Evaluating the Credit Loss Estimates in M&A / Capital Raise Scenarios. David H. Ruffin Director DHG Credit Risk Management

|

|

|

- Flora Betty Taylor

- 5 years ago

- Views:

Transcription

1 Evaluating the Credit Loss Estimates in M&A / Capital Raise Scenarios David H. Ruffin Director DHG Credit Risk Management

2 Agenda (September 14, 2017) A decade of credit mark / portfolio loss estimates What do we mean by credit mark / loss estimate, etc.? The community bank conundrum: problem loans Quantitative & qualitative compares in M&A Questions

3 A decade of credit mark / portfolio loss estimates

4 Loan Portfolio Due Diligence (Loss Estimates) ~260 Due Diligence Transactions since '08 + Capital Raise 43% Data current as of Q M&A 47% Loss Share 10% Accurate and back-tested results Expertise in both sides: Credit Mark & Loan Review Efficient process 2-Phases to support Go / No-Go Decision Time Frame Range of Credit Marks* % % % Recent for CRMa / % DHG-CRM *Ranges only general estimates from CRM work and not necessarily representative of a national averages

5 Key Data Needed for Credible Loss Estimates Flat File (Interagency or Loan Data file) Impairment Calculations Past Due List flat file date Watch List/Special Assets Update Reports (detailed workout plans, etc.) Relationship Groupings TDR & Non-Accrual List Letters of Credit List Policy Manual with RG Definitions Look Back Study Loan data (i.e. core system download, snapshot ) at each month s end over a TBD month look back period ending on the Estimate Date ( Look Back Period ). Individual charge-offs and recoveries recorded, by note number, over the Look Back Period along with the date of the respective charge-off or recovery.* Impairments recorded by the Bank on loans evaluated under ASC 310, Receivables (formerly SFAS 114), by individual note number. *Individual charge-offs and recoveries should be produced as a list of "Note Number / Charge- Off Amount / Charge-Off Date" (with multiple partial charge downs being listed multiple times) or a list of "Note Number / Total Charge-Off Amount / First Charge-Off Date" (with multiple partial charge downs being aggregated).

6 What do we mean by credit mark / loss estimate, etc.?

7 What Do We Mean by the Following? Credit mark Portfolio loss estimate Yield mark Day one (valuation of loans at purchase) Day two CECL

8 The community bank conundrum: problem loans

9 NPA s Structurally Larger at Smaller Banks NPA S+90 PD / Tang Equity+ALLL (%) NCO s / Average Loans (%) Small Banks Big Banks Big Banks Small Banks Smaller Banks couldn t flush and made bet to keep more capital and more NPA s

10 Loan Portfolio Composition by Asset Size March 31, 2016 Small Institutions Larger Institutions 37% 63% Loans Tied To Real Estate Source FDIC

11 Smaller the Bank: Greater the Loss Given Default From Blind Pool Data

12 Possible Disproportionate CECL Impact? Community Banks have higher CECLrisk than industry as a whole Source FDIC

13 Quantitative & qualitative compares in M&A

14 M&A: Common Fears / Risks of Credit DD s Explaining easily to staff unlike capital raises Satisfying multiple suitors, wanting to do their own work Under-(or significantly over-) shooting the credit mark Confusing the credit and the accounting Navigating between the wink & nods and burn-downs Drilling down below call report data How bifurcated is risk / production? Using regulatory examinations as proxies for credit quality Short-cutting (or just estimating) the credit mark Syncing lending philosophies, delivery modes, and talent levels? Addressing the social issues conundrum objectively? Planning credible integration strategies

% Speculative RE Unmonitored C&I")

Traditional ratios (TDR s / NPL s / TDR s / Texas Ratio) Miss-read of Weighted Average Risk Grades OREO (low-to-medium loss rates w/")

15 What to Look for on a Bank s Balance Sheet Quality of Risk Management Transparency (not just relying on regulators / other audit functions) Bifurcation between production and risk Credit skills Board (involvement in the lending process & borrowing) % Speculative RE Unmonitored C&I History with stress testing Risk grade migrations Growth rates in loan types ALLL / new guidance (CECL) Losses imbedded in OLEM / Substandard (and Weak Pass) Traditional ratios (TDR s / NPL s / TDR s / Texas Ratio) Miss-read of Weighted Average Risk Grades OREO (low-to-medium loss rates w/ large pool remaining)

16 Portfolio: Granular Segmentation Granular model segmentation for both PD and LGD seeks to establish both risk homogeneity and meaningfulness for the bank. Segmentation typically along product / call report lines. Further sub-product segmentation if mix has varied over time. Migration performed by risk grade or delinquency cycle. A vintage-based segmentation may provide further differentiation across borrowers.

17 Another Use of Macro Data: Creating the Targeted Credit Mark or Loss Estimate A comprehensive loan review, combined with: Risk grade migrations Probabilities of default (PD s) Loss given default (LGD s) PD s X LGD s = EL (Estimated Losses) Probabilistic modeling Comparative analysis

18 The Sampling Process: Modern Loan Review Line of business / new loans / vintage / collateral type / perceived rogue lender or market Large exposures Risk-based Random

19 Risk Grade Migration Analysis

20 Loss Distribution Estimation and Stress Testing

")

21 M&A? Comparatives: PD s Commercial (2 Year)

22 LGD Parameter Quantification

23 M&A? Comparatives: LGD s

")

