Energy and Loan Performance Data Project Stakeholder Feedback Webinar

|

|

|

- Jared McGee

- 5 years ago

- Views:

Transcription

1 Energy and Loan Performance Data Project Stakeholder Feedback Webinar November 22, 2013

2 Agenda Introduction to Project Team Project Goals and Overview Presentation of Data, Analyses, and Dashboard Feedback and Questions

3 Project Team EDF Investor Confidence Project Standards for Energy Efficiency Project Development and Measurement National network of Financial and Origination Allies Clean Energy Finance Center University of Chicago Data Science for Social Good Fellowship Matt Gee, Fellowship Organizer & Team Lead Alex Fedell Julie Cooper

4 EDF Investor Confidence Project Our Mission is to enable a market for investment in quality energy efficiency projects by reducing transaction costs and engineering overhead, while increasing the reliability and consistency of savings. History EDF focus on barriers to capital participation in energy efficiency Three year foundation funded consensus effort Broad participation from investors, engineers, programs, energy service companies, and building owners Key Goals Increase Deal Flow Manage Performance Risk Create Actionable Data

5 Data Project Snap Shot 1) Collect and aggregate energy efficiency loan and energy performance data from different residential and commercial lending programs. 2) Create publicly available database and dashboard. 3) Develop energy efficiency loan data specification. Standardized fields and definitions In collaboration with Lawrence Berkeley Lab and SEE Action Network Financing Workgroup

6 Data Project Goals Long-term goal: Create standardized infrastructure for the collection, aggregation, and analysis of EE loan and energy performance data to support the scaling of EE finance Project goals: State of the Union on EE Loan and Performance Data Identify EE loan data user needs Provide access publicly to currently available EE loan data Develop a standard EE loan data specification that meets the needs of data users Identify important gaps Gaps in how data are currently collected, analyzed, and shared/reported Starting point for detailed conversation about data requirements and standardization

7 Project Partners Funders and Collaborators Citigroup Foundation U.S. DOE, Dept. of Energy Efficiency & Renewable Energy Lawrence Berkeley National Labs Data Providers Pennsylvania Treasury (Keystone HELP) New York State Energy Research & Development Authority Clean Energy Works Oregon Greater Cincinnati Energy Alliance

8 What data have we collected and analyzed? All are residential loans Almost no commercial loan data publicly available 4 programs - 12,000 loans total 17% are on-bill, 83% are off-bill Personally identifiable information (PII) removed Data is not yet investment grade No time-series data collected yet Greater level of detail/granularity needed More loan volume and diversity (e.g., geographic) needed Data field categories (total of 95 fields) 1) Borrower and property information 2) Loan information 3) Project information 4) Energy savings information (quite limited)

9 Data Users Lenders and investors Banks, credit unions, CDFIs, originators & servicers, rating agencies, others Policymakers Public utility commissions, local/state/federal agencies, legislators, advocates, others Program administrators Local/state/federal agencies, utilities, green banks, others Other stakeholders Product and service providers, consultants/advisory groups, building owners, others

10 Related Data Efforts U.S. Department of Energy SEE Action Network Financing Workgroup: conducting an EE loan data scoping study Building Performance Database Building Energy Data Exchange Specification (BEDES) Solar Access to Public Capital (NREL) California EE loan data efforts Developing infrastructure to collect, store, protect and analyze EE loan data Support EE financing pilots

11 What Questions Can the Data Help Answer? What are some of the defining characteristics of EE loans, and how do they compare across loan programs? How does EE loan performance compare to that of other asset classes, such as auto, credit cards, solar loan/lease, or time-shares? Will EE loan performance deteriorate somewhat in the future as lending expands beyond first adopters? Is there a correlation between energy savings and loan performance?

12 What Questions Can the Data Help Answer? (continued) With acceptance of protocols, will lenders use energy savings in the underwriting process? Will methods to secure loans (e.g., OBR, PACE) make a significant difference in loan volume and terms? Do certain characteristics of loan products result in greater levels of energy efficiency? Do certain characteristics of loan products matter more for secondary markets?

13 Project Plan Going Forward Milestone Interview data users and obtain feedback on database/dashboard (EDF/LBNL) Deliverable January 2014 Publish database and dashboard (EDF) February Publish EE data specification (EDF/LBNL) May Publish Issues & Recommendations report (LBNL) June

14

15 Overview What We ve Done Main Findings Loan Performance Data: Ideal vs. Reality Data Preview Underwriting Differences Characterizing Performance Suggestive Relationships Data Dashboard Next Steps

16 What We ve Done Standardize Format Documentation Understand Underwriting Differences Performance Analysis Explore Unique Predictors Identify Gaps

17 Commitment to Open Data & Analysis Data Available Through Google Fusion Tables Documentation & Analysis Available on Github.com Visualization Available through Chartio.com Dashboard

18 Main Findings Program structure and incentives matter EE loans in portfolio have relatively low charge off rates and relatively high pre-payment rates Some suggestive evidence on unique predictors of performance Higher frequency data over more years are needed to answer critical stakeholder questions Need pre- and post-retrofit energy use data linked with loan data

19 Main Challenges No standard products: differences in underwriting and terms make comparisons across programs difficult No standard data collection: differences in fields collected by programs make cross-program analysis difficult Short histories and very low charge-off rates limit the power of the analysis No standard for and little emphasis on tracking project performance

20 11,947 Loans 7,216 Loans 3,446 Loans 1,166 Loans 119 Loans

21 Total Loan Volume: $103,649,269 $54,837,059 $32,845,566 $14,911,852 $1,054,812

22

23

24 Standard Loan Performance Data Static Features Dynamic Features Borrower Characteristics Loan Characteristics Project Characteristics Monthly payment history Outstanding Balance Loss mitigation

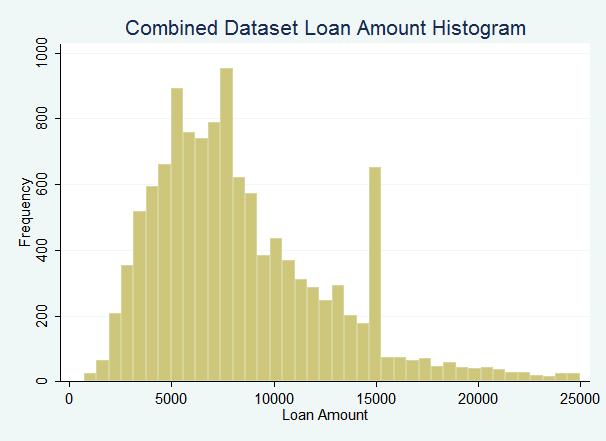

25 You can t always get what you want Static Features Borrower Characteristics Loan Characteristics Project Characteristics Dynamic Features! Monthly payment history Outstanding Balance Loss mitigation

26 Combined Data Overview: What We ve Got Information About Borrower and Property Information About the Loan Limited Information on Payments Limited Information About the Project No Information About Energy Usage

27 Information About the Borrower and Property Data Field Oregon NYSERDA PA Treasury GCEA Credit Score x x x x Zip x x x x State x x x x DTI x x x City x x x Borrowers Annual Income x x x County x x x Year Constructed x x x Floorspace x x x Building Type x x Number of occupants x x

28 Information About the Loan Data Field Oregon NYSERDA PA Treasury GCEA Loan Amount x x x x Loan Interst Rate x x x x Original Loan Term x x x x Loan Approval Date x x x x Current Principal Balance x x x Loan Status x x x Days Past Due x x x Next Principal Due Date x x x Next Interest Due Date x x x Last Payment Date x x x Last Payment Amount x x # Payments Made x x Loan Product x x Open Date x x Charge Off Amount x x Regular Payment Due Amount x x Lender Name x x

