Chapter 11. Economic Analysis of Banking Regulation

|

|

|

- Kathleen Alexander

- 5 years ago

- Views:

Transcription

1 Chapter 11 Economic Analysis of Banking Regulation

2 Asymmetric Information and Bank Regulation Government safety net: Deposit insurance and the FDIC Short circuits bank failures and contagion effect Payoff method Purchase and assumption method Moral Hazard Depositors do not impose discipline of marketplace Banks have an incentive to take on greater risk Adverse Selection Risk-lovers find banking attractive Depositors have little reason to monitor bank Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-2

3 Too Big to Fail Government provides guarantees of repayment to large uninsured creditors of the largest banks even when they are not entitled to this guarantee Uses the purchase and assumption method Increases moral hazard incentives for big banks Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-3

4 Financial Consolidation Larger and more complex banking organizations challenge regulation Increased too big to fail problem Extends safety net to new activities, increasing incentives for risk taking in these areas Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-4

5 Restrictions on Asset Holding and Bank Capital Requirements Attempts to restrict banks from too much risk taking Promote diversification Prohibit holdings of common stock Set capital requirements Minimum leverage ratio Basel Accord: risk-based capital requirements Regulatory arbitrage Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-5

6 Bank (Prudential) Supervision: Chartering and Examination Chartering (screening of proposals to open new banks) to prevent adverse selection Examinations (scheduled and unscheduled) to monitor capital requirements and restrictions on asset holding to prevent moral hazard Capital adequacy Asset quality Management Earnings Liquidity Sensitivity to market risk Filing periodic call reports Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-6

7 Assessment of Risk Management Greater emphasis on evaluating soundness of management processes for controlling risk Trading Activities Manual of 1994 for risk management rating based on Quality of oversight provided Adequacy of policies and limits Quality of the risk measurement and monitoring systems Adequacy of internal controls Interest-rate risk limits Internal policies and procedures Internal management and monitoring Implementation of stress testing and Value-at risk (VAR) Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-7

8 Disclosure Requirements Requirements to adhere to standard accounting principles and to disclose wide range of information Eurocurrency Standing Committee of the G-10 Central Banks also recommends estimates of financial risk generated by the firm s internal monitoring system be adapted for public disclosure Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-8

9 Consumer Protection Truth-in-lending mandated under the Consumer Protection Act of 1969 Fair Credit Billing Act of 1974 Equal Credit Opportunity Act of 1974, extended in 1976 Community Reinvestment Act Copyright 2007 Pearson Addison-Wesley. All rights reserved. 11-9

10 Restrictions on Competition Justified by moral hazard incentives to take on more risk as competition decreases profitability Branching restrictions (eliminated in 1994) Glass-Steagall Act (repeated in 1999) Disadvantages Higher consumer charges Decreased efficiency Copyright 2007 Pearson Addison-Wesley. All rights reserved

11 Copyright 2007 Pearson Addison-Wesley. All rights reserved

12 Copyright 2007 Pearson Addison-Wesley. All rights reserved

13 Copyright 2007 Pearson Addison-Wesley. All rights reserved

14 International Banking Regulation Similar to U.S. Chartered and supervised Deposit insurance Capital requirement Particular problems Easy to shift operations from one country to another Unclear jurisdiction lines Copyright 2007 Pearson Addison-Wesley. All rights reserved

15 Regulation Applies to a moving target Calls for resources and expertise Details are important Political pressures Copyright 2007 Pearson Addison-Wesley. All rights reserved

16 Copyright 2007 Pearson Addison-Wesley. All rights reserved

17 1980s S&L and Banking Crisis Financial innovation and new financial instruments increasing risk taking Increased deposit insurance led to increased moral hazard Deregulation Depository Institutions Deregulation and Monetary Control Act of 1980 Depository Institutions Act of 1982 Copyright 2007 Pearson Addison-Wesley. All rights reserved

18 1980s S&L and Banking Crisis (cont d) Managers did not have expertise in managing risk Rapid growth in new lending, real estate in particular Activities expanded in scope; regulators at FSLIC did not have expertise or resources High interest rates and recession increased incentives for moral hazard Copyright 2007 Pearson Addison-Wesley. All rights reserved

19 1980s S&L and Banking Crisis: Later Stages Regulatory forbearance by FSLIC Insufficient funds to close insolvent S&Ls Established to encourage growth Did not want to admit agency was in trouble Zombie S&Ls taking on high risk projects and attracting business from healthy S&Ls Competitive Equality in Banking Act of 1987 Inadequate funding Continued forbearance Copyright 2007 Pearson Addison-Wesley. All rights reserved

20 Principal-Agent Problem for Regulators and Politicians Agents for voters-taxpayers Regulators Wish to escape blame (bureaucratic gambling) Want to protect careers Passage of legislation to deregulate Shortage of funds and staff Politicians Lobbied by S&L interests Necessity of campaign contributions for expensive political races Copyright 2007 Pearson Addison-Wesley. All rights reserved

21 The Financial Institutions Reform, Recovery, and Enforcement Act of 1989 Regulatory apparatus restructured Federal Home Loan Bank Board relegated to the OTS FSLIC given to the FDIC RTC established to manage and resolve insolvent thrifts Cost of the bailout approximately $150 billion Re-restricted asset choices Copyright 2007 Pearson Addison-Wesley. All rights reserved

22 The Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (cont d) Increased core-capital leverage requirements Imposed same risk-based capital standards as those on commercial banks Enhanced enforcement powers of regulators Did not focus on underlying moral hazard and adverse selection problems Copyright 2007 Pearson Addison-Wesley. All rights reserved

23 Federal Deposit Insurance Corporation Improvement Act of 1991 Recapitalize the Bank Insurance Fund Increase ability to borrow from the Treasury Higher deposit insurance premiums until the loans could be paid back and reserves of 1.25% of insured deposits maintained Reform the deposit insurance and regulatory system to minimize taxpayer losses Too-big-to-fail policy substantially limited Prompt corrective action provisions Risk-based insurance premiums Copyright 2007 Pearson Addison-Wesley. All rights reserved

24 Copyright 2007 Pearson Addison-Wesley. All rights reserved

25 Copyright 2007 Pearson Addison-Wesley. All rights reserved

26 Copyright 2007 Pearson Addison-Wesley. All rights reserved

27 Copyright 2007 Pearson Addison-Wesley. All rights reserved

28 Deja Vu It is the existence of a government safety net that increases moral hazard incentives for excessive risk taking on the part of banks Copyright 2007 Pearson Addison-Wesley. All rights reserved

