TOWARDS MORE INCLUSIVE MEASUREMENT AND MONITORING OF BROADER DEVELOPMENT FINANCE

|

|

|

- Miranda McCoy

- 5 years ago

- Views:

Transcription

1 TOWARDS MORE INCLUSIVE MEASUREMENT AND MONITORING OF BROADER DEVELOPMENT FINANCE SIXTH SESSION OF OIC-STATCOM, 5-6 November 2016, Konya, Turkey WILLEM LUIJKX

2 Presentation 1. The OECD and the DAC 2. Our work on development finance statistics 3. Measuring broader development finance: Total Official Support for Sustainable Development (TOSSD)

3

4 1. THE ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT (OECD) AND THE DEVELOPMENT ASSISTANCE COMMITTEE (DAC)

The")

5 The OECD and the Development Assistance Committee (DAC) The OECD: 35 members The DAC: 29 members Subsidiary bodies

6 The mandate of the DAC... promote development co-operation and other policies so as to contribute to sustainable development, including pro-poor economic growth, poverty reduction, improvement of living standards in developing countries, and a future in which no country will depend on aid.

. DAC Network on Governance (GOVNET). DAC International Network on Conflict and Fragility (INCAF).")

7 DAC Subsidiary Bodies DAC Working Party on Development Finance Statistics (WP-STAT). DAC Network on Development Evaluation (EVALNET). DAC Network on Gender Equality (GENDERNET). DAC Network on Environment and Development Co-operation (ENVIRONET). DAC Network on Governance (GOVNET). DAC International Network on Conflict and Fragility (INCAF). Advisory Group on Investment and Development (AGID). 7

8 DAC engagement : the DAC s relations with countries that are not members. 1. DAC Participants: the UAE and Qatar 2. Members of the OECD (e.g. Turkey) 3. OECD accession countries 4. Key partners: Brazil, China, India, Indonesia and South Africa 5. Other countries

9 Engagement with regional and international organisations. Multilateral financial institutions: the Arab Fund, BADEA, the Islamic Development Bank and the OPEC Fund. The Arab Co-ordination Group Institutions. The Organisation of Islamic Cooperation?

10 2. OUR WORK ON DEVELOPMENT FINANCE STATISTICS

11

12 SDG target Developed countries to implement fully their official development assistance commitments, including the commitment by many developed countries to achieve the target of 0.7 per cent of ODA/GNI to developing countries and 0.15 to 0.20 per cent of ODA/GNI to least developed countries;

13 Our work on development finance statistics. The concept of Official Development Assistance. Our work on development finance statistics.

14 The ODA definition Official development assistance flows are defined as those flows to countries and territories on the DAC List of ODA Recipients and to multilateral development institutions which are: i. provided by official agencies, including state and local governments, or by their executive agencies; and ii. each transaction of which: a) is administered with the promotion of the economic development and welfare of developing countries as its main objective; and b) is concessional in character.

15 The concept of Official Development Assistance (ODA). ODA, since 1969 A 1970 United Nations resolution urges developed countries to dedicate 0.7% of their GDP to ODA. In reality, the average ODA/GDP ratio of DAC members was 0.3% in Only 6 countries reached the 0.7% target in 2015.

16 constant 2013 USD billion 1960 ODA has increased steadily for the past 15 years (a) 1992 (a) (b) ODA as percent of GNI ODA/GNI (right scale) Total net ODA (left scale) (a) Total DAC excludes debt forgiveness of non-oda claims in 1990, 1991 and (b) 2014 preliminary estimate

17 Our work on development finance statistics. Policy recommendations Standard setting Development Finance Knowledge dissemination Data collection Analysis

18 Data collection and dissemination +/- 20 Non-DAC countries, including: Turkey, UAE, Qatar, Saudi Arabia and Kazakhstan 29 DAC members Quality control activities annually +/- 40 Multilateral organisations 1 private foundation Online databases: Aidflows.org and other external users. Web site analysis /financing-sustainabledevelopment/

19 Example of analytical work - 1

20 Example of analytical work - 2

21 Statistical engagement and capacity building 20 emerging providers report to OECD on development co-operation (including south-south co-operation). Support to set up data collection system, incountry co-ordination, a methodology/guidelines etc. Statistical workshops (Kazakhstan 2015, Qatar 2014). Also dialogue on statistics and reporting (Turkey 2016, UAE 2015). Participation in WP-STAT. Offer support, possibly together with SESRIC?

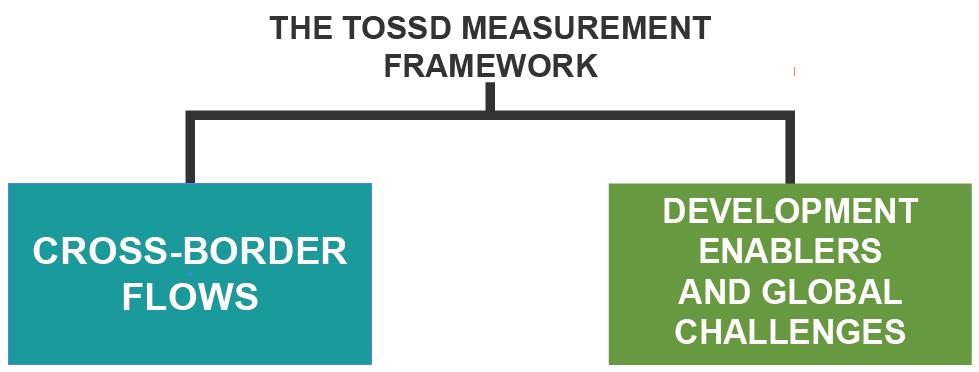

22 3. INCLUSIVE MEASUREMENT OF BROADER DEVELOPMENT FINANCE: TOTAL OFFICIAL SUPPORT FOR SUSTAINABLE DEVELOPMENT (TOSSD)

23

24 Points to discuss 1. Why do we need a more inclusive measure of broader development finance? 2. What is TOSSD? 3. What is the way forward for establishing this measure? 4. How can the measure be implemented?

25 1. Why do we need a more inclusive measure of broader development finance? Greater diversity amongst developing countries. Increased importance of: Non-traditional instruments to provide development co-operation. Emerging providers of development cooperation. Global public goods: the environment.

