Tax Law Update. Agenda 10/17/2017. October 17, 2017

|

|

|

- Gwenda Marsh

- 5 years ago

- Views:

Transcription

1 Tax Law Update October 17, 2017 Agenda President s October 12, Directive Disaster Legislation myra Phaseout Qualified Small Employer HRA Form 1098 T Reporting Private Debt Collection Partnership Penalty Relief due to FAST Act Small Business Research Credit Offset ITIN Renewals Substitute for Return Changes Misc. Issues 2 1

2 Presidents October 12, 2017 Directive Presidential Executive Order Promoting Healthcare Choice and Competition Across the United States Section 1. Facilitate the purchase of insurance across State lines and develop and operate a healthcare system that provides high quality care at affordable prices for the American people The Patient Protection and Affordable Care Act (PPACA), however, has severely limited the choice of healthcare options available Produced large premium increases 3 Presidents October 12, 2017 Directive The average exchange premium in 39 States that are using in 2017 is more than doubled the average overall individual market premium recorded in 2013 The PPACA has failed to provide meaningful choice or competition between insurers, currently one third of America's counties having only one insurer in

3 Presidents October 12, 2017 Directive Section 1 Three areas for improvement in the near term will be prioritize: Association Health Plans (AHPs) Short Term, Limited Duration Insurance (STLDI) and Health Reimbursement Arrangements (HRAs) Expanding access to AHPs can help small businesses overcome the competitive disadvantage, allowing them to group together to self insure or purchase large group health insurance 5 Presidents October 12, 2017 Directive Short term, limited duration insurance (STLDI) is exempt from the onerous and expensive insurance mandates and regulations included in Title I of the PPACA Appealing and affordable to alternative to government run exchanges for many people without coverage available to them through their workplaces Heath Reimbursement Arrangements (HRAs) are taxadvantaged, account based arrangements that employers can establish for employees to give employees more flexibility and choices regarding their healthcare 6 3

4 Presidents October 12, 2017 Directive Section 2 Expanded Access to Association Health Plans: within 60 days the Secretary of Labor shall consider proposing regulations or revising guidance, consistent with law, to expand access to health coverage by allowing more employers to form AHPs Consider ways to promote AHP formation 7 Presidents October 12, 2017 Directive Section 3 Expanded Availability of Short Term, Limited Duration Insurance Consider proposing regulations or revising guidance, consistent with law, to expand the availability of STLDI Consider allowing such insurance to cover longer periods and be renewed by the consumer 8 4

5 Presidents October 12, 2017 Directive Section 4 Expanded Availability and Permitted Use of Health Reimbursement Arrangements Consider proposing regulations or revising guidance to increase the usability of HRAs, to expand employers' ability to offer HRAs to their employees, and to allow HRAs to be used in conjunction with nongroup coverage 9 Disaster 10 5

6 H.R.3823 Disaster Tax Relief and Airport and Airway Extension Act of 2017, P.L The new law allows the purchase of private flood insurance offered outside of the National Flood Insurance Program The private insurance will satisfy the requirement for homeowners to maintain flood insurance coverage on properties that have: Federally backed mortgages and Are located in a flood zone 11 H.R.3823 Disaster Tax Relief and Airport and Airway Extension Act of 2017 The bill modifies several tax provisions and rules for individuals and businesses in areas affected by Hurricanes Harvey, Irma, and Maria, including provisions regarding: Early withdrawals and loans from retirement plans Employment related tax credits Deductions for charitable contributions Deductions for personal casualty losses, and Income requirements for the earned income tax credit and the child tax credit 12 6

7 Disaster Losses Current Law Under 165(a) a taxpayer generally may claim a deduction for any loss sustained during the tax year and not compensated by insurance or otherwise An individuals personal loss from a casualty is deductible only to the extent that (1) it exceeds $100, and (2) all casualty losses (after application of the $100 floor) for the tax year must generally exceed 10% of adjusted gross income (AGI) 13 Disaster Losses Current Law If the disaster occurs in a federally declared disaster area, the taxpayer may elect to take into account the casualty loss in the tax year immediately preceding the tax year in which the disaster occurs or in the year of the loss The deduction for casualty losses is an itemized deduction Schedule A 14 7

8 Declared Disaster Area Net disaster loss The Act defines a net disaster loss as the excess of qualified disaster related personal casualty losses over personal casualty gains A qualified disaster related personal casualty losses, are losses that arise: In the Hurricane Harvey disaster area on or after Aug. 23, 2017, and which are attributable to Hurricane Harvey specific areas are defined by FEMA 15 Declared Disaster Area Hurricane Irma disaster area on or after Sept. 4, 2017, and which are attributable to Hurricane Irma in the specified areas defined by FEMA or Hurricane Maria disaster area on or after Sept. 16, 2017, and which are attributable to Hurricane Maria in the specified areas defined by FEMA 16 8

9 Other Conditions No reduction for taxpayers subject to AMT The Act provides that 56, which generally disallows the standard deduction for alternative minimum tax (AMT) purposes, does not apply for the portion of the standard deduction attributable to the net disaster loss Increased floor In addition, the Act increases the $100 per casualty floor to $500 for qualified disaster related personal casualty losses 17 Retirement Account Current Law A loan from a qualified employer plan to a participant or beneficiary is treated as a plan distribution unless, among other things: (i) the loan amount doesn't exceed the lesser of: (A) $50,000, or (B) Half of the present value of the employee's nonforfeitable accrued benefit under the plan (a loan up to $10,000 is allowed, even if it's more than half the employee's accrued benefit) and (ii) the loan is required to be repaid within five years except that a longer repayment is available for a principal residence loan 18 9

10 Retirement Account Current Law Early (generally, pre age 59 1/2) withdrawals from a qualified retirement plan result in regular tax plus an additional tax equal to 10% of the amounts withdrawn that are includible in gross income The additional tax applies unless the taxpayer qualifies for one of several specific exceptions 19 H.R.3823 Disaster Tax Relief and Airport and Airway Extension Act of 2017 The new law allows Qualified Hurricane Distributions The law provides an exception to the 10 percent early retirement plan withdrawal penalty for qualified hurricane relief distributions Allows for the re contribution of retirement plan withdrawals for home purchases cancelled due to eligible disasters Increases the limit on loans not treated as retirement distributions from $50,000 to $100,

11 Qualified Hurricane Distribution A qualified hurricane distribution is any distribution from an eligible retirement plan, as defined by 402(c)(8)(B) (which includes IRAs) Time frames for the distribution are defined as: On or after Aug. 23, 2017, and before Jan. 1, 2019, to an individual whose principal place of abode on Aug. 23, 2017, is located in the Hurricane Harvey disaster area and who has sustained an economic loss by reason of Hurricane Harvey 21 Qualified Hurricane Distribution On or after Sept. 4, 2017, and before Jan. 1, 2019, to an individual whose principal place of abode on Sept. 4, 2017, is located in the Hurricane Irma disaster area and who has sustained an economic loss by reason of Hurricane Irma; and On or after Sept. 16, 2017, and before Jan. 1, 2019, to an individual whose principal place of abode on Sept. 16, 2017, is located in the Hurricane Maria disaster area and who has sustained an economic loss by reason of Hurricane Maria 22 11

12 Other Provisions Penalty relief The law excepts qualified hurricane distributions from the 10% early retirement plan withdrawal penalty Eased inclusion rules In addition the law allows taxpayers to spread out any income inclusion resulting from such withdrawals over a 3 year period, beginning with the year that any amount is required to be included (or elect out) 23 The Favorable Re Contribution Rule If re contributed to a eligible retirement plan other than an IRA, the taxpayer is treated as having received the qualified hurricane distribution in an eligible rollover distribution and as having transferred the amount to an eligible retirement plan in a direct, trustee to trustee transfer within 60 days of the distribution If recontributed to an IRA, the qualified hurricane distribution is treated as a distribution that is transferred to an eligible retirement plan in a direct trustee to trustee distribution within 60 days of the distribution 24 12

