Career Day. Diane Hamilton Mortgage Specialist Equity Resources, Inc..

|

|

|

- Jewel Taylor

- 5 years ago

- Views:

Transcription

1 Career Day Diane Hamilton Mortgage Specialist Equity Resources, Inc..

2 Responsibilities of my Career 1. I need to make sure that I have the families best interest in mind at all times. 2. Complete understanding of the families money situation and life situation. 2

3 Required Schooling 1. Licensed through the State of Ohio and the United States. 2. A good understanding of formulas and math. 3

4 Number of Hours Worked per Week 1. My hours will vary some weeks I will work hours and some I will work hours. 4

5 What is a Mortgage? The definition through Wikipedia is: A conveyance of an interest in property as security for the repayment of money borrowed. People will use a mortgage to purchase a home if they do not have enough cash to be able to pay for it. People will also refinance the mortgage they currently have to make the payments lower. 5

6 What is Credit? According to Wikipedia: Confidence in a purchaser s ability and intention to pay, displayed by entrusting the buyer with goods or services without immediate payment. 6

7 The Three C s of Credit Your credit score is a measure of factors that may affect your ability to repay credit. It s a complex formula that takes into account how you ve repaid the previous loans, any outstanding debt, and your current salary. A credit score is dynamic and can change positively or negatively depending upon how much debt you accrue and how you manage your bills. The factors that determine your credit score are called The Three C s of Credit Character, Capital & Capacity. 7

8 Character From your credit history, a lender may decide whether you possess the honesty and reliability to repay a debt. Considerations may include: Have you used credit before? Do you pay your bills on time? How long have you lived at your present address? How long have you been at your present job? 8

9 Capital A lender will want to know if you have valuable assets such as real estate, personal property, investments, or savings with which to repay debt if income is unavailable. What is Collateral (or Capital)? In lending agreements, collateral is a borrower s pledge of specific property to a lender, to secure repayment of a loan. The collateral serves as protection for a lender against a borrower s default that is, any borrower failing to pay the principal and interest under the terms of a loan obligation. If a borrower does default on a loan (due to insolvency or other event), that borrower forfeits (gives up) the property pledged as collateral and the lender then becomes the owner of the collateral. In a typical mortgage loan transaction, for instance, the real estate being acquired with the help of the loan serves as collateral. Should the buyer fail to pay the loan under the mortgage loan agreement, the ownership of the real estate is transferred to the bank. The bank uses a legal process called foreclosure to obtain real estate from a borrower who defaults on a mortgage loan obligation. A pawnbroker is an easy and common example of a business that may accept a wide range of items rather than just dealing with cash. 9

Is the job you have stable? Do you have a history in that line of work?")

10 Capacity What is Capacity? This refers to your ability to repay the debt. The lender will look to see if you have been working regularly in an occupation that is likely to provide enough income to support your credit use. The following questions may help the lender determine this: What is your current annual income? Do you make enough money to support your current and future liabilities (the 28/36 rule) Is the job you have stable? Do you have a history in that line of work? How many other loan payments do you have? (the 28/36 rule) What are your current living expenses? (rent? Living with family?) What are your current debts? (cars, credit cards, student loans?) How many dependents do you have? (Why?) 10

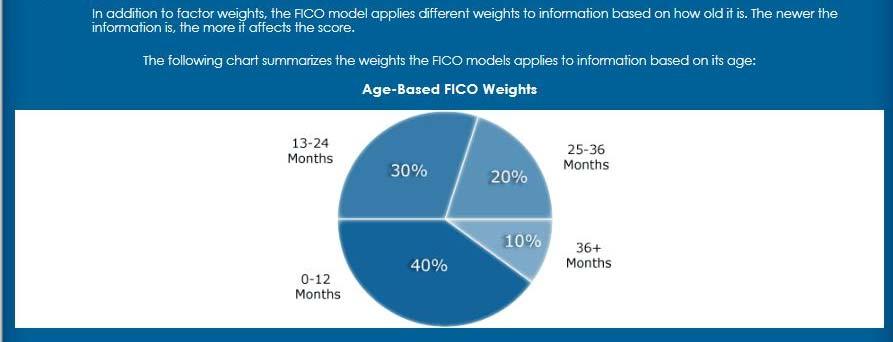

11 FICO Weights 11

12 Age of Information 12

13 Credit Myths 13

14 Challenges in my Career

15 What I Like About My Career Choice

16 A Typical Day In My Career

17 Building Financial Responsibility Age 14: Establish a savings account. For every dollar the child deposits, the parent matches. Funds cannot be withdrawn. This account is designed to save for the down payment on a car. Trust me - the vehicle will mean more when they have a vested interest.

