Tax and Financial Planning Aspects of Hurricane Harvey

|

|

|

- Bruce Simmons

- 5 years ago

- Views:

Transcription

1 Schreiber & Schreiber Certified Public Accountants Tax and Financial Planning Aspects of Hurricane Harvey Houston Financial Planners November 14, Gerard H. Schreiber, Jr., CPA 1 Jerry Schreiber Partner with Schreiber & Schreiber Author, Documenting a Casualty Loss, Journal of Accountancy, November Casualty+Loss.htm Presentations include Hurricanes Katrina, Rita, Wilma, Gustav, Ike, Isaac, Irene, Sandy, Matthew, Harvey, and Irma, 2010 Nashville TN flooding, 2012 Colorado Springs Fires, 2014 Oklahoma Tornadoes, South Carolina 2015 Flooding, Spring 2016 Louisiana Flooding, August 2016 Louisiana Flooding, Member, AICPA IRS Advocacy and Relations Committee Author, "An Overview of AICPA and IRS Rules of Practice, The Tax Adviser, February 2014 Author, Tax Practice Quality Control, The Tax Adviser, November 2012 Author, "Circular 230 Best Practices, The Tax Adviser, April 2010 Author, Strengthening Tax Services' Foundation, Journal of Accountancy, May 2009 Contact at: ghschreiber@bellsouth.net Phone

2 Today s Topics Financial Planning Considerations General Overview and Resources IRS Filing Dates Casualty Losses Disaster Relief and FAA Act of Schreiber & Schreiber Certified Public Accountants Financial Planning Considerations 4 2

3 The Whole Team Has To Be Involved Legal Charitable Accounting and Tax Investments Insurance 5 Planning Considerations Financial Plan Budgetary Home owner s insurance Personal umbrellas Flood insurance Supplemental flood Deductibles Co insurance Self insuring (budgetary) Contents including jewelry and art objects Mortgage debt 6 3

4 Schreiber & Schreiber Certified Public Accountants General Overview and Resources 7 8 4

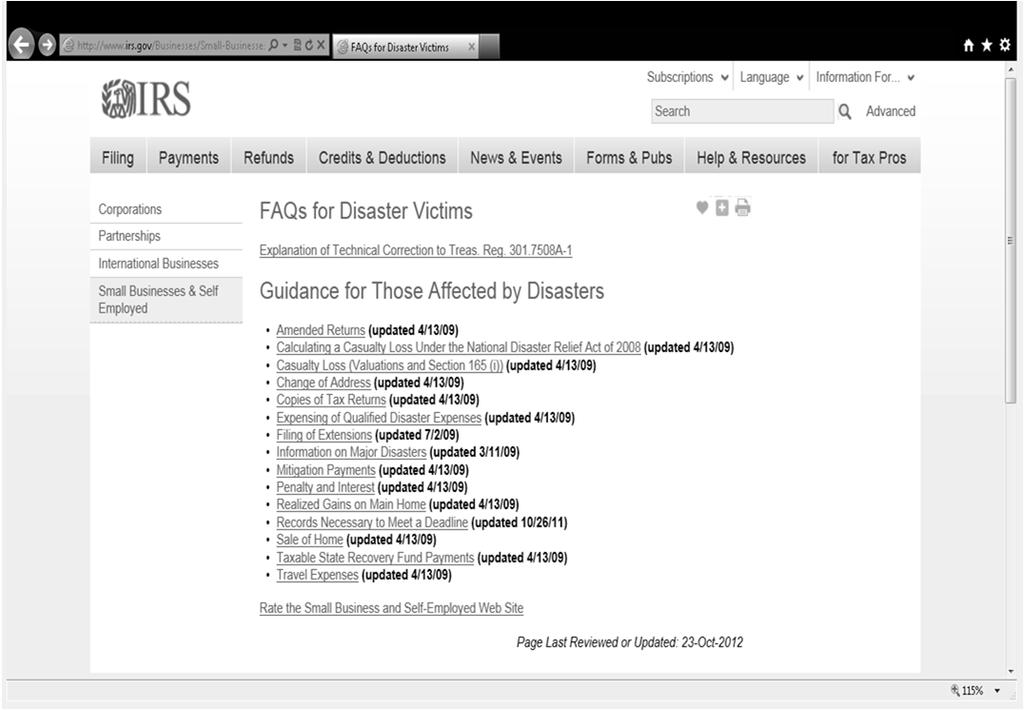

5 The Most Important Thing About A Disaster: Your Comfort Zone Disappears 9 Resources IRS FAQ s Disaster Victims Disaster-Victims CPA Disaster Yahoo Group Local Network Groups DisasterAssistance.gov FEMA Social Media Insurance Company List United Policyholders

6

7

8

9 Here is a list of claim contact numbers: A AAA Insurance (Auto Club Family Insurance Company) ext Acadia Insurance Company , ext ACE Private Risk Services ACE USA Clients receive individual 800 numbers or call (ACE USA/ACE Recreational Marine claims); (Disaster Mortgage Protection claims) Acuity AGCS Marine Alabama Department of Insurance Alabama Municipal Insurance Corporation AMIC Alfa Insurance Group Allmerica Allstate STORM ( ) Allstate Floridian Insurance Company STORM ( ) America First Insurance America s Health Insurance Plans (AHIP) American Bankers Insurance Company American Federation Insurance Company American General Property Insurance Company of Florida American International Group, Inc. (AIG) American National Property & Casualty Company & Affiliates American Reliable Insurance Company American Security Insurance Company American Skyline Insurance Company American States Insurance Company American Strategic Insurance 866-ASI-LOSS ( ) American Superior Insurance Arch Insurance

10

11 Claims Diary/Workbook 22 FEMA Individual v. Public Assistance 23 11

12 Individual Assistance The Individuals and Households Program (IHP) can assist those affected by the recent storms by providing financial assistance for housing or other needs. The program is available to all people who qualify regardless of race, sex, religion, color or national origin. FEMA s IHP is available to both homeowners and renters. The IHP has two provisions; Housing Assistance and Other Needs Assistance. Housing Assistance can provide funding for: Referrals for rental housing Financial assistance to rent a different place to live Repairs to make the home safe, sanitary and functional Replacement - financial assistance to replace destroyed homes Other Needs Assistance may include funding for: Medical, dental and funeral expenses Essential personal property such as furniture, clothing and some appliances Repair or replacement of damaged vehicles Other disaster-related expenses 24 Individual Assistance(Continued)- Individual assistance can also be in the form of federal low-interest disaster loans from the U.S. Small Business Administration (SBA) for homeowners, renters, businesses of all sizes, and private non-profit organizations. Homeowners may borrow up to $200,000 to repair or replace their primary residence. Renters and homeowners may borrow up to $40,000 to replace personal property. Up to $2 million may be borrowed by businesses for any combination of property damage or economic injury. The SBA also offers working capital loans to small businesses and most private, non-profit organizations of all sizes having difficulty meeting obligations as a result of the disaster. For information on SBA disaster loans, call (800) or visit Hearing- or speech-impared individuals may call (800)

13 Public Assistance Under the Public Assistance Grant Program, FEMA awards grants to assist state and local governments and certain private nonprofit organizations with the response to and recovery from disasters. The program provides funding for debris removal, implementation of emergency protective measures and permanent restoration of infrastructure. The program also encourages protection from future damage by providing assistance for hazard mitigation measures during the recovery process. The program runs on a cost share with FEMA and the applicant who may be the state or local governments. Public assistance is based on a partnership between FEMA, state and local officials. FEMA is responsible for managing the program, approving grants and providing technical Qualified Disaster Payments Section 139 Payments Revenue Ruling 131, IRB ,7 Revenue Ruling

14 REV. RUL , I.R.B. 283 (1/21/2003) CERTAIN DISASTER RELIEF PAYMENTS ARE TAX-FREE WASHINGTON The Internal Revenue Service today issued guidance holding that individuals who are disaster victims will generally not have to pay taxes on assistance payments they receive. Taxpayers in a Presidentially declared disaster area who receive grants from state programs, charitable organizations or employers to cover medical, transportation, or temporary housing expenses do not include these grants in their income. The Victims of Terrorism Tax Relief Act of 2001 added Section 139 to the Internal Revenue Code, excluding from income qualified disaster relief payments to individuals. Today's ruling explains how that and other tax law sections apply in hypothetical disaster situations. 28 Qualified Disaster Payments A qualified disaster relief payment includes an amount (to the extent not compensated by insurance or otherwise) paid to or for the benefit of an individual: To reimburse or pay reasonable and necessary personal, family, living, or funeral expenses incurred as a result of a qualified disaster (which includes a federal disaster), To reimburse or pay reasonable and necessary expenses incurred to repair or rehabilitate a personal residence (including a rented residence) or repair or replace its contents to the extent that the need for the work results from a qualified disaster, and If the amount is paid by a federal, state, or local government, or an agency or instrumentality of those governments, in connection with a qualified disaster in order to promote the general welfare (but not if payments are made to businesses or for income replacement or unemployment compensation)

