Payments 101. An Overview the US Payment Networks. René M Pelegero, President, Retail Payments Global Consulting Group

|

|

|

- Lynn Lester

- 5 years ago

- Views:

Transcription

1 Retail Payments Global Consulting Group L.L.C. Payments 101 An Overview the US Payment Networks René M Pelegero, President, Retail Payments Global Consulting Group

2 A Payment is an Exchange of Value Value Financial Non Financial In Financial Institutions Outside Financial Institutions Reward Miles & Points Goods & Services Deposits Credit Lines Credit Lines Cash Other Today, most payments are funded by credit lines and deposits being held at financial institutions

3 RPGC Payments Framework Delivery Layer Wallets Gateways Aggregators Other This layer evolved to address the deficiencies in traditional payment instruments Sometimes consumers think of this as the payment instrument Instrument Layer Credit Cards Debit Cards Prepaid Cards Network Layer VI/MC/AX. etc. EFT Networks ACH Networks RTN/Acct Numbers Check/Paper Clearing Houses Paper Docs (Checks, Boletos, etc.) Pre-Paid Vendors Value holders (e.g. financial institutions,) provide Payment Instruments to access the value Instruments contain credentials used to initiate transactions Payment instructions initiated by credentials must travel through payment networks Networks are sometimes branded & brands often extend to the instruments (e.g. Visa / Mastercard) Value Layer Credit Lines Deposit Accounts Stored Value Typically value is money which is kept in Financial Institutions Value is also a credit line or a stored value in a pre-paid account Copyright RPGC Group LLC All rights reserved

OBeP userid & password Phone # Network Layer VI/MC/AX etc.")

4 RPGC Payments Framework New Players New Instrument, Network, and Value layer elements are being introduced Players expanding their presence across other layers Delivery Layer Wallets Gateways Aggregators Other Instrument Layer Credit Cards Debit Cards Prepaid Cards RTN/Acct Numbers Paper Docs (Checks, Boletos, etc.) OBeP userid & password Phone # Network Layer VI/MC/AX etc. EFT Networks ACH Networks Check/Paper Clearing Houses Pre-Paid Vendors Telco carriers OBeP services C-stores Value Layer Credit Lines Deposit Accounts Stored Value Telco/Retailer Credit Lines Third Party Credit Lines Cash Other (e.g. FF miles, mobile minutes) Copyright RPGC Group LLC All rights reserved

5 Payments is A Mix and Match Pay Before Pay Now Pay Later How/when consumers pay Merchant Pull Consumer Push How merchants collect funds Batch Based Networks Real Time Networks Speed of funds transfer Paper Checks Bank Transfers (ACH, Giro) Local Payment or Pre-paid Cards Int l Credit & Debit Cards ATM/EFT Wire Transfer (SWIFT, Fedwire)

6 Payment Networks Around The World

7 Retail Payments Global Consulting Group L.L.C. Payments 101 Card Based Networks

8 General Purpose Payment Cards (GPPC) Can be used globally Can support multiple currencies Can be credit or debit depending account type being accessed Strength is their brand recognition

9 Local Payment Cards Can only be used in the country of issuance Generally support only one currency Most are debit cards Well recognized in their countries but many are cobranded allowing them to be used internationally

10 PIN Based Cards Can only be used with a PIN (PIN Pad) Most are domestic cards only Primarily debit cards

11 Cards Can Have Multiple Personalities Signature based, international use Signature based, international use International ATM use International ATM use International POS use International POS use Domestic ATM use Domestic ATM & POS use Domestic ATM & POS use Domestic ATM use

12 Co-Branded Cards and Affinity Cards GPPCs issued with a third party name on the face of the card Issued by a bank ( funding source is a bank credit line) Third party (retailer or sponsor) actively engaged in recruiting cardholders for a bounty

13 Corporate and Purchasing Cards Specialized cards issued to corporations for purchases and for travel & entertainment Specialized issuers that provide detailed reporting to corporate accounting depts. Different fee structure than consumer cards

14 Private Label Credit Cards Funding source normally outside financial institutions Generally, they can only be used at the retailer that issued the card Provide more consumer data than GPPCs

or closed loop (e.g.")

15 Pre-Paid & Stored Value Cards Issued by retailers, financial institutions, and companies that specialize in the business Can be open loop (e.g. Visa or MasterCard) or closed loop (e.g. Starbucks) Huge growth area in last few years

16 Card Processing Models Two Corners Merchant issues card and has direct relationship with cardholder Sometimes a third party acts as issuer on behalf of merchant (e.g. GE, Citi) Pros Lower payment cost, support promotions, better consumer data Cons Credit losses, cardholder can only use card at issuing merchant Merchant Cardholder

17 Card Processing Models Three Corners A Third Party card issuer has relationships with both cardholder and merchant and acts as intermediary between them in a transaction Pros Access additional consumers Cons Higher payment costs, additional contract & reconciliation processes Some 3-corner model brands turning into 4- corner Merchant Cardholder

18 Card Processing Models Four Corners Card Issuer has a relationship with cardholder but not merchant; Card Acquirer has a relationship with merchant but not cardholder. GPPC Brands ( i.e. VI/MC) act as intermediaries between four parties in transaction Acquirer Issuer Merchant Cardholder

, Independent Sales")

19 Card Processing Models Acquirers, Processors, ISOs, & Gateways Acquirers and Issuer can perform their functions themselves or engage third party processor to perform some or all of their functions Merchant can connect directly to acquirer (or processors performing the work on behalf of an acquirer), Independent Sales Organizations or ISOs, or Gateways Gateways and processors do not assume financial responsibility for transactions, ISOs and Acquirers do Acquirers Issuers Processor Processor ISO Gateway Merchant

20 Four Corner Model Authorization Request Merchant swipes card through POS device and enters transaction amount POS devices composes message including CVV and Track 2 data and sends it to merchant acquiring bank Acquiring bank sends authorization request to Issuer via the VI/MC switch Acquirer Issuer Merchant-Device-ID CC Number Amount Curr CVV TRK2 ExDt Time Stamp USD 425 xxxxx 01/ Merchant Cardholder

21 Four Corner Model Authorization Request Processing Issuer (or its processor) receives authorization request Issuer performs a number of checks prior to authorize transaction Response must be delivered back to VI/MC in less than 5 seconds average Issuer Approved Ask customer to sign sales receipt Declined Ask for another payment instrument Check card data (e.g. check digit) & run fraud checks Run velocity & limits checks Run behavioral checks Check balances and open to buy Place HOLD on authorization amount Compose response message Call (referral) Contact voice authorization center Pick-up Keep card No Match Keep card & Code 10

22 Four Corner Model Authorization Request Reply Issuer replies with a response code and an authorization code If transaction is approved, customer must be asked to sign receipt and merchant captures the transaction If transaction is declined, customer must be asked for another payment instrument Merchant-Device-ID CC Number Amount Curr CVV TRK2 ExDt Resp Auth # Time Stamp USD 425 xxxxx 01/ Acquirer Issuer Merchant Cardholder

23 Four Corner Model CNP Authorization Request* Merchant asks for billing address and Card Verification Value (CVV) Merchant servers compose message and sends it to merchant acquiring bank Acquiring bank sends authorization request to Issuer via the VI/MC switch Acquirer Issuer Merchant-Device-ID CC Number Amount Curr CVV2 Billing Address ExDt Time Stamp USD Main St. Anytown, CA / * Not including 3DSecure processing Merchant Cardholder 3 digit Card Verification Number

Contact voice")

24 Four Corner Model CNP Authorization Processing* Issuer (or its processor) receives authorization request Issuer performs a number of checks prior to authorize transaction Response must be delivered back to VI/MC in less than 5 seconds average Additional Checks Issuer Approved Declined Ask customer to sign sales receipt Ask for another payment instrument Check card data (e.g. check digit) & run fraud checks Check CVV and AVS Run velocity & limits checks Run behavioral checks Check balances and open to buy Place HOLD on authorization amount Compose response message Call (referral) Contact voice authorization center Pick-up Keep card No Match Keep card & Code 10 * Not including 3DSecure processing

25 Four Corner Model CNP Authorization Reply* Issuer replies with a response code, an authorization code, AND a CVV and AVS codes If transaction is approved, CVV and AVS match, proceed with, and capture, transaction If transaction is approved, but CVV and AVS do not match, merchant must decide if to proceed If transaction is declined, customer must be asked for another payment instrument Merchant-Device-ID CC Number Amount Curr CVV ExDt Resp Auth # CVN AVS Time Stamp USD / Y P Acquirer Issuer Merchant Cardholder * Not including 3DSecure processing

26 Four Corner Model Special Authorization Cases Stand-In Processing Provided by VI/MC whenever an Issuer cannot deliver a timely response to authorization requests (positive or negative files, limits & velocity checks, name match, etc.) VI/MC also provide fraud detection tools through the use of neural networks, delivering risk scores to the acquirer Balance Inquiries & Partial Authorizations In support of pre-paid cards and allowance of split tender Single Message vs Dual Message authorizations Estimated Authorization Amounts Allowed only to special merchant category codes (e.g. T&E and transit, fuel dispensers, some service related merchants) Allows for incremental authorizations Authorization Reversals To undo the effects of an authorization when transaction is not completed or amount is less than authorized amount Must be done within 24 hours (Card Present) or 72 hours (Card Not Present) E-Commerce/MOTO (Card Not Present) Merchants Additional information requirements Batch processing 3D Secure Account Updater Program

Acquirer collects all transactions from all its merchants and submits them to the appropriate card scheme (e.g.")

