan A unit-linked life assurance plan that can provide cover throughout your life for information only. this product is closed to new business The Financial Conduct Authority

Key features of THE skandia plan A unit-linked life assurance plan that can provide cover throughout your life for information only. this product is closed to new business The Financial Conduct Authority

Your Guide to Life Insurance for Families

Your Guide to Life Insurance for Families (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance for Families Contents Does My Family Need Life Insurance? 4 Types of Life Insurance for Families

Your Guide to Life Insurance for Families (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance for Families Contents Does My Family Need Life Insurance? 4 Types of Life Insurance for Families

Key Features of the Flexible Protection Plan

Key Features of the Flexible Protection Plan LV= Personal Sick Pay The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important information to help

Key Features of the Flexible Protection Plan LV= Personal Sick Pay The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important information to help

Guide to. buying an annuity

Guide to buying an annuity 2 Guide to buying an annuity Welcome to our guide to buying an annuity You now have more flexibility than ever before when it comes to using your pension savings. Of course all

Guide to buying an annuity 2 Guide to buying an annuity Welcome to our guide to buying an annuity You now have more flexibility than ever before when it comes to using your pension savings. Of course all

Key Features of the Pension Annuity (including the Enhanced Pension Annuity)

") Key Features of the Pension Annuity (including the Enhanced Pension Annuity) Key Features of the Pension Annuity (including the Enhanced Pension Annuity) The Financial Conduct Authority is a financial

Key Features of the Pension Annuity (including the Enhanced Pension Annuity) Key Features of the Pension Annuity (including the Enhanced Pension Annuity) The Financial Conduct Authority is a financial

Co-Director Insurance. it s. for you. A Guide to Co-Director Insurance

Co-Director Insurance it s for you A Guide to Co-Director Insurance Introducing ROYAL LONDON Ever since we started as a Friendly Society over 150 years ago, at Royal London we ve believed that our difference

Co-Director Insurance it s for you A Guide to Co-Director Insurance Introducing ROYAL LONDON Ever since we started as a Friendly Society over 150 years ago, at Royal London we ve believed that our difference

Pension Report. Savers vs Spenders

Pension Report Savers vs Spenders Exec summary Recent government figures show that while the number of people saving for retirement is at a record high, the average amount they are saving is at a record

Pension Report Savers vs Spenders Exec summary Recent government figures show that while the number of people saving for retirement is at a record high, the average amount they are saving is at a record

Mortgage Insurance. The True Help Canadian Financial Security Program. What To Consider Before You Buy

The True Help Canadian Financial Security Program Mortgage Insurance What To Consider Before You Buy The Safest Way To Protect One of Life s Biggest Assets Mortgage Insurance What To Consider Before You

The True Help Canadian Financial Security Program Mortgage Insurance What To Consider Before You Buy The Safest Way To Protect One of Life s Biggest Assets Mortgage Insurance What To Consider Before You

ABOUT PACIFIC LIFE RE

ABOUT PACIFIC LIFE RE WHO ARE WE? We are a life reinsurance company working with our clients to manage their mortality, morbidity and longevity risk. We have built a strong, experienced team with a reputation

ABOUT PACIFIC LIFE RE WHO ARE WE? We are a life reinsurance company working with our clients to manage their mortality, morbidity and longevity risk. We have built a strong, experienced team with a reputation

Income Protection. Key Features. "Why should I read this document?"

Income Protection Key Features "Why should I read this document?" The Financial Conduct Authority is a financial services regulator. It requires us, the Metropolitan Police Friendly Society, to give you

Income Protection Key Features "Why should I read this document?" The Financial Conduct Authority is a financial services regulator. It requires us, the Metropolitan Police Friendly Society, to give you

ABOUT PACIFIC LIFE RE

ABOUT PACIFIC LIFE RE WHO ARE WE? We are a life reinsurance company working with our clients to manage their mortality, morbidity and longevity risk. We have built a strong, experienced team with a reputation

ABOUT PACIFIC LIFE RE WHO ARE WE? We are a life reinsurance company working with our clients to manage their mortality, morbidity and longevity risk. We have built a strong, experienced team with a reputation

Critical Illness Cover

Critical Illness Cover Contents Page 3 Critical Illness Cover Page 4 5 Could it happen? Page 6 7 Why Legal & General? Page 8 Critical Illness Cover Page 9 Critical Illness Extra Page 10 Children s Critical

