Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

|

|

|

- Egbert Parrish

- 5 years ago

- Views:

Transcription

1 Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

2 Definition Define Liabilities?

3 Definition of Liabilities Liabilities represent an obligation of an entity. This obligation needs to be satisfied by the entity through payment of cash or the surrendering of entity s assets or services.

4 Definition of Liabilities According to Malaysian accounting standard FRS 101- Presentation of Financial Statement, a liability shall be classified as current when it satisfies any of the following criteria:

5 Definition of Liabilities (a) it is expected to be settled in the entity's normal operating cycle; (b) it is held primarily for the purpose of being traded; (c) it is due to be settled within twelve months after the balance sheet date; or

6 Definition of Liabilities (d) the entity does not have an unconditional right to defer settlement of the liability for at least twelve months after the balance sheet date. All other liabilities shall be classified as non-current.

7 Current Liabilities Current liabilities are obligations by an entity that need to be settled using current assets or by creating another current liability within a period of one year.

8 Current Liabilities

9 Bank Overdraft What is Bank overdraft?

10 Bank Overdraft Bank overdraft is a facility given by banks to current account holders that enable the holder to draw cheques larger than the holder s bank balance. An overdraft is indicated by a credit balance in a firm s cash account.

11 Bank Overdraft Bank will charge firm a fixed interest rate for the overdraft amount. The original amount plus the interest must be paid by the current account s holder.

12 Bank Loan Bank loan is also refers to as notes payable represent borrowing made by businesses. Borrowings can be long term or short term. Short term refers to borrowing that needs to be paid within a period of one year.

13 Bills Payables Bill payable is a note issued by one entity, promising to pay another entity. It is usually issued when you as the debtor are unable to pay for your account payable balance to your supplier (creditor).

14 Dividend Payables Dividends payable is liability unique to companies. It arises as a result of the difference in the date when dividend is declared and the date dividend is paid.

15 Long term Liabilities Long term liabilities are obligations of an entity that need to be settled in a period of more than twelve months than the date of reporting. The obligation is settled by giving up (sacrificing) the entity s current assets.

16 Long term Liabilities

17 Long term Bank Loan Long term bank loans (notes payable) are borrowings that needs to be paid within a period of more than twelve months.

18 Current Assets According to Malaysian accounting standard FRS 101 Presentation of Financial Statement, an asset is classified as a current asset when it is:

19 Current Assets In other words, current assets include cash or cash equivalent and other assets that can be converted into cash, and other assets that can be resold or used in manufacturing goods within a period of one accounting year or less.

20 Mortgage Loan Mortgage loans refer to borrowings made by an entity (for example bank), that involves securing loan against an asset. In other word the amount of borrowing is tied against the entity assets (building, vehicle or land).

21 Bonds & Debentures Bonds and debentures are issued by an entity in order to finance its activities. Normally big corporations and government will issue bonds. You might have heard about Islamic bond issued by the HDFC in Maldives, amounting to RVR 50 million and due in November 2013.

22 Bonds & Debentures The issuer will have an obligation to pay the interest payment to the bond holder, normally semi annually until the bond matures. The face value or bond will be paid by the issuer on maturity.

23 Equity It is the owner s residual claims of the business assets after paying off liabilities.

24 Equity of Sole Trader For a single proprietorship the equity section of a balance sheet will have only one account i.e. Capital account. The balance of capital account represents: (a) the original amount contributed by the owner; (b) any increase or decrease as a result of profits or losses;

25 Equity of Sole Trader (c) any increase as a result of additional contribution by owner; and (d) any decrease as a result of drawings made by owner.

26 Equity of Sole Trader

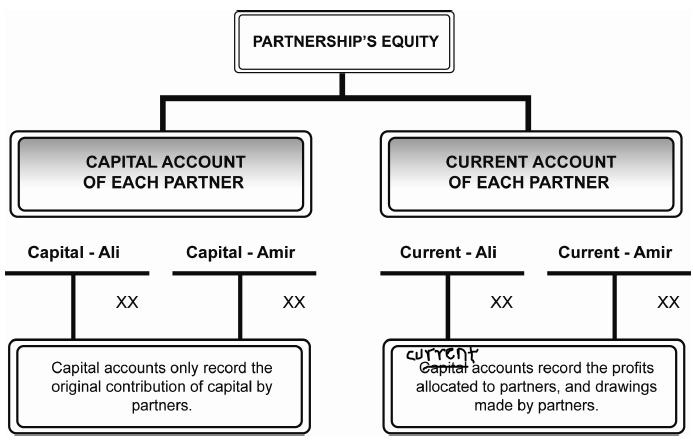

27 Equity of Partnership

28 Equity of a Company Equity component of a company comprises of: (i) shareholder s fund; (ii) retained earnings; and (iii) reserves.

29 Equity of a Company

30 Shareholders Funds Shareholder funds are the par value of shares times the number of shares issued by a company. For example, if a company issues 3 million ordinary shares of RM1 par value each, then the shareholder fund is RM3 million. Let us look at the characteristics of these shares.

31 Ordinary or Common Shares Holders of common shares are the true owner of a company. They have the rights to vote. Ordinary shareholders right to dividend is after preference shareholders. Ordinary share s dividend amount is not fixed.

32 Ordinary or Common Shares In the event that a business turns bad, company do not have an obligation to declare dividends for ordinary shares. However, once a company declares its dividend, the company must fulfill its obligation to pay.

33 Preference Shares Holders of preference share do not have the rights to vote. Preference shares have special rights attached to them, i.e. rights to receive dividends before ordinary shareholders and also rights to the residual assets before ordinary shareholders if the company wind up.

34 Preference Shares The preference shares dividend amount is fixed. Preference shares will be issued with fixed dividend rates. A company has the obligation to pay this dividend regardless whether business is good or bad. Hence, in ratio analysis, preference shares are treated as liabilities rather than equity.