26 Different countries, different instruments

27 Emerging economies are increasing their development co-operation Estimated development cooperation by 29 countries beyond the DAC (of which 19 report data to the DAC) % of total global ODA Net ODA by 28 DAC member countries (constant prices)

28 as well as their international cooperation beyond ODA. International co-operation beyond ODA, by 30 emerging providers could reach: USD 300 billion Source: upcoming OECD working paper on emerging providers international co-operation.

29 Addis Ababa Action Agenda Domestic public resources Domestic and international private business and finance International development cooperation International trade as an engine for development Debt and Debt Sustainability Addressing systemic issues Science, technology, innovation and capacity building

30 2. What is TOSSD? More than just a bad acronym

31 Some principles Access to comprehensive statistics on development finance is essential for the Agenda 2030 financing framework. To be fit for purpose it should: promote transparency and facilitate monitoring of international public finance. carry the right incentives to maximise resources mobilisation, their smart allocation and catalytic use. be based on international standards for measuring and monitoring international public finance.

32 STATISTICAL COMPONENTS

33 I. THE CROSS-BORDER FLOW COMPONENT ALL SDGs SECTORS COVERED (WITHIN ELIGIBILITY) ALL PROVIDERS & MOST INSTRUMENTS Type of support covered: Concessional grants and loans Non-concessional loans Private sector instruments (equity, mezz ) PPPs, Private finance mobilised Humanitarian aid? Export credits? Unclear whether support covered?? Debt relief?? In-donor costs?

34 What s the difference between ODA and TOSSD? ODA Members of the OECD DAC and other providers who report on their development co-operation Eligibility criteria based on promotion of economic development and welfare and the level of concessionality Accountability of DAC members to longstanding commitments TOSSD All providers of public international finance Eligibility criteria based on supporting the Agenda 2030 (addressing GPGs or finance aligned with country priorities). No targets or associated commitments so as not to dilute ODA promises

35 Pilot study Denmark Gross ODA 2,819 In-donor refugee costs, outer year Net ODA 2,693 TOSSD 3,075 memo item 625 UN mandated peacekeeping operations Security and Justice In-donor refugee costs, first year Equity investm ents Capital of developm ental loans Private sector resources mobilised* (stock figures) ODA components Possible additionnal TOSSD components Human rights GPG - Standardsetting international organisation s GPG - Standardsetting international organisation s Associated financing * TOSSD memo item

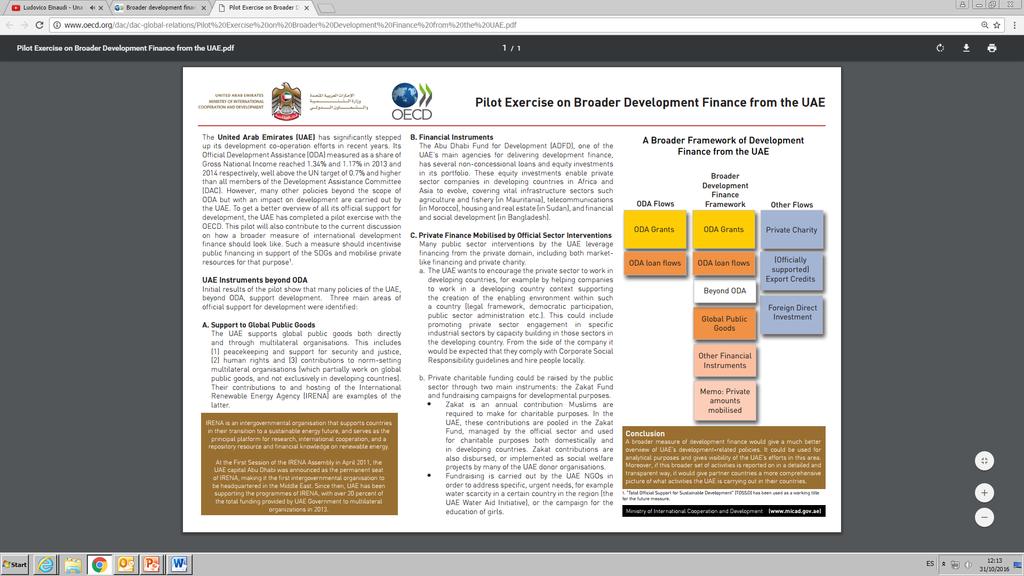

36 Pilot study United Arab Emirates United Arab Emirates instruments beyond ODA: Support to development enablers and global public goods Financial instruments beyond ODA Private financed mobilised by public sector interventions: raising private charity, accompany private investment with technical co-operation etc. Conclusion: TOSSD measure works for UAE.

37 UAE pilot

38 Senegal pilot 5, , , , , , , , , Concessional flows (DAC and multilaterals) Private flows at market terms Remittances Non-concessional flows (DAC and multilaterals) Private grants

39 TOSSD Compendium Part I Overview: origins, purpose, components, structure and implementation Part II Conceptual underpinnings and statistical features A. Coverage: 2030 Agenda B. Core architecture: provider and recipient perspectives C. TOSSD-eligible activities, countries and instruments D. Measurement issues and features

40 TOSSD compendium requests feedback on: 1. List of TOSSD-eligible countries and providers 2. Boundaries of projects that support development enablers and address global challenges 3. Governance arrangement including providers and stakeholders beyond the DAC (see next steps)

41 3. Way forward GPEDC High-Level event highten political awareness (November) Landmark global TOSSD première (early 2017) High-Level Policy Dialogue secure broader endorsement of governance arrangements (2017 during UN event, tbc) Drafting of international directives (throughout 2017)

42 4. Implementation Securing broad-based international support for TOSSD. Developing a network of TOSSD data co-ordination and aggregation entities. Developing tools and processes to enhance the quality and consistency of data (peer review learning events, linkages and support to statistical capacity building, measuring results/impact at country level, etc.). Developing and agreeing an inclusive TOSSD measurement framework governance/management arrangement.

43 THANK YOU FOR YOUR ATTENTION!

44 Q & A session The why: one single measure for all providers and all instruments in support of the SDGs? The what: does it measure the right things? The how: how should TOSSD be implemented? How should the concept be governed?

45 Q & A session on the purpose Are the objectives of the TOSSD measurement framework clear? A single measure for all providers? A measure covering support to the SDGs? A measure covering all financial instruments? More transparency on amounts mobilised from the private sector?