Critical Illness Cover Contents Page 3 Critical Illness Cover Page 4 5 Could it happen? Page 6 7 Why Legal & General? Page 8 Critical Illness Cover Page 9 Critical Illness Extra Page 10 Children s Critical

Income Protection and Budget Income Protection

Income Protection and Budget Income Protection Key Features of the Flexible Protection Plan The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important

Income Protection and Budget Income Protection Key Features of the Flexible Protection Plan The Financial Conduct Authority is a financial services regulator. It requires us, LV=, to give you this important

DEMONSTRATING OUR PROTECTION EXPERIENCE

2016 CLAIMS STATISTICS DEMONSTRATING OUR PROTECTION EXPERIENCE This information is for UK financial adviser use only and should not be distributed or relied upon by any other person. SCOTTISH WIDOWS SCOTTISH

2016 CLAIMS STATISTICS DEMONSTRATING OUR PROTECTION EXPERIENCE This information is for UK financial adviser use only and should not be distributed or relied upon by any other person. SCOTTISH WIDOWS SCOTTISH

TO FIT YOUR BUSINESS

For employers Retirement Solutions TAILORED SOLUTIONS TO FIT YOUR BUSINESS A guide for employers WORK SMARTER NOT HARDER These days, offering your workers a good pension is vital. Of course, as pensions

For employers Retirement Solutions TAILORED SOLUTIONS TO FIT YOUR BUSINESS A guide for employers WORK SMARTER NOT HARDER These days, offering your workers a good pension is vital. Of course, as pensions

Key features of the Adaptable Life Plan Helping you decide

Key features of the Adaptable Life Plan Helping you decide This important document gives you a summary of the Adaptable Life Plan. Please read this with your illustration, if you have one, before you decide

Key features of the Adaptable Life Plan Helping you decide This important document gives you a summary of the Adaptable Life Plan. Please read this with your illustration, if you have one, before you decide

Explaining risk, return and volatility. An Octopus guide

Explaining risk, return and volatility An Octopus guide Important information The value of an investment, and any income from it, can fall as well as rise. You may not get back the full amount they invest.

Explaining risk, return and volatility An Octopus guide Important information The value of an investment, and any income from it, can fall as well as rise. You may not get back the full amount they invest.

LV= LIFE LV LIFE INSURANCE. Plan Conditions Document reference: LVLI4

LV= LIFE LV LIFE INSURANCE INSURANCE Plan Conditions Document reference: LVLI4 LV= Life Insurance Plan Conditions Welcome to LV=, and thank you for choosing LV= Life Insurance These conditions and your

LV= LIFE LV LIFE INSURANCE INSURANCE Plan Conditions Document reference: LVLI4 LV= Life Insurance Plan Conditions Welcome to LV=, and thank you for choosing LV= Life Insurance These conditions and your

Key Features of the WorkSave Pension Plan. This is an important document which you should keep in a safe place.

Key Features of the WorkSave Pension Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information you need

Key Features of the WorkSave Pension Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information you need

THE NTT EUROPE COMPANY PENSION GROUP PERSONAL PENSION. A guide to help you prepare for the retirement you want

THE NTT EUROPE COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your NTT Europe company pension is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS

THE NTT EUROPE COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want Your NTT Europe company pension is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS

Life and protection insurance explained

Personal and family protection Life and protection insurance explained This guide explains the types of life and protection insurance available and how they can offer you valuable peace of mind. If you

Personal and family protection Life and protection insurance explained This guide explains the types of life and protection insurance available and how they can offer you valuable peace of mind. If you

Your Life Insurance. Life. Term Life Decreasing Cover Product. Policy booklet January 2017

Your Life Insurance Term Life Decreasing Cover Product Term Life Decreasing Cover Insurance designed to help loved ones when they need it most Policy booklet January 2017 Life Important Documents It is

Your Life Insurance Term Life Decreasing Cover Product Term Life Decreasing Cover Insurance designed to help loved ones when they need it most Policy booklet January 2017 Life Important Documents It is

Key features of the Adaptable Life Plan

Key features of the Adaptable Life Plan Contents Helping you decide This important document gives you a summary of the Adaptable Life Plan. Please read this with your illustration, if you have one, before

Key features of the Adaptable Life Plan Contents Helping you decide This important document gives you a summary of the Adaptable Life Plan. Please read this with your illustration, if you have one, before

YOUR COMPANY PENSION GROUP PERSONAL PENSION. A guide to help you prepare for the retirement you want