International Finance

International Finance FINA 5331 Lecture 3: The Banking System William J. Crowder Ph.D. Historical Development of the Banking System Bank of North America chartered in 1782 Controversy over the chartering

International Finance FINA 5331 Lecture 3: The Banking System William J. Crowder Ph.D. Historical Development of the Banking System Bank of North America chartered in 1782 Controversy over the chartering

1) Depositors lack of information about the quality of bank assets can lead to. A) bank panics B) bank booms C) sequencing D) asset transformation

Depositors lack of information about the quality of bank assets can lead to. A) bank panics B) bank booms C) sequencing D) asset transformation") Chapter 11 Economic Analysis of Banking Regulation 11.1 Asymmetric Information and Banking Regulation 1) Depositors lack of information about the quality of bank assets can lead to. A) bank panics B) bank

Chapter 11 Economic Analysis of Banking Regulation 11.1 Asymmetric Information and Banking Regulation 1) Depositors lack of information about the quality of bank assets can lead to. A) bank panics B) bank

Write your answers on the exam paper. You are encouraged to write comments on the exam paper as well.

Econ 353 Money, Banking and Financial Markets Summer 2008 Exam 3 Name ID # Note: Questions 1-20 worth 4 points each; Questions 21 worth 20 points; Write your answers on the exam paper. You are encouraged

Econ 353 Money, Banking and Financial Markets Summer 2008 Exam 3 Name ID # Note: Questions 1-20 worth 4 points each; Questions 21 worth 20 points; Write your answers on the exam paper. You are encouraged

Chapter 18. Financial Regulation. Chapter Preview

Chapter 18 Financial Regulation Chapter Preview The financial system is one of the most heavily regulated industries in our economy. In this chapter, we develop an economic analysis of why regulation of

Chapter 18 Financial Regulation Chapter Preview The financial system is one of the most heavily regulated industries in our economy. In this chapter, we develop an economic analysis of why regulation of

Chapter 2: Government Policies and Regulation Test Bank Solutions Principles of Bank Management 8th Edition by Koch Multiple Choice

Chapter 2: Government Policies and Regulation Test Bank Solutions Principles of Bank Management 8th Edition by Koch Multiple Choice 1. Historically, a commercial bank was defined as a firm that: a. accepted

Chapter 2: Government Policies and Regulation Test Bank Solutions Principles of Bank Management 8th Edition by Koch Multiple Choice 1. Historically, a commercial bank was defined as a firm that: a. accepted

Chapter 02 Financial Services: Depository Institutions

Financial Institutions Management A Risk Management Approach 9th Edition Saunders Test Bank Full Download: http://testbanklive.com/download/financial-institutions-management-a-risk-management-approach-9th-edition-sau

Financial Institutions Management A Risk Management Approach 9th Edition Saunders Test Bank Full Download: http://testbanklive.com/download/financial-institutions-management-a-risk-management-approach-9th-edition-sau

Chapter 2 Government Policies and Regulation

Chapter 2 Government Policies and Regulation Multiple Choice 1. Historically, a commercial bank was defined as a firm that: a. accepted NOW accounts and made consumer loans. b. accepted demand deposits

Chapter 2 Government Policies and Regulation Multiple Choice 1. Historically, a commercial bank was defined as a firm that: a. accepted NOW accounts and made consumer loans. b. accepted demand deposits

16. Because of the large amount of equity on a typical commercial bank balance sheet, credit risk is not a significant risk to bank managers.

ch2 Student: 1. In recent years, the number of commercial banks in the U.S. has been increasing. 2. Most of the change in the number of commercial banks since 1990 has been due to bank failures. 3. Commercial

ch2 Student: 1. In recent years, the number of commercial banks in the U.S. has been increasing. 2. Most of the change in the number of commercial banks since 1990 has been due to bank failures. 3. Commercial

Chapter Fourteen. Chapter 10 Regulating the Financial System 5/6/2018. Financial Crisis

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Overview of financial regulation

Last updated February 1, 2018 Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz 2/25 Outline Purpose of financial regulation

Last updated February 1, 2018 Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz 2/25 Outline Purpose of financial regulation

Chapter 9. Banking and the Management of Financial Institutions

Chapter 9 Banking and the Management of Financial Institutions Copyright 2007 Pearson Addison-Wesley. All rights reserved. 9-2 Basic Banking Cash Deposit First National Bank First National Bank Assets

Chapter 9 Banking and the Management of Financial Institutions Copyright 2007 Pearson Addison-Wesley. All rights reserved. 9-2 Basic Banking Cash Deposit First National Bank First National Bank Assets

Following a decade of neglect, the Bush administration and Congress moved

Journal of Economic Perspectives Volume 3, Number 4 Fall 1989 Pages 3 9 Symposium on Federal Deposit Insurance for S&L Institutions Dwight M. Jaffee Following a decade of neglect, the Bush administration

Journal of Economic Perspectives Volume 3, Number 4 Fall 1989 Pages 3 9 Symposium on Federal Deposit Insurance for S&L Institutions Dwight M. Jaffee Following a decade of neglect, the Bush administration

Notes on Mishkin Chapters 11/12: Part A U.S. Banking Structure & History. Leigh Tesfatsion

Notes on Mishkin Chapters 11/12: Part A U.S. Banking Structure & History Presenter: Leigh Tesfatsion Professor of Econ, Math, and ECpE Department of Economics Iowa State University Ames, Iowa 50011-1070

Notes on Mishkin Chapters 11/12: Part A U.S. Banking Structure & History Presenter: Leigh Tesfatsion Professor of Econ, Math, and ECpE Department of Economics Iowa State University Ames, Iowa 50011-1070

Dodd-Frank Act Section PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES. [As amended by Omnibus Spending Bill]

![Dodd-Frank Act Section PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES. [As amended by Omnibus Spending Bill]](/thumbs/89/98384633.jpg "Dodd-Frank Act Section PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES. [As amended by Omnibus Spending Bill]") Dodd-Frank Act Section 716 -- PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES. [As amended by Omnibus Spending Bill] (a) PROHIBITION ON FEDERAL ASSISTANCE. Notwithstanding any other provision

Dodd-Frank Act Section 716 -- PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES. [As amended by Omnibus Spending Bill] (a) PROHIBITION ON FEDERAL ASSISTANCE. Notwithstanding any other provision

Introduction. Learning Objectives. Learning Objectives. Economics Today Twelfth Edition. Chapter 15 Money Creation and Deposit Insurance

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 15 Money Creation and Deposit Insurance Introduction A quick response by the Federal Reserve to the September 11, 2001 terrorist attacks stabilized

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 15 Money Creation and Deposit Insurance Introduction A quick response by the Federal Reserve to the September 11, 2001 terrorist attacks stabilized

Chapter 20 (9) Financial Globalization: Opportunity and Crisis

Financial Globalization: Opportunity and Crisis") Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Purpose and Structure: Banks and Regulatory Agencies. 2013, Cerfis Group, Inc.