46 Q & A session on the measure itself Can activities motivated by the provider s selfinterest be included if they have an equally important developmental purpose or are expected to have a developmental impact? What further insights and proposals could be considered for defining the TOSSD-eligibility of activities addressing development enablers and global challenges at regional and global level in the areas of: Climate change? Migration? Peace and security? Human rights?

47 Q & A on TOSSD-eligibility Should TOSSD to all countries be counted? Which multilateral organisations should be TOSSD-eligible and how can they be identified?

48 Q & A session on the implementation How might an inclusive, representative, technically competent governance arrangement for TOSSD be structured? What institutions might be associated? Should we have TOSSD data collection institutions?

49 Back-up slides

50 II. THE DEVELOPMENT ENABLERS/CHALLENGES COMPONENT ALL PROVIDER COUNTRIES & MOST INSTRUMENTS

51 Clasificaciones Oficial vs. privado Concesional vs. non-concesional Bilateral vs. multilateral Histórico vs. futuro Compromisos vs. desembolsos

52 Puntos fuertes de la estadísticas del DAC sobre financiación para el desarrollo Global picture Comparable y fiable Rendición de cuentas Transparencia Coordinación de la cooperación

53 Público y privado Official Private Concessional Official development assistance (ODA) --grants --concessional loans --technical assistance NGO, foundation and other charitable flows Non-concessional Other official flows (OOF) --non-concessional loans (e.g. by DFIs) --investment-related transactions --export-related transactions Private flows at market terms --FDI and portfolio investment --export credits --bonds

54 Instrumentos de la cooperación al desarrollo Cooperación técnica Apoyo presupuestaria Contribuciones a organismos multilaterales, ONG etc. que trabajan en desarrollo Ayuda humanitaria Cancelación o reestructuración de deuda Gastos en el país proveedor (administrativos, para refugiados, becas y sensibilización) Proyectos

55 Difusión de la información Page views: Financing sustainable development topics page views a year a day visitors a year +640a day Very high demand for statistics Development co-operation statistics = top 4th of all OECD.stat exports + Data for 2015 records on excluding online databases

56 HLM outcomes: Modernising ODA (cont.) BEFORE: FULL FACE VALUE AFTER: ONLY THE GRANT EQUIVALENT OF A LOAN Grant Element Thresholds 25% 45% for LDCs and other LICs 15% for LMICs 10% for UMICs Discount Rates 10% Used for assessing the concessionality of a loan 5% base (current IMF discount rate) + adjustment factors of o 4% for LDCs and other LICs o 2% for LMICs o 1% for UMICs Used for both assessing the concessionality of a loan (does it meet the threshold?) and for calculating its ODA grant equivalent or the concessional portion of the loan. Measurement System Positive ODA when disbursed, negative ODA when repaid Grant equivalent of loan disbursements (grant element multiplied by amount disbursed). Repayment of past loans is not subtracted from ODA but will continue to be collected and published.

57 HLM outcomes: Better targeting of ODA Reverse declining trends of ODA to LDCs and improve targeting to countries most in need (LDCs, LICs, SIDS, LLDCs and fragile states) Enhance monitoring of members performance individually through DAC peer reviews and collectively at Senior Level Meetings (compendium of measures). Strengthen the empirical and analytical basis for better decision-making about smart ODA allocations.

58 HLM outcomes: Valorising the use of private-sector instruments Incentivise official sector use of instruments with a leveraging effect (e.g. equity, guarantees) by: Reflecting in ODA the effort of the official sector in catalysing private sector investment in effective development in ODA. Setting an international standard to measure the mobilisation effect of official interventions and collecting data on amounts mobilised in DAC statistics (under TOSSD or another category).

59 Cooperación técnica Actividades con el objetivo de aumenter el nivel de conocimiento y capacidades de las poblaciones de países socios. Se puede extender de varias formas: Personal del país proveedor (expertos, consultores, profesores etc.) Formación, investigación y otras actividades de capacitación Asistencia técnica enmarcada en proyectos

60 29 DAC Members 36 Multilateral organisations Australia Austria Belgium Czech Republic Canada Denmark European Union Finland France Germany Greece Iceland Ireland Italy Japan Korea Luxembourg The Netherlands New Zealand Norway Poland Portugal Slovak Republic Slovenia Spain Sweden Switzerland United Kingdom United States Adaptation Fund African Development Bank (AfDB) Arab Fund for Economic and Social Development (AFESD) Asian Development Bank (AsDB) Arab Bank for Economic Development in Africa (BADEA) Caribbean Development Bank (CarDB) Climate Investment Funds (CIFs) Council of Europe Development Bank (CEB) European Bank for Reconstruction and Development (EBRD) Food and Agriculture Organisation (FAO) The Global Alliance for Vaccines and Immunizations (GAVI) Global Environment Facility (GEF) Secretariat Global Fund to fight Aids, Tuberculosis and Malaria (GFATM) Global Green Growth Institute (GGGI) Inter-American Development Bank (IaDB) International Atomic Energy Agency (IAEA) International Fund for Agricultural Development (IFAD) International Finance Corporation (IFC) International Labour Organisation (ILO) IMF Concessional Trust Funds Islamic Development Bank (IsDB) Montreal Protocol Nordic Development Fund (NDF) OPEC Fund for International Development (OFID) Organization for Security and Co-operation in Europe (OSCE) UNAIDS UN Development Pogramme (UNDP) UN Economic Commission for Europe (UNECE) UN Population Fund (UNFPA) United Nations High Commissioner for Refugees (UNHCR) UNICEF UN Peacebuilding Fund (UNPBF) UN Relief and Works Agency (UNRWA) World Food Programme (WFP) World Health Organization (WHO) World Bank (IDA & IBRD) 21 non-dac countries OECD countries Estonia Hungary Israel Turkey Other countries Azerbaijan Bulgaria Cyprus Croatia Kazakhstan Kuwait (KFAED) Latvia Liechtenstein Lithuania Malta Romania Russia Saudi Arabia Chinese Taipei Thailand Timor Leste United Arab Emirates Private Foundation Bill and Melinda Gates Foundation

61 Draft architecture of the framework

DAC Working Party on Development Finance Statistics

Unclassified DCD/DAC/STAT(2017)16 DCD/DAC/STAT(2017)16 Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 08-Jun-2017 English

Unclassified DCD/DAC/STAT(2017)16 DCD/DAC/STAT(2017)16 Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 08-Jun-2017 English

