New England Mortgage Bankers Conference September 18, Providing Greater Purchase Certainty

|

|

|

- Beverley Barber

- 6 years ago

- Views:

Transcription

1 New England Mortgage Bankers Conference September 18, 2013 Providing Greater Purchase Certainty Kathy Caswell CMB Account Manager Rob Diehl- Product Development Angela Hsia- Customer Education Amy Morris Strategic Offering 1

2 Introduction What value would you find in having a tool that would assist you in determining that an individual mortgage meets Freddie Mac purchase requirements prior to loan delivery? 2

3 Providing Greater Purchase Certainty Making it easier for you to do business in today s housing market Tools: Loan Prospector, LQA, Uniform Collateral Data Portal 3

4 What you can expect from us Greater certainty to enable better business > A suite of new and enhanced tools and resources to support you throughout the entire loan manufacturing process > Increased transparency into our view of risk and QC file review strategies, findings, and trends > Confidence from knowing the loans you sell to Freddie Mac meet our purchase requirements Comprehensive support to help you manage your business > Continuing to work together to support your success under the new representation and warranty framework > Guidance to help you implement market and regulatory changes > Customer education resources > A laser focus on delivering results and providing you with the best possible customer experience 4

5 Greater Purchase Certainty Initiative Data Standards Freddie Mac Suite of Tools Uniform Loan Delivery Data Set Data elements required at loan delivery for Freddie Mac loans. Uniform Appraisal Data Set Standardizes definitions and includes all required fields for an appraisal submission. Uniform Closing Data Set Future Uniform Loan Application Data Set / AUS Future upgrade Third Party Data Verification Pre-Purchase Loan Prospector Assists lenders in manufacturing Freddie Mac eligible loans (credit and capacity). Home Value Explorer Provides collateral valuation for residential properties and insight during appraisal review into potentially inflated appraised values. UCDP Provides an early view into appraisal quality and any potential collateral risk. Loan Quality Advisor SM Validates for lenders that a Freddie Mac eligible loan was manufactured and is ready for delivery. At Purchase Selling System Prices and purchases loans from lenders based on agreed to terms. Data Validation Post-Purchase Quality Control Information Manager Secure web-based reporting system for Freddie Mac and our customers to share performing and nonperforming loan data and better manage repurchase and remedy requests. Loan Coverage Insight New online application that will serve as a single source for credit risk sharing information. Greater Purchase Certainty Comprehensive Support Data Quality Credit Quality Collateral Value/Quality Product Eligibility Risk Requirements 5

6 Our tools are designed to support your business Freddie Mac s suite of risk and eligibility assessment tools support you throughout the entire loan manufacturing process. These tools are how you get transparency into and clarity around our purchase eligibility requirements and, ultimately, the confidence that comes from greater purchase certainty. Plus, we re enhancing our current technology and adding new tools. We also offer training and other support resources to ensure successful adoption and usage Milestones Introduction of Loan Quality Advisor, our newest web-based risk and eligibility assessment tool designed to be easily adopted into your business processes. Enhanced Loan Prospector to provide you with clearer, more detailed feedback on our eligibility requirements and underwriting rules. Updated UCDP to implement Freddie Mac proprietary appraisal quality edits to provide an early view of possible appraisal issues. 6

ULDD File (MISMO 3.")

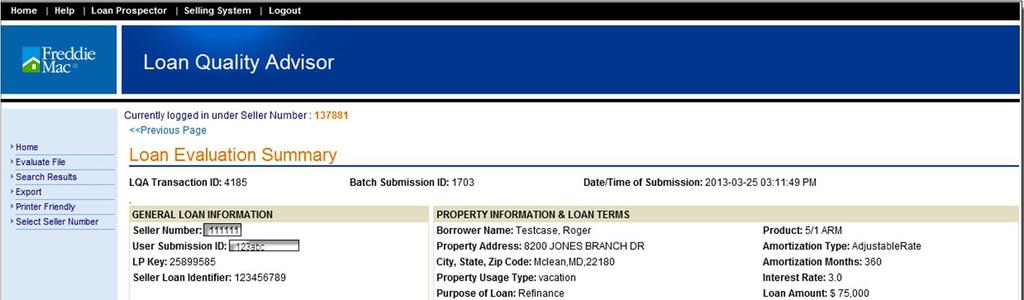

7 Loan Quality Advisor Services Customer Business Processes POS Processing Underwriting Closing Post-Closing QC Secondary Marketing Loan Delivery Loan Quality Advisor (web-based tool) ULDD File (MISMO 3.0) ULDD Appendix D file, or Create an LQA-specific ULDD data file 1 Loan Prospector loans Non-Loan Prospector loans and and Services Loan Prospector Data Compare Purchase Eligibility 2 Risk Assessment Loan Prospector LQA 1 Refer to LQA Implementation Guide ULDD* file *Uniform Loan Delivery Dataset 2 Future capability Wholesale Correspondent Retail 7

8 Loan Quality Advisor: Benefits LP Data Compare Risk Assessment Provides a comparison view of current loan data submitted to LQA against loan data used in the last Loan Prospector submission Identifies data discrepancies prior to loan delivery so that you can take action to ensure the accuracy of the loan s data and the corresponding Loan Prospector result Provides a summary of Freddie Mac s view of credit risk for loans not originated using Loan Prospector Indicates the likelihood of an LP Accept or LP Caution recommendation if the loan had been submitted to Loan Prospector Helps maintain the loan s LP Accept risk class so that any representation provided by the use of Loan Prospector can remain valid at loan purchase 8

9 Loan Quality Advisor: Services Loan Prospector Data Compare Service 9

Performs a format check on the file Evaluates the file Loan Prospector Data Compare Result Indicator: Green/Yellow/Red (or) Risk Assessment Result Indicator: Green/Yellow and, Purchase")

10 Loan Quality Advisor: Functionality The Process Upload a ULDD batch file containing one or multiple loan data files» Must be an acceptable file extension (.xml or.zip) Performs a format check on the file Evaluates the file Loan Prospector Data Compare Result Indicator: Green/Yellow/Red (or) Risk Assessment Result Indicator: Green/Yellow and, Purchase Eligibility A future capability 10