24 Comparatives: Discounted Potential Credit Loss ( dpcl ) Estimates

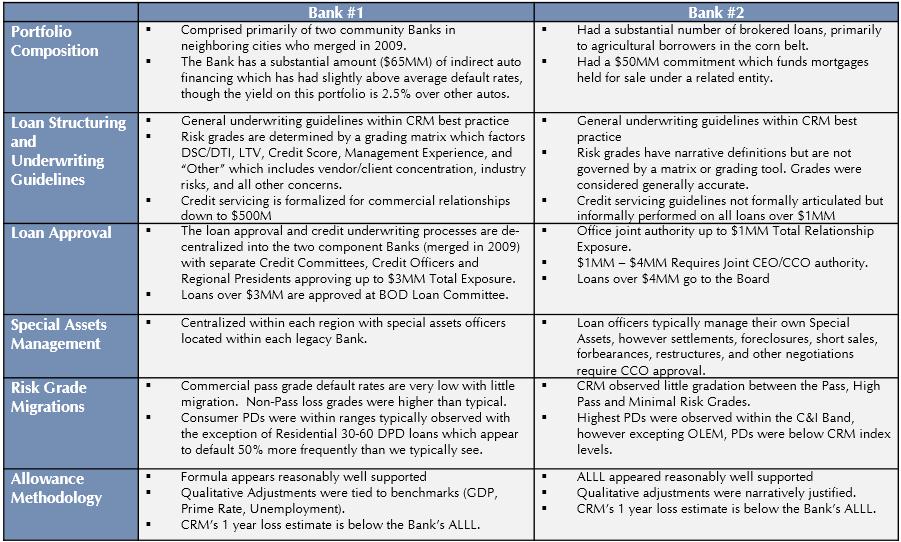

25 Risk Grade and Impairment Distribution

26 Policy Observations

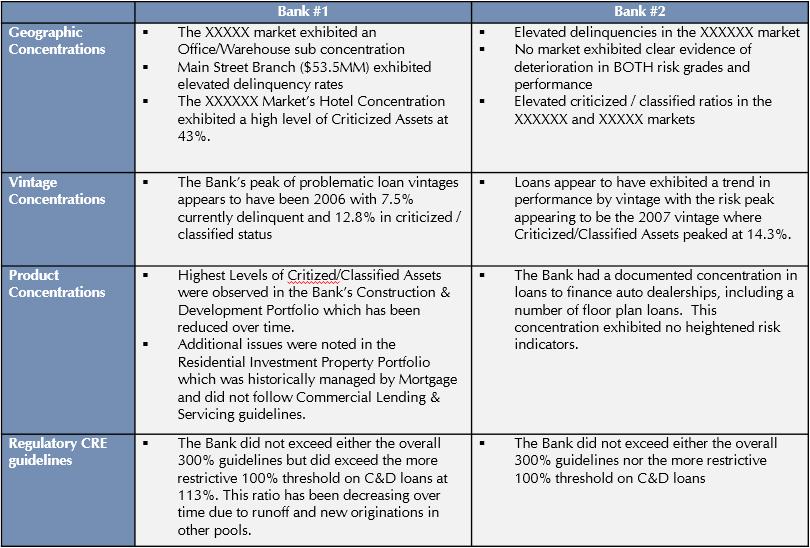

27 Concentration Comparison

28 Prospective Credit Culture Issues Impacting Merger Deliberations Create process for inventorying (horse-trading / best practices) each bank s: Credit policies Credit talent / redundancies Underwriting / delivery (hunter-skinner dynamic) Credit approval process Quality / format of loan review Pro-forma combined concentration (loan product / geographic) tolerances Pro-forma light DFAST impacts on Capital / IS / BS Hold on to classically trained/deep-experienced credit talent: it s a declining resource.

29 Conventional Due Diligence Process

30 Another Approach: Two Phase Due Diligence Phase I Remote Portfolio Assessment and Risk Identification Loss estimate modeling on bank(s) loan portfolios to develop PD s and LGD s and potential credit loss estimates based on the bank(s) own experience Credit Policy Observations Concentrations Portfolio Compositions Distribution of Risk Grades Phase II On-site Credit File Review with targeted sampling informed by Phase I Can be applied consistently to both banks in a potential MOE, or to one bank as part of a due diligence or reverse due diligence.

31 Time Line for Two Phase Due Diligence

32 Questions?

33 Contact Information

Loan Portfolio Management

Loan Portfolio Management Michael Wear 2016 1 2 ALLL Activity - Summary ($000) 2013 2014 2015 6/2016 Beginning 2,456 3,471 4,343 6,513 Balance Provisions 2,000 2,000 8,000 6,000 Net Charge-offs Ending

Loan Portfolio Management Michael Wear 2016 1 2 ALLL Activity - Summary ($000) 2013 2014 2015 6/2016 Beginning 2,456 3,471 4,343 6,513 Balance Provisions 2,000 2,000 8,000 6,000 Net Charge-offs Ending

ALLL Today: Challenges & Solutions.

ALLL Today: Challenges & Solutions. September 14 2016 ALLL Today: Challenges & Solutions. September 15, 2016 P R E S E N T E D B Y Tim McPeak Executive Risk Management Consultant Sageworks Agenda. Current

ALLL Today: Challenges & Solutions. September 14 2016 ALLL Today: Challenges & Solutions. September 15, 2016 P R E S E N T E D B Y Tim McPeak Executive Risk Management Consultant Sageworks Agenda. Current

All of the Method None of the Madness

CECL Simplified Current Expected Credit Losses ASU 2016-13 All of the Method None of the Madness The ProBank Austin 2017 Webinar Series November 9, 2017 11:00 AM ESDT Live Case Study - CECL I. Example

CECL Simplified Current Expected Credit Losses ASU 2016-13 All of the Method None of the Madness The ProBank Austin 2017 Webinar Series November 9, 2017 11:00 AM ESDT Live Case Study - CECL I. Example

Expanding Sensitivity Analysis and Stress Testing for CECL

Expanding Sensitivity Analysis and Stress Testing for CECL December 2016 Today s Speakers Michael L. Gullette, Vice President, Accounting and Financial Management, American Bankers Association Mike works

Expanding Sensitivity Analysis and Stress Testing for CECL December 2016 Today s Speakers Michael L. Gullette, Vice President, Accounting and Financial Management, American Bankers Association Mike works

ALLL and the New Estimate of Loan Losses

ALLL and the New Estimate of Loan Losses An update on the proposed impairment model and improving the measurement of credit losses MICH ARATEN, MANAGING DIRECTOR, CREDIT RISK CAPITAL ADVISORY CHRIS HENKEL,

ALLL and the New Estimate of Loan Losses An update on the proposed impairment model and improving the measurement of credit losses MICH ARATEN, MANAGING DIRECTOR, CREDIT RISK CAPITAL ADVISORY CHRIS HENKEL,

What are CECL gaps in the current ALLL process?

What are CECL gaps in the current ALLL process? Considerations for implementing the forthcoming Accounting for Financial Instruments: Credit Losses standard Zions Bancorporation Alexander Hume Controller

What are CECL gaps in the current ALLL process? Considerations for implementing the forthcoming Accounting for Financial Instruments: Credit Losses standard Zions Bancorporation Alexander Hume Controller

Are you prepared? FASB s CECL Model for Impairment Demystifying the Proposed Standard

Are you prepared? FASB s CECL Model for Impairment Demystifying the Proposed Standard Chad Kellar, CPA Senior Manager Crowe Horwath LLP Lauren Smith, CPA Senior Manager Primatics Financial Raj Mehra Executive

Are you prepared? FASB s CECL Model for Impairment Demystifying the Proposed Standard Chad Kellar, CPA Senior Manager Crowe Horwath LLP Lauren Smith, CPA Senior Manager Primatics Financial Raj Mehra Executive

M&A DILIGENCE CONSIDERATIONS: IS WHAT YOU SEE WHAT YOU GET

M&A DILIGENCE CONSIDERATIONS: IS WHAT YOU SEE WHAT YOU GET David W. Giesen Managing Director INTRODUCTION» Welcome Back.! Mergers and Acquisitions are back in vogue in Oregon and Washington after a couple

M&A DILIGENCE CONSIDERATIONS: IS WHAT YOU SEE WHAT YOU GET David W. Giesen Managing Director INTRODUCTION» Welcome Back.! Mergers and Acquisitions are back in vogue in Oregon and Washington after a couple

Cherry, Bekaert & Holland, L.L.P. The Allowance for Loan Losses and Current Credit Trends

Cherry, Bekaert & Holl, L.L.P. The Allowance for Loan Losses Current Cid Hickman, Partner, Industry Leader Services Group chickman@cbh.com www.cbh.com 919.782.1040 Agenda Current Bank Performance Framework,

Cherry, Bekaert & Holl, L.L.P. The Allowance for Loan Losses Current Cid Hickman, Partner, Industry Leader Services Group chickman@cbh.com www.cbh.com 919.782.1040 Agenda Current Bank Performance Framework,

Managing a Transition to a New ALLL Process

Managing a Transition to a New ALLL Process Chris Martin Manager Credit & Risk (ALLL) Synovus Financial Corp What is the ALLL? The Allowance for Losses on Loans and Leases (ALLL), originally referred to