13 In Addition No withholding The withholding rules under a qualified hurricane distributions aren't treated as eligible rollover distributions (which, unless certain requirements are met, are otherwise subject to 20% withholding) Relief for cancelled home purchases The law also allows for the re contribution of certain retirement plan withdrawals for home purchases or construction, which were received after Feb. 28, 2017 and before Sept. 21, 2017, where the home purchase or construction was cancelled on account of Hurricane Harvey, Irma, or Maria 25 Re Contribution A timely re contribution avoids tax on the plan withdrawal The re contribution must be made during the period beginning on Aug. 23, 2017, and ending on Feb. 28,

14 Eased Rules for Retirement Plan Loans With respect to retirement plan loans, the law: Increases the maximum amount that a participant or beneficiary can borrow from a qualified employer plan from $50,000 to $100,000 Removes the one half of present value limitation Allows for a longer repayment term, if the due date for any repayment with respect to the loan occurs during a qualified beginning date that is Hurricane specific and ends on Dec. 31, 2018, by delaying the due date of the first repayment by one year (and adjusting the due dates of subsequent repayments accordingly 27 H.R.3823 Disaster Tax Relief and Airport and Airway Extension Act of 2017 Charitable Deduction the law temporarily suspends limitations on charitable contributions associated with qualified hurricane relief if contributions are made made before December 31,

15 Charitable Deduction Current Law An individual who itemizes can deduct charitable contributions up to 50%, 30% or 20% of AGI, depending on the type of property contributed and the type of donee A corporation generally can deduct charitable contributions up to 10% of its taxable income Amounts that exceed the ceilings ( excess contributions ) can be carried forward for five years by both individuals and corporations, subject to various limitations and ordering rules For individuals, charitable contributions are deductible only as an itemized deduction 29 Charitable Deduction Disaster Changes For a qualifying charitable contributions associated with qualified hurricane relief, the law: Temporarily suspends the majority of the limitations on charitable contributions Provides that such contributions will not be taken into account for purposes of applying percentage limitations Eased rules governing the treatment of excess contributions; and Provides an exception from the overall limitation on itemized deductions for certain qualified contributions 30 15

16 Charitable Deduction Disaster Changes Qualified contributions must be paid during the period beginning on Aug. 23, 2017, and ending on Dec. 31, 2017, in cash to a qualified organization for relief efforts in the Hurricane Harvey, Irma, or Maria disaster areas Qualified contributions must also be substantiated, with a contemporaneous written acknowledge that the contribution was or is to be used for relief efforts and the taxpayer must make an election for the changes to apply For partnerships and S corporations, the election is made separately by each partner or shareholder 31 Employee Retention Tax Credit for Employers Current Law Certain business incentive credits are combined into one general business credit for purposes of determining each credit's allowance limitation for the tax year A General Business Credit claimed on Form 3800 is allowed against income tax for a particular tax year and equals the sum of: (1) The business credit carryforwards carried to the tax year (2) The current year General Business Credit and (3) The business credit carrybacks carried to the tax year A list of the component credits of the current year business credit is provided in 38(b) 32 16

17 H.R.3823 Disaster Tax Relief and Airport and Airway Extension Act of 2017 Employee Retention Credit for Employers The law provides a tax credit for 40% of wages (up to $6,000 per employee) paid by a disaster affected employer to an employee from a core disaster area In general, the credit is be treated as a credit listed under 38(b), and equals 40% of up to $6,000 of qualified wages with respect to each eligible employee of such employer for the tax year 33 Employee Retention Credit for Employers The law provides a new employee retention credit for eligible employers affected by Hurricanes Harvey, Irma, and Maria Eligible employers are generally defined as employers that conducted an active trade or business in a disaster zone as of a specified date (for Hurricane Harvey, Aug. 23, 2017; Irma, Sept. 4, 2017; and Maria, Sept. 16, 2017) and The active trade or business of which was, on any day between the specified date and Jan. 1, 2018, rendered inoperable as a result of damage sustained by the hurricane 34 17

18 Eligible Employee An eligible employee with respect to an eligible employer is one whose principal place of employment with the employer was in Hurricane Harvey, Irma, or Maria disaster zone as of the respective dates noted previously Qualified wages mean wages paid or incurred by an eligible employer with respect to an eligible employee on any day after the specified date and before Jan. 1, 2018, which occurs during the period: Beginning on the date on which the employer's trade or business first became inoperable at the principal place of employment of the employee immediately before the respective hurricane, and 35 Eligible Employee Ending on the date on which such trade or business has resumed significant operations at such principal place of employment Qualified wages include wages paid without regard to whether the employee performs no services, performs services at a different place of employment than such principal place of employment, or performs services at such principal place of employment before significant operations have resumed 36 18

19 Limitations An employee can not be taken into account more than one time for purposes of the employee retention tax credit For instance, if an employee is an eligible employee of an employer with respect to Hurricane Harvey for purposes of the credit, the employee cannot also be an eligible employee of the employer with respect to Hurricane Irma or Hurricane Maria The law also provides that rules similar to 51(i)(1) (which disallows the work opportunity tax credit, or WOTC, when the employee is considered related to the employer, and 52 which provides rules for apportioning the WOTC among commonly controlled businesses) 37 Special Rule for Determining the Earned Income Tax Credit and the Child Tax Credit Current Law EITC Under 32, an eligible individual is allowed an earned income tax credit (EITC) equal to the credit percentage of earned income (up to an earned income amount ) for the tax year For 2017, the earned income credit amount is $510 for taxpayers with no qualifying children, $3,400 for those with one qualifying child, and $5,616 for those with two qualifying children and $6,318 for those with three or more qualifying children For purposes of the EITC, earned income includes wages, salaries, tips, and other employee compensation, but only if those amounts are includible in gross income for the tax year; plus net earnings from selfemployment less the deduction for half of self employment tax for the year 38 19

20 Current Law Child Tax Credit Under 24, individuals can claim a $1,000 child tax credit for each qualifying child the taxpayer can claim as a dependent The child must be under 17 and a U.S. citizen or resident alien The amount of the allowable credit is reduced (not below zero) by $50 for each $1,000 (or fraction thereof) of modified adjusted gross income (AGI increased by excluded foreign, possession, and Puerto Rico income) above: $110,000 for joint filers $75,000 for unmarried individuals and $55,000 for married taxpayers filing separately To the extent the CTC exceeds the taxpayer's tax liability, the taxpayer is eligible for a refundable credit equal to 15% percent of earned income in excess of a threshold dollar amount 39 H.R.3823 Disaster Tax Relief and Airport and Airway Extension Act of 2017 Special Rule for Determining the Earned Income Tax Credit and the Child Tax Credit At the election of the taxpayer, the bill allows individuals to refer to earned income from the immediately preceding year for purposes of determining the Earned Income Tax Credit and the Child Tax Credit These credits can increase as income increases up to a certain level for certain taxpayers Many individuals were not able to work during these Hurricanes and as a result may have a lower income for taxable year

21 Disaster Provisions New Law The law provides that, in the case of a qualified individual, if the earned income of the taxpayer for the tax year which includes the applicable date is less than the taxpayer's earned income for the preceding tax year, then the taxpayer may, for purposes of the EITC and CTC, substitute the earned income for the preceding year for the earned income for the tax year that includes the applicable date If the election is made, it applies for both 24(d) and Disaster Provisions New Law For Hurricane Harvey, a qualified individual is one whose principal place of abode on Aug. 23, 2017 was located either in the Hurricane Harvey disaster zone, or in the Hurricane Harvey disaster area and the individual was displaced from their principal place of abode by reason of Hurricane Harvey Similar definitions apply for Hurricane Irma (using a Sept. 4, 2017 date) and Hurricane Maria (using a Sept. 16, 2017 date In the case of joint filers, the above election may apply if either spouse is a qualified individual 42 21

22 Notice Disaster PR and VI Notice provides relief for individuals who may otherwise lose their status as a bona fide resident of Puerto Rico or the U.S. Virgin Islands because of the unexpected and prolonged dislocation caused by Hurricane Irma and Hurricane Maria Notice extends the 14 day absence period to 117 days under Reg (c)(3)(i)(C)(1) Without this extension, individuals affected by the hurricanes might not be able to satisfy the physical presence test with respect to residency in Puerto Rico or the U.S. Virgin Islands, and might otherwise lose their status as a bona fide resident of a U.S. territory 43 Notice One Year Extension of Time to Replace Livestock, Drought Related Sales Notice provides an extension of one year of the relief previously provided by the IRS in 2016, to allow eligible farmers and ranchers until the end of the tax year after the first drought free year to replace the sold livestock The IRS has provided this extension to farmers and ranchers located in applicable regions that qualified for the four year replacement period if any county, parish, city, or district, that is included in the applicable regions is listed as suffering exceptional, extreme or severe drought conditions by the National Drought Mitigation Center (NDMC), during any weekly period between September 1, 2016, and August 31,

