RELEASE PRIOR TO PAYMENT PRIVILEGE

|

|

|

- Irma Gallagher

- 6 years ago

- Views:

Transcription

1 Ottawa, February 16, 2010 MEMORANDUM D In Brief RELEASE PRIOR TO PAYMENT PRIVILEGE 1. This departmental memorandum explains the Release Prior to Payment Privilege that was previously found in D This memorandum is revised as a result of the Paper Burden Reduction Initiative; the revisions are aimed at eliminating obsolete and duplicated requirements, streamlining certain commercial processes and modifying complex policies and forms. 3. The following sections have been expanded for further clarification of the subjects: (a) The Direct Security and GST Options (b) Procedures related to late payment and non-compliance (c) Maintaining security for importers and customs brokers

2 Ottawa, February 16, 2010 MEMORANDUM D RELEASE PRIOR TO PAYMENT PRIVILEGE This memorandum explains the policies and procedures related to the privilege associated with the release of imported shipments prior to payment of duties and taxes. GUIDELINES AND GENERAL INFORMATION 1. An importer or customs broker who wishes to obtain the Release Prior to Payment Privilege shall: (a) Register for an importer/exporter account (refer to D17-1-5); and (b) Post security (refer to D1-7-1). 2. The Release Prior to Payment Privilege entitles holders to: (a) Obtain release of goods from the Canada Border Services Agency (CBSA) before paying duties and taxes; (b) Defer accounting; and (c) Defer payment of duties and taxes. 3. In addition to the security deposit, a letter with the following information should be provided when applying for this privilege: (a) name and address of importer or customs broker posting security; (b) contact name, telephone and fax numbers; (c) business number; and (d) the central payment office, if requested. 4. The Release Prior to Payment Privilege is subject to the terms and conditions of this memorandum, D and D The CBSA reserves the right to suspend the importer s or customs broker s privilege based on noncompliance. IMPORTER SECURITY 5. Security can be in the form of cash, certified cheque, money order, transferable bond issued by the Government of Canada, or a D120 Customs Bond issued by either a surety or financial institution as detailed in Memorandum D1-7-1, paragraph four. 6. Security is to be posted at CBSA Headquarters, Brokers Licensing and Account Security Programs Unit (Ottawa) to obtain this privilege. 7. Security for resident importers is based on their average monthly duties and taxes owing (less the GST), up to a maximum of CAN$10 million. 8. Security for non-resident importers is based on their average monthly duties and taxes owing (including GST), up to a maximum of CAN$10 million. 9. The minimum security requirement for an importer to transact business at all CBSA offices in Canada is CAN$5, The minimum security requirement for an importer to transact business at one CBSA office is CAN$ A sample of an importer s D120 Customs Bond with completion instructions can be found in Appendix A. This form is available in a fillable format on the CBSA web site under publications and forms. 12. The Release Prior to Payment Privilege will be granted by the CBSA with an acknowledgement sent to the importer and the surety or financial institution, confirming receipt of the security and providing the five-digit account security number within 21 days from the date of receipt by Brokers Licensing and Account Security Programs Unit. Using the Services of a Customs Broker 13. Importers may authorize a licensed customs broker to transact business with the CBSA on their behalf. 14. Fees imposed by customs brokers are not regulated by the CBSA. 15. Importers are reminded that although they may choose to use the services of a licensed customs broker to transact business with the CBSA on their behalf, the importer is ultimately responsible for the accounting documentation, payment of all duties and taxes, and subsequent corrections. CUSTOMS BROKER SECURITY 16. Security for customs brokers is based on their average monthly duties and taxes owing (including GST) up to a maximum of CAN$10 million. 17. The minimum security requirement for a customs broker to transact business at all CBSA offices in Canada is CAN$25, The minimum security requirement for a customs broker to transact business at one CBSA office is CAN$5, A sample of a customs broker s D120 Customs Bond with completion instructions can be found in Appendix B.

3 2 This form is available in a fillable format on the CBSA web site under publications and forms. Direct Security Option 20. Customs brokers may arrange for clients to obtain their own Release Prior to Payment Privilege (account security number) by posting security with CBSA. This option allows customs brokers to reduce their level of security by the importer s average monthly duties and taxes, provided the importer completes a direct security letter, authorizing the customs broker(s) to transact on the importer s behalf. Under this option, business is transacted using the customs broker s account security number. Should the importer wish to authorize the disclosure of information regarding their account security profile to the customs broker, the letter is to be placed on file with the CBSA, Brokers Licensing and Account Security Programs Unit. A specimen of the Direct Security Letter can be found in Appendix C of this memorandum. 21. Importers on the Direct Security Option agree to pay the full amount of duties and taxes owing at a CBSA office, or to their customs broker with a cheque made payable to the Receiver General for Canada by the last business day of the month. If payment is not made by this date, this option may be suspended. Should a customs broker default or fail to pay the amount owing, the importer remains liable for the payment. Importers should advise their customs broker when they submit payment directly to a CBSA office. 22. The customs broker must reconcile the importer s payments on Form K84 (broker s monthly account statement reconciliation control sheet), as per the requirements of Memorandum D The CBSA will no longer be acknowledging direct security letters, however, if CBSA, Brokers Licensing and Account Security Programs Unit, receives a valid letter, it will be placed on the importer's account security file. In the event that a bond is amended, cancelled or suspended, the CBSA will notify the customs broker, within 21 days from the date of receipt by Brokers Licensing and Account Security Programs Unit. 24. The CBSA requires a written letter from the importer if they wish to have a customs broker removed from their account security profile. Once an acknowledgement is sent to all parties, the customs broker will no longer be notified of activities on the importer s account. Goods and Services Tax (GST) Option 25. In order to reduce a customs broker s security requirement, the customs broker may place resident importers on the GST Option, thus allowing for a reduction in security equivalent to the importer s monthly GST owing. 26. These importers must agree to provide payment for the full amount of GST for all transactions processed during a billing period, with a cheque payable to the Receiver General for Canada. The cheque must be given to a CBSA office or to the customs broker for remittance to CBSA. Importers should advise their customs broker when they submit payment directly to a CBSA office. 27. The customs broker must reconcile the importer s payments on Form K84 (broker s monthly account statement reconciliation control sheet), as per the requirements of Memorandum D Failure to provide payment by the due date may result in the loss of the option. Interim Payment Option 29. In lieu of increasing their current level of security, customs brokers may apply for an interim payment option. Under this option, a customs broker must commit to the CBSA, in writing that they will make payments whenever the amount of outstanding duties and taxes exceeds their level of security. Failure to make the necessary payments may result in the customs broker being removed from this option, thereby requiring an increase in their security level. A request to participate in the Interim Payment Option is to be submitted in writing, to CBSA, Brokers Licensing and Account Security Programs Unit. MAINTAINING SECURITY FOR IMPORTERS AND CUSTOMS BROKERS 30. Importers and customs brokers are responsible for the annual review of their security level and are to maintain a record of their review on file as CBSA may request a copy for verification purposes. When additional security is required, the importer or customs broker will submit a rider, endorsement or an amendment (Refer to D1-7-1, paragraph 23). The review period is from July 25 of the previous year to July 24 of the current year. 31. Failure to comply with security requirements may result in the suspension of the Release Prior to Payment Privilege. MONITORING OF LATE PAYMENT AND NON- COMPLIANCE 32. Payment history will be monitored by the CBSA. Importers who are late paying three times in a one-year period may be removed from the GST or Direct Security Options, and their customs broker will be notified by CBSA Headquarters, Brokers Licensing and Account Security Programs Unit. Should the customs broker continue to use their own account security privilege for these importers, the customs broker will be held responsible for these payments. The importer may be placed back on the GST or Direct Security Options after one year following their date of suspension.

4 3 33. Importers with their own account security, that are not on the Direct Security Option, may be suspended after their third late payment. The Brokers Licensing and Account Security Programs Unit will notify these importers, in writing, of their non-compliance; the third letter may result in a suspension of their Release Prior to Payment Privilege. 34. The Administrative Monetary Penalty System (AMPS) contravention applies to late payments on duties and taxes owing, please refer to D for further information. Customs brokers non-compliance 35. Customs brokers who do not pay their monthly K84 amount in full, by the due date, may be placed on a daily K84 payment schedule until the outstanding debt is paid. In addition, customs brokers may be required to pay at least 5% of the outstanding amount on all previous K84s, each day, until the outstanding debt is cleared. 36. Once a customs broker has been placed on daily payments, any failure to pay the daily K84 in full may result in the suspension of the customs brokers Release Prior to Payment Privilege until the outstanding amount has been paid. 37. If the outstanding amount is not paid in full by the end of the following month, the customs brokers Release Prior to Payment Privilege may be suspended until the outstanding amount is paid with a certified cheque. Further actions on the part of the CBSA will be determined on a case-by-case basis. CLAIMS AGAINST SECURITY 38. When the terms and conditions for which security is taken are not met, the CBSA will withhold a sufficient portion of the security to cover the amount owing. The CBSA will provide relevant documentation to substantiate the claim. 39. If the CBSA files a claim against security posted for the Release Prior to Payment Privilege, the importer will no longer be eligible for the privilege, nor the Direct Security or GST Options for a three (3) year period following the resolution of the collection action. ADDITIONAL INFORMATION 40. General questions may be addressed to the following: Border Information Service (BIS) Calls within Canada: Toll-Free Service in English: Service in French: For those with hearing or speech impairments: Calls outside of Canada: Long distance charges apply Service in English: or Service in French: or Address: General questions and information: cbsa-asfc@canada.gc.ca 41. Documents for the Release Prior to Payment Privilege should be submitted to the CBSA via registered mail: Brokers Licensing and Account Security Programs Canada Border Services Agency Ottawa ON K1A 0L8

