In summary, the MMR consists of eight main sections:

|

|

|

- Imogen Ryan

- 5 years ago

- Views:

Transcription

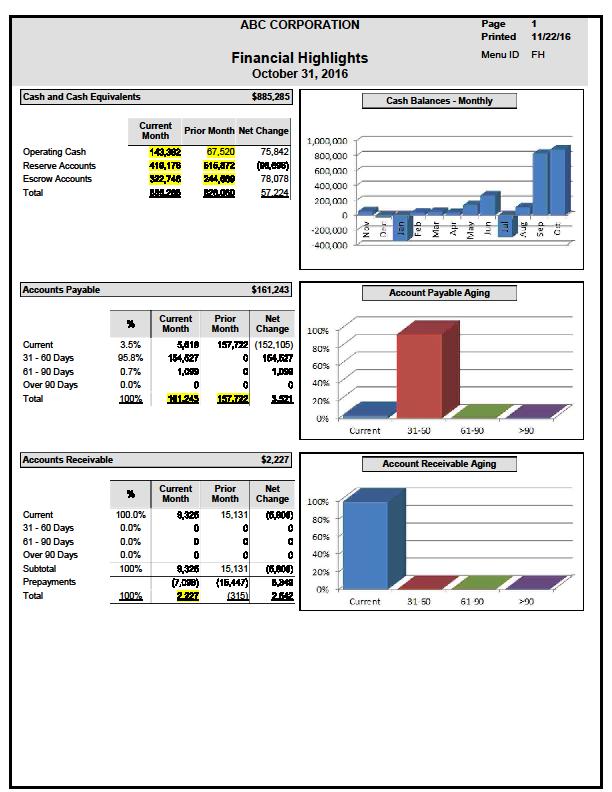

1 Welcome to the Charles H. Greenthal Monthly Management Report (MMR) tutorial. We have created this site as a guide to help you get the most out of your MMR. Please remember we have a team of Financial Analysts who are always available to answer any accounting or financial questions you may have. In summary, the MMR consists of eight main sections: 1. Financial Highlights & Cash (2) 2. Profit & Loss Summary and Detail (2) 3. Monthly Status Current and Past Tenants (2) 4. Aged Delinquency Report Current and Past (2) 5. Detail General Ledger 6. Cash Disbursements by Account 7. Unpaid Invoices 8. Bank Statements 1. A. FINANCIAL HIGHLIGHTS: Three important indicators are reported in this section of MMR. They are the book balances of all bank accounts, accounts payable and accounts receivable. In all three we report the balances at the beginning of the month, the change for the month and the closing balance. As indicated on the reports, these numbers correspond with the detailed ledgers found in sections 1A, 2A&B, 3A&B, 7 and 8. The correlation, especially to the bank statement is a strong indication that all transactions have been recorded and reconciled. The balances also illustrate in a snapshot the company s cash position as well as what it is owed and what it owes. The net of those three numbers, cash + receivables payables is one way to gauge the financial health of the company. If the result is a positive number the company should be able to meet its current obligations. If cash minus payable is positive that is even better. Our objective is to maintain adequate cash flow so that vendors & contractors can be paid in a timely fashion. This requires successful collection efforts and accurate forecasting. B. CASH: This page lists all the company s bank accounts in detail which can be traced back to the Status Report, the Disbursements, the Profit & Loss and the Financial Highlights.

2

3

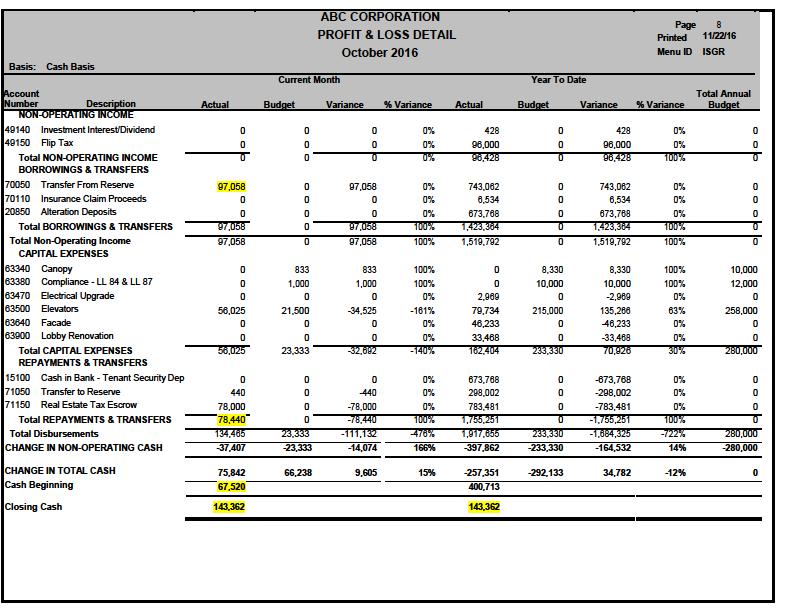

4 2. A&B. PROFIT & LOSS SUMMARY & DETAIL: The profit and Loss Statement is the report that compares actual results of operations to the operating budget. The Summary P&L presents the activity by category and the P&L Detail reports on an account by account basis with account numbers so you can trace the amounts being reported to individual transactions reported in the General Ledger Detail. Following the section in the Profit & Loss Reports where we report results of operations we have included the non operating income and expense items, capital assessments and expenditures, transfers, borrowings and repayments. The reasons for including these transactions which are not typically found in the P&L is to report all transactions that effect cash and thereby tie the closing cash balance in the operating account to the P&L, further enhancing the integrity of the report. The review of the P&L should focus first on the Year To Date variances. As a rule of thumb, a variance greater than $1,000 and 10% should be investigated and communicated to the Manager and Board if corrective action is recommended. Some variances should be investigated regardless of size, for example, Maintenance and Common Charges. Please note that the Profit & Loss Statements are currently prepared on the Cash Basis (Actual column is cash received or disbursed) and the budget is prepared on the Accrual Basis. A Modified Accrual Basis is available.

