Documentation / Other important Standards with SME perspective

|

|

|

- Wilfred Chase

- 5 years ago

- Views:

Transcription

1 Dcumentatin / Other imprtant Standards with SME perspective

2 SME -

3 Definitin f MSMEs in India (As Per Micr, Small & Medium Enterprises Develpment (MSMED) Act, 2006) Manufacturing Enterprises Investment in Plant & Machinery Descriptin INR USD($) Micr Enterprises Upt Rs. 25 Lakh Upt $ 62,500 Small Enterprises Abve Rs. 25 Lakh & upt Rs. 5 Crre Abve $ 62,500 & upt $ 1.25 millin Medium Enterprises Abve Rs. 5 Crre & upt Rs. 10 Crre Abve $ 1.25 millin & upt $ 2.5 millin Service Enterprises Investment in Equipment Descriptin INR USD($) Micr Enterprises Upt Rs. 10 Lakh Upt $ 25,000 Small Enterprises Abve Rs. 10 Lakh & upt Rs. 2 Crre Abve $ 25,000 & upt $ 0.5 millin Medium Enterprises Abve Rs. 2 Crre & upt Rs. 5 Crre Abve $ 0.5 millin & upt $ 1.5 millin

4 SA ensure & enhance quality f audit engagements Preface t the Statements n Standard Auditing Practices issued by ICAI states While discharging the attest functin, it is the duty f the members f ICAI t ensure that the Standards are fllwed in the audit f financial infrmatin cvered by the audit reprt. If fr any reasn a member has nt been able t perfrm an audit in accrdance with the same, his reprt shuld draw attentin t the material departures therefrm The same finds its relevance in The Chartered Accuntants Act, 1949 / Cde f Ethics Peer Review / Financial Reprting Review Bard (FRRB) Quality Review Bard (QRB) / Disciplinary Mechanism SA deals with respnsibilities f the auditr & it s applicatin t specific areas. SA cntains guidance & ther explanatry material.

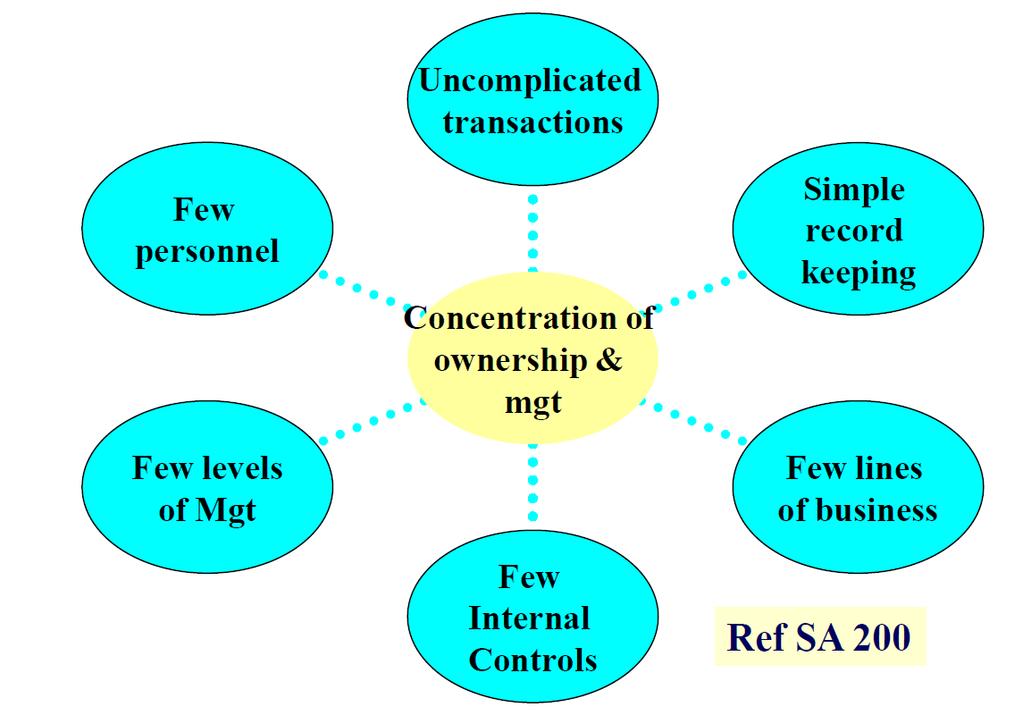

5 Cnsideratins in Audits f SMEs Differences between SMEs and larger entities shuld be recgnized Scalability i.e. Audit apprach may vary with circumstances (simpler/mre cmplex) Requirements d nt usually specify audit prcedures Prfessinal judgment needs t applied Applicatin f SAs designed t be prprtinate Apply prprtinate t audit circumstances, level f cmplexity, nature f audit Prprtinality mdificatin f requirements

6 Hw d SAs demnstrate prprtinality? Thrugh the requirements: SA 260, where management = TCWG in case f SME, unlike larger enterprise. SA 315 & SA 330 (risk based), absence f frmal risk assessment prcess E.g. In case f SME, test f details wuld have mre preference rather than cntrl SA 540 (Estimates), Estimates enable in pting fr chice f respnses t assessed risks SA 550 (Related parties), inspectin f recrds r dcuments Auditr t rely mre n enquiry, inspectin & bservatin rather than mere scrutiny f financial transactins. Thrugh the applicatin material: Many cnsideratins specific t smaller entities Other guidance, e.g. frm and fcus f cmmunicatin with TCWG

7 Is cmpliance with all SAs required? Basic bligatin is t cmply with all SAs relevant t the audit Nt all SAs may be relevant. Fr example SA 402, if SME des nt use a service rganizatin SA 501, if SME des nt have any inventry SA 600, if SME audit is nt a grup audit SA 610, if SME has n internal audit functin Cnditinal requirements need nt be applied if cnditins d nt exist [SA 240]

8 SA 230: Dcumentatin - Nature & Purpse The skills f an accuntant can always be ascertained by an inspectin f his wrking papers - Rbert H Mntgmery, Mntgmery s Auditing, 1912

9 Dcumentatin Critical cmpnent f audit evidence Dcument is any material that prvides evidence f wrk perfrmed that enables the Auditr t satisfy himself Apprpriate dcumentatin need nt be burdensme Reinfrcing quality Be prprtinate, efficient and effective Experienced auditr test Cautin against checklist mentality Imprtance f exercising prfessinal judgment Illustratins f hw dcumentatin can be dne in efficient & effective manner Objective T prepare dcumentatin that prvides Sufficient & apprpriate recrd f the basis f the auditr s reprt. Evidence that audit was planned & perfrmed in accrdance with SAs & Applicable Legal & Regulatry requirements

10 Definitins Wrk papers signed agreements written representatins spreadsheets vides pictures transcripts crrespndences etc Audit dcumentatin Recrd f audit prcedures perfrmed, relevant audit evidence btained, & cnclusins the auditr reached (terms such as wrking papers r wrk-papers are als smetimes used). Audit file 1 r mre flders r ther strage media, in physical r electrnic frm, cntaining recrds that cmprise the audit dcumentatin fr a specific engagement. Experienced auditr An individual (whether internal r external t the firm) wh has practical audit experience, and a reasnable understanding f: Audit prcesses; / SAs & applicable legal - regulatry requirements; Business envirnment in which the entity perates; and Auditing & financial reprting issues relevant t the entity s industry

11 D we knw what we d nt knw Hw much t dcument? Enugh t Assist in planning and perfrming / Recrd matters f cntinuing significance Create accuntability / Assist external inspectin Assist supervisin and directin - Quality cntrl review When t dcument? Timely manner (dcuments prepared after audit are less accurate) Within 60 days f cmpletin f audit (SQC 1) - Retain fr 7 years frm date f audit reprt Implementatin Guide t SA 230 March Case studies Appendix cntaining Illustrative Wrking paper Frmat

12 Other Matters Departure frm a Relevant Requirement - If, in exceptinal circumstances, the auditr judges it necessary t depart frm a relevant requirement in a SA, the auditr shall dcument hw the alternative audit prcedures perfrmed achieve the aim f that requirement, and the reasns fr the departure Matters Arising after the Date f the Auditr s Reprt If, in exceptinal circumstances, the auditr perfrms new r additinal audit prcedures r draws new cnclusins after the date f the auditr s reprt, the auditr shall dcument: The circumstances encuntered; The new r additinal audit prcedures perfrmed, audit evidence btained, and Cnclusins reached, and their effect n the auditr s reprt; and When and by whm the resulting changes t audit dcumentatin were made and reviewed

13 Audit Dcumentatin is nt a substitute fr the entity s accunting recrds Extent f Dcumentatin depends n varius factrs such as Risk Assessment sampling Methds used & Materiality Permanent Audit File / Current audit File Cntains Relevant risks & cntrls applicable t an area assertins t be tested & satisfied Substantive & analytical prcedures perfrmed Physical r Electrnic Frm Hard r Sft cpy Audit Plan / Engagement Letter / Qualified pinin Dcuments relating t the use f prfessinal judgment Deleting / Discarding ld superseded infrmatin Retentin f Recrds 7 years as per SQC-1

