Foreclosure Guidebook

|

|

|

- Calvin Lyons

- 5 years ago

- Views:

Transcription

1 Foreclosure Guidebook A helpful guide for individuals who may be facing foreclosure and reside in the Hudson Valley area of New York State. If you are struggling to make your mortgage payments or are already beind, and the word foreclosure has come up, you may be a looking for ways to better understand what foreclosure means and what your options are. 158 Orange Avenue, Walden, NY

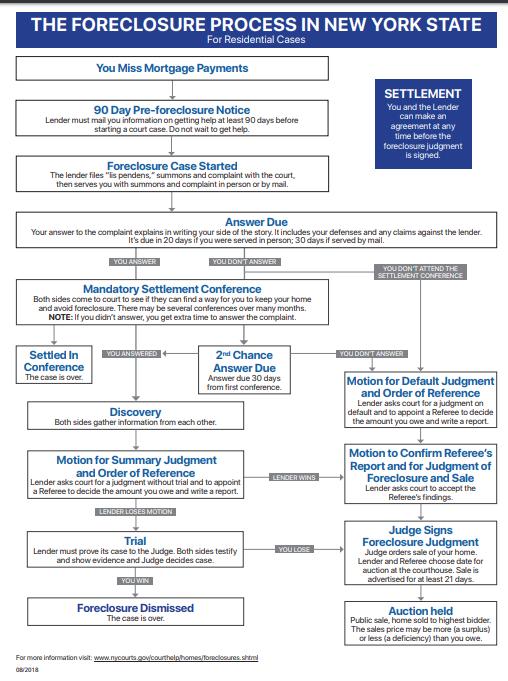

2 Introduction Foreclosures are not in the news much anymore, but ten years on from the financial crisis and housing market crash, many Hudson Valley homeowners are still facing the loss of their homes through foreclosure. According to RealtyTrac.com, the June 2018 rates of active foreclosure rates for local counties are as follows: 1 in 1,825 homes in Sullivan County are in foreclosure, 1 in 1,332 homes in Dutchess County are in foreclosure, 1 in 1,247 homes in Ulster County are in foreclosure, and 1 in 706 homes in Orange County are in foreclosure. It s nice for a borrower to know they are not statistically alone, but what a distressed borrower really wants to know is What can I do? Foreclosures can be complicated, frustrating, and stressful. An attorney can help a borrower evaluate their options, and provide guidance and advice throughout the process. Mortgage and Foreclosure Overview Here, we discuss some fundamental mortgage and foreclosure terms, and procedures a borrower should understand: The Note and Mortgage A promissory note is a document that evidences a loan from a lender to a borrower. The promissory note is a contract that obligates a borrower to repay money to a lender, and sets forth the terms, including the principal (amount borrowed), interest rate, repayment terms, and so forth. A mortgage creates a lien against property it is security for the loan obligation. The borrower is the mortgagor. The lender is the mortgagee. If and when the debt is paid the mortgage lien is terminated by the filing of a satisfaction of mortgage. If the loan is not repaid in accordance with the terms of the promissory note, the lender may enforce the mortgage by commencing a foreclosure action. Servicer and Assignments Lenders often use loan servicing companies to manage their loans. The servicer can prepare statements, collect payments, and commence and prosecute foreclosures. Lenders also often sell and assign loans to other lenders. Loan servicers and assignments are common and legal when the lender follows proper legal procedure. Borrowers may still find the transitions between lenders and servicers confusing and frustrating. If there is any question as to where payment should be remitted, a borrower should seek clarification from the lender directly to avoid a missed or delayed payment. While we 2