15 IRS Filing Issues and Dates

16 The postponement of time to file and pay does not apply to information returns in the W-2, 1098, 1099 series, or to Forms 1042-S or Penalties for failure to timely file information returns can be waived under existing procedures for reasonable cause. Likewise, the postponement does not apply to employment and excise tax deposits. The IRS, however, will abate penalties for failure to make timely employment and excise tax deposits due on or after August 23, 2017, and before September 8, 2017, will be abated as long as the tax deposits were made by September 7, Schreiber & Schreiber Certified Public Accountants Tax Return Filings 33 16

17 Code Section 7508A Section 7508A provides the Secretary of Treasury with authority to postpone the time for performing certain acts under the internal revenue laws for a taxpayer affected by a federally declared disaster as defined in section 165(h)(3)(C)(i), or A terrorist or military action.. The Secretary may specify a period of up to one year may be disregarded in determining,., in respect of any tax liability of such taxpayer whether the performance of acts were performed within the time prescribed without regard to extension. Special rules regarding pensions 34 Taxpayer Acts Eligible for Relief Filing of returns Payment of tax Contributions to retirement plan Filing of a Tax Court Petition Filing of a claim for refund Bringing a lawsuit upon a claim for credit/refund of tax All eligible acts listed in Rev. Proc ( _IRB/ar13.html) 35 17

18

19 Affected Taxpayers Any individual, any business entity or sole proprietor: whose principal residence or principal place of business, is located in the covered disaster area who is a relief worker affiliated with a recognized government or philanthropic organization and who is assisting in the covered disaster area whose principal residence or principal place of business, is not located in the covered disaster area, but whose records necessary to meet a filing or paying deadline are maintained in the covered disaster area 38 Affected Taxpayers (cont d) Any estate or trust that has tax records necessary to meet a filing or paying deadline in a covered disaster area The spouse of an affected taxpayer, solely with regard to a joint return of the husband and wife Any individual visiting the covered disaster area who was killed or injured as a result of the disaster Any other person determined by the IRS to be affected by a federally declared disaster 39 19

20 Government Acts Eligible for Relief Assessing tax Giving or making any notice or demand for payment of tax, or to any liability to the US in respect of any tax Collecting, by levy or otherwise, of any liability Bringing suit Allowing a credit or refund Any other acts specified in a revenue ruling, revenue procedure, notice, or other guidance 40 What May Be Postponed Under Code Sec. 7508A, IRS gives affected taxpayers until the extended date (specified by county, below) to file most tax returns (including individual, estate, trust, partnership, C corporation, and S corporation income tax returns; estate, gift, and generation-skipping transfer tax returns; and employment and certain excise tax returns), or to make tax payments, including estimated tax payments, that have either an original or extended due date falling on or after the onset date of the disaster (specified by county, below), and on or before the extended date. IRS also gives affected taxpayers until the extended date to perform other time-sensitive actions described in Reg A-1(c)(1) and Rev Proc , IRB 388, that are due to be performed on or after the onset date of the disaster, and on or before the extended date. This relief also includes the filing of Form 5500 series returns, in the way described in Rev Proc , Sec. 8. Additionally, the relief described in Rev Proc , Sec. 17, relating to like-kind exchanges of property, also applies to certain taxpayers who are not otherwise affected taxpayers and may include acts required to be performed before or after the period above

21 Key Terms of A-1 Federally declared disaster area Relief from interest, penalties, additional amounts, or additions to tax during postponement period Acts eligible for relief Affected taxpayers Definition of an Affected Taxpayer A taxpayer does not have to be located in a federally declared disaster area to be an affected taxpayer. Taxpayers are affected if records necessary to meet a filing or payment deadline postponed during the relief period are located in a covered disaster area. An affected taxpayer can be: An individual Any business entity or sole proprietor Any shareholder in an S Corporation Q: Does disaster relief apply to me if my tax preparer is in a disaster area but I m not? Disaster relief applies to tax preparers who are unable to file returns or make payments on behalf of the client because of the disaster. Therefore, if you are a taxpayer outside of the disaster area, you may qualify for relief if: your preparer is in the disaster area, and the preparer is unable to file or pay on your behalf. To get the postponement for filing or payment, you must: Call the Disaster Assistance Hotline at Explain that your necessary records are located in a covered disaster area Provide the FEMA Disaster Number of the county where your tax preparer is located 43 21

22 (10/11) Q: I own an interest in a partnership, or I am a shareholder in an S Corporation that is located in a federally declared disaster area. However, I do not live in the disaster area myself. I rely on information (Schedule K-1) from the partnership or S Corp to file my tax return. Do I qualify as an affected taxpayer for purposes of receiving filing and payment relief? Yes. If the affected partnership or S Corp cannot provide you the records necessary to file your return then you re also an affected taxpayer. Your filing and payment deadlines are postponed until the end of the postponement period just like the affected partnership or S Corp. To get the postponement for filing or payment, you must: Call the Disaster Assistance Hotline at Explain that your necessary records are located in a covered disaster area Provide the FEMA Disaster Number of the county where the affected partnership or S Corp is located See Treas. Reg A-1 and Rev. Proc for a list of taxpayer acts that may be postponed in response to a federally declared disaster 44 From IRS: The IRS automatically identifies taxpayers located in the covered disaster area and applies automatic filing and payment relief. But affected taxpayers who reside or have a business located outside the covered disaster area must call the IRS disaster hotline at to request this tax relief

23 7508A Information on Filing Returns The later of the extended due date or the end of the postponement period (Example-October 15 th (extended due date) or January 31st(end of postponement period) A Information on Payments Example 6. (i) A is an unmarried, calendar year taxpayer whose principal residence is located in County W in State Q. A intends to file a Form 1040 for the 2008 taxable year. The return is due on April 15, A timely files Form 4868, "Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. Due to A's timely filing of Form 4868, the extended filing deadline for A's 2008 tax return is October 15, Because A timely requested an extension of time to file, A will not be subject to the failure to file penalty under section 6651(a)(1), if A files the 2008 Form 1040 on or before October 15, However, A failed to pay the tax due on the return by April 15, 2009, and did not receive an extension of time to pay under section Absent reasonable cause, A is subject to the failure to pay penalty under section 6651(a)(2) and accrual of interest

24 Schreiber & Schreiber Certified Public Accountants Casualty Losses 48 Schreiber & Schreiber Certified Public Accountants Casualty Losses 49 24

![Casualty Casualty = the damage, destruction, or loss of property resulting from an identifiable event that is sudden, unexpected, or unusual, Such as an accident, a mishap, [or] some sudden invasion](/docs-images/93/112764614/images/25-1.jpg "by a hostile agency.")

25 Casualty Casualty = the damage, destruction, or loss of property resulting from an identifiable event that is sudden, unexpected, or unusual, Such as an accident, a mishap, [or] some sudden invasion by a hostile agency. For example, property that is lost or misplaced does not give rise to a casualty loss unless it results from an event that is: (1) identifiable; (2) damaging to property; and (3) sudden, unexpected, or unusual in nature. 50 Schreiber & Schreiber Certified Public Accountants Basis, Basis, Basis 51 25

26 Start with the Adjuster s Report 52 Start with the Adjuster s Report 53 26

27 Personal Casualty Losses Loss is smaller of adjusted basis in property or decrease in FMV of property as a result of casualty Loss must be reduced by insurance and other proceeds (including FEMA payments) which may convert the loss into a gain in some instances Example would be insurance paying replacement cost instead of depreciated value of FMV 54 General Rules IRC Code Section 165(a): There shall be allowed as a deduction any loss sustained during the taxable year and not compensated for by insurance or otherwise. IRS Regulation Section (b). The loss is the lesser of The decrease in FMV (before and after) The adjusted basis General rule-unless a total loss of business use property, then basis salvage value insurance 55 27

28 Insurance Recovery (Reimbursement) Loss must be reduced by the amount of insurance taxpayer expects to receive. Insurance claim must be filed for loss of personal use property (except for the deductible) Property insurance can result in a gain. Effect of recovery for an amount other than expected is taken in the year of the recovery 56 Amount of Loss IRS Regulation (a)(2). Change in Fair Market Value is determined by competent appraisal that recognizes the effects of any general market decline which may occur simultaneously with the casualty, in order to limit the deduction to the actual loss resulting from damage to the property

