Office of Auditor of State Oversight Tips & Best Practices

|

|

|

- Grace Cobb

- 5 years ago

- Views:

Transcription

1 Office of Auditor of State Oversight Tips & Best Practices 1

2 Today s agenda Daily and monthly operations Clerks duties / expectations Oversight duties & tips Notification requirements 2

3 Bank Accounts The number of bank accounts should be limited: Multiple bank accounts provide: More opportunity More risk Multiple accounts = multiple reconciliations Separate accounts vs. robust accounting system City Clerks should not be the only authorized signer on the bank accounts. If used correctly, counter signatures are a good control to have in place. 3

4 City Expenses Should not be paid in cash Petty cash funds Approved by the City Council Kept in a secure location Kept on an imprest basis Replenishment only after the Council s review and approval Surprise counts 4

5 Disbursement listing City Expenses Prior to checks being signed and disbursed Invoices/bills available for Council s review and approval Invoices/bills/receipts should be marked paid Once approved, should be signed by Mayor or designated Council member Should be filed with minutes of Council meeting 5

6 City Expenses Payment prior to Council approval Recurring Repetitive Predictable Requires a written policy Should be identified as prepaid and approved at next Council meeting 6

7 Initial receipts listing Collections Pre-numbered receipts Squares Pay-Pal For utilities cancelled remittance stubs. Periodically reconcile regardless of which of the above is used. 7

8 Monthly Utility Reconciliations Beginning balance due to the City. Add current month s total billings amount. Subtract collections received in current month. Subtract any accounts written off (which are approved by the City Council). Ending balance should tie to accounting records. 8

9 Bank Reconciliations Key word: Monthly bank reconciliations Timely manner Prepared by someone independent of processing financial transactions OR Thoroughly reviewed by an independent party. Resolution of variances 9

10 City Clerk / Treasurer s Reports Like the bank reconciliation, needs to be done in a timely manner Components should include: Beginning balance The month s deposits The month s payments The ending balance 10

11 Other City Clerk Duties Maintaining all financial records Prompt responses to inquiries from City officials regarding financial matters Minutes of Council meetings Prompt communications Review of timesheets for other City employees (determining reasonableness) 11

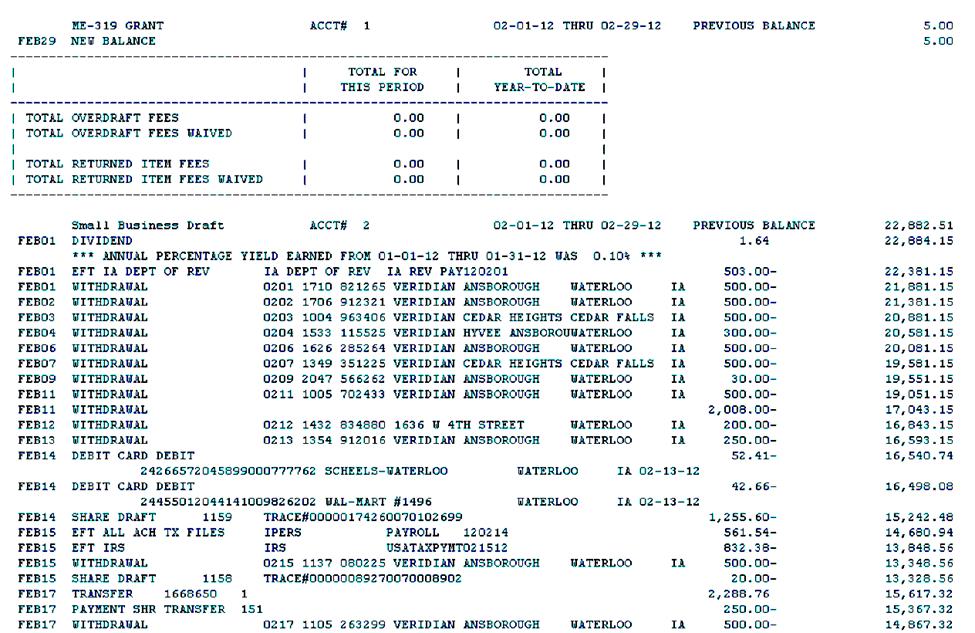

12 Oversight Duties Bank Statements Original bank statements What to look for in the bank statements appearance 12

13 13

14 14

15 15

16 Oversight Duties Bank Statements What to look for in the bank statements: Cash withdrawals Deposits followed by a cash withdrawal of the same amount Electronic payments to credit cards or vendors Inconsistent electronic payroll payments Payments including SQ NSF or overdraft fees 16

17 Oversight Duties Bank Statements What to look for in the bank statements: Images of redeemed checks Unexpected frequency of check payments Can be used to traced to authorized disbursement listing Check number out of sequence with other checks Deposit slips Composition of the deposits 17

18 .. 18

19 Utility Reconciliations The reconciliation reports should be backed up by monthly reports ran from the utility system at the time the reconciliation is prepared. There shouldn t be any reconciling items There shouldn t be repeating activity between monthly reconciliations. Ending balance should not be the same between months. Follow up on concerns in a timely manner. 19

20 Expenditures Actual to Budget Comparisons Prior to listing on A/P list Month-end Revenues Month-end Be considering need for budget amendment(s) near end of the 3 rd quarter. For any amendments made, be able to explain why they are needed. Ensure Department heads are properly monitoring financial position. 20

21 Don t sign blank checks Other Oversight Tips Don t keep counter-signed blank checks on hand for emergencies Keep your signature stamp Don t allow use of debit cards Limit use of credit cards 21