YOUR COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want WELCOME TO YOUR SCOTTISH WIDOWS WORKPLACE PENSION Everyone needs a plan for their retirement. This guide

YOUR COMPANY PENSION GROUP PERSONAL PENSION A guide to help you prepare for the retirement you want WELCOME TO YOUR SCOTTISH WIDOWS WORKPLACE PENSION Everyone needs a plan for their retirement. This guide

Tax Exempt Savings Plans With Life Cover Option

Tax Exempt Savings Plans With Life Cover Option Here for everyone Kingston Unity is a Friendly Society. We re totally different to banks, because we re owned by our members. We re run for the benefit of

Tax Exempt Savings Plans With Life Cover Option Here for everyone Kingston Unity is a Friendly Society. We re totally different to banks, because we re owned by our members. We re run for the benefit of

What if you could protect it all?

Zurich International Life What if you could protect it all? The importance of critical illness protection Critical illness Sometimes life takes an unexpected turn, that s why the people you love and the

Zurich International Life What if you could protect it all? The importance of critical illness protection Critical illness Sometimes life takes an unexpected turn, that s why the people you love and the

Stakeholder Pension. The simple way to start a pension plan. Retirement Investments Insurance Health

Stakeholder Pension The simple way to start a pension plan Retirement Investments Insurance Health Introduction Any decision you make about investing for your future retirement needs careful consideration

Stakeholder Pension The simple way to start a pension plan Retirement Investments Insurance Health Introduction Any decision you make about investing for your future retirement needs careful consideration

Key Features of the WorkSave Pension Plan. This is an important document which you should keep in a safe place.

Key Features of the WorkSave Pension Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information you need

Key Features of the WorkSave Pension Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information you need

GUIDE TO OUR MORTGAGE & PROTECTION SERVICES. Affordable and sustainable solutions designed for you

GUIDE TO OUR MORTGAGE & PROTECTION SERVICES Affordable and sustainable solutions designed for you 2 GUIDE TO OUR MORTGAGE & PROTECTION SERVICES Contents Intrinsic shares our values and beliefs about being

GUIDE TO OUR MORTGAGE & PROTECTION SERVICES Affordable and sustainable solutions designed for you 2 GUIDE TO OUR MORTGAGE & PROTECTION SERVICES Contents Intrinsic shares our values and beliefs about being

Care home fees and your property

Care home fees and your property This factsheet explains whether you will need to sell your property to pay care fees if you move into a care home permanently. It outlines alternatives such as deferred

Care home fees and your property This factsheet explains whether you will need to sell your property to pay care fees if you move into a care home permanently. It outlines alternatives such as deferred

Personal Sick Pay. Paying you an income if you can t work because of an accident or illness

Personal Sick Pay Paying you an income if you can t work because of an accident or illness Personal Sick Pay How it works when you can t Personal Sick Pay is a type of income protection insurance which

Personal Sick Pay Paying you an income if you can t work because of an accident or illness Personal Sick Pay How it works when you can t Personal Sick Pay is a type of income protection insurance which

For financial broker use only. Group Income Protection. Protecting what matters. Retirement Investment Insurance

For financial broker use only. Group Income Protection Protecting what matters Retirement Investment Insurance Contents Protecting the things that matter 2 Why Group Income Protection from Aviva is great

For financial broker use only. Group Income Protection Protecting what matters Retirement Investment Insurance Contents Protecting the things that matter 2 Why Group Income Protection from Aviva is great

Protection Relevant Life PLAN DETAILS FOR RELEVANT LIFE PLAN

Protection Relevant Life PLAN DETAILS FOR RELEVANT LIFE PLAN June 2018 WE GIVE THIS BOOKLET TO EVERYONE WHO BUYS A RELEVANT LIFE PLAN. IT CONTAINS THE PLAN S TERMS AND CONDITIONS, AND IT TELLS YOU HOW

Protection Relevant Life PLAN DETAILS FOR RELEVANT LIFE PLAN June 2018 WE GIVE THIS BOOKLET TO EVERYONE WHO BUYS A RELEVANT LIFE PLAN. IT CONTAINS THE PLAN S TERMS AND CONDITIONS, AND IT TELLS YOU HOW

Key features of the Zurich Life Protection policy

Key features of the Zurich Life Protection policy Contents Helping you decide This important document gives you a summary of the Zurich Life Protection policy. For more details on how this policy works,

