"CPA for NGO" social responsibility programme Planning, Budgeting and Forecasting

|

|

|

- Amos Stevenson

- 5 years ago

- Views:

Transcription

1 Presented by : Annie WONG Finance Manager, Baptist Oi Kwan Social Service Date: 6 July 2018 "CPA for NGO" social responsibility programme Planning, Budgeting and Forecasting

2 Content 1. Relationship between Planning, Budgeting and Forecasting 2. Planning 3. Budgeting 4. Forecasting 5. Roles of Directors in Budgeting process 1

3 Relationship between Planning, Budgeting and Forecasting 2

4 Relationship between Planning, Budgeting and Forecasting Each organization has its own Vision & Mission. Vision & mission, social needs, resources, Government policies and results from SWOT analysis shape up the strategic plan of an organization. Long-term plans and annual plan are derived from strategic plan of the organization. Budget is the annual plan expressed in figures. 3

5 Relationship between Planning, Budgeting and Forecasting By incorporate the year-to-date actual results to the budget figures generate a more realistic estimation for the year. Rolling forecast Continuously updated the forecast by adding a further accounting period when the earliest accounting period has expired. Results from forecast or rolling forecast may initiate amendments to the long-term plan. 4

6 Planning Strategic Plan Overall long-range goals and objectives of the organization Direction and financial objectives Both qualitative and quantitative e.g. operate youth centers in Hong Kong, Kowloon & New Territories 5

7 Planning Long-term Plan From 3 to 5 years, sometimes up to 10 years. Derive from strategic plan Attainable targets for a specific time period Need to revise if internal and/or external conditions changed. e.g. start up youth centers in Kowloon East district 6

8 Planning Annual Plan 1 st year of the long-term plan More detailed plans for different services, units and departments. Both operational and financial plans Fulfill requirements of Government & donors 7

9 Planning Annual Plan Look for different resources, including financial, human resource, technical, etc. Review and monitoring 8

10 Objectives: Quantify operational plans & targets Provide expected outcomes Functions: Planning Co-ordination Communication Control & evaluation 9

11 Functions Planning Define targets at different levels Provides specific deadlines for service units/departments to achieve their objectives Expected outcomes of units/departments contribute towards an organization s overall objectives 10

12 Functions Co-ordination Identify the strengths and weaknesses of the organization Set priorities for organization s objectives Better resources allocation to various units/departments Restrain the empire-building situation 11

13 Functions Communication All staff at different levels should be informed about the objectives, targets, programmes and timelines. I/Cs and managers should be informed of the resources available to achieve their targets. 12

14 Functions Control & evaluation During budget preparation, units submit estimates as they require, should include justifications of their needs. After budgets have been reviewed (amended if necessary) and approved by the Board, the final budgets become targets of all units. 13

15 Functions Control & evaluation A comparison of actual and budget results should be prepared periodically for performance evaluation. Deviations from budget ought to be identify as soon as possible, reasons of deviations should also be identified. 14

16 Functions Control & evaluation Rectification actions should be carried out in order to bring the operations back to the right track. Budgets are the basis of performance evaluation as they are the realistic estimates of expected performance. 15

17 Top-down approach Top management prepares the budget and passes it on to the service units/departments for implementation. Top management may take inputs from units/departments for the preparation of budget. 16

18 Top-down approach Top management is expected to realize the current social needs, the history and the strength of the organization. Service units/departments have less or no participation in the budgeting process. 17

19 Bottom-up approach Service units/departments prepared their budgets according to allocated resources, e.g. SWD LSG subvented units. Service units/departments prepared their budgets according to their operational plans, e.g. Self-financed restaurant. 18

20 Bottom-up approach All service units/departments submit their budgets to Finance Department for the compilation the entire budget. HR Department may required to verify the staff cost of the units/departments. 19

21 Bottom-up approach Finance Department submit the entire budget to CEO/Budget Committee for comments. If CEO/Budget Committee has queries, units/departments require to provide further information. 20

22 Bottom-up approach The entire budget then submitted to Board for approval. Service units/departments should be more committed to the budget as they have participated in the budgeting process. 21

23 Discussion question 1 What are the pros and cons of (1)Top-down approach budgeting? (2)Bottom-up approach budgeting? 22

24 Incremental Budgeting Assume all income and expense items exist in the budget year. Use current year s amount as foundation, add incremental % or amount to the budget period. 23

25 Incremental Budgeting For each income/expense item: Current year actual amount $ x + inflation a +/- other factors b Next year budget amount y Other factors examples:- Income > student numbers, sales volume Expenses > staff numbers, rates concession 24

26 Zero-based Budgeting (ZBB) All items reset to zero for the budget year, no reference to past years data. All income and expense items in the budget must supported by justification. Require more effort to analyze and prioritize activities and expenditures. 25

27 Zero-based Budgeting (ZBB) Avoid automatic budget increases (usually for expense items). Eliminate un-necessary cost, better allocation of resources. 26

28 Activity-based Budgeting (ABB) Require to identify cost drivers of the activities Variable cost vs Fixed cost Usually adopted in sales or production budgets More focus on cost savings 27

29 Rolling Budget During the year, the actual income and expenses amount of each month will be inserted to the budget template (replace the budget amount) after the month end process completed. Expect to provide more accurate estimation. 28

30 Rolling Budget Estimation would be accurate only if the organization prepare the monthly account using accrual basis. 29

31 Basic steps of budgeting process 1) Define objectives and targets of the budget year, breakdown in service and unit level if necessary. 2) Construct the budget calendar Allow sufficient time for service units/departments to collect data and prepare the budget. 30

32 Basic steps of budgeting process 2) Construct the budget calendar Allow sufficient time for management to review the combined budget. The combined budget should be approved by the Board before the budget year start. 31

33 Basic steps of budgeting process 3) Update budget assumptions Inflation rate, % increment of utilities, salary increment 4) Update available funding/subsidies amount to concerned service units/departments. e.g. LSG subvention, Community Chest funding, Lotteries Fund income, etc. 32

34 Basic steps of budgeting process 5) Service units/departments prepare their budgets. 6) Service units/departments submit their budgets to Finance Department for compilation of the 1 st draft combined budget. 7) CE review the 1 st draft combined budget and discuss with top management. 33

35 Basic steps of budgeting process 8) Service units/departments revise their budgets if necessary, then re-submit their budgets to Finance Department for compilation of the final combined budget. 9) Final combined budget submit to the Board for discussion and approval. 34

36 Budgetary control Prepare actual vs budget comparison reports periodically for management review. Any deviations should be rectified as soon as possible. If significant events occur, management may consider to revise the budgets to reflect the more realistic situation. 35

37 Limitation of Budgeting Budgeting, like planning, is based on assumptions and estimation, may not be 100% accurate. Success and fulfillment of budgets depend on the co-operation and participation of staff of all levels. 36

38 Limitation of Budgeting Budget is a means to provide detailed information, convert objectives into figures which may help in achieving the organization s objectives. Budget is only a tool, does not take over the position and functions of management. 37

39 Limitation of Budgeting Excessive emphasis on budgeting may cause lower level management and staff to provide inaccurate estimation on future income and expenses. Staff who have not involve in the budgeting process may not have ownership, may feel de-motivated. 38

40 Discussion question 2 Share with your group members of your agency s annual budgeting process. 39

41 Forecasting Functions of Forecasting More accurate financial estimation based on recent changes of internal and/or external factors/requirements. e.g. change in government policies, change in donor s requirements. Assists management to take immediate actions when conditions change 40

