HOW EFFECTIVE ARE REWARDS PROGRAMS IN PROMOTING PAYMENT CARD USAGE? EMPIRICAL EVIDENCE

|

|

|

- Osborne West

- 5 years ago

- Views:

Transcription

1 HOW EFFECTIVE ARE REWARDS PROGRAMS IN PROMOTING PAYMENT CARD USAGE? EMPIRICAL EVIDENCE Santiago Carbó-Valverde University of Granada & Federal Reserve Bank of Chicago* José Manuel Liñares Zegarra University of Granada May 25, 2009 * The views expressed are those of the authors and do not represent the views of the Federal Reserve Bank of Chicago or the Federal Reserve System.

2 Outline 2 1. Introduction 2. Background and hypothesis 3. An Econometric Model of Rational Consumer Choice 4. Data and estimation methodology 5. Incentive programs and consumer payment preferences: Logit results 6. Economic Impact 7. Conclusions

3 1. Introduction 3 Some recent studies have highlighted the cost and convenience benefits of using retail electronic payments and, in particular, card payment instruments: Humphrey et al. (2001,.2003) estimate that "if a country moves from a wholly paper-based payment system to close to an all electronic system, it may save 1% or more of its annual GDP once transaction costs are absorbed". Similar benefits have been estimated for Spain in Carbó et al. (2003). However, cash and other paper-based payment instruments are still being largely used by consumers in most developed countries.

4 4 Card issuers have incurred substantial costs to launch incentive programs to stimulate payments with debit and credit cards, presumably assuming that these rewards would significantly increase the use of these cards based on standard comparisons. However, they are facing a great uncertainty on how to allocate the resources to make the incentive programs as effective as desired. Little is known on how to encourage consumers to increase the use of debit and credit cards. This limited knowledge is, at least partially, due to the lack of comprehensive microeconomic data on consumers' preferences towards payment instruments and on the related role of incentive-related mechanisms.

5 5 The main goal of this paper is to empirically examine both the effects of incentive programs on payment preferences and the impact on the substitution of cash by cards. The contributions of this study are twofold: i) This is the first empirical study considering different types of rewards to estimate the relative impact of these rewards on the preferences for cards relative to cash. ii) It offers an estimation of the aggregate economic impact of reward programs on the use of cards across merchant activities. In order to address these goals, this paper uses unique survey data.

6 2. Background and hypotheses 6 Most studies on the role of rewards programs for general purchases (not specifically for card purchases) have been undertaken from a behavioral perspective and have shown significantly large and positive effects of incentive programs. Among these behavioral studies, there is only few (Feinberg, 1986; Soman, 2001) dealing with preferences towards cards, although none of them particularly examine the role of incentive programs in card payments. They compare the spending of consumers who paid with credit cards with those who used cash or checks, and they find that the former spend more.

7 7 In the banking literature, however, although some studies have examined preferences towards payment cards, most of them have not referred to rewards programs. Gross and Souleles (2002a and 2002b) have shown that consumers preferences towards cards vary considerably when contractual conditions (such interest rates, repayment schemes or rewards programs) change. In the case of credit cards, these changes in contractual conditions may well explain the stickiness of the use of credit cards to interest rates (Ausubel, 1991; Calem and Mester, 1995, Brito and Hartley, 1995). Carow and Staten (1999 and Kennickell and Kwast (1997) find that consumer-level variables such as schooling or financial wealth increase the likelihood of electronic payment instrument usage..

8 8 Other recent empirical studies have also explored consumer preferences towards payment instruments using surveys on household finances (Hayashi and Klee, 2003; Mester, 2003; Klee, 2006; Rysman, 2007 and Zinman, 2008). To our knowledge, only Ching and Hayashi (2008) identify some general effects of rewards on consumer choice of payment instruments. They find that consumers with credit card rewards use credit cards more intensively than those without rewards. Unlike Ching and Hayashi (2008) we provide information on the type of rewards, the relative impact of these rewards on the preferences for cards relative to paper-based instruments and the aggregate economic impact of the effects of reward programs across merchant activities.

9 9 3. An econometric model of rational consumer choice In order to place our hypotheses, the general empirical framework is based on hedonic models of demand in markets with differentiated products (Lancaster, 1971 and McFadden, 1974). These models allow for heterogeneous preferences for card usage relative to other payment instruments based on their comparative attributes. Consumers have two options for payment: i) paper-based payment instruments (cash). ii) electronic-based payment instruments (e.g. credit or debit card). Our behavioral model of consumers' choice incorporates cards' incentive programs to the standard consumer characteristics and consumer perceptions.

10 10 Considering this set of variables, the model assumes that cardholders will use at the checkout the payment instrument (cash or cards) with a higher utility: (1) Consumer i's utility of using the payment instrument j considering a set of k variables showing consumer s perceptions. A vector which includes a set of cardholders characteristics A vector of attributes of the payment instrument j that can be observed by consumer i. A vector which controls if the payment instrument j used by the consumer i incorporates any type of incentive program A vector which includes variables showing consumer's perceptions that could affect payment behavior at the checkout.

11 11 The random utility theory (McFadden, 1974; Domencich and McFadden, 1975 and Louviere et al., 2000) assumes that one part of the utility function is deterministic in each of the individual utility functions. This portion of the utility function is known with certainty by the consumer who takes a decision. A second part of the utility function embodies a random component that groups measurement errors and nonobservable attributes of the consumers' decisions. With these ingredients, the specification of consumer utility is:

12 12 A latent dichotomous variable is also added and takes the value "1" if the cardholder i uses the payment instrument j (cards) given a set of k variables showing consumer s perceptions, and zero otherwise. Hence, the probability that an individual chooses a certain payment alternative j is the probability that this alternative offers higher utility to the cardholder:

13 13 The estimation method is a logit model with the following specification: In equation (4) consumers choose the payment instrument that they prefer for every type of transaction and that offers them the higher utility, given a set of preferences and the role of incentive programs. We assume that consumers have access to all payment options.

14 4. Data and estimation methodology LOGIT METHODOLOGY: In order to analyze consumers preferences for payment instruments and the role of incentive programs, equation (4) is estimated as a binary mixed logit model. A mixed logit regression analysis isolates the effects of the individual characteristics and incentive programs on the use of payment instruments (cards versus cash), when other factors are held constant. The dependent (binomial) variable shows whether a consumer uses a payment card or cash at different types of merchant outlets. In the case of payment cards we also control whether cardholders enjoy any type of rewards. Equation (4) is also estimated for different merchant activities and for each payment instrument separately.

15 15 Our specification includes two main sets of explanatory variables. The first set corresponds to consumer characteristics: income, age, education, sex, members of the household that financially contribute to household expenditures, frequency of the use of a car, travel frequency and population of the territorial area where the consumer lives. The second set includes card-specific attributes: the availability of debit and/or credit rewards programs; the type of rewards (discounts, points, gifts and cash-back) and the attributes of the payment instruments that determine consumer preferences towards these instruments (convenience8, habits, control of domestic expenditure, ). A critical control in the second group is the easiness and availability of cash withdrawal delivery channels (ATMs) as well as the acceptance of the card at the point of sale (POS) by merchants. We also include regional dummies as controls for the geographical location of the cardholders.

16 DATA AND MAIN VARIABLES: We rely on survey evidence obtained from a set responses to a 2005 national survey of 2,961 individuals using cards. The individuals were asked 150 questions on the use of three payment instruments: debit cards, credit cards and cash. The survey includes information on consumers' demographic characteristics, payment behavior, self-reported payment preferences, attitudes towards incentive programs, and frequency of use of the different payment methods by merchant sector and perceptions on comparable attributes of the different payment methods (comfort, convenience, speed, safety, etc.). Figure 1 and Table 2 show, respectively, the variability in the share of payment instruments used at merchant outlets and in the different types of rewards that cardholders enjoy.

