HMDA: Haven or Havoc. Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble

|

|

|

- Juniper Jeremy Porter

- 6 years ago

- Views:

Transcription

1 HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble

2 About the Speaker 2 Cindy Prince is a Senior Compliance Advisor with the Temenos Compliance Advisory team. Cindy brings over 25 years of banking experience to the team, which includes 14 years of experience as a Compliance Officer and Advisor. Her career has also focused on risk management, training and audit. Cindy also held the position of Internal Auditor for (7) years at a community bank. Cindy is a Certified Regulatory Compliance Manager (CRCM) and is also a NAFCU Certified Compliance Officer (NCCO). Cindy was recently invited to the CFPB headquarters in Washington where she attended a LIVE demonstration of the CFPB s new HMDA Platform.

.")

3 Assisting with the Presentation 3 Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance Advisory team. Her background is specialized in BSA/AML, HMDA, and deposit compliance. Rachelle graduated from Grand Valley State University with her Master of Science in Accounting. She is also a Certified Regulatory Compliance Manager (CRCM). Matt Goble is also a Senior Compliance Advisor for the Temenos Compliance Advisory team. Matt advises over 700 institutions on federal regulatory compliance, specializing in TRID, E-Sign and Loan Origination Compensation. Matt was formerly the Compliance Officer for a large community bank.

4 Agenda Day Three 4 Three-Part HMDA Scenario Workshop 1. Part One - Collection and reporting of Demographics using sample applicant scenarios 2. Part Two Collection and reporting of new data elements involving Q&A and True/False based questions 3. Part Three - Gathering reportable data for completion of our data worksheet and our data collection register through the use of sample customer scenarios

5 HMDA Workshop 5

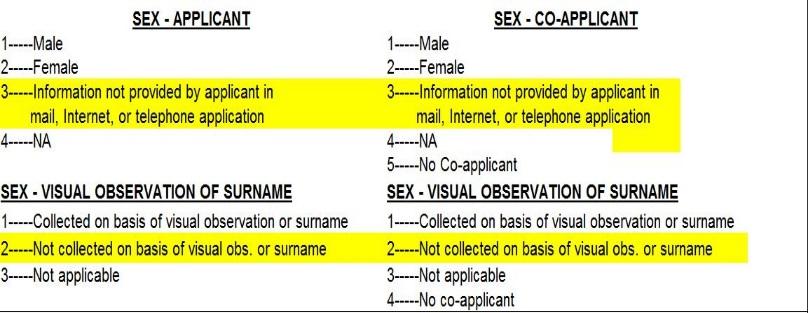

6 Part I - How to Collect and Complete Demographics and the Data Collection Form (Appendix B) 6

7 HMDA Workshop 7 Tiger Woodlands comes in to apply for a dwelling-secured mortgage loan at your institution. Tiger has a very interesting racial profile in that his father is on African- American, Chinese and Native American (Shawnee) descent. His mother is of Thai, Chinese and Dutch descent. He selects: Not Hispanic or Latino American Indian Shawnee Asian Chinese Other Asian Thai Black or African American White Male How would you handle completing the GMI Information and the HMDA Worksheet Ethnicity/Race/Sex section based on his selections?

8 Tiger Woodlands 8

9 Tiger Woodlands 9

10 Tiger Woodlands 10

11 HMDA Workshop 11 Jimmy Hernandez comes in to apply for a dwelling-secured mortgage loan at your institution. Jimmy brings his lovely wife, Veronica, along with him and they are applying for joint credit. Jimmy marks I do not wish to provide on his side of the application and Veronica completes her side with the following information: Hispanic or Latino Mexican Puerto Rican Other Hispanic Dominican White Female How do you handle collecting the GMI information for Jimmy and how would you complete the HMDA Worksheet Ethnicity/Race/Sex section for both applicants?

12 Jimmy & Veronica Hernandez 12 You would have to inform Jimmy that you are required to collect the data based on visual observation or surname. Based on his last name, you complete the GMI and complete the HMDA Worksheet Ethnicity/Race/Sex section as follows:

13 Jimmy & Veronica Hernandez 13

14 Jimmy & Veronica Hernandez 14

15 HMDA Workshop 15 Keith Rivers calls your office to apply for a dwelling-secured mortgage loan. He tells you that Bryan Marks will be applying jointly and is available to speak to you as well. You complete the application via telephone. You recite the appropriate information and ask for GMI information. Keith states that he is: Bryan states that he is: Not Hispanic or Latino Asian Chinese Native Hawaiian or Other Pacific Islander Native Hawaiian White Male Hispanic or Latino Puerto Rican Asian Filipino Other Asian Cebuano White Male Male How do you handle completing the GMI information and the HMDA Worksheet Ethnicity/Race/Sex section for both applicants?

16 Keith Rivers & Bryan Marks 16

17 Keith Rivers & Bryan Marks 17

18 Keith Rivers & Bryan Marks 18

19 HMDA Workshop 19 Ashley Douglas calls in to apply for a dwelling-secured loan at your institution. She is travelling and doesn t have time to apply in person. You complete the application via telephone. You recite the appropriate information and ask for GMI information. Ashley states that she is: Hispanic or Latino Puerto Rican American Indian Sioux Tribe Asian Chinese Filipino Korean Black or African American Native Hawaiian or Other Pacific Islander Native Hawaiian Samoan White Male When asked for gender information, Ashley states that she is in the process of transitioning from a female to a male so she would like to choose both Male and Female. How do you handle completing the GMI information and the HMDA Worksheet Ethnicity/Race/Sex section?

20 Ashley Douglas 20

21 Ashley Douglas 21

22 Ashley Douglas 22

23 HMDA Workshop 23 Cameron Pativ comes in to apply for a dwellingsecured mortgage loan at your institution. Cameron marks I do not wish to provide under all three categories on the GMI collection portion. How do you handle completing the GMI information and how would you complete the HMDA Worksheet Ethnicity/Race/Sex section?

24 Cameron Pativ 24 You would have to tell Cameron that you are required to collect race based on visual observation or surname. You complete the GMI and complete the HMDA Worksheet Ethnicity/Race/Sex section as follows:

25 Cameron Pativ 25

26 Cameron Pativ 26 This is based on our assumption that Cameron was a female. You may have determined that Cameron was a female and would report as indicated for male.

27 27 Part II Other Data Collection

28 Scenario 1: Property Address 28 George Adams is approved for a credit request to purchase a new principal dwelling located at 1234 Sycamore Street, Anytown, Anywhere The credit will be secured by this property in addition to his current principal residence located at 890 Pine Avenue, Anytown, Anywhere What do you report for property address?

29 Answer to Scenario 1: Property Address 29 It is your option. Where more than one property secures the loan, an institution reports the loan in a single entry on its LAR and provides the property address and location for only one property. The institution can choose the property for which it reports this information, but it must choose a property that secures the loan that includes a dwelling.

30 Answer to Scenario 1: Property Address 30 Small Entity Guide (Section 5.12) If more than one property secures the Covered Loan or, in the case of an Application, would have secured the Covered Loan, a Financial Institution reports the Covered Loan or Application in a single entry on its LAR and provides the property address and location for only one property. The Financial Institution can choose the property for which it reports this information, but it must choose a property that secures the Covered Loan (or, in the case of an Application, would have secured the Covered Loan) and that includes a Dwelling. If a single Multifamily Dwelling has more than one postal address, a Financial Institution reports one of the postal addresses. Comments 4(a)(9)-2 and -3.

31 Scenario 2: Occupancy Type 31 Nathan and Jon Wells are approved for a credit request to purchase a single family residence located at 123 Cherrytree Lane, Anytown, Anywhere The credit will be secured by this property. The purpose on the application form states investment purposes. How would you report Occupancy Type and Business or Commercial Purpose for this credit?

32 Answer to Scenario 2: Occupancy Type 32 You would need to ask for more information. Is either of the two going to occupy the property? Are they going to rent the property to generate income? If a covered loan or application is deemed to be primarily for a business or commercial purpose under Regulation Z, it is also deemed to be for a business or commercial purpose under the 2015 HMDA Rule.