22 Red Flags Employees with a lavish lifestyle that doesn t match their salary Employees who don t take vacation Employees who routinely stay late and work on weekends Tips or complaints about an employee 22

23 An employee who is reluctant to share his/her job function Large number of write-offs in accounts receivable Employees who seem to feel the rules don t apply to them

24 Biggest Fraud Inhibitors Effective internal controls: o o cost/benefit relationship integrity of employees Appropriate governing board oversight: o Absolutely critical in small organizations o Equally effective in large organizations when they ask the tough questions 24

25 Tone at the top emphasize ethics importance o o Ethical atmosphere created by leadership Tone of management will have a trickle-down effect on employees Trust... but verify! In God we trust, everyone else we audit! 25

26 How do you set the right tone? o o o o Communicate to employees what is expected of them Lead by example Provide a safe mechanism for reporting violations/concerns Reward integrity, not the opposite.

of the Code of Iowa.")

NOTE: The remaining steps must be tailored to each specific situation.")

27 Notification of the Office of Auditor of State is required for all governmental subdivisions by section 11.6(7) of the Code of Iowa. (Annette Campbell or Jim Cunningham, ) NOTE: The remaining steps must be tailored to each specific situation. Notify law enforcement Secure all necessary records

28 Consider need to: o Stopping access to bank accounts o Terminate network access o Stopping access to certain financial records and/or processes o Securing physical access to items at risk

29 Discuss with City officials advisability of placing individual on administrative leave Don t enter into a restitution agreement with the employee Take notes and write up any pertinent information

30 Questions? Annette Campbell, CPA, CIA, CGFM Deputy Auditor of State

FINANCE COMMITTEE PROCEDURES. Committee Responsibilities. Audit Process

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

1 FINANCE COMMITTEE PROCEDURES Committee Responsibilities The committee is responsible for overseeing financial operations. This includes: 1. Hiring a bookkeeper 2. Preparing a budget 3. Conducting an

Everyone (no matter the size) can have internal controls. By Peter S. Olsen, CPA

can have internal controls. By Peter S. Olsen, CPA") Everyone (no matter the size) can have internal controls By Peter S. Olsen, CPA Introduction This is me.. Agenda 1. Define small nonprofits 2. Detective vs. Preventive controls 3. Discuss the most important

Everyone (no matter the size) can have internal controls By Peter S. Olsen, CPA Introduction This is me.. Agenda 1. Define small nonprofits 2. Detective vs. Preventive controls 3. Discuss the most important

Corridor District of the North Carolina Conference The United Methodist Church

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

State Capitol Building Des Moines, Iowa

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

SANCTIONED GROUPS: POLICY REQUIREMENT

Updated April 19, 2018 P.O. Box 1009 753 Fort Sill Boulevard Lawton Oklahoma 73502-1009 Phone: (580) 357-6900 SANCTIONED GROUPS: Parent groups such as booster clubs and PTAs must be sanctioned EACH YEAR.

Updated April 19, 2018 P.O. Box 1009 753 Fort Sill Boulevard Lawton Oklahoma 73502-1009 Phone: (580) 357-6900 SANCTIONED GROUPS: Parent groups such as booster clubs and PTAs must be sanctioned EACH YEAR.

Board Policy No

Board Policy No. 2015-16-6 Fiscal Policies and Procedures Handbook Created by: TABLE OF CONTENTS Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Contracts... 2 Accounts Payable... 4 Bank Check

Board Policy No. 2015-16-6 Fiscal Policies and Procedures Handbook Created by: TABLE OF CONTENTS Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Contracts... 2 Accounts Payable... 4 Bank Check

Chapter II: Internal Controls II-10

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Chapter II: Internal Controls II-10 Section C. Internal Control Questionnaire The following Internal Control Questionnaire is intended to provide guidance for setting up an accounting system and a checklist

Internal Accounting Control Procedures

Internal Accounting Control Procedures The City of Clearwater wants to ensure public confidence and retain a financially healthy Community. Therefore it is the intent of the Internal Accounting Control

Internal Accounting Control Procedures The City of Clearwater wants to ensure public confidence and retain a financially healthy Community. Therefore it is the intent of the Internal Accounting Control

Procedure REVISION DATE CHAPTER TITLE CHAPTER NO. ADMINISTRATIVE MANUAL Financial & Management 7 MILWAUKEE COUNTY

7.17 IMPREST FUND (Petty Cash) PROCEDURES (1) PURPOSE. To provide a uniform method for replenishing a Petty Cash Imprest Fund for direct disbursements. (2) POLICY. It is the policy of Milwaukee County

7.17 IMPREST FUND (Petty Cash) PROCEDURES (1) PURPOSE. To provide a uniform method for replenishing a Petty Cash Imprest Fund for direct disbursements. (2) POLICY. It is the policy of Milwaukee County

Guidelines for Church Financial Review

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

Guidelines for Church Financial Review Catawba Presbytery - October 2016 The following are suggested procedures to be used by churches when they have their financial review to meet Presbytery/ Synod s

City of Wasco Internal Control Policy

City of Wasco Internal Control Policy 1. Introduction: The City Council of the City of Wasco and City management have a duty to be good fiscal stewards of government assets. This roll of stewardship includes

City of Wasco Internal Control Policy 1. Introduction: The City Council of the City of Wasco and City management have a duty to be good fiscal stewards of government assets. This roll of stewardship includes

BASIC POLICY STATEMENT

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

SAMPLE A Well Known FINANCIAL Philosophy POLICIES For & High PROCEDURES Standards HANDBOOK BASIC POLICY STATEMENT The BEST NONPROFIT, INCORPORATED (BIN) is committed to responsible financial management.

