Presentation of Financial Performance

|

|

|

- Alban Hood

- 5 years ago

- Views:

Transcription

1 Sourced from: Presentation of Financial Performance Module 2 Topic 3

2 Learning Objectives Explain the purpose and importance of measuring financial performance Explain the reporting period concept and the difference between accrual accounting and cash accounting Describe the measurement of financial performance Discuss the definition and classification of income Discuss the definition and classification of expenses Apply the recognition criteria to income and expenses Identify presentation formats for the statement of profit or loss Explain the nature of the statement of comprehensive income and statement of changes in equity Explain the relationship between the statement of profit or loss, the balance sheet, the statement of comprehensive income and the statement of changes in equity

3 Financial performance Profit or loss, a measure of financial performance, is an important item in financial statements. Profit reflects the outcome of an entity s investment and financing decisions. An entity should periodically report its performance to enable internal and external users to make informed decisions. The profit or loss will inform internal decisions such as the entity s pricing of goods and services and the need to review cost structures. The profit or loss will inform external decisions such as whether or not to invest in, or lend to, the business. Sourced from: ways-to-financially-improve-your.html

4 Sourced from: Sourced from: An entity that generates losses rather than profits is not sustainable. The statement of profit or loss reflects the accounting return for an entity for a specified time period. Periodic determination of an entity s profit or loss is necessary because users need to assess the profitability of an entity throughout its life. Users rely on periodic profit or loss figures to evaluate past decisions, revise predictions and make future decisions.

5 Accrual accounting vs. Cash accounting Accrual accounting is a system in which transactions are recorded in the period to which they relate, rather than in the period the entity receives or pays the cash related to the transaction. This means that the reported profit or loss based on the accrual system is the difference between income and expenses for the period. An entity required to comply with accounting standards must prepare its financial statements on an accrual basis. A cash accounting system, in contrast, would determine cash profit or loss as the difference between the cash received in relation to income items and the cash paid for expenses for the period. Entities not required to comply with accounting standards, such as many small businesses, may prepare their financial statements on a cash basis. Sourced from:

6 Measuring financial performance Profit or loss is not formally defined in the Conceptual Framework, but instead is identified as being measured as the difference between income and expenses in a reporting period. To measure the profit or loss of an entity, it is therefore necessary to identify and measure all income and expense items attributable to the reporting period.

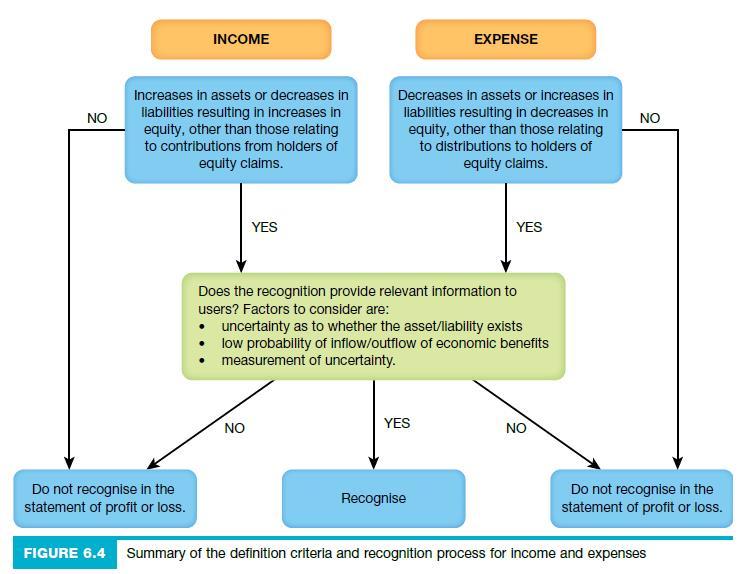

7 Income Sourced from: -guaranteed-income-for-life-doesnt-always-offerthe-best-retirement-options/ Income is defined in the proposed Conceptual Framework (para. 4.48) as: increases in assets or decreases in liabilities that result in increases in equity, other than those relating to contributions from holders of equity claims. Income encompasses both: Revenue arising in the ordinary course of activities (for example, sales, fees, dividends) Gains; all other inflows (for example, gains on disposal of non-current assets)

8 Recognition of income Revenue should be recognised only when: The increases in assets or reduction of liabilities have probably resulted from inflows of economic benefits and these movements can be reliably measured. Or can be more simply stated when the earning process is substantially complete and measurable and when the receipt of payment for the goods and services is reasonably certain.

9

10 Classification of income By income-generating activities By income types Sourced from: Sales, fees, commissions, interest, royalties, rent, non-reciprocal transfers Sourced from: Sourced from: Sourced from: ion-clip-art

as: decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, other than those")

11 Expenses Expenses are defined in the proposed Conceptual Framework (para. 4.49) as: decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, other than those relating to distributions to equity participants. Or put simply, a money sacrifice or the incurring of a liability in the pursuit of business objectives. Sourced from:

12 Cost of sales expense is the main expense incurred by a retailer in order to sell goods and generate income, the entity must purchase goods for resale. Sourced from: Sourced from: king_costs_delivery_price_transportation_tru ck_van_icon Sourced from: ation-clipart-of-a-dollar-bill-mascot-cartoon- character-holding-a-red-telephone-by-toons4biz- 489 Other expenses include wages and salaries, depreciation, rent, telephone, electricity, delivery costs, advertising. Note: drawings taken by owners (or dividends paid to shareholders) are not expenses.

13 Recognition of expense An expense should be recognised in the current period if:- It is probable that the decrease in economic benefits has occurred The amount can be reliably measured. Examples of expenses are, payment of wages, payment of electricity bill, purchasing a machine or other asset type, purchase of goods for resale.

14 Classification of expenses There is some choice as to how to display and classify expenses in the income statement. Smaller entities: often list all their expenses in the income statement Larger entities: aggregate their expenses into certain classes for reporting purposes Reporting entities: required to classify their expenses by nature or function

15 Decision tree for classifying assets and expenses

16

.")

17 Gross profit and cost of goods sold GROSS PROFIT = REVENUE COST OF SALES Not all businesses have COGS (cost of goods sold), generally service businesses do not (e.g. a law firm, or a tax accounting firm). Cost of Sales Beginning Inventory Purchases Ending Inventory

18 Timing is important Sourced from: Deciding when (i.e. in which accounting period) costs should be recognised as expenses: If an item or service is acquired during that year (or accounting period) and consumed during that year (period), therefore the expenses are recognised in that same accounting period. Whether or not the item has been paid for is not relevant.