29 Definitions IRS Regulation (a)(2)(i) indicates an independent appraisal by a qualified appraiser is mandatory in most situations Regulation (b)(1)(i) indicates the decrease in FMV is the difference between the property s value immediately before and immediately after the casualty 58 What is Immediately Before and Immediately After? FAQs for Disaster Victims - Casualty Loss (Valuations and Sections 165 (i) 8,00.html 59 29

30 60 Schreiber & Schreiber Certified Public Accountants Tax Section 30

31

32 Cost of Repairs as Evidence of Loss If, repairs are necessary to restore the property to its condition immediately before the casualty, the amount spent is not excessive, the repairs do not care for more than the damage suffered, and the value of the property after the repairs does not as a result of the repairs exceed the value of the property immediately before the casualty

33 66 Business Losses Limited to Basis for total destruction Partial losses are calculated in the same manner as they are for personal casualties The loss is the decline in the value of the property, limited to the adjusted basis as reduced by salvage value, insurance and other recoveries

Elections")

34 Issues for Business Property Can have gain from insurance Gain may be deferred Depreciation recapture Section 179 recapture Code Section 1033 provisions 68 Schreiber & Schreiber Certified Public Accountants Section 165(i) Elections 69 34

35 Schreiber & Schreiber Certified Public Accountants Involuntary Conversions 70 Involuntary Conversions Federally declared disaster areas: The period in which a taxpayer may replace involuntarily converted property is two years. Four years in the case of personal residence Code Section 1033(h)(1)(B)

36 Schreiber & Schreiber Certified Public Accountants 121 Exclusion 72 Schreiber & Schreiber Certified Public Accountants Personal Property 73 36

37

38 Practice Tips Get a copy of insurance adjuster s report Clients are unable to reconstruct basis Do you take into consideration a factor for forgotten/not listed items? 76 Schreiber & Schreiber Certified Public Accountants Disaster Relief and FAA Act of

39 HR hr3823enr.pdf SEC DEFINITIONS. (a) HURRICANE HARVEY DISASTER ZONE AND DISASTER AREA. For purposes of this title (1) HURRICANE HARVEY DISASTER ZONE. The term Hurricane Harvey disaster zone means that portion of the Hurricane Harvey disaster area determined by the President to warrant individual or individual and public assistance from the Federal Government under the Robert T. Stafford Disaster Relief and Emergency Assistance Act by reason of Hurricane Harvey. (2) HURRICANE HARVEY DISASTER AREA. The term Hurricane Harvey disaster area means an area with respect to which a major disaster has been declared by the President before September 21, 2017, under section 401 of such Act by reason of Hurricane Harvey. 78 HR hr3823enr.pdf ((A) IN GENERAL. The term qualified individual means any qualified Hurricane Harvey individual, any qualified Hurricane Irma individual, and any qualified Hurricane Maria individual. (B) QUALIFIED HURRICANE HARVEY INDIVIDUAL. The term qualified Hurricane Harvey individual means an individual whose principal place of abode on August 23, 2017, is located in the Hurricane Harvey disaster area and who has sustained an economic loss by reason of Hurricane Harvey

40 Personal Casualty Losses Prior law, casualty losses are taken as an itemized deduction subject to a $100 reduction per loss occurrence. The total annual deduction for all personal casualty and theft losses is further limited to that amount which exceeds 10 percent of the taxpayer's adjusted gross income. The Disaster Relief and FAA Act of 2017 modifies the reduction to $500 per occurrence but eliminates the need to exceed 10 percent of adjusted gross income. In addition, for taxpayers who do not itemize, the standard deduction is increased by the amount of the disaster loss. 80 (b) SPECIAL RULES FOR QUALIFIED DISASTER-RELATED PERSONAL CASUALTY LOSSES. (1) IN GENERAL. If an individual has a net disaster loss for any taxable year (A) the amount determined under section 165(h)(2)(A)(ii) of the Internal Revenue Code of 1986 shall be equal to the sum of (i) such net disaster loss, and (ii) so much of the excess referred to in the matter preceding clause (i) of section 165(h)(2) (A) of such Code (reduced by the amount in clause (i) of this subparagraph) as exceeds 10 percent of the adjusted gross income of the individual, (B) section 165(h)(1) of such Code shall be applied by substituting $500 for $500 ($100 for taxable years beginning after December 31, 2009), (C) the standard deduction determined under section 63(c) of such Code shall be increased by the net disaster loss, and (D) section 56(b)(1)(E) of such Code shall not apply to so much of the standard deduction as is attributable to the increase under subparagraph (C) of this paragraph

41 2) NET DISASTER LOSS. For purposes of this subsection, the term net disaster loss means the excess of qualified disaster-related personal casualty losses over personal casualty gains (as defined in section 165(h)(3)(A) of the Internal Revenue Code of 1986). (3) QUALIFIED DISASTER-RELATED PERSONAL CASUALTY LOSSES. For purposes of this subsection, the term qualified disaster-related personal casualty losses means losses described in section 165(c)(3) of the Internal Revenue Code of 1986 (A) which arise in the Hurricane Harvey disaster area on or after August 23, 2017, and which are attributable to Hurricane Harvey, (B) which arise in the Hurricane Irma disaster area on or after September 4, 2017, and which are attributable to Hurricane Irma, or (C) which arise in the Hurricane Maria disaster area on or after September 16, 2017, and which are attributable to Hurricane Maria. 82 Retirement Funds Tax favored withdrawals. An exception to the 10-percent early withdrawal penalty applies to qualified distributions from a qualified retirement or annuity plan, or an IRA. The qualified distribution may be included in income ratably over three years, or may be recontributed to an eligible retirement plan within three years. Qualified distributions include distributions made on or after the disaster date, and before January 1, 2019, to an individual whose principal residence is in the disaster area and who has sustained an economic loss by reason of the relevant hurricane. Such distributions are limited to $100,000. Recontributions of withdrawals for home purchases. Individuals who received certain distributions from qualified plans after February 28, 2017, and before September 21, 2017, which was intended to be used to purchase or construct a principal residence in the Hurricane Harvey, Irma or Maria disaster areas but could not do so because of the hurricane may recontribute the amount to the retirement plan. The recontribution of the distribution may be made without tax or penalty if it is recontributed between August 23, 2017 and February 28, Loans from qualified plans to individuals sustaining an economic loss. The Disaster Relief and FAA Act of 2017 provides an exception to the income inclusion rule for loans from a qualified employer plan if the loan is to an individual whose principal residence on the disaster date, is located in the disaster area and who has sustained an economic loss by reason of the hurricanes. The exception only applies to the extent that the loan (when added to the outstanding balance of all other loans to the participant from all plans maintained by the employer) does not exceed $100,

42 Special Rule for Determining Earned Income. Individuals whose principal residence was in a hurricane disaster area and who is displaced as a result may elect to calculate their refundable child tax credit and earned income credit for 2017 by using their earned income from the preceding tax year. 84 Charitable Contributions Charitable contributions. Individuals are allowed to elect to temporarily suspend for all "qualified contributions" the 50-percent contribution base limitation, and the limitation on overall itemized deductions. Qualified contributions means Any cash contribution made beginning on August 23, 2017, and ending on December 31, 2017; for relief effort in the Hurricanes Harvey, Irma, and Maria disaster areas; and for which the taxpayer has obtained contemporaneous written acknowledgement

43 Employee Retention Credit The employee retention credit allows eligible employers in the hurricane disaster areas a 40-percent credit for qualified wages paid to eligible employees. The amount of qualified wages which may be taken into account for any one eligible employee is limited to $6,000. The credit is part of the current year business credit and therefore is subject to tax liability limitations. This credit does not apply to wages paid to employee-owners who own more than fifty percent of the business. 86 An eligible employer is any employer that conducted an active trade or business in a hurricane disaster area which, as a result of damage sustained by reason of the hurricanes, became inoperable on any day from the applicable disaster date, and before January 1, For Hurricane Harvey, the disaster date is August 23, 2017; for Hurricane Irma, the date is September 4, 2017; and for Hurricane Maria the date is September 16, Eligible employees are employees whose principal place of employment on the applicable disaster date was with the eligible employer in a hurricane disaster area

44 Qualified wages are wages paid or incurred by an eligible employer with respect to an eligible employee on any day after the applicable disaster date, and before January 1, 2018, during the period: beginning on the date on which the trade or business first became inoperable at the principal place of employment of the employee immediately before the hurricane and ending on the date on which such trade or business has resumed significant operations at such principal place of employment. Qualified wages include wages paid without regard to whether the employee performs no services, performs services at a different place of employment other than the principal place of employment, or performs services at the principal place of employment before significant operations have resumed. Employers cannot claim a retention credit and a Work Opportunity Credit for the same employee. 88 Questions 89 44

45 Thank You Presented by: Gerard H. Schreiber, Jr

After the Flood: Getting Started with Recovery

Schreiber & Schreiber Certified Public Accountants After the Flood: Getting Started with Recovery University of Louisiana-Lafayette B. I. Moody III College of Business Administration September 16-17, 2016

Schreiber & Schreiber Certified Public Accountants After the Flood: Getting Started with Recovery University of Louisiana-Lafayette B. I. Moody III College of Business Administration September 16-17, 2016

Casualty loss deductions, election to claim for previous year. Casualty loss deductions, limitations eased.