18 Building Financial Responsibility Age 16: Car shop. The savings may not be enough. See if a community bank or credit union will allow the child to be on the loan to begin establishing credit history. Parent will need to be primary Borrower, but do NOT make the payments. Child will learn nothing unless they are responsible. If needed, pay them a weekly allowance that will cover the expense - but do not take care of it for them.

19 Building Financial Responsibility Age 18: Now a responsible adult. First, check credit history with free annual credit report to make sure no one has misused your information. You are not legally responsible if someone has used your information fraudulently before age 18 - just contact credit reporting agencies (you may have to provide proof of age). Start with a store credit card (Sears) or ask a parent to cosign a secured Visa. Charge $20 to $40 a month. Pay in full the minute the bill arrives. In approximately 6 months, open another account (gas, store or maybe by this point a Visa or Master Card). Charge $20 to $40 a month. Pay in full the minute the bill arrives.

20 Building Financial Responsibility Age 19: Open a small secured loan (car, if possible). Set up auto-pay so that it is always paid on time. If a car loan is not possible, apply for another unsecured account. Open one more credit line (Visa, MC, store, gas). Charge $20 to $40 a month. Pay in full the minute the bill arrives. With these 4 accounts - paid on time every month, a person can reach a great score (720ish) in no more than 2 years. Don't let the accounts go dormant. They have to be used - just don't ever max them out (that will lower your score). Use them for daily incidentals (food, gas, clothing) - as long as you pay them in full each month. Do not buy things you can't afford.

21 Motivations Of My Career

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

Chapter 10. Personal Loans and Purchasing Decisions Pearson Education, Inc. All rights reserved

Chapter 10 Personal Loans and Purchasing Decisions 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the key features and qualities of personal loans Explain the unique issues

Chapter 10 Personal Loans and Purchasing Decisions 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the key features and qualities of personal loans Explain the unique issues

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Shopping for an Automobile Loan. What Do I Need to Know?

Shopping for an Automobile Loan What Do I Need to Know? Automobiles 2 nd most expensive purchase for most consumers Usually purchased with Loan / credit Or cash if you have enough (uncommon) Ask yourself:

Shopping for an Automobile Loan What Do I Need to Know? Automobiles 2 nd most expensive purchase for most consumers Usually purchased with Loan / credit Or cash if you have enough (uncommon) Ask yourself:

Lesson 8 Borrowing Money

AOBF Financial Planning Lesson 8 Borrowing Money Student Resources Resource Description Student Resource 8.1 Reading: Why Borrow? Student Resource 8.2 Worksheet: Borrowing and Lending Terms Student Resource

AOBF Financial Planning Lesson 8 Borrowing Money Student Resources Resource Description Student Resource 8.1 Reading: Why Borrow? Student Resource 8.2 Worksheet: Borrowing and Lending Terms Student Resource

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Capacity Capital Collateral Credit history Character

Capacity Capital Collateral Credit history Character For advisor information only The 5 Cs of Credit Understanding credit qualification At B2B Bank, we know that you strive to provide your clients with

Capacity Capital Collateral Credit history Character For advisor information only The 5 Cs of Credit Understanding credit qualification At B2B Bank, we know that you strive to provide your clients with

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+ MODULE 4 // FINANCIAL SOCCER PROGRAM Financial Soccer is an educational video game designed to help students learn more about the fundamentals

MODULE 4 // HOW CREDITWORTHY ARE YOU? WORLD CLASS: AGES 18+ MODULE 4 // FINANCIAL SOCCER PROGRAM Financial Soccer is an educational video game designed to help students learn more about the fundamentals

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Secured and Unsecured (1)

") LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

LOANS The information contained in this document is for informational purposes only. The purpose of documents such as this is to promote general understanding and knowledge of various welfare topics. It

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

MODULE 7: Borrowing Basics PARTICIPANT GUIDE

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

Using Credit. services but do not require payments in full when the service is performed.