27 Four Corner Model Clearing, Settlement, Funds Transfer Merchant (or its processor/gateway) transmits all transactions to Acquirer for a given processing period (if Acquirer has not performed draft capture) Acquirer collects all transactions from all its merchants and submits them to the appropriate card scheme (e.g. Visa or MasterCard) Acquirer Issuer Merchant-Device-ID CC Number Amount Curr CVV ExDt Resp Auth # CVN AVS Time Stamp Merchant-Device-ID CC Number Amount Curr CVV ExDt Resp Auth # CVN AVS Time Stamp Merchant-Device-ID CC Number Amount USD Curr 425 CVV 01/08 ExDt 000 Resp Auth # Y CVN P AVS Time Stamp Merchant-Device-ID CC Number Amount USD Curr 425 CVV 01/08 ExDt 000 Resp Auth # Y CVN P AVS Time Stamp USD / Y P USD / Y P Merchant

for posting Check acquirer files Calculate acquirer fees and assessments Sort by BIN Calculate Issuer fees and assessments Calculate Net")

28 Four Corner Model Clearing, Settlement, Funds Transfer VI/MC collect transactions from all Acquirers (or their processors) VI/MC calculates interchange and fees and sorts transactions by destination BIN VI/MC sends files to issuers (or their processors) for posting Check acquirer files Calculate acquirer fees and assessments Sort by BIN Calculate Issuer fees and assessments Calculate Net Position for Acquirers and Issues Create and transmit outbound files to issuers * Not including 3DSecure processing

29 Interchange Transfer price between the Acquirer and Issuer Originally intended to reimburse issuers for specific costs (i.e. Authorization, Clearing, and Settlement) Explicit revenue to Card Issuer, cost to Merchant Acquirer Not a revenue source for Visa or MasterCard or Acquirers Set by the VI/MC to balance the needs of issuer incentives to issue cards and the reluctance of merchants to pay high swipe fees Card Brand 4% Acquirer 7% Interchange to Issuer 89% Approximate Breakdown of $1 Merchant Fees (USA)

30 Interchange Rate Change Process Card schemes define rates for different types of transactions Rates approved by respective card scheme boards Card schemes have two major software releases per year April and October - where changes to interchange are announced Multiple interchange categories Rates are set by each region and by countries within each region Corporate offices set International interchange Merchant Country (Seller Business Address) Card Type (Visa): Signature, Signature Preferred, Rewards, Other Ticket Size Micro, Large Security: AVS PIN CVV2/CVC2 Signature 3DS Determines Interchange Rate Category Buyer Country (Card Billing Address) Distribution Channel POS, Web MCC & Eligibility Airlines, Retail, Recurring; Registration Program Type: Consumer v Commerci Debit v Credit Reward Txn Performance Speed of auth/settle Amt Tolerance

31 Four Corner Model Clearing, Settlement, Funds Transfer Transaction initiated by a Visa Signature Credit Card issued in the US at a US retailer that qualifies for CPS/Retail Credit interchange category and which is properly authorized Acquirer Fee Type Rate Calculated Issuer Submit $100 Interchange - Ad Valorem 1.65% $1.65 Interchange Flat Fee $0.10 $0.10 Assessment 0.11% $0.11 Visa Network Acquirer Processing Fee Debit (NAPF) $ $ Visa Settlement Network Access Fee (Base II Fee) $ $ International Acquirer 0.45% $0.00 Misuse of authorization $0.045 $0.00 Unauthorized transaction $0.10 $0.00 Fixed Acquirer Network Fee (FANF) (Monthly fee by location) TBD $0.00 Acquirer Fees Total $1.88 Issuer Assessment and Fees Total $0.03 IS OWED $98.12 NET POSITION OWES $98.15

32 Four Corner Model Clearing, Settlement, Funds Transfer VI/MC settle Net Positions with its members through Wire Transfers (e.g. Fedwire or SWIFT) Issuer pays Visa (or MC) $98.15 for the $100 transaction and Visa (or MC) pay Acquirer $98.12 for the $100 transaction, netting $0.03 on that transaction Acquirer Issuer

33 Four Corner Model Clearing, Settlement, Funds Transfer Issuer collects $100 from cardholder plus any finance fees if the cardholder does not pay the full amount (i.e. revolves ). If no finance fees are paid, issuer nets $1.85 on that transaction Acquirer Issuer

34 Four Corner Model Clearing, Settlement, Funds Transfer Acquirer pays merchant the $100 MINUS all agreed fees Two ways for merchant to pay its fees Discount (e.g. 2.00% - Acquirer pays merchant $98.00 on that transaction, netting $0.12) Pass-through plus fee (e.g. $0.05/tx Acquirer pays merchant $98.07, netting $0.05) Acquirer Issuer Discount Transact ion Fee Pass-through fees Other Fees Interchange Assessments

35 Four Corner Model Dispute Processing Three Steps Copy or Retrieval Request Chargebacks Pre-Arbitration and Arbitration Chargeback types Technical Service Related Fraud Special Cases Mail Order and e-commerce Merchants Recurring Transactions

36 Four Corner Model Dispute Processing Copy/Retrieval request follows the same paths and it is usually performed before a dispute is submitted as a chargeback VI/MC send chargeback to Acquirer after Including financial impact on Net Position Acquirer forwards chargeback to merchant after including financial impact on net settlement Acquirer Issuer issuer sends chargeback Information electronically to VI/MC Merchant accepts the chargeback or resubmits transaction ( representation ) with supporting documentation to validate original transaction Merchant Cardholder cardholder initiates dispute

37 Four Corner Model Dispute Processing Visa and MasterCard differ regarding the handling of second chargebacks. Visa does not support 2 nd chargebacks, asking instead to go to pre-arbitration Acquirer reviews representation and, if it believes the supporting information is adequate represents transaction and supporting information to VI/MC Acquirer VI/MC forward representation to Issuer after Including financial impact on Net Position Issuer Issuer may accept representation and re-post transaction to cardholder s account or alternatively go to pre-arbitration (Visa issuers) or submit a second chargeback (MasterCard issuers) Merchant Cardholder

38 A Word on EMV What is EMV? EMV = Eurocard, MasterCard, Visa Name of security standard implemented on chip in credit cards Standard implemented across Europe, Asia and many other countries around the world (e.g. Canada) How does it work? Chip only POS reads Chip and ensures the card is authentic (i.e. not forged) Chip and PIN POS reads Chip and ensures the card is authentic (i.e. not forged) PIN ensures that the user of the card owns the card Deadlines 2013 Acquirers, payment processors and service providers must be certified Oct liability for counterfeit card transactions shifts to party not equipped with EMV (2017 for fuel dispensers)

39 Card Based Payment Attributes Global GPPC Cards are accepted pretty much anywhere around the world Timely Card payments are authorized and guaranteed to merchant. Payment to merchant is usually within 2 days Expensive Because of interchange, GPPC fees can be very expensive in certain countries

40 Retail Payments Global Consulting Group L.L.C. Payments 101 Bank Transfer or ACH Networks

")

41 Automated Clearing House (ACH) Origin Deposit and funds availability delay Printing and mailing costs Lost, stolen and fraudulent checks Mail Delays

")

42 Automated Clearing House (ACH) Origin

43 ACH Processing A Four Corner Model There are two Clearing House Operators in the US: The Federal Reserve Bank and The Clearing House (private) Originators are generally businesses and Receivers can be both Businesses and Consumers A Financial Institution can be both a ODFI and a RDFI at the same time Transactions can be both credits and debits to a Receiver s account ODFI Clearing House RDFI Originator Receiver