19 Format of the income statement Format of the income statement will be affected by the following factors: Size of the organisation Type of the organisation Types of users who will read the income statement

20 Income Statement format for a non-reporting entity For sole traders and partnerships, there are virtually no regulations covering the format. No prescribed reporting format for income statements prepared by non-reporting entities. Although presentation and classification of items may show great diversity, the purpose of the income statement does not change: to report the profit for the entity for the reporting period. The profit objective is not necessarily relevant for all entities.

21 Income Statement format for a non-reporting entity

22 Prescribed format for reporting entities The accounting standard governing the presentation of the statement of profit or loss requires the following to be presented on the statement of profit or loss: Revenue Cost of sales (if revenue from sales is disclosed) Finance costs Share of profit or loss of associates and joint ventures if equity accounted Tax expense Profit or loss.

23 Prescribed format for reporting entities

24 Material income and expenses must be disclosed separately via either the income statement or the notes. The determination of whether an item is material is based on: The size and/or nature of the item Whether its non-disclosure could influence users decision making

25 Revenue Less Cost of Sales Gross Profit Less Distribution Costs Administration Expenses Finance Costs Other Expenses Profit (Before Tax) Less Income Tax Expense Profit (After Tax) Victory Ltd Statement of Profit and Loss for the year ended 30 June 2014

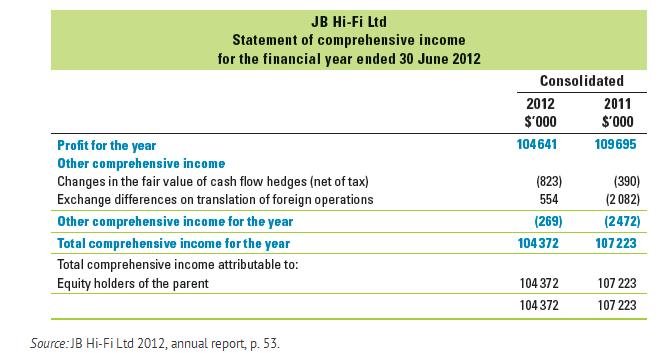

26 Statement of Comprehensive Income Reporting entities can elect to present all items of income and expense in a reporting period in a single statement of comprehensive income or in two statements: An Income Statement that shows the income and expenses associated with the determination of profit (or loss) for the reporting period. A statement beginning with profit or loss and displaying components of other comprehensive income is Statement of Comprehensive Income.

27 The Statement of Comprehensive Income shows all items of income and expense during the reporting period, including those items recognised in determining profit or loss, as well as items of other comprehensive income taken directly to equity. Comprehensive income items that may be added or subtracted from net profit to arrive at total comprehensive income for the period.

28 Comprehensive Income Items Increase in Fair Value of Property Gain or Loss related to Superannuation Benefit Plans Gain or Loss from Revaluation of Financial Assets Gain or Loss from Foreign Currency Transactions

29

30 Other comprehensive income (positive or negative) is added to the profit (or loss) this shows all non owner changes that have occurred in assets and liabilities that have occurred in the period. Examples: Unrealised gain (loss) on revaluation of properties Unrealised gain (loss) for the year on available for sale financial assets Gain (losses) on foreign currency translation of investments in foreign operations

31 Victory Ltd Statement of Profit and Loss and Other Comprehensive Income for the year ended 30 June 2014 Revenue Less Cost of Sales Gross Profit Less Distribution Costs Administration Expenses Finance Costs Other Expenses Profit (Before Tax) Less Income Tax Expense Profit (After Tax) Add Other Comprehensive Income Profit and Loss and Other Comprehensive Income

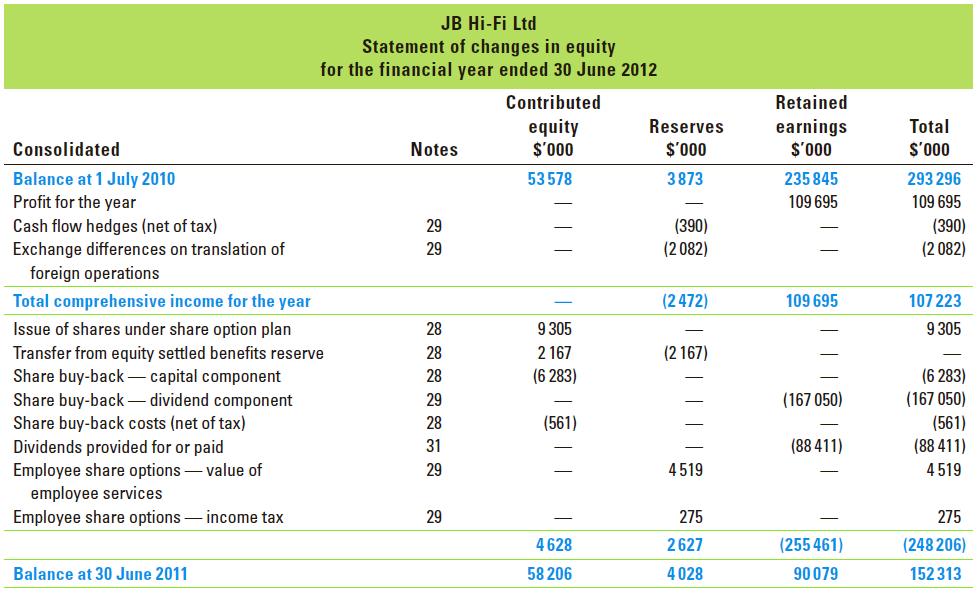

32 Statement of Changes in Equity The purpose of the statement of changes in equity is to report all owner changes to equity that are taken directly to the equity section of the balance sheet, together with the comprehensive income for the period. This, therefore, shows the total changes to the equity for the period. It enables users to observe the overall change in equity during a period.