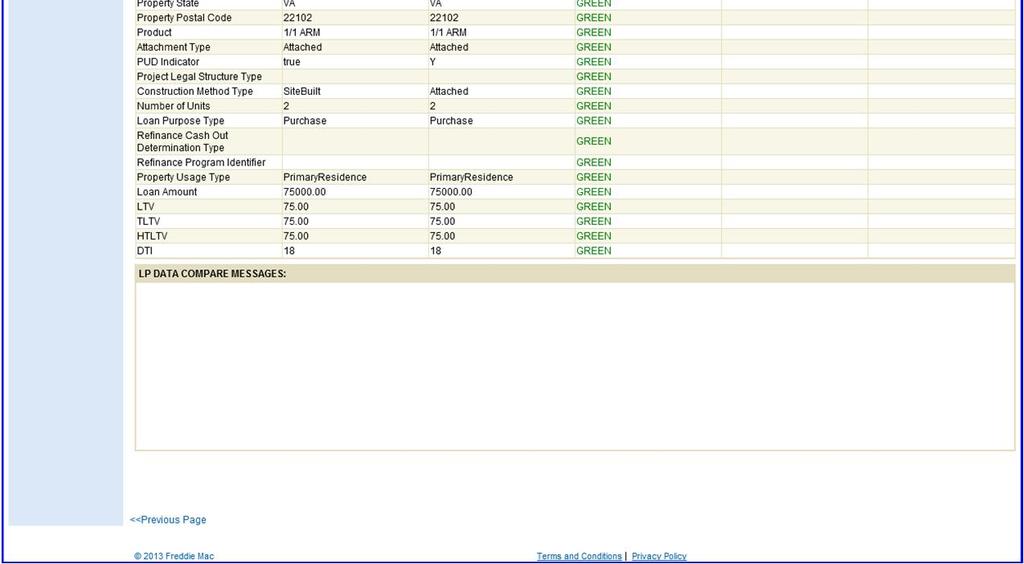

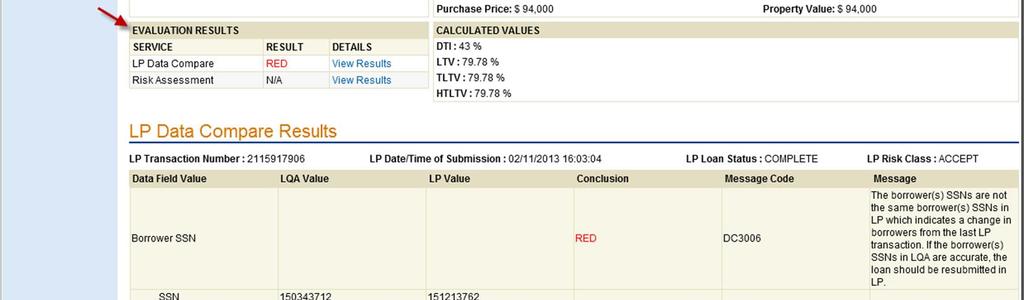

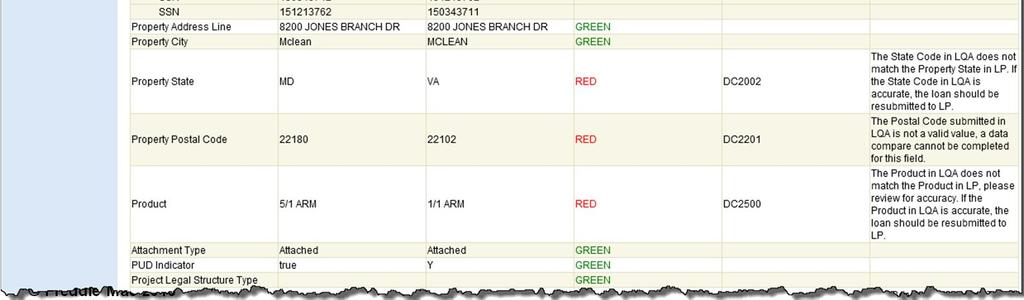

11 LQA Integration: Evaluation Results LP Data Compare Service Green The data submitted to LQA matches the data in the last Loan Prospector transaction Yellow The data submitted to LQA does not match the data in the last complete Loan Prospector transaction, however, any differences are within allowed tolerances* Red The data submitted to LQA does not match the data in the last Loan Prospector transaction. The differences indicate a resubmission to Loan Prospector may be warranted* No Seller action is necessary on this loan file You should perform a review of the data to ensure the data in the last Loan Prospector transaction still represents the current loan data* You should perform a review of the data to ensure the data in the last Loan Prospector transaction still represents the current loan data* 11 Color designations associated with LP Data Compare results are intended only as a visual guide for indicating the necessity (if any) for an LQA user to review the loan data for errors or inconsistencies. Such designations are not provided for any other reason, nor should they be used or relied upon except for purposes of triggering data file reviews as set forth in LQA, any LQA output, the User Guide or related documentation. *Refer to Seller/Servicer Guide Section If the current loan data does not match the data in Loan Prospector, you should resubmit to Loan Prospector to ensure the loan data supports the findings previously generated by Loan Prospector*

12 Loan Quality Advisor: Services Risk Assessment Provides a summary of Freddie Mac s view of credit risk for loans not originated using Loan Prospector 12

13 LQA Integration: Evaluation Results Risk Assessment Service Likelihood of an Accept Green Risk Assessment Results or Likelihood of a Caution Yellow 13 Color designations associated with Risk Assessment results are intended only as a visual guide for indicating the likelihood of the risk class associated with a data file. Such designations are not provided for any other reason, nor should they be used or relied upon except to identify the results of the risk assessment as set forth in LQA, any LQA output, the User Guide or related documentation.

14 Functionality: Batch File Results LQA Services: Loan Prospector Data Compare, or Risk Assessment 14

15 Evaluation Results: Loan Evaluation Summary-Green 15

16 Evaluation Results: Loan Evaluation Summary- Red 16

17 Origination Process(es) POS Processing Underwriting Closing Post-Closing QC Secondary Marketing Loan Delivery Retail POS Processing Underwriting Closing Post-Closing QC Secondary Marketing Loan Delivery Broker Wholesale POS Processing Underwriting Closing Post-Closing QC Secondary Marketing Loan Delivery Correspondent Aggregator 17

file format Leverages the same single-loan or multi-loan batch file")

18 Recap: Functionality/Evaluation Results Accepts a Uniform Loan Delivery Data (ULDD) file format Leverages the same single-loan or multi-loan batch file upload approach for submissions as used in the selling system Allows the user to view both batch-level and loan-level results Provides the ability to sort batch results to easily identify critical issues based on red, yellow and green indicators, as applicable Allows users to easily export results to the desktop 18

19 Next Steps Assess System impacts the tool is a great support to our existing processes Process Process/Policy impacts Best practices Plan Implementation target date easy to understand LP Data Compare Results 19

20 Resources Loan Quality Advisor website 20

21 Consumer Financial Protection Bureau Updates 21

22 Loan Prospector News We re enhancing Loan Prospector Updated functionality to increase system efficiency February 2013 Enhancing purchase eligibility feedback messages July 2013 Enhancing underwriting messages 4 th Q 2013 with more enhancements to come 22

23 Loan Prospector July Release Summary Loan Prospector purchase restriction messages are more specific References to product or program have been updated with more granular information Improved feedback messages will provide additional transparency into Freddie Mac s requirements 50+ generic messages will be replaced with 250+ loan specific messages 23

