Credit Line Use and Availability in the Financial Crisis: The Role of Hedging

|

|

|

- Pamela Hardy

- 6 years ago

- Views:

Transcription

1 Credit Line Use and Availability in the Financial Crisis: The Role of Hedging Jose M. Berrospide Federal Reserve Board Ralf R. Meisenzahl Federal Reserve Board October 2, 2012 Briana D. Sullivan University of California, San Diego Abstract What determined the corporate use of credit lines in the recent financial crisis? To address this question we hand-collect data on credit lines and interest rate hedging for a random sample of 600 COMPUSTAT firms. We document that drawdowns of credit lines had already increased in 2007, earlier than what previous work has found. The surge in drawdowns occurred precisely when disruptions in bank funding markets began. We distinguish between unused and available portions of credit lines, which we then use to disentangle credit supply and credit demand effects. On the supply side, we find covenant-induced reduction of credit supply to be small, and almost no evidence of credit line cancelations. On the demand side, our results confirm that while smaller and lower-rated firms use their credit lines more intensively in general, larger and higher-rated firms were more likely to draw on their credit lines during the financial crisis. We find that firms that use interest rate swaps to hedge the interest rate risk associated with their credit lines draw down significantly more from those lines than non-hedged firms. JEL Codes: G31, G32 Keywords: Credit Lines, Financial Crisis, Liquidity Management, Hedging. jose.m.berrospide@frb.gov, ralf.r.meisenzahl@frb.gov, & bdsulliv@ucsd.edu. Mailing address: Federal Reserve Board, 20th and C Streets NW, Washington, DC We thank Eric Hardy and Eric Kennedy for excellent research assistance. We thank Ian Christensen, Nada Mora, Rodney Ramcharan, Skander Van den Heuvel, seminar participants at the BIS, ECB, Federal Reserve Board, and participants of the BIS s Research Task Force workshop in Istanbul and the 2012 EEA-ESEM for helpful comments. The views expressed here are our own and do not necessarily reflect the views of the Board of Governors or the staff of the Federal Reserve System.

2 1 Introduction Credit lines are the most common type of bank lending. By extending these lines, banks commit to provide liquidity on demand during a contract period. Committed credit lines insure against future liquidity shocks, particularly during times of low market liquidity that is, when firms have only limited access to debt and equity markets. However, this insurance is not complete. Credit line use is contingent on firms compliance with financial covenants (restrictions on leverage, earnings, and collateral) and on banks ability or willingness to supply the committed funds. In this paper we study firm-specific credit line drawdown behavior and covenant-induced reduction in credit line availability during the financial crisis. We collect quarterly data on credit lines and interest rate hedging from regulatory filings for 600 public U.S. companies. The unique feature of our panel data is that we can track credit line drawdowns and availability at the firm level, which also allows us to separate supply and demand effects in the use of credit lines during the financial crisis. Our analysis has two main components. First, we study which firms were able to draw on their credit lines, and the timing and purpose of the credit-line drawdowns. Second, as credit lines have floating interest rates, we separate and quantify demand effects using interest rate derivative data. In particular, as explained below, we propose and test an interest rate risk channel, by which interest rate hedging increases credit line use. We also distinguish credit supply effects stemming from a covenant channel a reduction in credit line availability due to debt covenant violations and test whether interest rate hedging mitigates this channel. Previous work on credit lines provides evidence of increased drawdowns during the recent financial crisis. However, most of this work uses either aggregate, anecdotal, or survey data, which lacks detailed information at the firm level. For instance, Ivashina and Scharfstein (2010) document an increase in C&I lending associated with a rise in drawdowns of corporate credit lines. They use aggregate bank lending data and provide anecdotal evidence of firms that in response to the Lehman failure drew on credit lines due to uncertainty about banks ability to provide liquidity in the future. Similarly, Campello, Graham, and Harvey (2010) and Campello, Giambona, Graham, and Harvey (2011) study the use of corporate credit lines during They use CFO survey data and provide evidence of large credit-line drawdowns of financially-constrained firms. We extend this analysis in several ways. First, using our firm-level data we document a novel fact related to credit-line drawdown behavior during the financial crisis. Drawdowns accelerated in 2007:Q3, earlier than what previous work has found. The surge in drawdowns occurred precisely when disruptions in bank funding markets began, in particular, when the asset-backed commercial paper (ABCP) market collapsed. Drawdowns increased significantly after the Bear Stearns failure, 1

3 and peaked after the collapse of Lehman Brothers. From a bank s perspective, this drawdown behavior became the realization of off-balance sheet risks and provided a rationale for the bank liquidity hoarding that Cornett, McNutt, Strahan, and Tehranian (2011) document during the crisis. 1 Second, we study differences in drawdown behavior by firm characteristics. Our results indicate that smaller firms tended to draw on their lines early in the crisis, whereas, consistent with the anecdotal evidence in Ivashina and Scharfstein (2010), larger firms accounted for most drawdowns around the Lehman collapse. Third, credit availability, measured as change in credit limits due to binding debt covenants, decreased only after the Lehman failure, and only for firms that enter the crisis with weaker financing prospects. After documenting new facts in the credit-line drawdown behavior, the second part of our analysis uses information on interest rate derivatives to study credit supply and demand effects in more detail. On the demand side, we hypothesize that increased uncertainty about the future cost of credit was a crucial determinant of credit-line drawdowns. This is the case because credit line interest rates are usually indexed to the LIBOR the London Interbank Offered Rate which exhibited unprecedented volatility during the crisis. Firms that hedge interest rate risk mitigate the impact of future uncertainty on borrowing costs and, therefore, are more likely to use their credit lines in times of high uncertainty. We test this interest rate risk channel and find that the use of interest rate swaps to hedge the interest rate risk associated with credit facilities accounts for increased drawdowns of up to 6.7 percentage points for the average firm, and up to 8.5 percentage points for investment grade firms. Furthermore, our evidence suggests that firms drew on their credit lines to finance current operations. Hedged firms borrowed more by drawing down their credit lines when cash flows decreased at the start of the financial crisis in 2007:Q3, and repaid this debt when cash flows recovered in mid inventories. These firms also exhibit increases in their Compared with hedged counterparts, unhedged firms decreased inventories during the crisis. Contrary to a common view, we find little evidence that hedged firms hoard additional cash. This was the case at least during the crisis period. On the supply side we study the effect of debt covenants on drawdowns. The data show that not all firms have access to their credit lines because debt covenants can restrict the remaining available credit to a fraction of the unused credit line. 2 We find that credit line availability was only reduced 1 Drawdowns from ABCP back-up lines, and anticipated losses in loans and securities holdings are other liquidity hoarding motives (Berrospide, 2012). 2 A specific example helps to clarify the difference between unused and available portions of a credit line. The K of IEC Electronics Corp. states that:..., IEC has a line of credit with a maximum borrowing limit up to $6.0 mill based upon advances on eligible accounts receivable and inventory. Hence, the unused portion is $6 mill less the used portion. However, according to IEC s 10-K, the base formula for the available portion is the minimum of (1) $6 mill and (2) 0.85*accounts receivable+0.35*inventory. Cash flow and leverage based formulas are also common. In other cases, the available portion is reduced by letters of credit or by the use of commercial paper facilities. It follows that the maximum amount a firm can still draw is the available portion less the used portion. Unused commitments therefore tend to overstate credit availability to firms. 2