23 Notice Farmers and ranchers who previously were forced to sell livestock due to drought in an applicable region a county designated as eligible for federal assistance plus counties contiguous to that county have an additional year to replace the livestock and defer tax on any gains from the forced sales pursuant to 1033(e) IR the tax relief generally applies to capital gains realized by eligible farmers and ranchers on sales of livestock held for draft, dairy or breeding purposes 45 Notice Sales of other livestock, such as those raised for slaughter or held for sporting purposes, or poultry are not eligible To qualify, the sales must be solely due to drought, flooding or other severe weather causing the region to be designated as eligible for federal assistance Under these circumstances, livestock generally must be replaced within a four year period, instead of the usual two year period The IRS is also authorized to further extend this replacement period if the drought continues 46 23

24 myra 47 Phasing Out the myra Program The U.S. Department of the Treasury has decided to phase out the myra retirement savings program, and the program is no longer accepting new enrollments Existing accounts can remain open until further notice What is happening to accounts? The account remains open and taxpayers can continue to manage the account until further notice The funds in the account remain safe and in an investment issued by the U.S. Department of the Treasury 48 24

25 Phasing Out the myra Program Any myra with a zero ($0) balance as of September 15, 2017 or later, will be subject to possible automatic closure beginning on September 18, 2017 Treasury will be reaching out to all of the account holders with more information regarding the transfer or closure of the account over the next few weeks outlining when they will stop accepting and processing deposits 49 Phasing Out the myra Program It is recommended taxpayers log in to their account to make sure their contact information is complete and up to date They can also update their information by contacting customer service They can initiate a direct transfer of their full account balance to another Roth IRA at any time First identify or open an account at the new Roth IRA provider where they will continue to save and invest 50 25

26 Phasing Out the myra Program Then, work with a new Roth IRA provider selected to transfer the myra balance to the new Roth IRA By opening another Roth IRA and working with the new Roth IRA provider to initiate a transfer of the funds in the myra to the new Roth IRA, taxpayers avoid withholding and potential tax liabilities (including potential tax penalties) that may apply to earnings if funds are paid directly to them To request closure of the account, call myra customer support at or TTY/TDD or International Phasing Out the myra Program Remember that a myra follows Roth IRA rules To avoid tax liabilities that may apply to earnings if funds are paid directly to the taxpayer they will need to deposit the amount of the distribution (including any tax withholding) into a private sector Roth IRA within 60 days of the distribution Taxpayers may receive an additional payment due to a timing difference between when interest earned was reflected in the account balance, and when the requested a withdrawal or distribution is issued 52 26

27 Phasing Out the myra Program Transferring the account myra has no fees to move funds to another Roth IRA provider (or to withdraw funds and close the account) Have the taxpayer check with the new Roth IRA provider to learn whether they have applicable fees Can the taxpayer transfer or roll over the account into an employer sponsored retirement plan, such as a 401(k), or into a traditional IRA? No. As is the case with all Roth IRAs, the myra can t be transferred or rolled over into an employer sponsored retirement plan or a traditional IRA Roth IRAs must be transferred or rolled over into other Roth IRAs 53 Qualified Small Employer HRA 54 27

28 21 st Century Cures Act H.R. 34, P.L Amends the Internal Revenue Code, the Patient Protection and Affordable Care Act (PPACA), and other laws to exempt qualified small employer health reimbursement arrangements (HRAs) from certain requirements that apply to group health plans A qualified small employer HRA is offered by employers that have fewer than 50 full time employees and do not offer group health plans to any of their employees 55 21st Century Cures Act H.R. 34, P.L A qualified small employer HRA must: Be provided on the same terms to all eligible employees of the employer Be funded solely by the employer without salary reduction contributions Provide, after an employee provides proof of coverage, for the payment or reimbursement of medical expenses of the employee and family members and Limit annual payments and reimbursements to specified dollar amounts, $4,950 for single and $10,000 for family this amount will be indexed in future years 56 28

29 21st Century Cures Act H.R. 34, P.L QSEHRAs that meet these requirements are not considered group health plans and are exempt from various requirements that apply to group health plans, including coverage and cost sharing requirements (Under current law, employers that sponsor group health plans that do not meet specified requirements are subject to an excise tax) Coverage and payments under a qualified HRA are excluded from gross income, unless the employee does not have minimum essential coverage for the month in which the medical care was provided 57 21st Century Cures Act H.R. 34, P.L Employers offering a qualified HRA must notify employees in advance regarding permitted benefits and report benefit information on W 2 forms and to health exchanges The bill sets forth requirements for determining whether an employee covered under an HRA is also eligible for premium subsidies under PPACA Effective January 1,

30 Additional Issues An employer is only able to exclude the following individuals from this benefit: Employees who have not completed 90 days of service Employees under age 25 Part time and seasonal employees Union employees (unless the union agreement provides for eligibility) Non resident aliens without income from sources within the United States 59 Notice of Coverage QSEHRA availability must be provided to the employee at least 90 days in advance of the start of the year or The start of the new employee s eligibility Due to the fact the law was passed very late in the 2016 year, issuing the 90 day notice in advance of the 2017 calendar year was not possible Employers will be in compliance as long as they issue a 2017 notice by March 13, 2017 (90 days of the law being signed) Notice extends the period for an employer to furnish an initial written notice to its eligible employees regarding a qualified small employer health reimbursement arrangement (QSEHRA) 60 30

31 The Notice is Required to Include Specific Criteria: The amount of the employee s yearly benefit eligibility The employee is required to report the benefit when applying for renewing coverage purchased through an exchange/marketplace and The employee will pay taxes on QSEHRA payments if the employee fails to maintain health insurance coverage during any period when they are receiving the QSEHRA payments The requirements of the notice are highly specific, and failure to provide proper and timely notice to employees can result in financial penalties (o) A $50 penalty per employee incident is imposed on any employer funding a qualified small employer health reimbursement arrangement who fails to provide written notice to each eligible employee capped at $2,500 per year The penalty will not apply if the failure to provide notice is due to reasonable cause and not to willful neglect Until the IRS issues a new deadline for the distribution of the notices to eligible employees, no penalties will be imposed 62 31

32 W 2 Reporting Requirements NEW If the client was covered under a QSEHRA, the employer reports the annual permitted benefit in Box 12 of the Form W 2 with code FF If the QSEHRA is affordable for a month, no Premium Tax Credit is allowed for the month If the QSEHRA is unaffordable for a month, the taxpayer must reduce the monthly Premium Tax Credit (but not below 0 ) by the monthly permitted benefit amount and they must write QSEHRA in the top margin on page 1 of Form 8962 to explain the entry and avoid delay in the processing of the return 63 New Form 8809 Application for Extension of Time to File Information Returns 64 32

33 Form 8809 Application for Extension of Time to File Information Returns New Version is dated September 2017 Contains a new line to indicate they qualify to use the form for extension of Form W 2 or an additional extension 65 Box 5 Form

34 Form 1098 T Reporting T: Box 1 Will Be Required for Tax Year 2018 Reporting The Internal Revenue Service (IRS) is not planning to grant any further relief from the Box 1 reporting requirement on the Form 1098 T Colleges and universities will still be allowed to use the Box 2 reporting method for 2017 (forms filed in early 2018) Institutions are expected without further guidance from the IRS to report amounts paid for qualified tuition and related expenses in Box 1 of the 2018 Form 1098 T (furnished to students and the IRS in early 2019) 68 34

based on")

35 1098 T: Box 1 Will Be Required for Tax Year 2018 Reporting Box 2 reporting will not be an option for the 2018 form New federal regulations addressing Form 1098 T reporting requirements are not expected until later this year Institutions of higher education will be expected to make a good faith effort to report the required amounts in Box 1 for tax year 2018 (filed in early 2019) based on existing rules and instructions 69 Form 1098 T 70 35