24 Loan Prospector July Release Summary More specific information for the following: LTV, TLTV, & HTLTV for type of mortgage Home Possible, Super Conforming, Construction Conversion and Renovation Mortgages Primary Residences Investment Properties - Second Homes Manufactured Homes ARMs 24

25 Examples LTV messages 25

26 More examples Home Possible, Manufactured Homes, ARMs 26

27 Loan Prospector Underwriting Feedback Enhancements The changes to the income feedback messages include adding: More loan-specific, customized messages relevant to the income type. New messages with specific underwriting guidelines for income types and are not currently returned based on the loan data provided. Consistent message format that eliminates unnecessary information and includes key information to help underwrite to Freddie Mac requirements. 27

28 Loan Prospector Underwriting Feedback Enhancements Loan Specific Feedback Messages Currently, feedback messages relevant to each income type are returned on all loans. In the future the feedback messages will only be returned when that specific income type is provided on the loan Current Feedback Message Future Feedback Message If using alimony, child support or separate maintenance payments to qualify, obtain copy of signed court order documenting payor's obligation to Borrower for previous six months and evidence payor is obligated to make payments to Borrower for the next three years. File must contain proof of consistent receipt for total court ordered amount for most recent six months. Alimony or child support income for ~BORR name~ must be supported by copy of signed court order documenting payor s obligation for previous 6 months and evidence payor is obligated to make payments to Borrower for next 3 years. File must contain proof of consistent receipt of total court ordered amount for most recent 6 months. For child support, file must contain proof of ages of children to prove 3-year continuance. Consistent Feedback Messages All income feedback messages will be concise, easy-to-read, follow a consistent format for each message returned, and include key underwriting documentation requirements for each borrower. Current Feedback Message Future Feedback Messages (DOC-CV) Obtain most recent YTD paystub documenting 1 full month, W-2(s) from the most recent tax year, and a verbal VOE, using Form 90 or comparable form, dated no more than 10 Business Days prior to the Note Date or after the Note Date but prior to the Delivery Date; or, a written VOE for 12 full months and a verbal VOE dated no more than 10 Business Days prior to the Note Date or after the Note Date but prior to the Delivery Date for ~EmplBorr~. Employment/base income for ~Borrower name~ must be supported by a YTD paystub documenting at least 30 days of income and W-2(s) for the most recent tax year or a written VOE covering the most recent year. A verbal VOE for ~BORR name~ is required from each employer for which income is used to qualify. If a verbal VOE cannot be obtained, obtain a written VOE or third-party VOE. The VOE must be dated no more than 10 Business Days prior to the Note Date or after the Note Date but prior to the Delivery Date 28

29 Loan Prospector Full Feedback Certificate with New Feedback Messages 29

30 FreddieMac.com/singlefamily/news/2013/0430_greater_purchase.html FreddieMac.com/singlefamily/loanqualityadvisor.html 30

31 Resources visit the following web pages:» (access Loan Prospector for the latest information and updates)» (access the Learning Center for easy-toprint quick references, self-study materials and live training events)» (access a comprehensive list of resources for Sellers/Servicers)» (access the latest Freddie Mac single family announcements related to Loan Prospector) Call Customer Service: Sellers: 800-FREDDIE Brokers: 888-LPONWEB 31

Automated Collateral Evaluation

What is automated collateral evaluation? Freddie Mac s automated collateral evaluation provides Sellers with the option to waive the appraisal requirements for certain Product Mortgages. The tools within

What is automated collateral evaluation? Freddie Mac s automated collateral evaluation provides Sellers with the option to waive the appraisal requirements for certain Product Mortgages. The tools within

Loan Quality Advisor User Guide

Loan Quality Advisor User Guide December 2017 This document is not a replacement or substitute for the information found in the Single-Family Seller/Servicer Guide, and /or terms of your Master Agreement

Loan Quality Advisor User Guide December 2017 This document is not a replacement or substitute for the information found in the Single-Family Seller/Servicer Guide, and /or terms of your Master Agreement

Loan Prospector December 13 Release New and Updated Feedback Messages

Loan Prospector December 13 Release New and Updated Feedback Messages On December 13, we re updating Loan Prospector to align with previously announced underwriting and credit requirement changes. To help

Loan Prospector December 13 Release New and Updated Feedback Messages On December 13, we re updating Loan Prospector to align with previously announced underwriting and credit requirement changes. To help

Loan Collateral Advisor SM FAQs August 24, 2016

Loan Collateral Advisor SM FAQs August 24, 2016 These FAQs are intended to help you answer customer questions related to Loan Collateral Advisor SM. Q1: What is Loan Collateral Advisor? A: Loan Collateral

Loan Collateral Advisor SM FAQs August 24, 2016 These FAQs are intended to help you answer customer questions related to Loan Collateral Advisor SM. Q1: What is Loan Collateral Advisor? A: Loan Collateral

Understanding Loan Collateral Advisor Results

What is Loan Collateral Advisor? Loan Collateral Advisor, a component of Freddie Mac Loan Advisor Suite, is a web-based tool that analyzes appraisal reports submitted to the Uniform Collateral Data Portal

What is Loan Collateral Advisor? Loan Collateral Advisor, a component of Freddie Mac Loan Advisor Suite, is a web-based tool that analyzes appraisal reports submitted to the Uniform Collateral Data Portal

Collateral Representation and Warranty Relief with an Appraisal: Loan Product Advisor Information

Collateral Representation and Warranty Relief with an Appraisal: Loan Product Loan Product Advisor is our enhanced automated underwriting system that gives you access to Freddie Mac s credit requirements

Collateral Representation and Warranty Relief with an Appraisal: Loan Product Loan Product Advisor is our enhanced automated underwriting system that gives you access to Freddie Mac s credit requirements

Collateral Representation and Warranty Relief with an Appraisal: Loan Collateral Advisor Information

Collateral Representation and Warranty Relief with an Appraisal: Loan Loan Collateral Advisor is a web-based tool that analyzes appraisal reports and provides a view of appraisal quality and valuation

Collateral Representation and Warranty Relief with an Appraisal: Loan Loan Collateral Advisor is a web-based tool that analyzes appraisal reports and provides a view of appraisal quality and valuation

Understanding the Uniform Mortgage Data Program (UMDP) Updates

Updates") Understanding the Uniform Mortgage Data Program (UMDP) Updates Prepared for: NAFCU 2011 Fannie Mae 1 What is the Uniform Mortgage Data Program? Fannie Mae and Freddie Mac are working together to implement

Understanding the Uniform Mortgage Data Program (UMDP) Updates Prepared for: NAFCU 2011 Fannie Mae 1 What is the Uniform Mortgage Data Program? Fannie Mae and Freddie Mac are working together to implement

TO: Freddie Mac Servicers February 15,

TO: Freddie Mac Servicers February 15, 2017 2017-1 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Obtaining and evaluating tax transcripts Revisions to our requirements for obtaining and evaluating