Using Credit How would you like to pay for this, cash or charge? Chances are you have heard this question asked. Cash or charge? is really asking you, the buyer, if you want to use the cash or the money

Using Credit How would you like to pay for this, cash or charge? Chances are you have heard this question asked. Cash or charge? is really asking you, the buyer, if you want to use the cash or the money

City of Plymouth Credit Union Ltd

Loan Requirement Details Purpose of Loan Loan Application Requested amount to be repaid Weekly Fortnightly Monthly 4-Weekly Repayment Method Standing Order Payroll Deduction Collection Point Office Benefit

Loan Requirement Details Purpose of Loan Loan Application Requested amount to be repaid Weekly Fortnightly Monthly 4-Weekly Repayment Method Standing Order Payroll Deduction Collection Point Office Benefit

MODULE 7: Borrowing Basics INSTRUCTOR GUIDE. MONEY SMART for Adults

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

MODULE 7: Borrowing Basics MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public confidence in

Borrowing Basics. FDIC Money Smart for Young Adults. Building: Knowledge, Security, Confidence

Borrowing Basics FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Define credit Explain why credit is important Identify three types of loans Identify the costs associated

Borrowing Basics FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Define credit Explain why credit is important Identify three types of loans Identify the costs associated

THE ECONOMY: PERSONAL FINANCES Financial literacy is an issue that should command our attention because many Americans are not adequately organizing

THE ECONOMY: PERSONAL FINANCES Financial literacy is an issue that should command our attention because many Americans are not adequately organizing finances for their education, healthcare, and retirement.

THE ECONOMY: PERSONAL FINANCES Financial literacy is an issue that should command our attention because many Americans are not adequately organizing finances for their education, healthcare, and retirement.

Maximizing Purchasing Power: Make the Most of Your Credit Score

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

When life happens... Maximizing Purchasing Power: Make the Most of Your Credit Score Consolidated Credit Counseling Services, Inc. 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 How

Teens. lesson seven. about credit

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

Borrowing. Evaluating the Benefits and Costs of Credit

Unit 9 Borrowing Lesson 9B: Evaluating the Benefits and Costs of Credit Rule 9: Pay on time and in full. While borrowing has both benefits and costs, at times it is an indication that something has gone

Unit 9 Borrowing Lesson 9B: Evaluating the Benefits and Costs of Credit Rule 9: Pay on time and in full. While borrowing has both benefits and costs, at times it is an indication that something has gone

Mortgages. Amount of Mortgage: difference between sale price and the down payment.

Mortgages Mortgage: a long-term installment loan for the purpose of buying a home. If payments are not made on the loan, the lender may take possession of the property. Down Payment: A percentage of the

Mortgages Mortgage: a long-term installment loan for the purpose of buying a home. If payments are not made on the loan, the lender may take possession of the property. Down Payment: A percentage of the

Settle in faster with RBC Newcomer Advantage. Banking made easy for newcomers to Canada

Settle in faster with RBC Newcomer Advantage Banking made easy for newcomers to Canada 1 RBC Royal Bank Banking made easy 2 10newcomers to Canada We know how important it is to choose the right banking

Settle in faster with RBC Newcomer Advantage Banking made easy for newcomers to Canada 1 RBC Royal Bank Banking made easy 2 10newcomers to Canada We know how important it is to choose the right banking

Introduction. Purpose. Student Introductions. Objectives (Continued) Objectives

Objectives") Introduction Instructor and student introductions Module overview Borrowing Basics 1 Borrowing Basics 2 Your name Student Introductions Expectations, questions, and concerns about borrowing money Purpose

Introduction Instructor and student introductions Module overview Borrowing Basics 1 Borrowing Basics 2 Your name Student Introductions Expectations, questions, and concerns about borrowing money Purpose

Presentation Slides. Lesson Four. Credit 04/09

Presentation Slides $ Lesson Four Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

Presentation Slides $ Lesson Four Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Student Loans And Credit: An Overview Tanya Tanaro, Manager Higher Education Partnerships, ASA

Student Loans And Credit: An Overview 12.14.15 Tanya Tanaro, Manager Higher Education Partnerships, ASA Agenda 2 Borrowing realities Credit reports and scores Student loan and credit card impact Conversation

Student Loans And Credit: An Overview 12.14.15 Tanya Tanaro, Manager Higher Education Partnerships, ASA Agenda 2 Borrowing realities Credit reports and scores Student loan and credit card impact Conversation

Essential Standard Understand business credit and risk management.

