TECUMSEH LOCAL SCHOOL DISTRICT

|

|

|

- Barry Morgan

- 5 years ago

- Views:

Transcription

1 TECUMSEH LOCAL SCHOOL DISTRICT ACTIVITIES HANDBOOK Student Activity Accounts Principal Fund Accounts Athletic Accounts Tecumseh Local School District 9760 West National Road, New Carlisle, Ohio

2 [This page intentionally left blank.] 2

3 TABLE OF CONTENTS INTRODUCTION BUILDING ACTIVITY FUNDS Purpose Fund Types STUDENT ACTIVITY/ATHLETIC FUNDS Purpose Fund Types FUND ADMINISTRATION STATE REGULATIONS BOARD POLICY REFERENCES ADMINISTRATIVE GUIDELINE REFERENCES Forms GENERAL RULES ANNUAL REQUIREMENTS How do we get started? Why do we have so many procedures?.11 How do we know if an activity is required to complete the various forms?.11 How is a new activity started? Budget Proposal Parts 1 and Purpose Budget Signatures Due Dates Revenue Documentation & Reporting Activity Deposit Slip Prenumbered Cash Receipts and Transmittal of Recipt Types of Revenue Admissions Dues/Fees Sales Donations Purchasing/Expenditure Requirements Fundraising Sales Project Activity Application Proof of Cash Financial Reports... 16

4 TABLE OF CONTENTS THE DO S OF FUNDRAISING THE DON TS OF FUNDRAISING CHECKLIST FOR ACTIVITIES SAMPLE FORMS SECTION BUDGET PROPOSAL PART BUDGET PROPOSAL PART ACTIVITY DEPOSIT SLIP PRENUMBERED RECEIPTS TRANSMITTAL OF RECEIPTS FORM SALES PROJECT ACTIVITY APPLICATION PROOF OF CASH INVENTORY RECORD FORM REPORT OF TICKET SALES SPONSOR AGREEMENT FORM... 30

5 INTRODUCTION If you are reading this handbook, you are probably an activity advisor, coach, or involved some other way with programs outside of the students classroom work. Thank you for making this extra effort! Your focus is on the students. We want to make the financial and reporting requirements as easy as possible. Direct communications are always the best way to answer questions. For those times when you prefer written explanations or instructions, we hope this handbook will meet your needs. BUILDING ACTIVITY FUNDS Purpose Funds generated at the building level that are used to support and enhance the students' educational activities and support the financial activities of the building staff. The uses of these funds are limited by the Uniform School Accounting System (USAS) and by Board Policy. This allows for the proper monitoring and use of all funds raised. Fund Type Principal Funds ( thru 9052) - Principal Funds are those funds generated at the building level which are used to enhance the student's educational experience or account for student activity support. Revenue is typically generated through fundraisers and donations. STUDENT ACTIVITY/ATHLETIC FUNDS Purpose A program of co-curricular activities established by the Board of Education should ensure that students have an opportunity to take part in co-curricular and extra-classroom experiences; should provide efficient procedures for their creation, operation, and termination; and should outline a system for the safeguarding, accounting, and internal control of extra-classroom activity funds. The raising and expending of activity money by these student groups should have the main purposes of promoting the general welfare, education, and morale of all the students; financing the normal, legitimate co-curricular activities of the student body organization; and promoting community involvement that will help students become aware of the needs of others. Fund Types 1. Activity Funds (USAS 200-9XXX) - Activity funds where the students are involved in the management of the funds (i.e., Student Council, FFA, etc.). 2. Athletic Funds (USAS 300-9XXX) - Activity funds where the students are not involved in the management of the funds (i.e., fund for a specific sport). 5

6 FUND ADMINISTRATION Superintendent The Superintendent is responsible for administering all board policies, except those required of the Treasurer. Principal/Athletic Director The principal, athletic director, or authorized administrator shall be responsible for the approval of the Budget Proposals Part 1 and 2, Sponsor Agreement Form, Sales Project Activity Application, Proof of Cash, Inventory Record, approval of requisitions, and any other duties as assigned by the Superintendent of the school district. Advisors/Head Coaches/Sponsors The duties and responsibilities of the advisor/head coach/sponsor shall be at the discretion of the Board of Education and should consist of the following: 1. Completing the Budget Proposal Parts 1 and 2, appointing a sponsor, completing a Sponsor Agreement form, and getting those approved; 2. Supervising the activities of the activity group, including preparation of sales project activity application prior to the activity, proofs of cash, requisitions, other appropriate documentation; 3. Maintaining account records in an up-to-date manner; 4. Performing any other duties as assigned by the proper administrative authority. Treasurer In every school district, the Treasurer of the Board of Education shall be the Treasurer of the school funds. Although it is the sole responsibility of the Board to establish such policies, they may appoint a designee to execute such policies. 6

7 STATE REGULATIONS Section , Revised Code, permits a Board of Education to expend funds for student activity programs. This section states: A. The Board of Education of any school district may expend moneys from its general revenue fund for the operation of such student activity programs as may be approved by the State Board of Education and included in the program of each school district as authorized by its Board of Education. Such expenditure shall not exceed five-tenths of one percent of the board s annual operating budget. B. The State Board of Education shall develop, and review biannually, a list of approved student activity programs. C. If more than fifty dollars a year is received through a student activity program, the moneys from such a program shall be paid into an activity fund established by the Board of Education of the school district. The board shall adopt regulations governing the establishment and maintenance of such fund, including a system of accounting to separate and verify such transaction and to show the source from which the fund revenue is received, the amount collected from each source, and the amount expended for each purpose. Expenditures from the fund shall be subject to the approval of the board. The Auditor of State has adopted and required within each school district the use of a uniform system of cost accounting, prescribed in Chapter 177-2, Ohio Administrative Code, whereby the direct and indirect costs of all school district activities, including athletic and non-instructional activities, regardless of the sources of funding, can be analyzed. This system, known as the Uniform School Accounting System (USAS), can be found in Chapter 117 of the Ohio Administrative Code. 7

8 BOARD POLICY REFERENCES The Tecumseh Board of Education has adopted a comprehensive set of policies to govern all aspects of the school district. Listed below are some Board Policies that reference the administration of the types of funds and activities covered by this handbook. Board Policy changes from time to time. Additional policies may be added to govern these types of funds and activities. For the most current policy, please use the link on the district's webpage or go to Advisors, coaches, sponsors, and administrators are to be aware of and follow all Board Policies. Policy Number Title 2430 District Sponsored Clubs and Activities 3214 Staff Gifts 5722 School Sponsored Publications and Productions 5830 Student Fund-Raising 5840 Student Groups 5850 School Social Events 6600 Deposit of Public Funds and Cash Collection Points 6605 Crowdfunding 6610 Student Activity Funds 7230 Gifts, Grants, and Bequests 7540 Technology Web Content, Services, and Apps 7543 Utilization of the Districts Website/Remote Access to the District's Network 8550 Competitive Food Sales 8900 Anti-Fraud Advertising and Commercial Activities 8

9 ADMINISTRATIVE GUIDELINES REFERENCES In conjunction with the Board Polices, the District Administration has adopted Administrative Guidelines to further clarify the administration of these types of funds and activities. Listed below are some Administrative Guidelines that reference the administration of the types of funds and activities covered by this handbook. Administrative guidelines change from time to time. Additional guidelines may be added to govern these types of funds. For the most current guidelines, please use the link on the district's webpage or go to Advisors, coaches, and administrators are to be aware of and follow all Administrative Guidelines. Guideline Number Title 2430 District Sponsored Clubs and Activities 5722 School Sponsored Student Publications and Productions 5830 Student Fundraising 6320 Purchasing 6605 Crowdfunding 6610 Student Activity Funds 6611 Ticket Sales Web-Page Specifications 8550 Competitive Food Sales 9700B Criteria for Commercial Messages Forms General forms are adopted and presented on the Neola website. However, for the purposes of the student activities referenced in this book, please use the specific forms referenced in this handbook and/or on the district s website. 9

10 GENERAL RULES 1. The Board of Education must authorize, by resolution recorded in the official meeting minutes, those student activity programs it wishes to be operational, by the adoption of a Budget Proposal Parts 1 and Budget Proposal Parts 1 and 2 must be adopted and modified by the Board of Education on a fiscal year basis. 3. All expenditures from these accounts will be made by check and only after the proper procedures have been followed. No purchases can be made until a purchase order has been approved. The approved purchase order and other documentation must be received and properly authorized for payments to be issued. 4. All monies received by school district personnel for a school-sponsored activity must be deposited into a school district account or with the Treasurer of the Board of Education within a 24-hour period following the collection, if practicable, or on the first business day following the event. 5. All cash donations of $500 or more to the activity funds and donations of non-cash items with a value exceeding $500 should be accepted by the Board of Education. The donation, whether cash or non-cash, should be communicated to the Treasurer to be taken before the Board of Education. 6. All forms required by the Auditor of State and adopted by the Board of Education shall be completed and copies retained by the activity sponsor. 7. Student activity funds should not be used for any purpose that represents an accommodation, loan, or credit to Board of Education employees or other persons. Postdated checks should not be accepted, and checks should not be cashed for anyone. Board of Education employees or others should not take advantage of purchasing privileges. 8. All expenditures should be in accordance with the approved budget of the group. The authorization for the expenditures will be an approved purchase order. Installment and lease purchases are prohibited. 9. All expenditures shall be deemed in accordance with "public purpose" if included on an approved school district activity Budget Proposal Parts 1 and 2, are within the scope of State law and legal opinions, and a reasonable expense based on the fund activity. 10. Investment procedures and the allocation of interest earnings shall be handled in accordance with Ohio law and Board of Education policy. 11. A system of internal controls shall be implemented in order to safeguard the assets of the funds to ensure that the benefits sought will be attained. 10