35 Retained Earnings The second component of equity for company is retained earning. Retained earning account is the accumulation of company s net earnings (profit) after tax after distributions to shareholders and/or reserves.

36 Retained Earnings

37 Reserves A company might also create reserves to set aside funds from earnings for the following purposes: (i) to cover themselves from future loses; (ii) to buy fixed assets; (iii) to repay liabilities; and (iv) to buy back their shares.

38 Reserves The most common reserve created is the general reserves, and this will be reported in the equity section of the balance sheet.

39 Equity Component of Company in Summery

40 Q & A

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Assets Define Assets? Assets Financial Reporting Standard (FRS) defines assets as resources controlled by an entity

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Assets Define Assets? Assets Financial Reporting Standard (FRS) defines assets as resources controlled by an entity

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction Indirect taxes include sales tax, service tax, custom and excise duties. The Government of Malaysia

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction Indirect taxes include sales tax, service tax, custom and excise duties. The Government of Malaysia

What are some of the terms included in a written partnership agreement?

CHAPTER 15 STRUCTURED QUESTIONS 1. What are some of the terms included in a written partnership agreement? 2. If there is no written agreement in a partnership company, what are the main provisions of

CHAPTER 15 STRUCTURED QUESTIONS 1. What are some of the terms included in a written partnership agreement? 2. If there is no written agreement in a partnership company, what are the main provisions of

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction Imagine the world without traffic law and enforcement! Think how people will behave. Introduction

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction Imagine the world without traffic law and enforcement! Think how people will behave. Introduction

CLASS XII SAMPLE PAPER ACCOUNTANCY

CLASS XII SAMPLE PAPER ACCOUNTANCY Time Allowed: 3 Hrs. Maximum Marks:80 General instructions:- (1)This question paper is divided in two parts. (2)All parts of a question should be solved at one place

CLASS XII SAMPLE PAPER ACCOUNTANCY Time Allowed: 3 Hrs. Maximum Marks:80 General instructions:- (1)This question paper is divided in two parts. (2)All parts of a question should be solved at one place

Chapter 1 Financial Management Introduction & Goals of the Firm

Chapter 1 Financial Management Introduction & Goals of the Firm Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction This topic introduces the area of

Chapter 1 Financial Management Introduction & Goals of the Firm Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction This topic introduces the area of

ACCN3 Additional Specimen Questions

TEACHER RESOURCE BANK GCE Accounting Additional Sample Questions and Mark Schemes New/Modified Topics: ACCN3 First issue 2010 The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee

TEACHER RESOURCE BANK GCE Accounting Additional Sample Questions and Mark Schemes New/Modified Topics: ACCN3 First issue 2010 The Assessment and Qualifications Alliance (AQA) is a company limited by guarantee

The Statement of Cash Flows

1 The Statement of Cash Flows Purpose of a statement of cash flows: To provide information about the cash inflows and outflows of an entity during a period. To summarize the operating, investing, and financing

1 The Statement of Cash Flows Purpose of a statement of cash flows: To provide information about the cash inflows and outflows of an entity during a period. To summarize the operating, investing, and financing

Kelda Finance (No.2) Limited. Condensed Interim Financial Statements Registered number For the six months ended 30 September 2017

Limited. Condensed Interim Financial Statements Registered number For the six months ended 30 September 2017") Condensed Interim Financial Statements Registered number 08072102 For the six months ended Contents Information to accompany the condensed interim financial statements 2 Condensed Profit and Loss Account

Condensed Interim Financial Statements Registered number 08072102 For the six months ended Contents Information to accompany the condensed interim financial statements 2 Condensed Profit and Loss Account

AMALGAMATION, ABSORPTION AND RECONSTRUCTION

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

1 SOURCES OF FINANCE

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

CHAPTER 14 FINANCIAL MANAGEMENT

CHAPTER 14 FINANCIAL MANAGEMENT Chapter content Introduction The financial function and financial management Concepts in financial management Objective and fundamental principles of financial management

CHAPTER 14 FINANCIAL MANAGEMENT Chapter content Introduction The financial function and financial management Concepts in financial management Objective and fundamental principles of financial management

Chapter 13 Financial management

Chapter 13 Financial management 1. Concept in financial management... 3 1.1. Balance sheet, asset and financing structure... 3 1.2. Capital... 3 1.3. Income... 3 1.4. Costs... 4 1.4.1. Fixed costs... 4

Chapter 13 Financial management 1. Concept in financial management... 3 1.1. Balance sheet, asset and financing structure... 3 1.2. Capital... 3 1.3. Income... 3 1.4. Costs... 4 1.4.1. Fixed costs... 4

Financial Instruments: Presentation INTRODUCTION

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

PARTNERSHIP ACCOUNTS

CHAPTER-2 Q. 1. Thin, Short and Fat were in partnership sharing profits and losses in the ratio of 2 : 2 : 1. On 30th September, 2012 their Balance Sheet was as follows : Capital Accounts : Premises 50,000

CHAPTER-2 Q. 1. Thin, Short and Fat were in partnership sharing profits and losses in the ratio of 2 : 2 : 1. On 30th September, 2012 their Balance Sheet was as follows : Capital Accounts : Premises 50,000

CHAPTER 24. Statement of cash flows CONTENTS

CHAPTER 24 Statement of cash flows CONTENTS 24.1 Simple statement of cash flows 24.2 Statement of cash flows for a sole trader 24.3 Statement of cash flows for a partnership 24.4 Statement of cash flows

CHAPTER 24 Statement of cash flows CONTENTS 24.1 Simple statement of cash flows 24.2 Statement of cash flows for a sole trader 24.3 Statement of cash flows for a partnership 24.4 Statement of cash flows

Chapter 10. An overview of accounting for liabilities. Liabilities defined 3/17/2017. Liabilities defined (cont.)

