Coaching Farmers Applying for Credit. Gary Matteson, Farm Credit Council

|

|

|

- Doreen Phillips

- 5 years ago

- Views:

Transcription

1 Coaching Farmers Applying for Credit Gary Matteson, Farm Credit Council

2 Are your clients willing to be exceptional?

3 Defining success Potential borrowers should be able to say: What they want their business to look like What they want their LIFE to look like That success is about more than financial gain. BUT, know that profitability is a pre-requisite to achieving other, non-financial goals.

4 All Success Stories Share One Thing: Regardless of overall goals, all sustainable businesses must have enough net profit to cover costs, including owner draw and capital investment.

5 prepare clients for their future by understanding other businesses

6 Teach the future as being an exercise in resilience

7 Beginning Farmer Humility Lesson Nobody owes you anything. You have to prove you are worthy of trust. What, how, or why you farm does not mean you deserve any more assistance, resources, or opportunities than any other farmer. Scott Marlow, RAFI

8 Planning to succeed Your help is needed by many farmers

9 Being asked the right questions leads to appropriate goals (understanding mindset of a lender) How will the borrowed money be used to make a profit that can repay the loan? How will the loan benefit the business? What happens if things go wrong?

10 The advisor as translator: The language of lenders Speaking in numbers Calculating contingencies

11 The advisor as coach: Three basic business skills: 1. Financial 2. Production 3. Marketing A beginning farmer is lucky to have two of these skills. Coach them where to get the skill they don t have.

12 Management is key to profitability Production management What is unit cost? quality, cost, and quantity Marketing management Who will buy it? Current sales volume and prices Potential customers Financial management Can I pay my bills? managerial accounting

13 The Advisor as Zen Master: The big picture Dispassionate analysis Confidence in the face of challenge Willingness to learn Chart courtesy of Scott Marlow, RAFI

14 The advisor as Mom: Keep good records, they re good for you Set measurable goals and evaluation standards Demonstrate management capacity Demonstrate planning capacity Establish eligibility for WFRP crop insurance

15 what a lender wants to hear explaining your farm business idea in words and numbers

16

17

18

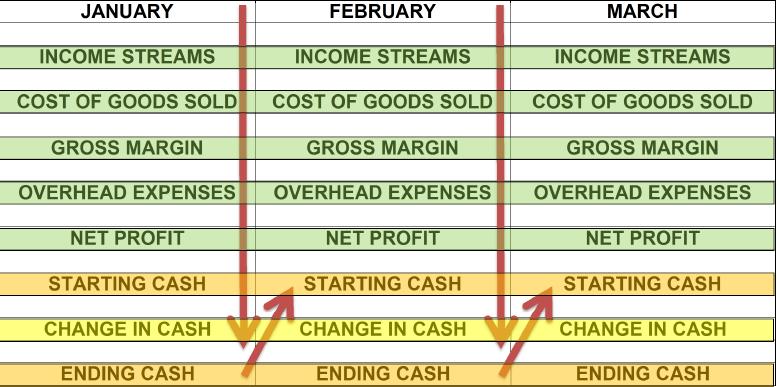

19 The 5-Line Income Statement

20 Showing Annual Business Results This 5-Line Income Statement Becomes the basis of this Cash Flow Analysis Spreadsheet

21 Cash Flow Budgeting

22

23 Outsider s perception of a lending operation Goal: Show me how to get what I want

Probability of loss Collateral Risk mitigation (crop insurance, contracts) Other security (cosigner, guarantee, etc.")

24 What the lender is thinking Income sources (anticipated vs. assured) Probability of loss Collateral Risk mitigation (crop insurance, contracts) Other security (cosigner, guarantee, etc.) 5 C s of Credit (Character, Capital, Capacity, Collateral, Conditions) Goal: Single version of the truth

25 What a lender wants to see Balance sheet Snapshot of business financial health Income statement Business income & expenses over time Cash Flow Budget Shows where money goes and when

26 The Balance Sheet Assets (what you own or control) Cash, inventory, money that customers owe you (A/R), real estate, prepaid expenses, machinery Liabilities - = (what you owe) Loans, A/P, capital leases, accrued expenses Net worth

27 The Income Statement Income Revenues & sales Expenses - = Supplies, feed, payroll, overhead Net income

28

29 How a Farm Lender Hears You: The 5 C s of Credit Character Conditions Capacity Capital Collateral

30 Character Credit Score (should be 700+) Character Demonstrates performance on past loans Conditions Capital Capacity Collateral Indicates existing debt Know what is on your report Share and explain any problems that exist.

31 Conditions Character Capacity Capacity to Repay How will you repay the loan? What are your earnings today? What will they be after the investment? History is important: Income statements Cash flow statements Capital Collateral Tax returns Projections & Budgets What if things don t go as planned? Off-farm income may be important

32 Conditions Character Capacity Collateral The Lender s Fall Back Position Real estate is best Livestock Machinery/Equipment Inventory What is it really worth? Capital Collateral Fair market value (FMV) Net recovery value (NRV) What will it get at auction?

33 Capital Conditions Character Capacity Do you have skin in the game? Net Worth or Debt-to-Asset Ratio How much do you own net of debt? Capital Collateral Market value vs. Book value Balance Sheet

34 Conditions The Deal Terms of the loan: Character Conditions Capacity Capital Collateral Real Estate years Machinery/Equipment 3-7 years Livestock 1-3 years Inventory less than 1 year Loan term should be equal to or shorter than the life of the asset financed

35 Character The Individual Who are we lending to? How do lenders arrive at a decision? Capacity Capital Repayment Ability Where is the business going? Financial Position & Financial Progress Where does the operation stand today? How did it get there? Collateral & Conditions Basis of approval How much risk is involved?