33

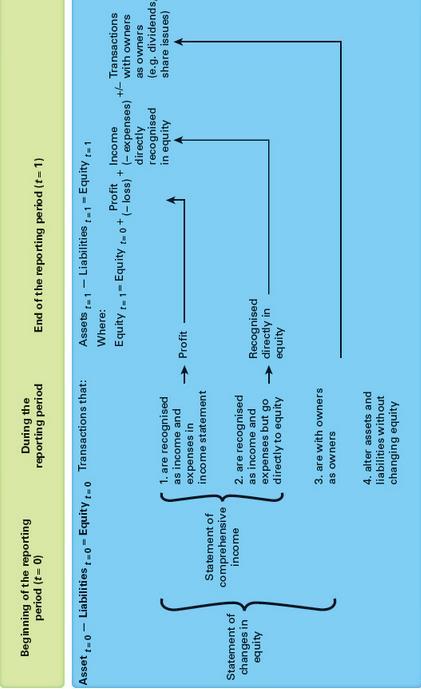

34 Link between financial statements It is important to understand the relationships between the financial statements, rather than viewing each statement in isolation. The Income Statement presents the profit or loss made by the entity during the reporting period. The Statement of Comprehensive Income reports the profit or loss and other comprehensive income. The Statement of Changes in Equity explains the changes in equity from the start to the end of the reporting period.

35 The Balance Sheet shows the financial position of the entity as at the end of the reporting period. The profit or loss for the reporting period is added to the retained earnings as at the start of the period. The entity can make distributions from retained earnings (i.e. dividends or drawings) and transfers to or from retained earnings. The balance of the retained earnings as at the end of the reporting period is included as an equity item in the balance sheet.

36

. Accounting (9 th ed.). Milton, Qld: John Wiley & Sons.")

37 Deferrals and Accruals Sourced from: Beattie, C., Chalmers, K., Edwards, L., Hellmann, A., Hoggett, J., Medlin, J., Maxfield, J. (2015). Accounting (9 th ed.). Milton, Qld: John Wiley & Sons.

38 Prepaid Expenses - Prepayments They are payments made in advance. The portion of the payment relating to the unexpired portion of the benefit (e.g. insurance) is reflected as a current asset in the balance sheet of the business. The portion that has been expired (or used up) is expressed as an expense in the period to which it relates (e.g. January 20X4).

39 Accrued Expenses - Accruals Expenses that have been incurred but are not yet recorded in the accounts. A good example is an electricity invoice because these invoices are based on usage they are received in the next accounting period. Estimated value has to be accrued using following entries: Expense (Income Statement) Accrued Expense (Balance Sheet - Current Liability) The entry is usually reversed at the beginning of the next accounting period and exact value is recorded under Payables once the invoice is received.

40 Debtors Sourced from: Commonly known as Accounts Receivable, however the terms are interchangeable and mean the same thing. Debtor occurs when a business sells goods or services to a third party on credit terms, i.e. when the goods or services are sold on the understanding that payment will be received at a later date. The amount will be recognised as an Accounts Receivable (Debtors) on the Balance Sheet under the heading Current Assets to be received within a year. At the same time it will be recognised as a Sale on the Income Statement.

41 Bad Debts In reality, most businesses will not collect all money owed to it. There are some debtors who will not/cannot pay. When payment cannot be collected the amount is referred to as a bad debt, some reasons for bad debts could be: Debtors bankruptcy Death of the debtor Disagreement regarding the contract for goods/services provided Sourced from: /bad-debts

42 Allowance for Doubtful Debts A common method in medium to large businesses is to provide or allow for an amount every month for doubtful debts, not specifically relating to any debtor, but for the purpose of creating an allowance account for the amount that we expect debtors not to pay. Allowance for doubtful debt is recorded as a contra asset account and expensed under Bad Debt Expense on the Income Statement.

43 Trade Creditors Established businesses find it more convenient to establish accounts with suppliers and pay for their purchases after they have received the goods or services. The amount will be recognised as an Accounts Payable (Creditors) on the Balance Sheet under the heading Current Liabilities which are payable within a year. The amount of time the business has to pay will depend on the credit terms established by the supplier.

44 Exercise Items to be categorised Accrued Interest Accumulated Depreciation Depreciation Expense Cost of Sales Drawings Goodwill Interest Expense Sales Prepaid Rent Telephone Wages Motor Vehicle Fees received Income Statement Balance Sheet

45 Items to be categorised Accrued Interest Accumulated Depreciation Depreciation Expense Cost of Sales Drawings Goodwill Interest Expense Sales Prepaid Rent Telephone Wages Motor Vehicle Fees Received Income Statement Depreciation Expense Cost of Sales Interest Expense Sales Telephone Wages Fees Received Balance Sheet Accrued Interest Accumulated Depreciation Drawings Goodwill Prepaid Rent Motor Vehicle

46 References Birt, J., Brooks, A., Chalmers, K., Maloney, S., Oliver, J. (2017). Accounting: business reporting for decision making (6 th ed.). Milton, Qld: John Wiley & Sons. Beattie, C., Chalmers, K., Edwards, L., Hellmann, A., Hoggett, J., Medlin, J., Maxfield, J. (2015). Accounting (9 th ed.). Milton, Qld: John Wiley & Sons. Birt, J., Brooks, A., Chalmers, K., Maloney, S., Oliver, J. (2014). Accounting: business reporting for decision making (5 th ed.). Milton, Qld: John Wiley & Sons.

Statement of Financial Position Module 1 Topic 2

Sourced from: https://www.dreamstime.com/illustration/balance-sheet.html Statement of Financial Position Module 1 Topic 2 Learning Objectives Describe the characteristics of business transactions Identify

Sourced from: https://www.dreamstime.com/illustration/balance-sheet.html Statement of Financial Position Module 1 Topic 2 Learning Objectives Describe the characteristics of business transactions Identify

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

Part 5: GLOSSARY OF TERMS

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

Introduction to Financial Accounting & Key Financial Statements (Chapter 1)

") Introduction to Financial Accounting & Key Financial Statements (Chapter 1) 14/10/2017 5:29:00 pm Accounting = process of identifying, measuring and communicating economic information to assist users in

Introduction to Financial Accounting & Key Financial Statements (Chapter 1) 14/10/2017 5:29:00 pm Accounting = process of identifying, measuring and communicating economic information to assist users in

- A resource - Controlled by the entity - As a result of a past event - From economic benefits are expected to flow to the entity.