4 for smaller firms between mid-2009 and mid Disatnik, Duchin, and Schmidt (2010) postulate that hedging makes debt covenants less likely to be a binding constraint. Consistent with this covenant channel, we find that covenants are less binding for hedged firms. However, this effect which accounts for 12.7 percentage points of the credit line availability at the 10th percentile of the availability distribution is economically small when we consider all the firms in the sample. We account for potential simultaneity between drawdowns and use of interest rate derivatives, and for potential endogeneity in the decision to use interest rate derivatives. We account for those issues in several ways. First, we identify hedging firms (e.g. interest rate swap users) with a dummy variable, which is our main explanatory variable and enters all our regression models with a lag. Second, we use fixed effect regressions, which implicitly control for unobserved firm characteristics (e.g. managerial skills) that remain constant from quarter-to-quarter. These two procedures alleviate simultaneity concerns. Third, we model the decision to hedge using a probit model and document that firms with larger credit lines, less tangible assets, and lower bond ratings are more likely to hedge. Using the predicted value from the probit equation we then control for the firm s propensity to hedge in measuring the effect of hedging on the use of credit lines. Nevertheless, establishing causality using quarterly data is challenging. We cannot rule out the possibility that firms hedge in anticipation of future drawdowns. While this issue may complicate the interpretation of our estimated effects of hedging, the results still support the existence of the interest rate risk channel as firms hedge to avoid interest rate risk on anticipated future drawdowns. Our analysis contributes to the liquidity management literature. In line with with previous results, we find a trade-off between cash, credit lines, and hedging decisions. Looking at interest rate derivatives on credit lines, our data indicate a substitution between cash holdings and hedging. For example, the cash share of assets is 7 percent for hedged firms and 14 percent for unhedged firms. This finding suggests a role of interest rate hedging as part of a liquidity management strategy that has not been explored at length in the literature. Finally, hedging may also introduce systematic risk in the spirit of Acharya, Almeida, and Campello (2010). These authors provide a model of systematic liquidity demand in which a large number of firms draw on their credit lines simultaneously. Such systematic drawdowns may pose significant liquidity risk for banks. Our findings suggest that hedging may be a proxy for systematic liquidity demand during times of elevated uncertainty. The paper is organized as follows. Section 2 briefly reviews the literature on credit lines and hedging. In section 3 we describe the data collection process. Next, we present summary statistics and report stylized facts in section 4. The regression framework and the main results are presented in section 5. Section 6 concludes. 3

5 2 Credit Line Use and Hedging This section reviews the theoretical and empirical literature that motivates our analysis. We first review the work on credit lines and then focus on hedging in the context of credit lines. 2.1 Credit Lines - Theory and Evidence The key rationale for firms to have credit lines in the theoretical literature is the ability to insure against liquidity shocks. Specifically, a firm may need liquidity in states of the world in which it has insufficient cash flows either to continue a current project for instance, the firm may be unable to pay for intermediate goods or the wage bill or to realize new investment opportunities. In such an environment, credit lines can be efficient in providing the required funding (Boot, Thakor, and Udell (1987), Holmström and Tirole (1998), and Thakor (2005)). 3 Existing empirical evidence suggests that credit lines are widely used by firms to manage their liquidity needs. For instance, Shockley and Thakor (1997) document that most of the U.S. commercial bank lending to corporations is done via bank loan commitments. More recently, the literature has focused on the determinants of credit line use. Mian and Santos (2011), using data from the Shared National Credit program, document the cyclical behavior of credit line use and refinancing decisions. Sufi (2009) argues that while lines of credit are a liquidity substitute for firms with high cash flow, low cash flow firms rely more on cash as credit line covenants are tied to cash flow. Demiroglu, James, and Kizilaslan (2009), collecting data on bank lines of private firms and using Sufi s sample of publicly listed companies as comparison, show that tight credit conditions reduce access to credit more for privately held firms. Demiroglu and James (2011) provide a review of the evidence on the importance of credit lines on liquidity management. 4 Regarding the impact of financing constraints on firm s liquidity management (e.g. decision between cash and credit lines), Campello, Giambona, Graham, and Harvey (2011) and Campello, Giambona, Graham, and Harvey (2012) use a CFO survey with responses from 31 countries and find that constrained firms (small, private, non-investment grade, and unprofitable) were more likely to draw on their credit lines in the recent financial crisis. This study, which relies on firm information at two points in time, also concludes that constrained firms faced somewhat less favorable conditions for credit line renewal. Santos (2011), using LPC s Dealscan, links credit supply to bank health. 3 Early work on credit lines and their usage shows that firms use credit lines frequently (Shockley and Thakor, 1997). 4 While most of the evidence in the literature uses U.S. data, Jiménez, Lopez, and Saurina (2009) provide evidence from Spanish firms and reach similar conclusions. The authors also conclude that previous default leads to less credit line use, which may be the result of more intense bank monitoring. Lins, Servaes, and Tufano (2010) use an international survey to examine international difference in liquidity policies more closely. They find that firms make grater use of credit lines when external credit markets are poorly developed. 4

6 Here credit supply is measured as loan terms of new credit during and after the crisis. Montoriol- Garriga and Sekeris (2009) and Huang (2010) exploit the Federal Reserve s Survey of Terms of Business Loans to argue that there was a run on credit lines in the financial crisis. Finally, Thakor (2005) and Acharya, Almeida, and Campello (2010) propose models in which a large portion of firms draw on their credit lines simultaneously, for example, in response to an aggregate liquidity shortfall. Thakor (2005) argues that credit lines insure against credit contractions and that overlending may occur in times when debt covenants are not binding. Acharya, Almeida, and Campello (2010) point out that the firm s exposure to aggregate liquidity risk is a key determinant of their choice between cash and credit lines. 2.2 Hedging and Credit Lines There is a large body of theoretical and empirical literature that studies why firms hedge. On the theory side, Stulz (1984) and Smith and Stulz (1985) suggest that hedging helps corporations reduce bankruptcy costs. Hedging may also help reduce underinvestment costs when external funds are costly, by providing capital during low cash flow states (Froot, Scharfstein and Stein, 1993). The empirical literature generally finds positive effects of hedging on risk management and debt capacity (for example, Graham and Rogers (2002) and Guay and Kothari (2003)). Others have argued that firms use derivates for speculative purposes (Faulkender (2005) and Chernenko and Faulkender (2012)). Unlike the vast corporate hedging literature, there are very few studies on the effects of interest rate risk hedging on the use and availability of credit lines. So far, this literature has focused on cash flow hedging because debt covenants featuring cash flow targets may restrict the use of a firm s credit line. The possibility of cash flow hedging in the context of liquidity provision was first studied by Holmström and Tirole (2000). More recently Disatnik, Duchin, and Schmidt (2010) model the fact that credit lines are not fully committed but rather contingent since debt covenants, such as cash flow or leverage restrictions, can reduce the access to credit lines (Nini, Smith, and Sufi (2009), Sufi (2009) and Huang (2010)).They argue that firms hedge their cash flow to maintain access to their credit line. In other words, firms hedge to render the covenant channel irrelevant. Their empirical analysis shows that cash flow hedging firms rely more on credit lines, measured as total credit line size, and less on cash. Campello, Graham, and Harvey (2010) provide survey evidence that the surging interest rates were a constraint in the crisis, but they do not assess this channel separate from quantity constraints or renewals. An early formalization of an interest rate risk channel can be found in Boot, Thakor, and Udell (1987). However, contrary to the empirical evidence, Boot, Thakor, and Udell (1987) assumed that credit lines bear a fixed interest rate and not a floating rate. We are specifically 5

7 interested whether hedging interest rate risk affected drawdown behavior. Hedging interest rates on the credit line reduces the uncertainty about future cost of funding and therefore, hedged firms should use their credit lines more intensely in general. In the crisis interest rate risk increased. As hedged firms are not exposed to this risk, we expect these firms to rely even more on credit lines as source of funding. To our knowledge, there is no empirical evidence on this interest rate risk channel. In sum, the literature on credit lines postulates two hypotheses about the role of hedging in the context of credit lines. First, hedging interest rates increases credit-line drawdowns (interest rate risk channel). Second, hedging should increase credit line availability (covenant channel). We test these two hypothesis and focus our empirical analysis on our proposed interest rate risk channel, that is, on whether hedge firms draw down differentially more during times of higher interest rate uncertainty. 3 Data This section first describes the sampling methods and data sources. We then provide a discussion of the sample properties and provide summary statistics. 3.1 Data Collection Process We use two main data sources: COMPUSTAT and SEC regulatory filings (10-Ks and 10-Qs). Our sample selection criterion for the universe of COMPUSTAT firms is that the firm was in operation in 2006:Q1 and in 2008:Q3, and was not an agricultural, utility, or financial service company. We stratify the remaining firms by industry and size to ensure the representativeness of our sample. We then randomly sample a total of 600 firms in 75 strata. We use the company s name and tax number to obtain the 10-Ks and 10-Qs for each firm from 2006:Q1 to 2011:Q1. To identify credit line users, we conduct a key word search in the regulatory filings. Specifically, we search for credit facility, credit facilities, credit line, credit lines, line of credit, lines of credit, loan facility, loan facilities, revolving facility, term loan, and term loans. We then read the respective paragraphs to extract the relevant information on credit lines and their use. 5 Firms incur fees on the unused portion of their facility or on the total commitment. Firms 5 Since firms sometimes convert credit line debt into term loans, we found including term loan(s) in the search useful. We observe that sometimes term loan facilities are not immediately drawn, though most are drawn within the quarter they are received. We also find situations in which firms have a combination of term loans and delayed draw term loans. These latter term loans must usually be drawn within a year of commitment, otherwise the firm pays a commitment fee on the remaining unused portion. In some other cases, the credit agreement is negotiated to include a revolving line and a term loan; while at other times the term loan is added later. 6