THE FUTURE OF DEVELOPMENT FINANCE: Modernising Measures and Instruments

THE FUTURE OF DEVELOPMENT FINANCE: Modernising Measures and Instruments Ms. Suzanne Steensen Manager Development Finance Architecture Unit Statistics and Development Finance Division OECD Development Co-operation

THE FUTURE OF DEVELOPMENT FINANCE: Modernising Measures and Instruments Ms. Suzanne Steensen Manager Development Finance Architecture Unit Statistics and Development Finance Division OECD Development Co-operation

DEVELOPMENT AID AT A GLANCE

DEVELOPMENT AID AT A GLANCE STATISTICS BY REGION 5. EUROPE 6 edition 5.. ODA TO EUROPE - SUMMARY 5... Top ODA receipts by recipient USD million, net disbursements in 5... Trends in ODA Turkey % Ukraine

DEVELOPMENT AID AT A GLANCE STATISTICS BY REGION 5. EUROPE 6 edition 5.. ODA TO EUROPE - SUMMARY 5... Top ODA receipts by recipient USD million, net disbursements in 5... Trends in ODA Turkey % Ukraine

OECD DAC s Contribution to the Financing for Development Agenda

OECD DAC s Contribution to the Financing for Development Agenda Presentation at the International Conference on Development Cooperation Vilnius, Lithuania 22 October 2015 Raundi Halvorson-Quevedo, Statistics

OECD DAC s Contribution to the Financing for Development Agenda Presentation at the International Conference on Development Cooperation Vilnius, Lithuania 22 October 2015 Raundi Halvorson-Quevedo, Statistics

8822/16 YML/ik 1 DG C 1

Council of the European Union Brussels, 12 May 2016 (OR. en) 8822/16 OUTCOME OF PROCEEDINGS From: On: 12 May 2016 To: General Secretariat of the Council Delegations No. prev. doc.: 8530/16 Subject: DEVGEN

Council of the European Union Brussels, 12 May 2016 (OR. en) 8822/16 OUTCOME OF PROCEEDINGS From: On: 12 May 2016 To: General Secretariat of the Council Delegations No. prev. doc.: 8530/16 Subject: DEVGEN

Council conclusions on "First Annual Report to the European Council on EU Development Aid Targets"

COUNCIL OF THE EUROPEAN UNION Council conclusions on "First Annual Report to the European Council on EU Development Aid Targets" 3091st FOREIGN AFFAIRS Council meeting Brussels, 23 May 2011 The Council

COUNCIL OF THE EUROPEAN UNION Council conclusions on "First Annual Report to the European Council on EU Development Aid Targets" 3091st FOREIGN AFFAIRS Council meeting Brussels, 23 May 2011 The Council

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Delegations will find in the Annex to this note the above Council Conclusions, which were adopted by the Council on 23 May 2011.

COUNCIL OF THE EUROPEAN UNION Brussels, 23 May 2011 10593/11 DEVGEN 162 FIN 350 ACP 131 PTOM 28 COLAT 17 COASI 92 NOTE From: General Secretariat No. prev. doc.: 10187/11 Subject: Council Conclusions: First

COUNCIL OF THE EUROPEAN UNION Brussels, 23 May 2011 10593/11 DEVGEN 162 FIN 350 ACP 131 PTOM 28 COLAT 17 COASI 92 NOTE From: General Secretariat No. prev. doc.: 10187/11 Subject: Council Conclusions: First

Approach to Employment Injury (EI) compensation benefits in the EU and OECD

compensation benefits in the EU and OECD") Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

April aid spending by DAC donors in factsheet

April 2018 aid spending by DAC donors in 2017 factsheet In this factsheet we provide an overview of key trends in official development assistance (ODA) emerging from the April 2017 Organisation for Economic

April 2018 aid spending by DAC donors in 2017 factsheet In this factsheet we provide an overview of key trends in official development assistance (ODA) emerging from the April 2017 Organisation for Economic

Climate change and development are intrinsically linked

Climate-related development finance in 2013 Improving the statistical picture External development finance plays a key role to support developing countries in their transition to a low-carbon, climate-resilient

Climate-related development finance in 2013 Improving the statistical picture External development finance plays a key role to support developing countries in their transition to a low-carbon, climate-resilient

Health Financing: Unpacking Trends in ODA for Health CROSS-EUROPEAN ANALYSIS

Health Financing: Unpacking Trends in ODA for Health CROSS-EUROPEAN ANALYSIS BRIEFING PAPER JUNE 2015 Health Financing: Unpacking Trends in ODA for Health CROSS-EUROPEAN ANALYSIS 2 Introduction In the

Health Financing: Unpacking Trends in ODA for Health CROSS-EUROPEAN ANALYSIS BRIEFING PAPER JUNE 2015 Health Financing: Unpacking Trends in ODA for Health CROSS-EUROPEAN ANALYSIS 2 Introduction In the

FINANCING ENERGY PROJECTS IN DEVELOPING COUNTRIES

FINANCING ENERGY PROJECTS IN DEVELOPING COUNTRIES HOSSEIN RAZAVI, PHD CONTENTS List of Executive Overviews Summaries Figures Tables Preface Acknowledgments Abbreviations and Acronyms Units and Conversion

FINANCING ENERGY PROJECTS IN DEVELOPING COUNTRIES HOSSEIN RAZAVI, PHD CONTENTS List of Executive Overviews Summaries Figures Tables Preface Acknowledgments Abbreviations and Acronyms Units and Conversion

8959/18 YML/ik 1 DG C 1B

Council of the European Union Brussels, 22 May 2018 (OR. en) 8959/18 OUTCOME OF PROCEEDINGS From: On: 22 May 2018 To: General Secretariat of the Council Delegations No. prev. doc.: 8551/18 Subject: DEVGEN

Council of the European Union Brussels, 22 May 2018 (OR. en) 8959/18 OUTCOME OF PROCEEDINGS From: On: 22 May 2018 To: General Secretariat of the Council Delegations No. prev. doc.: 8551/18 Subject: DEVGEN

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

AID TARGETS SLIPPING OUT OF REACH?