29 Information About the Project Data Field Oregon NYSERDA PA Treasury GCEA Project Work Done x x x Total Invoiced Cost x x

30 Information About Energy Savings!

31 What Stakeholders Want to See Underwriting Criteria Delinquency Defaults Prepayment Losses

32 Combined Dataset Summary Statistics Data Field Range Median Mean # of Loans Loan Amount $701-$30,000 $7,500 $8,675 11,947 Loan Term ,947 Loan Interest 0.99%-12% 5.99% 5.6% 11,947 Credit Score ,929 DTI ,774 Annual Income 0-$725,000 $65,000 $77,460 4,724

33 Summary Statistics by Program Loan Amounts: Data Set Range Median Mean # of Loans Oregon $1,000-$30,000 $11,689 $12,788 1,166 NYSERDA $701-$25,000 $8,439 $9,531 3,446 PA Treasury $1,000-$15,000 $7,032 $7,599 7,216 GCEA $1,000-$21,000 $7,538 $8,

34 Summary Statistics by Program Borrowers Credit Scores: Data Set Range Median Mean # of Obs Oregon ,166 NYSERDA ,454 PA Treasury ,216 GCEA

35 Summary Statistics by Program

36 Summary Statistics by Program Borrowers DTI: Data Set Range Median Mean # of Loans Oregon NYSERDA ,446 PA Treasury ,216 GCEA

37 Summary Statistics by Program

38 Analysis of Loan Amounts Combined Dataset 11,947 Loans Range: $701-$30,000 Mean: $8,675, Median: $7,500 Total Amount Lent: $103,649,269

39

40 Analysis of Charge Offs 11,828 Loans 106 (0.89%) Charged Off, We Have Date and Amount Data For 103 Charged Off Amounts Range from $901- $25,000 Median: $5,824 Mean: $6,182 Total Principal Lost: $642,917

41 Analysis of Charge Offs by Program Data Set % Charged # Charged Range of Charged Off Amounts Median Amount Mean Amount Oregon 0.17% 2 N/A N/A N/A NYSERDA 0.4% 13 $1,368-$25,000 $6,495 $7,426 PA Treasury 1.26% 91 $903-$15,000 $5,695 $6,004 GCEA N/A N/A N/A N/A N/A

42 Analysis of Charge Offs by Loan Term Data Set % Charged # Charged Range of Charged Off Amounts Median Amount Mean Amount 36-Month 0.68% 7 $903-$6,524 $2,908 $3, Month 1.02% 24 $2,074-$8,340 $3,263 $3, Month 1.32% 66 $2,741-$14,897 $6,430 $7, Month 0.31% 7 $1,368-$25,000 $7,669 $9, Month 0.18% 2 N/A N/A N/A

43 Charge Off Rates Over Time Rate of Charge Off increases as loans age to around 2 years then plateaus Measured rate is significantly less meaningful above 3 years because of small sample size

44

45 Prepayment Analysis 11,828 Loans 2,040 (17.24%) Prepaid

46 Prepayment Rate by Program Loan Program # of Loans # of Early Payoffs Early Payoff Rate PA Treasury % NYSERDA % Oregon %

47 Prepayment Rate by Loan Term Loan Term in Months # of Loans # of early payoffs Early Payoff Rate % % % % %

48 Losses Analysis 11,947 Loans $103,649,269 loaned out $34,294,175 in expected interest payments $137,943,444 expected to be paid back

49 Combined Dataset Losses Analysis 103 Charge Offs $642,917 in lost principal, $163,175 in lost interest $806,092 in total losses, which is 0.58% of the total expected payback

50 Combined Dataset Losses Analysis 2,040 Prepayments $301,910 in lost interest, which is 0.22% of the total expected payback $1,108,002 in total losses, which is 0.8% of the total expected payback

51 Losses by Program Program Principal Losses from Chargeoffs Interest Losses from Chargeoffs Total Losses from Chargeoffs Interest Losses from Payoffs Total Losses Total Losses as a Percent Oregon N/A N/A N/A $20,158 $20,158 N/A NYSERDA $96,453 $22,435 $118,888 $2,739 $121, % PA Treas. $546,373 $140,739 $687,112 $279,011 $966, %

52 Losses by Loan Term Loan Term Principal Losses from Chargeoffs Interest Losses from Chargeoffs Total Losses from Chargeoffs Interest Losses from Payoffs Total Losses Total Losses as a Percent 36-Month $24,014 $1,432 $25,446 $112,142 $137, % 60-Month $89,942 $8,581 $98,523 $99,010 $197, % 120- Month 180- Month 240- Month $463,717 $135,561 $599,278 $70,222 $695, % $65,241 $17,600 $82,841 $375 $83, % N/A N/A $19,203 $19203 N/A

53 Delinquency Analysis As of 7/31/2013, the combined dataset 30-day delinquency rate was 1.9% Without time-series data, a more meaningful delinquency analysis was not possible

54 Online Dashboard Demo

55 What s Special About EE Loans? On-bill vs Off-bill Energy savings & loan performance Whole home vs single measure Cost effectiveness criteria

56 Gaps in Data Shared core of loan & borrower characteristics Monthly or quarterly payment data Portfolios with longer payment history Project characteristics Energy performance data

57 Gaps in Knowledge Driving demand: an information problem? Pricing mismatch? Loan performance and energy performance On-bill vs off-bill

58 Future Direction Documentation and data standard More data Fannie Mae EE Loan Data? Energy performance and loan performance Single measure vs whole home Better comparisons groups Opportunities for demand-side transparency

59 Feedback and Questions What additional questions should we be considering? Are there key stakeholders we are missing? Are there pockets of Commercial Loan Data? Where? How important is, or will be, the correlation of energy performance and loan performance? Where would you like to see this project go in the future? Anything else is on your mind!

60 Energy and Loan Performance Data Project For More Information: Matt Golden Senior Energy Finance Consultant Environmental Defense Fund Craig Diamond Executive Director Clean Energy Finance Center

The Data Disconnect Experiences in Secondary Markets Securitization ACEEE Energy Finance Forum 5/14/2013

The Data Disconnect Experiences in Secondary Markets Securitization ACEEE Energy Finance Forum 5/14/2013 Jeff Pitkin, Treasurer New York State Energy Research and Development Authority Background Green

The Data Disconnect Experiences in Secondary Markets Securitization ACEEE Energy Finance Forum 5/14/2013 Jeff Pitkin, Treasurer New York State Energy Research and Development Authority Background Green

Financing Program Data Practices

Financing Program Data Practices June 2, 2015 ACEEE Finance Forum Johanna Zetterberg, US DOE (Moderator) Emily Martin Fadrhonc, LBNL About SEE Action Network of 200+ leaders and professionals, led by state

Financing Program Data Practices June 2, 2015 ACEEE Finance Forum Johanna Zetterberg, US DOE (Moderator) Emily Martin Fadrhonc, LBNL About SEE Action Network of 200+ leaders and professionals, led by state

Energy Efficiency Financing for Lowand Moderate-Income Households. Greg Leventis, Lawrence Berkeley National Laboratory ACEEE Finance Forum

Energy Efficiency Financing for Lowand Moderate-Income Households Greg Leventis, Lawrence Berkeley National Laboratory ACEEE Finance Forum May 23, 2017 Coming soon! Coming soon! To be notified when published,

Energy Efficiency Financing for Lowand Moderate-Income Households Greg Leventis, Lawrence Berkeley National Laboratory ACEEE Finance Forum May 23, 2017 Coming soon! Coming soon! To be notified when published,