8 may incur a fee if they terminate the agreement prior to the maturity date. A typical credit line contract includes debt covenants in the form of requirements on maximum leverage, minimum profitability and quality of collateral (the most common being receivables and inventories). In some cases, there are also material adverse change (MAC) provisions allowing the lender to terminate the loan agreement if the borrower experiences material changes in its financial conditions. These provisions are subject to legal interpretation, and invoking them usually leads to litigation. 6 The most common interest rates on credit lines are a bank s prime rate or the 1 or 3 month LIBOR. Margins on LIBOR are higher than margins on prime rates. After the financial crisis, many (re-)negotiated lines have minimum interest rates or LIBOR/prime floors. The most common covenant violations are failure to submit the SEC filings on time, minimum EBITDA violations, collateral and cash flow violations, and leverage ratio violations. Generally, after a violation of covenant(s), firms also experience an increase in the LIBOR/prime margin, and the banks will waive the violation and modify the covenants. If a firm experiences violations over several quarters, the firm will either enter into a forbearance agreement and negotiate another line (possibly with another bank), or stop borrowing from existing credit lines. In certain situations, although a company does not violate a covenant, the fact that it exceeds a maximum ratio or falls below a minimum ratio leads to restrictive covenants that limit their borrowing capacity. Our firm level data extracted from regulatory filings includes: the total amount of the credit facility, the amount drawn, the remaining unused amount, the amount available, and information on covenant violations and terms of credit described above (interest rate, maturity, unused commitment fees, and, in some cases, the lender). To identify firms that use interest rate derivatives to hedge interest rate risk of their credit lines, we extend our key word search. More specifically, we require that one of the following strings appears within 1,500 characters around each of the key words in the paragraph above: interest rate agreement, interest rate agreements, interest rate exchange agreement, interest rate exchange agreements, interest rate hedge, interest rate hedges, interest rate swap, or interest rate swaps. We then again read the respective paragraphs to ensure that the firm explicitly states that their hedging activity is related to the credit facility. We note that the number of firms that are engaged in some hedging activity (for example the use of currency swaps to hedge exchange rate risk) is significantly higher than the number of firms hedging the interest rate risk associated with their credit line. In fact, the proximity requirement reduces the number of firms with positive 6 A bank may not invoke MAC provisions when it is in good financial health. However, when needed, a bank may directly influence the volumes of drawdowns by reducing credit availability to borrowers who are not in compliance with covenants, or whose collateral has declined in value. For a more comprehensive discussion, see Sufi (2009) and Huang (2010). 7

9 search results on the hedging key words by about 70 percent. In our sample, 110 firms state hedging activity related to their credit lines. In 12 of these cases, interest rate swaps were a requirement of the original credit agreement (mandatory hedging). We complement our database with financial variables from COMPUSTAT. As additional controls in our analysis we add cash, cash and short term investments, credit ratings, long and short term debt measures, shareholder s equity, total assets, total debt, total expenses, total revenue, and working capital. 3.2 Sample Summary Statistics Table 1 provides summary statistics for firms in our sample and for firms in the whole COMPUSTAT universe. Firm characteristics include size, leverage, cash holdings, cash flows, profits, and asset tangibility. We measure firm size using both, total assets and total revenues, in millions of dollars. Comparing the variables describing firm characteristics in our sample, shown in the top panel of table 1, with those in the COMPUSTAT universe in the bottom panel, we conclude that our sample is representative of the COMPUSTAT universe. Total assets for the average firm in our sample is about $3.3 billion somewhat than higher total assets for average firm in COMPUSTAT($2.6 billion). However, this differece is mostly driven by a few very large firms. The cash to total assets ratio is 21 percent for firms in our sample and 22 percent for the universe of firms in COMPUSTAT. Leverage, measured by the ratio of total debt to total assets is about 23 percent in our sample, slightly above the 19 percent of the COMPUSTAT universe. The market-to-book ratio (defined as book value of liabilities plus market value of equity divided by book value of liabilities plus book value of assets) is about 2.4 in our sample and 2.1 in the COMPUSTAT universe. Table 1 also shows a widespread use of credit lines for firms in our sample. About 75 percent of firms in our sample have a credit line. On average, the ratio of credit line to total assets is 20 percent, relatively similar to the cash ratio, and larger than the cash flow ratio. 7 4 Credit Line Usage of Non-financial Firms during the Crisis This section presents novel facts about credit line drawdowns during the crisis. First, we document credit line usage over the sample period. Second, we study differences by firm size. Third, we 7 For comparison, Sufi (2007) reports that 85 percent of firms in his sample have a line of credit between 1996 and 2003, and the line of credit is about 16 percent of assets. Campello, Giambona, Graham, and Harvey (2011) report average ratio of credit lines of 24 percent of total assets, 12 percent for cash holdings, and 9 percent for cash flows for their sample of 397 U.S. non-financial firms based on their 2009 CFO Survey. The difference in the cash holdings and cash flow ratios reflects not only the differences in our definitions of cash and cash flows relative to theirs, but also the fact that our sample covers the financial crisis period, when as already documented firms significantly boost their cash holdings and savings from cash flows in anticipation of liquidity pressures. 8

10 relate drawdowns to interest rate risk. Last, we split the sample by the firms hedging decisions and study differences in credit line drawdowns and availability. 4.1 Drawdown Patterns For this part of the analysis we focus on the revolving portion of credit lines. The revolving portion is the amount that firms can draw down, repay and continue drawing down for the duration of the facility. Figure 1 shows the revolving portion of credit lines over all firms in our sample. 8 Firms started to tap their revolving credit lines during the first half of 2007 and continued to increase credit line usage after the beginning of the financial panic in short-term funding markets (August 2007). Credit line usage (the solid blue line) increased significantly after the Bear Sterns failure in March 2008, spiked after the collapse of Lehman, and reached a peak during the first quarter of 2009, right before the results of the stress tests for large BHCs were announced. Credit line usage in our sample increased about $14 billion, an increase by almost 100 percent, between 2007 and mid Total revolving lines of credit (red line) followed a similar pattern. They went up by $35 billion during the same period, with almost all of the increase occurring in While the drawdowns before the Lehman collapse have not been documented before, the spike in usage around the Lehman collapse and the reduction in total lines of credit are consistent with the evidence from aggregate data and new syndicated loans presented in Ivashina and Scharfstein (2010). First, we split the sample by firm size. As figure 2 illustrates, large firms account for most of the drawdowns and large firms tend to have a higher credit availability. This evidence is consistent with previous findings on the use of credit lines during the recent financial crisis. First, corporations were increasingly drawing down funds from their committed credit lines, especially after September 2008 (Ivashina and Scharfstein, 2010). Second, constrained firms (small, private, non-investment grade, and unprofitable) are more likely to draw down their credit lines in general (Campello, Giambona, Graham, and Harvey, 2011). However, in the crisis large firms appear to account for most of the drawdowns. Small firms appear to have used their credit lines early in the crisis. A possible explanation for this distinct behavior is that compared with large firms, small ones faced harder liquidity pressures and higher constraints. Larger firms may have been in a better financial position to repay their credit lines soon after interest rates plunged and bond markets returned to normality, providing alternative funding sources again. The timing of the survey used by Campello, Giambona, Graham, and Harvey (2011) may explain the differences in our findings. Small firms appear to have been more constrained than large firms, as measured by the credit line availability 8 We exclude four companies. Anadarko Petroleum Corporation, First Data Management, and ConocoPhillips have large bridge loan facilities due to merger and acquisition activities. Alltel was the target of a LBO. 9 The Lehman failure was not followed by credit line cancelation though the Lehman portion in syndicated loans was typically not taken up by another bank in the syndicate which reduced total revolving lines somewhat. 9