11 ANNUAL REQUIREMENTS How do we get started? Before June 1 in preparation for the following school year, the Principals and Athletic Director should meet with the sponsors of any clubs that fall under their responsibility. A Budget Proposal Parts 1 and 2, and a sponsor agreement should be completed and submitted to the Treasurer s office. The Treasurer will review the Budget and sponsor agreement and return to the appropriate supervisor if any corrections are needed. After the forms have been properly filled out, the Treasurer will present them to the Board of Education for approval. A blank sponsor agreement form can be found on page 30. Why do we have so many procedures? Everybody agrees that completing the paperwork is not the best part of an activity. So why do we have all the paperwork? The simple answer is protection. Although the natural thought is that the only thing being protected is the money, it is really much more than that. Following proper procedures helps to keep all people involved in an activity protected from questions and accusations. The minimum standards are set by Ohio Revised Code, Board Policy, Administrative Guidelines, and procedures developed in handbooks such as this one. Following proper procedures and providing documentation can help protect individuals and the district from damaging headlines. On the positive side, the paperwork can be used as a learning tool for students. Although the advisor or coach is responsible for submitting the forms, students can help compile the information to complete the paperwork. How do we know if an activity is required to complete the various forms? The simple answer is that if an activity plans to do anything in the upcoming year, they should submit paperwork. The amount of paperwork required depends on the amount of activities planned. As described below, the Budget Proposal Parts 1 and 2 gives an overall purpose of the activity. Even if there are no plans to raise or spend money, the purpose portion of the statement gives the Board of Education an opportunity to become aware of the reasons the various groups exist. How is a new activity started? Any activity with financial transactions must be covered under a new or existing activity group. Most activity groups or teams are on-going. The advisors or coaches may change, but the activities continue to exist. If you would plan to start something new, the first step is to discuss it with your building principal (or athletic director for a team). They need to know what is planned for their buildings. The next discussion should involve the Treasurer s Office to determine if this can be included with an existing group or if a new activity group should be created. Board Policies 5840 and 6610 and Administrative Guidelines 2430 and 6610 give the specifics on creating a new activity. 11

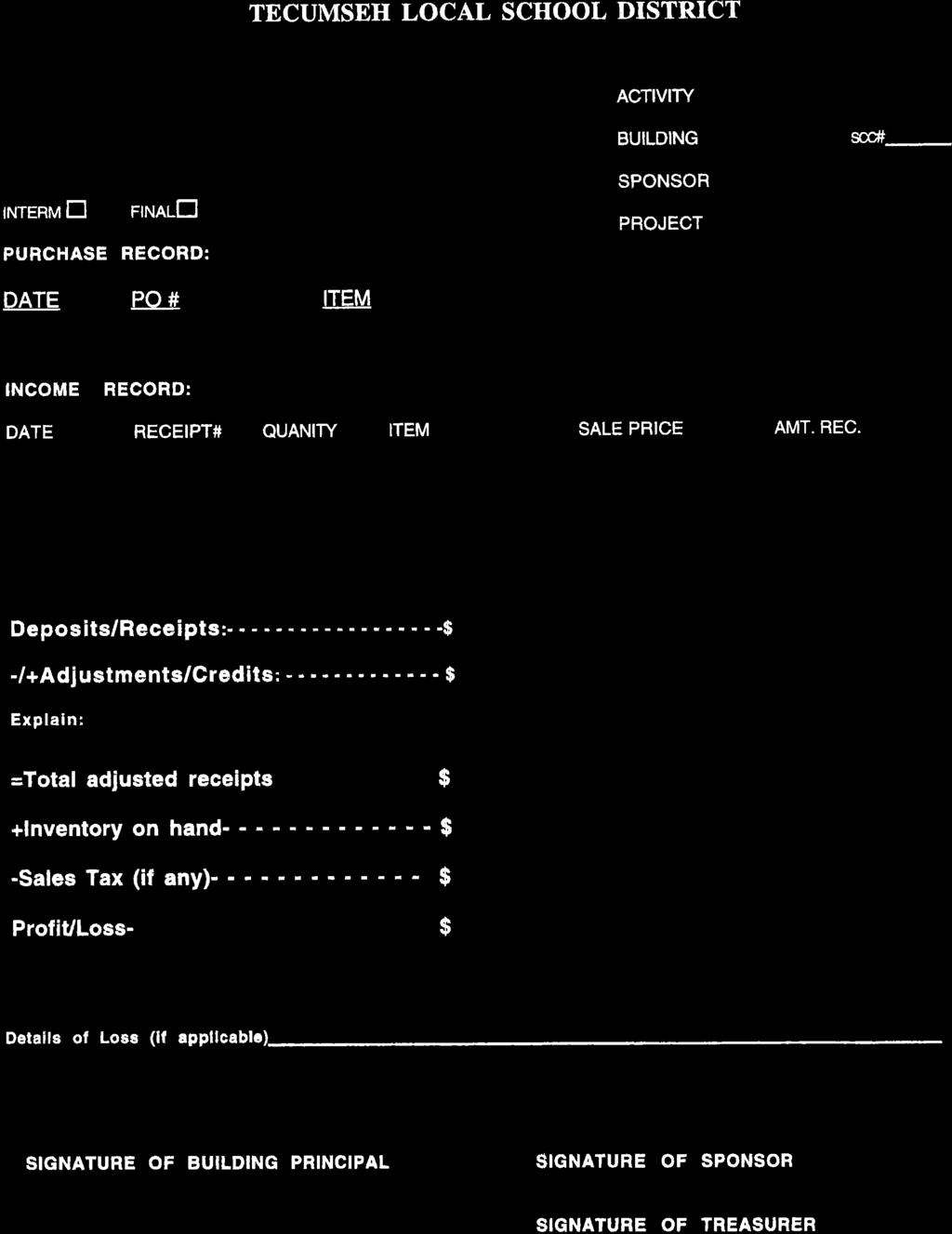

12 Budget Proposal Parts 1 and 2 The Budget Proposal Parts 1 and 2 is the first form you will complete. The first thing you need is your activity name. The activity name is the overall group or team that will be conducting the activities. For example, Junior High Student Council is an activity name. The individual events under the activity, such as a dance, will be covered by the other forms to be discussed later. The fund number is a seven-digit code that accounts for each activity. You can tell the type of activity by the first three digits (018 Principal Funds, 200 Student Activities, 300 Athletics). The fund number will be used in all of your reports. The number is assigned by the Treasurer s Office. Purpose The purpose part of the statement is very important. This statement explains why you are forming this group or why it is in existence. This not only lets the Board of Education know why the activity exists, but their approval tells the State Auditor s Office that the Board is in agreement with your activities. A sentence or two should be all you need. It can be as simple as to provide support to the football team with additional activities, supplies, and equipment for the limited purpose groups. A larger group such as Student Council will probably need to be a little more descriptive. An example is to provide support to students, staff, and the community through activities involving students. The support will include activities, incentives for students and staff, and charitable fundraisers, and scholarships. The idea is to be specific in how you plan to do things, but not too specific to limit the group to one small activity (eg. Contributions to a specific charity). Budget The budget portion of the form can be completed by filling in the blanks. Schools operate on a July 1 June 30 fiscal year. You can find your beginning balance by looking at the previous June 30 monthly report. If you are new to the activity or cannot find the report, please call the Treasurer s Office for your beginning balance. For new activities (such as the freshman class), list $0 as the beginning balance. Next, list the sources of revenue and estimates (i.e., name of fundraiser, types of donations, club dues, etc.). Please do not use terms that are too general, such as fundraiser or donations. Be as specific as possible. For example, list the type of fundraiser you are planning or where you will be asking for donations. Remember, this is a planning document. We all understand plans change. No one is going to hold you to the exact numbers. Revised budgets can be submitted throughout the year. After revenue, list the uses or how you will be spending your funds. Like revenue, you do not want to be too general. For example, rather than just listing supplies, you should list fundraising supplies, t-shirts, food, etc. Rather than a broad statement of donations, you could break it down into categories such as adopt a family project, charitable organization donation, and annual student scholarship. Miscellaneous expenditures should not exceed 1% of the total expenditures. Again, these are estimates and the actual amounts will vary. We recognize plans change and budgets can be adjusted later to reflect the change in plans. 12