Essential Standard 5.00 Understand business credit and risk management. 1 Objective 5.01 Understand credit management 2 3 Topics Main types of credit Common advantages and disadvantages of businesses using

Essential Standard 5.00 Understand business credit and risk management. 1 Objective 5.01 Understand credit management 2 3 Topics Main types of credit Common advantages and disadvantages of businesses using

Advantages & Disadvantages to Using Credit

Advantages & Disadvantages to Using Credit Advantages to Using Credit Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing cheques Consolidates

Advantages & Disadvantages to Using Credit Advantages to Using Credit Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing cheques Consolidates

Building a strong credit history. A public education campaign brought to you by MasterCard

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Building a strong credit history A public education campaign brought to you by MasterCard Buying your first car, renting your first apartment, starting college, beginning your first real job master your

Chapter 25. What Is Credit? pp

What Is Credit? pp. 404-417 Learning Objectives After completing this chapter, you ll be able to: 1. Describe the nature of credit. 2. Explain the advantages and disadvantages of using credit. continued

What Is Credit? pp. 404-417 Learning Objectives After completing this chapter, you ll be able to: 1. Describe the nature of credit. 2. Explain the advantages and disadvantages of using credit. continued

Credit Guide. An introduction to credit and how it s used in your financial plan. Educators Credit Union. Shopper. Buyer. Planner. Spender.

Educators Credit Union Credit Guide An introduction to credit and how it s used in your financial plan. Shopper. Buyer. Planner. Spender. For the teacher in you. 262.886.5900 ecu.com Table of contents

Educators Credit Union Credit Guide An introduction to credit and how it s used in your financial plan. Shopper. Buyer. Planner. Spender. For the teacher in you. 262.886.5900 ecu.com Table of contents

In comparison, borrowing from a bank or building society is a business transaction with clearly defined rules to follow.

Teacher s notes money from friends/family People can borrow money from a friend or family member, in which case the arrangements for paying the money back are entirely up to the individuals. Although friends

Teacher s notes money from friends/family People can borrow money from a friend or family member, in which case the arrangements for paying the money back are entirely up to the individuals. Although friends

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC. Financial Literacy Workbook, Grades 9-12

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 Credit is a valuable commodity. Having the ability to borrow funds enables us to obtain things we would otherwise have to save years to afford: homes, cars, a college

Federal Reserve Bank of Philadelphia 1 Credit is a valuable commodity. Having the ability to borrow funds enables us to obtain things we would otherwise have to save years to afford: homes, cars, a college

Teens. lesson seven. about credit

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

Teens lesson seven about credit advantages and disadvantages of credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing checks

This helpful resource translates some commonly used financial terms into plain English.

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

Creditworthiness (UXL)

") Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

City of Plymouth Credit Union Ltd

Loan Requirement Details Purpose of Loan City of Plymouth Credit Union Ltd Personal Loan for New Members Application Requested amount to be repaid Monthly Fortnightly Weekly 4-Weekly Repayment Method Standing

Loan Requirement Details Purpose of Loan City of Plymouth Credit Union Ltd Personal Loan for New Members Application Requested amount to be repaid Monthly Fortnightly Weekly 4-Weekly Repayment Method Standing

Credit Education Program

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Presentation Notes Give Me Some Credit

Page1 Slide 1 : Page2 Slide 2 Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas Education Agency (TEA) and may not be reproduced without

Page1 Slide 1 : Page2 Slide 2 Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas Education Agency (TEA) and may not be reproduced without

Personal Financial Literacy

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

Personal Financial Literacy 7 Unit Overview Being financially literate means taking responsibility for learning how to manage your money. In this unit, you will learn about banking services that can help

Name Period. Finance charge Loan term Grace period Late fee Cash Advance Fee Prepayment Penalty Origination Fee Amortization Collateral Capital

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy

Name Period GOOD DEBT, BAD DEBT: USING CREDIT WISELY ACCELERATED Say you dream of buying a $15,000 car. Even if you saved $200 a month, it would still take you seven years to save what you needed to buy

INDEX. AMT (Alternative Minimum Tax), 20, 95

, 20, 95") Weston_Index.qxd 7/20/05 12:23 PM Page 201 INDEX A adjustable-rate mortgages, 79-80 airline-affiliated credit cards, 64 alimony payments, renegotiating, 172 all-in-one loans (construction loans), 101 Alternative

Weston_Index.qxd 7/20/05 12:23 PM Page 201 INDEX A adjustable-rate mortgages, 79-80 airline-affiliated credit cards, 64 alimony payments, renegotiating, 172 all-in-one loans (construction loans), 101 Alternative

Lending with a Purpose

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

Lending with a Purpose 7 Steps to Loaning Money to Family and Friends 2 Table of Contents Family and Friend Loans Risks and Rewards... 3 When it goes well... 3 When it goes bad... 3 A matter of trust...