TO: Freddie Mac Servicers February 15, 2017 2017-1 SUBJECT: SERVICING UPDATES This Guide Bulletin announces: Obtaining and evaluating tax transcripts Revisions to our requirements for obtaining and evaluating

Processing FHA TOTAL Mortgages

Introduction This reference contains information to help you process Federal Housing Administration (FHA) mortgages using Freddie Mac Loan Product Advisor SM, including information on data entry requirements,

Introduction This reference contains information to help you process Federal Housing Administration (FHA) mortgages using Freddie Mac Loan Product Advisor SM, including information on data entry requirements,

Automated Income Assessment (Employer Data) with Loan Product Advisor

with Loan Product Advisor") Automated Income Assessment (Employer Data) with Loan Product Advisor Introduction This reference is intended to assist you with using our automated income assessment (employer data) offering, a part of

Automated Income Assessment (Employer Data) with Loan Product Advisor Introduction This reference is intended to assist you with using our automated income assessment (employer data) offering, a part of

Bulletin NUMBER: TO: Freddie Mac Sellers November 15, 2011

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Freddie Mac Revises Miscellaneous Eligibility and Property Requirements

Freddie Mac Revises Miscellaneous Eligibility and Property Requirements By Anna DeSimone, President October 15, 2014 On October 15, 2014, Freddie Mac issued Bulletin 2014-18: Selling Updates. This Single-Family

Freddie Mac Revises Miscellaneous Eligibility and Property Requirements By Anna DeSimone, President October 15, 2014 On October 15, 2014, Freddie Mac issued Bulletin 2014-18: Selling Updates. This Single-Family

Frequently Asked Questions

Frequently Asked Questions About the Uniform Closing Dataset (UCD) Requirement 1. What is UCD? Is it a form? Is it a regulation? Effective September 25, 2017, the Federal Housing Finance Agency (FHFA)

Frequently Asked Questions About the Uniform Closing Dataset (UCD) Requirement 1. What is UCD? Is it a form? Is it a regulation? Effective September 25, 2017, the Federal Housing Finance Agency (FHFA)

Loan Selling Advisor Tips for Resolving Delivery Edits

Loan Selling Advisor Tips for Resolving Delivery Edits When a loan is evaluated, Loan Selling Advisor SM returns error messages (also known as loan or purchase edits) to notify the user that the data entered

Loan Selling Advisor Tips for Resolving Delivery Edits When a loan is evaluated, Loan Selling Advisor SM returns error messages (also known as loan or purchase edits) to notify the user that the data entered

Loan Prospector Documentation Matrix

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Loan Quality Initiative (LQI) FAQs Updated July 29, 2010

FAQs Updated July 29, 2010") Loan Quality Initiative (LQI) FAQs Updated July 29, 2010 These FAQs provide additional information related to Lender Letter LL-2010-03, An Introduction to Fannie Mae s Loan Quality Initiative, Announcements

Loan Quality Initiative (LQI) FAQs Updated July 29, 2010 These FAQs provide additional information related to Lender Letter LL-2010-03, An Introduction to Fannie Mae s Loan Quality Initiative, Announcements

Industry Letter. To: Freddie Mac Sellers and Servicers October 19, Page 1

Industry Letter To: Freddie Mac Sellers and Servicers October 19, 2012 SUBJECT: QUALITY CONTROL AND ENFORCEMENT PRACTICES On September 11, 2012, Freddie Mac issued Single-Family Seller/Servicer Guide (

Industry Letter To: Freddie Mac Sellers and Servicers October 19, 2012 SUBJECT: QUALITY CONTROL AND ENFORCEMENT PRACTICES On September 11, 2012, Freddie Mac issued Single-Family Seller/Servicer Guide (

Loan Product Advisor SM Documentation Matrix

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

Bulletin NUMBER: TO: Freddie Mac Sellers and Servicers August 16, 2011

Bulletin NUMBER: 2011-15 TO: Freddie Mac Sellers and Servicers August 16, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are: Quality control Revising Guide Chapter

Bulletin NUMBER: 2011-15 TO: Freddie Mac Sellers and Servicers August 16, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are: Quality control Revising Guide Chapter

Assigning and Releasing Loans in Loan Product Advisor

Assigning and Releasing Loans in Loan Product Advisor This job aid provides information to help you assign and release loans in Loan Product Advisor through Loan Advisor Suite. Originating brokers or sellers

Assigning and Releasing Loans in Loan Product Advisor This job aid provides information to help you assign and release loans in Loan Product Advisor through Loan Advisor Suite. Originating brokers or sellers

At-A-Glance Loan Product Advisor Enhancements

July 2016 Release Interface changes, version 4.3.00, usability enhancements and evolution to Loan Product Advisor Number of Messages Impacted: 1 New Purchase Restriction; 13 New Underwriting; 69 Messages

July 2016 Release Interface changes, version 4.3.00, usability enhancements and evolution to Loan Product Advisor Number of Messages Impacted: 1 New Purchase Restriction; 13 New Underwriting; 69 Messages

TO: Freddie Mac Sellers October 31,

TO: Freddie Mac Sellers October 31, 2018 2018-19 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Origination and underwriting Updates to our rental income requirements March 1, 2019 Updates to

TO: Freddie Mac Sellers October 31, 2018 2018-19 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Origination and underwriting Updates to our rental income requirements March 1, 2019 Updates to

Loan Prospector Documentation Matrix

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Bulletin NUMBER: TO: Freddie Mac Sellers and Servicers May 25, 2011

Bulletin NUMBER: 2011-10 TO: Freddie Mac Sellers and Servicers May 25, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are updating certain selling requirements. We are

Bulletin NUMBER: 2011-10 TO: Freddie Mac Sellers and Servicers May 25, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are updating certain selling requirements. We are

Fannie Mae Technology Solutions Certainty. Efficiency. Opportunity.

Fannie Mae Technology Solutions Certainty. Efficiency. Opportunity. Rosemary Maieron Norwood Note: This group meeting is intended to discuss general mortgage and housing industry challenges facing Fannie

Fannie Mae Technology Solutions Certainty. Efficiency. Opportunity. Rosemary Maieron Norwood Note: This group meeting is intended to discuss general mortgage and housing industry challenges facing Fannie

Ordering Merged Credit (Loan Product Advisor Systemto-System

Ordering Merged Credit (Loan Product Advisor Systemto-System Access) Loan Product Advisor SM will obtain infile credit reports unless you request a merged credit report (with or without a Reference Number.

Ordering Merged Credit (Loan Product Advisor Systemto-System Access) Loan Product Advisor SM will obtain infile credit reports unless you request a merged credit report (with or without a Reference Number.

Section 1.04 Automated Underwriting

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated Approve or Accept...

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated Approve or Accept...