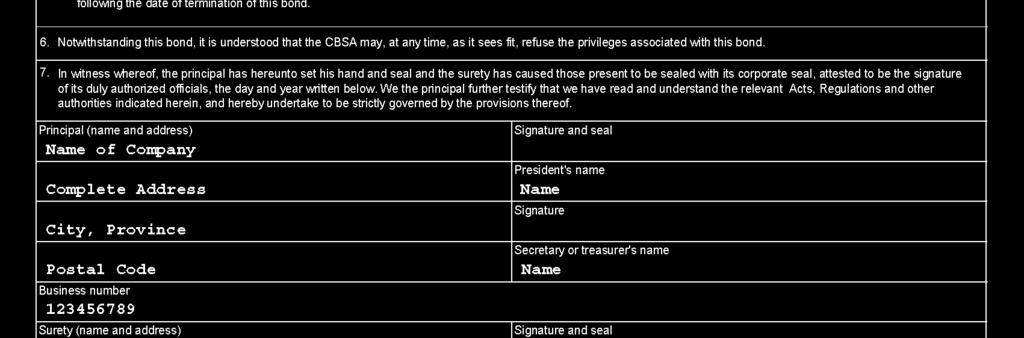

5 4 APPENDIX A INSTRUCTIONS FOR THE COMPLETION OF FORM D120, CUSTOMS BOND FOR IMPORTERS 1. Indicate the bond number, if applicable. 2. In field 1, state the specific bonded activity that will be secured. For this privilege, indicate the following: Release of goods from the CBSA prior to payment of duties. 3. Identify the relevant authority by writing in the appropriate legislation. Accounting for imported goods and payment of duties regulations. 4. Write the amount of security in words. 5. Write the amount of security in figures. 6. In field 3, insert the effective date (Month XX, YEAR) the bond is being completed by the surety or financial institution. Release prior to payment bonds must be continuous. 7. In field 4, state the CBSA office where the activities are to be conducted. For the national privilege, state All CBSA offices in Canada. For the local privilege input the applicable CBSA office. 8. In field 7, along with the principal s business number, state the principal's legal name and address. 9. Affix the signatures of two duly authorized officers of the principal, indicate their names, titles and impress the document with the corporate seal. 10. State the surety s or financial institution s name and address. 11. Affix the signature of authorized individuals of the surety company or financial institution, indicate their names, titles and impress the document with the corporate seal. 12. In field 8, affix the name, signature and the seal of the witnesses, if required. 13. In field 9, state the date the bond was signed and sealed.

6 5 IMPORTER BOND SAMPLE

7 6 APPENDIX B FOR CUSTOMS BROKERS 1. Indicate the bond number, if applicable. INSTRUCTIONS FOR THE COMPLETION OF FORM D120, CUSTOMS BOND 2. In field 1, state the specific bonded activity that will be secured. For the release of goods prior to payment privilege, insert the following: Remittance to Canada Border Services Agency, within the delays applicable to the importers and/or owners under relevant legislative authority for the release of goods prior to the payment of duties, of all monies that the principal, as agent for the importer and/or owner has taken to remit on account of duties. 3. Identify the relevant authority by writing in the appropriate legislation. Accounting for imported goods and payment of duties regulations. 4. Write the amount of security in words. 5. Write the amount of security in figures. 6. In field 3, insert the effective date the bond is being completed by the surety or financial institution. Release prior to payment bonds must be continuous. 7. In field 4, state the CBSA office where the activities are to be conducted. For the national privilege, state All CBSA offices in Canada. For the local privilege input the applicable CBSA office. 8. In field 7, along with the principal s business number, state the principal's legal name and address. 9. Affix the signatures of two duly authorized officers of the principal, indicate their names, titles and impress the document with the corporate seal. 10. State the surety s or financial institution s name and address. 11. Affix the signature of authorized individuals of the surety company or financial institution, indicate their names, titles and impress the document with the corporate seal. 12. In field 8, affix the name, signature and the seal of the witnesses, if required. 13. In field 9, state the date the bond was signed and sealed.

8 7 CUSTOMS BROKER BOND SAMPLE

9 8 APPENDIX C DIRECT SECURITY LETTER Date NAME OF IMPORTER has posted security for the release of goods prior to the payment of duties and taxes, and has been given the account security number A/S NUMBER. The business number of NAME OF IMPORTER is xxxxxxxxx. NAME OF BROKER will release and account for imports by NAME OF IMPORTER under the broker s account security number A/S NUMBER. NAME OF BROKER and NAME OF IMPORTER agree that: NAME OF IMPORTER will provide payment for the full amount of duties and taxes owing on imported goods; NAME OF IMPORTER agrees to pay the Canada Border Services Agency (CBSA) directly by the last business day of the month, or to provide NAME OF BROKER with a cheque made payable to the Receiver General for Canada each month, for the full amount of duties and taxes owing. The cheque is to be made available to NAME OF BROKER for remittance to CBSA, by the last business day of the month; NAME OF IMPORTER accepts responsibility and liability for the payment of penalties and interest applied by the CBSA resulting from any late payment of duties and taxes. Failure to provide payment to the CBSA by the due date will result in the application of penalties and interest to NAME OF IMPORTER on any amounts owing. Importers who are late paying 3 times in a one-year period may be removed from this option. NAME OF IMPORTER may benefit once again from the option program after one year from the date of suspension. NAME OF IMPORTER is reminded that although they may choose to use the services of a licensed customs broker to transact business with the CBSA on their behalf, the importer is ultimately responsible for the accounting documentation, payment of all duties and taxes, and subsequent corrections; NAME OF IMPORTER authorizes NAME OF BROKER to communicate with the Canada Revenue Agency (CRA) regarding collections activity related to amounts owing on imported goods released under this agreement, and to release information on these transactions to the CRA; NAME OF IMPORTER authorizes the disclosure of information pertaining to their Account Security Profile by officers of the Brokers Licensing and Account Security Programs, CBSA, to NAME OF CUSTOMS BROKER. All queries regarding this letter and the payment of duties and taxes on imported goods by NAME OF IMPORTER should be directed to: Contact name Title Address Telephone Fax number Signed (Importer) Signed (Broker)

10 9 APPENDIX D GST LETTER Date NAME OF IMPORTER is a resident of Canada. The business number of NAME OF IMPORTER is xxxxxxxxx. NAME OF BROKER will release and account for imports by NAME OF IMPORTER under the broker s account security number A/S NUMBER. NAME OF BROKER and NAME OF IMPORTER agree that: NAME OF IMPORTER will provide payment for the full amount of the goods and services tax (GST) levied on imported goods under the Excise Tax Act; NAME OF IMPORTER agrees to pay the Canada Border Services Agency (CBSA) directly by the last business day of the month, or to provide NAME OF BROKER with a cheque made payable to the Receiver General for Canada each month, for the full amount of GST owing. The cheque must be made available to NAME OF BROKER for remittance to CBSA, by the last business day of the month; NAME OF IMPORTER accepts responsibility and liability for the payment of penalties and interest applied by the CBSA resulting from any late payment of GST. Failure to provide payment to the CBSA by the due date will result in the application of penalties and interest to NAME OF IMPORTER on any amounts owing. Importers who are late paying 3 times in a one-year period may be removed from this option. NAME OF IMPORTER may benefit once again from the option program after one year from the date of suspension. NAME OF IMPORTER is reminded that although they may choose to use the services of a licensed customs broker to transact business with the CBSA on their behalf, the importer is ultimately responsible for the accounting documentation, payment of all duties and taxes, and subsequent corrections; NAME OF IMPORTER authorizes NAME OF BROKER to communicate with the Canada Revenue Agency (CRA) regarding collections activity related to amounts owing on imported goods released under this agreement, and to release information on these transactions to the CRA. All queries regarding this letter and the payment of GST on imported goods by NAME OF IMPORTER should be directed to: Contact name Title Address Telephone Fax number Signed (Importer) Signed (Broker)

11 10 REFERENCES ISSUING OFFICE Brokers Licensing and Account Security Programs Licensing, Export, and Accounting Policy Division Admissibility Branch HEADQUARTERS FILE 7640 LEGISLATIVE REFERENCES Customs Act, Section 35, 133(1) & (2) OTHER REFERENCES D1-7-1 D SUPERSEDED MEMORANDA D D dated May 16, 2002 Services provided by the Canada Border Services Agency are available in both official languages.