44 ACH Processing Written Authorization An Originator must have a written authorization (sometimes called a mandate) to debit a consumer s bank account Written Authorization is a paper document which is NOT sent to the RDFI and is only used in case of disputes ODFI Clearing House RDFI AUTHORIZATION AGREEMENT FOR DIRECT PAYMENTS (ACH DEBITS) Company Company Name ID Number I (we) hereby authorize, hereinafter called COMPANY, to initiate debit entries to my (our) Checking Account / Savings Account (select one) indicated below at the depository financial institution named below, hereafter called DEPOSITORY, and to debit the same to such account. I (we) acknowledge that the origination of ACH transactions to my (our) account must comply with the provisions of U.S. law. Depository Name Branch City State Zip Routing Account Number Number This authorization is to remain in full force and effect until COMPANY has received written notification from me (or either of us) of its termination in such time and in such manner as to afford COMPANY and DEPOSITORY a reasonable opportunity to act on it. Originator Name(s) ID Number (Please Print) Date Signature NOTE: DEBIT AUTHORIZATIONS MUST PROVIDE THAT THE RECEIVER MAY REVOKE THE AUTHORIZATION ONLY BY NOTIFYING THE ORIGINATOR IN THE MANNER SPECIFIED IN THE AUTHORIZATION. Receiver

45 ACH Processing Origination Originator sends daily file(s) to ODFI with all credits and debits transactions ODFI collects all the transactions (both credits and debits) from all Originators and sends them to Clearing House Sometimes the net value of these files can be $0.00 ODFI Clearing House RDFI Originator Receiver

46 ACH Processing Clearing House Processing Clearing House calculates all processing fees and net position there is NO INTERCHANGE Clearing House pays/gets paid on the ENTIRE FILE, even though account existence and funds availability may not have been verified Clearing House Check acquirer files & validate data Sort by ABA- RTN Calculate processing and NACHA fees Calculate Net Position for ODFIs and RDFIs Create and transmit outbound files to issuers

47 ACH Processing Clearing, Settlement, Funds Transfer Clearing House settles net positions by crediting and debiting the DFI s accounts with the Federal reserve Bank NACHA also collects a fee on every transaction to offset rule making costs ODFI Clearing House RDFI

48 ACH Processing Clearing, Settlement, Funds Transfer ODFI pays or gest paid by Originator on the entire value of the file submitted, even though account existence and funds availability may not have been verified, charging the Originator a fee of a few pennies per transaction RDFI credits or debits Receivers directly to bank account. If Receiver is an individual, generally no fee is charged ODFI Clearing House RDFI Originator Receiver

49 ACH Processing Dispute Processing Copy/Retrieval request follows the same paths and it is usually performed before a dispute is submitted as a chargeback Clearing House send Return to RDFI after Including financial impact on Net Position ODFI forwards Return to merchant after including financial impact on net settlement ODFI Clearing House RDFI RDFI sends return Information to ODFI via Clearing House Merchant accepts the return, resubmits transaction ( representation ), or contacts Receiver for alternative account information. There can be as many as 3 representations for a single transaction Originator Receiver Receiver initiates Dispute by submitting a WSSUP

50 ACH Processing Attributes Domestic only International ACH only through gateways Inexpensive A flat transaction fee, usually pennies per transaction Time delay Lack of authorization and validation capabilities and delays in confirmation of payment increase the risk of debit transactions

51 Retail Payments Global Consulting Group L.L.C. Payments 101 EFT Networks

52 US EFT Network Topography Fragmented EFT Network environment

53 EFT Processing Similar to GPPC MERCHANT More expensive BANK More profitable Less expensive * Price differential applies only to unregulated debit cards. All regulated debit cards cost the same to the merchant and generate the same revenue to bank Less profitable

54 EFT Network Attributes PIN Requirements Merchant must invest in PIN Pad devices Domestic Only Most PIN based cards can only be used domestically Less Expensive than GPPC Applies only to Non Durbin Regulated Debit Cards Less Prone to Fraud PIN based transactions have proven to be more secure than signature based transactions

55 Retail Payments Global Consulting Group L.L.C. Payments 101 Online Banking epayments (OBeP)

56 OBeP Attributes How they work Link consumers from the merchant web site to the consumers online banking where buyers are authenticated by the bank and the payment authorized online. API Screen Scraping Settlement of transaction can happen in real time or through the ACH. Value proposition Consumer Safety of financial information Convenience Merchant Lower fees Sales lift Guaranteed payment, no chargebacks

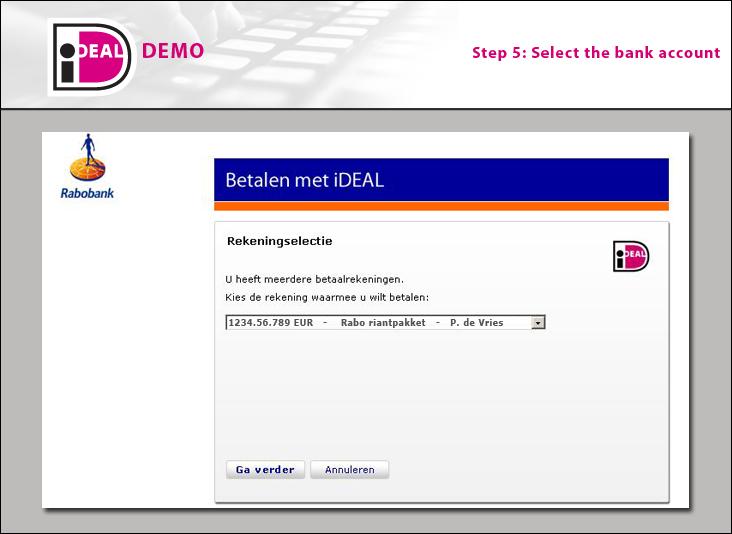

57 The Netherlands - ideal Demo

58 OBeP Attributes Inexpensive Real time authorizations and payments made on real time or next day Safe No chargebacks, no disclosure of financial information to third parties Fragmented No standardized APIs, each bank is a different implementation

59 Retail Payments Global Consulting Group L.L.C. Payments 101 Payment Network Economics

60 Payment Economics Cost per $50 Transaction in $$ Card present, Visa & MC using Signature and World card types, all transactions are domestic and properly authorized. Fees like FANF and similar monthly fees not added

61 Payment Economics Cost per $50 Transaction as % Card present, Visa & MC using Signature and World card types, all transactions are domestic and properly authorized. Fees like FANF and similar monthly fees not added

62 Contact Information th Ave NE Woodinville, WA 98077, U.S.A. Phone: Web: RPGC Group LLC Proprietary and Confidential

Payments 101. An Overview the US Payment Networks. René M Pelegero, President, Retail Payments Global Consulting Group

Payments 101 An Overview the US Payment Networks René M Pelegero, President, Retail Payments Global Consulting Group A Payment is an Exchange of Value Value Financial Non Financial In Financial Institutions

Payments 101 An Overview the US Payment Networks René M Pelegero, President, Retail Payments Global Consulting Group A Payment is an Exchange of Value Value Financial Non Financial In Financial Institutions

Payment Processing 101

Payment Processing 101 Timelines & Deliverables PRESENTED BY Pg: 1 March 7, 2018 www.clearwaterpayments.com Quick Agenda Credit/Debit Transactions Industry Definitions Transaction Process Cost/Pricing

Payment Processing 101 Timelines & Deliverables PRESENTED BY Pg: 1 March 7, 2018 www.clearwaterpayments.com Quick Agenda Credit/Debit Transactions Industry Definitions Transaction Process Cost/Pricing

A report showing the merchant s settlement. The acquirer settlement report is generated by the acquiring bank at the end of every billing cycle.

A Acquirer (acquiring bank) An acquirer is an organisation that is licensed as a member of Visa/MasterCard as an affiliated bank and processes credit card transactions for (online) businesses. Acquirers

A Acquirer (acquiring bank) An acquirer is an organisation that is licensed as a member of Visa/MasterCard as an affiliated bank and processes credit card transactions for (online) businesses. Acquirers

UPCOMING SCHEME CHANGES

UPCOMING SCHEME CHANGES MERCHANTS/PARTNERS/ISO COPY Payvision Ref: Payvision-Upcoming Scheme Changes (v1.0)-october 2015 Page 1 Rights of use: COMPLYING WITH ALL APPLICABLE COPYRIGHT LAWS IS THE RESPONSABILITY

UPCOMING SCHEME CHANGES MERCHANTS/PARTNERS/ISO COPY Payvision Ref: Payvision-Upcoming Scheme Changes (v1.0)-october 2015 Page 1 Rights of use: COMPLYING WITH ALL APPLICABLE COPYRIGHT LAWS IS THE RESPONSABILITY

April 2018 Pass Through Fees. Information provided below is for the convience of the reader and may not include all fee from the Card Brands

Visa FACS North FDS North Omaha Memphis Rate Fee Definition Visa US Acquirer Service Fee (Assessment Fee) Debit Products Visa US Acquirer Service Fee (Assessment Fee) Credit Products FSC 274 FSC 244 FSC

Visa FACS North FDS North Omaha Memphis Rate Fee Definition Visa US Acquirer Service Fee (Assessment Fee) Debit Products Visa US Acquirer Service Fee (Assessment Fee) Credit Products FSC 274 FSC 244 FSC

Overview of Cards ecosystem. April 2016

Overview of Cards ecosystem April 2016 Content Debit card ecosystem Card processes overview Revenue flow in the ecosystem Charges Slide 2 Content Debit card ecosystem Card processes overview Revenue flow

Overview of Cards ecosystem April 2016 Content Debit card ecosystem Card processes overview Revenue flow in the ecosystem Charges Slide 2 Content Debit card ecosystem Card processes overview Revenue flow

Handling Debit Card Chargebacks

Handling Debit Card Chargebacks Rules, Rights and Best Practices Diana Kern, AAP Senior Trainer Disclaimer: The following does not constitute legal advice. The information provided herein may not be applicable

Handling Debit Card Chargebacks Rules, Rights and Best Practices Diana Kern, AAP Senior Trainer Disclaimer: The following does not constitute legal advice. The information provided herein may not be applicable

Authorization Approval of a transaction by the financial institution that issued a paycard or other payment card.