3 refer to a lender/mortgagee in this Guidebook, typically a servicer can do on lender s behalf whatever that lender is obligated to do. Foreclosure Procedural Overview Foreclosure is the legal process for lender/mortgagee to recover the home or property for sale at auction to satisfy the mortgage loan when the borrower has defaulted in payment. Default is a borrower s failure to abide by any of their obligations as set forth in the mortgage loan documents, but in the context of foreclosure, the default is a failure to pay sums due to their lender. This process for a lender/mortgagee to enforce its security interest in real property (foreclosure) is governed generally by New York State law (Real Property Actions and Proceedings Law and Civil Practice Law and Rules). There are many procedural steps within the foreclosure action that a lender needs to take. The lender cannot just take a borrower s house. The lender must follow strict procedures and take many steps to ultimately obtain a judgment of foreclosure and sale in order to hold a foreclosure auction of the borrower s house. In cases where a lender is aggressively moving the foreclosure forward, it can still take approximately a year. Many cases take much longer, sometimes years, even where the borrower is not defending against the foreclosure. Required Notices The lender/mortgagee is required to provide certain notices to the borrower prior to commencing a foreclosure action. The lender must provide any notices that are required by the loan documents, the promissory note and the mortgage. The lender/mortgagee is also required by statute (Real Property to provide a ninety (90) day notice to the borrower that the borrower is at risk of losing their home, providing a list of government approved housing counseling agencies, and advising the borrower of some of their rights and options. Summons and Complaint A lender starts a foreclosure action by serving and filing the Summons and Complaint. The Complaint can be served personally, by being handed to the borrower, or it can be handed to a person of suitable age and discretion that lives with the borrower or it can be left at the borrower s residence and mailed to the borrower. The complaint will set forth the lender s allegation concerning the note, mortgage, and default. 3

4 Answer The Answer is a response to the Complaint that includes any applicable defenses. The Answer is served upon (sent to) the lender s attorneys and then filed with the Court. The homeowner/borrower must Answer the Complaint in order to participate in the foreclosure action and make issue of any procedural missteps or lender s failure to negotiate in good faith (discussed below). Potential Defenses There are many potential defenses for borrowers, including procedural deficiencies the lender failed to serve a notice of default or the 90 day notice. The lender may have improperly served the borrower, or not served the borrower at all. The lender may have named the wrong parties. Substantive defenses include instances where the foreclosing lender is not the holder of the note and/or mortgage, perhaps due to issues with mortgage assignments. Of course, the defenses will depend on the facts of each case. Mandatory Foreclosure Settlement Conferences In New York State settlement conferences before the Court are mandatory in residential foreclosure cases. While the foreclosure case is in settlement, the lender cannot procedurally move the foreclosure case forward. There may be one conference, or there may be many conferences depending on what resolution or issues the parties are addressing. The foreclosure settlement conference provides an opportunity for the parties to resolve the matter, usually with a workout option, such as a mortgage modification, short sale, sale, or deed in lieu of foreclosure, which are discussed in further detail below. Further, the lender has a statutory duty to negotiate in good faith to resolve the matter. (So does the borrower, but they rarely need reminding by the Courts and legislature?) Where a lender causes undue delays, fails to obey court directives and rules, is unprepared for conferences, or engages in other conduct deemed to be a failure to negotiate in good faith, the Court can cancel interest and fees, award damages, and impose a civil penalty payable to the state. If a workout is agreed upon, the case can be settled and discontinued. If the case is not settled, it will be released from the settlement conference, and the lender will then be able to proceed with the legal process of foreclosure before the Court. 4

5 Motion for Summary Judgement and Appointment of a Referee Now, lender is off to the races, procedurally. The next step to move the action forward is lender s motion for summary judgment and appointment of a referee. A simplified explanation for the sake of brevity: The lender must prove its case by demonstrating with submission of the loan documents that it is the holder of the note and mortgage and that the borrower has defaulted in making payments. In order to defeat this motion, the borrower would have to raise a credible issue that the note and mortgage are not enforceable (i.e. lender does not hold the note or mortgage, or the statute of limitations has expired) or that borrower did not default (lender lost or misapplied payments, or induced the default). Procedurally, defects such as improper service or failure to provide the required notices and any other defenses that were asserted in borrower s Answer should be put forth to oppose the lender s motion. If the lender is successful, the case moves forward and the court appoints a referee, an independent third party attorney to calculate how much the lender is entitled to from borrower under the loan documents. If the lender is not successful, it must prove its case at trial where both lender and borrower provide evidence (documents, testimony) regarding the foreclosure and defenses. Motion for Judgement of Foreclosure and Sale The next step after the motion for summary judgment is granted to the lender is the lender s motion to confirm the referee s report and for a judgment of foreclosure and sale. If granted, the Court issues an order allowing the lender to auction the borrower s home. Foreclosure Auction The foreclosure auction must be advertised for at least 21 days. At the foreclosure auction, the Court-appointed Referee conducts the auction. The mortgagee/lender makes the first bid and then others may bid. The highest bidder will become the owner of the property after paying the lender the winning bid amount. If there are no outside bidders, the lender will obtain title to the property. If property is auctioned for more than is required to pay off borrower s Judgment of Foreclosure, then the Referee sends the surplus monies to the County Commissioner of Finance and a surplus money proceeding will be held to determined who (other creditors or the mortgagee/borrowers) is entitled to the surplus monies. 5