") Chapter 10 An overview of accounting for liabilities 10-1 Liabilities defined A liability is defined as: a present obligation of the entity arising from past events, the settlement of which is expected

Chapter 10 An overview of accounting for liabilities 10-1 Liabilities defined A liability is defined as: a present obligation of the entity arising from past events, the settlement of which is expected

HONG LEONG BANK BERHAD (97141-X) (Incorporated in Malaysia)

(Incorporated in Malaysia)") Condensed Financial Statements Unaudited Statements of Financial Position As At 30 June 2017 ASSETS As at As at As at As at Note Cash and short-term funds 10,823,310 7,473,964 10,199,194 5,657,847 Deposits

Condensed Financial Statements Unaudited Statements of Financial Position As At 30 June 2017 ASSETS As at As at As at As at Note Cash and short-term funds 10,823,310 7,473,964 10,199,194 5,657,847 Deposits

- 8 - INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF MALAYSIA PACIFIC CORPORATION BERHAD (Company No: M) (Incorporated in Malaysia)

(Incorporated in Malaysia)") - 8 - MALAYSIA PACIFIC CORPORATION BERHAD Report on the Financial Statements We were engaged to audit the financial statements of Malaysia Pacific Corporation Berhad, which comprise the statements of financial

- 8 - MALAYSIA PACIFIC CORPORATION BERHAD Report on the Financial Statements We were engaged to audit the financial statements of Malaysia Pacific Corporation Berhad, which comprise the statements of financial

ADVANCED ACCOUNTING b.com part II

ADVANCED ACCOUNTING b.com part II 2014 Regular & Private (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks.

ADVANCED ACCOUNTING b.com part II 2014 Regular & Private (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks.

Prepare the necessary journal entries to correct the above. Narrations are not required.

Correction of errors HKDSE (2017, 5) (Correction of errors) ABC Limited drafted a trial balance as at 31 December 2016, before the preparation of the closing entries. As the trial balance did not agree,

Correction of errors HKDSE (2017, 5) (Correction of errors) ABC Limited drafted a trial balance as at 31 December 2016, before the preparation of the closing entries. As the trial balance did not agree,

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2011

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 31 December 31 December Note ASSETS Cash and short-term funds 9 1,577,456 1,173,318 1,577,454

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 31 December 31 December Note ASSETS Cash and short-term funds 9 1,577,456 1,173,318 1,577,454

National Association of Community Legal Centres

National Association of Community Legal Centres Financial report For the year ended 30 June 2016 TABLE OF CONTENTS Financial report Statement of profit or loss and other comprehensive income... 1 Statement

National Association of Community Legal Centres Financial report For the year ended 30 June 2016 TABLE OF CONTENTS Financial report Statement of profit or loss and other comprehensive income... 1 Statement

Accounting & Reporting of Financial Instruments 2016

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

Unit 2. Banking and Customer Relationship

Unit 2 Banking and Customer Relationship Introduction The Indian Banking Regulation Act of 1949 Section 5 (1) defines bank as Accepting of deposit of money from the public, for the purpose of lending or

Unit 2 Banking and Customer Relationship Introduction The Indian Banking Regulation Act of 1949 Section 5 (1) defines bank as Accepting of deposit of money from the public, for the purpose of lending or

Bought to you by AS- Level Accounting Unit 2 Revision Notes

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

PROPERTY PERFECT PUBLIC COMPANY LIMITED AND ITS SUBSIDIARIES REPORT AND CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2007 AND 2006

PROPERTY PERFECT PUBLIC COMPANY LIMITED AND ITS SUBSIDIARIES REPORT AND CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2007 AND 2006 Report of Independent Auditor To the Shareholders of Property Perfect

PROPERTY PERFECT PUBLIC COMPANY LIMITED AND ITS SUBSIDIARIES REPORT AND CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2007 AND 2006 Report of Independent Auditor To the Shareholders of Property Perfect

Members Shares in Co-operative Entities and Similar Instruments

IFRIC INTERPRETATION 2 Members Shares in Co-operative Entities and Similar Instruments References IAS 32 Financial Instruments: Disclosure and Presentation (as revised in 2003) IAS 39 Financial Instruments:

IFRIC INTERPRETATION 2 Members Shares in Co-operative Entities and Similar Instruments References IAS 32 Financial Instruments: Disclosure and Presentation (as revised in 2003) IAS 39 Financial Instruments:

TRADING, PROFIT & LOSS ACCOUNT (INCOME STATEMENT) FOR THE YEAR ENDED 31 AUGUST 20*7

FOR THE YEAR ENDED 31 AUGUST 20*7") GCSE Revision- Unit 2 Finance 1. What are the advantages and disadvantages of a large business using the following sources of finance: (5 marks) Retained profits: these are profits that the owners put

GCSE Revision- Unit 2 Finance 1. What are the advantages and disadvantages of a large business using the following sources of finance: (5 marks) Retained profits: these are profits that the owners put

BASKETBALLSCOTLAND LIMITED ( LIMITED BY GUARANTEE ) ANNUAL REPORT AND UNAUDITED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017

ANNUAL REPORT AND UNAUDITED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017") Company Registration No. SC288195 (Scotland) BASKETBALLSCOTLAND LIMITED ANNUAL REPORT AND UNAUDITED FINANCIAL STATEMENTS Johnston Smillie Ltd Chartered Accountants 6 Redheughs Rigg Edinburgh EH12 9DQ COMPANY

Company Registration No. SC288195 (Scotland) BASKETBALLSCOTLAND LIMITED ANNUAL REPORT AND UNAUDITED FINANCIAL STATEMENTS Johnston Smillie Ltd Chartered Accountants 6 Redheughs Rigg Edinburgh EH12 9DQ COMPANY

Paper Reference(s) 6002/01 London Examinations GCE. Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level

