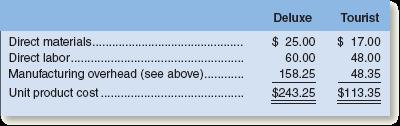

Costs for direct materials and direct labor for one unit of each product are given below:

|

|

|

- Daisy Diane Ball

- 6 years ago

- Views:

Transcription

per unit, and total direct labor-hours per year are provided below: Costs for direct materials and direct labor for one unit of each product are given")

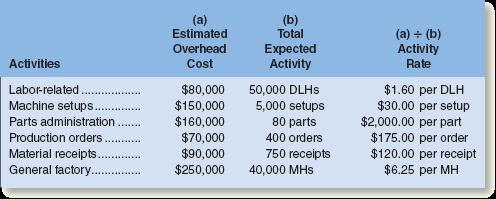

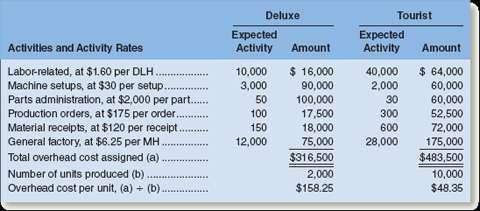

1 REVIEW PROBLEM: ACTIVITY-BASED COSTING Aerodec, Inc., manufactures and sells two types of wooden deck chairs: Deluxe and Tourist. Annual sales in units, direct labor-hours (DLHs) per unit, and total direct labor-hours per year are provided below: Costs for direct materials and direct labor for one unit of each product are given below: Manufacturing overhead costs total $800,000 each year. The breakdown of these costs among the company's six activity cost pools is given below. The activity measures are shown in parentheses. 1. Classify each of Aerodec's activities as either a unit-level, batch-level, product-level, or facility-level activity. 2. Assume that the company applies overhead cost to products on the basis of direct labor-hours. a. Compute the predetermined overhead rate. b. Determine the unit product cost of each product, using the predetermined overhead rate computed in (2)(a) above. 3. Assume that the company uses activity-based costing to compute overhead rates. a. Compute the activity rate for each of the six activities listed above. b. Using the rates developed in (3)(a) above, determine the amount of overhead cost that would be assigned to a unit of each product. c. Determine the unit product cost of each product and compare this cost to the cost computed in (2)(b) above. Solution to Review Problem a.

2 b. 3. a. b. c.

in 2(b) to apply overhead cost to products results in too little overhead cost being applied to the Deluxe deck chair (the lowvolume product) and too much overhead")

3 Under activity-based costing, the unit product cost of the Deluxe deck chair is much greater than the cost computed in 2(b), and the unit product cost of the Tourist deck chair is much less. Using volume (direct labor-hours) in 2(b) to apply overhead cost to products results in too little overhead cost being applied to the Deluxe deck chair (the lowvolume product) and too much overhead cost being applied to the Tourist deck chair (the high-volume product). THE FOUNDATIONAL 15 Hickory Company manufactures two products 14,000 units of Product Y and 6,000 units of Product Z. The company uses a plantwide overhead rate based on direct labor-hours. It is considering implementing an activity-based costing (ABC) system that allocates all of its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products Y and Z: 1. What is the company's plantwide overhead rate? 2. Using the plantwide overhead rate, how much manufacturing overhead cost is allocated to Product Y? How much is allocated to Product Z? 3. Page 142 What is the activity rate for the Machining activity cost pool? 4. What is the activity rate for the Machine Setups activity cost pool? 5. What is the activity rate for the Product Design activity cost pool? 6. What is the activity rate for the General Factory activity cost pool? 7. Which of the four activities is a batch-level activity? Why? 8. Which of the four activities is a product-level activity? Why? 9. Using the ABC system, how much total manufacturing overhead cost would be assigned to Product Y? 10. Using the ABC system, how much total manufacturing overhead cost would be assigned to Product Z? 11. Using the plantwide overhead rate, what percentage of the total overhead cost is allocated to Product Y? What percentage is allocated to Product Z? 12. Using the ABC system, what percentage of the Machining cost is assigned to Product Y? What percentage is assigned to Product Z? Are these percentages similar to those obtained in question 11? Why? 13. Using the ABC system, what percentage of Machine Setups cost is assigned to Product Y? What 14. Using the ABC system, what percentage of the Product Design cost is assigned to Product Y? What 15. Using the ABC system, what percentage of the General Factory cost is assigned to Product Y? What

![EXERCISE 3 10 Contrasting ABC and Conventional Product Costs [LO2, LO3, LO4] Rocky Mountain Corporation makes two types of hiking boots Xactive and Pathbreaker.](/docs-images/80/81112391/images/4-0.jpg "Data concerning these two product lines appear below: The company has a conventional costing system in which manufacturing overhead is applied to units based on direct labor-hours.")