6 Summary An attorney can help a borrower through the procedural aspects of foreclosure. This simplified overview is meant to show borrowers the many procedural steps that a lender must take in order to get to the foreclosure auction. It can take months or sometimes years, and all the while, the borrower owns the home and is entitled to possession. Borrowers Options When Facing Impending Foreclosure There are two sides to foreclosure defense the procedural track before the Court discussed above, while at the same time dealing with the lender on workout options. Prior to or during and within the foreclosure action, a borrower can work out a resolution with the lender. First and foremost, a borrower should not panic and move out with no plan. A borrower owns their home and is entitled to live there until the home is deeded to the successful bidder at the foreclosure auction. This can give a borrower breathing room to regain their financial footing. A prudent homeowner in this situation will set aside some money each month, ideally equivalent to a housing payment, so that they will be able to afford their next housing situation when the time comes. In order to evaluate their options a borrower should first decide whether they want to keep their house. This is a decision a borrower needs to make based on many factors, such as the value of the home as compared to the loan, whether the monthly payments as modified will be affordable and/or lower than the housing payment on an alternate situation, as well as personal considerations - maybe borrower wants their kids to stay in this school district, maybe borrower has a job offer out of the area, maybe the house needs repairs in which borrower does not want to invest. Trying to Keep the Home. Retention Options: Reinstatement If a borrower wants to keep a home, they can seek to reinstate the loan with a lump sum payment of arrears, or through a payment plan where the arrears are paid over a short period of time (several months). This is a good option if the hardship causing the default has passed and borrower can afford such payments. 6

7 Modification Another retention option is a loan modification where the lender agrees to change the terms of the loan in order to lower the monthly payments. Lenders modify loans by reducing the interest rate and/or extending the life of the loan, rather than reducing the principal balance. The modified loan will typically be more expensive over the life of the loan, but if the monthly payments are affordable, this is a viable option for borrowers who want to stay put. A borrower will need to apply to their lender for a modification in a process that is similar to the original loan application process. A borrower will need to provide proof of income (i.e. tax returns, pay stubs, bank statements, statement of benefits etc.) to demonstrate the need for a modification and an ability to afford the modified payments. However, lenders are not required to modify loans and Courts cannot order lenders to modify loans. Also note that a borrower is not required to default in order to qualify for a loan modification. Refinancing Refinancing may be an option for borrowers who anticipate trouble affording the mortgage, but who still have strong enough credit to qualify for a new loan on better terms than their existing mortgage loan. Once borrowers have establishing a negative payment history, refinance will not be an option. Leaving the Home. Non-Retention Options: Short Sale In a short sale, borrower finds a buyer and seeks approval from the bank to accept a payoff on the loan that is less than what is owed. Any other liens on the property need to be satisfied as well. The borrower will have to submit an application to the lender for approval, much like a modification application. The application and approval process can be time consuming. It is important to address in the short sale contract that the sale is subject to lender s approval. Where the mortgaged property is worth more than is owed, this is an ordinary sale. Where borrowers can sell the house and satisfy all the liens (other mortgages and or judgments) and closing costs (transfer taxes, broker commissions, attorneys fees, etc.) without asking the lender to accept less than is owed on the mortgage loan, borrower can sell the house without lender s approval. 7