6002/01 London Examinations GCE. Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level") Paper Reference(s) 6002/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level Unit 2 Corporate and Management Accounting Thursday 16 June 2011 Morning Source booklet

Paper Reference(s) 6002/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level Unit 2 Corporate and Management Accounting Thursday 16 June 2011 Morning Source booklet

Use the data provided to answer the questions that follow relating to Newtech Ltd for 2014: Abbreviated Balance Sheet:

POST GRAD DIPLOMA IN MANAGEMENT FINANCIAL MANAGEMENT REVISION QUESTIONS QUESTION 1 Use the data provided to answer the questions that follow relating to Newtech Ltd for 2014: Abbreviated Balance Sheet:

POST GRAD DIPLOMA IN MANAGEMENT FINANCIAL MANAGEMENT REVISION QUESTIONS QUESTION 1 Use the data provided to answer the questions that follow relating to Newtech Ltd for 2014: Abbreviated Balance Sheet:

Questions 1. What is a bond? What determines the price of this financial asset?

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS

, HALF-YEAR AND FULL YEAR RESULTS") PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS 1(a)(i) An income statement (for the group) together with a comparative statement for the corresponding

PART I - INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS 1(a)(i) An income statement (for the group) together with a comparative statement for the corresponding

Preparing Financial Statements for Companies IAS 1

Preparing Financial Statements for Companies IAS 1 Preparing Financial Statements for Companies We will focus today on the preparation of financial statements of a limited company. IAS 1 Presentation of

Preparing Financial Statements for Companies IAS 1 Preparing Financial Statements for Companies We will focus today on the preparation of financial statements of a limited company. IAS 1 Presentation of

Limited Companies Question: Explain the meaning of the following terms so as to make clear the differences between them: Ordinary Shares are

Limited Companies Explain the meaning of the following terms so as to make clear the differences between them: Ordinary Shares are certificates of ownership to a company. They are issued to shareholders

Limited Companies Explain the meaning of the following terms so as to make clear the differences between them: Ordinary Shares are certificates of ownership to a company. They are issued to shareholders

Notes to the Parent Company financial statements

Note 1 Accounting policies Basis of preparation The Parent Company financial statements have been prepared on a going concern basis using the historical cost convention modified for the revaluation of

Note 1 Accounting policies Basis of preparation The Parent Company financial statements have been prepared on a going concern basis using the historical cost convention modified for the revaluation of

The financial System Lecture One Introduction to the Financial System

The financial System 25556 Lecture One Introduction to the Financial System A financial system Consists of the financial institutions, markets and instruments that together provide financial services for

The financial System 25556 Lecture One Introduction to the Financial System A financial system Consists of the financial institutions, markets and instruments that together provide financial services for

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2011

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 31 December 31 December Note ASSETS Cash and short-term funds 9 1,298,187 1,173,318 1,298,185

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 31 December 31 December Note ASSETS Cash and short-term funds 9 1,298,187 1,173,318 1,298,185

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI

, CHENNAI") LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.Com. DEGREE EXAMINATION CORPORATE SECRETARYSHIP THIRD SEMESTER NOVEMBER 2016 BC 3502 COMPANY ACCOUNTS Date: 04-11-2016 Dept. No. Max. : 100 Marks Time: 09:00-12:00

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 B.Com. DEGREE EXAMINATION CORPORATE SECRETARYSHIP THIRD SEMESTER NOVEMBER 2016 BC 3502 COMPANY ACCOUNTS Date: 04-11-2016 Dept. No. Max. : 100 Marks Time: 09:00-12:00

SUBJECT: ACCOUNTING GRADE 12 CHAPTER: COMPANIES LESSON: PUBLISHED FINANCIAL STATEMENTS LESSON OVERVIEW (KNOWLEDGE AREAS) LESSON INTRODUCTION

LESSON INTRODUCTION") SUBJECT: ACCOUNTING GRADE 12 CHAPTER: COMPANIES LESSON: PUBLISHED FINANCIAL STATEMENTS LESSON OVERVIEW (KNOWLEDGE AREAS) LESSON 1. Introduction 2. Income Statement 3. Balance sheet INTRODUCTION A company

SUBJECT: ACCOUNTING GRADE 12 CHAPTER: COMPANIES LESSON: PUBLISHED FINANCIAL STATEMENTS LESSON OVERVIEW (KNOWLEDGE AREAS) LESSON 1. Introduction 2. Income Statement 3. Balance sheet INTRODUCTION A company

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management

Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management") BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

Financed by: Share capital 304, ,000 Reserves 47,645 43,395 SHAREHOLDERS' EQUITY 351, ,395

UNAUDITED INTERIM FINANCIAL STATEMENTS CONDENSED BALANCE SHEETS AS AT 30 SEPTEMBER Note ASSETS Cash and short-term funds 8 450,425 587,326 Deposits and placements with banks and other financial institutions

UNAUDITED INTERIM FINANCIAL STATEMENTS CONDENSED BALANCE SHEETS AS AT 30 SEPTEMBER Note ASSETS Cash and short-term funds 8 450,425 587,326 Deposits and placements with banks and other financial institutions

RANBAXY AUSTRALIA PTY LTD ABN

RANBAXY AUSTRALIA PTY LTD ABN 17 110 871 826 Financial Statements for the year ended Level 6 468 St Kilda Road Melbourne VIC 3004 Australia Telephone: (03) 9820 6400 Facsimile: (03) 9820 6499 Email: sothertons@sothertonsmelbourne.com.au

RANBAXY AUSTRALIA PTY LTD ABN 17 110 871 826 Financial Statements for the year ended Level 6 468 St Kilda Road Melbourne VIC 3004 Australia Telephone: (03) 9820 6400 Facsimile: (03) 9820 6499 Email: sothertons@sothertonsmelbourne.com.au

ACCOUNTING. From the following information provided by the proprietor of the business, Jeremy, you are required to prepare:

Question 1 From the following information provided by the proprietor of the business, Jeremy, you are required to prepare: a. Trading and Profit and Loss Account for the year ended 31 December 20x1 (13

Question 1 From the following information provided by the proprietor of the business, Jeremy, you are required to prepare: a. Trading and Profit and Loss Account for the year ended 31 December 20x1 (13

BANK OF CHINA (MALAYSIA) BERHAD (Incorporated in Malaysia)

BERHAD (Incorporated in Malaysia)") Company No. 511251 V BANK OF CHINA (MALAYSIA) BERHAD REPORTS AND FINANCIAL STATEMENTS FOR THE SECOND QUARTER UNAUDITED INTERIM FINANCIAL STATEMENTS CONDENSED BALANCE SHEETS AS AT 30 JUNE Note ASSETS Cash

Company No. 511251 V BANK OF CHINA (MALAYSIA) BERHAD REPORTS AND FINANCIAL STATEMENTS FOR THE SECOND QUARTER UNAUDITED INTERIM FINANCIAL STATEMENTS CONDENSED BALANCE SHEETS AS AT 30 JUNE Note ASSETS Cash

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Responsibility A responsibility centre is a function or department of an organization that is headed by a manager

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Responsibility A responsibility centre is a function or department of an organization that is headed by a manager

IPCC MAY 2016 QUESTION PAPER PAPER 1 ACCOUNTING

IPCC MAY 2016 QUESTION PAPER PAPER 1 ACCOUNTING Questions No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part

IPCC MAY 2016 QUESTION PAPER PAPER 1 ACCOUNTING Questions No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part

ACCOUNTANCY. Part B. Q17. State the significance of Analysis of Financial Statements to the Lenders. (1 mark)

") ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

SEMINAR PAPER PRESENTED TO CASHFLOW FINANCE AUSTRALIA

SEMINAR PAPER PRESENTED TO CASHFLOW FINANCE AUSTRALIA BY BLAIR PLEASH AND KATHLEEN VOURIS PARTNERS OF HALL CHADWICK Chartered Accountants and Business Advisors Sydney Melbourne Brisbane Level 40 Level

SEMINAR PAPER PRESENTED TO CASHFLOW FINANCE AUSTRALIA BY BLAIR PLEASH AND KATHLEEN VOURIS PARTNERS OF HALL CHADWICK Chartered Accountants and Business Advisors Sydney Melbourne Brisbane Level 40 Level

Chapter # 1. Accounting for Company Issuance of Shares & Debentures. Sameer Hussain.

Accounting for Company Issuance of Shares & Debentures SYLLABUS ACCORDING TO UNIVERSITY OF KARACHI: Accounting for companies. Issuance of shares and bonds. Appropriation of retained earnings. Declaration

Accounting for Company Issuance of Shares & Debentures SYLLABUS ACCORDING TO UNIVERSITY OF KARACHI: Accounting for companies. Issuance of shares and bonds. Appropriation of retained earnings. Declaration

This helpful resource translates some commonly used financial terms into plain English.

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

FINANCIAL JARGON This helpful resource translates some commonly used financial terms into plain English. One of the things that can make the world of personal finance so confusing is that it seems to come

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") All Rights Reserved No. of Pages - 10 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II INTAKE VII (GROUP B) END SEMESTER

All Rights Reserved No. of Pages - 10 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II INTAKE VII (GROUP B) END SEMESTER

CIMB BANK BERHAD (13491-P) CONDENSED INTERIM FINANCIAL STATEMENTS UNAUDITED STATEMENTS OF FINANCIAL POSITION AS AT 31 MARCH 2017

CONDENSED INTERIM FINANCIAL STATEMENTS UNAUDITED STATEMENTS OF FINANCIAL POSITION AS AT 31 MARCH 2017") CIMB BANK BERHAD (13491-P) CONDENSED INTERIM FINANCIAL STATEMENTS UNAUDITED STATEMENTS OF FINANCIAL POSITION AS AT 31 MARCH 2017 31 Mar 2017 31 Dec 2016 31 Mar 2017 31 Dec 2016 Note Assets Cash and short

CIMB BANK BERHAD (13491-P) CONDENSED INTERIM FINANCIAL STATEMENTS UNAUDITED STATEMENTS OF FINANCIAL POSITION AS AT 31 MARCH 2017 31 Mar 2017 31 Dec 2016 31 Mar 2017 31 Dec 2016 Note Assets Cash and short

Professor Vipin Conversion of Partnership into Company. Meaning

Meaning Conversion of Partnership into Company For various reasons, an existing partnership may sell its entire business to an existing Joint Stock Company. It can also convert itself into a Joint Stock

Meaning Conversion of Partnership into Company For various reasons, an existing partnership may sell its entire business to an existing Joint Stock Company. It can also convert itself into a Joint Stock

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 SEPTEMBER 2011

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 SEPTEMBER 31 December 31 December Note ASSETS Cash and short-term funds 9 1,366,063 1,173,318 1,366,061

INTERIM FINANCIAL STATEMENTS UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 SEPTEMBER 31 December 31 December Note ASSETS Cash and short-term funds 9 1,366,063 1,173,318 1,366,061

PHILLIP ISLAND GOLF CLUB INC. A F SPECIAL PURPOSE FINANCIAL REPORT FOR THE YEAR ENDED

SPECIAL PURPOSE FINANCIAL REPORT FOR THE YEAR ENDED 30 JUNE 2016 STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME NOTE 2016 2015 Revenue from ordinary activities 2 832,297 819,317 Cost of goods

SPECIAL PURPOSE FINANCIAL REPORT FOR THE YEAR ENDED 30 JUNE 2016 STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME NOTE 2016 2015 Revenue from ordinary activities 2 832,297 819,317 Cost of goods