Deciding which car and car loan you can afford

car loan you can afford In this simulation activity, students calculate monthly installment loan payments and total costs for three different cars to apply a common strategy for purchasing big-ticket items.

car loan you can afford In this simulation activity, students calculate monthly installment loan payments and total costs for three different cars to apply a common strategy for purchasing big-ticket items.

NEW HOME BUYER Guide

NEW HOME BUYER Guide???? 1. INITIAL CONSULTATION 8. CLEAR TO CLOSE 9. NUMBERS REVIEW 2. PRE-APPROVAL 7. CLOSING PACKAGE 10. CLOSING DAY! 3. FINDING YOUR HOME 6. UNDERWRITING APPROVAL 4. APPRAISAL 5. PROCESSING

NEW HOME BUYER Guide???? 1. INITIAL CONSULTATION 8. CLEAR TO CLOSE 9. NUMBERS REVIEW 2. PRE-APPROVAL 7. CLOSING PACKAGE 10. CLOSING DAY! 3. FINDING YOUR HOME 6. UNDERWRITING APPROVAL 4. APPRAISAL 5. PROCESSING

c» BALANCE c» Financially Empowering You Credit Matters Podcast

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Depository Institutions

1.7.3 Depository Institutions Grade Level 10-12 Take Charge of Your Finances Original Source: Shelly Stanton, Business Teacher, Billings West High School, Billings, MT Time to complete: 90 minutes National

1.7.3 Depository Institutions Grade Level 10-12 Take Charge of Your Finances Original Source: Shelly Stanton, Business Teacher, Billings West High School, Billings, MT Time to complete: 90 minutes National

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Pnc auto loan payoff amount

Pnc auto loan payoff amount 11. ETFCU's Platinum Rewards Credit Card Intro 0% for 6 billing cycles on balance transfers, NO FEE. How do I make my auto loan payment online?. Retrouvez tous les BONUS de

Pnc auto loan payoff amount 11. ETFCU's Platinum Rewards Credit Card Intro 0% for 6 billing cycles on balance transfers, NO FEE. How do I make my auto loan payment online?. Retrouvez tous les BONUS de

Credit Repair Company

6 Business Credit Secrets Every Credit Repair Company Should Know 6 Business Credit Secrets Every Credit Repair Company Should Know About Business Credit is credit that is obtained in a Business Name.

6 Business Credit Secrets Every Credit Repair Company Should Know 6 Business Credit Secrets Every Credit Repair Company Should Know About Business Credit is credit that is obtained in a Business Name.

Fresh Start. Living DebtFree. By Douglas Hoyes. BA, CA, CIRP, CBV, Licensed Insolvency Trustee. Co-Founder of

Fresh Start A Concise Guide to Living DebtFree By Douglas Hoyes BA, CA, CIRP, CBV, Licensed Insolvency Trustee Co-Founder of Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP,

Fresh Start A Concise Guide to Living DebtFree By Douglas Hoyes BA, CA, CIRP, CBV, Licensed Insolvency Trustee Co-Founder of Fresh Start A Concise Guide to Living Debt Free By Douglas Hoyes BA, CA, CIRP,

Homebuyer Guide Presented by:

Homebuyer Guide Presented by: HNB Mortgage 432-683-0081 www.hnbmortgage.com info@hnbmortgage.com Fax:(432)687-2612 NMLS: 205935 The basics What is a mortgage? A mortgage is a loan secured by real estate.

Homebuyer Guide Presented by: HNB Mortgage 432-683-0081 www.hnbmortgage.com info@hnbmortgage.com Fax:(432)687-2612 NMLS: 205935 The basics What is a mortgage? A mortgage is a loan secured by real estate.

Private Loans. Private Loans Get the big picture

Private Loans Private Loans Get the big picture How do I compare private loans? Let s say that you have exercised all other available options and decided that you must borrow a private loan to meet your

Private Loans Private Loans Get the big picture How do I compare private loans? Let s say that you have exercised all other available options and decided that you must borrow a private loan to meet your

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+ MODULE 4 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management

MODULE 4 // HOW CREDITWORTHY ARE YOU? HALL OF FAME: AGES 18+ MODULE 4 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial management

Money Matters: Making Cents of It All

Slide 1 Money Matters: Making Cents of It All Dollars and Sense Page1 Slide 2 Copyright Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas

Slide 1 Money Matters: Making Cents of It All Dollars and Sense Page1 Slide 2 Copyright Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas

For Further Information Money Smart for Young Adults Page 2 of 38

Table of Contents Money Smart for Young Adults Modules... 3 Your Guides... 3 Checking In... 5 Welcome... 5 Purpose... 5 Objectives... 5 Student Materials... 5 Pre-Assessment... 6 Borrowing Basics... 9