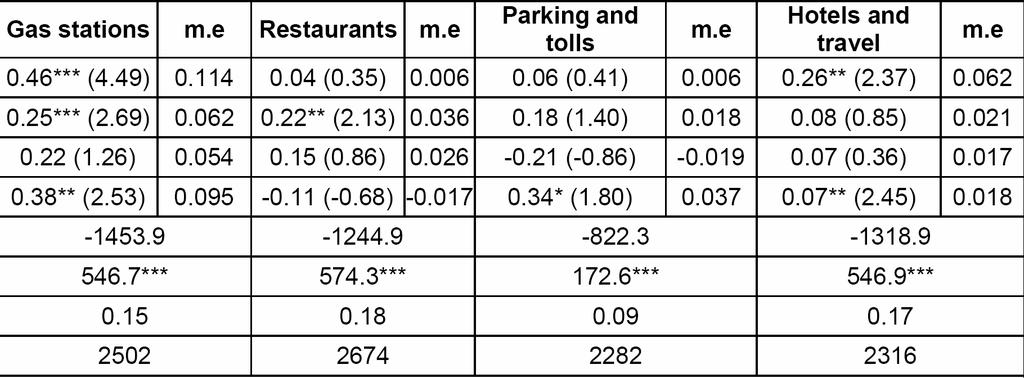

17 17

18 18 Table 2. Sample distribution of incentive programs

19 19 5. Incentive programs and consumer payment preferences: Logit results There are two set of logit results: The first refers to the estimations for all sectors and the effects of rewards programs overall (without distinguishing the type or reward or the merchant activity). The second set of results summarizes the main coefficients of the rewards parameters when the estimations are undertaken for different type of merchant activities and/or different type of rewards program.

20 20 Table 3 shows the results for all sectors and distinguishing between all cardholders, credit and debit cardholders. These results show the effects of enjoying rewards programs no matter the type of reward. Marginal effects for unit increase in x are shown as "m.e" in the tables. All coefficients related to the role of incentive programs are positive and significant and exhibit one of the highest marginal effects on the probability of using a card instead of cash for consumption purposes. In particular, cardholders enjoying rewards programs may increase the probability of using cards (relative to cash) by 3.8%. This marginal effect, however, is found to be larger for debit cardholders (5.0%) that for credit cardholders (2.1%).

21 21 Table 3. Logit results. All sectors (a)

22 22 Table 3. Logit results. All sectors (b)

23 23 Table 3. Logit results. All sectors (c)

24 24 Table 4 shows the logit results distinguishing different types of incentive programs and/or merchant activities. PANEL A (by reward type): Discounts, points and cash-back are generally found to have a positive and significant effect on the use of cards relative to cash while gifts are not significant. Cash-back incentives exhibit the higher marginal effect (4.1%). PANEL B (by merchant type): A high positive and significant effect of rewards of card usage in department stores (8.5%), hotels and travel (6.9%), supermarkets (6.7%), gas stations (4.5%), restaurants (3.4%) and boutiques (3.1%). PANEL C (by reward and merchant type): It confirms that cash-back appears to be the most effective incentive to foster the use of cards relative to cash. In particular, the marginal effects of cash-back are found to be positive and significant in supermarkets (6.4%), department stores (7.0%), boutiques (1.1%), gas stations (0.9%) and parking and tolls (3.7%).

25 25

26 26

27 27

28 28 6. Economic impact of the incentive programs 6.1. Methodology We investigate the economic impact of incentive programs on the use of payment instruments comparing the use of cards (relative to cash) between cardholders enjoying any type or rewards and those without rewards. In order to perform this analysis, the main ingredients are the predicted usage shares assigned to cards relative to cash from previous logit estimations. The main aim of this empirical analysis is to extrapolate the sample estimations of the impact of rewards on cards vs. card usage to i) All cardholders, debit cardholders and credit cardholders. ii) Eight different merchant sectors.

29 29 We then need to compute the average shares for each one of these groups using a representative weighting factor across these groups in Spain. According to logit estimations age seems to be an appropriate discriminating factor and it is the only continuous variable within the set of explanatory factors. To compute this average, we first compute the share of card usage (relative to cash) for consumers of different ages year by year from 17 to 70 years old. Secondly, we compare the (age) weighted average for reward receivers and nonreward receivers. Estimating card usage shares for both groups reveals to what extent reward receivers use their payment cards relative to nonreward receivers.

30 30 To analyze differences between both types of consumers, the quantitative indicator Reward Impact (RI) is then computed as: n=70 n'=70 RI= ( weighted card share(with incentives) ) - ( weighted card share(without incentives) ij m=17 m'=17 ij Only if RI>0, the incentive programs will be useful tool to change the preferences of consumers to increase payment cards usage relative to cash.

31 31 Then, We examine the total impact by merchant sectors (RIS): 4 RIS = ( RI *share of reward i in our sample across sectors j) j i= 1 ij j = 1,...8 (commercial sectors) i = 1,...4 (incentive programs) The RIS is also estimated for different types of rewards across merchant sectors (RIR). It analyzes the impact of both the type of rewards and the type of card for all sectors considered jointly. 8 RIR = ( RIS * GDP of merchant activity j over aggregate GDP) j j= 1 ij j = 1,...,8 (commercial sectors) i = 1,...,4 (incentive programs) Finally, we will estimate the macroeconomic effect (total impact) across sectors and individuals as the sum of all the previous effects.

32 The effect of the incentive programs on cash substitution by merchant sector (RIS) Table 5 shows the predicted share of card usage relative to cash across merchant sectors for three different categories of cardholders (all cardholders, debit cardholders and credit cardholders). As expected, the average use of cards relative to cash appears to be larger for cardholders holding cards with incentive programs. Debit and credit cardholders buying at department stores that may benefit from points, gifts and cash-back exhibit a significantly higher use of cards, with the RI indicator being 3.7%, 4.9% and 6.8%, respectively. Mean-difference tests reveal that differences across type of rewards are statistically significant at 5% level.

33 33 Other groups showing a high economic impact of rewards on cards vs. cash are cardholders buying at gas stations where they can benefit from discounts and cash-back (11.2% and 9.3%) as well as debit cardholders paying at gas stations where they can potentially benefit from cash-back options (13.5%). Table 5 also shows that the effect of rewards on the use of cards also varies depending on the type of rewards and depending on the type of card employed. As for the aggregate effect of rewards by sector (RIS) and type of card, the positive effect of rewards on the usage of cards relative to cash is found for all merchant activities and for debit and credit cardholders with the only exceptions of both debit and credit cardholders buying at grocery stores and supermarkets.

34 34

35 The impact of rewards programs by of type reward and sectors: controlling for merchant s acceptance Table 6 analyzes the impact of both the type of rewards and the type of card for three different groups of sectors depending on merchant s acceptance: Grocery stores and parking and tolls are considered in group 1 with very low use of cards. Supermarkets, boutiques and clothing, gas stations, restaurants, hotels and travel and leisure are jointly considered in group 2. This is potentially the benchmark group since both cash and cards are generally accepted by merchants and, therefore, preferences may play a more significant role in the choice of the payment instrument. Finally, group 3 incorporates department stores and superstores where card payments are typically far more frequent than cash, mainly as a consequence of the larger size of transactions.

36 36 As shown in Table 6, the impact of rewards is 8.7% and 8.6% for cardholders enjoying rewards programs in groups 2 and 3, respectively. The differences between both groups are not found to be statistically significant according to meandifference tests (not shown). However, as expected, the impact is considerably lower (1.4%) in merchant sectors under group 1 and the differences with the other two groups are found to be statistically significant. The results also show differences in the behavior of debit and credit cardholder across sectors. The impact of rewards seems to be considerably higher for debit cardholders.