Analysis and Interpretation of Financial Statements

Analysis and Interpretation of Financial Statements Prof Pieter Pelle INTRODUCTION Objective of financial reporting provide information for decision making Primary statements income statement, balance

Analysis and Interpretation of Financial Statements Prof Pieter Pelle INTRODUCTION Objective of financial reporting provide information for decision making Primary statements income statement, balance

Unit 1. Negotiable Instruments

Unit 1 Negotiable Instruments Introduction Money can very easily and safely be transferred from one place to another with the help of negotiable i.e., cheque etc. The holder of these negotiable/ instruments

Unit 1 Negotiable Instruments Introduction Money can very easily and safely be transferred from one place to another with the help of negotiable i.e., cheque etc. The holder of these negotiable/ instruments

UNIVERSITY OF MALTA SECONDARY EDUCATION CERTIFICATE SEC ACCOUNTING. May Marking Scheme Paper I

UNIVERSITY OF MALTA SECONDARY EDUCATION CERTIFICATE SEC ACCOUNTING May 2011 Marking Scheme Paper I MATRICULATION AND SECONDARY EDUCATION CERTIFICATE EXAMINATIONS BOARD PAPER I Answer ALL questions. Question

UNIVERSITY OF MALTA SECONDARY EDUCATION CERTIFICATE SEC ACCOUNTING May 2011 Marking Scheme Paper I MATRICULATION AND SECONDARY EDUCATION CERTIFICATE EXAMINATIONS BOARD PAPER I Answer ALL questions. Question

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

HONG LEONG BANK BERHAD (97141-X) (Incorporated in Malaysia)

(Incorporated in Malaysia)") Condensed Financial Statements Unaudited Statements of Financial Position As At 30 September 2016 ASSETS As at As at As at As at 30/09/2016 30/06/2016 30/09/2016 30/06/2016 Note Cash and short-term funds

Condensed Financial Statements Unaudited Statements of Financial Position As At 30 September 2016 ASSETS As at As at As at As at 30/09/2016 30/06/2016 30/09/2016 30/06/2016 Note Cash and short-term funds

Investec plc silo financial information (excluding the results of Investec Limited)

") Investec plc silo financial information (excluding the results of Investec Limited) Unaudited consolidated financial information for the six months ended 30 September 2008 IFRS - Pounds Sterling Overview

Investec plc silo financial information (excluding the results of Investec Limited) Unaudited consolidated financial information for the six months ended 30 September 2008 IFRS - Pounds Sterling Overview

PRINCIPLES OF ACCOUNTS 7110/2

Centre Number Candidate Number Candidate Name CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Ordinary Level PRINCIPLES OF ACCOUNTS 7110/2 PAPER 2 MAY/JUNE SESSION 2002 1 hour 45

Centre Number Candidate Number Candidate Name CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Ordinary Level PRINCIPLES OF ACCOUNTS 7110/2 PAPER 2 MAY/JUNE SESSION 2002 1 hour 45

Methods on Debt Collection and Risk Control

Copyright,. All Rights Reserved. Methods on Debt Collection and Risk Control Preface In the early days when there was a shortage of materials, usually the supply was not enough to meet the demand in the

Copyright,. All Rights Reserved. Methods on Debt Collection and Risk Control Preface In the early days when there was a shortage of materials, usually the supply was not enough to meet the demand in the

Certificate in Accounting

Certificate in Accounting ASE3012 Level 3 Thursday 4 April 2013 Time allowed: 3 hours Information There are 5 questions in this question paper. Total marks available: 100 All questions carry equal marks.

Certificate in Accounting ASE3012 Level 3 Thursday 4 April 2013 Time allowed: 3 hours Information There are 5 questions in this question paper. Total marks available: 100 All questions carry equal marks.

Chapter 21. Financial Instruments

Reference: IAS 32; IAS 39 and IFRS 7 Financial Instruments Contents: Page 1. Introduction 648 2. Definitions Example 1: financial assets Example 2: financial liabilities 3. Financial Risks 3.1 Overview

Reference: IAS 32; IAS 39 and IFRS 7 Financial Instruments Contents: Page 1. Introduction 648 2. Definitions Example 1: financial assets Example 2: financial liabilities 3. Financial Risks 3.1 Overview

Name of authorised official (in capital letters): Due date for this return:

: Due date for this return:") FORM K48 Quarterly statistics of pension and provident funds Name of authorised official (in capital letters): Quarter ended:... Tel:...Ext:... Fax:... E-mail:... Due date for this return: Signature...

FORM K48 Quarterly statistics of pension and provident funds Name of authorised official (in capital letters): Quarter ended:... Tel:...Ext:... Fax:... E-mail:... Due date for this return: Signature...

Kelda Finance (No.3) PLC. Condensed Interim Financial Statements Registered number For the six months ended 30 September 2017

PLC. Condensed Interim Financial Statements Registered number For the six months ended 30 September 2017") Condensed Interim Financial Statements Registered number 08270049 For the six months ended Contents Information to accompany the condensed interim financial statements 2 Condensed Profit and Loss Account

Condensed Interim Financial Statements Registered number 08270049 For the six months ended Contents Information to accompany the condensed interim financial statements 2 Condensed Profit and Loss Account

Advanced Financial Management Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Cost of Capital

Study Notes & Tutorial Questions Chapter 3: Cost of Capital") Advanced Financial Management Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Cost of Capital 1 INTRODUCTION Cost of capital is an integral part of investment

Advanced Financial Management Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Cost of Capital 1 INTRODUCTION Cost of capital is an integral part of investment

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2014 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

Demo FRS 102 Section 1A UNAUDITED FINANCIAL STATEMENTS for the year ended 31 December 2016

Company registration number: 12345678 Demo FRS 102 Section 1A UNAUDITED FINANCIAL STATEMENTS for the year ended 31 December 2016 Sally 5, Chartered Accountant 1 Number Street, Numberville, Cheshire, NU1