Table of Contents Money Smart for Young Adults Modules... 3 Your Guides... 3 Checking In... 5 Welcome... 5 Purpose... 5 Objectives... 5 Student Materials... 5 Pre-Assessment... 6 Borrowing Basics... 9

GLOSSARY OF LOAN TERMS

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

Economic Education for Consumers Chapter 10 Study Guide Credit: You re In Charge

Economic Education for Consumers Chapter 10 Study Guide Credit: You re In Charge Section 10.1 What is Credit? The ability to borrow money in return for a promise of future payment is When you are using

Economic Education for Consumers Chapter 10 Study Guide Credit: You re In Charge Section 10.1 What is Credit? The ability to borrow money in return for a promise of future payment is When you are using

CHAPTER 4 INTEREST RATES AND PRESENT VALUE

CHAPTER 4 INTEREST RATES AND PRESENT VALUE CHAPTER OBJECTIVES Once you have read this chapter you will understand what interest rates are, why economists delineate nominal from real interest rates, how

CHAPTER 4 INTEREST RATES AND PRESENT VALUE CHAPTER OBJECTIVES Once you have read this chapter you will understand what interest rates are, why economists delineate nominal from real interest rates, how

Determining how down payments affect loans

payments affect loans Students calculate how monthly payments for installment loans change based on the size of the down payment. Learning goals Big idea Installment loans can help people purchase big-ticket

payments affect loans Students calculate how monthly payments for installment loans change based on the size of the down payment. Learning goals Big idea Installment loans can help people purchase big-ticket

BUYERS GUIDE IMPORTANT THINGS TO CONSIDER WHEN BUYING A HOME COURTESY OF

BUYERS GUIDE IMPORTANT THINGS TO CONSIDER WHEN BUYING A HOME COURTESY OF OWNING MAKES SENSE When comparing the cost of owning a home to renting, there is more than the difference in house payment against

BUYERS GUIDE IMPORTANT THINGS TO CONSIDER WHEN BUYING A HOME COURTESY OF OWNING MAKES SENSE When comparing the cost of owning a home to renting, there is more than the difference in house payment against

Financial Math Project Math 118 SSII

SSII 2014 1 Name: Introduction: The goal of this project is for you to learn about the process of saving money, investing, and purchasing a home. For this project we will assume you finish your degree

SSII 2014 1 Name: Introduction: The goal of this project is for you to learn about the process of saving money, investing, and purchasing a home. For this project we will assume you finish your degree

Understanding. What you need to know about the most widely used credit scores

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Understanding What you need to know about the most widely used credit scores 300 850 The score lenders use. FICO Scores are the most widely used credit scores according to a recent CEB TowerGroup analyst

Presented by Dr. Rebecca Neumann for Academic Staff

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

If you're like most Americans, owning your own home is a major

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

How the Fannie Mae Foundation can help. If you're like most Americans, owning your own home is a major part of the American dream. The Fannie Mae Foundation wants to help you understand the steps you have

Lesson 5: Credit and Debt

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

Lesson 5: Credit and Debt debt: something owed to a person or an organization credit: the privilege granted to approved clients to receive goods or services and to pay for them in the future In February

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Reviewing C YouR CRedit RepoRt

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Module Four: Building Financial Foundations Homes, Loans and Automobiles

Financial Empowerment Curriculum Moving Ahead Through Financial Management Module Four: Building Financial Foundations Homes, Loans and Automobiles 1 Financial Empowerment Curriculum Module Five: Creating

Financial Empowerment Curriculum Moving Ahead Through Financial Management Module Four: Building Financial Foundations Homes, Loans and Automobiles 1 Financial Empowerment Curriculum Module Five: Creating

Closing Costs Explained

Closing Costs Explained When you apply for a home loan, you will receive a Good Faith Estimate of Settlement Charges, and a booklet that will explain these costs in detail. Loan Origination Fee: This fee

Closing Costs Explained When you apply for a home loan, you will receive a Good Faith Estimate of Settlement Charges, and a booklet that will explain these costs in detail. Loan Origination Fee: This fee

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

Understanding Your Credit Card Essentials

Understanding Your Credit Card Essentials 7.4.2.F1 Twenty-one year old Jenny felt rich when she received her first credit card during her junior year of college. She charged $2,500, her credit limit, the

Understanding Your Credit Card Essentials 7.4.2.F1 Twenty-one year old Jenny felt rich when she received her first credit card during her junior year of college. She charged $2,500, her credit limit, the