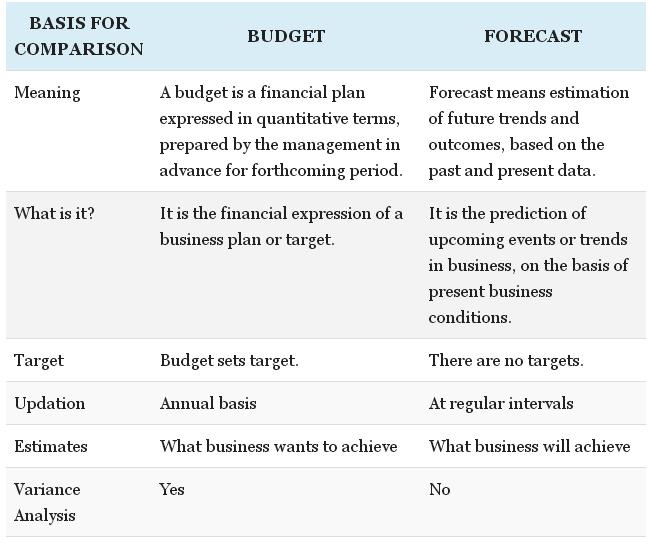

42 Forecasting Budget vs Forecast Budget operational plans and targets expressed in monetary terms for the coming year - what is expected 41

43 Forecasting Budget vs Forecast Forecast use actual operating results and current conditions to project the remaining periods performance for the year - what will happen 42

44 Source: 43

45 Board s Roles in Budgeting Process SWD LSG Manual (2016 Oct. version) (extract) 3.20 NGOs are advised to have annual financial budgeting at the beginning of each financial year. If they anticipate financial difficulty, their Board should have thorough deliberation and inform SWD in advance, so that remedial measures can be taken as appropriate before the NGOs exhaust their reserves. 44

46 Board s Roles in Budgeting Process SWD LSG Manual (2016 Oct. version) (extract) Role of NGO Boards/Management Committees 5.4 NGOs Boards and Management Committees are responsible for the governance of the NGO... In general, NGO Boards/Management Committees are tasked to: (a) set the mission and goals of the NGO (b) determine service delivery modes which meet the changing needs of the community; 45

47 Board s Roles in Budgeting Process SWD LSG Manual (2016 Oct. version) (extract) Role of NGO Boards/Management Committees (con d) 5.4 (d) assume responsibility for programme planning and budgeting, as well as for human resources management;. 46

48 Board s Roles in Budgeting Process Efficiency Unit Guide to Corporate Governance for Subvented Organsations (2015 June) (extract) Chapter 2 Board Structure and Composition BEST PRACTICES - Matters reserved for the board Business strategy Approval of strategy objectives and strategic plan Approval of proposals for major expansion or closures Approval of budgets Approval of priorities and performance indicators/ measures 47

49 Board s Roles in Budgeting Process ICAC Governance and Internal Control in Non- Governmental Organisations (extract) Chapter 2 Financial Management 3.3 Budgeting Produce at the beginning of each financial year a programme of activities and the budget for approval by the Board (or the Finance Committee, if one is established) and, if required, for information/ endorsement by the Government bureau or department concerned. 48

50 Reference materials Efficiency Unit Guide to Corporate Governance for Subvented Organsations (2015 June) ICAC Governance and Internal Control in Non- Governmental Organisations 49

51 Source: Planning, Budgeting and Forecasting-An eye on the future (KPMG) 50

52 Thank you! 51

Control: Actual results can be compared against the budget and action is taken as appropriate.

Understanding Budgeting Budgeting is a key aspect of management accounting and particularly impacts on the areas of planning, control and performance management. A budget is a quantitative plan prepared

Understanding Budgeting Budgeting is a key aspect of management accounting and particularly impacts on the areas of planning, control and performance management. A budget is a quantitative plan prepared

"CPAs for NGOs" social responsibility programme. Implications and interpretation of financial statements and auditor's report

Presented by: Jacky Lai, Partner, Assurance, Ernst & Young Date: 17 June 2016 "CPAs for NGOs" social responsibility programme Implications and interpretation of financial statements and auditor's report

Presented by: Jacky Lai, Partner, Assurance, Ernst & Young Date: 17 June 2016 "CPAs for NGOs" social responsibility programme Implications and interpretation of financial statements and auditor's report

BUDGETING, PLANNING & MANAGEMENT REPORTING

BUDGETING, PLANNING & MANAGEMENT REPORTING SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE This training course takes a practical approach to budgeting, planning and management

BUDGETING, PLANNING & MANAGEMENT REPORTING SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE This training course takes a practical approach to budgeting, planning and management

explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy

Budgeting Outcome By the end of this session you should be able to: explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy describe the factors which influence

Budgeting Outcome By the end of this session you should be able to: explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy describe the factors which influence

Review Criteria. Robotics Program. Reviewer SCORE SUMMARY. Extent of Need 25 Goals Objectives and Milestones

Proposal Lead Agency: Proposal Title: Review Criteria [Additional Information]: Robotics Program Reviewer Reviewer: Signature: Date: SCORE SUMMARY Section Maximum Score Extent of Need 25 Goals Objectives

Proposal Lead Agency: Proposal Title: Review Criteria [Additional Information]: Robotics Program Reviewer Reviewer: Signature: Date: SCORE SUMMARY Section Maximum Score Extent of Need 25 Goals Objectives

University of Alaska Performance Evaluation Guidelines

University of Alaska Performance Evaluation Guidelines Board of Regents April 8-9, 2008 Valdez, Alaska Prepared by Statewide Planning and Budget 450-8180 Table of Contents Performance Evaluation Guidelines...

University of Alaska Performance Evaluation Guidelines Board of Regents April 8-9, 2008 Valdez, Alaska Prepared by Statewide Planning and Budget 450-8180 Table of Contents Performance Evaluation Guidelines...

Fact Sheet 13 Roles and responsibilities in project partnerships

Roles and responsibilities in project partnerships Valid from Valid to Main changes Version 3 03.05.17 -Minor wording change recommending the use of the same FLC for local partnerships. -Clarified the

Roles and responsibilities in project partnerships Valid from Valid to Main changes Version 3 03.05.17 -Minor wording change recommending the use of the same FLC for local partnerships. -Clarified the

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 291 thereof,

L 244/12 COMMISSION IMPLEMTING REGULATION (EU) No 897/2014 of 18 August 2014 laying down specific provisions for the implementation of cross-border cooperation programmes financed under Regulation (EU)

L 244/12 COMMISSION IMPLEMTING REGULATION (EU) No 897/2014 of 18 August 2014 laying down specific provisions for the implementation of cross-border cooperation programmes financed under Regulation (EU)

AFGHANISTAN ALLOCATION GUIDELINES 22 JANUARY 2014

AFGHANISTAN ALLOCATION GUIDELINES 22 JANUARY 2014 I. Contents Introduction... 2 Purpose... 2 Scope... 2 Rationale... 2 Acronyms... 2 I. Funding Mechanisms... 3 A. Eligibility... 3 B. Standard Allocation...

AFGHANISTAN ALLOCATION GUIDELINES 22 JANUARY 2014 I. Contents Introduction... 2 Purpose... 2 Scope... 2 Rationale... 2 Acronyms... 2 I. Funding Mechanisms... 3 A. Eligibility... 3 B. Standard Allocation...