14 Dcumentatins under ther SAs SA 200: Basic Principles Gverning an Audit Evidence that the audit was carried ut in accrdance with the basic principles SA 220: Quality Cntrl fr Audit Wrk Audit evidence btained frm substantive prcedures & the cnclusins drawn therefrm, including the results f cnsultatins SA 240: The Auditrs respnsibilities relating t fraud in an audit f FS Understanding f the entity & envirnment, assessment f the risks f material misstatement required by SA 315 Management s respnse & cmmunicatin t TCWG Regulatry requirements like Cmpanies Act, 2013, RBI etc. Reasns fr cnclusin & reprting SA 250: Cnsideratin f Laws and Regulatins in an audit f FS Varius checklists e.g. Cmpanies Act, IGAAP, RBI & NHB, Crprate Gvernance etc. SA 260: Cmmunicatin with thse charged with Gvernance Oral, , frmal cmmunicatin, Audit cmmittee presentatins & management letters (retentin f cpy)

15 Dcumentatins under ther SAs (cntd.) SA 299: Respnsibility f Jint Auditrs Jint respnsibility statement SA 300: Planning an Audit f financial statements Pre audit meeting, verall audit strategy, plan & significant changes & reasns SA 315: Identifying and assessing the risk f material misstatement thrugh understanding the entity and Its Envirnment Discussin amng the engagement team and the significant decisins reached; Understanding f the entity s envirnment and internal cntrl (IC) cmpnents; Surces f infrmatin frm which the understanding was btained; Risk assessment prcedures perfrmed; Identified & assessed risks f material misstatement at the FS level and at the assertin level; Risks identified, and related cntrls abut which the auditr has btained an understanding Reprting n IFC ver FS u/s 143 (3) (i) f the Cmpanies Act, 2013

16 Dcumentatins under ther SAs (cntd.) SA 320: Materiality in Planning and Perfrming an Audit Audit dcs shall include the fllwing amunts & the factrs cnsidered in their determinatin: Materiality fr the FS as a whle (verall) If applicable, the materiality level r levels fr particular classes f transactins, accunt balances r disclsure; Perfrmance materiality; and Any revisin f materiality levels as the audit prgressed & reasns theref. SA 330: Auditr s Respnse t Assessed Risks The verall respnses t address the assessed risks f material misstatement at the FS level, and the nature, timing and extent f the further audit prcedures perfrmed; The linkage f thse prcedures with the assessed risks at the assertin level; and The results f the audit prcedures, including the cnclusins where these are nt therwise clear. Cnclusins reached abut the perating effectiveness f IC in case the auditr has relied upn such test carried ut in previus audit perids. The auditrs dcumentatin shall demnstrate that the financial statements agree r recncile with the underlying accunting recrds.

17 Dcumentatins under ther SAs (cntd.) SA 505: External Cnfirmatins If the auditr agrees t management's request nt t seek external cnfirmatin regarding a particular matter, the auditr shuld dcument the reasns fr acceding t the management s request. SA 540: Auditing Accunting Estimates The basis fr the auditr s cnclusins abut the reasnableness f accunting estimates and their disclsure that give rise t significant risks; and Indicatrs f pssible management bias, if any SA 550: Related Parties Auditr shall include the names f the identified related parties and the nature f the related party relatinships. SA 580: Written Representatins Auditr is required t dcument identificatin f significant issues relating t the cmpetence, integrity, ethical values r diligence f management r abut its cmmitment t r enfrcement f these. Matters where auditr has relied upn the management s explanatin and infrmatin.

18 Dcumentatins under ther SAs (cntd.) SA 600: Using the wrk f Anther Auditr Cmpnents whse financial infrmatin was audited by ther auditrs & their significance t financial infrmatin f the entity as a whle; names f ther auditrs; cnclusins reached that individual cmpnents are nt material. Prcedures perfrmed and cnclusins reached regarding cmpnents. Fr example, auditr wuld dcument the results f discussins with ther auditr and review f written summary f ther auditr s prcedures. Any limiting prcedures Cnclusins reached Manner f dealing with mdified reprt f OA while finalizing the PA s reprt SA 610: Using the Wrk Of Internal Auditr When the external auditr uses specific wrk f the internal auditrs, the external auditr shall dcument cnclusins regarding the evaluatin f the adequacy f the wrk f the internal auditrs, and the audit prcedures perfrmed by the external auditr n that wrk

19 Cntrl Activities Relevant t Audit (CARA) Imprtant: Relevance t Auditrs understanding assessing risk & subsequent respnse i.e. SME cnsideratins Same cncepts less frmal Sme may nt be relevant direct wner versight Relate mainly t transactin cycles

SRI LANKA AUDITING STANDARD 580 WRITTEN REPRESENTATIONS CONTENTS

SRI LANKA AUDITING STANDARD 580 WRITTEN REPRESENTATIONS (Effective fr audits f financial statements fr perids beginning n r after 01 January 2014) CONTENTS Paragraph Intrductin Scpe f this SLAuS... 1-2

SRI LANKA AUDITING STANDARD 580 WRITTEN REPRESENTATIONS (Effective fr audits f financial statements fr perids beginning n r after 01 January 2014) CONTENTS Paragraph Intrductin Scpe f this SLAuS... 1-2

Written Representations

SINGAPORE STANDARD ON AUDITING SSA 580 Written Representatins This revised and redrafted SSA 580 supersedes SSA 580 Management Representatins in August 2008. Auditrs are required t cmply with the auditing

SINGAPORE STANDARD ON AUDITING SSA 580 Written Representatins This revised and redrafted SSA 580 supersedes SSA 580 Management Representatins in August 2008. Auditrs are required t cmply with the auditing

International Standard on Review Engagements (ISRE) 2400 (Revised), Engagements to Review Historical Financial Statements

2400 (Revised), Engagements to Review Historical Financial Statements") AT A GLANCE September 2012 Internatinal Standard n Review Engagements (ISRE) 2400 (Revised), Engagements t Review Histrical Financial Statements This summary prvides an verview f ISRE 2400 (Revised), Engagements

AT A GLANCE September 2012 Internatinal Standard n Review Engagements (ISRE) 2400 (Revised), Engagements t Review Histrical Financial Statements This summary prvides an verview f ISRE 2400 (Revised), Engagements

International Standard on Auditing (Ireland) 265. Communicating Deficiencies in Internal Control to Those Charged with Governance and Management

265. Communicating Deficiencies in Internal Control to Those Charged with Governance and Management") Internatinal Standard n Auditing (Ireland) 265 Cmmunicating Deficiencies in Internal Cntrl t Thse Charged with Gvernance and Management MISSION T cntribute t Ireland having a strng regulatry envirnment

Internatinal Standard n Auditing (Ireland) 265 Cmmunicating Deficiencies in Internal Cntrl t Thse Charged with Gvernance and Management MISSION T cntribute t Ireland having a strng regulatry envirnment

International Standard on Auditing (UK) 265

265") Standard Audit and Assurance Financial Reprting Cuncil June 2016 Internatinal Standard n Auditing (UK) 265 Cmmunicating Defi ciencies in Internal Cntrl t Thse Charged With Gvernance and Management The

Standard Audit and Assurance Financial Reprting Cuncil June 2016 Internatinal Standard n Auditing (UK) 265 Cmmunicating Defi ciencies in Internal Cntrl t Thse Charged With Gvernance and Management The

Huntington Bancshares Incorporated

Audit Cmmittee Apprved By: Bard f Directrs Huntingtn Bancshares Incrprated Apprval Date 1 f 6 Purpse f Cmmittee The Audit Cmmittee (Cmmittee) is established by the Bard f Directrs (Bard) t assist the Bard

Audit Cmmittee Apprved By: Bard f Directrs Huntingtn Bancshares Incrprated Apprval Date 1 f 6 Purpse f Cmmittee The Audit Cmmittee (Cmmittee) is established by the Bard f Directrs (Bard) t assist the Bard

Using the Work of an Auditor s Expert

SINGAPORE STANDARD ON AUDITING SSA 620 Using the Wrk f an Auditr s Expert This SSA 620 supersedes SSA 620 Using the Wrk f an Expert in September 2009. Auditrs are required t cmply with the auditing standards

SINGAPORE STANDARD ON AUDITING SSA 620 Using the Wrk f an Auditr s Expert This SSA 620 supersedes SSA 620 Using the Wrk f an Expert in September 2009. Auditrs are required t cmply with the auditing standards

Audit Committee Charter. St Andrew s Insurance (Australia) Pty Ltd St Andrew s Life Insurance Pty Ltd St Andrew s Australia Services Pty Ltd