11 to total credit line ratio (figure 2, lower panel). Large firms had higher availability, even at the height of the financial crisis (90 percent on average), whereas small firms faced tighter restrictions as their availability dropped from 90 percent before the crisis to 83 percent after the crisis. Our evidence based on firm size suggests increased credit line use by large firms and tighter constraints for small firms. Next, we split the sample by users of commercial paper. One possible explanation for the drawdown behavior, especially of large firms, is that the disruption of the asset-backed commercial paper (ABCP) market, which is dominated by financial firms, affected non-financial firms ability to issue commercial paper. 10 Gatev and Strahan (2006) suggest that in such a case firms substitute away from commercial paper to drawing on the credit lines that back up commercial paper facilities. We would then expect see an increase in credit line usage and availability for commercial paper issuing firms. However, the upper panel of figure 3 shows that non-financial firms with commercial paper programs did not significantly increase drawdowns during the crisis. 11 Issuing commercial paper reduces credit line availability, in most cases exactly by the amount of commercial paper issuance. The lower panel of figure 3 shows that credit line availability increased for firms with commercial paper programs after the Lehman failure, suggesting that they were either not able or not willing to roll over their short-term commercial paper. Despite this increased availability, the fact that there was not a significant increase in the credit line use of commercial paper issuing firms suggests that these firms reduced their demand for short-term funding. Such lower demand seemed to have occurred in the context of a recession, and even when interest rates were historically low. In sum, our evidence based on commercial paper use suggests that there was no significant increase in credit line drawdowns from commercial paper issuing firms. Having documented the drawdown patterns throughout the crisis, we now relate drawdowns to interest rate movements. Figure 4 compares revolving credit line usage with a common measure of funding pressures on banks, the TED spread (difference in yield between LIBOR and a Treasury Bill of similar maturity) and its 3-month standard deviation. There is a strong and positive correlation between drawdowns and both measures of uncertainty in bank funding markets (correlation coefficient of 0.62 with the TED spread and 0.64 with the 3-month standard deviation of the TED Spread). Moreover, the increase in the TED spread and its volatility seems to predate the use of revolving lines of credit, which suggests that firms decided to draw on their revolving 10 The behavior of financial firms issuing ABCP through conduits and drawing on back-up liquidity lines from banks is beyond the scope of our study since our data includes only non-financial firms. 11 This finding appears to be counterintuitive. However, out of the 33 firms that use commercial paper in our sample, only 4 small firms drew significant amounts (about $200 mill. each) from their credit lines in 2008:Q4. Large firms with commercial paper facilities do not record similar drawdowns. This behavior is consistent with Kacperczyk and Schnabl (2010) who also document that the decline in commercial paper was driven by financial firms and did not affect non-financial firms. 10

12 credit lines in response to the uncertainty created by disruptions in short-term funding markets for banks. This fact is consistent with the anecdotal evidence in Ivashina and Scharfstein (2010), which shows that at least some firms drew on their credit lines in anticipation of potential inability of banks to fund their commitments. After policy interventions, the TED spread returned to precrisis levels, reducing uncertainty about its future behavior. The success of policy intervention in reducing uncertainty about future bank funding, which can be seen in the sharp drop in the TED spread, may explain why many firms appear to have paid off their revolving credit lines, as indicated by the sharp contraction in credit line use after 2009:Q2. The evidence thus suggests that credit-line drawdowns increased with higher interest rate risk. To link drawdowns and interest rate risk more tightly, we provide evidence that these drawdowns were made by firms that hedged their interest rate risk in the next section. 4.2 Credit Line Use, Credit Line Availability, and Interest Rate Hedging Table 2 reports some descriptive statistics for the firms in our sample grouped by their decision to hedge their interest rate exposure. A univariate comparison of key firm characteristics between hedgers and non-hedgers shows some obvious differences between the two groups. 12 Hedged firms are much larger in terms of their total assets and their total revenues. The total assets of the median hedged firm ($1,354 million) are almost two times that of the non-hedged firm ($607 million). The median hedged firm s revenue ($270 million) is more than double that of the non-hedged firm ($147 million). Hedged firms are more levered than their non-hedged counterparts. Leverage for the median hedged firm (38 percent) is twice as large as the leverage of the non-hedged firm (19 percent). Non-hedged firms, however, have more tangible assets. Hedging activity is concentrated in a few sectors. In particular, more than 10 percent of firms in mining, manufacturing, retail trade, and specialized services hedged credit line interest rate risk. Using the comparison between the hedged and non-hedged firms, table 2 also confirms previous findings in the literature on the trade-off between cash holdings and the use of credit lines in the presence of hedging. Having access to more funds from credit facilities, hedged firms also depend less on cash holdings. The cash-to-assets ratio is only 4 percent for the median hedged firm relative to the ratio of 9 percent for the median non-hedged firms. The differences in size, leverage, credit line use and availability, and cash holdings are all significant at the 1 percent level. To illustrate the difference in use of credit facilities and access to credit facilities between 12 Throughout the paper we use the terms hedged and non-hedged firms loosely as synonyms for interest rate swap users and non-users. As already mentioned, our definition of hedging is constrained to mitigating the interest rate risk associated with the used portion of the credit line, either the revolving component or the term loan component. Furthermore, some work in the hedging literature argues that it is not clear whether firms use interest rate derivatives for hedging purposes or for speculation. For further details, see for example Faulkender (2005). 11

13 interest rate swap users and non-users, figure 5 depicts the use (top panel) and availability of credit lines (bottom panel) for the two types of firms. Hedged firms have greater availability and use disproportionally more of their credit lines than their non-hedged counterparts. The median hedged firm has a ratio of credit lines to total assets (34 percent) that is two times larger than the ratio of their non-hedged counterpart (17 percent). Moreover, the used credit line as a percentage of total assets is much larger for the median hedged firm (63 percent versus 8 percent). Although there is only a small difference in the availability ratio between the two groups, the differences in credit line use are striking. Derivative users drew down their credit lines significantly more than non-users during the months leading to the financial crisis. The used portion increased from 50 percent before 2008 to 65 percent during the fall of This behavior notably contrasts with credit lines use by non-hedged firms. Non-hedged firms kept their credit line use almost constant at 25 percent even during the financial crisis. In short, our univariate analysis based on the decision to hedge indicates that, in general, hedged firms draw down more funds from their credit lines than unhedged firms. Consistent with the interest rate risk channel, hedged firms increase their drawdowns during the crisis more than their non-hedged counterparts. Consistent with the covenant channel, hedged firms have a larger fraction of their credit line available than unhedged firms. 5 Econometric Analysis To determine the effects of interest rate hedging on credit line use we first study the firm s determinants of the decision to have a credit line. Second, we study the key drivers in the decision to hedge interest rate risk associated with credit lines, and then we evaluate the effects of hedging on a firm s ability to draw on its credit line and on its credit availability. Lastly, we address the likely endogeneity in the decision to hedge. 5.1 Determinants of the Credit Line Decision Following Disatnik, Duchin, and Schmidt (2010), we expect that large cash holdings reduce the likelihood of having a credit line. Furthermore, conditional on having a credit line, cash holdings and cash flow should reduce the likelihood of hedging interest rate risk. In addition, we expect that firms with large exposure to interest rate risk namely, firms with large credit lines relative to assets are more likely to hedge. Table 3 reports the results of a probit regression on the decision to have a credit line, measured by a dummy that identifies credit line users. Controlling for firm characteristics, we find that 12

14 firms with large cash holding are less likely to have a credit line. This result holds for different subgroups of firms: investment grade firms, non-investment grade firms, and firms without a bond rating (columns 2 through 4). Our evidence is consistent with previous findings in the literature documenting the substitution between cash holdings and credit lines. We find no significant differences on the credit line decision across firms based on their bond ratings. 5.2 Determinants of the Interest Rate Hedging Decision In the subsample of firms with existing credit lines, we study the determinants of the use of an interest rate swap to hedge the interest rate risk on their credit facilities. Table 4 summarizes the probit regression results for firms that have a credit line and use interest rate derivatives. Consistent with previous results in the literature, firms with more cash holdings are less likely to hedge. The probability of hedging is higher for larger firms, and firms with larger credit lines. We also find that non-investment grade firms are significantly more likely to hedge. In this subgroup, firms with a large share of tangible assets are less likely to hedge, perhaps because tangible assets may work as collateral that allows these firms to finance themselves with senior secured debt on the bond market. 5.3 Hedging and Credit Line Usage Following previous work in the literature of corporate credit lines, we study the effects of hedging on a firm s credit line usage and availability using the following empirical specification: Credit Line ratio i,t = c i + τ t + β 1 Swap i,t 1 + β 2 Crisis t + j λ j Rating j i,t 1 + β 3 Swap i,t 1 Crisis t + j α j Crisis t Rating j i,t 1 (1) + j δ j Swap i,t 1 Crisis t Rating j i,t 1 +γ X i,t 1+ɛ i,t. In this regression specification, our dependent variable Credit Line ratio refers to the ratio of the used portion of a credit line to the total amount of the credit line. Note that the credit line ratio is censored at zero for firms not using their credit lines and at one for firms that have drawn their credit lines completely. Therefore, we employ Tobit models to address the censoring issue. We also estimate fixed effect panel regressions to control for unobserved firm characteristics. In the baseline regressions we include a crisis dummy, spanning from 2007:Q3, when the ABCP 13