IMPORTER NAME/ACCOUNT NUMBER OR BUSINESS NUMBER CHANGES

Ottawa, August 27, 2008 MEMORANDUM D17-2-3 In Brief IMPORTER NAME/ACCOUNT NUMBER OR BUSINESS NUMBER CHANGES This memorandum has been updated to: include information formerly contained in Customs Notice

Ottawa, August 27, 2008 MEMORANDUM D17-2-3 In Brief IMPORTER NAME/ACCOUNT NUMBER OR BUSINESS NUMBER CHANGES This memorandum has been updated to: include information formerly contained in Customs Notice

MEMORANDUM D In Brief. Ottawa, January 15, 2010

Ottawa, January 15, 2010 MEMORANDUM D19-10-3 In Brief ADMINISTRATION OF THE EXPORT AND IMPORT PERMITS ACT (EXPORTATIONS) 1. This memorandum has been updated to reflect changes to the 's (CBSA) role in

Ottawa, January 15, 2010 MEMORANDUM D19-10-3 In Brief ADMINISTRATION OF THE EXPORT AND IMPORT PERMITS ACT (EXPORTATIONS) 1. This memorandum has been updated to reflect changes to the 's (CBSA) role in

MEMORANDUM D In Brief. Ottawa, July 8, 2009 CUSTOMS VALUATION PURCHASER IN CANADA REGULATIONS (CUSTOMS ACT, SECTION 48)

") Ottawa, July 8, 2009 MEMORANDUM D13-1-3 In Brief CUSTOMS VALUATION PURCHASER IN CANADA REGULATIONS (CUSTOMS ACT, SECTION 48) 1. This memorandum provides information on the treatment of a purchaser in Canada

Ottawa, July 8, 2009 MEMORANDUM D13-1-3 In Brief CUSTOMS VALUATION PURCHASER IN CANADA REGULATIONS (CUSTOMS ACT, SECTION 48) 1. This memorandum provides information on the treatment of a purchaser in Canada

MEMORANDUM D In Brief. Ottawa, July 6, 2007

Ottawa, July 6, 2007 MEMORANDUM D17-1-22 In Brief ACCOUNTING FOR THE HARMONIZED SALES TAX, PROVINCIAL SALES TAX, PROVINCIAL TOBACCO TAX AND ALCOHOL MARKUP/FEE ON CASUAL IMPORTATIONS IN THE COURIER AND

Ottawa, July 6, 2007 MEMORANDUM D17-1-22 In Brief ACCOUNTING FOR THE HARMONIZED SALES TAX, PROVINCIAL SALES TAX, PROVINCIAL TOBACCO TAX AND ALCOHOL MARKUP/FEE ON CASUAL IMPORTATIONS IN THE COURIER AND

SUBJECT MAINTENANCE OF RECORDS AND BOOKS IN CANADA BY EXPORTERS AND PRODUCERS TABLE OF CONTENTS

MEMORANDUM D20-1-5 Ottawa, January 1, 1994 SUBJECT MAINTENANCE OF RECORDS AND BOOKS IN CANADA BY EXPORTERS AND PRODUCERS This Memorandum provides information relative to the records and books that must

MEMORANDUM D20-1-5 Ottawa, January 1, 1994 SUBJECT MAINTENANCE OF RECORDS AND BOOKS IN CANADA BY EXPORTERS AND PRODUCERS This Memorandum provides information relative to the records and books that must

In Brief TARIFF PREFERENCE LEVELS

Ottawa, June 10, 2009 MEMORANDUM D11-4-22 In Brief 1. Memorandum D11-4-22 has been revised to reflect: TARIFF PREFERENCE LEVELS (a) increases in Tariff Preference Levels (TPLs) for importations of specific

Ottawa, June 10, 2009 MEMORANDUM D11-4-22 In Brief 1. Memorandum D11-4-22 has been revised to reflect: TARIFF PREFERENCE LEVELS (a) increases in Tariff Preference Levels (TPLs) for importations of specific

In Brief CUSTOMS SELF ASSESSMENT PROGRAM FOR IMPORTERS

Ottawa, August 14, 2009 MEMORANDUM D17-1-7 In Brief CUSTOMS SELF ASSESSMENT PROGRAM FOR IMPORTERS Memorandum D17-1-7 has been written to provide information and guidelines regarding the Customs Self Assessment

Ottawa, August 14, 2009 MEMORANDUM D17-1-7 In Brief CUSTOMS SELF ASSESSMENT PROGRAM FOR IMPORTERS Memorandum D17-1-7 has been written to provide information and guidelines regarding the Customs Self Assessment

Excise and GST/HST News

Excise and GST/HST News No. 63 Winter 2007 Table of Contents Notice of Ways and Means Motion... 1 Exemption for midwifery services... 4 Application for direct sellers to use the alternate collection method...

Excise and GST/HST News No. 63 Winter 2007 Table of Contents Notice of Ways and Means Motion... 1 Exemption for midwifery services... 4 Application for direct sellers to use the alternate collection method...

Part 1 Information for authorized agents who may receive contributions

Income Tax Information Circular NO.: DATE: November 2016 SUBJECT: Contributions to a Registered Party, a Registered Association or to a Candidate at a Federal Election This circular cancels and replaces

Income Tax Information Circular NO.: DATE: November 2016 SUBJECT: Contributions to a Registered Party, a Registered Association or to a Candidate at a Federal Election This circular cancels and replaces

Auditing Charities T4118(E)

") Auditing Charities T4118(E) Table of contents Page hy does the Canada Revenue Agency audit charities?... 3 hat triggers a charity audit?... 3 How do we conduct an audit?... 3 hat happens when the audit

Auditing Charities T4118(E) Table of contents Page hy does the Canada Revenue Agency audit charities?... 3 hat triggers a charity audit?... 3 How do we conduct an audit?... 3 hat happens when the audit

InBrief SUBJECT VISITING FORCES PERSONNEL TARIFF ITEM NO

Memorandumn D21-4-3 Locator Code: 192B Ottawa, February 29, 2000 InBrief SUBJECT VISITING FORCES PERSONNEL TARIFF ITEM NO. 9827.00.00 1. This Memorandum was amended to reflect changes to tariff item No.

Memorandumn D21-4-3 Locator Code: 192B Ottawa, February 29, 2000 InBrief SUBJECT VISITING FORCES PERSONNEL TARIFF ITEM NO. 9827.00.00 1. This Memorandum was amended to reflect changes to tariff item No.

MEMORANDUM D In Brief. Ottawa, March 16, 2006

Ottawa, March 16, 2006 MEMORANDUM D11-4-2 In Brief PROOF OF ORIGIN Memorandum D11-4-2, Proof of Origin, has been revised to include references to the Canada-Costa Rica Free Trade Agreement (CCRFTA), to

Ottawa, March 16, 2006 MEMORANDUM D11-4-2 In Brief PROOF OF ORIGIN Memorandum D11-4-2, Proof of Origin, has been revised to include references to the Canada-Costa Rica Free Trade Agreement (CCRFTA), to

CHAPTER FOUR ORIGIN PROCEDURES ARTICLE 4.3:

CHAPTER FOUR ORIGIN PROCEDURES ARTICLE 4.1: DEFINITIONS For the purposes of this Chapter: customs authority means the authority that is responsible under the law of a Party for the administration and application

CHAPTER FOUR ORIGIN PROCEDURES ARTICLE 4.1: DEFINITIONS For the purposes of this Chapter: customs authority means the authority that is responsible under the law of a Party for the administration and application

Memo. SECTION 3 Fees, Dues, Levies and Exemptions 3.2 JOINING FEES

Memo To: From: Date: RE: All OMREB Members Janice Myers, Executive Director June 7, 2012 (June 11 UPDATE text addition for clarification) OMREB Regulation Revisions: SECTION 3 Fees, Dues, Levies & Exemptions

Memo To: From: Date: RE: All OMREB Members Janice Myers, Executive Director June 7, 2012 (June 11 UPDATE text addition for clarification) OMREB Regulation Revisions: SECTION 3 Fees, Dues, Levies & Exemptions

Canada Border Services Agency ("CBSA") gets specific about specific information'

gets specific about specific information'") July 2013 international trade bulletin Canada Border Services Agency ("CBSA") gets specific about specific information' thrust of the recent changes to CBSA's Reason to Believe' ("RTB") and Reassessment

July 2013 international trade bulletin Canada Border Services Agency ("CBSA") gets specific about specific information' thrust of the recent changes to CBSA's Reason to Believe' ("RTB") and Reassessment

ONTARIO REGULATION made under the PAYDAY LOANS ACT, 2008 GENERAL. Skip Table of Contents

ONTARIO REGULATION made under the PAYDAY LOANS ACT, 2008 GENERAL Skip Table of Contents CONTENTS DEFINITIONS 1. Definitions LICENCES OR RENEWAL OF LICENCES 2. Application process 3. Eligibility requirements

ONTARIO REGULATION made under the PAYDAY LOANS ACT, 2008 GENERAL Skip Table of Contents CONTENTS DEFINITIONS 1. Definitions LICENCES OR RENEWAL OF LICENCES 2. Application process 3. Eligibility requirements