36 Private Debt Collection 71 Private Debt Collection IRS May Expand Private Debt Collection Program Earlier this year, the IRS rolled out its private debt collection program, which was authorized by the Fixing America's Surface Transportation (FAST) Act The program enables four private sector collection agencies to collect, on the government's behalf, unpaid income tax debts of individual taxpayers At a recent IRS Nationwide Tax Forum, Mary Beth Murphy, commissioner of the IRS Small Business/Self employed Division, indicated that the IRS may expand the program to other types of tax debt, such as penalties and business tax liabilities This is scheduled to occur in 2019 as the program matures Reported by Thompson Reuters 72 36

37 Private Debt Collection CP 40 Notice 73 Private Debt Collection CP 40 Notice 74 37

38 Private Debt Collection CP 40 Notice 75 Private Debt Collection CP 40 Notice 76 38

39 Gambling Winnings 77 TD 9824 Withholding on Payments of Certain Gambling Winnings The final regulation covers horse races, dog races, and jai alai and on certain other payments of gambling winnings The final regulations state that these rules apply to reportable gambling winnings paid with respect to a winning event that occurs on or after 45 days from the date the final regulations are published, scheduled for September 27, 2017 If you have a gambling establishment a review of the new withholding requirements is suggested 78 39

40 Partnership Issues 79 IRS Provides Penalty Relief for Partnerships that Filed Late Returns in 2017 The Internal Revenue Service issued guidance providing penalty relief for certain partnerships that did not file the required returns by the new due date for tax years beginning in 2016 Partnerships file Form 1065 or Form 1065 B or request an automatic extension by filing Form 7004 The Surface Transportation and Veterans Health Care Choice Improvement Act of 2015 changed the date by which a partnership must file its annual return 80 40

41 IRS Provides Penalty Relief for Partnerships that Filed Late Returns in 2017 For calendar year partnerships, the due date for filing the annual return or request for an extension changed from April 15 (April 18 in 2017) to March 15 Notice provides penalty abatement for these partnerships, provided: (1) the partnership filed the returns with the IRS and furnished copies to the recipients (as appropriate) by the date that would have been timely, or (2) the partnership filed Form 7004 to request an extension of time to file by the date that would have been timely 81 IRS Provides Penalty Relief for Partnerships that Filed Late Returns in 2017 Taxpayers who qualify for relief under Notice will not be treated as having received a first time abatement under the IRS s administrative penalty waiver program The new deadlines were provided in the instructions for Form 1065 and the instructions for Form 1065 B For calendar year partnerships, the due date for filing a return after receiving an extension is Sept

42 Updated N Notice initially provided penalty relief to certain partnerships that filed untimely returns or requests for extensions of time to file those returns This updated notice now applies to both partnerships and real estate mortgage investment conduits (REMICs), which are treated as partnerships for purposes of subtitle F of the Internal Revenue Code (dealing with procedure and administration) 83 Updated N Partnerships and REMICs that filed certain untimely returns or untimely requests for extension of time to file those returns for the first taxable year that began after December 31, 2015, by the fifteenth day of the fourth month following the close of that taxable year will receive relief from the penalty for failure to timely file 84 42

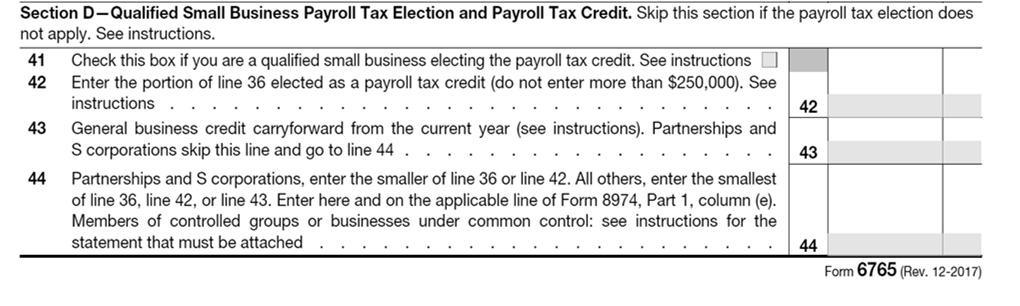

43 Small Business Research Credit Offset 85 Small Business Research Credit Offset Revised Form 6765 Credit for Increasing Research Activities The credit for increasing research activities has been made permanent The credit for increasing research activities of an eligible small business may offset alternative minimum tax Qualified small businesses may elect to apply up to $250,000 of the credit against the employer portion of social security taxes A Qualified Small Business Payroll Tax Election and Payroll Tax Credit, was added to reflect that a qualified small business may elect to claim a certain amount of its research credit as a payroll tax credit 86 43

44 Qualified Business A qualified small business means, with respect to any taxable year, a corporation, partnership, person or entity, if the gross receipts for the taxable year are less than $5,000,000, and such entity did not have gross receipts for any taxable year preceding the 5 taxable year period ending with such taxable year (2012 year) A qualified small business shall not include an organization that is exempt from income taxation under Qualified Research Qualified research means research for which expenses may be treated as 174 expenses This research must be undertaken for discovering information that is technological in nature, and its application must be intended for use in developing a new or improved business component of the taxpayer In addition, substantially all of the activities of the research must be elements of a process of experimentation relating to a new or improved function, performance, reliability, or quality All of the research activities must be applied separately with respect to each business component of the taxpayer 88 44

45 The Research Credit Generally is not Allowed for the Following Types of Activities Research conducted after the beginning of commercial production Research adapting an existing product or process to a particular customer s need Duplication of an existing product or process Surveys or studies Research relating to certain internal use computer software Research conducted outside the United States, Puerto Rico, or a U.S. possession Research in the social sciences, arts, or humanities. Research funded by another person (or governmental entity) Election to Take the Qualified Small Business Payroll Tax Credit Election Complete Section D of Form 6765 Complete Section D only if you are making the payroll tax election Before completing this section, the client must complete Form 3800 if they are a qualified small business other than a partnership or an S corporation Line 41 Check the box on line 41 if they are a qualified small business electing to claim a certain portion of the research credit as a payroll tax credit 90 45

46 Form Form

47 Line 42 Enter the portion of the research credit, figured on line 36, that they are claiming as a payroll tax credit Do not enter more than $250, Line 43 Use the worksheet in the instructions to figure the general business credit carryforward for the current year 94 47

48 Line 44 Enter the amount from line 44 on Form 8974, Qualified Small Business Payroll Tax Credit for Increasing Research Activities, line 5 Use Form 8974 to figure the amount to be applied to the payroll taxes A qualified small business claiming a portion of the research credit as a payroll tax credit must adjust the research credit carryforward for the payroll tax credit claimed

49 Form 8974 Qualified Small Business Payroll Tax Credit for Increasing Research Activities 97 Form 8974 Qualified Small Business Payroll Tax Credit for Increasing Research Activities 98 49

50 Form 941 and the Qualified Small Business Payroll Tax Credit for Increasing Research Activities 99 Form 941 and the Qualified Small Business Payroll Tax Credit for Increasing Research Activities

51 ITIN Renewals 101 Renewal Applications for ITINs Set to Expire by End of 2017 IR IRS will send the CP 48 Notice that explains the steps to take to renew the ITIN if it will be included on a U.S. tax return filed in 2018 ITINs that have not been used on a federal tax return at least once in the last three consecutive years will expire Dec. 31, 2017, and ITINs with middle digits 70, 71, 72 or 80 will also expire at the end of 2017 Affected taxpayers who expect to file a tax return in 2018, for the 2017 tax year, must submit a renewal application As a reminder, ITINs with middle digits of 78 and 79 already expired at the end of

52 Renewal Applications for ITINs Set to Expire by End of 2017 IR , June 21, 2017 Taxpayers with these ITIN numbers can renew at any time To renew an ITIN, a taxpayer must complete a Form W 7 and submit all required documentation Taxpayers submitting a Form W 7 to renew their ITIN are not required to attach a federal tax return, but attach a reason for needing an ITIN on the Form W Renewal Applications for ITINs Set to Expire by End of 2017 IR , June 21, 2017 Family Option Remains Available Taxpayers with an ITIN with middle digits 70, 71, 72 or 80 have the option to renew ITINs for their entire family at the same time Those who have received a renewal letter from the IRS can choose to renew the family s ITINs together even if family members have an ITIN with middle digits other than 70, 71, 72 or 80 Family members include the tax filer, spouse and any dependents claimed on the tax return