Dear Client: If you suffered a loss as a result of Hurricane Harvey, you may be able to recoup a portion of that loss through several different tax benefits that may be available to you. These include

Dear Client: If you suffered a loss as a result of Hurricane Harvey, you may be able to recoup a portion of that loss through several different tax benefits that may be available to you. These include

HOW THE TAX LAW HELPS VICTIMS OF DISASTERS PART I

page 1 of 7 HOW THE TAX LAW HELPS VICTIMS OF DISASTERS PART I The many victims of Hurricanes Harvey, Irma and Maria, as well as other recent storms, doubtless are now preoccupied with salvaging what they

page 1 of 7 HOW THE TAX LAW HELPS VICTIMS OF DISASTERS PART I The many victims of Hurricanes Harvey, Irma and Maria, as well as other recent storms, doubtless are now preoccupied with salvaging what they

FILING DEADLINES EXTENDED

IRS Depa r t ment s Tax Relief Provisions for Disaster Losses Shirley Dennis-Escoffier Weather-related casualty losses have been on the increase with Hurricanes Harvey, Irma, and Maria recently leaving

IRS Depa r t ment s Tax Relief Provisions for Disaster Losses Shirley Dennis-Escoffier Weather-related casualty losses have been on the increase with Hurricanes Harvey, Irma, and Maria recently leaving

A-1 Postponement of certain tax-related deadlines by reasons of a federally declared disaster or terroristic or military action

301.7508A-1 Postponement of certain tax-related deadlines by reasons of a federally declared disaster or terroristic or military action (a) Scope. This section provides rules by which the Internal Revenue

301.7508A-1 Postponement of certain tax-related deadlines by reasons of a federally declared disaster or terroristic or military action (a) Scope. This section provides rules by which the Internal Revenue

H.R. 1 s Impact on Retirement Plans and Recordkeepers

February 9, 2018 Robert Neis Benefits Tax Counsel Office of the Benefits Tax Counsel Department of the Treasury 1500 Pennsylvania Avenue, NW, Room 3044 Washington, D.C. 20220 Re: H.R. 1 s Impact on Retirement

February 9, 2018 Robert Neis Benefits Tax Counsel Office of the Benefits Tax Counsel Department of the Treasury 1500 Pennsylvania Avenue, NW, Room 3044 Washington, D.C. 20220 Re: H.R. 1 s Impact on Retirement

SENATE FINANCE COMMITTEE REPUBLICAN TAX STAFF SUMMARY OF MIDWESTERN DISASTER TAX RELIEF BILL (S. 3322)

") SENATE FINANCE COMMITTEE REPUBLICAN TAX STAFF SUMMARY OF MIDWESTERN DISASTER TAX RELIEF BILL (S. 3322) A request for a revenue estimate for all of the following proposals has been made to the Joint Committee

SENATE FINANCE COMMITTEE REPUBLICAN TAX STAFF SUMMARY OF MIDWESTERN DISASTER TAX RELIEF BILL (S. 3322) A request for a revenue estimate for all of the following proposals has been made to the Joint Committee

Checkpoint Special Study: Tax Provisions in the 2017 Disaster Tax Relief Bill

Checkpoint Special Study: Tax Provisions in the 2017 Disaster Tax Relief Bill On September 29, President Trump signed into law P.L. 115-63, the Disaster Tax Relief and Airport and Airway Extension Act

Checkpoint Special Study: Tax Provisions in the 2017 Disaster Tax Relief Bill On September 29, President Trump signed into law P.L. 115-63, the Disaster Tax Relief and Airport and Airway Extension Act

T.D DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 Relief for Service in Combat Zone and for Presidentially Declared

T.D. 8911 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 Relief for Service in Combat Zone and for Presidentially Declared Disaster AGENCY: Internal Revenue Service (IRS), Treasury.

T.D. 8911 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 Relief for Service in Combat Zone and for Presidentially Declared Disaster AGENCY: Internal Revenue Service (IRS), Treasury.

TIMELY INFORMATION Agriculture & Natural Resources

AG ECONOMICS SERIES TIMELY INFORMATION Agriculture & Natural Resources THE KATRINA EMERGENCY TAX RELIEF ACT OF 2005 J.L. Novak, Ext. Specialist and Prof., Auburn University, AL October 19,2005 Congressional

AG ECONOMICS SERIES TIMELY INFORMATION Agriculture & Natural Resources THE KATRINA EMERGENCY TAX RELIEF ACT OF 2005 J.L. Novak, Ext. Specialist and Prof., Auburn University, AL October 19,2005 Congressional

Relief for Service in Combat Zone and for Presidentially Declared Disaster Announcement

(IRS), Treasury. ACTION: Notice of proposed rulemaking. SUMMARY: This document contains proposed regulations relating to the postponement of certain tax-related deadlines due either to service in a combat

(IRS), Treasury. ACTION: Notice of proposed rulemaking. SUMMARY: This document contains proposed regulations relating to the postponement of certain tax-related deadlines due either to service in a combat

Three-Year Repayment Period for Qualified Hurricane Distributions

October 27, 2017 DISASTER TAX RELIEF ACT PROVISIONS AFFECTING RETIREMENT PLANS HURRICANES HARVEY, IRMA, AND MARIA QUESTIONS AND SUGGESTIONS FOR GUIDANCE The SPARK Institute is pleased to submit this list

October 27, 2017 DISASTER TAX RELIEF ACT PROVISIONS AFFECTING RETIREMENT PLANS HURRICANES HARVEY, IRMA, AND MARIA QUESTIONS AND SUGGESTIONS FOR GUIDANCE The SPARK Institute is pleased to submit this list

Tax Provisions to Assist with Disaster Recovery

Tax Provisions to Assist with Disaster Recovery Erika K. Lunder Legislative Attorney Carol A. Pettit Legislative Attorney Jennifer Teefy Information Research Specialist November 29, 2012 CRS Report for

Tax Provisions to Assist with Disaster Recovery Erika K. Lunder Legislative Attorney Carol A. Pettit Legislative Attorney Jennifer Teefy Information Research Specialist November 29, 2012 CRS Report for

CRS Report for Congress

Order Code RS22261 September 14, 2005 CRS Report for Congress Received through the CRS Web Hurricane Katrina: The Response by the Internal Revenue Service Summary Erika Lunder Legislative Attorney American

Order Code RS22261 September 14, 2005 CRS Report for Congress Received through the CRS Web Hurricane Katrina: The Response by the Internal Revenue Service Summary Erika Lunder Legislative Attorney American

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans Description Normal Loan Rules CA Wildfires Loans General Disaster Loans What types of loans are available? General purpose loans,

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans Description Normal Loan Rules CA Wildfires Loans General Disaster Loans What types of loans are available? General purpose loans,

Tax Implications for California Wildfire Survivors. ABA Tax Section February 10, 2018

Tax Implications for California Wildfire Survivors ABA Tax Section February 10, 2018 Panelists James Creech Law Offices of James Creech San Francisco, CA Bruce McGovern Professor of Law and Director, Tax

Tax Implications for California Wildfire Survivors ABA Tax Section February 10, 2018 Panelists James Creech Law Offices of James Creech San Francisco, CA Bruce McGovern Professor of Law and Director, Tax

Citizens insurance auto claims number

Citizens insurance auto claims number We partner with the best local, knowledgeable independent agents. Dairyland Insurance Company (see Sentry Insurance) Drive Insurance from Progressive 800-925-2886.

Citizens insurance auto claims number We partner with the best local, knowledgeable independent agents. Dairyland Insurance Company (see Sentry Insurance) Drive Insurance from Progressive 800-925-2886.