AID TARGETS SLIPPING OUT OF REACH? www.oecd.org/dac/stats AID TARGETS SLIPPING OUT OF REACH? Overview Aid continued to increase in 2007, once exceptional debt relief is excluded from the figures. But the

AID TARGETS SLIPPING OUT OF REACH? www.oecd.org/dac/stats AID TARGETS SLIPPING OUT OF REACH? Overview Aid continued to increase in 2007, once exceptional debt relief is excluded from the figures. But the

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Climate change and development are intrinsically linked

Climate-related development finance in 2013 Improving the statistical picture Update June 2015* External development finance plays a key role to support developing countries in their transition to a low-carbon,

Climate-related development finance in 2013 Improving the statistical picture Update June 2015* External development finance plays a key role to support developing countries in their transition to a low-carbon,

Development Assistance for HealTH

Chapter : Development Assistance for HealTH The foremost goal of this research is to estimate the total volume of health assistance from 199 to 7. In this chapter, we present our estimates of total health

Chapter : Development Assistance for HealTH The foremost goal of this research is to estimate the total volume of health assistance from 199 to 7. In this chapter, we present our estimates of total health

At its meeting on 26 May 2015, the Council adopted the Council conclusions as set out in the annex to this note.

Council of the European Union Brussels, 26 May 2015 (OR. en) 9144/15 DEVGEN 78 RELEX 415 ACP 82 FIN 377 NOTE From: To: Subject: General Secretariat of the Council Delegations Annual Report 2015 to the

Council of the European Union Brussels, 26 May 2015 (OR. en) 9144/15 DEVGEN 78 RELEX 415 ACP 82 FIN 377 NOTE From: To: Subject: General Secretariat of the Council Delegations Annual Report 2015 to the

WIDER Development Conference September 2018: Aid Policy Continuity or Change? Richard Manning

WIDER Development Conference 13-15 September 2018: Aid Policy Continuity or Change? Richard Manning Total ODA USD billion (2016 prices and exchange rates) (Source OECD) ODA as percentage of GNI 1960 1961

WIDER Development Conference 13-15 September 2018: Aid Policy Continuity or Change? Richard Manning Total ODA USD billion (2016 prices and exchange rates) (Source OECD) ODA as percentage of GNI 1960 1961

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

Compendium of members recent efforts to support countries most in need

Compendium of members recent efforts to support countries most in need Recognising members specific circumstances and the diversity of their individual incentive frameworks, this compendium presents individual

Compendium of members recent efforts to support countries most in need Recognising members specific circumstances and the diversity of their individual incentive frameworks, this compendium presents individual

Chapter 2. Non-core funding of multilaterals

2. NON-CORE FUNDING OF MULTILATERALS 45 Chapter 2 Non-core funding of multilaterals This chapter concludes that non-core funding can contribute to a wide range of complementary activities, although they

2. NON-CORE FUNDING OF MULTILATERALS 45 Chapter 2 Non-core funding of multilaterals This chapter concludes that non-core funding can contribute to a wide range of complementary activities, although they

Global ODA Trends. Topics

Global ODA Trends In "Transforming our world: the 2030 agenda for sustainable development," adopted by the UN General Assembly in September 2015, "ODA providers reaffirm their respective commitments, including

Global ODA Trends In "Transforming our world: the 2030 agenda for sustainable development," adopted by the UN General Assembly in September 2015, "ODA providers reaffirm their respective commitments, including

Summary of key findings

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

Recommendation of the Council on Tax Avoidance and Evasion

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

Recommendation of the Council on Tax Avoidance and Evasion OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument

Programme for Government Joe Reynolds Director Programme for Government and Delivering Social Change

Programme for Government 2016-21 Joe Reynolds Director Programme for Government and Delivering Social Change Context the rationale for change Current PfG is a list of 82 Commitments Executive record on

Programme for Government 2016-21 Joe Reynolds Director Programme for Government and Delivering Social Change Context the rationale for change Current PfG is a list of 82 Commitments Executive record on

Funding. Context. Who Funds OHCHR?

Funding Context OHCHR s global funding needs are covered by the United Nations regular budget at a rate of approximately 40 per cent, with the remainder coming from voluntary contributions from Member

Funding Context OHCHR s global funding needs are covered by the United Nations regular budget at a rate of approximately 40 per cent, with the remainder coming from voluntary contributions from Member

Targeting aid to reach the poorest people: LDC aid trends and targets

Targeting aid to reach the poorest people: LDC aid trends and targets Briefing 2015 April Development Initiatives exists to end extreme poverty by 2030 www.devinit.org Focusing aid on the poorest people

Targeting aid to reach the poorest people: LDC aid trends and targets Briefing 2015 April Development Initiatives exists to end extreme poverty by 2030 www.devinit.org Focusing aid on the poorest people

Funding. Context UN HUMAN RIGHTS REPORT

Funding Context The income of the UN Human Rights Office comes, at a rate of approximately 40 per cent, from the United Nations regular budget. The remainder is covered by voluntary contributions from

Funding Context The income of the UN Human Rights Office comes, at a rate of approximately 40 per cent, from the United Nations regular budget. The remainder is covered by voluntary contributions from

Global Monitoring Report: Findings on Progress since Monterrey

Global Monitoring Report: Findings on Progress since Monterrey Governance, institutions, and capacity A number of developing regions have made considerable progress toward regulatory reform, but Sub-Saharan

Global Monitoring Report: Findings on Progress since Monterrey Governance, institutions, and capacity A number of developing regions have made considerable progress toward regulatory reform, but Sub-Saharan

Consolidated Annual Financial Report of the Administrative Agent of the Peacebuilding Fund

PEACEBUILDING FUND CONSOLIDATED ANNUAL FINANCIAL REPORT 2014 Consolidated Annual Financial Report of the Administrative Agent of the Peacebuilding Fund for the period 1 January to 31 December 2014 Multi-Partner

PEACEBUILDING FUND CONSOLIDATED ANNUAL FINANCIAL REPORT 2014 Consolidated Annual Financial Report of the Administrative Agent of the Peacebuilding Fund for the period 1 January to 31 December 2014 Multi-Partner

Measuring Aid to Health

Measuring Aid to Health Statistics presented in this note relate to Official Development Assistance (ODA) for health, population programmes and reproductive health (hereafter referred to as aid to health)

Measuring Aid to Health Statistics presented in this note relate to Official Development Assistance (ODA) for health, population programmes and reproductive health (hereafter referred to as aid to health)

Funding. Context. recent increases, remains at just slightly over 3 per cent of the total UN budget.