5

6 3. MONTHLY STATUS CURRENT & PAST TENANTS: There are two Monthly Status Reports, Current Tenants and Past Tenants. They report similar activity including the opening balance, charges, payments received and closing balance. At the end of each report is a summary of activity for the month which combined ties back to the Income section found in the Profit & Loss Statement Detail (Cash Basis).

7 4. AGED DELINQUENCY REPORT CURRENT & PAST TENANTS: These two reports show all tenant accounts with balances due and prepaid. When combined, the totals due in the report summaries ties back to the Accounts Receivable section in the financial highlights.

8 5. DETAIL GENERAL LEDGER: This report (Cash Basis) includes all of the cash transactions for the month in the income, expense, non operating, capital and transfer, borrowing and repayment accounts. It is in general ledger account number order to make it easy to reference to the Profit & Loss Detail.

9 6. CASH DISBURSEMENTS BY ACCOUNT: This report provides the details of each cash disbursement including amount, invoice number, invoice date (date entered into payables),check number, vendor number, payee name and comments. It is presented in general ledger account number order. On the last page of this report is a summary of what was disbursed by general ledger account number.

10 7. UNPAID INVOICES: This reports lists the unpaid invoices, in the system, as of the end of the month. 8. BANK STATEMENTS: Includes the operating account statement and bank reconciliation for the month prior and the reserve account bank statements for the current month.

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

An Auditor s Perspective of NCAA Agreed-Upon Procedures

An Auditor s Perspective of NCAA Agreed-Upon Procedures Ken Kurdziel, Partner Trey Long, Manager James Moore & Company, P.L. NCAA Agreed-Upon Procedures Are they mandatory? Yes the document issued by the

An Auditor s Perspective of NCAA Agreed-Upon Procedures Ken Kurdziel, Partner Trey Long, Manager James Moore & Company, P.L. NCAA Agreed-Upon Procedures Are they mandatory? Yes the document issued by the

Case CMA Doc 161 Filed 01/24/17 Ent. 01/24/17 10:40:57 Pg. 1 of 40

Case 16-15618-CMA Doc 161 Filed 01/24/17 Ent. 01/24/17 10:40:57 Pg. 1 of 40 Case 16-15618-CMA Doc 161 Filed 01/24/17 Ent. 01/24/17 10:40:57 Pg. 2 of 40 Case Number 16-15618 Debtor Door To Door Storage,

Case 16-15618-CMA Doc 161 Filed 01/24/17 Ent. 01/24/17 10:40:57 Pg. 1 of 40 Case 16-15618-CMA Doc 161 Filed 01/24/17 Ent. 01/24/17 10:40:57 Pg. 2 of 40 Case Number 16-15618 Debtor Door To Door Storage,

A Queen s University Production

A Queen s University Production Alternative formats for this presentation can be found on the Financial Services website. For assistance, visit or contact us at: Website: www.queensu.ca/financialservices/support.html

A Queen s University Production Alternative formats for this presentation can be found on the Financial Services website. For assistance, visit or contact us at: Website: www.queensu.ca/financialservices/support.html

BASIS OF ACCOUNTING WHICH ONE SHOULD YOU USE?

Basis of Accounting, in its simplest form, is an accounting term that describes the timing for recording the various financial transactions (e.g., Revenues and Expenses) for your homeowners association.

Basis of Accounting, in its simplest form, is an accounting term that describes the timing for recording the various financial transactions (e.g., Revenues and Expenses) for your homeowners association.

Project Cost Management

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

List of Audit Schedules for FY12

List of Audit Schedules for FY Data PART I - Prior to preliminary fieldwork, email the following: Check Sequences for all accounts Receipt Sequences, if applicable Student Activity Accounts check sequences

List of Audit Schedules for FY Data PART I - Prior to preliminary fieldwork, email the following: Check Sequences for all accounts Receipt Sequences, if applicable Student Activity Accounts check sequences

NOTE: Attach a current Balance Sheet and Income (Profit & Loss) Statement.

Statement.") MONTHLY SCHEDULE OF RECEIPTS AND DISBURSEMENTS (cont d) Detail of Other Receipts and Other Disbursements OTHER RECEIPTS: N/A Describe Each Item of Other Receipt and List Amount of Receipt. Write totals

MONTHLY SCHEDULE OF RECEIPTS AND DISBURSEMENTS (cont d) Detail of Other Receipts and Other Disbursements OTHER RECEIPTS: N/A Describe Each Item of Other Receipt and List Amount of Receipt. Write totals

PROCEDURE FOR PAYING COMMISSION

As orders and invoices are entered into the system, the commission is automatically posted to the commission file at the appropriate time. Priodically, the commission that has been accumulated is reviewed,

As orders and invoices are entered into the system, the commission is automatically posted to the commission file at the appropriate time. Priodically, the commission that has been accumulated is reviewed,

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS 99 100 101 102 CITY OF GEORGETOWN, SOUTH CAROLINA Schedule of Findings and Questioned Costs For the Year Ended June 30, 2008 A. Summary

ADDITIONAL INFORMATION REQUIRED BY GOVERNMENT AUDITING STANDARDS 99 100 101 102 CITY OF GEORGETOWN, SOUTH CAROLINA Schedule of Findings and Questioned Costs For the Year Ended June 30, 2008 A. Summary

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

Annual Report. Page 10 Revenues, Expenditures & Reconciliation

Annual Report Page 10 Revenues, Expenditures & Reconciliation 1 Step 1 Print an Account Activity Report from IFS 2 Review Balance Sheet Accounts on Account Activity Report Check Beginning and Ending Balances

Annual Report Page 10 Revenues, Expenditures & Reconciliation 1 Step 1 Print an Account Activity Report from IFS 2 Review Balance Sheet Accounts on Account Activity Report Check Beginning and Ending Balances

J. Appendix 1. PHFA Supporting Data for Audited Financial Statements

J. Appendix 1 PHFA Supporting Data for Audited Financial Statements - 47 - Accounts and Notes Receivable (Other than from regular tenants) Original Interest Original Balance Name Date Rate Terms Amount

J. Appendix 1 PHFA Supporting Data for Audited Financial Statements - 47 - Accounts and Notes Receivable (Other than from regular tenants) Original Interest Original Balance Name Date Rate Terms Amount

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2014 to June

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2014 to June 30, 2015 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2014 to June 30, 2015 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Introduction... 4 Cash vs Accrual Components of the Balance Sheet How to Get a Snapshot View with Balance Sheet Accounts Ratios...