UNITED STATES PUBLIC LAWS 109th Congress - First Session Convening January 7, 2005 GULF OPPORTUNITY ZONE ACT OF 2005

UNITED STATES PUBLIC LAWS 109th Congress - First Session Convening January 7, 2005 PL 109-135 (HR 4440) December 21, 2005 GULF OPPORTUNITY ZONE ACT OF 2005 An Act To amend the Internal Revenue Code of

UNITED STATES PUBLIC LAWS 109th Congress - First Session Convening January 7, 2005 PL 109-135 (HR 4440) December 21, 2005 GULF OPPORTUNITY ZONE ACT OF 2005 An Act To amend the Internal Revenue Code of

Hurricanes Florence and Michael: Casualty Loss Deductions

What s News in Tax Analysis that matters from Washington National Tax Hurricanes Florence and Michael: Casualty Loss Deductions October 15, 2018 by Lynn Afeman and James Atkinson, Washington National Tax

What s News in Tax Analysis that matters from Washington National Tax Hurricanes Florence and Michael: Casualty Loss Deductions October 15, 2018 by Lynn Afeman and James Atkinson, Washington National Tax

News. Bipartisan Budget Act of 2018

News Release Date: 2/12/18 Bipartisan Budget Act of 2018 Cross References H.R. 1892 On February 9, 2018, the President signed into law H.R. 1892, the Bipartisan Budget Act of 2018, which extends federal

News Release Date: 2/12/18 Bipartisan Budget Act of 2018 Cross References H.R. 1892 On February 9, 2018, the President signed into law H.R. 1892, the Bipartisan Budget Act of 2018, which extends federal

Public Law H.R Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221

9/5/2008 Housing Assistance Tax Act of 2008 Public Law 110-289 H.R. 3221 Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221 H.R. 3221, the Housing and Economic Recovery Act of

9/5/2008 Housing Assistance Tax Act of 2008 Public Law 110-289 H.R. 3221 Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221 H.R. 3221, the Housing and Economic Recovery Act of

TECHNICAL EXPLANATION OF THE SMALL BUSINESS AND WORK OPPORTUNITY TAX ACT OF 2007 AND PENSION RELATED PROVISIONS CONTAINED IN H.R

TECHNICAL EXPLANATION OF THE SMALL BUSINESS AND WORK OPPORTUNITY TAX ACT OF 2007 AND PENSION RELATED PROVISIONS CONTAINED IN H.R. 2206 AS CONSIDERED BY THE HOUSE OF REPRESENTATIVES ON MAY 24, 2007 Prepared

TECHNICAL EXPLANATION OF THE SMALL BUSINESS AND WORK OPPORTUNITY TAX ACT OF 2007 AND PENSION RELATED PROVISIONS CONTAINED IN H.R. 2206 AS CONSIDERED BY THE HOUSE OF REPRESENTATIVES ON MAY 24, 2007 Prepared

4/16/2018 (c) William P. Streng 1

William P. Streng 1") Chapter 10 p.583 Interest, Taxes & Losses Interest expense is deductible, subject to various limitations. 163(a). What is interest? Rent for the use of money. Why provide a deduction for interest expense?

Chapter 10 p.583 Interest, Taxes & Losses Interest expense is deductible, subject to various limitations. 163(a). What is interest? Rent for the use of money. Why provide a deduction for interest expense?

Schwab RT SQL Recordkeeping Operations Library Katrina Emergency Tax Relief Act of 2005 (KETRA)

") Schwab RT SQL Recordkeeping Operations Library Katrina Emergency Tax Relief Act of 2005 (KETRA) Schwab Retirement Technologies Recordkeeping Operations Library Schwab RT Recordkeeping Operations Library

Schwab RT SQL Recordkeeping Operations Library Katrina Emergency Tax Relief Act of 2005 (KETRA) Schwab Retirement Technologies Recordkeeping Operations Library Schwab RT Recordkeeping Operations Library

Disaster Unemployment Assistance (DUA)

") Julie M. Whittaker Specialist in Income Security Updated October 19, 2018 Congressional Research Service 7-5700 www.crs.gov RS22022 Summary Disaster Unemployment Assistance (DUA) benefits are available

Julie M. Whittaker Specialist in Income Security Updated October 19, 2018 Congressional Research Service 7-5700 www.crs.gov RS22022 Summary Disaster Unemployment Assistance (DUA) benefits are available

Tax Treatment of Employee Hardship and Disaster Relief

Tax Treatment of Employee Hardship and Disaster Relief TAX UPDATE Volume 2017, Issue 6 Lisa B. Petkun petkunl@pepperlaw.com Recent hurricanes and fires have caused employers to focus on how to help employees

Tax Treatment of Employee Hardship and Disaster Relief TAX UPDATE Volume 2017, Issue 6 Lisa B. Petkun petkunl@pepperlaw.com Recent hurricanes and fires have caused employers to focus on how to help employees

2017 Tax Considerations

2017 Tax Considerations Tax Laws Enacted During 2017 Individual Income Tax Provisions Education Trust, Estate & Descendent Income Tax Estate, Gift & Generation-Skipping Transfer Taxes Pension & IRA Provisions

2017 Tax Considerations Tax Laws Enacted During 2017 Individual Income Tax Provisions Education Trust, Estate & Descendent Income Tax Estate, Gift & Generation-Skipping Transfer Taxes Pension & IRA Provisions

York County Hazard Mitigation Plan. 1. Disaster Mitigation Act of 2000

1. Disaster Mitigation Act of 2000 PUBLIC LAW 106 390 OCT. 30, 2000 DISASTER MITIGATION ACT OF 2000 VerDate 11-MAY-2000 04:55 Dec 06, 2000 Jkt 089139 PO 00390 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL390.106

1. Disaster Mitigation Act of 2000 PUBLIC LAW 106 390 OCT. 30, 2000 DISASTER MITIGATION ACT OF 2000 VerDate 11-MAY-2000 04:55 Dec 06, 2000 Jkt 089139 PO 00390 Frm 00001 Fmt 6579 Sfmt 6579 E:\PUBLAW\PUBL390.106

NEW LEGISLATION INDIVIDUAL

NEW LEGISLATION INDIVIDUAL 1 Land Grant University Tax Education Foundation Tax Rates.............................. 2 Inflation Adjustments Based on Chained CPI...................... 4 Increase in and

NEW LEGISLATION INDIVIDUAL 1 Land Grant University Tax Education Foundation Tax Rates.............................. 2 Inflation Adjustments Based on Chained CPI...................... 4 Increase in and

Processing Hardships. Agenda. Has it Become a Hardship Itself?

Processing Hardships Has it Become a Hardship Itself? Agenda Legal & Regulatory Requirements Documentation Requirements Recent Commentary From the IRS 2 1 Legal and Regulatory Requirements Hardship Distributions

Processing Hardships Has it Become a Hardship Itself? Agenda Legal & Regulatory Requirements Documentation Requirements Recent Commentary From the IRS 2 1 Legal and Regulatory Requirements Hardship Distributions

MassMutual s Regulatory Advisory Services Congress Provides Additional Relief for Victims of Hurricanes Harvey, Irma and Maria

MassMutual s Regulatory Advisory Services Congress Provides Additional Relief for Victims of Hurricanes Harvey, Irma and Maria Hurricane Withdrawals, Extended Loan Repayment Periods, and Staggered Taxable

MassMutual s Regulatory Advisory Services Congress Provides Additional Relief for Victims of Hurricanes Harvey, Irma and Maria Hurricane Withdrawals, Extended Loan Repayment Periods, and Staggered Taxable

10/26/2017 (c) William P. Streng 1

William P. Streng 1") Chapter 10 p.583 Interest, Taxes & Losses Interest expense is deductible, subject to various limitations. 163(a). What is interest? Rent for the use of money. Why provide a deduction for interest expense?

Chapter 10 p.583 Interest, Taxes & Losses Interest expense is deductible, subject to various limitations. 163(a). What is interest? Rent for the use of money. Why provide a deduction for interest expense?