36 Lender turn-offs Poor records High existing debt Low credit scores Relying too much on collateral not enough earnings Low personal investment Unrealistic expectations No plan-b, i.e. What if?... Prices fall The weather doesn t cooperate A buyer goes away Build it and they will come business plans Lack of cooperation & commitment when times get tough We re in it for keeps! You need to be too!

37 What s the dream farm? and where does the money to make it happen come from?

38 Equity Financing- Investment Start-up or venture capital Often high cost (ownership) High risk of failure Debt Financing Loans Finance ongoing operations or expansion Does not dilute ownership cost is limited to interest Banks live here Usually comes from self, relatives, angel investor. NOTE: Traditional lenders like Farm Credit and Banks are not really in the business of financing start-ups. They primarily provide capital to ongoing enterprises with collateral. You are unlikely to walk in with a business plan and a dream and come out with a loan.

39 Spectrum of sources of capital How much money can you get and how long does it take?

40 Don t Finance Beyond the Useful Life of an Asset ONE MORE YEAR OF PAYMENTS AND SHE S ALL MINE!

41 Don t Borrow Your Last Dollar COST OVERRUNS HAPPEN DON T GET CAUGHT!

42 Capitalizing Operational Debt WHAT WILL CHANGE SO YOU WON T DO IT AGAIN NEXT YEAR?

43 Lack of Commitment WHEN THE GOING GETS TOUGH THE TOUGH STICK IT OUT!

44 Things to do Before Starting Save money Protect credit rating ( Gain experience Network Plan Observe

Accessing Capital: 5Cs of Credit. Richard Gianni Market President, Houston Regional President, East Texas Region

Accessing Capital: 5Cs of Credit Richard Gianni Market President, Houston Regional President, East Texas Region 888.215.2373 houston@liftfund.com LiftFund.com AGENDA Who we Are What We Offer Who We Serve

Accessing Capital: 5Cs of Credit Richard Gianni Market President, Houston Regional President, East Texas Region 888.215.2373 houston@liftfund.com LiftFund.com AGENDA Who we Are What We Offer Who We Serve

Introduction Slide SET. Host Organization s Name July 30, Business Smart is a business education series developed by

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

Introduction Slide Business Smart is a business education series developed by SET Host Organization s Name July 30, 2015 1 Business Smart Workshop 3 Modules READY SET GO 2 Today s Presenter Add Name of

NET WORTH STATEMENT - FARMERS AND RANCHERS Name: Date of Statement: Valuation Method: Market Cost

NET WORTH STATEMENT - FARMERS AND RANCHERS Name: Address: Phone: Date of Statement: Valuation Method: Cost Note: This net worth statement should be filled in as a single entity. If you are able to separate

NET WORTH STATEMENT - FARMERS AND RANCHERS Name: Address: Phone: Date of Statement: Valuation Method: Cost Note: This net worth statement should be filled in as a single entity. If you are able to separate

E2E Presentation What do Banks Look For?

What is Lee Bank? Been in business here in Berkshire County since 1852. What does a bank like Lee Bank do? How does it help individuals and businesses? Bank s are businesses. How does a bank make a profit?

What is Lee Bank? Been in business here in Berkshire County since 1852. What does a bank like Lee Bank do? How does it help individuals and businesses? Bank s are businesses. How does a bank make a profit?

Module 4 Preparing Agricultural Financial Statements: The Balance Sheet. Module Outline

Module 4 Preparing Agricultural Financial Statements: The Balance Sheet Introduction Roadside Chat #1 Balance Sheet Considerations Timing Balance Sheet Assets Liabilities Owner Equity Road Test #1 Assets

Module 4 Preparing Agricultural Financial Statements: The Balance Sheet Introduction Roadside Chat #1 Balance Sheet Considerations Timing Balance Sheet Assets Liabilities Owner Equity Road Test #1 Assets

Business Financing 101- What It Takes to Borrow Money

OSC1 Business Financing 101- What It Takes to Borrow Money The Ohio State University South Centers SBDC Slide 1 OSC1 OSU South Centers, 7/6/2011 What will the lender be looking for from me and my business?

OSC1 Business Financing 101- What It Takes to Borrow Money The Ohio State University South Centers SBDC Slide 1 OSC1 OSU South Centers, 7/6/2011 What will the lender be looking for from me and my business?

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

where you stand A Simple Guide to Your Company s

UNDERSTANDING where you stand A Simple Guide to Your Company s Financial Statements SMALL BUSINESS DEVELOPMENT CENTER OF HAMPTON ROADS, INC. Where business comes to talk business. HAMPTON ROADS CHAMBER

UNDERSTANDING where you stand A Simple Guide to Your Company s Financial Statements SMALL BUSINESS DEVELOPMENT CENTER OF HAMPTON ROADS, INC. Where business comes to talk business. HAMPTON ROADS CHAMBER

Understanding Where You Stand

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

3/14/2017. Welcome. FINANCIAL FUNDAMENTALS FOR FOOD HUBS, PART 4: STATEMENT OF CASH FLOWS Tuesday, March 14, Presentation Outline

An NGFN Webinar FINANCIAL FUNDAMENTALS FOR FOOD HUBS, PART 4: STATEMENT OF CASH FLOWS Tuesday, March 14, 2017 Presentation Outline Welcome Wallace Center at Winrock International Statement of Cash Flows

An NGFN Webinar FINANCIAL FUNDAMENTALS FOR FOOD HUBS, PART 4: STATEMENT OF CASH FLOWS Tuesday, March 14, 2017 Presentation Outline Welcome Wallace Center at Winrock International Statement of Cash Flows

Working with Your Lender Thomas R. Stocksdale PNC Agricultural Banking

Working with Your Lender Thomas R. Stocksdale PNC Agricultural Banking Futuring the Dairy Farm Business: In, Out, Moving Ahead November 4, 2010 Dairy Practices Council Agenda Are you: IN, OUT, MOVING AHEAD?