Bank Operations Institute Dallas, Texas October 13, 2013 Purpose and Structure: Banks and Regulatory Agencies Financial Intermediaries Commercial banks (community) Thrifts Savings banks Savings and Loans

Bank Operations Institute Dallas, Texas October 13, 2013 Purpose and Structure: Banks and Regulatory Agencies Financial Intermediaries Commercial banks (community) Thrifts Savings banks Savings and Loans

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015

Instructor: Prof. Menzie Chinn UW Madison Fall 2015") Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

SEC PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES.

SEC. 716. PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES. (a) PROHIBITION ON FEDERAL ASSISTANCE. Notwithstanding any other provision of law (including regulations), no Federal assistance

SEC. 716. PROHIBITION AGAINST FEDERAL GOVERNMENT BAILOUTS OF SWAPS ENTITIES. (a) PROHIBITION ON FEDERAL ASSISTANCE. Notwithstanding any other provision of law (including regulations), no Federal assistance

Depository Institutions

Economics of Financial Intermediation March 2, 2017 Historical trends Historically, Commericial banks have operated as more diversified institutions, having a large concentration of residental mortgage

Economics of Financial Intermediation March 2, 2017 Historical trends Historically, Commericial banks have operated as more diversified institutions, having a large concentration of residental mortgage

Regulatory Implementation Slides

Regulatory Implementation Slides Table of Contents 1. Nonbank Financial Companies: Path to Designation as Systemically Important 2. Systemic Oversight of Bank Holding Companies 3. Systemic Oversight of

Regulatory Implementation Slides Table of Contents 1. Nonbank Financial Companies: Path to Designation as Systemically Important 2. Systemic Oversight of Bank Holding Companies 3. Systemic Oversight of

How Curb Risk In Wall Street. Luigi Zingales. University of Chicago

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

Chapter 2. Government Policies and Regulation

Chapter 2 Government Policies and Regulation Chapter Objectives 1. Describe the regulatory environment in which financial services companies compete. 2. Describe the goals and functions of depository institutions.

Chapter 2 Government Policies and Regulation Chapter Objectives 1. Describe the regulatory environment in which financial services companies compete. 2. Describe the goals and functions of depository institutions.

Chapter 10. Banking Industry: Structure and Competition

Chapter 10 Banking Industry: Structure and Competition Historical Development of the Banking Industry Outcome: Multiple Regulatory Agencies 1. Federal Reserve 2. FDIC 3. Office of the Comptroller of the

Chapter 10 Banking Industry: Structure and Competition Historical Development of the Banking Industry Outcome: Multiple Regulatory Agencies 1. Federal Reserve 2. FDIC 3. Office of the Comptroller of the

The Financial System: Opportunities and Dangers

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

CHAPTER 20 : Opportunities and Dangers Modified for ECON 2204 by Bob Murphy 2016 Worth Publishers, all rights reserved IN THIS CHAPTER, YOU WILL LEARN: the functions a healthy financial system performs

Remarks given at IADI conference on Designing an Optimal Deposit Insurance System

Remarks given at IADI conference on Designing an Optimal Deposit Insurance System Stefan Ingves Chairman of the Basel Committee on Banking Supervision Keynote address at IADI Conference Basel, Friday 2

Remarks given at IADI conference on Designing an Optimal Deposit Insurance System Stefan Ingves Chairman of the Basel Committee on Banking Supervision Keynote address at IADI Conference Basel, Friday 2

The Rise of Modern Financial Regulation. J. Parman (College of William & Mary) Regulation of Markets, Spring 2013 April 22, / 21

Regulation of Markets, Spring 2013 April 22, / 21") The Rise of Modern Financial Regulation J. Parman (College of William & Mary) Regulation of Markets, Spring 2013 April 22, 2013 1 / 21 The Rise of Modern Financial Regulation J. Parman (College of William

The Rise of Modern Financial Regulation J. Parman (College of William & Mary) Regulation of Markets, Spring 2013 April 22, 2013 1 / 21 The Rise of Modern Financial Regulation J. Parman (College of William

LIBRARY. CP New York Financial Writers JUN T k 2r- JÒlÌoojlW, Remarks by. L. William Seidman Chairman Federal Deposit Insurance Corporation

LIBRARY JUN26 1989 T k 2r- JÒlÌoojlW, FEDERAL DEPOSIT INSURANCE CORPORATION Remarks by. %m L. William Seidman Chairman Federal Deposit Insurance Corporation Before CP New York Financial Writers New York,

LIBRARY JUN26 1989 T k 2r- JÒlÌoojlW, FEDERAL DEPOSIT INSURANCE CORPORATION Remarks by. %m L. William Seidman Chairman Federal Deposit Insurance Corporation Before CP New York Financial Writers New York,

Prepared for Members and Committees of Congress

Prepared for Members and Committees of Congress Œ œ Ÿ In a 1989 legislative response to financial troubles in the thrift industry, the Financial Institutions Reform, Recovery, and Enforcement Act of 1989

Prepared for Members and Committees of Congress Œ œ Ÿ In a 1989 legislative response to financial troubles in the thrift industry, the Financial Institutions Reform, Recovery, and Enforcement Act of 1989

Chapter 11. The Nature of Financial Intermediation. Learning Objectives. The Economics of Financial Intermediation

Chapter 11 The Nature of Financial Intermediation Learning Objectives Explain the benefits of financial intermediation and how it partially solves the adverse selection and moral hazard problems Understand

Chapter 11 The Nature of Financial Intermediation Learning Objectives Explain the benefits of financial intermediation and how it partially solves the adverse selection and moral hazard problems Understand

Chapter 2. An Overview of the Financial System

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage

Money and Banking ECON3303. Lecture 12: Banking Industry: Structure and Competition. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 12: Banking Industry: Structure and Competition William J. Crowder Ph.D. Historical Development of the Banking System Bank of North America chartered in 1782 Controversy

Money and Banking ECON3303 Lecture 12: Banking Industry: Structure and Competition William J. Crowder Ph.D. Historical Development of the Banking System Bank of North America chartered in 1782 Controversy