TABLE OF CONTENTS Introduction... 4 Cash vs Accrual... 5 Components of the Balance Sheet... 6 How to Get a Snapshot View with Balance Sheet Accounts... 7 Ratios... 8 Entrepreneurial Finance: Bonus Ratios

TABLE OF CONTENTS Introduction... 4 Cash vs Accrual... 5 Components of the Balance Sheet... 6 How to Get a Snapshot View with Balance Sheet Accounts... 7 Ratios... 8 Entrepreneurial Finance: Bonus Ratios

ACCOUNTING & BOOKKEEPING ESSENTIALS

ACCOUNTING & BOOKKEEPING ESSENTIALS Prepared by Bruce N. Director, C.P.A. SCORE NYC for New York Public Library Science, Industry & Business Library (SIBL) SIBL SEMINAR OUTLINE I. 10 Common Causes of Business

ACCOUNTING & BOOKKEEPING ESSENTIALS Prepared by Bruce N. Director, C.P.A. SCORE NYC for New York Public Library Science, Industry & Business Library (SIBL) SIBL SEMINAR OUTLINE I. 10 Common Causes of Business

Welcome to the period end closing topic.

Welcome to the period end closing topic. 1 In this course we will discuss how to prepare for and perform period-end closing. 2 Imagine that your company creates an annual financial statement once a year.

Welcome to the period end closing topic. 1 In this course we will discuss how to prepare for and perform period-end closing. 2 Imagine that your company creates an annual financial statement once a year.

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

Make $ Make Nonprofit Essentials Conference August 9, 2016 Minneapolis, MN. Curt Klotz, Finance Director Nonprofits Assistance Fund 2016

Make $ Make 2016 Nonprofit Essentials Conference August 9, 2016 Minneapolis, MN Curt Klotz, Finance Director Nonprofits Assistance Fund 2016 About NAF Nonprofits Assistance Fund invests capital and expertise

Make $ Make 2016 Nonprofit Essentials Conference August 9, 2016 Minneapolis, MN Curt Klotz, Finance Director Nonprofits Assistance Fund 2016 About NAF Nonprofits Assistance Fund invests capital and expertise

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

Chippewa Valley Schools Clinton Township, Michigan. Financial Report with Supplemental Information June 30, 2012

Clinton Township, Michigan Financial Report with Supplemental Information June 30, 2012 Contents Independent Auditor's Report 1-2 Management's Discussion and Analysis 3-12 Basic Financial Statements District-wide

Clinton Township, Michigan Financial Report with Supplemental Information June 30, 2012 Contents Independent Auditor's Report 1-2 Management's Discussion and Analysis 3-12 Basic Financial Statements District-wide

Finance Committee Meeting January 16, :00 pm - Regular Meeting

Finance Committee Meeting January 16, 2018 2:00 pm - Regular Meeting CDA Office, 7645 Currell Blvd., Woodbury 1 BOARD OF COMMISSIONERS WASHINGTON COUNTY COMMUNITY DEVELOPMENT AGENCY WASHINGTON COUNTY,

Finance Committee Meeting January 16, 2018 2:00 pm - Regular Meeting CDA Office, 7645 Currell Blvd., Woodbury 1 BOARD OF COMMISSIONERS WASHINGTON COUNTY COMMUNITY DEVELOPMENT AGENCY WASHINGTON COUNTY,

Internal Accounting Procedures. Approval / Amendments June 24, 2015 (AGM) Amendment 1 Amendment 2

Amendment 1 Amendment 2") Internal Accounting Procedures Approval / Amendments Approval Date June 24, 2015 (AGM) Amendment 1 Amendment 2 This manual addresses Community Futures Big Country Accounting Procedures; its importance

Internal Accounting Procedures Approval / Amendments Approval Date June 24, 2015 (AGM) Amendment 1 Amendment 2 This manual addresses Community Futures Big Country Accounting Procedures; its importance

Financial Health Reporting

Financial Health Reporting Financial Health Reporting Table of Contents Recommended Reports and Accounts to Review 3 Standard List Tools 3 Order Lists 4 Booked Orders List 4 Booked Orders Compare List

Financial Health Reporting Financial Health Reporting Table of Contents Recommended Reports and Accounts to Review 3 Standard List Tools 3 Order Lists 4 Booked Orders List 4 Booked Orders Compare List

Debtors Account Validity Help

Debtors Account Validity Help An Account Validity is run prior to sending out the monthly accounts. This ensures that the correct billing is sent to the Families, if there are any errors they must be corrected

Debtors Account Validity Help An Account Validity is run prior to sending out the monthly accounts. This ensures that the correct billing is sent to the Families, if there are any errors they must be corrected

A Simple Start to Managing Your Business Finances

A Simple Start to Managing Your Business Finances A Guide to the Essentials QB_10/2004_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

A Simple Start to Managing Your Business Finances A Guide to the Essentials QB_10/2004_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

Redford Manor Limited Dividend Housing Association Limited Partnership (a Michigan limited partnership) MSHDA Development No. 1061

MSHDA Development No. 1061") Redford Manor Limited Dividend Housing Association (a Michigan limited partnership) MSHDA Development No. 1061 Financial Report with Additional Information December 31, 2013 MSHDA Development No. 1061

Redford Manor Limited Dividend Housing Association (a Michigan limited partnership) MSHDA Development No. 1061 Financial Report with Additional Information December 31, 2013 MSHDA Development No. 1061

Oakland Woods Limited Dividend Housing Association Limited Partnership. (a Michigan limited partnership) MSHDA Development No.