The Episcopal Diocese of Kansas

The Episcopal Diocese of Kansas Internal control and audit standards for parish funds and assets Adopted by the Council of Trustees May 15, 2007; revised September 18, 2007 Purpose: From the Manual of

The Episcopal Diocese of Kansas Internal control and audit standards for parish funds and assets Adopted by the Council of Trustees May 15, 2007; revised September 18, 2007 Purpose: From the Manual of

FISCAL POLICIES AND PROCEDURES

FISCAL POLICIES AND PROCEDURES OVERVIEW The Board of Directors of HARRIET TUBMAN VILLAGE SCHOOL has reviewed and adopted the following policies and procedures to ensure the most effective use of the funds

FISCAL POLICIES AND PROCEDURES OVERVIEW The Board of Directors of HARRIET TUBMAN VILLAGE SCHOOL has reviewed and adopted the following policies and procedures to ensure the most effective use of the funds

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

Exercises: Set B. 28 B-Exercises

28 B-Exercises Identify the principles of internal control. (LO 2), C weaknesses over cash receipts and suggest (LO 2, 3) weaknesses for cash disbursements and suggest (LO 2, 4) (LO 5) Exercises: Set B

28 B-Exercises Identify the principles of internal control. (LO 2), C weaknesses over cash receipts and suggest (LO 2, 3) weaknesses for cash disbursements and suggest (LO 2, 4) (LO 5) Exercises: Set B

2014 ANNUAL FINANCIAL REPORT

Parish/School # 2014 ANNUAL FINANCIAL REPORT Diocese of Des Moines Finance Department Parish/School: City: Contact: Phone: Email: Annual Financial Report Instructions This report covers the fiscal year

Parish/School # 2014 ANNUAL FINANCIAL REPORT Diocese of Des Moines Finance Department Parish/School: City: Contact: Phone: Email: Annual Financial Report Instructions This report covers the fiscal year

ACCOUNTING POLICIES AND PROCEDURES MANUAL

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

Fraud in Nonprofits: Real Stories. Presented by: Mike Hablewitz, CPA, Senior Manager

Fraud in Nonprofits: Real Stories Presented by: Mike Hablewitz, CPA, Senior Manager Fraud Triangle 3 factors are generally present in any fraud: Pressure Rationalization Fraud Triangle! Opportunity Case

Fraud in Nonprofits: Real Stories Presented by: Mike Hablewitz, CPA, Senior Manager Fraud Triangle 3 factors are generally present in any fraud: Pressure Rationalization Fraud Triangle! Opportunity Case

Peralta Community College District AP 6300

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

ADMINISTRATIVE PROCEDURE 6300 GENERAL ACCOUNTING A. Functions The Accounting Office, under the direction of the Vice Chancellor for Finance and Administration and the Associate Vice Chancellor for Finance

Chapter 5. Cash Control Systems

Chapter 5 Cash Control Systems 5-1 Terms checking account: a bank account from which payments can be ordered by a depositor code of conduct: a statement that guides the ethical behavior of a company and

Chapter 5 Cash Control Systems 5-1 Terms checking account: a bank account from which payments can be ordered by a depositor code of conduct: a statement that guides the ethical behavior of a company and

FISCAL MANAGEMENT (Replaces current SBCCD AP 6300)

") 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 AP 6300 AP 6300 San Bernardino Community College District Administrative Procedure

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 AP 6300 AP 6300 San Bernardino Community College District Administrative Procedure

DIOCESE OF ST. PETERSBURG INTERNAL CONTROL QUESTIONNAIRE

DIOCESE OF ST. PETERSBURG - 2016 Parish City, State FISCAL YEAR - JULY 1, 2015 to JUNE 30, 2016 This questionnaire is to be completed by each parish annually. Each question must be answered, and "no" answers

DIOCESE OF ST. PETERSBURG - 2016 Parish City, State FISCAL YEAR - JULY 1, 2015 to JUNE 30, 2016 This questionnaire is to be completed by each parish annually. Each question must be answered, and "no" answers

SPECIFIC PRACTICES Cash Management Page 1

SPEIFI PRATIES 4510 ash Management Page 1 SUBJET: Petty ash and hange Fund Accounts PURPOSE: To describe a procedure for the creation and management of a petty cash or change fund account. DISUSSION: This

SPEIFI PRATIES 4510 ash Management Page 1 SUBJET: Petty ash and hange Fund Accounts PURPOSE: To describe a procedure for the creation and management of a petty cash or change fund account. DISUSSION: This

Toronto Children s Services Operating Criteria. Financial Management Criteria. January 2010

Toronto Children s Services Operating Criteria Financial Management Criteria January 00 FINANCIAL MANAGEMENT CRITERIA For all funded programs: Child Care Centres, Home Child Care Agencies, Special Needs

Toronto Children s Services Operating Criteria Financial Management Criteria January 00 FINANCIAL MANAGEMENT CRITERIA For all funded programs: Child Care Centres, Home Child Care Agencies, Special Needs

Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]

![Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]](/thumbs/84/90567506.jpg "Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]") Diocese of North Carolina Procedures for Audit Committee Revised for the 2014 audit year and forward until such time as Diocesan Council requests a change. Canon 17 Business Methods in Church Affairs [Renumbered

Diocese of North Carolina Procedures for Audit Committee Revised for the 2014 audit year and forward until such time as Diocesan Council requests a change. Canon 17 Business Methods in Church Affairs [Renumbered

BANKING PROCEDURE AND CONTROL OF CASH

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

BANKING PROCEDURE AND CONTROL OF CASH 6-1 Chapter 6 Learning Objectives 1. Depositing, writing, and endorsing checks for a checking account. 2. Reconciling a bank statement. 3. Establishing and replenishing