Bank Resolution Powers and Tools. Oana Nedelescu Senior Financial Sector Expert IMF

Bank Resolution Powers and Tools Oana Nedelescu Senior Financial Sector Expert IMF Disclaimer The views expressed in this material are those of the author and do not necessarily represent those of the

Bank Resolution Powers and Tools Oana Nedelescu Senior Financial Sector Expert IMF Disclaimer The views expressed in this material are those of the author and do not necessarily represent those of the

Intra-Group Transactions and Exposures Principles

Intra-Group Transactions and Exposures Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Intra-Group Transactions and Exposures Principles THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

EMERGING CONSUMER RISKS FOR COMMUNITY BANKS

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

November 14, 2016 1 EMERGING CONSUMER RISKS FOR COMMUNITY BANKS 2016 ANNUAL RISK MANAGEMENT CONFERENCE NOVEMBER 14, 2016 November 14, 2016 2 Paul J. Stark, SVP & Chief Credit Officer Civista Bank, Sandusky

BANK STRUCTURAL REFORM POSITION OF THE EUROSYSTEM ON THE COMMISSION S CONSULTATION DOCUMENT

24 January 2013 BANK STRUCTURAL REFORM POSITION OF THE EUROSYSTEM ON THE COMMISSION S CONSULTATION DOCUMENT This document provides the Eurosystem s reply to the Consultation Document by the European Commission

24 January 2013 BANK STRUCTURAL REFORM POSITION OF THE EUROSYSTEM ON THE COMMISSION S CONSULTATION DOCUMENT This document provides the Eurosystem s reply to the Consultation Document by the European Commission

U.S. Treasury Report Proposes Changes to the Financial Regulatory System

June 22, 2017 U.S. Treasury Report Proposes Changes to the Financial Regulatory System The U.S. Department of the Treasury has issued its first in a series of reports required by Executive Order 13772

June 22, 2017 U.S. Treasury Report Proposes Changes to the Financial Regulatory System The U.S. Department of the Treasury has issued its first in a series of reports required by Executive Order 13772

Copyrighted Material. Mathias Dewatripont, Jean-Charles Rochet, and Jean Tirole

CHAPTER 1 Introduction Mathias Dewatripont, Jean-Charles Rochet, and Jean Tirole The recent financial crisis was a mix of unique and much more conventional events. This short book offers our perspective

CHAPTER 1 Introduction Mathias Dewatripont, Jean-Charles Rochet, and Jean Tirole The recent financial crisis was a mix of unique and much more conventional events. This short book offers our perspective

REFORMING PCA. Addendum to Submitted Statements of. Mary Cunningham. and. William Raker. to the. National Credit Union Administration s

REFORMING PCA Addendum to Submitted Statements of Mary Cunningham and William Raker to the National Credit Union Administration s Summit on Credit Union Capital Representing the Credit Union National Association

REFORMING PCA Addendum to Submitted Statements of Mary Cunningham and William Raker to the National Credit Union Administration s Summit on Credit Union Capital Representing the Credit Union National Association

Corporate Finance 2 - Lesson 4 CHAPTER 17 THRIFT INSTITUTIONS AND MORTGAGE BANKS

CHAPTER 17 THRIFT INSTITUTIONS AND MORTGAGE BANKS 2 Topics Covered in Chapter Thrift Institutions Savings Associations Savings Banks Credit Unions Finance Companies 3 Historical Development of Thrift Institutions

CHAPTER 17 THRIFT INSTITUTIONS AND MORTGAGE BANKS 2 Topics Covered in Chapter Thrift Institutions Savings Associations Savings Banks Credit Unions Finance Companies 3 Historical Development of Thrift Institutions

PROMOTING JAPANESE RECOVERY

PROMOTING JAPANESE RECOVERY by Frederic S. Mishkin Graduate School of Business, Columbia University and National Bureau of Economic Research Uris Hall 619 Columbia University New York, New York 10027 Phone:

PROMOTING JAPANESE RECOVERY by Frederic S. Mishkin Graduate School of Business, Columbia University and National Bureau of Economic Research Uris Hall 619 Columbia University New York, New York 10027 Phone:

Cross-border banking regulating according to risk. Thorsten Beck

Cross-border banking regulating according to risk Thorsten Beck Following 2008: Lots of regulatory reforms Basel 3: Higher quantity and quality of capital and liquid assets Additional capital buffers for

Cross-border banking regulating according to risk Thorsten Beck Following 2008: Lots of regulatory reforms Basel 3: Higher quantity and quality of capital and liquid assets Additional capital buffers for

Financial System Crisis Preparedness and Management. Prepared by D.S. Hoelscher and presented by David Walker, IADI

Financial System Crisis Preparedness and Management Prepared by D.S. Hoelscher and presented by David Walker, IADI Overview of session I. Presentation #1 Financial System Crisis Preparedness and Management

Financial System Crisis Preparedness and Management Prepared by D.S. Hoelscher and presented by David Walker, IADI Overview of session I. Presentation #1 Financial System Crisis Preparedness and Management

LIQUIDITY RISK MANAGEMENT: GETTING THERE

LIQUIDITY RISK MANAGEMENT: GETTING THERE Alok Tiwari A bank must at all times maintain overall financial resources, including capital resources and liquidity resources, which are adequate, both as to amount

LIQUIDITY RISK MANAGEMENT: GETTING THERE Alok Tiwari A bank must at all times maintain overall financial resources, including capital resources and liquidity resources, which are adequate, both as to amount

viewpoint What Do Initial Assessments Show?