TO: All Freddie Mac Sellers and Servicers March 4, 2009

Bulletin NUMBER: 2009-5 TO: All Freddie Mac Sellers and Servicers March 4, 2009 SUBJECTS In support of the federal Making Home Affordable Program announced today, with this Single-Family Seller/Servicer

Bulletin NUMBER: 2009-5 TO: All Freddie Mac Sellers and Servicers March 4, 2009 SUBJECTS In support of the federal Making Home Affordable Program announced today, with this Single-Family Seller/Servicer

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017 Freedom from reps & warrants plus greater speed and simplicity for Fannie Mae s lender partners DU Validation

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017 Freedom from reps & warrants plus greater speed and simplicity for Fannie Mae s lender partners DU Validation

TO: Freddie Mac Sellers April 9,

TO: Freddie Mac Sellers April 9, 2015 2015-4 SUBJECT: SELLING UPDATES This Single-Family Seller/Servicer Guide ( Guide ) Bulletin announces: Credit underwriting Changes to requirements for Mortgages with

TO: Freddie Mac Sellers April 9, 2015 2015-4 SUBJECT: SELLING UPDATES This Single-Family Seller/Servicer Guide ( Guide ) Bulletin announces: Credit underwriting Changes to requirements for Mortgages with

Exhibit 19 Credit Fees in Price

Exhibit 19 Credit Fees in Price 1. Credit Fees in Price for Mortgages with Special Attributes This Credit Fee in Price Matrix sets forth the Credit Fee in Price amounts and/or Credit Fee in Price rates

Exhibit 19 Credit Fees in Price 1. Credit Fees in Price for Mortgages with Special Attributes This Credit Fee in Price Matrix sets forth the Credit Fee in Price amounts and/or Credit Fee in Price rates

Section 1.04 Automated Underwriting

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 General... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated

Section 1.04 Automated Underwriting In This Section This section contains the following topics. Overview... 2 General... 2 Related Bulletins... 2 AUS Guidelines... 3 Implementation... 3 Loans Not Rated

Using Home Value Explorer (HVE) via Loan Product Advisor for Relief Refinance Mortgages

via Loan Product Advisor for Relief Refinance Mortgages") 0 Using Home Value Explorer (HVE) via Loan Product Advisor for Relief Refinance Seller/Servicers may determine the value of the Mortgaged Premises for certain Freddie Mac Relief Refinance SM using a point

0 Using Home Value Explorer (HVE) via Loan Product Advisor for Relief Refinance Seller/Servicers may determine the value of the Mortgaged Premises for certain Freddie Mac Relief Refinance SM using a point

Using Loan Product Advisor SM Merged Credit Report Options

Using Loan Product Advisor SM Merged Credit Report Options Loan Product Advisor will obtain infile credit reports unless you request a merged credit report (with or without a Reference Number). This document

Using Loan Product Advisor SM Merged Credit Report Options Loan Product Advisor will obtain infile credit reports unless you request a merged credit report (with or without a Reference Number). This document

Construction Conversion and Renovation Mortgages

Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation Mortgages, refer to Freddie Mac s

Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation Mortgages, refer to Freddie Mac s

Loan Product Advisor Documentation Matrix

Effective for Mortgages with Settlement Dates on and after November 30, 2018, but Sellers may implement the changes in their entirety immediately Use the following information as a reference for documenting

Effective for Mortgages with Settlement Dates on and after November 30, 2018, but Sellers may implement the changes in their entirety immediately Use the following information as a reference for documenting

Freddie Mac Single-Family Seller/Servicer Guide Bulletin /29/2016 Page E19-1

1. Postsettlement Delivery Fees ( delivery fees ) for Mortgages with Special Attributes This Delivery Fee Matrix sets forth the delivery fee amounts and/or delivery fee rates and credits applicable to

1. Postsettlement Delivery Fees ( delivery fees ) for Mortgages with Special Attributes This Delivery Fee Matrix sets forth the delivery fee amounts and/or delivery fee rates and credits applicable to

Selling Guide Lender Letter LL

Selling Guide Lender Letter LL-2012-07 To: All Fannie Mae Single-Family Sellers and Servicers Fannie Mae s Quality Control Process Additional Information October 19, 2012 On September 11, 2012, Fannie

Selling Guide Lender Letter LL-2012-07 To: All Fannie Mae Single-Family Sellers and Servicers Fannie Mae s Quality Control Process Additional Information October 19, 2012 On September 11, 2012, Fannie

Loan Product Advisor SM Documentation Matrix

Effective for Mortgages with Freddie Mac Settlement Dates on or after July 6, 2017; but Sellers may implement for Mortgages with Settlement Dates on or after March 6, 2017 Use the following information

Effective for Mortgages with Freddie Mac Settlement Dates on or after July 6, 2017; but Sellers may implement for Mortgages with Settlement Dates on or after March 6, 2017 Use the following information

SUBJECT: SELLING UPDATES

TO: Freddie Mac Sellers August 29, 2018 2018-13 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Home Possible Enhanced credit flexibilities and simplified Home Possible Mortgage requirements through

TO: Freddie Mac Sellers August 29, 2018 2018-13 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Home Possible Enhanced credit flexibilities and simplified Home Possible Mortgage requirements through

Second Home and Investment Properties Messages - March 16, 2017

Updated s LPR 2E Each Borrower individually and all Borrowers Each borrower individually and all borrowers collectively must collectively must not own and/or be obligated on not be obligated on more than

Updated s LPR 2E Each Borrower individually and all Borrowers Each borrower individually and all borrowers collectively must collectively must not own and/or be obligated on not be obligated on more than

UPDATES RELATED TO ELIGIBLE DISASTER AREAS IMPACTED BY RECENT DISASTERS

TO: Freddie Mac Sellers February 28, 2018 2018-3 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Updates related to Eligible Disaster Areas impacted by recent disasters Updates concerning automated

TO: Freddie Mac Sellers February 28, 2018 2018-3 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Updates related to Eligible Disaster Areas impacted by recent disasters Updates concerning automated

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

Uniform Appraisal Dataset (UAD) Overview February 18, 2011

Overview February 18, 2011") Uniform Appraisal Dataset (UAD) Overview February 18, 2011 To improve the quality and consistency of appraisal data on loans delivered to the government-sponsored enterprises (GSEs), Fannie Mae and Freddie

Uniform Appraisal Dataset (UAD) Overview February 18, 2011 To improve the quality and consistency of appraisal data on loans delivered to the government-sponsored enterprises (GSEs), Fannie Mae and Freddie

Exhibit B: Guide Chapter K33 Mortgages for Newly Constructed Homes

Exhibit B: Guide Chapter K33 for Newly Constructed Homes K33.1: Overview This chapter details the requirements for the three types of for Newly Constructed Homes: Newly Built Home Conversion Renovation