MSHDA Development No.") Oakland Woods Limited Dividend Housing Association Limited Partnership (a Michigan limited partnership) Financial Report with Additional Information December 31, 2016 Partnership Certification I hereby

Oakland Woods Limited Dividend Housing Association Limited Partnership (a Michigan limited partnership) Financial Report with Additional Information December 31, 2016 Partnership Certification I hereby

Blackman Limited Dividend Housing Association Limited Partnership (a Michigan limited partnership) MSHDA Development No. 3047

MSHDA Development No. 3047") Blackman Limited Dividend Housing Association (a Michigan limited partnership) MSHDA Development No. 3047 Financial Report with Additional Information December 31, 2010 MSHDA Development No. 3047 Partnership

Blackman Limited Dividend Housing Association (a Michigan limited partnership) MSHDA Development No. 3047 Financial Report with Additional Information December 31, 2010 MSHDA Development No. 3047 Partnership

MONTHLY FINANCIAL REPORT FOR CORPORATE OR PARTNERSHIP DEBTOR

UST10 COVER SHEET MONTHLY FINANCIAL REPORT FOR CORPORATE OR PARTNERSHIP DEBTOR Case No. Report Month/Year 1611767CMA Debtor Northwest Territorial Mint, LLC July 2018 INSTRUCTIONS: The debtor s monthly

UST10 COVER SHEET MONTHLY FINANCIAL REPORT FOR CORPORATE OR PARTNERSHIP DEBTOR Case No. Report Month/Year 1611767CMA Debtor Northwest Territorial Mint, LLC July 2018 INSTRUCTIONS: The debtor s monthly

Your Business Finances

ASi Simple Start tto Managing Your Business Finances A Guide to the Essentials QB_05/2005_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

ASi Simple Start tto Managing Your Business Finances A Guide to the Essentials QB_05/2005_01 Financial Management Essentials 1. Introduction to Financial Management 2. Why Accounts are Important 3. Using

STATE OF MARYLAND PETITION FUND REPORT

Page 1 of Pages STATE OF MARYLAND PETITION FUND REPORT Statewide Referendum Petition to: The Secretary of State Public Local Law Referendum to: The Secretary of State Charter Board Petition to: County

Page 1 of Pages STATE OF MARYLAND PETITION FUND REPORT Statewide Referendum Petition to: The Secretary of State Public Local Law Referendum to: The Secretary of State Charter Board Petition to: County

All About the General Ledger

All About the General Ledger Overview In a typical month the main functions under the GL menu (General Ledger) you will use are to verify receipts entered and record them onto deposit slips, reconcile

All About the General Ledger Overview In a typical month the main functions under the GL menu (General Ledger) you will use are to verify receipts entered and record them onto deposit slips, reconcile

Understanding and assessing financial risk. By Dennis A. Kaan

Understanding and assessing financial risk By Dennis A. Kaan While it is impossible to avoid all sources of risk in production agriculture, it can be managed. Exposure to financial risk comes from three

Understanding and assessing financial risk By Dennis A. Kaan While it is impossible to avoid all sources of risk in production agriculture, it can be managed. Exposure to financial risk comes from three

Shareholder Maintenance Worksheet.

Maintenance Income) that the building will receive in the upcoming year. The Total Projected Income is an addition of the Total projected yearly rent, commercial and other income. Shareholder Maintenance

Maintenance Income) that the building will receive in the upcoming year. The Total Projected Income is an addition of the Total projected yearly rent, commercial and other income. Shareholder Maintenance

Financial Statements for the Construction Industry. Understanding the Requirements What are Key Benchmarks

Financial Statements for the Construction Industry Understanding the Requirements What are Key Benchmarks Presented by Marlene Van Sickle, MSM, CPA/CGMA Client Services Director The Mangold Group, CPAs,

Financial Statements for the Construction Industry Understanding the Requirements What are Key Benchmarks Presented by Marlene Van Sickle, MSM, CPA/CGMA Client Services Director The Mangold Group, CPAs,

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent Accountant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2013 to June

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent ant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2013 to June 30, 2014 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For the Period

ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL Independent ant s Report on Applying Agreed-Upon Procedures For the Period from July 1, 2013 to June 30, 2014 ST. BERNARD OF CLAIRVAUX CATHOLIC SCHOOL For the Period

RAMAH WATER AND SANITATION DISTRICT INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES FOR THE YEAR ENDED JUNE 30, 2012

INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES FOR THE YEAR ENDED JUNE 30, 2012 TABLE OF CONTENTS JUNE 30, 2012 Page No. OFFICIAL ROSTER... i INDEPENDENT ACCOUNTANTS REPORT ON APPLYING

INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES FOR THE YEAR ENDED JUNE 30, 2012 TABLE OF CONTENTS JUNE 30, 2012 Page No. OFFICIAL ROSTER... i INDEPENDENT ACCOUNTANTS REPORT ON APPLYING

MONTHLY FINANCIAL REPORT FOR CORPORATE OR PARTNERSHIP DEBTOR

UST10 COVER SHEET MONTHLY FINANCIAL REPORT FOR CORPORATE OR PARTNERSHIP DEBTOR Case No. Report Month/Year 1611767CMA Debtor Northwest Territorial Mint, LLC April 2018 INSTRUCTIONS: The debtor s monthly