Kaduna State Government

Kaduna State Government Process Guidelines Ministry of Economic September, 2013 Table of Contents Abbreviations and acronyms... 3 Section 1: Introduction... 4 1.1 Background... 4 Figure 1: State Level

Kaduna State Government Process Guidelines Ministry of Economic September, 2013 Table of Contents Abbreviations and acronyms... 3 Section 1: Introduction... 4 1.1 Background... 4 Figure 1: State Level

NEPAD/Spanish Fund for African Women s empowerment

NEPAD/Spanish Fund for African Women s empowerment Project Proposal Format Annex 0 1 P age Proposal Format Proposal Cover Page: PROPOSAL TO THE NEPAD- SPANISH FUND FOR AFRICAN WOMEN s EMPOWERMENT Organization

NEPAD/Spanish Fund for African Women s empowerment Project Proposal Format Annex 0 1 P age Proposal Format Proposal Cover Page: PROPOSAL TO THE NEPAD- SPANISH FUND FOR AFRICAN WOMEN s EMPOWERMENT Organization

Finance and Budget Modeling Town Hall. March 27 & 28, 2018

Finance and Budget Modeling Town Hall March 27 & 28, 2018 FINANCE AND BUDGET MODELING TASK FORCE Charge The Finance and Budget Modeling Task Force will create a new budget model that is transparent, data-driven,

Finance and Budget Modeling Town Hall March 27 & 28, 2018 FINANCE AND BUDGET MODELING TASK FORCE Charge The Finance and Budget Modeling Task Force will create a new budget model that is transparent, data-driven,

Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures

EBA/GL/2017/16 23/04/2018 Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures 1 Compliance and reporting obligations Status of these guidelines 1. This document contains

EBA/GL/2017/16 23/04/2018 Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures 1 Compliance and reporting obligations Status of these guidelines 1. This document contains

Risk assessment concept and practical guidance

Risk assessment concept and practical guidance FOR THE IMPLEMENTATION OF The EEA Financial Mechanism & The Norwegian Financial Mechanism 2004-2009 adopted by the EEA Financial Mechanism Committee and the

Risk assessment concept and practical guidance FOR THE IMPLEMENTATION OF The EEA Financial Mechanism & The Norwegian Financial Mechanism 2004-2009 adopted by the EEA Financial Mechanism Committee and the

Hers Institute Budgeting. This Session Will Include a Discussion of:

Hers Institute 2016 Budgeting This Session Will Include a Discussion of: The Purpose of the Budgeting Process Budget Types Approaches to Budgeting The Budget Process Why do we participate in the budget

Hers Institute 2016 Budgeting This Session Will Include a Discussion of: The Purpose of the Budgeting Process Budget Types Approaches to Budgeting The Budget Process Why do we participate in the budget

STRATEGIC PLANNING PROCESS (2017) 1.1 The Association s strategic planning framework consists of the preparation of the following documents;

1.1 The Association s strategic planning framework consists of the preparation of the following documents;") 1.0 INTRODUCTION STRATEGIC PLANNING PROCESS (2017) 1.1 The Association s strategic planning framework consists of the preparation of the following documents; Corporate Management Plan Departmental Service

1.0 INTRODUCTION STRATEGIC PLANNING PROCESS (2017) 1.1 The Association s strategic planning framework consists of the preparation of the following documents; Corporate Management Plan Departmental Service

4 Planning, Budgeting, and Institutional Effectiveness

4 Planning, Budgeting, and Institutional Effectiveness Approved by Executive Council 10-11-2016 Updated 11-15-15 Approved by Executive Council 04-16-2013 INTRODUCTION Lurleen B. Wallace Community College

4 Planning, Budgeting, and Institutional Effectiveness Approved by Executive Council 10-11-2016 Updated 11-15-15 Approved by Executive Council 04-16-2013 INTRODUCTION Lurleen B. Wallace Community College

Alternatives Development, Project Justification, and Financial Realities Financial Considerations

Alternatives Development, Project Justification, and Financial Realities Financial Considerations Joe Hebert Manager, Financial Analysis and PFC Branch, FAA Office of Airports joe.hebert@faa.gov 1 Overview

Alternatives Development, Project Justification, and Financial Realities Financial Considerations Joe Hebert Manager, Financial Analysis and PFC Branch, FAA Office of Airports joe.hebert@faa.gov 1 Overview

CIMA defines planning as the establishment of objectives, and the formulation,

Chapter 8 Solutions Solution 8.1 a) Outline the main objectives of budgetary planning CIMA defines planning as the establishment of objectives, and the formulation, evaluation and selection of the policies,

Chapter 8 Solutions Solution 8.1 a) Outline the main objectives of budgetary planning CIMA defines planning as the establishment of objectives, and the formulation, evaluation and selection of the policies,

PART 7: OVERVIEW ON PROJECT IMPLEMENTATION PRINCIPLES

Applicants Manual for the period 2014-2020 Version 1.1 PART 7: OVERVIEW ON PROJECT IMPLEMENTATION PRINCIPLES edited by the Managing Authority/Joint Secretariat Budapest, Hungary, 2015 Applicants Manual

Applicants Manual for the period 2014-2020 Version 1.1 PART 7: OVERVIEW ON PROJECT IMPLEMENTATION PRINCIPLES edited by the Managing Authority/Joint Secretariat Budapest, Hungary, 2015 Applicants Manual

Guidance for Member States on Integrated Sustainable Urban Development (Article 7 ERDF Regulation)

") EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on Integrated Sustainable Urban Development (Article 7 ERDF Regulation) p10 addition of 3 bullet points for specific

EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on Integrated Sustainable Urban Development (Article 7 ERDF Regulation) p10 addition of 3 bullet points for specific

GUIDANCE REGARDING DUE DILIGENCE IN RESPECT OF MULTI ACADEMY COMPANIES (MACs)

") GUIDANCE REGARDING DUE DILIGENCE IN RESPECT OF MULTI ACADEMY COMPANIES (MACs) DUE DILIGENCE IN RELATION TO MULTI ACADEMY COMPANIES (MACs) WHAT IS DUE DILIGENCE? A fair translation of due diligence is an

GUIDANCE REGARDING DUE DILIGENCE IN RESPECT OF MULTI ACADEMY COMPANIES (MACs) DUE DILIGENCE IN RELATION TO MULTI ACADEMY COMPANIES (MACs) WHAT IS DUE DILIGENCE? A fair translation of due diligence is an

Integrated Planning, Monitoring and Reporting

1. Purpose This procedure describes the integrated planning, monitoring and ing cycle of the European Chemicals Agency, including the preparation of the Single Programming Document (SPD). This procedure

1. Purpose This procedure describes the integrated planning, monitoring and ing cycle of the European Chemicals Agency, including the preparation of the Single Programming Document (SPD). This procedure

MANAGING YOUR EO BUDGET BEFORE IT MANAGES YOU. Brian Yacker, JD/CPA Stacey Bergman, CPA

MANAGING YOUR EO BUDGET BEFORE IT MANAGES YOU Brian Yacker, JD/CPA Stacey Bergman, CPA August 18, 2015 1. WHAT IS A BUDGET? DEFINITION Strategic organizational plan Based on facts, events in progress &

MANAGING YOUR EO BUDGET BEFORE IT MANAGES YOU Brian Yacker, JD/CPA Stacey Bergman, CPA August 18, 2015 1. WHAT IS A BUDGET? DEFINITION Strategic organizational plan Based on facts, events in progress &

Financial Essentials for Nonprofit. Managers

Financial Essentials for Nonprofit Chapter 1: Managers What Every Nonprofit Manager Should Know About Accounting and Finance 1. Recognize financing options available to nonprofit organizations. 2. Identify

Financial Essentials for Nonprofit Chapter 1: Managers What Every Nonprofit Manager Should Know About Accounting and Finance 1. Recognize financing options available to nonprofit organizations. 2. Identify

MODULE 4 PLANNING AND CONTROL

MODULE 4 PLANNING AND CONTROL OUTLINES The purpose of budgetary control system Alternative approaches to budgeting, including incremental budgeting, Zero-based budgeting, Activity-based budgeting, rolling

MODULE 4 PLANNING AND CONTROL OUTLINES The purpose of budgetary control system Alternative approaches to budgeting, including incremental budgeting, Zero-based budgeting, Activity-based budgeting, rolling

JITS funding guide. JITS Network Secretariat. 08 January Version 3

JITS funding guide JITS Network Secretariat 08 January 2018 Version 3 Table of Contents I. Background... 2 II. Scope and conditions... 2 II.1. Travel and accommodation... 4 II.2. Interpretation and translation...