Exhibit B: Guide Chapter K33 for Newly Constructed Homes K33.1: Overview This chapter details the requirements for the three types of for Newly Constructed Homes: Newly Built Home Conversion Renovation

Loan Product Advisor Documentation Matrix

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

TEMPORARY SELLING REQUIREMENTS FOR PROPERTIES IMPACTED BY THE CALIFORNIA WILDFIRES

TO: Freddie Mac Sellers December 6, 2018 2018-25 SUBJECT: TEMPORARY SELLING REQUIREMENTS RELATED TO CALIFORNIA WILDFIRES AND UPDATES TO ELIGIBILITY FOR PROPERTIES IMPACTED BY HURRICANE IRMA Freddie Mac

TO: Freddie Mac Sellers December 6, 2018 2018-25 SUBJECT: TEMPORARY SELLING REQUIREMENTS RELATED TO CALIFORNIA WILDFIRES AND UPDATES TO ELIGIBILITY FOR PROPERTIES IMPACTED BY HURRICANE IRMA Freddie Mac

DEFINING RESPONSIBLE LENDING WITH CHANGES TO LENDER GIFT AND GRANT REQUIREMENTS

TO: Freddie Mac Sellers July 6, 2017 DEFINING RESPONSIBLE LENDING WITH CHANGES TO LENDER GIFT AND GRANT REQUIREMENTS Freddie Mac remains committed to working with our customers, and the industry, to provide

TO: Freddie Mac Sellers July 6, 2017 DEFINING RESPONSIBLE LENDING WITH CHANGES TO LENDER GIFT AND GRANT REQUIREMENTS Freddie Mac remains committed to working with our customers, and the industry, to provide

Leveraging Data to Drive a Fully Digital Mortgage Process March 2017

Leveraging Data to Drive a Fully Digital Mortgage Process March 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 Objective: Describe how Fannie Mae is leveraging Data in the industry Discuss Day1 Certainty

Leveraging Data to Drive a Fully Digital Mortgage Process March 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 Objective: Describe how Fannie Mae is leveraging Data in the industry Discuss Day1 Certainty

Both Selling and Servicing requirements are amended in this Bulletin.

Bulletin NUMBER: 2006-1 TO: All Freddie Mac Sellers and Servicers February 17, 2006 SUBJECTS Both Selling and Servicing requirements are amended in this Bulletin. We are: Increasing the maximum LTV/TLTV/HTLTV

Bulletin NUMBER: 2006-1 TO: All Freddie Mac Sellers and Servicers February 17, 2006 SUBJECTS Both Selling and Servicing requirements are amended in this Bulletin. We are: Increasing the maximum LTV/TLTV/HTLTV

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

Uniform Collateral Data Portal Reference Series for the Lender Admin: 4 - Managing Lender Agents

Uniform Collateral Data Portal Reference Series for the Lender Admin: 4 - Managing Lender Agents This reference is the fourth in a series of four references for the Lender Administrator, a Uniform Collateral

Uniform Collateral Data Portal Reference Series for the Lender Admin: 4 - Managing Lender Agents This reference is the fourth in a series of four references for the Lender Administrator, a Uniform Collateral

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

Uniform Loan Delivery Dataset (ULDD) FAQs

FAQs") Uniform Loan Delivery Dataset (ULDD) FAQs Updated November 7, 2017 This document provides answers to questions frequently asked about the Uniform Loan Delivery Dataset (ULDD), which provides common requirements

Uniform Loan Delivery Dataset (ULDD) FAQs Updated November 7, 2017 This document provides answers to questions frequently asked about the Uniform Loan Delivery Dataset (ULDD), which provides common requirements

Construction Conversion and Renovation Mortgages

Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation Mortgages, refer to Freddie Mac s

Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation Mortgages, refer to Freddie Mac s

TO: Freddie Mac Sellers and Servicers November 15,

TO: Freddie Mac Sellers and Servicers November 15, 2013 2013-23 SUBJECTS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin updates and revises our selling and Servicing requirements, including:

TO: Freddie Mac Sellers and Servicers November 15, 2013 2013-23 SUBJECTS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin updates and revises our selling and Servicing requirements, including:

Freddie Mac LP Open Access (Relief Refinance Mortgages) (CF30OAFR & CF15OAFR)

(CF30OAFR & CF15OAFR)") Table of Contents 1. Eligible Transactions...2 2. Ineligible Transactions...2 3. Eligible Borrowers...3 4. Borrower Benefit...3 5. Underwriting Method...3 6. Credit (Derogatory)...4 7. LTV/TLTV...4 8.

Table of Contents 1. Eligible Transactions...2 2. Ineligible Transactions...2 3. Eligible Borrowers...3 4. Borrower Benefit...3 5. Underwriting Method...3 6. Credit (Derogatory)...4 7. LTV/TLTV...4 8.

Section DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Announcement March 5, Updates and Clarifications for Streamlined Refinance Products

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Announcement 08-03 March 5, 2008 Amends these Guides: Selling Updates and Clarifications for Streamlined Refinance Products With this Announcement, Fannie is updating the eligibility guidelines for its

Chapter 23: Maximum Loan Amounts and LTV, TLTV and HTLTV Ratios

May 2, 2008 Guide Bulletin Chapter 23: Maximum Loan Amounts and LTV, TLTV and HTLTV Ratios 23.5: Maximum financing (05/02/08) Financing to the maximum loan-to value (LTV) ratio, as set forth in Section

May 2, 2008 Guide Bulletin Chapter 23: Maximum Loan Amounts and LTV, TLTV and HTLTV Ratios 23.5: Maximum financing (05/02/08) Financing to the maximum loan-to value (LTV) ratio, as set forth in Section

SUBJECT: SUBSEQUENT TRANSFERS OF SERVICING AND INTRA-SERVICER PORTFOLIO MOVES

TO: Freddie Mac Servicers July 6, 2018 2018-11 SUBJECT: SUBSEQUENT TRANSFERS OF SERVICING AND INTRA-SERVICER PORTFOLIO MOVES In Guide Bulletin 2018-6, we announced the automation of the following via the

TO: Freddie Mac Servicers July 6, 2018 2018-11 SUBJECT: SUBSEQUENT TRANSFERS OF SERVICING AND INTRA-SERVICER PORTFOLIO MOVES In Guide Bulletin 2018-6, we announced the automation of the following via the

Bulletin NUMBER: TO: All Freddie Mac Sellers and Servicers April 16, 2009

Bulletin NUMBER: 2009-9 TO: All Freddie Mac Sellers and Servicers April 16, 2009 SUBJECTS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin provides complete requirements regarding the increased

Bulletin NUMBER: 2009-9 TO: All Freddie Mac Sellers and Servicers April 16, 2009 SUBJECTS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin provides complete requirements regarding the increased

INCREASES TO THE LTV/TLTV/HTLTV RATIOS FOR PURCHASE AND NO CASH-OUT REFINANCE MORTGAGES SECURED BY SECOND HOMES AND 2-UNIT PRIMARY RESIDENCES