33 Answer to Scenario 2: Occupancy Type 33 Small Entity Guide (Section 5.14) A property is an investment property if the applicant or borrower does not occupy the property. For example, if a person purchases a property, does not occupy the property, and generates income by renting the property, the property is an investment property. Similarly, if a person purchases a property, does not occupy the property, and does not generate income by renting the property, but intends to generate income by selling the property, the property is an investment property. Comment 4(a)(6)-4.

34 Scenario 3: Construction Method, Manufactured Property Type & Manufactured Land Property Interest 34 Carrie Glass is approved to refinance the loan secured by her manufactured home only (no real estate), which is located on a lot she leases from her mom and dad. She does not have a formal lease agreement, but pays them $75 each month in rental fees to maintain septic and water utilities for her home. Assume that it DOES NOT have the appropriate HUD certification or meet the definition of manufactured home in HUD s regulations. How would you report Construction Method, Manufactured Home Property Type and Manufactured Land Property Interest for this loan?

35 Answer to Scenario 3: Construction Method, Manufactured Property Type & Manufactured Land Property Interest 35 Manufactured Home Property Type: NA Construction Method Site Built Manufactured Land Property Interest NA

36 Answer to Scenario 3: Construction Method, Manufactured Property Type & Manufactured Land Property Interest 36 Small Entity Guide, (page 27): A Manufactured Home is a residential structure that satisfies the definition of manufactured home in the U.S. Department of Housing and Urban Development s (HUD s) regulations, 24 CFR , for establishing manufactured home construction and safety standards. 12 CFR (l). A modular home or factory-built home that does not meet HUD s regulations is not a Manufactured Home under the 2015 HMDA Rule. A Manufactured Home will generally bear a HUD Certification Label and data plate noting compliance with the Federal standards. Comment 2(l)-2.

37 Scenario 4: Application Channel 37 Little Town Mortgage Broker has a relationship with Big Town Bank to accept applications for real estate loans. However, as part of their relationship, Little Town Mortgage Broker can only accept the applications. They do not have enough authority to approve the loan. Ashley Douglas is looking to buy a new home and her business is located next to Little Town Mortgage Broker s office, so on her lunch break she applies with Little Town Mortgage Broker to purchase a nice 1-4 family dwelling. Little Town Mortgage Broker accepts her application and forwards it on to Big Town Bank for approval. What would be the correct code for Application Channel, for the data field Submission of the Application?

38 Answer to Scenario 4: Application Channel 38 Code 2- Not submitted directly to your institution.

39 Answer to Scenario 4: Application Channel 39 CFPB Guide- page 48 If an applicant contacted and completed an Application with a broker or correspondent that forwarded the Application to the Financial Institution for approval, the Application was not submitted directly to the Financial Institution. Comment 4(a)(33)(i)-1.iii. Comment (a)(33)(i)-1.iii If an applicant contacted and completed an application with a broker or correspondent that forwarded the application to a financial institution for approval, an application was not submitted to the financial institution.

40 Scenario 5: Application Channel 40 After Big Town Bank reviews Ashley s application they have determined that they are going to approve the loan, but then the appraisal comes back too low. Big Town Bank then makes the decision to deny the request for credit and sends Ashley an adverse action notice with the reason of insufficient collateral. What would be the correct code for Application Channel, for the data field Initially Payable to Your Institution?

41 Answer to Scenario 5: Application Channel 41 Code 3- Not applicable

42 Answer to Scenario 5: Application Channel 42 CFPB Guide- page 48 For an Application that is withdrawn, denied, or closed for incompleteness, a Financial Institution reports that the requirement is not applicable if the Financial Institution had not determined, at the time it took final action on the Application, whether the loan would be initially payable to the Financial Institution. Comment 4(a)(33)(ii)-2.

43 Scenario 6: Loan Type 43 Jane Smith visits First State Bank to apply for a loan to purchase a manufactured home (HUD certified) that is located on her aunt and uncle s property to be away from the city. She thinks this will be the perfect home for her because she doesn t have to sign a lease to keep her home there. She only has to pay for her utilities. When she applies for the loan, the lender suggests that she apply under USDA Rural Housing Service. She agrees and the loan closes two months later. What would be the correct Loan Type reported on the LAR?

44 Answer to Scenario 6: Loan Type 44 Code 4- USDA Rural Housing Service or Farm Service Agency guaranteed (RHS or FSA)

45 Answer to Scenario 6: Loan Type 45 CFPB Guide page 49 A Financial Institution reports whether the Covered Loan is or the Application was for a Covered Loan that would have been: 1. Insured by the Federal Housing Administration; 2. Guaranteed by the Veterans Administration; 3. Guaranteed by the Rural Housing Service or the Farm Service Agency; or 4. Not insured or guaranteed by any of these Federal agencies (i.e., conventional). 12 CFR (a)(2).

46 Scenario 6: Bonus Question Loan Type 46 Since this is a manufactured home that has the HUD certification, what would be the correct codes used for Construction Method, Manufactured Home Secured Property Type and Manufactured Home Land Property Interest?

47 Answer to Scenario 6: Bonus Question Loan Type 47 Construction Method- Code 2 Manufactured home Secured Property Type- Code 2 Manufactured home and not land Land Property Interest- Code 4 Unpaid leasehold

48 Answer to Scenario 6: Bonus Question Loan Type 48 CFPB Guide page A residential structure that satisfies the definition of manufactured home under HUD s regulations, 24 CFR , is reported as a Manufactured Home. 12 CFR (l). A Manufactured Home will generally bear a HUD Certification Label and data plate noting compliance with the Federal standards. Comment 2(l)-2.

49 Answer to Scenario 6: Bonus Question Loan Type 49 CFPB Guide page Manufactured home information If a Dwelling on the Identified Property is a Manufactured Home and not a Multifamily Dwelling (i.e., it has four or fewer individual dwelling units), the Financial Institution must report both: Secured Property Type. Whether the Covered Loan is or the Application would have been secured by: (a) both a Manufactured Home and land; or (b) a Manufactured Home and not land. 12 CFR (a)(29). A Financial Institution reports that a Covered Loan is or would have been secured only by a Manufactured Home and not land if the Covered Loan is not secured by the land, even if the Manufactured Home is considered real property under applicable State law. Comment 4(a)(29)-1. Land Property Interest. Information about the applicant s or borrower s property interest in the land on which the Manufactured Home is or would have been located, reported as one of the following: Unpaid Leasehold. For example, an unpaid leasehold occurs when the borrower locates the Manufactured Home on land owned by a family member, does not have a written lease, and does not have an agreement regarding rent payments. Comment 4(a)(30)-2.

50 Scenario 7: Loan Purpose 50 John Johnson applies for a loan at your bank. He states that the loan is to purchase an old farm home and he also needs funds to make improvements on the home. What would you report as the Loan Purpose?

51 Answer to Scenario 7: Loan Purpose 51 Code 1- Home Purchase

52 Scenario 8: Loan Purpose 52 Big Town Bank is trying to determine how to report one of their originated loans. Documentation in the loan file indicates the loan is secured by the borrower s primary residence, and the borrower received proceeds of $25,000. However, there is no indication in the loan file of what the proceeds were used for. The lender that took the application is out on maternity leave, so they are unable to inquire with her on what the proceeds were used for. What would you report as the Loan Purpose?

53 Answer to Scenario 8: Loan Purpose 53 Code 4- Other Purpose

54 Answer to Scenario 8: Loan Purpose 54 CFPB Guide page 52 A Financial Institution may rely on an applicant s oral or written statement regarding the proposed use of the loan proceeds. For example, a Financial Institution could use a check box or a purpose line on an Application form. If an applicant provides no statement as to the proposed use of the proceeds, and the Covered Loan is not a Home Purchase Loan, cash-out Refinancing, or Refinancing, a Financial Institution reports the Covered Loan as for an other purpose. Comment 4(a)(3)-1.

55 Scenario 9: Loan Purpose 55 Michael White applies for a loan at your bank. He wants to refinance his current mortgage on his vacation home and use proceeds of the loan to add a swimming pool at his vacation home. What would you report as the Loan Purpose?