37 37

38 7. Conclusions 38 We show that rewards programs can also significantly affect the preferences for cards relative to cash payments and that the marginal effect of these programs is the higher among the posited set of explanatory factors. Importantly, the effects of these rewards vary significantly among merchant sectors and the impact of rewards on card usage is higher for debit cardholders that for credit cardholders. Policymakers should have a closer look at the structure of incentives in the payment industry and the path of substitution of cash by card payments.

39 39 At the same time, the large expenses that card issuers undertake on incentive programs need to be confronted with the effectiveness of the different rewards programs on card usage (relative to cash) across merchant activities. Finally, the monetary value of the total impact of rewards show that, debit cardholders with rewards increase the value of purchases by 326,89 Euros for every 100 transactions they make. In the case of credit cards, this value of extra sales is 531,1 Euros.

The Costs and Benefits of Interchange Fee Regulation: An Empirical Investigation

The Costs and Benefits of Interchange Fee Regulation: An Empirical Investigation Santiago Carbo Valverde (U of Granada and Federal Reserve Bank of Chicago Sujit Chakravorti (Federal Reserve Bank of Chicago

The Costs and Benefits of Interchange Fee Regulation: An Empirical Investigation Santiago Carbo Valverde (U of Granada and Federal Reserve Bank of Chicago Sujit Chakravorti (Federal Reserve Bank of Chicago

Monetary Policy Implications of Electronic Currency: An Empirical Analysis. Christopher Fogelstrom. Ann L. Owen* Hamilton College.

Monetary Policy Implications of Electronic Currency: An Empirical Analysis Christopher Fogelstrom Ann L. Owen* Hamilton College February 2004 Abstract Using the 2001 Survey of Consumer Finances, we find

Monetary Policy Implications of Electronic Currency: An Empirical Analysis Christopher Fogelstrom Ann L. Owen* Hamilton College February 2004 Abstract Using the 2001 Survey of Consumer Finances, we find

Consumption, Credit Cards, and Monetary Policy

RESEARCH PROPOSAL: Consumption, Credit Cards, and Monetary Policy By: Mujtaba Zia, Ph.D. Candidate University of North Texas Department of Finance Abstract Oftentimes the purpose of a monetary policy action

RESEARCH PROPOSAL: Consumption, Credit Cards, and Monetary Policy By: Mujtaba Zia, Ph.D. Candidate University of North Texas Department of Finance Abstract Oftentimes the purpose of a monetary policy action

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables

Appendix A: Appendix Figures and Tables") ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

ONLINE APPENDIX (NOT FOR PUBLICATION) Appendix A: Appendix Figures and Tables 34 Figure A.1: First Page of the Standard Layout 35 Figure A.2: Second Page of the Credit Card Statement 36 Figure A.3: First

UPDATED IAA EDUCATION SYLLABUS

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

TOURISM GENERATION ANALYSIS BASED ON A SCOBIT MODEL * Lingling, WU **, Junyi ZHANG ***, and Akimasa FUJIWARA ****

TOURISM GENERATION ANALYSIS BASED ON A SCOBIT MODEL * Lingling, WU **, Junyi ZHANG ***, and Akimasa FUJIWARA ****. Introduction Tourism generation (or participation) is one of the most important aspects

TOURISM GENERATION ANALYSIS BASED ON A SCOBIT MODEL * Lingling, WU **, Junyi ZHANG ***, and Akimasa FUJIWARA ****. Introduction Tourism generation (or participation) is one of the most important aspects

The Impact of Mutual Recognition Agreements on Foreign Direct Investment and. Export. Yong Joon Jang. Oct. 11, 2010

The Impact of Mutual Recognition Agreements on Foreign Direct Investment and Export Yong Joon Jang Oct. 11, 2010 In this paper, I will attempt to analyze how MRAs affect horizontal FDI relative to the

The Impact of Mutual Recognition Agreements on Foreign Direct Investment and Export Yong Joon Jang Oct. 11, 2010 In this paper, I will attempt to analyze how MRAs affect horizontal FDI relative to the

Payment Card Reward Programs and Consumer Payment Choice

Payment Card Reward Programs and Consumer Payment Choice Andrew Ching University of Toronto Fumiko Hayashi Federal Reserve Bank of Kansas City The views expressed in this article are those of the authors

Payment Card Reward Programs and Consumer Payment Choice Andrew Ching University of Toronto Fumiko Hayashi Federal Reserve Bank of Kansas City The views expressed in this article are those of the authors

How Do Speed and Security Influence Consumers Payment Behavior?

How Do Speed and Security Influence Consumers Payment Behavior? No. 15-1 Scott Schuh and Joanna Stavins Abstract: The Federal Reserve named improvements in the speed and security of the payment system

How Do Speed and Security Influence Consumers Payment Behavior? No. 15-1 Scott Schuh and Joanna Stavins Abstract: The Federal Reserve named improvements in the speed and security of the payment system

The role of interchange fees in two-sided markets: An empirical investigation on payment. cards. Santiago Carbó Valverde (Bangor Business School)

") The role of interchange fees in two-sided markets: An empirical investigation on payment cards Santiago Carbó Valverde (Bangor Business School) Sujit Chakravorti (formerly Federal Reserve Bank of Chicago)

The role of interchange fees in two-sided markets: An empirical investigation on payment cards Santiago Carbó Valverde (Bangor Business School) Sujit Chakravorti (formerly Federal Reserve Bank of Chicago)

HOUSEHOLDS INDEBTEDNESS: A MICROECONOMIC ANALYSIS BASED ON THE RESULTS OF THE HOUSEHOLDS FINANCIAL AND CONSUMPTION SURVEY*

HOUSEHOLDS INDEBTEDNESS: A MICROECONOMIC ANALYSIS BASED ON THE RESULTS OF THE HOUSEHOLDS FINANCIAL AND CONSUMPTION SURVEY* Sónia Costa** Luísa Farinha** 133 Abstract The analysis of the Portuguese households

HOUSEHOLDS INDEBTEDNESS: A MICROECONOMIC ANALYSIS BASED ON THE RESULTS OF THE HOUSEHOLDS FINANCIAL AND CONSUMPTION SURVEY* Sónia Costa** Luísa Farinha** 133 Abstract The analysis of the Portuguese households

Consumer Response to Changes in Credit Supply: Evidence from Credit Card Data

Financial Institutions Center Consumer Response to Changes in Credit Supply: Evidence from Credit Card Data by David B. Gross Nicholas S. Souleles 00-04-B The Wharton Financial Institutions Center The

Financial Institutions Center Consumer Response to Changes in Credit Supply: Evidence from Credit Card Data by David B. Gross Nicholas S. Souleles 00-04-B The Wharton Financial Institutions Center The

Import Protection, Business Cycles, and Exchange Rates:

Import Protection, Business Cycles, and Exchange Rates: Evidence from the Great Recession Chad P. Bown The World Bank Meredith A. Crowley Federal Reserve Bank of Chicago Preliminary, comments welcome Any

Import Protection, Business Cycles, and Exchange Rates: Evidence from the Great Recession Chad P. Bown The World Bank Meredith A. Crowley Federal Reserve Bank of Chicago Preliminary, comments welcome Any

Factors Affecting Foreign Investor Choice in Types of U.S. Real Estate

JOURNAL OF REAL ESTATE RESEARCH Factors Affecting Foreign Investor Choice in Types of U.S. Real Estate Deborah Ann Ford* Hung-Gay Fung* Daniel A. Gerlowski* Abstract. Using transaction level data, we present

JOURNAL OF REAL ESTATE RESEARCH Factors Affecting Foreign Investor Choice in Types of U.S. Real Estate Deborah Ann Ford* Hung-Gay Fung* Daniel A. Gerlowski* Abstract. Using transaction level data, we present

Use of Credit Cards Before and After Bank and Credit Cards Law No in Turkey 1. Suleyman Acikalin 2

Journal of Economics and Development Studies December 2015, Vol. 3, No. 4, pp. 13-18 ISSN: 2334-2382 (Print), 2334-2390 (Online) Copyright The Author(s). All Rights Reserved. Published by American Research