Company registration number: 12345678 Demo FRS 102 Section 1A UNAUDITED FINANCIAL STATEMENTS for the year ended 31 December 2016 Sally 5, Chartered Accountant 1 Number Street, Numberville, Cheshire, NU1

FANLING LUTHERAN SECONDARY SCHOOL

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)

FANLING LUTHERAN SECONDARY SCHOOL 2012 2013 2 nd Term Examination S.5 BUSINESS, ACCOUNTING AND FINANCIAL STUDIES Accounting Module Date : 20th June, 2013 Time allowed: 8:30 am - 11:00 am (2 hour 30 minutes)

Notes to the financial statements

Note 1 UK GAAP accounting policies The separate financial statements of the Company are presented as required by the Companies Act 1985. As permitted by that Act, the separate financial statements have

Note 1 UK GAAP accounting policies The separate financial statements of the Company are presented as required by the Companies Act 1985. As permitted by that Act, the separate financial statements have

Professional Level Essentials Module, P2 (MYS)

") Answers Professional Level Essentials Module, P2 (MYS) Corporate Reporting (Malaysia) June 2008 Answers 1 (a) The functional currency is the currency of the primary economic environment in which the entity

Answers Professional Level Essentials Module, P2 (MYS) Corporate Reporting (Malaysia) June 2008 Answers 1 (a) The functional currency is the currency of the primary economic environment in which the entity

SHARES 101. Differences Between Stocks And Shares. What Is A Stock? Five Things To Know About Shares. What Is A Stock Market?

SHARES 101 Differences Between Stocks And Shares None. There are always questions being asked about the differences between stocks and shares. The bottom line is that stocks and shares are the same thing,

SHARES 101 Differences Between Stocks And Shares None. There are always questions being asked about the differences between stocks and shares. The bottom line is that stocks and shares are the same thing,

ntifinancial Reporting Framework for Small- and Medium-Sized E

ntifinancial Reporting Framework for Small- and Medium-Sized E Private Companies Practice Section November 2017 Financial Reporting Framework for Small- and Medium-Sized Entities Presentation and Checklist

ntifinancial Reporting Framework for Small- and Medium-Sized E Private Companies Practice Section November 2017 Financial Reporting Framework for Small- and Medium-Sized Entities Presentation and Checklist

CBC HOLDING COMPANY AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2017

CBC HOLDING COMPANY AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditor s Report... 1 Consolidated Financial Statements Consolidated Balance Sheets... 2 Consolidated

CBC HOLDING COMPANY AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditor s Report... 1 Consolidated Financial Statements Consolidated Balance Sheets... 2 Consolidated

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

MARK SCHEME for the October/November 2011 question paper for the guidance of teachers 0452 ACCOUNTING. 0452/23 Paper 2, maximum raw mark 120

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the October/November question paper for the guidance of teachers 0452 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS International General Certificate of Secondary Education MARK SCHEME for the October/November question paper for the guidance of teachers 0452 ACCOUNTING

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 6 Total number of printed pages : 10

Roll No... : 1 : 325 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 10 NOTE : 1. Answer ALL Questions. 2. All working notes should be shown distinctly.

Roll No... : 1 : 325 Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 10 NOTE : 1. Answer ALL Questions. 2. All working notes should be shown distinctly.

Basic Accounting Terms. Samir K Mahajan

Basic Accounting Terms Business Entity A business entity is a commercial (corporate or other) organisation that is formed in order to engage in business activities, usually for the sale of a product or

Basic Accounting Terms Business Entity A business entity is a commercial (corporate or other) organisation that is formed in order to engage in business activities, usually for the sale of a product or

The Business Guys. September Newsletter. Accounting.

The Business Guys September Newsletter Accounting. Final Accounts. If you re stuck for sample questions, here s a Final Accounts question and solution for you (Sole Trader Variety). Don t forget to give

The Business Guys September Newsletter Accounting. Final Accounts. If you re stuck for sample questions, here s a Final Accounts question and solution for you (Sole Trader Variety). Don t forget to give

Cymao Holdings Berhad (Co. No U) (Incorporated in Malaysia)

(Incorporated in Malaysia)") Cymao Holdings Berhad Reports and Financial Statements For The Financial Year Ended 31 December 2017 (In Ringgit Malaysia) Contents Pages Directors report 1 4 Statement by Directors 5 Statutory declaration

Cymao Holdings Berhad Reports and Financial Statements For The Financial Year Ended 31 December 2017 (In Ringgit Malaysia) Contents Pages Directors report 1 4 Statement by Directors 5 Statutory declaration

FINANCIAL ACCOUNTING PILOT PAPER

SUBJECT NO 15J FINANCIAL ACCOUNTING PILOT PAPER The examination paper is divided into TWO Sections. Section A is compulsory and carries 40 marks. Candidates should attempt THREE questions from Section

SUBJECT NO 15J FINANCIAL ACCOUNTING PILOT PAPER The examination paper is divided into TWO Sections. Section A is compulsory and carries 40 marks. Candidates should attempt THREE questions from Section

PROPOSED PRIVATE PLACEMENT OF UP TO TEN PERCENT (10%) OF THE ISSUED AND PAID-UP SHARE CAPITAL OF MUHIBBAH ( PROPOSED PRIVATE PLACEMENT )

OF THE ISSUED AND PAID-UP SHARE CAPITAL OF MUHIBBAH ( PROPOSED PRIVATE PLACEMENT )") MUHIBBAH ENGINEERING (M) BHD ( MUHIBBAH OR THE COMPANY ) PROPOSED PRIVATE PLACEMENT OF UP TO TEN PERCENT (10%) OF THE ISSUED AND PAID-UP SHARE CAPITAL OF MUHIBBAH ( PROPOSED PRIVATE PLACEMENT ) 1. INTRODUCTION