56 Answer to Scenario 9: Loan Purpose 56 Code 31- Refinancing

57 Answer to Scenario 9: Loan Purpose 57 Multiple Purposes Home Purchase Loan and Home Improvement Loan Home Purchase Loan and Refinancing Home Purchase Loan and cash-out Refinancing Home Purchase Loan and other Home Improvement Loan and Refinancing Home Improvement Loan and cash-out Refinancing Refinancing and other Cash-out Refinancing and other Home Improvement Loan and other Reportable Purpose Home Purchase Loan Home Purchase Loan Home Purchase Loan Home Purchase Loan Refinancing Cash-out Refinancing Refinancing Cash-out Refinancing Home Improvement Loan

58 Scenario 10: Contractual Features 58 Little City Bank originates a business-purpose loan to Jane s Rental Homes. The loan is exempt from Regulation Z, because it is a business purpose loan. The borrower, Jane s Rental Homes, uses the proceeds to purchase a 5 unit home and the loan is secured by the 5 unit home. During the application process, the lender decides that the loan should include a balloon payment, but didn t provide the required disclosures under Regulation Z, which covers balloon loans. Should the bank report the Balloon Payment on the LAR?

59 Answer to Scenario 10: Contractual Features 59 Yes, even though business purpose loans are exempt from Regulation Z, Little City Bank is still required to report that there is a Balloon Payment feature for the loan to Jane s Rental Homes.

60 Answer to Scenario 10: Contractual Features 60 CFPB Guide page 78 Ficus Bank originates a business-purpose transaction that is exempt from Regulation Z. The borrower, a corporation, uses the loan proceeds to finance the purchase of a Multifamily Dwelling. The loan is secured by a mortgage on the Multifamily Dwelling. The loan includes a balloon payment, as defined by Regulation Z, 12 CFR (s)(5)(i), at the end of the loan term. Even though the borrower is not a natural person, the loan is for a business purpose, and a Multifamily Dwelling is not a dwelling under Regulation Z, Ficus Bank reports the business-purpose transaction as having a balloon payment.

61 Scenario 11: Credit Score 61 ABC Bank obtains credit scores from Equifax and Experian for all home loan borrowers. During their underwriting process the credit decision is based on the lowest credit score obtained. In this instance, the lowest score was from Experian for both the applicant and the coapplicant. How would they complete the Credit Scoring Model section?

62 Answer to Scenario 11: Credit Score 62 The Financial Institution would enter the score used and then choose option 2 for the scoring model (Experian) for the applicant and the coapplicant

63 Answer to Scenario 11: Credit Score 63 Small Entity Guide (Section 5.22) When a Financial Institution obtained or created two or more credit scores for a single applicant or borrower but relied on only one score in making the credit decision (e.g., by relying on the lowest, highest, most recent, or average of all of the scores), the Financial Institution reports the credit score it actually used.

64 Scenario 12: Credit Score 64 A financial institution has an application from Joe Blank to purchase a primary residence. During their credit analysis they use a scoring grid that considers each of the scores obtained. The scores were not combined into a composite or average score. Which score should be reported and which model should be referenced?

65 Answer to Scenario 12: Credit Score 65 The financial institution would enter only one of the scores used in making the credit decision and reference the appropriate model.

66 Answer to Scenario 12: Credit Score 66 Small Entity Guide (Section 5.22) When a Financial Institution relied on multiple scores for the applicant or borrower (e.g., by relying on a scoring grid that considers each of the scores obtained or created for the applicant or borrower without combining the scores into a composite score), the Financial Institution must report one of the credit scores that it relied on in making the credit decision. In choosing which credit score to report, a Financial Institution need not use the same approach for its entire HMDA data submission, but it should be generally consistent (e.g., by routinely using one approach within a particular division of the Financial Institution or for a category of Covered Loans). The Financial Institution reports the name and version of the credit-scoring model for the score reported. Comment 4(a)(15)-2. Note: The credit score data point is not applicable for: Purchased covered loans, If the FI did not rely on a credit score, If the file was closed for incompleteness (even if the score was obtained), if the application was withdrawn before the credit decision was made (even if the credit score was obtained), or if the applicant or co-applicant is not a natural person.

67 Scenario 13: Automated Underwriting System 67 ABC Bank offers multiple mortgage programs and during the application process for David Smith (no co-applicant) obtains multiple results from the DU, LP, and GUS underwriting systems during the credit decision process. All results were favorable and eligibility was approved. Which of the AUS system and AUS results would the FI report on the LAR? Note: In order for a system to be an AUS, the system must provide a result regarding both the credit risk of the applicant and the eligibility of the loan to be originated, purchased, insured, or guaranteed by the securitizer, Federal government insurer, or Federal government guarantor that developed the system being used to evaluate the Application. For example, if a system is an electronic tool that provides a determination of the loan s eligibility to be purchased, but the system does not also provide an assessment of the applicant s creditworthiness such as an evaluation of the applicant s income, debt, and credit history the system is not an AUS. Comment 4(a)(35)-2.

68 Answer to Scenario 13: Automated Underwriting System 68 ABC Bank would report each of the AUS systems used to evaluate the applicant. In this scenario, the Bank would report 1 DU, 2 LP, and 4 GUS for the system, and 1 approve/eligible, 3 refer/eligible, 14 eligible for the AUS results as applicable to the systems used.

69 Answer to Scenario 13: Automated Underwriting System 69 Small Entity Guide (Section 5.23) If the Financial Institution simultaneously obtains multiple results closest in time to the credit decision, the Financial Institution reports each of the multiple AUS results that it obtained and the AUSs that generated each of those results up to a total of five results and five AUSs. The Financial Institution will never report more than five results or five AUSs. If the Financial Institution used more than five AUSs or it obtained more than five results, the Financial Institution chooses five AUSs and five results to report. Comment 4(a)(35)-3.

70 Scenario 14: Automated Underwriting System 70 The FI receives an application for credit from Robert and Mary John to purchase their primary residence. The application is being evaluated to sell on the secondary market. For this particular purchaser, the FI uses the LP system to evaluate each of the applicant s credit risk and eligibility. It is determined that the application is eligible for approval. In this scenario, how would the FI report the AUS system and the AUS results?

71 Answer to Scenario 14: Automated Underwriting System 71 The FI would report 2 LP for the AUS system and `1 approve/eligible, 3 refer/eligible, or 14 eligible indicating the result produced by LP. Note: The only instances where the FI would not report the AUS data point would be: 1) if the FI does not use an AUS to evaluate applicants, 2) when the applicant and/or co-applicant, are not natural persons, and 3) for purchased covered loans

72 Scenario 15: Preapproval Program 72 Ralph Sides found a home that he was interested in purchasing. The realtor suggested that he obtain a letter from the Bank indicating that he would be eligible for the purchase price offer which would give him more credibility. The Bank sent him a congratulations letter stating that he is potentially eligible for a mortgage up to $250,000. They noted in the letter that the amount and terms would be subject to all normal underwriting conditions and to contact his loan officer for additional information and completion of the application process. The loan was later originated by the Bank. How should the Bank complete the preapproval section on the LAR?

73 Answer to Scenario 15: Preapproval Program 73 The Bank would report 2 Preapproval not requested. It appears that the Bank does not have a formal preapproval program as defined by the new rules.

74 Answer to Scenario 15: Preapproval Program 74 Small Entity Guide (Section 4.2.1) The written commitment issued as part of the Preapproval Program can be subject to only the following types of conditions: 1. Conditions that require the identification of a suitable property; 2. Conditions that require that no material change occur regarding the applicant s financial condition or creditworthiness prior to closing; and 3. Limited conditions that (a) are not related to the applicant s financial condition or creditworthiness 12 CFR (b)(2); comment 2(b)-3.

75 True or False 1 75 A home purchase loan includes: a combined construction-to-permanent loan that is secured by a Dwelling; a permanent loan that replaces a construction loan if the permanent loan is secured by a dwelling; and a dwelling-secured subordinate mortgage loan that finances some or all of the home purchaser s down payment.