8 Deed in Lieu of Foreclosure In a deed-in-lieu, borrower deeds the house to the bank in satisfaction of the loan debt. Any other liens on the property need to be cleared up for a lender to accept a deedin-lieu. The borrower will have to submit an application to the lender for approval, much like a modification application. The application and approval process can be surprisingly time consuming considering that borrower is seeking to transfer the property to the lender without going through the time and expense of a foreclosure action. Walking Away Does Not Work When faced with foreclosure, many an overwhelmed borrower has devised the following plan : Let s just move out, let the bank have the house, and get this over with. Moving out of the house does not do anything to move the foreclosure process along or transfer ownership of the house to the lender, and it can put financially strained borrowers in a worse position. First, as discussed above, a mortgagee/lender cannot just take the house. Moving out of the house likely means a borrower taking on monthly rental payments. Remaining in the mortgaged home can save the borrower money because in New York, a borrower owns their home until the end of the foreclosure. As record owner, a borrower is entitled to use and possession of the home, and can remain in the home, even if not able to make the mortgage payments, until the house is deeded to the successful bidder at the foreclosure auction, which may or may not be the lender. This can give a borrower breathing room to regain their financial footing. Ignoring a foreclosure action does not expedite it and it can also result in a deficiency judgment against the borrower. A deficiency judgment is a money judgment against the borrower for the difference between the amount owed to the lender and the higher of the market value or the sale price of the foreclosed property. Although it is unusual for a lender to enforce a deficiency judgment, a loan application is a road map to a borrower s assets and income streams. What borrower wants to risk a wage garnishment and restrained bank accounts after losing their house? If a borrower really wants to be done with the foreclosure, they should try to work out a deed in lieu of foreclosure with the lender, or consent to certain aspects of a foreclosure action which can help expedite the matter, in exchange for a waiver of the deficiency judgment. 8

9 Not Over Borrowing: A Strategy One way to avoid a possible foreclosure is to not over borrow when initially taking out the mortgage loan. Borrowers should be able to afford their mortgage payments, as well as not only necessities, but other things that are important to them. Here is a sample budget worksheet to help borrowers evaluate how much they can and want to spend on a house. Monthly income Total take-home pay (earnings, wages, tips) Child Support Spousal support Investment income Government benefits Other sources Monthly bills and expenses Spousal support Child support Housing payment (rent, mortgage, property tax) Car payments Student loan payments Credit cards Heath insurance premiums Medical bills Cell/internet Electricity Gas (your heating/cooling bill) Telephone service Cable/satellite service Water and sewer service Renter's insurance (divide the yearly premium by 12) Groceries and household supplies Clothing Health club dues TOTAL: $ $ $ 9

10 Other fees or dues Fuel and repairs for your car Commuting train, bus Books, movies, video rentals, dining out, etc. Incidental purchases Vacation Gifts Savings Enter your total monthly income from the calculation above Enter your total monthly expenses calculated above Subtract the second figure from the first TOTAL: TOTAL: Conclusion If facing default or foreclosure, a borrower should remember that their lender is not on their side, but that time most likely is. Foreclosure is a relatively slow process, which may allow borrower time to work something out with their lender. An attorney can help a borrower understand their options and protect their rights and interests. An attorney can assist a borrower in evaluating their retention options (modification, reinstatement) and non-retention options (short sale, deed in lieu of foreclosure). An attorney can also facilitate the workout process, which can be overwhelming and frustrating for borrowers, and ensure that the lender follows the proper procedure in the foreclosure action. Foreclosure Resources 10

11 Following are New York State and local housing counseling agencies which provide free or very low-cost counseling: HOPP Homeowners Protection Program #855.Home.456 or at HUD United States Department of Housing and Urban Development at Orange County Rural Development Advisory Corporation in Walden # Hudson River Housing in Poughkeepsie # Putnam County Housing Corporation in Carmel # RUPCO in Kingston # Rural Sullivan Housing Corporation in Monticello # Housing Action Council in Tarrytown # Rockland Housing Action Coalition in New City # Community Housing Innovations, Inc., in White Plains # Housing Action Council in Tarrytown # Human Development Services of Westchester, Inc., in Port Chester # New York State Department of Financial Services Resource Center at New York State Department of Financial Services Foreclosure Relief Unit at 11

12 12

13 This is not intended to be legal advice. You should contact an attorney for advice regarding your specific situation. This workbook is prepared by Jacobowitz and Gubits LLP, September

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

NEW YORK S RESIDENTIAL MORTGAGE FORECLOSURE PROCESS. Western New York Law Center, Inc. Tanisha T. Bramwell, Esq.