MUHIBBAH ENGINEERING (M) BHD ( MUHIBBAH OR THE COMPANY ) PROPOSED PRIVATE PLACEMENT OF UP TO TEN PERCENT (10%) OF THE ISSUED AND PAID-UP SHARE CAPITAL OF MUHIBBAH ( PROPOSED PRIVATE PLACEMENT ) 1. INTRODUCTION

COMPOSED BY SADIA ALI SADI (MBA)

") Mega File MGT101 Fall 2011 Question No: 7 ( Marks: 1 ) - Please choose one Which of the following business publishes the Financial Statements? Sole-Proprietorship Partnership Trust Public Limited Company

Mega File MGT101 Fall 2011 Question No: 7 ( Marks: 1 ) - Please choose one Which of the following business publishes the Financial Statements? Sole-Proprietorship Partnership Trust Public Limited Company

FINANCIAL INSTRUMENTS

page 48 student accountant NOVEMBER/DECEMBER 2008 FINANCIAL INSTRUMENTS understanding the basics RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 This article aims to help students better understand accounting

page 48 student accountant NOVEMBER/DECEMBER 2008 FINANCIAL INSTRUMENTS understanding the basics RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 This article aims to help students better understand accounting

School of Distance Education UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION. B Com. III Semester. Core Course CORPORATE ACCOUNTING QUESTION BANK

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION B Com (2011 Admission Onwards) III Semester Core Course CORPORATE ACCOUNTING QUESTION BANK 1. is an artificial person created by law A. Firm B. Sole trader

UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION B Com (2011 Admission Onwards) III Semester Core Course CORPORATE ACCOUNTING QUESTION BANK 1. is an artificial person created by law A. Firm B. Sole trader

NATIONAL SENIOR CERTIFICATE GRADE 12

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2009 MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. Accounting 2 DoE/Feb. March 2009 INSTRUCTIONS AND INFORMATION Read

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2009 MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. Accounting 2 DoE/Feb. March 2009 INSTRUCTIONS AND INFORMATION Read

Accounting Fundamentals July 2010

Accounting Fundamentals July 2010 s and examiner s comments Important notice When reading these suggested answers, please note that the answers are intended as an indication of what is required rather

Accounting Fundamentals July 2010 s and examiner s comments Important notice When reading these suggested answers, please note that the answers are intended as an indication of what is required rather

ALLIED FOR ACCOUNTING & AUDITING ARAB CHARTERED ACCOUNTANTS (E&Y) (RSM INTERNATIONAL)

(RSM INTERNATIONAL)") ALLIED FOR ACCOUNTING & AUDITING (E&Y) ARAB CHARTERED ACCOUNTANTS (RSM INTERNATIONAL) TALAAT MOSTAFA GROUP HOLDING COMPANY "TMG HOLDING" (S.A.E) SEPARATE FINANCIAL STATEMENTS FOR THE PERIOD FROM 1 JANUARY

ALLIED FOR ACCOUNTING & AUDITING (E&Y) ARAB CHARTERED ACCOUNTANTS (RSM INTERNATIONAL) TALAAT MOSTAFA GROUP HOLDING COMPANY "TMG HOLDING" (S.A.E) SEPARATE FINANCIAL STATEMENTS FOR THE PERIOD FROM 1 JANUARY

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

6 The following terms are used in this Standard with the meanings specified: Cash comprises cash on hand and demand deposits.

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Notes To The Financial Statements For the year ended 31 December 2014

1. Corporate information Ornapaper Berhad is a public limited liability company, incorporated and domiciled in Malaysia, and is listed on the Main Market of Bursa Malaysia Securities Berhad. The principal

1. Corporate information Ornapaper Berhad is a public limited liability company, incorporated and domiciled in Malaysia, and is listed on the Main Market of Bursa Malaysia Securities Berhad. The principal

[ ] Examples of what constitutes a close company or not (Tax Instruction refers)

![[ ] Examples of what constitutes a close company or not (Tax Instruction refers)](/thumbs/86/93870404.jpg "[ ] Examples of what constitutes a close company or not (Tax Instruction refers)") [13-02-02] Examples of what constitutes a close company or not (Tax Instruction 13-01-02 refers) Part 13, Chapter 1 TCA 1997 This document should be read in conjunction with section 430 et seq. TCA 1997

[13-02-02] Examples of what constitutes a close company or not (Tax Instruction 13-01-02 refers) Part 13, Chapter 1 TCA 1997 This document should be read in conjunction with section 430 et seq. TCA 1997

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS GCE Ordinary Level (2017) (Syllabus 7175) CONTENTS Page INTRODUCTION 2 AIMS 2 ASSESSMENT OBJECTIVES 3 SCHEME OF ASSESSMENT 4 USE OF CALCULATORS 4 SYLLABUS OUTLINE 5 SUBJECT CONTENT

PRINCIPLES OF ACCOUNTS GCE Ordinary Level (2017) (Syllabus 7175) CONTENTS Page INTRODUCTION 2 AIMS 2 ASSESSMENT OBJECTIVES 3 SCHEME OF ASSESSMENT 4 USE OF CALCULATORS 4 SYLLABUS OUTLINE 5 SUBJECT CONTENT

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014 In this lesson we: Introduction Lesson Description Look at analysing financial statements and its purpose Consider users of financial statements

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014 In this lesson we: Introduction Lesson Description Look at analysing financial statements and its purpose Consider users of financial statements

The methodological basis for the compilation of the financial accounts is the ESA2010 (the European System of Accounts).

.") 3. FINANCIAL ACCOUNTS METHODOLOGY 3.1 ESA2010 methodology The methodological basis for the compilation of the financial accounts is the ESA2010 (the European System of Accounts). The financial accounts

3. FINANCIAL ACCOUNTS METHODOLOGY 3.1 ESA2010 methodology The methodological basis for the compilation of the financial accounts is the ESA2010 (the European System of Accounts). The financial accounts