76 Answer to True or False 1 76 TRUE

77 Answer to True or False 1 77 Small Entity Guide (Section 5.7): A Home Purchase Loan is a Closed-End Mortgage Loan or Open-End Line of Credit that is for the purpose, in whole or part, of purchasing a Dwelling. 12 CFR (j). A Home Purchase Loan includes: (a) a Closed-End Mortgage Loan or Open-End Line of Credit secured by one Dwelling and used to purchase another Dwelling; (b) a combined construction-topermanent loan that is secured by a Dwelling; (c) a permanent loan that replaces a construction loan if the permanent loan is secured by a Dwelling; and (d) a Dwelling-secured subordinate mortgage loan that finances some or all of the home purchaser s down payment. Comments 2(j)-1, -3, and -4.

78 True or False 2 78 Since the new rules require the borrower s age, we re going to have to require applicant s to bring in their birth certificates.

79 Answer to True and False 2 79 FALSE The institution can rely on the information provided on the application form provided by the applicant

80 Answer to true and False 2 80 Small Entity Guide (Section 5.1.2) A Financial Institution reports the applicant s age (as of the Application date) as the number of whole years derived from the date of birth shown on the Application form. 12 CFR (a)(10)(ii); comment 4(a)(10)(ii)-1.

81 Part III Gathering Data, Completing Data Worksheet and Loan Application Register 81

82 Tools we will be using 82 Temenos Data Collection Register Temenos Data Worksheet

83 Tools we will be using: 83 Commercial Application URLA Form 1003 Uniform Residential Loan App. Universal/HELOC Application

84 Scenario 1: Home Purchase 84 John A. Homeowner and his wife, Mary A. Homeowner, come into your branch to apply for a home purchase. John and Mary are newlyweds who are currently residing with Mary s parents so they would like to complete the application while at the institution so they can hopefully speed up the process. The application is approved, the loan is originated and will be held in-house by your institution. Using the SCENARIO 1 application in your materials, complete the HMDA Worksheet and then transfer that information to the HMDA Data Collection Register.

85 Scenario 1: Home Purchase 85 Information not provided on the application form: Credit Score: John 800 Mary 800 Credit Scoring Model: Equifax Beacon 5.0 AUS System: TOTAL Scorecard AUS Results: 1. Approve/Eligible DTI Ratio:.06% (if you calculate from app) CLTV Ratio: 76% Geocoding Info: MSA/MD Code: State: 11 County Code: 001 Tract Code: Loan Info: No preapproval requested; Conventional loan is originated on 2/15/18; Loan will not be sold on the secondary market No prepayment penalty, no negative amortization or any other non-amortizing features 1% Origination Charge ($2,100), Discount Points - $2,100, Lender Credits - $0, Total Loan Costs - $4,110 Rate Spread: N/A Not a HOEPA loan

86 Scenario 1: Data Worksheet 86

87 Scenario 1: Data Worksheet 87

88 Scenario 1: Data Worksheet 88

89 Scenario 2: Refinance 89 Sue V. Summer is applying online for a refinance on investment property she currently has financed with a different institution. Since she does not rent this property and is not using this property for business purposes, you determine that this is a consumer purpose loan. The application is approved, the loan is originated and will be held in-house by your institution. Using the SCENARIO 2 application in your materials, complete the HMDA Worksheet and then transfer that information to the HMDA Data Collection Register.

90 90 Information not provided on the application form: Credit Score: 750 Credit Scoring Model: Equifax Beacon 5.0 AUS System: Not applicable DTI Ratio: 43% (Did not calculate) CLTV Ratio: 56% Geocoding Info: MSA/MD Code: State Code: 12 County Code: 131 Census Tract: Loan Info: No preapproval requested; Conventional loan is originated on 3/15/18; Loan will not be sold on the secondary market No prepayment penalty, no negative amortization or any other non-amortizing features $2,500 1% Origination Charge ($1,200), $0 Discount Points, $0 Lender Credits, Total Loan Costs - Rate Spread: N/A Not a HOEPA loan

91 Scenario 2: Data Worksheet 91

92 Scenario 2: Data Worksheet 92

93 Scenario 2: Data Worksheet 93

94 Scenario 3: Refinance/Business 94 Jack E. Shopper is applying in person for a refinance on investment property he currently has financed with a different institution. Since this is investment property producing rental income, you determine that this is a business purpose loan. Since the purpose is to refinance a dwelling and the loan will be secured by a dwelling, it will be HMDA reportable. The application is approved, the loan is originated and will be held in-house by your institution. Using the SCENARIO 3 application in your materials, complete the HMDA Worksheet and then transfer that information to the HMDA Data Collection Register.

95 Scenario 3: Refinance/Business 95 Information not provided on the application form: Check Digit 83 Credit Score: 780 Credit Scoring Model: Equifax Fair Isaac AUS System: Debt Underwriter (DU) AUS Results: Approved/Eligible DTI Ratio: 43% (Did not calculate) CLTV Ratio: 75% (Did not calculate) Geocoding Info: MSA/MD Code: State Code: 12 County Code: 151 Census Tract: Loan Info: No preapproval requested; Conventional loan is originated on 3/23/18; Loan will not be sold on the secondary market No prepayment penalty, no negative amortization or any other non-amortizing features $0 Discount Points, $0 Lender Credits, Total Loan Costs - $2,500 Rate Spread: N/A Not a HOEPA loan

96 Scenario 3: Data Worksheet 96

97 Scenario 3: Data Worksheet 97

98 Scenario 3: Data Worksheet 98

99 Scenario 4: HELOC 99 Don Jones and Judy Jones are applying via mail for a HELOC secured by their personal residence. Since this is open-end credit secured by a dwelling, it is now reportable (HELOCs are no longer optional). Don and Judy both marked I do not wish to provide on the application form and the loan officer indicated the GMI was not required because the purpose was not to purchase or refinance. The application is approved, the loan is originated and will be held in-house by your institution. Using the SCENARIO 4 application in your materials, complete the HMDA Worksheet and then transfer that information to the HMDA Data Collection Register.

100 Scenario 4: HELOC 100 Information not provided on the application form: ULI Including Check Digit: 123X45A2232 Applicant Credit Score: 850 Credit Scoring Model: Equifax Beacon CoApplicant Credit Score: 835 Credit Scoring Model: Equifax Beacon AUS System: N/A DTI Ratio: 43% (Did not calculate) CLTV Ratio: 28% (Did not calculate) Geocoding Info: MSA/MD Code: NA State Code: 01 County Code: 036 Census Tract: Loan Info: No preapproval requested; Conventional loan is originated on 3/15/18; Loan will not be sold on the secondary market No prepayment penalty, no negative amortization or any other non-amortizing features $0 Discount Points, $0 Lender Credits, Total Loan Costs - $0 Rate Spread: N/A Not a HOEPA loan

101 Scenario 4: Data Worksheet 101

102 Scenario 4: Data Worksheet 102

103 Scenario 4: Data Worksheet 103

104 Scenario 4: Bonus 104 This loan has a violation for not collecting GMI information because it is HMDA reportable and you must collect GMI information for all reportable loans. TRUE OR FALSE?

105 Scenario 4: Bonus 105 It actually depends on the situation, in this case. Normally, yes, you would collect the GMI because it is a HMDA reportable loan, but since this application was received via mail, you must ask for the information from the applicant (It was provided on the application form), but you cannot require it. Had they not marked I do not wish to provide then if they had come into the institution to finish the application process, the LO would be required to ask for the GMI info and if they did not provide it, he would have to complete based on visual observation or surname. If the meeting took place after the application process was completed, there is no requirement to collect the information.

106 Completed Data Collection Register 106

107 Completed Data Collection Register 107

108 Completed Data Collection Register 108

109 Completed Data Collection Register 109

110 Questions? 110

111 Thank you!

HMDA: Haven or Havoc. Michigan Bankers Association. Compliance Services 2016 Temenos USA. All rights reserved.