Journal of Economics and Development Studies December 2015, Vol. 3, No. 4, pp. 13-18 ISSN: 2334-2382 (Print), 2334-2390 (Online) Copyright The Author(s). All Rights Reserved. Published by American Research

2015 SCPC Table of Contents Adoption of Accounts and Payment Instruments

2015 SCPC Table of Contents Adoption of Accounts and Payment Instruments Table 1 Current Ownership of Accounts and Account Access Technologies Table 2 Table 3 Table 4 Table 5a Table 5b Table 6 Table 7

2015 SCPC Table of Contents Adoption of Accounts and Payment Instruments Table 1 Current Ownership of Accounts and Account Access Technologies Table 2 Table 3 Table 4 Table 5a Table 5b Table 6 Table 7

Interpretation issues in heteroscedastic conditional logit models

Interpretation issues in heteroscedastic conditional logit models Michael Burton a,b,*, Katrina J. Davis a,c, and Marit E. Kragt a a School of Agricultural and Resource Economics, The University of Western

Interpretation issues in heteroscedastic conditional logit models Michael Burton a,b,*, Katrina J. Davis a,c, and Marit E. Kragt a a School of Agricultural and Resource Economics, The University of Western

Cash back on every purchase

BENEFITS GUIDE RBC Business Cash Back Mastercard Cash back on every purchase BUSINESS No annual fee. No complications. Just cash back. Thank you for choosing the RBC Business Cash Back Mastercard. It gives

BENEFITS GUIDE RBC Business Cash Back Mastercard Cash back on every purchase BUSINESS No annual fee. No complications. Just cash back. Thank you for choosing the RBC Business Cash Back Mastercard. It gives

Potential Effects of an Increase in Debit Card Fees

No. 11-3 Potential Effects of an Increase in Debit Card Fees Joanna Stavins Abstract: Recent changes to debit card interchange fees could lead to an increase in the cost of debit cards to consumers. This

No. 11-3 Potential Effects of an Increase in Debit Card Fees Joanna Stavins Abstract: Recent changes to debit card interchange fees could lead to an increase in the cost of debit cards to consumers. This

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1 Sumit Agarwal Georgetown University Amit Bubna Cornerstone Research Molly Lipscomb University of Virginia Abstract The within-month

Timing to the Statement: Understanding Fluctuations in Consumer Credit Use 1 Sumit Agarwal Georgetown University Amit Bubna Cornerstone Research Molly Lipscomb University of Virginia Abstract The within-month

Consumer Payment Choice: A Central Bank Perspective. Scott Schuh Federal Reserve Bank of Boston October 1, 2013

Consumer Payment Choice: A Central Bank Perspective Scott Schuh Federal Reserve Bank of Boston October 1, 2013 Originally presented to PULSE Financial Institution Oversight Committee, Washington, DC The

Consumer Payment Choice: A Central Bank Perspective Scott Schuh Federal Reserve Bank of Boston October 1, 2013 Originally presented to PULSE Financial Institution Oversight Committee, Washington, DC The

Working PaPer SerieS. regulating two-sided markets an empirical investigation. no 1137 / december 2009

RETAIL PAYMENTS: INTEGRATION AND INNOVATION Working PaPer SerieS no 1137 / december 2009 regulating two-sided markets an empirical investigation by Santiago Carbó-Valverde, Sujit Chakravorti and Francisco

RETAIL PAYMENTS: INTEGRATION AND INNOVATION Working PaPer SerieS no 1137 / december 2009 regulating two-sided markets an empirical investigation by Santiago Carbó-Valverde, Sujit Chakravorti and Francisco

No. 2006/19 Credit Cards: Facts and Theories. Carol C. Bertaut and Michael Halisassos

No. 2006/19 Credit Cards: Facts and Theories Carol C. Bertaut and Michael Halisassos Center for Financial Studies The Center for Financial Studies is a nonprofit research organization, supported by an

No. 2006/19 Credit Cards: Facts and Theories Carol C. Bertaut and Michael Halisassos Center for Financial Studies The Center for Financial Studies is a nonprofit research organization, supported by an

Hang Seng enjoy Commercial Card / Business Card Benefits Directory

Hang Seng enjoy Commercial Card / Business Card Benefits Directory Contents Important Points to Remember Page 1 Customer Privileges - Hang Seng enjoy Card Rewards Programme Page 2 - Online Shopping Security

Hang Seng enjoy Commercial Card / Business Card Benefits Directory Contents Important Points to Remember Page 1 Customer Privileges - Hang Seng enjoy Card Rewards Programme Page 2 - Online Shopping Security

The Composition Effect of Consumption around Retirement: Evidence from Singapore

The Composition Effect of Consumption around Retirement: Evidence from Singapore By SUMIT AGARWAL, JESSICA PAN AND WENLAN QIAN* * Agarwal: National University of Singapore, 15 Kent Ridge Drive, NUS Business

The Composition Effect of Consumption around Retirement: Evidence from Singapore By SUMIT AGARWAL, JESSICA PAN AND WENLAN QIAN* * Agarwal: National University of Singapore, 15 Kent Ridge Drive, NUS Business

Nordea Mastercard. Cardholder s guide

Nordea Mastercard Cardholder s guide 1 If you have any questions about your card, we will be happy to help you. and With Nordea Mastercard you can pay for products and services in Finland, abroad on the

Nordea Mastercard Cardholder s guide 1 If you have any questions about your card, we will be happy to help you. and With Nordea Mastercard you can pay for products and services in Finland, abroad on the

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The analysis of credit scoring models Case Study Transilvania Bank

The analysis of credit scoring models Case Study Transilvania Bank Author: Alexandra Costina Mahika Introduction Lending institutions industry has grown rapidly over the past 50 years, so the number of

The analysis of credit scoring models Case Study Transilvania Bank Author: Alexandra Costina Mahika Introduction Lending institutions industry has grown rapidly over the past 50 years, so the number of

Cash holdings determinants in the Portuguese economy 1

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

An ex-post analysis of Italian fiscal policy on renovation

An ex-post analysis of Italian fiscal policy on renovation Marco Manzo, Daniela Tellone VERY FIRST DRAFT, PLEASE DO NOT CITE June 9 th 2017 Abstract In June 2012, the share of dwellings renovation costs

An ex-post analysis of Italian fiscal policy on renovation Marco Manzo, Daniela Tellone VERY FIRST DRAFT, PLEASE DO NOT CITE June 9 th 2017 Abstract In June 2012, the share of dwellings renovation costs

Available online at ScienceDirect. Procedia Environmental Sciences 22 (2014 )

") Available online at www.sciencedirect.com ScienceDirect Procedia Environmental Sciences 22 (2014 ) 414 422 12th International Conference on Design and Decision Support Systems in Architecture and Urban

Available online at www.sciencedirect.com ScienceDirect Procedia Environmental Sciences 22 (2014 ) 414 422 12th International Conference on Design and Decision Support Systems in Architecture and Urban

Consumer Payment Choice: A Central Bank Perspective

Consumer Payment Choice: A Central Bank Perspective Scott Schuh Federal Reserve Bank of Boston September 29, 2009 Fiserv Cash and Logistics Connect Forum 2009 Boston Marriott Copley Place Presentation

Consumer Payment Choice: A Central Bank Perspective Scott Schuh Federal Reserve Bank of Boston September 29, 2009 Fiserv Cash and Logistics Connect Forum 2009 Boston Marriott Copley Place Presentation

Third project management meeting for reducing cash transactions in Kosovo. June 15 th, 2011

Third project management meeting for reducing cash transactions in Kosovo Project management group within the National Payments Council (NPC) June 15 th, 2011 CENTRAL BANK OF THE REPUBLIC OF KOSOVO 1.