Key features of the Zurich Life Protection policy Contents Helping you decide This important document gives you a summary of the Zurich Life Protection policy. For more details on how this policy works,

RETIREMENT REPORT ADEQUATE SAVINGS INDEX

RETIREMENT REPORT 2017 ADEQUATE SAVINGS INDEX Since 2005, the annual Scottish Widows Retirement Report Adequate Savings Index has provided a barometer of retirement savings levels across the UK. Over the

RETIREMENT REPORT 2017 ADEQUATE SAVINGS INDEX Since 2005, the annual Scottish Widows Retirement Report Adequate Savings Index has provided a barometer of retirement savings levels across the UK. Over the

Standard Life Active Retirement For accessing your pension savings

Standard Life Active Retirement For accessing your pension savings Standard Life Active Retirement our ready-made investment solution that allows you to access your pension savings while still giving your

Standard Life Active Retirement For accessing your pension savings Standard Life Active Retirement our ready-made investment solution that allows you to access your pension savings while still giving your

Key Features of the WorkSave Pension Plan. This is an important document which you should keep in a safe place.

Key Features of the WorkSave Pension Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains the important information you need to know

Key Features of the WorkSave Pension Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains the important information you need to know

Financial protection for you and your family

KEY GUIDE Financial protection for you and your family KEY GUIDE January 2019 Financial protection for you and your family 2 Introduction PROTECTING WHAT MATTERS MOST Most people s finances are like a

KEY GUIDE Financial protection for you and your family KEY GUIDE January 2019 Financial protection for you and your family 2 Introduction PROTECTING WHAT MATTERS MOST Most people s finances are like a

Week 3 Supplemental: The Odds......Never tell me them. Stat 305 Notes. Week 3 Supplemental Page 1 / 23

Week 3 Supplemental: The Odds......Never tell me them Stat 305 Notes. Week 3 Supplemental Page 1 / 23 Odds Odds are a lot like probability, but are calculated differently. Probability of event = Times

Week 3 Supplemental: The Odds......Never tell me them Stat 305 Notes. Week 3 Supplemental Page 1 / 23 Odds Odds are a lot like probability, but are calculated differently. Probability of event = Times

PROTECTION FOR LIFE POLICY PROVISIONS. Life Cover PFL LC (2016)

") PROTECTION FOR LIFE POLICY PROVISIONS Life Cover PFL LC (2016) INTRODUCTION THIS BOOKLET PROVIDES DETAILS FOR A LIFE COVER POLICY. EACH SCHEDULE ISSUED BY SCOTTISH WIDOWS LIMITED ( SCOTTISH WIDOWS ) AND

PROTECTION FOR LIFE POLICY PROVISIONS Life Cover PFL LC (2016) INTRODUCTION THIS BOOKLET PROVIDES DETAILS FOR A LIFE COVER POLICY. EACH SCHEDULE ISSUED BY SCOTTISH WIDOWS LIMITED ( SCOTTISH WIDOWS ) AND

INCOME INSURANCE - COMPANY

PENSIONS INVESTMENTS LIFE INSURANCE INCOME INSURANCE - COMPANY PROTECT YOUR EMPLOYEES EARNINGS ABOUT US Established in Ireland in 1939, Irish Life is now part of the Great-West Lifeco group of companies,

PENSIONS INVESTMENTS LIFE INSURANCE INCOME INSURANCE - COMPANY PROTECT YOUR EMPLOYEES EARNINGS ABOUT US Established in Ireland in 1939, Irish Life is now part of the Great-West Lifeco group of companies,

Flexible Income Annuity

Flexible Income Annuity Key Features This is an important document and you should read it before deciding whether to buy your pension annuity from us Purpose of this document This Key Features booklet

Flexible Income Annuity Key Features This is an important document and you should read it before deciding whether to buy your pension annuity from us Purpose of this document This Key Features booklet

Key Features of the Group Personal Pension 2000 Plan. This is an important document which you should keep in a safe place.

Key Features of the Group Personal Pension 2000 Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

Key Features of the Group Personal Pension 2000 Plan This is an important document which you should keep in a safe place. Welcome to your Key Features Document. It explains all the important information

Can knowledge of Protection Claims support Financial Advice?