T Supplement Package

Protected B when completed T1134-1 Supplement Package Reporting Entity and Information Sheet This T1134-1 Supplement Package is to be used in conjunction with the T1134 Information Return Relating to Controlled

Protected B when completed T1134-1 Supplement Package Reporting Entity and Information Sheet This T1134-1 Supplement Package is to be used in conjunction with the T1134 Information Return Relating to Controlled

POST-IMPORTATION PAYMENTS OR FEES SUBSEQUENT PROCEEDS

Ottawa, July 8, 2009 MEMORANDUM D13-4-13 In Brief POST-IMPORTATION PAYMENTS OR FEES SUBSEQUENT PROCEEDS (Customs Act, Section 48) 1. This memorandum provides information on the treatment of post-importation

Ottawa, July 8, 2009 MEMORANDUM D13-4-13 In Brief POST-IMPORTATION PAYMENTS OR FEES SUBSEQUENT PROCEEDS (Customs Act, Section 48) 1. This memorandum provides information on the treatment of post-importation

Law Firm Self-Report Guidelines to Complete the Self-Report

These guidelines are designed for the Law Firm Self-Report. A separate FAQ document has been prepared for the accountants to assist in the completion of the Accountant s Report. A user guide has also been

These guidelines are designed for the Law Firm Self-Report. A separate FAQ document has been prepared for the accountants to assist in the completion of the Accountant s Report. A user guide has also been

ICMA GMRA 2000 and GMRA 2011 FATCA Approaches 1. "Code", the United States of America Internal Revenue Code of 1986, as amended; and

1(a). GMRA 2000 Master Agreement: Insert new definitions as follows: ICMA GMRA 2000 and GMRA 2011 FATCA Approaches 1 "Code", the United States of America Internal Revenue Code of 1986, as amended; and

1(a). GMRA 2000 Master Agreement: Insert new definitions as follows: ICMA GMRA 2000 and GMRA 2011 FATCA Approaches 1 "Code", the United States of America Internal Revenue Code of 1986, as amended; and

1. Background Filing Deadline A. Late Filings Reporting Requirements... 5

Trust Safety: Release: Final January 2018 Table of Contents 1. Background... 4 2. Filing Deadline... 4 A. Late Filings... 4 3. Reporting Requirements... 5 A. Firm Practice Profile... 6 B. Bank Accounts...

Trust Safety: Release: Final January 2018 Table of Contents 1. Background... 4 2. Filing Deadline... 4 A. Late Filings... 4 3. Reporting Requirements... 5 A. Firm Practice Profile... 6 B. Bank Accounts...

STANDARD CONSTRUCTION CONTRACT. THESE ARTICLES OF AGREEMENT made in duplicate and effective the day of 2017: NEW BRUNSWICK POWER CORPORATION

STANDARD CONSTRUCTION CONTRACT THESE ARTICLES OF AGREEMENT made in duplicate and effective the day of 2017: BETWEEN: NEW BRUNSWICK POWER CORPORATION (referred to herein as the Owner) AND (referred to herein

STANDARD CONSTRUCTION CONTRACT THESE ARTICLES OF AGREEMENT made in duplicate and effective the day of 2017: BETWEEN: NEW BRUNSWICK POWER CORPORATION (referred to herein as the Owner) AND (referred to herein

Retirement Compensation Arrangements Guide

Retirement Compensation Arrangements Guide 2005 T4041(E) Rev. 05 Before you start Is this guide for you? This guide is for you if one of the following applies: You are an employer and you make contributions

Retirement Compensation Arrangements Guide 2005 T4041(E) Rev. 05 Before you start Is this guide for you? This guide is for you if one of the following applies: You are an employer and you make contributions

Application to Participate in the Auction for Spectrum Licences for Advanced Wireless Services and other Spectrum in the 2 GHz Range

Bidder Identification Number 0 5 Application to Participate in the Auction for Spectrum Licences for Advanced Wireless Services and other Spectrum in the 2 GHz Range (Please print or type all information

Bidder Identification Number 0 5 Application to Participate in the Auction for Spectrum Licences for Advanced Wireless Services and other Spectrum in the 2 GHz Range (Please print or type all information

NEW YORK TRANSMITTERS OF MONEY

New York State Regulations Section 406.1. Introduction This Part contains regulations relating to the transmission of money by licensees and their agents under article XIII-B of the Banking Law. For purposes

New York State Regulations Section 406.1. Introduction This Part contains regulations relating to the transmission of money by licensees and their agents under article XIII-B of the Banking Law. For purposes

Contents. Application. What is the difference between a Technical Interpretation and a Ruling? INCOME TAX INFORMATION CIRCULAR

INCOME TAX INFORMATION CIRCULAR NO.: IC70-6R7 DATE: April 22, 2016 SUBJECT: Advance Income Tax Rulings and Technical Interpretations This version is only available electronically. Contents Application

INCOME TAX INFORMATION CIRCULAR NO.: IC70-6R7 DATE: April 22, 2016 SUBJECT: Advance Income Tax Rulings and Technical Interpretations This version is only available electronically. Contents Application

distill spirits is called the Excise Act, 2001 (the ).

.") distill spirits is called the Excise Act, 2001 (the ). Revenue Agency ( ) tax services office. (See ) or by contacting their region s excise duty manager. (See for regional excise duty managers contact

distill spirits is called the Excise Act, 2001 (the ). Revenue Agency ( ) tax services office. (See ) or by contacting their region s excise duty manager. (See for regional excise duty managers contact

Duty Free Shop Inventory Control and Sales Requirements

ISSN 2369-2391 Memorandum D4-3-5 Ottawa, September 22, 2015 Duty Free Shop Inventory Control and Sales Requirements In Brief 1. This memorandum has been revised to reflect organizational changes resulting

ISSN 2369-2391 Memorandum D4-3-5 Ottawa, September 22, 2015 Duty Free Shop Inventory Control and Sales Requirements In Brief 1. This memorandum has been revised to reflect organizational changes resulting

Excise and GST/HST News

Excise and GST/HST News No. 56 Spring 2005 Table of Contents New name for the GST/HST News... 1 First Nations Advisory Committee... 1 Bill C-43 Budget 2005... 2 GST/HST health care rebate... 2 Directors

Excise and GST/HST News No. 56 Spring 2005 Table of Contents New name for the GST/HST News... 1 First Nations Advisory Committee... 1 Bill C-43 Budget 2005... 2 GST/HST health care rebate... 2 Directors

PARTNERS IN PROTECTION (PIP) PROCESS DOCUMENTATION

PROCESS DOCUMENTATION") PARTNERS IN PROTECTION (PIP) PROCESS DOCUMENTATION ACCEPTANCE / REJECTION Applications are received and reviewed to assess eligibility (See Appendix A) and to ensure minimum-security requirements are met.

PARTNERS IN PROTECTION (PIP) PROCESS DOCUMENTATION ACCEPTANCE / REJECTION Applications are received and reviewed to assess eligibility (See Appendix A) and to ensure minimum-security requirements are met.

Complaints and Disputes

Complaints and Disputes includes information about CRA Service Complaints Program RC4540(E) Rev. 16 Is this guide for you? T his guide is for you if you are not satisfied with the service, the assessment,

Complaints and Disputes includes information about CRA Service Complaints Program RC4540(E) Rev. 16 Is this guide for you? T his guide is for you if you are not satisfied with the service, the assessment,

Table of Contents. General Information INCOME TAX INFORMATION CIRCULAR

INCOME TAX INFORMATION CIRCULAR NO.: IC72-17R6 DATE: September 29, 2011 SUBJECT: Procedures concerning the disposition of taxable Canadian property by non-residents of Canada Section 116 This version is

INCOME TAX INFORMATION CIRCULAR NO.: IC72-17R6 DATE: September 29, 2011 SUBJECT: Procedures concerning the disposition of taxable Canadian property by non-residents of Canada Section 116 This version is

ARL Webinar: Open Payment Credits on Statement of Account (SOA)

") ARL Webinar: Open Payment Credits on Statement of Account (SOA) Date: Wednesday May 10 and 17, 2017 Time: 12:30 pm 2:00 pm, Eastern Daylight Time Meeting Number: 550 071 281 1 SOA Credit History Context

ARL Webinar: Open Payment Credits on Statement of Account (SOA) Date: Wednesday May 10 and 17, 2017 Time: 12:30 pm 2:00 pm, Eastern Daylight Time Meeting Number: 550 071 281 1 SOA Credit History Context

KGS-Alpha Capital Markets, L.P.