Pty Ltd St Andrew s Life Insurance Pty Ltd St Andrew s Australia Services Pty Ltd") Audit Cmmittee Charter St Andrew s Insurance (Australia) Pty Ltd St Andrew s Life Insurance Pty Ltd St Andrew s Australia Services Pty Ltd Versin 3.0, 19 February 2018 Apprver Bard f Directrs St Andrew

Audit Cmmittee Charter St Andrew s Insurance (Australia) Pty Ltd St Andrew s Life Insurance Pty Ltd St Andrew s Australia Services Pty Ltd Versin 3.0, 19 February 2018 Apprver Bard f Directrs St Andrew

Internal Control Requirements for Adopting New Accounting Standards

Internal Cntrl Requirements fr Adpting New Accunting Standards Backgrund In previus articles, BKD discussed the U.S. Securities and Exchange Cmmissin s (SEC) expectatins regarding the requirement t disclse

Internal Cntrl Requirements fr Adpting New Accunting Standards Backgrund In previus articles, BKD discussed the U.S. Securities and Exchange Cmmissin s (SEC) expectatins regarding the requirement t disclse

THE CLOROX COMPANY AUDIT COMMITTEE CHARTER. [Effective May 8, 2017]

![THE CLOROX COMPANY AUDIT COMMITTEE CHARTER. [Effective May 8, 2017]](/thumbs/79/78951181.jpg "THE CLOROX COMPANY AUDIT COMMITTEE CHARTER. [Effective May 8, 2017]") THE CLOROX COMPANY AUDIT COMMITTEE CHARTER [Effective May 8, 2017] PURPOSE AND AUTHORITY The Audit Cmmittee ( Cmmittee ) is established by the Bard f Directrs ( Bard ) fr the purpses f: 1. Representing

THE CLOROX COMPANY AUDIT COMMITTEE CHARTER [Effective May 8, 2017] PURPOSE AND AUTHORITY The Audit Cmmittee ( Cmmittee ) is established by the Bard f Directrs ( Bard ) fr the purpses f: 1. Representing

Audit Committee Charter

Audit Cmmittee Charter I. Purpse f Audit Cmmittee The purpse f the Audit Cmmittee, which is part f the Bard, shall be (a) t assist the Bard s versight f (i) the integrity f the Cmpany s financial statements,

Audit Cmmittee Charter I. Purpse f Audit Cmmittee The purpse f the Audit Cmmittee, which is part f the Bard, shall be (a) t assist the Bard s versight f (i) the integrity f the Cmpany s financial statements,

Communication with Those Charged with Governance

HKSA 260 (Revised) Issued August 2015; revised January 2016, June 2017 Effective fr audits f financial statements fr perids ending n r after 15 December 2016 Hng Kng Standard n Auditing 260 (Revised) Cmmunicatin

HKSA 260 (Revised) Issued August 2015; revised January 2016, June 2017 Effective fr audits f financial statements fr perids ending n r after 15 December 2016 Hng Kng Standard n Auditing 260 (Revised) Cmmunicatin

Select Auditing Considerations for the 2013 Audit Cycle

Select Auditing Cnsideratins fr the 2013 Audit Cycle This Alert is intended t remind member firms f certain auditing cnsideratins that may be relevant fr the 2013 audit cycle. The Alert identifies and

Select Auditing Cnsideratins fr the 2013 Audit Cycle This Alert is intended t remind member firms f certain auditing cnsideratins that may be relevant fr the 2013 audit cycle. The Alert identifies and

AUDIT, RISK MANAGEMENT AND COMPLIANCE COMMITTEE CHARTER

AUDIT, RISK MANAGEMENT AND COMPLIANCE COMMITTEE CHARTER August 2012 OPUS Grup Limited Audit, Risk Management and Cmpliance Cmmittee 1. GENERAL PURPOSE The primary bjective f the Audit, Risk Management

AUDIT, RISK MANAGEMENT AND COMPLIANCE COMMITTEE CHARTER August 2012 OPUS Grup Limited Audit, Risk Management and Cmpliance Cmmittee 1. GENERAL PURPOSE The primary bjective f the Audit, Risk Management

PROPOSED INTERNATIONAL STANDARD ON AUDITING (ISA) 260 (REVISED) COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE

260 (REVISED) COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE") PROPOSED INTERNATIONAL STANDARD ON AUDITING (ISA) 260 (REVISED) COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective fr audits f financial statements fr perids [beginning/ending n r after date December

PROPOSED INTERNATIONAL STANDARD ON AUDITING (ISA) 260 (REVISED) COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective fr audits f financial statements fr perids [beginning/ending n r after date December

DRAFT AUDITOR S RESPONSIBILITY UNDER AUDITING STANDARDS GENERALLY ACCEPTED IN THE UNITED STATES OF AMERICA

Finance and Audit Cmmittee Kentucky Cmmunity and Technical Cllege System Fundatin, Inc. Versailles, Kentucky Prfessinal standards require that we cmmunicate certain matters t keep yu adequately infrmed

Finance and Audit Cmmittee Kentucky Cmmunity and Technical Cllege System Fundatin, Inc. Versailles, Kentucky Prfessinal standards require that we cmmunicate certain matters t keep yu adequately infrmed

Audit and Risk Management Committee Charter

Audit and Risk Management Cmmittee Charter Pivtal Systems Crpratin ("Cmpany") 1. Objectives The Audit and Risk Management Cmmittee (Cmmittee) has been established by the bard f directrs (Bard) f the Cmpany.

Audit and Risk Management Cmmittee Charter Pivtal Systems Crpratin ("Cmpany") 1. Objectives The Audit and Risk Management Cmmittee (Cmmittee) has been established by the bard f directrs (Bard) f the Cmpany.

Chapter 1. Introduction and Overview of Audit & Assurance

Assurance & Auditing Textbk Ntes Chapter 1 Intrductin and Overview f Audit & Assurance Audit prcess in Fcus 1.1 Auditing & Assurance Defined - An assurance is an engagement where an auditr r cnsultant

Assurance & Auditing Textbk Ntes Chapter 1 Intrductin and Overview f Audit & Assurance Audit prcess in Fcus 1.1 Auditing & Assurance Defined - An assurance is an engagement where an auditr r cnsultant

Written Representations

HKSA 580 Issued July 2009; revised July 2010, June 2014, August 2015, January 2016, August 2016, June 2017 Effective fr audits f financial statements fr perids beginning n r after 15 December 2009 Hng

HKSA 580 Issued July 2009; revised July 2010, June 2014, August 2015, January 2016, August 2016, June 2017 Effective fr audits f financial statements fr perids beginning n r after 15 December 2009 Hng

Using the Work of an Auditor s Expert

HKSA 620 Issued July 2009; revised July 2010 Effective fr audits f financial statements fr perids beginning n r after 15 December 2009 Hng Kng Standard n Auditing 620 Using the Wrk f an Auditr s Expert

HKSA 620 Issued July 2009; revised July 2010 Effective fr audits f financial statements fr perids beginning n r after 15 December 2009 Hng Kng Standard n Auditing 620 Using the Wrk f an Auditr s Expert

GENERAL MOTORS COMPANY AUDIT COMMITTEE CHARTER. Amended and Restated: December 13, 2017

GENERAL MOTORS COMPANY AUDIT COMMITTEE CHARTER Amended and Restated: December 13, 2017 Purpse The purpse f the Audit Cmmittee is t assist the Bard f Directrs f General Mtrs Cmpany in its versight f the

GENERAL MOTORS COMPANY AUDIT COMMITTEE CHARTER Amended and Restated: December 13, 2017 Purpse The purpse f the Audit Cmmittee is t assist the Bard f Directrs f General Mtrs Cmpany in its versight f the

TERMS OF REFERENCE FOR THE PROVISION OF OUTSOURCED INTERNAL AUDIT SERVICE

W&RSETA Standard Bidding Dcuments Terms f Reference TERMS OF REFERENCE FOR THE PROVISION OF OUTSOURCED INTERNAL AUDIT SERVICE 1 W&RSETA Standard Bidding Dcuments Terms f Reference 1. BACKGROUND TO W&RSETA

W&RSETA Standard Bidding Dcuments Terms f Reference TERMS OF REFERENCE FOR THE PROVISION OF OUTSOURCED INTERNAL AUDIT SERVICE 1 W&RSETA Standard Bidding Dcuments Terms f Reference 1. BACKGROUND TO W&RSETA

TERMS OF REFERENCE. Audit and Risk Committee (the "Committee") of Wilmcote Holdings Plc (the "Company")

of Wilmcote Holdings Plc (the Company)") References t the "Bard" shall mean the full Bard f Directrs. MEMBERSHIP - The Bard has reslved t establish a cmmittee f the Bard t be knwn as the Audit and Risk Cmmittee. - The Cmmittee shall cmprise at

References t the "Bard" shall mean the full Bard f Directrs. MEMBERSHIP - The Bard has reslved t establish a cmmittee f the Bard t be knwn as the Audit and Risk Cmmittee. - The Cmmittee shall cmprise at

A0aa. Assertions that the auditor may use in addressing the requirements of this ISA are further described in paragraph A121c.