APA Visa Paycard Portal Glossary of Terms Account Number A unique number assigned by a financial institution to a customer s account. The account number for a paycard is embossed or imprinted on the card

APA Visa Paycard Portal Glossary of Terms Account Number A unique number assigned by a financial institution to a customer s account. The account number for a paycard is embossed or imprinted on the card

Chargebacks 101. Do draft retrievals result in upfront debits? No, draft retrievals are non-monetary.

Chargebacks 101 Can a telephone recording of a conversation with the cardholder be accepted as evidence that the cardholder no longer disputes? Unfortunately, the networks are not able to accept telephone

Chargebacks 101 Can a telephone recording of a conversation with the cardholder be accepted as evidence that the cardholder no longer disputes? Unfortunately, the networks are not able to accept telephone

A to Z Jargon buster. Call +44 (0) to discuss your upgrade options

to discuss your upgrade options") A to Z Jargon buster Call +44 (0) 844 209 4370 to discuss your upgrade options www.pxp-solutions.com sales@pxp-solutions.com twitter: @pxpsolutions Are you trying to navigate your way around what can seem

A to Z Jargon buster Call +44 (0) 844 209 4370 to discuss your upgrade options www.pxp-solutions.com sales@pxp-solutions.com twitter: @pxpsolutions Are you trying to navigate your way around what can seem

Retrieval & Chargeback Best Practices. Visa MasterCard Discover American Express. A Merchant User Guide to Help Manage Disputes.

Retrieval & Chargeback Best Practices A Merchant User Guide to Help Manage Disputes Visa MasterCard Discover American Express April 2018 www.firstdata.com This guide is provided as a courtesy and is to

Retrieval & Chargeback Best Practices A Merchant User Guide to Help Manage Disputes Visa MasterCard Discover American Express April 2018 www.firstdata.com This guide is provided as a courtesy and is to

Alternative Payments. methods of payment

Alternative Payments An overview of new (and some not so new) methods of payment June, 2010 What Is A Payment? Change of ownership of value Value can be in multiple forms Monetary Non monetary Monetary

Alternative Payments An overview of new (and some not so new) methods of payment June, 2010 What Is A Payment? Change of ownership of value Value can be in multiple forms Monetary Non monetary Monetary

Best Practices for Handling Retrievals and Chargebacks. Lodging

Best Practices for Handling Retrievals and Chargebacks Lodging January 30, 2018 Table of Contents Authorization Processing... 3 Transaction Processing... 3 Proper Disclosure... 4 Deterring Fraud... 4 VISA

Best Practices for Handling Retrievals and Chargebacks Lodging January 30, 2018 Table of Contents Authorization Processing... 3 Transaction Processing... 3 Proper Disclosure... 4 Deterring Fraud... 4 VISA

Visa Claims Resolution manual

Visa Claims Resolution manual Date: 2/15/18 Simon Carmiggeltstraat 6-50 1011 DJ Amsterdam The Netherlands Page 1 2018 Adyen BV www.adyen.com Introduction... 3 1.1 VCR... 3 1.2 The main changes... 3 1.2.1

Visa Claims Resolution manual Date: 2/15/18 Simon Carmiggeltstraat 6-50 1011 DJ Amsterdam The Netherlands Page 1 2018 Adyen BV www.adyen.com Introduction... 3 1.1 VCR... 3 1.2 The main changes... 3 1.2.1

PREPAID CARD GLOSSARY

PREPAID CARD GLOSSARY ACH Remitter: The bank that receives the electronic funds transfer via Automated Clearing House (ACH) to load funds to a prepaid card. A known remitter is one that is logged in the

PREPAID CARD GLOSSARY ACH Remitter: The bank that receives the electronic funds transfer via Automated Clearing House (ACH) to load funds to a prepaid card. A known remitter is one that is logged in the

Payments POCKET GUIDE. in Your Pocket

Payments POCKET GUIDE in Your Pocket 1 Definitions 3D Secure An XML-based protocol that is designed to add an extra layer of security for online credit and debit card transactions. It has been adopted

Payments POCKET GUIDE in Your Pocket 1 Definitions 3D Secure An XML-based protocol that is designed to add an extra layer of security for online credit and debit card transactions. It has been adopted

Merchant Operating Guide: Payment Processing Solutions

Merchant Operating Guide: Payment Processing Solutions Merchant Operating Guide MOG200506 1 About Your Card Program... 1 Types of Cards... 1 About Transaction Processing... 2 Parties Involved in Your Card

Merchant Operating Guide: Payment Processing Solutions Merchant Operating Guide MOG200506 1 About Your Card Program... 1 Types of Cards... 1 About Transaction Processing... 2 Parties Involved in Your Card

RentWorks Version 4 Credit Card Processing (CCPRO) User Guide

User Guide") RentWorks Version 4 Credit Card Processing (CCPRO) User Guide Table of Contents Overview... 2 Retail Processing Method... 3 Auto Rental Method... 4 How to Run a Draft Capture... 5 Draft Capture Failures.....6

RentWorks Version 4 Credit Card Processing (CCPRO) User Guide Table of Contents Overview... 2 Retail Processing Method... 3 Auto Rental Method... 4 How to Run a Draft Capture... 5 Draft Capture Failures.....6

UPCOMING PAYMENT SCHEMES RULES CHANGES

UPCOMING PAYMENT SCHEMES RULES CHANGES Sara Novakovič, Dispute Operations Department Koper, June 2017 CONTENT 1 Payment schemes groups and chargeback reason codes 2 MasterCard rules changes 3 Visa rules

UPCOMING PAYMENT SCHEMES RULES CHANGES Sara Novakovič, Dispute Operations Department Koper, June 2017 CONTENT 1 Payment schemes groups and chargeback reason codes 2 MasterCard rules changes 3 Visa rules

MERCHANT ACCOUNT INSTRUCTIONS

MERCHANT ACCOUNT INSTRUCTIONS Please open this applica;on using Adobe Reader so all fields read correctly Now that you re ready to get your account setup, please have all your personal, business and banking

MERCHANT ACCOUNT INSTRUCTIONS Please open this applica;on using Adobe Reader so all fields read correctly Now that you re ready to get your account setup, please have all your personal, business and banking

2009 North49 Business Solutions Inc. All rights reserved.

2009 North49 Business Solutions Inc. All rights reserved. Paytelligence, Paytelligence logos, North49 Business Solutions, North49 Business Solutions logos, and all North49 Business Solutions product and

2009 North49 Business Solutions Inc. All rights reserved. Paytelligence, Paytelligence logos, North49 Business Solutions, North49 Business Solutions logos, and all North49 Business Solutions product and

MERCHANT MEMBER PACKAGE AGREEMENT & APPLICATION

MERCHANT MEMBER PACKAGE AGREEMENT & APPLICATION Vantage Card Services, Inc. 2230 Towne Lake Parkway Building 400, Suite 110 Woodstock, GA 30189 (800) 397-2380 (770) 928-5688 Fax (770) 928-9328 www.vantagecard.com

MERCHANT MEMBER PACKAGE AGREEMENT & APPLICATION Vantage Card Services, Inc. 2230 Towne Lake Parkway Building 400, Suite 110 Woodstock, GA 30189 (800) 397-2380 (770) 928-5688 Fax (770) 928-9328 www.vantagecard.com

Table of Contents. Overview. What is payment processing? Who s Who. Types of Payment Solutions. Online Transactions. Interchange Process

Overview Credit Card Processing 101 is your go-to handbook for navigating the payments industry. This document provides a quick and thorough understanding on how businesses accept electronic payments,

Overview Credit Card Processing 101 is your go-to handbook for navigating the payments industry. This document provides a quick and thorough understanding on how businesses accept electronic payments,