15 market collapsed; to 2008:Q4, when policy interventions such as TARP helped contain the turmoil in financial markets. 13 To deal with simultaneity between credit line use and hedging we require that a firm was hedged in the quarter preceding the credit-line drawdown (Swap i,t 1 ). However, fixed costs of hedging may prevent some firms from using interest rate derivatives. We will deal with potential biases in measuring the effect of hedging due to firms ability to hedge and firms willingness to use interest rate derivatives in section 5.5. Here, we will focus on whether the effect of hedging on credit line use varies during the crisis period and across different firms grouped by their credit ratings. Therefore, our most preferred specification includes interaction terms of our lagged swap dummy, a crisis dummy, and firms credit ratings (indexed by j = investment grade, non-investment grade, and no bond rating). We expect the coefficients on Swap t 1, its interaction with Crisis t and its interaction with Crisis t and Rating j i,t 1 to be positive and statistically significant (β 1 > 0, β 3 > 0, δ j > 0). Positive and significant coefficients are consistent with our proposed interest rate risk channel that is, with the hypothesis that hedged firms have larger credit-line drawdowns and increase those during times of high interest rate uncertainty more than unhedged firms. Note that all interaction terms are interactions of dummy variables. Hence, to avoid collinearity issues we omit either an interaction with one rating group, or some double interaction terms. We also include a vector X i,t 1 of lagged firm characteristics that likely influence the firm s use and availability of credit lines such as firm size (log of total assets), cash holdings, cash flow, asset tangibility, the market to book ratio of assets and firms credit ratings (investment grade, non-investment grade and no bond rating). Table 5 presents the regression results of equation (1) for three different specifications. The first specification (columns 1 and 2) uses a pooled Tobit estimation with clustered, robust standard errors to address potential bias due to censoring in our dependent variable. We also include time and industry fixed effects in this regression. Our second specification is a random effects (panel) Tobit regression (columns 3 and 4). Although this latter regression assumes normally distributed random effects, it provides a better fit than the pooled Tobit regression as it controls for firm heterogeneity in the context of a nonlinear panel model. To control for unobserved firm characteristics we use a linear fixed effect model as a third specification (columns 5 and 6). The coefficient on the lagged Swap t 1 dummy is positive and significant across all specifications. The coefficients suggest that credit line use of firms hedging interest rate risk on credit lines is up to 30 percentage points larger than unhedged firms. This is consistent with the summary statistics that exhibit a use of 55 percent of hedged firms and 26 percent of unhedged firms (table 2). The firm fixed effect model shows a smaller coefficient than the pooled Tobit estimates, but this is to 13 We also consider two narrower definitions of the crisis. First, we classify 2008:Q1 to 2008:Q4 as crisis, covering Bears Stearns collapse and the Lehman failure. Second, we only consider the the quarters of the Lehman failure 2008:Q3 and 2008:Q4. We obtain results similar to regressions with the baseline definition. 14

16 be expected. In the fixed effect regression, being hedged accounts for drawdowns that are about 5 percentage points larger. The random effects tobit estimation shows a coefficient of hedging closer to the linear fixed effect model (7 percent) suggesting that unobserved charateristics significantly contribute to the pooled Tobit estmates. By controlling for unobservable factors, we are closer to a causal link from interest rate hedging to credit line use. In the crisis, this effect is even larger. Our estimates on the interaction of the lagged swap and the crisis dummy (β 3 ) are significant in all specifications and suggest that hedged firms increased their drawdowns more than their non-hedged counterparts during the financial crisis, that is, between 2007:Q3 and 2008:Q4. Most of the interaction terms enter the regression with the expected sign. In general, our panel tobit estimates are close to the fixed effect estimates, though they are measured with more sample uncertainty. Thus, in what follows we use the fixed effect model as our most preferred specification. To further investigate the type of firms that were able to increase drawdowns during the crisis using our different interactions between hedging, crisis, and credit rating dummy variables (δ j ), table 6 presents several specifications with using our fixed effect model. For brevity, we omit the coefficients on our firm characteristics. The second specification explores whether different firms indexed by their credit ratings were able to draw more on their lines during the financial crisis; whereas the third specification shows whether hedging allowed a particular group of firms increase their credit line usage. The last specification includes all the interaction terms to disaggregate the combined effects even further. Our results in table 6 indicate that having a credit rating allowed corporations to increase their credit line use during the financial crisis. Column 3 suggests that rated firms increased their drawdowns during the crisis. The coefficients on the triple interaction terms in column 4 suggest that hedged investment grade firms drew down about 8.5 percentage points more than their unhedged counterparts and significantly more than hedged non-investment grade firms. Also hedged firms with no bond rating exhibit significantly larger drawdowns (4.7 percentage points). Column 5 includes all interactions and shows that rated firms increased credit line drawdowns during the crisis regardless of whether they were hedged or not. In other words, when the regression includes both the double interactions between the crisis dummy and the credit ratings dummy, the coefficients of the triple interaction between hedging, crisis and rating for non-investment grade firms turns out to be insignificant. Hedged firms without credit rating also exhibit significantly larger drawdowns (5.6 percentage points) while unrated, unhedged firms did not draw significantly on their lines. This result seems reasonable and is consistent with the idea that in the face of more restricted access to bond or equity markets, unrated firms could have resorted to interest rate hedging to be able to drawdown more from their credit lines during the crisis. When interpreting the results, we have to consider that out of the approximately 100 firms that hedge their interest rate risk in our sample, only about half of them were hedged and had a credit rating. The use of 15

17 multiple interaction terms aimed at identifying different effects simultaneously is thus restricted by a small number of observations in our sample. Although not explicitly shown, our results on firm characteristics are consistent with previous findings in the literature of liquidity management. For example, we find evidence of the trade-off between cash and credit lines. Firms with large cash holdings and large internal cash flows reduce their use of credit lines. Although we interpret this result as suggesting that the causality runs from changes in cash holdings and internal cash flows to changes in the use of credit lines, one could argue that the results may also suggest a reverse causality. 14 Our results also indicate that, on average, firms issuing commercial paper reduce their credit line use by about 30 percentage points. In short, we find that, consistent with the interest rate risk channel, hedged firms were able to drawdown more from their credit lines than their non-hedged counterparts. Hedged firms increased their drawdowns significantly during times of high interest rate uncertainty. We will address some potential benefits of hedging to these firms by exploring how companies used the funds withdrawn from credit lines in section 5.6 below. 5.4 Effect of Hedging on Credit Line Availability We also address the question of whether hedging allows more access to credit lines by alleviating potential covenant restrictions. Covenant restrictions can prevent firms from drawing down from existing credit lines (Sufi (2009), Huang (2010)). Since the likelihood of covenant violations increases during bad economic times, the available credit dropped during the financial crisis. Disatnik, Duchin, and Schmidt (2010) argue that cash flow hedging becomes a valuable corporate strategy because it reduces the probability of covenant violations and therefore maintains credit availability. To test the validity of this argument, we examine the ratio of available lines to total credit lines for the firms in our sample. As mentioned above, firms are required to disclose when a violation of the covenant associated with their credit lines occurs. Covenant violations automatically restrict the availability of credit lines. In other words, when a covenant violation occurs, a firm can only use a portion of the total amount of their existing lines. Therefore, we expect that the line availability ratio, defined here as the sum of used and remaining availableplay a significant role ans our results unused credit line portion, measures the extent to which firms face binding borrowing constraints due to covenant breaches. Table 7 depicts the ratio of available lines to total credit lines (line availability ratio) for hedged and non-hedged firms before, during and after the crisis. The table shows that for different firms 14 At this point we do not control for potential endogeneity problems (except for the fact that we use lagged values for the main explanatory variables) but so far our results are consistent with Campello, Giambona, Graham, and Harvey (2011) who find that cash holdings and cash flow savings reduce the use of committed lines, but fewer drawdowns do not explain large cash holdings and more cash flows. 16