Third project management meeting for reducing cash transactions in Kosovo Project management group within the National Payments Council (NPC) June 15 th, 2011 CENTRAL BANK OF THE REPUBLIC OF KOSOVO 1.

Introducing CashPay. The payroll card that delivers convenience and purchasing power. CashPay Card Guide

Introducing CashPay The payroll card that delivers convenience and purchasing power CashPay Card Guide Get started with CashPay card convenience now When you enroll to have your pay direct deposited to

Introducing CashPay The payroll card that delivers convenience and purchasing power CashPay Card Guide Get started with CashPay card convenience now When you enroll to have your pay direct deposited to

Market Variables and Financial Distress. Giovanni Fernandez Stetson University

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

Market Variables and Financial Distress Giovanni Fernandez Stetson University In this paper, I investigate the predictive ability of market variables in correctly predicting and distinguishing going concern

DOES THE DEVELOPMENT OF NON-CASH PAYMENTS AFFECT BANK LENDING?

DOES THE DEVELOPMENT OF NON-CASH PAYMENTS AFFECT BANK LENDING? Santiago Carbó Valverde* University of Granada and Federal Reserve Bank of Chicago Rafael López del Paso Economist Abstract: Previous studies

DOES THE DEVELOPMENT OF NON-CASH PAYMENTS AFFECT BANK LENDING? Santiago Carbó Valverde* University of Granada and Federal Reserve Bank of Chicago Rafael López del Paso Economist Abstract: Previous studies

Does the Equity Market affect Economic Growth?

The Macalester Review Volume 2 Issue 2 Article 1 8-5-2012 Does the Equity Market affect Economic Growth? Kwame D. Fynn Macalester College, kwamefynn@gmail.com Follow this and additional works at: http://digitalcommons.macalester.edu/macreview

The Macalester Review Volume 2 Issue 2 Article 1 8-5-2012 Does the Equity Market affect Economic Growth? Kwame D. Fynn Macalester College, kwamefynn@gmail.com Follow this and additional works at: http://digitalcommons.macalester.edu/macreview

Survey of Consumer Payment Choice: Preliminary Results 2008

Survey of Consumer Payment Choice: Preliminary Results 2008 Marianne Crowe Federal Reserve Bank of Boston FedExchange 2009 May 6, 2009 Presentation Overview Survey of Consumer Payment Choice (SCPC) Program

Survey of Consumer Payment Choice: Preliminary Results 2008 Marianne Crowe Federal Reserve Bank of Boston FedExchange 2009 May 6, 2009 Presentation Overview Survey of Consumer Payment Choice (SCPC) Program

Content Added to the Updated IAA Education Syllabus

IAA EDUCATION COMMITTEE Content Added to the Updated IAA Education Syllabus Prepared by the Syllabus Review Taskforce Paul King 8 July 2015 This proposed updated Education Syllabus has been drafted by

IAA EDUCATION COMMITTEE Content Added to the Updated IAA Education Syllabus Prepared by the Syllabus Review Taskforce Paul King 8 July 2015 This proposed updated Education Syllabus has been drafted by

Egyptian Married Women Don t desire to Work or Simply Can t? A Duration Analysis. Rana Hendy. March 15th, 2010

Egyptian Married Women Don t desire to Work or Simply Can t? A Duration Analysis Rana Hendy Population Council March 15th, 2010 Introduction (1) Domestic Production: identified as the unpaid work done

Egyptian Married Women Don t desire to Work or Simply Can t? A Duration Analysis Rana Hendy Population Council March 15th, 2010 Introduction (1) Domestic Production: identified as the unpaid work done

Discrete Choice Modeling

[Part 1] 1/15 0 Introduction 1 Summary 2 Binary Choice 3 Panel Data 4 Bivariate Probit 5 Ordered Choice 6 Count Data 7 Multinomial Choice 8 Nested Logit 9 Heterogeneity 10 Latent Class 11 Mixed Logit 12

[Part 1] 1/15 0 Introduction 1 Summary 2 Binary Choice 3 Panel Data 4 Bivariate Probit 5 Ordered Choice 6 Count Data 7 Multinomial Choice 8 Nested Logit 9 Heterogeneity 10 Latent Class 11 Mixed Logit 12

Introduction to Depository Institutions

Introduction to Depository Institutions Advanced Level What is a Depository Institution? Depository institution businesses that provide financial services What is the name of one depository institution

Introduction to Depository Institutions Advanced Level What is a Depository Institution? Depository institution businesses that provide financial services What is the name of one depository institution

CAN AGENCY COSTS OF DEBT BE REDUCED WITHOUT EXPLICIT PROTECTIVE COVENANTS? THE CASE OF RESTRICTION ON THE SALE AND LEASE-BACK ARRANGEMENT

CAN AGENCY COSTS OF DEBT BE REDUCED WITHOUT EXPLICIT PROTECTIVE COVENANTS? THE CASE OF RESTRICTION ON THE SALE AND LEASE-BACK ARRANGEMENT Jung, Minje University of Central Oklahoma mjung@ucok.edu Ellis,

CAN AGENCY COSTS OF DEBT BE REDUCED WITHOUT EXPLICIT PROTECTIVE COVENANTS? THE CASE OF RESTRICTION ON THE SALE AND LEASE-BACK ARRANGEMENT Jung, Minje University of Central Oklahoma mjung@ucok.edu Ellis,

The pass-through from market interest rates to bank lending rates in Germany

The pass-through from market interest rates to bank lending rates in Germany Bank lending rates play a key role in the process of monetary policy transmission. An in-depth analysis was therefore made of

The pass-through from market interest rates to bank lending rates in Germany Bank lending rates play a key role in the process of monetary policy transmission. An in-depth analysis was therefore made of

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

2017 IAA EDUCATION SYLLABUS

2017 IAA EDUCATION SYLLABUS 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging areas of actuarial practice. 1.1 RANDOM

2017 IAA EDUCATION SYLLABUS 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging areas of actuarial practice. 1.1 RANDOM

A MODIFIED MULTINOMIAL LOGIT MODEL OF ROUTE CHOICE FOR DRIVERS USING THE TRANSPORTATION INFORMATION SYSTEM

A MODIFIED MULTINOMIAL LOGIT MODEL OF ROUTE CHOICE FOR DRIVERS USING THE TRANSPORTATION INFORMATION SYSTEM Hing-Po Lo and Wendy S P Lam Department of Management Sciences City University of Hong ong EXTENDED

A MODIFIED MULTINOMIAL LOGIT MODEL OF ROUTE CHOICE FOR DRIVERS USING THE TRANSPORTATION INFORMATION SYSTEM Hing-Po Lo and Wendy S P Lam Department of Management Sciences City University of Hong ong EXTENDED

MBF1923 Econometrics Prepared by Dr Khairul Anuar

MBF1923 Econometrics Prepared by Dr Khairul Anuar L1 Introduction to Econometrics www.notes638.wordpress.com What is Econometrics? Econometrics means economic measurement. The scope of econometrics is

MBF1923 Econometrics Prepared by Dr Khairul Anuar L1 Introduction to Econometrics www.notes638.wordpress.com What is Econometrics? Econometrics means economic measurement. The scope of econometrics is

Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact and forecasting

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 21, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact and forecasting

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 21, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact and forecasting

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking?