CASH MANAGEMENT SCHEDULE WIRE TRANSFER SERVICES ON SANTANDER TREASURY LINK

CASH MANAGEMENT SCHEDULE WIRE TRANSFER SERVICES ON SANTANDER TREASURY LINK This Schedule is entered into by and between Santander Bank, N.A. (the Bank ) and the customer identified in the Cash Management

CASH MANAGEMENT SCHEDULE WIRE TRANSFER SERVICES ON SANTANDER TREASURY LINK This Schedule is entered into by and between Santander Bank, N.A. (the Bank ) and the customer identified in the Cash Management

Payments Fraud Liability Matrix

s Fraud Liability Matrix s Fraud Liability Matrix Prepared by the Federal Reserve Bank of Minneapolis s, Standards, and Outreach Group April 2018 2018 Federal Reserve Bank of Minneapolis, not to be used

s Fraud Liability Matrix s Fraud Liability Matrix Prepared by the Federal Reserve Bank of Minneapolis s, Standards, and Outreach Group April 2018 2018 Federal Reserve Bank of Minneapolis, not to be used

IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from. The Tri-County Bank 106 N Main St Stuart, NE (402)

") IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from The Tri-County Bank 106 N Main St Stuart, NE 68780 (402)924-3861 ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types

IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS from The Tri-County Bank 106 N Main St Stuart, NE 68780 (402)924-3861 ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types

INTERCHANGE RATE SCHEDULE (Effective October, 2016)

") This Interchange Rate Schedule contains a summary of the primary qualification criteria established by Visa, MasterCard, and Discover Network (sometimes referred to as Discover) for most interchange programs

This Interchange Rate Schedule contains a summary of the primary qualification criteria established by Visa, MasterCard, and Discover Network (sometimes referred to as Discover) for most interchange programs

Exactly what kind of bank is South State Bank?

Business Banking Exactly what kind of bank is South State Bank? Yours. The right banking relationship can make a big difference in your success. Whether you need a new business checking account, more effective

Business Banking Exactly what kind of bank is South State Bank? Yours. The right banking relationship can make a big difference in your success. Whether you need a new business checking account, more effective

France - Domestic Interchange Fees

France - Domestic Interchange Fees Consumer Card Interchange Fees Valid From: 1-Mar-19 Payment Product Fee Tier General Bill Payment and Government (4) Mastercard Consumer Credit Low Value Payments (1)

France - Domestic Interchange Fees Consumer Card Interchange Fees Valid From: 1-Mar-19 Payment Product Fee Tier General Bill Payment and Government (4) Mastercard Consumer Credit Low Value Payments (1)

MERCHANT APPLICATION

Business Information Legal Name (as it appears on your income tax return): MERCHANT APPLICATION Merchant # New Location Note: Failure to provide accurate information may result in a withholding of merchant

Business Information Legal Name (as it appears on your income tax return): MERCHANT APPLICATION Merchant # New Location Note: Failure to provide accurate information may result in a withholding of merchant

Banking and Receivables

Banking and Receivables Deduct from Expenditures Definition Commonly referred to as a DFE. This transaction reduces a specific account. The account balance is increased by this transaction. This type of

Banking and Receivables Deduct from Expenditures Definition Commonly referred to as a DFE. This transaction reduces a specific account. The account balance is increased by this transaction. This type of

April 2017 Discover Interchange Qualification Guide

April 2017 Discover Interchange Qualification Guide Discover categorizes interchange qualification into the following levels: Prime Submission Level (PSL) for Consumer Credit, Rewards, Premium and Debit

April 2017 Discover Interchange Qualification Guide Discover categorizes interchange qualification into the following levels: Prime Submission Level (PSL) for Consumer Credit, Rewards, Premium and Debit

France - Domestic Interchange Fees

France Domestic Interchange Fees Consumer Card Interchange Fees Payment Product Fee Tier General MasterCard Consumer Credit Low Value Payments (1) Contactless Terminal (1) Contactless Terminal High Value

France Domestic Interchange Fees Consumer Card Interchange Fees Payment Product Fee Tier General MasterCard Consumer Credit Low Value Payments (1) Contactless Terminal (1) Contactless Terminal High Value

Morgantown Parking Authority 300 Spruce Street Morgantown, WV REQUEST FOR PROPOSAL (RFP) ELECTRONIC CREDIT CARD PROCESSING SERVICES

ELECTRONIC CREDIT CARD PROCESSING SERVICES") M M M O R G A N T O W N P A R K I N G A U T O R ITY A A Morgantown Parking Authority Morgantown Parking Authority 300 Spruce Street Morgantown, WV 26508 REQUEST FOR PROPOSAL (RFP) ELECTRONIC CREDIT CARD

M M M O R G A N T O W N P A R K I N G A U T O R ITY A A Morgantown Parking Authority Morgantown Parking Authority 300 Spruce Street Morgantown, WV 26508 REQUEST FOR PROPOSAL (RFP) ELECTRONIC CREDIT CARD

Bill Pay User Terms and Agreements

Bill Pay User Terms and Agreements First Community Bank hereby publishes the following terms and conditions for User's use of bill payment services via telephone, personal computer or any other device

Bill Pay User Terms and Agreements First Community Bank hereby publishes the following terms and conditions for User's use of bill payment services via telephone, personal computer or any other device

Merchant Operating Guide

August 2012 Table of Contents Chapter 1: About Your Card Program...1 About Transaction Processing... 2 General Operating Guidelines... 2 Additional Services... 4 Chapter 2: Processing Transactions...6

August 2012 Table of Contents Chapter 1: About Your Card Program...1 About Transaction Processing... 2 General Operating Guidelines... 2 Additional Services... 4 Chapter 2: Processing Transactions...6

Payment Card Industry Training 2014

Payment Card Industry Training 2014 Phone Line Terminal & Hosted Order Page/Secure Acceptance Redirect Merchants Contact * Carole Fallon * 614-292-7792 * fallon.82@osu.edu Updated May 2014 AGENDA A. Payment

Payment Card Industry Training 2014 Phone Line Terminal & Hosted Order Page/Secure Acceptance Redirect Merchants Contact * Carole Fallon * 614-292-7792 * fallon.82@osu.edu Updated May 2014 AGENDA A. Payment

Commercial Banking Online Service Agreement

Effective November 1, 2017 Commercial Banking Online Service Agreement Download PDF Welcome to Commercial Banking Online at Washington Federal. This Commercial Banking Online Service Agreement ( Agreement

Effective November 1, 2017 Commercial Banking Online Service Agreement Download PDF Welcome to Commercial Banking Online at Washington Federal. This Commercial Banking Online Service Agreement ( Agreement

Interchange Best Practices. web conferencing services

Interchange Best Practices courtesy of web conferencing services powered by 1 Housekeeping notes If you re not connected by phone or can t hear audio: 1. Dial 866.551.1530 or 212.401.6760 2. Enter PIN

Interchange Best Practices courtesy of web conferencing services powered by 1 Housekeeping notes If you re not connected by phone or can t hear audio: 1. Dial 866.551.1530 or 212.401.6760 2. Enter PIN

Universal APPLICATION FOR MERCHANT CARD PROCESSING ISO/ISA

Universal APPLICATION FOR MERCHANT CARD PROCESSING ISO/ISA An application must be completed for each merchant that is applying for bankcard processing. If an applicant has more than one business, using

Universal APPLICATION FOR MERCHANT CARD PROCESSING ISO/ISA An application must be completed for each merchant that is applying for bankcard processing. If an applicant has more than one business, using

AN 1213 Revised Standards Signature Requirements

AN 1213 Revised Standards Signature Requirements Generated on 18 October 2017 Published On 18 October 2017 This PDF was created from content on the Mastercard Technical Resource Center, which is updated

AN 1213 Revised Standards Signature Requirements Generated on 18 October 2017 Published On 18 October 2017 This PDF was created from content on the Mastercard Technical Resource Center, which is updated

Fees There are currently no separate monthly or transaction fees assessed by the Bank for use of the Online Banking Service including the External

Online Banking Account Agreement General This Online Banking Agreement (Agreement) for accessing your TrustTexas Bank, SSB account(s) via the Internet explains the terms and conditions of Online Banking.

Online Banking Account Agreement General This Online Banking Agreement (Agreement) for accessing your TrustTexas Bank, SSB account(s) via the Internet explains the terms and conditions of Online Banking.