18 within the distribution of the line availability ratio, credit lines became less available after the crisis. This information is consistent with previous empirical evidence suggesting that during bad economic times banks tighten their lending standards and become tougher in negotiating their credit commitments. To further investigate how significant the differences are in credit line availability between hedged and non-hedged firms, we estimate equation (1) with line availability ratio as the dependent variable to test whether hedging increases the firm s access to credit lines. If by smoothing future cash flows interest rate hedging helps corporations ameliorate the possibility of covenant breaching, then we would expect a positive relationship between hedging and line availability. Table 8 shows the results. In addition to our Tobit regressions, we present quantile regressions for the 10th, 25th, and 40th percentiles of the distribution. The results confirm the findings in Table 7. Consistent with the prevalence of debt covenants on leverage and cash flow, higher leverage reduces the available share of the credit line while higher cash flow increases it. In the Tobit regressions, the coefficient on the interest rate swap is small and insignificant for the average firm. The coefficient is larger and statistically significant for firms in the lowest percentiles. The effect is largest in the group that is most constrained the 10th percentile and declines the less constrained firms are. However, the effect of hedging on credit line availability, which accounts for 12.7 percentage points of the total line at the 10th percentile, is economically small when we look at the whole sample. Overall, our findings suggest that interest rate hedging alleviates the impact of automatic covenant restrictions only for a small number of firms. In other words, we find only partial evidence for the existence of the covenant channel. A possible interpretation of this result, given that we examine the hedging decision against a very specific type of risk related to the use of credit lines, is that the benefits of hedging are transmitted through a different channel. As we argue above, interest rate swaps effectively convert floating rates on the used portion of the credit lines into fixed rates. By doing so, interest rate hedging effectively reduces the uncertainty about the cost of credit and allows corporations to draw down more funds from their lines. 5.5 Regression Model with Hedging Propensity One potential issue in measuring the effect of hedging on credit lines is that we may need to distinguish firms that were unable to hedge (for instance, because the amount to be hedged is too small), firms that were able to hedge and chose not to, and firms that hedged. Following Faulkender and Petersen (2011), we expand our previous empirical specification for the credit line ratio and replace our swap dummy with two new variables of interest: the propensity that a firm uses swap contracts to hedge the interest rate risk associated with its credit line Swapi,t 1, and 17

19 the unexplained (residual) component of hedging Swap i,t 1 Swap i,t 1 ; while the first distinction addresses the endogeneity concerns on the decision to hedge, the second distinction identifies the effect of hedging. Credit Line ratio i,t = c i +τ t +β 1 Swap [ i,t 1 + β 2 Swap i,t 1 Swap ] i,t 1 + β 3 Crisis i,t + j λ j Rating j i,t 1 + β 4 Swap i,t 1 Crisis i,t + j α j Crisis i,t Rating j i,t 1 (2) + j δ j Swap i,t 1 Crisis i,t Rating j i,t 1 +γ X i,t 1+ɛ i,t In this specification the effect of interest rate hedging is measured by the coefficient β 2, while the total effect of hedging propensity is given by β 1 β 2. We take Swap as the predicted value from the regression in the first column of table 4. As before, we provide estimates for three models (1) pooled Tobit regressions with firm-level clustered standard errors, industry and time fixed-effects, (2) a random effects Tobit regression to control for unobserved heterogeneity in the context of a panel model and (3) linear fixed-effect regressions with time effects. Table 9 shows the estimation results of equation (2) when our dependent variable is the ratio of used lines to total credit lines. As before, we present the results for two different specifications in each model. The coefficient on hedging propensity is positive and significant in all specifications. This result confirms our findings in section 5.3 that hedged firms are able to draw down their credit lines more than non-hedged firms. Estimates of the pooled Tobit model (columns 1 and 2) show that firms that hedge their interest rate risk with swap contracts have drawdowns from committed lines that are 21 percentage points larger. This estimate is smaller than the estimated effect (30 percentage points) when using only a swap dummy variable. As before, both the random effects Tobit models (columns 3 and 4) and the firm fixed effect model (columns 5 and 6), which control for unobserved firm characteristics, show a positive and significant effect of interest rate hedging on credit line usage, though, as expected, the coefficients are much smaller than the Tobit estimates (by 3 to 4 percentage points). As we did in table 6, we show the estimation results of equation (3) for several specifications that include different interactions between the hedging, crisis and credit rating dummy variables in table 10. The interaction between our Swap and Crisis dummies is significant in the fixed effect regression, indicating that hedged firms were capable of drawing on their credit lines more than unhedged firms during the financial crisis. The coefficients on the triple interaction terms in the fourth specification confirm that hedged investment grade firms were able to draw down more funds 18

20 during the times of financial distress. The linear fixed effect model suggests that hedging was also beneficial for firms without a credit rating. Next, we estimate equation (2) with the credit line availability ratio as dependent variable. Table 11 shows the results. Again, we employ Tobit regressions and quantile regressions for the 10th, 25th, and 40th percentiles of the distribution. The results confirm the findings in section 5.4. After controlling for firm specific characteristics, the coefficient on the interest rate swap, β 2, is close to zero for the average firm. As before, the coefficient is larger and statistically significant for firms in the lowest percentiles, accounting for 11.7 percentage points of the total line at the 10th percentile. In unreported robustness tests we also run two-stage regressions (instrumental variable and simultaneous equation specifications) to address the endogeneity concern on the decision to hedge. For this purpose, we follow the idea that the decision to hedge may be concave in leverage because highly leveraged firms may have no incentives to hedge even if they expect larger bankruptcy costs (see Purnanandam, 2008). We use then the squared value of leverage as an instrument in a first stage probit regression for the decision to hedge. We obtain similar results in the second stage regression that uses the predicted value for our Swap variable from the probit regression. In short, our results in this section confirm that, compared to non-hedged firms, hedged firms draw down more funds from credit lines, particularly during the difficult times of the financial crisis. We also confirm that hedged firms have a somewhat higher credit line availability. However, the effect of hedging on credit line availability is economically small. This finding casts doubt on the covenant channel being the main channel through which hedging affects firm s drawdown behavior. Our results suggest that the drawdown patterns during the crisis are more consistent with the interest rate risk channel. 5.6 Discussion In a nutshell, our results on the role of hedging indicate that firms that hedged the interest rate exposure associated with their credit lines drew down differentially more from those lines when uncertainty about future borrowing cost was high than non-hedged firms. To understand better the potential benefits of hedging for firms, we examine the uses of the funds drawn from credit lines. For this purpose, we look at the firms cash-flows, cash holdings, and inventories in more detail. Figure 6 depicts these key variables for hedged and unhedged firms. As theory suggests, firms are expected to increase credit-line drawdowns during low cash flow states. That was precisely the situation during the fall of 2007 and most of Unhedged firms also appear to make greater use of their credit lines during the time of low cash flows, though the variation in cash flows that exclude drawdowns is considerably less pronounced than for hedged firms. This finding suggests 19