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

PREVIEW OF CHAPTER 5-2

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Visit Free Slides and Ebooks : CHAPTER 23. Statement of Cash Flows

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

Unappropriated retained earnings (accumulated deficit) Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear

Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear") Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime The FRC's mission is to promote transparency and

Standard Accounting and Reporting Financial Reporting Council March 2018 FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime The FRC's mission is to promote transparency and

Cambridge IGCSE Accounting (0452)

") www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

CASH FLOWS FROM OPERATING ACTIVITIES

1 CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers (calc a) Cash paid to suppliers and employees (calc b) Cash generated from / (used in) operations Dividends received Interest received

1 CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers (calc a) Cash paid to suppliers and employees (calc b) Cash generated from / (used in) operations Dividends received Interest received

Financial Statement Balance Sheet Page 1 of 5 Financial Statement Balance Sheet Accounting Title 2013/09/30 2012/12/31 2012/09/30 2011/12/31 Balance Sheet Assets Current assets Cash and cash equivalents

Financial Statement Balance Sheet Page 1 of 5 Financial Statement Balance Sheet Accounting Title 2013/09/30 2012/12/31 2012/09/30 2011/12/31 Balance Sheet Assets Current assets Cash and cash equivalents

1

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

www.accountancyknowledge.com 1 CIMA C02 Fundamental of Financial Accounting Overview of Financial Accounting www.accountancyknowledge.com 2 Definitions of Accounting Accounting is the language of the business

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

st IFRS Consolidated Financial Statements

2461 2018 1st IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2018/03/31 2017/12/31 2017/03/31 Assets Current assets Cash and cash equivalents 1,552,283

2461 2018 1st IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2018/03/31 2017/12/31 2017/03/31 Assets Current assets Cash and cash equivalents 1,552,283

ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ DETAILED BALANCE SHEET. ASSETS I- Current Assets

ASSETS I- Current Assets A- Cash and Cash Equivalents 14 3.775.262.937 3.504.676.959 1- Cash 14 54.840 62.857 2- Cheques Received 3- Banks 14 3.388.494.332 3.105.334.647 4- Cheques Given and Payment Orders

ASSETS I- Current Assets A- Cash and Cash Equivalents 14 3.775.262.937 3.504.676.959 1- Cash 14 54.840 62.857 2- Cheques Received 3- Banks 14 3.388.494.332 3.105.334.647 4- Cheques Given and Payment Orders

ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ DETAILED BALANCE SHEET ASSETS

ASSETS I- Current Assets A- Cash and Cash Equivalents 14 3.815.809.477 3.504.676.959 1- Cash 14 45.563 62.857 2- Cheques Received - - 3- Banks 14 3.402.899.507 3.105.334.647 4- Cheques Given and Payment

ASSETS I- Current Assets A- Cash and Cash Equivalents 14 3.815.809.477 3.504.676.959 1- Cash 14 45.563 62.857 2- Cheques Received - - 3- Banks 14 3.402.899.507 3.105.334.647 4- Cheques Given and Payment

Financial Statement Overview. Introduction

Financial Statement Overview Bankers Insight Group, LLC Jeffery W. Johnson Introduction Financial Statement Analysis is the Cornerstone of a Bank s credit decision making process They report on an economic

Financial Statement Overview Bankers Insight Group, LLC Jeffery W. Johnson Introduction Financial Statement Analysis is the Cornerstone of a Bank s credit decision making process They report on an economic

Ray Sigorta Anonim Şirketi Balance Sheet As At 30 June 2016 (Currency: Turkish Lira (TL))

)") Balance Sheet ASSETS Current Period 30 June 2016 Audited 31 December 2015 I- Current Assets A- Cash and Cash Equivalents 280.951.812 226.401.451 1- Cash 53.648 45.712 2- Cheques Received 12 12 3- Banks

Balance Sheet ASSETS Current Period 30 June 2016 Audited 31 December 2015 I- Current Assets A- Cash and Cash Equivalents 280.951.812 226.401.451 1- Cash 53.648 45.712 2- Cheques Received 12 12 3- Banks

Course Outline. Introduction to accounting and accounting equation Ch.2, book 1 Section A

Course Outline Course Title: Fundamentals of Accounting Course No: BS (A&F): ACC 103 Class: BS (A &F), BS (Commerce), Course No: BS (Commerce): ACC 103 B.Com (Annual system): B.Com (Annual system): Part

Course Outline Course Title: Fundamentals of Accounting Course No: BS (A&F): ACC 103 Class: BS (A &F), BS (Commerce), Course No: BS (Commerce): ACC 103 B.Com (Annual system): B.Com (Annual system): Part

ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ DETAILED BALANCE SHEET (TRY) ASSETS I- Current Assets

ASSETS I- Current Assets") ASSETS I- Current Assets A- Cash and Cash Equivalents 14 3.066.806.799 3.217.463.827 1- Cash 14 30.243 35.109 2- Cheques Received 3- Banks 14 2.669.454.374 2.795.907.111 4- Cheques Given and Payment Orders

ASSETS I- Current Assets A- Cash and Cash Equivalents 14 3.066.806.799 3.217.463.827 1- Cash 14 30.243 35.109 2- Cheques Received 3- Banks 14 2.669.454.374 2.795.907.111 4- Cheques Given and Payment Orders

Income: Both revenue and gains, excluding contributions from equity participants

IAS 18 Revenue Definitions Income: Both revenue and gains, excluding contributions from equity participants Revenue: Income that arises in the course of ordinary activities of the entity Major revenue

IAS 18 Revenue Definitions Income: Both revenue and gains, excluding contributions from equity participants Revenue: Income that arises in the course of ordinary activities of the entity Major revenue

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5:

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5: 1 IAS 1 PRESENTATION OF FINANCIAL STATEMENTS OVERVIEW IAS 1 Presentation of Financial Statements sets out the overall requirements for financial

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5: 1 IAS 1 PRESENTATION OF FINANCIAL STATEMENTS OVERVIEW IAS 1 Presentation of Financial Statements sets out the overall requirements for financial

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Making sense of the dollars Understanding Financial Statements

Making sense of the dollars Understanding Financial Statements Presented by Nick Gaudion AUSTLAW WEBINAR 2015 FEBRUARY 2015 1.0 Introduction 1.1 Have you ever looked at a set of financial statements and

Making sense of the dollars Understanding Financial Statements Presented by Nick Gaudion AUSTLAW WEBINAR 2015 FEBRUARY 2015 1.0 Introduction 1.1 Have you ever looked at a set of financial statements and

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities

for Small and Medium-sized Entities") International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

Eumundi Combined Community Organisation Ltd ABN

Financial Statements ML Taylor & Associates 3/18 Mary Street Noosaville Qld 4566 Phone: 07 54499004 Email: louise@mltaylorassociates.com.au Contents Directors' Report Statement of Profit or Loss and Other

Financial Statements ML Taylor & Associates 3/18 Mary Street Noosaville Qld 4566 Phone: 07 54499004 Email: louise@mltaylorassociates.com.au Contents Directors' Report Statement of Profit or Loss and Other