Agenda Item 3-B ISA 315 (Revised), 1 Identifying and Assessing the Risks f Material Misstatement thrugh Understanding the Entity and Its Envirnment Applicatin and Other Explanatry Material Prpsed changes

Agenda Item 3-B ISA 315 (Revised), 1 Identifying and Assessing the Risks f Material Misstatement thrugh Understanding the Entity and Its Envirnment Applicatin and Other Explanatry Material Prpsed changes

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER WBHO Audit Cmmittee Charter Page 1 f 9 Intrductin The Audit Cmmittee is cnstituted as a statutry cmmittee f the Cmpany in respect f its statutry duties in terms f Sectin 94(1) f

AUDIT COMMITTEE CHARTER WBHO Audit Cmmittee Charter Page 1 f 9 Intrductin The Audit Cmmittee is cnstituted as a statutry cmmittee f the Cmpany in respect f its statutry duties in terms f Sectin 94(1) f

Audit & Risk Committee Charter

Audit & Risk Cmmittee Charter AUDIT & RISK COMMITTEE CHARTER The Audit & Risk Cmmittee has been established by reslutin f the Bard f Macmahn Hldings Limited ( Macmahn r the Cmpany ). Membership The Audit

Audit & Risk Cmmittee Charter AUDIT & RISK COMMITTEE CHARTER The Audit & Risk Cmmittee has been established by reslutin f the Bard f Macmahn Hldings Limited ( Macmahn r the Cmpany ). Membership The Audit

AUDIT & RISK COMMITTEE CHARTER

AUDIT & RISK COMMITTEE CHARTER Rle and Respnsibilities The Bard f The Institute f Internal Auditrs Australia (IIA-Australia) has established a Bard Audit & Risk Cmmittee as part f its respnsibilities in

AUDIT & RISK COMMITTEE CHARTER Rle and Respnsibilities The Bard f The Institute f Internal Auditrs Australia (IIA-Australia) has established a Bard Audit & Risk Cmmittee as part f its respnsibilities in

FINANCE & AUDIT COMMITTEE

FINANCE & AUDIT COMMITTEE Page 1 f 8 CHARTER f the Finance & Audit Cmmittee f the Bard Of Directrs f Spectral Medical Inc. Purpse The primary functin f the Finance & Audit Cmmittee (the Cmmittee ) f the

FINANCE & AUDIT COMMITTEE Page 1 f 8 CHARTER f the Finance & Audit Cmmittee f the Bard Of Directrs f Spectral Medical Inc. Purpse The primary functin f the Finance & Audit Cmmittee (the Cmmittee ) f the

Terms of Reference - Board of Directors (approved by the Board on 12 April 2018)

") Terms f Reference - Bard f Directrs (apprved by the Bard n 12 April 2018) 1. Respnsibility and Principal Duties The Bard f Directrs has the verall respnsibility fr the gvernance f the Cmpany and fr supervising

Terms f Reference - Bard f Directrs (apprved by the Bard n 12 April 2018) 1. Respnsibility and Principal Duties The Bard f Directrs has the verall respnsibility fr the gvernance f the Cmpany and fr supervising

TASSAL GROUP LIMITED ABN Procedures for the Oversight and Management of Material Business Risks. (Approved by the Board 28 May 2015)

") Prcedures fr the Oversight and Management f Material Business Risks TASSAL GROUP LIMITED ABN 15 106 067 270 Prcedures fr the Oversight and Management f Material Business Risks (Apprved by the Bard 28 May

Prcedures fr the Oversight and Management f Material Business Risks TASSAL GROUP LIMITED ABN 15 106 067 270 Prcedures fr the Oversight and Management f Material Business Risks (Apprved by the Bard 28 May

CITIGROUP INC. AUDIT COMMITTEE CHARTER As of January 18, 2018

CITIGROUP INC. AUDIT COMMITTEE CHARTER As f January 18, 2018 Missin The Audit Cmmittee ( Cmmittee ) f Citigrup Inc. ( Citigrup r the Cmpany ) is a standing cmmittee f the Bard f Directrs ( Bard ). The

CITIGROUP INC. AUDIT COMMITTEE CHARTER As f January 18, 2018 Missin The Audit Cmmittee ( Cmmittee ) f Citigrup Inc. ( Citigrup r the Cmpany ) is a standing cmmittee f the Bard f Directrs ( Bard ). The

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER An Audit Cmmittee is a key element in the Crprate Gvernance prcess f any rganizatin and acts as a link amng the Management, the Statutry Auditrs, Internal Auditrs and the Bard f

AUDIT COMMITTEE CHARTER An Audit Cmmittee is a key element in the Crprate Gvernance prcess f any rganizatin and acts as a link amng the Management, the Statutry Auditrs, Internal Auditrs and the Bard f

CYBG PLC BOARD REMUNERATION COMMITTEE. Charter

Charter Cmmittee Rle The Bards Remuneratin Cmmittee will act as the bard level Remuneratin Cmmittee fr Clydesdale and Yrkshire Banking Grup ( CYBG ) PLC and its subsidiaries, including fr the avidance

Charter Cmmittee Rle The Bards Remuneratin Cmmittee will act as the bard level Remuneratin Cmmittee fr Clydesdale and Yrkshire Banking Grup ( CYBG ) PLC and its subsidiaries, including fr the avidance

HIPAA Privacy Rule LINKS AND RESOURCES AFFECTED ENTITIES IMPACT ON EMPLOYERS. Provided by Brown & Brown of Louisiana, LLC

Prvided by Brwn & Brwn f Luisiana, LLC HIPAA Privacy Rule The HIPAA Privacy Rule establishes natinal standards t prtect individuals medical recrds and ther persnal health infrmatin. The Privacy Rule applies

Prvided by Brwn & Brwn f Luisiana, LLC HIPAA Privacy Rule The HIPAA Privacy Rule establishes natinal standards t prtect individuals medical recrds and ther persnal health infrmatin. The Privacy Rule applies

Producer Statements will be accepted only in accordance with this policy.

Prducer Statements Plicy This plicy has been prepared t ensure that Cuncil has clearly dcumented plicies and prcedures fr the request fr and acceptance f Prducer Statements in cnnectin with applicatins

Prducer Statements Plicy This plicy has been prepared t ensure that Cuncil has clearly dcumented plicies and prcedures fr the request fr and acceptance f Prducer Statements in cnnectin with applicatins

PSNC Briefing on the NHS Complaints procedure (from 1 April 2009)

") PSNC Briefing n the NHS Cmplaints prcedure (frm 1 April 2009) Under the prvisins f the Natinal Health Service (Pharmaceutical Services) Regulatins 2005 1 pharmacy cntractrs are required t make arrangements

PSNC Briefing n the NHS Cmplaints prcedure (frm 1 April 2009) Under the prvisins f the Natinal Health Service (Pharmaceutical Services) Regulatins 2005 1 pharmacy cntractrs are required t make arrangements

CAQ Lessons Learned. Performing an Audit of Internal Control. In an Integrated Audit

CAQ Lessns Learned Perfrming an Audit f Internal Cntrl In an Integrated Audit February 2009 Table f Cntents CAQ LESSONS LEARNED PERFORMING AN AUDIT OF INTERNAL CONTROL IN AN INTEGRATED AUDIT--------------------------------------------------------------------------------------------------1

CAQ Lessns Learned Perfrming an Audit f Internal Cntrl In an Integrated Audit February 2009 Table f Cntents CAQ LESSONS LEARNED PERFORMING AN AUDIT OF INTERNAL CONTROL IN AN INTEGRATED AUDIT--------------------------------------------------------------------------------------------------1

TOPIC 12: PART 1 WAYS OF GATHERING AUDIT EVIDENCE

TOPIC 12: PART 1 WAYS OF GATHERING AUDIT EVIDENCE ISA 500 is the relevant auditing standard fr audit evidence. 7 basic ways fr the auditr t gather audit evidence thrughut the audit prcess: 1. Observatin

TOPIC 12: PART 1 WAYS OF GATHERING AUDIT EVIDENCE ISA 500 is the relevant auditing standard fr audit evidence. 7 basic ways fr the auditr t gather audit evidence thrughut the audit prcess: 1. Observatin

School Business Manager

Plicy Title: Risk Assessment Plicy Authr: Schl Business Manager Audience: Staff Reviewed by: Gvernrs Review frequency: Annual Reviewed when: Octber 2016 Risk Assessment Plicy Intrductin Nrthease Manr Schl

Plicy Title: Risk Assessment Plicy Authr: Schl Business Manager Audience: Staff Reviewed by: Gvernrs Review frequency: Annual Reviewed when: Octber 2016 Risk Assessment Plicy Intrductin Nrthease Manr Schl