Working with Your Lender Thomas R. Stocksdale PNC Agricultural Banking Futuring the Dairy Farm Business: In, Out, Moving Ahead November 4, 2010 Dairy Practices Council Agenda Are you: IN, OUT, MOVING AHEAD?

A Guide to Buying Your Own Home

A Guide to Buying Your Own Home banking on people Getting started Getting on the property ladder can be a big step for anyone to take. With this handy guide, you ll find helpful tips for planning ahead,

A Guide to Buying Your Own Home banking on people Getting started Getting on the property ladder can be a big step for anyone to take. With this handy guide, you ll find helpful tips for planning ahead,

Credit Card Basics.

Credit Card Basics http://www.nbc.com/saturday-night-live/video/dont-buystuff/n12020 Silly seems obvious! In reality, it is EASY to get caught up with credit card debt Seems like it s free money and it

Credit Card Basics http://www.nbc.com/saturday-night-live/video/dont-buystuff/n12020 Silly seems obvious! In reality, it is EASY to get caught up with credit card debt Seems like it s free money and it

Part III Cash flow management

Bank of America Merrill Lynch White Paper Part III Cash flow management Managing your cash flow Executive summary Your financial statements balance sheet, income statement and cash flow statement are the

Bank of America Merrill Lynch White Paper Part III Cash flow management Managing your cash flow Executive summary Your financial statements balance sheet, income statement and cash flow statement are the

Farm Financial Update

Farm Financial Update Tina Barrett Nebraska Farm Business, Inc. Nebraska Farm Business, Inc. The Nebraska Farm Business Association was started in 1976 as part of Cooperative Extension & The University

Farm Financial Update Tina Barrett Nebraska Farm Business, Inc. Nebraska Farm Business, Inc. The Nebraska Farm Business Association was started in 1976 as part of Cooperative Extension & The University

Understanding the Concept of Borrowing Money

Lesson D1 2 Understanding the Concept of Borrowing Money Unit D. Basic Agribusiness Principles and Skills Problem Area 1. Managing Personal Finances Lesson 2. Understanding the Concept of Borrowing Money

Lesson D1 2 Understanding the Concept of Borrowing Money Unit D. Basic Agribusiness Principles and Skills Problem Area 1. Managing Personal Finances Lesson 2. Understanding the Concept of Borrowing Money

How to be a Ninja Investor

Kevin Wright What is a Ninja Investor? How to be a Ninja Investor Ninja Investors are property investors just like you, except that they have acquired the knowledge to legally break the rules that the

Kevin Wright What is a Ninja Investor? How to be a Ninja Investor Ninja Investors are property investors just like you, except that they have acquired the knowledge to legally break the rules that the

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02 NF Net Worth Statement Instructions The Samuel Roberts Noble Foundation Introduction: Good financial management is very important to being

Net Worth Statement Instructions & Forms Dan Childs NF-AE-01-02 NF Net Worth Statement Instructions The Samuel Roberts Noble Foundation Introduction: Good financial management is very important to being

Session 12 - Structuring a Start-up Transaction

- Structuring a Start-up Transaction All common stock deals Alernatives to all common stock deals Restricted stock Structuring a start-up as a flow-through entity (S corp, partnership) when venture capital

- Structuring a Start-up Transaction All common stock deals Alernatives to all common stock deals Restricted stock Structuring a start-up as a flow-through entity (S corp, partnership) when venture capital

Financial Statement Facelift

Financial Statement Facelift Improving your financial statements for presentation to carriers, reinsurers, business partners, lenders, or equity sources. Outline Why is this important? Basic Acronyms Balance

Financial Statement Facelift Improving your financial statements for presentation to carriers, reinsurers, business partners, lenders, or equity sources. Outline Why is this important? Basic Acronyms Balance

BUYERS GUIDE IMPORTANT THINGS TO CONSIDER WHEN BUYING A HOME COURTESY OF

BUYERS GUIDE IMPORTANT THINGS TO CONSIDER WHEN BUYING A HOME COURTESY OF OWNING MAKES SENSE When comparing the cost of owning a home to renting, there is more than the difference in house payment against

BUYERS GUIDE IMPORTANT THINGS TO CONSIDER WHEN BUYING A HOME COURTESY OF OWNING MAKES SENSE When comparing the cost of owning a home to renting, there is more than the difference in house payment against

Non-recourse business funding with no personal guarantee required

1 Non-recourse business funding with no personal guarantee required A personal guarantee on a business loan means that you are personally responsible for the repayment of that money if the business fails

1 Non-recourse business funding with no personal guarantee required A personal guarantee on a business loan means that you are personally responsible for the repayment of that money if the business fails

I m going to cover 6 key points about FCF here:

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

By JW Warr

By JW Warr 1 WWW@AmericanNoteWarehouse.com JW@JWarr.com 512-308-3869 Have you ever found out something you already knew? For instance; what color is a YIELD sign? Most people will answer yellow. Well,

By JW Warr 1 WWW@AmericanNoteWarehouse.com JW@JWarr.com 512-308-3869 Have you ever found out something you already knew? For instance; what color is a YIELD sign? Most people will answer yellow. Well,

How to Package a Project Loan Request By James Conlow

How to Package a Project Loan Request By James Conlow Financing is about one thing: Profitable Exit for the Financier. The financing request for a loan must satisfy a single basic requirement: 1. Verified

How to Package a Project Loan Request By James Conlow Financing is about one thing: Profitable Exit for the Financier. The financing request for a loan must satisfy a single basic requirement: 1. Verified

Funding Your Business 101

Funding Your Business 101 website: www.sbtdc.org e-mail: info@sbtdc.org George McAllister 704-548-1090 gmcallister@sbtdc.org Small Business and Technology Development Center (SBTDC) The SBTDC is administered

Funding Your Business 101 website: www.sbtdc.org e-mail: info@sbtdc.org George McAllister 704-548-1090 gmcallister@sbtdc.org Small Business and Technology Development Center (SBTDC) The SBTDC is administered

YOUR GUIDE TO PRE- SETTLEMENT ADVANCES

YOUR GUIDE TO PRE- SETTLEMENT ADVANCES What is a pre-settlement advance? If you have hired an attorney to bring a lawsuit, and if you need cash now, you may be able to obtain a pre-settlement advance on

YOUR GUIDE TO PRE- SETTLEMENT ADVANCES What is a pre-settlement advance? If you have hired an attorney to bring a lawsuit, and if you need cash now, you may be able to obtain a pre-settlement advance on

Building a strong credit history. A public education campaign brought to you by MasterCard

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Short Selling Mini-Lesson

Short Selling Mini-Lesson 1. Explain that sometimes people can make money on stocks when the actual stocks themselves lose value and this mini-simulation will demonstrate how. 2. Cut apart the cards for

Short Selling Mini-Lesson 1. Explain that sometimes people can make money on stocks when the actual stocks themselves lose value and this mini-simulation will demonstrate how. 2. Cut apart the cards for

Small business funding options

Small business funding options 60 minutes of straight talk! Donna J. Davis Former Regional Administrator U.S. Small Business Administration 11/16/17 WiFi: QBConnect Password not required About today s

Small business funding options 60 minutes of straight talk! Donna J. Davis Former Regional Administrator U.S. Small Business Administration 11/16/17 WiFi: QBConnect Password not required About today s

Work with a partner. All these words are connected to getting a mortgage. Do you know their meaning?

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

Warm Up Work with a partner. Are you planning to move house in the near future? Conversation Practice with a partner. Well I finally did it! I ve decided to buy a house! That s great! Have you found a

Introduction To The Income Statement

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

Money 101 Presenter s Guide

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

What is a SHORT SALE?

Frequently Asked Questions What is a SHORT SALE? What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property.

Frequently Asked Questions What is a SHORT SALE? What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property.

BUSINESS TOOLS. How Lending Decisions Are Made. How the Five Cs of Credit are used

Every lending institution has a set of credit standards or guidelines that are used to analyze and approve loans. At Northwest Farm Credit Services, these guidelines ensure constructive credit to help

Every lending institution has a set of credit standards or guidelines that are used to analyze and approve loans. At Northwest Farm Credit Services, these guidelines ensure constructive credit to help

Securities Based Lending The Smarter Alternative to a Loan or Mortgage 01/15/2010

Securities Based Lending The Smarter Alternative to a Loan or Mortgage 01/15/2010 Contents Product General Description Parameters Criteria what securities can and cannot be used Loan Process Security Info

Securities Based Lending The Smarter Alternative to a Loan or Mortgage 01/15/2010 Contents Product General Description Parameters Criteria what securities can and cannot be used Loan Process Security Info

Business Planning using Cash Flow Analysis. Gary Matteson, Farm Credit Council

Business Planning using Cash Flow Analysis Gary Matteson, Farm Credit Council Looking to the Future What are your skills? What is your tolerance for risk? What is your capacity to deal with ambiguity?

Business Planning using Cash Flow Analysis Gary Matteson, Farm Credit Council Looking to the Future What are your skills? What is your tolerance for risk? What is your capacity to deal with ambiguity?

Credit Unit Test Bank

1.4.0.M1 Credit Unit Test Bank Total Points Earned 30 Total Points Possible Percentage Name Date Class Directions: Circle the correct answer for each question. 1. A characteristic of installment credit

1.4.0.M1 Credit Unit Test Bank Total Points Earned 30 Total Points Possible Percentage Name Date Class Directions: Circle the correct answer for each question. 1. A characteristic of installment credit

ENDURING THE CYCLE Lessons learned from those who have survived difficult times. Bob Boyle 1 ABSTRACT

ENDURING THE CYCLE Lessons learned from those who have survived difficult times. Bob Boyle 1 ABSTRACT The last several years produced strong profits for hay producers and enabled significant growth in

ENDURING THE CYCLE Lessons learned from those who have survived difficult times. Bob Boyle 1 ABSTRACT The last several years produced strong profits for hay producers and enabled significant growth in

MANAGING YOUR BUSINESS S CASH FLOW. Managing Your Business s Cash Flow. David Oetken, MBA CPM