13 Beginning balance plus sources (anticipated receipts) less uses (anticipated expenses) equals your projected ending (June 30) balance. The projected ending balance number must equal zero or above. Signatures All student activity (Fund 200) accounts are required to have student involvement in all aspects of running the account. If the Budget Proposal Parts 1 and 2 is for a student activity, please review the form with the students. Your signature as Activity Advisor/Sponsor is your guarantee that you will adhere to Board Policies and Administrative Guidelines as it relates to these activity funds. As the advisor, head coach, or sponsor of the activity, you should also review the form carefully. Your signature is your guarantee that you will adhere to Board Policy and Administrative Guidelines as related to these activities. The Budget Proposal Parts 1 and 2 should then be forwarded to the proper administrator (Building Principal, Assistant Principal, or Athletic Director) for his or her signature. That signature is an assurance that the Administrator has reviewed and supports the planned activities. The Budget Proposal Parts 1 and 2 should be forwarded to the Treasurer s office for review, approval, and then presentation to the Board for approval (performed by the Treasurer). Due Dates The first Budget Proposal Parts 1 and 2 for the school year is due by May 31 st of the preceding school year (i.e., in school year 17-18, by May 31 st for the school year proposal). The May 31 st due date will allow time for the statements to be submitted to the Board of Education for approval at the regularly scheduled June meeting. If there is a need for a modified budget later in the year, it can be submitted anytime. Sample Budget Proposal Parts 1 and 2 can be found on pages 21 & 22 of the handbook. Revenue Documentation & Reporting According to the State Auditor's office, all revenues should be able to be documented in some fashion. All records should be maintained per the Board of Education s approved retention schedule. All revenue must be deposited with the Treasurer's Office or into a school depository within the Board adopted timelines for such activity. The Administrative Guideline 6610 states that all monies collected are to be deposited within 24 hours or on the next business day. All deposits must include an Activity Deposit Slip and the information contained on the Student Receipts Summary form. You may substitute another form, as long as it contains the same information. Activity Deposit Slip The Activity Deposit Slip provides the documentation to show how much was collected and when/where the funds were deposited. Your schools head administrative assistant will fill this out with information provided by the sponsor. A sample Activity Deposit Slip can be found on page

14 Prenumbered Cash Receipts and Transmittal of Receipt Prenumbered Cash Receipts and the Transmittal of Receipt provides the documentation of how much was turned in by each student and what the money was for. Prenumbered Cash Receipts normally come in receipt books and are in triplicate (white, yellow, and pink copies). The white copy of the receipt goes to the student, teacher, advisor, parent, etc. who is paying the money to the individual receiving it (coach, principal, secretary, sponsor, etc.). The yellow copy goes with the Transmittal of Receipt (which is forwarded to the Treasurer s office). And finally, the pink copy stays with the receipt book. The date, dollars $ amount, how paid, and by should be completed for every receipt, every time. The address and account information should only be used if necessary for keeping accurate records. A sample Prenumbered Cash Receipts can be found on page 24. The Transmittal of Receipts is normally completed by the building secretary and should be detailed enough to provide a proof of cash (ie.10 shirts sold at $10 per shirt for a deposit of $100). The building secretary will be able to provide the account codes as long as the advisor/sponsor tells them what student activity the money has been collected for. A sample Transmittal of Receipt can be found on page 25. These two forms (Prenumbered Cash Receipts and Transmittal of Receipt), which should be submitted with the deposit, are important for your protection and to maintain the integrity of the event/fundraiser in case of allegations of mishandling of funds. With the exception of dues, Sales Project Activity Application and Proof of Cash must be completed for all types of activities collecting money. These forms will be explained later in the handbook. Types of Revenue Admissions All revenue from any type of admission must be documented. For admission events using tickets, use a Student Activity Report of Ticket Sales form.. The form will utilize beginning and ending ticket numbers to calculate the potential revenue. The form will be used for presale of numbered tickets and numbered tickets sold at the door (if applicable). Please review the Student Activity Report of Ticket Sales form on page 29. Dues/Fees Membership lists should be maintained. The list should include the name, the amount of dues and/or fees paid and when they were paid. Reasons and records of other fees should also be maintained. Sales Sales of goods require an inventory of items to be maintained to document items ordered, returned, and revenue collections by individuals. At the end of the sale a Student Activity Inventory Record should be turned into the Treasurer s office. The inventory record should list any inventory still held for resale and any credits, returns, lost items, etc. A sample Inventory Record can be found on page

15 Concession stand sales will be the hardest to document. Efforts should be made to document the possible income. Beginning and ending inventories of goods and supplies will help in your efforts. Please consult with the Treasurer s office for proper record keeping. Donations If an activity is planning to solicit donations, the solicitation should be handled like a fundraiser with all the necessary reports. If the activity receives a one-time donation from an individual, the fundraiser reports are not required. All cash donations over $500 should be accepted by the Board of Education. All non-cash donations valued at $500 or more should also be accepted by the Board of Education. Purchasing/Expenditure Requirements All expenditures must be made by the school district. Purchases cannot be made with funds (cash) that have been collected. No purchase can be made without having an approved purchase order. Please remember that a requisition is NOT an approved purchase order. The following are guidelines to the process. Prior to the signing of a contract or entering into any verbal agreement for supplies or services, the Activity Advisor/Head Coach/Sponsor must have an approved purchase order. An approved purchase order is required before making a purchase even if you are the one making purchases and requesting reimbursements. The individual wanting to make a purchase should go to the building secretary who will submit a requisition (requisition will have the vendor, items to be purchased, price, etc.) Once the requisition has been submitted, the system will forward it to the proper Administrator for first level approval. Like all requisitions, it will require the approval of the Superintendent and Treasurer before it is converted to a purchase order. The building secretary will receive an with the purchase order once it has been created. Fundraising An essential financial part of all activity accounts is the necessity to raise funds for the group s activities. All fundraising activities must be coordinated and approved by the Principal (or Athletic Director) and the Superintendent at least two (2) weeks prior to the sale or event (Administrative Guidelines 6610). The approval of the fundraising activity is requested through the Sales Project Activity Application form, which is explained below. As with all revenue and expenditures of the school, this activity must be included in the budget. Requisitions may be completed after the Sales Project Activity Application form has been approved. All approved purchase orders must be received by the Activity Advisor/Head Coach/Sponsor prior to the start of the sale if expenditures are required as part of the project. At the completion of the fundraising activity, a Proof of Cash must be completed. 15

16 Sales Project Activity Application Sales Project Activity Application describes what you will be doing to collect money. It is also used to estimate revenue, expenses, and profit. Everybody understands it is an estimate and estimates are rarely 100% accurate. An estimate is simply your best guess with all of the information available to you when you complete the form. The important part is to give the best descriptions and expectations for the project. A blank Sales Project Activity Application can be found on page 26. Proof of Cash The Proof of Cash summarizes the details of the fundraising project. This report is completed after the project is final, so it is not an estimate. You can contact the Treasurer s Office for assistance. A blank Proof of Cash can be found on page 27. Financial Reports The building secretaries have access to financial reports through our computer consortium (MVECA). Also, if you are in need of a specific report or information, the building secretary can be contacted and if he/she cannot provide the answer then please ask the Treasurer s office for assistatnce. 16

17 THE DO S OF FUNDRAISING DO check to be sure the fundraiser fits the District s fundraising guidelines. DO check with the Treasurer s office if you have any questions prior to planning an event. DO check and closely follow any Board Policies regarding contracts and expenditures of funds for the procuring of goods and services. DO review contracts a) Check quantities ordered carefully b) Check process; be sure they are the same as quoted c) Be sure all verbal commitments are in the written contracts d) Provide for the return of unsold merchandise in the contract DO check the delivery against the packing slip and account for all items. DO require strict accounting for all goods and funds for all projects: a) Require for students and other sellers to sign for the materials they take b) Issue receipts for all goods or money received from students or other sellers DO make safety of participants a major concern: a) Provide for actual physical supervision of activity fundraisers (i.e. car washes) b) Establish safety precautions to prevent injury to students and property during the event c) Require a check for instruction of the involved students in the safety precautions pertinent to the undertaken activity and to the use of any equipment to be used for the project d) Provide for a safety check of any equipment to be used for the project e) Monitor events and institute further safety and/or disciplinary precautions as experience suggests DO deposit funds collected per Board Policy DO use your Student Code of Conduct and normal school discipline to collect money or goods owed by students. 17

18 THE DON TS OF FUNDRAISING DON T allow an activity to be school sponsored unless you, as the Advisor, can control all aspects of the event/sale. DON T collect money for an event/activity being run by a parent organization (i. e. PTA, booster groups) during work hours or when the perception might be that you are collecting on behalf of Tecumseh Local School District. Every effort should be made to make it clear that it is an event/activity of this outside organization. DON T hold on to funds collected they must be deposited within 24 hours or next available business day. DON T order items without a purchase order in place. DON T use cash on hand collected from the fundraising event to pay for other expenses of the event. All money collected MUST be deposited. Purchase orders need to be in place to cover expenses. DON T cash checks for anyone We are not a bank. DON T sign for goods that may make you personally liable for payment under the terms of a contract. DON T allow students to take more product than they can reasonably sell quickly. DON T allow the acceptance of special gifts or special bonuses for undertaking the fundraiser or for achieving certain quotas by yourself, your staff, or your students. DON T allow supervisors of physical activities to encourage students to perform beyond their level of training and experience. DON T KEEP CASH IN YOUR DESK OR CLASSROOM. DON T TAKE CASH HOME. 18