HKAS 12 Income Taxes 1 November 2005

HKAS 12 Income Taxes 1 November 2005 HKAS 12 Income Taxes deals with both current taxes and deferred taxes but the most complex issue in HKAS 12 is no doubt rested on deferred taxes. HKAS 12 adopts a balance

HKAS 12 Income Taxes 1 November 2005 HKAS 12 Income Taxes deals with both current taxes and deferred taxes but the most complex issue in HKAS 12 is no doubt rested on deferred taxes. HKAS 12 adopts a balance

Module 7 Statement of Cash Flows

IFRS for SMEs Standard (2015) + Q&As IFRS Foundation Supporting Material for the IFRS for SMEs Standard Module 7 Statement of Cash Flows IFRS Foundation Supporting Material for the IFRS for SMEs Standard

IFRS for SMEs Standard (2015) + Q&As IFRS Foundation Supporting Material for the IFRS for SMEs Standard Module 7 Statement of Cash Flows IFRS Foundation Supporting Material for the IFRS for SMEs Standard

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") All Rights Reserved No. of Pages - 17 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II (INTAKE V GROUP B) END SEMESTER

All Rights Reserved No. of Pages - 17 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II (INTAKE V GROUP B) END SEMESTER

Total cash and cash equivalents 4,256,691 4,114,055

Historical Financial Statement Balance Sheet Provided by: FSP Technology Inc. Finacial year: Yearly Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents

Historical Financial Statement Balance Sheet Provided by: FSP Technology Inc. Finacial year: Yearly Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents

HON HAI PRECISION INDUSTRY CO., LTD. AND SUBSIDIARIES CONSOLIDATED SHEETS 2016 IFRS Consolidated Financial Statements

HON HAI PRECISION INDUSTRY CO., LTD. AND SUBSIDIARIES CONSOLIDATED SHEETS 2016 IFRS Consolidated Financial Statements Unit: NT$ thousand Accounting Title 2016/12/31 2015/12/31 Balance Sheet Assets Current

HON HAI PRECISION INDUSTRY CO., LTD. AND SUBSIDIARIES CONSOLIDATED SHEETS 2016 IFRS Consolidated Financial Statements Unit: NT$ thousand Accounting Title 2016/12/31 2015/12/31 Balance Sheet Assets Current

A. II. B. I. III. A. B.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

Full text edition Grant Thornton International Ltd. All rights reserved. PDF created with pdffactory Pro trial version

Full text edition 2008 Grant Thornton International Ltd. All rights reserved. 2008 Grant Thornton International Ltd. All rights reserved. Member firms of the Grant Thornton International organisation are

Full text edition 2008 Grant Thornton International Ltd. All rights reserved. 2008 Grant Thornton International Ltd. All rights reserved. Member firms of the Grant Thornton International organisation are

DOING BUSINESS IN UNITED KINGDOM

COMPANY FORMATION IN THE MAIN FORMS OF COMPANY/BUSINESS IN THE The legal structures for setting up a commercial business entity in the UK are: Incorporated entities - Private limited company - Public limited

COMPANY FORMATION IN THE MAIN FORMS OF COMPANY/BUSINESS IN THE The legal structures for setting up a commercial business entity in the UK are: Incorporated entities - Private limited company - Public limited

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Glossary of Terms NEL G-1

Glossary of Terms This glossary provides definitions for many terms in financial accounting 1 and refers readers back to those chapter sections in which the terms are discussed. If a good definition or

Glossary of Terms This glossary provides definitions for many terms in financial accounting 1 and refers readers back to those chapter sections in which the terms are discussed. If a good definition or

Berger Paints Jamaica Limited 1999

Berger Paints Jamaica Limited 1999 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31,1999 1 IDENTIFICATION The main activity of the company, which is incorporated in Jamaica, is the manufacture

Berger Paints Jamaica Limited 1999 NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31,1999 1 IDENTIFICATION The main activity of the company, which is incorporated in Jamaica, is the manufacture

Digging Into The Balance Sheet and Income Statement. The Balance Sheet

Digging Into The Balance Sheet and Income Statement Jim Menard, CCE email: jsmenard62@gmail.com The Balance Sheet Also called the statement of condition or statement of financial position Financial Condition

Digging Into The Balance Sheet and Income Statement Jim Menard, CCE email: jsmenard62@gmail.com The Balance Sheet Also called the statement of condition or statement of financial position Financial Condition

Update of the Registration Document Filed with the Autorité des Marchés Financiers on 29 June 2005 under reference number D.

Update of the Registration Document Filed with the Autorité des Marchés Financiers on 29 June 2005 under reference number D.05-0952 Update filed with the Autorité des Marchés Financiers 21 November 2005

Update of the Registration Document Filed with the Autorité des Marchés Financiers on 29 June 2005 under reference number D.05-0952 Update filed with the Autorité des Marchés Financiers 21 November 2005

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Number Key Question Number Key 1 B 16 B 2 D 17 C 3 B 18 B 4 A 19 A 5 D 20 D 6 A 21 C 7 C 22 A 8 D 23 D 9 A 24 B 10 C 25 C 11 C 26 C 12 B 27

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Number Key Question Number Key 1 B 16 B 2 D 17 C 3 B 18 B 4 A 19 A 5 D 20 D 6 A 21 C 7 C 22 A 8 D 23 D 9 A 24 B 10 C 25 C 11 C 26 C 12 B 27

th IFRS Consolidated Financial Statements

2461 2017 4th IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2017/12/31 2016/12/31 Assets Current assets Cash and cash equivalents Total cash and

2461 2017 4th IFRS Consolidated Financial Statements Balance Sheet Balance Sheet Unit: NT$ thousand Accounting Title 2017/12/31 2016/12/31 Assets Current assets Cash and cash equivalents Total cash and

Computershare Limited ABN

ASX PRELIMINARY FINAL REPORT Computershare Limited ABN 71 005 485 825 30 June 2007 Lodged with the ASX under Listing Rule 4.3A Contents Results for Announcement to the Market 2 Appendix 4E item 2 Preliminary

ASX PRELIMINARY FINAL REPORT Computershare Limited ABN 71 005 485 825 30 June 2007 Lodged with the ASX under Listing Rule 4.3A Contents Results for Announcement to the Market 2 Appendix 4E item 2 Preliminary

Consolidated Cash Flow Statement for the year ended 30th June, 2002

Consolidated Cash Flow Statement for the year ended 30th June, 2002 Notes Net cash inflow from operating activities (a) 4,916,217 6,797,641 Returns on investments and servicing of finance Interest received