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized THE WORLD BANK GROUP FINANCIAL AND PRIVATE SECTOR DEVELOPMENT VICE PRESIDENCY OCTOBER

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized THE WORLD BANK GROUP FINANCIAL AND PRIVATE SECTOR DEVELOPMENT VICE PRESIDENCY OCTOBER

The Banking Crisis and Its Regulatory Response in Europe

The Banking Crisis and Its Regulatory Response in Europe Mathias Dewatripont National Bank of Belgium and Single Supervisory Mechanism Bruegel 10 th Anniversary Conference at NBB January 28, 2016 Outline

The Banking Crisis and Its Regulatory Response in Europe Mathias Dewatripont National Bank of Belgium and Single Supervisory Mechanism Bruegel 10 th Anniversary Conference at NBB January 28, 2016 Outline

Written Testimony of Mark Zandi Chief Economist and Cofounder Moody s Economy.com. Before the House Financial Services Committee

Written Testimony of Mark Zandi Chief Economist and Cofounder Moody s Economy.com Before the House Financial Services Committee "Experts' Perspectives on Systemic Risk and Resolution Issues September 24,

Written Testimony of Mark Zandi Chief Economist and Cofounder Moody s Economy.com Before the House Financial Services Committee "Experts' Perspectives on Systemic Risk and Resolution Issues September 24,

Chapter 2. Overview of the Financial System. Chapter Preview

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

Test Bank all chapters download

Test Bank for Bank Management 8th Edition by Timothy W. Koch, S. Scott MacDonald Test Bank all chapters download https://testbankarea.com/download/bank-management-8th-edition-testbank-koch-macdonald/ Related

Test Bank for Bank Management 8th Edition by Timothy W. Koch, S. Scott MacDonald Test Bank all chapters download https://testbankarea.com/download/bank-management-8th-edition-testbank-koch-macdonald/ Related

EC248-Financial Innovations and Monetary Policy Assignment. Andrew Townsend

EC248-Financial Innovations and Monetary Policy Assignment Discuss the concept of too big to fail within the financial sector. What are the arguments in favour of this concept, and what are possible negative

EC248-Financial Innovations and Monetary Policy Assignment Discuss the concept of too big to fail within the financial sector. What are the arguments in favour of this concept, and what are possible negative

Federal Reserve System/IMF/World Bank. Seminar for Senior Bank Supervisors October 19 30, David S. Hoelscher

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

Federal Reserve System/IMF/World Bank Seminar for Senior Bank Supervisors October 19 30, 2009 David S. Hoelscher Money and Capital Markets Department International Monetary Fund Typology of Crises Type

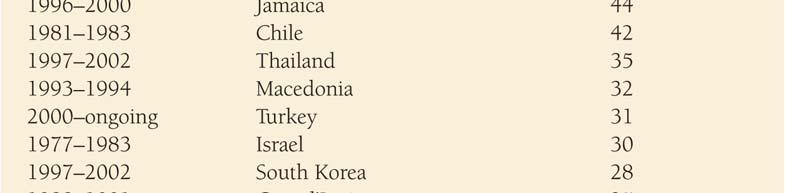

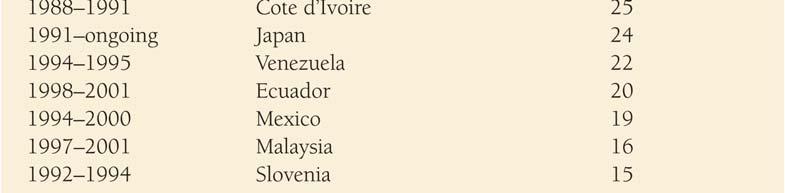

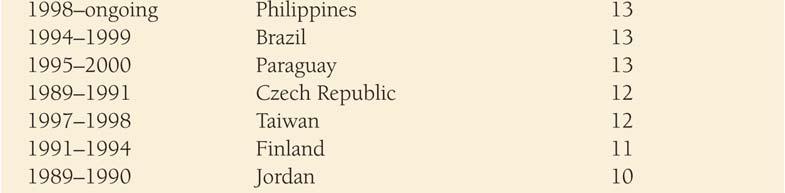

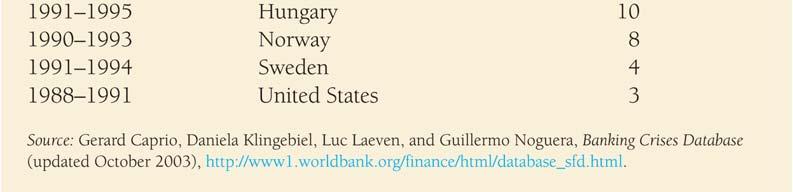

Banking Crises Throughout the World

18 Appendix 2 to Chapter Banking Crises Throughout the World In this appendix, we examine in more detail many of the banking crisis episodes listed in Table 18.2 that took place in other countries. We

18 Appendix 2 to Chapter Banking Crises Throughout the World In this appendix, we examine in more detail many of the banking crisis episodes listed in Table 18.2 that took place in other countries. We

Too Big to Fail Financial Institutions The U.S., the Crisis and Beyond Cirano & Ecole Polytechnique Montreal September 16, 2011

Too Big to Fail Financial Institutions The U.S., the Crisis and Beyond Cirano & Ecole Polytechnique Montreal September 16, 2011 David Min Associate Director for Financial Markets Policy Center for American

Too Big to Fail Financial Institutions The U.S., the Crisis and Beyond Cirano & Ecole Polytechnique Montreal September 16, 2011 David Min Associate Director for Financial Markets Policy Center for American

Ministry Banking Update

Courageous Leadership in Challenging Times Ministry Banking Update CLA Church Leaders Summit April 2010 Courageous Leadership in Challenging Times Session Overview Financial institution (FI) industry update

Courageous Leadership in Challenging Times Ministry Banking Update CLA Church Leaders Summit April 2010 Courageous Leadership in Challenging Times Session Overview Financial institution (FI) industry update

For over a decade, up through 2007, bank failures were few and far between.

Prompt Corrective Action PETER G. WEINSTOCK With the number of bank failures growing, bankers need to understand the regulatory ramifications when they begin to experience problems. In this article, the

Prompt Corrective Action PETER G. WEINSTOCK With the number of bank failures growing, bankers need to understand the regulatory ramifications when they begin to experience problems. In this article, the

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 12 Banking Industry: Structure and Competition

Chapter 12 Banking Industry: Structure and Competition") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 12 Banking Industry: Structure and Competition 12.1 Historical Development of the Banking System 1) The modern commercial banking system

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 12 Banking Industry: Structure and Competition 12.1 Historical Development of the Banking System 1) The modern commercial banking system

Banking Union in Europe Glass Half Full or Glass Half Empty. Thorsten Beck

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

Banking Union in Europe Glass Half Full or Glass Half Empty Thorsten Beck ` Bank resolution a critical part of the regulatory reform agenda Many regulatory reforms over past five years: Basel 3: capital

ADVISORY Dodd-Frank Act

ADVISORY Dodd-Frank Act July 21, 2010 SYSTEMIC RISK REGULATION AND ORDERLY LIQUIDATION OF SYSTEMICALLY IMPORTANT FIRMS On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform

ADVISORY Dodd-Frank Act July 21, 2010 SYSTEMIC RISK REGULATION AND ORDERLY LIQUIDATION OF SYSTEMICALLY IMPORTANT FIRMS On July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform

An EU Framework for Cross-Border Crisis Management in the Banking Sector

An EU Framework for Cross-Border Crisis Management in the Banking Sector Elisa Ferreira BUILDING A NEW FINANCIAL ARCHITECTURE Lisbon, 26-03-2010 Context Final total bill weighted too much on taxpayers,

An EU Framework for Cross-Border Crisis Management in the Banking Sector Elisa Ferreira BUILDING A NEW FINANCIAL ARCHITECTURE Lisbon, 26-03-2010 Context Final total bill weighted too much on taxpayers,

FEDERAL DEPOSIT INSURANCE CORPORATION Washington, DC FORM 10-K

FEDERAL DEPOSIT INSURANCE CORPORATION Washington, DC 20549 FORM 10-K [X] ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended December 31, 2011

FEDERAL DEPOSIT INSURANCE CORPORATION Washington, DC 20549 FORM 10-K [X] ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended December 31, 2011

Banking reform in Britain

Banking reform in Britain John Vickers All Souls College, Oxford University Hoover Institution, Stanford University 21 March 2017 Relative sizes of banking sectors Big hit to UK economy from the crisis

Banking reform in Britain John Vickers All Souls College, Oxford University Hoover Institution, Stanford University 21 March 2017 Relative sizes of banking sectors Big hit to UK economy from the crisis

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017 Significance of Capital Adequacy Capital is the foundation of any business.

Meridian Finance & Investment Limited Disclosure under Pillar III on Capital Adequacy and Market Discipline As on December 31, 2017 Significance of Capital Adequacy Capital is the foundation of any business.

What should be of interest in Dodd-Frank to non-u.s. banks wanting to do business in the United States?

Dodd-Frank Update Full title of the law is The Dodd-Frank Wall Street Reform and Consumer Protection Act Public Law 111-203 was signed into law on July 21, 2010 Major changes made to financial regulation

Dodd-Frank Update Full title of the law is The Dodd-Frank Wall Street Reform and Consumer Protection Act Public Law 111-203 was signed into law on July 21, 2010 Major changes made to financial regulation

INTRODUCTION TO FINANCE MGMT 005 INTRODUCTION TO BUSINESS AND FINANCE

INTRODUCTION TO FINANCE MGMT 005 INTRODUCTION TO BUSINESS AND FINANCE DEFINITION OF FINANCE The science that describes the management, creation and study of money, banking, credit, investments, assets

INTRODUCTION TO FINANCE MGMT 005 INTRODUCTION TO BUSINESS AND FINANCE DEFINITION OF FINANCE The science that describes the management, creation and study of money, banking, credit, investments, assets

Chapter 19. Introduction. Learning Objectives. Policies and Prospects for Global Economic Growth

Chapter 19 Policies and Prospects for Global Economic Growth Introduction Builders in Brazil devote much time and expense to obtain legal permits from local and national government agencies. Construction

Chapter 19 Policies and Prospects for Global Economic Growth Introduction Builders in Brazil devote much time and expense to obtain legal permits from local and national government agencies. Construction

Safe and Sound Banking, 20 Years Later: What Was Proposed and What Has Been Adopted

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Safe and Sound Banking, 20 Years Later: What Was Proposed and What Has Been Adopted Fred Furlong Federal Reserve Bank of San Francisco Simon Kwan

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Safe and Sound Banking, 20 Years Later: What Was Proposed and What Has Been Adopted Fred Furlong Federal Reserve Bank of San Francisco Simon Kwan

Why Bank Equity is Not Expensive

Why Bank Equity is Not Expensive Anat Admati Finance Watch Finance and Society Conference March 27, 2012 Beware: Confusing Jargon! Hold or set aside suggests capital is the same as idle reserves. This

Why Bank Equity is Not Expensive Anat Admati Finance Watch Finance and Society Conference March 27, 2012 Beware: Confusing Jargon! Hold or set aside suggests capital is the same as idle reserves. This

GUIDELINES FOR THE MANAGEMENT OF COUNTRY RISK

SUPERVISORY AND REGULATORY GUIDELINES: 2006-0 11 th April, 2006 GUIDELINES FOR THE MANAGEMENT OF COUNTRY RISK I. INTRODUCTION The Central Bank of The Bahamas ( the Central Bank ) is responsible for the

SUPERVISORY AND REGULATORY GUIDELINES: 2006-0 11 th April, 2006 GUIDELINES FOR THE MANAGEMENT OF COUNTRY RISK I. INTRODUCTION The Central Bank of The Bahamas ( the Central Bank ) is responsible for the

Resolution Funding: Who pays when financial institutions fail?

Resolution Funding: Who pays when financial institutions fail? OCTOBER 25, 2018 Marc Dobler Monetary and Capital Markets Department INTERNATIONAL MONETARY FUND 1 Content Resolution Funding Objectives Why

Resolution Funding: Who pays when financial institutions fail? OCTOBER 25, 2018 Marc Dobler Monetary and Capital Markets Department INTERNATIONAL MONETARY FUND 1 Content Resolution Funding Objectives Why

MODULE 10 Supervision and Regulation. Introduction

MODULE 10 Supervision and Regulation Introduction In this Module, we will discuss supervision and regulation of the IB system. The Basel Committee and Basel Accord will be discussed comprehensively, especially

MODULE 10 Supervision and Regulation Introduction In this Module, we will discuss supervision and regulation of the IB system. The Basel Committee and Basel Accord will be discussed comprehensively, especially

TESTIMONY OF GEORGE E. BURNS COMMISSIONER FINANCIAL INSTITUTIONS DIVISION STATE OF NEVADA S.B. 81. Savings & Loan Statute Modernization.

TESTIMONY OF GEORGE E. BURNS COMMISSIONER FINANCIAL INSTITUTIONS DIVISION STATE OF NEVADA On S.B. 81 Savings & Loan Statute Modernization Before the NEVADA LEGISLATURE Page 2 of 5 INTRODUCTION Existing

TESTIMONY OF GEORGE E. BURNS COMMISSIONER FINANCIAL INSTITUTIONS DIVISION STATE OF NEVADA On S.B. 81 Savings & Loan Statute Modernization Before the NEVADA LEGISLATURE Page 2 of 5 INTRODUCTION Existing

Bank Regulatory Practice

Bank Regulatory Practice SEPTEMBER 2016 Does the Federal Reserve Board have Authority to Set Incentive Compensation? Earlier this year, the Agencies 1 published a Notice of Proposed Rulemaking (the Proposed

Bank Regulatory Practice SEPTEMBER 2016 Does the Federal Reserve Board have Authority to Set Incentive Compensation? Earlier this year, the Agencies 1 published a Notice of Proposed Rulemaking (the Proposed

Overview of Mortgage Lending

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Chapter 1 Overview of Mortgage 1 Chapter Objectives Contrast the primary mortgage market and secondary mortgage market. Identify entities involved in the primary mortgage market and the secondary market.

