Chapter 3: Diverse Paths to Growth

|

|

|

- Ralf Mills

- 5 years ago

- Views:

Transcription

1 Chapter 3: Diverse Paths to Growth Is wealthier healthier? Determinants of growth in health and education Inequality and HDI Market, State, and Institutions Microfinance

2 Economic Growth and Changes in Health and Education

3 Income, Life Expectancy and Education: Level Relationship

4 Income, Health, and Education There is strong positive association between level of income and level of education and health. There is a weak association between change in income and change in level of education and health. The apparent contradiction is resolved by the fact that there is strong association between level of income and level of education and health for high income (HDI) countries, but no association between level of income and level of education and health for low income (HDI) countries.

5 Reasons for Rapid Improvement in Health Outcomes for Low Income Countries 1. Rapid innovations in medicine and medical practices and their faster diffusion 2. International co-operation, education, and public awareness 3. Political reforms particularly expansion of democracy and participatory government

6 Reasons for Rapid Improvement in Educational Outcomes for Low Income Countries 1. Shift from agriculture to industry and services 2. Expansion of democracy 3. Increasing focus on equality 4. International co-operation

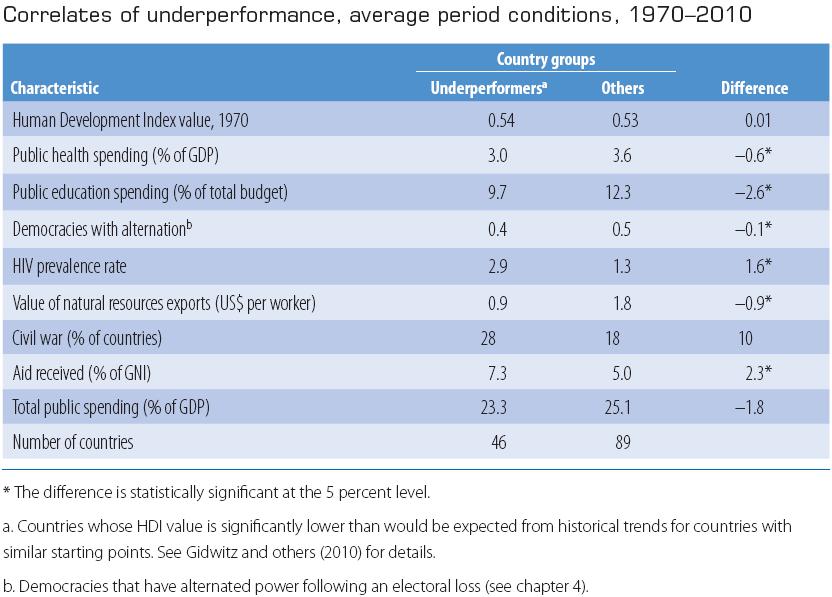

7 Factors of Underperformance

8 Factors Conducive for Faster Growth in HDI 1. Urbanization 2. Strong institutions: rule of law, quality of bureaucracy, ease of opening businesses, internal conflicts 3. Gender equity

9 Urbanization Natural Population Growth Migration from rural areas to urban areas: 1. Internal (within country) 2. External (from outside country)

10 Migration Pull Factors: Factors which make urban area attractive (more economic opportunities, better amenities, better infrastructure (physical and social)) Push Factors: Factors which make living in rural areas difficult (technological changes, natural calamities, environmental degradation, law and order etc.)

11 Agglomeration Effect of Urbanization 1. Agglomeration effect: Cost advantages to producers and consumers from location in cities, which take the forms of urbanization economies and localization economies. a. Urbanization economies: Agglomeration effects associated with the general growth of a concentrated geographical region. b. Localization economies: Agglomeration effects captured by particular sectors of the economy, such as finance or autos, as they grow within area. c. Emergence of industrial/financial clusters. d. Economies of scale (fall in cost as volume increases). It also affords division of labor i.e. people/work-force, firms can specialize according to their comparative advantage.

12 Pitfalls of Urbanization 1. Congestion effect: Limited land supply, higher cost of real estate, increased cost of providing facilities (transport, water, sanitation etc.). 2. Emergence of mega cities: Large cities by concentrating resources may adversely affect development of smaller cities (Urban Giantism Problem). 3. Emergence of Slums: A significant section of urban population living in bad conditions.

13 Policies to Reduce Inequality 1. Fiscal Policy: It refers to tax and government expenditure policies. There are two types of taxes: (i) Direct Tax: It is a tax whose incidence (or tax burden) cannot be shifted (e.g. income tax, corporate tax). (ii) Indirect Tax: It is a tax whose incidence (or tax burden) can be shifted (e.g. HST). Using progressive income taxes in which individuals with higher income pay larger proportion of their income as tax and poor individuals receive income subsidy can improve income distribution. Using taxes to finance goods and services used by poor (e.g. health, education, unemployment insurance etc.) can reduce inequality. Targeted transfers to poor households (food-stamp, social housing etc.) also reduces inequality.

14 Monetary and Financial Market Policies 2. Monetary and Financial Market Policies These policies refer to policies governing interest rate, banking, insurance, and other financial institutions. Poorer households have least access to financial institutions. Thus, they have to rely on informal sector (e.g. money-lenders, borrowing from relatives and friends) in order to meet their financial needs. The informal sector borrowing is usually inadequate and/or very costly. Poorer households are unable to receive loans from formal banking sector for variety of reasons: (i) lack of collateral (ii) lack of information about borrowers (credit history) (iii) weak enforcement of contracts (iv) high monitoring cost and (v) asymmetric information Asymmetric information is of two types: (i) adverse selection: lenders do not know the true ability of borrowers or true quality of projects (hidden quality) (ii) moral hazard (hidden action): lenders are not able to observe the efforts or actions of borrowers. Improving access of poorer households to financial sector increases their productive capacity and goes a long way in reducing inequality.

15 Informal Credit Market Sources of Demand for Credit: (1) Fixed Capital: Investment made in capital stock (machines, buildings etc.). They increase the production capacity. (2) Working Capital: Credit required to meet ongoing cost of production (wages, purchase of inputs etc.). (3) Consumption Credit: Credit required to meet increase in expenditure (e.g. health cost, wedding expenses, death etc.) or shortfall in income (e.g. crop failure, unemployment).

16 Informal Credit Market Supply of Credit (1) Institutional Lenders (2) Informal Lenders (e.g. Money Lender, Landlord)

17 Characteristics of Informal Credit Market (1) Informational Constraints: a) Adeverse Selection b) Moral Hazard c) Enforcement Problems (2) Segmentation: Many credit relationships are personalized and take time to build up. Typically, a moneylender serves a fixed clientele, whose members he lends to on a repeated basis. Usually, they do not lend individuals outside this circle. (3) Interlinked Credit Transactions: Typically, lender and borrower interact with each other in many markets (product market, labor market).

18 Characteristics of Informal Credit Market (4) Interest Rate Variation: Due to segmentation informal interest rates on loans vary a great deal (geographical location, sources of funds, characteristics of the borrowers). (5) Rationing: These markets are characterized by widespread rationing: upper limits on how much a borrower can receive. (6) Exclusivity: Moneylenders typically dislike situations in which their borrowers are borrowing from more than a single source.

19 Informal Credit Market Why money lenders succeed where formal banking sector does not? (1) Superior Information (2) Better Enforcement (3) Wide Variety of Collateral

20 Micro-Finance Microfinance refers to financial services, particularly but not only credit, supplied in small allotments to people who might otherwise have no access to them or have access only on very unfavorable terms. Microfinance institution: A bank or NGO that provides microfinance, particularly to the poor.