Personal Credit Fundamentals &

Personal Credit Fundamentals & Your Credit Score Presented by: Harvard University Employees Credit Union Harvard Student Sources of Financial Education Sources of consumer finance education Formal Program

Personal Credit Fundamentals & Your Credit Score Presented by: Harvard University Employees Credit Union Harvard Student Sources of Financial Education Sources of consumer finance education Formal Program

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards)

Texas Essential Knowledge and Skills (Prerequisite standards)") Lesson Description Students learn how to compare various small loans including easy access loans. Through the use of an online calculator, students determine the total repayment as well as the total interest

Lesson Description Students learn how to compare various small loans including easy access loans. Through the use of an online calculator, students determine the total repayment as well as the total interest

Making the Most of Your Money

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

The Newfi First-Time Homebuyer s Guide

The Newfi First-Time Homebuyer s Guide Newfi is a licensed tradename of Nexera Holding LLC. NMLS No. 1231327; HUD Lender ID 0038900004. Newfi is an Equal Housing Lender. The basics What is a mortgage?

The Newfi First-Time Homebuyer s Guide Newfi is a licensed tradename of Nexera Holding LLC. NMLS No. 1231327; HUD Lender ID 0038900004. Newfi is an Equal Housing Lender. The basics What is a mortgage?

Lesson 24 Annuities. Minds On

Lesson 24 Annuities Goals To define define and understand how annuities work. To understand how investments, loans and mortgages work. To analyze and solve annuities in real world situations (loans, investments).

Lesson 24 Annuities Goals To define define and understand how annuities work. To understand how investments, loans and mortgages work. To analyze and solve annuities in real world situations (loans, investments).

Lifetime Mortgage. Advantages You benefit from any future house price inflation.

Lifetime Mortgage What is it? Lifetime mortgages are one of the two main types of equity release. The other is a home reversion plan. A lifetime mortgage is a long term loan where you borrow money secured

Lifetime Mortgage What is it? Lifetime mortgages are one of the two main types of equity release. The other is a home reversion plan. A lifetime mortgage is a long term loan where you borrow money secured

Introduction The Goals and Nature of Credit Analysis

Chapter 1 Introduction The Goals and Nature of Credit Analysis Credit analysis is an art, not a science. The goal of credit analysis is to make a judgment about an obligor s ability and willingness to

Chapter 1 Introduction The Goals and Nature of Credit Analysis Credit analysis is an art, not a science. The goal of credit analysis is to make a judgment about an obligor s ability and willingness to

Credit and Debt.notebook August 28, 2014

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

BAFS Compulsory Part Basics of Personal Financial Management

Basics of Personal Financial Management Personal Financial Management - Technology Education Section Curriculum Development Institute Education Bureau, HKSARG April 2009 1 Discussion Having been working

Basics of Personal Financial Management Personal Financial Management - Technology Education Section Curriculum Development Institute Education Bureau, HKSARG April 2009 1 Discussion Having been working

Homebuyer Education TEST

To obtain the required Homebuyer Education Certificate through the Ohio Housing Finance Agency (OHFA), you will need to complete this test and related budget form. Once your loan is reserved, you may upload

To obtain the required Homebuyer Education Certificate through the Ohio Housing Finance Agency (OHFA), you will need to complete this test and related budget form. Once your loan is reserved, you may upload

Buying Your First Home: Three Steps to Successful Mortgage Shopping

ABCs of Mortgages Series Buying Your First Home: Three Steps to Successful Mortgage Shopping Smart mortgage decisions start here Note: FCAC s Mortgage Calculator tool, available at itpaystoknow.gc.ca,

ABCs of Mortgages Series Buying Your First Home: Three Steps to Successful Mortgage Shopping Smart mortgage decisions start here Note: FCAC s Mortgage Calculator tool, available at itpaystoknow.gc.ca,

BASIC FINANCIAL LITERACY. Economics Marshall High School Mr. Cline Unit Three DD

BASIC FINANCIAL LITERACY Economics Marshall High School Mr. Cline Unit Three DD * Nothing So Simple Has Ever Been So Hard Reconciling their account on a regular basis could have helped prevent this! Credit

BASIC FINANCIAL LITERACY Economics Marshall High School Mr. Cline Unit Three DD * Nothing So Simple Has Ever Been So Hard Reconciling their account on a regular basis could have helped prevent this! Credit

Rich Dad's Guide to Investing with Other People's Money

Rich Dad's Guide to Investing with Other People's Money Introduction One of the most important tools for gaining mastery of wealth and ensuring personal prosperity is Other People s Money or OPM. This

Rich Dad's Guide to Investing with Other People's Money Introduction One of the most important tools for gaining mastery of wealth and ensuring personal prosperity is Other People s Money or OPM. This

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

Copyright Texas Education Agency, All rights reserved.