UST10 COVER SHEET MONTHLY FINANCIAL REPORT FOR CORPORATE OR PARTNERSHIP DEBTOR Case No. Report Month/Year 1611767CMA Debtor Northwest Territorial Mint, LLC April 2018 INSTRUCTIONS: The debtor s monthly

Financial Statements Demystified. September 9, 2012

Financial Statements Demystified September 9, 2012 Overview of Session Review the types of basic financial statements Review terminology, ratios and indicators of financial well-being Look at what those

Financial Statements Demystified September 9, 2012 Overview of Session Review the types of basic financial statements Review terminology, ratios and indicators of financial well-being Look at what those

Escapia Training Guide

Escapia Training Guide 4: Opening Balances 2014 Homeaway Inc. 1 Class Prerequisites: Prior to attending this session, you will need to compile the following and bring it to the training: Business Opening

Escapia Training Guide 4: Opening Balances 2014 Homeaway Inc. 1 Class Prerequisites: Prior to attending this session, you will need to compile the following and bring it to the training: Business Opening

Oddo Brothers CPAs Certified Public Accountants P.O. Box 68 Fayetteville, GA 30214

Oddo Brothers CPAs Certified Public Accountants P.O. Box 68 Fayetteville, GA 30214 Please print this organizer as your guide and return to us with your work..year-end CHECKLIST for your BUSINESS Using

Oddo Brothers CPAs Certified Public Accountants P.O. Box 68 Fayetteville, GA 30214 Please print this organizer as your guide and return to us with your work..year-end CHECKLIST for your BUSINESS Using

Entering Credit Card Charges

Entering Credit Card Charges Entering Credit Card Charges QuickBooks lets you choose when you enter your credit card charges. You can enter credit card charges when you charge an item or when you receive

Entering Credit Card Charges Entering Credit Card Charges QuickBooks lets you choose when you enter your credit card charges. You can enter credit card charges when you charge an item or when you receive

Account - A record of financial transactions that are similar in terms of a given frame of reference such as purpose, objective, or source.

This section includes definitions of terms used in this guide and additional terms necessary for the understanding of financial accounting procedures for internal funds. Internal funds are defined as all

This section includes definitions of terms used in this guide and additional terms necessary for the understanding of financial accounting procedures for internal funds. Internal funds are defined as all

Example Audit Prepared by Client List Please note that not every item will be relevant for your business. Example File Ref.

Audit Prepared by Client List Please note that not every item will be relevant for your business. Ref Item 1 General Copy of the up-to-date group structure 1.1 Budget/forecasts for the 12 months after

Audit Prepared by Client List Please note that not every item will be relevant for your business. Ref Item 1 General Copy of the up-to-date group structure 1.1 Budget/forecasts for the 12 months after

Why Cash is Different

BY STEVE ANTILL Why do we say cash is king? It s one of the most powerful assets in your company, because it sets the reality for your business every day of your project cycle not just at year-end when

BY STEVE ANTILL Why do we say cash is king? It s one of the most powerful assets in your company, because it sets the reality for your business every day of your project cycle not just at year-end when

GST Report User Guide

GST Report User Guide Created in version 2009.4.0.117 1/9 Table of Contents GST Processing... 2 GST Reports... 4 Balance the GST... 6 Combined Cash GST/Accrual Accounting... 6 Debtors Invoice Report...

GST Report User Guide Created in version 2009.4.0.117 1/9 Table of Contents GST Processing... 2 GST Reports... 4 Balance the GST... 6 Combined Cash GST/Accrual Accounting... 6 Debtors Invoice Report...

Streamlining year-ends

Streamlining year-ends Michael Ford, Intuit TWN Member, Jonathan Carter, 12/5/17 WiFi: QBConnect Password: Connect2017 CPD Process In order to receive CPD credit Be sure to sign in or scan your badge for

Streamlining year-ends Michael Ford, Intuit TWN Member, Jonathan Carter, 12/5/17 WiFi: QBConnect Password: Connect2017 CPD Process In order to receive CPD credit Be sure to sign in or scan your badge for

TOWN OF WINDSOR REDEVELOPMENT SUCCESSOR AGENCY

TOWN OF WINDSOR REDEVELOPMENT SUCCESSOR AGENCY INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES PURSUANT TO AB 1484 (LOW AND MODERATE INCOME HOUSING FUND) INDEPENDENT ACCOUNTANTS REPORT

TOWN OF WINDSOR REDEVELOPMENT SUCCESSOR AGENCY INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES PURSUANT TO AB 1484 (LOW AND MODERATE INCOME HOUSING FUND) INDEPENDENT ACCOUNTANTS REPORT

Session Description. Learning Outcomes BALANCE SHEET ASSETS CURRENT ASSETS. In-Your-Face Financial Statements

In-Your-Face Financial Statements Session Description FEBRUARY 4, 2014 10 11:00 AM Presenter(s): David O Brien, Director of Construction Services // Weber O Brien Ltd., Toledo, OH James Weber // Weber

In-Your-Face Financial Statements Session Description FEBRUARY 4, 2014 10 11:00 AM Presenter(s): David O Brien, Director of Construction Services // Weber O Brien Ltd., Toledo, OH James Weber // Weber

New_SA_GAAP Planning by Reviewed Performed by Final review 11.15

1. General 1.1. A balanced trial balance 1.2. Draft financial statements 1.3. Copies of minutes and resolutions not yet pasted into the minute books including those in the process of being signed. Statutory

1. General 1.1. A balanced trial balance 1.2. Draft financial statements 1.3. Copies of minutes and resolutions not yet pasted into the minute books including those in the process of being signed. Statutory

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Week 2, Completing the accounting cycle. 1/5

Week 2 Horngren, Chapter 4, including the appendix, Completing the accounting cycle. In this chapter we will be using the full accounting worksheet to complete the accounting cycle. The learning objectives