Tim Hopkins, Senior Business Leader Dispute Resolution Management. The Ever Changing Fraud Chargeback

Tim Hopkins, Senior Business Leader Dispute Resolution Management The Ever Changing Fraud Chargeback #GlobalRisk @ MasterCardNews The Fraud Chargeback in the 70s Country Club Billing was the norm in the

Tim Hopkins, Senior Business Leader Dispute Resolution Management The Ever Changing Fraud Chargeback #GlobalRisk @ MasterCardNews The Fraud Chargeback in the 70s Country Club Billing was the norm in the

Copyright 2017 Lakeland Bank. All rights reserved. This material is proprietary to and published by Lakeland Bank for the sole benefit of its

ACH Originator Guide Copyright 2017 Lakeland Bank. All rights reserved. This material is proprietary to and published by Lakeland Bank for the sole benefit of its clients. Reproduction, distribution, disclosure

ACH Originator Guide Copyright 2017 Lakeland Bank. All rights reserved. This material is proprietary to and published by Lakeland Bank for the sole benefit of its clients. Reproduction, distribution, disclosure

Amstar Brands Payment Methods Manual. First Data Locations

Amstar Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

Amstar Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

Payment Card Acceptance Administrative Policy

Administrative Procedure Approved By: Brandon Gilliland, AVP for Finance and Controller Effective Date: January 15, 2016 History: Approval Date: September 25, 2014 Revisions: December 15, 2015 Type: Administrative

Administrative Procedure Approved By: Brandon Gilliland, AVP for Finance and Controller Effective Date: January 15, 2016 History: Approval Date: September 25, 2014 Revisions: December 15, 2015 Type: Administrative

Advanced Card Payments Overview Dan Kramer

Advanced Card Payments Overview Dan Kramer Senior Vice President, SHAZAM Agenda PIN-Based Transactions Signature-Based Transactions EFT Regulations Tokenization PIN-Based Transactions Intra-Network PIN-Based

Advanced Card Payments Overview Dan Kramer Senior Vice President, SHAZAM Agenda PIN-Based Transactions Signature-Based Transactions EFT Regulations Tokenization PIN-Based Transactions Intra-Network PIN-Based

Chargeback Reason Code List - U.S.

AL Airline Transaction Dispute AP Automatic Payment AW Altered Amount CA Cash Advance Dispute CD Credit Posted as Card Sale CR Cancelled Reservation This chargeback occurs because of a dispute on an Airline

AL Airline Transaction Dispute AP Automatic Payment AW Altered Amount CA Cash Advance Dispute CD Credit Posted as Card Sale CR Cancelled Reservation This chargeback occurs because of a dispute on an Airline

Departmental Funds Receipting

Departmental Funds Receipting 05.141 Authority: History: Source of Authority: Vice Chancellor Business Affairs Effective November 1, 1990, entitled Cash Receipts ; updated May 26, 1999, updated November

Departmental Funds Receipting 05.141 Authority: History: Source of Authority: Vice Chancellor Business Affairs Effective November 1, 1990, entitled Cash Receipts ; updated May 26, 1999, updated November

Convenience Services Application

Convenience Services Application I am applying for the following service(s). (Note: A separate application is needed for each accountholder applying for services.) Cash & Check Debit Card (w/ ATM access)

Convenience Services Application I am applying for the following service(s). (Note: A separate application is needed for each accountholder applying for services.) Cash & Check Debit Card (w/ ATM access)

ACH FUNDAMENTALS: UNDER THE MICROSCOPE. Heather Spencer, AAP Implementation Coordinator, MY CU Services, LLC. Disclaimer

ACH FUNDAMENTALS: UNDER THE MICROSCOPE Heather Spencer, AAP Implementation Coordinator, MY CU Services, LLC www.mycuservices.com Disclaimer This material is not intended to provide any warranties or legal

ACH FUNDAMENTALS: UNDER THE MICROSCOPE Heather Spencer, AAP Implementation Coordinator, MY CU Services, LLC www.mycuservices.com Disclaimer This material is not intended to provide any warranties or legal

ORIGINATING ACH ENTRIES REFERENCE

ORIGINATING ACH ENTRIES REFERENCE The following information has been provided so that customers can be familiar with their requirements under the NACHA Operating Rules (The Rules). This quick reference

ORIGINATING ACH ENTRIES REFERENCE The following information has been provided so that customers can be familiar with their requirements under the NACHA Operating Rules (The Rules). This quick reference

Contact information for account assistance is listed on the last page of this brochure. Please read the following terms and conditions carefully.

Rules and Regulations Governing Electronic Services ELECTRONIC FUND TRANSFER DISCLOSURES AND AGREEMENT Effective March 23, 2018 The following disclosures and agreement ( Disclosures and Agreement ) describe

Rules and Regulations Governing Electronic Services ELECTRONIC FUND TRANSFER DISCLOSURES AND AGREEMENT Effective March 23, 2018 The following disclosures and agreement ( Disclosures and Agreement ) describe

Spring Mandate Updated

Spring Mandate 2011 - Updated ** As a result of the Mandate Q&A Sessions held last week, this documentation has been updated to clarify any questions and to provide additional information. Changes have

Spring Mandate 2011 - Updated ** As a result of the Mandate Q&A Sessions held last week, this documentation has been updated to clarify any questions and to provide additional information. Changes have

Managing Your Total Cost of Credit Card Acceptance

Managing Your Total Cost of Credit Card Acceptance February 25, 2009 2:00-3:30 Eastern Time Introductions Eric Mock Director Partnership Development Steve Brookbank GM Program Relations Group Presenters

Managing Your Total Cost of Credit Card Acceptance February 25, 2009 2:00-3:30 Eastern Time Introductions Eric Mock Director Partnership Development Steve Brookbank GM Program Relations Group Presenters

Please complete the attached Direct Deposit Authorization Form indicating your choice and return it to your manager.

Employee Packet PAPERLESS PAYROLL We are pleased to announce that we are moving to paperless payroll for all employees. In addition to being environmentally friendly, electronic payroll gives you faster

Employee Packet PAPERLESS PAYROLL We are pleased to announce that we are moving to paperless payroll for all employees. In addition to being environmentally friendly, electronic payroll gives you faster

ACH Industry Update, Audit Weaknesses and Emerging Payment Trends

ACH Industry Update, Audit Weaknesses and Emerging Payment Trends Presented by Adrian Brown, AAP Director of Education The Payments Authority is the association for payments people. ACH CARD CHECK WIRE

ACH Industry Update, Audit Weaknesses and Emerging Payment Trends Presented by Adrian Brown, AAP Director of Education The Payments Authority is the association for payments people. ACH CARD CHECK WIRE

City of Poulsbo Finance Department

CITY CREDIT CARD PROGRAM US BANK VISA CARD Introduction The City of Poulsbo recognizes that the use of credit cards is a customary and economical business practice to improve cash management, reduce costs,

CITY CREDIT CARD PROGRAM US BANK VISA CARD Introduction The City of Poulsbo recognizes that the use of credit cards is a customary and economical business practice to improve cash management, reduce costs,

MERCHANT ACCOUNT INSTRUCTIONS

MERCHANT ACCOUNT INSTRUCTIONS Please open this applica;on using Adobe Reader so all fields read correctly Now that you re ready to get your account setup, please have all your personal, business and banking

MERCHANT ACCOUNT INSTRUCTIONS Please open this applica;on using Adobe Reader so all fields read correctly Now that you re ready to get your account setup, please have all your personal, business and banking

MERCHANT APPLICATION Merchant # New Location

Business Information Legal Name (as it appears on your income tax return): MERCHANT APPLICATION Merchant # New Location Note: Failure to provide accurate information may result in a withholding of merchant

Business Information Legal Name (as it appears on your income tax return): MERCHANT APPLICATION Merchant # New Location Note: Failure to provide accurate information may result in a withholding of merchant

SUB-MERCHANT AGREEMENT

SUB-MERCHANT AGREEMENT This Sub-Merchant Agreement ( Agreement ) is a legal agreement between Vantage Card Services, Inc. ( Vantage ), and the business entity ( Merchant ) set forth on the Merchant Application

SUB-MERCHANT AGREEMENT This Sub-Merchant Agreement ( Agreement ) is a legal agreement between Vantage Card Services, Inc. ( Vantage ), and the business entity ( Merchant ) set forth on the Merchant Application

Operating Guide November 2016

November 2016 Table of Contents Chapter 1: About Your Card Program... 1 About Transaction Processing... 2 General Operating Guidelines... 2 Additional Services... 4 Chapter 2: Processing Transactions...

November 2016 Table of Contents Chapter 1: About Your Card Program... 1 About Transaction Processing... 2 General Operating Guidelines... 2 Additional Services... 4 Chapter 2: Processing Transactions...