TABLE OF CONTENTS. Introduction. Required Basic Accounting Records. Internal Control Requirement. Chapter 1--Uniform Chart of Accounts

www.michigan.gov (To Print: use your browser's print function) Release Date: December 18, 2001 Last Update: May 14, 2002 Uniform Accounting Procedures Manual TABLE OF CONTENTS Introduction Required Basic

www.michigan.gov (To Print: use your browser's print function) Release Date: December 18, 2001 Last Update: May 14, 2002 Uniform Accounting Procedures Manual TABLE OF CONTENTS Introduction Required Basic

Money Matters for ALL PTA Leaders

Money Matters for ALL PTA Leaders Pam Grigorian and Nicole Ponziani PTA 2016 Convention Leadership Training Money Matters to the Board Board members are expected to use good business judgement when making

Money Matters for ALL PTA Leaders Pam Grigorian and Nicole Ponziani PTA 2016 Convention Leadership Training Money Matters to the Board Board members are expected to use good business judgement when making

Ch.6 Internal Control and Accounting for Cash

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Ch.6 Internal Control and Accounting for Cash Internal control and its objectives Understand cash and internal control procedures related to cash Accounting for petty cash Combined Journal Prepare a bank

Job Description for Treasurer

Treasurer The treasurer is an elected officer and the authorized custodian of all funds of the local PTA. Some responsibilities of the office are specified in the unit bylaws and others are established

Treasurer The treasurer is an elected officer and the authorized custodian of all funds of the local PTA. Some responsibilities of the office are specified in the unit bylaws and others are established

Safeguarding the Financial Assets of Your Church. Indiana Conference of the United Methodist Church

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist Church July 2012 Safeguarding the Financial Assets of Your Church Indiana Conference of the United Methodist

Internal Controls: Best Practices

Internal Controls: Best Practices Christie Rice Diocese of Des Moines What are internal controls? Systems of checks and balances: Detect errors Discourage/reveal fraud Why do we need them? Maintain accurate

Internal Controls: Best Practices Christie Rice Diocese of Des Moines What are internal controls? Systems of checks and balances: Detect errors Discourage/reveal fraud Why do we need them? Maintain accurate

Accounting Policies and Procedures Manual

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

Managing Community Council Money Self-assessment Tool

Managing Community Council Money Self-assessment Tool This self-assessment tool is divided into key areas for the effective management of community council money: 1. Members 2. Council meetings and minutes

Managing Community Council Money Self-assessment Tool This self-assessment tool is divided into key areas for the effective management of community council money: 1. Members 2. Council meetings and minutes

PTO/Booster Club Financial Guidelines

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

Diocese of Oregon. The Episcopal Church in Western Oregon. Audit Program for Parishes and Missions February 26th, 2011

Diocese of Oregon The Episcopal Church in Western Oregon Audit Program for Parishes and Missions February 26th, 2011 HOW TO USE THIS MANUAL This booklet has been prepared for use as a manual. Please do

Diocese of Oregon The Episcopal Church in Western Oregon Audit Program for Parishes and Missions February 26th, 2011 HOW TO USE THIS MANUAL This booklet has been prepared for use as a manual. Please do

State Capitol Building Des Moines, Iowa

OFFICE OF AUDITOR OF STATE STATE OF IOW A State Capitol Building Des Moines, Iowa 50319-0004 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

OFFICE OF AUDITOR OF STATE STATE OF IOW A State Capitol Building Des Moines, Iowa 50319-0004 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

PRESBYTERY OF CINCINNATI ACCOUNTING POLICIES AND PROCEDURES MANUAL TABLE OF CONTENTS

TABLE OF CONTENTS 1.00 Introduction 3 2.00 Chart of Accounts.. Appendix A 3.00 Division of Duties 4 3.1 Presbytery.. 4 3.2 Treasurer 4 3.3 Business Administrator. 4 3.4 Bookkeeper.. 4 3.5 Administrative

TABLE OF CONTENTS 1.00 Introduction 3 2.00 Chart of Accounts.. Appendix A 3.00 Division of Duties 4 3.1 Presbytery.. 4 3.2 Treasurer 4 3.3 Business Administrator. 4 3.4 Bookkeeper.. 4 3.5 Administrative

OFFICE OF THE STATE AUDITOR

OFFICE OF THE STATE AUDITOR Timothy M Keller Hanover Mutual Domestic Water Consumers Association Independent Accountant s Report on Applying Agreed-Upon For the Year Ended December 31, 2014 Hanover Mutual

OFFICE OF THE STATE AUDITOR Timothy M Keller Hanover Mutual Domestic Water Consumers Association Independent Accountant s Report on Applying Agreed-Upon For the Year Ended December 31, 2014 Hanover Mutual

SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

1203 SALT LAKE COUNTY COUNTYWIDE POLICY ON PETTY CASH AND OTHER IMPREST FUNDS Purpose - Scope - This policy provides procedures for establishing, operating, reconciling, handling discrepancies in, reviewing,

OVERVIEW: Establish Petty Cash or Imprest Funds. Turnover Rate and Increasing or Decreasing Funds

OVERVIEW: A petty cash fund may be established so that cash payments can be made for small, incidental expenses or refunds. An imprest fund is a petty cash fund that has been converted into a checking

OVERVIEW: A petty cash fund may be established so that cash payments can be made for small, incidental expenses or refunds. An imprest fund is a petty cash fund that has been converted into a checking