JITS funding guide JITS Network Secretariat 08 January 2018 Version 3 Table of Contents I. Background... 2 II. Scope and conditions... 2 II.1. Travel and accommodation... 4 II.2. Interpretation and translation...

South Sudan Common Humanitarian Fund (South Sudan CHF) Terms of Reference (TOR)

Terms of Reference (TOR)") South Sudan Common Humanitarian Fund (South Sudan CHF) Terms of Reference (TOR) 14 February 2012 List of Acronyms AA Administrative Agent AB Advisory Board CAP Consolidated Appeal Process CHF Common Humanitarian

South Sudan Common Humanitarian Fund (South Sudan CHF) Terms of Reference (TOR) 14 February 2012 List of Acronyms AA Administrative Agent AB Advisory Board CAP Consolidated Appeal Process CHF Common Humanitarian

PEFA Training. Dakar, Senegal January & February 1, #PEFA. PEFA Secretariat

www.pefa.org #PEFA PEFA Training Dakar, Senegal January 30-31 & February 1, 2019 PEFA Secretariat Improving public financial management. Supporting sustainable development. INTRODUCTION Introductions Participant

www.pefa.org #PEFA PEFA Training Dakar, Senegal January 30-31 & February 1, 2019 PEFA Secretariat Improving public financial management. Supporting sustainable development. INTRODUCTION Introductions Participant

PLANNING, BUDGETING AND FORECASTING 101 SEPTEMBER / NOVEMBER CFU LESSON 1

PLANNING, BUDGETING AND FORECASTING 101 SEPTEMBER / NOVEMBER 2018-6 CFU LESSON 1 ICE BREAKER TWO TRUTHS AND A LIE 2 COURSE INTRODUCTION One of the natural job opportunities of the Business Administration

PLANNING, BUDGETING AND FORECASTING 101 SEPTEMBER / NOVEMBER 2018-6 CFU LESSON 1 ICE BREAKER TWO TRUTHS AND A LIE 2 COURSE INTRODUCTION One of the natural job opportunities of the Business Administration

Strategic Planning, Forecasting & Budgeting

Strategic Planning, Forecasting & Budgeting Overview Many organisations use budgeting and forecasting as a means of providing and updating tactical operating plans and controlling costs; but world class

Strategic Planning, Forecasting & Budgeting Overview Many organisations use budgeting and forecasting as a means of providing and updating tactical operating plans and controlling costs; but world class

Management Accountant

Position Description Management Accountant Finance Business Unit 1 Position Description Management Accountant Context Lincoln University is New Zealand s specialist land-based university, with a mission

Position Description Management Accountant Finance Business Unit 1 Position Description Management Accountant Context Lincoln University is New Zealand s specialist land-based university, with a mission

UNDP Initiation Plan to programme the project preparation grant received from the GEF. (otherwise called GEF PPG)

") UNDP Initiation Plan to programme the project preparation grant received from the GEF (otherwise called GEF PPG) effective for all PIFs approved as of GEF November work programme 2017 A. Background: The

UNDP Initiation Plan to programme the project preparation grant received from the GEF (otherwise called GEF PPG) effective for all PIFs approved as of GEF November work programme 2017 A. Background: The

New Campus Budget Model

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

New Campus Budget Model Moving to an All Funds Model May 25, 2016 Presented By: Nancy Warter-Perez Chair of the Academic Senate Peter McAllister Dean, College of Arts and Letters Lisa Chavez Vice President

SIU Management and Monitoring System PROGRESS REPORT USER MANUAL PART 2

SIU Management and Monitoring System PROGRESS REPORT USER MANUAL PART 2 Version 1.0 of 14 August 2018 European Regional Development Fund www.italy-croatia.eu TABLE OF CONTENTS INTRODUCTION... 2 4.4.2 SECTION

SIU Management and Monitoring System PROGRESS REPORT USER MANUAL PART 2 Version 1.0 of 14 August 2018 European Regional Development Fund www.italy-croatia.eu TABLE OF CONTENTS INTRODUCTION... 2 4.4.2 SECTION

Office of the Academic Senate One Washington Square San Jose, California Fax:

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 At its meeting of February 25, 2002, the Academic

A campus of The California State University Office of the Academic Senate One Washington Square San Jose, California 95192-0024 408-924-2440 Fax: 408-924-2451 At its meeting of February 25, 2002, the Academic

FINANCIAL ANALYSIS, PLANNING & CONTROLLING BUDGETS SECTOR / FINANCE

FINANCIAL ANALYSIS, PLANNING & CONTROLLING BUDGETS SECTOR / FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE This 10-days training seminar brings together important areas of Financial Management, Planning

FINANCIAL ANALYSIS, PLANNING & CONTROLLING BUDGETS SECTOR / FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE This 10-days training seminar brings together important areas of Financial Management, Planning

University of Maine System and Component Units. Core Financial Ratios and Composite Financial Index. FY10 and FY11

University of Maine System Office of Finance and Treasurer January 2012 TABLE OF CONTENTS Page Introduction 1 Component Units 1 Primary Reserve Ratio 2 Net Operating Revenues Ratio 3 Return on Net Assets

University of Maine System Office of Finance and Treasurer January 2012 TABLE OF CONTENTS Page Introduction 1 Component Units 1 Primary Reserve Ratio 2 Net Operating Revenues Ratio 3 Return on Net Assets

ERC reporting in FP7. June Presenters: Bethan Jones Research Operations

ERC reporting in FP7 June 2014 Presenters: Bethan Jones Email: bethan.jones@admin.cam.ac.uk ERC Reporting Requirements Activity reports Completed at the mid-way and end point of the grant (usually months

ERC reporting in FP7 June 2014 Presenters: Bethan Jones Email: bethan.jones@admin.cam.ac.uk ERC Reporting Requirements Activity reports Completed at the mid-way and end point of the grant (usually months

New Mexico Highlands University Annual Operating Budget Process. approved Fall 2016

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

New Mexico Highlands University Annual Operating Budget Process approved Fall 2016 Appendix I added Spring 2017 2 Table of Contents Introduction... 3 NMHU Budget Values and the NMHU Strategic Plan... 4

North Orange County Community College District Integrated. Planning Manual March 2014 Update

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

2013 Integrated Planning Manual March 2014 Update 2013 Integrated Planning Manual NOCCCD Mission Statement The mission of the is to serve and enrich our diverse communities by providing a comprehensive

REPORT Regional Workshop Budgeting for Roma Integration Policies Skopje, March 2017

Roma Integration 2020 is co-funded by: European Union REPORT Regional Workshop Budgeting for Roma Integration Policies Skopje, 20-21 March 2017 Report prepared by: Merima Avdagić, Leading Consultant Zuhra

Roma Integration 2020 is co-funded by: European Union REPORT Regional Workshop Budgeting for Roma Integration Policies Skopje, 20-21 March 2017 Report prepared by: Merima Avdagić, Leading Consultant Zuhra