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

HMDA: Haven or Havoc Michigan Bankers Association 1 2016 Temenos USA. All rights reserved. About the Speaker Rachelle Dekker CRCM Rachelle Dekker is a Senior Compliance Advisor with the Temenos Compliance

HMDA LAR Fields Effective 1/1/2018 Comparison with Current HMDA Fields - Updated 7/17/2016 Current Field New/Revised Field

Current New/Revised Record Identifier Record Identifier 2 2 software may enter this value or bank will enter on every line of LAR this entry is on every line No change Respondent ID Value depends upon

Current New/Revised Record Identifier Record Identifier 2 2 software may enter this value or bank will enter on every line of LAR this entry is on every line No change Respondent ID Value depends upon

S (a) Impact Data. Unchanged Value 01 Record Identifier x 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) x

Impact Data. Unchanged Value 01 Record Identifier x 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) x") Eempt 01 Record Identifier 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) 02 Universal Loan Identifier (ULI) / Non Universal Loan Identifier (NULI) 03 Universal Loan Identifier (ULI)

Eempt 01 Record Identifier 01 Legal Entity Identifier (LEI) 02 Legal Entity Identifier (LEI) 02 Universal Loan Identifier (ULI) / Non Universal Loan Identifier (NULI) 03 Universal Loan Identifier (ULI)

Compliance Policy 2003-ALL

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

Overview The following policy describes how CMG Mortgage, Inc., dba CMG Financial, NMLS #1820, ( CMG ) complies with the Home Mortgage Disclosure Act (HMDA) and its implementing regulation, Regulation

Filing instructions guide for HMDA data collected in 2018

August 2017 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

August 2017 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

HMDA Regulations and New 1003 Application - Part 2

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

HMDA Regulations and New 1003 Application - Part 2 Broker / Correspondent Training May 10 & 12, 2017 1Nations Direct Mortgage Agenda Overview of New Regulations New and Modified HMDA Data Fields Detail

Filing instructions guide for HMDA data collected in 2019

October 2018 Filing instructions guide for HMDA data collected in 2019 OMB Control #3170-0008 Version log The following is a version log that tracks changes from the previous version of the Filing Instructions

October 2018 Filing instructions guide for HMDA data collected in 2019 OMB Control #3170-0008 Version log The following is a version log that tracks changes from the previous version of the Filing Instructions

Filing instructions guide for HMDA data collected in 2018

September 2018 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date

September 2018 Filing instructions guide for HMDA data collected in 2018 OMB Control #3170-0008 Version log The following is a version log that tracks the history of this document and its updates: Date

HMDA: Haven or Havoc. Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Agenda Day One 1. Effective dates 2. Overview of reporting requirements Annual expectations

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Agenda Day One 1. Effective dates 2. Overview of reporting requirements Annual expectations

2018 HMDA Implementation. Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

2018 HMDA Implementation Presented By: Karen Ruckle, Director of Compliance Bank of the Ozarks 2018 HMDA Loan Volume Test # Loans #Loans #Loans Home Purchase Or Refi (Dwelling Secured) in prior calendar

What do HMDA Rule Changes Mean for Covered Institutions?

What do HMDA Rule Changes Mean for Covered Institutions? Tips to prepare for regulatory and institutional change Paula Witt, Director, Consumer Finance & Fair Banking Elizabeth Rozsa, Manager, Consumer

What do HMDA Rule Changes Mean for Covered Institutions? Tips to prepare for regulatory and institutional change Paula Witt, Director, Consumer Finance & Fair Banking Elizabeth Rozsa, Manager, Consumer

HMDA: Haven or Havoc. Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Recap Day One 2 1. Annual expectations 2. Two proposals and a new final rule 3. Key definitions

HMDA: Haven or Havoc Cindy Prince, Presenter December 5, 6 & 7, 2017 Assisted by Rachelle Dekker and Matt Goble Recap Day One 2 1. Annual expectations 2. Two proposals and a new final rule 3. Key definitions

Home Mortgage Disclosure Act (HMDA) 2014 FIS and/or its subsidiaries. All Rights Reserved.

2014 FIS and/or its subsidiaries. All Rights Reserved.") Home Mortgage Disclosure Act (HMDA) 2014 FIS and/or its subsidiaries. All Rights Reserved. 1 Home Mortgage Disclosure Act (HMDA) 12 CFR 1003 Purpose: Detect illegal discrimination Detect predatory lending

Home Mortgage Disclosure Act (HMDA) 2014 FIS and/or its subsidiaries. All Rights Reserved. 1 Home Mortgage Disclosure Act (HMDA) 12 CFR 1003 Purpose: Detect illegal discrimination Detect predatory lending

Summary of Reportable HMDA Data Regulatory Reference Chart a

Summary of Reportable HMDA Data Regulatory Reference Chart a This chart is intended to be used as a reference tool for data points required to be collected, recorded, and reported under Regulation C, as

Summary of Reportable HMDA Data Regulatory Reference Chart a This chart is intended to be used as a reference tool for data points required to be collected, recorded, and reported under Regulation C, as

Covered loans or applications if the property is

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

Application Date 1003.4(a)(1)(ii) Property Address State County Census Tract Covered loans or applications if the property address of the property securing the covered loan is not known (e.g., the property

HMDA Demographic Information Addendum Policy & Procedure

HMDA Demographic Information Addendum Policy & Procedure April 18, 2018 1. Overview The Home Mortgage Disclosure Act (HMDA), which is implemented as Regulation C, requires lenders to collect and publicly

HMDA Demographic Information Addendum Policy & Procedure April 18, 2018 1. Overview The Home Mortgage Disclosure Act (HMDA), which is implemented as Regulation C, requires lenders to collect and publicly

A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data

Data") September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

September, 2015 A Look at Tennessee Mortgage Activity: A one-state analysis of the Home Mortgage Disclosure Act (HMDA) Data 2004-2013 Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE OF CONTENTS

HMDA 2018 IMPLEMENTATION PLANNING. HMDA Process Inventory

Affected Products Application Methods (Face to face (online, paper), Mail, Online, Telephone, Fax HMDA Process Inventory Demographic Data Gathering Methods LAR Software Used or Manual LAR Preparation Responsible

Affected Products Application Methods (Face to face (online, paper), Mail, Online, Telephone, Fax HMDA Process Inventory Demographic Data Gathering Methods LAR Software Used or Manual LAR Preparation Responsible

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C

Revisions to Regulation C") ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

ICBA Summary of the Home Mortgage Disclosure Act (HMDA) Revisions to Regulation C June 2017 INSERT YEAR HERE Contact Information: Rhonda Thomas-Whitley Assistant Vice President & Regulatory Counsel Rhonda.Thomas-Whitley@icba.org

HMDA LET S GET IT RIGHT!

HMDA LET S GET IT RIGHT! Home Mortgage Disclosure Act December 19, 2017 Joan Crenshaw, CRCM, CAFP Director jcrenshaw@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

HMDA LET S GET IT RIGHT! Home Mortgage Disclosure Act December 19, 2017 Joan Crenshaw, CRCM, CAFP Director jcrenshaw@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they

The New CFPB HMDA Rules

The New CFPB HMDA Rules What You Need to Know Thank you for attending. The webinar has started. Today s Panelists Kathleen Ryan Counsel BuckleySandler LLP Leonard Ryan President QuestSoft Corporation Moderator

The New CFPB HMDA Rules What You Need to Know Thank you for attending. The webinar has started. Today s Panelists Kathleen Ryan Counsel BuckleySandler LLP Leonard Ryan President QuestSoft Corporation Moderator

Home Mortgage Disclosure Act 2017, 2018, and Beyond. Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

Home Mortgage Disclosure Act 2017, 2018, and Beyond Presented by Marissa Blundell Bankers Advisory A CliftonLarsonAllen LLP Division Home Mortgage Disclosure Act (HMDA) Consumer Financial Protection Bureau

1) The credit union's assets total more than $44 million as of December 31, 2017,

The credit union's assets total more than $44 million as of December 31, 2017,") Exemption: This regulation only applies if the following criteria are met: 1) The credit union's assets total more than $44 million as of December 31, 2017, 2) The credit union has a home or branch office

Exemption: This regulation only applies if the following criteria are met: 1) The credit union's assets total more than $44 million as of December 31, 2017, 2) The credit union has a home or branch office

Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA)

CFPB Home Mortgage Disclosure Act (HMDA)") Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA) Impact: Federal and State Chartered Credit Unions Relevant Department: CEO / Lending Priority Level: High Background / Credit Union Summary

Comment Call (14-15) CFPB Home Mortgage Disclosure Act (HMDA) Impact: Federal and State Chartered Credit Unions Relevant Department: CEO / Lending Priority Level: High Background / Credit Union Summary