Consolidated Cash Flow Statement for the year ended 30th June, 2002 Notes Net cash inflow from operating activities (a) 4,916,217 6,797,641 Returns on investments and servicing of finance Interest received

Millî Reasürans Türk Anonim Şirketi Unconsolidated Balance Sheet As At 30 September 2018 (Currency: Turkish Lira (TL))

)") Unconsolidated Balance Sheet As At ASSETS 1 Audited 31 December 2017 I- Current Assets A- Cash and Cash Equivalents 4.2,14 1.654.893.371 1.223.132.413 1- Cash 4.2,14 58.270 5.842 2- Cheques Received 3-

Unconsolidated Balance Sheet As At ASSETS 1 Audited 31 December 2017 I- Current Assets A- Cash and Cash Equivalents 4.2,14 1.654.893.371 1.223.132.413 1- Cash 4.2,14 58.270 5.842 2- Cheques Received 3-

CHAPTER 11 Current liabilities and contingencies

CHAPTER 11 Current liabilities and contingencies LEARNING OBJECTIVES 11-1. Describe the nature of liabilities and differentiate between financial and non-financial liabilities. 11-2. Describe the nature

CHAPTER 11 Current liabilities and contingencies LEARNING OBJECTIVES 11-1. Describe the nature of liabilities and differentiate between financial and non-financial liabilities. 11-2. Describe the nature

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Consolidated Financial Statements (In Canadian dollars) thescore, Inc. Years ended August 31, 2017 and 2016

thescore, Inc. Years ended August 31, 2017 and 2016") Consolidated Financial Statements (In Canadian dollars) thescore, Inc. Years ended August 31, 2017 and 2016 KPMG LLP Bay Adelaide Centre 333 Bay Street, Suite 4600 Toronto ON M5H 2S5 Canada Tel 416-777-8500

Consolidated Financial Statements (In Canadian dollars) thescore, Inc. Years ended August 31, 2017 and 2016 KPMG LLP Bay Adelaide Centre 333 Bay Street, Suite 4600 Toronto ON M5H 2S5 Canada Tel 416-777-8500

ANNUAL REPORT The Year in Review. Volume 2

ANNUAL REPORT The Year in Review Volume 2 Financial Statements and Independent Audit Reports Western Sydney University Western Sydney University Enterprises Pty Limited trading as Western Sydney University

ANNUAL REPORT The Year in Review Volume 2 Financial Statements and Independent Audit Reports Western Sydney University Western Sydney University Enterprises Pty Limited trading as Western Sydney University

PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

Executive Level. Financial Accounting & Reporting Fundamentals. (3) Section 1(a): 10 multiple choice questions (MCQs) all questions are compulsory.

Section 1(a): 10 multiple choice questions (MCQs) all questions are compulsory.") Copyright Reserved No. of pages: 14 Executive Level Financial Accounting & Reporting Fundamentals Instructions to candidates (1) Time allowed: Reading and planning 15 minutes Writing 3 hours (2) Total:

Copyright Reserved No. of pages: 14 Executive Level Financial Accounting & Reporting Fundamentals Instructions to candidates (1) Time allowed: Reading and planning 15 minutes Writing 3 hours (2) Total:

Paper No:34 Solved by Chanda Rehman & ABr

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

Talking Accounting Definitions

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Talking Accounting Definitions Introduction to Accounting week 1 Accounting The information system that measures business activities, processes that information into reports, and communicates the result

Financial statements. The University of Newcastle. newcastle.edu.au F1. 52 The University of Newcastle, Australia

Financial statements The University of Newcastle 52 The University of Newcastle, Australia newcastle.edu.au F1 Contents Income statement................. 54 Statement of comprehensive income..... 55 Statement

Financial statements The University of Newcastle 52 The University of Newcastle, Australia newcastle.edu.au F1 Contents Income statement................. 54 Statement of comprehensive income..... 55 Statement

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Millî Reasürans Türk Anonim Şirketi Unconsolidated Balance Sheet As At 30 June 2018 (Currency: Turkish Lira (TL))

)") Unconsolidated Balance Sheet As At ASSETS. 1 31 December 2017 I- Current Assets A- Cash and Cash Equivalents 4.2,14 1.237.184.185 1.223.132.413 1- Cash 4.2,14 52.698 5.842 2- Cheques Received 3- Banks

Unconsolidated Balance Sheet As At ASSETS. 1 31 December 2017 I- Current Assets A- Cash and Cash Equivalents 4.2,14 1.237.184.185 1.223.132.413 1- Cash 4.2,14 52.698 5.842 2- Cheques Received 3- Banks

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA. Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA31) FINANCIAL ACCOUNTING AND REPORTING

FINANCIAL ACCOUNTING AND REPORTING") ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA31) FINANCIAL ACCOUNTING AND REPORTING The following common mistakes, deficiencies were identified

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA31) FINANCIAL ACCOUNTING AND REPORTING The following common mistakes, deficiencies were identified

INTRODUCTION TO ACCOUNTING THEORY AND PRINCIPLES

SECTION 1 INTRODUCTION TO ACCOUNTING CHAPTER 1 THEORY AND PRINCIPLES Note in many cases with theory based questions, alternative answers or additional information may be appropriate. Solution 1.1 Directors,

SECTION 1 INTRODUCTION TO ACCOUNTING CHAPTER 1 THEORY AND PRINCIPLES Note in many cases with theory based questions, alternative answers or additional information may be appropriate. Solution 1.1 Directors,

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an):

- Please choose one Wages outstanding given in the trial balance will be treated as a (an):") Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

Question No: 1 ( Marks: 1 ) - Please choose one Wages outstanding given in the trial balance will be treated as a (an): Asset Liability Revenue Deferred expense Question No: 2 ( Marks: 1 ) - Please choose

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

KCE Electronics Public Company Limited and its subsidiaries

Statements of financial position Consolidated Separate financial financial 31 December 31 December Assets Note 2012 2011 2012 2011 Current assets Cash and cash equivalents 7 397,177,878 535,535,464 94,974,827

Statements of financial position Consolidated Separate financial financial 31 December 31 December Assets Note 2012 2011 2012 2011 Current assets Cash and cash equivalents 7 397,177,878 535,535,464 94,974,827

+44 (0) International Accounting Standards (IAS) Guidance: Terminology and Presentation