Cash Operations Training Mary H. Loomis, CPA, Comptroller

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

Cash Operations Training - 2012 Mary H. Loomis, CPA, Comptroller Purpose of the Cash Operations Manual The purpose of the cash operations manual is to consolidate the cash handling/cash operations policies

How to Prevent and Detect Fraud: Implementing Internal Controls

How to Prevent and Detect Fraud: Implementing Internal Controls League of Minnesota Cities 2018 Clerks Orientation Conference June 21, 2018 St. Cloud, Minnesota Mark F. Kerr, JD, CFE Special Investigations

How to Prevent and Detect Fraud: Implementing Internal Controls League of Minnesota Cities 2018 Clerks Orientation Conference June 21, 2018 St. Cloud, Minnesota Mark F. Kerr, JD, CFE Special Investigations

Fundamental Accounting Principles, Volume 1, Fifteenth Canadian Edition

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

Chapter 7 Internal Control and Cash 1) A properly designed internal control system is a key part of systems design, analysis, and performance. Answer: TRUE Diff: 1 Type: TF Topic: 07-02 Purpose of Internal

CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Number: 205.1 Date: February 20, 2008 Section: Budget & Fiscal CONTRA COSTA COUNTY Office of the County Administrator ADMINISTRATIVE BULLETIN SUBJECT: CASH RECEIVING, SAFEGUARDING AND DEPOSITING This bulletin

Healthwatch Brighton and Hove CIC Financial Policy and Procedures

Healthwatch Brighton and Hove CIC Financial Policy and Procedures Agreed 14.01.15 1. Roles and responsibilities 1.1. Observations 1.1.1. There will be appropriate segregation of duties to prevent one person

Healthwatch Brighton and Hove CIC Financial Policy and Procedures Agreed 14.01.15 1. Roles and responsibilities 1.1. Observations 1.1.1. There will be appropriate segregation of duties to prevent one person

Claims Auditing Process Policy

Claims Auditing Process Policy Who is Responsible? Five members of the Common Council are assigned, by the Mayor, to serve on the Audit Committee. The Audit Committee is responsible for auditing claims

Claims Auditing Process Policy Who is Responsible? Five members of the Common Council are assigned, by the Mayor, to serve on the Audit Committee. The Audit Committee is responsible for auditing claims

Solutions. I. Auditing Cash and Cash Equivalents. A. Learning Question Answers

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Solutions I. Auditing Cash and Cash Equivalents A. Learning Question Answers 1. A is correct. As a result, cash and cash equivalents are typically shown in the same financial statement line item on the

Financial Policies and Procedures Government Funds

THE FORT MONROE AUTHORITY FMA-F-001 Financial Policies and Procedures Government Funds Approved by: Chairman, Fort Monroe Authority Board of Trustees Fort Monroe Authority Executive Director Fort Monroe

THE FORT MONROE AUTHORITY FMA-F-001 Financial Policies and Procedures Government Funds Approved by: Chairman, Fort Monroe Authority Board of Trustees Fort Monroe Authority Executive Director Fort Monroe

STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR

REBECCA OTTO STATE AUDITOR STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR SUITE 500 525 PARK STREET SAINT PAUL, MN 55103-2139 (651) 296-2551 (Voice) (651) 296-4755 (Fax) state.auditor@state.mn.us (E-mail)

REBECCA OTTO STATE AUDITOR STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR SUITE 500 525 PARK STREET SAINT PAUL, MN 55103-2139 (651) 296-2551 (Voice) (651) 296-4755 (Fax) state.auditor@state.mn.us (E-mail)

XVI. Financial Policies

XVI. Financial Policies XVI-A: Budget and Finances The Mahomet Public Library has a Board-approved written budget. This budget is developed annually as a cooperative process between the Board s finance

XVI. Financial Policies XVI-A: Budget and Finances The Mahomet Public Library has a Board-approved written budget. This budget is developed annually as a cooperative process between the Board s finance

SOLUTIONS. Learning Goal 25

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

Learning Goal 25: Report and Control Cash S1 Learning Goal 25 Multiple Choice 1. d Bank errors must be an adjustment to the bank balance, not the book balance, even though these items can be added or subtracted

SOLUTIONS TO BRIEF EXERCISES

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 8-1 1. Financial Pressure 2. Rationalization 3. Financial Pressure 4. Opportunity BRIEF EXERCISE 8-2 1. True. 2. True. 3. False. The Sarbanes-Oxley Act requires

SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 8-1 1. Financial Pressure 2. Rationalization 3. Financial Pressure 4. Opportunity BRIEF EXERCISE 8-2 1. True. 2. True. 3. False. The Sarbanes-Oxley Act requires

Audit Committee Certificate

Audit Committee Certificate Date To the Wardens, and Vestry of Parish at Location (City and State). Subject: Review of Financial Records for the Calendar Year We have inspected the statement of financial

Audit Committee Certificate Date To the Wardens, and Vestry of Parish at Location (City and State). Subject: Review of Financial Records for the Calendar Year We have inspected the statement of financial

IMPREST ACCOUNTS. Policy i

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

Table of Contents IMPREST ACCOUNTS Policy 511.1 PURPOSE... 1.4 ESTABLISHMENT... 1.5 PETTY CASH... 1 5.1 USE AND DOCUMENTATION OF PETTY CASH... 1 5.1 PROHIBITED USES... 2 5.2 PETTY CASH REPLENISHMENT...