PENSIONS INVESTMENTS LIFE INSURANCE Can knowledge of Protection Claims support Financial Advice? Martin Duffy ACII, DLDU & DLDC (AMS) Chartered Insurer Head of Underwriting & Protection Claims Webinar,

PENSIONS INVESTMENTS LIFE INSURANCE Can knowledge of Protection Claims support Financial Advice? Martin Duffy ACII, DLDU & DLDC (AMS) Chartered Insurer Head of Underwriting & Protection Claims Webinar,

If you think there s little point in having Income Protection if it doesn t pay out...

CLAIMS BROCHURE Real stories from 10 years of claims If you think there s little point in having Income Protection if it doesn t pay out......the feeling s mutual Angela, aged 52 Aviation Services Manpower

CLAIMS BROCHURE Real stories from 10 years of claims If you think there s little point in having Income Protection if it doesn t pay out......the feeling s mutual Angela, aged 52 Aviation Services Manpower

Welcome Insurer Life Insurance Critical Illness budgetinsurance.com

Your Policy Summary Welcome We ve sent you this as a brief guide to our products and because the Insurer is required to do so by the Financial Conduct Authority. This important information will help you

Your Policy Summary Welcome We ve sent you this as a brief guide to our products and because the Insurer is required to do so by the Financial Conduct Authority. This important information will help you

KEY FEATURES OF THE SCOTTISH WIDOWS ENHANCED ANNUITY. Important information you need to read

KEY FEATURES OF THE SCOTTISH WIDOWS ENHANCED ANNUITY Important information you need to read THE FINANCIAL CONDUCT AUTHORITY (FCA) IS A FINANCIAL SERVICES REGULATOR. IT REQUIRES US, SCOTTISH WIDOWS, TO

KEY FEATURES OF THE SCOTTISH WIDOWS ENHANCED ANNUITY Important information you need to read THE FINANCIAL CONDUCT AUTHORITY (FCA) IS A FINANCIAL SERVICES REGULATOR. IT REQUIRES US, SCOTTISH WIDOWS, TO

KEY FEATURES OF CRITICAL ILLNESS COVER PROTECTION FOR LIFE. Important information you need to read

KEY FEATURES OF CRITICAL ILLNESS COVER PROTECTION FOR LIFE Important information you need to read THE FINANCIAL CONDUCT AUTHORITY IS A FINANCIAL SERVICES REGULATOR. IT REQUIRES US, SCOTTISH WIDOWS, TO

KEY FEATURES OF CRITICAL ILLNESS COVER PROTECTION FOR LIFE Important information you need to read THE FINANCIAL CONDUCT AUTHORITY IS A FINANCIAL SERVICES REGULATOR. IT REQUIRES US, SCOTTISH WIDOWS, TO

KEY FEATURES OF THE SELF-INVESTED PERSONAL PENSION (SIPP) FOR INCOME DRAWDOWN OR PHASED RETIREMENT. Important information you need to read

FOR INCOME DRAWDOWN OR PHASED RETIREMENT. Important information you need to read") KEY FEATURES OF THE SELF-INVESTED PERSONAL PENSION (SIPP) FOR INCOME DRAWDOWN OR PHASED RETIREMENT Important information you need to read THE FINANCIAL CONDUCT AUTHORITY IS A FINANCIAL SERVICES REGULATOR.

KEY FEATURES OF THE SELF-INVESTED PERSONAL PENSION (SIPP) FOR INCOME DRAWDOWN OR PHASED RETIREMENT Important information you need to read THE FINANCIAL CONDUCT AUTHORITY IS A FINANCIAL SERVICES REGULATOR.

Mortgage advice you can depend on

Mortgage advice you can depend on Whether buying your first home, buying to let, or remortgaging it s a big commitment. This guide aims to help you understand what you need to think about making you feel

Mortgage advice you can depend on Whether buying your first home, buying to let, or remortgaging it s a big commitment. This guide aims to help you understand what you need to think about making you feel

Special Report HOW TO AVOID OVERPAYING FOR YOUR MORTGAGE LIFE INSURANCE AND MORTGAGE CRITICAL ILLNESS INSURANCE HARVEST MOON LIFE INSURANCE

Special Report HARVEST MOON LIFE INSURANCE HOW TO AVOID OVERPAYING FOR YOUR MORTGAGE LIFE INSURANCE AND MORTGAGE CRITICAL ILLNESS INSURANCE www.hmli.ca By: Terry Bialek Congratulations! You ve just bought

Special Report HARVEST MOON LIFE INSURANCE HOW TO AVOID OVERPAYING FOR YOUR MORTGAGE LIFE INSURANCE AND MORTGAGE CRITICAL ILLNESS INSURANCE www.hmli.ca By: Terry Bialek Congratulations! You ve just bought

Increase Your Agency s. Life, Annuities, Long Term Care, and Disability Income Sales

Increase Your Agency s Life, Annuities, Long Term Care, and Disability Income Sales Table of Contents Introduction... 01 Business Development... 09 My Personal Approach... 13 Concepts I Share With Clients...