Managing a Transition to a New ALLL Process Chris Martin Manager Credit & Risk (ALLL) Synovus Financial Corp What is the ALLL? The Allowance for Losses on Loans and Leases (ALLL), originally referred to

Current Expected Loss Model: A Practical Implementation Approach for Community Banks

Current Expected Loss Model: A Practical Implementation Approach for Community Banks David Heneke, CPA, CISA, Principal Liz Rider, CPA, Principal Investment advisory services are offered through CliftonLarsonAllen

Current Expected Loss Model: A Practical Implementation Approach for Community Banks David Heneke, CPA, CISA, Principal Liz Rider, CPA, Principal Investment advisory services are offered through CliftonLarsonAllen

Inside the new credit loss model

August 2016 Inside the new credit loss model Requirements and implementation considerations An article by Chad Kellar, CPA, and Matthew A. Schell, CPA, CFA Audit / Tax / Advisory / Risk / Performance Smart

August 2016 Inside the new credit loss model Requirements and implementation considerations An article by Chad Kellar, CPA, and Matthew A. Schell, CPA, CFA Audit / Tax / Advisory / Risk / Performance Smart

CECL: Data, Scenarios and Cash Flow Thoughts

CECL: Data, Scenarios and Cash Flow Thoughts H. Walter Young November 14, 2016 2016 Risk Management Association Annual Risk Management Conference Dallas, Texas Table of Contents I. Data: Not all data is

CECL: Data, Scenarios and Cash Flow Thoughts H. Walter Young November 14, 2016 2016 Risk Management Association Annual Risk Management Conference Dallas, Texas Table of Contents I. Data: Not all data is

Unravelling the Guidelines in Preparation for CECL (ASU ) 11/29/2016

11/29/2016") Unravelling the Guidelines in Preparation for CECL (ASU 2016-13) 11/29/2016 1 Today s Agenda Introductions CECL Overview Impact on the Institution i Calculation Methodologies Data Requirements Disclosure

Unravelling the Guidelines in Preparation for CECL (ASU 2016-13) 11/29/2016 1 Today s Agenda Introductions CECL Overview Impact on the Institution i Calculation Methodologies Data Requirements Disclosure

What will Basel II mean for community banks? This

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

MST Loan Loss Analyzer Platform for CECL

MST Loan Loss Analyzer Platform for CECL MST empowers financial institutions with confidence in their allowance estimations and transition to CECL through innovative software solutions, advisory services,

MST Loan Loss Analyzer Platform for CECL MST empowers financial institutions with confidence in their allowance estimations and transition to CECL through innovative software solutions, advisory services,

Corporate America Credit Union Annual Meeting Preparing for FASB Current Expected Credit Loss (CECL) Model April 2017

Model April 2017") Corporate America Credit Union Annual Meeting Preparing for FASB Current Expected Credit Loss (CECL) Model April 2017 Eve Rogers, Partner Atlanta, GA Merri Ellen Wadsworth, Senior Manager Atlanta, GA 2016

Corporate America Credit Union Annual Meeting Preparing for FASB Current Expected Credit Loss (CECL) Model April 2017 Eve Rogers, Partner Atlanta, GA Merri Ellen Wadsworth, Senior Manager Atlanta, GA 2016

Agenda. CECL Where are we and how did we get here? What is FASB s Expected Credit Loss Model? Expected Credit Loss Models - Challenges.

The CECL Model Agenda CECL Where are we and how did we get here? What is FASB s Expected Credit Loss Model? Expected Credit Loss Models - Challenges blank 2 Background Financial Crisis with credit as a

The CECL Model Agenda CECL Where are we and how did we get here? What is FASB s Expected Credit Loss Model? Expected Credit Loss Models - Challenges blank 2 Background Financial Crisis with credit as a

FedLinks. Connecting Policy with Practice. Expectations for Banks. How Examiners Assess the ALLL

FedLinks Connecting Policy with Practice ALLOWANCE FOR LOAN AND LEASE LOSSES JANUARY 2013 During periods of unstable financial conditions, meeting the supervisory expectations for maintaining an appropriate

FedLinks Connecting Policy with Practice ALLOWANCE FOR LOAN AND LEASE LOSSES JANUARY 2013 During periods of unstable financial conditions, meeting the supervisory expectations for maintaining an appropriate

CECL Modeling FAQs. CECL FAQs

CECL FAQs Moody s Analytics helps firms with implementation of expected credit loss and impairment analysis for CECL and other evolving accounting standards. We provide advisory services, data, economic

CECL FAQs Moody s Analytics helps firms with implementation of expected credit loss and impairment analysis for CECL and other evolving accounting standards. We provide advisory services, data, economic

CECL Time to Start Will Neeriemer, Partner DHG Financial Services. financial services

CECL Time to Start Will Neeriemer, Partner DHG Financial Services 1 About DHG DHG Financial Services, a national practice of Dixon Hughes Goodman, focuses on publicly traded and privately-held financial

CECL Time to Start Will Neeriemer, Partner DHG Financial Services 1 About DHG DHG Financial Services, a national practice of Dixon Hughes Goodman, focuses on publicly traded and privately-held financial

CECL: Current Expected Credit Loss

CECL: Current Expected Credit Loss Business Issues Forum May 1, 2018 Counselors of Real Estate Mid-Year Meeting Copyright 2017, Trepp LLC CECL What is it? Accounting Standard Update 2016-13, issued by

CECL: Current Expected Credit Loss Business Issues Forum May 1, 2018 Counselors of Real Estate Mid-Year Meeting Copyright 2017, Trepp LLC CECL What is it? Accounting Standard Update 2016-13, issued by

FASB s CECL Model: Navigating the Changes

FASB s CECL Model: Navigating the Changes Planning for Current Expected Credit Losses (CECL) By R. Chad Kellar, CPA, and Matthew A. Schell, CPA, CFA Audit Tax Advisory Risk Performance 1 Crowe Horwath

FASB s CECL Model: Navigating the Changes Planning for Current Expected Credit Losses (CECL) By R. Chad Kellar, CPA, and Matthew A. Schell, CPA, CFA Audit Tax Advisory Risk Performance 1 Crowe Horwath

Index. Managing Risks in Commercial and Retail Banking By Amalendu Ghosh Copyright 2012 John Wiley & Sons Singapore Pte. Ltd.

Index A absence of control criteria, as cause of operational risk, 395 accountability, 493 495 additional exposure, incremental loss from, 115 advances and loans, ratio of core deposits to, 308 309 advances,

Index A absence of control criteria, as cause of operational risk, 395 accountability, 493 495 additional exposure, incremental loss from, 115 advances and loans, ratio of core deposits to, 308 309 advances,

M a y 8, H o t e l N i k k o S a n F r a n c i s c o Aaron J. Axton

M a y 8, 2 0 1 7 H o t e l N i k k o S a n F r a n c i s c o Aaron J. Axton Managing Director, Depositories Investment Banking aaxton@kbw.com 415.591.5040 General Information and Limitations This presentation,

M a y 8, 2 0 1 7 H o t e l N i k k o S a n F r a n c i s c o Aaron J. Axton Managing Director, Depositories Investment Banking aaxton@kbw.com 415.591.5040 General Information and Limitations This presentation,

Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures

EBA/GL/2017/16 23/04/2018 Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures 1 Compliance and reporting obligations Status of these guidelines 1. This document contains

EBA/GL/2017/16 23/04/2018 Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures 1 Compliance and reporting obligations Status of these guidelines 1. This document contains

LOAN REVIEW PROGRAMS

LOAN REVIEW PROGRAMS GENERAL LOAN REVIEW Since CEIS Review s inception, the cornerstone of our business has been in providing top tier Independent Loan Review Programs for commercial lending institutions.