Disaster Losses and Related Tax Rules

Utah State University DigitalCommons@USU Rural Tax Education Archived USU Extension Publications 9-2017 Disaster Losses and Related Tax Rules JC Hobbs Oklahoma State University Follow this and additional

Utah State University DigitalCommons@USU Rural Tax Education Archived USU Extension Publications 9-2017 Disaster Losses and Related Tax Rules JC Hobbs Oklahoma State University Follow this and additional

Disaster Unemployment Assistance (DUA)

") Julie M. Whittaker Specialist in Income Security September 5, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov RS22022 Summary

Julie M. Whittaker Specialist in Income Security September 5, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research Service 7-5700 www.crs.gov RS22022 Summary

Disaster Unemployment Assistance (DUA)

") Julie M. Whittaker Specialist in Income Security Alison M. Shelton Analyst in Income Security May 6, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress

Julie M. Whittaker Specialist in Income Security Alison M. Shelton Analyst in Income Security May 6, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress

Why Keep Records? Kinds of Records To Keep

Why Keep Records? There are many reasons to keep records. In addition to tax purposes, you may need to keep records for insurance purposes or for getting a loan. Good records will help you: Identify sources

Why Keep Records? There are many reasons to keep records. In addition to tax purposes, you may need to keep records for insurance purposes or for getting a loan. Good records will help you: Identify sources

Application for Assistance

Atria Cares Application for Assistance PROGRAM GUIDELINES Atria Cares, Inc. is a public, nonprofit 501(c)(3) organization that grants temporary/short-term financial assistance to qualifying employees of

Atria Cares Application for Assistance PROGRAM GUIDELINES Atria Cares, Inc. is a public, nonprofit 501(c)(3) organization that grants temporary/short-term financial assistance to qualifying employees of

DISASTER ASSISTANCE FOR INDIVIDUALS

June, 2008 DISASTER ASSISTANCE FOR INDIVIDUALS When the President declares a disaster and authorizes providing Individual Assistance, FEMA s Individuals and Households Program (IHP) can help homeowners

June, 2008 DISASTER ASSISTANCE FOR INDIVIDUALS When the President declares a disaster and authorizes providing Individual Assistance, FEMA s Individuals and Households Program (IHP) can help homeowners

TABLE OF CONTENTS. General Rules

T41 1/18 10-1 10 Interest and Taxes TABLE OF CONTENTS KEY ISSUE DESCRIPTION PAGE Introduction... 10-1 10A Investment Interest Expense... 10-2 General Rules... 10-2 Reporting Deductible Investment Interest...

T41 1/18 10-1 10 Interest and Taxes TABLE OF CONTENTS KEY ISSUE DESCRIPTION PAGE Introduction... 10-1 10A Investment Interest Expense... 10-2 General Rules... 10-2 Reporting Deductible Investment Interest...

Deteriorating Residential Concrete Foundations. Joseph McCarthy CPA. Call in number: Access code:

Deteriorating Residential Concrete Foundations Call in number: 1.888.331.8226 Access code: 7766268 Joseph McCarthy CPA IRS Senior Stakeholder Liaison 203.415.1015 Casualty loss defined A casualty is damage,

Deteriorating Residential Concrete Foundations Call in number: 1.888.331.8226 Access code: 7766268 Joseph McCarthy CPA IRS Senior Stakeholder Liaison 203.415.1015 Casualty loss defined A casualty is damage,

2017 Year-End Income Tax Planning for Individuals December 2017

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

403(b) Plan Transaction Request Form

Plan Transaction Request Form") 403(b) Plan Transaction Request Form 900 S Capital of TX Hwy, Ste. 350 Austin, TX 78746 403b@tcgservices.com P: 800.943.9179 F: 888.989.9247 Please submit completed form via fax, email or mail Sections

403(b) Plan Transaction Request Form 900 S Capital of TX Hwy, Ste. 350 Austin, TX 78746 403b@tcgservices.com P: 800.943.9179 F: 888.989.9247 Please submit completed form via fax, email or mail Sections

2017 Schedule M1NC, Federal Adjustments

2017 Schedule M1NC, Federal Adjustments *171341* Minnesota has not adopted the federal law changes made after December 16, 2016, that affect federal taxable income for tax year 2017. Your First Name and

2017 Schedule M1NC, Federal Adjustments *171341* Minnesota has not adopted the federal law changes made after December 16, 2016, that affect federal taxable income for tax year 2017. Your First Name and

Selected Regulatory Developments: Governmental Plans. Terry A.M. Mumford Mary Beth Braitman Ice Miller LLP Indianapolis, Indiana

81 ALI-ABA Course of Study Retirement, Deferred Compensation, and Welfare Plans of Tax-Exempt and Governmental Employers September 4-6, 2008 Washington, D.C. Selected Regulatory Developments: Governmental

81 ALI-ABA Course of Study Retirement, Deferred Compensation, and Welfare Plans of Tax-Exempt and Governmental Employers September 4-6, 2008 Washington, D.C. Selected Regulatory Developments: Governmental

Disaster Recovery Grant Programs

Disaster Recovery Grant Programs Member Guidelines March 19, 2018 2018 FEDERAL HOME LOAN BANK OF NEW YORK 101 PARK AVENUE NEW YORK, NY 10178 WWW.FHLBNY.COM TABLE OF CONTENTS INTRODUCTION 3 MEMBER AND NON-PROFIT

Disaster Recovery Grant Programs Member Guidelines March 19, 2018 2018 FEDERAL HOME LOAN BANK OF NEW YORK 101 PARK AVENUE NEW YORK, NY 10178 WWW.FHLBNY.COM TABLE OF CONTENTS INTRODUCTION 3 MEMBER AND NON-PROFIT

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

CRS-2 DUA benefits are available only to those individuals who have become unemployed as a direct result of a declared major disaster. First created i

Order Code RS22022 Updated January 23, 2008 Disaster Unemployment Assistance (DUA) Summary Julie M. Whittaker Specialist in Income Security Domestic Social Policy Division The Disaster Unemployment Assistance

Order Code RS22022 Updated January 23, 2008 Disaster Unemployment Assistance (DUA) Summary Julie M. Whittaker Specialist in Income Security Domestic Social Policy Division The Disaster Unemployment Assistance

Amending IRA Documents

ing IRA Documents Supporting Your IRA Program retirement services college savings consulting compliance academy trust ing IRA Documents Change is inevitable especially in the IRA world. And, in this world,

ing IRA Documents Supporting Your IRA Program retirement services college savings consulting compliance academy trust ing IRA Documents Change is inevitable especially in the IRA world. And, in this world,

KEIR EDUCATIONAL RESOURCES

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

INCOME TAX PLANNING 2015 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com 2015

NEW LEGISLATION ADDITIONAL

NEW LEGISLATION ADDITIONAL 13 Land Grant University Tax Education Foundation New Legislation Additional......... 488 Foreign Tax Matters................. 550 Table of Expiration Dates............ 556 LEARNING

NEW LEGISLATION ADDITIONAL 13 Land Grant University Tax Education Foundation New Legislation Additional......... 488 Foreign Tax Matters................. 550 Table of Expiration Dates............ 556 LEARNING

With Year-End Deadline Looming IRS Issues Much Anticipated Hardship Guidance

With Year-End Deadline Looming IRS Issues Much Anticipated Hardship Guidance PUBLISHED: November 16, 2018 Plan sponsors and recordkeepers have been eagerly anticipating IRS guidance on changes to the hardship

With Year-End Deadline Looming IRS Issues Much Anticipated Hardship Guidance PUBLISHED: November 16, 2018 Plan sponsors and recordkeepers have been eagerly anticipating IRS guidance on changes to the hardship

2017 Loscalzo Institute, a Kaplan Company

September 25, 2017 Section: Circular 230 Change of Heart by Husband Resulted in Conflict of Interest for Representative... 2 Citation: Gebman v. Commissioner, TC Memo 2017-184, 9/18/17... 2 Section: 61

September 25, 2017 Section: Circular 230 Change of Heart by Husband Resulted in Conflict of Interest for Representative... 2 Citation: Gebman v. Commissioner, TC Memo 2017-184, 9/18/17... 2 Section: 61

Part 1 Nan Bobbett Today s Topics Trump s Tax Reform FRAMEWORK Update on Professional Employer Organizations Tax Planning

Part 1 Nan Bobbett Today s Topics Trump s Tax Reform FRAMEWORK Update on Professional Employer Organizations Tax Planning 1 Part 2 Wendy Hill Today s Topics Getting Ready for Tax Filing Season Natural

Part 1 Nan Bobbett Today s Topics Trump s Tax Reform FRAMEWORK Update on Professional Employer Organizations Tax Planning 1 Part 2 Wendy Hill Today s Topics Getting Ready for Tax Filing Season Natural

PACKET 3 Disaster Relief and Follow Up Introduction to Disaster Relief and Follow Up

3A Introduction to Disaster Relief and Follow Up Disaster Relief and Follow Up You have now completed your reassessment work and should have an indication of the appropriate values for damaged properties,

3A Introduction to Disaster Relief and Follow Up Disaster Relief and Follow Up You have now completed your reassessment work and should have an indication of the appropriate values for damaged properties,

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

FEMA Q&A. Q: What s the quickest way to apply for federal assistance? Q: What will I need to apply for federal assistance?