4 EXERCISE 3 10 Contrasting ABC and Conventional Product Costs [LO2, LO3, LO4] Rocky Mountain Corporation makes two types of hiking boots Xactive and Pathbreaker. Data concerning these two product lines appear below: The company has a conventional costing system in which manufacturing overhead is applied to units based on direct labor-hours. Data concerning manufacturing overhead and direct labor-hours for the upcoming year appear below: 1. Compute the predetermined overhead rate based on direct labor-hours. Using this rate and other data from the problem, determine the unit product cost of each product. 2. The company is considering replacing its conventional costing system with an activity-based costing system that would assign its manufacturing overhead to the following four activity cost pools: Determine the activity rate for each of the four activity cost pools. 3. Using the activity rates and other data from the problem, determine the unit product cost of each product. 4. Explain why the conventional and activity-based cost assignments differ. PROBLEM 3 12A Contrasting ABC and Conventional Product Costs [LO2, LO3, LO4] Precision Manufacturing Inc. (PMI) makes two types of industrial component parts the EX300 and the TX500. It annually produces 60,000 units of EX300 and 12,500 units of TX500. The company's conventional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the company's two product lines is shown below: The company is considering implementing an activity-based costing system that distributes all of its manufacturing overhead to four activities as shown below: Page 148

5 1. Compute the plantwide overhead rate that would be used in the company's conventional cost system. Using the plantwide rate, compute the unit product cost for each product. 2. Compute the activity rate for each activity cost pool. Using the activity rates, compute the unit product cost for each product. 3. Why do the conventional and activity-based cost assignments differ from one another? ROBLEM 3 17A Contrast Activity-Based Costing and Conventional Product Costs Puget World, Inc., manufactures two models of television sets, the N 800 XL model and the N 500 model. Data regarding the two products follow: Additional information about the company follows: a. Model N 800 XL requires $75 in direct materials per unit, and Model N 500 requires $25. b. The direct labor wage rate is $18 per hour. c. The company has always used direct labor-hours as the base for applying manufacturing overhead cost to d. Model N 800 XL is more complex to manufacture than Model N 500 and requires the use of special equipment. Consequently, the company is considering the use of activity-based costing to assign manufacturing overhead cost to Three activity cost pools have been identified as follows: 1. Assume that the company continues to use direct labor-hours as the base for applying overhead cost to a. Compute the predetermined overhead rate. b. Compute the unit product cost of each model. 2. Assume that the company decides to use activity-based costing to assign manufacturing overhead cost to a. Compute the activity rate for each activity cost pool and determine the amount of overhead cost that would be assigned to each model using the activity-based costing system. b. Compute the unit product cost of each model. 3. Explain why manufacturing overhead cost shifts from Model N 500 to Model N 800 XL under activity-based costing.

ACTIVITY BASE COSTING

ACTIVITY BASE COSTING Key Terms and Concepts to Know Single Plantwide Rate vs. Multiple Department Rates Job order costing relied on a single plantwide overhead rate to apply overhead to work-in-process.

ACTIVITY BASE COSTING Key Terms and Concepts to Know Single Plantwide Rate vs. Multiple Department Rates Job order costing relied on a single plantwide overhead rate to apply overhead to work-in-process.

ACTIVITY BASE COSTING

ACTIVITY BASE COSTING Key Terms and Concepts to Know Activity-Based Costing (ABC): Activity Based Costing is a two-stage costing method in which overhead costs are assigned to overhead cost pools and the

ACTIVITY BASE COSTING Key Terms and Concepts to Know Activity-Based Costing (ABC): Activity Based Costing is a two-stage costing method in which overhead costs are assigned to overhead cost pools and the

Fill-in-the-Blank Equations. Exercises

Chapter 26 Cost Allocation and Activity-Based Costing Study Guide Solutions Fill-in-the-Blank Equations 1. Total budgeted plantwide allocation base 2. Department factory overhead rate 3. Ratio of allocation

Chapter 26 Cost Allocation and Activity-Based Costing Study Guide Solutions Fill-in-the-Blank Equations 1. Total budgeted plantwide allocation base 2. Department factory overhead rate 3. Ratio of allocation

540,000 2,500 Inspection hrs. 2. Apply the activity rates to compute the manufacturing overhead assigned to each product.

Chapter 4 LO3, LO4, LO5, & LO6 Exercise 1 This exercise covers LO3, LO4, LO5, & LO6. Clackamas, Inc currently uses traditional volume-based cost system applies manufacturing overhead cost to products on

Chapter 4 LO3, LO4, LO5, & LO6 Exercise 1 This exercise covers LO3, LO4, LO5, & LO6. Clackamas, Inc currently uses traditional volume-based cost system applies manufacturing overhead cost to products on

Module 1. Introduction

C9: Accounting and Finance Course Module 1 Introduction This module introduces the purpose of management accounting, the goals of the organisation and the role of management accounting in good corporate

C9: Accounting and Finance Course Module 1 Introduction This module introduces the purpose of management accounting, the goals of the organisation and the role of management accounting in good corporate

MANAGERIAL ACCOUNTING Hilton Chapter 3 Adobe Connect

1 MANAGERIAL ACCOUNTING Hilton Chapter 3 Adobe Connect We change gears dramatically in managerial accounting. Because of the limited time we have, we do not cover many advanced concepts. An overview of

1 MANAGERIAL ACCOUNTING Hilton Chapter 3 Adobe Connect We change gears dramatically in managerial accounting. Because of the limited time we have, we do not cover many advanced concepts. An overview of

Accounting For Decision Making

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

Chapter 8 Responsibility Accounting Chapter Review Solutions

Management Accounting in Australia - Solutions Chapter 8 Responsibility Accounting Chapter Review Solutions 1 F 220,500 Fixed 216,000 21,000 x $18.90 V 170,940 Variable 21,000 x $8.10 170,100 $391,440

Management Accounting in Australia - Solutions Chapter 8 Responsibility Accounting Chapter Review Solutions 1 F 220,500 Fixed 216,000 21,000 x $18.90 V 170,940 Variable 21,000 x $8.10 170,100 $391,440

Chapter 3 How Does an Organization Use Activity-Based Costing to Allocate Overhead Costs?