Filing instructions guide for HMDA data collected in 2017

August 07 Filing instructions guide for HMDA data collected in 07 OMB Control #70-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

August 07 Filing instructions guide for HMDA data collected in 07 OMB Control #70-0008 Version log The following is a version log that tracks the history of this document and its updates: Date Version

Uniform Residential Loan Application

To be completed by the Lender: Lender Loan No./Universal Loan Identifier Agency Case No. Verify and complete the information on this application. If you are applying for this loan with others, each additional

To be completed by the Lender: Lender Loan No./Universal Loan Identifier Agency Case No. Verify and complete the information on this application. If you are applying for this loan with others, each additional

The New CFPB HMDA Rules What You Need to Know

The presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC, you don t need to call in. While you are waiting, you may download the presentation online at:

The presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC, you don t need to call in. While you are waiting, you may download the presentation online at:

Freehold Savings Bank, 68 West Main Street, Freehold, N.J Commercial Mortgage Construction Loan Term Loan Equipment Loan Line of Credit

COMMERCIAL LOAN APPLICATION Thank you for considering us for your commercial loan needs. This application along with other information you supply will provide us with the information needed to review your

COMMERCIAL LOAN APPLICATION Thank you for considering us for your commercial loan needs. This application along with other information you supply will provide us with the information needed to review your

FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE

![FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE](/thumbs/89/97922501.jpg "FEDERAL RESERVE SYSTEM. 12 CFR Part 203. [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE") FEDERAL RESERVE SYSTEM 12 CFR Part 203 [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE AGENCY: Board of Governors of the Federal Reserve System. ACTION: Request for comment on revised formats

FEDERAL RESERVE SYSTEM 12 CFR Part 203 [Regulation C; Docket No. R-1186] HOME MORTGAGE DISCLOSURE AGENCY: Board of Governors of the Federal Reserve System. ACTION: Request for comment on revised formats

What s New in Mortgage Lending Compliance?

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

What s New in Mortgage Lending Compliance? Michael R. Christians Senior Federal Compliance Counsel Credit Union National Association Copyright 2016 by Credit Union National Association. All rights reserved.

Sue Quilty, Quilty & Associates (781)

") Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

Sue Quilty, Quilty & Associates susan.quilty@verizon.net (781)706-9235 Agenda HMDA Today: Review HMDA in the Future: Proposed Changes Surviving HMDA Reporting 2 HMDA Review HMDA Overview Why is HMDA Important

COMMERCIAL LOAN APPLICATION

COMMERCIAL LOAN APPLICATION Application Received Date: If more than one applicant is applying for financing, indicate if you are applying jointly by initialing below APPLICANT BUSINESS ENTITY Is your business

COMMERCIAL LOAN APPLICATION Application Received Date: If more than one applicant is applying for financing, indicate if you are applying jointly by initialing below APPLICANT BUSINESS ENTITY Is your business

Home Mortgage Disclosure Act. with Anne Lolley. / X4

TOTAL TRAINING SOLUTIONS SPECIAL CREDIT UNION WEBINAR HMDA Home Mortgage Disclosure Act with Anne Lolley DECEMBER 2014 alolley@cox.net / 877-778-5192 X4 Copyright Total Training Solutions and Anne Lolley

TOTAL TRAINING SOLUTIONS SPECIAL CREDIT UNION WEBINAR HMDA Home Mortgage Disclosure Act with Anne Lolley DECEMBER 2014 alolley@cox.net / 877-778-5192 X4 Copyright Total Training Solutions and Anne Lolley

Major Changes Looming for HMDA Reporting

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Major Changes Looming for HMDA Reporting CLIENT ALERT September 25, 2017 Scott D. Samlin samlins@pepperlaw.com Mark T. Dabertin dabertinm@pepperlaw.com In this article, we review the requirements of the

Non-Owner Occupied Fixed Rate Home Equity Loan

Whether you are looking to refinance an existing mortgage, finance large expenses like tuition, home improvements or debt consolidation, or secure a line of credit to keep available, we have the loans

Whether you are looking to refinance an existing mortgage, finance large expenses like tuition, home improvements or debt consolidation, or secure a line of credit to keep available, we have the loans

Home Mortgage Disclosure Act HMDA Part 1. Presented by: Aaron Kouhoupt, Esq.

Home Mortgage Disclosure Act HMDA Part 1 Presented by: Aaron Kouhoupt, Esq. Timeline January 1, 2018 Coverage and collection of expanded data required under new rule (Be careful!) March 1, 2019 Report

Home Mortgage Disclosure Act HMDA Part 1 Presented by: Aaron Kouhoupt, Esq. Timeline January 1, 2018 Coverage and collection of expanded data required under new rule (Be careful!) March 1, 2019 Report

Revised HMDA Reporting Overview, Implementation and Planning March 2017

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

Revised HMDA Reporting Overview, Implementation and Planning March 2017 Kathy Keller, Managing Director, Regulatory Compliance, Newbold Advisors, LLC NewboldAdvisors.com Agenda Overview of the New HMDA

Legal Description of Subject Property (attach description if necessary) Property will be: Refinance Construction-Permanent

Property will be: Refinance Construction-Permanent") This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

PERSONAL FINANCIAL STATEMENT AS OF

Applicant Name PERSONAL FINANCIAL STATEMENT AS OF PERSONAL INFORMATION Co-Applicant Name Home Address Home Address H o m e P h o n e N o. S o c i a l S e c u r i t y N o. of Birth H o m e P h o n e N o.

Applicant Name PERSONAL FINANCIAL STATEMENT AS OF PERSONAL INFORMATION Co-Applicant Name Home Address Home Address H o m e P h o n e N o. S o c i a l S e c u r i t y N o. of Birth H o m e P h o n e N o.

First National Bank MULTI-PURPOSE LOAN APPLICATION

If you intend to apply for joint credit, please initial here. YOUR PERSONAL HISTORY & LOAN REQUEST TYPE OF LOAN (Check All That Apply) INDIVIDUAL JOINT UNSECURED SECURED PURPOSE OF APPLICATION (Check All

If you intend to apply for joint credit, please initial here. YOUR PERSONAL HISTORY & LOAN REQUEST TYPE OF LOAN (Check All That Apply) INDIVIDUAL JOINT UNSECURED SECURED PURPOSE OF APPLICATION (Check All

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower" or "Co-Borrower",

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower" or "Co-Borrower",

ITEMS TO BE SUBMITTED WITH HOME EQUITY LOAN APPLICATION

ITEMS TO BE SUBMITTED WITH HOME EQUITY LOAN APPLICATION Bring In: Pay stubs from the last 30 days W-2 s and Tax Returns from the last 2 years Bank Statements from last 2 months (All Pages) Copy of Homeowner

ITEMS TO BE SUBMITTED WITH HOME EQUITY LOAN APPLICATION Bring In: Pay stubs from the last 30 days W-2 s and Tax Returns from the last 2 years Bank Statements from last 2 months (All Pages) Copy of Homeowner

HMDA Update Nov. 13, Nov. 13, 2018 HMDA Update 1. Our Agenda Today

HMDA Update Panel Discussion: Ongoing Challenges & Solutions Nov. 13, 2018 HMDA Update 1 Our Agenda Today HMDA Partial Exemption Common Data Collection Exceptions Panel Discussion The future of HMDA Nov.

HMDA Update Panel Discussion: Ongoing Challenges & Solutions Nov. 13, 2018 HMDA Update 1 Our Agenda Today HMDA Partial Exemption Common Data Collection Exceptions Panel Discussion The future of HMDA Nov.

