Learner Guide Municipal budgeting and implementation. Unit Standard Title Plan a municipal budgeting and reporting cycle. Unit Standard ID

|

|

|

- Kellie Shaw

- 5 years ago

- Views:

Transcription

1 Learner Guide Municipal budgeting and implementation Unit Standard Title Plan a municipal budgeting and reporting cycle Unit Standard ID

2 Notice This material has been developed by National Treasury as part of a broader skills development initiative to support the implementation of the Municipal Minimum Competency Regulations, Gazette 29967, June The material should be used as part of the broader context of curricular content and was designed to achieve the recognised municipal financial management qualifications Only those service providers that appear on the National Treasury website list of Service Providers and Modules are authorised to use this product, which must be used for the express purpose of providing approved learning programme(s) towards municipal competency regulations. Service providers will appear on this list only after formal accreditation in full or in part have been reviewed and approved in respect of related training by the National Treasury. Service Providers wishing to confirm if they have been listed as preferred service providers for use by municipalities should visit the National Treasury website at under Training and Validation which will be updated from time to time. Service Providers are not permitted to substantially amend or change this material without the express authorisation in writing of the National Treasury MFMA Implementation Unit. Any requests to amend or alter this publication must be submitted to mfma@treasury.gov.za, prior to the commencement of any training or activity that the material may relate to. Notwithstanding the above limitations, National Treasury encourages those Authorised Service Providers using this product to further develop the material with the inclusion of case studies and practical examples where appropriate, to enhance practical relevance for learners where possible. We remind you that this material has been provided as a resource to assist practitioners in local government to become qualified municipal finance management professionals, it is not intended to provide legal or other advice on which a municipality should rely on in fulfilling their statutory or social responsibilities. Other parties not referred to above, may use this material for training purposes only, provided that such purposes will be not for profit only, and prior approval is granted by National Treasury. MFMA Implementation Unit 3rd Floor, 40 Church Square, Pretoria September

3 Table of Content Module Outline UNIT STANDARD TITLE MODULE STRUCTURE UNIT STANDARD OUTCOMES UNIT STANDARD PURPOSE LEARNING ASSUMED TO BE IN PLACE UNIT STANDARD CONTENT UNIT STANDARD ASSESSMENT MODERATION REFERENCES Introduction to municipal budgeting and reporting cycle in South Africa LEARNING OUTCOMES KEY CONCEPTS LEARNING ASSUMED TO BE IN PLACE INTRODUCTION THE BUDGET AND REPORTING CYCLE A STRATEGIC APPROACH TO BUDGETING SEPARATION OF ROLES AND RESPONSIBILITIES ACCOUNTABILITY CYCLE CONSULTATIVE PROCESSES LEGISLATIVE FRAMEWORK ASSIGNMENTS ASSESSMENT CRITERIA Components of the budget and reporting cycle LEARNING OUTCOMES KEY CONCEPTS LEARNING ASSUMED TO BE IN PLACE INTRODUCTION BUDGET PREPARATION PROCESS BUDGET IMPLEMENTATION PROCESS

4 7. BUDGET EVALUATION PROCESS ASSIGNMENTS ASSESSMENT CRITERIA Roles and responsibilities in terms of the municipal budget and reporting cycle LEARNING OUTCOMES KEY CONCEPTS LEARNING ASSUMED TO BE IN PLACE INTRODUCTION ROLE OF THE COUNCIL ROLE OF THE MAYOR ROLE OF THE MUNICIPAL MANAGER (THE ACCOUNTING OFFICER) ROLES OF SENIOR MANAGERS AND OTHER OFFICIALS DELEGATIONS BY THE MUNICIPAL MANAGER ROLE OF THE CHIEF FINANCIAL OFFICER BUDGET AND TREASURY OFFICE ROLES AND RESPONSIBILITIES OF OTHER LEVELS OF GOVERNMENT ASSIGNMENTS ASSESSMENT CRITERIA Municipal finance management calendar LEARNING OUTCOMES KEY CONCEPTS LEARNING ASSUMED TO BE IN PLACE INTRODUCTION MUNICIPAL BUDGET AND REPORTING CALENDAR

5 Module Outline 1. UNIT STANDARD TITLE 1.1. Plan a municipal budgeting and reporting cycle, US MODULE STRUCTURE 2.1. Qualification: Certificate in Municipal Finance Management 2.2. Unit Standard: Plan a municipal budgeting and reporting cycle, US Credits: NQF level: Type: Core 2.6. Duration: 80 notional hours 2.7. The following table contains the unit standards required for qualification Certificate in Municipal Finance Management, NQF level 6 (SAQA ID 48965). Modules SAQA US ID Unit standard title Credit values Municipal legislative The Inter-governmental Fiscal 10 credits environment and policy NQF level 6 Relations Act in municipal financial management x South African legislation and 8 credits NQF level 6 policy affecting municipal financial management Cooperative Conduct stakeholder 8 credits Governance and NQF level 6 consultation around municipal stakeholder relations finance x Principles of ethics in a 10 credits NQF level 6 municipal environment Municipal financial x Conduct performance 12 credits reporting and NQF level 6 management in a South performance African municipal environment 4

6 Modules SAQA US ID Unit standard title Credit values management NQF level 6 Prepare and analyse municipal financial reports 12 credits Municipal strategic x Strategic planning process in a 15 credits planning and NQF level 6 South African municipality implementation x Apply approaches to 15 credits NQF level 6 managing municipal income and expenditure within a multiyear framework Managing risk in a Contribute to internal control 8 credits municipal context NQF level 6 and internal control evaluation framework Risk management in South 10 credits NQF level 6 African municipalities Contribute to audit planning 12 credits NQF level 5 and process in a South African municipality Municipal budgeting Apply the principles of 15 credits and implementation NQF level 5 budgeting within a municipality Municipal budgeting and 8 credits NQF level 6 reporting Management of Apply techniques and South 10 credits municipal assets and NQF level 6 African statutes to cash and liabilities investment management Manage a municipality s 11 credits NQF level 6 assets and liabilities Cost management and Contribute to capital planning 15 credits capital planning NQF level 6 and financing Apply costing principles to 11 credits NQF level 6 municipal operational and service-based costing 5

7 Modules SAQA US ID Unit standard title Credit values Manage information 8 credits NQF level 6 technology resources in a municipal finance environment Municipal supply chain Participate in the design and 12 credits management NQF level 6 implementation of municipal supply chain management Public-private Plan and implement public- 12 credits partnerships in NQF level 6 private partnerships for municipals service municipal service delivery delivery 2.8. Completion of this qualification provides a significant proportion of the unit standards required to meet the municipal competency levels. To meet the regulatory requirements for the minimum competency levels for prescribed positions in municipalities please refer to the local government: Municipal Finance Management Act: Municipal Regulations on Minimum Competency Levels at This unit standard may also be utilised in other qualifications. Refer to 3. UNIT STANDARD OUTCOMES 3.1. ON COMPLETION OF THIS UNIT STANDARD, YOU SHOULD BE ABLE TO: Advise on the application of the South African local government legislative framework for local government budgeting processes Advise on the timing of budget related events and the integration of budget related processes with budget processes to ensure compliance with the legislative requirements. 6

8 Ensure legal requirements that non-budget documentation is correctly referenced in budget documentation is complied with and vice versa Advise on the roles and responsibilities of financial and non-financial management and political executives in the budget process, which should contribute to the overall process of social and economic development. 4. UNIT STANDARD PURPOSE 4.1. This Unit Standard is intended for practitioners in local government who are involved in policy decision-making and strategic planning. Learners who are required to advise on the legislative mandate of municipalities from a provincial and national government perspective will also benefit from this Unit Standard The Unit Standard will contribute to social and economic transformation by equipping practitioners with skills in budgeting which could translate into better use of resources and improved delivery services. That is, the unit standard will contribute to understanding the vital role that local government plays in delivering basic services The scope of this unit standard covers the budget and reporting cycle in a municipality and in municipal entities. This unit standard provides considerable detail regarding the additional requirements where municipalities use municipal entities to deliver services. 5. LEARNING ASSUMED TO BE IN PLACE 5.1. IT IS ASSUMED THAT LEARNERS ARE COMPETENT IN: Communication at Level Mathematical Literacy at Level 4. 7

9 6. UNIT STANDARD CONTENT 6.1. Introduction to municipal budget and reporting cycle in South Africa 6.2. Components of the budget and reporting cycle 6.3. Roles and responsibilities in terms of the municipal budget and reporting cycle 6.4. Municipal finance management calendar 7. UNIT STANDARD ASSESSMENT 7.1. THE STRUCTURE OF THE ASSESSMENT IS AS FOLLOWS % Attendance % Participation in facilitated classroom environment % Presentation to class of selected assignment % Assignments % major assignment 7.2. ATTENDANCE (10%) The attendance mark shall be given for attending entire workshops. Attending a partial workshop will be assessed as non-attendance for that workshop. There are 6 workshops and full attendance for all six workshops will be awarded the full 10%. Attendance for 3 full workshops will be awarded 5% (3/6 * 10%). 8

10 7.3. PARTICIPATION (10%) To be eligible to receive a mark for participation the learner must demonstrate that they have successfully completed the MFMA learning modules assigned in the module notes. The facilitator must confirm this on the learner management database and award a zero for participation if the MFMA learning modules have not been completed A participation score out of 10 shall be given for each full workshop attended and the total divided by the number of full workshops attended to arrive at an average mark out of 10. As with attendance, the participation mark cannot be awarded for partial workshops attended. The facilitator will need to see that all learners are contributing to discussion in a way that demonstrates an understanding of the concepts and provides value to the discussion. < 5 Inadequate participation 5 6 Just adequate participation 7 Better than adequate participation 8 Good participation 9 10 Very good participation As an example, a learner attends 4 workshops and scores 5, 7, 6 and 10 for participation. Assuming they completed the required MFMA learning modules they would receive a participation mark of 7 (( ) / 4). If, however, the learner had not completed the required MFMA learning modules they would receive a participation mark of zero PRESENTATION OF SELECTED ASSIGNMENT (10%) In the first workshop the facilitator will nominate learners to present one assignment (not a major assignment). The facilitator will determine if some assignments may be presented by a group to ensure a fair distribution of assignments. However, all individual learners must make a presentation of 9

11 approximately 15 minutes. That presentation will be assessed based on the following: 5 marks for knowledge of subject and preparation of presentation 5 marks for presentation skills and leadership of discussion 7.5. ASSIGNMENTS (40%) Except for the two major assignments, the assignments at the end of each chapter are to be handed in to the facilitator at the beginning of the next workshop following the completion of the chapter MAJOR ASSIGNMENT (30%) The major assignment will count for 30% of the total assessment. Learners have two weeks to complete the assignment ASSESSMENT CRITERIA The assessment criteria are provided for each assignment Copying of the text is discouraged. Students should use their own words as much as possible to complete the activities The following areas should be considered: Originality, knowledge, insight, application, analysis ability, comprehension ASSESSMENT AND LEARNING METHODS Assessment for this module will be undertaken according to the five methods set out in section 7.1 above. It consists of A mark for attendance at class (workshop) 10