NEW YORK S RESIDENTIAL MORTGAGE FORECLOSURE PROCESS Western New York Law Center, Inc. Tanisha T. Bramwell, Esq. Mortgage Foreclosure In a mortgage foreclosure, the holder of the mortgage files a lawsuit

NEW YORK S RESIDENTIAL MORTGAGE FORECLOSURE PROCESS Western New York Law Center, Inc. Tanisha T. Bramwell, Esq. Mortgage Foreclosure In a mortgage foreclosure, the holder of the mortgage files a lawsuit

EARLY DELINQUENCY INTERVENTION WORKBOOK

EARLY DELINQUENCY INTERVENTION WORKBOOK If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

EARLY DELINQUENCY INTERVENTION WORKBOOK If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

Early Delinquency Intervention Workbook

Early Delinquency Intervention Workbook If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

Early Delinquency Intervention Workbook If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009

By E mail March 2, 2010 RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009 Dear SONYMA Servicer: On December 15,

By E mail March 2, 2010 RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009 Dear SONYMA Servicer: On December 15,

An Attorney s Options for Handling Clients in Trouble with Real Estate. Aka: Forbearance to Bankruptcy and Everything in Between

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

The Perfect Storm. Subprime crisis. How the foreclosure process works... pg. 2. FORECLOSURE SCAMS How to avoid predators... pg. 3

Subprime crisis The Perfect Storm How the foreclosure process works... pg. FORECLOSURE SCAMS How to avoid predators... pg. WHIRLWIND FORECLOSURE SALE 5 steps of buying a foreclosed property... pg. SEEKING

Subprime crisis The Perfect Storm How the foreclosure process works... pg. FORECLOSURE SCAMS How to avoid predators... pg. WHIRLWIND FORECLOSURE SALE 5 steps of buying a foreclosed property... pg. SEEKING

Early Delinquency Intervention SAVING YOUR HOME FROM FORECLOSURE

Early Delinquency Intervention SAVING YOUR HOME FROM FORECLOSURE BALANCE offers a variety of free and low-cost services to help you get out of debt, design a money management plan, and achieve your financial

Early Delinquency Intervention SAVING YOUR HOME FROM FORECLOSURE BALANCE offers a variety of free and low-cost services to help you get out of debt, design a money management plan, and achieve your financial

Instructions for Completing the Short Sale Package. Send Ocwen the completed package and supporting documentation

Instructions for Completing the Short Sale Package Step 1 Complete all the enclosed attachments Exhibit G Borrowers Response package Step 2 Send Ocwen the completed package and supporting documentation

Instructions for Completing the Short Sale Package Step 1 Complete all the enclosed attachments Exhibit G Borrowers Response package Step 2 Send Ocwen the completed package and supporting documentation

Foreclosure Process in Minnesota

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

A Lender s Guide to Massachusetts Foreclosures

A Lender s Guide to Massachusetts Foreclosures By Francesco A. De Vito and Jonathan C. Hayden Table of Contents Introduction 3 What to Do After Default 4 Foreclosing on Residential Property 6 Prior to

A Lender s Guide to Massachusetts Foreclosures By Francesco A. De Vito and Jonathan C. Hayden Table of Contents Introduction 3 What to Do After Default 4 Foreclosing on Residential Property 6 Prior to

Solving Money Problems

Solving Money Problems 14 th Edition Robin Leonard, J.D. Attorney Margaret Reiter Chapter 1 How Much Do You Owe?... 1 Learning Objectives... 1 Introduction... 1 How Much Do You Earn?... 2 How Much Do You

Solving Money Problems 14 th Edition Robin Leonard, J.D. Attorney Margaret Reiter Chapter 1 How Much Do You Owe?... 1 Learning Objectives... 1 Introduction... 1 How Much Do You Earn?... 2 How Much Do You