TO: Freddie Mac Sellers March 28, 2018 2018-5 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Increases to the LTV/TLTV/HTLTV ratios for purchase and no-cash-out refinance Mortgages secured by

TO: Freddie Mac Sellers March 28, 2018 2018-5 SUBJECT: SELLING UPDATES This Guide Bulletin announces: Increases to the LTV/TLTV/HTLTV ratios for purchase and no-cash-out refinance Mortgages secured by

Bulletin SUBJECTS NUMBER: TO: All Freddie Mac Sellers and Servicers October 14, 2005

Bulletin NUMBER: 2005-5 TO: All Freddie Mac Sellers and Servicers October 14, 2005 SUBJECTS Both Selling and Servicing requirements are amended in this Bulletin. We are: Introducing the Property Inspection

Bulletin NUMBER: 2005-5 TO: All Freddie Mac Sellers and Servicers October 14, 2005 SUBJECTS Both Selling and Servicing requirements are amended in this Bulletin. We are: Introducing the Property Inspection

Bulletin. TO: All Freddie Mac Sellers and Servicers October 17, 2008

Bulletin TO: All Freddie Mac Sellers and Servicers October 17, 2008 SUBJECTS Selling requirements are amended in this Single-Family Seller/Servicer Guide (Guide) Bulletin. This Bulletin provides final

Bulletin TO: All Freddie Mac Sellers and Servicers October 17, 2008 SUBJECTS Selling requirements are amended in this Single-Family Seller/Servicer Guide (Guide) Bulletin. This Bulletin provides final

Understanding Loan Product Advisor s Determination of Total Monthly Debt for Conventional Loans

Understanding Loan Product Advisor s Determination of Total Monthly As indicated in Freddie Mac s Single-Family Seller/Servicer Guide (Guide) Section 5401.2, the Borrower's liabilities must be reflected

Understanding Loan Product Advisor s Determination of Total Monthly As indicated in Freddie Mac s Single-Family Seller/Servicer Guide (Guide) Section 5401.2, the Borrower's liabilities must be reflected

Understanding UCD and Freddie Mac Loan Closing Advisor

March 21, 2017 Understanding UCD and Freddie Mac Loan Closing Advisor Webinar Start: 11:00 a.m. PT (2:00 p.m. ET) Dial-In: (866) 492-9043 Conference Code: 1024245 Ask a Question Submit questions via the

March 21, 2017 Understanding UCD and Freddie Mac Loan Closing Advisor Webinar Start: 11:00 a.m. PT (2:00 p.m. ET) Dial-In: (866) 492-9043 Conference Code: 1024245 Ask a Question Submit questions via the

Uniform Collateral Data Portal Reference Series for the Lender Admin: 4 - Managing Lender Agents

Uniform Collateral Data Portal Reference Series for the Lender Admin: 4 - Managing Lender Agents This reference is the fourth in a series of five references for the Lender Administrator, a Uniform Collateral

Uniform Collateral Data Portal Reference Series for the Lender Admin: 4 - Managing Lender Agents This reference is the fourth in a series of five references for the Lender Administrator, a Uniform Collateral

Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents

![Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents](/thumbs/94/118687243.jpg "Mortgage Processing Policy Manual Table of Contents [Sample Client] Table of Contents") Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING...

Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING...

Summary of Agency Income Guideline Revisions

Summary of Agency Guideline Revisions General Update Comments: All LP (i.e., Loan Prospector) references were changed to LPA (i.e., Loan Product Advisor) For purposes of the revised LP income requirements:

Summary of Agency Guideline Revisions General Update Comments: All LP (i.e., Loan Prospector) references were changed to LPA (i.e., Loan Product Advisor) For purposes of the revised LP income requirements:

Automated Asset Assessment with Loan Product Advisor

Automated Asset Assessment with Loan Product Advisor Introduction This reference is intended to assist you with using our automated asset assessment offering and provide information to help you understand:

Automated Asset Assessment with Loan Product Advisor Introduction This reference is intended to assist you with using our automated asset assessment offering and provide information to help you understand:

Uniform Closing Data in Point Webinar Q&A

Uniform Closing Data in Point Webinar Q&A The following questions were asked during the Calyx Uniform Closing Data (UCD) in Point webinar. Calyx has provided responses to questions that are specific to

Uniform Closing Data in Point Webinar Q&A The following questions were asked during the Calyx Uniform Closing Data (UCD) in Point webinar. Calyx has provided responses to questions that are specific to

Freddie Mac Valuation Update

Freddie Mac Valuation Update CoreLogic Mortgage Fraud & Valuation Consortium November 3, 2016 Freddie Mac s Twin Goals A Better Freddie Mac and a better housing finance system For families, customers and

Freddie Mac Valuation Update CoreLogic Mortgage Fraud & Valuation Consortium November 3, 2016 Freddie Mac s Twin Goals A Better Freddie Mac and a better housing finance system For families, customers and

Agency Guideline Revisions Note: Underlined items indicate an overlay.

Alimony, Child Support, and Maintenance Payments Products Texas Cash-Out Refi Income Income may be used if received for a minimum of six months and must continue for at least three years after the date

Alimony, Child Support, and Maintenance Payments Products Texas Cash-Out Refi Income Income may be used if received for a minimum of six months and must continue for at least three years after the date

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

Avoiding Common Underwriting Errors

September 2015 2012 Genworth Financial, Inc. All rights reserved. Agenda General Underwriting Tips Resources and tools Capacity Credit History Capital Common Sense Compliance 1 Resources Job Aides, Tools

September 2015 2012 Genworth Financial, Inc. All rights reserved. Agenda General Underwriting Tips Resources and tools Capacity Credit History Capital Common Sense Compliance 1 Resources Job Aides, Tools

AUTOMATED UNDERWRITING, CONVENTIONAL

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

HomeReady vs. Home Possible Comparison

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Best Practices for Best Efforts Commitments

This job aid provides information on the following topics related to Best Efforts execution of a contract: Modify Best Effort Import... 1 Quick Loan Data... 4 Best Practices... 5 Exhibit 19 Calculator...

This job aid provides information on the following topics related to Best Efforts execution of a contract: Modify Best Effort Import... 1 Quick Loan Data... 4 Best Practices... 5 Exhibit 19 Calculator...