Options for Raising Capital (and Leveraging Public Funds) for Residential Energy Loan Programs 1 1/25/2011 UNC Environmental Finance Center

for Residential Energy Loan Programs 1 1/25/2011 UNC Environmental Finance Center") Options for Raising (and Leveraging Public Funds) for Residential Energy Loan s 1 1/25/2011 UNC Environmental Finance Center As of January 2011, the USDOE supported Database of State Incentives for Renewables

Options for Raising (and Leveraging Public Funds) for Residential Energy Loan s 1 1/25/2011 UNC Environmental Finance Center As of January 2011, the USDOE supported Database of State Incentives for Renewables

Energy Efficiency Fund: A Model for Financing Energy Efficiency Improvements

Energy Efficiency Fund: A Model for Financing Energy Efficiency Improvements March 9, 2010 Presentation to Energy Efficiency Advisory Council Thomas Darling, Clean Energy Fellow 1 Introduction Three year

Energy Efficiency Fund: A Model for Financing Energy Efficiency Improvements March 9, 2010 Presentation to Energy Efficiency Advisory Council Thomas Darling, Clean Energy Fellow 1 Introduction Three year

Third-Party Administrators for Energy Efficiency: Funding & Contract Design Considerations

Third-Party Administrators for Energy Efficiency: Funding & Contract Design Considerations National Governors Association Retreat for Puerto Rico, January 19, 2016 Janine Migden-Ostrander RAP Principal

Third-Party Administrators for Energy Efficiency: Funding & Contract Design Considerations National Governors Association Retreat for Puerto Rico, January 19, 2016 Janine Migden-Ostrander RAP Principal

Energy Investment Partnerships Webinar Series

Webinar Series February 23, 2016 1 California Partners Reaching CA s energy and environmental goals through policies, planning, direct regulations, market approaches, incentives and voluntary efforts.

Webinar Series February 23, 2016 1 California Partners Reaching CA s energy and environmental goals through policies, planning, direct regulations, market approaches, incentives and voluntary efforts.

CDFA / / BNY MELLON DEVELOPMENT FINANCE WEBCAST SERIES New Models of Financing Energy Efficiency

CDFA / / BNY MELLON DEVELOPMENT FINANCE WEBCAST SERIES New Models of Financing Energy Efficiency The Broadcast will Begin at 1:00pm EDT Submit your questions in advance using the GoToWebinar control panel

CDFA / / BNY MELLON DEVELOPMENT FINANCE WEBCAST SERIES New Models of Financing Energy Efficiency The Broadcast will Begin at 1:00pm EDT Submit your questions in advance using the GoToWebinar control panel

Role of Green Banks and Energy Efficiency Financing

Role of Green Banks and Energy Efficiency Financing NGA State Workshop on Innovations in Energy Efficiency Policy February 20, 2014 Jeffrey Schub, Vice President Coalition for Green Capital Agenda Washington,

Role of Green Banks and Energy Efficiency Financing NGA State Workshop on Innovations in Energy Efficiency Policy February 20, 2014 Jeffrey Schub, Vice President Coalition for Green Capital Agenda Washington,

Craft3 & Self-Help Single-Family Residential Energy Efficiency Loan Sale. June 2015

Craft3 & Self-Help Single-Family Residential Energy Efficiency Loan Sale June 2015 Craft3 A Community Development Financial Institution (CDFI) A nonprofit and charitable corporation Not a bank or credit

Craft3 & Self-Help Single-Family Residential Energy Efficiency Loan Sale June 2015 Craft3 A Community Development Financial Institution (CDFI) A nonprofit and charitable corporation Not a bank or credit

Financing and Funding Energy Efficiency Initiatives.

Financing and Funding Energy Efficiency Initiatives www.efc.unc.edu Paying for Energy Programs Two main program elements Finance program design Sources of capital Programs around the state and country

Financing and Funding Energy Efficiency Initiatives www.efc.unc.edu Paying for Energy Programs Two main program elements Finance program design Sources of capital Programs around the state and country

Establishing a Local Green Bank

Establishing a Local Green Bank MONTGOMERY COUNTY AND THE ROLE OF GOVERNMENT IN EXPANDING THE ENERGY FINANCE MARKET M I C H E L L E V I G E N, S E N I O R E N E R GY P L A N N E R M O N TG O M E R Y C

Establishing a Local Green Bank MONTGOMERY COUNTY AND THE ROLE OF GOVERNMENT IN EXPANDING THE ENERGY FINANCE MARKET M I C H E L L E V I G E N, S E N I O R E N E R GY P L A N N E R M O N TG O M E R Y C

The Total Resource Cost of Saved Energy for Utility Customer-Funded Energy Efficiency Programs

The work described in this presentation was funded by the National Electricity Delivery Division of the U.S. Department of Energy s Office of Electricity Delivery and Energy Reliability and the Office

The work described in this presentation was funded by the National Electricity Delivery Division of the U.S. Department of Energy s Office of Electricity Delivery and Energy Reliability and the Office

Presentation to Government Finance Officer Association

Presentation to Government Finance Officer Association Tom Deyo, CEO JANUARY 19, 2018 What is the Mission for a Green Bank? Clean Energy Finance Banks - Close gaps in financing markets for energy efficiency

Presentation to Government Finance Officer Association Tom Deyo, CEO JANUARY 19, 2018 What is the Mission for a Green Bank? Clean Energy Finance Banks - Close gaps in financing markets for energy efficiency

Evaluation, Measurement, and Verification (EM&V) of Residential Behavior-Based Energy Efficiency Programs: Issues and Recommendations

of Residential Behavior-Based Energy Efficiency Programs: Issues and Recommendations") Evaluation, Measurement, and Verification (EM&V) of Residential Behavior-Based Energy Efficiency Programs: Issues and Recommendations November 13, 2012 Michael Li U.S. Department of Energy Annika Todd

Evaluation, Measurement, and Verification (EM&V) of Residential Behavior-Based Energy Efficiency Programs: Issues and Recommendations November 13, 2012 Michael Li U.S. Department of Energy Annika Todd

Role of Green Banks and Energy Efficiency Financing

Role of Green Banks and Energy Efficiency Financing 2014 ACEEE Energy Efficiency Finance Forum May 12, 2014 Jeffrey Schub, Vice President Coalition for Green Capital Green banks overcome existing barriers

Role of Green Banks and Energy Efficiency Financing 2014 ACEEE Energy Efficiency Finance Forum May 12, 2014 Jeffrey Schub, Vice President Coalition for Green Capital Green banks overcome existing barriers

On-Bill Financing: Exploring the Energy Efficiency Opportunities and Diversity of Approaches

On-Bill Financing: Exploring the Energy Efficiency Opportunities and Diversity of Approaches National Conference of State Legislatures: Everybody Wins Driving Economic Growth and Energy Efficiency with

On-Bill Financing: Exploring the Energy Efficiency Opportunities and Diversity of Approaches National Conference of State Legislatures: Everybody Wins Driving Economic Growth and Energy Efficiency with

Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s

, this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s") Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s explorations into manufactured home mortgage data. This

Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s explorations into manufactured home mortgage data. This

October 18, Policy Framework for PACE Financing Programs

Policy Framework for PACE Financing Programs The following Policy Framework has been developed by the White House and the relevant agencies as a policy framework for Property Assessed Clean Energy (PACE)

Policy Framework for PACE Financing Programs The following Policy Framework has been developed by the White House and the relevant agencies as a policy framework for Property Assessed Clean Energy (PACE)

Native American Indian Housing Council 2018 Annual Conference. San Diego, CA May 30, Collaborating with Fannie Mae to Expand Affordable Housing