21 The Grameen Bank of Bangladesh The Grameen Bank was started by Dr. Muhamad Yunus, an economist, in mid- 70 s in order to provide loans and other financial services to the poor. His research showed that the lack of access to credit on the part of poor was one of key constraints in improving their condition. He wanted to demonstrate that it was possible to lend to the poor without collateral and poor are good risks. Today the bank has over 6 million borrowers and its success has led to rapid expansion of microfinance institutions all around the world. The bank mainly lends to women. Nearly, 97% of its borrowers are women. Borrowers are generally limited to those who own less than half an acre of land. On average the bank charges interest rate of 12% per-annum on loans. Despite lending to poor without collateral, the repayment rate of loan is 97%. Dr. Yunus was awarded the Nobel Peace Prize in 2006 for his pioneering work.

22 Group Lending and the Use of Information In order to borrow from the bank, borrowers have form a group (usually of four). Money is lent sequentially to the group. One borrower is first lent the money and only if she repays the loan, the loan is given to the next member and so on. In the case, a member of the group defaults, the entire group is excluded from future borrowing.

23 Group Lending and the Use of Information The formation of group and the sequential lending solves many of the informational problems faced by the formal banks and reduces the cost of monitoring and default due to: 1. Positive assortative matching: Borrowers have incentive to form a good group. It reduces adverse selection problem. 2. Peer monitoring: If a member borrows, other members have incentive to monitor the borrower. It reduces moral hazard problem. 3. Collateral: Since other members of the group require credit, their requirement of credit serves as collateral. In other words, other members serve as guarantors of the loan.

24 Performance of Micro-Finance (1) Does it pull out poor households out of poverty permanently? Answer Varies. In Bangladesh, micro-finance seems to have lasting impact on poor households. But evidence from Thailand and India suggests only temporary and small effects on poor households. (2) To what extent it serves only better-off sections of the poor and leaves out the ``core poor". Most of the empirical evidence suggests that micro-finance institutions mainly benefit relatively ``better-off" poor. These institutions either do not lend to very poor due relatively high risk of default and also very poor do not approach these institutions due relatively high interest rate and high cost of default.

25 Performance of Micro-Finance (3) Is it a cost-effective means of transferring income to the poor? Results vary. Most micro-finance institutions require subsidy either from the government, development, or aid agencies. In some cases (e.g. Grameen Bank) these subsidies have been found to be cost-effective, but not in all cases. (4) Mission Drift: See the article by Dr. Yunus in New York Times.

26 Labor Market Policies Introduction of minimum wage Unemployment Insurance Policies to reduce discrimination in labor market particularly against women and indigenous people

27 Role of Market and State in Human Development 1. There is enormous heterogeneity in the experiences of high growth countries. In some successful countries, states have played a leading role in the provision of education and health. In other successful countries, markets provide these services. 2. Both markets and state are complementary. Markets do not operate in vacuum. Poorly regulated markets can cause enormous damages (e.g. recent Gulf oil spill-over, financial crisis) 3. Every society needs institutions to ensure and enforce basic property rights and uphold rule of law. These are typically provided by states.

Recent Developments In Microfinance. Robert Lensink

Recent Developments In Microfinance Robert Lensink Myth 1: MF is about providing loans. Most attention to credit. Credit: Addresses credit constraints However, microfinance is the provision of diverse

Recent Developments In Microfinance Robert Lensink Myth 1: MF is about providing loans. Most attention to credit. Credit: Addresses credit constraints However, microfinance is the provision of diverse

Development Economics 855 Lecture Notes 7

Development Economics 855 Lecture Notes 7 Financial Markets in Developing Countries Introduction ------------------ financial (credit) markets important to be able to save and borrow: o many economic activities

Development Economics 855 Lecture Notes 7 Financial Markets in Developing Countries Introduction ------------------ financial (credit) markets important to be able to save and borrow: o many economic activities

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble MBA - I, Finance What is Microfinance? Microfinance is the supply of loans, savings, and other basic financial services to the

Microfinance Demonstration of at the bottom of pyramid theory Dipti Kamble MBA - I, Finance What is Microfinance? Microfinance is the supply of loans, savings, and other basic financial services to the

Financial markets in developing countries (rough notes, use only as guidance; more details provided in lecture) The role of the financial system

The role of the financial system") Financial markets in developing countries (rough notes, use only as guidance; more details provided in lecture) The role of the financial system matching savers and investors (otherwise each person needs

Financial markets in developing countries (rough notes, use only as guidance; more details provided in lecture) The role of the financial system matching savers and investors (otherwise each person needs

Ex ante moral hazard on borrowers actions

Lecture 9 Capital markets INTRODUCTION Evidence that majority of population is excluded from credit markets Demand for Credit arises for three reasons: (a) To finance fixed capital acquisitions (e.g. new

Lecture 9 Capital markets INTRODUCTION Evidence that majority of population is excluded from credit markets Demand for Credit arises for three reasons: (a) To finance fixed capital acquisitions (e.g. new

Development Economics 455 Prof. Karaivanov

Development Economics 455 Prof. Karaivanov Notes on Credit Markets in Developing Countries Introduction ------------------ credit markets intermediation between savers and borrowers: o many economic activities

Development Economics 455 Prof. Karaivanov Notes on Credit Markets in Developing Countries Introduction ------------------ credit markets intermediation between savers and borrowers: o many economic activities

Credit Lecture 23. November 20, 2012

Credit Lecture 23 November 20, 2012 Operation of the Credit Market Credit may not function smoothly 1. Costly/impossible to monitor exactly what s done with loan. Consumption? Production? Risky investment?

Credit Lecture 23 November 20, 2012 Operation of the Credit Market Credit may not function smoothly 1. Costly/impossible to monitor exactly what s done with loan. Consumption? Production? Risky investment?

Asha for Education Fellowship Application Form

Asha for Education Fellowship Application Form SECTION I: Personal Contact Information Name : Sanju Kumar Address : H.No.144, 2 nd Cross, Behind Bus Stand C.I.B Colony, Gulbarga-585104 Karnataka State,

Asha for Education Fellowship Application Form SECTION I: Personal Contact Information Name : Sanju Kumar Address : H.No.144, 2 nd Cross, Behind Bus Stand C.I.B Colony, Gulbarga-585104 Karnataka State,

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT Summary A new World Bank policy research report (PRR) from the Finance and Private Sector Research team reviews

FINANCE FOR ALL? POLICIES AND PITFALLS IN EXPANDING ACCESS A WORLD BANK POLICY RESEARCH REPORT Summary A new World Bank policy research report (PRR) from the Finance and Private Sector Research team reviews

Journal of Global Economics

$ Journal of Global Economics Research Article Journal of Global Economics Selvaraj, J Glob Econ 2016, 4:4 DOI: OMICS Open International Access Impact of Micro-Credit on Economic Empowerment of Women in

$ Journal of Global Economics Research Article Journal of Global Economics Selvaraj, J Glob Econ 2016, 4:4 DOI: OMICS Open International Access Impact of Micro-Credit on Economic Empowerment of Women in

Ghana : Financial services for women entrepreneurs in the informal sector

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized No. 136 June 1999 Findings occasionally reports on development initiatives not assisted

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized No. 136 June 1999 Findings occasionally reports on development initiatives not assisted