Fannie Mae DU Refi Plus ; Conforming High Balance Changes and New Appraisal Pricing

MSI Mortgage Services III, LLC Wholesale Partner Announcement At MSI Your Interest Is Our Priority! A Subsidiary of First State Bank Member FDIC Issue Date 5/07/09 Effective Date As Noted WPA 2009-020

MSI Mortgage Services III, LLC Wholesale Partner Announcement At MSI Your Interest Is Our Priority! A Subsidiary of First State Bank Member FDIC Issue Date 5/07/09 Effective Date As Noted WPA 2009-020

Home Possible and Home Possible Advantage

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Processing VA Mortgages

Introduction The Department of Veterans Affairs (VA) Freddie Mac allows Loan Product Advisor automated underwriting service to assess VA loan applications. The Department of Veterans Affairs then guarantees

Introduction The Department of Veterans Affairs (VA) Freddie Mac allows Loan Product Advisor automated underwriting service to assess VA loan applications. The Department of Veterans Affairs then guarantees

FHLMC Relief Refinance Open Access

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

Understanding Loan Product Advisor s Determination of Total Funds to be Verified

Understanding Loan Product Advisor s Determination of Total Funds to be Verified Loan Product Advisor uses the information submitted to help determine the amount of funds required from the borrower(s)

Understanding Loan Product Advisor s Determination of Total Funds to be Verified Loan Product Advisor uses the information submitted to help determine the amount of funds required from the borrower(s)

Avoiding Common Underwriting Errors

November 2016 2012 Genworth Financial, Inc. All rights reserved. Agenda Introduction General Underwriting Tips Resources Examining and Documenting Files Specific Errors and Recommendations Capacity, Credit

November 2016 2012 Genworth Financial, Inc. All rights reserved. Agenda Introduction General Underwriting Tips Resources Examining and Documenting Files Specific Errors and Recommendations Capacity, Credit

Correspondent XChange SM Functionality Manual. April 2019

SM Functionality Manual April 2019 Table of Contents Overview of SM... 2 Third Party Process Flow for the... 2 Originator Pipeline, Navigation and Functions... 2 Create and Access Loans in Loan Selling

SM Functionality Manual April 2019 Table of Contents Overview of SM... 2 Third Party Process Flow for the... 2 Originator Pipeline, Navigation and Functions... 2 Create and Access Loans in Loan Selling

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Underwriting Procedures

Underwriting Section 4 Underwriting Procedures ----------------------------------------------------------------- 4.2 Underwriting Turn-Around --------------------------------------------------------------

Underwriting Section 4 Underwriting Procedures ----------------------------------------------------------------- 4.2 Underwriting Turn-Around --------------------------------------------------------------

Doctor Loan Portfolio Plus

Overview Offered to our HVF Premier Partners. Contact your Account Executive to learn how to become eligible. Underwriting follows Freddie Mac Loan Product Advisor (LPA) findings unless specified differently

Overview Offered to our HVF Premier Partners. Contact your Account Executive to learn how to become eligible. Underwriting follows Freddie Mac Loan Product Advisor (LPA) findings unless specified differently

Mortgage and Real Estate Data Standards - MISMO. Ted Adams Information Technology July 15, 2010

Mortgage and Real Estate Data Standards - MISMO Ted Adams Information Technology July 15, 2010 Uniform Mortgage Data Program The Federal Housing Finance Agency (FHFA) announced that under its direction

Mortgage and Real Estate Data Standards - MISMO Ted Adams Information Technology July 15, 2010 Uniform Mortgage Data Program The Federal Housing Finance Agency (FHFA) announced that under its direction

SUBJECT: SELLING REPRESENTATION AND WARRANTY FRAMEWORK LIFE-OF- LOAN EXCLUSIONS EXCLUSIONS LIFE-OF-LOAN SELLING REPRESENTATIONS AND WARRANTIES

TO: Freddie Mac Sellers and Servicers November 20, 2014 2014-21 SUBJECT: SELLING REPRESENTATION AND WARRANTY FRAMEWORK LIFE-OF- LOAN EXCLUSIONS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin

TO: Freddie Mac Sellers and Servicers November 20, 2014 2014-21 SUBJECT: SELLING REPRESENTATION AND WARRANTY FRAMEWORK LIFE-OF- LOAN EXCLUSIONS This Single-Family Seller/Servicer Guide ( Guide ) Bulletin

Conventional Loan Program - Quick Reference Guide

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Collateral Representation and Warranty Relief with an Appraisal: Loan Coverage Advisor Information

Collateral Representation and Warranty Relief with an Appraisal: Loan Coverage Advisor establishes and tracks the representation and warranty relief dates for all loans sold to Freddie Mac. It provides

Collateral Representation and Warranty Relief with an Appraisal: Loan Coverage Advisor establishes and tracks the representation and warranty relief dates for all loans sold to Freddie Mac. It provides

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

Servicing Released Premium Adjustment Guide

Through the Freddie Mac Cash-Released XChange SM execution, formerly known as the Servicing Released Sales Process (SRSP), Sellers sell to Freddie Mac and concurrently transfer the mortgage servicing rights

Through the Freddie Mac Cash-Released XChange SM execution, formerly known as the Servicing Released Sales Process (SRSP), Sellers sell to Freddie Mac and concurrently transfer the mortgage servicing rights

Uniform Collateral Data Portal Reference Series for the Lender Admin: 5 - Managing Aggregator Profile

Uniform Collateral Data Portal Reference Series for the Lender Admin: 5 - Managing Aggregator Profile This reference is the fifth in a series of references for the Lender Administrator, a Uniform Collateral

Uniform Collateral Data Portal Reference Series for the Lender Admin: 5 - Managing Aggregator Profile This reference is the fifth in a series of references for the Lender Administrator, a Uniform Collateral

Enhanced Property Inspection Waiver Frequently Asked Questions

Enhanced Property Inspection Waiver Frequently Asked Questions Updated November 28, 2016 Property inspection waiver (PIW) is an offer to waive the appraisal for certain refinance transactions. PIW offers

Enhanced Property Inspection Waiver Frequently Asked Questions Updated November 28, 2016 Property inspection waiver (PIW) is an offer to waive the appraisal for certain refinance transactions. PIW offers

Correspondent Guidelines. Loan Program: 7/1 LIBOR ARM 5/2/5 Dollar Bank (1700) LTV Limits:

LTV Limits:") Loan Program: 7/1 LIBOR ARM 5/2/5 Dollar Bank (1700) LTV Limits: Occupancy Primary Residence Investment & Non-Owner PURCHASE AND LIMITED CASH-OUT REFINANCE MORTGAGES Property Type 1 Unit Max LTV Max TLTV

Loan Program: 7/1 LIBOR ARM 5/2/5 Dollar Bank (1700) LTV Limits: Occupancy Primary Residence Investment & Non-Owner PURCHASE AND LIMITED CASH-OUT REFINANCE MORTGAGES Property Type 1 Unit Max LTV Max TLTV

DU Validation Service

DU Validation Service Frequently Asked Questions Updated September 11, 2017 Fannie Mae s Desktop Underwriter (DU ) validation service is designed to provide customers with enhanced loan origination controls,

DU Validation Service Frequently Asked Questions Updated September 11, 2017 Fannie Mae s Desktop Underwriter (DU ) validation service is designed to provide customers with enhanced loan origination controls,