KGS-Alpha Capital Markets, L.P. TERMS OF BUSINESS Last Updated: December 10, 2014 (Effective: December 11, 2014) By doing business with KGS-Alpha Capital Markets, L.P. ( KGS ), You, the Customer, accept

KGS-Alpha Capital Markets, L.P. TERMS OF BUSINESS Last Updated: December 10, 2014 (Effective: December 11, 2014) By doing business with KGS-Alpha Capital Markets, L.P. ( KGS ), You, the Customer, accept

West. irginia State Publication TSD-404 (Rev. December 2007) Timber Sever. ements

Timber Sever. ements") West Vir irginia State te Tax Depar partment Publication TSD-404 (Rev. December 2007) Timber Sever erance Tax Requir equirements ements For Nonresidents The purpose of this publication is to provide general

West Vir irginia State te Tax Depar partment Publication TSD-404 (Rev. December 2007) Timber Sever erance Tax Requir equirements ements For Nonresidents The purpose of this publication is to provide general

Completing the Tax Return Where Registration of a Charity is Revoked

Completing the Tax Return Where Registration of a Charity is Revoked RC4424(E) Rev. 09 Change of name In this publication, we use the name Canada Revenue Agency and the acronym CRA to represent the Canada

Completing the Tax Return Where Registration of a Charity is Revoked RC4424(E) Rev. 09 Change of name In this publication, we use the name Canada Revenue Agency and the acronym CRA to represent the Canada

Revenu Québec 3800, rue de Marly Québec (Québec) G1X 4A5. This version of bulletin ADM. 4 supersedes that of March 31, 2004.

G1X 4A5. This version of bulletin ADM. 4 supersedes that of March 31, 2004.") INTERPRETATION AND ADMINISTRATIVE PRACTICE CONCERNING THE LAWS AND REGULATIONS Income Tax Revenu Québec 3800, rue de Marly Québec (Québec) G1X 4A5 Page: 1of 8 Subject: Voluntary Disclosures This version

INTERPRETATION AND ADMINISTRATIVE PRACTICE CONCERNING THE LAWS AND REGULATIONS Income Tax Revenu Québec 3800, rue de Marly Québec (Québec) G1X 4A5 Page: 1of 8 Subject: Voluntary Disclosures This version

PROTOCOL AMENDING THE CONVENTION BETWEEN THE GOVERNMENT OF JAPAN AND THE GOVERNMENT OF THE REPUBLIC OF INDIA FOR THE AVOIDANCE OF DOUBLE TAXATION AND

PROTOCOL AMENDING THE CONVENTION BETWEEN THE GOVERNMENT OF JAPAN AND THE GOVERNMENT OF THE REPUBLIC OF INDIA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES

PROTOCOL AMENDING THE CONVENTION BETWEEN THE GOVERNMENT OF JAPAN AND THE GOVERNMENT OF THE REPUBLIC OF INDIA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES

Processing and Maintenance Procedures for Old Style Bonds (S42)

") Processing and Maintenance Procedures for Old Style Bonds (S42) CSB SERIES 1 TO 31 (1946 76), COUPONS, GOVERNMENT OF CANADA MARKET ISSUE BONDS, DOMINION OF CANADA BONDS, TREASURY BILLS AND WAR SAVINGS

Processing and Maintenance Procedures for Old Style Bonds (S42) CSB SERIES 1 TO 31 (1946 76), COUPONS, GOVERNMENT OF CANADA MARKET ISSUE BONDS, DOMINION OF CANADA BONDS, TREASURY BILLS AND WAR SAVINGS

2 BUSINESS OF THE MEETING

(the "Company") Minutes of a meeting of the board of directors of the Company held at "Meeting"). Present on (the ("Chairman") In attendance 1 QUORUM AND NOTICE 1.1 It was resolved to appoint as Chairman

(the "Company") Minutes of a meeting of the board of directors of the Company held at "Meeting"). Present on (the ("Chairman") In attendance 1 QUORUM AND NOTICE 1.1 It was resolved to appoint as Chairman

INTERIM ECONOMIC DEVELOPMENT RATE-ATTRACTION AGREEMENT (Post Resolution E-4675) Form I

Form I") Southern California Edison Revised Cal. PUC Sheet No. 55472-E Rosemead, California (U 338-E) Cancelling Original Cal. PUC Sheet No. 47234-E Sheet 1 INTERIM ECONOMIC DEVELOPMENT RATE-ATTRACTION AGREEMENT

Southern California Edison Revised Cal. PUC Sheet No. 55472-E Rosemead, California (U 338-E) Cancelling Original Cal. PUC Sheet No. 47234-E Sheet 1 INTERIM ECONOMIC DEVELOPMENT RATE-ATTRACTION AGREEMENT

CLIENT AGREEMENT (The Agreement )

") CLIENT AGREEMENT (The Agreement ) 1. DEFINITIONS: In this Agreement "I", "me", and "my" mean the individual who has signed the Signature Card. If more than one individual has signed the Signature Card,

CLIENT AGREEMENT (The Agreement ) 1. DEFINITIONS: In this Agreement "I", "me", and "my" mean the individual who has signed the Signature Card. If more than one individual has signed the Signature Card,

SURETY BOND OF SELF INSURER OF WORKERS COMPENSATION. THAT Employer and Address

_ STATE of WEST VIRGINIA INSURANCE COMMISSIONER OF WEST VIRGINIA SELF-INSURANCE UNIT 1124 SMITH STREET POST OFFICE BOX 11410 CHARLESTON, WEST VIRGINIA 25339-1410 SURETY BOND OF SELF INSURER OF WORKERS

_ STATE of WEST VIRGINIA INSURANCE COMMISSIONER OF WEST VIRGINIA SELF-INSURANCE UNIT 1124 SMITH STREET POST OFFICE BOX 11410 CHARLESTON, WEST VIRGINIA 25339-1410 SURETY BOND OF SELF INSURER OF WORKERS

Table of Contents CORPORATE ACTIONS ACCOUNT AND TRANSACTION CONTROL MARGIN TRADING SYSTEM

Central Depository Company of Pakistan Limited CENTRAL DEPOSITORY SYSTEM (CDS) STANDARD OPERATING PROCEDURES CDS STANDARD OPERATING PROCEDURES Table of Contents CORPORATE ACTIONS 1. Procedure for Corporate

Central Depository Company of Pakistan Limited CENTRAL DEPOSITORY SYSTEM (CDS) STANDARD OPERATING PROCEDURES CDS STANDARD OPERATING PROCEDURES Table of Contents CORPORATE ACTIONS 1. Procedure for Corporate

Bill 24. An Act mainly to combat consumer debt overload and modernize consumer credit rules. Introduction

SECOND SESSION THIRTY-NINTH LEGISLATURE Bill 24 An Act mainly to combat consumer debt overload and modernize consumer credit rules Introduction Introduced by Mr. Jean-Marc Fournier Minister of Justice

SECOND SESSION THIRTY-NINTH LEGISLATURE Bill 24 An Act mainly to combat consumer debt overload and modernize consumer credit rules Introduction Introduced by Mr. Jean-Marc Fournier Minister of Justice

Texas FAIR Plan Producer Requirements and Performance Standards

Texas FAIR Plan Producer Requirements and Performance Standards John W. Polak, CPCU 2002 The following Texas FAIR Plan Association ("Association") requirements and producer performance standards ("Requirements

Texas FAIR Plan Producer Requirements and Performance Standards John W. Polak, CPCU 2002 The following Texas FAIR Plan Association ("Association") requirements and producer performance standards ("Requirements

Chapter 4 FINANCE AND PERSONNEL

Chapter 4 FINANCE AND PERSONNEL Table of Contents Article I. In General... 2 Sec. 4-01. Fiscal year.... 2 Sec. 4-02. Budget.... 2 Sec. 4-03. Compensation schedule.... 3 Sec. 4-04. Method of approving financial

Chapter 4 FINANCE AND PERSONNEL Table of Contents Article I. In General... 2 Sec. 4-01. Fiscal year.... 2 Sec. 4-02. Budget.... 2 Sec. 4-03. Compensation schedule.... 3 Sec. 4-04. Method of approving financial

GENERAL PROCEDURES UNDER CENTRAL EXCISE

5 GENERAL PROCEDURES UNDER CENTRAL EXCISE SIGNIFICANT NOTIFICATIONS/CIRCULARS ISSUED BETWEEN 01.05.2014 AND 30.04.2015 1. Following amendments have been made in Central Excise Rules, 2002 [CER] vide Notification

5 GENERAL PROCEDURES UNDER CENTRAL EXCISE SIGNIFICANT NOTIFICATIONS/CIRCULARS ISSUED BETWEEN 01.05.2014 AND 30.04.2015 1. Following amendments have been made in Central Excise Rules, 2002 [CER] vide Notification

AL RAJHI SAVINGS ACCOUNT-i AGREEMENT

Original Bank Copy Duplicate Customer Copy AL RAJHI SAVINGS ACCOUNT-i AGREEMENT BETWEEN AL RAJHI BANKING & INVESTMENT CORPORATION (MALAYSIA) BHD (719057-X) AND CUSTOMER S NAME: REGISTRATION NO./NRIC NO./PASSPORT

Original Bank Copy Duplicate Customer Copy AL RAJHI SAVINGS ACCOUNT-i AGREEMENT BETWEEN AL RAJHI BANKING & INVESTMENT CORPORATION (MALAYSIA) BHD (719057-X) AND CUSTOMER S NAME: REGISTRATION NO./NRIC NO./PASSPORT

AL RAJHI CURRENT ACCOUNT-i AGREEMENT

Original Bank Copy Duplicate Customer Copy AL RAJHI CURRENT ACCOUNT-i AGREEMENT BETWEEN AL RAJHI BANKING & INVESTMENT CORPORATION (MALAYSIA) BHD (719057-X) AND CUSTOMER S NAME: REGISTRATION NO./NRIC NO./PASSPORT