Funding Context Approximately 40 per cent of OHCHR s global funding needs are covered by the United Nations regular budget, with the remainder coming from voluntary contributions from Member States and

Funding Context Approximately 40 per cent of OHCHR s global funding needs are covered by the United Nations regular budget, with the remainder coming from voluntary contributions from Member States and

FCCC/SBI/2010/10/Add.1

United Nations Framework Convention on Climate Change Distr.: General 25 August 2010 Original: English Subsidiary Body for Implementation Contents Report of the Subsidiary Body for Implementation on its

United Nations Framework Convention on Climate Change Distr.: General 25 August 2010 Original: English Subsidiary Body for Implementation Contents Report of the Subsidiary Body for Implementation on its

Updates and revisions of national SUTs for the November 2013 release of the WIOD

Updates and revisions of national SUTs for the November 2013 release of the WIOD Edited by Marcel Timmer (University of Groningen) With contributions from: Abdul A. Erumban, Reitze Gouma and Gaaitzen J.

Updates and revisions of national SUTs for the November 2013 release of the WIOD Edited by Marcel Timmer (University of Groningen) With contributions from: Abdul A. Erumban, Reitze Gouma and Gaaitzen J.

APA & MAP COUNTRY GUIDE 2018 UKRAINE. New paths ahead for international tax controversy

APA & MAP COUNTRY GUIDE 2018 UKRAINE New paths ahead for international tax controversy UKRAINE APA PROGRAM KEY FEATURES Competent authority Relevant provisions Types of APAs available Acceptance criteria

APA & MAP COUNTRY GUIDE 2018 UKRAINE New paths ahead for international tax controversy UKRAINE APA PROGRAM KEY FEATURES Competent authority Relevant provisions Types of APAs available Acceptance criteria

aid flows 13 flows (USD 000, 2009 constant)

") AIDFORTRADE AT A GLANCE 2011 Basic indicators Population (thousands, ) 1 6 320 GDP (millions current USD, ) 2 5 939 GDP real growth rate (annual %, ) 3 6.4 GDP per capita, PPP (current international dollars,

AIDFORTRADE AT A GLANCE 2011 Basic indicators Population (thousands, ) 1 6 320 GDP (millions current USD, ) 2 5 939 GDP real growth rate (annual %, ) 3 6.4 GDP per capita, PPP (current international dollars,

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Withholding Tax Rate under DTAA

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Japan s ODA and JICA. Chapter 1 Japan s ODA and an Overview of JICA Programs

Chapter 1 Japan s ODA and an Overview of JICA Programs Livestock farmers attending a lecture by a repatriate participant of JICA training programs held in Japan (Livestock husbandry training in Northern

Chapter 1 Japan s ODA and an Overview of JICA Programs Livestock farmers attending a lecture by a repatriate participant of JICA training programs held in Japan (Livestock husbandry training in Northern

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

FOREWORD. Erik Solheim, DAC Chair

FOREWORD Multilateral co-operation plays a vital role in responding to today s global development challenges. Donors and governments use the multilateral system to invest and channel large amounts of money

FOREWORD Multilateral co-operation plays a vital role in responding to today s global development challenges. Donors and governments use the multilateral system to invest and channel large amounts of money

Recommendation of the Council on Establishing and Implementing Pollutant Release and Transfer Registers (PRTRs)

") Recommendation of the Council on Establishing and Implementing Pollutant Release and Transfer Registers (PRTRs) OECD Legal Instruments This document is published under the responsibility of the Secretary-General

Recommendation of the Council on Establishing and Implementing Pollutant Release and Transfer Registers (PRTRs) OECD Legal Instruments This document is published under the responsibility of the Secretary-General

Voice and Governance Reform in the BWIs An Update. Amar Bhattacharya G24 Secretariat May 26, 2010

Voice and Governance Reform in the BWIs An Update Amar Bhattacharya G24 Secretariat May 26, 2010 Total Votes for Developed and Developing Countries in Shares 70 60 50 40 30 20 10 0 IMF IBRD AsDB IADB Developed

Voice and Governance Reform in the BWIs An Update Amar Bhattacharya G24 Secretariat May 26, 2010 Total Votes for Developed and Developing Countries in Shares 70 60 50 40 30 20 10 0 IMF IBRD AsDB IADB Developed

Official Development Finance for Infrastructure: With a Special Focus on Multilateral Development Banks

Official Development Finance for Infrastructure: With a Special Focus on Multilateral Development Banks Kaori Miyamoto and Emilio Chiofalo OECD DEVELOPMENT CO-OPERATION WORKING PAPER 30 Authorised for

Official Development Finance for Infrastructure: With a Special Focus on Multilateral Development Banks Kaori Miyamoto and Emilio Chiofalo OECD DEVELOPMENT CO-OPERATION WORKING PAPER 30 Authorised for

At its meeting on 19 May 2014, the Council (Foreign Affairs/Development) adopted the Conclusions set out in the Annex to this note.

adopted the Conclusions set out in the Annex to this note.") COUNCIL OF THE EUROPEAN UNION Brussels, 19 May 2014 (OR. en) 9989/14 DEVGEN 135 RELEX 427 ACP 89 WTO 170 ONU 64 OCDE 4 NOTE From: To: Subject: General Secretariat of the Council Delegations Council Conclusions

COUNCIL OF THE EUROPEAN UNION Brussels, 19 May 2014 (OR. en) 9989/14 DEVGEN 135 RELEX 427 ACP 89 WTO 170 ONU 64 OCDE 4 NOTE From: To: Subject: General Secretariat of the Council Delegations Council Conclusions

Consolidated Annual Financial. Report of the Administrative Agent. of the Peacebuilding Fund

Consolidated Annual Financial Report of the Administrative Agent of the Peacebuilding Fund for the period 1 January to 31 December 2015 Multi-Partner Trust Fund Office Bureau of Management United Nations

Consolidated Annual Financial Report of the Administrative Agent of the Peacebuilding Fund for the period 1 January to 31 December 2015 Multi-Partner Trust Fund Office Bureau of Management United Nations

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems. 5 October 2017

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems 5 October 2017 Deutsche Börse Group 1 Settlement services: single point of access to cost-effective, low risk and

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems 5 October 2017 Deutsche Börse Group 1 Settlement services: single point of access to cost-effective, low risk and

LONG-TERM PROJECTIONS OF PUBLIC PENSION EXPENDITURE

7. FINANCES OF RETIREMENT-INCOME SYSTEMS LONG-TERM PROJECTIONS OF PUBLIC PENSION EXPENDITURE Key results Public spending on pensions has been on the rise in most OECD countries for the past decades, as