Did Banking Reforms of the Early 1990s Fail? Lessons from Comparing Two Banking Crises

Economic Brief June 2015, EB15-06 Did Banking Reforms of the Early 1990s Fail? Lessons from Comparing Two Banking Crises By Eliana Balla, Helen Fessenden, Edward Simpson Prescott, and John R. Walter New

Economic Brief June 2015, EB15-06 Did Banking Reforms of the Early 1990s Fail? Lessons from Comparing Two Banking Crises By Eliana Balla, Helen Fessenden, Edward Simpson Prescott, and John R. Walter New

RESERVE BANK OF MALAWI RISK MANAGEMENT SURVEY RESULTS

RESERVE BANK OF MALAWI RISK MANAGEMENT SURVEY RESULTS SEPTEMBER 2007 1 Contents page Foreword 2 Executive Summary 4 Introduction 6 Coverage of Questionnaire 7 Survey Results 8 Summary and Conclusion 14

RESERVE BANK OF MALAWI RISK MANAGEMENT SURVEY RESULTS SEPTEMBER 2007 1 Contents page Foreword 2 Executive Summary 4 Introduction 6 Coverage of Questionnaire 7 Survey Results 8 Summary and Conclusion 14

Function of Financial Markets

Econ135: Lecture 2 Function of Financial Markets Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage of funds Direct finance:

Econ135: Lecture 2 Function of Financial Markets Perform the essential function of channeling funds from economic players that have saved surplus funds to those that have a shortage of funds Direct finance:

NPLs in Europe. Cyprus 5 th February 2016 Lars Nyberg

NPLs in Europe Cyprus 5 th February 2016 Lars Nyberg NPL development Crisis countries that cut NPL ratios (peak of crisis to end 2014) Latvia (18 to 5) Lithuania (25 to 8) Iceland (18 to 5) Ireland (30

NPLs in Europe Cyprus 5 th February 2016 Lars Nyberg NPL development Crisis countries that cut NPL ratios (peak of crisis to end 2014) Latvia (18 to 5) Lithuania (25 to 8) Iceland (18 to 5) Ireland (30

THE FUNDING OF RESOLUTION. David G Mayes University of Auckland

THE FUNDING OF RESOLUTION David G Mayes University of Auckland THE RESEARCH QUESTION Who is likely to pay for bank resolution under the BRRD? Does this meet the objective of minimising the impact of bank

THE FUNDING OF RESOLUTION David G Mayes University of Auckland THE RESEARCH QUESTION Who is likely to pay for bank resolution under the BRRD? Does this meet the objective of minimising the impact of bank

Presented by Norman Mataruka Registrar of Banking Institutions: Reserve Bank of Zimbabwe July 18, /16/2016 1

Presented by Norman Mataruka Registrar of Banking Institutions: Reserve Bank of Zimbabwe nmataruka@rbz.co.zw July 18, 2012 9/16/2016 1 Financial Sector Stability Financial Stability Continuum Sources of

Presented by Norman Mataruka Registrar of Banking Institutions: Reserve Bank of Zimbabwe nmataruka@rbz.co.zw July 18, 2012 9/16/2016 1 Financial Sector Stability Financial Stability Continuum Sources of

GAZELLE PENSIONS ADVISORY UNDERSTANDING SCHEME PENSION RISK OF BANKS IN THE UK FINANCIAL INSTITUTIONS RESEARCH JANUARY 2013

UNDERSTANDING SCHEME PENSION RISK OF BANKS IN THE UK FINANCIAL INSTITUTIONS RESEARCH JANUARY 2013 Gazelle Corporate Finance Limited 41 Devonshire Street London W1G 7AJ www.gazellegroup.co.uk T+44 (0)2071827220

UNDERSTANDING SCHEME PENSION RISK OF BANKS IN THE UK FINANCIAL INSTITUTIONS RESEARCH JANUARY 2013 Gazelle Corporate Finance Limited 41 Devonshire Street London W1G 7AJ www.gazellegroup.co.uk T+44 (0)2071827220

CHAPTER 09 (Part B) Banking and Bank Management

Banking and Bank Management") CHAPTER 09 (Part B) Banking and Bank Management Financial Environment: A Policy Perspective S.C. Savvides Learning Outcomes Upon completion of this chapter, you will be able to: Discuss the developments

CHAPTER 09 (Part B) Banking and Bank Management Financial Environment: A Policy Perspective S.C. Savvides Learning Outcomes Upon completion of this chapter, you will be able to: Discuss the developments

Paulson Proposes Financial Regulatory Overhaul

Date: March 31, 2008 To: Re: Interested Persons Paulson Proposes Financial Regulatory Overhaul Treasury Secretary Henry M. Paulson, Jr. has proposed a sweeping overhaul of the U.S. financial regulatory

Date: March 31, 2008 To: Re: Interested Persons Paulson Proposes Financial Regulatory Overhaul Treasury Secretary Henry M. Paulson, Jr. has proposed a sweeping overhaul of the U.S. financial regulatory

Introduction to U.S. Banks and Financial Institutions

Introduction to U.S. Banks and Financial Institutions Federal Reserve Bank of New York Central Banking Seminar Preparatory Workshop in Financial Markets, Instruments and Institutions Stavros Peristiani

Introduction to U.S. Banks and Financial Institutions Federal Reserve Bank of New York Central Banking Seminar Preparatory Workshop in Financial Markets, Instruments and Institutions Stavros Peristiani

BBI2353 Commercial Bank Management Prepared by Dr Khairul Anuar

BBI2353 Commercial Bank Management Prepared by Dr Khairul Anuar L7: Lending Policies and Procedures: Managing Credit Risk www.lecturenotes638.wordpress.com 16-2 Key Topics Types of Loans Banks and Competing

BBI2353 Commercial Bank Management Prepared by Dr Khairul Anuar L7: Lending Policies and Procedures: Managing Credit Risk www.lecturenotes638.wordpress.com 16-2 Key Topics Types of Loans Banks and Competing

5. Consider the T-account for Cambridge Mutual Savings Bank below. Which of the following transactions is recorded on this T-account?

