Transportation Select transportation for yourself and your spouse.

|

|

|

- Julianna Watson

- 5 years ago

- Views:

Transcription

1 Transportation Select transportation for yourself and your spouse. New Luxury Car Monthly payment: $1,170 Car insurance payment: $144 Gas for month: $300 Repairs: Under warranty Old Car Monthly payment: $0. Car paid for. Car insurance payment: $48 Gas for month: $300 Average monthly repair cost: $48 New Minivan Monthly payment: $708 Car insurance payment: $84 Gas for month: $360 Repairs: Under warranty New Sedan Monthly payment: $708 Car insurance payment: $72 Gas for month: $300 Repairs: Under warranty New Pickup Monthly payment: $630 Car insurance payment: $84 Gas for month: $360 Repairs: Under warranty New SUV Monthly payment: $930 Car insurance payment: $102 Gas for month: $360 Repairs: Under warranty Used Car Monthly payment: $408 Car insurance payment: $72 Gas for month: $300 Average monthly repair cost: $30 New 4WD Extended Cab Pickup Monthly payment: $930 Car insurance payment: $102 Gas for month: $390 Repairs: Under warranty Take The Bus, Save For a Car You bus to work while saving to purchase a vehicle. Monthly bus pass: $90

2 High-Cost Foods Groceries & Dining Select 1 choice of food for each week. Select at least 1 eating out choice. Select 1 coffee option for yourself and 1 for your spouse. Medium-Cost Foods Low-Cost Foods Steaks, roast beef, pork chops cost: $720 Casseroles, meatloaf, soups, mac & cheese cost: $480 Spaghetti, pizza, tacos, fish & chips cost: $360 Eat out at fast food restaurant Eat out at nice restaurant Coffee Shop $24 a visit for the whole family $48 a visit for you and your spouse $96 a month for a cup a day $19 a month for a cup a week $14 to buy supplies to make your own (1 per day for a month) All prices per person

3 Entertainment From the 3 pages of Entertainment activities, select at least 2 activities for each person age 2 or older in your household. Only 1 activity per person may be free. Bowl Visit the Zoo Trip to Black Hills Free admission $360 a person $12 a person per game Art Major League baseball game Picnic $30 for supplies $78 a person $5 a person Play board game Play Video Games Movie at Theater Free. You already have games. $66 to buy game $13 a person

4 Entertainment From the 3 pages of Entertainment activities, select at least 2 activities for each person age 2 or older in your household. Only 1 activity per person may be free. Rock Concert Party for family and friends Attend local school game $54 a person $120 $4 a person Visit Hawaii Visit London Vacation at Grandma s house $1,200 a person $1,440 a person $72 to take grandparents out for evening Camp Out Golf Fishing $120 $85 for gas and food/ $35 for camp site $36 a person for 9 holes Free. You already have a pole, equipment, and fishing license.

5 Entertainment From the 3 pages of Entertainment activities, select at least 2 activities for each person age 2 or older in your household. Only 1 activity per person may be free. Take a walk Free Join a gym $36 amonth for each person $90 a month for family membership Carnival $12 a person half-day $24 a person full-day Play with cat $24 a month for cat food Bicycle Free. You already have a bicycle. Ride a Horse $54 a person Dance $12 a person at a club Free at home

Fine")

Name")

6 Household Needs Select 1 from each category for your home. Furniture (select 1) Fine furniture: $180 a month Ordinary furniture: $120 a month Hand-me downs: Free Decorative (select 1) $120 a month for fine items $60 a month for nice items $30 a month for sale items Household needs (select 1) Name brand items: $30 a month Discount store items: $18 a month Thirft store items : $6 a month

7 Kid Care Formula is required for children 1 year old or younger. Diapers are required for children 3 years old or younger. This amount will automatically be deducted in the app. Make 1 selection from clothing, child care, and presents. Formula Diapers Clothing If your child is 1 year old or younger, you must buy formula. Cost: $160 a month If your child is 3 years old or younger, you must buy diapers. Cost: $150 a month $60 a month for brand name clothes $36 a month for department store clothes $12 a month for discount store clothes Free hand-me downs Child care Presents, books, and toys Because you are working, you must pay child care: $1080 a month for licensed day care provider $360 a month for grandma $36 a month for great stuff $24 a month for good stuff $12 a month for OK stuff $6 a month for stuff you buy used

Cell phone plan")

8 Shopping Choose at least one item to purchase. TV Charitable Donation Digital Camera Smart TV: $180 month 32 Classic HD TV: $30 a month $72 a month $48 a month $24 a month $12 a month $48 a month Includes camera, color printer, bag, and all accessories Boat Motorcycle Sound System $450 a month $300 monthly payment $150 a month for gas $480 a month $310 a month (for motorcycle) $170 a month for gas Great System: $54 a month Budget: $18 a month for music Computer Sports equipment and fees (per person) Cell phone plan Ultra System: $300 a month Plain System: $119 a month $90 a month for 3 sports $60 a month for 2 sports $30 a month for 1 sport Smart phone: $78 a month Plain phone: $42 a month Each additional plain phone: $12 a month

High-priced clothes: $180 a month per person (high-end specialty stores) Medium-priced")

Used clothes: $12 a month per person Personal Care (Select 1) $54 a month: Haircut every 3 weeks,")

9 Clothing & Personal Care Select 1 clothing option and 1 personal care option for both you and your spouse. Clothing (Select 1) High-priced clothes: $180 a month per person (high-end specialty stores) Medium-priced clothes: $90 a month per person (department stores) Low-priced clothes: $54 a month per person (discount stores) Used clothes: $12 a month per person Personal Care (Select 1) $54 a month: Haircut every 3 weeks, name brand shampoo, make-up, shaving supplies, etc. $30 a month: Haircut every 5 weeks, average shampoo, make-up, shaving supplies, etc. $8 a month: Haircut every 3 months, bulk shampoo, no make-up, no shaving supplies, etc.

Medium Apartment")

Personal possession insurance: $30 a month (optional) Small")

Large Apartment in Complex 2")

10 Housing & Utilities Select 1 housing choice, and then select phone, cable and Internet service. Purchase cell phones at Shopping. Large House 3 bedrooms, den Mortgage: $2,160 a month Electricity & heat: $300 a month Water & sewer: $78 a month Home Insurance (included) Medium Apartment Building 2 bedrooms Rent: $1,320 a month Electricity & heat: $102 a month Water & sewer: (included) Personal possession insurance: $30 a month (optional) Small House 2 bedrooms Mortgage: $1,320 a month Electricity & heat: $162 a month Water & sewer: $54 a month Home Insurance (included) Large Apartment in Complex 2 bedrooms, plus loft Rent: $1,680 a month Electricity & heat: $108 a month Water & sewer: (included) Personal possession insurance: $30 a month (optional) Small Apartment Building 1 bedroom Rent: $1,176 a month Electricity & heat: $66 a month Water & sewer: (included) Personal possession insurance: $30 a month (optional) Medium House 3 bedrooms Mortgage: $1,680 a month Electricity & heat: $222 a month Water & sewer: $54 a month Home Insurance (included) Mobile Home 3 bedrooms Mortgage: $780 a month Lot fee: $540 a month Electricity & heat: $120 a month Water & sewer: $54 a month Home Insurance (included) Phone/Cable/Internet Basic Phone: $30 a month Cable TV: add $48 a month Internet: add $36 a month