53 Note: When Renewing, Check the Renew Box Otherwise it Could Delay Processing Common Mistakes Federal returns that are submitted in 2018 with an expired ITIN will be processed Exemptions and/or certain tax credits will be disallowed Missing Information and insufficient supporting documentation Review the Form W 7 instructions for how to prepare and what documentation is needed to submit a valid request 105 Form W 7 Current Form

54 Substitute for Return Changes 107 IRM ( ) Substitute for Return (SFR) The Service has authority to prepare and process a tax return when a person fails to file a required return or files a false or fraudulent return The assessment date will start the period for the statute of limitations for collection but does not start the period of limitations for assessment If the taxpayer signs a SFR return prepared from income information received from the taxpayer, it becomes the taxpayer s return and starts the assessment period of limitations

55 IRM ( ) Substitute for Return (SFR) If the taxpayer signs a waiver of restriction on assessment it does not constitute a return in accordance with Rev. Rul If the Service has processed an unsigned Substitute for Return (SFR), the taxpayer may still file a signed tax return for the same tax year as the SFR return The assessment statute period for that tax year will begin with the received date of the taxpayer s signed return 109 Substitute for Return Program Suspended The SFR program, computers (without human involvement) (1) Detected the need to file and the lack of filing (2) Prepared substitutes for returns under 6020(b) based on the third party gross income information, and (3) Issue a letter to the taxpayer showing the proposed deficiency and balance due based on that substitute for return (essentially, a 30 day letter) The computer would automatically tack on late filing and late payment penalties to the tax balance due

56 Substitute for Return Program Suspended On September 26, 2017, Matthew Weir, the Assistant Inspector General of the Office of the Treasury Inspector General for Tax Administration (TIGTA) announced that the IRS had, for lack of sufficient financial resources, suspended its Automated Substitute for Return (ASFR) program 111 Miscellaneous Issues

57 Rev. Proc New, Simplified Procedure for Obtaining Extension to Make Estate Tax Portability Election The taxpayer is not required to file an estate tax return The taxpayer did not file an estate tax return within the time prescribed by Reg (a)(1) for filing an estate tax return required to elect portability The executor must file a complete and properly prepared Form 706 on or before the later of Jan. 2, 2018, or the second annual anniversary of the decedent's date of death; and The executor filing the Form 706 on behalf of the decedent's estate must state at the top of the Form 706 that the return is FILED PURSUANT TO REV. PROC TO ELECT PORTABILITY UNDER Code 2010(c)(5)(A) 113 Rev. Proc New, Simplified Procedure for Obtaining Extension to Make Estate Tax Portability Election Taxpayers that are not eligible for relief under this revenue procedure because the executor does not satisfy requirements detailed, may request an extension of time to make the portability election by requesting a letter ruling Note: A nonresident surviving spouse who is not a citizen of the United States may not take into account the DSUE amount of a deceased spouse, except to the extent allowed by treaty with his or her country of citizenship

58 New Revised Form 56 no Significant Changes 115 Form

59 Reg To reduce identity theft, the IRS issued proposed regulations that would permit employers to use truncated taxpayer identification numbers (TTINs) on Forms W 2, Wage and Tax Statement, issued to employees Permissible TTINs are Social Security numbers (SSNs) with the first five digits of the nine digit number replaced with asterisks or XXXs in the following formats: *** ** 1234 or XXX XX Reg Definition of a Dependent Most Significant Change Detailed in the Proposed Regulation Proposed Regulation , Special rule for a child of divorced or separated parents or parents who live apart A noncustodial parent must attach a copy of the written declaration to the parent's original or amended return for each taxable year for which the noncustodial parent claims an exemption for the child A noncustodial parent may submit a copy of the written declaration to the IRS during an examination to substantiate a claim to a dependency exemption for a child

60 Reg Definition of a Dependent A copy of a written declaration attached to an amended return, or provided during an examination, will not meet the requirement of this paragraph if the custodial parent signed the written declaration after the custodial parent filed a return claiming a dependency exemption for the child for the year at issue, and The custodial parent has not filed an amended return to remove that claim to a dependency exemption for the child 119 Reg Definition of a Dependent Current Reg (e)(2) requires that a noncustodial parent ( NCP ) claiming a child as a dependent must attach a copy of the written declaration to the parent s return for each taxable year in which the child is claimed as a dependent

61 Reg Definition of a Dependent Requirements when the Custodial Parent (CP) previously claimed exemption to which a Non Custodial Parent (NCP) is entitled Proposed Reg (e)(2)(i) states: A copy of a written declaration attached to an amended return, or provided during an examination, will not meet the requirement of paragraph (e) if the custodial parent signed the written declaration after the custodial parent filed a return claiming a dependency exemption for the child for the year at issue, and the custodial parent has not filed an amended return to remove that claim to a dependency exemption for the child 121 Reg Definition of a Dependent The new language is proposed to provide greater certainty, but the consequence of the language would be to leave the NCP who secured a Form 8332 from the CP after the CP filed the return with virtually no recourse against the CP for the Service s denial of his or her claim for dependency exemption(s)

62 Example 1 Custodial parent (CP) files her 2015 return on March 1, 2016, and claims a dependency exemption for child At noncustodial parent's (NCP) request, CP signs a Form 8332 for the 2015 tax year on April 15, 2016 On April 15, NCP files his return claiming a dependency exemption for Child and attaches the signed Form 8332 to his return Under 152(e) and paragraph (b) of this section, NCP is allowed a dependency exemption for Child for 2015, and CP is not allowed a dependency exemption for Child for that year The NCP has in his possession the Form 8332 at the time he files the return 123 Example 2 The facts are the same as in Example 1, except NCP files on April 15, 2016, a request for an extension to file his tax return because he does not have a signed Form 8332 CP signs the Form 8332 for the 2015 tax year in August of 2016, and NCP files his return a week later NCP claims a dependency exemption for Child and attaches the signed Form 8332 to his return NCP is allowed a dependency exemption for Child for 2015, and CP is not allowed a dependency exemption for Child for that year The NCP has in his possession the Form 8332 at the time he files the return

63 Example 3 CP files his 2015 return on March 1, 2016, and claims a dependency exemption for child NCP files her return on April 15, 2016, and does not claim a dependency exemption for child, even though her divorce decree allocates the dependency exemption for child to her CP signs a Form 8332 for the 2015 tax year in August of 2016, and NCP files an amended return a week later and attaches the signed Form 8332 to her amended return claiming a dependency exemption for child NCP is not allowed a dependency exemption for child for 2015 if CP has not amended his return to remove a claim to the dependency exemption for child for that year 125 Example 3 Note in this case the parent does not have Form 8332 in possession before filing return This is the change

64 Revocation The parent revoking the written declaration must attach a copy of the revocation to the parent's original or amended return for each taxable year for which the parent claims a child as a dependent as a result of the revocation The parent revoking the written declaration must keep a copy of the revocation and evidence of delivery of the notice to the other parent, or of the reasonable efforts to provide actual notice A parent may submit a copy of a revocation to the IRS during an examination to substantiate a claim to a dependency exemption for the child 127 Expired at the End of 2016 Most Common Issues Credit for nonbusiness energy property Certain credits for residential energy property, some expire in 2021 COD income exclusion for discharge of principal residence debt Mortgage insurance premium deduction as qualified residence interest Credit for constructing new energy efficient homes 3 year depreciation for racehorses 2 years old or younger

65 Expired at the End of 2016 Most Common Issues 7 year recovery period for motorsports entertainment complexes Accelerated depreciation for Indian reservation property 5 year cost recovery for certain energy property Special expensing rules for film and television productions Domestic production activities deduction for activities in Puerto Rico 7.5% of adjusted gross income (AGI) floor for individuals age 65 and older for medical expenses Deduction for qualified tuition and related expenses 129 Expired at the End of 2016 Energy Provisions Energy efficient commercial buildings deduction Alternative motor vehicle credit for qualified fuel cell motor vehicles Alternative fuel vehicle refueling property credit Qualified plug in electric drive motor vehicle credit for twowheeled vehicles Second generation biofuel producer credit. Special depreciation allowance for second generation biofuel plant property Income tax credits for biodiesel fuel, biodiesel used to produce a qualified mixture, and small agri biodiesel producers