The Role of Microfinance on Poverty Alleviation and Its Impacts on People and Society: Evidence From the Grameen Bank

The Role of Microfinance on Poverty Alleviation and Its Impacts on People and Society: Evidence From the Grameen Bank Muhammad Umar sultan Waqas Umar Latif Sana Ullah Rana Muhammad Sohail Jafar Safdar

The Role of Microfinance on Poverty Alleviation and Its Impacts on People and Society: Evidence From the Grameen Bank Muhammad Umar sultan Waqas Umar Latif Sana Ullah Rana Muhammad Sohail Jafar Safdar

OUR MicroLending. Changes in US & Cuba: The impact on Florida. Opening doors to your future. The Microcredit Impact October 13, 2011

OUR MicroLending Opening doors to your future Changes in US & Cuba: The impact on Florida The Microcredit Impact October 13, 2011 The Question: What People know about Microcredit? That somewhere near India

OUR MicroLending Opening doors to your future Changes in US & Cuba: The impact on Florida The Microcredit Impact October 13, 2011 The Question: What People know about Microcredit? That somewhere near India

Impact of Deprived Sector Credit Policy on Micro Financing Presented by Nepal Rastra Bank

Impact of Deprived Sector Credit Policy on Micro Financing Presented by Nepal Rastra Bank Introduction: The deprived sector credit policy is directed credit policy of Nepal Rastra Bank, which is designed

Impact of Deprived Sector Credit Policy on Micro Financing Presented by Nepal Rastra Bank Introduction: The deprived sector credit policy is directed credit policy of Nepal Rastra Bank, which is designed

WTO: The Question of Microfinance in LEDCs Cambridge Model United Nations 2018

Study Guide: The Question of Microfinance in LEDCs Committee: World Trade Organisation Topic: The Question of Microfinance in LEDC s Introduction: Micro financing has been used as a way of helping those

Study Guide: The Question of Microfinance in LEDCs Committee: World Trade Organisation Topic: The Question of Microfinance in LEDC s Introduction: Micro financing has been used as a way of helping those

BANKING WITH THE POOR

BANKING WITH THE POOR - Self Help Group Approach in India. by Ashok Kumar Valaboju M.Sc (Agric.), MBA, CAIIB Senior Branch Manager, Andhra Bank, Gurazala branch, Guntur Dist AP- India India has been fast

BANKING WITH THE POOR - Self Help Group Approach in India. by Ashok Kumar Valaboju M.Sc (Agric.), MBA, CAIIB Senior Branch Manager, Andhra Bank, Gurazala branch, Guntur Dist AP- India India has been fast

Credit II Lecture 25

Credit II Lecture 25 November 27, 2012 Operation of the Credit Market Last Tuesday I began the discussion of the credit market (Chapter 14 in Development Economics. I presented material through Section

Credit II Lecture 25 November 27, 2012 Operation of the Credit Market Last Tuesday I began the discussion of the credit market (Chapter 14 in Development Economics. I presented material through Section

SAMRUDHI Micro Fin Society (SMS) Brief Profile

Brief Profile") SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

SAMRUDHI Micro Fin Society (SMS) Brief Profile 1 The Problem Sixty percent of the population in India lives below poverty line and they suffers from high rates of hunger and malnutrition. To cope with

EVALUATIONS OF MICROFINANCE PROGRAMS

REPUBLIC OF SOUTH AFRICA GOVERNMENT-WIDE MONITORING & IMPACT EVALUATION SEMINAR EVALUATIONS OF MICROFINANCE PROGRAMS SHAHID KHANDKER World Bank June 2006 ORGANIZED BY THE WORLD BANK AFRICA IMPACT EVALUATION

REPUBLIC OF SOUTH AFRICA GOVERNMENT-WIDE MONITORING & IMPACT EVALUATION SEMINAR EVALUATIONS OF MICROFINANCE PROGRAMS SHAHID KHANDKER World Bank June 2006 ORGANIZED BY THE WORLD BANK AFRICA IMPACT EVALUATION

Credit Markets in Africa

Credit Markets in Africa Craig McIntosh, UCSD African Credit Markets Are highly segmented Often feature vibrant competitive microfinance markets for urban small-trading. However, MF loans often structured

Credit Markets in Africa Craig McIntosh, UCSD African Credit Markets Are highly segmented Often feature vibrant competitive microfinance markets for urban small-trading. However, MF loans often structured

in Italy An international case study Tommaso Busini i General Manager European Union Experts (

Microcredit & Microfinance in Italy An international case study Tommaso Busini i General Manager European Union Experts (www.euexperts.eu) What is Microcredit? «The extension of small loans to low-income

Microcredit & Microfinance in Italy An international case study Tommaso Busini i General Manager European Union Experts (www.euexperts.eu) What is Microcredit? «The extension of small loans to low-income

The Strategy for Development of the. Microfinance Sector in Sudan. A Central Bank Initiative

The Strategy for Development of the Microfinance Sector in Sudan A Central Bank Initiative Abda Y. El-Mahdi Managing Director Unicons Consultancy Ltd. The Status of the Microfinance Sector in Sudan A growing

The Strategy for Development of the Microfinance Sector in Sudan A Central Bank Initiative Abda Y. El-Mahdi Managing Director Unicons Consultancy Ltd. The Status of the Microfinance Sector in Sudan A growing

Development Economics

Development Economics Development Microeconomics (by) Bardhan and Udry Chapter 7 Rural credit markets [1] Importance Smoothing consumption in an environment where production is risky and insurance markets

Development Economics Development Microeconomics (by) Bardhan and Udry Chapter 7 Rural credit markets [1] Importance Smoothing consumption in an environment where production is risky and insurance markets

Dairying as Livelihood Activity among SHGs - An overview. Dr. K. Natchimuthu RAGACOVAS, Puducherry.

Dairying as Livelihood Activity among SHGs - An overview Dr. K. Natchimuthu RAGACOVAS, Puducherry. Introduction Organised but unregistered groups involved primarily in savings and credit. Neighbourhood

Dairying as Livelihood Activity among SHGs - An overview Dr. K. Natchimuthu RAGACOVAS, Puducherry. Introduction Organised but unregistered groups involved primarily in savings and credit. Neighbourhood

International Journal of Business and Administration Research Review, Vol. 1 Issue.11, July - Sep, Page 42

MICRO FINANCE IN INDIA: CHALLENGES Meenakshi,* Shweta Bathla** *Department of commerce, Arya P.G. College, Panipat, Haryana, India. **Department of commerce, Arya P.G. College, Panipat, Haryana, India.

MICRO FINANCE IN INDIA: CHALLENGES Meenakshi,* Shweta Bathla** *Department of commerce, Arya P.G. College, Panipat, Haryana, India. **Department of commerce, Arya P.G. College, Panipat, Haryana, India.