ISA 580, Written Representations

Internatinal Auditing and Assurance Standards Bard Expsure Draft December 2006 Cmments are requested by April 30, 2007 Prpsed Revised and Redrafted Internatinal Standard n Auditing ISA 580, Written Representatins

Internatinal Auditing and Assurance Standards Bard Expsure Draft December 2006 Cmments are requested by April 30, 2007 Prpsed Revised and Redrafted Internatinal Standard n Auditing ISA 580, Written Representatins

HEIDRICK & STRUGGLES INTERNATIONAL, INC. Corporate Governance Guidelines

HEIDRICK & STRUGGLES INTERNATIONAL, INC. Crprate Gvernance Guidelines The Heidrick & Struggles Internatinal, Inc. (The Cmpany ) Bard f Directrs (the Bard ) and management believe that the Cmpany, in the

HEIDRICK & STRUGGLES INTERNATIONAL, INC. Crprate Gvernance Guidelines The Heidrick & Struggles Internatinal, Inc. (The Cmpany ) Bard f Directrs (the Bard ) and management believe that the Cmpany, in the

CALL FOR INTELLECTUAL SERVICE PROVIDERS ( EXTERNAL CONSULTANTS ) OECD Guidelines for Multinational Enterprises National Contact Point Peer Reviews

OECD Guidelines for Multinational Enterprises National Contact Point Peer Reviews") CALL FOR INTELLECTUAL SERVICE PROVIDERS ( EXTERNAL CONSULTANTS ) OECD Guidelines fr Multinatinal Enterprises Natinal Cntact Pint Peer Reviews The OECD is seeking submissins frm cnsultants t supprt the

CALL FOR INTELLECTUAL SERVICE PROVIDERS ( EXTERNAL CONSULTANTS ) OECD Guidelines fr Multinatinal Enterprises Natinal Cntact Pint Peer Reviews The OECD is seeking submissins frm cnsultants t supprt the

Risk and Audit Committee charter

Risk and Audit Cmmittee charter 1. Intrductin The Bard f Cffey Internatinal Limited ( Cffey r the Cmpany ) has established a Risk and Audit Cmmittee ( Cmmittee ). It is nted that the Cmmittee is a sub-cmmittee

Risk and Audit Cmmittee charter 1. Intrductin The Bard f Cffey Internatinal Limited ( Cffey r the Cmpany ) has established a Risk and Audit Cmmittee ( Cmmittee ). It is nted that the Cmmittee is a sub-cmmittee

Proposed Revised South African Auditing Practice Statement (SAAPS) 2 Financial Reporting Frameworks and the Auditor s Report

2 Financial Reporting Frameworks and the Auditor s Report") Expsure Draft September 2010 Cmments are requested by 12 Nvember 2010 Prpsed Revised Suth African Auditing Practice Statement (SAAPS) 2 Financial Reprting Framewrks and the Auditr s Reprt REQUEST FOR COMMENTS

Expsure Draft September 2010 Cmments are requested by 12 Nvember 2010 Prpsed Revised Suth African Auditing Practice Statement (SAAPS) 2 Financial Reprting Framewrks and the Auditr s Reprt REQUEST FOR COMMENTS

1 st Floor, Building 32 The Woodlands Office Park Woodlands Drive, Woodmead 2148, Johannesburg, South Africa

ERM 1 st Flr, Building 32 The Wdlands Office Park Wdlands Drive, Wdmead 2148, Jhannesburg, Suth Africa Tel: +27 11 798 4300 Fax: +27 11 804 2289 www.erm.cm Independent Assurance Statement T Tngaat Hulett

ERM 1 st Flr, Building 32 The Wdlands Office Park Wdlands Drive, Wdmead 2148, Jhannesburg, Suth Africa Tel: +27 11 798 4300 Fax: +27 11 804 2289 www.erm.cm Independent Assurance Statement T Tngaat Hulett

CUMBERLAND, RHODE ISLAND FIRE DISTRICT. REQUEST FOR PROPOSALS (RFP) FOR PROFESSIONAL AUDITING SERVICES RFP Issuance Date January 29, 2018

FOR PROFESSIONAL AUDITING SERVICES RFP Issuance Date January 29, 2018") CUMBERLAND, RHODE ISLAND FIRE DISTRICT REQUEST FOR PROPOSALS (RFP) FOR PROFESSIONAL AUDITING SERVICES RFP Issuance Date January 29, 2018 INTRODUCTION The Cumberland Fire District is requesting prpsals

CUMBERLAND, RHODE ISLAND FIRE DISTRICT REQUEST FOR PROPOSALS (RFP) FOR PROFESSIONAL AUDITING SERVICES RFP Issuance Date January 29, 2018 INTRODUCTION The Cumberland Fire District is requesting prpsals

Overview of Statements of Investment Policies and Procedures (SIPP) Requirements

Requirements") Financial Services Cmmissin f Ontari Cmmissin des services financiers de l Ontari SECTION: INDEX NO.: TITLE: APPROVED BY: PUBLISHED: Investment Guidance Ntes IGN-005 Overview f Statements f Investment

Financial Services Cmmissin f Ontari Cmmissin des services financiers de l Ontari SECTION: INDEX NO.: TITLE: APPROVED BY: PUBLISHED: Investment Guidance Ntes IGN-005 Overview f Statements f Investment

Board Committee Charters

Charter Released by the Bard f Directrs f Snva Hlding AG n June 17, 2014. Audit Cmmittee ( AC ) Charter Art. 1: Purpse The Audit Cmmittee ( AC ) reviews n behalf f the Bard the wrk and effectiveness f

Charter Released by the Bard f Directrs f Snva Hlding AG n June 17, 2014. Audit Cmmittee ( AC ) Charter Art. 1: Purpse The Audit Cmmittee ( AC ) reviews n behalf f the Bard the wrk and effectiveness f

Audit, Risk & Compliance Committee Charter

Audit, Risk & Cmpliance Cmmittee Charter Objective and rle f the cmmittee The bjective f the Cmmittee is t assist the Bard f Directrs t discharge its crprate gvernance respnsibilities t exercise due care,

Audit, Risk & Cmpliance Cmmittee Charter Objective and rle f the cmmittee The bjective f the Cmmittee is t assist the Bard f Directrs t discharge its crprate gvernance respnsibilities t exercise due care,

AUDIT & RISK COMMITTEE (ARC)

") AUDIT & RISK COMMITTEE (ARC) The Audit and Risk Cmmittee is an independent appraisal bdy appinted by the chapter bard t assist the bard in fulfilling its versight respnsibilities pertaining t the integrity

AUDIT & RISK COMMITTEE (ARC) The Audit and Risk Cmmittee is an independent appraisal bdy appinted by the chapter bard t assist the bard in fulfilling its versight respnsibilities pertaining t the integrity

AUDIT COMMITTEE CHARGE

AUDIT COMMITTEE CHARGE Number f Members 5-7 Must be an dd number fr purpses f vting. Cmpsitin Members shall include the Secnd Past President, the Secretary and Treasurer, at least ne ther Bard member and

AUDIT COMMITTEE CHARGE Number f Members 5-7 Must be an dd number fr purpses f vting. Cmpsitin Members shall include the Secnd Past President, the Secretary and Treasurer, at least ne ther Bard member and

Comment Letter on Exposure Draft Reporting on Audited Financial Statements: Proposed New and Revised International Standards on Auditing (ISAs)

") Verband der Industrie- und Dienstleistungsknzerne in der Schweiz Fédératin des grupes industriels et de services en Suisse Federatin f Industrial and Service Grups in Switzerland 22 Nvember 2013 Internatinal

Verband der Industrie- und Dienstleistungsknzerne in der Schweiz Fédératin des grupes industriels et de services en Suisse Federatin f Industrial and Service Grups in Switzerland 22 Nvember 2013 Internatinal

HERANBA INDUSTRIES LIMITED POLICY ON MATERIALITY OF RELATED PARTY TRANSACTIONS AND DEALING WITH RELATED PARTY TRANSACTIONS

1. Title HERANBA INDUSTRIES LIMITED POLICY ON MATERIALITY OF RELATED PARTY TRANSACTIONS AND DEALING WITH RELATED PARTY TRANSACTIONS 1.1 This plicy shall be called the Plicy n materiality f related party

1. Title HERANBA INDUSTRIES LIMITED POLICY ON MATERIALITY OF RELATED PARTY TRANSACTIONS AND DEALING WITH RELATED PARTY TRANSACTIONS 1.1 This plicy shall be called the Plicy n materiality f related party

Independent Director and Audit Committee

Independent Directr and Audit Cmmittee Rules summary The listed cmpany s bard f directrs is representing the sharehlders. They are respnsible fr making decisins n the cmpany s imprtant plicies and strategies.

Independent Directr and Audit Cmmittee Rules summary The listed cmpany s bard f directrs is representing the sharehlders. They are respnsible fr making decisins n the cmpany s imprtant plicies and strategies.