A Manual for Audit Committees

A Manual for Audit Committees for the Episcopal Church in Vermont Prepared by the Financial Oversight and Audit Committee (Revised May 2010) THE MANUAL FOR AUDIT COMMITTEES OF THE DIOCESE OF VERMONT [THE

A Manual for Audit Committees for the Episcopal Church in Vermont Prepared by the Financial Oversight and Audit Committee (Revised May 2010) THE MANUAL FOR AUDIT COMMITTEES OF THE DIOCESE OF VERMONT [THE

Internal Controls Policy

Internal Controls Policy Purpose. This policy governs the internal controls over the processes of the Sunflower Community Association with respect to the financial and purchasing systems. Financial System.

Internal Controls Policy Purpose. This policy governs the internal controls over the processes of the Sunflower Community Association with respect to the financial and purchasing systems. Financial System.

Cash Management Policy Knox County Housing Authority 216 W. Simmons St. Galesburg, IL (309)

") Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

WASATCH FRONT REGIONAL COUNCIL/WASATCH FRONT ECONOMIC DEVELOPMENT DISTRICT ACCOUNTING AND ADMINISTRATIVE POLICY 10/26/2017 (revised)

") WASATCH FRONT REGIONAL COUNCIL/WASATCH FRONT ECONOMIC DEVELOPMENT DISTRICT ACCOUNTING AND ADMINISTRATIVE POLICY 10/26/2017 (revised) DESIGNATION OF THE TREASURER AND CLERK In compliance with Utah Code

WASATCH FRONT REGIONAL COUNCIL/WASATCH FRONT ECONOMIC DEVELOPMENT DISTRICT ACCOUNTING AND ADMINISTRATIVE POLICY 10/26/2017 (revised) DESIGNATION OF THE TREASURER AND CLERK In compliance with Utah Code

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check.

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

Learning Objectives LO1 Record a deposit on a check stub. LO2 Endorse checks using blank, special, and restrictive endorsements. LO3 Prepare a check stub and a check. Lesson 5-1 How Businesses Use Cash

ACCOUNTS PAYABLE POLICIES AND PROCEDURES...

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

ACCOUNTS PAYABLE POLICIES AND PROCEDURES..... Petty Cash Fund Procedures General Information Establishing a Petty Cash Fund Increasing a Petty Cash Fund Decreasing a Petty Cash Fund Changing a Custodian

SECTION 5 FINANCE AND ACCOUNTING

SECTION 5 FINANCE AND ACCOUNTING 5.01 ACCOUNTING POLICIES It shall be the policy of Collegiate Hall Charter School ( Collegiate Hall ) to create and maintain accounting, billing, and cash control policies,

SECTION 5 FINANCE AND ACCOUNTING 5.01 ACCOUNTING POLICIES It shall be the policy of Collegiate Hall Charter School ( Collegiate Hall ) to create and maintain accounting, billing, and cash control policies,

(385) ; TTY / fax. Scope and Methodology. May 22, 2018

; TTY / fax. Scope and Methodology. May 22, 2018") Salt Lake County Library Services 8030 South 1825 West West Jordan, UT 84088 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

Salt Lake County Library Services 8030 South 1825 West West Jordan, UT 84088 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON MBA, CIA, CFE Chief Deputy Auditor CAJohnson@slco.org

THE CORPORATION OF THE CITY OF WINDSOR POLICY

THE CORPORATION OF THE CITY OF WINDSOR POLICY Primary Owner: Finance Policy No.: CS.A7.07 Secondary Owner: n/a Approval Date: January 21, 2013 1. POLICY Approved By: M20-2013 Subject: Corporate-Wide Cash

THE CORPORATION OF THE CITY OF WINDSOR POLICY Primary Owner: Finance Policy No.: CS.A7.07 Secondary Owner: n/a Approval Date: January 21, 2013 1. POLICY Approved By: M20-2013 Subject: Corporate-Wide Cash

Treasurer 101. Presented by:

Treasurer 101 Presented by: Deadlines and Publications Presented By: Danielle Painter, CMC City Clerk / Treasurer City of New Plymouth Monthly Financial Reporting State Income Tax Withholding is due by

Treasurer 101 Presented by: Deadlines and Publications Presented By: Danielle Painter, CMC City Clerk / Treasurer City of New Plymouth Monthly Financial Reporting State Income Tax Withholding is due by

COUNCIL AUDITOR S OFFICE P R O C E D U R E S S U R R O U N D I N G C I T Y I M P R E S T A C C O U N T S

COUNCIL AUDITOR S OFFICE P R O C E D U R E S S U R R O U N D I N G C I T Y I M P R E S T A C C O U N T S Executive Summary Report #706 Background We performed a series of audits of imprest checking accounts

COUNCIL AUDITOR S OFFICE P R O C E D U R E S S U R R O U N D I N G C I T Y I M P R E S T A C C O U N T S Executive Summary Report #706 Background We performed a series of audits of imprest checking accounts

Table of Contents Executive Summary...1 Objectives...3 Scope...3 Methodology...3 Background...4 Overall Summary...7

Table of Contents Executive Summary...1 This audit addressed the City s imprest funds used for petty cash disbursements and police operations....1 Overall, the imprest funds were adequately accounted for

Table of Contents Executive Summary...1 This audit addressed the City s imprest funds used for petty cash disbursements and police operations....1 Overall, the imprest funds were adequately accounted for

Salt Lake County Library Imprest Fund

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

A Review of the A Report to the Citizens of Salt Lake County, the Mayor, and the County Council Salt Lake County Library Imprest Fund December 2010 Jeff Hatch Salt Lake County Auditor A Review of the

CREIA ACCOUNTING POLICIES AND PROCEDURES

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES Objective: To secure public funds and to protect the staff member, as well as the District, against any type of fraud or misapproation of funds that might

ALAMOGORDO PUBLIC SCHOOLS CASH CONTROL PROCEDURES Objective: To secure public funds and to protect the staff member, as well as the District, against any type of fraud or misapproation of funds that might