Increase Your Agency s Life, Annuities, Long Term Care, and Disability Income Sales Table of Contents Introduction... 01 Business Development... 09 My Personal Approach... 13 Concepts I Share With Clients...

Workplace pensions Frequently asked questions. This leaflet answers some of the questions you may have about workplace pensions

Workplace pensions Frequently asked questions This leaflet answers some of the questions you may have about workplace pensions July 2013 Page 1 of 16 About workplace pensions Q1. Is everyone being enrolled

Workplace pensions Frequently asked questions This leaflet answers some of the questions you may have about workplace pensions July 2013 Page 1 of 16 About workplace pensions Q1. Is everyone being enrolled

Pension Life Cover. For what s important to you

For what s important to you Contents Protection Cover from Aviva 1 Pension Life Cover 3 Personal Pension Protection Plan 4 Executive Pension Protection Plan 5 Pension life cover - Premiums 6 Pension life

For what s important to you Contents Protection Cover from Aviva 1 Pension Life Cover 3 Personal Pension Protection Plan 4 Executive Pension Protection Plan 5 Pension life cover - Premiums 6 Pension life

Guide to trusts. A brief guide to Trusts and our Trustbuilder tool. Trusts the basics. Settlor makes a gift to the trust

Guide to trusts A brief guide to Trusts and our Trustbuilder tool This brief guide explains some of the main features and benefits of our trusts, and gives you some information to help you decide whether

Guide to trusts A brief guide to Trusts and our Trustbuilder tool This brief guide explains some of the main features and benefits of our trusts, and gives you some information to help you decide whether

COMBINE YOUR PENSIONS

COMBINE YOUR PENSIONS PAGE 1 INTRODUCTION PAGE 2 WHY COMBINE MY PENSIONS WITH SCOTTISH WIDOWS? PAGE 3 ARE THERE ANY PENSIONS THAT CAN T BE COMBINED? PAGE 4 THINGS TO CONSIDER PAGE 8 USE ILLUSTRATIONS PAGE

COMBINE YOUR PENSIONS PAGE 1 INTRODUCTION PAGE 2 WHY COMBINE MY PENSIONS WITH SCOTTISH WIDOWS? PAGE 3 ARE THERE ANY PENSIONS THAT CAN T BE COMBINED? PAGE 4 THINGS TO CONSIDER PAGE 8 USE ILLUSTRATIONS PAGE

THE ARMED FORCES STAKEHOLDER PENSION SCHEME A GUIDE TO HELP YOU PREPARE FOR THE RETIREMENT YOU WANT

THE ARMED FORCES STAKEHOLDER PENSION SCHEME A GUIDE TO HELP YOU PREPARE FOR THE RETIREMENT YOU WANT The Official Armed Forces pension scheme is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS

THE ARMED FORCES STAKEHOLDER PENSION SCHEME A GUIDE TO HELP YOU PREPARE FOR THE RETIREMENT YOU WANT The Official Armed Forces pension scheme is provided by Scottish Widows. SUPPORTING LITERATURE AND TOOLS

Your Guide to Life Insurance When You re 50 or Older

Your Guide to Life Insurance When You re 50 or Older (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance When You re 50 or Older Contents I Have Insurance Through My Employer. Why Buy Now? 4

Your Guide to Life Insurance When You re 50 or Older (800) 827-9990 HealthMarkets.com Your Guide to Life Insurance When You re 50 or Older Contents I Have Insurance Through My Employer. Why Buy Now? 4

LIFESTYLE CARE COVER

LIFESTYLE CARE COVER Lifelong cover that pays out when you die, or earlier if you can t look after yourself. THE LONGER YOU LIVE, THE MORE LIKELY YOU ARE TO NEED HELP LOOKING AFTER YOURSELF * THE COSTS

LIFESTYLE CARE COVER Lifelong cover that pays out when you die, or earlier if you can t look after yourself. THE LONGER YOU LIVE, THE MORE LIKELY YOU ARE TO NEED HELP LOOKING AFTER YOURSELF * THE COSTS