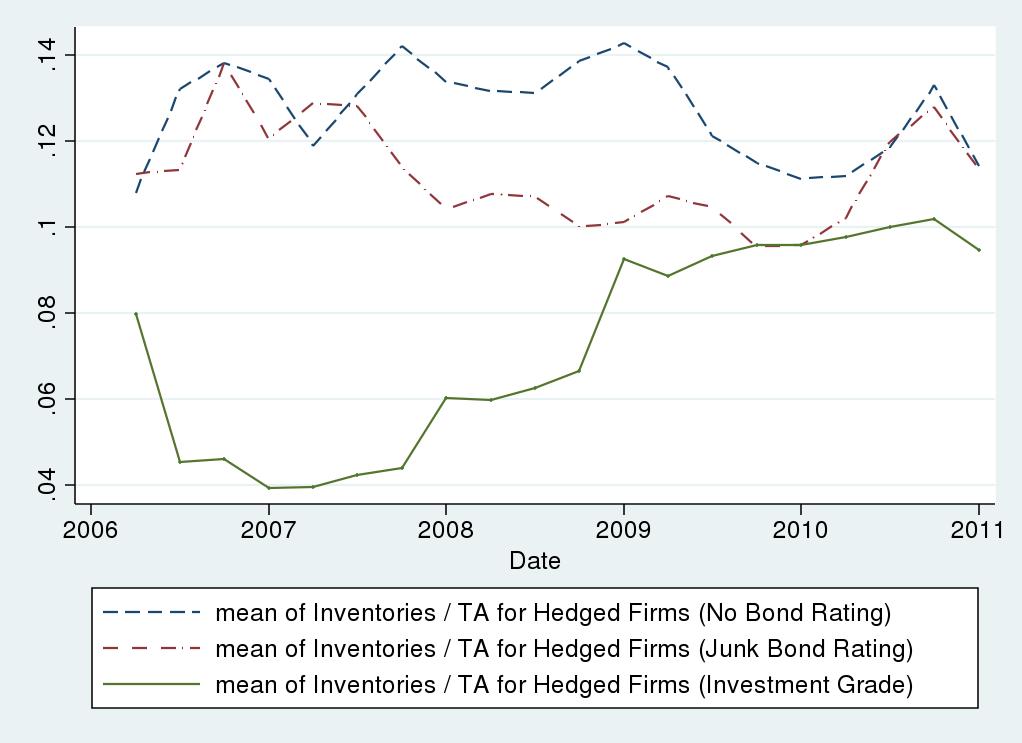

21 that hedged firms rely more on the credit line liquidity put to smooth their cash flows. Cash holdings (second panel of figure 6) shows that neither hedged nor unhedged firms hoarded their drawn funds, at least not at the early stage of the crisis. Hedged firms, for example, reduced their cash holdings until the Lehman failure in September 2008, indicating that drawdowns may have been used to finance current operations. Unhedged firms cash holdings were relatively constant during the crisis. Cash holdings of all, hedged and unhedged, firms increased notably in 2009, suggesting that firms were hoarding cash even after the end of the crisis, perhaps in response to uncertain economic conditions and in anticipation of a slow recovery. Inventories (third panel of figure 6) of all firms, hedged and unhedged, declined early in the crisis. While inventories of unhedged firms started to deteriorate fast in 2008:Q3, inventories of hedged firms increased from 2008:Q3 to 2009:Q2. Splitting the inventories for firms grouped by bond ratings, we find that while the decline in inventories is almost uniform across unhedged firms, hedged firms without bond rating and investment-grade firms increased their inventory during the financial crisis. Our regression results indicate that these two groups had the largest differential drawdowns during the crisis. Thus, our regression results together with the observed pattern in cash flows and inventory suggest that hedged firms use their credit-line drawdowns to avoid scaling back their operations. In other words, hedging allowed them to continue funding current operations with increased drawdowns during the financial crisis. One interpretation of this behavior is that hedged firms were able to bet on fast recovery, which would be consistent with the increase in inventories and the decrease in cash holdings early in the crisis. However, facing a weak economic outlook and low interest rates for an extended period, firms settled their interest rate derivatives, paid off their credit lines, and started to increase their cash holdings by early While we shed light on the purpose of credit line drawdowns, our analysis finds it hard to argue for substantial real effects of hedging. On the one hand drawdowns smooth the cash flows of hedged firms and help them avoid a cut in current production, at least during the first months of the crisis. On the other hand, the temporary increase in inventory may indicate that hedged firms could afford to bet on a short recession and a fast recovery, which did not materialize. In unreported analysis, we fail to find significant effects of hedging on firms investment spending which, again, is consistent with the view that firms may have used interest rate hedging as a first line of protection against increasing uncertainty in borrowing costs. A more detailed analysis of this issue is beyond the scope of the paper. 15 Our data show that almost half of the firms that had interest rate derivates on their credit lines had paid off their swaps by 2010:Q4. 20

22 6 Conclusion Using a unique dataset we document that credit line usage had already increased in 2007 when bank funding markets became more volatile. By distinguishing between unused and available portions of credit lines, we study credit supply and demand effects determining the use and availability of credit lines during the recent financial crisis. Moreover, we consider the role of interest rate hedging on the access, use, and availability of credit lines. On the demand side, we document a strong credit demand starting with the collapse of the ABCP market and spike with the Bear Stearns and Lehman failures. Firms hedging their interest rate exposure on credit facilities drew down significantly more funds than non-hedged firms. Moreover, among hedged firms, investment-grade firms were more likely to draw down their credit lines. During the crisis, having an interest rate swap for a credit facility accounts, on average, for additional drawdowns of up to 6.7 percentage points. This effect is economically large and robust to several specifications. We attribute the significance of our result to the uncertainty associated with the cost of funding the interest rate risk channel during bad economic times. The results of our analysis suggest that hedged firms financed current operations with credit line drawdowns. We find that credit supply measured as a firm s credit line availability exhibits only a small decline during the crisis. This decline is concentrated in firms that entered the crisis with weak financing prospects. Consistent with the covenant channel proposed by Disatnik, Duchin, and Schmidt (2010), we find that covenants are less likely to bind for firms that hedged credit facility interest rate risk. Our results indicate that this effect is large for (severely) constrained firms but is economically small when looking at the full sample. Finally, there are some caveats to our analysis. First, we only study publicly traded firms, which tend to be larger and less financially constrained than privately held firms. Hence, we may overstate credit availability and understate the covenant channel. Second, we assume that firms hedging behavior is explainable by firm characteristics. However, the anticipation of future drawdowns may cause firms to hedge their interest rate risk, reversing the causality of our findings. 21

23 References [1] Acharya, Viral, Hector Almeida, and Murillo Campello Aggregate Risk and the Choice between Cash and Credit Lines. NBER Working paper No Cambridge: National Bureau of Economic Research. [2] Berrospide, Jose M Liquidity Hoarding and the Financial Crisis: An Empirical Evaluation. manuscript, Washington, DC: Federal Reserve Board. [3] Boot, Arnoud, Anjan V. Thakor, and Gregory F. Udell Competition, Risk Neutrality and Loan Commitments. Journal of Banking and Finance Vol. 11(3), pp [4] Campello, Murillo, Erasmo Giambona, John R. Graham, and Campbell R. Harvey Liquidity Management and Corporate Investment During a Financial Crisis. Review of Financial Studies Vol. 24(6), pp [5] Campello, Murillo, Erasmo Giambona, John R. Graham, and Campbell R. Harvey Access to Liquidity and Corporate Investment in Europe During a Financial Crisis. Review of Finance Vol. 16(2), pp [6] Chava, Sudheer and Michael R. Roberts How Does Financing Impact Investment? The Role of Debt Covenants. Journal of Finance Vol. 63(5), pp [7] Chernenko, Sergey and Michael Faulkender The Two Sides of Derivatives Usage: Hedging and Speculating with Interest Rate Swaps. Journal of Financial and Quantitative Analysis Vol. 46(6), pp [8] Cornett, Marcia M., Jamie J. McNutt, Philip E. Strahan, Hassan Tehranian Liquidity Risk Management and Credit Supply in the Financial Crisis. Journal of Financial Economics Vol. 101(2), pp [9] Demiroglu, Cem and Christopher M. James The Use of Bank Lines of Credit in Corporate Liquidity Management: A Review of Empirical Evidence. Journal of Banking & Finance Vol. 35(4), pp [10] Demiroglu, Cem, Christopher M. James, and Atay Kizilaslan Credit Market Conditions and the Determinants and Value of Bank Lines of Credit for Private Firms. manuscript, Gainesville: University of Florida. [11] Disatnik, David, Ran Duchin, and Breno Schmidt Cash Flow Hedging and Liquidity Choices. manuscript, Ann Arbor: University of Michigan. 22

24 [12] Faulkender, Michael Hedging or Market Timing? Selecting the Interest Rate Exposure of Corporate Debt. Journal of Finance Vol. 60(2), pp [13] Faulkender, Michael and Mitchell Petersen Investment and Capital Constraints: Repatriations Under the American Jobs Creation Act. manuscript, Evanston: Northwestern University. [14] Froot, Kenneth A., David S. Scharfstein, and Jeremy C. Stein Risk Management: Coordinating Corporate Investment and Financing Policies. Journal of Finance Vol. 48, pp [15] Gatev, Evan and Philip E. Strahan Banks Advantage in Hedging Liquidity Risk: Theory and Evidence from the Commercial Paper Market. Journal of Finance Vol. 61, pp [16] Gorton, Gary Information, Liquidity, and the (Ongoing) Panic of American Economic Review, Papers and Proceedings Vol. 99(2), [17] Graham, John R., and Daniel A. Rogers Do Firms Hedge in Response to Tax Incentives? Journal of Finance Vol. 57, pp [18] Guay, Wayne and S. P. Kothari How Much Do Firms Hedge with Derivatives? Journal of Financial Economics Vol. 70(3), [19] Holmström, Bengt and Jean Tirole Liquidity and Risk Management. Journal of Money, Credit and Banking Vol. 32(3), pp [20] Huang, Rocco How Committed are Bank Lines of Credit? Experiences in the Subprime Mortgage Crisis. manuscript, East Lansing: Michigan State University. [21] Ivashina, Victoria and David S. Scharfstein Bank Lending during the Financial Crisis of Journal of Financial Economics Vol. 97(3), pp [22] Jiménez, Gabriel, Jose A. Lopez, and Jesús Saurina Empirical Analysis of Corporate Credit Lines. Review of Financial Studies Vol. 22(12), pp [23] Kacperczyk, Marcin and Philipp Schnabl When Safe Proved Risky: Commercial Paper during the Financial Crisis of Journal of Economic Perspectives Vol. 24(1), pp [24] Lins, Karl V., Henri Servaes, and Peter Tufano What Drives Corporate Liquidity? An International Survey of Cash Holdings and Lines of Credit. Journal of Financial Economics Vol. 98(1), pp