This is How Does an Organization Use Activity-Based Costing to Allocate Overhead Costs?, chapter 3 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons

This is How Does an Organization Use Activity-Based Costing to Allocate Overhead Costs?, chapter 3 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons

MANAGERIAL ACCOUNTING

MANAGERIAL ACCOUNTING _ Bob Livingston, PhD Cindy Moriarty Jerry Ramos Chapter 3: How Does an Organization Use Activity-Based Costing to Allocate Overhead Costs? 3.1 Why Allocate Overhead Costs? 3.2 Approaches

MANAGERIAL ACCOUNTING _ Bob Livingston, PhD Cindy Moriarty Jerry Ramos Chapter 3: How Does an Organization Use Activity-Based Costing to Allocate Overhead Costs? 3.1 Why Allocate Overhead Costs? 3.2 Approaches

MTP_Intermediate_Syllabus 2008_Jun2015_Set 2

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Accounting for Management: Concepts and Tools

Accounting for Management: Concepts and Tools Accounting for Management: Concepts and Tools Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by

Accounting for Management: Concepts and Tools Accounting for Management: Concepts and Tools Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by

Final Examination Semester 2 / Year 2011

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Management Accounting: Costing (MMAC)

") Management Accounting: Costing (MMAC) Question and answer book October 2018 AAT is a registered charity. No. 1050724 Questions Question 1 Buzz Electrics pays its production workers a group bonus of 20%

Management Accounting: Costing (MMAC) Question and answer book October 2018 AAT is a registered charity. No. 1050724 Questions Question 1 Buzz Electrics pays its production workers a group bonus of 20%

Job Costing Cost Accounting Horngreen, Datar, Foster 1

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

ACCT 361 MANAGEMENT ACCOUNTING FALL 2015 ASSIGNMENT 2 DUE MONDAY NOVEMBER 16

ACCT 361 MANAGEMENT ACCOUNTING FALL 2015 ASSIGNMENT 2 DUE MONDAY NOVEMBER 16 1. Auto Lavage is a Canadian company that owns and operates a large automatic carwash facility near Quebec. The following table

ACCT 361 MANAGEMENT ACCOUNTING FALL 2015 ASSIGNMENT 2 DUE MONDAY NOVEMBER 16 1. Auto Lavage is a Canadian company that owns and operates a large automatic carwash facility near Quebec. The following table

Chapter 2 Job-Order Costing: Calculating Unit Product Costs

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Institute of Certified Management Accountants of Sri Lanka Managerial Level November 2014 Examination

Copyright Reserved Serial No Institute of Certified Management Accountants of Sri Lanka Managerial Level November 2014 Examination Examination Date : 22 nd November 2014 Number of Pages : 06 Examination

Copyright Reserved Serial No Institute of Certified Management Accountants of Sri Lanka Managerial Level November 2014 Examination Examination Date : 22 nd November 2014 Number of Pages : 06 Examination

Chinese Costing Practices?

How Accurate Are Chinese Costing Practices? This is the third of three articles based on the recently completed study by the Institute of Management Accountants (IMA ) of the state of management accounting

How Accurate Are Chinese Costing Practices? This is the third of three articles based on the recently completed study by the Institute of Management Accountants (IMA ) of the state of management accounting

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing

Chapter 4 Job Costing") Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

0% (0 out of 25 correct)

") 0% (0 out of 25 correct) 1. The most difficult part of computing accurate unit costs is determining the proper amount of direct material cost to assign to each product. 2. Activity-based costing systems

0% (0 out of 25 correct) 1. The most difficult part of computing accurate unit costs is determining the proper amount of direct material cost to assign to each product. 2. Activity-based costing systems

Chapter 9 Activity-Based Costing

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Examination. Question 1:

Question 1: At an activity level of 8,800 units, Pember Corporation's total variable cost is $146,520 and its total fixed cost is $219,296. For the activity level of 8,900 units, compute the following

Question 1: At an activity level of 8,800 units, Pember Corporation's total variable cost is $146,520 and its total fixed cost is $219,296. For the activity level of 8,900 units, compute the following

SECTION I 14,000 14,200 19,170 10,000 8,000 10,400 12,400 9,600 8,400 11,200 13,600 18,320

QUESTION ONE SECTION I The following budget and actual results relates to Cypo Ltd. for the last three quarters for the year ended 31 March 200. Budget: Quarter 2 Quarter 3 Quarter to 30/9/2003 to 31/12/2003

QUESTION ONE SECTION I The following budget and actual results relates to Cypo Ltd. for the last three quarters for the year ended 31 March 200. Budget: Quarter 2 Quarter 3 Quarter to 30/9/2003 to 31/12/2003

Answer FOUR questions; THREE questions from Section A and ONE question from Section B.

UNIVERSITY OF EAST ANGLIA Norwich Business School Main Series Examination 2014-15 MANAGERIAL ACCOUNTING NBS-MC66 Time allowed: 3 hours Answer FOUR questions; THREE questions from Section A and ONE question

UNIVERSITY OF EAST ANGLIA Norwich Business School Main Series Examination 2014-15 MANAGERIAL ACCOUNTING NBS-MC66 Time allowed: 3 hours Answer FOUR questions; THREE questions from Section A and ONE question

Add: manufacturing overhead costs in inventory under absorption costing +27,000 Net operating income under absorption costing $4,727,000

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester One, 2018/19 Numerical Answer Question B1 Required production

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester One, 2018/19 Numerical Answer Question B1 Required production

Truck Division Variable costs: $3 per meal x 20,000 meals... $60,000 $3 per meal x 20,000 meals... $60,000 Fixed costs: 65% x $40,000...