GUIDELINE FOR ASSESSMENT OF LOCAL GOVERNMENTS ON THE MINIMUM CONDITIONS AND PERFORMANCE MEASURES TO ACCESS THE LDG

February 2014 KINGDOM OF LESOTHO MINISTRY OF LOCAL GOVERNMENT, CHIEFTAINSHIP AND PARLIAMENTARY AFFAIRS GUIDELINE FOR ASSESSMENT OF LOCAL GOVERNMENTS ON THE MINIMUM CONDITIONS AND PERFORMANCE MEASURES TO

February 2014 KINGDOM OF LESOTHO MINISTRY OF LOCAL GOVERNMENT, CHIEFTAINSHIP AND PARLIAMENTARY AFFAIRS GUIDELINE FOR ASSESSMENT OF LOCAL GOVERNMENTS ON THE MINIMUM CONDITIONS AND PERFORMANCE MEASURES TO

EN 1 EN. Rural Development HANDBOOK ON COMMON MONITORING AND EVALUATION FRAMEWORK. Guidance document. September 2006

Rural Development 2007-2013 HANDBOOK ON COMMON MONITORING AND EVALUATION FRAMEWORK Guidance document September 2006 Directorate General for Agriculture and Rural Development EN 1 EN CONTENTS 1. A more

Rural Development 2007-2013 HANDBOOK ON COMMON MONITORING AND EVALUATION FRAMEWORK Guidance document September 2006 Directorate General for Agriculture and Rural Development EN 1 EN CONTENTS 1. A more

DoRIS User manual. December 2011 version 1.0

DoRIS User manual December 2011 version 1.0 1. Introduction... 3 2. Using DoRIS... 3 2.1 What is DoRIS?... 3 2.2 Release 1... 4 2.3 Who can see and do what?... 4 2.3 The Inbox... 4 2.4 The Country view...

DoRIS User manual December 2011 version 1.0 1. Introduction... 3 2. Using DoRIS... 3 2.1 What is DoRIS?... 3 2.2 Release 1... 4 2.3 Who can see and do what?... 4 2.3 The Inbox... 4 2.4 The Country view...

The School District of Clayton s Budget Planning Guide. Zero-Based Budgeting An Overview. Helpful Definitions

The s Zero-Based Budgeting An Overview Transition to Zero-Based Budgeting (ZBB) is a major outcome within the Resource Management theme of the District s strategic plan. It is not a budget reduction process.

The s Zero-Based Budgeting An Overview Transition to Zero-Based Budgeting (ZBB) is a major outcome within the Resource Management theme of the District s strategic plan. It is not a budget reduction process.

REPORT 2015/178 INTERNAL AUDIT DIVISION. Audit of the United Nations Human Settlements Programme Regional Office for Arab States

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

Economic and Social Council

UNITED NATIONS E Economic and Social Council Distr. GENERAL CEP/AC.13/2005/4/Rev.1 23 March 2005 ENGLISH/ FRENCH/ RUSSIAN ECONOMIC COMMISSION FOR EUROPE COMMITTEE ON ENVIRONMENTAL POLICY High-level Meeting

UNITED NATIONS E Economic and Social Council Distr. GENERAL CEP/AC.13/2005/4/Rev.1 23 March 2005 ENGLISH/ FRENCH/ RUSSIAN ECONOMIC COMMISSION FOR EUROPE COMMITTEE ON ENVIRONMENTAL POLICY High-level Meeting

Study of relationship between Ministry of Health and Ministry of Finance in Ghana

Study of relationship between Ministry of Health and Ministry of Finance in Ghana Presentation at the Global Health Initiative, Woodrow Wilson International Center for Scholars June 24, 2009 Content of

Study of relationship between Ministry of Health and Ministry of Finance in Ghana Presentation at the Global Health Initiative, Woodrow Wilson International Center for Scholars June 24, 2009 Content of

BRIEF FOR THE LEGISLATIVE COUNCIL 2003 CIVIL SERVICE PAY ADJUSTMENT

File Ref: CSBCR/PG/4-085-001/33 BRIEF FOR THE LEGISLATIVE COUNCIL INTRODUCTION 2003 CIVIL SERVICE PAY ADJUSTMENT At the meeting of the Executive Council on 25 February 2003, the Council ADVISED and the

File Ref: CSBCR/PG/4-085-001/33 BRIEF FOR THE LEGISLATIVE COUNCIL INTRODUCTION 2003 CIVIL SERVICE PAY ADJUSTMENT At the meeting of the Executive Council on 25 February 2003, the Council ADVISED and the

INSTITUTIONAL EFFECTIVENESS POLICY AND PROCEDURE

Responsible Official: President Responsible Office: Office of the President Next Review Date: July 2019 Website Address: https://mymoc.moc.edu/services/ir/policies/public%20pol ices/institutionaleffectiveness.pdf

Responsible Official: President Responsible Office: Office of the President Next Review Date: July 2019 Website Address: https://mymoc.moc.edu/services/ir/policies/public%20pol ices/institutionaleffectiveness.pdf

Creating, Managing and Analyzing a Nonprofit Budget. Green River Community College (Kent Campus) June 20, 2017

June 20, 2017") Creating, Managing and Analyzing a Nonprofit Budget Chris McCauley, CPA, Esq. Green River Community College (Kent Campus) June 20, 2017 Agenda 1. Welcome and Introductions (6:00 PM 6:05 PM) 2. Learning

Creating, Managing and Analyzing a Nonprofit Budget Chris McCauley, CPA, Esq. Green River Community College (Kent Campus) June 20, 2017 Agenda 1. Welcome and Introductions (6:00 PM 6:05 PM) 2. Learning

University of Maine System and Component Units. Core Financial Ratios and Composite Financial Index. FY10 to FY12

University of Maine System Office of Finance and Treasurer January 2013 TABLE OF CONTENTS Page Introduction 1 Component Units 1 Primary Reserve Ratio 2 Net Operating Revenues Ratio 3 Return on Net Assets

University of Maine System Office of Finance and Treasurer January 2013 TABLE OF CONTENTS Page Introduction 1 Component Units 1 Primary Reserve Ratio 2 Net Operating Revenues Ratio 3 Return on Net Assets

PLAN AND MANAGE THE BUDGET POLICY & PROCEDURE MANUAL

PLAN AND MANAGE THE BUDGET POLICY & PROCEDURE MANUAL THABA CHWEU LOCAL MUNICIPALITY Approved 25 June 2012 Resolution no: A50/2012 TABLE OF CONTENTS 1 INTRODUCTION... 1 1.1 Vision and value statement...

PLAN AND MANAGE THE BUDGET POLICY & PROCEDURE MANUAL THABA CHWEU LOCAL MUNICIPALITY Approved 25 June 2012 Resolution no: A50/2012 TABLE OF CONTENTS 1 INTRODUCTION... 1 1.1 Vision and value statement...