Native American Indian Housing Council 2018 Annual Conference San Diego, CA May 30, 2018 Collaborating with Fannie Mae to Expand Affordable Housing 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Agenda Who

Native American Indian Housing Council 2018 Annual Conference San Diego, CA May 30, 2018 Collaborating with Fannie Mae to Expand Affordable Housing 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Agenda Who

Financing Energy Efficiency: Overview and Lessons

Financing Energy Efficiency: Overview and Lessons Matthew H. Brown Harcourt Brown LLC Matthew.Brown@HarcourtBrown.com 720 246 8847 Harcourt Brown LLC Consulting firm with a specialty in financing for clean

Financing Energy Efficiency: Overview and Lessons Matthew H. Brown Harcourt Brown LLC Matthew.Brown@HarcourtBrown.com 720 246 8847 Harcourt Brown LLC Consulting firm with a specialty in financing for clean

Energy Efficiency Proposals in Fannie Mae and Freddie Mac s Draft Underserved Markets Plans

Energy Efficiency Proposals in Fannie Mae and Freddie Mac s Draft Underserved Markets Plans Prepared May 17, 2017 by the National Association of State Energy Officials (NASEO) Contact: Sandy Fazeli (sfazeli@naseo.org)

Energy Efficiency Proposals in Fannie Mae and Freddie Mac s Draft Underserved Markets Plans Prepared May 17, 2017 by the National Association of State Energy Officials (NASEO) Contact: Sandy Fazeli (sfazeli@naseo.org)

Investor Confidence Project Europe

Environmental Defense Fund s Investor Confidence Project Europe First Session of the Group of Experts on Energy Efficiency United Nations, Geneva, Switzerland November 17, 2014 Europe s Climate and Energy

Environmental Defense Fund s Investor Confidence Project Europe First Session of the Group of Experts on Energy Efficiency United Nations, Geneva, Switzerland November 17, 2014 Europe s Climate and Energy

Our recommendations for improving the Plans, with additional detail below, are:

July 10, 2017 Jim Gray Duty to Serve Program Manager Federal Housing Finance Agency 400 Seventh Street SW Room 10276 Washington, DC 20219 Dear Jim, Re: Comments on Fannie Mae s and Freddie Mac s Proposed

July 10, 2017 Jim Gray Duty to Serve Program Manager Federal Housing Finance Agency 400 Seventh Street SW Room 10276 Washington, DC 20219 Dear Jim, Re: Comments on Fannie Mae s and Freddie Mac s Proposed

The role of information on energy costs in mortgage underwriting

The role of information on energy costs in mortgage underwriting October 5, 2011 Resources for the Future First Wednesday Seminar Cliff Majersik Executive Director, IMT cliff@imt.org Can Creative Financing

The role of information on energy costs in mortgage underwriting October 5, 2011 Resources for the Future First Wednesday Seminar Cliff Majersik Executive Director, IMT cliff@imt.org Can Creative Financing

On-bill financing programs are a promising way for utilities to help customers

NRDC Issue brief august 2012 ib:12-08-a On-Bill Financing Overview and Key Considerations for Program Design Author Philip Henderson Natural Resources Defense Council On-bill financing programs are a promising

NRDC Issue brief august 2012 ib:12-08-a On-Bill Financing Overview and Key Considerations for Program Design Author Philip Henderson Natural Resources Defense Council On-bill financing programs are a promising

Lending TRAINING AND EVENTS. aba.com/lendingtraining

Lending TRAINING AND EVENTS aba.com/lendingtraining Enhance your lending expertise. Adapt to a dynamic economic landscape through sound lending practices, underwriting considerations and regulatory risk

Lending TRAINING AND EVENTS aba.com/lendingtraining Enhance your lending expertise. Adapt to a dynamic economic landscape through sound lending practices, underwriting considerations and regulatory risk

HOMESTYLE ENERGY MORTGAGES & PROPERTY ASSESSED CLEAN ENERGY LOANS (FANNIE MAE ONLY)

") OVERVIEW HOMESTYLE ENERGY MORTGAGES There are a number of HomeStyle Energy financing options available to a borrower who wishes to improve the energy and/or water efficiency of an existing property and

OVERVIEW HOMESTYLE ENERGY MORTGAGES There are a number of HomeStyle Energy financing options available to a borrower who wishes to improve the energy and/or water efficiency of an existing property and

Evolution of Residential Loan Programs: Building Markets by Reducing Risk & Fostering Collaboration

Evolution of Residential Loan Programs: Building Markets by Reducing Risk & Fostering Collaboration ACEEE Finance Forum May 22, 2018 Connecticut Green Bank Delivering Results for Connecticut Investment

Evolution of Residential Loan Programs: Building Markets by Reducing Risk & Fostering Collaboration ACEEE Finance Forum May 22, 2018 Connecticut Green Bank Delivering Results for Connecticut Investment

U.S. General Services Administration. WEX Online Data Analysis Reporting Tools Sharon Linnane Government Account Manager Wright Express Corporation

U.S. General Services Administration WEX Online Data Analysis Reporting Tools Sharon Linnane Government Account Manager Wright Express Corporation July 31 and August 2, 2012 This material is intended for

U.S. General Services Administration WEX Online Data Analysis Reporting Tools Sharon Linnane Government Account Manager Wright Express Corporation July 31 and August 2, 2012 This material is intended for

In recent years, home energy efficiency (EE) has progressed from the margins to the

has progressed from the margins to the") Community Development INVESTMENT REVIEW 63 Home Energy Efficiency and Mortgage Risks: An Extended Abstract Nikhil Kaza UNC Center for Community Capital Department of City and Regional Planning University

Community Development INVESTMENT REVIEW 63 Home Energy Efficiency and Mortgage Risks: An Extended Abstract Nikhil Kaza UNC Center for Community Capital Department of City and Regional Planning University

RESIDENTIAL ENERGY EFFICIENCY FINANCING MARKET TRENDS. Presented: 5/23/2016

RESIDENTIAL ENERGY EFFICIENCY FINANCING MARKET TRENDS Presented: 5/23/2016 Overview Trends throughout the country A closer look at CA Where our data comes from What s Out There: Energy Efficiency Financing

RESIDENTIAL ENERGY EFFICIENCY FINANCING MARKET TRENDS Presented: 5/23/2016 Overview Trends throughout the country A closer look at CA Where our data comes from What s Out There: Energy Efficiency Financing

MW Bancorp, Inc. Consolidated Financial Statements. June 30, 2018 and 2017

Consolidated Financial Statements June 30, 2018 and 2017 June 30, 2018 and 2017 Contents Independent Auditor s Report... 1 Financial Statements Consolidated Balance Sheets... 2 Consolidated Statements

Consolidated Financial Statements June 30, 2018 and 2017 June 30, 2018 and 2017 Contents Independent Auditor s Report... 1 Financial Statements Consolidated Balance Sheets... 2 Consolidated Statements

Financing Energy Efficiency Projects:

Financing Energy Efficiency Projects: Blending ARRA Funds with Commercial Finance March 7, 2011 Presented by: John MacLean Energy Efficiency Finance Corp. on behalf of USDOE financial advisory team jmaclean@eefinance.net

Financing Energy Efficiency Projects: Blending ARRA Funds with Commercial Finance March 7, 2011 Presented by: John MacLean Energy Efficiency Finance Corp. on behalf of USDOE financial advisory team jmaclean@eefinance.net

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME 4 REASONS WHY YOU SHOULD CHOOSE PPG UPFRONT UNDERWRITING And pre-approvals! This reduces your stress when buying a home. EASY MOBILE APPLICATION We keep

BUYER S EDGE A GUIDE TO FINANCING YOUR DREAM HOME 4 REASONS WHY YOU SHOULD CHOOSE PPG UPFRONT UNDERWRITING And pre-approvals! This reduces your stress when buying a home. EASY MOBILE APPLICATION We keep

Andrew Satchwell*, Charles Goldman*, Peter Larsen*, Donald Gilligan**, and Terry Singer**

A Survey of the U.S. Energy Service Company (ESCO) Industry: Market Growth and Development from 2008 to 2011 Andrew Satchwell*, Charles Goldman*, Peter Larsen*, Donald Gilligan**, and Terry Singer** *Lawrence

A Survey of the U.S. Energy Service Company (ESCO) Industry: Market Growth and Development from 2008 to 2011 Andrew Satchwell*, Charles Goldman*, Peter Larsen*, Donald Gilligan**, and Terry Singer** *Lawrence

Whereas, solar energy is an abundant, domestic, renewable, and non-polluting energy resource.