19 CHECKLIST FOR ACTIVITIES This checklist is provided to assist you in seeing that all required procedures are followed before, during, and after your event. I have read the Student. I have completed the Budget Proposal Parts 1 and 2 and a Sponsor Agreement Form which have been approved by the Superintendent and accepted by the Board of Education. I have allowed more than two (2) weeks in advance of the event to begin the planning process. Checked the school calendar for conflicts. Completed a Sales Project Activity Application Form for Student Activities. Attached copies of vendor contracts and/or other documents. Sales Project Activity Application Form has been approved prior to starting the event/project/fundraiser. If your event requires chaperones, staff and/or police supervision, check with your building principal to make arrangements. Prepare an information sheet for participants and encourage them to share this information with their parents. The information should include the following: Reason for fundraiser Monetary goals for the group and each participant Dates of sale Advisor s name Due date of any order forms along with how, where, and when to submit payments Delivery date of merchandise Participant s responsibility for money and merchandise Any prize information Copies of all fundraising materials/order forms have been provided to participants. Have a plan for advertising your event (i.e. newsletters, school website, posters, etc.) Assign someone to be responsible for payment collection and be sure they understand their responsibility for accounting for sales. If tickets are needed for your event, arrangements have been made to obtain, record, and use tickets. Set-up and take-down/clean up arrangements have been made. If vendors require payment at the event (i.e. DJ s, security), plan well ahead. Plans for concessions have been made. Plans for advance and at-the-door ticket sales have been made. Needed purchase orders have been approved. I HAVE READ THE GUIDELINES/PROCEDURES FOR MY TYPE OF EVENT/ACTIVITY. 19

20 SAMPLE FORMS SECTION 20

21

22

23 OOOOOOOOO OOOOOOOO OOO

24

25 NORTHEASTERN LOCAL BOARD OF EDUCATION Tecumseh Local School District 1414 Bowman Road 9760 West National Road Springfield, Ohio New Carlisle, Ohio TRANSMITTAL RECEIPTS CENTRAL OFFICE USE ONLY Date Receipt No. DATE:. BUILDING:. Activity:. SUBMITTED BY:. Cashier:. No. Description FUND RECEIPT SCC SUBJECT OPU AMOUNT $ TOTAL $ Description should include details of monies banked (i.e., Tee $15.00) to enable a "proof of cash" analysis to be made at completion Prepare deposit tickets in quadruplicate. They are to be deposited per Board Policy 6600 Deposit of Public Funds. Use this form for submitting receipts of fees, student activity sales, dues, donations, commissions, athletic events, etc. Manual receipt numbers should be written in the description area. Submit one copy to the Treasurer's Office at the time of the deposit and maintain one copy. You should tie out the Treasurer's receipt to your transmittal and your transmittals to your FISCWEB reports. Revised 12/2017

26

27

-------- 2) -------- 3) -------- 4) -------- 5) -------- 6) -------- 7) -------- 8) -------- 9)")

28 Tecumseh Local School Di Lric1 m eh.k 12.oh.us Wes! a1ional Road, New Carlisle, Ohio STUDENT ACTIVITY INVENTORY RECORD SALES PROJECT QUANTITY 1) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) SALE PRICE DATE ACTIVITY # BUILDING # SPONSOR PROJECT TOTAL $ $ TOTAL VALUE OF INVENTORY Items Returned to Company for Credit: (Attach credit record) ITEM 1) ) ) ) ) ) ) ) ) ) Is this project closed? QUANTITY Yes SALE PRICE TOTAL $ TOTAL VALUE OF CREDIT $ No If no, what are the plans? Submitted by

29

30

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY TABLE OF CONTENTS Section Page Number Guidelines 1-3 Annual Checklist 4 Forms and Instructions 5-9 Technical Assistance 10-12 (Non Authoritative/Best

COOPERATIVE ORGANIZATIONS THE SCHOOL DISTRICT OF LEE COUNTY TABLE OF CONTENTS Section Page Number Guidelines 1-3 Annual Checklist 4 Forms and Instructions 5-9 Technical Assistance 10-12 (Non Authoritative/Best

Student Activity Account Guidelines For Burlington Public Schools

Student Activity Account Guidelines For Burlington Public Schools * Information and text in this document was adapted for the Burlington Public Schools by the Finance Manager from the Student Activity

Student Activity Account Guidelines For Burlington Public Schools * Information and text in this document was adapted for the Burlington Public Schools by the Finance Manager from the Student Activity

FUND RAISERS. Procedures for Fundraising and Other Revenue Programs at the Local School

Procedures for Fundraising and Other Revenue Programs at the Local School Accounting Issues Related to Fundraisers, Cash Receipts, Go Fund Me, and Similar Programs AASBO LSFM CERTIFICATION PROGRAM SONJA

Procedures for Fundraising and Other Revenue Programs at the Local School Accounting Issues Related to Fundraisers, Cash Receipts, Go Fund Me, and Similar Programs AASBO LSFM CERTIFICATION PROGRAM SONJA

STUDENT ACTIVITY PROCEDURE MANUAL

SCHOOL DISTRICT OF RIVERVIEW GARDENS STUDENT ACTIVITY PROCEDURE MANUAL This manual is designed to provide a set of standardized accounting guidelines and procedures for the administration of the Riverview

SCHOOL DISTRICT OF RIVERVIEW GARDENS STUDENT ACTIVITY PROCEDURE MANUAL This manual is designed to provide a set of standardized accounting guidelines and procedures for the administration of the Riverview

JOHNSTON COUNTY PUBLIC SCHOOLS INTERNAL AUDIT DEPARTMENT PTA, PTO AND BOOSTER CLUB HANDBOOK

JOHNSTON COUNTY PUBLIC SCHOOLS INTERNAL AUDIT DEPARTMENT 2017-2018 PTA, PTO AND BOOSTER CLUB HANDBOOK Table of Contents Organization Guidelines 3 Financial Guidelines 3 Fundraiser Guidelines 4 Treasurer

JOHNSTON COUNTY PUBLIC SCHOOLS INTERNAL AUDIT DEPARTMENT 2017-2018 PTA, PTO AND BOOSTER CLUB HANDBOOK Table of Contents Organization Guidelines 3 Financial Guidelines 3 Fundraiser Guidelines 4 Treasurer

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL INTRODUCTION In view of the large amount of monies received from and expended for student/campus activities, the demand has developed for efficient,

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL INTRODUCTION In view of the large amount of monies received from and expended for student/campus activities, the demand has developed for efficient,

BEREA CITY SCHOOL DISTRICT

BEREA CITY SCHOOL DISTRICT STUDENT ACTIVITIES HANDBOOK Berea City School District 390 Fair Street Berea OH 44017 www.berea.k12.oh.us 216.898.8300 Page 0 Board Approved September 21, 2015 BEREA CITY SCHOOL

BEREA CITY SCHOOL DISTRICT STUDENT ACTIVITIES HANDBOOK Berea City School District 390 Fair Street Berea OH 44017 www.berea.k12.oh.us 216.898.8300 Page 0 Board Approved September 21, 2015 BEREA CITY SCHOOL

Booster and Support Organization Guidelines

Booster and Support Organization Guidelines July 2016 Parent Support Organizations provide an invaluable service to our schools. Many of our programs and activities could not exist without your volunteer

Booster and Support Organization Guidelines July 2016 Parent Support Organizations provide an invaluable service to our schools. Many of our programs and activities could not exist without your volunteer

Fundraising Procedures Manual

Fundraising Procedures Manual Fiscal Year 2016-2017 Dripping Springs Independent School District The Board of Trustees and administration of Dripping Springs Independent School District are charged with

Fundraising Procedures Manual Fiscal Year 2016-2017 Dripping Springs Independent School District The Board of Trustees and administration of Dripping Springs Independent School District are charged with

4/30/2015 FINANCIAL PROCEDURES FOR LOCAL SCHOOLS. Accounting for Extra-Curricular Activities. Student Organizations

Accounting for Extra-Curricular Activities Sonja Peaspanen Alabama Department of Education May 5, 2015 FINANCIAL PROCEDURES FOR LOCAL SCHOOLS APPROVED June 10, 2010 www.alsde.edu Department Offices LEA

Accounting for Extra-Curricular Activities Sonja Peaspanen Alabama Department of Education May 5, 2015 FINANCIAL PROCEDURES FOR LOCAL SCHOOLS APPROVED June 10, 2010 www.alsde.edu Department Offices LEA

3/11/2016. Student Activity Funds. Basic Facts about Student Activity Funds

Student Activity Funds Presented by: Natalie Rew, CPA Basic Facts about Student Activity Funds WI Stats, s. 120.16(2) authorizes a school district treasurer to receive money raised in extra-curricular

Student Activity Funds Presented by: Natalie Rew, CPA Basic Facts about Student Activity Funds WI Stats, s. 120.16(2) authorizes a school district treasurer to receive money raised in extra-curricular

Lewisville Independent School District BOOSTER CLUB GUIDELINES. Debate

Lewisville Independent School District BOOSTER CLUB GUIDELINES Debate Booster Clubs A school district approved club formed by parents and other interested non-student adults to work for the best interest