PERSONAL FINANCIAL STATEMENT. In Dollars (Omit cents)

") PERSONAL FINANCIAL STATEMENT IMPORTANT: Read these directions before completing this Statement. If you are applying for individual credit in your own name and are relying on your own income or assets of

PERSONAL FINANCIAL STATEMENT IMPORTANT: Read these directions before completing this Statement. If you are applying for individual credit in your own name and are relying on your own income or assets of

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

P E R S O N A L F I N A N C I A L S T A T E M E N T

Businesspurpose credit * in my name or that I personally guaranty. I am relying solely on my income and assets as the basis for repayment. Instructions: Complete this statement based on your financial

Businesspurpose credit * in my name or that I personally guaranty. I am relying solely on my income and assets as the basis for repayment. Instructions: Complete this statement based on your financial

CONSUMER CREDIT APPLICATION

CONSUMER CREDIT APPLICATION CREDIT REQUEST Which product are you applying for? Personal Loan Term Requested: Overdraft Protection for Account #: Personal Line of Credit Amount Requested: Loan Purpose (check

CONSUMER CREDIT APPLICATION CREDIT REQUEST Which product are you applying for? Personal Loan Term Requested: Overdraft Protection for Account #: Personal Line of Credit Amount Requested: Loan Purpose (check

Home Mortgage Disclosure (Regulation C)

") October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting

October 2017 OMB Control No. 3170-0008 Home Mortgage Disclosure (Regulation C) Small Entity Compliance Guide Version Log The Bureau updates this guide on a periodic basis. Below is a version log noting

Business - Loan Application

Type of Request: IMPORTANT INFORMATION ABOUT PROCEDURES FOR APPLYING FOR A LOAN LOAN REQUEST Joint (Complete Co-Applicant Section) Business - Loan Application To help the government fight the funding of

Type of Request: IMPORTANT INFORMATION ABOUT PROCEDURES FOR APPLYING FOR A LOAN LOAN REQUEST Joint (Complete Co-Applicant Section) Business - Loan Application To help the government fight the funding of

FIXED RATE SECOND MORTGAGE LOANS

FIXED RATE SECOND MORTGAGE LOANS WHY T LET THE EQUITY IN YOUR HOME WORK FOR YOU? Having equity in your home is a huge advantage of home ownership. You can use your equity for home improvements, tuition,

FIXED RATE SECOND MORTGAGE LOANS WHY T LET THE EQUITY IN YOUR HOME WORK FOR YOU? Having equity in your home is a huge advantage of home ownership. You can use your equity for home improvements, tuition,

BUSINESS LOAN APPLICATION COMPANY INFORMATION

BUSINESS LOAN APPLICATION Thank you for considering your Credit Union for your business borrowing needs. Your Credit Union will be utilizing the services of Cooperative Business Services, LLC ("CBS") to

BUSINESS LOAN APPLICATION Thank you for considering your Credit Union for your business borrowing needs. Your Credit Union will be utilizing the services of Cooperative Business Services, LLC ("CBS") to

Branch: If this is an application for joint credit with another person, complete all Sections providing information in B about the joint applicant.

Branch: If you need help completing this application, please contact us IMPORTANT: Read these Directions before completing this Application. (Check appropriate box) If you are applying for individual credit

Branch: If you need help completing this application, please contact us IMPORTANT: Read these Directions before completing this Application. (Check appropriate box) If you are applying for individual credit

CFPB Home Mortgage Disclosure Act (HMDA) Final Rule. Webinar August 4, 2016

Final Rule. Webinar August 4, 2016") CFPB Home Mortgage Disclosure Act (HMDA) Final Rule Webinar August 4, 2016 Topics Regulation C, the Bureau s HMDA rule 1. Overview of the final rule 2. Institutional coverage 3. Transactional coverage

CFPB Home Mortgage Disclosure Act (HMDA) Final Rule Webinar August 4, 2016 Topics Regulation C, the Bureau s HMDA rule 1. Overview of the final rule 2. Institutional coverage 3. Transactional coverage

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

Uniform Residential Loan Application

To be completed by the Lender: Lender Loan No./Universal Loan Identifier Agency Case No. Verify and complete the information on this application. If you are applying for this loan with others, each additional

To be completed by the Lender: Lender Loan No./Universal Loan Identifier Agency Case No. Verify and complete the information on this application. If you are applying for this loan with others, each additional

A Guide to Data File Extracts

A Guide to Data File Extracts MARQUIS 5160 Tennyson Parkway Suite 1000E Plano, TX 75024 Technical Support: (800) 627-5388 Sales/Training/Consulting: (800) 365-4274 www.gomarquis.com 1 Copyright 1996-2014.

A Guide to Data File Extracts MARQUIS 5160 Tennyson Parkway Suite 1000E Plano, TX 75024 Technical Support: (800) 627-5388 Sales/Training/Consulting: (800) 365-4274 www.gomarquis.com 1 Copyright 1996-2014.

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower" or "Co-Borrower",

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower" or "Co-Borrower",

HOME MODEL YEAR HOME MANUFACTURER HOME LENGTH HOME WIDTH LOT RENT STREET ADDRESS OF MANUFACTURED HOME CITY STATE ZIP CODE

STERLING ASSOCIATES MANUFACTURED HOME FINANCING TEL. (800) 286-8073 / FAX (508) 234-1557 / WWW.MHBANKER.COM / 49 CHURCH ST. WHITINSVILLE, MA 01588 Sean Rogers- NMLS # 688947 *** Jeffrey Kosinski- NMLS#

STERLING ASSOCIATES MANUFACTURED HOME FINANCING TEL. (800) 286-8073 / FAX (508) 234-1557 / WWW.MHBANKER.COM / 49 CHURCH ST. WHITINSVILLE, MA 01588 Sean Rogers- NMLS # 688947 *** Jeffrey Kosinski- NMLS#

APPLICATION FOR CREDIT

APPLICATION FOR CREDIT APPLICANT (A) FULL NAME - Last, First, Middle Birthdate (mm/dd/yy): Social Security Number: Sex: (opt.) circle one Marital Status: please circle one # Dependents: Ages of Dependents:

APPLICATION FOR CREDIT APPLICANT (A) FULL NAME - Last, First, Middle Birthdate (mm/dd/yy): Social Security Number: Sex: (opt.) circle one Marital Status: please circle one # Dependents: Ages of Dependents:

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT

Dear Loan Applicant, Thank you for your interest in obtaining a loan through Murphy Bank. We at Murphy Bank hope that we can set up a loan that will be just what you are looking for. Attached is an application

Dear Loan Applicant, Thank you for your interest in obtaining a loan through Murphy Bank. We at Murphy Bank hope that we can set up a loan that will be just what you are looking for. Attached is an application

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

Business Purpose/Commercial Loan Application

Business Purpose/Commercial Loan Application Applicants should complete this from (including the referenced addenda, if applicable) as Borrower or Co-Borrower, as applicable. Co-Borrower information must

Business Purpose/Commercial Loan Application Applicants should complete this from (including the referenced addenda, if applicable) as Borrower or Co-Borrower, as applicable. Co-Borrower information must

Procedures for Denying Loans at the Branch Level (Updated )

") Procedures for Denying Loans at the Branch Level (Updated 2-22-2018) Applies to Loans in the Active Pipeline as well as Loans in the Pre-Approval Pipeline -----------------------------------------------------------------------------------------------

Procedures for Denying Loans at the Branch Level (Updated 2-22-2018) Applies to Loans in the Active Pipeline as well as Loans in the Pre-Approval Pipeline -----------------------------------------------------------------------------------------------

HMDA Road Trip: Get Directions Before Navigating the Expanded Data Fields, Including the GMI. October 4, 2017

HMDA Road Trip: Get Directions Before Navigating the Expanded Data Fields, Including the GMI October 4, 2017 Wolters Kluwer HMDA Webinar Series 1. June 29, 2017 HMDA: The Ultimate Road Trip - Pre-Trip

HMDA Road Trip: Get Directions Before Navigating the Expanded Data Fields, Including the GMI October 4, 2017 Wolters Kluwer HMDA Webinar Series 1. June 29, 2017 HMDA: The Ultimate Road Trip - Pre-Trip

HOME EQUITY LINE OF CREDIT APPLICATION PACKET

HOME EQUITY LINE OF CREDIT APPLICATION PACKET Thank you for applying for a Home Equity Line of Credit with Investors Bank. We will consider loans on one to four family homes which are owner-occupied as

HOME EQUITY LINE OF CREDIT APPLICATION PACKET Thank you for applying for a Home Equity Line of Credit with Investors Bank. We will consider loans on one to four family homes which are owner-occupied as