Week 2 Horngren, Chapter 4, including the appendix, Completing the accounting cycle. In this chapter we will be using the full accounting worksheet to complete the accounting cycle. The learning objectives

POHNPEI FISHERIES CORPORATION FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT YEARS ENDED SEPTEMBER 30, 2000, 1999 AND 1998 Deloitte & Touche LLP 361 South Marine Drive Tamuning, Guam 96913-3911 Tel: (671)646-3884 Fax: (671)649-4932

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT YEARS ENDED SEPTEMBER 30, 2000, 1999 AND 1998 Deloitte & Touche LLP 361 South Marine Drive Tamuning, Guam 96913-3911 Tel: (671)646-3884 Fax: (671)649-4932

Chapter 9. #17 is a bad question if it is changed as follows the answer is d

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

Chapter 9 Multiple choice 1. a 2. d 3. b 4. d 5. b 6. b 7. d 8. c 9. b 10. b 11. b 12. c 13. d 14. b 15. b 16. c #17 is a bad question if it is changed as follows the answer is d 17. The audit of accounts

BLUEWATER ACRES DOMESTIC WATER USERS ASSOCIATION INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES FOR THE YEAR ENDED JUNE 30, 2015

BLUEWATER ACRES DOMESTIC WATER USERS ASSOCIATION INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES FOR THE YEAR ENDED JUNE 30, 2015 BLUEWATER ACRES DOMESTIC WATER USERS ASSOCIATION TABLE

BLUEWATER ACRES DOMESTIC WATER USERS ASSOCIATION INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES FOR THE YEAR ENDED JUNE 30, 2015 BLUEWATER ACRES DOMESTIC WATER USERS ASSOCIATION TABLE

CREIA ACCOUNTING POLICIES AND PROCEDURES

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

Liabilities at July 31, 2016 Loan from CRF $24, Outstanding amount from page 2

For the period April 1, 2016 to July 31, 2016 Balance Sheet Contingency Operating Reserve Assets at July 31, 2016 Fund (OF) Fund(CRF) Petty Cash $300.00 Bank available funds $5,501.58 $149,315.52 From

For the period April 1, 2016 to July 31, 2016 Balance Sheet Contingency Operating Reserve Assets at July 31, 2016 Fund (OF) Fund(CRF) Petty Cash $300.00 Bank available funds $5,501.58 $149,315.52 From

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Sage UBS Accounting Sample Report. Sage UBS Accounting. Sample Report 1.0. VIVID SOLUTIONS SDN BHD

Sage UBS Accounting Sample Report 1.0 www.vivid.com.my 1 Contents Chapter 1: Debtors... 6 1.1: Chart of Account... 6 1.2: Tax Code Maintenance... 6 1.3: Debtors Listing... 7 1.4: Print Labels... 7 1.5:

Sage UBS Accounting Sample Report 1.0 www.vivid.com.my 1 Contents Chapter 1: Debtors... 6 1.1: Chart of Account... 6 1.2: Tax Code Maintenance... 6 1.3: Debtors Listing... 7 1.4: Print Labels... 7 1.5:

Visual Cash Focus - User Tip 16

Visual Cash Focus - User Tip 16 What are Cash Flow profiles and how do I modify them? Background Cash Focus uses a double entry accounting engine to simultaneously build the profit & loss, balance sheet

Visual Cash Focus - User Tip 16 What are Cash Flow profiles and how do I modify them? Background Cash Focus uses a double entry accounting engine to simultaneously build the profit & loss, balance sheet

STATE OF NEW MEXICO VILLAGE OF VIRDEN Independent Accountants Report on Applying Agreed-Upon Procedures

Independent Accountants Report on Applying Agreed-Upon Procedures For the Year Ended June 30, 2010 Harshwal & Company LLP Certified Public Accountants 500 Marquette Avenue NW, Suite 280 Albuquerque, NM

Independent Accountants Report on Applying Agreed-Upon Procedures For the Year Ended June 30, 2010 Harshwal & Company LLP Certified Public Accountants 500 Marquette Avenue NW, Suite 280 Albuquerque, NM

City of Bingham. Cumulative Problem. For use with McGraw-Hill/Irwin Accounting for Governmental and Nonprofit Entities, 13 th Edition

City of Bingham Cumulative Problem For use with McGraw-Hill/Irwin Accounting for Governmental and Nonprofit Entities, 13 th Edition By Earl R. Wilson and Susan C. Kattelus Table of Contents Foreword 1

City of Bingham Cumulative Problem For use with McGraw-Hill/Irwin Accounting for Governmental and Nonprofit Entities, 13 th Edition By Earl R. Wilson and Susan C. Kattelus Table of Contents Foreword 1

Completed by Initials Date

Example Co-operative Limited Audit Requirements Year Ending 30 th June 2009 AUDIT INFORMATION REQUIRED General Trial balance with account numbers in excel format for the year ended 30 th June 2009 Reconciliations

Example Co-operative Limited Audit Requirements Year Ending 30 th June 2009 AUDIT INFORMATION REQUIRED General Trial balance with account numbers in excel format for the year ended 30 th June 2009 Reconciliations

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Accounting System Requirements

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Agricultural Accounting

Agricultural Accounting Steven M. Bragg Chapter 1 Introduction to Agricultural Accounting... 1 Learning Objectives... 1 Introduction... 1 A Note on Terminology... 1 The Economic Entity Concept... 1 Financial

Agricultural Accounting Steven M. Bragg Chapter 1 Introduction to Agricultural Accounting... 1 Learning Objectives... 1 Introduction... 1 A Note on Terminology... 1 The Economic Entity Concept... 1 Financial