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking? October 19, 2009 Ulrike Malmendier, UC Berkeley (joint work with Stefan Nagel, Stanford) 1 The Tale of Depression Babies I don t know

Retailer Payment Systems: Relative Merits of Cash and Payment Cards. Executive Summary. Economists Incorporated

Retailer Payment Systems: Relative Merits of Cash and Payment Cards Executive Summary Economists Incorporated November 19, 2014 Executive Summary Some merchants do not accept credit or debit cards ( payment

Retailer Payment Systems: Relative Merits of Cash and Payment Cards Executive Summary Economists Incorporated November 19, 2014 Executive Summary Some merchants do not accept credit or debit cards ( payment

Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 29, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact Fatoumata

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 29, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact Fatoumata

An Analysis of the Factors Affecting Preferences for Rental Houses in Istanbul Using Mixed Logit Model: A Comparison of European and Asian Side

The Empirical Economics Letters, 15(9): (September 2016) ISSN 1681 8997 An Analysis of the Factors Affecting Preferences for Rental Houses in Istanbul Using Mixed Logit Model: A Comparison of European

The Empirical Economics Letters, 15(9): (September 2016) ISSN 1681 8997 An Analysis of the Factors Affecting Preferences for Rental Houses in Istanbul Using Mixed Logit Model: A Comparison of European

Revisiting The Household s Savings Function in Karak, Pakistan

23 Revisiting The Household s Savings Function in Karak, Pakistan Asmatullah 1, Dr. Bashir Ahmad Khiliji 2, Dr. Syed Waqar Hussain 3, Dr. M. Khalid Mughal 4 Abstract The present study was undertaken in

23 Revisiting The Household s Savings Function in Karak, Pakistan Asmatullah 1, Dr. Bashir Ahmad Khiliji 2, Dr. Syed Waqar Hussain 3, Dr. M. Khalid Mughal 4 Abstract The present study was undertaken in

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

The corporate bond issuance global frenzy, what role for US Quantitative Easing?

The 2009-2013 corporate bond issuance global frenzy, what role for US Quantitative Easing? Lo Duca Marco, Nicoletti Giulio, Vidal Ariadna European Central Bank XI Emerging Markets Workshop Bank of Spain

The 2009-2013 corporate bond issuance global frenzy, what role for US Quantitative Easing? Lo Duca Marco, Nicoletti Giulio, Vidal Ariadna European Central Bank XI Emerging Markets Workshop Bank of Spain

PERCEPTION OF CARD USERS TOWARDS PLASTIC MONEY

PERCEPTION OF CARD USERS TOWARDS PLASTIC MONEY This chapter analyses the perception of card holders towards plastic money in India. The emphasis has been laid on the adoption, usage, value attributes,

PERCEPTION OF CARD USERS TOWARDS PLASTIC MONEY This chapter analyses the perception of card holders towards plastic money in India. The emphasis has been laid on the adoption, usage, value attributes,

CREDIT CARD PRODUCT INFORMATION BROCHURE

CREDIT CARD PRODUCT INFORMATION BROCHURE Effective from 1st March 2018 A CREDIT CARD IS A GREAT WAY TO MAKE PURCHASES IN-STORE, ONLINE OR OVER THE PHONE. IF USED EFFECTIVELY, IT CAN ALSO BE A GREAT WAY

CREDIT CARD PRODUCT INFORMATION BROCHURE Effective from 1st March 2018 A CREDIT CARD IS A GREAT WAY TO MAKE PURCHASES IN-STORE, ONLINE OR OVER THE PHONE. IF USED EFFECTIVELY, IT CAN ALSO BE A GREAT WAY

Do Domestic Chinese Firms Benefit from Foreign Direct Investment?

Do Domestic Chinese Firms Benefit from Foreign Direct Investment? Chang-Tai Hsieh, University of California Working Paper Series Vol. 2006-30 December 2006 The views expressed in this publication are those

Do Domestic Chinese Firms Benefit from Foreign Direct Investment? Chang-Tai Hsieh, University of California Working Paper Series Vol. 2006-30 December 2006 The views expressed in this publication are those

The Risk Tolerance and Stock Ownership of Business Owning Households

The Risk Tolerance and Stock Ownership of Business Owning Households Cong Wang and Sherman D. Hanna Data from the 1992-2004 Survey of Consumer Finances were used to examine the risk tolerance and stock

The Risk Tolerance and Stock Ownership of Business Owning Households Cong Wang and Sherman D. Hanna Data from the 1992-2004 Survey of Consumer Finances were used to examine the risk tolerance and stock

Discussion Reactions to Dividend Changes Conditional on Earnings Quality

Discussion Reactions to Dividend Changes Conditional on Earnings Quality DORON NISSIM* Corporate disclosures are an important source of information for investors. Many studies have documented strong price

Discussion Reactions to Dividend Changes Conditional on Earnings Quality DORON NISSIM* Corporate disclosures are an important source of information for investors. Many studies have documented strong price

Contrarian Trades and Disposition Effect: Evidence from Online Trade Data. Abstract

Contrarian Trades and Disposition Effect: Evidence from Online Trade Data Hayato Komai a Ryota Koyano b Daisuke Miyakawa c Abstract Using online stock trading records in Japan for 461 individual investors

Contrarian Trades and Disposition Effect: Evidence from Online Trade Data Hayato Komai a Ryota Koyano b Daisuke Miyakawa c Abstract Using online stock trading records in Japan for 461 individual investors

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies Ihtsham ul Haq Padda and Naeem Akram Abstract Tax based fiscal policies have been regarded as less policy tool to overcome the

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies Ihtsham ul Haq Padda and Naeem Akram Abstract Tax based fiscal policies have been regarded as less policy tool to overcome the

Financial Constraints and Consumers Response to Cash Flow News: Direct Evidence from Federal Tax Return Filings

Financial Constraints and Consumers Response to Cash Flow News: Direct Evidence from Federal Tax Return Filings Brian Baugh The Ohio State University, Fisher College of Business Itzhak (Zahi) Ben-David

Financial Constraints and Consumers Response to Cash Flow News: Direct Evidence from Federal Tax Return Filings Brian Baugh The Ohio State University, Fisher College of Business Itzhak (Zahi) Ben-David

The purpose of this paper is to examine the determinants of U.S. foreign

Review of Agricultural Economics Volume 27, Number 3 Pages 394 401 DOI:10.1111/j.1467-9353.2005.00234.x U.S. Foreign Direct Investment in Food Processing Industries of Latin American Countries: A Dynamic

Review of Agricultural Economics Volume 27, Number 3 Pages 394 401 DOI:10.1111/j.1467-9353.2005.00234.x U.S. Foreign Direct Investment in Food Processing Industries of Latin American Countries: A Dynamic

UK Plastic Cards 2009 The Way We Pay

UK Plastic Cards 2009 The Way We Pay Plastic cards are the most popular non-cash payment method in the UK. They allow cardholders to pay for goods and services easily and conveniently, and provide a secure

UK Plastic Cards 2009 The Way We Pay Plastic cards are the most popular non-cash payment method in the UK. They allow cardholders to pay for goods and services easily and conveniently, and provide a secure

CREDIT RISK AND STRESS TESTING OF THE BANKING SECTOR IN THE CZECH REPUBLIC 57

CREDIT RISK AND STRESS TESTING OF THE BANKING SECTOR IN THE CZECH REPUBLIC 57 CREDIT RISK AND STRESS TESTING OF THE BANKING SECTOR IN THE CZECH REPUBLIC Petr Jakubík and Jaroslav Heřmánek, CNB This article

CREDIT RISK AND STRESS TESTING OF THE BANKING SECTOR IN THE CZECH REPUBLIC 57 CREDIT RISK AND STRESS TESTING OF THE BANKING SECTOR IN THE CZECH REPUBLIC Petr Jakubík and Jaroslav Heřmánek, CNB This article

Lecture 1: Logit. Quantitative Methods for Economic Analysis. Seyed Ali Madani Zadeh and Hosein Joshaghani. Sharif University of Technology

Lecture 1: Logit Quantitative Methods for Economic Analysis Seyed Ali Madani Zadeh and Hosein Joshaghani Sharif University of Technology February 2017 1 / 38 Road map 1. Discrete Choice Models 2. Binary

Lecture 1: Logit Quantitative Methods for Economic Analysis Seyed Ali Madani Zadeh and Hosein Joshaghani Sharif University of Technology February 2017 1 / 38 Road map 1. Discrete Choice Models 2. Binary