7. FINANCES OF RETIREMENT-INCOME SYSTEMS LONG-TERM PROJECTIONS OF PUBLIC PENSION EXPENDITURE Key results Public spending on pensions has been on the rise in most OECD countries for the past decades, as

2016 Progress Report by the OECD

TFFS 16/17b Meeting of the Task Force on Finance Statistics IMF Headquarters, Washington D.C., United States March 17 18, 2016 2016 Progress Report by the OECD Prepared by the OECD 2016 Progress Report

TFFS 16/17b Meeting of the Task Force on Finance Statistics IMF Headquarters, Washington D.C., United States March 17 18, 2016 2016 Progress Report by the OECD Prepared by the OECD 2016 Progress Report

A Note on Estimating China s Foreign Aid Using New Data: 2015 Preliminary Figures. Naohiro Kitano 2

JICA Research Institute 1 Tokyo, May 26, 2017 A Note on Estimating China s Foreign Aid Using New Data: 2015 Preliminary Figures Naohiro Kitano 2 This note presents revised and updated estimates of China

JICA Research Institute 1 Tokyo, May 26, 2017 A Note on Estimating China s Foreign Aid Using New Data: 2015 Preliminary Figures Naohiro Kitano 2 This note presents revised and updated estimates of China

ide: FRANCE Appendix A Countries with Double Taxation Agreement with France

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Donor Government Funding for Family Planning in 2016

REPORT Donor Government Funding for Family Planning in 2016 December 2017 Prepared by: Eric Lief Consultant and Adam Wexler and Jen Kates Kaiser Family Foundation Donor government funding for family planning

REPORT Donor Government Funding for Family Planning in 2016 December 2017 Prepared by: Eric Lief Consultant and Adam Wexler and Jen Kates Kaiser Family Foundation Donor government funding for family planning

TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA)

") TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA) In the period January - June 2018 the exports of goods from Bulgaria to the EU increased by 10.7% 2017 and amounted

TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA) In the period January - June 2018 the exports of goods from Bulgaria to the EU increased by 10.7% 2017 and amounted

IFC / CWDI 2010 Report: Accelerating Board Diversity

IFC / CWDI 2010 Report: Accelerating Board Diversity Comparative Percentages of Women Directors -- Europe Country # of in Survey Percentage of with Women Directors Percent of Women Directors Norway 517

IFC / CWDI 2010 Report: Accelerating Board Diversity Comparative Percentages of Women Directors -- Europe Country # of in Survey Percentage of with Women Directors Percent of Women Directors Norway 517

Rev. Proc Implementation of Nonresident Alien Deposit Interest Regulations

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Third Revised Decision of the Council concerning National Treatment

Third Revised Decision of the Council concerning National Treatment OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD

Third Revised Decision of the Council concerning National Treatment OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD

Withholding tax rates 2016 as per Finance Act 2016

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

G-20 Trade Aggregates Based on IMF s Balance of Payments Database

Twenty-Eighth Meeting of the IMF Committee on Balance of Payments Statistics Rio de Janeiro, Brazil October 27 29, 2015 BOPCOM 15/22 G-20 Trade Aggregates Based on IMF s Balance of Payments Database Prepared

Twenty-Eighth Meeting of the IMF Committee on Balance of Payments Statistics Rio de Janeiro, Brazil October 27 29, 2015 BOPCOM 15/22 G-20 Trade Aggregates Based on IMF s Balance of Payments Database Prepared

United Nations Environment Programme

UNITED NATIONS United Nations Environment Programme Distr. GENERAL 14 March 2012 EP ORIGINAL: ENGLISH EXECUTIVE COMMITTEE OF THE MULTILATERAL FUND FOR THE IMPLEMENTATION OF THE MONTREAL PROTOCOL Sixty-sixth

UNITED NATIONS United Nations Environment Programme Distr. GENERAL 14 March 2012 EP ORIGINAL: ENGLISH EXECUTIVE COMMITTEE OF THE MULTILATERAL FUND FOR THE IMPLEMENTATION OF THE MONTREAL PROTOCOL Sixty-sixth

Table of Contents. 1 created by

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017

(CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017") Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

The Global Tax Reset 2017 Audit Committee Symposium

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

Tax Newsflash January 31, 2014

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%

![Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%](/thumbs/88/116150947.jpg "Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%") Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

CRS Report for Congress

CRS Report for Congress Received through the CRS Web Order Code RS22032 Updated May 23, 2005 Foreign Aid: Understanding Data Used to Compare Donors Summary Larry Nowels Specialist in Foreign Affairs Foreign

CRS Report for Congress Received through the CRS Web Order Code RS22032 Updated May 23, 2005 Foreign Aid: Understanding Data Used to Compare Donors Summary Larry Nowels Specialist in Foreign Affairs Foreign

Funding. Context. OHCHR Funding Overview

Funding Context The global funding needs of the Office of the High Commissioner for Human Rights (OHCHR or UN Human Rights) are covered by the United Nations regular budget at a rate of approximately 40

Funding Context The global funding needs of the Office of the High Commissioner for Human Rights (OHCHR or UN Human Rights) are covered by the United Nations regular budget at a rate of approximately 40

Spain France. England Netherlands. Wales Ukraine. Republic of Ireland Czech Republic. Romania Albania. Serbia Israel. FYR Macedonia Latvia

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Goal 8: Develop a Global Partnership for Development

112 Goal 8: Develop a Global Partnership for Development Snapshots In 21, the net flow of official development assistance (ODA) to developing economies amounted to $128.5 billion which is equivalent to.32%

112 Goal 8: Develop a Global Partnership for Development Snapshots In 21, the net flow of official development assistance (ODA) to developing economies amounted to $128.5 billion which is equivalent to.32%

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

APA & MAP COUNTRY GUIDE 2017 CANADA

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

Consolidated Annual Financial. Report of the Administrative Agent. for. the Peacebuilding Fund

Consolidated Annual Financial Report of the Administrative Agent for the Peacebuilding Fund for the period 1 January to 31 December 2016 Multi-Partner Trust Fund Office Bureau for Management Services United

Consolidated Annual Financial Report of the Administrative Agent for the Peacebuilding Fund for the period 1 January to 31 December 2016 Multi-Partner Trust Fund Office Bureau for Management Services United