12 A mark for participation in class discussion activities A mark for presentation to class of one assignment A mark for turned in assignments A mark for turned in major assignment The suggested approach for teaching and learning is as follows: The module is split into 5 chapters. Chapter 1 is the module outline and contains general information. Chapters 2 5 contain the module learning material and assignments. Module outline Introduction to municipal budget and reporting cycle in South Africa Components of the budget and reporting cycle Roles and responsibilities in terms of the municipal budget and reporting cycle Municipal finance management calendar Chapters 2 4 consist of module notes, assigned additional reading and study activities, class discussion activities, assignments, and 1 Major assignment Chapter 5 consists of a reproduction of the municipal finance management calendar published by the National Treasury. 11

13 Learners are expected to review the module notes, complete assigned additional reading and study, and prepare for class discussion activities prior to each workshop Except for the major assignment, they are expected to complete the assignments after the workshop in which the material is covered and hand prepared answers in for marking at the commencement of the following workshop There is one major assignment which must be handed in for marking no later than one week after the final workshop. Estimated learning hours required Workshops 4 x 8 hours = 32 hours Individual Study 4 x 8 hours = 32 hours Major assignment = 16 hours Total = 80 notional hours Note that individual study includes reading the module notes, additional assigned reading, completing assigned MFMA learning modules, preparing answers to in class discussion activities and assignments. Workshop topic plan workshop 1 Chapter 2 workshop 2 First part of Chapter 3 workshop 3 Conclude Chapter 3 and Chapter 4 workshop 4 Chapter 5 Sample learning methodology Pre Workshop 1 Read through the module notes applicable to workshop 1 12

14 Complete any additional reading or study as required by the module notes (e.g. a module of MFMA learning) Complete the discussion activities these will be discussed in workshop 1 During Workshop 1 The facilitator will present the material in the module notes related to this workshop Discussion activities will be discussed by the group in the workshop at the relevant point Pre Workshop 2 Complete the assignments from workshop 1 to be handed in at workshop 2 Read through the module notes applicable to workshop 2 Complete any required additional reading or study as required by the module notes (e.g. a module of MFMA learning) Complete the discussion activities these will be discussed in workshop 2 During Workshop 2 Turn in answers to assignments from workshop 1 The learners who have selected assignments for presentation will make a 15 minute presentation to answer the chosen activity. 15 minutes will be allowed for discussion. The facilitator will present the material in the module notes related to this workshop Discussion activities will be discussed by the group in the workshop at the relevant point 13

15 Workshops 3 and 4 Same as workshop 2, also refer to the relevant chapters for further information under the heading Learning assumed to be in place. 8. MODERATION 8.1. This module has been designed to have marks for attendance, participation, a presentation, completed assignments (short and 1 major assignment). The assignments incorporate both formative and summative assessment. 14

16 9. REFERENCES 9.1. REFERENCES USED IN THIS MODULE: National Treasury website Local Government: Finance Management Act, No. 56 of Local Government: Municipal Budget and Reporting Regulations Local Government: Municipal Systems Act, No. 32 of The Constitution of the Republic of South Africa Chapter 7, Chapter 13 (sec 215 & 216), schedules 4 & White Paper on Local Government (National Treasury) MFMA Learning: Module 3 Budget Process Module 6 Annual Reporting 9.2. OTHER REFERENCES APPLICABLE TO LOCAL GOVERNMENT: Local Government: Municipal Structures Act, No. 117 of Local Government: Municipal Property Rates Act, No. 6 of Local Government: Municipal Demarcation Act, No. 51 of Intergovernmental Fiscal Relations Act, No. 97 of Intergovernmental Relations Framework Act, No. 13 of

17 Local Government Transitions Act Second Amendment Act, No 97 of Municipal Fiscal Powers and Functions Act, No 12 of MFMA Budget Format Guide July 2008 (National Treasury) Introductory Guide to the MFMA, Updated Edition August 2004 (National Treasury) A Guide to Municipal Financial Management for Councillors (National Treasury) Specimen Annual Financial Statements, June 2005 (National Treasury) Funding Compliance Guideline, March 2008 (National Treasury) National Treasury MFMA Circulars: Circular 42 Funding a Municipal Budget (30 March 2007) Circular 32 The Oversight Report (15 Mar 2006) Circular 28 Budget Content and Format (12 Dec 2005) Circular 19 Budget Process 2006/07 (15 Aug 2005) Circular 13 Service Delivery and Budget Implementation Plan (31 Jan 2005) Circular 10 Budget Process 2005/06 (8 Oct 2004) 16

18 TO EACH WORKSHOP, PLEASE BRING ALONG: MFMA pocket guide (National Treasury) Municipal Budget and Reporting Regulations The Constitution of the Republic of South Africa Local Government: Municipal Systems Act, Act 32 of 2000 as amended ACCESS TO: MFMA learning modules (National Treasury) 17

19 Introduction to municipal budgeting and reporting cycle in South Africa 1. LEARNING OUTCOMES 1.1. Understand the concept of the budget and reporting cycle in a municipal context and the legislative framework. 2. KEY CONCEPTS 2.1. Key stages of the budget and reporting cycle 2.2. Budget preparation process 2.3. Budget Implementation process 2.4. Budget evaluation process 2.5. Accountability cycle 2.6. IDP, sector plans, budget, SDBIP, adjustments budget, in-year reports, annual financial statements, annual reports, oversight reports 2.7. Monthly budget statements, quarterly reports, mid-year budget and performance assessment 2.8. Schedule of key deadlines 2.9. Medium Term Revenue and Expenditure Framework (MTREF) Municipal budget policy statement Consultation in terms of the budget and reporting cycle 18

20 3. LEARNING ASSUMED TO BE IN PLACE 3.1. Communication at level Mathematical literacy at level The learner is reminded that prior to attending a workshop on this chapter they must: read this chapter module notes; complete assigned reading or study which includes MFMA Learning modules bring completed answers to the activities/class discussion for this chapter for discussion during the workshop. 4. INTRODUCTION 4.1. A budgeting and reporting cycle is a sequence of interrelated events that occur throughout a budget period. The cycle is continuous and repetitive, meaning that events reoccur in a predictable and carefully planned sequence In the modern day local government context, a number of budget and reporting cycles are occurring concurrently and are interrelated, each informing and contributing to the other. This is because the cycle of budgeting spans beyond any given financial year generally commencing one year before the start of the financial year and concluding almost one year after the financial year end. 19

21 ENTITIES and the budget cycle Note that municipalities with municipal entities will have an added layer of complexity to deal with in planning the municipal budget and reporting cycle. The mayor of the municipality must coordinate the budget process including the inputs required from municipal entities. Notwithstanding the added complexities many of the concepts for planning a municipal budget and reporting process generally apply to municipal entities 5. THE BUDGET AND REPORTING CYCLE 5.1. Let s illustrate a single budget and reporting cycle for the 2008/09 financial year. Diagram 2a: A single budget and reporting cycle BUDGET PREPARATION PROCESS BUDGET IMPLEMENTION PROCESS BUDGET EVALUATION PROCESS 2008/09 BUDGET 1 Aug 07 May 08 2 Jul 08 Jun 09 3 Jul 09 Mar 10 DOCUMENTS & REPORTING IDP SP MTREF MBPS Schedule Key Deadlines SDBIP AB MBS QPR MBPA AFS AR OR BEC Key to abbreviations: IDP Integrated Development Plan SP Sector Plans MTREF Medium Term Revenue and Expenditure Framework MBPS Municipal Budget Policy Statement SDBIP Service Delivery and Budget Implementation Plan AB Adjustments Budget MBS Monthly Budget Statements, S.71 MFMA QPR Quarterly Performance Report, S.52(d) MFMA MBPA Mid-year Budget and Performance Assessment, S.72 MFMA AFS Annual Financial Statements AR Annual Report OR Oversight Report BEC Budget Evaluation Checklist 20

22 5.2. Diagram 2a shows that the 2008/09 cycle begins with the budget preparation process, which includes reviewing the IDP and preparing the budget and (SDBIP) documentation. The second phase of the cycle is the budget implementation process, which includes implementing and monitoring implementation. The third phase of the cycle is the budget evaluation process which includes the audited Annual Financial Statements, Annual Report and Oversight Report Now let s see how in practice, multiple budget and reporting cycles occur concurrently and demonstrate how at any one point in time the municipality will be operating in a different process of each of the three cycles. Diagram 2b below shows a typical municipal scenario where three budget and reporting cycles are in operation. Diagram 2b: Multiple budget and reporting cycles BUDGET PREPARATION PROCESS BUDGET IMPLEMENTATION PROCESS BUDGET EVALUATION PROCESS 2008/09 BUDGET 1 Aug 07 May 08 2 Jul 08 Jun 09 3 Jul 09 Mar /10 BUDGET 1 Aug 08 May 09 2 Jul 09 Jun 10 3 Jul 10 Mar /11 BUDGET 1 Aug 09 May 10 2 Jul 10 Jun 11 3 Jul 11 Mar 12 DOCUMENTS & REPORTING IDP SP MTREF MBPS Schedule Key Deadlines SDBIP AB MBS QPR MBPA AFS AR OR BEC 5.4. Diagram 2b shows the budget and reporting cycles for 2008/09, 2009/10 and 2010/11. The un-shaded area represents a particular point in time where the municipality is busy with it s: 21

23 budget preparation process for 2010/11; budget implementation process for 2009/10; and budget evaluation process for 2008/ Note how the date ranges in the un-shaded boxes overlap The diagram above also shows the key documentation that needs to be prepared for each of the three processes Note that throughout the three processes there are a range of technical activities which in the main are managed by the budget and treasury office. For example, these include: maintaining accounting and information systems for management, statutory and other requirements; maintaining systems of internal control and risk management; preparing budget estimates for recurring activities and new programmes / capital projects; identifying potential efficiency savings and alternative sources of revenue; testing funding compliance of the budget; providing budget documentation which facilitates prioritisation by council; preparing management reporting and providing advice; preparing in-year reports required for submission to the mayor, council and stakeholders supporting the council committees in place dealing with financial matters; and 22

24 preparing statutory reporting such as the 5.8. These technical activities are mentioned to provide the learner with insight into what sits behind the three budget and reporting processes but are not covered in detail by this unit standard The next chapter will consider the three processes (preparation, implementation, and evaluation) in detail. ACTIVITY / CLASS DISCUSSION: Consider the budget and reporting cycle in your municipality. Using those listed in the diagram above as a checklist, write down the documents and reports currently prepared. Which ones are not being prepared? Do you think there is a common understanding amongst the key role players that there are three processes going on at any one time? What could you do to improve that understanding? 23