66 Expired at the End of 2016 Energy Provisions Income tax credits for renewable diesel fuel and renewable diesel used to produce a qualified mixture Beginning of construction date for renewable power facilities eligible to claim the electricity production credit or investment credit in lieu of the production credit 2016/2019/2021 various provisions expire in specific years Credit for hybrid solar lighting, geothermal heat pump, fuel cell, and power plant property 131 Expired at the End of 2016 Other Provisions Special rate for qualified timber gains Credit for production of Indian coal Indian employment tax credit Railroad track maintenance credit Mine rescue team training credit Election to expense advanced mine safety equipment. Allocation of bond cap for qualified zone academy bonds Zone and Disaster Area Incentives Empowerment zone tax incentives Excise tax credits and outlay payments for alternative fuels and alternative fuel mixtures. Temporary increase in limit on excise tax revenues on distilled spirits (from $10.50 to $13.25 per proof gallon) to Puerto Rico and the Virgin Islands

67 Excise Taxes Expiring in 2017 All but 4.3 per gallon of taxes on noncommercial aviation kerosene and noncommercial aviation gasoline Expires 09/30/2017 Domestic and international air passenger ticket taxes and ticket tax exemption for aircraft in fractional ownership aircraft programs 09/30/2017 Air cargo tax 09/30/2017 Oil Spill Liability Trust Fund financing rate 12/31/2017 Temporary increase in limit on excise tax revenues on distilled spirits (from $10.50 to $13.25 per proof gallon) to Puerto Rico and the Virgin Islands Suspension of medical device excise tax 133 Iowa Important News For Tax Year 2017 What is optional? Any business registered with an Iowa withholding permit and/or filing using a bulk filer may submit 1099 and W 2s with no Iowa withholding information for tax year 2017 IDR will not issue permits and Business efile Numbers (BENs) for purposes of electronically filing 1099s or W 2s with no withholding

68 Iowa Important News For Tax Year 2017 Can IDR make filing easier? The Department will work with software vendors to register and test software prior to the 1/31/2018 filing deadline As a result, IDR will be able to guide businesses who are required to file W 2s for tax year 2017 to a list of vendors who have completed testing, offer their software services for sale, and who support the IA W 2 and 1099 file formats Look for an bulletin announcing the list is available on the IDR website later this fall 135 Iowa Important News For Tax Year 2017 Filed in 2018 These are the same requirements in place for tax year The proposed change delays the filing requirement for businesses with fewer than 50 W 2s out to tax year 2018 What am I required to file? Businesses with 50 or more Iowa W 2s in tax year 2017 must electronically file by 1/31/2018 Businesses with 50 or more Iowa W 2s in tax year 2016 who received a filing extension for tax year 2016 must electronically file on or before 1/31/

69 Iowa Important News For Tax Year 2017 When will I know if the IDR proposal was approved? Stay tuned in to these bulletins for updates about Iowa s W 2/1099 filing program. When more information is available, IDR will notify you here Webinar: Electronic Submission of W 2s & 1099s October 18, 2017 This online course will provide an overview of the requirements for the electronic submission of W 2s and 1099s to the Iowa Department of Revenue. Topics covered will include: Requirements Prior to Tax Year 2016 Requirements for Tax Year 2016 Requirements for Tax Year 2017 and Future Years Submitting Wage Statements and Information Returns Information Resources Time will be left at the end for any general questions. 137 To Register for W 2 Iowa Seminar 46dcd7c24e00bf0acd2b

70 Form I 9 Changes January 2017 Changes September 18, 2017 Form asks for other last names One key change is that users must enter N/A in any fields that they previously would have left blank For example, if there is nothing to enter in the fields asking for a middle initial, or apartment number or Social Security number, those fields can no longer be left blank 139 Iowa Important News For Tax Year 2017 What changed? In order to give small businesses additional time to comply with W 2/1099 filing requirements, the Iowa Department of Revenue (IDR) proposed the following changes to tax year 2017 filing requirements: Businesses with fewer than 50 W 2s will not be required to file W 2s for tax year 2017 No entities will be required to file 1099s for tax year

71 Form I 9 Changes January 2017 Foreign Workers Another modification lessens the administrative burden on foreign workers If the new hire attests to being a foreign national authorized to work in the U.S., he or she can provide either an alien registration number, Form I 94 admission number or foreign passport number Previously, foreign nationals authorized to work were required to provide both an I 94 number and foreign passport information 141 Form I 9 Changes January 2017 The new form allows for up to five preparers and/or translators to each sign and date the form in his or her own field The prior form had one field for potentially multiple preparers and translators to fit their signatures "The employee [now] needs to affirmatively check a box indicating that he or she did not use a preparer or translator if that's in fact the case This is an important double check for all employers to ensure that this box is completed by the new hire"

72 Form I 9 Changes January 2017 The employer representative verifying employment eligibility must be in the physical presence of the person being verified and must also see the original documents being presented A dedicated area for including additional information rather than having to add it in the margins has been made available The revised Form I 9 is also easier to complete on a computer 143 Form I 9 Changes September 2017 New form will be required to be used dated 07/17/2017 form and instructions

73 Form I 9 Changes 2017 There are now three ways for users to complete the Form I 9: Print it and fill it out manually, pen to paper Fill it out electronically, then print and sign it Take note that using the online "smart" version of the form does not qualify as a compliant electronic I 9 If the online fillable version is used, it must be printed and signed pen to paper Use an electronic I 9 vendor 145 The Scoop Upcoming Dates October 18 November 1 December 13, 2017 Held at 8:00 am and 12:00 pm Central time

74 Up Coming Webinars node field seminardate/month New Partnership Audit Rules October 19 Farm Expenses October 24, 2017 Farm Income October 26, The Schedule is Finalized for the 44th Annual Federal Income Tax Schools November 2 3, 2017 Maquoketa, Iowa Centerstone Inn and Suites November 6 7, 2017 Le Mars, Iowa Le Mars Convention Center November 8 9, 2017 Atlantic, Iowa Cass County Community Center November 9 10, 2017 Mason City, Iowa North Iowa Area Community College November 16 17, 2017 Ottumwa, Iowa Indian Hills Community College November 20 21, 2017 Waterloo, Iowa Hawkeye Community College December 11 12, 2017 Ames, Iowa and Live Webinar Quality Inn and Suites 74

75 The CALT Staff William Edwards Interim Director for the Beginning Farmer Center Interim Director for the Center for Agricultural Law and Taxation Heady 518 Farm House Ln Ames. Iowa Kristine A. Tidgren Assistant Director E mail: ktidgren@iastate.edu Phone: (515) Fax: (515) The CALT Staff Kristy S. Maitre Tax Specialist E mail: ksmaitre@iastate.edu Phone: (515) Fax: (515) Tiffany L. Kayser Program Administrator E mail: tlkayser@iastate.edu Phone: (515) Fax: (515)

76 Depreciation Rev. Proc Amendments related to PATH Act related to: Expensing section 179 property Additional first year depreciation deduction 168(k) Qualified Indian reservation property depreciation provision 168(j) 151 Summary of Changes Made permanent the permission granted to revoke without the consent of the Commissioner of Internal Revenue any election made under 179 applies to any year after 2014 Allowing certain air conditioning or heating units to be eligible as 179 property per 179(d)(1) The procedure clarifies the kinds of air conditioning and heating units that qualify for expensing under 179 Two categories of units are identified: 1245 property, such as portable window air conditioners or plug in heaters HVAC components that are qualified real property under 179(f)(2) and components identified by the revenue procedure include motors, compressors, pipes and ducts