International Accounting Standards (IAS) Guidance: Terminology and Presentation") internationalenquiries@ediplc.com +44 (0) 2476 518951 www.lcci.org.uk International Accounting Standards (IAS) Guidance: Terminology and Presentation Contents Introduction 3 1 First Level 4 1.1 Terminology

internationalenquiries@ediplc.com +44 (0) 2476 518951 www.lcci.org.uk International Accounting Standards (IAS) Guidance: Terminology and Presentation Contents Introduction 3 1 First Level 4 1.1 Terminology

4/10/2012. Statement of Cash Flows. Learning Objectives (LO) LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)

LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)") Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

SSAP 12 STATEMENT OF STANDARD ACCOUNTING PRACTICE 12 INCOME TAXES

SSAP 12 STATEMENT OF STANDARD ACCOUNTING PRACTICE 12 INCOME TAXES (Issued August 2002) Contents Paragraphs OBJECTIVE SCOPE 1-4 DEFINITIONS 5-11 Tax Base 7-11 RECOGNITION OF CURRENT TAX LIABILITIES AND

SSAP 12 STATEMENT OF STANDARD ACCOUNTING PRACTICE 12 INCOME TAXES (Issued August 2002) Contents Paragraphs OBJECTIVE SCOPE 1-4 DEFINITIONS 5-11 Tax Base 7-11 RECOGNITION OF CURRENT TAX LIABILITIES AND

FRS 102 Ltd. Report and Financial Statements. 31 December 2015

Registered number 123456 FRS 102 Ltd Report and Financial Statements 31 December 2015 Report and accounts Contents Page Company information 1 Directors' report 2 Strategic report 4 Independent auditors'

Registered number 123456 FRS 102 Ltd Report and Financial Statements 31 December 2015 Report and accounts Contents Page Company information 1 Directors' report 2 Strategic report 4 Independent auditors'

Millî Reasürans Türk Anonim Şirketi Consolidated Balance Sheet As At 30 September 2017 (Currency: Turkish Lira (TL))

)") Consolidated Balance Sheet As At ASSETS Restated Audited 31 December 2016 I- Current Assets A- Cash and Cash Equivalents 14 4.776.447.134 4.342.688.861 1- Cash 14 81.993 52.555 2- Cheques Received 450.000

Consolidated Balance Sheet As At ASSETS Restated Audited 31 December 2016 I- Current Assets A- Cash and Cash Equivalents 14 4.776.447.134 4.342.688.861 1- Cash 14 81.993 52.555 2- Cheques Received 450.000

Chapter 2. The balance sheet: a snapshot of assets and liabilities of the enterprise

Chapter 2 The balance sheet: a snapshot of assets and liabilities of the enterprise 1 Fundamental Structure Resources Assets Claims to be satisfied Liabilities Asset: Resource owned or controlled by the

Chapter 2 The balance sheet: a snapshot of assets and liabilities of the enterprise 1 Fundamental Structure Resources Assets Claims to be satisfied Liabilities Asset: Resource owned or controlled by the

Workings. (40,000 x 45)- (40,000 x 4.5)-320,000 =1,300,000

- (40,000 x 4.5)-320,000 =1,300,000") Advanced Financial Accounting and Finance (AFF / OL 2) Operational Level Pilot Paper - Suggested Answer Scheme Section I Question No. Answer Segmental Learning Outcome (1) (D) Describe the structure, components

Advanced Financial Accounting and Finance (AFF / OL 2) Operational Level Pilot Paper - Suggested Answer Scheme Section I Question No. Answer Segmental Learning Outcome (1) (D) Describe the structure, components

FInAnCIAl StAteMentS

Financial STATEMENTS The University of Newcastle ABN 157 365 767 35 Contents 106 Income statement 107 Statement of comprehensive income 108 Statement of financial position 109 Statement of changes in equity

Financial STATEMENTS The University of Newcastle ABN 157 365 767 35 Contents 106 Income statement 107 Statement of comprehensive income 108 Statement of financial position 109 Statement of changes in equity

Power of association. Annual Report 2010

Power of association Annual Report Leadership and representation Power of association Financial Report Statement of Comprehensive Income for the year ended 0 June Revenue 9,6,798 0,0,0 Less: expenses Membership

Power of association Annual Report Leadership and representation Power of association Financial Report Statement of Comprehensive Income for the year ended 0 June Revenue 9,6,798 0,0,0 Less: expenses Membership

Lake Powell Almond Property Trust No.2

Lake Powell Almond Property Trust No.2 Annual report June 2010 Lake Powell Almond Property Trust No.2 Seven Fields Management Limited Responsible Entity Report The Directors of the Responsible Entity present

Lake Powell Almond Property Trust No.2 Annual report June 2010 Lake Powell Almond Property Trust No.2 Seven Fields Management Limited Responsible Entity Report The Directors of the Responsible Entity present

Learn Africa Plc. Quarter 2 Unaudited Financial Statement 1 st January to 30 th June 2016

Learn Africa Plc Quarter 2 Unaudited Financial Statement 1 st January to 30 th June 2016 1 Contents Statements of Accounting Policies 3 Statement of Comprehensive Income 11 Statement of Financial Position

Learn Africa Plc Quarter 2 Unaudited Financial Statement 1 st January to 30 th June 2016 1 Contents Statements of Accounting Policies 3 Statement of Comprehensive Income 11 Statement of Financial Position

CHAPTER 1 Accounting The information system that communicates the economic events of an entity to interested users (p. 7).

.") CHAPTER 1 Accounting The information system that communicates the economic events of an entity to interested users (p. 7). Accounting entity assumption An assumption that economic events can be identified

CHAPTER 1 Accounting The information system that communicates the economic events of an entity to interested users (p. 7). Accounting entity assumption An assumption that economic events can be identified

Financial summary. The Reporting Entity. Financial performance 38 ANNUAL REPORT 16/17

Financial summary The Reporting Entity TEQ, constituted under the Tourism and Events Queensland Act 2012, is a statutory body within the meaning given in the Financial Accountability Act 2009 and is controlled

Financial summary The Reporting Entity TEQ, constituted under the Tourism and Events Queensland Act 2012, is a statutory body within the meaning given in the Financial Accountability Act 2009 and is controlled

Australian Hotels Association Northern Territory Branch Inc.