11 Bite of Reality Clothing / Personal Care The following is a list of codes for the clothing / personal care table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. ITEM High-priced Clothing Medium-priced Clothing Low-priced Clothing Used Clothing $45 Personal Care $25 Personal Care CODE C1 C2 C3 C4 P1 P2 $8 Personal Care P3

12 Bite of Reality Entertainment The following is a list of codes for the entertainment table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. ITEM CODE Art Board Games Ballgame Bike Ride Black Hills Trip Bowling Camp Out Carnival Half Day Carnival Full Day Dance at Club Dance at Home Gym Membership-Per Person Gym Membership-Family Fishing Local Golf High School Game Movie Theater Picnic Play with a Cat Ride a Horse Rock Concert Take a Walk Throw a Party Vacation at Grandma s House Video Games Visit Hawaii Visit London Zoo Art GAME BASE BIKE BH BOWL CAMP CARNH CARNF DANCEC DANCEH GYM FGYM FISH GOLF SGAME MOVIE PIC CAT HORSE Rock WALK PARTY GRAN VGame HAWAII LONDON Zoo

13 Bite of Reality Household Needs The following is a list of codes for the household needs table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. ITEM Fine Furniture Ordinary Furniture Hand-me Downs Fine Décor Nice Décor Sale Décor Name-brand Needs Discount Store Thrift Store items CODE F1 F2 Free D1 D2 D3 H1 H2 H3

14 Bite of Reality Kid Care The following is a list of codes for the kid care table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. ITEM Name Brand Dept. Store Discount Store Hand-me Downs Licensed Daycare Grandma Daycare CODE C1 C2 C3 Free D1 D2 Great Toys G1 Good Toys Ok Toys Used Toys G2 G3 G4 If your child is 1 years old or younger, you must buy formula The cost is $160 a month. If your child is 3 years old or younger, you must buy diapers The cost is $150 a month. The app will automatically add these cost to the Kid Care purchase, when it applies

15 Bite of Reality Shopping The following is a list of codes for the shopping table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. Students may choose up to ten items. ITEM CODE Smart TV 32 Classic HD TV Charitable Donation Charitable Donation Charitable Donation Charitable Donation Digital Camera Boat Motorcycle Sound system Budget system Ultra-computer Plain computer 3 Sports/month 2 Sports/month 1 Sport/month Smart Phone Plain Phone Addt l Plain Phone TV1 TV2 CH1 CH2 CH3 CH4 DC Boat MOTO SS1 SS2 C1 C2 SP3 SP2 SP1 CP1 CP2 CP3

16 Bite of Reality Housing / Utilities The following is a list of codes for the housing / utilities table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. ITEM CODE Large House Medium House Small House Mobile Home Large Apartment Small 2bd Apartment Small 1bd Apartment Basic Phone Cable TV Internet Acess H1 H2 H3 H4 A1 A2 A3 PH CA IN

17 Bite of Reality Groceries / Dining The following is a list of codes for the groceries / dining table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. ITEM High-Cost Food Med-Cost Food Low-Cost Food Fast Food Nice Restaurant Coffee Daily Coffee Weekly Buy a months supply to make your own CODE F1 F2 F3 Di1 Di2 Dr1 Dr2 Dr3

18 Bite of Reality Transportation The following is a list of codes for the transportation table to help students make their purchases. Once a student has made a decision, please provide them with the corresponding code. ITEM New Luxury Car New Sedan Used Car Old Car New Pickup New 4WD Truck New Minivan New SUV Bus Pass CODE Sport Sedan Used Old Pickup 4Wheel Van Suv Bus

19 Transportation Please review the choices offered on the Transportation options sheet. What to Expect Participants will come to your shop to purchase transportation for themselves and possibly for their spouses. They may buy 2 vehicles, or 1 vehicle and 1 bus pass. They cannot purchase 2 bus passes. The car dealer in our program is full service! Transportation is where buyers go to select a new or used vehicle; pay for insurance, gas, and repairs; and purchase bus passes. Expect a rush at the beginning of the session. Participants typically visit either the housing or transportation tables first. What to do Show selections to participants and let them make choices. Don t analyze what they really need or can afford. Avoid discussing features or any particular make or model. This is not the time to discuss how to buy a car. What to say Your role is to sell, not to help the participant make the best choice. For example, say things like: You re going to need a new minivan if you want to take your family on trips. Get the luxury car! You deserve it after walking around campus for years! Haven t you always wanted a new truck? If you get a line at your table, it s OK to remind participants with a comment in character: Hello. I m Jan. I m sorry, I m busy with another customer right now. You could shop at Kid Care or Entertainment and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements 1. Each adult must have at least 1 form of transportation. 2. Participants have the option of taking the bus instead of buying a vehicle, but only one person in the household can take the bus. 3. For each vehicle selected, there are 4 costs that must be entered on My Budget Work Sheet:* (1) Monthly payment (2) Car insurance payment (3) Gas per month (4) Repairs *Only when using the paper version of the program. Not relevant when using the app.

20 Transportation Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don't know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* My Budget Work Sheet Tips* If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide the right answers. If you find an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. *Only when using the paper version of the program. Not relevant when using the app.

21 Groceries & Dining Merchant Directions Please review the choices offered on the Groceries & Dining options sheet. What to Expect Participants will visit your shop to pay for groceries, eating out, and coffee. Groceries & Dining is the combination of grocery stores, restaurants, and coffee shops. What to do Show selections to participants and let them make choices. Don t analyze what they really need or can afford. Avoid discussing details. What to say Your role is to sell, not to help the participant make the best choice. For example, say things like: You both work hard. Go out! No one needs to cook every night. Everyone needs at least one latte a day. Don t you really want a steak at least once a week? If you get a line at your table, it s OK to remind participants with a comment in character: Hello. I m Jan. I m sorry, I m busy with another customer right now. You could shop at Transportation or Housing & Utilities and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements Participants must select food choice based on cost (high, medium, or low). Participants must select 1 eating out option either fine dining or fast food. Participants must select at least 1 coffee option for themselves, and 1 coffee option for their spouses if married. Tips Encourage participants to budget for eating out. * Only when using the paper version of the program. Not relevant when using the app.

22 Groceries & Dining Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don t know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* My Budget Work Sheet Tips* If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide the right answers. If you find an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. * Only when using the paper version of the program. Not relevant when using the app.

23 Entertainment Merchant Directions Please review the choices offered on the Entertainment options sheet. What to expect Participants will come to your shop to purchase entertainment a vacation, a game of golf, movie tickets, or art supplies. Some items, such as visits to the zoo and board games, are free. Each person age 2 and older in the household will select 2 activities from the 3 pages of activities. Only 1 of the activities per person may be free. What to do Show participants the selections and let them make choices. Don t analyze what they really need or can afford. Avoid discussing details. What to say Your role is to sell entertainment, not to help the participant make the best choice. For example, say things like: You and your wife are both working hard. Wouldn t a trip to Hawaii be a great vacation? Your child deserves the best experience possible. Wouldn t a gym membership be a good way to keep in shape? If you get a line at your table, it s OK to remind participants with a comment in character: Hello. I m Jan. I m sorry, I m busy with another customer right now. You could shop at Transportation or Housing & Utilities and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements Depending on the size of the family, there will be either 4 or 6 items purchased for entertainment. Only 1 free activity is allowed per person. Enter $0.00 for free activities.* * Only when using the paper version of the program. Not relevant when using the app.