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

What is your credit score? A community empowerment program brought to you by MasterCard

What is your credit score? A community empowerment program brought to you by MasterCard Understand what a credit score is so you can make sure you re making smart decisions right from the start. 2 Master

What is your credit score? A community empowerment program brought to you by MasterCard Understand what a credit score is so you can make sure you re making smart decisions right from the start. 2 Master

Prepared by: THE COMPLETE GUIDE to Starting and Running Your Own Franchise

Prepared by: THE COMPLETE GUIDE to Starting and Running Your Own Franchise Starting your own business is a big undertaking. For those with the entrepreneurial spirit, it is the best way to express your

Prepared by: THE COMPLETE GUIDE to Starting and Running Your Own Franchise Starting your own business is a big undertaking. For those with the entrepreneurial spirit, it is the best way to express your

Planning for Successful Operations and Succession

Planning for Successful Operations and Succession Brenik Iverson, C.P.A. Odessa, Washington (509) 982-2922 www.leffelotiswarwick.com Planning for Successful Operations and Succession Operating Budget Tax

Planning for Successful Operations and Succession Brenik Iverson, C.P.A. Odessa, Washington (509) 982-2922 www.leffelotiswarwick.com Planning for Successful Operations and Succession Operating Budget Tax

Agricultural Accounting

Agricultural Accounting Steven M. Bragg Chapter 1 Introduction to Agricultural Accounting... 1 Learning Objectives... 1 Introduction... 1 A Note on Terminology... 1 The Economic Entity Concept... 1 Financial

Agricultural Accounting Steven M. Bragg Chapter 1 Introduction to Agricultural Accounting... 1 Learning Objectives... 1 Introduction... 1 A Note on Terminology... 1 The Economic Entity Concept... 1 Financial

Shopping for an Automobile Loan. What Do I Need to Know?

Shopping for an Automobile Loan What Do I Need to Know? Automobiles 2 nd most expensive purchase for most consumers Usually purchased with Loan / credit Or cash if you have enough (uncommon) Ask yourself:

Shopping for an Automobile Loan What Do I Need to Know? Automobiles 2 nd most expensive purchase for most consumers Usually purchased with Loan / credit Or cash if you have enough (uncommon) Ask yourself:

Making the loans that make rural Arkansas a better place to live and work! OF ARKANSAS

Making the loans that make rural Arkansas a better place to live and work! OF ARKANSAS Farm Credit is a lot of things, but we re... NOT an insurance company NOT a part of the government. NOT a bank. NOT

Making the loans that make rural Arkansas a better place to live and work! OF ARKANSAS Farm Credit is a lot of things, but we re... NOT an insurance company NOT a part of the government. NOT a bank. NOT

those who, regardless of life s ups and downs and periods of tight cash flow, always find a way to pay cannot pay back loan.

Five C s of Credit: A summary on the merit of a typical loan application. by Charles Pope, MBA, Certified Commercial Lender Managing Director GPA Capital 1. Character Most people immediately assume it

Five C s of Credit: A summary on the merit of a typical loan application. by Charles Pope, MBA, Certified Commercial Lender Managing Director GPA Capital 1. Character Most people immediately assume it

Business Financing 101 What It Takes to Borrow Money

Business Financing 101 What It Takes to Borrow Money Brad Bapst Business Development Specialist The OSU South Centers Business Development Network 1864 Shyville Rd. Piketon, OH 45661 740-289-2071 Ext.

Business Financing 101 What It Takes to Borrow Money Brad Bapst Business Development Specialist The OSU South Centers Business Development Network 1864 Shyville Rd. Piketon, OH 45661 740-289-2071 Ext.

What s My Note Worth? The Note Value Handbook

What s My Note Worth? The Note Value Handbook Inside Information Regarding Valuation of your Seller Financed Note in the Note Investor Market Compiled and published by Nationwide Secured Capital Retail

What s My Note Worth? The Note Value Handbook Inside Information Regarding Valuation of your Seller Financed Note in the Note Investor Market Compiled and published by Nationwide Secured Capital Retail

Understanding Financial Statements: The Basics

Coaching Program Understanding Financial Statements: The Basics 2010-18 As business owners or investors, most of us are at least familiar with the concept of financial statements. We understand that we

Coaching Program Understanding Financial Statements: The Basics 2010-18 As business owners or investors, most of us are at least familiar with the concept of financial statements. We understand that we

Evaluating the Financial Viability of the Business

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

Evaluating the Financial Viability of the Business Just as it is important to construct a new building on a strong foundation, it is important to build the economic future of your business on a sound financial

Module 3. Farming the Business

152 Module 3 How do I take my business to the next level? Module 3 Farming the Business 153 Module 3 Module 3 How do I take my business to the next level? The aim of Module 3 is to introduce some of the

152 Module 3 How do I take my business to the next level? Module 3 Farming the Business 153 Module 3 Module 3 How do I take my business to the next level? The aim of Module 3 is to introduce some of the

Loans for College. Defer: Some federal loans let you defer or delay paying the loan back until after you graduate.