INTERNATIONAL MONETARY FUND AND THE INTERNATIONAL DEVELOPMENT ASSOCIATION MALAWI

INTERNATIONAL MONETARY FUND AND THE INTERNATIONAL DEVELOPMENT ASSOCIATION MALAWI Poverty Reduction Strategy 2003/04 Annual Progress Report Joint Staff Advisory Note Prepared by the Staffs of the IMF and

INTERNATIONAL MONETARY FUND AND THE INTERNATIONAL DEVELOPMENT ASSOCIATION MALAWI Poverty Reduction Strategy 2003/04 Annual Progress Report Joint Staff Advisory Note Prepared by the Staffs of the IMF and

Municipal Budgeting. Certified Government Finance Officer Review Session February 2017

Municipal Budgeting Certified Government Finance Officer Review Session February 2017 Ann Marie Ricardi, CGFO CFO City of Naples Michael D. Perry, CGFO Budget Officer City of Tampa Agenda Tuesday February

Municipal Budgeting Certified Government Finance Officer Review Session February 2017 Ann Marie Ricardi, CGFO CFO City of Naples Michael D. Perry, CGFO Budget Officer City of Tampa Agenda Tuesday February

Regulation on the implementation of the European Economic Area (EEA) Financial Mechanism

Financial Mechanism") the European Economic Area (EEA) Financial Mechanism 2014-2021 Adopted by the EEA Financial Mechanism Committee pursuant to Article 10.5 of Protocol 38c to the EEA Agreement on 8 September 2016 and confirmed

the European Economic Area (EEA) Financial Mechanism 2014-2021 Adopted by the EEA Financial Mechanism Committee pursuant to Article 10.5 of Protocol 38c to the EEA Agreement on 8 September 2016 and confirmed

GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY. for the programming period

Final version of 25/07/2008 COCOF 08/0014/02-EN GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY for the 2007 2013 programming period Table of contents 1. Introduction... 3 2. Main functions

Final version of 25/07/2008 COCOF 08/0014/02-EN GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY for the 2007 2013 programming period Table of contents 1. Introduction... 3 2. Main functions

Municipal Budgeting Certified Government Finance Officer Review Session

Municipal Budgeting Certified Government Finance Officer Review Session Diane M. Smith, MA, CGFO Budget Manager Alachua County Agenda Budget Process/Budget Types Fiscal Polices & Best Practices Performance

Municipal Budgeting Certified Government Finance Officer Review Session Diane M. Smith, MA, CGFO Budget Manager Alachua County Agenda Budget Process/Budget Types Fiscal Polices & Best Practices Performance

Competency standards for Fellows of the NTAA auditing SMSFs

Competency standards for Fellows of the NTAA auditing SMSFs National Tax & Accountants Association Ltd. 1 Contents Introduction.. 3 Background. 4 Auditing an SMSF.. 5 The planning phase of the audit ASA

Competency standards for Fellows of the NTAA auditing SMSFs National Tax & Accountants Association Ltd. 1 Contents Introduction.. 3 Background. 4 Auditing an SMSF.. 5 The planning phase of the audit ASA

COMMON BUDGETARY FRAMEWORK

STANDARD OPERATING PROCEDURES for COUNTRIES ADOPTING the DELIVERING AS ONE APPROACH August 2014 GUIDE TO THE COMMON BUDGETARY FRAMEWORK The Common Budgetary Framework, with all planned and costed UN programme

STANDARD OPERATING PROCEDURES for COUNTRIES ADOPTING the DELIVERING AS ONE APPROACH August 2014 GUIDE TO THE COMMON BUDGETARY FRAMEWORK The Common Budgetary Framework, with all planned and costed UN programme

Informal EB Briefing. Management Plan May 2018

Informal EB Briefing Management Plan 2019-2021 15 May 2018 Agenda 1 2 3 4 Management Plan timeline & structure Strategic & financial context Building the Management Plan A. Overall approach and preliminary

Informal EB Briefing Management Plan 2019-2021 15 May 2018 Agenda 1 2 3 4 Management Plan timeline & structure Strategic & financial context Building the Management Plan A. Overall approach and preliminary

Handbook. CEWARN Rapid Response Fund (RRF)

") CEWARN Rapid Response Fund (RRF) Handbook Version: authorised by the CEWARN Steering Committee on: 1.0 16 th of January, 2009 This handbook is maintained by Mr. Abdirashid Warsame, Response Coordinator,

CEWARN Rapid Response Fund (RRF) Handbook Version: authorised by the CEWARN Steering Committee on: 1.0 16 th of January, 2009 This handbook is maintained by Mr. Abdirashid Warsame, Response Coordinator,

INDIVIDUAL CONSULTANT PROCUREMENT NOTICE TOR - CONSULTANCY IC/2012/026. Date: 16 April 2012

INDIVIDUAL CONSULTANT PROCUREMENT NOTICE IC/2012/026 TOR - CONSULTANCY Date: 16 April 2012 Position: Consultant - RESOURCE MOBILISATION STRATEGY 2012-2015 for UNCT ETHIOPIA Duty Station: Addis Ababa, Ethiopia

INDIVIDUAL CONSULTANT PROCUREMENT NOTICE IC/2012/026 TOR - CONSULTANCY Date: 16 April 2012 Position: Consultant - RESOURCE MOBILISATION STRATEGY 2012-2015 for UNCT ETHIOPIA Duty Station: Addis Ababa, Ethiopia

Macau (China) Dispute Resolution Profile. (Last updated: 29 June 2017) General Information

Dispute Resolution Profile. (Last updated: 29 June 2017) General Information") 1 Macau (China) Dispute Resolution Profile (Last updated: 29 June 2017) General Information Macau (China) tax treaties are available at: http://www.dsf.gov.mo/download/tax/e_prb_tax_content.html http://www.dsf.gov.mo/download/tax/p_lei_106_99_m.html

1 Macau (China) Dispute Resolution Profile (Last updated: 29 June 2017) General Information Macau (China) tax treaties are available at: http://www.dsf.gov.mo/download/tax/e_prb_tax_content.html http://www.dsf.gov.mo/download/tax/p_lei_106_99_m.html

Terms of Reference (ToR)

") Terms of Reference (ToR) Mid -Term Evaluations of the Two Programmes: UNDP Support to Deepening Democracy and Accountable Governance in Rwanda (DDAG) and Promoting Access to Justice, Human Rights and Peace

Terms of Reference (ToR) Mid -Term Evaluations of the Two Programmes: UNDP Support to Deepening Democracy and Accountable Governance in Rwanda (DDAG) and Promoting Access to Justice, Human Rights and Peace

Notes to the Reportable Short Position Form

Notes to the Reportable Short Position Form 1. The Reportable Short Position Form (the Form) to be submitted to the Securities and Futures Commission (the Commission) pursuant to Rule 4(2) or 4(4) of the

Notes to the Reportable Short Position Form 1. The Reportable Short Position Form (the Form) to be submitted to the Securities and Futures Commission (the Commission) pursuant to Rule 4(2) or 4(4) of the

Proposal for a COUNCIL REGULATION

EUROPEAN COMMISSION Brussels, 30.1.2019 COM(2019) 64 final 2019/0031 (APP) Proposal for a COUNCIL REGULATION on measures concerning the implementation and financing of the general budget of the Union in

EUROPEAN COMMISSION Brussels, 30.1.2019 COM(2019) 64 final 2019/0031 (APP) Proposal for a COUNCIL REGULATION on measures concerning the implementation and financing of the general budget of the Union in

Factsheet N 6 Project implementation: delivering project outputs, achieving project objectives and bringing about the desired change

Project implementation: delivering project outputs, achieving project objectives and bringing about the desired change Version No 13 of 23 November 2018 Table of contents I. GETTING STARTED: THE INITIATION

Project implementation: delivering project outputs, achieving project objectives and bringing about the desired change Version No 13 of 23 November 2018 Table of contents I. GETTING STARTED: THE INITIATION

Guidance on the Actuarial Function MARCH 2018

Guidance on the Actuarial Function MARCH 2018 Disclaimer No responsibility or liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board constituted by the Society of Lloyd

Guidance on the Actuarial Function MARCH 2018 Disclaimer No responsibility or liability is accepted by the Society of Lloyd s, the Council, or any Committee of Board constituted by the Society of Lloyd

Education, Audiovisual and Culture Executive Agency

Education, Audiovisual and Culture Executive Agency MEDIA Unit EUROPEAN UNION - MEDIA 2007 PROGRAMME established by European Parliament and Council Decision N 1718/2006/EC (JO L 327 of 24.11.2006) SUPPORT

Education, Audiovisual and Culture Executive Agency MEDIA Unit EUROPEAN UNION - MEDIA 2007 PROGRAMME established by European Parliament and Council Decision N 1718/2006/EC (JO L 327 of 24.11.2006) SUPPORT

Financial Guidance. Guidance on how to carry out financial management and reporting under the EEA and Norwegian Financial Mechanisms for

Financial Guidance Guidance on how to carry out financial management and reporting under the EEA and Norwegian Financial Mechanisms for 2014-2021 Version November 2017 Table of contents 1 INTRODUCTION...