24 Entertainment Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don t know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* My Budget Work Sheet tips* If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide right answers. If you fine an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. * Only when using the paper version of the program. Not relevant when using the app.

25 Household Needs Merchant Directions Please review the choices offered on the Household Needs options sheet What to expect Participants will come to your shop to purchase furniture, decorative items such as lamps and rugs, and household needs like dishes and towels. What to do Show selections to participants and let them make choices. Don t analyze what they really need or can afford. Avoid discussing details. This is not the time to teach participants how to shop for deals or how to save money. What to say Your role is to sell, not to help the participant make the best choice. For example, you might say things like: Fine furniture would really look great in your house! You have such a nice home. Why do you want to fill it with cheap items? Name brand items are always the best. If you get a line at your table, it s OK to remind people with a comment in character: Hello. I m Jan. I m sorry, I m busy with another customer right now. You could shop at Kid Care or Entertainment and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements Participants must select 1 item from each of the 3 categories on the selection sheet. My Budget Work Sheet tips* If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide right answers. If you fine an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. * Only when using the paper version of the program. Not relevant when using the app.

26 Household Needs Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return: 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don t know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* * Only when using the paper version of the program. Not relevant when using the app.

27 Kid Care Merchant Directions Please review the choices offered on the Kid Care options sheet. What to expect Participants with kids will come to your shop to purchase formula, diapers, clothing, child care, and presents/books/toys. What to do Show selections to participants and let them make choices. Don t analyze what they really need or can afford. Avoid discussing details. What to say Your role is to sell, not to help the participant make the best choice. For example, say things like: All parents want their child to have the best. Books and toys help your child learn. Seeing kids open their presents is the best part of the birthday party. If you get a line at your table, it s OK to remind participants with a comment in character: Hello. I m Jan. I m sorry, I m busy with another customer right now. You could shop at Transportation or Entertainment and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements Some families will need to purchase formula and diapers, depending on the ages of their children. When using the app, these items will be automatically deducted;there are no codes for diapers and formula. Formula is required for children 1 year old and younger. Diapers are required for children 3 years old and younger. There are 5 selections that must be purchased: Clothing Diapers (for child 3 years or younger) Formula (for child 1 year or younger) Child care Presents/books/toys * Only when using the paper version of the program. Not relevant when using the app.

28 Kid Care Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return: 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don t know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* My Budget Work Sheet tips* * If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide the right answers. If you find an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. * Only when using the paper version of the program. Not relevant when using the app.

29 Shopping Merchant Directions Please review the choices offered on the Shopping options sheet. What to expect Participants visit Shopping to purchase TVs, cell phones and service, digital cameras, sound systems, sports equipment, computers, boats, and motorcycles. They also make charitable contributions at the Shopping table. What to do Show selections to participants and let them make choices. Don t analyze what they really need or can afford. Avoid discussing details. What to say Your role is to sell, not to help the participant make the best choice. For example, say things like: So, you aren t going to have even one TV in your house? You only got a land line at Housing & Utilities. You won t have a cell phone unless you buy one from me. Looks like you ll have to go to the library to get online if you don t buy a computer. If you get a line at your table, it s OK to remind participants with a comment in character: Hello. I m Jan. I m sorry, I m busy with another customer right now. You could shop at Transportation or Housing & Utilities and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements Participants must make at least one purchase at your table. However, they may choose to purchase up to 10 items. * Only when using the paper version of the program. Not relevant when using the app.

30 Shopping Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return: 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don t know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* My Budget Work Sheet tips* If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide the right answers. If you find an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. * Only when using the paper version of the program. Not relevant when using the app.

31 Clothing & Personal Care Merchant Directions Please review the choices offered on the Clothing & Personal Care options sheet. What to expect Participants will come to your shop for clothing and personal care for themselves and for their spouse. Personal care covers things like shampoo, haircuts, makeup, and shaving supplies. What to do Show selections to participants and let them make choices. Don t analyze what they really need or can afford. Avoid discussing details. This is not the time to teach participants how to shop for deals or how to save money. What to say Your role is to sell, not to help the participant make the best choice. For example, you might say things like: High priced clothes make you look smart. Isn t that important at your job? Looking good really could help you get that promotion at work. Don t skimp on good makeup. Frequent haircuts will make your wife (or husband) look great. If you get a line at your table, it s OK to remind participants with a comment in character: Hello. I m Jan. I m sorry, I m busy with another customer right now. You could shop at Kid Care or Entertainment and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements Participants must make 1 clothing selection for themselves and 1 for their spouses, if married. Participants must make 1 personal care selection for themselves and 1 for their spouses, if married. * Only when using the paper version of the program. Not relevant when using the app.

32 Clothing & Personal Care Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return: 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don t know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* My Budget Work Sheet tips* If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide the right answers. If you find an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. * Only when using the paper version of the program. Not relevant when using the app.

33 Housing & Utilities Merchant Directions Please review the choices offered on the Housing & Utilities options sheet. What to expect The real-estate agent in the future is full service! This is where the participant goes to purchase housing, set up phone service, and pay utilities. Expect a rush at the beginning of the session. Participants typically visit either the housing or transportation tables first. What to do Show selections to participants and let them make choices. Don t analyze what they really need or can afford. Avoid discussing mortgage details or purchase options. This is not the time to teach students how to shop for a house or how to save money. What to say Your role is to sell, not to help the participant make the best choice. For example, you might say things like: There s a lot of room in a large house. How old is your child? She could have a special playroom in the extra bedroom. More space is always nice. That way you and your husband (or wife) can have room for your hobbies. Buy something big you can grow into. Then, when you have a larger family, you won t have to move. If you get a line at your table, it s OK to remind participants with a comment in character: Hi, I m Jan. I m sorry, I m busy with another customer right now. You could shop at Kid Care or Entertainment and stop back later. Payment tips* If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly. Requirements* Make sure participants have entered the correct amounts of My Budget Work Sheet for: Mortgage/ rent Electricity/heat Water/sewer Phone Insurance (optional for renters) * Only when using the paper version of the program. Not relevant when using the app.

34 Housing & Utilities Merchant Directions Have merchant appeal! Make your shop visually interesting by placing sales sheets and the provided props on your table. Returns Do not mention that returns are an option when you are selling. The goal is for participants to see the effects of spending more than they earn. Remember, you want to help them spend as much money as possible! As participants complete their budget, some may realize that they have over spent. If they ask to return an item, send them to the Credit Union for financial counseling. Only after counseling can they come back to you to return an item for something less expensive. How to process a return: 1. Ask if the participant has been to the Credit Union for financial counseling. 2. Tell the participant to select a new item. 3. If participants don t know how to re-balance their registers, send them to the Credit Union for help.* 4. There is no need for a new check; they will simply record the change on their registers.* My Budget Work Sheet tips* If necessary, show participants where to enter the information on My Budget Work Sheet. Don t correct math errors or provide the right answers. If you find an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. The amount entered for the cost of a phone is for a land line only. Participants can purchase cell phones and service at Bite of Reality Mall. * Only when using the paper version of the program. Not relevant when using the app.