Safeguards Phase 2 Section 600/Non-assurance Services (NAS) Part 4A International Independence Standards for Audits and Reviews

Part 4A International Independence Standards for Audits and Reviews") Agenda Item C-5 Safeguards Phase 2 Sectin 600/Nn-assurance Services (NAS) Nte: Text that is shaded in gray has been develped in cnjunctin with, and will be presented by the Structure TF. Part 4A Internatinal

Agenda Item C-5 Safeguards Phase 2 Sectin 600/Nn-assurance Services (NAS) Nte: Text that is shaded in gray has been develped in cnjunctin with, and will be presented by the Structure TF. Part 4A Internatinal

CORPORATE GOVERNANCE POLICY

CORPORATE GOVERNANCE POLICY Bard Missin Sagicr Real Estate X Fund Limited ( X Fund r the Cmpany ) was incrprated in 2011 under the laws f St. Lucia as an Internatinal Business Cmpany (IBC). X Fund is cmmitted

CORPORATE GOVERNANCE POLICY Bard Missin Sagicr Real Estate X Fund Limited ( X Fund r the Cmpany ) was incrprated in 2011 under the laws f St. Lucia as an Internatinal Business Cmpany (IBC). X Fund is cmmitted

The Committee is specifically charged with the following duties and responsibilities:

CORPORATE GOVERNANCE POLICY AND PROCEDURES MANUAL AUDIT AND RISK COMMITTEE CHARTER The Bard has reslved t establish a Cmmittee f the Bard t be knwn as the Audit and Risk Cmmittee. This Cmmittee will replace

CORPORATE GOVERNANCE POLICY AND PROCEDURES MANUAL AUDIT AND RISK COMMITTEE CHARTER The Bard has reslved t establish a Cmmittee f the Bard t be knwn as the Audit and Risk Cmmittee. This Cmmittee will replace

HUMAN RESOURCES AND COMPENSATION COMMITTEE CHARTER

HUMAN RESOURCES AND COMPENSATION COMMITTEE CHARTER PURPOSE The Human Resurces and Cmpensatin Cmmittee (the Cmmittee ) f Precisin Drilling Crpratin (the Crpratin ) is a standing cmmittee f the bard f directrs

HUMAN RESOURCES AND COMPENSATION COMMITTEE CHARTER PURPOSE The Human Resurces and Cmpensatin Cmmittee (the Cmmittee ) f Precisin Drilling Crpratin (the Crpratin ) is a standing cmmittee f the bard f directrs

Guidelines and Recommendations Guidelines on periodic information to be submitted to ESMA by Credit Rating Agencies

Guidelines and Recmmendatins Guidelines n peridic infrmatin t be submitted t ESMA by Credit Rating Agencies 23 June 2015 ESMA/2015/609 Table f Cntents 1 Scpe... 3 2 Definitins... 3 3 Purpse f Guidelines...

Guidelines and Recmmendatins Guidelines n peridic infrmatin t be submitted t ESMA by Credit Rating Agencies 23 June 2015 ESMA/2015/609 Table f Cntents 1 Scpe... 3 2 Definitins... 3 3 Purpse f Guidelines...

Corporate Governance Principles

Crprate Gvernance Principles Revised 05-03-2018 Amphenl s Crprate Gvernance Principles have been apprved by the Bard f Directrs and, tgether with the Cmpany s Certificate f Incrpratin, as amended and/r

Crprate Gvernance Principles Revised 05-03-2018 Amphenl s Crprate Gvernance Principles have been apprved by the Bard f Directrs and, tgether with the Cmpany s Certificate f Incrpratin, as amended and/r

Information concerning the constitution, goals and functions of the agency, including 1 :

Annual Reprt cmpliance checklist This checklist utlines the gvernance, perfrmance, reprting cmpliance and prcedural requirements f the Financial Administratin and Audit Act 1977 and the Financial Management

Annual Reprt cmpliance checklist This checklist utlines the gvernance, perfrmance, reprting cmpliance and prcedural requirements f the Financial Administratin and Audit Act 1977 and the Financial Management

We have carried out the following assurance activities:

Independent Assurance Reprt T the Bard f Directrs and Management f Trnt-Dminin Bank (the Bank ) Our respnsibilities Our limited assurance engagement has been planned and perfrmed in accrdance with the

Independent Assurance Reprt T the Bard f Directrs and Management f Trnt-Dminin Bank (the Bank ) Our respnsibilities Our limited assurance engagement has been planned and perfrmed in accrdance with the

TASSAL GROUP LIMITED ABN

Plicy fr the Selectin and Appintment f Directrs TASSAL GROUP LIMITED ABN 15 106 067 270 Plicy fr the Selectin and Appintment f Directrs (Reviewed by the Bard 25 June 2013) 1 Reviewed by the Bard - 25 June

Plicy fr the Selectin and Appintment f Directrs TASSAL GROUP LIMITED ABN 15 106 067 270 Plicy fr the Selectin and Appintment f Directrs (Reviewed by the Bard 25 June 2013) 1 Reviewed by the Bard - 25 June

AUDIT and ASSURANCE COMMITTEE TERMS OF REFERENCE

AUDIT and ASSURANCE COMMITTEE TERMS OF REFERENCE P U R P O S E The Cmmittee is an perating Cmmittee f the Grup Bard and is charged with the respnsibility f gaining assurance fr the Grup Bard that the rganisatin

AUDIT and ASSURANCE COMMITTEE TERMS OF REFERENCE P U R P O S E The Cmmittee is an perating Cmmittee f the Grup Bard and is charged with the respnsibility f gaining assurance fr the Grup Bard that the rganisatin

County of Riverside OFFICE OF THE AUDITOR-CONTROLLER STANDARD PRACTICE MANUAL

Cunty f Riverside OFFICE OF THE AUDITOR-CONTROLLER STANDARD PRACTICE MANUAL SECTION: 5 POLICY NUMBER: 510 SUBJECT: CATEGORY: CONSTRUCTION-IN-PROGRESS CAPITAL ASSET POLICIES REVISED DATE: 07/01/17 APPROVED

Cunty f Riverside OFFICE OF THE AUDITOR-CONTROLLER STANDARD PRACTICE MANUAL SECTION: 5 POLICY NUMBER: 510 SUBJECT: CATEGORY: CONSTRUCTION-IN-PROGRESS CAPITAL ASSET POLICIES REVISED DATE: 07/01/17 APPROVED

STATE OF NEW YORK MUNICIPAL BOND BANK AGENCY

STATE OF NEW YORK MUNICIPAL BOND BANK AGENCY Recvery Act Bnd Prgram Written Prcedures fr Tax Cmpliance and Internal Mnitring, adpted September 12, 2013 PROGRAM OVERVIEW The State f New Yrk Municipal Bnd

STATE OF NEW YORK MUNICIPAL BOND BANK AGENCY Recvery Act Bnd Prgram Written Prcedures fr Tax Cmpliance and Internal Mnitring, adpted September 12, 2013 PROGRAM OVERVIEW The State f New Yrk Municipal Bnd

NCTJ Conflicts of Interest Policy and Procedures

NCTJ Cnflicts f Interest Plicy and Prcedures Purpse This plicy aims t draw attentin t the pssibility f cnflicts, minimise r prevent a cnflict ccurring and manage cnflicts that have arisen. Definitin f

NCTJ Cnflicts f Interest Plicy and Prcedures Purpse This plicy aims t draw attentin t the pssibility f cnflicts, minimise r prevent a cnflict ccurring and manage cnflicts that have arisen. Definitin f

CHARTER OF RESERVES, HEALTH, SAFETY, ENVIRONMENT AND SOCIAL RESPONSIBILITY COMMITTEE 2018

CHARTER OF RESERVES, HEALTH, SAFETY, ENVIRONMENT AND SOCIAL RESPONSIBILITY COMMITTEE 2018 The Reserves, Health, Safety, Envirnment and Scial Respnsibility Cmmittee Charter utlines the specific rles and

CHARTER OF RESERVES, HEALTH, SAFETY, ENVIRONMENT AND SOCIAL RESPONSIBILITY COMMITTEE 2018 The Reserves, Health, Safety, Envirnment and Scial Respnsibility Cmmittee Charter utlines the specific rles and

Summary Plan Descriptions (SPD)

") Descriptins (SPD) SPDs What Are They and Wh Needs Them? What is an SPD? The DOL defines the SPD as the Primary vehicle fr infrming participants and beneficiaries abut their plan and hw it perates. Must

Descriptins (SPD) SPDs What Are They and Wh Needs Them? What is an SPD? The DOL defines the SPD as the Primary vehicle fr infrming participants and beneficiaries abut their plan and hw it perates. Must

IRDA Update: Draft Guidelines on Web Aggregators

IRDA Update: Draft Guidelines n Web Aggregatrs 17 March 2011 By way f an update, the IRDA has issued draft guidelines n web aggregatrs n 16 th March 2011. Cmments have been invited by 31 st March 2011.