FEMA Q&A FEMA, the Federal Emergency Management Agency, coordinates the federal government s response following the declaration of a major disaster. For up-to-date information, visit www.fema.gov. Q: What

FEMA Q&A FEMA, the Federal Emergency Management Agency, coordinates the federal government s response following the declaration of a major disaster. For up-to-date information, visit www.fema.gov. Q: What

North Carolina Public Employee Deferred Compensation Plan (NC 457 Plan)

") North Carolina Public Employee Deferred Compensation Plan (NC 457 Plan) Revised December 14, 2017 Table of Contents Page Article I The Plan and the Trust... 1 Section 1.1 Establishment of the Plan... 1

North Carolina Public Employee Deferred Compensation Plan (NC 457 Plan) Revised December 14, 2017 Table of Contents Page Article I The Plan and the Trust... 1 Section 1.1 Establishment of the Plan... 1

Chapter 10 p.583 Interest, Taxes & Losses

Chapter 10 p.583 Interest, Taxes & Losses Interest expense is deductible, subject to various limitations. 163(a). Limitation examples: 1) Limit on investment interest - 163(d). 2) Obligations not in registered

Chapter 10 p.583 Interest, Taxes & Losses Interest expense is deductible, subject to various limitations. 163(a). Limitation examples: 1) Limit on investment interest - 163(d). 2) Obligations not in registered

Recent Changes in Tax Laws Affect Qualified Retirement Plans and Health & Welfare Benefits

Recent Changes in Tax Laws Affect Qualified Retirement Plans and Health & Welfare Benefits The Tax Cuts and Jobs Act of 2017 ( Tax Cuts Act ), the Bipartisan Budget Act of 2018 ( Budget Act ), and other

Recent Changes in Tax Laws Affect Qualified Retirement Plans and Health & Welfare Benefits The Tax Cuts and Jobs Act of 2017 ( Tax Cuts Act ), the Bipartisan Budget Act of 2018 ( Budget Act ), and other

STATUTORY RULES FOR TAX-FREE DISASTER RELIEF PAYMENTS

OVERVIEW OF EXISTING LAW, ADMINISTRATIVE RELIEF AND LEGISLATION PERTAINING TO COMPENSATION AND EMPLOYEE BENEFITS PROVIDED FOR PERSONS AFFECTED BY HURRICANES KATRINA, RITA AND WILMA STATUTORY RULES FOR

OVERVIEW OF EXISTING LAW, ADMINISTRATIVE RELIEF AND LEGISLATION PERTAINING TO COMPENSATION AND EMPLOYEE BENEFITS PROVIDED FOR PERSONS AFFECTED BY HURRICANES KATRINA, RITA AND WILMA STATUTORY RULES FOR

Tax Law Update. Agenda 10/17/2017. October 17, 2017

Tax Law Update October 17, 2017 Agenda President s October 12, Directive Disaster Legislation myra Phaseout Qualified Small Employer HRA Form 1098 T Reporting Private Debt Collection Partnership Penalty

Tax Law Update October 17, 2017 Agenda President s October 12, Directive Disaster Legislation myra Phaseout Qualified Small Employer HRA Form 1098 T Reporting Private Debt Collection Partnership Penalty

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

1. a demand loan where interest is payable on the loan at a rate less than the applicable federal rate [IRC Sec. 7872(e)(1)(A)], or

![1. a demand loan where interest is payable on the loan at a rate less than the applicable federal rate [IRC Sec. 7872(e)(1)(A)], or](/thumbs/88/117035883.jpg "1. a demand loan where interest is payable on the loan at a rate less than the applicable federal rate [IRC Sec. 7872(e)(1)(A)], or") 990 2/18 15-9 Example 15B-1 Related party interest. Forney First, Inc. (FFI), an accrual basis organization exempt under IRC Sec. 501(c)(3), provides food and shelter to needy families in Forney. FFI augments

990 2/18 15-9 Example 15B-1 Related party interest. Forney First, Inc. (FFI), an accrual basis organization exempt under IRC Sec. 501(c)(3), provides food and shelter to needy families in Forney. FFI augments

Safe Harbor Explanations Eligible Rollover Distributions. Notice I. PURPOSE

Safe Harbor Explanations Eligible Rollover Distributions Notice 2018-74 I. PURPOSE This notice modifies the two safe harbor explanations in Notice 2014-74, 2014-50 I.R.B. 937, that may be used to satisfy

Safe Harbor Explanations Eligible Rollover Distributions Notice 2018-74 I. PURPOSE This notice modifies the two safe harbor explanations in Notice 2014-74, 2014-50 I.R.B. 937, that may be used to satisfy

Answers to Frequently Asked Questions for Registered Domestic Partners and Individuals in Civil Unions

Answers to Frequently Asked Questions for Registered Domestic Partners and Individuals in Civil Unions The following questions and answers provide information to individuals of the same sex and opposite

Answers to Frequently Asked Questions for Registered Domestic Partners and Individuals in Civil Unions The following questions and answers provide information to individuals of the same sex and opposite

SUPERIOR COURT OF CALIFORNIA COUNTY OF ORANGE SELF-HELP CENTER

SUPERIOR COURT OF CALIFORNIA COUNTY OF ORANGE SELF-HELP CENTER www.occourts.org/self-help DISSOLUTION, LEGAL SEPARATION OR NULLITY OF MARRIAGE STEP 3: DECLARATION OF DISCLOSURE All documents must be typed

SUPERIOR COURT OF CALIFORNIA COUNTY OF ORANGE SELF-HELP CENTER www.occourts.org/self-help DISSOLUTION, LEGAL SEPARATION OR NULLITY OF MARRIAGE STEP 3: DECLARATION OF DISCLOSURE All documents must be typed

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA

Traditional IRA Roth IRA") GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

Hatch modification to Amendment #25 (Hatch #25)

") Hatch modification to Amendment #25 (Hatch #25) The amendment is modified to read as follows: Short title: To provide modifications, clarifications, and additions to the Chairman s mark of the Tax Cuts

Hatch modification to Amendment #25 (Hatch #25) The amendment is modified to read as follows: Short title: To provide modifications, clarifications, and additions to the Chairman s mark of the Tax Cuts

G. TAXPAYER INQUIRIES

E. RELIEF FROM PENALTY FOR FAILING TO FILE PARTNERSHIP RETURN BY MAGNETIC MEDIA Any partnership that is an affected taxpayer, as defined in Notice 2001 61 and this notice, and that is required to file

E. RELIEF FROM PENALTY FOR FAILING TO FILE PARTNERSHIP RETURN BY MAGNETIC MEDIA Any partnership that is an affected taxpayer, as defined in Notice 2001 61 and this notice, and that is required to file

Instructions for Completing Wisconsin Schedule I 2017

Caution: The revised version of the 2017 Schedule I instructions was placed on the Internet on February 2, 2018. The instructions have been revised to include changes to federal law that were made by Public

Caution: The revised version of the 2017 Schedule I instructions was placed on the Internet on February 2, 2018. The instructions have been revised to include changes to federal law that were made by Public

AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

Income Tax Planning for IRAs & Qualified Plans

Income Tax Planning for IRAs & Qualified Plans Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Foundation Concepts Tax Brackets 2 Foundation Concepts General Income Tax Treatment Tax Deduction

Income Tax Planning for IRAs & Qualified Plans Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Foundation Concepts Tax Brackets 2 Foundation Concepts General Income Tax Treatment Tax Deduction

Individual Retirement Account (IRA)

") Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

G. Modify Rules Governing Tax-Exempt Bonds for Section 501(c)(3) Organizations as Applied to Organizations Engaged in Timber Conservation Activities

(3) Organizations as Applied to Organizations Engaged in Timber Conservation Activities") CONTENTS I. MARGINAL TAX RATE REDUCTION... 1 A. Individual Income Tax Rate Structure (secs. 2 and 3 of the House bill, sec. 101 of the Senate amendment and sec. 1 of the Code)... 1 B. Increase Starting

CONTENTS I. MARGINAL TAX RATE REDUCTION... 1 A. Individual Income Tax Rate Structure (secs. 2 and 3 of the House bill, sec. 101 of the Senate amendment and sec. 1 of the Code)... 1 B. Increase Starting

Disaster Losses. Phone: Fax: Your California solution since 1975

www.caltax.com E-mail: CPE@spidell.com Phone: 714-776-7850 Fax: 714-776-9906 Your California solution since 1975 This publication is distributed with the understanding that the authors and publisher are

www.caltax.com E-mail: CPE@spidell.com Phone: 714-776-7850 Fax: 714-776-9906 Your California solution since 1975 This publication is distributed with the understanding that the authors and publisher are

made simple Landlords Package Policy Insurance What s inside:

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

Model Disaster Relief Documents For Employer-Controlled Charities

Model Disaster Relief Documents For Employer-Controlled Charities September 7, 2005 Providing aid to victims of civil or natural disasters has historically been a critical function of charitable organizations.

Model Disaster Relief Documents For Employer-Controlled Charities September 7, 2005 Providing aid to victims of civil or natural disasters has historically been a critical function of charitable organizations.