Risk Management on Prepaid Cards

Responsibilities CenterState Bank of Florida, NA (CSBF) is the issuing financial institution of all prepaid cards and owner of the associated network BINs. CSBF is responsible for all program monitoring

Responsibilities CenterState Bank of Florida, NA (CSBF) is the issuing financial institution of all prepaid cards and owner of the associated network BINs. CSBF is responsible for all program monitoring

Event Merchant Card Services

Event 317 - Merchant Card Services Statement of Work A. Overview: It is the intent of the Bexar County Tax Assessor-Collector to solicit proposals to establish a contract with a vendor to provide merchant

Event 317 - Merchant Card Services Statement of Work A. Overview: It is the intent of the Bexar County Tax Assessor-Collector to solicit proposals to establish a contract with a vendor to provide merchant

Cardholder Authentication Guide

Business Gateway Cardholder Authentication Guide V5.3 May 2016 Use this help to find out: How cardholder authentication works How liability shift affects you Cardholder Authentication Guide > Contents

Business Gateway Cardholder Authentication Guide V5.3 May 2016 Use this help to find out: How cardholder authentication works How liability shift affects you Cardholder Authentication Guide > Contents

Bank of Mauritius. National Payment Switch

Bank of Mauritius National Payment Switch January 2016 1 Introduction The Bank of Mauritius (Bank) is empowered under the Bank of Mauritius Act to safeguard the safety, soundness and efficiency of payment,

Bank of Mauritius National Payment Switch January 2016 1 Introduction The Bank of Mauritius (Bank) is empowered under the Bank of Mauritius Act to safeguard the safety, soundness and efficiency of payment,

Funds Transfer Services

Funds Transfer Services Understanding the Terms and Conditions of your Account as well as the Federal laws and regulations that outline your rights and responsibilities as a Consumer and Non-Consumer (Commercial

Funds Transfer Services Understanding the Terms and Conditions of your Account as well as the Federal laws and regulations that outline your rights and responsibilities as a Consumer and Non-Consumer (Commercial

Propertyware epayments. Powered by RealPage

Propertyware epayments Powered by RealPage Page i Copyrights 2002-2011 Propertyware, Inc. All rights reserved. No part of this publication may be reproduced, transmitted or stored in any archives without

Propertyware epayments Powered by RealPage Page i Copyrights 2002-2011 Propertyware, Inc. All rights reserved. No part of this publication may be reproduced, transmitted or stored in any archives without

CARD ISSUER DUTIES & RESPONSIBILITIES. Copyright 2013 CO-OP Financial Services

SECTION 3 Operating Rules and Regulations without the prior written permission of CO-OP Financial Services. All Rights Reserved Card Issuers shall have the following responsibilities in addition to those

SECTION 3 Operating Rules and Regulations without the prior written permission of CO-OP Financial Services. All Rights Reserved Card Issuers shall have the following responsibilities in addition to those

Consumer Electronic Fund Transfer Agreement and Disclosure

Consumer Electronic Fund Transfer Agreement and Disclosure For use with our Account Agreement and Disclosures TABLE OF CONTENTS CONSUMER ELECTRONIC FUND TRANSFER SERVICES AGREEMENT AND DISCLOSURE 1 CONSUMER

Consumer Electronic Fund Transfer Agreement and Disclosure For use with our Account Agreement and Disclosures TABLE OF CONTENTS CONSUMER ELECTRONIC FUND TRANSFER SERVICES AGREEMENT AND DISCLOSURE 1 CONSUMER

GUIDE TO BENEFITS MERIDIAN VISA * CASH BACK CARD M40001 (11/16)

") GUIDE TO BENEFITS MERIDIAN VISA * CASH BACK CARD M40001 (11/16) WELCOME Your new Meridian Visa Cash Back Card is your key to earning cash back and more for simply making everyday purchases. You ll be

GUIDE TO BENEFITS MERIDIAN VISA * CASH BACK CARD M40001 (11/16) WELCOME Your new Meridian Visa Cash Back Card is your key to earning cash back and more for simply making everyday purchases. You ll be

Focused on card fraud prevention

Focused on card fraud prevention The evolution of credit card fraud As EMV adoption increases, counterfeit cards are harder to create and use 76% decrease in counterfeit fraud at U.S. chip-enabled merchants*

Focused on card fraud prevention The evolution of credit card fraud As EMV adoption increases, counterfeit cards are harder to create and use 76% decrease in counterfeit fraud at U.S. chip-enabled merchants*

INVOICE POLICY AND FEE SCHEDULES. Copyright 2016 CO-OP Financial Services

SECTION 8 INVOICE POLICY AND FEE SCHEDULES Operating Rules and Regulations without the prior written permission of CO-OP Financial Services. All Rights Reserved Network transaction fees that are included

SECTION 8 INVOICE POLICY AND FEE SCHEDULES Operating Rules and Regulations without the prior written permission of CO-OP Financial Services. All Rights Reserved Network transaction fees that are included

get cash withdrawals from savings account(s) with an ATM card get cash withdrawals from savings account(s) with a debit card

with an ATM card get cash withdrawals from savings account(s) with a debit card") ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types of Electronic Fund Transfers we are capable of handling, some of which may not apply to your account. Please read this

ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types of Electronic Fund Transfers we are capable of handling, some of which may not apply to your account. Please read this

Payments terminology and acronyms

Payments terminology COMMON ACRONYMS AML anti-money laundering anti-money laundering (aml) is a term mainly used in the legal and financial industries to describe a set of procedures, regulations, or legal

Payments terminology COMMON ACRONYMS AML anti-money laundering anti-money laundering (aml) is a term mainly used in the legal and financial industries to describe a set of procedures, regulations, or legal

Chargeback Management Guidelines for Visa Merchants

Chargeback Management Guidelines for Visa Merchants Table of Contents Introduction.............................................................. 1 Section 1: Getting Down to Basics..........................................

Chargeback Management Guidelines for Visa Merchants Table of Contents Introduction.............................................................. 1 Section 1: Getting Down to Basics..........................................

Beneficial State Bank ONLINE BANKING ACCESS AGREEMENT AND ELECTRONIC FUNDS TRANSFER ACT DISCLOSURE

Beneficial State Bank Services and Prices Effective 2-1-2018 ONLINE BANKING ACCESS AGREEMENT AND ELECTRONIC FUNDS TRANSFER ACT DISCLOSURE Agreement This Agreement is a contract which establishes the rules

Beneficial State Bank Services and Prices Effective 2-1-2018 ONLINE BANKING ACCESS AGREEMENT AND ELECTRONIC FUNDS TRANSFER ACT DISCLOSURE Agreement This Agreement is a contract which establishes the rules

Visa Payment Acceptance Best Practices for Retail Petroleum Merchants. February 2010

Visa Payment Acceptance Best Practices for Retail Petroleum Merchants February 2010 Table of Contents About This Guide......................................................... 1 Background.............................................................1

Visa Payment Acceptance Best Practices for Retail Petroleum Merchants February 2010 Table of Contents About This Guide......................................................... 1 Background.............................................................1

QUALIFICATION AND INTERCHANGE CHART

INTERCHANGE CATEGORY VISA CONSUMER S: CPS/Retail CPS/ Retail EIRF (Electronic Interchange Reimbursement Fee) EIRF Standard Paper Standard Paper Changes effective April 2007 in bold. This information is

INTERCHANGE CATEGORY VISA CONSUMER S: CPS/Retail CPS/ Retail EIRF (Electronic Interchange Reimbursement Fee) EIRF Standard Paper Standard Paper Changes effective April 2007 in bold. This information is

BUSINESS MASTERCARD CARDHOLDER DISCLOSURE AND AGREEMENT STANDARD AND CASH REWARDS MASTERCARDS

BUSINESS MASTERCARD CARDHOLDER DISCLOSURE AND AGREEMENT STANDARD AND CASH REWARDS MASTERCARDS This Business MasterCard Disclosure and Agreement sets forth the terms of your Account and includes this document,

BUSINESS MASTERCARD CARDHOLDER DISCLOSURE AND AGREEMENT STANDARD AND CASH REWARDS MASTERCARDS This Business MasterCard Disclosure and Agreement sets forth the terms of your Account and includes this document,

DISCLOSURE FOR ELECTRONIC FUND TRANSACTIONS (EFT) AND WIRE TRANSFER NOTIFICATION

AND WIRE TRANSFER NOTIFICATION") www.efirstflight.com DISCLOSURE FOR ELECTRONIC FUND TRANSACTIONS (EFT) AND WIRE TRANSFER NOTIFICATION First Flight Federal Credit Union offers various electronic fund transfer services to our members.

www.efirstflight.com DISCLOSURE FOR ELECTRONIC FUND TRANSACTIONS (EFT) AND WIRE TRANSFER NOTIFICATION First Flight Federal Credit Union offers various electronic fund transfer services to our members.