Credit, Intermediation and Poverty Reduction

Credit, Intermediation and Poverty Reduction By Robert M. Townsend University of Chicago 1. Introduction The purpose of this essay is to show how credit markets influence development and to argue that

Credit, Intermediation and Poverty Reduction By Robert M. Townsend University of Chicago 1. Introduction The purpose of this essay is to show how credit markets influence development and to argue that

Microfinance: Coping Up with Emerging Banking Needs

Microfinance: Coping Up with Emerging Banking Needs Smt. Hiral Trivedi 2-A, Bhagyoday Society, City ring road, Nr. Talaja Jagat naka, Bhavnagar. Received Feb. 16, 2015 Accepted March. 01, 2015 ABSTRACT

Microfinance: Coping Up with Emerging Banking Needs Smt. Hiral Trivedi 2-A, Bhagyoday Society, City ring road, Nr. Talaja Jagat naka, Bhavnagar. Received Feb. 16, 2015 Accepted March. 01, 2015 ABSTRACT

The Role of Microfinance in Reducing Poverty

Melody Nelson 15.249B Special Seminar in International Management India Dr. Amar Gupta April 23, 2003 The Role of Microfinance in Reducing Poverty Introduction This paper explores the topic of microfinance

Melody Nelson 15.249B Special Seminar in International Management India Dr. Amar Gupta April 23, 2003 The Role of Microfinance in Reducing Poverty Introduction This paper explores the topic of microfinance

MAIN OBJECTIVES OF THE MICROFINANCE INSTITUTION

CHAPTER 4 MARKET FOR MICROFINANCE INDUSTRY MEANING OF MARKET A target market is a group of potential clients who share certain characteristics, tend to behave in similar ways, and are likely to be attracted

CHAPTER 4 MARKET FOR MICROFINANCE INDUSTRY MEANING OF MARKET A target market is a group of potential clients who share certain characteristics, tend to behave in similar ways, and are likely to be attracted

Session 1: SME financing in Asia and the Pacific and Latin America An overview. SME financing in Asia and the Pacific An introduction to the workshop

Session 1: SME financing in Asia and the Pacific and Latin America An overview SME financing in Asia and the Pacific An introduction to the workshop A presentation by Alberto Isgut, Financing for Development

Session 1: SME financing in Asia and the Pacific and Latin America An overview SME financing in Asia and the Pacific An introduction to the workshop A presentation by Alberto Isgut, Financing for Development

AN ASSESSMENT OF MICROFINANCE AS A TOOL FOR POVERTY REDUCTION AND SOCIAL CAPITAL FORMATION: EVIDENCE ON NIGERIA 1

AN ASSESSMENT OF MICROFINANCE AS A TOOL FOR POVERTY REDUCTION AND SOCIAL CAPITAL FORMATION: EVIDENCE ON NIGERIA 1 Dr. Ben E. Aigbokhan 2 Ambrose Alli University, Nigeria E-mail: baigbokhan@yahoo.com Abel

AN ASSESSMENT OF MICROFINANCE AS A TOOL FOR POVERTY REDUCTION AND SOCIAL CAPITAL FORMATION: EVIDENCE ON NIGERIA 1 Dr. Ben E. Aigbokhan 2 Ambrose Alli University, Nigeria E-mail: baigbokhan@yahoo.com Abel

Poverty, Vulnerability, and Vulnerable Groups:

Reaching Vulnerable Children and Youth in MENA Client-Staff Learning Workshop June 16-17 th, 2004 Washington DC Poverty, Vulnerability, and Vulnerable Groups: The Evolving Role of Social Protection and

Reaching Vulnerable Children and Youth in MENA Client-Staff Learning Workshop June 16-17 th, 2004 Washington DC Poverty, Vulnerability, and Vulnerable Groups: The Evolving Role of Social Protection and

Problems in Rural Credit Markets

Problems in Rural Credit Markets Econ 435/835 Fall 2012 Econ 435/835 () Credit Problems Fall 2012 1 / 22 Basic Problems Low quantity of domestic savings major constraint on investment, especially in manufacturing

Problems in Rural Credit Markets Econ 435/835 Fall 2012 Econ 435/835 () Credit Problems Fall 2012 1 / 22 Basic Problems Low quantity of domestic savings major constraint on investment, especially in manufacturing

Credit Markets in Developing Countries: Introduction

Credit Markets in Developing Countries: Introduction 1. Introduction 1 Credit markets link savers to investors. What is so special about credit markets? Matches talents and skills with resources. Helps

Credit Markets in Developing Countries: Introduction 1. Introduction 1 Credit markets link savers to investors. What is so special about credit markets? Matches talents and skills with resources. Helps

Dynamic Lending under Adverse Selection and Limited Borrower Commitment: Can it Outperform Group Lending?

Dynamic Lending under Adverse Selection and Limited Borrower Commitment: Can it Outperform Group Lending? Christian Ahlin Michigan State University Brian Waters UCLA Anderson Minn Fed/BREAD, October 2012

Dynamic Lending under Adverse Selection and Limited Borrower Commitment: Can it Outperform Group Lending? Christian Ahlin Michigan State University Brian Waters UCLA Anderson Minn Fed/BREAD, October 2012

EOCNOMICS- MONEY AND CREDIT

EOCNOMICS- MONEY AND CREDIT Banks circulate the money deposited by customers in the banks by lending it out to businesses at a rate of interest as a credit, which then acts as the income of the bank....

EOCNOMICS- MONEY AND CREDIT Banks circulate the money deposited by customers in the banks by lending it out to businesses at a rate of interest as a credit, which then acts as the income of the bank....

Indian microfinance: lessons from Bangladesh

MPRA Munich Personal RePEc Archive Indian microfinance: lessons from Bangladesh Debnarayan Sarker Centre for Economic Studies, Department of Economics, Presidency College, Kolkata, India 2008 Online at

MPRA Munich Personal RePEc Archive Indian microfinance: lessons from Bangladesh Debnarayan Sarker Centre for Economic Studies, Department of Economics, Presidency College, Kolkata, India 2008 Online at

Executive Summary The Supply of Financial Services

Executive Summary Over the past 20 years Nepal s financial sector has become deeper and the number and type of financial intermediaries have grown rapidly. In addition, recent reforms have made banks more

Executive Summary Over the past 20 years Nepal s financial sector has become deeper and the number and type of financial intermediaries have grown rapidly. In addition, recent reforms have made banks more

Modeling Credit Markets. Abhijit Banerjee Department of Economics, M.I.T.

Modeling Credit Markets Abhijit Banerjee Department of Economics, M.I.T. The neo-classical model of the capital market Everyone faces the same interest rate, adjusted for risk. i.e. if there is a d% riskof

Modeling Credit Markets Abhijit Banerjee Department of Economics, M.I.T. The neo-classical model of the capital market Everyone faces the same interest rate, adjusted for risk. i.e. if there is a d% riskof

The Research on Microfinance Models for BOP Market in Rural Areas of China

The Research on Microfinance Models for BOP Market in Rural Areas of China SHAO Xi,SU Pingping,and TONG Yunhuan Abstract:This article studies the financial innovation models for the market of low-income

The Research on Microfinance Models for BOP Market in Rural Areas of China SHAO Xi,SU Pingping,and TONG Yunhuan Abstract:This article studies the financial innovation models for the market of low-income

A COMPARATIVE STUDY ON MICROFINANCE IN INDIA AND ABROAD

I J A B E R, Vol. 14, No. 8, (2016): 5471-5476 A COMPARATIVE STUDY ON MICROFINANCE IN INDIA AND ABROAD J. Pavithra * and M. Ganesan ** INTRODUCTION Micro finance can be characterized as the methods by

I J A B E R, Vol. 14, No. 8, (2016): 5471-5476 A COMPARATIVE STUDY ON MICROFINANCE IN INDIA AND ABROAD J. Pavithra * and M. Ganesan ** INTRODUCTION Micro finance can be characterized as the methods by