Loans for College After you ve applied for financial aid and have received your results (your award letters), you may find that you still have a gap an unmet need. Sometimes even the amount that the federal

Loans for College After you ve applied for financial aid and have received your results (your award letters), you may find that you still have a gap an unmet need. Sometimes even the amount that the federal

Unit E: Understanding the Use of Money and Obtaining Credit. Lesson 2: Understanding the Concept of Borrowing Money

Unit E: Understanding the Use of Money and Obtaining Credit Lesson 2: Understanding the Concept of Borrowing Money Student Learning Objectives: Instruction in this lesson should result in students achieving

Unit E: Understanding the Use of Money and Obtaining Credit Lesson 2: Understanding the Concept of Borrowing Money Student Learning Objectives: Instruction in this lesson should result in students achieving

An old stock market saying is, "Bulls can make money, bears can make money, but pigs end up getting slaughtered.

In this lesson, you will learn about buying on margin and selling short. You will learn how buying on margin and selling short can increase potential gains on stock purchases, but at the risk of greater

In this lesson, you will learn about buying on margin and selling short. You will learn how buying on margin and selling short can increase potential gains on stock purchases, but at the risk of greater

The Basic Framework of Budgeting

7-1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget

7-1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget

Export, Mitigate Risks, Get Paid

Export, Mitigate Risks, Get Paid Pre-export Finance Solutions for Small, Medium-Sized Enterprises William Laraque Country Eligibility Support provided for countries in accordance with Eximbank s Country

Export, Mitigate Risks, Get Paid Pre-export Finance Solutions for Small, Medium-Sized Enterprises William Laraque Country Eligibility Support provided for countries in accordance with Eximbank s Country

Balance Sheet-A Financial Management Tool

Balance Sheet-A Financial Management Tool Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-291 by Dr. Michael Langemeier Kansas State University Department of Agricultural

Balance Sheet-A Financial Management Tool Robin Reid (robinreid@ksu.edu) and Kevin Herbel (kherbel@ksu.edu) Revision of MF-291 by Dr. Michael Langemeier Kansas State University Department of Agricultural

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

In the previous session we learned about the various categories of Risk in agriculture. Of course the whole point of talking about risk in this educational series is so that we can talk about managing

Lesson 8 Borrowing Money

AOBF Financial Planning Lesson 8 Borrowing Money Student Resources Resource Description Student Resource 8.1 Reading: Why Borrow? Student Resource 8.2 Worksheet: Borrowing and Lending Terms Student Resource

AOBF Financial Planning Lesson 8 Borrowing Money Student Resources Resource Description Student Resource 8.1 Reading: Why Borrow? Student Resource 8.2 Worksheet: Borrowing and Lending Terms Student Resource

Module 5 Preparing Agricultural Financial Statements: The Income Statement and Cash Flow Module Outline

Module 5 Preparing Agricultural Financial Statements: Module Outline Introduction Income Statement Overview Cash Income Statement What is not included on an income statement? Roadside Chat #1 Limitations

Module 5 Preparing Agricultural Financial Statements: Module Outline Introduction Income Statement Overview Cash Income Statement What is not included on an income statement? Roadside Chat #1 Limitations

Econ 466 Spring, 2005 Exam I February 22, 2005 K E Y

Econ 466 Spring, 2005 Exam I February 22, 2005 K E Y I. Short Answers (5 points each) 1. As part of a cost-cutting move at Iowa State, it has been proposed that the course in agricultural finance be eliminated.

Econ 466 Spring, 2005 Exam I February 22, 2005 K E Y I. Short Answers (5 points each) 1. As part of a cost-cutting move at Iowa State, it has been proposed that the course in agricultural finance be eliminated.

PROJECT PRO$PER. The Basics of Building Wealth

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

Consolidated Balance Sheets

Consolidated Balance Sheets March 31, 2008 and 2009 ASSETS 2008 2009 2009 Current assets Cash and cash equivalents... 1,628,547 2,444,280 $ 24,883 Time deposits... 134,773 45,178 460 Marketable securities...

Consolidated Balance Sheets March 31, 2008 and 2009 ASSETS 2008 2009 2009 Current assets Cash and cash equivalents... 1,628,547 2,444,280 $ 24,883 Time deposits... 134,773 45,178 460 Marketable securities...

Frequently Asked Questions

Short Sale 101 Frequently Asked Questions What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property. In

Short Sale 101 Frequently Asked Questions What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property. In

An Interview with Renaud Laplanche. Renaud Laplanche, CEO, Lending Club, speaks with Growthink University s Dave Lavinsky

An Interview with Renaud Laplanche Renaud Laplanche, CEO, Lending Club, speaks with Growthink University s Dave Lavinsky Dave Lavinsky: Hello everyone. This is Dave Lavinsky from Growthink. Today I am

An Interview with Renaud Laplanche Renaud Laplanche, CEO, Lending Club, speaks with Growthink University s Dave Lavinsky Dave Lavinsky: Hello everyone. This is Dave Lavinsky from Growthink. Today I am

Introduction: Food Truck & Trailer Financing F.A.Q.'s

Introduction: Food Truck & Trailer Financing F.A.Q.'s If you're reading this guide, you are obviously considering financing your food truck or food trailer purchase. After talking to literally hundreds

Introduction: Food Truck & Trailer Financing F.A.Q.'s If you're reading this guide, you are obviously considering financing your food truck or food trailer purchase. After talking to literally hundreds

FIRST TIME HOME BUYERS GUIDE TO SUCCESS! Presented by Mike Cordell with Platinum Realty

FIRST TIME HOME BUYERS GUIDE TO SUCCESS! Presented by Mike Cordell with Platinum Realty So where do I start? Okay so you know that you are ready to purchase your first home, but where do you start? What