25 [25] Mian, Atif and Joao A. C. Santos Liquidity Risk and Maturity Management over the Credit Cycle. manuscript, Berkeley: University of California. [26] Montoriol-Garriga, Judit and Evan Sekeris A Question of Liquidity: The Great Banking Run of 2008? Federal Reserve Bank of Boston Working Paper No. QAU09-4. [27] Nini, Greg, David C. Smith, and Amir Sufi Creditor Control Rights and Firm Investment Policy. Journal of Financial Economics Vol. 92(3), pp [28] Purnanandam, Amiyatoish Financial Distress and Corporate Risk Management: Theory and Evidence. Journal of Financial Economics Vol. 87(3), pp [29] Shockley, Richard L. and Anjan V. Thakor Bank Loan Commitment Contracts: Data, Theory, and Tests. Journal of Money, Credit, and Banking Vol. 29(4), pp [30] Smith, Clifford W. and Rene Stulz The Determinants of Firms Hedging Policies. Journal of Financial and Quantitative Analysis Vol. 28, pp [31] Stulz, Rene Optimal Hedging Policies. Journal of Financial and Quantitative Analysis Vol. 19, pp [32] Sufi, Amir Bank Lines of Credit in Corporate Finance: An Empirical Analysis. Review of Financial Studies Vol. 22(3), pp [33] Thakor, Anjan V. Do Loan Commitments Cause Overlending? Journal of Money, Credit and Banking Vol. 36(6), pp

26 Figure 1: Revolving Portion of Credit Lines 25

27 Figure 2: Credit Line Usage and Availability by Firm Size 26

28 Figure 3: Credit Line Usage and Availability by Commercial Paper Use 27

29 Figure 4: Revolving Portion of Credit Lines 28

30 Figure 5: Credit Line Usage and Availability by Hedging Decision 29

31 Figure 6: Cash Flow, Cash Holdings, and Inventories by Hedging Decision 30

The Real Effects of Credit Line Drawdowns

The Real Effects of Credit Line Drawdowns Jose M. Berrospide Federal Reserve Board Ralf R. Meisenzahl Federal Reserve Board January 31, 2013 Abstract Do firms use credit line drawdowns to finance investment?

The Real Effects of Credit Line Drawdowns Jose M. Berrospide Federal Reserve Board Ralf R. Meisenzahl Federal Reserve Board January 31, 2013 Abstract Do firms use credit line drawdowns to finance investment?

Liquidity Management and Corporate Investment During a Financial Crisis

RFS Advance Access published April 2, 2011 Liquidity Management and Corporate Investment During a Financial Crisis Murillo Campello Cornell University & NBER Erasmo Giambona University of Amsterdam John

RFS Advance Access published April 2, 2011 Liquidity Management and Corporate Investment During a Financial Crisis Murillo Campello Cornell University & NBER Erasmo Giambona University of Amsterdam John

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

Macroeconomic Factors in Private Bank Debt Renegotiation

University of Pennsylvania ScholarlyCommons Wharton Research Scholars Wharton School 4-2011 Macroeconomic Factors in Private Bank Debt Renegotiation Peter Maa University of Pennsylvania Follow this and

University of Pennsylvania ScholarlyCommons Wharton Research Scholars Wharton School 4-2011 Macroeconomic Factors in Private Bank Debt Renegotiation Peter Maa University of Pennsylvania Follow this and

Liquidity Insurance in Macro. Heitor Almeida University of Illinois at Urbana- Champaign

Liquidity Insurance in Macro Heitor Almeida University of Illinois at Urbana- Champaign Motivation Renewed attention to financial frictions in general and role of banks in particular Existing models model

Liquidity Insurance in Macro Heitor Almeida University of Illinois at Urbana- Champaign Motivation Renewed attention to financial frictions in general and role of banks in particular Existing models model

May 19, Abstract

LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Boston College gatev@bc.edu Philip E. Strahan Boston College, Wharton Financial Institutions Center & NBER philip.strahan@bc.edu May 19, 2008 Abstract

LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Boston College gatev@bc.edu Philip E. Strahan Boston College, Wharton Financial Institutions Center & NBER philip.strahan@bc.edu May 19, 2008 Abstract

Why Do Non-Financial Firms Select One Type of Derivatives Over Others?

Why Do Non-Financial Firms Select One Type of Derivatives Over Others? Hong V. Nguyen University of Scranton The increase in derivatives use over the past three decades has stimulated both theoretical

Why Do Non-Financial Firms Select One Type of Derivatives Over Others? Hong V. Nguyen University of Scranton The increase in derivatives use over the past three decades has stimulated both theoretical

Debt Maturity and the Cost of Bank Loans

Debt Maturity and the Cost of Bank Loans Chih-Wei Wang a, Wan-Chien Chiu b,*, and Tao-Hsien Dolly King c September 2016 Abstract We study the extent to which a firm s debt maturity structure affects its

Debt Maturity and the Cost of Bank Loans Chih-Wei Wang a, Wan-Chien Chiu b,*, and Tao-Hsien Dolly King c September 2016 Abstract We study the extent to which a firm s debt maturity structure affects its

Capital structure and the financial crisis

Capital structure and the financial crisis Richard H. Fosberg William Paterson University Journal of Finance and Accountancy Abstract The financial crisis on the late 2000s had a major impact on the financial

Capital structure and the financial crisis Richard H. Fosberg William Paterson University Journal of Finance and Accountancy Abstract The financial crisis on the late 2000s had a major impact on the financial

Aggregate Risk and the Choice Between Cash and Lines of Credit

Aggregate Risk and the Choice Between Cash and Lines of Credit Viral V Acharya NYU-Stern, NBER, CEPR and ECGI with Heitor Almeida Murillo Campello University of Illinois at Urbana Champaign, NBER Introduction

Aggregate Risk and the Choice Between Cash and Lines of Credit Viral V Acharya NYU-Stern, NBER, CEPR and ECGI with Heitor Almeida Murillo Campello University of Illinois at Urbana Champaign, NBER Introduction

RESEARCH STATEMENT. Heather Tookes, May My research lies at the intersection of capital markets and corporate finance.

RESEARCH STATEMENT Heather Tookes, May 2013 OVERVIEW My research lies at the intersection of capital markets and corporate finance. Much of my work focuses on understanding the ways in which capital market

RESEARCH STATEMENT Heather Tookes, May 2013 OVERVIEW My research lies at the intersection of capital markets and corporate finance. Much of my work focuses on understanding the ways in which capital market

Firm Debt Outcomes in Crises: The Role of Lending and. Underwriting Relationships

Firm Debt Outcomes in Crises: The Role of Lending and Underwriting Relationships Manisha Goel Michelle Zemel Pomona College Very Preliminary See https://research.pomona.edu/michelle-zemel/research/ for

Firm Debt Outcomes in Crises: The Role of Lending and Underwriting Relationships Manisha Goel Michelle Zemel Pomona College Very Preliminary See https://research.pomona.edu/michelle-zemel/research/ for

NBER WORKING PAPER SERIES LIQUIDITY RISK AND SYNDICATE STRUCTURE. Evan Gatev Philip Strahan. Working Paper

NBER WORKING PAPER SERIES LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Philip Strahan Working Paper 13802 http://www.nber.org/papers/w13802 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Philip Strahan Working Paper 13802 http://www.nber.org/papers/w13802 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

If the market is perfect, hedging would have no value. Actually, in real world,