SCREENING BY THE COMPANY YOU KEEP: JOINT LIABILITY LENDING AND THE PEER SELECTION EFFECT

SCREENING BY THE COMPANY YOU KEEP: JOINT LIABILITY LENDING AND THE PEER SELECTION EFFECT Author: Maitreesh Ghatak Presented by: Kosha Modi February 16, 2017 Introduction In an economic environment where

SCREENING BY THE COMPANY YOU KEEP: JOINT LIABILITY LENDING AND THE PEER SELECTION EFFECT Author: Maitreesh Ghatak Presented by: Kosha Modi February 16, 2017 Introduction In an economic environment where

Microfinance in Sudan Is Still At Infancy Stage

Microfinance in Sudan Is Still At Infancy Stage Dina Ahmed Mohamed Ghandour Lecturer Department Of Accounting and Finance Faculty Of Business Administration University of Medical Sciences and Technology

Microfinance in Sudan Is Still At Infancy Stage Dina Ahmed Mohamed Ghandour Lecturer Department Of Accounting and Finance Faculty Of Business Administration University of Medical Sciences and Technology

Rural Financial Intermediaries

Rural Financial Intermediaries 1. Limited Liability, Collateral and Its Substitutes 1 A striking empirical fact about the operation of rural financial markets is how markedly the conditions of access can

Rural Financial Intermediaries 1. Limited Liability, Collateral and Its Substitutes 1 A striking empirical fact about the operation of rural financial markets is how markedly the conditions of access can

Credit Markets. Abhijit Banerjee. Department of Economics, M.I.T.

Credit Markets Abhijit Banerjee Department of Economics, M.I.T. 1 The neo-classical model of the capital market Everyone faces the same interest rate, adjusted for risk. i.e. if there is a d% risk of default

Credit Markets Abhijit Banerjee Department of Economics, M.I.T. 1 The neo-classical model of the capital market Everyone faces the same interest rate, adjusted for risk. i.e. if there is a d% risk of default

A STUDY ABOUT THE MICROFINANCE MODELS AND ROLE OF FINANCIAL INSTITUTION IN EMPOWERING RURAL FINANCE: - AN OVERVIEW.

ISSN: 2454-132X IMPACT FACTOR: 4.295 (Volume2, Issue6) Available online at: www.ijariit.com A STUDY ABOUT THE MICROFINANCE MODELS AND ROLE OF FINANCIAL INSTITUTION IN EMPOWERING RURAL FINANCE: - AN OVERVIEW.

ISSN: 2454-132X IMPACT FACTOR: 4.295 (Volume2, Issue6) Available online at: www.ijariit.com A STUDY ABOUT THE MICROFINANCE MODELS AND ROLE OF FINANCIAL INSTITUTION IN EMPOWERING RURAL FINANCE: - AN OVERVIEW.

Agricultural Credit Policy

Agricultural Credit Policy Steven R. Koenig, Economic Research Service, USDA Damona G. Doye, Oklahoma State University Background Modern agricultural production systems are capital intensive, but relatively

Agricultural Credit Policy Steven R. Koenig, Economic Research Service, USDA Damona G. Doye, Oklahoma State University Background Modern agricultural production systems are capital intensive, but relatively

Is Financial Democracy a Click Away? Peer-to-Peer Lending and Beyond

Is Financial Democracy a Click Away? Peer-to-Peer Lending and Beyond Moderator: Thomas Debass (USAID/MD) Presenter: Jennifer Powers (EA Consultants) Commentators: Harvey Grasty (MicroPlace) Steve Ma (Investors

Is Financial Democracy a Click Away? Peer-to-Peer Lending and Beyond Moderator: Thomas Debass (USAID/MD) Presenter: Jennifer Powers (EA Consultants) Commentators: Harvey Grasty (MicroPlace) Steve Ma (Investors

ADVERSE SELECTION PAPER 8: CREDIT AND MICROFINANCE. 1. Introduction

PAPER 8: CREDIT AND MICROFINANCE LECTURE 2 LECTURER: DR. KUMAR ANIKET Abstract. We explore adverse selection models in the microfinance literature. The traditional market failure of under and over investment

PAPER 8: CREDIT AND MICROFINANCE LECTURE 2 LECTURER: DR. KUMAR ANIKET Abstract. We explore adverse selection models in the microfinance literature. The traditional market failure of under and over investment

Chapter 9. Development

Chapter 9 Development The world is divided between relatively rich and relatively poor countries. Geographers try to understand the reasons for this division and learn what can be done about it. Rich and

Chapter 9 Development The world is divided between relatively rich and relatively poor countries. Geographers try to understand the reasons for this division and learn what can be done about it. Rich and

Credit for Water and Sanitation Improvements: a Case Study of Women s Self-Help Groups in Tamil Nadu, India

Credit for Water and Sanitation Improvements: a Case Study of Women s Self-Help Groups in Tamil Nadu, India Executive summary In 2003, WaterPartners initiated a program which utilized micro-finance to

Credit for Water and Sanitation Improvements: a Case Study of Women s Self-Help Groups in Tamil Nadu, India Executive summary In 2003, WaterPartners initiated a program which utilized micro-finance to

Poverty Profile Executive Summary. Azerbaijan Republic

Poverty Profile Executive Summary Azerbaijan Republic December 2001 Japan Bank for International Cooperation 1. POVERTY AND INEQUALITY IN AZERBAIJAN 1.1. Poverty and Inequality Measurement Poverty Line

Poverty Profile Executive Summary Azerbaijan Republic December 2001 Japan Bank for International Cooperation 1. POVERTY AND INEQUALITY IN AZERBAIJAN 1.1. Poverty and Inequality Measurement Poverty Line

Chapter 5 Poverty, Inequality, and Development

Chapter 5 Poverty, Inequality, and Development Distribution and Development: Seven Critical Questions What is the extent of relative inequality, and how is this related to the extent of poverty? Who are

Chapter 5 Poverty, Inequality, and Development Distribution and Development: Seven Critical Questions What is the extent of relative inequality, and how is this related to the extent of poverty? Who are

Participation, Empowerment and Networks How people cooperate in restoration: Role of microfinance and its impact. Pornprapa Sakulsaeng 食料生産管理学

食料生産管理学 Participation, Empowerment and Networks How people cooperate in restoration: Role of microfinance and its impact Pornprapa Sakulsaeng 1 Contents Introduction Concept of microfinance Microfinance

食料生産管理学 Participation, Empowerment and Networks How people cooperate in restoration: Role of microfinance and its impact Pornprapa Sakulsaeng 1 Contents Introduction Concept of microfinance Microfinance

JOT-CREDIT PROBLEMS OF RURAL CREDIT COOPERATIVE AND SUGGESTIONS: THE CASE OF XIN LE COUNTRY, SHIJIAZHUANG CITY, HEBEI PROVINCE, CHINA

International Journal of Business and Society, Vol. 17 No. 3, 2016, 535-542 JOT-CREDIT PROBLEMS OF RURAL CREDIT COOPERATIVE AND SUGGESTIONS: THE CASE OF XIN LE COUNTRY, SHIJIAZHUANG CITY, HEBEI PROVINCE,

International Journal of Business and Society, Vol. 17 No. 3, 2016, 535-542 JOT-CREDIT PROBLEMS OF RURAL CREDIT COOPERATIVE AND SUGGESTIONS: THE CASE OF XIN LE COUNTRY, SHIJIAZHUANG CITY, HEBEI PROVINCE,

MICROFINANCE: Enabling The Power of Ideas & Entrepreneurial Energy for the Other Half. Vinod Khosla May 2004