25 5.10. MEDIUM TERM REVENUE AND EXPENDITURE FRAMEWORK (MTREF) As with the national and provincial governments, municipalities are required to table and adopt an annual budget covering three-years. Through a continuous cycle of forecasting, implementation and review municipalities must manage their finances across the three-year timeframe By adopting three-year budgets linked to longer-term goals contained in the IDP, municipalities can adopt more forward looking and better-informed approaches and make better judgements about the future priorities for capital development and service delivery in their communities SEVEN YEAR HORIZON During the budget prepartion process it is useful to consider a seven year horizon. In the diagram below a municipality is preparing the 2008/09 Budget, which is a Medium Term Revenue and Expentiture Framework (MTREF). A municipality bases its 2008/09 MTREF on the strategic direction in the IDP and information about past performance, including the current year and audited information on previous years This format above is consistent with National and Provincial budget requirements It provides for three years of audited outcome figures providing background trend verification. which overcomes the disadvantage that one year of audited history alone is not a sound basis of performance comparison. The additional information will improve the analysis of the budget as an early-warning mechanism and a forecasting tool. 24

26 Four columns are required for the year currently being implemented - Original Budget, Adjusted Budget, Full-year forecast and Pre-audit outcome. The term Full-year forecast is also known as estimated actual outcome. This information of recent trends and performance is vital for strategic decisions on the new budget. Furthermore, it is critical to note the importance of the original budget as this was the budget that was extensively consulted on. Significant differences between the original budget, adjusted budget and full year forecast would tend to indicate poor planning and unrealistic budgets Three columns are required for the medium term revenue and expenditure framework (MTREF), showing the budget year, and the projections for two years following the budget year. This is now a standard feature for municipalities In South Africa, the local, provincial and national spheres of government are required to focus on three simultaneous budget cycles. So while preparing the budget for the next three years, each is still implementing the current year s budget whilst also closing off and preparing financial statements and annual reports for the previous financial year Planning for a budget cycle requires an understanding of the sequence of events and the governance principals that underpin sound financial management. The following headings will discuss these important principals and the legislative framework behind the budget and reporting cycle. 6. A STRATEGIC APPROACH TO BUDGETING 6.1. At this point it is worth briefly noting the new focus on a strategic approach to budgeting Prior to the reforms of the Municipal Finance Management Act 2003 (MFMA) and Municipal Systems Act 2000 (MSA) municipal budgets focused on one-year of estimates and were based mainly on applying increments to the previous year s budget. The budgeting and planning processes were not integrated, often operating completely separately. Budgets were not presented to council in a summary form to highlight the financial implication of policy decisions. This 25

27 hampered effective policy and planning processes making consultation unwieldy; revenue and capital estimates were unrealistic, resulting in poor service-delivery performance and disappointing community expectations; and there appeared to be little or no linkage to a comprehensive long-term fiscal or financial strategy With the introduction of the MFMA these past practices have been addressed. The following extract provides a synopsis of the objective behind the change. Extract from the White Paper on Local Government, March 1998 Municipal budgets are a critical tool for re-focusing the resources and capacity of the municipality behind developmental goals. To this end, budgets must be developed in relation to the policies and programmes put forward in municipal integrated development plans. Given that resources are scarce, community participation in the development of both integrated development plans and municipal budgets is essential. Participation provides an opportunity for community groups to present their needs and concerns. It enables them to be involved in the process of prioritisation, and to understand and accept the trade-offs which need to be made between competing demands for resources. 7. SEPARATION OF ROLES AND RESPONSIBILITIES 7.1. Councillors have a constitutional role as politically elected representatives of the community, to approve policies and budgets proposed by the executive mayor or committee and then oversee the performance of the municipality in implementing these policies and budgets. For this reason, the MFMA assumes a separation between councillors serving on the executive (i.e. mayor or executive committee) and non-executive councillors. The executive mayor or executive committee are expected to provide the municipality with political leadership, by proposing policies, budgets and performance targets for the municipality and its officials. 26

28 7.2. The MFMA differentiates between the role of executive councillors and municipal officials by making the executive mayor or committee responsible for policy and outcomes and the municipal manager and other senior managers for implementation and outputs. The executive mayor or committee is expected to oversee the performance of its officials, using the service delivery and budget implementation plan (SDBIP) and monitoring performance through monthly progress reports. Non-executive councillors are expected to hold both the executive mayor or committee and the officials accountable for performance, on the basis of monthly, quarterly, mid-year and annual reports This separation of responsibilities between executive councillors, non-executive councillors and officials is important for good governance and is in line with modern practices of effective public management. The aim of the MFMA is to allow managers to manage, but to make them more accountable All these various roles are possible only because of the reporting requirements of the MFMA, as the MFMA recognises that effective service delivery is possible only with good-quality and timely management information. Such information allows management to be proactive, identifying and solving problems as they arise. Roles and responsibilities of the key players is discussed in detail in Chapter 5 of these module notes. 8. ACCOUNTABILITY CYCLE 8.1. The requirements for municipal budgeting in South Africa have undergone a significant modernization since Municipal budgeting is now seen as a strategic tool focusing on non-financial as well as financial targets. Targets in a municipal Integrated Development Plan (IDP) are linked to the targets in the: budget; the service delivery and budget implementation plan (SDBIP); and annual performance agreements of senior managers. 27

29 8.2. Once the three items above are finalised the SDBIP is used as a tool to implement the budget. Monitoring and evaluation of performance against budget is done through mid year and annual reporting. It s a constant process to review strategic direction, plan, implement, assess actual performance and discharge accountability At this point it is useful to consider some key definitions and concepts. The purposes of the definitions below are to give a brief introduction and not to teach everything there is to know. DEFINITIONS: IDP Budget SDBIP An Integrated Development Plan (IDP) is an all encompassing strategic plan for the municipality giving due regard to community needs and the strategic plans of other stakeholders such as national and provincial departments, public entities and other municipalities. It contains long term strategic goals and targets. In the municipal context a budget is a Medium Term Revenue and Expenditure Framework (MTREF) covering at least 7 years. Three years of audited history, the current year being implemented, the budget year and two outer year forecasts. The objective of the budget is to allocate limited resources to policy priorities set out in the IDP. The medium term aspect of a municipal budget facilitates a more strategic and sustainable result. The Service Delivery and Budget Implementation Plan, is more detailed than the budget. It is the operational plan required to implement the budget and will include quarterly service delivery targets and monthly targets for revenue and expenditure. Managers can use the SDBIP as an implementation tool and council can use it to assess performance. 28

30 DEFINITIONS: Adjustments Budget In-year Reports Annual Financial Statements Annual Report Oversight Report An adjustments budget is the mechanism to amend an approved budget under certain specified conditions. The most appropriate time for an adjustments budget would be together with the mid-year budget and performance review although other circumstances may require alternate timing and regulations will specify requirements. In-year reports for municipalities consist of monthly budget statements, quarterly reports and a mid-year budget and performance assessment. The annual financial statements of a municipality conform with accounting standards applicable to local government. They reflect the financial performance and financial position of a municipality and increasingly include information on non-financial performance. Annual Financial Statements must be audited and an audit opinion is expressed on their accuracy. The municipal annual report is a comprehensive public document that encompasses the audited financial statements and focuses on accountability for financial and non-financial performance against the targets in the SDBIP for the year completed. The municipal oversight report contains council s comments on the annual report and includes a statement approving, rejecting or referring the annual report back for revision and thus completing the accountability cycle Council has a key oversight role in order to ensure accountability to the community and other stakeholders. This process is known as the accountability cycle and is illustrated by the following diagrams. A basic knowledge of the definitions above will assist your understanding of the diagrams The first diagram focuses on the processes in the accountability cycle and the second diagram shows the roles and responsibilities in the accountability cycle. 29

31 ACTIVITY / STUDY: Take 5 minutes to study the first diagram referring back to key definitions and concepts. Think about the role of each step in terms of preparing, implementing and monitoring and evaluating the budget. ACTIVITY / STUDY: Take 5 minutes to study the second diagram whilst reading the explanatory text below the diagram. Think about the roles and responsibilities of each role player in terms of: budget preparation budget implementation (including monitoring) budget evaluation 30

32 Diagram 2c: Accountability cycle processes 31

33 Diagram 2d: Accountability cycle roles & responsibilities 8.6. The accountability cycle commences with policy direction from the community and other stakeholders through council to the municipal administration. In turn the administration is accountable to council for implementing policy. The council is accountable for performance to the community and other stakeholders. 9. CONSULTATIVE PROCESSES 9.1. Both the MSA and MFMA require extensive consultations with the local community and other stakeholders for important decisions like budgets, borrowing, IDPs, performance systems, and annual reports Section 16 of the MFMA requires the budget resolutions; proposed revisions to the IDP; budget related policies; and other required supporting documentation to be tabled before a full council meeting by 1 April (i.e. at least 90 days before the start of the budget year). This allows adequate time for consultation prior to 32

34 approval of the budget and ensures that councillors are aware of the budget implications so they can consult with their constituents The MFMA also requires consultation with relevant government departments and municipalities affected by the budget. Consultation with provincial and national sector departments such as, Agriculture, Health, Housing, Education, Welfare, Water Affairs and Mineral and Energy Affairs will ensure improved co-operative governance between the spheres. It is recommended that municipalities contact their Provincial Treasuries to coordinate consultation meetings with relevant provincial departments. This engagement will ensure better coordination, alignment and resource allocation from provincial and national governments District and local municipalities must consult each other when finalising plans and budgets to ensure that allocations between them are aligned, priorities are addressed and implementation is executed during the year. Historically, delays in project approval, spending and implementation have occurred undermining service delivery due to a lack of this early consultation. District municipalities must consult all municipalities within its area and must notify relevant municipalities of projected allocations, for the next three budget years, no later than 2 March (120 days prior to the start of the budget year). These allocations must be published with the draft municipal budget and will be audited by the Office of the Auditor- General to ensure consistency of amounts reflected in the transferring municipality and the recipient municipality The MFMA requires that municipalities submit their tabled and approved budgets to National Treasury and the relevant provincial treasury Municipalities will need to keep abreast of developments in the various sectors to ensure their budgets for water, sanitation, electricity etc are well informed. Municipal IDPs and budgets should inform and be informed by the development plans of sector departments to ensure a coordinated approach to infrastructure planning and service delivery. Furthermore, municipalities should have a good knowledge of all grants from government departments including their objectives, conditions and medium term allocations as gazetted. To assist municipalities in proper planning and budgeting all role-players are to provide information on 33

35 allocations in provincial budgets and the annual Division of Revenue Act around February and March that reflect transfers to municipalities over a multi year period Hence, it is critical that early on in the budget process, the mayor coordinates a schedule of key deadlines for all of the required meetings, workshops, community forums etc and makes this schedule public so that those being consulted are aware of their opportunities for input into the IDP and budget process. ACTIVITY / CLASS DISCUSSION: List the different consultative processes undertaken at your municipality. Are they considered as part of ONE overall process? 10. LEGISLATIVE FRAMEWORK For the purposes of planning a municipal budget and reporting cycle it is necessary to have a broad understanding of the legislative framework applicable to local government. The following discussion considers some of the more important aspects and synergies between the applicable legislation. Learners should understand the applicable legislation so that they are able to refer to specific requirements in practice The Municipal Finance Management Act (MFMA) must be read with other national legislation, particularly close linkages and alignment between the MFMA and the Municipal Systems Act (MSA). This should be recognised early on for a better understanding, correct interpretation and application of the two pieces of legislation. These two Acts are complementary to each other in many areas, and should therefore be read together. For example, chapter 5 of the MSA deals with IDPs and the preparatory process, whilst chapter 4 of the MFMA deals with budgets and their preparatory process. These two processes are however ONE 34