FIRST TIME HOME BUYERS GUIDE TO SUCCESS! Presented by Mike Cordell with Platinum Realty So where do I start? Okay so you know that you are ready to purchase your first home, but where do you start? What

Simple Steps for Starting Your Business. Financial Projections

Simple Steps for Starting Your Business Financial Projections Simple Steps for Starting Your Business Session 4: Financial Plan & Projections Agenda Importance of financial planning Building your financial

Simple Steps for Starting Your Business Financial Projections Simple Steps for Starting Your Business Session 4: Financial Plan & Projections Agenda Importance of financial planning Building your financial

AGRICULTURAL BALANCE SHEET

AGRICULTURAL BALANCE SHEET 240 W. 4th St. P.O. 797 Colby, KS 67701 (785) 460-3321 (785) 460-9727 Fax Name(s): SSN or Tax ID No. Date: Residence Address: GENERAL INFORMATION Ownership of Assets/Liabilities

AGRICULTURAL BALANCE SHEET 240 W. 4th St. P.O. 797 Colby, KS 67701 (785) 460-3321 (785) 460-9727 Fax Name(s): SSN or Tax ID No. Date: Residence Address: GENERAL INFORMATION Ownership of Assets/Liabilities

Session 2: Business Planning and Farm Finance Introduction. UVM Farmer Training Program. Mark Cannella. Farm Business Management Specialist

Session 2: Business Planning and Farm Finance Introduction UVM Farmer Training Program Mark Cannella Farm Business Management Specialist Mark.Cannella@uvm.edu 802-223-2389 UVM Extension Farm Viability

Session 2: Business Planning and Farm Finance Introduction UVM Farmer Training Program Mark Cannella Farm Business Management Specialist Mark.Cannella@uvm.edu 802-223-2389 UVM Extension Farm Viability

PLANNING FOR YOUR AGRIPRENEURSHIP BUSINESS

PLANNING FOR YOUR AGRIPRENEURSHIP BUSINESS 1 Creating a basic business plan: Understanding your financials Introduction: Welcome to How to Write Your Business Plan 101! As agricultural entrepreneurs, or

PLANNING FOR YOUR AGRIPRENEURSHIP BUSINESS 1 Creating a basic business plan: Understanding your financials Introduction: Welcome to How to Write Your Business Plan 101! As agricultural entrepreneurs, or

How to Find and Qualify for the Best Loan for Your Business

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

How to Find and Qualify for the Best Loan for Your Business With so many business loans available to you these days, where do you get started? What loan product is right for you, and how do you qualify

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

Career Day. Diane Hamilton Mortgage Specialist Equity Resources, Inc..

Career Day Diane Hamilton Mortgage Specialist Equity Resources, Inc.. Responsibilities of my Career 1. I need to make sure that I have the families best interest in mind at all times. 2. Complete understanding

Career Day Diane Hamilton Mortgage Specialist Equity Resources, Inc.. Responsibilities of my Career 1. I need to make sure that I have the families best interest in mind at all times. 2. Complete understanding

How to Get Business Loans with Bad Credit

How to Get Business Loans with Bad Credit Name : Phone : Email : How to Get Business Loans with Bad Credit Most entrepreneurs think that because they have bad credit there is no chance of them getting

How to Get Business Loans with Bad Credit Name : Phone : Email : How to Get Business Loans with Bad Credit Most entrepreneurs think that because they have bad credit there is no chance of them getting

THIS HANDY LITTLE GUIDE EXPLORES THE BASICS OF CREDIT SCORING AND CREDIT REPORTING IN AUSTRALIA. TABLE OF CONTENTS

CREDIT MADE SIMPLE THIS HANDY LITTLE GUIDE This handy little guide explores the basics of credit scoring and credit reporting in Australia. EXPLORES THE BASICS OF CREDIT SCORING AND CREDIT REPORTING IN

CREDIT MADE SIMPLE THIS HANDY LITTLE GUIDE This handy little guide explores the basics of credit scoring and credit reporting in Australia. EXPLORES THE BASICS OF CREDIT SCORING AND CREDIT REPORTING IN

MODULE 7: Borrowing Basics PARTICIPANT GUIDE

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

The Stock Market. What It Is and How It Works. Ashlee Garn, Brokerage Consultant Fidelity Investments

The Stock Market What It Is and How It Works Ashlee Garn, Brokerage Consultant Fidelity Investments Topics We Will Cover: 1. How corporations raise money. Debt vs. Equity 2. How stocks are bought and sold

The Stock Market What It Is and How It Works Ashlee Garn, Brokerage Consultant Fidelity Investments Topics We Will Cover: 1. How corporations raise money. Debt vs. Equity 2. How stocks are bought and sold

Executive Women in Agriculture

Executive Women in Agriculture FINANCIAL STATEMENT FUNDAMENTALS Understanding what your lender needs 1 OR How can this benefit me? What does 2014 have in store? Lower commodity prices Increasing input

Executive Women in Agriculture FINANCIAL STATEMENT FUNDAMENTALS Understanding what your lender needs 1 OR How can this benefit me? What does 2014 have in store? Lower commodity prices Increasing input

Lending with a Purpose

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

Do you need it? KS2 Learning Resources. Experian

Do you need it? KS2 Learning Resources 1.0 LESSON 1 OUTLINE Lesson 1 The Cost of a Loan You will need: Do You Need It? - Interactive Storybook 1.1 Factsheet: Loans for each group/pair 1.2 Matching Loan

Do you need it? KS2 Learning Resources 1.0 LESSON 1 OUTLINE Lesson 1 The Cost of a Loan You will need: Do You Need It? - Interactive Storybook 1.1 Factsheet: Loans for each group/pair 1.2 Matching Loan

How Can You Afford to be a Farmer?