PART I MULTIPLE CHOICE (50 points, 2 points each) - Clearly mark the best answer. 1. Banks use restrictive covenants to limit the problem of a) Adverse selection b) Compensating balances c) Excessive volatility

PART I MULTIPLE CHOICE (50 points, 2 points each) - Clearly mark the best answer. 1. Banks use restrictive covenants to limit the problem of a) Adverse selection b) Compensating balances c) Excessive volatility

Markus K. Brunnermeier

Markus K. Brunnermeier 1 Overview 1. Underlying mechanism Fire-sale externality + Liquidity spirals (due to maturity mismatch) Hoarding externality (interconnectedness) Runs 2. Crisis prevention Macro-prudential

Markus K. Brunnermeier 1 Overview 1. Underlying mechanism Fire-sale externality + Liquidity spirals (due to maturity mismatch) Hoarding externality (interconnectedness) Runs 2. Crisis prevention Macro-prudential

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Chapter 2 * The Architecture of Financial Regulation

Chapter 2 * The Architecture of Financial Regulation Overview Assuming the financial architecture will continue to be dominated by institutions imposing high levels of systemic risk, the creation of a

Chapter 2 * The Architecture of Financial Regulation Overview Assuming the financial architecture will continue to be dominated by institutions imposing high levels of systemic risk, the creation of a

Chapter 4. Understanding Interest Rates

Chapter 4 Understanding Interest Rates Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright 2007 Pearson Addison-Wesley. All rights reserved.

Chapter 4 Understanding Interest Rates Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright 2007 Pearson Addison-Wesley. All rights reserved.

Printable Lesson Materials

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

Printable Lesson Materials Print these materials as a study guide These printable materials allow you to study away from your computer, which many students find beneficial. These materials consist of two

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords Basel Committee on Banking Supervision ( BCBS ) (www.bis.org: bcbs230 September 2012) Basel Committee on Banking

The Basel Core Principles for Effective Banking Supervision & The Basel Capital Accords Basel Committee on Banking Supervision ( BCBS ) (www.bis.org: bcbs230 September 2012) Basel Committee on Banking

Management Information Systems Reporting Supervisory Expectations James Dennison Managing Director

Management Information Systems Reporting Supervisory Expectations James Dennison Managing Director 23rd XBRL International Conference: Enhancing Business Performance October 25, 2011 About OSFI Independent

Management Information Systems Reporting Supervisory Expectations James Dennison Managing Director 23rd XBRL International Conference: Enhancing Business Performance October 25, 2011 About OSFI Independent

Federal Housing Finance Agency Perspectives on Housing Finance Reform. An Ongoing Conservatorship is Not Sustainable and Needs to End

Federal Housing Finance Agency Perspectives on Housing Finance Reform January 16, 2018 An Ongoing Conservatorship is Not Sustainable and Needs to End The current form of government support for the housing

Federal Housing Finance Agency Perspectives on Housing Finance Reform January 16, 2018 An Ongoing Conservatorship is Not Sustainable and Needs to End The current form of government support for the housing

CITIBANK, N.A. SOUTH AFRICA BRANCH QUARTERLY PUBLIC DISCLOSURE INFORMATION

CITIBANK, N.A. SOUTH AFRICA BRANCH QUARTERLY PUBLIC DISCLOSURE INFORMATION Citibank, N.A. is incorporated in the United States of America and has a national bank charter under the National Bank Act of

CITIBANK, N.A. SOUTH AFRICA BRANCH QUARTERLY PUBLIC DISCLOSURE INFORMATION Citibank, N.A. is incorporated in the United States of America and has a national bank charter under the National Bank Act of

Chapter 3 BASEL III IMPLEMENTATION: CHALLENGES AND OPPORTUNITIES IN CAMBODIA. By Ban Lim 1

Chapter 3 BASEL III IMPLEMENTATION: CHALLENGES AND OPPORTUNITIES IN CAMBODIA By Ban Lim 1 1. Introduction 1.1 Objective and Scope of Study The Basel Agreement of 1993 explicitly incorporated the different

Chapter 3 BASEL III IMPLEMENTATION: CHALLENGES AND OPPORTUNITIES IN CAMBODIA By Ban Lim 1 1. Introduction 1.1 Objective and Scope of Study The Basel Agreement of 1993 explicitly incorporated the different

Economic Brief. Basel III and the Continuing Evolution of Bank Capital Regulation

Economic Brief June 2011, EB11-06 Basel III and the Continuing Evolution of Bank Capital Regulation By Huberto M. Ennis and David A. Price Adopted in part as a response to the 2007 08 financial crisis,

Economic Brief June 2011, EB11-06 Basel III and the Continuing Evolution of Bank Capital Regulation By Huberto M. Ennis and David A. Price Adopted in part as a response to the 2007 08 financial crisis,

McGraw-Hill/Irwin Bank Management and Financial Services, 7/e 2008 The McGraw-Hill Companies, Inc., All Rights Reserved.

Funding the Bank Key Issues Depository Institutions Are Faced With: 12-2 1. Where can funds be raised at lowest possible cost? 2. How can management ensure that there are enough deposits to support lending

Funding the Bank Key Issues Depository Institutions Are Faced With: 12-2 1. Where can funds be raised at lowest possible cost? 2. How can management ensure that there are enough deposits to support lending

Banks Amendment Bill. Presented by: Mark Brits 21 April 2015

Banks Amendment Bill Presented by: Mark Brits 21 April 2015 What is BASA? 1 BASA is the industry representative body of Banks in South Africa Exists to contribute to the enablement of a conducive banking

Banks Amendment Bill Presented by: Mark Brits 21 April 2015 What is BASA? 1 BASA is the industry representative body of Banks in South Africa Exists to contribute to the enablement of a conducive banking

Senior Supervisors Group:

Senior Supervisors Group: Observations on Risk Management Practices During the Recent Market Turbulence Jon Greenlee Associate Director, Risk Management Division of Banking Supervision and Regulation Federal

Senior Supervisors Group: Observations on Risk Management Practices During the Recent Market Turbulence Jon Greenlee Associate Director, Risk Management Division of Banking Supervision and Regulation Federal

1-1. Chapter 1: Basic Concepts

TEST BANK 1-1 Chapter 1: Basic Concepts 1. Which of the following statements is (are) true? a. A risk-preferring individual always prefers the riskier of two gambles that involve different expected value.

TEST BANK 1-1 Chapter 1: Basic Concepts 1. Which of the following statements is (are) true? a. A risk-preferring individual always prefers the riskier of two gambles that involve different expected value.