Lewisville Independent School District BOOSTER CLUB GUIDELINES Debate Booster Clubs A school district approved club formed by parents and other interested non-student adults to work for the best interest

Brownfield ISD Business Office Procedures Manual

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

CIRCLEVILLE CITY SCHOOL DISTRICT STUDENT ACTIVITY HANDBOOK

CIRCLEVILLE CITY SCHOOL DISTRICT STUDENT ACTIVITY HANDBOOK Approved May 18, 2011 TABLE OF CONTENTS DISTRICT PHILOSOPHY..4 STATE LAWS AS GOVERNED BY AUDITOR OF STATE.5 AUTHORITY. 5 PRINCIPLES..6 FUND 200

CIRCLEVILLE CITY SCHOOL DISTRICT STUDENT ACTIVITY HANDBOOK Approved May 18, 2011 TABLE OF CONTENTS DISTRICT PHILOSOPHY..4 STATE LAWS AS GOVERNED BY AUDITOR OF STATE.5 AUTHORITY. 5 PRINCIPLES..6 FUND 200

THE SCHOOL DISTRICT OF GREENVILLE COUNTY

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

Communication and Public Information

School Fund Raising Guidelines Introduction Student Activity accounts are those funds which are owned, operated, and managed by organizations, clubs, or groups within the student body under the guidance

School Fund Raising Guidelines Introduction Student Activity accounts are those funds which are owned, operated, and managed by organizations, clubs, or groups within the student body under the guidance

Fiscal Accounting & Reporting. Crook County School District #1. Activity Funds. Procedures Manual

Fiscal Accounting & Reporting DI-R Crook County School District #1 Activity Funds Procedures Manual CROOK COUNTY SCHOOL DISTRICT #1 ACTIVITY FUNDS PROCEDURES MANUAL This procedures manual is designed to

Fiscal Accounting & Reporting DI-R Crook County School District #1 Activity Funds Procedures Manual CROOK COUNTY SCHOOL DISTRICT #1 ACTIVITY FUNDS PROCEDURES MANUAL This procedures manual is designed to

ONTARIO LOCAL SCHOOL DISTRICT

ONTARIO LOCAL SCHOOL DISTRICT Fund Raising Packet Summary Page Page 1 Fund Raising Request Form Page 2 Fund Raising Procedures Page 3 Board Policy File IGDF R Page 4 Profit and Loss Statement Page 5 Collections

ONTARIO LOCAL SCHOOL DISTRICT Fund Raising Packet Summary Page Page 1 Fund Raising Request Form Page 2 Fund Raising Procedures Page 3 Board Policy File IGDF R Page 4 Profit and Loss Statement Page 5 Collections

SECTION 1 GENERAL INFORMATION

BRONTE ISD ACTIVITY FUND MANUAL SECTION 1 GENERAL INFORMATION 1.1 PURPOSE OF ACTIVITY FUNDS The Activity fund is designed to account for funds held by a school in a trustee capacity or as an agent for

BRONTE ISD ACTIVITY FUND MANUAL SECTION 1 GENERAL INFORMATION 1.1 PURPOSE OF ACTIVITY FUNDS The Activity fund is designed to account for funds held by a school in a trustee capacity or as an agent for

Accounting and Purchasing Manual. A manual provided for schools to guide them in appropriate cash handling and procurement procedures

Accounting and Purchasing Manual A manual provided for schools to guide them in appropriate cash handling and procurement procedures June, 2009 **IMPORTANT REMINDERS** Applies to all cash received at schools

Accounting and Purchasing Manual A manual provided for schools to guide them in appropriate cash handling and procurement procedures June, 2009 **IMPORTANT REMINDERS** Applies to all cash received at schools

CASH HANDLING PROCEDURES FOR ACTIVITY FUND CUSTODIANS

Mika Barton, Treasurer Ext. 1646 CASH HANDLING PROCEDURES FOR ACTIVITY FUND CUSTODIANS Absolutely NO Petty Cash permitted at any time. RECEIPTING Before allowing teachers/sponsors to collect money from

Mika Barton, Treasurer Ext. 1646 CASH HANDLING PROCEDURES FOR ACTIVITY FUND CUSTODIANS Absolutely NO Petty Cash permitted at any time. RECEIPTING Before allowing teachers/sponsors to collect money from

SECTION 1. ACCOUNTING AND REPORTING PROCEDURES

SECTION 1. ACCOUNTING AND REPORTING PROCEDURES All schools shall use the SchoolFunds software. The school finance officer (treasurer) shall follow the procedures outlined in the SchoolFunds manual for

SECTION 1. ACCOUNTING AND REPORTING PROCEDURES All schools shall use the SchoolFunds software. The school finance officer (treasurer) shall follow the procedures outlined in the SchoolFunds manual for

FINANCIAL GUIDE FOR PARENT ORGANIZATIONS Westminster Public Schools

FINANCIAL GUIDE FOR PARENT ORGANIZATIONS Westminster Public Schools TABLE OF CONTENTS INTRODUCTION... 1 OPTION 1... 2 OPTION 2 AND 3... 2 GENERAL GUIDELINES FOR ALL PARENT ORGANIZATION GROUPS WITHIN DISTRICT...

FINANCIAL GUIDE FOR PARENT ORGANIZATIONS Westminster Public Schools TABLE OF CONTENTS INTRODUCTION... 1 OPTION 1... 2 OPTION 2 AND 3... 2 GENERAL GUIDELINES FOR ALL PARENT ORGANIZATION GROUPS WITHIN DISTRICT...

FUNDRAISING. The District s Board Policy No limits fundraising activities to the following:

ASB PROCEDURES MANUAL FUNDRAISING REVISED DATE 07/04 PURPOSES State law permits associated student bodies to conduct fundraising activities, including but not limited to, soliciting donations to raise

ASB PROCEDURES MANUAL FUNDRAISING REVISED DATE 07/04 PURPOSES State law permits associated student bodies to conduct fundraising activities, including but not limited to, soliciting donations to raise

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

Fleming County Schools

Fleming County s Fundraiser Packet 216-17 Where kids are first and learning never ends! Updated on 7/1/216 Fundraising proceeds must benefit the entire group of students involved, regardless of participation

Fleming County s Fundraiser Packet 216-17 Where kids are first and learning never ends! Updated on 7/1/216 Fundraising proceeds must benefit the entire group of students involved, regardless of participation

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

St. Tammany Parish School Board Booster Clubs and Support Organizations Policy The St. Tammany Parish Public School System recognizes that schools receive substantial assistance in providing co-curricular

STUDENT ACTIVITY FUND GUIDANCE

STUDENT ACTIVITY FUND GUIDANCE OVERVIEW Student activities require the participation of students. Student activity funds are monies generated by students participation, authorized to be spent by students,

STUDENT ACTIVITY FUND GUIDANCE OVERVIEW Student activities require the participation of students. Student activity funds are monies generated by students participation, authorized to be spent by students,

Board Approved 9/20/16 OUTSIDE SUPPORT ORGANIZATION MANUAL

OUTSIDE SUPPORT ORGANIZATION MANUAL 1 2 Board Approved 9/20/16 Outside Support Organizations The School District encourages citizens to form Outside Support Organizations (OSO). These organizations support

OUTSIDE SUPPORT ORGANIZATION MANUAL 1 2 Board Approved 9/20/16 Outside Support Organizations The School District encourages citizens to form Outside Support Organizations (OSO). These organizations support

INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITIES ACCOUNTS

1 INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITIES ACCOUNTS TABLE OF CONTENTS Introduction 4 Responsibilities of Advisors, Bookkeeper, and Principal 5 General Requirements for Accounting for Activities

1 INSTRUCTIONS FOR OPERATION OF STUDENT ACTIVITIES ACCOUNTS TABLE OF CONTENTS Introduction 4 Responsibilities of Advisors, Bookkeeper, and Principal 5 General Requirements for Accounting for Activities

ASB Fundraiser Packet

Packet # ASB Fundraiser Packet Fundraiser Name: Completion of this packet is a requirement specific to ASB fundraisers. Anytime money is collected or items are sold, it is considered a fundraiser. All

Packet # ASB Fundraiser Packet Fundraiser Name: Completion of this packet is a requirement specific to ASB fundraisers. Anytime money is collected or items are sold, it is considered a fundraiser. All

School Support Organizations & Groups. Rutherford County Schools Boardroom 6:30 PM, Monday, Aug. 20, 2018

School Support Organizations & Groups Rutherford County Schools Boardroom 6:30 PM, Monday, Aug. 20, 2018 SSG - School Support Group SSG can be either Booster Club or a PTO SSG semi-independent group that

School Support Organizations & Groups Rutherford County Schools Boardroom 6:30 PM, Monday, Aug. 20, 2018 SSG - School Support Group SSG can be either Booster Club or a PTO SSG semi-independent group that

Crook County School District School District #1970 Prineville, Oregon. Student Activity Accounting Procedures

Crook County School District School District #1970 Prineville, Oregon Student Activity Accounting Procedures January 9, 2009 Revised January 9, 2015 3 rd Revision August 10, 2017 Student Activity Accounting