35 The Credit Union Financial Institution What to expect This instruction sheet is for when using the BOR2 app and not the paper version Bite of Reality has a fantastic credit union for young adults. Here s where participants have checking/ share draft accounts, save for future goals, pay their credit card debt, and get financial advice. Participants may come to you for help with deciding what they can afford, making a credit card payment or return item(s) they have purchased. Participants will start the simulation with their monthly salaries already direct deposited to their checking accounts. The app will automatically deducted any Medical Insurance copay and Student loan payments. What to do Ensure that each participant has been assigned an identity on the BOR2 app. Participants will need to enter two passwords to start the app. The first code will be provided by the facilitator. The second password is "Start". You may have periods of time when no one comes to your table. After participants make a few purchases, they ll realize they have spent to much money and will need to come to the credit union for counseling or to make their credit card payment. They will need to pay the minimum payment on their card and will have the opportunity to pay an additional amount and the end.

36

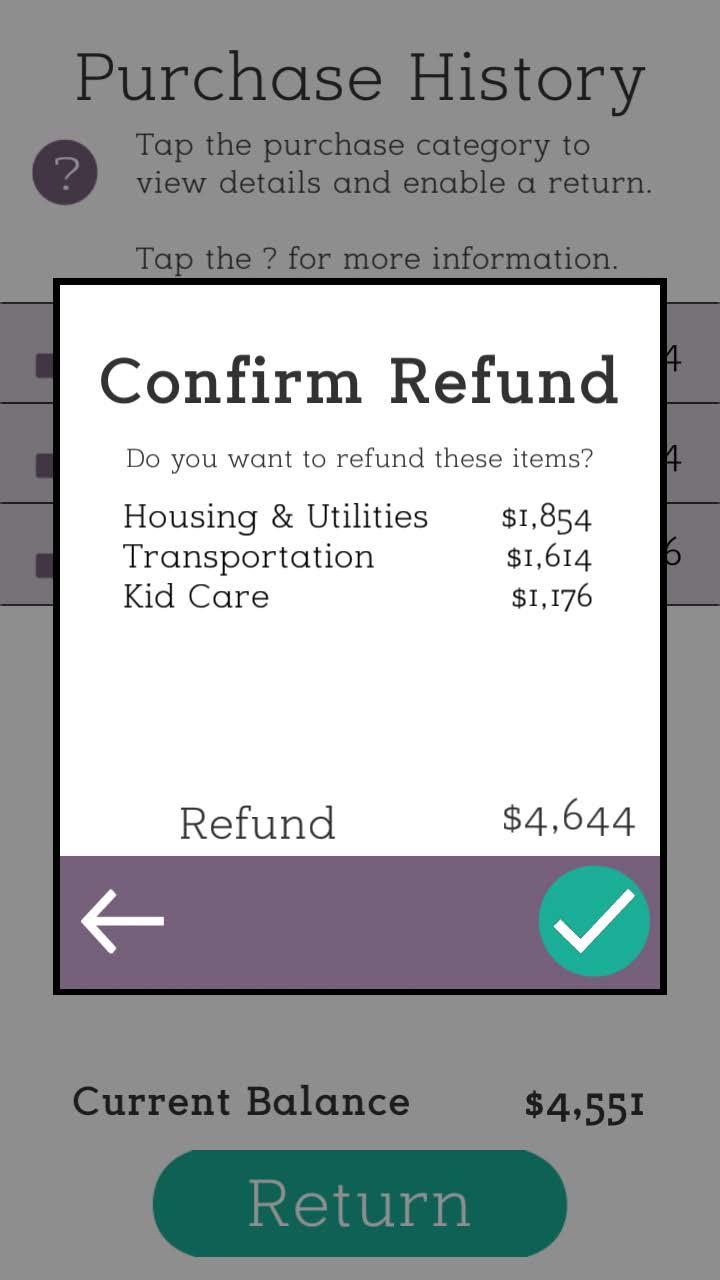

37 The Credit Union Financial Institution NOTE: Staff members at the credit union are different from the other merchants because their role is to help participants, not to sell them the most expensive merchandise. If participants end up in debt,use good financial counseling skills to help participants realize what to do. For example, if they complain they can t afford day care because they don t have enough money, ask them to look at their expenses. Can they live in a less expensive home? Suggest they look at transportation, food, clothing, and so on, in the same way. Ask questions that force them to think and make their own choices. Suggest that participants return items. For example, if a student chose 2 luxury cars, one or both could be returned for less expensive options. Participants may re-visit a merchant to make a new purchase after they have visited the credit union table for counseling and have made a return. Typical participant questions Why do I have to pay for more than the minimum on my credit card debt? It costs you less. If you only pay the minimum, it could take years to pay off the original charge plus the interest. (Try to avoid a lengthy lecture, but do provide short tips on the dangers of credit card debt.) Have merchant appeal! You may choose to display your credit union's logo at the Credit Union table. You may display banners or props from your credit union as space permits. How to process a return If a participant comes to you because they have accidentally pressed the budget pie chart and have been lock out of the app, enter the "BORA" code to access the return screen. If the student does not want to make a return, press the green return button. The app will confirm you are not making a return, press the green check and the participant is ready to continue shopping, Once participant have overspent, the app will lock. Enter the code "BORA" and press the green check to review their purchases. Help the participant decide on what to return. After they have made a decision on what items to return, press on the lock icon next to that station to unlock that purchase. Next press the unlock icon to confirm the return. You may return more that one station, however you will have to unlock each station one at a time. Once all stations to be returned have been selected, press return and then the green check to confirm. The participant will now have to go back to those stations to make a new purchase. When all purchases have been made, the participants will return to the credit union table to complete the survey. Wifi is required to have the survey ed to a teacher / origination leader. You may choose to do a paper version survey.

38 Fickle Finger of Fate Unplanned expenses and windfalls * Please review the Fickle Finger of Fate cards. They consist of windfalls, and unplanned expenses. Also review the Uh oh, I didn t plan for this and the Great! An Unexpected Windfall sections on My Budget Work Sheet that students complete during the session. When using the app, there is no need for a volunteer to play this role. Each participant will have Fickle Finger of Fate events pop up automatically during the simulation. This instruction sheet is provided only for those offering the paper program. What to expect The Fickle Finger of Fate (FFF) character represents life happens events and emergencies. He or she periodically and randomly gives each participant checks or bills. You may get realistic reactions ranging from anger and surprise to happiness and relief. News of your appearance will spread quickly. Participants may try to avoid you or even try to convince you that they already received enough bills. Rely on appropriate and realistic humor to help you deliver to news. What to do The FFF doesn t need to have a table unless you have a large group. About 10 minutes after the participants have started to shop in Bite of Reality, the FFF roams around the room stopping people to give them a windfall or expense. Each participant should get at least one unplanned expense and one windfall, but not at the same time. Plan your time and keep track so that you visit each participant twice. The FFF can use his/her discretion to select a fate especially for each participant. For example, if you know that the participant is renting and did not purchase personal possession insurance, give him or her the unplanned expense bill that describes Fire! What to say Use humor and realistic situations when delivering the fates. For example: Using the Oh, no! I ruined my jeans! bill... Hi. I met you at the neighborhood picnic last week. You sure did like the barbeque! You like it so much that you spilled it on yourself. Guess what? You ruined your jeans and have to buy a new pair. Pick how much you want to spend and pay me. Using the Remember the oldies but goodies? check... Hello. What s your favorite recording artist? Who don t you like? Well, it s a good thing you decided to sell all those (name group) CDs you don t want anymore. Smart move. You just made a little money to put in your retirement account. * Only when using the paper version of the program. Not relevant when using the app.