Original Bank Copy Duplicate Customer Copy AL RAJHI CURRENT ACCOUNT-i AGREEMENT BETWEEN AL RAJHI BANKING & INVESTMENT CORPORATION (MALAYSIA) BHD (719057-X) AND CUSTOMER S NAME: REGISTRATION NO./NRIC NO./PASSPORT

SHARE HANDLING REGULATIONS

(Translation for Reference Purpose Only) SHARE HANDLING REGULATIONS (Amended as of April 1, 2013) ANA HOLDINGS INC. (TRANSLATION) SHARE HANDLING REGULATIONS CHAPTER I GENERAL PROVISIONS Article 1 (Purpose)

(Translation for Reference Purpose Only) SHARE HANDLING REGULATIONS (Amended as of April 1, 2013) ANA HOLDINGS INC. (TRANSLATION) SHARE HANDLING REGULATIONS CHAPTER I GENERAL PROVISIONS Article 1 (Purpose)

Articles of Association of Bangkok Bank Public Company Limited. Chapter 1 General Provision

Articles of Association of Bangkok Bank Public Company Limited Chapter 1 General Provision Article 1. In these Articles of Association, Company means Bangkok Bank Public Company Limited. Acts means the

Articles of Association of Bangkok Bank Public Company Limited Chapter 1 General Provision Article 1. In these Articles of Association, Company means Bangkok Bank Public Company Limited. Acts means the

GST/HST Memoranda Series

GST/HST Memoranda Series 16.3 January 2009 Cancellation or Waiver of Penalties and/or Interest Note: This memorandum of Chapter 16 supersedes GST Memorandum 500-3-2-1, Cancellation or Waiver of Penalties

GST/HST Memoranda Series 16.3 January 2009 Cancellation or Waiver of Penalties and/or Interest Note: This memorandum of Chapter 16 supersedes GST Memorandum 500-3-2-1, Cancellation or Waiver of Penalties

PAYDAY LOANS ACT REGULATIONS

c t PAYDAY LOANS ACT REGULATIONS PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this regulation, current to September 1, 2015. It is intended for information

c t PAYDAY LOANS ACT REGULATIONS PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this regulation, current to September 1, 2015. It is intended for information

APPENDIX 1 OPERATIONAL CERTIFICATION PROCEDURES FOR THE RULES OF ORIGIN

APPENDIX 1 OPERATIONAL CERTIFICATION PROCEDURES FOR THE RULES OF ORIGIN For the purposes of implementing Annex 3, the following operational procedures on the issuance of a Certificate of Origin, verification

APPENDIX 1 OPERATIONAL CERTIFICATION PROCEDURES FOR THE RULES OF ORIGIN For the purposes of implementing Annex 3, the following operational procedures on the issuance of a Certificate of Origin, verification

Self-Insurer Applicant:

Self-Insurer Applicant: Application for workers' disability compensation self-insured authority is made on Form WC-402. Questions 1through 10 must be completed. Requests for attached information as stated

Self-Insurer Applicant: Application for workers' disability compensation self-insured authority is made on Form WC-402. Questions 1through 10 must be completed. Requests for attached information as stated

NATIONAL INSURANCE COMMISSION, ABUJA

NATIONAL INSURANCE COMMISSION, ABUJA OPERATIONAL GUIDELINES 2011 (INTERMEDIARIES) 1 P age Table of Contents: 0.0 PREAMBLE 1.0 ACCOUNTING AND RETURNS 1.1 Filing of Annual Return and Accounts a. Insurance

NATIONAL INSURANCE COMMISSION, ABUJA OPERATIONAL GUIDELINES 2011 (INTERMEDIARIES) 1 P age Table of Contents: 0.0 PREAMBLE 1.0 ACCOUNTING AND RETURNS 1.1 Filing of Annual Return and Accounts a. Insurance

Table of Contents CORPORATE ACTIONS ACCOUNT AND TRANSACTION CONTROL MARGIN TRADING SYSTEM

Central Depository Company of Pakistan Limited CENTRAL DEPOSITORY SYSTEM (CDS) STANDARD OPERATING PROCEDURES CDS STANDARD OPERATING PROCEDURES Table of Contents CORPORATE ACTIONS 1. Procedure for Corporate

Central Depository Company of Pakistan Limited CENTRAL DEPOSITORY SYSTEM (CDS) STANDARD OPERATING PROCEDURES CDS STANDARD OPERATING PROCEDURES Table of Contents CORPORATE ACTIONS 1. Procedure for Corporate

Brokerage Agreement Between Standard Lines Brokerage, Inc. (Hereinafter called SLB) and. (Hereinafter called Agency)

and. (Hereinafter called Agency)") Brokerage Agreement Between Standard Lines Brokerage, Inc. (Hereinafter called SLB) and (Hereinafter called Agency) Agency s Federal Identification Number THIS BROKERAGE AGREEMENT ( Agreement ) is made

Brokerage Agreement Between Standard Lines Brokerage, Inc. (Hereinafter called SLB) and (Hereinafter called Agency) Agency s Federal Identification Number THIS BROKERAGE AGREEMENT ( Agreement ) is made

Canadian Standard Form of Contract for Architectural Services

The Royal Architectural Institute of Canada Canadian Standard Form of Contract for Architectural Services DOCUMENT SIX 2006 Edition ADAPTED FOR: (NAME of PROJECT AND / OR PROJECT NUMBER) Affix RAIC Authorization

The Royal Architectural Institute of Canada Canadian Standard Form of Contract for Architectural Services DOCUMENT SIX 2006 Edition ADAPTED FOR: (NAME of PROJECT AND / OR PROJECT NUMBER) Affix RAIC Authorization

CANADA QUÉBEC AGREEMENT ON ENGLISH-LANGUAGE SERVICES TO

CANADA QUÉBEC AGREEMENT ON ENGLISH-LANGUAGE SERVICES 2016 2017 TO 2017 2018 THIS AGREEMENT was concluded in English and in French, this day of 2017, BETWEEN: AND: HER MAJESTY THE QUEEN IN RIGHT OF CANADA,

CANADA QUÉBEC AGREEMENT ON ENGLISH-LANGUAGE SERVICES 2016 2017 TO 2017 2018 THIS AGREEMENT was concluded in English and in French, this day of 2017, BETWEEN: AND: HER MAJESTY THE QUEEN IN RIGHT OF CANADA,

Oh Canada. Is Compliance The Same?

Oh Canada Is Compliance The Same? We Look The Same (Sort Of ) We Speak The Same (Or Do We?) We Say Creek Roof Presentation Chesterfield Tea Towel Bunnyhug Pogie Garburator Runners You Say Creek Roof Presentation

Oh Canada Is Compliance The Same? We Look The Same (Sort Of ) We Speak The Same (Or Do We?) We Say Creek Roof Presentation Chesterfield Tea Towel Bunnyhug Pogie Garburator Runners You Say Creek Roof Presentation

Revenu Québec 3800, rue de Marly Québec (Québec) G1X 4A5

G1X 4A5") INTERPRETATION AND ADMINISTRATIVE PRACTICE CONCERNING THELAWSANDREGULATIONS Income Tax Revenu Québec 3800, rue de Marly Québec (Québec) G1X 4A5 Page: 1of 8 Subject: Voluntary Disclosures This version of

INTERPRETATION AND ADMINISTRATIVE PRACTICE CONCERNING THELAWSANDREGULATIONS Income Tax Revenu Québec 3800, rue de Marly Québec (Québec) G1X 4A5 Page: 1of 8 Subject: Voluntary Disclosures This version of

Unique Context of GST/HST Regime. August 19, Via

August 19, 2016 Via email: Kevin.Morgan@cra-arc.gc.ca Kevin Morgan Manager Voluntary Disclosures Program Horizontal Integration Directorate Assessment, Benefit and Services Branch Canada Revenue Agency

August 19, 2016 Via email: Kevin.Morgan@cra-arc.gc.ca Kevin Morgan Manager Voluntary Disclosures Program Horizontal Integration Directorate Assessment, Benefit and Services Branch Canada Revenue Agency

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS. Revised June 30, 2008

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS Revised June 30, 2008 TABLE of CONTENTS A Letter to Employers..3 The Student Loan Program.4-5 The Basic Steps Employers Follow for

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS Revised June 30, 2008 TABLE of CONTENTS A Letter to Employers..3 The Student Loan Program.4-5 The Basic Steps Employers Follow for

GUIDELINES FOR JAMAICA DEPOSITARY RECEIPTS

SR-GUID 15-/04-0024 GUIDELINES FOR JAMAICA DEPOSITARY RECEIPTS The Financial Services Commission 39-43 Barbados Avenue Kingston 5, Jamaica W.I. Telephone No. (876) 906-3010 April 13, 2015 1.0 INTRODUCTION

SR-GUID 15-/04-0024 GUIDELINES FOR JAMAICA DEPOSITARY RECEIPTS The Financial Services Commission 39-43 Barbados Avenue Kingston 5, Jamaica W.I. Telephone No. (876) 906-3010 April 13, 2015 1.0 INTRODUCTION