Crook County School District School District #1970 Prineville, Oregon Student Activity Accounting Procedures January 9, 2009 Revised January 9, 2015 3 rd Revision August 10, 2017 Student Activity Accounting

General Cash Collections

General Cash Collections Presented by Internal Accounts Support Staff Accounting Services Top-performing urban school district in Florida 1 Overview of Process for Collecting and Depositing Money There

General Cash Collections Presented by Internal Accounts Support Staff Accounting Services Top-performing urban school district in Florida 1 Overview of Process for Collecting and Depositing Money There

District Business Office Staff YES NO N/A Comments

Internal Controls Checklist by Job Responsibility A No response to any of the following questions may indicate an internal control weakness. The district should perform a self-evaluation and investigate

Internal Controls Checklist by Job Responsibility A No response to any of the following questions may indicate an internal control weakness. The district should perform a self-evaluation and investigate

ASSOCIATED STUDENT BODY FUND (ASB)

") The modified accrual basis of accounting is to be used in measuring financial position and operating results unless the district had less than 1,000 full-time equivalent students the previous fiscal year

The modified accrual basis of accounting is to be used in measuring financial position and operating results unless the district had less than 1,000 full-time equivalent students the previous fiscal year

Booster Clubs Questions and Answers (in italics)

") Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

GRANITE SCHOOL DISTRICT. Fiscal Policy Manual DEVELOPED BY THE BUSINESS SERVICES DIVISION

GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 This manual

GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 GRANITE SCHOOL DISTRICT DEVELOPED BY THE BUSINESS SERVICES DIVISION Adopted September 3, 2013 This manual

CHAPTER IX SECTION IX-ASB ASSOCIATED STUDENT BODY FUND (ASB)

") CHAPTER IX SECTION IX-ASB ASSOCIATED STUDENT BODY FUND (ASB) Special Revenue Funds -- to account for the proceeds of specific revenue sources (other than expendable trust or for major capital projects)

CHAPTER IX SECTION IX-ASB ASSOCIATED STUDENT BODY FUND (ASB) Special Revenue Funds -- to account for the proceeds of specific revenue sources (other than expendable trust or for major capital projects)

Information for Sumner County School Support Organizations

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

REDBOOK FREQUENTLY ASKED QUESTIONS. Redbook Version: July 1, 2013

REDBOOK FREQUENTLY ASKED QUESTIONS Redbook Version: July 1, 2013 Common Terms and Definitions Pages 1-2 Receipts Pages 3-6 Expenditures Pages 7-11 External Support Groups/Organizations Pages 11-16 8/1/2015

REDBOOK FREQUENTLY ASKED QUESTIONS Redbook Version: July 1, 2013 Common Terms and Definitions Pages 1-2 Receipts Pages 3-6 Expenditures Pages 7-11 External Support Groups/Organizations Pages 11-16 8/1/2015

K-0481 KBE-R RELATIONS WITH PARENT ORGANIZATIONS

K-0481 KBE-R Parent/Citizen Group Guidelines RELATIONS WITH PARENT ORGANIZATIONS In order for a parent/citizen group to be approved by the school and the District, the following guidelines must be observed.

K-0481 KBE-R Parent/Citizen Group Guidelines RELATIONS WITH PARENT ORGANIZATIONS In order for a parent/citizen group to be approved by the school and the District, the following guidelines must be observed.

Extra-Classroom Activity Fund. Northern Adirondack Central School September 2014

Extra-Classroom Activity Fund Northern Adirondack Central School September 2014 GUIDELINES The State University of New York, State Education Department, The Safeguarding, Accounting, and Auditing of Extra-Classroom

Extra-Classroom Activity Fund Northern Adirondack Central School September 2014 GUIDELINES The State University of New York, State Education Department, The Safeguarding, Accounting, and Auditing of Extra-Classroom

Business Operating Procedures

Business Operating Procedures 2016-2017 Learning Today. Leading Tomorrow. Accounting Procedures The Business Manager is responsible for all accounting functions in the district. It is important that he/she

Business Operating Procedures 2016-2017 Learning Today. Leading Tomorrow. Accounting Procedures The Business Manager is responsible for all accounting functions in the district. It is important that he/she

District Activity Funds

The National Council on Educational Statistics requires that schools remit some traditional activity funds to district-level accounts called District Activity Funds so these funds may be included in funding

The National Council on Educational Statistics requires that schools remit some traditional activity funds to district-level accounts called District Activity Funds so these funds may be included in funding

KISD September

Many organizations offer valuable assistance to the District in fundraising, voluntary help, and substantial fan support for school activities. Although the intent of these organizations is to assist and

Many organizations offer valuable assistance to the District in fundraising, voluntary help, and substantial fan support for school activities. Although the intent of these organizations is to assist and

To establish NUAMES policy and procedure governing the initiation, authorization, and review of all expenditures of the school.

NUAMES Cash Disbursement Policy Approved: 23 October 2013 1. PURPOSE AND PHILOSOPHY To establish NUAMES policy and procedure governing the initiation, authorization, and review of all expenditures of the

NUAMES Cash Disbursement Policy Approved: 23 October 2013 1. PURPOSE AND PHILOSOPHY To establish NUAMES policy and procedure governing the initiation, authorization, and review of all expenditures of the

I n t r o d u c t i o n

I n t r o d u c t i o n Booster Clubs are organized to help promote, support, and improve the extra curricular activities of the schools in Wasatch County School District. Each administrator is responsible

I n t r o d u c t i o n Booster Clubs are organized to help promote, support, and improve the extra curricular activities of the schools in Wasatch County School District. Each administrator is responsible

Leon County Schools. School Internal Accounts Procedures Manual. Page 1 of 57

Leon County Schools School Internal Accounts Procedures Manual Page 1 of 57 TABLE OF CONTENTS CHAPTER 1 GENERAL OVERVIEW... 7 A. DEFINITION INTERNAL ACCOUNTS... 7 B. INTRODUCTION... 7 C. BASIC PRINCIPLES...

Leon County Schools School Internal Accounts Procedures Manual Page 1 of 57 TABLE OF CONTENTS CHAPTER 1 GENERAL OVERVIEW... 7 A. DEFINITION INTERNAL ACCOUNTS... 7 B. INTRODUCTION... 7 C. BASIC PRINCIPLES...

CHAPTER 14 STUDENT ACTIVITY ACCOUNTING

CHAPTER 14 STUDENT ACTIVITY ACCOUNTING Uniform Financial Accounting and Reporting Standards Chapter 14 Manual for Activity Fund Accounting (MAFA) Minnesota Department of Education Division of School Finance

CHAPTER 14 STUDENT ACTIVITY ACCOUNTING Uniform Financial Accounting and Reporting Standards Chapter 14 Manual for Activity Fund Accounting (MAFA) Minnesota Department of Education Division of School Finance

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

BOOSTER CLUB TRAINING. Department of Athletics Temple Independent School District

BOOSTER CLUB TRAINING Department of Athletics Temple Independent School District Booster Club Website www.wildcatstrong.com Hover over Wildcat HQ Select Booster Clubs Board Policy GE Local The Board is

BOOSTER CLUB TRAINING Department of Athletics Temple Independent School District Booster Club Website www.wildcatstrong.com Hover over Wildcat HQ Select Booster Clubs Board Policy GE Local The Board is

SCHOOL ACTIVITY FUND ACCOUNTING HANDBOOK

SCHOOL ACTIVITY FUND ACCOUNTING HANDBOOK TA BL E OF C ONT E NTS 2017-2018 General Information...4 Definition and Management of Student Groups...4 Responsibility of Activity Fund... 5 PRINCIPAL/DESIGNEES...5

SCHOOL ACTIVITY FUND ACCOUNTING HANDBOOK TA BL E OF C ONT E NTS 2017-2018 General Information...4 Definition and Management of Student Groups...4 Responsibility of Activity Fund... 5 PRINCIPAL/DESIGNEES...5

BOOSTER CLUB HANDBOOK

BOOSTER CLUB HANDBOOK Pikeville Junior High/High School 120 Championship Drive Pikeville, KY 41501 (606) 432-0185 Message From the School Dear Stakeholders, On behalf of the students, faculty, and administration

BOOSTER CLUB HANDBOOK Pikeville Junior High/High School 120 Championship Drive Pikeville, KY 41501 (606) 432-0185 Message From the School Dear Stakeholders, On behalf of the students, faculty, and administration

JACKSON COUNTY BOARD OF EDUCATION

JACKSON COUNTY BOARD OF EDUCATION Jackson County School System FINANCIAL GUIDELINES FOR SCHOOL ACTIVITY FUNDS AND SCHOOL SYSTEM ACCOUNTS Updated: October 2004 2 JACKSON COUNTY BOARD OF EDUCATION FINANCIAL

JACKSON COUNTY BOARD OF EDUCATION Jackson County School System FINANCIAL GUIDELINES FOR SCHOOL ACTIVITY FUNDS AND SCHOOL SYSTEM ACCOUNTS Updated: October 2004 2 JACKSON COUNTY BOARD OF EDUCATION FINANCIAL

BRYANT SCHOOL DISTRICT. GUIDELINES for AFFILIATED SUPPORT ORGANIZATIONS

BRYANT SCHOOL DISTRICT GUIDELINES for AFFILIATED SUPPORT ORGANIZATIONS Adopted by School Board March 1, 2010 Booster Clubs and Support Organizations Policy The Bryant Public School District recognizes

BRYANT SCHOOL DISTRICT GUIDELINES for AFFILIATED SUPPORT ORGANIZATIONS Adopted by School Board March 1, 2010 Booster Clubs and Support Organizations Policy The Bryant Public School District recognizes

The purpose of this session is to give the user a high-level overview of the process flow for managing an Activity Fund Account.