39 Fickle Finger of Fate Unplanned expenses and windfalls * Payment tips If your session is not using the app, participants will pay for their purchases with a check. Do not accept checks that are not written correctly.* The app will automatically deliver 2 FFF to each student and deduct it from their register. Ensure that each participant receives at least 1 windfall check and 1 unplanned expense bill and applies the correct amounts to the budget. Don t worry if you can t remember whether or not you gave a participant a card. You may ask participants to see the Uh oh, I didn t plan for this or Great! An unexpected windfall sections of the My Budget Work Sheet to see how many unplanned expenses or unexpected windfalls they received. My Budget Work Sheet Tips If necessary, show participants where to enter the information on My Budget Work Sheet. Unplanned expenses are entered on the Uh oh, I didn t plan for this section. Windfalls are entered on the Great! An unexpected windfall section. Don t correct math errors or provide the right answers. If you find an error, ask the participant to redo the addition. Say, This doesn t add up to the right amount. Please redo it. * Only when using the paper version of the program. Not relevant when using the app.

40 The Credit Union Financial Institution These instructions are for when using the paper version of the program. Please review the Savings & Contributions, Great! An unexpected windfall, and the My Debt sections of My Budget Work Sheet that participants complete during the session. What to expect Bite of Reality has a fantastic credit union for young adults. Here s where participants have checking/ share draft accounts, save for future goals, pay their credit card debt, add to their retirement accounts, and get financial advice. Participants will start the simulation with their monthly salaries already direct deposited to their checking accounts. What to do Ensure that the correct total amount of the participant s monthly household income is entered in the deposit column of their check register. (In Bite of Reality all couples have a joint checking account.) You may have periods of time when no one comes to your table. After participants make a few purchases, they ll realize they have to come to the credit union to pay their credit card debt. They will need to determine their minimum payment and pay an extra amount. Ensure that they have figured the amount accurately. You do not need to check the addition for every entry, but make sure the participants are keeping an accurate balance. What to say Participants may come to you for help with: Using a check register Deciding what they can afford Determining their credit card payments. NOTE: Staff members at the credit union are different from the other merchants because their role is to help participants, not to sell them the most expensive merchandise. If participants end up in debt Use good financial counseling skills to help participants realize what to do. For example, if they complain they can t afford day care because they don t have enough money, ask them to look at their expenses. Can they live in a less expensive home? Suggest they look at transportation, food, clothing, and so on, in the same way. Ask questions that force them to think and make their own choices

41 The Credit Union Financial Institution Suggest that participants return items or renegotiate with a vendor. For example, if a student chose 2 luxury cars, one or both could be returned for less expensive options. Remind the student to re-balance the register once a new item is selected. Participants may return items to a merchant if they have received financial counseling from the Credit Union. Typical participant questions Why do I have to pay more than the minimum on my credit card debt? It costs you less. If you only pay the minimum, it could take years to pay off the original charge plus the interest. (Try to avoid a lengthy lecture, but do provide short tips on the dangers of credit card debt.) Requirements Make sure participants have entered the correct amounts on My Budget Work Sheet for: Savings & Contributions My Debt Great! An unexpected windfall Make sure that participants are balancing their account in their registers. Make sure that participants are transferring totals from My Budget Work Sheet to My Spending & Savings Plan. Have merchant appeal! You may choose to display your credit union's logo at the Credit Union table. You may display banners or props from your credit union as space permits.

Value of Education: Education and Earning Power

Value of Education: Education and Earning Power Preparation Grade Level: 4-9 Group Size: 20-30 Time: 45-60 Minutes Presenters: 3-5 Objectives Students will be able to: Calculate monthly & annual earnings

Value of Education: Education and Earning Power Preparation Grade Level: 4-9 Group Size: 20-30 Time: 45-60 Minutes Presenters: 3-5 Objectives Students will be able to: Calculate monthly & annual earnings

YOUR GUIDE TO HEALTHY FINANCES GET YOUR FINANCES IN SHAPE

YOUR GUIDE TO HEALTHY FINANCES GET YOUR FINANCES IN SHAPE GETTING YOUR FINANCES UNDER CONTROL NEEDN T BE A HEADACHE Help is at hand with these easy-to-follow tips for getting your finances in shape. Whether

YOUR GUIDE TO HEALTHY FINANCES GET YOUR FINANCES IN SHAPE GETTING YOUR FINANCES UNDER CONTROL NEEDN T BE A HEADACHE Help is at hand with these easy-to-follow tips for getting your finances in shape. Whether

budget fixed expense flexible expense

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

VOLUNTEER TRAINING INFORMATION

VOLUNTEER TRAINING INFORMATION VOLUNTEER TRAINING Volunteers generally feel more comfortable in staffing a table if they have been provided with advance information about the concept and have time to read

VOLUNTEER TRAINING INFORMATION VOLUNTEER TRAINING Volunteers generally feel more comfortable in staffing a table if they have been provided with advance information about the concept and have time to read

Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if

Budgeting Your Money

Student Activities $ Lesson Three Budgeting Your Money 04/09 lesson 3 quiz: budgeting vocabulary choose the correct answer. 1. Which of these is not a source of income? a. Allowance b. Salary c. Interest

Student Activities $ Lesson Three Budgeting Your Money 04/09 lesson 3 quiz: budgeting vocabulary choose the correct answer. 1. Which of these is not a source of income? a. Allowance b. Salary c. Interest

Lifestyle Choices. An Exercise in Timbit Economics

Lifestyle Choices An Exercise in Timbit Economics Objective Participants will gain a better understanding of the relationship between money, choice and power through the experience of planning and implementing

Lifestyle Choices An Exercise in Timbit Economics Objective Participants will gain a better understanding of the relationship between money, choice and power through the experience of planning and implementing

Major Expenditure Mania Note-Taking Guide

2.15.2.L1 Note-taking guide Major Expenditure Mania Note-Taking Guide Total Points Earned Total Points Available Percentage My Money Bag Name Class Date Family Economics & Financial Education December

2.15.2.L1 Note-taking guide Major Expenditure Mania Note-Taking Guide Total Points Earned Total Points Available Percentage My Money Bag Name Class Date Family Economics & Financial Education December

Your money goals. Choosing a goal

Choosing a goal 01 Your money goals Next, think about a money goal that you most want to pursue towards that dream. Write down some ideas on how you could start working towards them. My money goal is:

Choosing a goal 01 Your money goals Next, think about a money goal that you most want to pursue towards that dream. Write down some ideas on how you could start working towards them. My money goal is:

Unit 5. Budgeting. Budget Trade-Offs A Penny Here and a Penny There. Rule 5: Live within your means.