Problem A-11 1. Auto Division Truck Division Variable costs: $3 per meal x 35,000 meals... $105,000 $3 per meal x 20,000 meals... $60,000 Fixed costs: 65% x $40,000... 26,000 35% x $40,000... 14,000 Total

Problem A-11 1. Auto Division Truck Division Variable costs: $3 per meal x 35,000 meals... $105,000 $3 per meal x 20,000 meals... $60,000 Fixed costs: 65% x $40,000... 26,000 35% x $40,000... 14,000 Total

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Course Code Chief Course Instructor Course Instructor UM15MB605 Dr. Anitha S Yadav Course Credits 4 No. of Hours Credit pattern ISA 52 Lecture Tutorial Practical/ Seminar Self study

MANAGEMENT ACCOUNTING Course Code Chief Course Instructor Course Instructor UM15MB605 Dr. Anitha S Yadav Course Credits 4 No. of Hours Credit pattern ISA 52 Lecture Tutorial Practical/ Seminar Self study

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

ACCA Paper F5. Performance Management. Class Notes

ACCA Paper F5 Performance Management Class Notes December 2011 The Accountancy College Ltd, June 2011 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or

ACCA Paper F5 Performance Management Class Notes December 2011 The Accountancy College Ltd, June 2011 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or

Historical information collected from a research in relation to sales of a company are as follows. Year Cost of promotion Sales revenue

Question bank 05-SA- English Short Answer Questions Question 01 Activity based costing system is used to allocate fixed production overhead in a more representative manner. Explain following terms in relation

Question bank 05-SA- English Short Answer Questions Question 01 Activity based costing system is used to allocate fixed production overhead in a more representative manner. Explain following terms in relation

B.Com II Cost Accounting

B.Com II Cost Accounting Chapter - 1 Cost Accounting: An Overview of Fundamental Aspects 2009 (1) Discuss the objectives of Cost Accounting. 2011 (1) Discuss importance of cost accounting. 2012 (1) What

B.Com II Cost Accounting Chapter - 1 Cost Accounting: An Overview of Fundamental Aspects 2009 (1) Discuss the objectives of Cost Accounting. 2011 (1) Discuss importance of cost accounting. 2012 (1) What

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester Two, 2017/18 Numerical answers Question B1 (a) The company's DL

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester Two, 2017/18 Numerical answers Question B1 (a) The company's DL

STANDARD COSTS AND VARIANCE ANALYSIS

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

MGMT Managerial Accounting and Finance ( version L )

") MGMT 1135 - Managerial Accounting and Finance ( version 213L ) Course Title Course Development Support Managerial Accounting and Finance Course Description Standard No The focus of this course is to acquire

MGMT 1135 - Managerial Accounting and Finance ( version 213L ) Course Title Course Development Support Managerial Accounting and Finance Course Description Standard No The focus of this course is to acquire

Product Costs Cost Direct Direct Manufacturing Period Item Materials Labor Overhead Costs

Problems: Set C P14-1C Grossman Company specializes in manufacturing football helmets. The company has enough orders to keep the factory production at 20,000 football helmets per month. Grossman s monthly

Problems: Set C P14-1C Grossman Company specializes in manufacturing football helmets. The company has enough orders to keep the factory production at 20,000 football helmets per month. Grossman s monthly

PTP_Intermediate_Syllabus 2012_Dec2015_Set 3 Paper 10 Cost & Management Accountancy

Paper 10 Cost & Management Accountancy Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B PTP_Intermediate_Syllabus 2012_Dec2015_Set

Paper 10 Cost & Management Accountancy Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B PTP_Intermediate_Syllabus 2012_Dec2015_Set

MERMAID. Manufacturers of surf gear Established The firm

BOARDIES @ MERMAID Manufacturers of surf gear Established 1960 The firm Boardies @ Mermaid (Boardies) is a manufacturer of items of surf gear. What began as a small family business has now grown into a

BOARDIES @ MERMAID Manufacturers of surf gear Established 1960 The firm Boardies @ Mermaid (Boardies) is a manufacturer of items of surf gear. What began as a small family business has now grown into a

MANAGEMENT ACCOUNTING

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

AGENDA: MANAGEMENT ACCOUNTING

14-1 Management Accounting Tutorial 8 (, chapter 13, 14, 1, 2, 3) Mid Module Review Bangor University Transfer Abroad Programme 1. Globalization. 2. Strategy. 3. Organizational structure. 4. Process management.

14-1 Management Accounting Tutorial 8 (, chapter 13, 14, 1, 2, 3) Mid Module Review Bangor University Transfer Abroad Programme 1. Globalization. 2. Strategy. 3. Organizational structure. 4. Process management.