The purpose of this session is to give the user a high-level overview of the process flow for managing an Activity Fund Account. The user is responsible to read the GPISD Business Operations Manual to

The purpose of this session is to give the user a high-level overview of the process flow for managing an Activity Fund Account. The user is responsible to read the GPISD Business Operations Manual to

SECTION 5: FINANCIAL INFORMATION

SECTION 5: FINANCIAL INFORMATION ACCOUNT INFORMATION Several different accounts are used in conjunction with programming in your hall. They are: The Hall Program Account The SFO Account AD, RHD and CStaff

SECTION 5: FINANCIAL INFORMATION ACCOUNT INFORMATION Several different accounts are used in conjunction with programming in your hall. They are: The Hall Program Account The SFO Account AD, RHD and CStaff

Booster Clubs and School Related Organizations Guidelines

Booster Clubs and School Related Organizations Guidelines 1 FOWARD This manual is designed to assist Booster Club officers, School Support Organizations ( club(s) and/or organization(s) ) and members by

Booster Clubs and School Related Organizations Guidelines 1 FOWARD This manual is designed to assist Booster Club officers, School Support Organizations ( club(s) and/or organization(s) ) and members by

Sumner County School Support Organizations

Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information Additional information and resources for School Support Organizations may be found

Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information Additional information and resources for School Support Organizations may be found

Dollars and Sense. The Role of the Treasurer

Dollars and Sense The Role of the Treasurer 2014-15 What do I need to know? Your PTA s tax number, formally called the Employer Identification Number (EIN). Your PTA s bank and bank account number. The

Dollars and Sense The Role of the Treasurer 2014-15 What do I need to know? Your PTA s tax number, formally called the Employer Identification Number (EIN). Your PTA s bank and bank account number. The

Field Trip Checklist

Field Trip Checklist Anytime students leave the school facilities on a field trip, there are many exposures that are present. Many of these exposures can be avoided. Clear Risk Solutions is always available

Field Trip Checklist Anytime students leave the school facilities on a field trip, there are many exposures that are present. Many of these exposures can be avoided. Clear Risk Solutions is always available

4/25/2017. Sample Agenda ~ Spring Meeting DEVELOPING A TRAINING PROGRAM FOR NEW LOCAL SCHOOL BOOKKEEPERS MAY 3, 2017

DEVELOPING A TRAINING PROGRAM FOR NEW LOCAL SCHOOL BOOKKEEPERS MAY 3, 2017 AASBO Annual Conference Karen O Bannon, CSFO Madison County Schools kobannon@mcssk12.org Training Program for Local School Bookkeepers

DEVELOPING A TRAINING PROGRAM FOR NEW LOCAL SCHOOL BOOKKEEPERS MAY 3, 2017 AASBO Annual Conference Karen O Bannon, CSFO Madison County Schools kobannon@mcssk12.org Training Program for Local School Bookkeepers

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS The principal shall be responsible to the county board of education for financial management of his school. He shall authorize

DODDRIDGE COUNTY SCHOOLS MANUAL OF FINANCIAL RECORDS FOR INDIVIDUAL SCHOOLS The principal shall be responsible to the county board of education for financial management of his school. He shall authorize

PTA Guidelines. Financial Policies and Procedures See Texas PTA Handbook

PTA Guidelines Organization Establishment and Approval Go to www.txpta.org Financial Policies and Procedures See Texas PTA Handbook www.txpta.org NOTE: The Federal Tax Number and the Texas Sales and Use

PTA Guidelines Organization Establishment and Approval Go to www.txpta.org Financial Policies and Procedures See Texas PTA Handbook www.txpta.org NOTE: The Federal Tax Number and the Texas Sales and Use

Welcome! The Booster Club is a volunteer organization whose purpose is best exemplified by our mission statement:

Welcome! Welcome to the Liberty Booster Club! Whether you are a coach, adviser, program parent representative or general member, we thank you for the time and energy you spend to ensure that our students

Welcome! Welcome to the Liberty Booster Club! Whether you are a coach, adviser, program parent representative or general member, we thank you for the time and energy you spend to ensure that our students

UNIVERSITY OF WISCONSIN-SUPERIOR INFORMATION PACKET FOR CONDUCTING CLASS A RAFFLES

UNIVERSITY OF WISCONSIN-SUPERIOR INFORMATION PACKET FOR CONDUCTING CLASS A RAFFLES (Raffles where some or all of the tickets are sold on days other than the day of the raffle drawing.) Any university department

UNIVERSITY OF WISCONSIN-SUPERIOR INFORMATION PACKET FOR CONDUCTING CLASS A RAFFLES (Raffles where some or all of the tickets are sold on days other than the day of the raffle drawing.) Any university department

FORMS. Document Description. Document Number

FORMS All transactions shall, at a minimum, be in accordance within the guidelines of this document, Accounting Procedures for Kentucky Activity Funds (Redbook), and using the forms contained in this Forms

FORMS All transactions shall, at a minimum, be in accordance within the guidelines of this document, Accounting Procedures for Kentucky Activity Funds (Redbook), and using the forms contained in this Forms

PTO/Booster Club Financial Guidelines

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

PTO/Booster Club Financial Guidelines Revised August 2015 Accounting Procedures Parent Organizations/Booster Clubs should include written instructions on the recording of accounting transactions in their

CHAPTER 9 Information Unique to Each Fund

CHAPTER 9 Information Unique to Each Fund Table of Contents Page INTRODUCTION... 1 GENERAL FUND... 1 ASSOCIATED STUDENT BODY FUND (ASB)... 2 Introduction... 2 Associated Student Body Moneys... 2 Trust

CHAPTER 9 Information Unique to Each Fund Table of Contents Page INTRODUCTION... 1 GENERAL FUND... 1 ASSOCIATED STUDENT BODY FUND (ASB)... 2 Introduction... 2 Associated Student Body Moneys... 2 Trust

PURCHASING CARD GUIDE

Southern Utah University PURCHASING CARD GUIDE The Southern Utah University Purchasing Card is a campus owned credit card issued to an employee to assist in their daily purchasing activities. The Purchasing

Southern Utah University PURCHASING CARD GUIDE The Southern Utah University Purchasing Card is a campus owned credit card issued to an employee to assist in their daily purchasing activities. The Purchasing

Accounting Procedures for Student and Parent Organizations

Accounting Procedures for Student and Parent Organizations AASBO LSFM Program May 2015 David Smith, Executive Director Alabama Association of School Business Officials 1 Accounting Procedures for Student

Accounting Procedures for Student and Parent Organizations AASBO LSFM Program May 2015 David Smith, Executive Director Alabama Association of School Business Officials 1 Accounting Procedures for Student

Operating Policies and Procedures for Regional Campuses Trustee Accounts Effective September 9, 2011

University of Connecticut Department of Student Activities Operating Policies and Procedures for Regional Campuses Trustee Accounts Effective September 9, 2011 This document supersedes all previous policies,

University of Connecticut Department of Student Activities Operating Policies and Procedures for Regional Campuses Trustee Accounts Effective September 9, 2011 This document supersedes all previous policies,

for FISCAL REPORTING to the DISTRICT for ORGANIZATIONS USING the DISTRICT S EIN and NOT FOR PROFIT STATUS

GUIDELINES and PROCEDURES for FISCAL REPORTING to the DISTRICT for ORGANIZATIONS USING the DISTRICT S EIN and NOT FOR PROFIT STATUS November 2015 The Beaver Dam Unified School District does not discriminate

GUIDELINES and PROCEDURES for FISCAL REPORTING to the DISTRICT for ORGANIZATIONS USING the DISTRICT S EIN and NOT FOR PROFIT STATUS November 2015 The Beaver Dam Unified School District does not discriminate

FUND RAISER PACKET (To be handed out before each Fund Raising Activity)

") Capac Community Schools FUND RAISER PACKET (To be handed out before each Fund Raising Activity) Revised August 24, 2006 PROCEDURE TO BECOME EFFECTIVE SEPTEMBER 1, 2006 FOR ALL FUND RAISING ACTIVITIES CAPAC

Capac Community Schools FUND RAISER PACKET (To be handed out before each Fund Raising Activity) Revised August 24, 2006 PROCEDURE TO BECOME EFFECTIVE SEPTEMBER 1, 2006 FOR ALL FUND RAISING ACTIVITIES CAPAC

Activity Fund Manual GILMER I.S.D.