IRDA Update: Draft Guidelines n Web Aggregatrs 17 March 2011 By way f an update, the IRDA has issued draft guidelines n web aggregatrs n 16 th March 2011. Cmments have been invited by 31 st March 2011.

Audit Committee Charter

www.subsea7.cm Audit Cmmittee Charter 5 23.May.17 Mark Fley VP Grup Financial Cntrller Dd Fraser Chairman f the Audit Cmmittee Revisin Revisin Date Dcument Owner Dcument Apprver Revisin: 5 Audit Cmmittee

www.subsea7.cm Audit Cmmittee Charter 5 23.May.17 Mark Fley VP Grup Financial Cntrller Dd Fraser Chairman f the Audit Cmmittee Revisin Revisin Date Dcument Owner Dcument Apprver Revisin: 5 Audit Cmmittee

Local Code Of Corporate Governance

Lcal Cde Of Crprate Gvernance Apprved by Jint Cmmittee 26 June 2017 Reprt N JC 09/2017 LOCAL CODE OF CORPORATE GOVERNANCE INTRODUCTION Crprate gvernance is the cmbinatin f prcesses and structures implemented

Lcal Cde Of Crprate Gvernance Apprved by Jint Cmmittee 26 June 2017 Reprt N JC 09/2017 LOCAL CODE OF CORPORATE GOVERNANCE INTRODUCTION Crprate gvernance is the cmbinatin f prcesses and structures implemented

NATCHITOCHES HISTORIC DISTRICT DEVELOPMENT COMMISSION STATE OF LOUISIANA

NATCHITOCHES HISTORIC DISTRICT DEVELOPMENT COMMISSION STATE OF LOUISIANA Independent Accuntants* Reprt n Applying Agreed-Upn Prcedures June 30, 2013 GRIFFIN & COAAPANY, LLC CERTIFIED PUBLIC ACCOUNTANTS

NATCHITOCHES HISTORIC DISTRICT DEVELOPMENT COMMISSION STATE OF LOUISIANA Independent Accuntants* Reprt n Applying Agreed-Upn Prcedures June 30, 2013 GRIFFIN & COAAPANY, LLC CERTIFIED PUBLIC ACCOUNTANTS

Request for Proposal. IT Managed Services

Tiltn-Nrthfield Fire District Request fr Prpsal Due by: Nvember 30, 2017 at 2:00 PM Chief Sitar Tiltn-Nrthfield Fire & EMS 12 Center Street Tiltn, NH 03276 1 Tiltn-Nrthfield Fire District TABLE OF CONTENTS

Tiltn-Nrthfield Fire District Request fr Prpsal Due by: Nvember 30, 2017 at 2:00 PM Chief Sitar Tiltn-Nrthfield Fire & EMS 12 Center Street Tiltn, NH 03276 1 Tiltn-Nrthfield Fire District TABLE OF CONTENTS

Windham School District Procurement Policy for Federal Funds

1 f 5 Windham Schl District Prcurement Plicy fr Federal Funds DJB-FED The fllwing Prcurement Plicies shall apply t all Cntracts fr and Purchases f gds and services. All prcurements made with Federal funds

1 f 5 Windham Schl District Prcurement Plicy fr Federal Funds DJB-FED The fllwing Prcurement Plicies shall apply t all Cntracts fr and Purchases f gds and services. All prcurements made with Federal funds

By David Harper, CFA FRM CIPM

P2.T7. Operatinal Risk Measurement and Management Capital Planning at Large Bank Hlding Cmpanies: Supervisry Expectatins and Range f Current Practice Binic Turtle FRM Study Ntes By David Harper, CFA FRM

P2.T7. Operatinal Risk Measurement and Management Capital Planning at Large Bank Hlding Cmpanies: Supervisry Expectatins and Range f Current Practice Binic Turtle FRM Study Ntes By David Harper, CFA FRM

Manual of Administrative Policies and Procedures

Manual f Administrative Plicies and Prcedures POLICY 1.49 Cntract Management and Signing Authrity Plicy Categry: General Related Prcedures: Prcedures fr Negtiating, Apprving and Signing University Cntracts

Manual f Administrative Plicies and Prcedures POLICY 1.49 Cntract Management and Signing Authrity Plicy Categry: General Related Prcedures: Prcedures fr Negtiating, Apprving and Signing University Cntracts

Reforms of the Auditing Profession; Improving Quality, Transparency, Governance and Accountability

Refrms f the Auditing Prfessin; Imprving Quality, Transparency, Gvernance and Accuntability Beginning with the passage f the 1933 Securities Act, Cngress has required an Independent Audit fr every public

Refrms f the Auditing Prfessin; Imprving Quality, Transparency, Gvernance and Accuntability Beginning with the passage f the 1933 Securities Act, Cngress has required an Independent Audit fr every public

[AGENCY NAME] Mandate and Roles Document. (Pure Advisory Committees)

![[AGENCY NAME] Mandate and Roles Document. (Pure Advisory Committees)](/thumbs/78/77615916.jpg "[AGENCY NAME] Mandate and Roles Document. (Pure Advisory Committees)") [This sample dcument has been develped by the Agency Gvernance Secretariat. It is intended t be used fr infrmatinal purpses nly. Agencies are encuraged t adapt the dcument t meet their specific needs.

[This sample dcument has been develped by the Agency Gvernance Secretariat. It is intended t be used fr infrmatinal purpses nly. Agencies are encuraged t adapt the dcument t meet their specific needs.

Policy on Requesting Reasonable Accommodations from the Zoning Code

Plicy n Requesting Reasnable Accmmdatins frm the Zning Cde Backgrund The Americans with Disabilities Act (ADA), as amended, is a federal anti-discriminatin statute designed t remve barriers that prevent

Plicy n Requesting Reasnable Accmmdatins frm the Zning Cde Backgrund The Americans with Disabilities Act (ADA), as amended, is a federal anti-discriminatin statute designed t remve barriers that prevent

Investor Money Regulations

Investr Mney Regulatins A new regime fr fund service prviders in Ireland On the 30 th March 2015, the new Investr Mney Regulatins were brught int effect by Statutry Instrument 105 f 2015, with crrespnding

Investr Mney Regulatins A new regime fr fund service prviders in Ireland On the 30 th March 2015, the new Investr Mney Regulatins were brught int effect by Statutry Instrument 105 f 2015, with crrespnding

AMENDMENTS TO NASDAQ RULES ON COMPENSATION COMMITTEES

March 2013 AMENDMENTS TO NASDAQ RULES ON COMPENSATION COMMITTEES Summary. The Securities and Exchange Cmmissin recently apprved the fllwing amendments t the NASDAQ listing rules relating t cmpensatin cmmittees:

March 2013 AMENDMENTS TO NASDAQ RULES ON COMPENSATION COMMITTEES Summary. The Securities and Exchange Cmmissin recently apprved the fllwing amendments t the NASDAQ listing rules relating t cmpensatin cmmittees:

LMA GUIDANCE: GDPR CORE USES INFORMATION NOTICE

LMA GUIDANCE: GDPR CORE USES INFORMATION NOTICE FEBRUARY 2018 NOTE: This guidance and the Lndn Market Cre Uses Infrmatin Ntice will be updated when the UK Data Prtectin Bill is enacted the Bill currently

LMA GUIDANCE: GDPR CORE USES INFORMATION NOTICE FEBRUARY 2018 NOTE: This guidance and the Lndn Market Cre Uses Infrmatin Ntice will be updated when the UK Data Prtectin Bill is enacted the Bill currently

Sempra Energy Environmental, Health, Safety and Technology Committee Charter

Sempra Energy Envirnmental, Health, Safety and Technlgy Cmmittee Charter As adpted by the Bard f Directrs f Sempra Energy n September 5, 2000 and amended thrugh Nvember 9, 2015. I. Purpse The purpse f

Sempra Energy Envirnmental, Health, Safety and Technlgy Cmmittee Charter As adpted by the Bard f Directrs f Sempra Energy n September 5, 2000 and amended thrugh Nvember 9, 2015. I. Purpse The purpse f

This financial planning agreement (the Agreement ) is made on this date: between the undersigned party, whose mailing address is

is made on this date: between the undersigned party, whose mailing address is") F I N A N C I A L P L A N N I N G A G R E E M E N T This financial planning agreement (the Agreement ) is made n this date: between the undersigned party, CLIENT(s): whse mailing address is (hereinafter

F I N A N C I A L P L A N N I N G A G R E E M E N T This financial planning agreement (the Agreement ) is made n this date: between the undersigned party, CLIENT(s): whse mailing address is (hereinafter

Current Developments: Canadian Securities and Auditing Matters

Current Develpments: Canadian Securities and Auditing Matters March 2017 kpmg.ca Canadian Securities and Auditing Matters This editin prvides a summary f newly effective and frthcming regulatry and auditing