How Can You Afford to be a Farmer? Wisconsin Local Food Summit January 30, 2015 Wisconsin Rapids Paul Dietmann, Emerging Markets Specialist Badgerland Financial Paul.dietmann@badgerlandfinancial.com (608)

How Can You Afford to be a Farmer? Wisconsin Local Food Summit January 30, 2015 Wisconsin Rapids Paul Dietmann, Emerging Markets Specialist Badgerland Financial Paul.dietmann@badgerlandfinancial.com (608)

Name Period. Finance charge Loan term Grace period Late fee Cash Advance Fee Prepayment Penalty Origination Fee Amortization Collateral Capital

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy

Understanding Financial Data

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

Commercial Credit Risk Analysis and Approval: Behind the Scenes. January 21, 2016

Commercial Credit Risk Analysis and Approval: Behind the Scenes January 21, 2016 Comerica Bank Presenters Joyce Conley, CTP, Vice President, Treasury Management Sales Joyce joined Comerica Bank in 2012

Commercial Credit Risk Analysis and Approval: Behind the Scenes January 21, 2016 Comerica Bank Presenters Joyce Conley, CTP, Vice President, Treasury Management Sales Joyce joined Comerica Bank in 2012

Financial Well-being. Debt and Credit

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

Financial Well-being Debt and Credit Debt and Credit When evaluating financial wellness, debt has a real impact on your ability to reach your goals. Debt feels like a four letter word. However, it can

How Do You Determine if Your Farm Can Take on a New Partner? Adam J. Kantrovich, Ph.D. Michigan State University Extension

How Do You Determine if Your Farm Can Take on a New Partner? Adam J. Kantrovich, Ph.D. Michigan State University Extension 1 Is This Going to be a Marriage Made in Heaven or One that Ends in Divorce? 2

How Do You Determine if Your Farm Can Take on a New Partner? Adam J. Kantrovich, Ph.D. Michigan State University Extension 1 Is This Going to be a Marriage Made in Heaven or One that Ends in Divorce? 2

Harvesting a Profit: Session III: Funding

Harvesting a Profit: Session III: Funding A guide to growing a financially sustainable agricultural business Copyright 2015 Farm Credit East. All Rights Reserved. Version 2.0 1 Today s Presenters Katelyn

Harvesting a Profit: Session III: Funding A guide to growing a financially sustainable agricultural business Copyright 2015 Farm Credit East. All Rights Reserved. Version 2.0 1 Today s Presenters Katelyn

The Current Environment for Bond Investing

JOEY THOMPSON 2013-06-21 The Current Environment for Bond Investing U. S. Government bonds are often thought of as safe investments, but like all investments, there is risk involved. When yields and inflation

JOEY THOMPSON 2013-06-21 The Current Environment for Bond Investing U. S. Government bonds are often thought of as safe investments, but like all investments, there is risk involved. When yields and inflation

As of December 31, As of. Assets Current assets:

CONSOLIDATED BALANCE SHEETS (In millions, except share and par value amounts which are reflected in thousands, and par value per share amounts) Assets Current assets: As of December 31, 2011 As of December

CONSOLIDATED BALANCE SHEETS (In millions, except share and par value amounts which are reflected in thousands, and par value per share amounts) Assets Current assets: As of December 31, 2011 As of December

Balance Sheets- step one for your 2018 farm analysis

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

Page 1 of 21 Name Address Phone Email Balance Sheets- step one for your 2018 farm analysis The farm s balance sheet is a snapshot, on one day in time, of what the farm business owns, (its assets), and

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656 Farm Business Planning Building a Farm Business Plan Lenders Perspective Financing Options How to Build

Tony Bowers Farm Loan Officer USDA Farm Service Agency 820 Industrial Drive, Suite 1 Sparta, WI 54656 Farm Business Planning Building a Farm Business Plan Lenders Perspective Financing Options How to Build

MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

If you're like most Americans, owning your own home is a major

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GUIDE TO FUNDING HOME IMPROVEMENTS

GUIDE TO FUNDING HOME IMPROVEMENTS FUNDING HOME IMPROVEMENTS If you re a budding property developer, renovating your home is the perfect way to get the house of your dreams for a fraction of the price.

GUIDE TO FUNDING HOME IMPROVEMENTS FUNDING HOME IMPROVEMENTS If you re a budding property developer, renovating your home is the perfect way to get the house of your dreams for a fraction of the price.

The Path To A Successful Loan Application

The Path To A Successful Loan Application Being Bankable-Establishing Borrowing Power Presented by: Caiser Hogan Vice President & Small Business Resource Officer Zions Bank Strong Business Owners Understand

The Path To A Successful Loan Application Being Bankable-Establishing Borrowing Power Presented by: Caiser Hogan Vice President & Small Business Resource Officer Zions Bank Strong Business Owners Understand

Making Your Balance Sheet Work for You

Downloaded from the Family Practice Management Web site at www.aafp.org/fpm. Copyright 2001 American Academy of Family Physicians. For the private, noncommercial use of one individual user of the Web site.

Downloaded from the Family Practice Management Web site at www.aafp.org/fpm. Copyright 2001 American Academy of Family Physicians. For the private, noncommercial use of one individual user of the Web site.