CHAPTER 7 General Journal Entries

ing Manual for Public School Districts CHAPTER 7 Journal Entries Table of Contents Page INTRODUCTION... 1 JOURNAL ENTRIES... 2 Opening Entries... 2 Fiscal Year Opening Entry All Funds Except Fiduciary

ing Manual for Public School Districts CHAPTER 7 Journal Entries Table of Contents Page INTRODUCTION... 1 JOURNAL ENTRIES... 2 Opening Entries... 2 Fiscal Year Opening Entry All Funds Except Fiduciary

DRAFT FOR PUBLIC COMMENT

CITY OF IMPERIAL SUCCESSOR AGENCY FOR THE FORMER REDEVELOPMENT AGENCY DUE DILIGENCE REVIEW PURSUANT TO AB1484 LOW AND MODERATE INCOME HOUSING FUND TABLE OF CONTENTS INDEPENDENT ACCOUNTANTS REPORT 3 ATTACHMENT

CITY OF IMPERIAL SUCCESSOR AGENCY FOR THE FORMER REDEVELOPMENT AGENCY DUE DILIGENCE REVIEW PURSUANT TO AB1484 LOW AND MODERATE INCOME HOUSING FUND TABLE OF CONTENTS INDEPENDENT ACCOUNTANTS REPORT 3 ATTACHMENT

Australian Hardware. Financial Management Policies & Procedures Manual

Australian Hardware Financial Management Policies & Procedures Manual Wollongong Store This document sets out Australian Hardware policies and procedures that are to be adhered to by owners, managers and

Australian Hardware Financial Management Policies & Procedures Manual Wollongong Store This document sets out Australian Hardware policies and procedures that are to be adhered to by owners, managers and

Name Neighborhood Association

Include neighborhood background, if desired. Include neighborhood association background, if desired. This audit program is only a guide and is not intended to replace the auditors judgment. The audit

Include neighborhood background, if desired. Include neighborhood association background, if desired. This audit program is only a guide and is not intended to replace the auditors judgment. The audit

CITY OF SCHENECTADY INDUSTRIAL DEVELOPMENT AGENCY (A New York Public Authority)

") FINANCIAL STATEMENTS - STATUTORY BASIS and INDEPENDENT AUDITOR S REPORT December 31, 2009 FINANCIAL STATEMENTS - STATUTORY BASIS and INDEPENDENT AUDITOR S REPORT December 31, 2009 C O N T E N T S INDEPENDENT

FINANCIAL STATEMENTS - STATUTORY BASIS and INDEPENDENT AUDITOR S REPORT December 31, 2009 FINANCIAL STATEMENTS - STATUTORY BASIS and INDEPENDENT AUDITOR S REPORT December 31, 2009 C O N T E N T S INDEPENDENT

Construction Accounting

Construction Accounting Steven M. Bragg Chapter 1 Overview of the Construction Industry... 1 Learning Objectives... 1 Introduction... 1 Nature of the Construction Contractor... 2 Bonding Requirements...

Construction Accounting Steven M. Bragg Chapter 1 Overview of the Construction Industry... 1 Learning Objectives... 1 Introduction... 1 Nature of the Construction Contractor... 2 Bonding Requirements...

YEAR END CLOSE. A guide to closing the year using NAV2013 R2

YEAR END CLOSE A guide to closing the year using NAV2013 R2 My name is Michael Carr CPA and I am Vice President, Finance of Philadelphia Scientific LLC a small family owned light manufacturer and designer

YEAR END CLOSE A guide to closing the year using NAV2013 R2 My name is Michael Carr CPA and I am Vice President, Finance of Philadelphia Scientific LLC a small family owned light manufacturer and designer

Collectors Work Queue

Collectors Work Queue Credit control is a vital process that establishes controls both pre and post sales to ensure a timely recovery of income owed to the University. Many factors need to be taken into

Collectors Work Queue Credit control is a vital process that establishes controls both pre and post sales to ensure a timely recovery of income owed to the University. Many factors need to be taken into

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Audit Program for Cash

Form AP 10 Index Reference Audit Program for Cash Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Form AP 10 Index Reference Audit Program for Cash Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Advantage Multiple Currency Support Current Procedures

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate

Advantage Multiple Currency Support Current Procedures Overview: This document explains how to process multiple currencies in a single database; how to convert to a HOME currency and how to consolidate

U.S. Department of Labor Office of Labor-Management Standards (OLMS) Condu... Page 1 of 32 E-mail This Page Office of Labor-Management Standards (OLMS) Conducting Audits in Small Unions A Guide for Trustees

U.S. Department of Labor Office of Labor-Management Standards (OLMS) Condu... Page 1 of 32 E-mail This Page Office of Labor-Management Standards (OLMS) Conducting Audits in Small Unions A Guide for Trustees

RICHLAND COUNTY, OHIO

SANDUSKY TOWNSHIP RICHLAND COUNTY, OHIO AGREED UPON PROCEDURES For the Years Ended December 31, 2016 and 2015 Board of Trustees 5201 Hook Road Crestline, Ohio 44827 We have reviewed the Independent Accountant

SANDUSKY TOWNSHIP RICHLAND COUNTY, OHIO AGREED UPON PROCEDURES For the Years Ended December 31, 2016 and 2015 Board of Trustees 5201 Hook Road Crestline, Ohio 44827 We have reviewed the Independent Accountant

Activant Prophet 21. Cash and Bank Reconciliation

Activant Prophet 21 Cash and Bank Reconciliation This class is designed for Customers who want to learn the Bank Reconciliation feature to facilitate balancing deposits and disbursements to your bank statement.

Activant Prophet 21 Cash and Bank Reconciliation This class is designed for Customers who want to learn the Bank Reconciliation feature to facilitate balancing deposits and disbursements to your bank statement.