36 process, and not two separate processes, as the IDP and budget must be fully aligned and consistent with each other Other legislation impacting on local government includes, the Constitution of the Republic of South Africa, Intergovernmental Fiscal Relations Act, Structures Act, Demarcation Act, Property Rates Act, Water Services Act, Electricity Act, Transport Act, annual Division of Revenue Act, Municipal Fiscal Powers and Functions Act and their supporting regulations. Below we discuss only some of the main areas of linkages and alignment that must be considered CONSTITUTIONAL AMENDMENTS Areas of significance include recent amendments to the Constitution. The first relates to section 230A on borrowing, providing that loans may be raised for capital or current expenditure, with loans for current expenditure limited to use for bridging purposes during the fiscal year, and binding current and future councils to honour this decision. The other significant amendment relates to section 139 and deals with provincial interventions in a municipality. This allows the provincial executive to take appropriate steps in the event of a municipality s failure to fulfil an executive or legislative obligation, including the power to dissolve a council. The legislative obligation relates to the approval of a budget or other revenue-raising measures. This includes the imposition of a recovery plan in the case of an emergency when there is a persistent material breach of its obligations to provide basic services or to meet financial commitments THE MFMA AND THE MUNICIPAL SYSTEMS ACT Both the Municipal Systems Act and the MFMA deal with the internal processes, consultative processes, performance systems and reporting and accountability mechanisms. Parliament devoted a great deal of effort to ensure that the two Acts are totally consistent with each other, leading to amendments to the MSA. It is important to ensure that the MSA is read with the two sets of amendments, as per the Local Government Laws Amendment Act (Act 51 of 2002) and the MSA Amendment Act (Act 44 of 2003). 35

37 10.6. DEFINITIONS The first point to note is that the definitions in both the MSA and MFMA are similar, and there is much cross-referencing in the MFMA to definitions in the Municipal Systems Act. This applies to key definitions on municipal services, service delivery agreements, local community etc IDP AND BUDGETS The MFMA and the Municipal Systems Act contain practical synergies that relate to good governance, consultation and accountability issues. A direct interrelationship exists when a municipality contemplates its processes with regards planning and budgeting. The amendment to the Municipal Systems Act and the MFMA chapter on budgeting require that a revised IDP be adopted at the time of adopting the budget. It follows that, in practice, the planning and budgeting processes will commence together at least 10 months before the start of the municipal financial year, when the mayor announces the process for revising the IDP and preparation of budget. Also, the alignment of policies through the adoption of the budget and other related policies such as the levying of fees for municipal services is made more explicit at the time of drafting and adopting the budget PERFORMANCE SYSTEMS AND ANNUAL REPORTS Both the MFMA and MSA are built on the adoption by the municipality of a performance system. The budget of the municipality must contain performance targets and measurable objectives, which are set out at the beginning of the financial year (section 17 of the MFMA). Linked to these performance targets are the adoption of the annual service delivery and budget implementation plan (SDBIP) and annual performance agreement between the mayor (or executive committee) and municipal manager (refer to section 57 of the MSA as amended, and sections 53 and 69 of the MFMA) At the end of the financial year, the municipality must publish an annual report, reporting on both its financial and non-financial performance. Whilst the MFMA 36

38 focuses on financial performance (chapter 12), the MSA focuses on non-financial performance (section 46 of MSA as amended). The annual report will be considered by the municipal council using the process outlined in chapter 12 of the MFMA ROLES OF MAYOR, COUNCILLORS AND OFFICIALS Both the MSA and MFMA make common assumptions about the role of various stakeholders in the municipality. Such roles also inform the code of conduct for councillors and officials as set out in Schedules 1 and 2 of the MSA. In addition, if there are financial transgressions, financial misconduct provisions and criminal sanctions apply in terms of chapter 15 of the MFMA. Where councillors or officials transgress their role or code of conduct, strict provisions apply ASSIGNMENT OF FUNCTIONS Cooperation between governments is strengthened through these Acts, and when there is an assignment of a function or power to a municipality there must be comment by the Financial and Fiscal Commission and consultation with the Minister of Finance on the assignment, including possible liabilities. This aspect strengthens co-operative government and links with chapter 5 of the MFMA and directly impacts on the Division of Revenue Act. The other area of cooperation relates to the provision of services through service delivery agreements and the use of external mechanisms. An important area of alignment relates to the process of establishing an external mechanism to provide municipal services. The community consultation, assessments, capacity, feasibility studies, value for money, measurement of risk, projected borrowing and fiscal implications are all linked to the IDP and budget process OTHER LEGISLATION AND THE MFMA The earlier sections draw attention to those linkages with other legislation that set the foundations of the system and structure of local government, but also important is the sector-specific focus. Apart from the Constitution and Municipal Systems Act and other national local government legislation like the Local 37

39 Government: Municipal Structures Act, Property Rates Act and Municipal Demarcation, there are a number of national Acts of Parliament that impact on the MFMA. These include the following: Financial legislation like the Constitution of the Republic, Intergovernmental Fiscal Relations Act, Financial and Fiscal Relations Act, Preferential Procurement Policy Framework Act and the annual Division of Revenue Act Other local government legislation like the Municipal Structures Act, Demarcation Act and Property Rates Act Sectoral legislation like the Water Services Act, Electricity Act, Transport and Environment Acts The Remuneration of Political Office-bearers Act Planning legislation like the Land Development Objectives Act Labour legislation, including the Labour Relations Act, Skills Development Act, as well as pension and medical aid legislation The Intergovernmental Fiscal Relations Act establishes the process of consultation for budget allocations, including the role of the Budget Forum. The annual Division of Revenue Act is one of the important pieces of budget legislation for local government, as it provides national allocations for the local government sphere by municipality, for each of the coming three years The Financial and Fiscal Commission Act (FFC) is also important for the local sphere. Not only does it spell out the process for filling vacancies to the FFC, but also includes rigorous provisions in the revised section 5 on the role of the FFC before any new function is shifted to local government. This assignment clause should also be read with section 10 of the amended MSA. Some of the other pieces of legislation that impact on and should be read with the MFMA are the sectoral legislation relating to water and electricity and transport. The Water Services Act, Act 108 of 1997, contains provisions relating to norms and 38

40 standards, the development of plans and tariff mechanisms. Whilst the Electricity Act, Act 41 of 1987 (as amended), also contains provisions relating to the electricity regulator, it deals with aspects of licensing, the sale and supply of electricity within municipalities and tariffs. Note that where there is any conflict between such national legislation and the MFMA or MSA, it is the latter two Acts that take precedence, depending on the issue Particular note should be made of sections 42 and 43 of the MFMA, which take precedence over section 94(1)(c) and section 10 of the Water Services Act if a municipality properly consults (in terms of sections 33 and 46) with the relevant national departments when setting tariffs for long-term contracts. The applicability of these provisions and those in the MFMA especially that relating to budget preparation and consultation in chapter 4, co-operative government and pricing of bulk services in chapter 5 will assist in better management of processes whilst offering a mechanism for dispute resolution between organs of state. The MFMA requires that a structured process be followed to ensure that consultation is appropriately addressed. The improvement in the content and quality of municipal budgets will also assist. These provisions promote cooperative government between the national and local spheres in the tariff setting process. Sector departments will have to monitor the achievement of sector priorities The Property Rates Act contains further related provisions that deal with the adoption and contents of a rates policy, increases and their timing and documentation that must accompany the budget as outlined in the MFMA. It also requires alignment with community participatory processes and specifically publication of information with the budget. The period for which rates are levied is the same as the budget, unless imposed as part of a recovery plan. The limitation on increases in rates is directly aligned with the MFMA. There are also linkages with the supply chain management framework when securing the services of private providers in the execution of the municipal valuation exercise. 39

41 SUMMARY The above brief explanation should not be considered as exhaustive, but it highlights the linkages and synergies with the MFMA and other legislation. It also attempts to clarify the policies of government. It should serve as an illustration of the extent to which other pieces of legislation impact on the applicability of the MFMA and vice versa. ACTIVITY / CLASS DISCUSSION: What are the two main pieces of legislation impacting on the municipal budget and reporting cycle? Why have they been synchronised? 11. ASSIGNMENTS The following assignments are to be completed after the workshop on this chapter and handed in prior to, or at the beginning of, the next workshop ASSIGNMENT 2.1 (15 MARKS) Describe the budget and reporting cycle. Explain how the processes interrelate using an example ASSIGNMENT 2.2 (11 MARKS) In the context of the municipal budget and reporting cycle explain the need for separation of roles and responsibilities. 40

42 12. ASSESSMENT CRITERIA In terms of the regulatory framework for the municipal budget cycle, identify the roles and responsibilities of municipal political executives, accounting officers and senior managers in the budget preparation [SO1AC2] Include roles and responsibilities of Mayor, municipal manager, council, CFO, senior managers [SO1ACR1] Plan the tabling and adoption of a municipal budget as required by legislation [SO2AC1] 41

43 Components of the budget and reporting cycle 1. LEARNING OUTCOMES 1.1. Understand the components of the budget and reporting cycle in a municipal context. 2. KEY CONCEPTS 2.1. Budget preparation process Budget preparation process timeline Six steps to preparing a budget (Planning, Strategising, Preparing, Tabling, Approving, Finalising) Schedule of key deadlines Budget evaluation checklist Format of budget documentation to be tabled Consultation 2.2. Budget implementation process Using the budget and SDBIP to implement the budget Monthly budget statements Quarterly reports Mid year budget and performance assessments Adjustments budgets conditions and frequency 42

44 Shifting funds between multi-year appropriations 2.3. Budget evaluation process 2.4. Audited annual financial statements 2.5. Annual reports 2.6. Oversight reports 3. LEARNING ASSUMED TO BE IN PLACE 3.1. Prior to commencing this chapter of the module notes the learner must have completed the previous chapter(s) The learner is reminded that prior to attending a workshop on this chapter they must: read this chapter module notes; complete assigned reading or study which includes MFMA Learning modules bring completed answers to the activities/class discussion for this chapter for discussion during the workshop bring completed answers to the short assignments for the previous chapter to be handed in for marking. 4. INTRODUCTION 4.1. This chapter will consider the detail behind the budget and reporting cycle processes (preparation, implementation and evaluation). Chapter 5 will then 43