MICROFINANCE: Enabling The Power of Ideas & Entrepreneurial Energy for the Other Half Vinod Khosla May 2004 Story: 1994 First Inspiration SHARE: History 1998-99 Active Clients 1999-2000 2000-2001 2001-02

MICROFINANCE: Enabling The Power of Ideas & Entrepreneurial Energy for the Other Half Vinod Khosla May 2004 Story: 1994 First Inspiration SHARE: History 1998-99 Active Clients 1999-2000 2000-2001 2001-02

Impact Assessment of Microfinance For SIDBI Foundation for Micro Credit (SFMC)

") Impact Assessment of Microfinance For SIDBI Foundation for Micro Credit (SFMC) Phase 1 Report July 2001 March 2002 By Putting people first EDA Rural Systems Pvt Ltd 107 Qutab Plaza, DLF Qutab Enclave-1,

Impact Assessment of Microfinance For SIDBI Foundation for Micro Credit (SFMC) Phase 1 Report July 2001 March 2002 By Putting people first EDA Rural Systems Pvt Ltd 107 Qutab Plaza, DLF Qutab Enclave-1,

To Get That Little: A Computational Model of Microfinance

To Get That Little: A Computational Model of Microfinance Miriam Goldberg, Yale University and Santa Fe Institute Samuel Bowles, Santa Fe Institute John Miller, Santa Fe Institute and Carnegie Mellon University

To Get That Little: A Computational Model of Microfinance Miriam Goldberg, Yale University and Santa Fe Institute Samuel Bowles, Santa Fe Institute John Miller, Santa Fe Institute and Carnegie Mellon University

Microfinance Institutions

Microfinance Institutions History of Business Networks Dr. Gordon Winder Seminar für Wirtschaftsgeschichte LMU München Date: 06-30-2008 Speaker: Tilman Weber Do you know him? Lasting Peace can not be achieved

Microfinance Institutions History of Business Networks Dr. Gordon Winder Seminar für Wirtschaftsgeschichte LMU München Date: 06-30-2008 Speaker: Tilman Weber Do you know him? Lasting Peace can not be achieved

Regulation of Microfinance Institutions in India

Regulation of Microfinance Institutions in India Santadarshan Sadhu, Kenny Kline, Justin Oliver CMF-IFMR 20 th April 2011 Study Outline Microfinance sector - overview Analysis of the existing regulatory

Regulation of Microfinance Institutions in India Santadarshan Sadhu, Kenny Kline, Justin Oliver CMF-IFMR 20 th April 2011 Study Outline Microfinance sector - overview Analysis of the existing regulatory

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD By A Ramanathan, Chief General Manager Micro Finance Innovations Department NABARD Mumbai What is

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD By A Ramanathan, Chief General Manager Micro Finance Innovations Department NABARD Mumbai What is

IB Economics Development Economics 4.1: Economic Growth and Development

IB Economics: www.ibdeconomics.com 4.1 ECONOMIC GROWTH AND DEVELOPMENT: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: Absolute poverty Closed economy

IB Economics: www.ibdeconomics.com 4.1 ECONOMIC GROWTH AND DEVELOPMENT: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: Absolute poverty Closed economy

FINANCIAL EMPOWERMENT: THE NEED TO DEVELOP A MORE RESPONSIVE, PRO-POOR STRATEGY IN FINANCING A SUSTAINABLE LINKAGE IN NIGERIA

FINANCIAL EMPOWERMENT: THE NEED TO DEVELOP A MORE RESPONSIVE, PRO-POOR STRATEGY IN FINANCING A SUSTAINABLE LINKAGE IN NIGERIA A paper contributed by the Nigeria National Strategy Team Against the background

FINANCIAL EMPOWERMENT: THE NEED TO DEVELOP A MORE RESPONSIVE, PRO-POOR STRATEGY IN FINANCING A SUSTAINABLE LINKAGE IN NIGERIA A paper contributed by the Nigeria National Strategy Team Against the background

What is Inclusive growth?

What is Inclusive growth? Tony Addison Miguel Niño Zarazúa Nordic Baltic MDB meeting Helsinki, Finland January 25, 2012 Why is economic growth important? Economic Growth to deliver sustained poverty reduction

What is Inclusive growth? Tony Addison Miguel Niño Zarazúa Nordic Baltic MDB meeting Helsinki, Finland January 25, 2012 Why is economic growth important? Economic Growth to deliver sustained poverty reduction

SOCIAL PROTECTION: ROLE OF MICRO FINANCE. A.R. Kemal

SOCIAL PROTECTION: ROLE OF MICRO FINANCE A.R. Kemal Social Safety Nets Because of the rising unemployment and poverty levels the Social safety nets have assumed great significance. They are required for

SOCIAL PROTECTION: ROLE OF MICRO FINANCE A.R. Kemal Social Safety Nets Because of the rising unemployment and poverty levels the Social safety nets have assumed great significance. They are required for

Does Participation in Microfinance Programs Improve Household Incomes: Empirical Evidence From Makueni District, Kenya.

AAAE Conference proceedings (2007) 405-410 Does Participation in Microfinance Programs Improve Household Incomes: Empirical Evidence From Makueni District, Kenya. Joy M Kiiru, John Mburu, Klaus Flohberg

AAAE Conference proceedings (2007) 405-410 Does Participation in Microfinance Programs Improve Household Incomes: Empirical Evidence From Makueni District, Kenya. Joy M Kiiru, John Mburu, Klaus Flohberg

Stability and Capacity of Property Liability Insurance Markets. Neil Doherty Cartagena, Colombia May 2007

Stability and Capacity of Property Liability Insurance Markets Neil Doherty Cartagena, Colombia May 2007 1.4 1.3 1.2 1.1 1 0.9 0.8 0.7 0.6 Market Stability: Combined Ratio in Colombia Life P&C 1975 1976

Stability and Capacity of Property Liability Insurance Markets Neil Doherty Cartagena, Colombia May 2007 1.4 1.3 1.2 1.1 1 0.9 0.8 0.7 0.6 Market Stability: Combined Ratio in Colombia Life P&C 1975 1976

On the Implicit Interest Rate in the Yunus Equation

On the Implicit Interest Rate in the Yunus Equation PHEAKDEI MAUK Laboratoire J.A. Dieudonné May 10, 2011 1 Introduction 2 3 4 5 Microcredit Yunus Equation What is Microcredit? The provision of very small

On the Implicit Interest Rate in the Yunus Equation PHEAKDEI MAUK Laboratoire J.A. Dieudonné May 10, 2011 1 Introduction 2 3 4 5 Microcredit Yunus Equation What is Microcredit? The provision of very small

KIÚTPROGRAM Executive Summary

KIÚTPROGRAM Executive Summary 1. VISION The mission of the Kiútprogram MFI (KP) is to help people living in deepest poverty mainly of Roma origin to improve their situation with dignity, by providing them

KIÚTPROGRAM Executive Summary 1. VISION The mission of the Kiútprogram MFI (KP) is to help people living in deepest poverty mainly of Roma origin to improve their situation with dignity, by providing them

Institutional Differences in Provision of Credit to Women in Developing Countries - Evidence from Uganda

Institutional Differences in Provision of Credit to Women in Developing Countries - Evidence from Uganda Economics Master's thesis Annastiina Hintsa 2011 Department of Economics Aalto University School

Institutional Differences in Provision of Credit to Women in Developing Countries - Evidence from Uganda Economics Master's thesis Annastiina Hintsa 2011 Department of Economics Aalto University School