Vancity Credit Card Agreement (for Business Use)

") Vancity Credit Card Agreement (for Business Use) Table of Contents 1. INTRODUCTION 1 2. DEFINITIONS 1 3. ACCOUNT OPENING AND CARD ISSUANCE 2 4. TAKING CARE OF THE VISA* CARD AND VISA ACCOUNT 3 5. HOW AUTHORIZED

Vancity Credit Card Agreement (for Business Use) Table of Contents 1. INTRODUCTION 1 2. DEFINITIONS 1 3. ACCOUNT OPENING AND CARD ISSUANCE 2 4. TAKING CARE OF THE VISA* CARD AND VISA ACCOUNT 3 5. HOW AUTHORIZED

Paying the Employee Section 5

Paying the Employee Section 5 Table of Contents INTRODUCTION... 2 TOPICS FROM CONTENT OUTLINE... 2 KNOWLEDGE, SKILLS AND ABILITIES... 2 PAY FREQUENCY... 3 PAYMENT ON TERMINATIOṆ... 3 PAYMENT METHODS...

Paying the Employee Section 5 Table of Contents INTRODUCTION... 2 TOPICS FROM CONTENT OUTLINE... 2 KNOWLEDGE, SKILLS AND ABILITIES... 2 PAY FREQUENCY... 3 PAYMENT ON TERMINATIOṆ... 3 PAYMENT METHODS...

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

Arvest Bank ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE The federal Electronic Fund Transfer Act and Regulation E require financial institutions to provide certain information to consumers (i.e.,

Arvest Bank ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE The federal Electronic Fund Transfer Act and Regulation E require financial institutions to provide certain information to consumers (i.e.,

ADVANTAGES OF A RISK BASED AUTHENTICATION STRATEGY FOR MASTERCARD SECURECODE

ADVANTAGES OF A RISK BASED AUTHENTICATION STRATEGY FOR MASTERCARD SECURECODE Purpose This document explains the benefits of using Risk Based Authentication (RBA) a dynamic method of cardholder authentication

ADVANTAGES OF A RISK BASED AUTHENTICATION STRATEGY FOR MASTERCARD SECURECODE Purpose This document explains the benefits of using Risk Based Authentication (RBA) a dynamic method of cardholder authentication

Australia Post Load&Go China Card Short-Form Product Disclosure Statement

Australia Post Load&Go China Card Short-Form Product Disclosure Statement This Short-Form Product Disclosure Statement (Short-Form PDS) is dated 30 June 2017. This Short-Form PDS provides summary information

Australia Post Load&Go China Card Short-Form Product Disclosure Statement This Short-Form Product Disclosure Statement (Short-Form PDS) is dated 30 June 2017. This Short-Form PDS provides summary information

Card FAQ. The City Bank Ltd

Card FAQ The City Bank Ltd Version: 2 Updated as of 28 th Dec, 2017 Contents General Questions... 2 Card Sales... 2 Card Payment... 2 Credit Limit... 3 Interest Rate & Payment... 3 Other General Questions...

Card FAQ The City Bank Ltd Version: 2 Updated as of 28 th Dec, 2017 Contents General Questions... 2 Card Sales... 2 Card Payment... 2 Credit Limit... 3 Interest Rate & Payment... 3 Other General Questions...

Selected Terms & Conditions for Wells Fargo Business Debit, ATM and Deposit Cards

Selected Terms & Conditions for Wells Fargo Debit, ATM and Deposit Cards Terms and Conditions effective 04/24/2017. Introduction page 1 Using Your Card page 2 Using Your Card Through a Mobile Device page

Selected Terms & Conditions for Wells Fargo Debit, ATM and Deposit Cards Terms and Conditions effective 04/24/2017. Introduction page 1 Using Your Card page 2 Using Your Card Through a Mobile Device page

HSBC Visa Credit Card User Guide

HSBC Visa Credit Card User Guide Welcome to the world full of privileges for HSBC Visa Credit Cardholders. You are about to discover the exclusive privileges brought to you by HSBC Credit Cards. You ll

HSBC Visa Credit Card User Guide Welcome to the world full of privileges for HSBC Visa Credit Cardholders. You are about to discover the exclusive privileges brought to you by HSBC Credit Cards. You ll

State Bank Financial State Bank Shelby 4020 Mormon Coulee Road La Crosse WI ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE

State Bank Financial State Bank Shelby 4020 Mormon Coulee Road 608.788.0400 ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our"

State Bank Financial State Bank Shelby 4020 Mormon Coulee Road 608.788.0400 ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSURE For purposes of this disclosure and agreement the terms "we", "us" and "our"

First Savings Bank of Hegewisch

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT First Savings Bank of Hegewisch For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to First Savings Bank of Hegewisch.

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT First Savings Bank of Hegewisch For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to First Savings Bank of Hegewisch.

Understanding Merchant Pricing

Understanding Merchant Pricing Contents Pricing Structures... 3 Tiered Pricing... 3 Flat Rate Pricing:... 5 Cost Plus Pricing:... 6 Additional Resources... 7 Visa Interchange Fees Table... 8 MasterCard

Understanding Merchant Pricing Contents Pricing Structures... 3 Tiered Pricing... 3 Flat Rate Pricing:... 5 Cost Plus Pricing:... 6 Additional Resources... 7 Visa Interchange Fees Table... 8 MasterCard

YOUR RIGHTS AND RESPONSIBILITIES

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT YOUR RIGHTS AND RESPONSIBILITIES www.morris.bank For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to Morris Bank. The

ELECTRONIC FUND TRANSFER DISCLOSURE AND AGREEMENT YOUR RIGHTS AND RESPONSIBILITIES www.morris.bank For purposes of this disclosure and agreement the terms "we", "us" and "our" refer to Morris Bank. The

PREPAID CARDHOLDER AGREEMENT

Toll Free Phone: 1-866-231-0373 Toll Free Fax: 1-403-451-3069 Web Site: www.dcbank.ca PREPAID CARDHOLDER AGREEMENT between DirectCash Bank ("DCBank"), and the "Cardholder" PREPAID CARDHOLDER AGREEMENT

Toll Free Phone: 1-866-231-0373 Toll Free Fax: 1-403-451-3069 Web Site: www.dcbank.ca PREPAID CARDHOLDER AGREEMENT between DirectCash Bank ("DCBank"), and the "Cardholder" PREPAID CARDHOLDER AGREEMENT

General Information for Cardholder s on PIN & PAY

General Information for Cardholder s on PIN & PAY As part of our on-going initiative to enhance security, we are pleased to introduce the 6-digit PIN (Personal Identification Number) for validation, replacing

General Information for Cardholder s on PIN & PAY As part of our on-going initiative to enhance security, we are pleased to introduce the 6-digit PIN (Personal Identification Number) for validation, replacing

UNL PAYMENT CARD POLICIES AND PROCEDURES. Table of Contents

UNL PAYMENT CARD POLICIES AND PROCEDURES Table of Contents Payment Card Merchant Security Standards Policy and Procedures... 2 Introduction... 4 Payment Card Industry Data Security Standard... 4 Definitions...

UNL PAYMENT CARD POLICIES AND PROCEDURES Table of Contents Payment Card Merchant Security Standards Policy and Procedures... 2 Introduction... 4 Payment Card Industry Data Security Standard... 4 Definitions...

Frequently Asked Questions Guide

Global Card Access Frequently Asked Questions Guide Table of Contents Section I: General Overview... 2 Section II: Registration... 2 Section III: Alerts... 3 Section IV: Online PIN Check... 5 Section V:

Global Card Access Frequently Asked Questions Guide Table of Contents Section I: General Overview... 2 Section II: Registration... 2 Section III: Alerts... 3 Section IV: Online PIN Check... 5 Section V:

ELECTRONIC FUNDS DISCLOSURE

ELECTRONIC FUNDS DISCLOSURE Peoples Bank & Trust Pana Facility 200 S. Locust Street PO Box 350 Pana, IL 62557 March 1, 2018 This disclosure contains information about terms, fees, and interest rates for

ELECTRONIC FUNDS DISCLOSURE Peoples Bank & Trust Pana Facility 200 S. Locust Street PO Box 350 Pana, IL 62557 March 1, 2018 This disclosure contains information about terms, fees, and interest rates for

Glossary of ACH Terms

ABA NUMBER See Routing Number/Transit ACH - The Automated Clearing House network ACCESS DEVICE - A card, code, or other means of access to a consumer s account that may be used to initiate electronic funds

ABA NUMBER See Routing Number/Transit ACH - The Automated Clearing House network ACCESS DEVICE - A card, code, or other means of access to a consumer s account that may be used to initiate electronic funds

protect fraudulent against transactions your business Introduction What is a fraudulent transaction? Merchant Responsibilities Card Present

protect your business against fraudulent transactions Reg. No. 1929/001225/06. Introduction There is a real possibility that your business could be a victim of fraudulent card transactions given the sophistication

protect your business against fraudulent transactions Reg. No. 1929/001225/06. Introduction There is a real possibility that your business could be a victim of fraudulent card transactions given the sophistication