45 present a financial management calendar which incorporates all of the legislative requirements for the budget and reporting cycle. ACTIVITY / STUDY: Complete module 3 of MFMA Learning now. 5. BUDGET PREPARATION PROCESS 5.1. The budget preparation process will commence about 12 months before the start of the budget year. It is considered that a well-run budget preparation process that incorporates the IDP review will facilitate community input, encourage discussion, promote a better understanding of community needs, provide an opportunity for feedback and improve accountability and responsiveness to the needs of the local communities. It also positions the municipality to represent the needs of the community and to provide useful inputs to the relevant provincial and national department strategies and budgets for the provision of services such as schools, clinics, hospitals and police stations SIX STEPS TO PREPARING A BUDGET The following table sets out six distinct steps to the preparation of a budget. It is important to mention up front that consultation on the budget occurs throughout the preparation process. 44

46 Diagram 3a: Six steps to preparing a budget ACTIVITY / STUDY: Study the table above and refer to the budget preparation process timeline below. 45

47 Diagram 3b: Budget preparation process timeline Now let us consider each of the steps in more detail STEP 1: PLANNING The Mayor will lead a review of the previous budget process and incorporate findings into planning the next budget process. This step commences at the latest on the 1st of July and must be completed by no later than 31st of August with the tabling of the schedule of key deadlines Coordination of the budget preparation process Section 21 of the MFMA is the primary provision relating to the municipal budget preparation process. It requires the mayor to coordinate the processes for preparing the annual budget and for reviewing the Integrated Development Plan (IDP) and budget related policies. The mayor must table in council by 31 August (10 months before the start of the budget year) a schedule of key deadlines for various budget related activities spelled out in section 21. The accounting officer 46

48 is tasked by section 68 of the MFMA with assisting the mayor in developing and implementing the budget preparation process. The process should provide for both internal (within municipality) and external (local community and other stakeholder) consultations. ACTIVITY / READ: Read sections 21 and 68 of the MFMA The schedule of key deadlines (below) is an example that can be adapted to suit individual municipalities. Please note that where a specific time frame is shown in the example, it is a deadline requirement of the MFMA and must be complied with. Municipalities are advised to make public a simplified version of the schedule to ensure the community is aware of the timelines, process and opportunities and to have input to the IDP and budget. A simplified version of the schedule should be placed in local newspapers, newsletters and the municipal website alerting the public that more information on the budget process is available on the municipal website and in offices, including how the public can make an input into the budget process. ACTIVITY / STUDY: Spend 30 minutes studying the schedule of key deadlines below. Read each section of the appropriate Act referred to and note the definitions at the end of the schedule. 47

49 Diagram 3c: Time schedule of key deadlines TIME SCHEDULE OF KEY DEADLINES Mayor to Table in Council 10 Months Prior to Start of Budget Year Month Municipality Budget Year Mayor and Council / Entity Board Administration - Municipality and Entity July August Mayor begins planning for next three-year budget in accordance with co-ordination role of budget process MFMA s 53 Planning includes review of the previous years budget process and completion of the Budget Evaluation Checklist Mayor tables in Council a time schedule outlining key deadlines for: preparing, tabling and approving the budget; reviewing the IDP (as per s 34 of MSA) and budget related policies and consultation processes at least 10 months before the start of the budget year. MFMA s 21,22, 23; MSA s 34, Ch 4 as amended Mayor establishes committees and consultation forums for the budget process Accounting officers and senior officials of municipality and entities begin planning for next three-year budget MFMA s 68, 77 Accounting officers and senior officials of municipality and entities review options and contracts for service delivery MSA s

50 TIME SCHEDULE OF KEY DEADLINES Mayor to Table in Council 10 Months Prior to Start of Budget Year Month Municipality Budget Year Mayor and Council / Entity Board Administration - Municipality and Entity September Council through the IDP review process determines strategic objectives for service delivery and development for next threeyear budgets including review of provincial and national government sector and strategic plans Budget offices of municipality and entities determine revenue projections and proposed rate and service charges and drafts initial allocations to functions and departments for the next financial year after taking into account strategic objectives Engages with Provincial and National sector departments on sector specific programmes for alignment with municipalities plans (schools, libraries, clinics, water, electricity, roads, etc) October Accounting officer does initial review of national policies and budget plans and potential price increases of bulk resources with function and department officials MFMA s 35, 36, 42; MTBPS November Accounting officer reviews and drafts initial changes to IDP MSA s 34 December Council finalises tariff (rates and service charges) policies for next financial year MSA s 74, 75 Accounting officer and senior officials consolidate and prepare proposed budget and plans for next financial year taking into account previous years performance as per audited financial statements 49

51 TIME SCHEDULE OF KEY DEADLINES Mayor to Table in Council 10 Months Prior to Start of Budget Year Month Municipality Budget Year Mayor and Council / Entity Board Administration - Municipality and Entity January February Entity board of directors must approve and submit proposed budget and plans for next three-year budgets to parent municipality at least 150 days before the start of the budget year MFMA s 87(1) Council considers municipal entity proposed budget and service delivery plan and accepts or makes recommendations to the entity MFMA s 87(2) Accounting officer reviews proposed national and provincial allocations to municipality for incorporation into the draft budget for tabling. (Proposed national and provincial allocations for three years must be available by 20 January) MFMA s 36 Accounting officer finalises and submits to Mayor proposed budgets and plans for next three-year budgets taking into account the recent mid-year review and any corrective measures proposed as part of the oversight report for the previous years audited financial statements and annual report Accounting officer to notify relevant municipalities of projected allocations for next three budget years 120 days prior to start of budget year MFMA s 37(2) 50

52 TIME SCHEDULE OF KEY DEADLINES Mayor to Table in Council 10 Months Prior to Start of Budget Year Month Municipality Budget Year Mayor and Council / Entity Board Administration - Municipality and Entity March April Entity board of directors considers recommendations of parent municipality and submit revised budget by 22nd of month MFMA s 87(2) Mayor tables municipality budget, budgets of entities, resolutions, plans, and proposed revisions to IDP at least 90 days before start of budget year MFMA s 16, 22, 23, 87; MSA s 34 Consultation with national and provincial treasuries and finalise sector plans for water, sanitation, electricity etc MFMA s 21 Accounting officer publishes tabled budget, plans, and proposed revisions to IDP, invites local community comment and submits to NT, PT and others as prescribed MFMA s 22 & 37; MSA Ch 4 as amended Accounting officer reviews any changes in prices for bulk resources as communicated by 15 March MFMA s 42 Accounting officer assists the Mayor in revising budget documentation in accordance with consultative processes and taking into account the results from the third quarterly review of the current year 51

53 TIME SCHEDULE OF KEY DEADLINES Mayor to Table in Council 10 Months Prior to Start of Budget Year Month Municipality Budget Year Mayor and Council / Entity Board Administration - Municipality and Entity May Public hearings on the budget, and council debate. Council Accounting officer assists the Mayor in preparing the final budget consider views of the local community, NT, PT, other provincial documentation for consideration for approval at least 30 days before the and national organs of state and municipalities. Mayor to be start of the budget year taking into account consultative processes and provided with an opportunity to respond to submissions during any other new information of a material nature consultation and table amendments for council consideration. Council to consider approval of budget and plans at least 30 days before start of budget year. MFMA s 23, 24; MSA Ch 4 as amended Entity board of directors to approve the budget of the entity not later than 30 days before the start of the financial year, taking into account any hearings or recommendations of the council of the parent municipality MFMA s 87 52