MANAGEMENT LETTER. Noncompliance Findings

MANAGEMENT LETTER Village of Boston Heights 45 E. Boston Mills Road Hudson, Ohio 44236 To the Village Council: We have audited the financial statements of the Village of Boston Heights,, Ohio (the Village)

MANAGEMENT LETTER Village of Boston Heights 45 E. Boston Mills Road Hudson, Ohio 44236 To the Village Council: We have audited the financial statements of the Village of Boston Heights,, Ohio (the Village)

TownofGibsland Gibsland, Louisiana. Agreed Upon Procedures For the Period July 1,2006 to December 31,2006

2-2 5" / RECEIVED ATE AUOITjR 2007 MAR -7 PMI2= 12 TownofGibsland Gibsland, Louisiana Agreed Upon Procedures For the Period July 1,2006 to December 31,2006 Under provisions of state law, this report is

2-2 5" / RECEIVED ATE AUOITjR 2007 MAR -7 PMI2= 12 TownofGibsland Gibsland, Louisiana Agreed Upon Procedures For the Period July 1,2006 to December 31,2006 Under provisions of state law, this report is

SOUTHERN CHAUTAUQUA FEDERAL CREDIT UNION ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

SOUTHERN CHAUTAUQUA FEDERAL CREDIT UNION ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and

SOUTHERN CHAUTAUQUA FEDERAL CREDIT UNION ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR AUTHORITY AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A AS

5:31-7 Appendix A LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR AUTHORITY AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A AS

Diocese of Western North Carolina Audit Program Checklist. For use with Audit Committee Audits

Diocese of Western North Carolina Audit Program Checklist Dear Treasurer For use with Audit Committee Audits If you have any questions, comments or suggestions relative to this audit guide, please give

Diocese of Western North Carolina Audit Program Checklist Dear Treasurer For use with Audit Committee Audits If you have any questions, comments or suggestions relative to this audit guide, please give

SHARED SERVICES Office of Financial Services

SHARED SERVICES Services Procedure Title: Procedure Number: Petty Cash DHS OHA-040-017-01 Version: 1.0 Effective Date: 03/28/2014 Jim Scherzinger, DHS Chief Operating Officer Suzanne Hoffman, OHA Chief

SHARED SERVICES Services Procedure Title: Procedure Number: Petty Cash DHS OHA-040-017-01 Version: 1.0 Effective Date: 03/28/2014 Jim Scherzinger, DHS Chief Operating Officer Suzanne Hoffman, OHA Chief

CHAPTER VI: AUDIT GUIDELINES FOR CONGREGATIONS CHAPTER CONTENTS

CHAPTER VI: AUDIT GUIDELINES FOR CONGREGATIONS CHAPTER CONTENTS Introduction...VI-2 Purpose...VI-2 Pre-Audit Advice...VI-2 Reasons for an Audit...VI-2 Approved Auditors...VI-2 The Committee Examination...VI-3

CHAPTER VI: AUDIT GUIDELINES FOR CONGREGATIONS CHAPTER CONTENTS Introduction...VI-2 Purpose...VI-2 Pre-Audit Advice...VI-2 Reasons for an Audit...VI-2 Approved Auditors...VI-2 The Committee Examination...VI-3

STAGNI & COMPANY, LLC

CERTIFIED PUBLIC ACCOUNTANTS & CONSULTANTS AGREED-UPON PROCEDURES REPORT Lafourche Parish Government Independent Accountant s Report On Applying Agreed-Upon Procedures For the Period January 1, 2017 December

CERTIFIED PUBLIC ACCOUNTANTS & CONSULTANTS AGREED-UPON PROCEDURES REPORT Lafourche Parish Government Independent Accountant s Report On Applying Agreed-Upon Procedures For the Period January 1, 2017 December

Audit Program for Cash

Form AP 10 Index Reference Audit Program for Cash Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Form AP 10 Index Reference Audit Program for Cash Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Accounting Terms Chap 1-8

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

Accounting Terms Chap - TERM DEFINITION CHAPTER Account Account balance A record that summarizes all the transactions pertaining to a single item in the equation. The difference between the increases and

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan. August 10, 1998

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan August 10, 1998 County Treasurer's Responsibility for Trust Accounts Prepared by Richard L. Baldermann,

MICHIGAN ASSOCIATION OF COUNTY TREASURERS Summer Conference Amway Grand Hotel Grand Rapids, Michigan August 10, 1998 County Treasurer's Responsibility for Trust Accounts Prepared by Richard L. Baldermann,

County of Chester. Office of the Prothonotary. Management Letter. Valentino F. DiGiorgio, III, Controller

County of Chester Office of the Prothonotary Management Letter Valentino F. DiGiorgio, III, Controller To: Bryan Walters, Prothonotary Introduction On April 30, 2013, Internal Audit completed an audit

County of Chester Office of the Prothonotary Management Letter Valentino F. DiGiorgio, III, Controller To: Bryan Walters, Prothonotary Introduction On April 30, 2013, Internal Audit completed an audit

26 PTA Audit. Overview. The Purpose of an Audit. Compiled Financial Statements

PTA Audit Overview Auditing involves examining financial records and transactions to ensure that receipts have been properly accounted for and expenditures have been properly authorized and recorded in

PTA Audit Overview Auditing involves examining financial records and transactions to ensure that receipts have been properly accounted for and expenditures have been properly authorized and recorded in

Chapter 5: Cash Control Systems

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

Chapter 5: Cash Control Systems Goals of Chapter 5: Define accounting terms related to using a checking account and a petty cash fund Identify accounting concepts and practices related to using a checking