Borrower SIGNATURE REQUIRED ONLY IF APPLYING FOR JOINT CREDIT Co-Borrower SIGNATURE REQUIRED ONLY IF APPLYING FOR JOINT CREDIT

HOME EQUITY FIXED RATE LOAN APPLICATION Sign Below Only If this is an application for joint credit, Applicant and Co-Applicant each agree that we intend to apply for joint credit X X Borrower SIGNATURE

HOME EQUITY FIXED RATE LOAN APPLICATION Sign Below Only If this is an application for joint credit, Applicant and Co-Applicant each agree that we intend to apply for joint credit X X Borrower SIGNATURE

MEMBER FDIC. Initial: Page 1 of 4

MEMBER FDIC EQUAL HOUSING OPPORTUNITY Main Office Northeast Branch University Branch North Pole Branch Delta Branch 500 Fourth Ave. 1248 Old Steese Hwy. 1380 University Ave. 45 St. Nicholas Dr. 1380 Richardson

MEMBER FDIC EQUAL HOUSING OPPORTUNITY Main Office Northeast Branch University Branch North Pole Branch Delta Branch 500 Fourth Ave. 1248 Old Steese Hwy. 1380 University Ave. 45 St. Nicholas Dr. 1380 Richardson

HOME EQUITY LINE OF CREDIT APPLICATION PACKET

HOME EQUITY LINE OF CREDIT APPLICATION PACKET Thank you for applying for a Home Equity Line of Credit with Investors Bank. We will consider loans on one to four family homes which are owner-occupied as

HOME EQUITY LINE OF CREDIT APPLICATION PACKET Thank you for applying for a Home Equity Line of Credit with Investors Bank. We will consider loans on one to four family homes which are owner-occupied as

Property Information

LOAN APPLICATION Page 1 of 7 Property Information Street Address City State Zip Purchase Price $ Estimated Property Value $ Requested Loan $ OR Requested LTV % What is the estimated property value based

LOAN APPLICATION Page 1 of 7 Property Information Street Address City State Zip Purchase Price $ Estimated Property Value $ Requested Loan $ OR Requested LTV % What is the estimated property value based

Instructions for Completing the Uniform Residential Loan Application

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Kemba Commercial Loan Application

Kemba Commercial Loan Application GENERAL BUSINESS INFORMATION Applicant: DBA: Business Address: Business Phone: Legal Status:! Individual(s)! Corporation (C Corp)! LLC! LP/LLP! S Corp! Other: Date Founded:

Kemba Commercial Loan Application GENERAL BUSINESS INFORMATION Applicant: DBA: Business Address: Business Phone: Legal Status:! Individual(s)! Corporation (C Corp)! LLC! LP/LLP! S Corp! Other: Date Founded:

HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

FACILITATE THOUGHT ENGAGE DIALOGUE ENCOURAGE SMART RISK CULTIVATE A NETWORK BUILD KNOWLEDGE HMDA FACT SHEET YOUR MAP TO REGULATORY CHANGE Regulation C implements the Home Mortgage Disclosure Act (HMDA),

Executive Summary of the 2018 HMDA Interpretive and Procedural Rule

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

Bureau of Consumer Financial Protection 1700 G Street NW Washington, D.C. 20552 August 31, 2018 Executive Summary of the 2018 HMDA Interpretive and Procedural Rule On August 31, 2018, the Bureau of Consumer

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "Co-," as applicable. Co-

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "Co-," as applicable. Co-

2900 Decker Drive, Baytown, TX HOME EQUITY LOANS COMPLETE THIS SIMPLE WORKSHEET TO SEE IF YOU QUALIFY!

2900 Decker Drive, Baytown, TX 77521 281.422.3611 www.crcu.org HOME EQUITY LOANS How can I use the money from a Community Resource Credit Union Home Equity loan? Education Debit and / or Credit Card Consolidation

2900 Decker Drive, Baytown, TX 77521 281.422.3611 www.crcu.org HOME EQUITY LOANS How can I use the money from a Community Resource Credit Union Home Equity loan? Education Debit and / or Credit Card Consolidation

HMDA / Regulation C Amendments New 1003 Application

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

HMDA / Regulation C Amendments New 1003 Application January 2017 1Nations Direct Mortgage, LLC Mission Statement - To lead the third party residential mortgage industry by providing products and services

Please submit all of the above forms via one of the following options:

Dear Applicant(s): Thank you for applying for a Home Equity Loan with Investors Bank. In order to begin the application process, please complete the paperwork within this Application Packet: 1. ECOA Notice

Dear Applicant(s): Thank you for applying for a Home Equity Loan with Investors Bank. In order to begin the application process, please complete the paperwork within this Application Packet: 1. ECOA Notice

Home Mortgage Disclosure Act Report ( ) Submitted by Jonathan M. Cabral, AICP

Submitted by Jonathan M. Cabral, AICP") Home Mortgage Disclosure Act Report (2008-2015) Submitted by Jonathan M. Cabral, AICP Introduction This report provides a review of the single family (1-to-4 units) mortgage lending activity in Connecticut

Home Mortgage Disclosure Act Report (2008-2015) Submitted by Jonathan M. Cabral, AICP Introduction This report provides a review of the single family (1-to-4 units) mortgage lending activity in Connecticut

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "", as applicable. information must also be provided (and the

This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "", as applicable. information must also be provided (and the

PROPERTY INFORMATION

CHECK BOX FOR JOINT ACCOUNT: [ ] If you are applying for a joint account or an account that you and another person will use, complete all sections, providing information about the Joint Applicant or user.

CHECK BOX FOR JOINT ACCOUNT: [ ] If you are applying for a joint account or an account that you and another person will use, complete all sections, providing information about the Joint Applicant or user.

Executive DataBook 2014 ORIGINATION TRENDS

ONE VOICE. ONE VISION. ONE RESOURCE. Executive DataBook 2014 ORIGINATION TRENDS Prepared by MBA Research & Economics mba.org/research 15531 Executive DataBook 2014 ORIGINATION TRENDS Prepared by MBA Research

ONE VOICE. ONE VISION. ONE RESOURCE. Executive DataBook 2014 ORIGINATION TRENDS Prepared by MBA Research & Economics mba.org/research 15531 Executive DataBook 2014 ORIGINATION TRENDS Prepared by MBA Research

Presentation Topics. Changing Data Requirements Will Effect. Census data update and implications for CRA, HMDA and Fair Lending

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Changing Data Requirements Will Effect the CRA and Fair Lending Environment Prepared for the 2012 National Community Reinvestment Conference by Glenn Canner March 28, 2012 The views expressed are those

Consumer Financial Protection Bureau. March 15, Draft, Sensitive and Pre-Decisional Not for External Distribution

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Consumer Financial Protection Bureau March 15, 2016 Draft, Sensitive and Pre-Decisional Not for External Distribution Outline Home Mortgage Disclosure Act 1) Background 2) Rule Making 3) Changes Coming

Fewer Applications, Falling Denial Rates

August 2016 Fewer Applications, Falling Denial Rates Identifying Home Loan Trends in Tennessee from Home Mortgage Disclosure Act (HMDA) Data Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE

August 2016 Fewer Applications, Falling Denial Rates Identifying Home Loan Trends in Tennessee from Home Mortgage Disclosure Act (HMDA) Data Hulya Arik, Ph.D. Tennessee Housing Development Agency TABLE

Uniform Residential Loan Application

#ADV Southwest Mortgage Loans, INC, NMLS# 402333 This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "", as applicable.

#ADV Southwest Mortgage Loans, INC, NMLS# 402333 This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "", as applicable.

Uniform Residential Loan Application

FIRST NATIONAL BANK OF MOOSE LAKE, NMLS # 401475 Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete

FIRST NATIONAL BANK OF MOOSE LAKE, NMLS # 401475 Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete

FIRST BANK OF MANHATTAN MORTGAGE LOAN ORIGINATORS NMLS ID #405508

ITEMS TO BE SUBMITTED WITH MORTGAGE PREAPPROVAL APPLICATION Bring In: Pay stubs from the last 30 days W-2 s and Tax Returns from the last 2 years Bank Statements from last 2 months (All Pages) Copy of