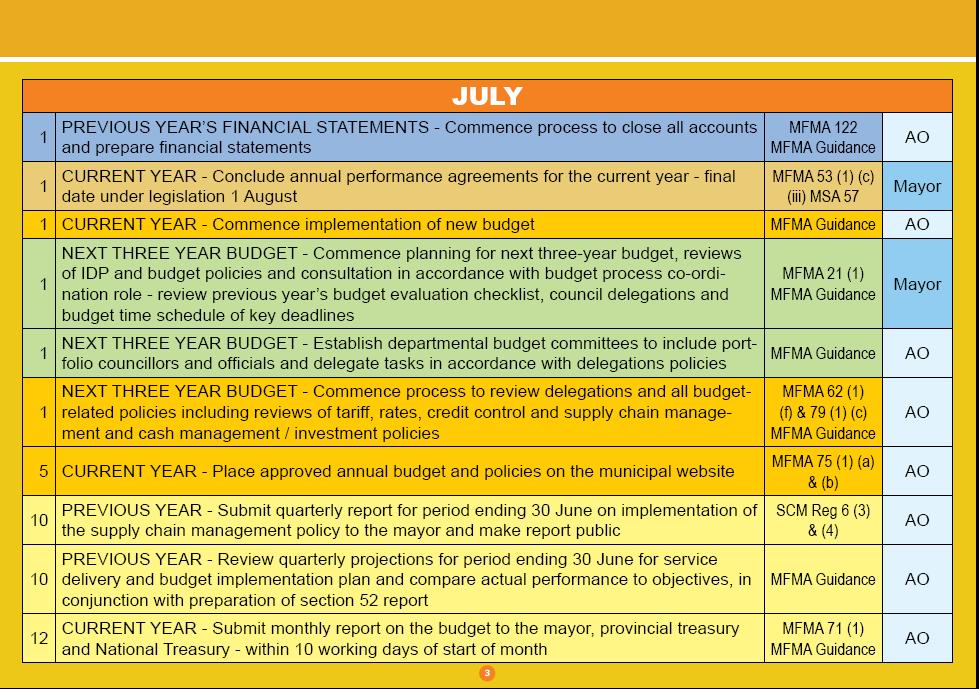

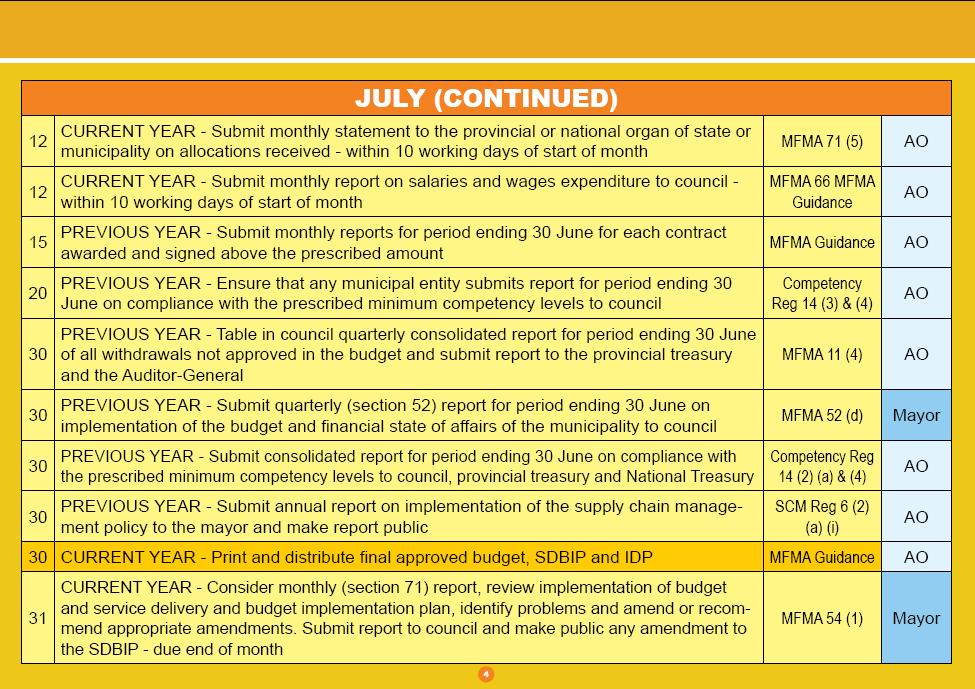

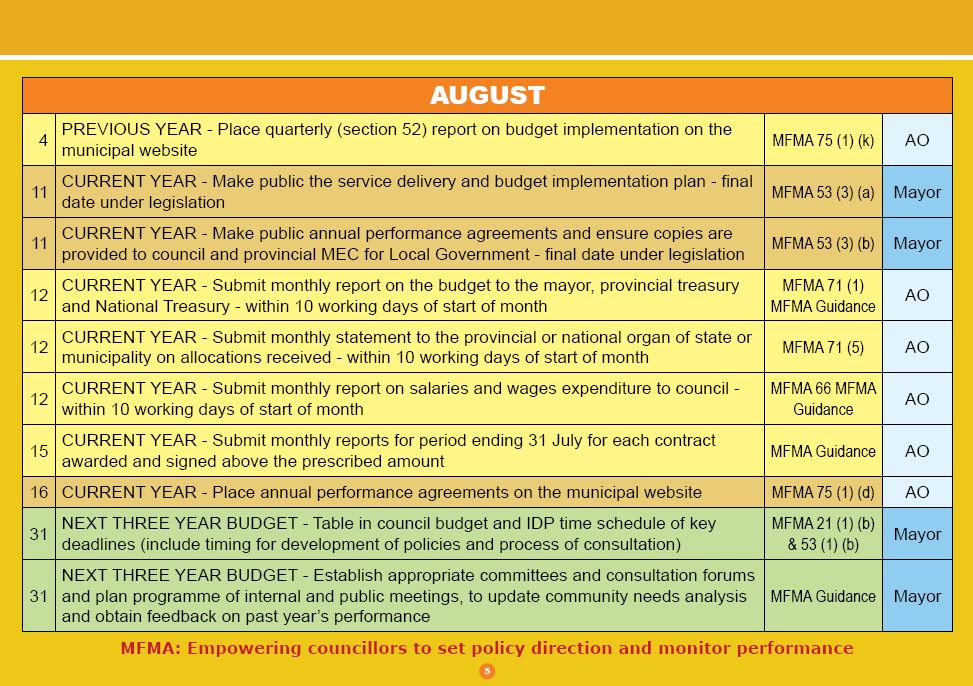

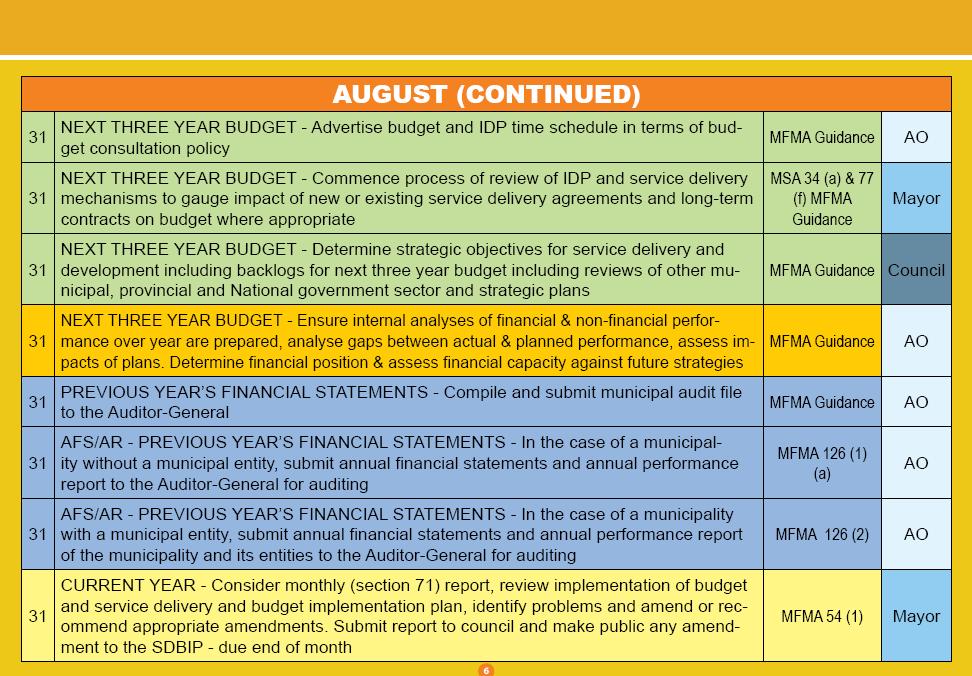

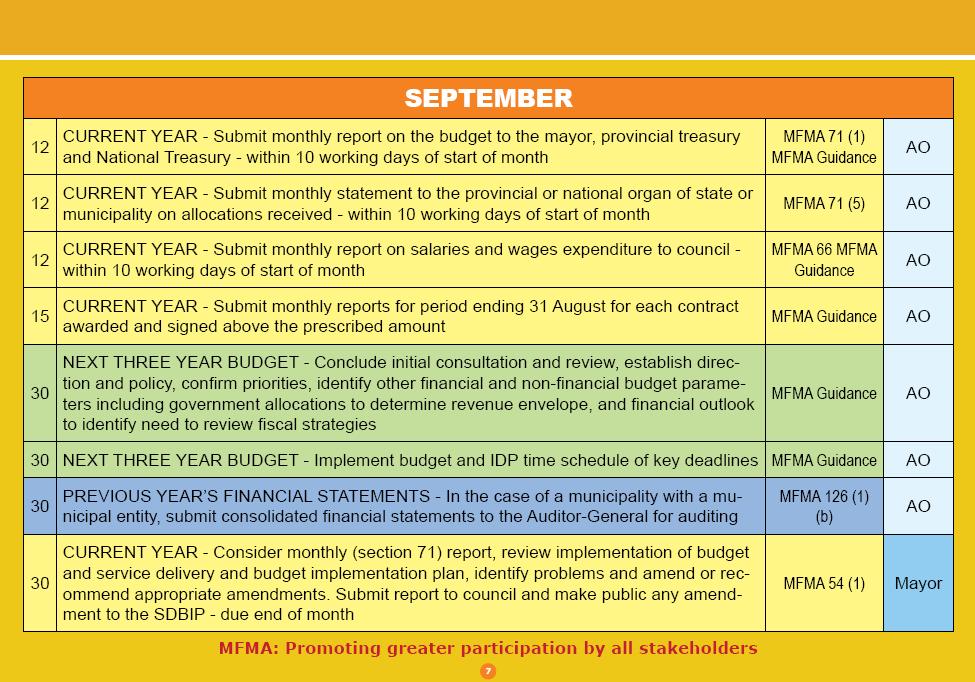

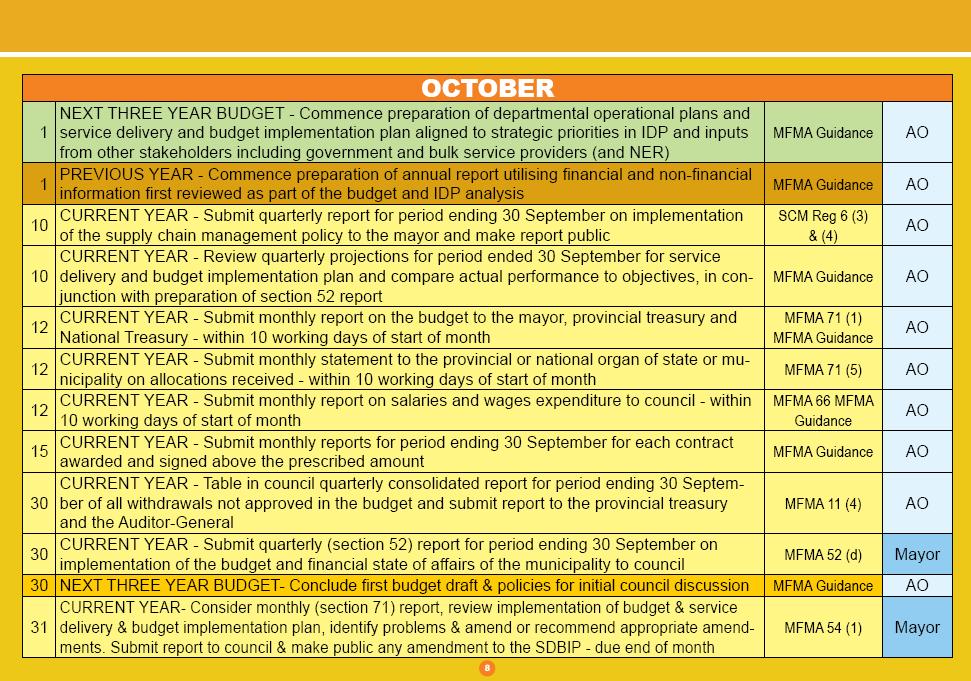

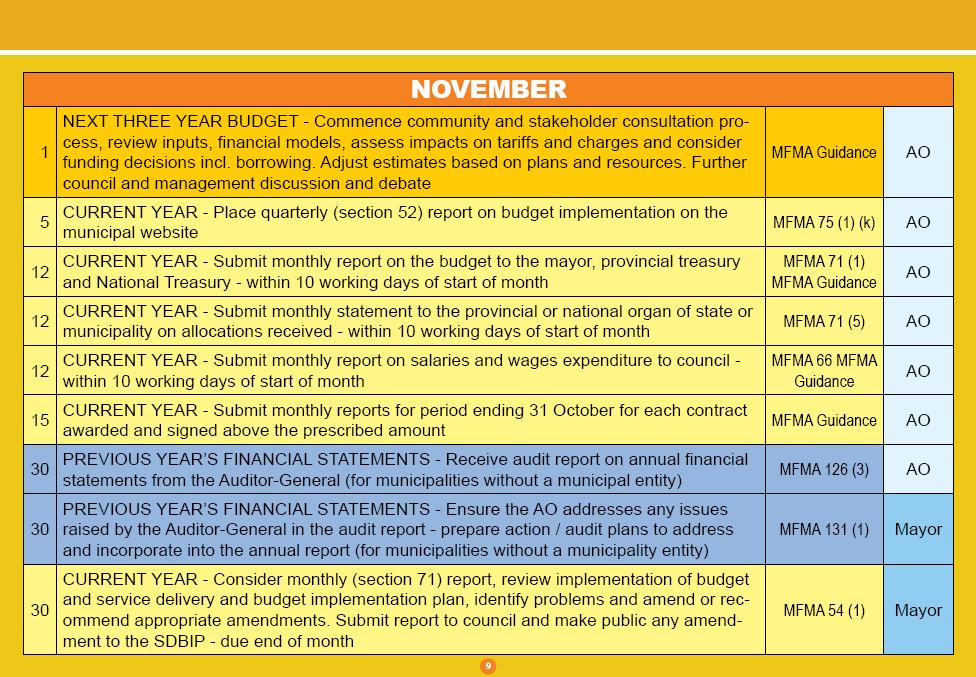

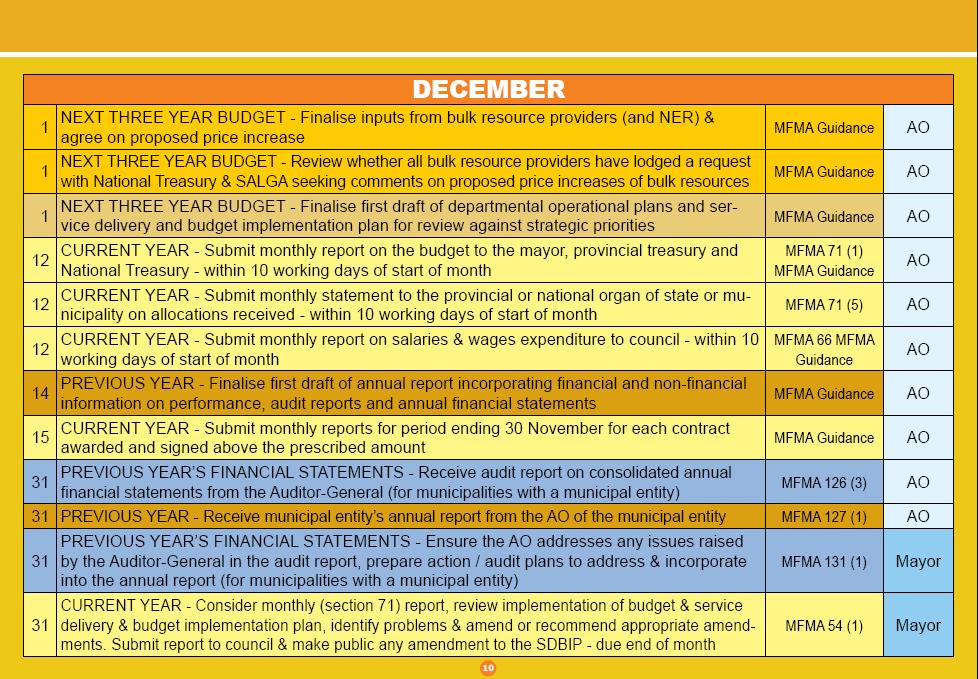

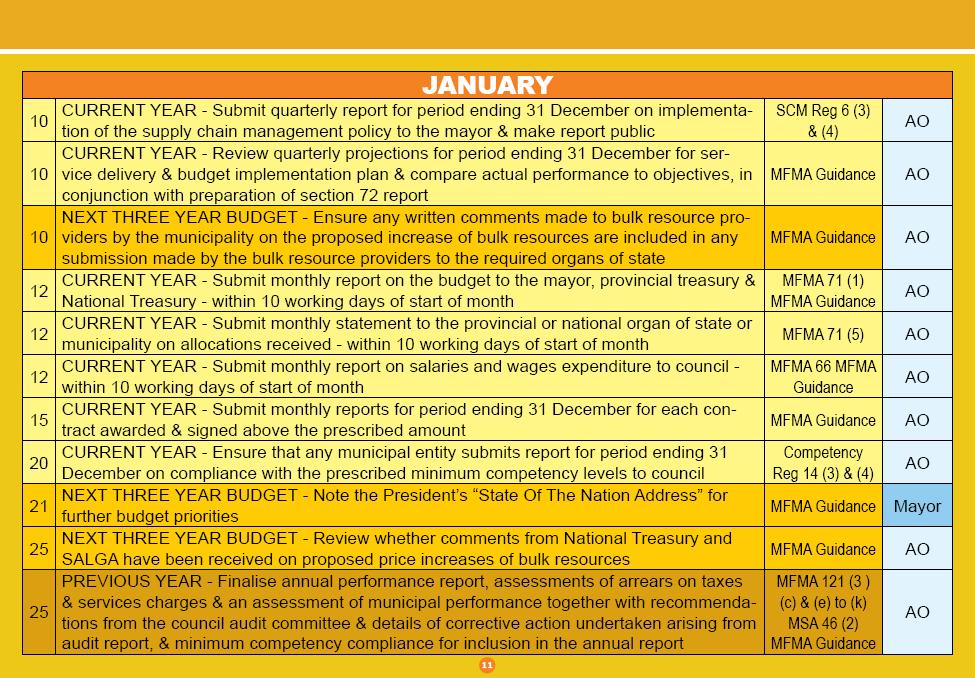

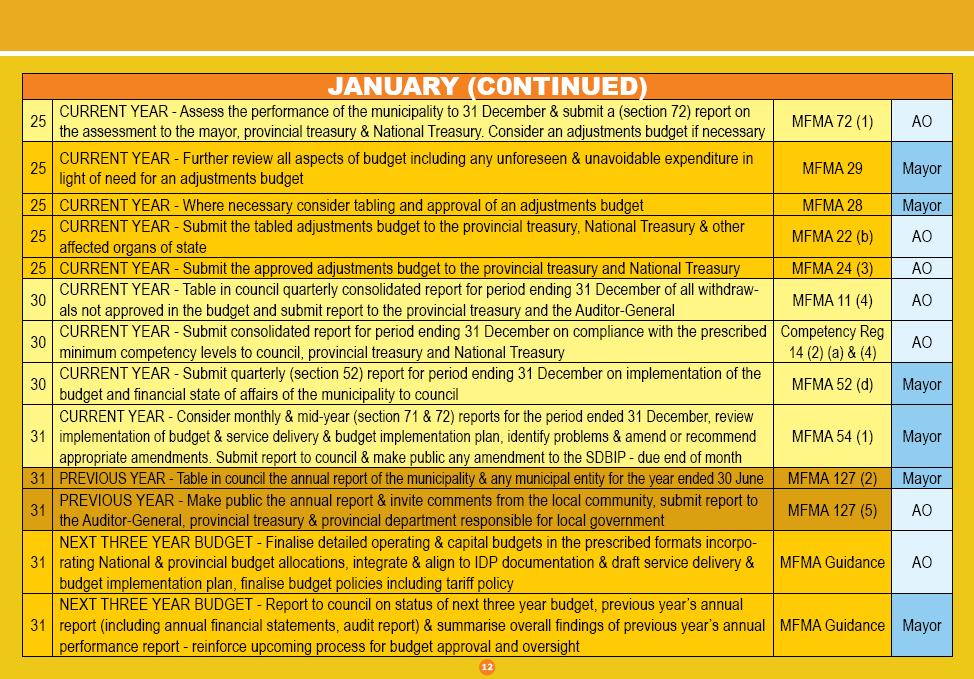

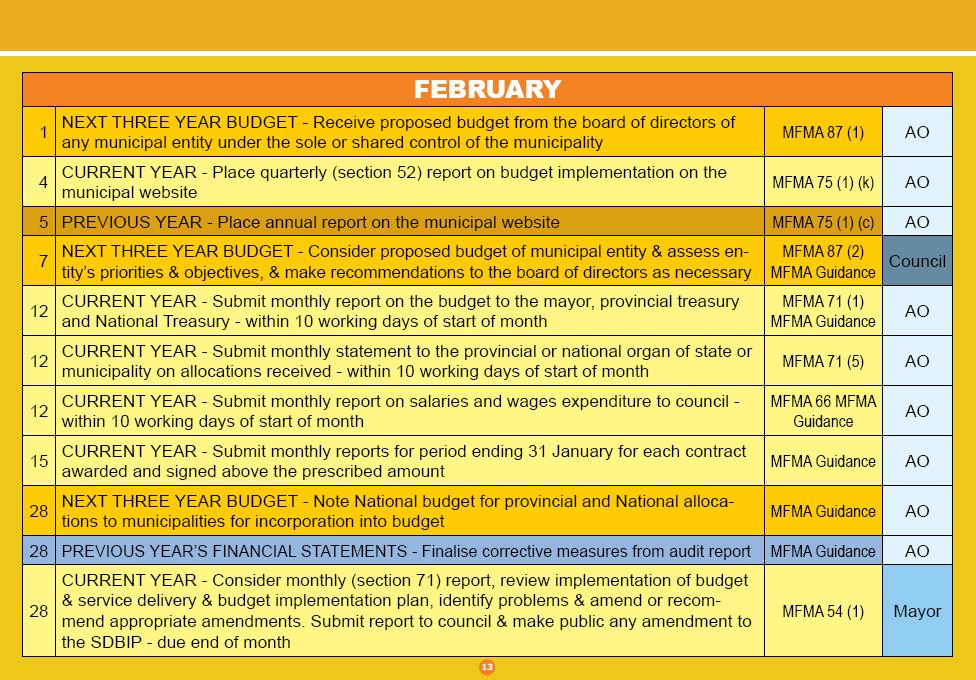

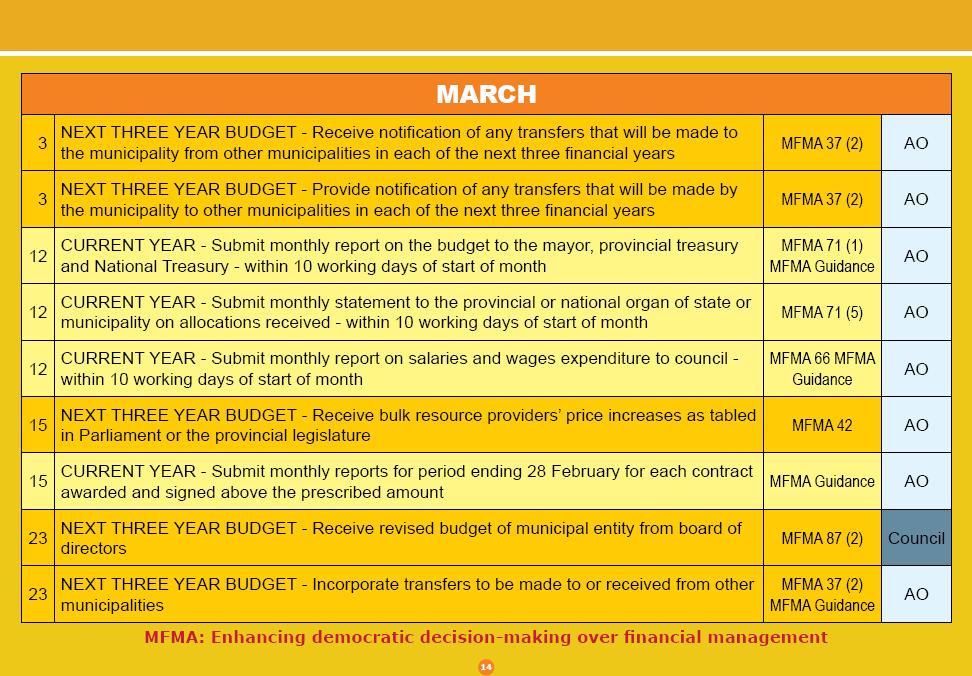

54 TIME SCHEDULE OF KEY DEADLINES Mayor to Table in Council 10 Months Prior to Start of Budget Year Month Municipality Budget Year Mayor and Council / Entity Board Administration - Municipality and Entity June Council must approve annual budget by resolution, setting taxes Accounting officer submits to the mayor no later than 14 days after and tariffs, approving changes to IDP and budget related policies, approval of the budget a draft of the SDBIP and annual performance approving measurable performance objectives for revenue by agreements required by s 57(1)(b) of the MSA. source and expenditure by vote before start of budget year MFMA s 69; MSA s 57 MFMA s 16, 24, 26, 53 Accounting officers of municipality and entities publishes adopted budget Mayor must approve SDBIP within 28 days after approval of the and plans budget and ensure that annual performance contracts are MFMA s 75, 87 concluded in accordance with s 57(2) of the MSA. Mayor to ensure that the annual performance agreements are linked to the measurable performance objectives approved with the budget and SDBIP. The mayor submits the approved SDBIP and performance agreements to council, MEC for local government and makes public within 14 days after approval. MFMA s 53; MSA s 38-45, 57(2) Council must finalise a system of delegations. MFMA s 59, 79, 82; MSA s Abbreviations: IDP - Integrated Development Plan; MFMA - Local Government: Municipal Finance Management Act, No. 56 of 2003; MSA - Local Government: Municipal Systems Act, No. 32 of 2000, as amended; MTBPS - National Treasury annual publication, Medium Term Budget and Policy Statement; NT - National Treasury; PT - Provincial Treasuries; SDBIP - Service Delivery and Budget Implementation Plan 53

55 Review of previous budget process budget evaluation checklist While the MFMA does not explicitly require a review of the previous budget process, it is strongly recommended that this is undertaken in July (and completed by 31 August) by the mayor and municipal manager before determining the new schedule of key deadlines. Such a review can provide information about what worked well, what didn t, where to improve and issues to address for legislative compliance A Budget Evaluation Checklist (BEC) template has been developed and will assist municipalities to evaluate the budget process. This is available on the National Treasury website for learners that may be interested ( ENTITIES and planning the budget process Municipalities with entities will have a slightly more complex budget preparation process as they must include plan for coordination of entity budget preparation processes. The entity budget processes must be shaped by, and be within the framework of, the municipality s budget process. This will be coordinated by the mayor. In particular, it will be necessary to ensure that the entities strategic plan and budget is consistent with the direction of the parent municipality s IDP and budget STEP 2: STRATEGISING This step involves the review of the Integrated Development Plan and budget related policies through internal and external consultations. Internal consultation means consultation with staff within the municipality. External consultation means consultation with the community and other stakeholders. This step commences early in the process and carries on until October. 54

56 Review of IDP and budget related policies The Municipal Systems Act (MSA) and chapter 4 of the MFMA require that a revised IDP be adopted at the time of adopting the budget. Therefore, the process leading to the adoption of the 2005/06 budget and IDP must be incorporated into the one process, together with the approval of taxes, levies, user charges and budget related policies. This will ensure credible plans and budgets that are realistic and implementable. Furthermore, the IDP should be informing the entire budget, not just the capital budget, which has been the case prior to the MFMA coming into effect Budget related policies include but are not limited to policies on: tariff setting; credit control / debt collection; indigents; cost recovery; investment; borrowing; cash management; spending delegations or authorisations; other supply chain considerations such as purchasing limits for sole supplier versus quote or tender; and so on. Some of these are required to be passed as a by-law and may require significant planning before changes can be made. ACTIVITY / READ: Read the provisions of the Municipal Budget and Reporting Regulations Preparing and amending budget-related policies Internal consultations within the municipality The Budget process is consultative and the collective product of many role players within a municipality. If treated as an accounting exercise only, the mayor and accounting officer will have failed in their obligations to the municipality and the community. The budget process must involve all the senior managers and, importantly, it must be guided by the strategic priorities of the municipality. 55