Australian Hotels Association Northern Territory Branch Inc. General Purpose Financial Report for the year ended 30 June 2016 Contents Independent Auditor Report 1 Certificate by Prescribed Designated

Australian Hotels Association Northern Territory Branch Inc. General Purpose Financial Report for the year ended 30 June 2016 Contents Independent Auditor Report 1 Certificate by Prescribed Designated

INTRODUCTION PARTNERSHIPS

NCEA LEVEL 3 ACCOUNTING By Elizabeth Pitu 2013 BOOK 1 INTRODUCTION and PARTNERSHIPS Teacher Manual NCEA LEVEL 3 ACCOUNTING By Elizabeth Pitu 2013 BOOK 1 INTRODUCTION and PARTNERSHIPS Student Workbook STUDENT

NCEA LEVEL 3 ACCOUNTING By Elizabeth Pitu 2013 BOOK 1 INTRODUCTION and PARTNERSHIPS Teacher Manual NCEA LEVEL 3 ACCOUNTING By Elizabeth Pitu 2013 BOOK 1 INTRODUCTION and PARTNERSHIPS Student Workbook STUDENT

COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6)

") COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6) Problem A-I Multiple Choice. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. 1. 2. 3.

COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6) Problem A-I Multiple Choice. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. 1. 2. 3.

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Wiley CPAexcel EXAM REVIEW FOCUS NOTES

2016 Wiley CPAexcel EXAM REVIEW FOCUS NOTES 2016 Wiley CPAexcel EXAM REVIEW FOCUS NOTES FINANCIAL ACCOUNTING AND REPORTING Cover Design: Wiley Cover image: turtleteeth/istockphoto Copyright 2016 by John

2016 Wiley CPAexcel EXAM REVIEW FOCUS NOTES 2016 Wiley CPAexcel EXAM REVIEW FOCUS NOTES FINANCIAL ACCOUNTING AND REPORTING Cover Design: Wiley Cover image: turtleteeth/istockphoto Copyright 2016 by John

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Learn Africa Plc. Quarter 1 Unaudited Financial Statement 1 st January to 31 st March 2018

Learn Africa Plc Quarter 1 Unaudited Financial Statement 1 st January to 31 st March 2018 1 Contents Statements of Accounting Policies 3 Statement of Comprehensive Income 11 Statement of Financial Position

Learn Africa Plc Quarter 1 Unaudited Financial Statement 1 st January to 31 st March 2018 1 Contents Statements of Accounting Policies 3 Statement of Comprehensive Income 11 Statement of Financial Position

Cash Flow Statement Analysis

Cash Flow Statement Analysis 1. INTRODUCTION Recall from the article on the income statement that a company will recognize revenue regardless of when payment is received. For example, a company may sell

Cash Flow Statement Analysis 1. INTRODUCTION Recall from the article on the income statement that a company will recognize revenue regardless of when payment is received. For example, a company may sell

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows -350- LKAS 7 OTHER DISCLOSURES 48 52 EFFECTIVE DATE 53 ILLUSTRATIVE EXAMPLES A B Statement of cash flows for an entity other than a financial

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows -350- LKAS 7 OTHER DISCLOSURES 48 52 EFFECTIVE DATE 53 ILLUSTRATIVE EXAMPLES A B Statement of cash flows for an entity other than a financial

INTRODUCTION FORMAT OF THE INCOME STATEMENT:

INTRODUCTION What is the Income Statement ( Earning Statement)? Income statement is the report that measures the success of a company operations for a given period of time. What is the Usefulness of income

INTRODUCTION What is the Income Statement ( Earning Statement)? Income statement is the report that measures the success of a company operations for a given period of time. What is the Usefulness of income

Annual Qualification Review

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

Framework for the Preparation and Presentation of Financial Statements

Framework for the Preparation and Presentation of Financial Statements The IASB Framework was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001.

Framework for the Preparation and Presentation of Financial Statements The IASB Framework was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001.

Unilever Caribbean Limited

Financial Statements (Expressed In Trinidad and Tobago Dollars) Contents Page Auditors Report 1 Profit and Loss Account 2 Balance Sheet 3 Statement of Changes in Equity 4 Cash Flow Statement 5 Accounting

Financial Statements (Expressed In Trinidad and Tobago Dollars) Contents Page Auditors Report 1 Profit and Loss Account 2 Balance Sheet 3 Statement of Changes in Equity 4 Cash Flow Statement 5 Accounting

Accounting Title 2016/3/ /12/ /3/31 Balance Sheet

Financial Statement Balance Sheet Accounting Title 2016/3/31 2015/12/31 2015/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 626,334 624,357 540,732 Current

Financial Statement Balance Sheet Accounting Title 2016/3/31 2015/12/31 2015/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 626,334 624,357 540,732 Current

ANNUAL REPORT 2013/2014 C.28

ANNUAL REPORT 2013/2014 C.28 Annual Report 2013/2014 Message from the Chair and Chief Executive............................................................... 1 Financial Performance... 3 Directors Responsibility

ANNUAL REPORT 2013/2014 C.28 Annual Report 2013/2014 Message from the Chair and Chief Executive............................................................... 1 Financial Performance... 3 Directors Responsibility

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

John Ogilvie High School. Higher Accounting. Company Accounts

John Ogilvie High School Higher Accounting Company Accounts Question 1 The following figures were taken from the records of Ochil Industries plc as at 31 December Year 2. Dr Cr 000 000 Revenue of finished

John Ogilvie High School Higher Accounting Company Accounts Question 1 The following figures were taken from the records of Ochil Industries plc as at 31 December Year 2. Dr Cr 000 000 Revenue of finished

Original SSAP and Current Authoritative Guidance: SSAP No. 69

Statutory Issue Paper No. 92 Statement of Cash Flow STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 69 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current

Statutory Issue Paper No. 92 Statement of Cash Flow STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 69 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current

Examples of assets that would not be recognized:

Near-Term Financial Resources Overview Information about spending and resources available for spending Report amount available for spending in the next period Near-term would be a specific period of time,

Near-Term Financial Resources Overview Information about spending and resources available for spending Report amount available for spending in the next period Near-term would be a specific period of time,

IAS 7 : STATEMENT OF CASH FLOWS COMPILED BY: MR. YAGNESH DESAI.

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

PERTH REGION NRM Inc. FINANCIAL REPORT FOR THE YEAR ENDED 30 JUNE 2016

PERTH REGION NRM Inc. FINANCIAL REPORT FOR THE YEAR ENDED 30 JUNE 2016 Table of Contents Page No. Directors Report 2 Statement of Financial Position 3 Statement of Change in Equity 4 Cash Flow Statement

PERTH REGION NRM Inc. FINANCIAL REPORT FOR THE YEAR ENDED 30 JUNE 2016 Table of Contents Page No. Directors Report 2 Statement of Financial Position 3 Statement of Change in Equity 4 Cash Flow Statement