77 Air Conditioning Units Qualifying as 179 Property Rev. Proc clarifies that, in addition to portable air conditioning or heating units meeting the requirements to be classified as 179 property, if a component of a central air conditioning or heating system meets the definition of qualified real property and the component is placed in service by the taxpayer in a taxable year beginning after 2015, the component may qualify as 179 property if the taxpayer elects to apply 179(f) Qualified real property includes qualified leasehold improvement property, qualified restaurant property, and qualified retail improvement property 153 Air Conditioning Units Qualifying as 179 Property Allows certain air conditioning or heating units to be eligible as 179 property under 179(d)(1) Portable air conditioners, such as window air conditioning units Portable heaters, such as portable plug in unit heaters Placed in service by the taxpayer in a taxable year beginning after 2015 An example of an air conditioning or heating unit that will not qualify as 179 property is any component of a central air conditioning or heating system of a building, including motors, compressors, pipes, and ducts, whether the 154 component is in, on, or adjacent to a building 77

78 Revoke or Amend 179 Election The law made permanent the permission granted under 179(c)(2) to revoke without consent of the Commissioner of Internal Revenue any election made under 179 and any specification contained in that election 155 Extending the Placed in Service Date for Property to Qualify for the Additional First Year Depreciation Rev. Proc amends the placed in service date for property to qualify for the additional first year depreciation deduction Qualified property includes property acquired by the taxpayer before January 1, 2020, or acquired pursuant to a written contract entered into before January 1, 2020, assuming all other requirements are met The term first placed in service means the first time the building is placed in service by any person A building is first placed in service when first placed in a condition or state of readiness and availability for a specifically assigned function, whether in a trade or business, in the production of income, in a tax exempt activity, or in a personal activity

79 Modifying the Definition of Qualified Property under 168(k)(2) 168(k)(3) defines the term qualified improvement property to include: Any improvement to an interior portion of a building that is nonresidential real property if the improvement is placed in service after the date the building was first placed in service 157 Modifying the Definition of Qualified Property under 168(k)(2) However, qualified improvement property does not include any improvement attributable to the: Enlargement of the building Any elevator or escalator, or Internal structural framework of the building

80 Qualified Improvement Property Example In 2010, Thomas places in service a new office building In February 2016, Thomas sells this office building to John at fair market value John uses the office building in its trade or business In March 2016, John begins to construct improvements to the interior portion of the office building and places the improvements in service in December Qualified Improvement Property Example Because the office building was first placed in service in 2010 and the improvements made by John to the interior portion of the office building are placed in service after that date, the improvements that are 1250 property are qualified improvement property Assuming all other requirements in 168(k)(3) and 1.168(k) 1(c) are met

81 Qualified Improvement Property Example 2 In 2015, Thomas Textiles, a corporation and manufacturer, enters into a written contract with Xander for them to construct a new building for use in its trade or business The building will house a manufacturing operation and office space The initial construction plans did not include a private restroom for the owner of Thomas Textiles 161 Qualified Improvement Property Example 2 During the construction of the building, Thomas Textiles enters into a written contract with Build a Space to construct a private restroom in the new building for the owner On May 27, 2016, Thomas Textiles places in service the building, except for the private restroom On May 28, 2016, the private restroom in the building for the owner is placed in service

82 Qualified Improvement Property Example 2 Because the building is first placed in service on May 27, 2016, and the private restroom is placed in service on May 28, 2016, the assets in the private restroom that are 1250 property are qualified improvement property Assuming all other requirements in 168(k)(3) and 1.168(k) 1(c), are met 163 AMT Issues History Since 2008, an election has been available to forgo bonus depreciation in favor of accelerating a portion of AMT credits The portion of bonus depreciation that can be converted into accelerated AMT credits before any AMT based limits is 20% of the excess additional first year depreciation allowed by bonus depreciation over the depreciation allowed without regard to available bonus depreciation for eligible property

83 AMT The amount that would be allowed without bonus depreciation is determined using modified accelerated cost recovery system (MACRS) rules But, the election itself requires the use of the straight line method in determining the current year depreciation deduction for property to which the election applies 165 AMT The election applies to all property eligible for bonus depreciation that is placed in service in the year of the election and controls the depreciation method for all future years with respect to that property Taxpayers can make the election annually with respect to property placed in service each year and are not bound by a prior year election This is different than under the prior law, where once an election was made, it applied to all property placed in service in the year of the election and property placed in service in future years

84 AMT Example A taxpayer places into service $100 of five year property that is otherwise eligible for bonus depreciation The amount that would be deducted in the first year is $60, equal to $50 of bonus depreciation plus $10 of firstyear depreciation on the remaining $50 of depreciable basis (MACRS depreciation using a five year life and a half year convention) The amount that would be deducted without bonus depreciation in the first year is $ AMT Example Cont d The excess additional first year depreciation allowed by bonus depreciation is $40 (the difference between $60 and $20 not the available $50 of bonus depreciation), and the amount that can be converted into accelerated AMT credits is $8 (20% of $40)

85 AMT Accelerated AMT credits are used first to reduce the current year tax liability including minimum tax Excess credits accelerated by this election are refundable Unfortunately, to the extent a refund payment is attributable to a refund of prior year minimum tax, it is subject to payment reductions under the budget sequestration requirements The sequestration reduction rate for these refund payments processed from Oct. 1, 2016, through Sept. 30, 2017, will be 6.9% regardless of the period of the claim or when a return was received 169 Other Changes AMT Extending and modifying the election under 168(k)(4) to increase the alternative minimum tax (AMT) credit limitation in lieu of the additional first year depreciation deduction With regard to adjustments to AMT, Rev. Proc states that if a calendar year taxpayer elects out of bonus depreciation for a class of property that is qualified property placed in service in 2016, there is no AMT adjustment under 56 for that property For fiscal year filers, the depreciation adjustments under 56 apply to property placed in service in 2015 to which the election applies; however the deprecation adjustments under 56 do not apply to such property placed in service in

86 Plants Bearing Fruits and Nuts 171 Plants Bearing Fruits and Nuts The new law added 168(k)(5), which allows a taxpayer to elect to deduct the additional first year depreciation for certain plants bearing fruits and nuts before such plants are placed in service Planted or grafted by the taxpayer during the taxable year for which the election is made If a taxpayer makes the election for a specified plant, (i) The additional first year depreciation deduction is allowed for that specified plant for regular tax and alternative minimum tax purposes for the taxable year in which the specified plant is planted or grafted by the taxpayer

87 Plants Bearing Fruits and Nuts You can elect to claim 50% special depreciation allowance for the adjusted basis of certain specified plants (defined later) bearing fruits and nuts planted or grafted after December 31, 2015, and before January 1, 2020, in the ordinary course of a farming business (as defined in section 263A(e)(4)) 173 A Specified Plant is: Any tree or vine that bears fruits or nuts, and Any other plant that will have more than one yield of fruits or nuts and generally has a pre productive period of more than 2 years from planting or grafting to the time it begins bearing fruits or nuts Any property planted or grafted outside the United States does not qualify as a specified plant If the client elects to claim the special depreciation allowance for any specified plant, the special depreciation allowance applies only for the tax year in which the plant is planted or grafted

88 Plants Bearing Fruits and Nuts The plant will not be treated as qualified property eligible for the special depreciation allowance in the subsequent tax year in which it is placed in service To make the election, attach a statement to the timely filed return (including extensions) for the tax year in which the client planted or grafted the specified plant(s) Indicate the election to apply 168(k)(5) and identify the specified plant(s) for which they are making the election The election once made cannot be revoked without IRS consent 175 Other Changes Plant Bearing Fruits and Nuts 263A does not apply to any amount deducted under this election The election must be made in the manner prescribed on Form 4562, Depreciation and Amortization, and its instructions

89 Other Changes Plant Bearing Fruits and Nuts Deemed election Not timely Applies to a taxpayer that did not make the election for a specified plant planted or grafted by the taxpayer after December 31, 2015, on its timely filed Federal tax return for its taxable year beginning in 2015 and ending in 2016 or its taxable year of less than 12 months beginning and ending in Other Changes Plant Bearing Fruits and Nuts The taxpayer will be treated as making the election for that specified plant if the taxpayer: (A) On that return, deducted the 50 percent additional first year depreciation for that specified plant; and (B) Did not revoke the deemed election within the time and in the manner provided