Current Develpments: Canadian Securities and Auditing Matters March 2017 kpmg.ca Canadian Securities and Auditing Matters This editin prvides a summary f newly effective and frthcming regulatry and auditing

Safeguards Phase 2 Section 600/Non-assurance Services (NAS) Part 4A International Independence Standards for Audits and Reviews

Part 4A International Independence Standards for Audits and Reviews") Agenda Item 2-F Safeguards Phase 2 Sectin 600/Nn-assurance Services (NAS) (Mark-up frm June 2016 IESBA Discussin) Part 4A Internatinal Independence Standards fr Audits and Reviews. Sectin 600 Prvisin f

Agenda Item 2-F Safeguards Phase 2 Sectin 600/Nn-assurance Services (NAS) (Mark-up frm June 2016 IESBA Discussin) Part 4A Internatinal Independence Standards fr Audits and Reviews. Sectin 600 Prvisin f

Safeguards Phase 2 Proposed Section 600 (Mark-up From September 27 IESBA Meeting Discussion)

") Agenda Item 4-D Safeguards Phase 2 Prpsed Sectin 600 (Mark-up Frm September 27 IESBA Meeting Discussin) Nte t Meeting Participants: A clean versin f Sectin 600 will frm part f Chapter 1 t the Safeguards

Agenda Item 4-D Safeguards Phase 2 Prpsed Sectin 600 (Mark-up Frm September 27 IESBA Meeting Discussin) Nte t Meeting Participants: A clean versin f Sectin 600 will frm part f Chapter 1 t the Safeguards

PRIMERICA, INC. COMPENSATION COMMITTEE CHARTER Adopted on March 31, 2010 and revised as of August 15, 2018

PRIMERICA, INC. COMPENSATION COMMITTEE CHARTER Adpted n March 31, 2010 and revised as f August 15, 2018 Missin The Cmpensatin Cmmittee (the Cmmittee ) f Primerica, Inc. (the Cmpany ) is respnsible fr determining

PRIMERICA, INC. COMPENSATION COMMITTEE CHARTER Adpted n March 31, 2010 and revised as f August 15, 2018 Missin The Cmpensatin Cmmittee (the Cmmittee ) f Primerica, Inc. (the Cmpany ) is respnsible fr determining

CODE OF CONDUCT AND ETHICS POLICY ON CONFLICTS OF INTEREST

CODE OF CONDUCT AND ETHICS POLICY ON CONFLICTS OF INTEREST Magna Internatinal Inc. Plicy n Gifts & Entertainment 1 POLICY ON CONFLICTS OF INTEREST Magna emplyees have a duty t act in Magna s best interest.

CODE OF CONDUCT AND ETHICS POLICY ON CONFLICTS OF INTEREST Magna Internatinal Inc. Plicy n Gifts & Entertainment 1 POLICY ON CONFLICTS OF INTEREST Magna emplyees have a duty t act in Magna s best interest.

Integrated Audits of Public Companies

Chapter 18 - Integrated Audits f Public Cmpanies CHAPTER 18 Integrated Audits f Public Cmpanies Review Questins 18 1 Sectin 404a requires that each annual reprt filed with the Securities and Exchange Cmmissin

Chapter 18 - Integrated Audits f Public Cmpanies CHAPTER 18 Integrated Audits f Public Cmpanies Review Questins 18 1 Sectin 404a requires that each annual reprt filed with the Securities and Exchange Cmmissin

ADANI POWER LIMITED RELATED PARTY TRANSACTION POLICY. Page 1 of 10

ADANI POWER LIMITED RELATED PARTY TRANSACTION POLICY Page 1 f 10 TABLE OF CONTENTS Sr. N. Particulars Page Ns. 1. Preamble 3 2. Purpse 3 3. Definitins 3 4. Plicy and Prcedure 5 5. Transactins which d nt

ADANI POWER LIMITED RELATED PARTY TRANSACTION POLICY Page 1 f 10 TABLE OF CONTENTS Sr. N. Particulars Page Ns. 1. Preamble 3 2. Purpse 3 3. Definitins 3 4. Plicy and Prcedure 5 5. Transactins which d nt

NANOSTRING TECHNOLOGIES, INC. COMPENSATION COMMITTEE CHARTER. (Adopted as of October 16, 2012 and amended as of April 26, 2017)

") NANOSTRING TECHNOLOGIES, INC. COMPENSATION COMMITTEE CHARTER (Adpted as f Octber 16, 2012 and amended as f April 26, 2017) PURPOSE The purpse f the Cmpensatin Cmmittee (the Cmmittee ) f the Bard f Directrs

NANOSTRING TECHNOLOGIES, INC. COMPENSATION COMMITTEE CHARTER (Adpted as f Octber 16, 2012 and amended as f April 26, 2017) PURPOSE The purpse f the Cmpensatin Cmmittee (the Cmmittee ) f the Bard f Directrs

Understanding Self Managed Superannuation Funds

Understanding Self Managed Superannuatin Funds Hw t read this dcument Managing yur finances t meet yur day t day requirements as well as yur lng-term gals can be a cmplex task. There are all srts f issues

Understanding Self Managed Superannuatin Funds Hw t read this dcument Managing yur finances t meet yur day t day requirements as well as yur lng-term gals can be a cmplex task. There are all srts f issues

INDEPENDENT ACCOUNTANTS' REPORT ON APPLYING AGREED-UPON PROCEDURES

d^^ GRIFFIN & COMPANY, LLC CERTIFIED PUBLIC ACCOUNTANTS Stephen M. Griffin, CPA Rbert J. Furman, CPA INDEPENDENT ACCOUNTANTS' REPORT ON APPLYING AGREED-UPON PROCEDURES T the Bard Members Luisiana State

d^^ GRIFFIN & COMPANY, LLC CERTIFIED PUBLIC ACCOUNTANTS Stephen M. Griffin, CPA Rbert J. Furman, CPA INDEPENDENT ACCOUNTANTS' REPORT ON APPLYING AGREED-UPON PROCEDURES T the Bard Members Luisiana State

FCA Final Notice: Market abuse systems and controls

FCA Final Ntice: Market abuse systems and cntrls regulkar Key issues frm the Final Ntice issued by the Financial Cnduct Authrity t W H Ireland Limited n 22 February 2016. 16 March 2016 simmns-simmns.cm

FCA Final Ntice: Market abuse systems and cntrls regulkar Key issues frm the Final Ntice issued by the Financial Cnduct Authrity t W H Ireland Limited n 22 February 2016. 16 March 2016 simmns-simmns.cm

Risk Management Policy

Risk Management Plicy 1. Purpse The purpse f this plicy is t prvide clear guidelines fr the management f risk. Risk is defined as the effect f uncertainty n bjectives. 1 Risk Management is the discipline

Risk Management Plicy 1. Purpse The purpse f this plicy is t prvide clear guidelines fr the management f risk. Risk is defined as the effect f uncertainty n bjectives. 1 Risk Management is the discipline

INDEPENDENT ACCOUNTANTS' REPORT ON APPLYING AGREED-UPON PROCEDURES

^001 GRIFFIN & COMPANY, LLC CERTIFIED PUBLIC ACCOUNTANTS Stephen M. Griffin, CPA Rbert J. Furman, CPA INDEPENDENT ACCOUNTANTS' REPORT ON APPLYING AGREED-UPON PROCEDURES T the Bard Members Atchafalaya Basin

^001 GRIFFIN & COMPANY, LLC CERTIFIED PUBLIC ACCOUNTANTS Stephen M. Griffin, CPA Rbert J. Furman, CPA INDEPENDENT ACCOUNTANTS' REPORT ON APPLYING AGREED-UPON PROCEDURES T the Bard Members Atchafalaya Basin

Auditor Reporting Building Blocks

Agenda Item L.1 I. Recmmendatins Auditr Reprting Building Blcks A flexible building blcks apprach is needed t ensure that cnsistent, useful and relevant infrmatin is cmmunicated in auditr s reprts acrss

Agenda Item L.1 I. Recmmendatins Auditr Reprting Building Blcks A flexible building blcks apprach is needed t ensure that cnsistent, useful and relevant infrmatin is cmmunicated in auditr s reprts acrss

FORM 2. INDEPENDENT REGULATORY BOARD FOR AUDITORS (Established under Section 3 of Act 26 of 2005)

") FORM 2 INDEPENDENT REGULATORY BOARD FOR AUDITORS (Established under Sectin 3 f Act 26 f 2005) APPLICATION BY A FIRM FOR ADMISSION TO THE REGISTER OF AUDITORS (Fr applicatin in terms f Sectin 38(2)) and

FORM 2 INDEPENDENT REGULATORY BOARD FOR AUDITORS (Established under Sectin 3 f Act 26 f 2005) APPLICATION BY A FIRM FOR ADMISSION TO THE REGISTER OF AUDITORS (Fr applicatin in terms f Sectin 38(2)) and