AUTOMATIC EXCHANGE OF INFORMATION (AEOI)

") AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

Public Pension Spending Trends and Outlook in Emerging Europe. Benedict Clements Fiscal Affairs Department International Monetary Fund March 2013

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

APA & MAP COUNTRY GUIDE 2017 DENMARK

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

Global Overview of 2012 Pooled Funding

Global Overview of 2012 Pooled Funding CERF, CHFs and ERFs 15 February 2013 Page 0 1. Introduction This overview provides key funding information on the Central Emergency Response fund (CERF), Common Humanitarian

Global Overview of 2012 Pooled Funding CERF, CHFs and ERFs 15 February 2013 Page 0 1. Introduction This overview provides key funding information on the Central Emergency Response fund (CERF), Common Humanitarian

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

COOPERATION JOURNAL. Editorial. Content. Biannual publication no. 9 year V October Editorial 1. Macroeconomic framework

COOPERATION JOURNAL Biannual publication no. 9 year V October 2016 Content Editorial Editorial 1 Macroeconomic framework Now in its fifth year, the Cooperation Journal continues to pursue its objective

COOPERATION JOURNAL Biannual publication no. 9 year V October 2016 Content Editorial Editorial 1 Macroeconomic framework Now in its fifth year, the Cooperation Journal continues to pursue its objective

FATCA Update May 2014

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

Ukraine. WTS Global Country TP Guide Last Update: December Legal Basis

Ukraine WTS Global Country TP Guide Last Update: December 2017 1. Legal Basis Is there a legal requirement to prepare TP documentation? Since when does a TP documentation requirement exist in your country?

Ukraine WTS Global Country TP Guide Last Update: December 2017 1. Legal Basis Is there a legal requirement to prepare TP documentation? Since when does a TP documentation requirement exist in your country?

Global Forum on Transparency and Exchange of Information for Tax Purposes. Statement of Outcomes

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

IDA13. Further Options for IDA13 Grant Financing

IDA13 Further Options for IDA13 Grant Financing International Development Association January 2004 1. During the IDA13 Mid-Term Review discussions on November 4-5, 2003, Deputies considered several approaches

IDA13 Further Options for IDA13 Grant Financing International Development Association January 2004 1. During the IDA13 Mid-Term Review discussions on November 4-5, 2003, Deputies considered several approaches

Export and import operations Tax & Legal, April 2017

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

Summary 715 SUMMARY. Minimum Legal Fee Schedule. Loser Pays Statute. Prohibition Against Legal Advertising / Soliciting of Pro bono

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Economic and Social Council

United Nations ECE/MP.PP/WG.1/2011/L.7 Economic and Social Council Distr.: Limited 25 November 2010 Original: English Economic Commission for Europe Meeting of the Parties to the Convention on Access to

United Nations ECE/MP.PP/WG.1/2011/L.7 Economic and Social Council Distr.: Limited 25 November 2010 Original: English Economic Commission for Europe Meeting of the Parties to the Convention on Access to

Burden of Taxation: International Comparisons

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Briefing Pack. The Executive Board

1. T H E E X E C U T I V E B O A R D A N D I T S F U N C T I O N S On 1 January 1996, following the adoption of parallel resolutions by the United Nations General Assembly and the Conference of the Food

1. T H E E X E C U T I V E B O A R D A N D I T S F U N C T I O N S On 1 January 1996, following the adoption of parallel resolutions by the United Nations General Assembly and the Conference of the Food

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Regulated Open-ended Fund Assets and Flows Trends

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Regulated Open-ended Fund Assets and Flows Trends

DOMESTIC CUSTODY & TRADING SERVICES

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Alter Domus IRELAND WE RE WHERE YOU NEED US.

WE RE WHERE YOU NEED US. Alter Domus is a fully integrated Fund and Corporate services provider, dedicated to international private equity & infrastructure houses, real estate firms, multinationals, private

WE RE WHERE YOU NEED US. Alter Domus is a fully integrated Fund and Corporate services provider, dedicated to international private equity & infrastructure houses, real estate firms, multinationals, private

Scale of Assessment of Members' Contributions for 2008

General Conference GC(51)/21 Date: 28 August 2007 General Distribution Original: English Fifty-first regular session Item 13 of the provisional agenda (GC(51)/1) Scale of Assessment of s' Contributions

General Conference GC(51)/21 Date: 28 August 2007 General Distribution Original: English Fifty-first regular session Item 13 of the provisional agenda (GC(51)/1) Scale of Assessment of s' Contributions

International Tax Conference

International Tax Conference Hong Kong s Experience with its International Tax Treaty Network Richard Wong Commissioner of Inland Revenue 19 June 2014 1 Introduction Purpose of signing a tax treaty Fairness

International Tax Conference Hong Kong s Experience with its International Tax Treaty Network Richard Wong Commissioner of Inland Revenue 19 June 2014 1 Introduction Purpose of signing a tax treaty Fairness

Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol

European Treaty Series - No. 127 Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol Strasbourg, 1.VI.2011 Annex B Competent authorities (*) States From A to F

European Treaty Series - No. 127 Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol Strasbourg, 1.VI.2011 Annex B Competent authorities (*) States From A to F

AID FOR TRADE IN 2010 CONTINUED GROWTH, MODEST OUTLOOK

AID FOR TRADE IN 2010 CONTINUED GROWTH, MODEST OUTLOOK AID FOR TRADE IN 2010 CONTINUED GROWTH, MODEST OUTLOOK TABLE OF CONTENTS EXECUTIVE SUMMARY... 4 Introduction... 5 1. How much aid for trade was committed

AID FOR TRADE IN 2010 CONTINUED GROWTH, MODEST OUTLOOK AID FOR TRADE IN 2010 CONTINUED GROWTH, MODEST OUTLOOK TABLE OF CONTENTS EXECUTIVE SUMMARY... 4 Introduction... 5 1. How much aid for trade was committed

2010 DAC REPORT ON MULTILATERAL AID

2010 DAC REPORT ON MULTILATERAL AID EXECUTIVE SUMMARY This second DAC Report on Multilateral Aid covers recent trends in multilateral aid and total use (core and non-core) of the multilateral system, with

2010 DAC REPORT ON MULTILATERAL AID EXECUTIVE SUMMARY This second DAC Report on Multilateral Aid covers recent trends in multilateral aid and total use (core and non-core) of the multilateral system, with