Financial Guidance Guidance on how to carry out financial management and reporting under the EEA and Norwegian Financial Mechanisms for 2014-2021 Version November 2017 Table of contents 1 INTRODUCTION...

REVENUE RECOGNITION ASU /23/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Drew Speed, CPA Partner, Accounting and Auditing Director, Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB

FINANCIAL MANAGEMENT FOR EVERYONE

NONPROFIT FINANCIAL MANAGEMENT TRAINING FINANCIAL MANAGEMENT FOR EVERYONE Developed by Nonprofits Assistance Fund WHO WE ARE OUR MISSION IS TO BUILD FINANCIALLY HEALTHY NONPROFITS THAT FOSTER COMMUNITY

NONPROFIT FINANCIAL MANAGEMENT TRAINING FINANCIAL MANAGEMENT FOR EVERYONE Developed by Nonprofits Assistance Fund WHO WE ARE OUR MISSION IS TO BUILD FINANCIALLY HEALTHY NONPROFITS THAT FOSTER COMMUNITY

Planning and Budgeting Manual, 2015

Oil and Natural Gas Corporation Limited Planning and Budgeting Manual, 2015 P a g e 1 Table of Contents 1. Introduction... 3 1.1. Objectives... 3 1.2. Importance of Budgetary Controls... 3 1.3. Advantages

Oil and Natural Gas Corporation Limited Planning and Budgeting Manual, 2015 P a g e 1 Table of Contents 1. Introduction... 3 1.1. Objectives... 3 1.2. Importance of Budgetary Controls... 3 1.3. Advantages

FICHE 4A. Version 1 4 April 2013

FICHE 4A IMPLEMENTING ACT ON THE MODEL FOR THE ANNUAL AND FINAL IMPLEMENTATION REPORT UNDER THE INVESTMENT FOR GROWTH AND JOBS GOAL Version 1 4 April 2013 Regulation Article Article 44 Implementation Reports

FICHE 4A IMPLEMENTING ACT ON THE MODEL FOR THE ANNUAL AND FINAL IMPLEMENTATION REPORT UNDER THE INVESTMENT FOR GROWTH AND JOBS GOAL Version 1 4 April 2013 Regulation Article Article 44 Implementation Reports

Part 1 : 07/27/10 21:26:38

Question 1 - CMA 692 H9 - Planning and Budgeting Concepts Strategy is a broad term that usually means the selection of overall objectives. Strategic analysis ordinarily excludes the A. Target product mix

Question 1 - CMA 692 H9 - Planning and Budgeting Concepts Strategy is a broad term that usually means the selection of overall objectives. Strategic analysis ordinarily excludes the A. Target product mix

ACTUARIAL SOCIETY OF HONG KONG CONTINUOUS PROFESSIONAL DEVELOPMENT ( CPD ) FREQUENTLY ASKED QUESTIONS

FREQUENTLY ASKED QUESTIONS") ACTUARIAL SOCIETY OF HONG KONG CONTINUOUS PROFESSIONAL DEVELOPMENT ( CPD ) FREQUENTLY ASKED QUESTIONS These are frequently asked questions about the operation of the CPD requirements. These requirements

ACTUARIAL SOCIETY OF HONG KONG CONTINUOUS PROFESSIONAL DEVELOPMENT ( CPD ) FREQUENTLY ASKED QUESTIONS These are frequently asked questions about the operation of the CPD requirements. These requirements

Review of the SET Plan implementation for the period

Review of the SET Plan implementation for the period 2010 2012 Sherpa Meeting 3 December 2012 SETIS SET-Plan Information System (SETIS) Led by JRC, it enables the monitoring of the SET Plan actions, the

Review of the SET Plan implementation for the period 2010 2012 Sherpa Meeting 3 December 2012 SETIS SET-Plan Information System (SETIS) Led by JRC, it enables the monitoring of the SET Plan actions, the

FINANCIAL ANALYSIS, BUDGETS PLANNING & CONTROLLING. 24 Sep - 05 Oct 2018, Amsterdam Dec 2018, Amsterdam

24 Sep - 05 Oct 2018, Amsterdam 10-21 Dec 2018, Amsterdam Introduction This 10-days GLOMACS training seminar brings together important areas of Financial Management, Planning and Control: Financial Analysis,

24 Sep - 05 Oct 2018, Amsterdam 10-21 Dec 2018, Amsterdam Introduction This 10-days GLOMACS training seminar brings together important areas of Financial Management, Planning and Control: Financial Analysis,

Budgeting Basics for Presenters Developed by Nonprofits Assistance Fund

Nonprofit Financial Management Training Budgeting Basics for Presenters Developed by Nonprofits Assistance Fund Budgets are the foundation of nonprofit finance and are vital to your organization s strategic

Nonprofit Financial Management Training Budgeting Basics for Presenters Developed by Nonprofits Assistance Fund Budgets are the foundation of nonprofit finance and are vital to your organization s strategic

United Nations Educational, Scientific and Cultural Organization Executive Board

ex United Nations Educational, Scientific and Cultural Organization Executive Board Hundred and sixty-second Session 162 EX/35 PARIS, 3 August 2001 Original: English Item 7.10 of the provisional agenda

ex United Nations Educational, Scientific and Cultural Organization Executive Board Hundred and sixty-second Session 162 EX/35 PARIS, 3 August 2001 Original: English Item 7.10 of the provisional agenda

REVENUE RECOGNITION ASU /8/2016. CPAs & ADVISORS ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

CPAs & ADVISORS experience clarity // ACCOUNTING AND AUDITING UPDATE FOR ARKANSAS HFMA Tracy Young, CPA Partner, BKD Health Care Group Little Rock REVENUE RECOGNITION ASU 2014-09 1 FASB/IASB ORIGINAL REVENUE

This document can be shared by CB participants with Centers for input in advance of Board deliberations. Document Category Standard Document

Version: 28 June 2016 For Information CGIAR Consortium CRP2 Value for Money (V4M) Analysis Purpose: This paper provides, as a companion document to the Consortium Office prepared paper titled Developing

Version: 28 June 2016 For Information CGIAR Consortium CRP2 Value for Money (V4M) Analysis Purpose: This paper provides, as a companion document to the Consortium Office prepared paper titled Developing

Learning Objectives. Managing for Results 3/7/2016

Chapter 15 Managing for Results Granof, et al. 7th edition 2016 John Wiley & Sons, Inc. All rights reserved. Chapter 15 1 Learning Objectives Roles of accountants in the management of governmental and

Chapter 15 Managing for Results Granof, et al. 7th edition 2016 John Wiley & Sons, Inc. All rights reserved. Chapter 15 1 Learning Objectives Roles of accountants in the management of governmental and

23/06/2017. Agenda. Myanmar Humanitarian Fund. Project Proposal Design Training. What is the MHF? MHF Governance and Management

Agenda Myanmar Humanitarian Fund Project Proposal Design Training 1. MHF Overview 2. Eligibility 3. Grant Management System 4. MHF Programme Cycle 5. MHF Feedback & Complaints Mechanism 6. MHF Visibility

Agenda Myanmar Humanitarian Fund Project Proposal Design Training 1. MHF Overview 2. Eligibility 3. Grant Management System 4. MHF Programme Cycle 5. MHF Feedback & Complaints Mechanism 6. MHF Visibility