An Act Relating to the Establishment of a Community Solar Program For Restructured States Whereas, solar energy is an abundant, domestic, renewable, and non-polluting energy resource. Whereas, local solar

An Act Relating to the Establishment of a Community Solar Program For Restructured States Whereas, solar energy is an abundant, domestic, renewable, and non-polluting energy resource. Whereas, local solar

Performance Budgeting for Federal Agencies. A Framework. JOHN MERCER (link to John Mercer's Website) IN PARTNERSHIP WITH AMS MARCH 18, 2002

IN PARTNERSHIP WITH AMS MARCH 18, 2002") Performance Budgeting for Federal Agencies A Framework JOHN MERCER (link to John Mercer's Website) IN PARTNERSHIP WITH AMS MARCH 18, 2002 For additional information please contact us at: John Mercer: GPRA@john-mercer.com

Performance Budgeting for Federal Agencies A Framework JOHN MERCER (link to John Mercer's Website) IN PARTNERSHIP WITH AMS MARCH 18, 2002 For additional information please contact us at: John Mercer: GPRA@john-mercer.com

SDG&E s Energy Efficiency Business Plan WCEC Affiliates Forum. May 2017

SDG&E s Energy Efficiency Business Plan WCEC Affiliates Forum May 2017 1 Who We Serve 4,000+ employees serve clean, reliable energy to 3.5 million customers in San Diego and Southern Orange counties We

SDG&E s Energy Efficiency Business Plan WCEC Affiliates Forum May 2017 1 Who We Serve 4,000+ employees serve clean, reliable energy to 3.5 million customers in San Diego and Southern Orange counties We

PACE Loans: Does Sale Value Reflect Improvements?

Winter 2016 Volume 21 Number 4 www.iijsf.com PACE Loans: Does Sale Value Reflect Improvements? LAURIE S. GOODMAN AND JUN ZHU The Voices of Influence iijournals.com PACE Loans: Does Sale Value Reflect Improvements?

Winter 2016 Volume 21 Number 4 www.iijsf.com PACE Loans: Does Sale Value Reflect Improvements? LAURIE S. GOODMAN AND JUN ZHU The Voices of Influence iijournals.com PACE Loans: Does Sale Value Reflect Improvements?

Income Trends of Residential PV Adopters An analysis of household-level income estimates

Income Trends of Residential PV Adopters An analysis of household-level income estimates Galen Barbose, Naïm Darghouth, Ben Hoen, and Ryan Wiser Lawrence Berkeley National Laboratory April 2018 This analysis

Income Trends of Residential PV Adopters An analysis of household-level income estimates Galen Barbose, Naïm Darghouth, Ben Hoen, and Ryan Wiser Lawrence Berkeley National Laboratory April 2018 This analysis

Scaling-up energy efficiency investment in buildings. Part of the Investor Confidence Project Europe Presentation for UK stakeholders 17 June, 2015

Scaling-up energy efficiency investment in buildings Part of the Investor Confidence Project Europe Presentation for UK stakeholders 17 June, 2015 Agenda Introduction UK market need and current status

Scaling-up energy efficiency investment in buildings Part of the Investor Confidence Project Europe Presentation for UK stakeholders 17 June, 2015 Agenda Introduction UK market need and current status

Fintech Lending: Financial Inclusion, Risk Pricing, and Alternative Information

Fintech Lending: Financial Inclusion, Risk Pricing, and Alternative Information IAES Conference, Montreal October 6-8, 2017 Julapa Jagtiani and Cathy Lemieux Agenda Growth in Fintech Lending Objective

Fintech Lending: Financial Inclusion, Risk Pricing, and Alternative Information IAES Conference, Montreal October 6-8, 2017 Julapa Jagtiani and Cathy Lemieux Agenda Growth in Fintech Lending Objective

Share Your Experience With Debt

Native CDFIs: Growing with Debt Capital Lisa Wagner, Bluestem Consulting Emily Trump, First Nations Oweesta Corporation Share Your Experience With Debt What types of sources of debt do you currently have?

Native CDFIs: Growing with Debt Capital Lisa Wagner, Bluestem Consulting Emily Trump, First Nations Oweesta Corporation Share Your Experience With Debt What types of sources of debt do you currently have?

Policy Proposals for Reducing Health Care Costs. Marc Boutin, JD Chief Executive Officer

Policy Proposals for Reducing Health Care Costs Marc Boutin, JD Chief Executive Officer April 25, 2017 Project Goal and Approach Develop policy recommendations from the patient perspective about health

Policy Proposals for Reducing Health Care Costs Marc Boutin, JD Chief Executive Officer April 25, 2017 Project Goal and Approach Develop policy recommendations from the patient perspective about health

Lending and Collateral Q&A

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

November 14, 2017 Note - Each answer in this document is written as if it were a stand-alone response. Therefore, some information may be repeated. What is an advance and how do advances work? The FHLBanks

How to Originate and Deliver HomeReady Mortgages

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

Financing: Leveraging Capital Markets to Scale Building Energy Efficiency in China

Financing: Leveraging Capital Markets to Scale Building Energy Efficiency in China Presented by Carolyn Szum, China Energy Group, Lawrence Berkeley National Laboratory March 5, 2018 Discussion Topics 1.

Financing: Leveraging Capital Markets to Scale Building Energy Efficiency in China Presented by Carolyn Szum, China Energy Group, Lawrence Berkeley National Laboratory March 5, 2018 Discussion Topics 1.

ECLIPSE: Aligning Data to Track Local Greenhouse Gas Emissions and Health Improvement

ECLIPSE: Aligning Data to Track Local Greenhouse Gas Emissions and Health Improvement Alan M. Delmerico, PhD Center for Health and Social Research, SUNY Buffalo State & Eric Walker Director of Energy Development

ECLIPSE: Aligning Data to Track Local Greenhouse Gas Emissions and Health Improvement Alan M. Delmerico, PhD Center for Health and Social Research, SUNY Buffalo State & Eric Walker Director of Energy Development

USA Palm Desert Energy Independence Program

USA Palm Desert Energy Independence Program Context Palm Desert Energy Independence Program is one of a number of Property Assessed Clean Energy (PACE) Schemes implemented in the United States. Under these

USA Palm Desert Energy Independence Program Context Palm Desert Energy Independence Program is one of a number of Property Assessed Clean Energy (PACE) Schemes implemented in the United States. Under these

Cost effective the present value of the energy saved is more than the cost of the energy package (including maintenance) The maximum mortgage amount

The maximum mortgage amount") What is an EEM Cost effective the present value of the energy saved is more than the cost of the energy package (including maintenance) The maximum mortgage amount for an area can be exceeded by the amount