Unit 5 Budgeting Lesson 5B: Budget Trade-Offs A Penny Here and a Penny There Rule 5: Live within your means. People work to earn income to purchase goods and services now (spending), later (saving), or

Unit 5 Budgeting Lesson 5B: Budget Trade-Offs A Penny Here and a Penny There Rule 5: Live within your means. People work to earn income to purchase goods and services now (spending), later (saving), or

Volunteer Guide. Curriculum made possible by:

Volunteer Guide Curriculum made possible by: Updated 9/22/2014 Volunteer Overview Welcome! Thank you for joining us at JA Finance Park for what promises to be an exciting learning experience. For several

Volunteer Guide Curriculum made possible by: Updated 9/22/2014 Volunteer Overview Welcome! Thank you for joining us at JA Finance Park for what promises to be an exciting learning experience. For several

BUDGETING SESSION OBJECTIVES SUBJECT INDEX

BUDGETING SESSION OBJECTIVES 8 Budgeting is the foundation of personal financial planning. Budgeting allows us to manage our money by tracking our income and expenses. Since every person is different,

BUDGETING SESSION OBJECTIVES 8 Budgeting is the foundation of personal financial planning. Budgeting allows us to manage our money by tracking our income and expenses. Since every person is different,

Income and Expense Statement Advanced Level

Income and Expense Statement Advanced Level The Costs Add Up How much do you think each item would cost if purchased every day for one month? Item Average Cost of Item Approximate Cost Per Month if purchased

Income and Expense Statement Advanced Level The Costs Add Up How much do you think each item would cost if purchased every day for one month? Item Average Cost of Item Approximate Cost Per Month if purchased

Volunteer Guide. Curriculum made possible by:

Volunteer Guide Curriculum made possible by: Updated September 2017 Volunteer Overview Welcome! Thank you for joining us at JA Finance Park for what promises to be an exciting learning experience. For

Volunteer Guide Curriculum made possible by: Updated September 2017 Volunteer Overview Welcome! Thank you for joining us at JA Finance Park for what promises to be an exciting learning experience. For

The Build-a- BudgeT Book

The Build-a- Budget Book The Build-a-Budget Book County Stamp Prepared by Marilyn Furry, associate professor of financial education and literacy programs, and Judith Ikenberry, former program assistant

The Build-a- Budget Book The Build-a-Budget Book County Stamp Prepared by Marilyn Furry, associate professor of financial education and literacy programs, and Judith Ikenberry, former program assistant

Making the Most of Your Money

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

Making the Most of Your Money A Handbook for Young Adults Table of Contents Let s start from the beginning:.....................1 Creating a budget:.............................. 2 Budget Worksheet:.............................

Income and Expense Statement Advanced Level

Income and Expense Statement Advanced Level The Costs Add Up How much do you think each item would cost if purchased every day for one month? Item Average Cost of Item Approximate Cost Per Month if purchased

Income and Expense Statement Advanced Level The Costs Add Up How much do you think each item would cost if purchased every day for one month? Item Average Cost of Item Approximate Cost Per Month if purchased

Chapter 1: How to Make and Stick to a Budget

Chapter 1: How to Make and Stick to a Budget How to Make and Stick to a Budget What s the first thing you think of when you hear the word budget? If you re like most people, you think of saving money and

Chapter 1: How to Make and Stick to a Budget How to Make and Stick to a Budget What s the first thing you think of when you hear the word budget? If you re like most people, you think of saving money and

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards)

Texas Essential Knowledge and Skills (Prerequisite standards)") Grade Level: 4 Smart Cash Lesson: 5 Lesson Description As in Mr. Cash s class, your students will play a game called Smart Cash. Groups of 3-4 students will use a game board and a set of game cards. Each

Grade Level: 4 Smart Cash Lesson: 5 Lesson Description As in Mr. Cash s class, your students will play a game called Smart Cash. Groups of 3-4 students will use a game board and a set of game cards. Each

Part 1: Situation and Savings (35 minutes)

") Volunteer Guide Introduction: Do you remember the first big decision you faced in using money? Were you prepared to make a good choice? How we manage our income really affects our lives and our families.

Volunteer Guide Introduction: Do you remember the first big decision you faced in using money? Were you prepared to make a good choice? How we manage our income really affects our lives and our families.

Budgeting: Making the Most of Your Money

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

HOW TO GET COMPLETELY OUT OF DEBT, INCLUDING YOUR MORTGAGE, IN 5 10 YEARS OR LESS. by Michael Harris

FINANCIAL FREEDOM BLUEPRINT DEBT FREE LIVING QUICK START GUIDE HOW TO GET COMPLETELY OUT OF DEBT, INCLUDING YOUR MORTGAGE, IN 5 10 YEARS OR LESS by Michael Harris DISCLAIMER: I don t give financial advice.

FINANCIAL FREEDOM BLUEPRINT DEBT FREE LIVING QUICK START GUIDE HOW TO GET COMPLETELY OUT OF DEBT, INCLUDING YOUR MORTGAGE, IN 5 10 YEARS OR LESS by Michael Harris DISCLAIMER: I don t give financial advice.

Act Your Wage. Learning to budget based on your income , Take Charge America

Act Your Wage Learning to budget based on your income. 2015, Take Charge America What is a Budget? A plan for spending your money. Understanding: what s coming in what s going out where it s going The

Act Your Wage Learning to budget based on your income. 2015, Take Charge America What is a Budget? A plan for spending your money. Understanding: what s coming in what s going out where it s going The

Fo od Bu dgeting Made Easy

Fo od Bu dgeting Made Easy 125 Fo od Bu dgeting Made Easy To The Educator: Energy is an important part of the learning environment. Once energy begins to decline, you can sense it. Eye contact with learners

Fo od Bu dgeting Made Easy 125 Fo od Bu dgeting Made Easy To The Educator: Energy is an important part of the learning environment. Once energy begins to decline, you can sense it. Eye contact with learners

The Budget Zone. Saving for A New Car Without Breaking the Bank. Course objectives learn about:

financialgenius.usbank.com Course objectives learn about: Setting Your Financial Goals Budgeting Your Income Understanding Interest and the Power of Investing The Budget Zone Saving for A New Car Without

financialgenius.usbank.com Course objectives learn about: Setting Your Financial Goals Budgeting Your Income Understanding Interest and the Power of Investing The Budget Zone Saving for A New Car Without

2. Analyze your spending. See how much you spend in each category. Notice any trends and look for expenses you can eliminate or cut back on.

Tool 1: Spending tracker Most people can t tell you how they spend their money during a month. Before deciding on changes to your spending, it is a good idea to understand how you use your money now. This

Tool 1: Spending tracker Most people can t tell you how they spend their money during a month. Before deciding on changes to your spending, it is a good idea to understand how you use your money now. This

Personal Budget Project

Personal Budget Project Students will prepare a personal budget that summarizes typical monthly expenses for a single person, living alone and newly entering the job market. The early part of the project

Personal Budget Project Students will prepare a personal budget that summarizes typical monthly expenses for a single person, living alone and newly entering the job market. The early part of the project

Budgeting for Success

UNIT 1 Being Financially Responsible Topic Budgeting for Success LEARNING OBJECTIVE(S) Students will: understand the steps involved in developing a budget, including identifying sources of income and the

UNIT 1 Being Financially Responsible Topic Budgeting for Success LEARNING OBJECTIVE(S) Students will: understand the steps involved in developing a budget, including identifying sources of income and the

Your Spending and Saving Plan

MODULE 4: Your Spending and Saving Plan MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public

MODULE 4: Your Spending and Saving Plan MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public

Episode 116: Budgeting Basics

Episode 116: Budgeting Basics Episode 116 Synopsis: BIZ KID$ The Biz Kid$ learn the first rule of money management: you can t manage what you don t know. Join the kids and you ll look at spending and expenses

Episode 116: Budgeting Basics Episode 116 Synopsis: BIZ KID$ The Biz Kid$ learn the first rule of money management: you can t manage what you don t know. Join the kids and you ll look at spending and expenses

YNAB Budgeting System User Guide

Budgeting System User Guide Table of Contents Introduction... 3 User Interface... 3 Legend... 4 Features... 4 A portable budget... 4 Budget with strategy... 4 Simple management... 5 Save money faster...

Budgeting System User Guide Table of Contents Introduction... 3 User Interface... 3 Legend... 4 Features... 4 A portable budget... 4 Budget with strategy... 4 Simple management... 5 Save money faster...