LOAN REVIEW PROGRAMS GENERAL LOAN REVIEW Since CEIS Review s inception, the cornerstone of our business has been in providing top tier Independent Loan Review Programs for commercial lending institutions.

Analyzing Current Loan Performance Under CECL. A Discussion Paper of the AMERICAN BANKERS ASSOCIATION. ABA Contact: Michael L.

Analyzing Current Loan Performance Under CECL A Discussion Paper of the AMERICAN BANKERS ASSOCIATION ABA Contact: Michael L. Gullette SVP Tax and Accounting mgullette@aba.com 202-663-4986 address the practical

Analyzing Current Loan Performance Under CECL A Discussion Paper of the AMERICAN BANKERS ASSOCIATION ABA Contact: Michael L. Gullette SVP Tax and Accounting mgullette@aba.com 202-663-4986 address the practical

How to Justify a Change in Your ALLL

How to Justify a Change in Your ALLL Ed Bayer, Managing Director Tim McPeak, Senior Risk Management Consultant Sageworks O - (919) 851-7474 F - (919) 851-6718 info@sageworks.com www.sageworksanalyst.com

How to Justify a Change in Your ALLL Ed Bayer, Managing Director Tim McPeak, Senior Risk Management Consultant Sageworks O - (919) 851-7474 F - (919) 851-6718 info@sageworks.com www.sageworksanalyst.com

Eye on the Prize: Accounting s Impact on the Bottom Line Gina Anderson and Sara Dopkin. financial services

Eye on the Prize: Accounting s Impact on the Bottom Line Gina Anderson and Sara Dopkin 1 Presenters: Gina Anderson and Sara Dopkin Gina has more than 18 years of experience specializing in audit and accounting

Eye on the Prize: Accounting s Impact on the Bottom Line Gina Anderson and Sara Dopkin 1 Presenters: Gina Anderson and Sara Dopkin Gina has more than 18 years of experience specializing in audit and accounting

The Journey to Implementation Continues

POINT OF VIEW The Journey to Implementation Continues Shifting from an Incurred Loss to an Expected Loss Model Current Expected Credit Loss (CECL) is a new accounting standard that will replace ASC 450-20

POINT OF VIEW The Journey to Implementation Continues Shifting from an Incurred Loss to an Expected Loss Model Current Expected Credit Loss (CECL) is a new accounting standard that will replace ASC 450-20

CECL Initial and Subsequent Measurement

CECL Initial and Subsequent Measurement About the Presenter Neekis Hammond, CPA Advisory Services www.sageworks.com Implementation Timelines. 1. SEC Filing Institutions. Implementation Timelines. 2. Non-SEC

CECL Initial and Subsequent Measurement About the Presenter Neekis Hammond, CPA Advisory Services www.sageworks.com Implementation Timelines. 1. SEC Filing Institutions. Implementation Timelines. 2. Non-SEC

NACUSAC Conference CECL Implementation and Impact to Capital Crowe Horwath LLP

NACUSAC Conference CECL Implementation and Impact to Capital 2018 Crowe Horwath LLP Agenda Session 1 CECL Overview CECL Standard Refresher Recent Regulatory Updates Session 2 - Practical Risk Assessment

NACUSAC Conference CECL Implementation and Impact to Capital 2018 Crowe Horwath LLP Agenda Session 1 CECL Overview CECL Standard Refresher Recent Regulatory Updates Session 2 - Practical Risk Assessment

Minding Your Ps and Qs: Strategic Q Factor Analysis for Today and Tomorrow

Minding Your Ps and Qs: Strategic Q Factor Analysis for Today and Tomorrow September 15, 2016 Mike Gullette, ABA mgullette@aba.com aba.com 1-800-BANKERS Your Presenter Mike Gullette ABA FASB CECL Roundtable

Minding Your Ps and Qs: Strategic Q Factor Analysis for Today and Tomorrow September 15, 2016 Mike Gullette, ABA mgullette@aba.com aba.com 1-800-BANKERS Your Presenter Mike Gullette ABA FASB CECL Roundtable

Stress Testing. Webinar: Dodd Frank Act Stress Test (DFAST) for $10-$50 billion banks. John Lankenau Vice President, Product Management

for $10-$50 billion banks. John Lankenau Vice President, Product Management") Stress Testing Webinar: Dodd Frank Act Stress Test (DFAST) for $10-$50 billion banks John Lankenau Vice President, Product Management John Lankenau Vice President of Product Management, Primatics Financial

Stress Testing Webinar: Dodd Frank Act Stress Test (DFAST) for $10-$50 billion banks John Lankenau Vice President, Product Management John Lankenau Vice President of Product Management, Primatics Financial

July 1, To: The Officer Responsible for Filing the Financial Statements of U.S. Nonbank Subsidiaries Held by Foreign Banking Organizations

33 LIBERTY STREET, NEW YORK, NY 10045-0001 PATRICIA SELVAGGI ASSISTANT VICE PRESIDENT July 1, 2013 To: The Officer Responsible for Filing the Financial Statements of U.S. Nonbank Subsidiaries Held by Foreign

33 LIBERTY STREET, NEW YORK, NY 10045-0001 PATRICIA SELVAGGI ASSISTANT VICE PRESIDENT July 1, 2013 To: The Officer Responsible for Filing the Financial Statements of U.S. Nonbank Subsidiaries Held by Foreign

CECL SUMMER GAMES Part 5: Key Disclosures & Reports 6/29/2017

CECL SUMMER GAMES Part 5: Key Disclosures & Reports 6/29/2017 1 CPE Credits Visible Equity and the content of this webinar is officially approved with the NASBA (National Association of State Boards of

CECL SUMMER GAMES Part 5: Key Disclosures & Reports 6/29/2017 1 CPE Credits Visible Equity and the content of this webinar is officially approved with the NASBA (National Association of State Boards of

Welcome to the participants of ICAI- Dubai Chapter on IFRS 9 Presentation

Welcome to the participants of ICAI- Dubai Chapter on IFRS 9 Presentation By Dr. Mohammad Belgami Director Corporate Finance International Dubai, Date: 15/10/2016 A word About. CFI A Grade 3 Licensee by

Welcome to the participants of ICAI- Dubai Chapter on IFRS 9 Presentation By Dr. Mohammad Belgami Director Corporate Finance International Dubai, Date: 15/10/2016 A word About. CFI A Grade 3 Licensee by

Allowance for Loan Losses A Practical Approach. May 19, 2013 Bart P. Ferrin, CPA Ferrin & Company, LLC

Allowance for Loan Losses A Practical Approach May 19, 2013 Bart P. Ferrin, CPA Ferrin & Company, LLC Accounting Standards Guidance FASB Guidance July 2010, the FASB issued Accounting Standards Update

Allowance for Loan Losses A Practical Approach May 19, 2013 Bart P. Ferrin, CPA Ferrin & Company, LLC Accounting Standards Guidance FASB Guidance July 2010, the FASB issued Accounting Standards Update