What is an EEM Cost effective the present value of the energy saved is more than the cost of the energy package (including maintenance) The maximum mortgage amount for an area can be exceeded by the amount

ELEMENTS OF A WELL-DESIGNED C-PACE STATUTE AND PROGRAM TO ATTRACT PRIVATE CAPITAL AND FOSTER GREATER TRANSACTION VOLUMES JANUARY 16, 2018

ELEMENTS OF A WELL-DESIGNED C-PACE STATUTE AND PROGRAM TO ATTRACT PRIVATE CAPITAL AND FOSTER GREATER TRANSACTION VOLUMES JANUARY 16, 2018 OVERVIEW As more states, counties and municipalities launch Commercial

ELEMENTS OF A WELL-DESIGNED C-PACE STATUTE AND PROGRAM TO ATTRACT PRIVATE CAPITAL AND FOSTER GREATER TRANSACTION VOLUMES JANUARY 16, 2018 OVERVIEW As more states, counties and municipalities launch Commercial

GSE Efforts to Improve emortgage Adoption:

GSE Efforts to Improve emortgage Adoption: A Follow-up to the 2016 GSE Survey Findings Report November 2017 1 Joint GSE Follow up Report Background Fannie Mae and Freddie Mac (the GSEs) are working together

GSE Efforts to Improve emortgage Adoption: A Follow-up to the 2016 GSE Survey Findings Report November 2017 1 Joint GSE Follow up Report Background Fannie Mae and Freddie Mac (the GSEs) are working together

Financing Energy Efficiency & Renewable Energy Projects

Financing Energy Efficiency & Renewable Energy Projects Program Concepts & Finance Models for State Governments NGA Center for Best Practices Draft January 4, 2009 Matthew H. Brown - ConoverBrown John

Financing Energy Efficiency & Renewable Energy Projects Program Concepts & Finance Models for State Governments NGA Center for Best Practices Draft January 4, 2009 Matthew H. Brown - ConoverBrown John

IFF Position Description. Title: Managing Director, Credit and Policy. Reports to: Senior Vice President, Capital Solutions.

IFF Position Description Title: Reports to: Department: Department Function: Managing Director, Credit and Policy Senior Vice President, Capital Solutions Capital Solutions Maintain a program of affordable,

IFF Position Description Title: Reports to: Department: Department Function: Managing Director, Credit and Policy Senior Vice President, Capital Solutions Capital Solutions Maintain a program of affordable,

Mortgage Delinquencies and Foreclosures: Hawaii

Mortgage Delinquencies and Foreclosures: Hawaii Craig Nolte Community Development Department Federal Reserve Bank of San Francisco October 16, 2008 Do not cite or reproduce without permission. Overview

Mortgage Delinquencies and Foreclosures: Hawaii Craig Nolte Community Development Department Federal Reserve Bank of San Francisco October 16, 2008 Do not cite or reproduce without permission. Overview

Federal Home Loan Bank of Des Moines

Federal Home Loan Bank of Des Moines 1 AGENDA FHLB System FHLB Des Moines Overview How Members Utilize FHLB Des Moines 2 FHLB System Overview POWER OF PARTNERSHIP 3 FHLB SYSTEM OVERVIEW FHLB STRUCTURE

Federal Home Loan Bank of Des Moines 1 AGENDA FHLB System FHLB Des Moines Overview How Members Utilize FHLB Des Moines 2 FHLB System Overview POWER OF PARTNERSHIP 3 FHLB SYSTEM OVERVIEW FHLB STRUCTURE

The Utility Business Model and Energy Efficiency

The Utility Business Model and Energy Efficiency i Arkansas Sustainable Energy Resources Docket July 15, 2009 Richard Sedano The Regulatory Assistance Project 50 State Street, Suite 3 Montpelier, Vermont

The Utility Business Model and Energy Efficiency i Arkansas Sustainable Energy Resources Docket July 15, 2009 Richard Sedano The Regulatory Assistance Project 50 State Street, Suite 3 Montpelier, Vermont

ELEMENTS OF A WELL-DESIGNED C-PACE STATUTE AND PROGRAM TO ATTRACT PRIVATE CAPITAL AND FOSTER GREATER TRANSACTION VOLUMES JULY 2, 2018

ELEMENTS OF A WELL-DESIGNED C-PACE STATUTE AND PROGRAM TO ATTRACT PRIVATE CAPITAL AND FOSTER GREATER TRANSACTION VOLUMES JULY 2, 2018 OVERVIEW As more states, counties and municipalities launch Commercial

ELEMENTS OF A WELL-DESIGNED C-PACE STATUTE AND PROGRAM TO ATTRACT PRIVATE CAPITAL AND FOSTER GREATER TRANSACTION VOLUMES JULY 2, 2018 OVERVIEW As more states, counties and municipalities launch Commercial

Practical Guide to Home Upgrade Financing Part 1

Practical Guide to Home Upgrade Financing Part 1 February 27, 2014 1 Energy Upgrade California Home Upgrade Energy Upgrade California offers rebates for saving energy and making homes more comfortable

Practical Guide to Home Upgrade Financing Part 1 February 27, 2014 1 Energy Upgrade California Home Upgrade Energy Upgrade California offers rebates for saving energy and making homes more comfortable

Data Release Information Sheet

Data Release Information Sheet Data Summary Dataset name: Global Health Spending 1995-2015 Date of release: April 18, 2018 Summary: Research by the Global Burden of Disease Health Financing Collaborator

Data Release Information Sheet Data Summary Dataset name: Global Health Spending 1995-2015 Date of release: April 18, 2018 Summary: Research by the Global Burden of Disease Health Financing Collaborator

Pay-for-Performance Pilot Conceptual Framework

Pay-for-Performance Pilot Conceptual Framework Home Performance Conference February 14, 2018 What is Pay-for-Performance (P4P)? 2 Simple Idea: Pay for ACTUAL energy savings What is Pay-for-Performance

Pay-for-Performance Pilot Conceptual Framework Home Performance Conference February 14, 2018 What is Pay-for-Performance (P4P)? 2 Simple Idea: Pay for ACTUAL energy savings What is Pay-for-Performance

HMDA / Regulation C Amendments New 1003 Application

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

R - P A C E. Residential Property Assessed Clean Energy: A Primer for State and Local Energy Officials. MARK WOLFE Executive Director June 2017

R - P A C E Residential Property Assessed Clean Energy: A Primer for State and Local Energy Officials MARK WOLFE Executive Director June 2017 Introduction Statistics Program Details Comparisons Opposition

R - P A C E Residential Property Assessed Clean Energy: A Primer for State and Local Energy Officials MARK WOLFE Executive Director June 2017 Introduction Statistics Program Details Comparisons Opposition

Securitizing Reperforming Loans into Agency Mortgage Backed Securities: A Program Primer

Securitizing Reperforming Loans into Agency Mortgage Backed Securities: A Program Primer Fannie Mae recently announced plans to securitize single-family, fixed-rate reperforming loans (RPLs) into Agency

Securitizing Reperforming Loans into Agency Mortgage Backed Securities: A Program Primer Fannie Mae recently announced plans to securitize single-family, fixed-rate reperforming loans (RPLs) into Agency

Identifying, Assessing and Mitigating Potential Redlining Risk

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Identifying, Assessing and Mitigating Potential Redlining Risk Objectives Understanding Potential Redlining Risk Understanding the Reasonable Expected Market Area (REMA) vs CRA Assessment Area Understanding

Whereas, solar energy is an abundant, domestic, renewable, and non-polluting energy resource.