57 The budget process should be preceded by a number of strategic and consultation processes within the municipality, involving the mayoral/executive committee and councillors. These processes are not legislated and are left to the discretion of each municipality The internal strategic consultation should be undertaken during September/October, with the mayor convening a meeting of the mayoral or executive committee and senior managers. The purpose is to determine the priorities of the municipality for the coming budget, taking into account the financial and political pressures facing the municipality. It should also consider what revisions should be considered to its current IDP. This process need not involve any non-executive councillors at this stage The above process ideally would culminate in a major council strategic workshop around the beginning of October involving the entire council (or if the council is too large, at least the chairpersons of all council committees). The purpose of the workshop is to gain understanding of budgetary pressures and to win the support of councillors to the budget priorities proposed by the mayor. It should be noted that at this stage the mayor and mayoral/executive committee determine the budget priorities the council should not be asked to vote on such priorities and the mayor should strive to only win the broad support of the council. The actual priorities will be approved by the council when it approves the budget and revisions to the IDP at the end of the process The budget priorities are tentative at this stage and offer a basis for consulting with internal stakeholders. It may be necessary for the mayor to revise the priorities following the consultation process. Note that external consultation with the community and other stakeholders is discussed under its own heading further on. ENTITIES and strategising Consultation and setting of priorities in the IDP must take into account all 56

58 services provided by the municipality whether through municipal departments or external mechanisms such as municipal entities STEP 3: PREPARING The preparation of the budget is a lengthy process spanning many months. It can be said to start in August at the time the mayor tables the schedule of key deadlines and concludes when the mayor approves the Service Delivery and Budget Implementation Plan and annual performance agreements with senior managers In practice the budget preparation process is an ongoing function where processes and budget years will overlap. There are generally three different budget processes operating in parallel all the time - reporting on the past year (e.g. annual reports and audited financial statements), current year implementation, and preparations for the coming budget year. Refer to diagram 2b which shows how there are always three budget and reporting cycles in progress at any one time Budget preparation includes the following: assessment of previous year performance and corrective action to be incorporated in the next budget; prioritising activities to be included in the annual budget and MTREF winning support for the priorities that will shape the way budget allocations will be determined; integration of strategic objectives with budget allocations; 57

59 appropriate planning and improved project management; assessing affordability of rates and service charges, and identifying poor households unable to afford such rates and charges; accurate estimation of revenue and expenditure projections Projecting the cost of existing routine activities Developing costed proposals for new programmes and capital projects; consultation and review of national, provincial and local priorities; testing of funding compliance to ensure budget is funded according to the MFMA; and preparing budget documentation Previous performance Throughout the budget process, and specifically at key times, consideration should be given to the effect that previous performance will have on the medium term plan and the current and forthcoming budgets. This should include past year and current year information Whilst the technical preparation of the Budget is undertaken by the municipal manager, senior managers and chief financial officer, it is important that the mayor meet with the municipal manager and CFO on a monthly basis after the priorities are set, particularly during November, January, February and March. Such political oversight is necessary to guide officials and to assist in making the hard trade-offs necessary to determine the budget A key step in preparing the budget occurs at the end of January, when the mayor is required to table the annual report for the past year and the mid-year report on the current financial year. 58