Accounting Update for Financial Institutions

2013 CliftonLarsonAllen LLP Accounting Update for Financial Institutions September 16, 2013 3:15 pm 4:15 pm 11 Topics 1. ALLL 2. TDRs 3. Acquired Loans 4. Other Real Estate Owned 5. Investments 6. Proposed

2013 CliftonLarsonAllen LLP Accounting Update for Financial Institutions September 16, 2013 3:15 pm 4:15 pm 11 Topics 1. ALLL 2. TDRs 3. Acquired Loans 4. Other Real Estate Owned 5. Investments 6. Proposed

CALHOUN BANKSHARES, INC. AND SUBSIDIARY GRANTSVILLE, WEST VIRGINIA CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT

GRANTSVILLE, WEST VIRGINIA CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2016 2 TABLE OF CONTENTS PAGE Independent Auditor s Report 3-4 Consolidated Balance Sheets 5 Consolidated

GRANTSVILLE, WEST VIRGINIA CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT DECEMBER 31, 2016 2 TABLE OF CONTENTS PAGE Independent Auditor s Report 3-4 Consolidated Balance Sheets 5 Consolidated

Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures

Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures European Banking Authority (EBA) www.managementsolutions.com Research and Development December Página 2017 1 List of

Guidelines on PD estimation, LGD estimation and the treatment of defaulted exposures European Banking Authority (EBA) www.managementsolutions.com Research and Development December Página 2017 1 List of

Basel III: Proposed Revisions to Standardized Approach to Credit Risk

BOARD OF GOVERNORS of the FEDERAL RESERVE SYSTEM Basel III: Proposed Revisions to Standardized Approach to Credit Risk Seminar for Senior Bank Supervisors from Emerging Economies October 30, 2017 Disclaimer

BOARD OF GOVERNORS of the FEDERAL RESERVE SYSTEM Basel III: Proposed Revisions to Standardized Approach to Credit Risk Seminar for Senior Bank Supervisors from Emerging Economies October 30, 2017 Disclaimer

Overview of ASC (CECL)

") Overview of ASC 326-20 (CECL) FASB Accounting Standards Update (ASU) 2016-13, Financial Instruments Credit Losses Topic 326 was approved in June 2016. FASB replaced the current incurred loss accounting

Overview of ASC 326-20 (CECL) FASB Accounting Standards Update (ASU) 2016-13, Financial Instruments Credit Losses Topic 326 was approved in June 2016. FASB replaced the current incurred loss accounting

Corporate CPM strategy in a down turn

Corporate CPM strategy in a down turn Investec corporate impairments seminar BANKING GROUP financial & operating review Jacques Mouton Head of Corporate Credit 20 November 2009 Agenda Setting the scene

Corporate CPM strategy in a down turn Investec corporate impairments seminar BANKING GROUP financial & operating review Jacques Mouton Head of Corporate Credit 20 November 2009 Agenda Setting the scene

Loan Portfolio Analysis. Agribusiness Finance LESE 306 Fall 2009

Loan Portfolio Analysis Agribusiness Finance LESE 306 Fall 2009 What is it? Focus is on the lender s existing loan portfolio. Looking for areas of strengths and weaknesses. Data mining at segment level

Loan Portfolio Analysis Agribusiness Finance LESE 306 Fall 2009 What is it? Focus is on the lender s existing loan portfolio. Looking for areas of strengths and weaknesses. Data mining at segment level

Navigating a sea change US Current Expected Credit Losses (CECL) survey

survey") Navigating a sea change US Current Expected Credit Losses (CECL) survey Foreword...1 Executive summary...2 Introduction...4 About the survey...5 A comprehensive CECL program...6 Implementation timetable

Navigating a sea change US Current Expected Credit Losses (CECL) survey Foreword...1 Executive summary...2 Introduction...4 About the survey...5 A comprehensive CECL program...6 Implementation timetable

Audit Tax Advisory Risk Performance Crowe Horwath LLP 1

PACB Annual Convention FASB s Current Expected Credit Loss (CECL) Model: Navigating the Changes September 28, 2015 Matthew Schell, Partner Crowe Horwath LLP Washington, DC 2015 Crowe Horwath LLP 1 Agenda

PACB Annual Convention FASB s Current Expected Credit Loss (CECL) Model: Navigating the Changes September 28, 2015 Matthew Schell, Partner Crowe Horwath LLP Washington, DC 2015 Crowe Horwath LLP 1 Agenda

STATE DEPARTMENT FEDERAL CREDIT UNION

FINANCIAL STATEMENTS (With Independent Auditor s Report Thereon) TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Condition... 3 Statements of Income...

FINANCIAL STATEMENTS (With Independent Auditor s Report Thereon) TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Condition... 3 Statements of Income...

Enhanced Disclosure Task Force 2015 Progress Report Appendix 4: Leading Practice Examples of EDTF Recommendations. October 2015

Enhanced Disclosure Task Force 2015 Progress Report Appendix 4: Leading Practice Examples of EDTF Recommendations October 2015 1 Table of Contents Page 1 General recommendations 4 2 Risk governance and

Enhanced Disclosure Task Force 2015 Progress Report Appendix 4: Leading Practice Examples of EDTF Recommendations October 2015 1 Table of Contents Page 1 General recommendations 4 2 Risk governance and

Estimating Credit Losses: Evaluating Loss Emergence Period and Qualitative Factors

Estimating Credit Losses: Evaluating Loss Emergence Period and Qualitative Factors INTRODUCTION The AICPA Audit and Accounting Guide Depository and Lending Institutions: Banks and Savings Institutions,

Estimating Credit Losses: Evaluating Loss Emergence Period and Qualitative Factors INTRODUCTION The AICPA Audit and Accounting Guide Depository and Lending Institutions: Banks and Savings Institutions,

Allowance for Loan Losses - Understanding CECL and Current Trends

2014 CliftonLarsonAllen LLP Presentation for the National Association of Federal Credit Unions Allowance for Loan Losses - Understanding CECL and Current Trends September 2, 2015 CLAconnect.com Today s

2014 CliftonLarsonAllen LLP Presentation for the National Association of Federal Credit Unions Allowance for Loan Losses - Understanding CECL and Current Trends September 2, 2015 CLAconnect.com Today s

RCAP jurisdictional assessments: self-reporting monitoring template for RCAP follow-up actions

RCAP jurisdictional assessments: self-reporting monitoring template for RCAP follow-up actions Jurisdiction: United States Status as of: 31 December 2016 With reference to RCAP report(s): Assessment of

RCAP jurisdictional assessments: self-reporting monitoring template for RCAP follow-up actions Jurisdiction: United States Status as of: 31 December 2016 With reference to RCAP report(s): Assessment of

Credit Modeling, CECL, Concentration, and Capital Stress Testing

Credit Modeling, CECL, Concentration, and Capital Stress Testing Presented by Wilary Winn Douglas Winn, President Brenda Lidke, Director Frank Wilary, Principal Matt Erickson, Director September 26, 2016

Credit Modeling, CECL, Concentration, and Capital Stress Testing Presented by Wilary Winn Douglas Winn, President Brenda Lidke, Director Frank Wilary, Principal Matt Erickson, Director September 26, 2016

2013 Financial Institutions Conference Loan Acquisition Accounting

2013 Financial Institutions Conference Loan Acquisition Accounting Today s Objectives Understand main drivers/inputs in initial valuation (Day 1) Understand how impact of those drivers/inputs impact go-forward