Microcredit: The Good, the Bad, and the Ugly

Microcredit: The Good, the Bad, and the Ugly Unraveling the confusion behind microcredit: how some models help alleviate poverty, while others exploit the poor to make the rich richer. by David Korten

Microcredit: The Good, the Bad, and the Ugly Unraveling the confusion behind microcredit: how some models help alleviate poverty, while others exploit the poor to make the rich richer. by David Korten

Credit Market Problems in Developing Countries

Credit Market Problems in Developing Countries November 2007 () Credit Market Problems November 2007 1 / 25 Basic Problems (circa 1950): Low quantity of domestic savings major constraint on investment,

Credit Market Problems in Developing Countries November 2007 () Credit Market Problems November 2007 1 / 25 Basic Problems (circa 1950): Low quantity of domestic savings major constraint on investment,

SOCIAL SECURITY IN INDIA: STATUS, ISSUES AND WAYS FORWARD

SOCIAL SECURITY IN INDIA: STATUS, ISSUES AND WAYS FORWARD D Rajasekhar Centre for Decentralisation and Development, ISEC, Bangalore Presentation to the International Conference on Social Security Systems

SOCIAL SECURITY IN INDIA: STATUS, ISSUES AND WAYS FORWARD D Rajasekhar Centre for Decentralisation and Development, ISEC, Bangalore Presentation to the International Conference on Social Security Systems

Share of the Informal Loans in Total Borrowing in Pakistan: A Case Study of District Peshawar Fazal Wahid & Zia Ur Rehman

Share of the Informal Loans in Total Borrowing in Pakistan: A Case Study of District Peshawar Fazal Wahid & Zia Ur Rehman Abstract The main objectives of the study is to analyze the share of informal loan

Share of the Informal Loans in Total Borrowing in Pakistan: A Case Study of District Peshawar Fazal Wahid & Zia Ur Rehman Abstract The main objectives of the study is to analyze the share of informal loan

CIA Annual Meeting Assemblée annuelle de l ICA

CIA Annual Meeting Assemblée annuelle de l ICA June 28 & 29, 2007 Les 28 et 29 juin 2007 Vancouver, BC Denis Garand Denis@garandnet.net Micro insurance Millennium development goals ERADICATE EXTREME POVERTY

CIA Annual Meeting Assemblée annuelle de l ICA June 28 & 29, 2007 Les 28 et 29 juin 2007 Vancouver, BC Denis Garand Denis@garandnet.net Micro insurance Millennium development goals ERADICATE EXTREME POVERTY

Modeling Credit Markets. Abhijit Banerjee Department of Economics, M.I.T.

Modeling Credit Markets Abhijit Banerjee Department of Economics, M.I.T. 1 1 The neo-classical model of the capital market Everyone faces the same interest rate, adjusted for risk. i.e. if there is a d%

Modeling Credit Markets Abhijit Banerjee Department of Economics, M.I.T. 1 1 The neo-classical model of the capital market Everyone faces the same interest rate, adjusted for risk. i.e. if there is a d%

TURNING UNPAID DOMESTIC AND CARE WORK INTO DEVELOPMENT DIVIDENDS

TURNING UNPAID DOMESTIC AND CARE WORK INTO DEVELOPMENT DIVIDENDS ISSUES AFFECTING ASIA-PACIFIC Asia Pacific is seeing high economic growth and a lowering of poverty rates. For example, from 2002 to 2012,

TURNING UNPAID DOMESTIC AND CARE WORK INTO DEVELOPMENT DIVIDENDS ISSUES AFFECTING ASIA-PACIFIC Asia Pacific is seeing high economic growth and a lowering of poverty rates. For example, from 2002 to 2012,

Public Disclosure Authorized. Public Disclosure Authorized. Public Disclosure Authorized. Public Disclosure Authorized

69052 Tajikistan Agriculture Sector: Policy Note 3 Demand and Supply for Rural Finance Improving Access to Rural Finance The Asian Development Bank has conservatively estimated the capital investment needs

69052 Tajikistan Agriculture Sector: Policy Note 3 Demand and Supply for Rural Finance Improving Access to Rural Finance The Asian Development Bank has conservatively estimated the capital investment needs

MATRIX OF STRATEGIC VISION AND ACTIONS TO SUPPORT SUSTAINABLE CITIES

Urban mission and overall strategy objectives: To promote sustainable cities and towns that fulfill the promise of development for their inhabitants in particular, by improving the lives of the poor and

Urban mission and overall strategy objectives: To promote sustainable cities and towns that fulfill the promise of development for their inhabitants in particular, by improving the lives of the poor and

PROGRAM INFORMATION DOCUMENT (PID) CONCEPT STAGE July 21, 2017 Report No.: MG Public Finance Sustainability and Investment II DPO

CONCEPT STAGE July 21, 2017 Report No.: MG Public Finance Sustainability and Investment II DPO") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM INFORMATION DOCUMENT (PID) CONCEPT STAGE July 21, 2017 Report No.: 120763 Operation

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM INFORMATION DOCUMENT (PID) CONCEPT STAGE July 21, 2017 Report No.: 120763 Operation

MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK]

![MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK]](/thumbs/76/74334829.jpg "MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK]") MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK] 1. What is collateral? Collateral is an asset that the borrower owns such as land, building, vehicle, livestock, deposits with the banks and uses

MONEY AND CREDIT VERY SHORT ANSWER TYPE QUESTIONS [1 MARK] 1. What is collateral? Collateral is an asset that the borrower owns such as land, building, vehicle, livestock, deposits with the banks and uses

Finance and Guarantees in Rural Development

Finance and Guarantees in Rural Development By Zvi Galor www.coopgalor.com 1. Introduction. In this brief article, I will try to examine the needs existing in rural development organizations to finance

Finance and Guarantees in Rural Development By Zvi Galor www.coopgalor.com 1. Introduction. In this brief article, I will try to examine the needs existing in rural development organizations to finance

Ghana: Promoting Growth, Reducing Poverty

Findings reports on ongoing operational, economic and sector work carried out by the World Bank and its member governments in the Africa Region. It is published periodically by the Africa Technical Department

Findings reports on ongoing operational, economic and sector work carried out by the World Bank and its member governments in the Africa Region. It is published periodically by the Africa Technical Department

PROCEEDINGS OF THE AGRICULTURAL ECONOMISTS HELD AT CORNELL UNIVERSITY, ITHACA; NEW YORK, AUGUST 18 TO AUGUST 29, 1930

PROCEEDINGS OF THE SECOND,, INTERNATIONAL. CONFERENCE OF AGRICULTURAL ECONOMISTS HELD AT CORNELL UNIVERSITY, ITHACA; NEW YORK, AUGUST 18 TO AUGUST 29, 1930 U:l]e

PROCEEDINGS OF THE SECOND,, INTERNATIONAL. CONFERENCE OF AGRICULTURAL ECONOMISTS HELD AT CORNELL UNIVERSITY, ITHACA; NEW YORK, AUGUST 18 TO AUGUST 29, 1930 U:l]e

LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT

45 LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT Edward M. Gramlich Member, Board of Governors of the Federal Reserve System Introduction I am pleased to be here today to kick off the conference

45 LUNCHEON ADDRESS: SMALL BUSINESS ACCESS TO CAPITAL AND CREDIT Edward M. Gramlich Member, Board of Governors of the Federal Reserve System Introduction I am pleased to be here today to kick off the conference