Final Examination Booklet. Managerial Accounting

Final Examination Booklet Managerial Accounting Managerial Accounting Note: You should complete all lesson exams before you take the final exam. Complete the following exam by answering the questions and

Final Examination Booklet Managerial Accounting Managerial Accounting Note: You should complete all lesson exams before you take the final exam. Complete the following exam by answering the questions and

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") No. of Pages - 15 No of Questions -07 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II (Group A) END SEMESTER EXAMINATION DECEMBER 2014

No. of Pages - 15 No of Questions -07 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II (Group A) END SEMESTER EXAMINATION DECEMBER 2014

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING FORMATION 2 EXAMINATION - AUGUST 2011 NOTES: Section A - Questions 1 and 2 are compulsory. You have to answer Part A or Part B only of Question 2. (If you provide answers to both

MANAGEMENT ACCOUNTING FORMATION 2 EXAMINATION - AUGUST 2011 NOTES: Section A - Questions 1 and 2 are compulsory. You have to answer Part A or Part B only of Question 2. (If you provide answers to both

Revision of management accounting

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

This article discusses the selection of and changes in accounting policies, changes in accounting estimates and corrections of errors.

HKAS 8 Accounting policies, changes in accounting estimates and errors (Relevant to AAT Examination Paper 7 Financial Accounting) Dr. M H Ho, School of Continuing & Professional Studies, The Chinese University

HKAS 8 Accounting policies, changes in accounting estimates and errors (Relevant to AAT Examination Paper 7 Financial Accounting) Dr. M H Ho, School of Continuing & Professional Studies, The Chinese University

6. Activity Based Costing (ABC)

") 6. Activity Based Costing (ABC) Background Traditional cost accounting is characterized by considerable aggregation a small number of synthetic variables Overhead is allocated neglecting finer details

6. Activity Based Costing (ABC) Background Traditional cost accounting is characterized by considerable aggregation a small number of synthetic variables Overhead is allocated neglecting finer details

Prepare, Apply, and Confirm

Prepare, Apply, and Confirm etext Features Keep students engaged in learning on their own time, while helping them achieve greater conceptual understanding of course material through author-created solutions

Prepare, Apply, and Confirm etext Features Keep students engaged in learning on their own time, while helping them achieve greater conceptual understanding of course material through author-created solutions

Marginal and. this chapter covers...

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

Management Accounting

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

ABSA 205: Cost and Management Accounting I. Tutorial Exercises. Christos Minas PhD (Cand), FAIA, MSc, BA

, FAIA, MSc, BA") ABSA 205: Cost and Management Accounting I Tutorial Exercises Christos Minas PhD (Cand), FAIA, MSc, BA SUBJECT OUTLINE Objectives of the subject The aims of this course are to develop the students understanding

ABSA 205: Cost and Management Accounting I Tutorial Exercises Christos Minas PhD (Cand), FAIA, MSc, BA SUBJECT OUTLINE Objectives of the subject The aims of this course are to develop the students understanding

Activity-cost driver. 90,000 orders 15,000 maintenance hours 45,000 setups 21,000 inspections

~Pff~53U: ~~f4 : :iljg;tbwj : 0223 ep.:;;: : 3 Answer questions (1) to (4) using the information below: Mayan Potters manufactures two sizes of ceramic paperweights, regular and jumbo. TI1e following information

~Pff~53U: ~~f4 : :iljg;tbwj : 0223 ep.:;;: : 3 Answer questions (1) to (4) using the information below: Mayan Potters manufactures two sizes of ceramic paperweights, regular and jumbo. TI1e following information

The budgeted information on the two business opportunities that Green Bush records are currently considering investing in is as follows:

ICB Cost and Management Accounting Playlist Handbook SECTION A: REVISION VIDEO QUESTIONS Break-even analysis The budgeted information on the two business opportunities that Green Bush records are currently

ICB Cost and Management Accounting Playlist Handbook SECTION A: REVISION VIDEO QUESTIONS Break-even analysis The budgeted information on the two business opportunities that Green Bush records are currently

Chapter 2 Lecture Notes. I. Summary of the types of cost classifications. Cost classifications for assigning costs to cost objects

Chapter 2 Lecture Notes 1 Chapter theme: This chapter explains how managers need to rely on different cost classifications for different purposes. The four main purposes emphasized in this chapter include

Chapter 2 Lecture Notes 1 Chapter theme: This chapter explains how managers need to rely on different cost classifications for different purposes. The four main purposes emphasized in this chapter include

Flexible Budgets and Standard Costing QUESTIONS

Chapter 21 Flexible Budgets and Standard Costing QUESTIONS 1. Fixed budget performance reports have limited usefulness because they do not reflect differences in revenues and variable costs that can occur

Chapter 21 Flexible Budgets and Standard Costing QUESTIONS 1. Fixed budget performance reports have limited usefulness because they do not reflect differences in revenues and variable costs that can occur

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Performance Pillar. P1 Performance Operations. Tuesday 28 February 2012

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO Performance Pillar P1 Performance Operations Instructions to candidates Tuesday 28 February 2012 You are allowed three hours to answer this question

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO Performance Pillar P1 Performance Operations Instructions to candidates Tuesday 28 February 2012 You are allowed three hours to answer this question

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

CHAPTER 6. Master Budgeting and Responsibility Accounting

CHAPTER 6 Master Budgeting and Responsibility Accounting 1 Budget Defined The quantitative expression of a proposed plan of action by management for a specified period, and An aid to coordinating what

CHAPTER 6 Master Budgeting and Responsibility Accounting 1 Budget Defined The quantitative expression of a proposed plan of action by management for a specified period, and An aid to coordinating what

MANAGERIAL (COST) ACCOUNTING

ACCOUNTING") MANAGERIAL (COST) ACCOUNTING EXERCISE BOOK ERASMUS WINTER SEMESTER 2014 Exercise 2.1 Consider the following company, Chip Making Systems, that manufactures computer chips. It incurs the following costs

MANAGERIAL (COST) ACCOUNTING EXERCISE BOOK ERASMUS WINTER SEMESTER 2014 Exercise 2.1 Consider the following company, Chip Making Systems, that manufactures computer chips. It incurs the following costs

Answer FOUR questions; THREE questions from Section A and ONE question from section B.