DNB W o r k i n g P a p e r. Digitization of Retail Payments. No. 270 / December Wilko Bolt and Sujit Chakravorti

DNB Working Paper No. 270 / December 2010 Wilko Bolt and Sujit Chakravorti Digitization of Retail Payments DNB W o r k i n g P a p e r Digitization of Retail Payments Wilko Bolt and Sujit Chakravorti *

DNB Working Paper No. 270 / December 2010 Wilko Bolt and Sujit Chakravorti Digitization of Retail Payments DNB W o r k i n g P a p e r Digitization of Retail Payments Wilko Bolt and Sujit Chakravorti *

An Empirical Analysis on the Relationship between Health Care Expenditures and Economic Growth in the European Union Countries

An Empirical Analysis on the Relationship between Health Care Expenditures and Economic Growth in the European Union Countries Çiğdem Börke Tunalı Associate Professor, Department of Economics, Faculty

An Empirical Analysis on the Relationship between Health Care Expenditures and Economic Growth in the European Union Countries Çiğdem Börke Tunalı Associate Professor, Department of Economics, Faculty

News Media Channels: Complements or Substitutes? Evidence from Mobile Phone Usage. Web Appendix PSEUDO-PANEL DATA ANALYSIS

1 News Media Channels: Complements or Substitutes? Evidence from Mobile Phone Usage Jiao Xu, Chris Forman, Jun B. Kim, and Koert Van Ittersum Web Appendix PSEUDO-PANEL DATA ANALYSIS Overview The advantages

1 News Media Channels: Complements or Substitutes? Evidence from Mobile Phone Usage Jiao Xu, Chris Forman, Jun B. Kim, and Koert Van Ittersum Web Appendix PSEUDO-PANEL DATA ANALYSIS Overview The advantages

An Analysis of Spain s Sovereign Debt Risk Premium

The Park Place Economist Volume 22 Issue 1 Article 15 2014 An Analysis of Spain s Sovereign Debt Risk Premium Tim Mackey '14 Illinois Wesleyan University, tmackey@iwu.edu Recommended Citation Mackey, Tim

The Park Place Economist Volume 22 Issue 1 Article 15 2014 An Analysis of Spain s Sovereign Debt Risk Premium Tim Mackey '14 Illinois Wesleyan University, tmackey@iwu.edu Recommended Citation Mackey, Tim

Bank Loan Officers Expectations for Credit Standards: evidence from the European Bank Lending Survey

Bank Loan Officers Expectations for Credit Standards: evidence from the European Bank Lending Survey Anastasiou Dimitrios and Drakos Konstantinos * Abstract We employ credit standards data from the Bank

Bank Loan Officers Expectations for Credit Standards: evidence from the European Bank Lending Survey Anastasiou Dimitrios and Drakos Konstantinos * Abstract We employ credit standards data from the Bank

NSTTUTE RESEARCH. POVERTYD,scWK~~~~ i;~(i UNIVERSI1Y OF WISCONSIN -MADISON. FILE (:()py :DO NOT REMOVE William Bradford and Timothy Bates

py :DO NOT REMOVE William Bradford and Timothy Bates") FILE (:()py :DO NOT REMOVE 269-75 \ NSTTUTE RESEARCH FOR ON POVERTYD,scWK~~~~ LOAN DEFAULT AMONG BLACK ENTREPRENEURS FORMING NEW CENTRAL CITY BUSINESSES William Bradford and Timothy Bates ~~ UNIVERSI1Y

FILE (:()py :DO NOT REMOVE 269-75 \ NSTTUTE RESEARCH FOR ON POVERTYD,scWK~~~~ LOAN DEFAULT AMONG BLACK ENTREPRENEURS FORMING NEW CENTRAL CITY BUSINESSES William Bradford and Timothy Bates ~~ UNIVERSI1Y

International Review of Business Research Papers Vol. 4 No.3 June 2008 Pp

International Review of Business Research Papers Vol. 4 No.3 June 2008 Pp.213-221 Budget Size and Risk Perception in Capital Budgeting Decisions of German Managers Uma V. Sridharan and Ulrich Schuele In

International Review of Business Research Papers Vol. 4 No.3 June 2008 Pp.213-221 Budget Size and Risk Perception in Capital Budgeting Decisions of German Managers Uma V. Sridharan and Ulrich Schuele In

Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence

ISSN 2029-4581. ORGANIZATIONS AND MARKETS IN EMERGING ECONOMIES, 2012, VOL. 3, No. 1(5) Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence from and the Euro Area Jolanta

ISSN 2029-4581. ORGANIZATIONS AND MARKETS IN EMERGING ECONOMIES, 2012, VOL. 3, No. 1(5) Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence from and the Euro Area Jolanta

Bank Lending Shocks and the Euro Area Business Cycle

Bank Lending Shocks and the Euro Area Business Cycle Gert Peersman Ghent University Motivation SVAR framework to examine macro consequences of disturbances specific to bank lending market in euro area

Bank Lending Shocks and the Euro Area Business Cycle Gert Peersman Ghent University Motivation SVAR framework to examine macro consequences of disturbances specific to bank lending market in euro area

1 Excess burden of taxation

1 Excess burden of taxation 1. In a competitive economy without externalities (and with convex preferences and production technologies) we know from the 1. Welfare Theorem that there exists a decentralized

1 Excess burden of taxation 1. In a competitive economy without externalities (and with convex preferences and production technologies) we know from the 1. Welfare Theorem that there exists a decentralized

Potential drivers of insurers equity investments

Potential drivers of insurers equity investments Petr Jakubik and Eveline Turturescu 67 Abstract As a consequence of the ongoing low-yield environment, insurers are changing their business models and looking

Potential drivers of insurers equity investments Petr Jakubik and Eveline Turturescu 67 Abstract As a consequence of the ongoing low-yield environment, insurers are changing their business models and looking

Oesterreichische Nationalbank. Eurosystem. Workshops. Proceedings of OeNB Workshops. Macroeconomic Models and Forecasts for Austria

Oesterreichische Nationalbank Eurosystem Workshops Proceedings of OeNB Workshops Macroeconomic Models and Forecasts for Austria November 11 to 12, 2004 No. 5 Comment on Evaluating Euro Exchange Rate Predictions

Oesterreichische Nationalbank Eurosystem Workshops Proceedings of OeNB Workshops Macroeconomic Models and Forecasts for Austria November 11 to 12, 2004 No. 5 Comment on Evaluating Euro Exchange Rate Predictions

Understanding the Consumer Price Index (CPI)

") ESO PUBLICATIONS Consumer Price Index (CPI) Reports Quarterly Economic Reports (QER) Labour Force Survey (LFS) Reports Annual Overseas Trade Reports Annual Compendium of Statistics Annual Economics Report

ESO PUBLICATIONS Consumer Price Index (CPI) Reports Quarterly Economic Reports (QER) Labour Force Survey (LFS) Reports Annual Overseas Trade Reports Annual Compendium of Statistics Annual Economics Report

ARE PUBLIC SECTOR WORKERS MORE RISK AVERSE THAN PRIVATE SECTOR WORKERS? DON BELLANTE and ALBERT N. LINK*

ARE PUBLIC SECTOR WORKERS MORE RISK AVERSE THAN PRIVATE SECTOR WORKERS? DON BELLANTE and ALBERT N. LINK* Available evidence suggests that stability of employment is greater in the public sector than in

ARE PUBLIC SECTOR WORKERS MORE RISK AVERSE THAN PRIVATE SECTOR WORKERS? DON BELLANTE and ALBERT N. LINK* Available evidence suggests that stability of employment is greater in the public sector than in

Why do patients prefer hospital emergency visits? A nested multinomial logit analysis for patient-initiated contacts

Health Care Management Science 1 1998) 39 52 39 Why do patients prefer hospital emergency visits? A nested multinomial logit analysis for patient-initiated contacts Jaume Puig-Junoy a, Marc Saez b and