Poverty and development Week 11 March 15. Readings: Ray chapter 8

Poverty and development Week 11 March 15 Readings: Ray chapter 8 1 Introduction Poverty is both of intrinsic and functional significance. Poverty has enormous implications for the way in which entire economies

Poverty and development Week 11 March 15 Readings: Ray chapter 8 1 Introduction Poverty is both of intrinsic and functional significance. Poverty has enormous implications for the way in which entire economies

Lab #7. Chapter 7 Growth, Productivity, and Wealth in the Long Run

University of Lethbridge - Department of Economics ECON 1012 Introduction to Macroeconomics LAB Instructor: Michael G. Lanyi Lab #7 Chapter 7 Growth, Productivity, and Wealth in the Long Run Answer Sheet

University of Lethbridge - Department of Economics ECON 1012 Introduction to Macroeconomics LAB Instructor: Michael G. Lanyi Lab #7 Chapter 7 Growth, Productivity, and Wealth in the Long Run Answer Sheet

The Global Hunger Project and Affiliates. Consolidated Financial Report December 31, 2013

The Global Hunger Project and Affiliates Consolidated Financial Report December 31, 2013 Contents Independent Auditor s Report 1-2 Financial Statements Consolidated Balance Sheet 3 Consolidated Statement

The Global Hunger Project and Affiliates Consolidated Financial Report December 31, 2013 Contents Independent Auditor s Report 1-2 Financial Statements Consolidated Balance Sheet 3 Consolidated Statement

Maitreesh Ghatak and Timothy W. Guinnane. The Economics of Lending with Joint Liability: Theory and Practice

The Economics of Lending with Joint Liability: Theory and Practice Maitreesh Ghatak and Timothy W. Guinnane Introduction We have looked at 3 kinds of problems in the credit markets: Adverse Selection,

The Economics of Lending with Joint Liability: Theory and Practice Maitreesh Ghatak and Timothy W. Guinnane Introduction We have looked at 3 kinds of problems in the credit markets: Adverse Selection,

EU FUNDING PROGRAMMES IN THE FIELD OF DEVELOPMENT AID

EU FUNDING PROGRAMMES IN THE FIELD OF DEVELOPMENT AID EU FORDERUNG FUR MIGRANTEN ORGANISATIONEN UND TRAGER DER PARTICIPATIONS UND INTEGRATIONS ARBEIT IN BERLIN MOVE GLOBAL 25 October 2014, Berlin About

EU FUNDING PROGRAMMES IN THE FIELD OF DEVELOPMENT AID EU FORDERUNG FUR MIGRANTEN ORGANISATIONEN UND TRAGER DER PARTICIPATIONS UND INTEGRATIONS ARBEIT IN BERLIN MOVE GLOBAL 25 October 2014, Berlin About

Chapter 8 An Economic Analysis of Financial Structure

Chapter 8 An Economic Analysis of Financial Structure Multiple Choice 1) American businesses get their external funds primarily from (a) bank loans. (b) bonds and commercial paper issues. (c) stock issues.

Chapter 8 An Economic Analysis of Financial Structure Multiple Choice 1) American businesses get their external funds primarily from (a) bank loans. (b) bonds and commercial paper issues. (c) stock issues.

Private Sector Initiatives in Slums

Private Sector Initiatives in Slums May 27, 2008 Background Upgrading (trends) Private Sector involvement (trends) Challenges and Opportunities Economy and state of the private sector Will affect resources,

Private Sector Initiatives in Slums May 27, 2008 Background Upgrading (trends) Private Sector involvement (trends) Challenges and Opportunities Economy and state of the private sector Will affect resources,

Agricultural Commodity Risk Management: Policy Options and Practical Instruments with Emphasis on the Tea Economy

Agricultural Commodity Risk Management: Policy Options and Practical Instruments with Emphasis on the Tea Economy Alexander Sarris Director, Trade and Markets Division, FAO Presentation at the Intergovernmental

Agricultural Commodity Risk Management: Policy Options and Practical Instruments with Emphasis on the Tea Economy Alexander Sarris Director, Trade and Markets Division, FAO Presentation at the Intergovernmental

UNIT 10 EXERCISE ANSWERS UNIT 10 ANSWERS TO EXERCISES EXERCISE 10.1 THE CONSEQUENCES OF PURE IMPATIENCE

UNIT 10 ANSWERS TO EXERCISES EXERCISE 10.1 THE CONSEQUENCES OF PURE IMPATIENCE 1. Draw the indifference curves of a person who is more impatient than Julia in Figure 10.3b, for any level of consumption

UNIT 10 ANSWERS TO EXERCISES EXERCISE 10.1 THE CONSEQUENCES OF PURE IMPATIENCE 1. Draw the indifference curves of a person who is more impatient than Julia in Figure 10.3b, for any level of consumption

An economic analysis of indebtedness of marginal and small farmers in Punjab

Internationl Research Journal of Agricultural Economics and Statistics Volume 3 Issue 2 September, 2012 235-239 Research Paper An economic analysis of indebtedness of marginal and small farmers in Punjab

Internationl Research Journal of Agricultural Economics and Statistics Volume 3 Issue 2 September, 2012 235-239 Research Paper An economic analysis of indebtedness of marginal and small farmers in Punjab

Statement for the Record. American Bankers Association. Agriculture Committee. United States House of Representatives

Statement for the Record On Behalf of the American Bankers Association before the Agriculture Committee of the United States House of Representatives Statement for the Record On behalf of the American

Statement for the Record On Behalf of the American Bankers Association before the Agriculture Committee of the United States House of Representatives Statement for the Record On behalf of the American

India Country Profile 2014

India Country Profile 2014 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Region: South Asia Income Group: Lower middle income Population:

India Country Profile 2014 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Region: South Asia Income Group: Lower middle income Population:

MICROFINANCE: ITS EVOLUTION AND VARIOUS MODELS FOR ENPOWERMENT OF RURAL POOR IN INDIA

MICROFINANCE: ITS EVOLUTION AND VARIOUS MODELS FOR ENPOWERMENT OF RURAL POOR IN INDIA * Mrs. Ghousia Shameen, Assistant Prof., Millennium Institute of Management, Aurangabad. INTRODUCTION: The major concern

MICROFINANCE: ITS EVOLUTION AND VARIOUS MODELS FOR ENPOWERMENT OF RURAL POOR IN INDIA * Mrs. Ghousia Shameen, Assistant Prof., Millennium Institute of Management, Aurangabad. INTRODUCTION: The major concern

Participation, Empowerment and Networks How people cooperate in restoration: Role of microfinance and its impact. Pornprapa Sakulsaeng

Participation, Empowerment and Networks How people cooperate in restoration: Role of microfinance and its impact Pornprapa Sakulsaeng 1 Contents Introduction Concept of microfinance Microfinance development

Participation, Empowerment and Networks How people cooperate in restoration: Role of microfinance and its impact Pornprapa Sakulsaeng 1 Contents Introduction Concept of microfinance Microfinance development

Lebanon Country Profile 2013

Lebanon Country Profile 2013 ENTERPRISE SURVEYS Region: Middle East & North Africa Income Group: Upper middle income Population: 4,424,888 GNI per capita: US$9,190.00 Contents Introduction Business Environment

Lebanon Country Profile 2013 ENTERPRISE SURVEYS Region: Middle East & North Africa Income Group: Upper middle income Population: 4,424,888 GNI per capita: US$9,190.00 Contents Introduction Business Environment