UNIVERSITY OF EAST ANGLIA Norwich Business School UG Main Series Examination 2012-13 MANAGEMENT ACCOUNTING NBS-2F1Y Time allowed: 3 hours Answer FOUR questions; THREE questions from Section A and ONE question

UNIVERSITY OF EAST ANGLIA Norwich Business School UG Main Series Examination 2012-13 MANAGEMENT ACCOUNTING NBS-2F1Y Time allowed: 3 hours Answer FOUR questions; THREE questions from Section A and ONE question

Financial Comparison $ billions Income Statement Mar-02 Mar-02 Mar-00 Mar-99 Mar-98 Revenue

2.008 For-Profit manufacturing firms Performance Measures Ownership: Market value = PV (Earning) PV (Growth Opportunity) Management: Performance Targets 2 Automotive Market Share in the U.S. 3 30% 2 20%

2.008 For-Profit manufacturing firms Performance Measures Ownership: Market value = PV (Earning) PV (Growth Opportunity) Management: Performance Targets 2 Automotive Market Share in the U.S. 3 30% 2 20%

CHAPTER 4 JOB COSTING

CHAPTER 4 JOB ING 4-1 Cost pool a grouping of individual cost items. Cost tracing the assigning of direct costs to the chosen cost object. Cost allocation the assigning of indirect costs to the chosen

CHAPTER 4 JOB ING 4-1 Cost pool a grouping of individual cost items. Cost tracing the assigning of direct costs to the chosen cost object. Cost allocation the assigning of indirect costs to the chosen

LO 1: Budgeting. Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack

Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack LO 1: Budgeting Long-range planning Master budget Operating budget Financial budget Benefits of Budgeting: Planning

Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack LO 1: Budgeting Long-range planning Master budget Operating budget Financial budget Benefits of Budgeting: Planning

SERIES 3 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL. (Code No: 3023) FRIDAY 15 JUNE

FRIDAY 15 JUNE") SERIES 3 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) FRIDAY 15 JUNE Instructions to Candidates (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions. All

SERIES 3 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) FRIDAY 15 JUNE Instructions to Candidates (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions. All

(Final solutions in the last page) PART A

PART A") MANAGEMENT ACCOUNTING Spring semester 2011/2012 Mid-term test DATE: April 11, 2012 LENGTH: 1h 20 m Procedures: The test is composed of Parts A and B; The questions must be answered in the following stapled

MANAGEMENT ACCOUNTING Spring semester 2011/2012 Mid-term test DATE: April 11, 2012 LENGTH: 1h 20 m Procedures: The test is composed of Parts A and B; The questions must be answered in the following stapled

Chapter 6 Overheads & Absorption Costing. Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Chapter 6 Overheads & Absorption Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Overheads Overheads is the cost incurred in the course of making a product,

Chapter 6 Overheads & Absorption Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Overheads Overheads is the cost incurred in the course of making a product,

5_MGT402_Spring_2010_Final_Term_Solved_paper

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

CHAPTER 4 JOB COSTING

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool a grouping of individual indirect cost items. Cost tracing the assigning of direct costs to

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool a grouping of individual indirect cost items. Cost tracing the assigning of direct costs to

SELECTED FINANCIAL AND OPERATING INFORMATION

1 TSX: PSD OTCQX: PLSDF Q1 For the three months ended March 31, 2018 SELECTED FINANCIAL AND OPERATING INFORMATION (thousands of dollars except per share data, numbers of shares and kilometres of seismic

1 TSX: PSD OTCQX: PLSDF Q1 For the three months ended March 31, 2018 SELECTED FINANCIAL AND OPERATING INFORMATION (thousands of dollars except per share data, numbers of shares and kilometres of seismic

Practice Costing and Operation Control

Note to student: Some of the following activities will require the student to use a calculator. Scenario: You are an accountant for Scrumptious, a large food manufacturing plant, and you work in the accounting

Note to student: Some of the following activities will require the student to use a calculator. Scenario: You are an accountant for Scrumptious, a large food manufacturing plant, and you work in the accounting

Index COPYRIGHTED MATERIAL

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

UNIVERSITY OF SWAZILAND MAIN EXAMINATION PAPER. THE TOTAL NUMBER OF QUESTIONS ON mis PAPER ARE FIVE (5) 2. ANSWER QUESTION ONE AND ANY omer THREE

2. ANSWER QUESTION ONE AND ANY omer THREE") COURSE CODE: AC 214 (M) 2012 UNIVERSITY OF SWAZILAND DEPARTMENT OF ACCOUNTING MAIN EXAMINATION PAPER DEGREEIDIPLOMA AND YEAR OF STUDY TITLE OF PAPER B. COMMII INTRODUCTION COST ACCOUNTING COURSE CODE TIME