Country-by-Country Reporting: Data Access & Usage. TDM Part

Tax and Duty Manual Part 38-03-20 Country-by-Country Reporting: Data Access & Usage TDM Part 38-03-20 This document should be read in conjunction with section 891H of the Taxes Consolidation Act 1997 Document

Tax and Duty Manual Part 38-03-20 Country-by-Country Reporting: Data Access & Usage TDM Part 38-03-20 This document should be read in conjunction with section 891H of the Taxes Consolidation Act 1997 Document

2 nd INDEPENDENT EXTERNAL EVALUATION of the EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA)

") 2 nd INDEPENDENT EXTERNAL EVALUATION of the EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA) TECHNICAL SPECIFICATIONS 15 July 2016 1 1) Title of the contract The title of the contract is 2nd External

2 nd INDEPENDENT EXTERNAL EVALUATION of the EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA) TECHNICAL SPECIFICATIONS 15 July 2016 1 1) Title of the contract The title of the contract is 2nd External

Trends, challenges and Opportunities for Resource Mobilization in Myanmar for Sustainable Development

Trends, challenges and Opportunities for Resource Mobilization in Myanmar for Sustainable Development 6 12 2018 Outline Revenue and expenditure and Financing Trends Challenges for resource mobilization

Trends, challenges and Opportunities for Resource Mobilization in Myanmar for Sustainable Development 6 12 2018 Outline Revenue and expenditure and Financing Trends Challenges for resource mobilization

MANGAUNG METROPOLITAN MUNICIPALITY BUDGET POLICY

MANGAUNG METROPOLITAN MUNICIPALITY BUDGET POLICY 2 INDEX 1. Statutory Framework... 3 2. Policy Objectives... 8 3. Votes, Categories of Expenditure and Line Items... 8 4. Capital Budget Mythology... 9 5.

MANGAUNG METROPOLITAN MUNICIPALITY BUDGET POLICY 2 INDEX 1. Statutory Framework... 3 2. Policy Objectives... 8 3. Votes, Categories of Expenditure and Line Items... 8 4. Capital Budget Mythology... 9 5.

Cross Border Co-operation between Bulgaria & Romania Multi-annual Programme Project Fiche for Programme Support

Cross Border Co-operation between Bulgaria & Romania Multi-annual Programme 2003 2006 2005 Project Fiche for Programme Support 1. Basic Information 1.1 CRIS Number: BG 2005/017-455.01;04 1.2 1.2 Title:

Cross Border Co-operation between Bulgaria & Romania Multi-annual Programme 2003 2006 2005 Project Fiche for Programme Support 1. Basic Information 1.1 CRIS Number: BG 2005/017-455.01;04 1.2 1.2 Title:

A n n u a l P e r f o r m a n c e A p p r a i s a l P r o c e s s F Y P r i n c i p l e & W o r k f l o w

A n n u a l P e r f o r m a n c e A p p r a i s a l P r o c e s s F Y 1 6 17 P r i n c i p l e & W o r k f l o w 2 A t t h e e n d o f t h e m a n u a l y o u w o u l d b e a b l e to Understand the objectives

A n n u a l P e r f o r m a n c e A p p r a i s a l P r o c e s s F Y 1 6 17 P r i n c i p l e & W o r k f l o w 2 A t t h e e n d o f t h e m a n u a l y o u w o u l d b e a b l e to Understand the objectives

Final draft Hong Kong margin and other risk mitigation standards for non-centrally cleared OTC derivatives

Final draft Hong Kong margin and other risk mitigation standards for non-centrally cleared OTC derivatives In December 2016, the Hong Kong Monetary Authority (HKMA) released a final draft of Supervisory

Final draft Hong Kong margin and other risk mitigation standards for non-centrally cleared OTC derivatives In December 2016, the Hong Kong Monetary Authority (HKMA) released a final draft of Supervisory

FIRST LEVEL CONTROL: PRINCIPLES AND PRACTICE

CENTRAL EUROPE PROGRAMME 2007-2013 Project financial management and controls Vienna, 7 th April 2011 FIRST LEVEL CONTROL: PRINCIPLES AND PRACTICE 1. Validation of expenditure: the FLC 2. General principles

CENTRAL EUROPE PROGRAMME 2007-2013 Project financial management and controls Vienna, 7 th April 2011 FIRST LEVEL CONTROL: PRINCIPLES AND PRACTICE 1. Validation of expenditure: the FLC 2. General principles

REVENUE RECOGNITION IMPLEMENTATION CONSIDERATIONS PRESENTED BY: JASON MYERS

REVENUE RECOGNITION IMPLEMENTATION CONSIDERATIONS PRESENTED BY: JASON MYERS UPDATE ON REVENUE RECOGNITION AICPA Update Technical items Variable consideration Disclosures Examples Implementation Advice

REVENUE RECOGNITION IMPLEMENTATION CONSIDERATIONS PRESENTED BY: JASON MYERS UPDATE ON REVENUE RECOGNITION AICPA Update Technical items Variable consideration Disclosures Examples Implementation Advice

SSAP 28 STATEMENT OF STANDARD ACCOUNTING PRACTICE 28 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

SSAP 28 STATEMENT OF STANDARD ACCOUNTING PRACTICE 28 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS (Issued January 2001) The standards, which have been set in bold italic type, should be read

SSAP 28 STATEMENT OF STANDARD ACCOUNTING PRACTICE 28 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS (Issued January 2001) The standards, which have been set in bold italic type, should be read

PROJECT PROPOSAL WRITING (A Tool for Resource Mobilization and Effective Attainment of Organization Objectives) OJI OGBUREKE, PhD November 2011

OJI OGBUREKE, PhD November 2011") PROJECT PROPOSAL WRITING (A Tool for Resource Mobilization and Effective Attainment of Organization Objectives) OJI OGBUREKE, PhD November 2011 OBJECTIVES OF THE PRESENTATION By the end of the presentation,

PROJECT PROPOSAL WRITING (A Tool for Resource Mobilization and Effective Attainment of Organization Objectives) OJI OGBUREKE, PhD November 2011 OBJECTIVES OF THE PRESENTATION By the end of the presentation,

Financial Monitoring of a Development Project by FMSF - A Concept Note

Financial Monitoring of a Development Project by FMSF - A Concept Note Section 1 About Monitoring 1.1 What is Monitoring? Monitoring is. To check that things are going as per plan. Monitoring is the systematic

Financial Monitoring of a Development Project by FMSF - A Concept Note Section 1 About Monitoring 1.1 What is Monitoring? Monitoring is. To check that things are going as per plan. Monitoring is the systematic

TONGA NATIONAL QUALIFICATIONS AND ACCREDITATION BOARD

TONGA NATIONAL QUALIFICATIONS AND ACCREDITATION BOARD RISK MANAGEMENT FRAMEWORK 2017 Overview Tonga National Qualifications and Accreditation Board (TNQAB) was established in 2004, after the Tonga National

TONGA NATIONAL QUALIFICATIONS AND ACCREDITATION BOARD RISK MANAGEMENT FRAMEWORK 2017 Overview Tonga National Qualifications and Accreditation Board (TNQAB) was established in 2004, after the Tonga National

Procurement Plan

Cork County Council Procurement Plan 2018-2019 2018 Page 1 of 14 Version 1.1 AUTHORS This document was prepared by: Procurement Section Finance Department Floor 6 County Hall Carrigrohane Road Cork VERSION

Cork County Council Procurement Plan 2018-2019 2018 Page 1 of 14 Version 1.1 AUTHORS This document was prepared by: Procurement Section Finance Department Floor 6 County Hall Carrigrohane Road Cork VERSION