Give Me Some Credit Copyright Texas Education Agency, 2012. These Materials are copyrighted and trademarked as the property of the Texas Education Agency (TEA) and may not be reproduced without the express

Give Me Some Credit Copyright Texas Education Agency, 2012. These Materials are copyrighted and trademarked as the property of the Texas Education Agency (TEA) and may not be reproduced without the express

Budgeting Module. a. True b. False

Budgeting Pretest 1. What is gross monthly pay? a. The monthly pay after taxes are deducted. b. The monthly pay before taxes and insurance are deducted. c. The hourly pay times 2080. 2. What is net monthly

Budgeting Pretest 1. What is gross monthly pay? a. The monthly pay after taxes are deducted. b. The monthly pay before taxes and insurance are deducted. c. The hourly pay times 2080. 2. What is net monthly

The steps to homeownership

Personal Banking Personal Banking Mortgage Mortgage The steps to homeownership A guide for first-time homebuyers Getting started. When you choose BMO Harris Bank for your mortgage, you ll get the resources

Personal Banking Personal Banking Mortgage Mortgage The steps to homeownership A guide for first-time homebuyers Getting started. When you choose BMO Harris Bank for your mortgage, you ll get the resources

PERSONAL FINANCE FINAL EXAM REVIEW. Click here to begin

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

PERSONAL FINANCE FINAL EXAM REVIEW Click here to begin FINAL EXAM REVIEW Once you work through the questions, you will have a good ideas of what will be on the final next week. Click here if you are too

BANKING & FINANCE (145)

") Page 1 of 9 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2018 Multiple Choice: (30 @ 2 points each) Financial Word Problems: (4 @ 3 points each) Parts of a Check: (6 @ 3 points each)

Page 1 of 9 Contestant Number: Time: Rank: BANKING & FINANCE (145) REGIONAL 2018 Multiple Choice: (30 @ 2 points each) Financial Word Problems: (4 @ 3 points each) Parts of a Check: (6 @ 3 points each)

Home Buyer Guide. Everything you need to know to help make buying your home easy and successful.

Home Buyer Guide Everything you need to know to help make buying your home easy and successful. Julie Jeffery Partner l Mortgage Agent DLC Elevation Mortgage C. 403.828.4832 Julie@elevationmortgage.ca

Home Buyer Guide Everything you need to know to help make buying your home easy and successful. Julie Jeffery Partner l Mortgage Agent DLC Elevation Mortgage C. 403.828.4832 Julie@elevationmortgage.ca

Understanding Debt Problems & Solutions

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

Understanding Debt Problems & Solutions The Debt Landscape 40% of Americans live on 110% of their income Total U.S. household debt = $11.2 trillion Finances are one of the top five causes of divorce Money

401(k) 529 plan a American Stock Exchange (ASE) annual fee annual percentage rate (APR) asset auto insurance b bad debt balance bank bankruptcy

529 plan a American Stock Exchange (ASE) annual fee annual percentage rate (APR) asset auto insurance b bad debt balance bank bankruptcy") 401(k) A retirement savings plan funded by employees and often matched by contributions from the employer; contributions are usually made before taxes and grow tax-free until withdrawn, although after-tax

401(k) A retirement savings plan funded by employees and often matched by contributions from the employer; contributions are usually made before taxes and grow tax-free until withdrawn, although after-tax

The person you authorise to hold your additional card will share your credit limit and you will receive one statement for both cards.

Website FAQs Applying for your card Who can apply for an AMIGO credit card? You can apply if you: Are over 18 years of age Have a regular income Are not bankrupt Are an Australian citizen or a permanent

Website FAQs Applying for your card Who can apply for an AMIGO credit card? You can apply if you: Are over 18 years of age Have a regular income Are not bankrupt Are an Australian citizen or a permanent

Mortgages. A mortgage from the Scottish. Opens lots of new doors

Mortgages A mortgage from the Scottish Opens lots of new doors Moving home made easy In branch experts Whether you re an existing customer or you re new to the Scottish, we value your business and we aim

Mortgages A mortgage from the Scottish Opens lots of new doors Moving home made easy In branch experts Whether you re an existing customer or you re new to the Scottish, we value your business and we aim