An Act Relating to the Establishment of a Community Solar Program For Vertically-Integrated States Whereas, solar energy is an abundant, domestic, renewable, and non-polluting energy resource. Whereas,

An Act Relating to the Establishment of a Community Solar Program For Vertically-Integrated States Whereas, solar energy is an abundant, domestic, renewable, and non-polluting energy resource. Whereas,

Growing Nevada s Clean Energy Markets Quickly with Green Bank Financing

Growing Nevada s Clean Energy Markets Quickly with Green Bank Financing Jeffrey Schub, Executive Director, CGC Nevada Interim Legislative Committee on Energy November 20, 2015 Exhibit K - ENERGY Document

Growing Nevada s Clean Energy Markets Quickly with Green Bank Financing Jeffrey Schub, Executive Director, CGC Nevada Interim Legislative Committee on Energy November 20, 2015 Exhibit K - ENERGY Document

How CECL Will Impact Your Credit Union & What You Can Do to Prepare For It. Randy C Thompson, Ph.D. TCT Risk Solutions, LLC

Attitude The longer I live, the more I realize the impact of attitude on life. Attitude to me, is more important than facts. It is more important than the past, than education, than money, than circumstances,

Attitude The longer I live, the more I realize the impact of attitude on life. Attitude to me, is more important than facts. It is more important than the past, than education, than money, than circumstances,

Assessing Strategic and Social Impact. Andrew Baldwin, Corporation for Supportive Housing (CSH) Who we are

Who we are") Assessing Strategic and Social Impact Andrew Baldwin, Corporation for Supportive Housing (CSH) Who we are Mission: To advance solutions that use housing as a platform for services to improve the lives

Assessing Strategic and Social Impact Andrew Baldwin, Corporation for Supportive Housing (CSH) Who we are Mission: To advance solutions that use housing as a platform for services to improve the lives

Hub Objective for Today

Hub Objective for Today Set the Stage Threshold Observations Performance Metrics OBF, Act 129 Projects; Cost-Recovery Bill Neutrality Context Existing Programs Scan Experience in other jurisdictions On-Bill

Hub Objective for Today Set the Stage Threshold Observations Performance Metrics OBF, Act 129 Projects; Cost-Recovery Bill Neutrality Context Existing Programs Scan Experience in other jurisdictions On-Bill

Trio is the best solution

Trio is the best solution Why trio exists W H Y T R I O E X I S T S : Here s the reality Approximately 30% of mortgage applicants are denied. The US housing market has high demand for an alternative to

Trio is the best solution Why trio exists W H Y T R I O E X I S T S : Here s the reality Approximately 30% of mortgage applicants are denied. The US housing market has high demand for an alternative to

ABS Research Clearing the Air Addressing Three Misconceptions of PACE

ABS Research Clearing the Air Addressing Three Misconceptions of PACE February 2017 Authors: Phoebe Xu Senior Vice President phoebe.xu@morningstar.com +1 646 560-4562 Stephanie K. Mah Director of Research

ABS Research Clearing the Air Addressing Three Misconceptions of PACE February 2017 Authors: Phoebe Xu Senior Vice President phoebe.xu@morningstar.com +1 646 560-4562 Stephanie K. Mah Director of Research

Vermont Public Service Department. Commercial PACE (Property Assessed Clean Energy) Study

Study") Vermont Public Service Department Commercial PACE (Property Assessed Clean Energy) Study Submitted to the Vermont General Assembly January 15, 2013 Executive Summary As originally designed, Property-Assessed

Vermont Public Service Department Commercial PACE (Property Assessed Clean Energy) Study Submitted to the Vermont General Assembly January 15, 2013 Executive Summary As originally designed, Property-Assessed

Payday Lending in America series (3 reports) Research began in 2011

Research began in 2011") Payday LendinginAmerica America: Policy Solutions www.pewtrusts.org/small loans Pew s Small Dollar Loans Project Payday Lending in America series (3 reports) Research began in 2011 Unique, nationally representative

Payday LendinginAmerica America: Policy Solutions www.pewtrusts.org/small loans Pew s Small Dollar Loans Project Payday Lending in America series (3 reports) Research began in 2011 Unique, nationally representative

A CECL Primer. About CECL

A CECL Primer Introduction The purpose of this paper is to provide a brief overview of Visible Equity s solution to CECL (Current Expected Credit Loss). Many facets of our CECL solution, such as the methods

A CECL Primer Introduction The purpose of this paper is to provide a brief overview of Visible Equity s solution to CECL (Current Expected Credit Loss). Many facets of our CECL solution, such as the methods

SMUD Home Performance Program: Neighborhoods Frequently Asked Questions (FAQs)

") SMUD Home Performance Program: Neighborhoods Frequently Asked Questions (FAQs) THE PROGRAM Q) What is the neighborhood program in a nutshell? A) The Neighborhood program is a simple, low cost, retrofit

SMUD Home Performance Program: Neighborhoods Frequently Asked Questions (FAQs) THE PROGRAM Q) What is the neighborhood program in a nutshell? A) The Neighborhood program is a simple, low cost, retrofit

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics. Key Lending Issues from an Examiner Perspective

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau. April 4, Dear Mr.

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau April 4, 2014 Dear Mr. Silberman, The Assets & Opportunity Network (the Network) is grateful for

David Silberman Associate Director, Research, Markets, and Regulation Consumer Financial Protection Bureau April 4, 2014 Dear Mr. Silberman, The Assets & Opportunity Network (the Network) is grateful for

Macroeconomic Adverse Selection: How Consumer Demand Drives Credit Quality

Macroeconomic Adverse Selection: How Consumer Demand Drives Credit Quality Joseph L. Breeden, CEO breeden@strategicanalytics.com 1999-2010, Strategic Analytics Inc. Preview Using Dual-time Dynamics, we

Macroeconomic Adverse Selection: How Consumer Demand Drives Credit Quality Joseph L. Breeden, CEO breeden@strategicanalytics.com 1999-2010, Strategic Analytics Inc. Preview Using Dual-time Dynamics, we

Residential Mortgage Credit Model

Residential Mortgage Credit Model June 2016 data made beautiful Four Major Components to the Credit Model 1. Transition Model: An idealized roll-rate model with three states: i. Performing (Current, 30-DPD)

Residential Mortgage Credit Model June 2016 data made beautiful Four Major Components to the Credit Model 1. Transition Model: An idealized roll-rate model with three states: i. Performing (Current, 30-DPD)

CCRS Tips Document. Key DoD Travel Shared Reports. November 2009

CCRS Tips Document Key DoD Travel Shared Reports November 2009 Account Activity Text File CD 100T Provides detailed information regarding transaction detail at the individual account level Account Listing

CCRS Tips Document Key DoD Travel Shared Reports November 2009 Account Activity Text File CD 100T Provides detailed information regarding transaction detail at the individual account level Account Listing

OVAE Customized Technical Assistance to States

OVAE Customized Technical Assistance to States Action Plan: Performance Based Funding for Oregon s Perkins Reserve Fund Prepared under contract to MPR Associates, Inc. Office of Vocational and Adult Education,

OVAE Customized Technical Assistance to States Action Plan: Performance Based Funding for Oregon s Perkins Reserve Fund Prepared under contract to MPR Associates, Inc. Office of Vocational and Adult Education,

(U 338-E) 2018 General Rate Case A Workpapers. 3 rd ERRATA. T&D- Grid Modernization SCE-02 Volume 10

2018 General Rate Case A Workpapers. 3 rd ERRATA. T&D- Grid Modernization SCE-02 Volume 10") (U 338-E) 2018 General Rate Case A.16-09-001 Workpapers 3 rd ERRATA T&D- Grid Modernization SCE-02 Volume 10 September 2016 124a Customer Interruption Cost Analysis Results Year 1 Customer Interruption