Sample Fiscal Policies & Procedures Manual

Sample Fiscal Policies & Procedures Manual Legal Disclaimer Please note that TREC does not provide legal advice. This sample Fiscal Policies and Procedures Manual discusses a topic of general interest

Sample Fiscal Policies & Procedures Manual Legal Disclaimer Please note that TREC does not provide legal advice. This sample Fiscal Policies and Procedures Manual discusses a topic of general interest

FINANCIAL REVIEW CHECKLIST

FINANCIAL REVIEW CHECKLIST PRESBYTERIAN CHURCH For the Fiscal Year Ended Date Committee Member s Signature Reconciliation of Bank & Investment Accounts Operating bank account # Month Bank account # Month

FINANCIAL REVIEW CHECKLIST PRESBYTERIAN CHURCH For the Fiscal Year Ended Date Committee Member s Signature Reconciliation of Bank & Investment Accounts Operating bank account # Month Bank account # Month

Financial Accounting

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

Drawings Assets expenses Capital Income Liabilities - Drawings - Capital - Assets - Income - Expenses - Liabilities Dt (Increases) Cr (Increases) Cr (decreases) Dt (decreases) Financial Accounting Financial

BUSINESS FINANCIAL BASICS

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

STATE OF NEW MEXICO Socorro Soil and Water Conservation District. Independent Accountant s Report on Applying Agreed-Upon Procedures (TIER 4)

") STATE OF NEW MEXICO Independent Accountant s Report on Applying Agreed-Upon Procedures (TIER 4) For the Fiscal Year Ended June 30, 2016 ASSURANCE TAX ACCOUNTING PC Office: (505) 620-8526 Financial Audits

STATE OF NEW MEXICO Independent Accountant s Report on Applying Agreed-Upon Procedures (TIER 4) For the Fiscal Year Ended June 30, 2016 ASSURANCE TAX ACCOUNTING PC Office: (505) 620-8526 Financial Audits

MSI Accounts Payable Version 5.0 Treasurer s Report Processing

MSI Accounts Payable Version 5.0 Treasurer s Report Processing User s Guide Municipal Software, Inc. 1850 W. Winchester Road, Ste 209 Libertyville, IL 60048 Phone: (847) 362-2803 Fax: (847) 362-3347 Contents

MSI Accounts Payable Version 5.0 Treasurer s Report Processing User s Guide Municipal Software, Inc. 1850 W. Winchester Road, Ste 209 Libertyville, IL 60048 Phone: (847) 362-2803 Fax: (847) 362-3347 Contents

Crusader Energy Group Inc. Cover Sheet to Monthly Operating Report June 1, 2009 through June 30, 2009

Crusader Energy Group Inc. Cover Sheet to Monthly Operating Report June 1, 2009 through June 30, 2009 Given the nature and format of the monthly operating reports, certain information concerning the assets

Crusader Energy Group Inc. Cover Sheet to Monthly Operating Report June 1, 2009 through June 30, 2009 Given the nature and format of the monthly operating reports, certain information concerning the assets

Activant Prophet 21 Overview of Prophet 21 version 11 New Features: Accounting

Activant Prophet 21 Overview of Prophet 21 version 11 New Features: Accounting Overview of Prophet 21 v11 New Features suite Course: 3 of 3 This class is designed for Accounting Personnel Accounts Payable

Activant Prophet 21 Overview of Prophet 21 version 11 New Features: Accounting Overview of Prophet 21 v11 New Features suite Course: 3 of 3 This class is designed for Accounting Personnel Accounts Payable

INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES

INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES 4215 County Road 23 Burgoon, Ohio 43407 We have performed the procedures enumerated below, which were agreed to by the Board of Trustees

INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED-UPON PROCEDURES 4215 County Road 23 Burgoon, Ohio 43407 We have performed the procedures enumerated below, which were agreed to by the Board of Trustees

List of deliverables. GEYSER & DU PLESSIS Geregistreerde Rekenmeesters & Ouditeure Registered Accountants & Auditors

GEYSER & DU PLESSIS Geregistreerde Rekenmeesters & Ouditeure Registered Accountants & Auditors List of deliverables This document contains a guideline of documents that the engagement team will need from

GEYSER & DU PLESSIS Geregistreerde Rekenmeesters & Ouditeure Registered Accountants & Auditors List of deliverables This document contains a guideline of documents that the engagement team will need from

Rocco Sabino MBA, CPA

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

SEAGATE TECHNOLOGY PLC CONDENSED CONSOLIDATED BALANCE SHEETS

CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) ASSETS 2013 (a) Current assets: Cash and cash equivalents $ 2,634 $ 1,708 Short-term investments 20 480 Restricted cash and investments 4 101 Accounts

CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) ASSETS 2013 (a) Current assets: Cash and cash equivalents $ 2,634 $ 1,708 Short-term investments 20 480 Restricted cash and investments 4 101 Accounts

The Springs at Santa Rita Homeowners Association. Fiscal Policies and Procedures

The Springs at Santa Rita Homeowners Association Fiscal Policies and Procedures Table of Contents Accounting Procedures... 1 Basis of Accounting... 1 Journal Entries... 1 Bank Reconciliations... 1 Internal

The Springs at Santa Rita Homeowners Association Fiscal Policies and Procedures Table of Contents Accounting Procedures... 1 Basis of Accounting... 1 Journal Entries... 1 Bank Reconciliations... 1 Internal

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Chapter 2: Overview. Analyzing and Recording Business Transactions

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Financial Accounting 4th Edition Kemp SOLUTIONS MANUAL Full download at: Financial Accounting 4th Edition Kemp TEST BANK Full download at: https://testbankreal.com/download/financial-accounting-4th-edition-kempsolutions-manual-2/

Bookkeeping (Explanation)

") Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and

Bookkeeping (Explanation) 1. Part 1 Introduction; Bookkeeping: Past and Present 2. Part 2 Accrual Method 3. Part 3 Double-Entry, Debits and Credits 4. Part 4 General Ledger Accounts 5. Part 5 Debits and