STATE OF MINNESOTA Office of the State Auditor

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

Fraud in the Government Realm. Introduction. What is Fraud? My career began with a local government fraud in 1993

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

Fraud in the Government Realm Introduction My career began with a local government fraud in 1993 2 What is Fraud? 3 1 Two Types of Fraud 4 Fraud Do not be think it is not happening 5 Your employees? 6

GENERAL ACCOUNTING POLICIES AND PROCEDURES MANUAL

Los Angeles Leadership Academy 2670 Griffin Avenue, Los Angeles, CA 90031 Ph. 213.381.8484 www.laleadership.org GENERAL ACCOUNTING POLICIES AND PROCEDURES MANUAL ACCOUNTING POLICIES Board Approved 09/09/2015

Los Angeles Leadership Academy 2670 Griffin Avenue, Los Angeles, CA 90031 Ph. 213.381.8484 www.laleadership.org GENERAL ACCOUNTING POLICIES AND PROCEDURES MANUAL ACCOUNTING POLICIES Board Approved 09/09/2015

Proper Controls and Handling of Cash

ARCHDIOCESE OF ST. LOUIS Proper Controls and Handling of Cash Best Practices Best Practices for Cash Handling and Management for Parishes This document serves to provide some best practices for cash handling

ARCHDIOCESE OF ST. LOUIS Proper Controls and Handling of Cash Best Practices Best Practices for Cash Handling and Management for Parishes This document serves to provide some best practices for cash handling

Resident Funds Management System ONLINE

Table of Contents Table of ContentsGetting Started... 1 Getting Started... 4 Overview... 4 Contact National Datacare... 5 Send Data... 5 Service Benefits... 6 What's New... 6 RFMS Concepts... 7 Direct

Table of Contents Table of ContentsGetting Started... 1 Getting Started... 4 Overview... 4 Contact National Datacare... 5 Send Data... 5 Service Benefits... 6 What's New... 6 RFMS Concepts... 7 Direct

Diocese of Madison. Policy for Parish Cash Management. A. Bank Accounts and Their Security

Diocese of Madison Policy for Parish Cash Management The handling of cash is a primary concern of financial control in any organization. Therefore, establishing good procedures and internal controls for

Diocese of Madison Policy for Parish Cash Management The handling of cash is a primary concern of financial control in any organization. Therefore, establishing good procedures and internal controls for

Policy and Procedure Manual

Policy and Procedure Manual Financial (FN) Table of Contents FN-01 FN-02 FN-03 FN-04 FN-05 FN-06 FN-07 FN-08 FN-09 FN-10 FN-11 FN-12 FN-13 FN-14 FN-15 FN-16 FN-17 FN-18 FN-19 FN-20 Chart of Accounts Insurance

Policy and Procedure Manual Financial (FN) Table of Contents FN-01 FN-02 FN-03 FN-04 FN-05 FN-06 FN-07 FN-08 FN-09 FN-10 FN-11 FN-12 FN-13 FN-14 FN-15 FN-16 FN-17 FN-18 FN-19 FN-20 Chart of Accounts Insurance

Parish Financial System

Parish Financial System 1. Financial Objectives A. The parish must establish a financial system that will accomplish the following objectives: 1) Identify, record and report all transactions of the parish

Parish Financial System 1. Financial Objectives A. The parish must establish a financial system that will accomplish the following objectives: 1) Identify, record and report all transactions of the parish

Town of Cross Plains, Wisconsin Accounting Procedures

Town of Cross Plains, Wisconsin Accounting Procedures Introduction The Board is responsible for establishing policies and procedures that govern the financial practices to be followed by the Town Clerk,

Town of Cross Plains, Wisconsin Accounting Procedures Introduction The Board is responsible for establishing policies and procedures that govern the financial practices to be followed by the Town Clerk,

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

LA s Promise Charter Schools Fiscal Policies & Procedures Approved by the Board of Directors, June 9, 2016

LA s Promise Charter Schools Approved by the Board of Directors, June 9, 2016 ver.20160609 LA s Promise Charter Schools Table of Contents Introduction... 1 Accounting Procedures... 1 Basis of Accounting...

LA s Promise Charter Schools Approved by the Board of Directors, June 9, 2016 ver.20160609 LA s Promise Charter Schools Table of Contents Introduction... 1 Accounting Procedures... 1 Basis of Accounting...

South Carolina Department of Transportation Division of Intermodal & Freight Programs. Human Service Provider Compliance and Oversight Questionnaire

South Carolina Department of Transportation Division of Intermodal & Freight Programs Human Service Provider Compliance and Oversight Questionnaire Fiscal Year(s): July 1, 2016 present AGENCY NAME OFFICE

South Carolina Department of Transportation Division of Intermodal & Freight Programs Human Service Provider Compliance and Oversight Questionnaire Fiscal Year(s): July 1, 2016 present AGENCY NAME OFFICE

Beans and Rice, Inc. ACCOUNTING POLICIES AND PROCEDURES MANUAL

Beans and Rice, Inc. ACCOUNTING POLICIES AND PROCEDURES MANUAL TABLE OF CONTENTS 1.00 BACKGROUND INFORMATION 1.01 Tax Status and Purpose... 1 1.02 Service Area... 1 2.00 CHART OF ACCOUNTS 2.01 Assets...

Beans and Rice, Inc. ACCOUNTING POLICIES AND PROCEDURES MANUAL TABLE OF CONTENTS 1.00 BACKGROUND INFORMATION 1.01 Tax Status and Purpose... 1 1.02 Service Area... 1 2.00 CHART OF ACCOUNTS 2.01 Assets...