2013 Financial Institutions Conference Loan Acquisition Accounting Today s Objectives Understand main drivers/inputs in initial valuation (Day 1) Understand how impact of those drivers/inputs impact go-forward

Effective Credit Risk Management with ErmsCo Dual Risking Rating System

Executive Brief Effective Credit Risk Management with ErmsCo Dual Risking Rating System 2007-2012 ErmsCo Inc Intellectual Property. All Rights Reserved. 103 Introduction to ErmsCo About ErmsCo ErmsCo is

Executive Brief Effective Credit Risk Management with ErmsCo Dual Risking Rating System 2007-2012 ErmsCo Inc Intellectual Property. All Rights Reserved. 103 Introduction to ErmsCo About ErmsCo ErmsCo is

RCAP jurisdictional assessments: self-reporting monitoring template for RCAP follow-up actions

RCAP jurisdictional assessments: self-reporting monitoring template for RCAP follow-up actions Jurisdiction: United States Status as of: 31 December 2017 With reference to RCAP report(s): Assessment of

RCAP jurisdictional assessments: self-reporting monitoring template for RCAP follow-up actions Jurisdiction: United States Status as of: 31 December 2017 With reference to RCAP report(s): Assessment of

CECL: Adapting to Adopt

CECL: Adapting to Adopt Chris Henkel, Senior Director, Advisory Services Anna Krayn, Senior Director, Regulatory & Accounting Solutions April 2018 Speakers Christian Henkel Senior Director Advisory Services

CECL: Adapting to Adopt Chris Henkel, Senior Director, Advisory Services Anna Krayn, Senior Director, Regulatory & Accounting Solutions April 2018 Speakers Christian Henkel Senior Director Advisory Services

FINANCIAL ACCOUNTING STANDARDS BOARD: CURRENT EXPECTED CREDIT LOSS MODEL

FINANCIAL ACCOUNTING STANDARDS BOARD: CURRENT EXPECTED CREDIT LOSS MODEL WHAT WILL BE THE IMPACT? CAPSTONE PROJECT AMERICAN BANKERS ASSOCIATION STONIER GRADUATE SCHOOL OF BANKING PETER G. BAILEY PRIMATICS

FINANCIAL ACCOUNTING STANDARDS BOARD: CURRENT EXPECTED CREDIT LOSS MODEL WHAT WILL BE THE IMPACT? CAPSTONE PROJECT AMERICAN BANKERS ASSOCIATION STONIER GRADUATE SCHOOL OF BANKING PETER G. BAILEY PRIMATICS

Agenda on-site pre-application meeting INSTITUTION NAME Address (including city) DATE, start time / finish time

DATE, start time / finish time") Agenda on-site pre-application meeting INSTITUTION NAME Address (including city) DATE, start time / finish time The ECB would like to discuss with INSTITUTION NAME the pre-application process and the main

Agenda on-site pre-application meeting INSTITUTION NAME Address (including city) DATE, start time / finish time The ECB would like to discuss with INSTITUTION NAME the pre-application process and the main

CECL Workshop Vintage Method

CECL Workshop Vintage Method John J. Doherty, CPA MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2017 Wolf & Company, P.C. Introduction John J. Doherty Member of the Firm jdoherty@wolfandco.com

CECL Workshop Vintage Method John J. Doherty, CPA MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2017 Wolf & Company, P.C. Introduction John J. Doherty Member of the Firm jdoherty@wolfandco.com

A CECL Primer. About CECL

A CECL Primer Introduction The purpose of this paper is to provide a brief overview of Visible Equity s solution to CECL (Current Expected Credit Loss). Many facets of our CECL solution, such as the methods

A CECL Primer Introduction The purpose of this paper is to provide a brief overview of Visible Equity s solution to CECL (Current Expected Credit Loss). Many facets of our CECL solution, such as the methods

Accounting Update. John Rieger, Deputy Chief Accountant, Federal Deposit Insurance Corporation, Washington, DC

A Regulatory Update John Rieger, Deputy Chief Accountant, Federal Deposit Insurance Corporation, Washington, DC Caren Hill, CPA, Western District, Office of the Comptroller of the Currency, Denver CO Tullus

A Regulatory Update John Rieger, Deputy Chief Accountant, Federal Deposit Insurance Corporation, Washington, DC Caren Hill, CPA, Western District, Office of the Comptroller of the Currency, Denver CO Tullus

CECL ONE YEAR CLOSER

CECL ONE YEAR CLOSER Greg Clausen Partner Eide Bailly LLP Darrell Lingle Partner Eide Bailly LLP CECL One Year Closer to Implementation Greg Clausen, CPA Partner gclausen@eidebailly.com 515.875.7595 Darrell

CECL ONE YEAR CLOSER Greg Clausen Partner Eide Bailly LLP Darrell Lingle Partner Eide Bailly LLP CECL One Year Closer to Implementation Greg Clausen, CPA Partner gclausen@eidebailly.com 515.875.7595 Darrell

CECL: A Discussion. June 16, 2016 P R E S E N T E D B Y

CECL: A Discussion June 16, 2016 P R E S E N T E D B Y About Sageworks. Neekis Hammond Neekis specializes in ALLL - ASC 450-20 and ASC 310-10; CECL preparation and methodology; acquired loan accounting

CECL: A Discussion June 16, 2016 P R E S E N T E D B Y About Sageworks. Neekis Hammond Neekis specializes in ALLL - ASC 450-20 and ASC 310-10; CECL preparation and methodology; acquired loan accounting

Center for Plain English Accounting

Report February 22, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members The Current Expected Credit Loss (CECL) Model Are You Ready? Background

Report February 22, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members The Current Expected Credit Loss (CECL) Model Are You Ready? Background

Capital Buffer under Stress Scenarios in Multi-Period Setting

Capital Buffer under Stress Scenarios in Multi-Period Setting 0 Disclaimer The views and materials presented together with omissions and/or errors are solely attributable to the authors / presenters. These

Capital Buffer under Stress Scenarios in Multi-Period Setting 0 Disclaimer The views and materials presented together with omissions and/or errors are solely attributable to the authors / presenters. These

COUNTDOWN TO CECL: IS YOUR FINANCIAL INSTITUTION ON TRACK?

COUNTDOWN TO CECL: IS YOUR FINANCIAL INSTITUTION ON TRACK? Presented by: Scott Deters David Klopfer Katie Schnieber COUNTDOWN TO CECL: IS YOUR FINANCIAL INSTITUTION ON TRACK? Presented by: Scott Deters

COUNTDOWN TO CECL: IS YOUR FINANCIAL INSTITUTION ON TRACK? Presented by: Scott Deters David Klopfer Katie Schnieber COUNTDOWN TO CECL: IS YOUR FINANCIAL INSTITUTION ON TRACK? Presented by: Scott Deters

CECL Prep: Key Changes and Crafting an Implementation Plan.