1. Referrals 2. Earn your business as clients 3. We are expanding & need help

3 Reasons Why We Are Here Tonight: 1. Referrals 2. Earn your business as clients 3. We are expanding & need help Do you have someone right now who handles your current financial needs other than yourselves?

3 Reasons Why We Are Here Tonight: 1. Referrals 2. Earn your business as clients 3. We are expanding & need help Do you have someone right now who handles your current financial needs other than yourselves?

EDUCATION FORM. Where do you plan to go? List all that apply - community college / four year institution and graduate school if applicable

Do you plan to attend college? EDUCATION FORM Where do you plan to go? List all that apply - community college / four year institution and graduate school if applicable Based on 2017 fees, how much will

Do you plan to attend college? EDUCATION FORM Where do you plan to go? List all that apply - community college / four year institution and graduate school if applicable Based on 2017 fees, how much will

Money Math for Teens. The Emergency Fund

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

Money Math for Teens The Emergency Fund This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education Foundation,

GATHER THE INFO STEP 1 - UNDERSTAND WHAT YOU EARN

Brought to you by Take Charge of Your Money GATHER THE INFO This workbook relates to Lessons 4 & 5 (the practical bits of creating a budget) but I would really encourage you to watch the videos in Lessons

Brought to you by Take Charge of Your Money GATHER THE INFO This workbook relates to Lessons 4 & 5 (the practical bits of creating a budget) but I would really encourage you to watch the videos in Lessons

A01. Single family. 5+ persons $250,000+ Homeowner. American Royalty Wealthy, influential couples and families living in prestigious suburbs

A A02 A03 A04 A05 A06 American Royalty Wealthy, influential couples and families living in prestigious suburbs James & Nancy 2.08% Who We Are Channel Preference Head of household age Type of property 51

A A02 A03 A04 A05 A06 American Royalty Wealthy, influential couples and families living in prestigious suburbs James & Nancy 2.08% Who We Are Channel Preference Head of household age Type of property 51

EDUCATION FORM. Where do you plan to go? List all that apply - community college / four year institution and graduate school if applicable

Do you plan to attend college? EDUCATION FORM Where do you plan to go? List all that apply - community college / four year institution and graduate school if applicable Based on 2016 fees, how much will

Do you plan to attend college? EDUCATION FORM Where do you plan to go? List all that apply - community college / four year institution and graduate school if applicable Based on 2016 fees, how much will

A budget is a spending plan. An estimation of income and expenses over time. A budget is simply spending your money with purpose.

Debt Free Seminar Agenda: Define Budget Why do we need to budget our finances? How to create a budget? How to pay off debt? How to identify Needs and Wants? What s Next? BUDGET WHAT IS IT? A budget is

Debt Free Seminar Agenda: Define Budget Why do we need to budget our finances? How to create a budget? How to pay off debt? How to identify Needs and Wants? What s Next? BUDGET WHAT IS IT? A budget is

Monthly Expenses Worksheet

Monthly Expenses Worksheet Education Rent or mortgage $ Tuition $ Heating (gas or oil) $ Books, papers and supplies $ Electricity $ Newspapers and magazines $ Water or sewage $ Lessons (sports, dance,

Monthly Expenses Worksheet Education Rent or mortgage $ Tuition $ Heating (gas or oil) $ Books, papers and supplies $ Electricity $ Newspapers and magazines $ Water or sewage $ Lessons (sports, dance,

How Much Does School Cost? Academic Costs (Domestic) Tuition and Fees = $6,992 - $10,710. Books & Supplies = $700 - $1300. TOTAL = $7,692 $12,010/year

Tuition and Fees = $6,992 - $10,710. Books & Supplies = $700 - $1300. TOTAL = $7,692 $12,010/year") Budgeting 101 Why Budget? So that you know what you can spend and when Helps you determine how you are going to stretch your resources (e.g. OSAP funding) over the entire year Allows you to live within

Budgeting 101 Why Budget? So that you know what you can spend and when Helps you determine how you are going to stretch your resources (e.g. OSAP funding) over the entire year Allows you to live within

Loans. Materials. What do you Want to Buy? Overhead 3-A. Beginner & Low-Intermediate

Loans Beginner & Low-Intermediate Materials Pre-reading What do you Want to Buy? Overhead 3-A Put a check ( ) next to the pictures of the things you might want to have or do. VALRC Money Talks Beginner/Low-Intermediate

Loans Beginner & Low-Intermediate Materials Pre-reading What do you Want to Buy? Overhead 3-A Put a check ( ) next to the pictures of the things you might want to have or do. VALRC Money Talks Beginner/Low-Intermediate

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards)

Texas Essential Knowledge and Skills (Prerequisite standards)") Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

TEACHER LESSON PLAN Lesson 2-4: Rights and Responsibilities OVERVIEW LEARNING OUTCOMES PREPARATION WHAT YOU WILL NEED NOTES:

TEACHER LESSON PLAN Lesson 2-4: Rights and Responsibilities OVERVIEW You probably don t think of a loan or credit-card application as a contract, but it is. By signing on the dotted line, you re entering

TEACHER LESSON PLAN Lesson 2-4: Rights and Responsibilities OVERVIEW You probably don t think of a loan or credit-card application as a contract, but it is. By signing on the dotted line, you re entering

FAMILIES & CREDIT CARDS

Purpose of Training FAMILIES & CREDIT CARDS A CONSUMER ACTION TRAINING GUIDE This training is designed to help you help parents provide their children with a better understanding of how to use credit wisely

Purpose of Training FAMILIES & CREDIT CARDS A CONSUMER ACTION TRAINING GUIDE This training is designed to help you help parents provide their children with a better understanding of how to use credit wisely

Volunteer Guide. Curriculum made possible by: Updated 1/22/18

Volunteer Guide Curriculum made possible by: Updated 1/22/18 Volunteer Overview Welcome! Thank you for joining us at Lincoln Finance Park for what promises to be an exciting learning experience. For several

Volunteer Guide Curriculum made possible by: Updated 1/22/18 Volunteer Overview Welcome! Thank you for joining us at Lincoln Finance Park for what promises to be an exciting learning experience. For several

Adding & Subtracting Percents

Ch. 5 PERCENTS Percents can be defined in terms of a ratio or in terms of a fraction. Percent as a fraction a percent is a special fraction whose denominator is. Percent as a ratio a comparison between

Ch. 5 PERCENTS Percents can be defined in terms of a ratio or in terms of a fraction. Percent as a fraction a percent is a special fraction whose denominator is. Percent as a ratio a comparison between

MONEY. Of course, going to college means. Managing Your Money CHAPTER 3. Watching everyday spending

CHAPTER 3 Managing Your Money MONEY Of course, going to college means attending classes, writing papers, and taking exams. But making money choices also is an important part of your college life. Good

CHAPTER 3 Managing Your Money MONEY Of course, going to college means attending classes, writing papers, and taking exams. But making money choices also is an important part of your college life. Good

Brought to you by. party PARTY LIST PARTY SONG HAPPY BIRTHDAY BANNER DJ FLASHY PARTY HIRE PARTY STORE

HAPPY BIRTHDAY BANNER DJ FLASHY PARTY HIRE PARTY STORE PARTY SONG Invisible Money It s Easy to Spend More Money than you Have! Brought to you by LIST PARTY party This Activity Answers The Question... PAGE