COURSE CODE: AC 214 (M) 2012 UNIVERSITY OF SWAZILAND DEPARTMENT OF ACCOUNTING MAIN EXAMINATION PAPER DEGREEIDIPLOMA AND YEAR OF STUDY TITLE OF PAPER B. COMMII INTRODUCTION COST ACCOUNTING COURSE CODE TIME

Cost Accounting Acct 362/562 Costing for Jobs or Batches. Homework Problems. Problem #69

Cost Accounting Acct 362/562 Costing for Jobs or Batches Homework Problems Problem #69 Basic - Linking jobs to the balance sheet and income statement. This problem focuses on job-order costing for the

Cost Accounting Acct 362/562 Costing for Jobs or Batches Homework Problems Problem #69 Basic - Linking jobs to the balance sheet and income statement. This problem focuses on job-order costing for the

Master Budget and Responsibility Accounting

Master Budget and Responsibility Accounting 1 Budgeting Cycle Performance planning Providing a frame of reference Investigating variations Corrective action Planning again 2 The Master Budget Master Budget

Master Budget and Responsibility Accounting 1 Budgeting Cycle Performance planning Providing a frame of reference Investigating variations Corrective action Planning again 2 The Master Budget Master Budget

Capítulo 6 Managerial Accounting and Cost Concepts

Capítulo 6 Managerial Accounting and Concepts Exercise 1-1 (15 minutes) Object Direct 1. The wages of pediatric nurses The pediatric department 2. Prescription drugs A particular patient 3. Heating the

Capítulo 6 Managerial Accounting and Concepts Exercise 1-1 (15 minutes) Object Direct 1. The wages of pediatric nurses The pediatric department 2. Prescription drugs A particular patient 3. Heating the

Allocation of Support-Department Costs, Common Costs, and Revenues

1 Allocation of Support-Department Costs, Common Costs, and Revenues A support department, also called a service department, provides the services that assist other internal departments (operating departments

1 Allocation of Support-Department Costs, Common Costs, and Revenues A support department, also called a service department, provides the services that assist other internal departments (operating departments

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 3,000 Ending Raw Materials Inventory 4,500 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 3,000 Ending Raw Materials Inventory 4,500 Purchases of Raw Materials

CLASSIFICATION OF COST

Cost Accounting Standard 1 CLASSIFICATION OF COST Draft Developed by Technical Support and Practice Development Committee Institute of Cost and Managemet Accountants of Pakistan Implementation Status This

Cost Accounting Standard 1 CLASSIFICATION OF COST Draft Developed by Technical Support and Practice Development Committee Institute of Cost and Managemet Accountants of Pakistan Implementation Status This

Chapter 16 Fundamentals of Variance Analysis

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team.

Solved by Mehreen Humayun vuzs Team.") FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

Introduction to Managerial Accounting and Job Order Cost Systems p. 1 The Differences Between Managerial and Financial Accounting p.

Introduction to Managerial Accounting and Job Order Cost Systems p. 1 The Differences Between Managerial and Financial Accounting p. 2 The Management Accountant in the Organization p. 4 Manufacturing Cost

Introduction to Managerial Accounting and Job Order Cost Systems p. 1 The Differences Between Managerial and Financial Accounting p. 2 The Management Accountant in the Organization p. 4 Manufacturing Cost

MANAGEMENT & COST ACCOUNTING LO 2: BASIC ASPECTS OF COST ACCOUNTING

MANAGEMENT & COST ACCOUNTING LO 2: BASIC ASPECTS OF COST ACCOUNTING LEARNING GOALS After completing this chapter you should be able to; 1) Explain why organizations need to know how much products, processes

MANAGEMENT & COST ACCOUNTING LO 2: BASIC ASPECTS OF COST ACCOUNTING LEARNING GOALS After completing this chapter you should be able to; 1) Explain why organizations need to know how much products, processes

Management Accounting

>f0t@wjy2[2`5k2[2h# Management Accounting Level 3 Series 2 2003 (Code 3023) Model Answers ASP M 1445 Management Accounting Level 3 Series 2 2003 How to use this booklet Model Answers have been developed

>f0t@wjy2[2`5k2[2h# Management Accounting Level 3 Series 2 2003 (Code 3023) Model Answers ASP M 1445 Management Accounting Level 3 Series 2 2003 How to use this booklet Model Answers have been developed

At 30 September 2002 the business s final accounts were drawn up as follows: Trading and Profit and Loss Account for the year ended 30 September 2002

PERFORMANCE MANAGEMENT MAY DIET 2016 MOCK EXAM QUESTION 1 On 1 October 2001Saint Mike and his wife formed a limited company, SAINT MIKE Ltd, to run a beautician s business, and each paid in N37500 as share

PERFORMANCE MANAGEMENT MAY DIET 2016 MOCK EXAM QUESTION 1 On 1 October 2001Saint Mike and his wife formed a limited company, SAINT MIKE Ltd, to run a beautician s business, and each paid in N37500 as share

Answer ALL questions in Section A and TWO questions from Section B. Section A carries a weight of 40%; Section B carries a weight of 60%

UNIVERSITY OF EAST ANGLIA School of Business Studies May/June PG Examination 2015-16 ACCOUNTING AND FINANCIAL ANALYSIS NBS-M056 Time allowed: 2 hours Answer ALL questions in Section A and TWO questions

UNIVERSITY OF EAST ANGLIA School of Business Studies May/June PG Examination 2015-16 ACCOUNTING AND FINANCIAL ANALYSIS NBS-M056 Time allowed: 2 hours Answer ALL questions in Section A and TWO questions