Individual Income Tax Organizer 2016

MICHAEL R. ANLIKER, CPA, P.C. 5348 Twin Hickory Rd. Glen Allen, VA 23059 TELEPHONE: (804) 237-6044 FAX: (804) 237-6064 www.anlikerfinancial.com Individual Income Tax Organizer 2016 This Tax Organizer is

MICHAEL R. ANLIKER, CPA, P.C. 5348 Twin Hickory Rd. Glen Allen, VA 23059 TELEPHONE: (804) 237-6044 FAX: (804) 237-6064 www.anlikerfinancial.com Individual Income Tax Organizer 2016 This Tax Organizer is

BNY MELLON INVESTMENT SERVICING TRUST COMPANY

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2018 DEADLINE EXTENSION FOR 2017 CONTRIBUTIONS

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2018 DEADLINE EXTENSION FOR 2017 CONTRIBUTIONS

To provide tax relief for the victims of Hurricane Florence, Hurricane Michael, and certain California wildfires. IN THE SENATE OF THE UNITED A BILL

115TH CONGRESS 2D SESSION S. To provide tax relief for the victims of Hurricane Florence, Hurricane Michael, and certain California wildfires. IN THE SENATE OF THE UNITED STATES Mr. BURR (for himself,

115TH CONGRESS 2D SESSION S. To provide tax relief for the victims of Hurricane Florence, Hurricane Michael, and certain California wildfires. IN THE SENATE OF THE UNITED STATES Mr. BURR (for himself,

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s 1120 Deskbook. Twenty-seventh Edition (October 2017)

") Route To: j Partners j Managers j Staff j File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1120 Deskbook Twenty-seventh Edition (October 2017) Highlights of this Edition Thefollowingaresomeoftheimportantupdatefeaturesofthe2017editionofPPC

Route To: j Partners j Managers j Staff j File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1120 Deskbook Twenty-seventh Edition (October 2017) Highlights of this Edition Thefollowingaresomeoftheimportantupdatefeaturesofthe2017editionofPPC

S. ll. To amend the Internal Revenue Code of 1986 to extend certain expiring provisions, to provide disaster tax relief, and for other purposes.

TH CONGRESS ST SESSION S. ll To amend the Internal Revenue Code of to extend certain expiring provisions, to provide disaster tax relief, and for other purposes. IN THE SENATE OF THE UNITED STATES llllllllll

TH CONGRESS ST SESSION S. ll To amend the Internal Revenue Code of to extend certain expiring provisions, to provide disaster tax relief, and for other purposes. IN THE SENATE OF THE UNITED STATES llllllllll

Federal Tax Code 2017 House and Senate Tax Reform Proposals

Current Law (Section) H.R. 1 Tax Cuts and Jobs Act (House version) House Comments and Recommendations H.R. 1 Tax Cuts and Jobs Act (Senate version) Senate Comments and Recommendations (26 U.S.C. 121) Exclusion

Current Law (Section) H.R. 1 Tax Cuts and Jobs Act (House version) House Comments and Recommendations H.R. 1 Tax Cuts and Jobs Act (Senate version) Senate Comments and Recommendations (26 U.S.C. 121) Exclusion

Employee Benefit Issues After Tax Reform. May 7 th, 2018 TEI Houston Tax School 2018

Employee Benefit Issues After Tax Reform May 7 th, 2018 TEI Houston Tax School 2018 2 Presenter Jeff Martin Partner, Grant Thornton LLP Washington National Tax Office Jeffrey.Martin@us.gt.com (202) 521-1526

Employee Benefit Issues After Tax Reform May 7 th, 2018 TEI Houston Tax School 2018 2 Presenter Jeff Martin Partner, Grant Thornton LLP Washington National Tax Office Jeffrey.Martin@us.gt.com (202) 521-1526

Calif. Resource Guide. December 2017

Insurance Recovery Group Client Resource Guide Reed Smith 2017 Southern Calif fornia Wildfire Relief Resource Guide December 2017 Reed Smith 2017 Southern California Wildfires Relief Resources Guide Though

Insurance Recovery Group Client Resource Guide Reed Smith 2017 Southern Calif fornia Wildfire Relief Resource Guide December 2017 Reed Smith 2017 Southern California Wildfires Relief Resources Guide Though

Instructions for Forms 1099-R and 5498

2009 Instructions for Forms 1099-R and 5498 Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Airline

2009 Instructions for Forms 1099-R and 5498 Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Airline

Landlords Package Policy Insurance. made simple

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

AMG FUNDS SIMPLE IRA

AMG FUNDS SIMPLE IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the SIMPLE Individual Retirement Account (SIMPLE IRA) Disclosure Statement For Tax Year 2018 2018 SIMPLE IRA CONTRIBUTION

AMG FUNDS SIMPLE IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the SIMPLE Individual Retirement Account (SIMPLE IRA) Disclosure Statement For Tax Year 2018 2018 SIMPLE IRA CONTRIBUTION

Tax Reform: Comparison of House and Senate Versions of the Tax Cuts and Jobs Act (H.R. 1)

") December 5, 2017 Tax Reform: Comparison of House and Senate Versions of the Tax Cuts and Jobs Act (H.R. 1) Modification of Non- Discrimination Rules Retirement Provisions If an employer closes a DB plan

December 5, 2017 Tax Reform: Comparison of House and Senate Versions of the Tax Cuts and Jobs Act (H.R. 1) Modification of Non- Discrimination Rules Retirement Provisions If an employer closes a DB plan

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA.

Traditional IRA SEP IRA.") PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA

TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA") Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED

3Q: Do I get a deduction if I donated my time to volunteer for an organization/church?

Frequently Asked Charitable Contribution Deductions Questions for Aid Given to Hurricane Irma, Harvey, and Maria Victims By Sonia Chang, Stetson University Valrie Chambers, Stetson University Gerard H.

Frequently Asked Charitable Contribution Deductions Questions for Aid Given to Hurricane Irma, Harvey, and Maria Victims By Sonia Chang, Stetson University Valrie Chambers, Stetson University Gerard H.

BNY MELLON INVESTMENT SERVICING TRUST COMPANY

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2019 DEADLINE EXTENSION FOR 2018 CONTRIBUTIONS

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2019 DEADLINE EXTENSION FOR 2018 CONTRIBUTIONS

Individual Taxpayer Issues ISSUES 4 8 MERRILL FROMER

Individual Taxpayer Issues ISSUES 4 8 MERRILL FROMER Issue #4 Charitable Contributions pg. 345 As of now only individuals who itemize can claim a charitable contribution (that was not always the case)

Individual Taxpayer Issues ISSUES 4 8 MERRILL FROMER Issue #4 Charitable Contributions pg. 345 As of now only individuals who itemize can claim a charitable contribution (that was not always the case)

97 Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 97 Department Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Credits, Deductions, etc. (For Shareholder's Use Only) Section references are to the Internal Revenue

97 Department Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Credits, Deductions, etc. (For Shareholder's Use Only) Section references are to the Internal Revenue

After Hurricane Irma CLIENT SUMMARY

After Hurricane Irma CLIENT SUMMARY After Hurricane Irma 2 Tax and financial implications of disaster-related casualties Hurricane Irma left many homeowners and businesses with major, unprecedented damage.

After Hurricane Irma CLIENT SUMMARY After Hurricane Irma 2 Tax and financial implications of disaster-related casualties Hurricane Irma left many homeowners and businesses with major, unprecedented damage.

Stephanie Alden Smithey

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Chapter 5: Personal Tax Credits. 05: Personal Tax Credits

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

10 NATP TAXPRO Journal / natptax.com

10 NATP TAXPRO Journal / natptax.com Top 25 Research Questions (and the answers, of course!) By NATP s Research Staff Throughout the year, NATP s Tax Knowledge Center answers tens of thousands of questions

10 NATP TAXPRO Journal / natptax.com Top 25 Research Questions (and the answers, of course!) By NATP s Research Staff Throughout the year, NATP s Tax Knowledge Center answers tens of thousands of questions

The Provincial Disaster Assistance Program Regulations, 2011

1 ASSISTANCE PROGRAM E-8.1 REG 2 The Provincial Disaster Assistance Program Regulations, 2011 being Chapter E-8.1 Reg 2 (effective April 1, 2010) as amended by the Statutes of Saskatchewan, 2014, c.s-32.21.

1 ASSISTANCE PROGRAM E-8.1 REG 2 The Provincial Disaster Assistance Program Regulations, 2011 being Chapter E-8.1 Reg 2 (effective April 1, 2010) as amended by the Statutes of Saskatchewan, 2014, c.s-32.21.