Activity Fund Manual GILMER I.S.D. INDEX SECTION 1: General Information 1.1 Definition and Purpose of Activity Fund 1.2 Responsibility for Activity Fund 1.3 Income and Dues 1.4 Interest Earnings 1.5 Auditing

Activity Fund Manual GILMER I.S.D. INDEX SECTION 1: General Information 1.1 Definition and Purpose of Activity Fund 1.2 Responsibility for Activity Fund 1.3 Income and Dues 1.4 Interest Earnings 1.5 Auditing

Booster Club & Parent Organization Guidelines

Booster Club & Parent Organization Guidelines October 2017 FOREWORD This manual is designed to assist Booster Club and Parent Organization officers and members by providing organizational and financial

Booster Club & Parent Organization Guidelines October 2017 FOREWORD This manual is designed to assist Booster Club and Parent Organization officers and members by providing organizational and financial

Auditor. Auditor Manual

Auditor Auditor Manual 2012-2013 1 The AYSO National Office TEL: (800) 872-2976 FAX: (310) 525-1155 www.ayso.org All rights reserved. 2012 American Youth Soccer Organization Reproduction in whole or in

Auditor Auditor Manual 2012-2013 1 The AYSO National Office TEL: (800) 872-2976 FAX: (310) 525-1155 www.ayso.org All rights reserved. 2012 American Youth Soccer Organization Reproduction in whole or in

OFFICER TRANSACTIONS: COMPLETE OVERVIEW. Student Organization Finance Office

OFFICER TRANSACTIONS: COMPLETE OVERVIEW Student Organization Finance Office Transaction Guidelines Only authorized officers are allowed to handle transactions with SOFO Officers who have submitted a SOFO

OFFICER TRANSACTIONS: COMPLETE OVERVIEW Student Organization Finance Office Transaction Guidelines Only authorized officers are allowed to handle transactions with SOFO Officers who have submitted a SOFO

Booster Club Workshop

Corona-Norco Unified School District Booster Club Workshop May 1, 2017 May 15, 2017 Presenter: Dusty Nevatt, Partner Vavrinek, Trine, Day & Co., LLP Workshop Overview Definition of a Booster Club Fundraising

Corona-Norco Unified School District Booster Club Workshop May 1, 2017 May 15, 2017 Presenter: Dusty Nevatt, Partner Vavrinek, Trine, Day & Co., LLP Workshop Overview Definition of a Booster Club Fundraising

INTERNAL ACCOUNTS PROCEDURES MANUAL

INTERNAL ACCOUNTS PROCEDURES MANUAL Sumter County School Board Finance Department 2680 West County Road 476 Bushnell, FL 33513 10/18/2016 TABLE OF CONTENTS Introduction Chapter 1 School Internal Fund Principles

INTERNAL ACCOUNTS PROCEDURES MANUAL Sumter County School Board Finance Department 2680 West County Road 476 Bushnell, FL 33513 10/18/2016 TABLE OF CONTENTS Introduction Chapter 1 School Internal Fund Principles

THE SCHOOL DISTRICT OF ESCAMBIA COUNTY OUTSIDE SUPPORT ORGANIZATIONS

THE SCHOOL DISTRICT OF ESCAMBIA COUNTY OUTSIDE SUPPORT ORGANIZATIONS Guidelines Manual APPROVED ESCAMBIA COUNTY SCHOOL BOARD OCT 1 8 2016 MALCOLM TH0' 1/'.S, SUPCR!MTE ldent VERIFIED BY RECORDING SECRETARY

THE SCHOOL DISTRICT OF ESCAMBIA COUNTY OUTSIDE SUPPORT ORGANIZATIONS Guidelines Manual APPROVED ESCAMBIA COUNTY SCHOOL BOARD OCT 1 8 2016 MALCOLM TH0' 1/'.S, SUPCR!MTE ldent VERIFIED BY RECORDING SECRETARY

OKALOOSA COUNTY SCHOOL DISTRICT PURCHASING PROCEDURES

REVISED 5/27/14 OKALOOSA COUNTY SCHOOL DISTRICT PURCHASING PROCEDURES SCHOOL DISTRICT OF OKALOOSA COUNTY ADMINISTRATION COMPLEX PURCHASING DEPARTMENT, RM #1 120 LOWERY PLACE, S.E. FT WALTON BEACH, FL 32548

REVISED 5/27/14 OKALOOSA COUNTY SCHOOL DISTRICT PURCHASING PROCEDURES SCHOOL DISTRICT OF OKALOOSA COUNTY ADMINISTRATION COMPLEX PURCHASING DEPARTMENT, RM #1 120 LOWERY PLACE, S.E. FT WALTON BEACH, FL 32548

FISCAL CONTROLS. Purpose. Policy. Procedure. Date of Approval: August 18, 2013

FISCAL CONTROLS Date of Approval: August 18, 2013 Purpose The Board believes in implementing and following fiscal management practices to ensure that the School s funds are appropriately managed in order

FISCAL CONTROLS Date of Approval: August 18, 2013 Purpose The Board believes in implementing and following fiscal management practices to ensure that the School s funds are appropriately managed in order

ASB Operations Manual

To Table of Contents Bellevue School District ASB Operations Manual Effective: September 1, 2011 Staff: Simone Sangster, Ed.D. Assistant Superintendant of Finance and Operations Marie Telecky Director

To Table of Contents Bellevue School District ASB Operations Manual Effective: September 1, 2011 Staff: Simone Sangster, Ed.D. Assistant Superintendant of Finance and Operations Marie Telecky Director

Massachusetts Department of Elementary and

Massachusetts Department of Elementary and Secondary Education Index INFORMATION CONTACT: Massachusetts Department of Elementary and Secondary Education (ESE) Contact: Jay Sullivan Phone Numbers: (781)

Massachusetts Department of Elementary and Secondary Education Index INFORMATION CONTACT: Massachusetts Department of Elementary and Secondary Education (ESE) Contact: Jay Sullivan Phone Numbers: (781)

Booster Clubs and PTA/PTO Groups. also available at wfisd.net

Booster Clubs and PTA/PTO Groups also available at wfisd.net Table of Contents Introduction I. Formation, name and registration Annual self-audit Obtaining an Employer Identification Number (EIN) Becoming

Booster Clubs and PTA/PTO Groups also available at wfisd.net Table of Contents Introduction I. Formation, name and registration Annual self-audit Obtaining an Employer Identification Number (EIN) Becoming

Kamehameha Schools Hawai`i Team/Club Apparel Sales Request for Approval Form (For non-fundraising effort)

") Kamehameha Schools Hawai`i Team/Club Apparel Sales Request for Approval Form (For non-fundraising effort) Team/Group: : Coach/Advisor: Period for apparel sale: NOTE: No more than 5 school days may be allowed

Kamehameha Schools Hawai`i Team/Club Apparel Sales Request for Approval Form (For non-fundraising effort) Team/Group: : Coach/Advisor: Period for apparel sale: NOTE: No more than 5 school days may be allowed

Southeastern Oklahoma State University. Purchasing Policy and Procedures Manual October 1, 2018

Purchasing Policy and Procedures Manual October 1, 2018 1 Southeastern Oklahoma State University Purchasing Policy and Procedures Manual October 1, 2018 Table of Contents Authority...3 Requirements RUSO

Purchasing Policy and Procedures Manual October 1, 2018 1 Southeastern Oklahoma State University Purchasing Policy and Procedures Manual October 1, 2018 Table of Contents Authority...3 Requirements RUSO

CAMPS & CLINICS Table of Contents

CAMPS & CLINICS Table of Contents DISTRICT GUIDELINES.. 2 Guidelines for School Sponsored Events.4 Extracurricular Addenda Agreement W-9 Financial Summary for Camps and Clinics Payroll Expenses 1099 Expenses

CAMPS & CLINICS Table of Contents DISTRICT GUIDELINES.. 2 Guidelines for School Sponsored Events.4 Extracurricular Addenda Agreement W-9 Financial Summary for Camps and Clinics Payroll Expenses 1099 Expenses

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

Diane Branstetter, CFO Teresa Carter, Finance Manager/Asst Treasurer Tracy Hargrove, Finance/Fixed Assets

Diane Branstetter, CFO Teresa Carter, Finance Manager/Asst Treasurer Tracy Hargrove, Finance/Fixed Assets Sanctioning is simply the official recognition of an organization by the local school board. Sanctioning

Diane Branstetter, CFO Teresa Carter, Finance Manager/Asst Treasurer Tracy Hargrove, Finance/Fixed Assets Sanctioning is simply the official recognition of an organization by the local school board. Sanctioning

CASH HANDLING PROCEDURES FOR COUNTY OFFICES

CASH HANDLING PROCEDURES FOR COUNTY OFFICES Safeguarding Monies Prior to deposit, provide adequate safeguard for cash and checks. All cash and checks must be secure at all times. Store cash and checks

CASH HANDLING PROCEDURES FOR COUNTY OFFICES Safeguarding Monies Prior to deposit, provide adequate safeguard for cash and checks. All cash and checks must be secure at all times. Store cash and checks

WICHITA FALLS INDEPENDENT SCHOOL DISTRICT GUIDELINES FOR OPERATIONS. BOOSTER CLUBS and PTA/PTO GROUPS

WICHITA FALLS INDEPENDENT SCHOOL DISTRICT GUIDELINES FOR OPERATIONS BOOSTER CLUBS and PTA/PTO GROUPS Table of Contents Introduction I. Formation, name and registration Annual self-audit Obtaining an Employer