CECL Prep: Key Changes and Crafting an Implementation Plan. May 16, 2016 PRESENTED BY Aaron Lenhart Senior Risk Management Consultant Sageworks Disclaimer. This presentation may include statements that

CECL Prep: Key Changes and Crafting an Implementation Plan. May 16, 2016 PRESENTED BY Aaron Lenhart Senior Risk Management Consultant Sageworks Disclaimer. This presentation may include statements that

Frequently Asked Questions: Supervisory Methodologies in CCAR 2012

Frequently Asked Questions: Supervisory Methodologies in CCAR 2012 On March 21 and March 22, 2012, the Federal Reserve held five industry outreach calls to provide the bank holding companies (BHCs) that

Frequently Asked Questions: Supervisory Methodologies in CCAR 2012 On March 21 and March 22, 2012, the Federal Reserve held five industry outreach calls to provide the bank holding companies (BHCs) that

CECL WHY IT S A BIG DEAL AND WHAT YOU NEED TO KNOW TO FULFILL YOUR OVERSIGHT ROLE. New Jersey Bankers Association Annual Conference May 2017

CECL WHY IT S A BIG DEAL AND WHAT YOU NEED TO KNOW TO FULFILL YOUR OVERSIGHT ROLE New Jersey Bankers Association Annual Conference May 2017 1 TODAY S PRESENTERS Faye Miller Partner, National Professional

CECL WHY IT S A BIG DEAL AND WHAT YOU NEED TO KNOW TO FULFILL YOUR OVERSIGHT ROLE New Jersey Bankers Association Annual Conference May 2017 1 TODAY S PRESENTERS Faye Miller Partner, National Professional

on credit institutions credit risk management practices and accounting for expected credit losses

EBA/GL/2017/06 20/09/2017 Guidelines on credit institutions credit risk management practices and accounting for expected credit losses 1 1. Compliance and reporting obligations Status of these guidelines

EBA/GL/2017/06 20/09/2017 Guidelines on credit institutions credit risk management practices and accounting for expected credit losses 1 1. Compliance and reporting obligations Status of these guidelines

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

FASB Releases the Final CECL Accounting Standard

FASB Releases the Final CECL Accounting Standard June 24, 2016 The Financial Accounting Standards Board s (FASB) latest Accounting Standards Update, ASU No. 2016-13, Financial Instruments Credit Losses

FASB Releases the Final CECL Accounting Standard June 24, 2016 The Financial Accounting Standards Board s (FASB) latest Accounting Standards Update, ASU No. 2016-13, Financial Instruments Credit Losses

TD BANK INTERNATIONAL S.A.

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

Bryn Mawr Bank Corporation Reports First Quarter Net Income of $9.0 Million, Improved Net Interest Margin

FOR RELEASE: IMMEDIATELY Frank Leto, President, CEO FOR MORE INFORMATION CONTACT: 610-581-4730 Mike Harrington, CFO 610-526-2466 Bryn Mawr Bank Corporation Reports First Quarter Net Income of $9.0 Million,

FOR RELEASE: IMMEDIATELY Frank Leto, President, CEO FOR MORE INFORMATION CONTACT: 610-581-4730 Mike Harrington, CFO 610-526-2466 Bryn Mawr Bank Corporation Reports First Quarter Net Income of $9.0 Million,

CECL: Update on Current Expected Credit Loss Approach By Dan St. Clair, Director, Audit Department

CECL: Update on Current Expected Credit Loss Approach By Dan St. Clair, Director, Audit Department Now that a year has passed since FASB issued Accounting Standards Update (ASU) No. 2016-13: Financial

CECL: Update on Current Expected Credit Loss Approach By Dan St. Clair, Director, Audit Department Now that a year has passed since FASB issued Accounting Standards Update (ASU) No. 2016-13: Financial

Here? CECL: Where Do We Go From. June 26, :45 to 12:45. Presented by:

CECL: Where Do We Go From Here? June 26, 2017 11:45 to 12:45 Presented by: Speaker Name Debbie Scanlon, Partner Gordon Dobner, Partner BKD, LLP 2800 Post Oak Boulevard Suite: 3200 Houston, TX 77056 P:

CECL: Where Do We Go From Here? June 26, 2017 11:45 to 12:45 Presented by: Speaker Name Debbie Scanlon, Partner Gordon Dobner, Partner BKD, LLP 2800 Post Oak Boulevard Suite: 3200 Houston, TX 77056 P:

PROPOSAL FOR A REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL. on prudential requirements for credit institutions and investment firms

EUROPEAN COMMISSION Brussels, 20.7.2011 COM(2011) 452 final PROPOSAL FOR A REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on prudential requirements for credit institutions and investment firms

EUROPEAN COMMISSION Brussels, 20.7.2011 COM(2011) 452 final PROPOSAL FOR A REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL on prudential requirements for credit institutions and investment firms

BMO Financial Corp Mid-Cycle Dodd-Frank Act Stress Test. Severely Adverse Scenario Results Disclosure

BMO Financial Corp. Mid-Cycle Dodd-Frank Act Stress Test Severely Adverse Scenario Results Disclosure October 22, Overview BMO Financial Corp. (BFC), a U.S. Intermediate Holding Company (IHC), is a wholly-owned

BMO Financial Corp. Mid-Cycle Dodd-Frank Act Stress Test Severely Adverse Scenario Results Disclosure October 22, Overview BMO Financial Corp. (BFC), a U.S. Intermediate Holding Company (IHC), is a wholly-owned

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Wells Fargo & Company. Basel III Pillar 3 Regulatory Capital Disclosures

Wells Fargo & Company Basel III Pillar 3 Regulatory Capital Disclosures For the quarter ended June 30, 2018 1 Table of Contents Disclosure Map.. 3 Introduction... 6 Executive Summary... 6 Company Overview

Wells Fargo & Company Basel III Pillar 3 Regulatory Capital Disclosures For the quarter ended June 30, 2018 1 Table of Contents Disclosure Map.. 3 Introduction... 6 Executive Summary... 6 Company Overview

CRE Concentrations: Practical Management Techniques

CRE Concentrations: Practical Management Techniques Tuesday, 6/27/2017 11:00:00 AM - 12:00:00 PM Presented by: Adam Mustafa Co-founder and Managing Partner Invictus Consulting Group 275 Madison Avenue,

CRE Concentrations: Practical Management Techniques Tuesday, 6/27/2017 11:00:00 AM - 12:00:00 PM Presented by: Adam Mustafa Co-founder and Managing Partner Invictus Consulting Group 275 Madison Avenue,

Frequently Asked Questions:

Frequently Asked Questions: CECL for Community Banks and Credit Unions What is the current expected credit loss (CECL)? The current expected credit loss (CECL) is a new GAAP accounting standard that will

Frequently Asked Questions: CECL for Community Banks and Credit Unions What is the current expected credit loss (CECL)? The current expected credit loss (CECL) is a new GAAP accounting standard that will

Supervisory Statement SS11/13 Internal Ratings Based (IRB) approaches. December 2013 (Updated November 2015)

approaches. December 2013 (Updated November 2015)") Supervisory Statement SS11/13 Internal Ratings Based (IRB) approaches December 2013 (Updated November 2015) Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority,

Supervisory Statement SS11/13 Internal Ratings Based (IRB) approaches December 2013 (Updated November 2015) Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority,

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics. Key Lending Issues from an Examiner Perspective

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

NCUA RLS Jerry Bonk 11/01/2016 3/10/ Lending Hot Topics Key Lending Issues from an Examiner Perspective Lending Hot Topics Credit Risk Related Items Concentration Risks & Trends Residential Real Estate

Securitization. Management exercises authority that should rest with the board or engages in activities that expose the institution to excessive risk.