60 For example, on 31 January 2009, the mayor will be tabling the 2007/08 annual report, and will be submitting the mid-year report on the 2008/09 budget. This mid-year report will also inform the mayor and municipal manager on adjustments that need to be made to the 2008/09 current year budget. It is recommended that a municipal adjustment budget be tabled at the end of February 2009 which takes into account adjustments to be addressed in the current budget, such as under-collection of revenue, to address emergencies and adjustments in national and provincial allocations. All the above considerations must be used to determine the coming budget for the 2009/10 budget year STEP 4: TABLING The MFMA stipulates that the budget and revised Integrated Development Plan must be tabled together 90 days before the start of the budget year, together with the draft resolutions and budget related policies This step may commence as early as January and must be completed no later than 31 March Diagram 3d below illustrates the sequence of events to table the proposed budget and amendments to the IDP. Diagram 3d: Budget tabling and approval timeline Tabling of annual budgets To ensure facilitation of consultation the budget tabled for consultation (at least 90 days before the start of the budget year) must be in exactly the same format as the budget that is approved. Furthermore, the budget tabled for consultation 59

61 must also be realistic and capable of being implemented as tabled. That is, the budget must be funded according to section 18 of the MFMA such that all resources are available to implement the budget. Tabling a budget which could not be implemented is not useful as a consultation device. The next heading briefly considers funding the budget Note that the MFMA does not talk about submitting a draft budget to council. It rather talks about tabling the budget to council. The word draft has deliberately been omitted because it has connotations of something incomplete. The budget tabled for consultation must in fact be capable of implementation to ensure useful consultation can take place Further to the points above, the proposed resolutions which accompany the tabled budget must be the resolutions that would be required to approve the tabled budget. Referring to the previous paragraphs, the tabled budget is capable of being implemented and therefore the proposed resolutions would give effect to the budget if they were in fact resolved by council. Council will note these proposed resolutions but cannot pass them until consultation has been completed The draft service delivery and budget implementation plan is the operational plan that would need to be carried out if the tabled budget was approved as tabled. The formulation of this plan is necessary to arrive at a realistic budget for tabling. Its existence proves that the tabled budget could be implemented as tabled. The portfolio committee responsible for the budget may decide whether this detailed plan should be tabled to council alongside the budget Once the budget is tabled the local community must be invited to make written submissions to the council on the budget and to make representation at the council hearings. Key stakeholders like national and provincial departments (e.g. treasuries, local government, water, environment, health) should also be invited to submit written comments to the hearings. 60

62 The council may also wish to host special sessions with community organisations, business organisations and public sector institutions prior to convening the hearings on the budget The council is required to have hearings on the budget before it considers the budget for adoption. Such hearings can take the form of various committee hearings and should be convened soon after tabling the budget. The hearings may need to extend over a number of weeks, after which a full council meeting should be convened to consider and make recommendations arising out of the hearings process. The council must consider all the submissions and representations received during its hearings process. The mayor must be given an opportunity to respond to the recommendations (at that or a subsequent council meeting), and where necessary, to make revisions and amend the tabled budget Funding the budget A budget must be credible and funded according to section 18 of the MFMA. All projected revenue and expenditure must be realistically achievable and backed by documented evidence The Municipal Budget and Reporting regulations set out the requirements for funding the budget including the determination of realistic revenue and expenditure projections, and the funding of reserves The intent is that funding can only be included in the budget when it is properly documented and the funding is certain to eventuate. Budgets that make unrealistic service delivery promises by inclusion of unrealistic funding sources are not useful planning devices and only serve to falsely raise the expectations of the community Likewise, estimates of expenditure need to be based on past performance and realistic future assumptions. 61