1. Each Participant will provide that the Certificate of Origin referred to in Article of the Agreement is:

MEMORANDUM OF UNDERSTANDING BETWEEN CANADA AND THE REPUBLIC OF KOREA CONCERNING UNIFORM REGULATIONS FOR THE INTERPRETATION, APPLICATION AND ADMINISTRATION OF CHAPTER FOUR OF THE FREE TRADE AGREEMENT BETWEEN

MEMORANDUM OF UNDERSTANDING BETWEEN CANADA AND THE REPUBLIC OF KOREA CONCERNING UNIFORM REGULATIONS FOR THE INTERPRETATION, APPLICATION AND ADMINISTRATION OF CHAPTER FOUR OF THE FREE TRADE AGREEMENT BETWEEN

PG&E Corporation Dividend Reinvestment and Stock Purchase Plan

Prospectus PG&E Corporation Dividend Reinvestment and Stock Purchase Plan 3,461,227 shares of PG&E Corporation common stock, no par value This prospectus describes the PG&E Corporation Dividend Reinvestment

Prospectus PG&E Corporation Dividend Reinvestment and Stock Purchase Plan 3,461,227 shares of PG&E Corporation common stock, no par value This prospectus describes the PG&E Corporation Dividend Reinvestment

GARNISHMENT Instructions for Employer

GARNISHMENT Instructions for Employer Garnishment is a legal procedure that a creditor uses to collect money from a debtor. The process permits the creditor to force you, the debtor s employer, to pay

GARNISHMENT Instructions for Employer Garnishment is a legal procedure that a creditor uses to collect money from a debtor. The process permits the creditor to force you, the debtor s employer, to pay

Table of Contents CORPORATE ACTIONS ACCOUNT AND TRANSACTION CONTROL MARGIN TRADING SYSTEM

Central Depository Company of Pakistan Limited CENTRAL DEPOSITORY SYSTEM (CDS) STANDARD OPERATING PROCEDURES CDS STANDARD OPERATING PROCEDURES Table of Contents CORPORATE ACTIONS 1. Procedure for Corporate

Central Depository Company of Pakistan Limited CENTRAL DEPOSITORY SYSTEM (CDS) STANDARD OPERATING PROCEDURES CDS STANDARD OPERATING PROCEDURES Table of Contents CORPORATE ACTIONS 1. Procedure for Corporate

Regulation 102 Waiver Application

Regulation 102 Waiver Application Is this form for you? Use this form if you are a: n-resident employee providing employment services in Canada, and you want to apply for a waiver of the tax required to

Regulation 102 Waiver Application Is this form for you? Use this form if you are a: n-resident employee providing employment services in Canada, and you want to apply for a waiver of the tax required to

Chapter RCW UNAUTHORIZED INSURERS

Chapter 48.15 RCW UNAUTHORIZED INSURERS Sections 48.15.020 Solicitation prohibited 48.15.023 Penalties for violations 48.15.030 Voidable contracts 48.15.040 Conditions for procurement of surplus line coverage

Chapter 48.15 RCW UNAUTHORIZED INSURERS Sections 48.15.020 Solicitation prohibited 48.15.023 Penalties for violations 48.15.030 Voidable contracts 48.15.040 Conditions for procurement of surplus line coverage

SUBJECT DEFENCE SUPPLIES AND DEFENCE PRODUCTION AND DEVELOPMENT SHARING ARRANGEMENTS BETWEEN CANADA AND THE UNITED STATES

MEMORANDUM D8-9-3 Ottawa, May 10, 2001 SUBJECT DEFENCE SUPPLIES AND DEFENCE PRODUCTION AND DEVELOPMENT SHARING ARRANGEMENTS BETWEEN CANADA AND THE UNITED STATES This Memorandum outlines the conditions

MEMORANDUM D8-9-3 Ottawa, May 10, 2001 SUBJECT DEFENCE SUPPLIES AND DEFENCE PRODUCTION AND DEVELOPMENT SHARING ARRANGEMENTS BETWEEN CANADA AND THE UNITED STATES This Memorandum outlines the conditions

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN The Government of Canada and the Government of Sweden, Resolved to continue their co-operation in the field of

AGREEMENT ON SOCIAL SECURITY BETWEEN THE GOVERNMENT OF CANADA AND THE GOVERNMENT OF SWEDEN The Government of Canada and the Government of Sweden, Resolved to continue their co-operation in the field of

International Fuel Tax Agreement. Information and Compliance Manual

Department of Revenue Division of Taxation International Fuel Tax Agreement Information and Compliance Manual Introduction The purpose of this manual is to outline the steps involved in licensing and reporting

Department of Revenue Division of Taxation International Fuel Tax Agreement Information and Compliance Manual Introduction The purpose of this manual is to outline the steps involved in licensing and reporting

Re National Bank Direct Brokerage Inc. Decision

Unofficial English Translation Re National Bank Direct Brokerage Inc. In the matter of: The Rules of the Investment Industry Regulatory Organization of Canada and The By-Laws of the Investment Dealers

Unofficial English Translation Re National Bank Direct Brokerage Inc. In the matter of: The Rules of the Investment Industry Regulatory Organization of Canada and The By-Laws of the Investment Dealers

THE KARNATAKA MUNICIPALITIES ACCOUNTING AND BUDGETING RULES, 2006 NOTIFICATION

1 THE KARNATAKA MUNICIPALITIES ACCOUNTING AND BUDGETING RULES, 2006 NOTIFICATION Whereas the draft The Karnataka Municipalities Accounting and Budgeting Rules, 2006 was published as required by sub-section

1 THE KARNATAKA MUNICIPALITIES ACCOUNTING AND BUDGETING RULES, 2006 NOTIFICATION Whereas the draft The Karnataka Municipalities Accounting and Budgeting Rules, 2006 was published as required by sub-section

ADDITIONAL TERMS FOR MARGIN This agreement should be used only when adding margin privileges to an existing CGMI investment account.

` < Account Number Box> ADDITIONAL TERMS FOR MARGIN This agreement should be used only when adding margin privileges to an existing CGMI investment account. CGMI Account No.: In consideration

` < Account Number Box> ADDITIONAL TERMS FOR MARGIN This agreement should be used only when adding margin privileges to an existing CGMI investment account. CGMI Account No.: In consideration

General Application for GST/HST Rebates

General Application for GST/HST Rebates Includes forms GST189, GST288, and GST507 RC4033(E) Rev. 12 Is this guide for you? T his guide gives general information and instructions to help you complete Form

General Application for GST/HST Rebates Includes forms GST189, GST288, and GST507 RC4033(E) Rev. 12 Is this guide for you? T his guide gives general information and instructions to help you complete Form

Guide for Employers Source Deductions and Contributions

Revenu Québec www.revenu.gouv.qc.ca Guide for Employers Source Deductions and Contributions 2009 Short Version The information contained in this guide does not constitute a legal interpretation of the

Revenu Québec www.revenu.gouv.qc.ca Guide for Employers Source Deductions and Contributions 2009 Short Version The information contained in this guide does not constitute a legal interpretation of the

INTERRENT REAL ESTATE INVESTMENT TRUST DISTRIBUTION REINVESTMENT AND UNIT PURCHASE PLAN

INTERRENT REAL ESTATE INVESTMENT TRUST DISTRIBUTION REINVESTMENT AND UNIT PURCHASE PLAN Purpose The InterRent Real Estate Investment Trust distribution reinvestment plan (the Plan ) enables registered

INTERRENT REAL ESTATE INVESTMENT TRUST DISTRIBUTION REINVESTMENT AND UNIT PURCHASE PLAN Purpose The InterRent Real Estate Investment Trust distribution reinvestment plan (the Plan ) enables registered

MANITOBA TELECOM SERVICES INC. DIVIDEND REINVESTMENT AND SHARE PURCHASE PLAN

MANITOBA TELECOM SERVICES INC. DIVIDEND REINVESTMENT AND SHARE PURCHASE PLAN MAY 12, 2010 SUMMARY Manitoba Telecom Services Inc. Dividend Reinvestment and Share Purchase Plan This is a summary of the features

MANITOBA TELECOM SERVICES INC. DIVIDEND REINVESTMENT AND SHARE PURCHASE PLAN MAY 12, 2010 SUMMARY Manitoba Telecom Services Inc. Dividend Reinvestment and Share Purchase Plan This is a summary of the features

Government of Gujarat Finance Department, Sachivalaya, Gandhinagar Dated the 1 st, 2006

Government of Gujarat Finance Department, Sachivalaya, Gandhinagar Dated the 1 st, 2006 No. (GHN- ) VAR (1) / 2005 / Th: - WHEREAS the Government of Gujarat is satisfied that circumstances exist which

Government of Gujarat Finance Department, Sachivalaya, Gandhinagar Dated the 1 st, 2006 No. (GHN- ) VAR (1) / 2005 / Th: - WHEREAS the Government of Gujarat is satisfied that circumstances exist which

PROMISSORY NOTE TERM TABLE. BORROWER S PRINCIPAL (manager):