HAPPY BIRTHDAY BANNER DJ FLASHY PARTY HIRE PARTY STORE PARTY SONG Invisible Money It s Easy to Spend More Money than you Have! Brought to you by LIST PARTY party This Activity Answers The Question... PAGE

Lesson Module 1: The Fundamentals of Net Worth

Lesson Module 1: The Fundamentals of Net Worth Module 1 Overview The entire game of football is based on a few basic skills: blocking, tackling, passing and running. To be a successful football player,

Lesson Module 1: The Fundamentals of Net Worth Module 1 Overview The entire game of football is based on a few basic skills: blocking, tackling, passing and running. To be a successful football player,

Product Guide. What is the Platinum Discount Network? FIVE STAR PASS. TheCreditPros Services. Advantages: Selling Platinum Discount Network

Product Guide What is the Platinum Discount Network? The Platinum Discount Network is an exclusive member s only savings program that offers discounts on travel, retail, dining, personal services, free

Product Guide What is the Platinum Discount Network? The Platinum Discount Network is an exclusive member s only savings program that offers discounts on travel, retail, dining, personal services, free

Schedule J: Your Expenses 12/13

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number _ (If known) Check if this is an amended filing

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number _ (If known) Check if this is an amended filing

Your Spending and Saving Plan

MODULE 4: Your Spending and Saving Plan MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public

MODULE 4: Your Spending and Saving Plan MONEY SMART for Adults SEPTEMBER 2018 The Federal Deposit Insurance Corporation is an independent agency created by the Congress to maintain stability and public

MAKE MONEY MAKE SENSE

Budgeting Activity Teaching aims of the session Possible teaching activity Learning outcomes To recap on the concept of budgeting and money management. To explain how to budget and explain how much things

Budgeting Activity Teaching aims of the session Possible teaching activity Learning outcomes To recap on the concept of budgeting and money management. To explain how to budget and explain how much things

Your financial plan workbook

Your financial plan workbook Purpose of this workbook This workbook is designed to help you collect and organize the information needed to develop your Financial Plan, and will include your goals and

Your financial plan workbook Purpose of this workbook This workbook is designed to help you collect and organize the information needed to develop your Financial Plan, and will include your goals and

Buying a Car. A Car Means Convenience. Which Car Is Right for You? New or Used?

Buying a Car Getting a car of your own is exciting, but it also involves a lot of work. For people with little or no credit history, a loan can be hard to get. Insurance is expensive and usually required

Buying a Car Getting a car of your own is exciting, but it also involves a lot of work. For people with little or no credit history, a loan can be hard to get. Insurance is expensive and usually required

You re On Your Own Checking Account Exercise

Checking Account Exercise Supplement to Making The Right Money Moves Check Writing Exercise You re On Your Own Imagine that you are now out on your own - moving on out to the big time and that new apartment.

Checking Account Exercise Supplement to Making The Right Money Moves Check Writing Exercise You re On Your Own Imagine that you are now out on your own - moving on out to the big time and that new apartment.

Contents About... 3 Features... 4 Method... 5 Rule One: Give Every Dollar a Job... 5 Rule Two: Save for a Rainy Day... 5 Rule Three: Roll With the

YNAB 4 USER GUIDE Contents About... 3 Features... 4 Method... 5 Rule One: Give Every Dollar a Job... 5 Rule Two: Save for a Rainy Day... 5 Rule Three: Roll With the Punches... 6 Rule Four: Live on Last

YNAB 4 USER GUIDE Contents About... 3 Features... 4 Method... 5 Rule One: Give Every Dollar a Job... 5 Rule Two: Save for a Rainy Day... 5 Rule Three: Roll With the Punches... 6 Rule Four: Live on Last

For many years we were happy to spend too freely, borrow too much and

For many years we were happy to spend too freely, borrow too much and hand our money over to someone else to manage, hoping to ride a market that always went up. Well, times have changed and today building

For many years we were happy to spend too freely, borrow too much and hand our money over to someone else to manage, hoping to ride a market that always went up. Well, times have changed and today building

Managing Money Together. A Workbook for Couples

Managing Money Together A Workbook for Couples Introduction Growing up, my parents argued about money. It wasn t a lot now that I look back, but I do remember thinking that I never wanted to do that. So,

Managing Money Together A Workbook for Couples Introduction Growing up, my parents argued about money. It wasn t a lot now that I look back, but I do remember thinking that I never wanted to do that. So,

Financial Decisions. What kinds of decisions can you make involving income, spending, saving, giving, and credit?

? Name Personal Financial 20.6 Literacy 3.9.F lso 3.4. Financial ecisions Essential Question What kinds of decisions can you make involving income, spending, saving, giving, and credit? MTHEMTIL PROESSES

? Name Personal Financial 20.6 Literacy 3.9.F lso 3.4. Financial ecisions Essential Question What kinds of decisions can you make involving income, spending, saving, giving, and credit? MTHEMTIL PROESSES

Student Guide: RWC Simulation Lab. Free Market Educational Services: RWC Curriculum

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Unit 1. Goals and Budgets. Literacy Level. Objectives:

Goals and Budgets Unit 1 Objectives: Identify goals, including personal, family, educational, and material. Identify income and expenses and create a budget. Identify ways to make adjustments to income

Goals and Budgets Unit 1 Objectives: Identify goals, including personal, family, educational, and material. Identify income and expenses and create a budget. Identify ways to make adjustments to income

Financial Needs Analysis Questionnaire (the involvement of ALL decision makers are required for an accurate assessment) Date: Time:

Date: Time:") Primary: D.O.B. Spouse / Partner: D.O.B. Address Primary s Cell phone: Home Phone: Spouse / Partner Cell phone: Primary s e-mail Spouse / Partner s e-mail Height Weight Any form of tobacco use? Height

Primary: D.O.B. Spouse / Partner: D.O.B. Address Primary s Cell phone: Home Phone: Spouse / Partner Cell phone: Primary s e-mail Spouse / Partner s e-mail Height Weight Any form of tobacco use? Height

Ric was named Best Talk Show Host in 1993 (AIR Awards) and continues to host weekly radio and television shows in Washington, D.C.

and continues to host weekly radio and television shows in Washington, D.C.") Wi$e Up Teleconference Call Budget to Save August 31, 2006 Speaker 2 Ric Edelman Jane Walstedt: Now, I'm going to turn the program over to Gail Patterson, who is part of the Women s Bureau team that plans

Wi$e Up Teleconference Call Budget to Save August 31, 2006 Speaker 2 Ric Edelman Jane Walstedt: Now, I'm going to turn the program over to Gail Patterson, who is part of the Women s Bureau team that plans

Creating My Lifestyle Budget

Page1 Slide 1 Creating My Lifestyle Budget Career Portals : Page2 Slide 2 Copyright Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas

Page1 Slide 1 Creating My Lifestyle Budget Career Portals : Page2 Slide 2 Copyright Copyright Texas Education Agency, 2014. These Materials are copyrighted and trademarked as the property of the Texas

MEET PRIYAH MEET JOSH MEET VANESSA MEET MARCO

GETTING READY FOR BIND Meet Priyah, Josh, Vanessa, and Marco. They are Medtronic employees who plan to enroll in a medical plan in November. Get to know their personal situations and what they consider

GETTING READY FOR BIND Meet Priyah, Josh, Vanessa, and Marco. They are Medtronic employees who plan to enroll in a medical plan in November. Get to know their personal situations and what they consider

Fast Track Couples Active, young, upper middle-class suburban couples and families living upwardly-mobile lifestyles. Who We Are 97.