Securitization Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

Securitization Standards Examiners should evaluate the above-captioned function against the following control and performance standards. The Standards represent control and performance objectives that

CECL Webinar Series: The Roadmap to Success. Irina Korablev, Senior Director Deniz Tudor, Director Anna Krayn, Senior Director

CECL Webinar Series: The Roadmap to Success Irina Korablev, Senior Director Deniz Tudor, Director Anna Krayn, Senior Director August 24, 2017 Moody s Analytics CECL Webinar Series: The Roadmap to Success

CECL Webinar Series: The Roadmap to Success Irina Korablev, Senior Director Deniz Tudor, Director Anna Krayn, Senior Director August 24, 2017 Moody s Analytics CECL Webinar Series: The Roadmap to Success

Asset Quality. Contents

Asset quality is a critical part of your financial analysis of an institution because it directly impacts the evaluation of other component areas such as capital, earnings, and liquidity. The assessment

Asset quality is a critical part of your financial analysis of an institution because it directly impacts the evaluation of other component areas such as capital, earnings, and liquidity. The assessment

PILLAR 3 REGULATORY CAPITAL DISCLOSURES

PILLAR 3 REGULATORY CAPITAL DISCLOSURES For the quarterly period ended Table of Contents Disclosure map Introduction Report overview Basel III overview Enterprise-wide risk management Risk governance

PILLAR 3 REGULATORY CAPITAL DISCLOSURES For the quarterly period ended Table of Contents Disclosure map Introduction Report overview Basel III overview Enterprise-wide risk management Risk governance

CECL Effective Date for Private Banks. A Discussion Paper of the AMERICAN BANKERS ASSOCIATION. ABA Contact: Michael L. Gullette

CECL Effective Date for Private Banks A Discussion Paper of the AMERICAN BANKERS ASSOCIATION ABA Contact: Michael L. Gullette SVP, Tax and Accounting mgullette@aba.com 202-663-4986 the practical and ongoing

CECL Effective Date for Private Banks A Discussion Paper of the AMERICAN BANKERS ASSOCIATION ABA Contact: Michael L. Gullette SVP, Tax and Accounting mgullette@aba.com 202-663-4986 the practical and ongoing

CP Draft Regulatory Technical Standards on the conditions to calculate KIRB in accordance with the purchased receivables approach

CP Draft Regulatory Technical Standards on the conditions to calculate KIRB in accordance with the purchased receivables approach Public hearing, 4 September 2018 Contents Mandate Optionality Flexibility

CP Draft Regulatory Technical Standards on the conditions to calculate KIRB in accordance with the purchased receivables approach Public hearing, 4 September 2018 Contents Mandate Optionality Flexibility

Leveraging Basel and Stress Testing Models for CECL and IFRS 9. Nihil Patel, Senior Director

Leveraging Basel and Stress Testing Models for CECL and IFRS 9 Nihil Patel, Senior Director October 2016 Moody s Analytics CECL webinar series 2016 Getting Ready for CECL Why Start Now? Recording now available

Leveraging Basel and Stress Testing Models for CECL and IFRS 9 Nihil Patel, Senior Director October 2016 Moody s Analytics CECL webinar series 2016 Getting Ready for CECL Why Start Now? Recording now available

FASB Financial Instruments Project

FASB Financial Instruments Project June 18, 2013 2:00 3:15 pm Presented by: Jean Joy, CPA Director of Financial Institutions Wolf & Company, P.C. 99 High Street Boston, MA 02110 P: (617) 428-5432 E: jjoy@wolfandco.com

FASB Financial Instruments Project June 18, 2013 2:00 3:15 pm Presented by: Jean Joy, CPA Director of Financial Institutions Wolf & Company, P.C. 99 High Street Boston, MA 02110 P: (617) 428-5432 E: jjoy@wolfandco.com

Accounting for Credit Losses, Where will the road end up?

Accounting for Credit Losses, Where will the road end up? PACB 137th ANNUAL CONFERENCE BARRY M. PELAGATTI, CPA Assurance Partner, BDO USA, LLP September 6, 2014 BDO USA, LLP, a Delaware limited liability

Accounting for Credit Losses, Where will the road end up? PACB 137th ANNUAL CONFERENCE BARRY M. PELAGATTI, CPA Assurance Partner, BDO USA, LLP September 6, 2014 BDO USA, LLP, a Delaware limited liability

ABBREVIATIONS... 4 GLOSSARY... 5 EXECUTIVE SUMMARY... 7 GUIDELINES FOR PROVISIONING... 8 RATIONALE AND OBJECTIVES... 8 STATUTORY AUTHORITY...

TABLE OF CONTENTS ABBREVIATIONS... 4 GLOSSARY... 5 EXECUTIVE SUMMARY... 7 GUIDELINES FOR PROVISIONING... 8 RATIONALE AND OBJECTIVES... 8 STATUTORY AUTHORITY... 10 SCOPE OF APPLICATION... 10 SUPERVISORY

TABLE OF CONTENTS ABBREVIATIONS... 4 GLOSSARY... 5 EXECUTIVE SUMMARY... 7 GUIDELINES FOR PROVISIONING... 8 RATIONALE AND OBJECTIVES... 8 STATUTORY AUTHORITY... 10 SCOPE OF APPLICATION... 10 SUPERVISORY

DISCLOSURE OF RESULTS OF STRESS TESTS UNDER THE DODD-FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT

DISCLOSURE OF RESULTS OF STRESS TESTS UNDER THE DODD-FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT Covering the period from January 1, 2016 through March 31, 2018 under a hypothetical, severely

DISCLOSURE OF RESULTS OF STRESS TESTS UNDER THE DODD-FRANK WALL STREET REFORM AND CONSUMER PROTECTION ACT Covering the period from January 1, 2016 through March 31, 2018 under a hypothetical, severely

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 9 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON INVESTMENT RISK MANAGEMENT OCTOBER 2004 This document was prepared by the Investments Subcommittee in consultation

Guidance Paper No. 9 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON INVESTMENT RISK MANAGEMENT OCTOBER 2004 This document was prepared by the Investments Subcommittee in consultation

Liquidity Coverage Ratio Information (Consolidated) Sumitomo Mitsui Financial Group, Inc. and Subsidiaries

Sumitomo Mitsui Financial Group, Inc. and Subsidiaries") Liquidity Coverage Ratio Information (Consolidated), Inc. and Subsidiaries Since, 2015, the Liquidity Coverage Ratio (hereinafter referred to as LCR ), the liquidity regulation under the Basel III, has

Liquidity Coverage Ratio Information (Consolidated), Inc. and Subsidiaries Since, 2015, the Liquidity Coverage Ratio (hereinafter referred to as LCR ), the liquidity regulation under the Basel III, has

ALVAREZ & MARSAL READINGS IN QUANTITATIVE RISK MANAGEMENT. Current Expected Credit Loss: Modeling Credit Risk and Macroeconomic Dynamics

ALVAREZ & MARSAL READINGS IN QUANTITATIVE RISK MANAGEMENT Current Expected Credit Loss: Modeling Credit Risk and Macroeconomic Dynamics CURRENT EXPECTED CREDIT LOSS: MODELING CREDIT RISK AND MACROECONOMIC

ALVAREZ & MARSAL READINGS IN QUANTITATIVE RISK MANAGEMENT Current Expected Credit Loss: Modeling Credit Risk and Macroeconomic Dynamics CURRENT EXPECTED CREDIT LOSS: MODELING CREDIT RISK AND MACROECONOMIC