Health Care Management Science 1 1998) 39 52 39 Why do patients prefer hospital emergency visits? A nested multinomial logit analysis for patient-initiated contacts Jaume Puig-Junoy a, Marc Saez b and

Networks Performance and Contractual Design: Empirical Evidence from Franchising

Networks Performance and Contractual Design: Empirical Evidence from Franchising Magali Chaudey, Muriel Fadairo To cite this version: Magali Chaudey, Muriel Fadairo. Networks Performance and Contractual

Networks Performance and Contractual Design: Empirical Evidence from Franchising Magali Chaudey, Muriel Fadairo To cite this version: Magali Chaudey, Muriel Fadairo. Networks Performance and Contractual

Econometric Methods for Valuation Analysis

Econometric Methods for Valuation Analysis Margarita Genius Dept of Economics M. Genius (Univ. of Crete) Econometric Methods for Valuation Analysis Cagliari, 2017 1 / 25 Outline We will consider econometric

Econometric Methods for Valuation Analysis Margarita Genius Dept of Economics M. Genius (Univ. of Crete) Econometric Methods for Valuation Analysis Cagliari, 2017 1 / 25 Outline We will consider econometric

1 A Simple Model of the Term Structure

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Comment on Dewachter and Lyrio s "Learning, Macroeconomic Dynamics, and the Term Structure of Interest Rates" 1 by Jordi Galí (CREI, MIT, and NBER) August 2006 The present paper by Dewachter and Lyrio

Part II 2011 Syllabus:

Part II 2011 Syllabus: Part II 2011 is comprised of Part IIA The Actuarial Control Cycle and Part IIB Investments and Asset Modelling. Part IIA The Actuarial Control Cycle The aim of the Actuarial Control

Part II 2011 Syllabus: Part II 2011 is comprised of Part IIA The Actuarial Control Cycle and Part IIB Investments and Asset Modelling. Part IIA The Actuarial Control Cycle The aim of the Actuarial Control

Discussion on Credit Cards and Consumption By Scott Fulford and Scott Schuh

Discussion on Credit Cards and Consumption By Scott Fulford and Scott Schuh Fumiko Hayashi Federal Reserve Bank of Kansas City Economics of Payments IX BIS November 16, 2018 The views are my own and do

Discussion on Credit Cards and Consumption By Scott Fulford and Scott Schuh Fumiko Hayashi Federal Reserve Bank of Kansas City Economics of Payments IX BIS November 16, 2018 The views are my own and do

CAUSAL RELATIONSHIP BETWEEN ISLAMIC AND CONVENTIONAL BANKING INSTRUMENTS IN MALAYSIA

CAUSAL RELATIONSHIP BETWEEN ISLAMIC AND CONVENTIONAL BANKING INSTRUMENTS IN MALAYSIA Ahmad Kaleem & Mansor Md Isa Islamic banking industry makes significant contributions to the economic development process

CAUSAL RELATIONSHIP BETWEEN ISLAMIC AND CONVENTIONAL BANKING INSTRUMENTS IN MALAYSIA Ahmad Kaleem & Mansor Md Isa Islamic banking industry makes significant contributions to the economic development process

Understanding Consumer Cash Use: Preliminary Findings from the 2016 Diary of Consumer Payment Choice

Introduction Understanding Consumer Cash Use: Preliminary Findings from the 2016 Diary of Consumer Payment Choice The public s demand for cash continues to grow as the amount of currency in circulation

Introduction Understanding Consumer Cash Use: Preliminary Findings from the 2016 Diary of Consumer Payment Choice The public s demand for cash continues to grow as the amount of currency in circulation

14.99% to 24.99%, based on your creditworthiness. This APR will vary with the market based on the Prime Rate.

Summary of Credit Terms PLEASE NOTE: If you apply for the Union Bank Visa Rewards Card and meet our eligibility criteria for the Visa Signature Card, you agree that we may consider your application as

Summary of Credit Terms PLEASE NOTE: If you apply for the Union Bank Visa Rewards Card and meet our eligibility criteria for the Visa Signature Card, you agree that we may consider your application as

Financial Risk Tolerance and the influence of Socio-demographic Characteristics of Retail Investors

Financial Risk Tolerance and the influence of Socio-demographic Characteristics of Retail Investors * Ms. R. Suyam Praba Abstract Risk is inevitable in human life. Every investor takes considerable amount

Financial Risk Tolerance and the influence of Socio-demographic Characteristics of Retail Investors * Ms. R. Suyam Praba Abstract Risk is inevitable in human life. Every investor takes considerable amount

The Lack of Persistence of Employee Contributions to Their 401(k) Plans May Lead to Insufficient Retirement Savings

Plans May Lead to Insufficient Retirement Savings") Upjohn Institute Policy Papers Upjohn Research home page 2011 The Lack of Persistence of Employee Contributions to Their 401(k) Plans May Lead to Insufficient Retirement Savings Leslie A. Muller Hope College

Upjohn Institute Policy Papers Upjohn Research home page 2011 The Lack of Persistence of Employee Contributions to Their 401(k) Plans May Lead to Insufficient Retirement Savings Leslie A. Muller Hope College

The trade balance and fiscal policy in the OECD

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

Analyzing the Determinants of Project Success: A Probit Regression Approach

2016 Annual Evaluation Review, Linked Document D 1 Analyzing the Determinants of Project Success: A Probit Regression Approach 1. This regression analysis aims to ascertain the factors that determine development

2016 Annual Evaluation Review, Linked Document D 1 Analyzing the Determinants of Project Success: A Probit Regression Approach 1. This regression analysis aims to ascertain the factors that determine development

Payment choice with Consumer Panel Data

Payment choice with Consumer Panel Data Michael Cohen Stern School of Business Marc Rysman Boston University November 5, 2012 Abstract We exploit scanner data to track payment choice for grocery purchases

Payment choice with Consumer Panel Data Michael Cohen Stern School of Business Marc Rysman Boston University November 5, 2012 Abstract We exploit scanner data to track payment choice for grocery purchases

The Mark of Your Achievement

The Mark of Your Achievement Maybank Visa Signature Welcome to the card that steps up your lifestyle to the next level. Set yourself apart from the rest by changing the game with Visa Signature, Indulge

The Mark of Your Achievement Maybank Visa Signature Welcome to the card that steps up your lifestyle to the next level. Set yourself apart from the rest by changing the game with Visa Signature, Indulge

This version: 15 August Empirical consumer payment price sensitivity has implications for theory, optimal

Debit or Credit? Jonathan Zinman a, * a Department of Economics, Dartmouth College, Hanover, NH 03755, United States This version: 15 August 2008 Abstract Empirical consumer payment price sensitivity has

Debit or Credit? Jonathan Zinman a, * a Department of Economics, Dartmouth College, Hanover, NH 03755, United States This version: 15 August 2008 Abstract Empirical consumer payment price sensitivity has

Evaluating the Macroeconomic Effects of a Temporary Investment Tax Credit by Paul Gomme

p d papers POLICY DISCUSSION PAPERS Evaluating the Macroeconomic Effects of a Temporary Investment Tax Credit by Paul Gomme POLICY DISCUSSION PAPER NUMBER 30 JANUARY 2002 Evaluating the Macroeconomic Effects

p d papers POLICY DISCUSSION PAPERS Evaluating the Macroeconomic Effects of a Temporary Investment Tax Credit by Paul Gomme POLICY DISCUSSION PAPER NUMBER 30 JANUARY 2002 Evaluating the Macroeconomic Effects

Econometrics and Economic Data

Econometrics and Economic Data Chapter 1 What is a regression? By using the regression model, we can evaluate the magnitude of change in one variable due to a certain change in another variable. For example,

Econometrics and Economic Data Chapter 1 What is a regression? By using the regression model, we can evaluate the magnitude of change in one variable due to a certain change in another variable. For example,