(U 338-E) 2018 General Rate Case A.16-09-001 Workpapers 3 rd ERRATA T&D- Grid Modernization SCE-02 Volume 10 September 2016 124a Customer Interruption Cost Analysis Results Year 1 Customer Interruption

California Alternative Energy and Advanced Transportation Financing Authority (CAEATFA) Sales and Use Tax Exclusion Program

Sales and Use Tax Exclusion Program") California Alternative Energy and Advanced Transportation Financing Authority (CAEATFA) Sales and Use Tax Exclusion Program Presented by: Melanie Holman, Program Analyst California State Treasurer s Office

California Alternative Energy and Advanced Transportation Financing Authority (CAEATFA) Sales and Use Tax Exclusion Program Presented by: Melanie Holman, Program Analyst California State Treasurer s Office

What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from Recent Fannie Mae Acquisitions

What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from Recent Fannie Mae Acquisitions Qiang Cai and Sarah Shahdad, Economic & Strategic Research Published 4/13/2015 Prospective homebuyers

What is the Mortgage Shopping Experience of Today s Homebuyer? Lessons from Recent Fannie Mae Acquisitions Qiang Cai and Sarah Shahdad, Economic & Strategic Research Published 4/13/2015 Prospective homebuyers

Supplementary Materials for

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Supplementary Materials for Can the US Keep the PACE? A Natural Experiment in Accelerating the Growth of Solar Electricity Nadia Ameli, Mauro Pisu, Daniel

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Supplementary Materials for Can the US Keep the PACE? A Natural Experiment in Accelerating the Growth of Solar Electricity Nadia Ameli, Mauro Pisu, Daniel

Energy Efficient Mortgages and Other Green Financial Products: New Drivers of Economic Development in Rhode Island

Energy Efficient Mortgages and Other Green Financial Products: New Drivers of Economic Development in Rhode Island Rhode Island Infrastructure Summit September 17, 2018 Carrie Gill Rhode Island Office

Energy Efficient Mortgages and Other Green Financial Products: New Drivers of Economic Development in Rhode Island Rhode Island Infrastructure Summit September 17, 2018 Carrie Gill Rhode Island Office

Financing for Energy & Sustainability

Financing for Energy & Sustainability Understanding the CFO and Translating Metrics This resource was completed with support from the Department of Energy s Office of Energy Efficiency and Renewable Energy

Financing for Energy & Sustainability Understanding the CFO and Translating Metrics This resource was completed with support from the Department of Energy s Office of Energy Efficiency and Renewable Energy

Historical Performance of the U.S. ESCO Industry: Results from the NAESCO Project Database

LBNL-46070 Historical Performance of the U.S. ESCO Industry: Results from the NAESCO Project Database C.A. Goldman, P. Juergens, M. Fowlie, J. Osborn & K. Kawamoto,LBNL, Terry Singer, NAESCO Environmental

LBNL-46070 Historical Performance of the U.S. ESCO Industry: Results from the NAESCO Project Database C.A. Goldman, P. Juergens, M. Fowlie, J. Osborn & K. Kawamoto,LBNL, Terry Singer, NAESCO Environmental

Findings from the HB 4050 Predatory Lending Database Pilot Program. Introduction

Findings from the HB 4050 Predatory Lending Database Pilot Program Introduction This report is the result of data collected by 11 HUD-certified Counseling Agencies that participated in the HB 4050 Predatory

Findings from the HB 4050 Predatory Lending Database Pilot Program Introduction This report is the result of data collected by 11 HUD-certified Counseling Agencies that participated in the HB 4050 Predatory

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

FINANCIAL STATEMENT ANALYSIS & RATIO ANALYSIS June 13, 2013 Presented By Mike Ensweiler Director of Business Development Agenda General duties of directors What questions should directors be able to answer

Mortgage Insurance What Have We Learned? (Part 2)

") Mortgage Insurance What Have We Learned? (Part 2) Prepared for: Prepared by: Date: CAS Special Interest Seminar Chicago, IL Michael A. Henk, FCAS, MAAA Consulting Actuary October 1, 2013 Anti-Trust Notice

Mortgage Insurance What Have We Learned? (Part 2) Prepared for: Prepared by: Date: CAS Special Interest Seminar Chicago, IL Michael A. Henk, FCAS, MAAA Consulting Actuary October 1, 2013 Anti-Trust Notice

Community Investments Vol. 11, Issue 1 Counting on Local Capital: Evolution of the Revolving Loan Fund Industry

Community Investments Vol. 11, Issue 1 Counting on Local Capital: Evolution of the Revolving Loan Fund Industry Author(s): Andrea Levere, Vice President, Corporation for Enterprise Development and David

Community Investments Vol. 11, Issue 1 Counting on Local Capital: Evolution of the Revolving Loan Fund Industry Author(s): Andrea Levere, Vice President, Corporation for Enterprise Development and David

EVALUATION, MEASUREMENT & VERIFICATION PLAN. For Hawaii Energy Conservation and Efficiency Programs. Program Year 2010 (July 1, 2010-June 30, 2011)

") EVALUATION, MEASUREMENT & VERIFICATION PLAN For Hawaii Energy Conservation and Efficiency Programs Program Year 2010 (July 1, 2010-June 30, 2011) Activities, Priorities and Schedule 3 March 2011 James

EVALUATION, MEASUREMENT & VERIFICATION PLAN For Hawaii Energy Conservation and Efficiency Programs Program Year 2010 (July 1, 2010-June 30, 2011) Activities, Priorities and Schedule 3 March 2011 James

Case Study Primer Purpose of a Case Study: Practical Uses for a Case Study: UpLift Solutions CDFI Case Study:

Case Study Primer Opportunity Finance Network is the leading national network of community development financial institutions (CDFIs) investing in opportunities that benefit low-income, low-wealth, and

Case Study Primer Opportunity Finance Network is the leading national network of community development financial institutions (CDFIs) investing in opportunities that benefit low-income, low-wealth, and

Evolution of Residential Loan Programs: Building Markets by Reducing Risk & Fostering Collaboration

Evolution of Residential Loan Programs: Building Markets by Reducing Risk & Fostering Collaboration ACEEE Finance Forum May 22, 2018 Connecticut Green Bank Delivering Results for Connecticut Investment

Evolution of Residential Loan Programs: Building Markets by Reducing Risk & Fostering Collaboration ACEEE Finance Forum May 22, 2018 Connecticut Green Bank Delivering Results for Connecticut Investment

Financial Statement Standards and Best Practices

Financial Statement Standards and Best Practices CDFI Financial Statement Working Group October 18, 2013 Why Working Group Got Started Discussion at industry forums about the considerable variation in

Financial Statement Standards and Best Practices CDFI Financial Statement Working Group October 18, 2013 Why Working Group Got Started Discussion at industry forums about the considerable variation in

Mortgage Rates, Household Balance Sheets, and the Real Economy

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

Mortgage Rates, Household Balance Sheets, and the Real Economy Ben Keys University of Chicago Harris Tomasz Piskorski Columbia Business School and NBER Amit Seru Chicago Booth and NBER Vincent Yao Fannie

HomePath Program Guidelines

The following guidelines apply to all DIRECTORS MORTGAGE s HomePath loan programs. All loans must adhere to the criteria of these guidelines. This guide addresses the specific areas needed to facilitate

The following guidelines apply to all DIRECTORS MORTGAGE s HomePath loan programs. All loans must adhere to the criteria of these guidelines. This guide addresses the specific areas needed to facilitate