:") PROMISSORY NOTE TERM TABLE PRINCIPAL (loan amount): ORIGINATION DATE: BORROWER: INTEREST (annualized): MATURITY DATE: BORROWER S PRINCIPAL (manager): ADDRESS: LIEN: First priority lien. Second priority

PROMISSORY NOTE TERM TABLE PRINCIPAL (loan amount): ORIGINATION DATE: BORROWER: INTEREST (annualized): MATURITY DATE: BORROWER S PRINCIPAL (manager): ADDRESS: LIEN: First priority lien. Second priority

General Terms and Conditions for the Use of the Bank s Services and Opening All Types of Foreign Currency Deposit Accounts

General Terms and Conditions for the Use of the Bank s Services and Opening All Types of Foreign Currency Deposit Accounts 1. A foreign currency deposit account may be opened in any currency which is acceptable

General Terms and Conditions for the Use of the Bank s Services and Opening All Types of Foreign Currency Deposit Accounts 1. A foreign currency deposit account may be opened in any currency which is acceptable

Partnership code. 8. Are any of the amounts (e.g., income, deductions, foreign tax credits) claimed by the reporting person/partnership in the current

claimed by the reporting person/partnership in the current") Do not use this area INFORMATION RETURN OF NON-ARM'S LENGTH TRANSACTIONS WITH NON-RESIDENTS T106 SUMMARY FORM Refer to the instruction sheet before you complete the T106 Summary and Slips. Complete a separate

Do not use this area INFORMATION RETURN OF NON-ARM'S LENGTH TRANSACTIONS WITH NON-RESIDENTS T106 SUMMARY FORM Refer to the instruction sheet before you complete the T106 Summary and Slips. Complete a separate

KGS-Alpha Capital Markets, L.P.

KGS-Alpha Capital Markets, L.P. TERMS OF BUSINESS Last Updated: March 15, 2017 (Effective: March 15, 2017) By doing business with KGS-Alpha Capital Markets, L.P. ( KGS ), You, the Customer, accept and

KGS-Alpha Capital Markets, L.P. TERMS OF BUSINESS Last Updated: March 15, 2017 (Effective: March 15, 2017) By doing business with KGS-Alpha Capital Markets, L.P. ( KGS ), You, the Customer, accept and

Construction Contract Between Owner and Construction Manager at Risk

FINAL 10/10/03 Date: Project Name: ASU Project Number: Construction Manager at Risk: Owner: Arizona Board of Regents for and on behalf of Arizona State University CMAR and Owner hereby agree as follows:

FINAL 10/10/03 Date: Project Name: ASU Project Number: Construction Manager at Risk: Owner: Arizona Board of Regents for and on behalf of Arizona State University CMAR and Owner hereby agree as follows:

Registered Charities Newsletter

Registered Charities Newsletter No. 26 Winter 2006 Contents From the Director General...1 Legalese for charities Part II..2 What s new?...4 Charities Partnership and Outreach Program...4 New on-line search

Registered Charities Newsletter No. 26 Winter 2006 Contents From the Director General...1 Legalese for charities Part II..2 What s new?...4 Charities Partnership and Outreach Program...4 New on-line search

Guide to the Canadian Standard Form of Contract for Architectural Services

Guide to the Canadian Standard Form of Contract for Architectural Services DOCUMENT SIX 2006 Edition NOTE: All terms which are defined and which are used throughout this document appear in italicized text

Guide to the Canadian Standard Form of Contract for Architectural Services DOCUMENT SIX 2006 Edition NOTE: All terms which are defined and which are used throughout this document appear in italicized text

Professional Corporation Application for Certificate of Authorization Form 4-6D

Chartered Professional Accountants of Ontario 69 Bloor Street East Toronto ON M4W 1B3 T. 416 962.1841 Toll free 1 800 387.0735 cpaontario.ca Professional Corporation Application for Certificate of Authorization

Chartered Professional Accountants of Ontario 69 Bloor Street East Toronto ON M4W 1B3 T. 416 962.1841 Toll free 1 800 387.0735 cpaontario.ca Professional Corporation Application for Certificate of Authorization

PRODUCER AGREEMENT PACKAGE

PRODUCER AGREEMENT PACKAGE Thank you for your interest in writing business with Evolution Insurance Brokers, LC ( EIB ). Attached is a copy of our Independent Producer s Agreement ( Agreement ), which

PRODUCER AGREEMENT PACKAGE Thank you for your interest in writing business with Evolution Insurance Brokers, LC ( EIB ). Attached is a copy of our Independent Producer s Agreement ( Agreement ), which

CANADIAN INTERNATIONAL TRADE TRIBUNAL. Appeals NOTICE OF APPEAL

Canadian International Trade Tribunal Tribunal canadien du commerce extérieur CANADIAN INTERNATIONAL TRADE TRIBUNAL Appeals NOTICE OF APPEAL TABLE OF CONTENTS NOTICE OF APPEAL... 1 APPELLANT IDENTIFICATION...

Canadian International Trade Tribunal Tribunal canadien du commerce extérieur CANADIAN INTERNATIONAL TRADE TRIBUNAL Appeals NOTICE OF APPEAL TABLE OF CONTENTS NOTICE OF APPEAL... 1 APPELLANT IDENTIFICATION...

Agreement for Setting up Margin Transaction Account

Revenue Stamp Agreement for Setting up Margin Transaction Account I/We hereby acknowledge that I/we have received and fully understood the explanation provided by your company regarding the margin transaction

Revenue Stamp Agreement for Setting up Margin Transaction Account I/We hereby acknowledge that I/we have received and fully understood the explanation provided by your company regarding the margin transaction

Articles of Association BANGKOK AVIATION FUEL SERVICES PUBLIC COMPANY LIMITED. Chapter 1 : General Provisions

(TRANSLATION) Articles of Association BANGKOK AVIATION FUEL SERVICES PUBLIC COMPANY LIMITED Chapter 1 : General Provisions Article 1. These Articles shall be called Articles of Association of Bangkok Aviation

(TRANSLATION) Articles of Association BANGKOK AVIATION FUEL SERVICES PUBLIC COMPANY LIMITED Chapter 1 : General Provisions Article 1. These Articles shall be called Articles of Association of Bangkok Aviation

ACCREDITATION COMMISSION FOR CONFORMITY ASSESSMENT BODIES. Schedule of ACCAB Fees Management System Certification Bodies

ACCREDITATION COMMISSION FOR CONFORMITY ASSESSMENT BODIES ACCREDITATION SCHEME MANUAL Document Title: Schedule of ACCAB Management System Certification Bodies Document Number: ACCAB-ASM-11.0-A-2 CONTROLLED

ACCREDITATION COMMISSION FOR CONFORMITY ASSESSMENT BODIES ACCREDITATION SCHEME MANUAL Document Title: Schedule of ACCAB Management System Certification Bodies Document Number: ACCAB-ASM-11.0-A-2 CONTROLLED

100TH GENERAL ASSEMBLY State of Illinois 2017 and 2018 HB0690

*LRB00000KTG00b* 0TH GENERAL ASSEMBLY State of Illinois 0 and 0 HB00 by Rep. Carol Ammons SYNOPSIS AS See Index INTRODUCED: Amends the Day and Temporary Labor Services Act. Requires a day and temporary

*LRB00000KTG00b* 0TH GENERAL ASSEMBLY State of Illinois 0 and 0 HB00 by Rep. Carol Ammons SYNOPSIS AS See Index INTRODUCED: Amends the Day and Temporary Labor Services Act. Requires a day and temporary

GUIDELINES TO OPENING ACCOUNTS CORPORATE DETAILS. Company/Trustee. Name. Corporate Address. RC No PERSONAL DETAILS. Name

A.R.M Securities Ltd (Member of the Nigerian Stock Exchange) 1/5 Mekunwen Rd, Ikoyi Lagos T: +234 (1) 4622736/8, 2701653/4, 8990740 ACCOUNT OPENING FORM Please tick to indicate preference Investor Type:

A.R.M Securities Ltd (Member of the Nigerian Stock Exchange) 1/5 Mekunwen Rd, Ikoyi Lagos T: +234 (1) 4622736/8, 2701653/4, 8990740 ACCOUNT OPENING FORM Please tick to indicate preference Investor Type:

New Business Checklist Form MM0200 (03/2004)

") New Business Checklist Form MM0200 (03/2004) This form should be completed when opening an account and on completion it should be submitted to the Manager, for approval, prior to the acceptance of the

New Business Checklist Form MM0200 (03/2004) This form should be completed when opening an account and on completion it should be submitted to the Manager, for approval, prior to the acceptance of the

7,1980s Public Disclosure Authorized MEMORANDUM OF AGREEMENT. between INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT. and

Public Disclosure Authorized LOAN NUMBER 1878 PAN MEMORANDUM OF AGREEMENT Public Disclosure Authorized (Colon Urban Development Project) between INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT Public

Public Disclosure Authorized LOAN NUMBER 1878 PAN MEMORANDUM OF AGREEMENT Public Disclosure Authorized (Colon Urban Development Project) between INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT Public