Exercise E21-1 page 932. (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000

Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000") Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

PAPER 10: COST & MANAGEMENT ACCOUNTANCY

PAPER 10: COST & MANAGEMENT ACCOUNTANCY Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B MTP_Intermediate_Syllabus 2012_Jun2015_Set

PAPER 10: COST & MANAGEMENT ACCOUNTANCY Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B MTP_Intermediate_Syllabus 2012_Jun2015_Set

MARK SCHEME for the October/November 2010 question paper for the guidance of teachers 9706 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level www.xtremepapers.com MARK SCHEME for the October/November 2010 question paper for the guidance of

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level www.xtremepapers.com MARK SCHEME for the October/November 2010 question paper for the guidance of

Chapter 4: Job Costing

Chapter 4: Job Costing Costing System Terminology: Cost Object Anything for which a separate measurement of costs is desired. Direct Cost Costs that are related to a particular cost object in an economically

Chapter 4: Job Costing Costing System Terminology: Cost Object Anything for which a separate measurement of costs is desired. Direct Cost Costs that are related to a particular cost object in an economically

CAS-3 (REVISED 2015) COST ACCOUNTING STANDARD ON PRODUCTION AND OPERATION OVERHEADS

COST ACCOUNTING STANDARD ON PRODUCTION AND OPERATION OVERHEADS") CAS-3 (REVISED 2015) COST ACCOUNTING STANDARD ON PRODUCTION AND OPERATION OVERHEADS The following is the Cost Accounting Standard on PRODUCTION AND OPERATION OVERHEADS (CAS-3) (Revised 2015) issued by

CAS-3 (REVISED 2015) COST ACCOUNTING STANDARD ON PRODUCTION AND OPERATION OVERHEADS The following is the Cost Accounting Standard on PRODUCTION AND OPERATION OVERHEADS (CAS-3) (Revised 2015) issued by

MANAGEMENT ACCOUNTING 2. Module Code: ACCT08004

School of Business & Enterprise Paisley & Hamilton Campus Session 015-016 Trimester 1 MANAGEMENT ACCOUNTING Module Code: ACCT08004 Date: 1st January 016 Time: 1400-1600 Answer THREE questions Question

School of Business & Enterprise Paisley & Hamilton Campus Session 015-016 Trimester 1 MANAGEMENT ACCOUNTING Module Code: ACCT08004 Date: 1st January 016 Time: 1400-1600 Answer THREE questions Question

Chapter 11 Flexible Budgets and Overhead Analysis

Chapter 11 Flexible Budgets and Overhead Analysis Solutions to Questions 11-1 A static budget is a budget prepared for a single level of activity. The static budget is not adjusted even if the activity

Chapter 11 Flexible Budgets and Overhead Analysis Solutions to Questions 11-1 A static budget is a budget prepared for a single level of activity. The static budget is not adjusted even if the activity

Module Title: Advanced Management Accounting 1

CORK INSTITUTE OF TECHNOLOGY INSTITIÚID TEICNEOLAÍOCHTA CHORCAÍ Semester 1 Examinations 2009/10 Module Title: Advanced Management Accounting 1 Module Code: ACCT7001 School: Business Studies (Department

CORK INSTITUTE OF TECHNOLOGY INSTITIÚID TEICNEOLAÍOCHTA CHORCAÍ Semester 1 Examinations 2009/10 Module Title: Advanced Management Accounting 1 Module Code: ACCT7001 School: Business Studies (Department

YORK UNIVERSITY School of Administrative Studies. AP/ADMS Section A Summer 2013 Mid-Term Examination, Sunday, July 7 th, 12 noon 3 pm

LAST NAME FIRST NAME STUDENT NUMBER - - SIGN IN # YORK UNIVERSITY School of Administrative Studies AP/ADMS 2510 3.0 Section A Summer 2013 Mid-Term Examination, Sunday, July 7 th, 12 noon 3 pm Instructions:

LAST NAME FIRST NAME STUDENT NUMBER - - SIGN IN # YORK UNIVERSITY School of Administrative Studies AP/ADMS 2510 3.0 Section A Summer 2013 Mid-Term Examination, Sunday, July 7 th, 12 noon 3 pm Instructions:

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1,000 Ending Raw Materials Inventory 2,500 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1,000 Ending Raw Materials Inventory 2,500 Purchases of Raw Materials

About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11

CONTENTS About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11 1 INTRODUCTION u Cost 1 u Costing 2 u Cost accounting 2 u Cost accountancy 2 u Classification of costs 3 u Distinction between

CONTENTS About the author I-5 Acknowledgement I-7 Preface I-9 Chapter-heads I-11 1 INTRODUCTION u Cost 1 u Costing 2 u Cost accounting 2 u Cost accountancy 2 u Classification of costs 3 u Distinction between

Higher National Diploma in Accountancy Third Year, First Semester Examination 2014 DA3101-Advanced Management Accounting

[All Rights Reserved] SLIATE SLIAE SRI LANKA INSTITUTE OF ADVANCED TECHNOLOGICAL EDUCATION (Established in the Ministry of Higher Education, vide in Act No. 29 of 1995) Higher National Diploma in Accountancy

[All Rights Reserved] SLIATE SLIAE SRI LANKA INSTITUTE OF ADVANCED TECHNOLOGICAL EDUCATION (Established in the Ministry of Higher Education, vide in Act No. 29 of 1995) Higher National Diploma in Accountancy