90 Other Changes Plant Bearing Fruits and Nuts Automatic 6 month extension If a taxpayer made the election for a specified plant, an automatic extension of 6 months is granted to revoke that election, provided the taxpayer timely filed the taxpayer s Federal tax return for that taxable year and, within this 6 month extension period The taxpayer, and all taxpayers whose tax liability would be affected also files an amended Federal tax return for that taxable year in a manner that is consistent with the revocation of the election 179 Other Changes Plant Bearing Fruits and Nuts Interaction with 179 If a taxpayer makes the election for a specified plant, the adjusted basis of that specified plant is reduced by the amount of the additional first year depreciation deduction allowed or allowable The remaining adjusted basis is the cost of the specified plant for purposes of

91 Other Changes Adding 168(k)(6), which provides a phase down of the additional first year depreciation deduction percentage for future tax years Regarding the phase down of bonus depreciation the revenue procedure provides tables, including one that outlines the special basis rules applicable to certain property with longer production periods, and certain aircraft 181 Phase Down of Bonus Depreciation

Checkpoint Special Study: Tax Provisions in the 2017 Disaster Tax Relief Bill

Checkpoint Special Study: Tax Provisions in the 2017 Disaster Tax Relief Bill On September 29, President Trump signed into law P.L. 115-63, the Disaster Tax Relief and Airport and Airway Extension Act

Checkpoint Special Study: Tax Provisions in the 2017 Disaster Tax Relief Bill On September 29, President Trump signed into law P.L. 115-63, the Disaster Tax Relief and Airport and Airway Extension Act

News. Bipartisan Budget Act of 2018

News Release Date: 2/12/18 Bipartisan Budget Act of 2018 Cross References H.R. 1892 On February 9, 2018, the President signed into law H.R. 1892, the Bipartisan Budget Act of 2018, which extends federal

News Release Date: 2/12/18 Bipartisan Budget Act of 2018 Cross References H.R. 1892 On February 9, 2018, the President signed into law H.R. 1892, the Bipartisan Budget Act of 2018, which extends federal

Casualty loss deductions, election to claim for previous year. Casualty loss deductions, limitations eased.

Dear Client: If you suffered a loss as a result of Hurricane Harvey, you may be able to recoup a portion of that loss through several different tax benefits that may be available to you. These include

Dear Client: If you suffered a loss as a result of Hurricane Harvey, you may be able to recoup a portion of that loss through several different tax benefits that may be available to you. These include

Summary of Tax Provisions in Bipartisan Budget Act of 2018

Page: 1 of 8 Summary of Tax Provisions in Bipartisan Budget Act of 2018 DIVISION B DISASTER RELIEF SUBDIVISION 2 TAX RELIEF AND MEDICAID CHANGES RELATING TO CERTAIN DISASTERS TITLE I CALIFORNIA FIRES Sec.

Page: 1 of 8 Summary of Tax Provisions in Bipartisan Budget Act of 2018 DIVISION B DISASTER RELIEF SUBDIVISION 2 TAX RELIEF AND MEDICAID CHANGES RELATING TO CERTAIN DISASTERS TITLE I CALIFORNIA FIRES Sec.

List of Expiring Federal Tax Provisions

List of Expiring Federal Tax Provisions 2016-2025 LIST OF EXPIRING FEDERAL TAX PROVISIONS 2016-2025 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2016 JCX-1-16 CONTENTS Page INTRODUCTION...1

List of Expiring Federal Tax Provisions 2016-2025 LIST OF EXPIRING FEDERAL TAX PROVISIONS 2016-2025 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2016 JCX-1-16 CONTENTS Page INTRODUCTION...1

SECTION-BY-SECTION SUMMARY OF H.R. 5771, THE TAX INCREASE PREVENTION ACT OF 2014

1 SECTION-BY-SECTION SUMMARY OF H.R. 5771, THE TAX INCREASE PREVENTION ACT OF 2014 H.R. 5771 would extend, for one year (generally through the end of 2014), a number of tax relief provisions that expired

1 SECTION-BY-SECTION SUMMARY OF H.R. 5771, THE TAX INCREASE PREVENTION ACT OF 2014 H.R. 5771 would extend, for one year (generally through the end of 2014), a number of tax relief provisions that expired

SUMMARY OF THE TAX EXTENDERS AGREEMENT DIVISION D REVENUE MEASURES TITLE I EXTENSION OF EXPIRING PROVISIONS

SUMMARY OF THE TAX EXTENDERS AGREEMENT DIVISION D REVENUE MEASURES TITLE I EXTENSION OF EXPIRING PROVISIONS Subtitle A Tax Relief for Families and Individuals Section 40201. Extension and modification

SUMMARY OF THE TAX EXTENDERS AGREEMENT DIVISION D REVENUE MEASURES TITLE I EXTENSION OF EXPIRING PROVISIONS Subtitle A Tax Relief for Families and Individuals Section 40201. Extension and modification

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

SUMMARY PLAN DESCRIPTION. Equinix, Inc. 401(k) Plan

Plan") SUMMARY PLAN DESCRIPTION Equinix, Inc. 401(k) Plan Equinix, Inc. 401(k) Plan Equinix, Inc. 401(k) Plan SUMMARY PLAN DESCRIPTION...1 I. BASIC PLAN INFORMATION...2 A. ACCOUNT...2 B. BENEFICIARY...2 C. DEFERRAL

SUMMARY PLAN DESCRIPTION Equinix, Inc. 401(k) Plan Equinix, Inc. 401(k) Plan Equinix, Inc. 401(k) Plan SUMMARY PLAN DESCRIPTION...1 I. BASIC PLAN INFORMATION...2 A. ACCOUNT...2 B. BENEFICIARY...2 C. DEFERRAL

2017 Year-End Income Tax Planning for Individuals December 2017

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

The American Taxpayer Relief Act of 2012

The American Taxpayer Relief Act of 2012 January 2013 kpmg.com The American Taxpayer Relief Act of 2012 President Obama on January 2, 2013, signed the American Tax Relief Act of 2012 (Act) averting the

The American Taxpayer Relief Act of 2012 January 2013 kpmg.com The American Taxpayer Relief Act of 2012 President Obama on January 2, 2013, signed the American Tax Relief Act of 2012 (Act) averting the

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans Description Normal Loan Rules CA Wildfires Loans General Disaster Loans What types of loans are available? General purpose loans,

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans Description Normal Loan Rules CA Wildfires Loans General Disaster Loans What types of loans are available? General purpose loans,

NEW LEGISLATION INDIVIDUAL

NEW LEGISLATION INDIVIDUAL 1 Land Grant University Tax Education Foundation Tax Rates.............................. 2 Inflation Adjustments Based on Chained CPI...................... 4 Increase in and

NEW LEGISLATION INDIVIDUAL 1 Land Grant University Tax Education Foundation Tax Rates.............................. 2 Inflation Adjustments Based on Chained CPI...................... 4 Increase in and

Highlights of 2017 Tax Law Changes

Highlights of 2017 Tax Law Changes Steve Ingraham 10/23/2017 Due Date Returns and payments otherwise due April 15, 2018, are timely if filed or paid by Tuesday, April 17, 2018 Expired Provisions Tuition

Highlights of 2017 Tax Law Changes Steve Ingraham 10/23/2017 Due Date Returns and payments otherwise due April 15, 2018, are timely if filed or paid by Tuesday, April 17, 2018 Expired Provisions Tuition

1. a demand loan where interest is payable on the loan at a rate less than the applicable federal rate [IRC Sec. 7872(e)(1)(A)], or

![1. a demand loan where interest is payable on the loan at a rate less than the applicable federal rate [IRC Sec. 7872(e)(1)(A)], or](/thumbs/88/117035883.jpg "1. a demand loan where interest is payable on the loan at a rate less than the applicable federal rate [IRC Sec. 7872(e)(1)(A)], or") 990 2/18 15-9 Example 15B-1 Related party interest. Forney First, Inc. (FFI), an accrual basis organization exempt under IRC Sec. 501(c)(3), provides food and shelter to needy families in Forney. FFI augments

990 2/18 15-9 Example 15B-1 Related party interest. Forney First, Inc. (FFI), an accrual basis organization exempt under IRC Sec. 501(c)(3), provides food and shelter to needy families in Forney. FFI augments

THE TAXATION OF INDIVIDUALS AND FAMILIES

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA

Traditional IRA Roth IRA") GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company