CHAPTER 244 FORECLOSURE AND REDEMPTION OF MORTGAGES*

CHAPTER 244 FORECLOSURE AND REDEMPTION OF MORTGAGES* *selected sections relating to foreclosures by sale Section 1 Foreclosure by entry or action; continued possession Section 1. A mortgagee may, after

CHAPTER 244 FORECLOSURE AND REDEMPTION OF MORTGAGES* *selected sections relating to foreclosures by sale Section 1 Foreclosure by entry or action; continued possession Section 1. A mortgagee may, after

TITLE CARD: WHAT HAPPENS ONCE A FORECLOSURE LAWSUIT IS FILED?

TITLE CARD: WHAT HAPPENS ONCE A FORECLOSURE LAWSUIT IS FILED? TITLE CARD: INTRODUCTION INT. COURTHOUSE DAY The PRESENTER faces the camera. PRESENTER Hello. This video will teach you about what happens

TITLE CARD: WHAT HAPPENS ONCE A FORECLOSURE LAWSUIT IS FILED? TITLE CARD: INTRODUCTION INT. COURTHOUSE DAY The PRESENTER faces the camera. PRESENTER Hello. This video will teach you about what happens

«Current_Date_Plus_1» «Mailing_Address_1» «Mailing_Address_2» «Mailing_Address_3» «Mailing_Address_4» «Mailing_Address_5» «Mailing_Address_6»

«Mailing_Address_1» «Mailing_Address_2» «Mailing_Address_3» «Mailing_Address_4» «Mailing_Address_5» «Mailing_Address_6» «Current_Date_Plus_1» RE: People s United Bank, N.A. Loan «Account_Number_2» Dear

«Mailing_Address_1» «Mailing_Address_2» «Mailing_Address_3» «Mailing_Address_4» «Mailing_Address_5» «Mailing_Address_6» «Current_Date_Plus_1» RE: People s United Bank, N.A. Loan «Account_Number_2» Dear

Once we have received and evaluated your information, we will contact you regarding your options and next steps.

We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect your ability to make timely mortgage payments, whether your challenges are temporary or long term.

We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect your ability to make timely mortgage payments, whether your challenges are temporary or long term.

Early Delinquency Intervention: Saving Your Home From Foreclosure

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

PURCHASING, LEASING OR SELLING A HOME HOMEBUYER S FINANCIAL WORKSHEET

- DISCLAIMER - The following form is provided by FindLaw, a Thomson Business, for informational purposes only and is intended to be used as a guide prior to consultation with an attorney familiar with

- DISCLAIMER - The following form is provided by FindLaw, a Thomson Business, for informational purposes only and is intended to be used as a guide prior to consultation with an attorney familiar with

LEARN ABOUT YOUR RIGHTS AND OPTIONS IN A FORECLOSURE

FORECLOSURE GUIDE LEARN ABOUT YOUR RIGHTS AND OPTIONS IN A FORECLOSURE The Nineteenth Judicial Circuit Center for Self-Representation 18 North County Street Waukegan, Illinois 60085 With Thanks to. Legal

FORECLOSURE GUIDE LEARN ABOUT YOUR RIGHTS AND OPTIONS IN A FORECLOSURE The Nineteenth Judicial Circuit Center for Self-Representation 18 North County Street Waukegan, Illinois 60085 With Thanks to. Legal

2016 Foreclosure Law Amendments and Vacant and Abandoned Property Legislation. Two Major Prongs to Legislation

2016 Foreclosure Law Amendments and Vacant and Abandoned Property Legislation November 2016 Jacob Inwald Legal Services NYC Two Major Prongs to Legislation Addressing Zombie Properties: Vacant and Abandoned

2016 Foreclosure Law Amendments and Vacant and Abandoned Property Legislation November 2016 Jacob Inwald Legal Services NYC Two Major Prongs to Legislation Addressing Zombie Properties: Vacant and Abandoned

OHIO FORECLOSURE PROCESS AND TIMELINE

OHIO FORECLOSURE PROCESS AND TIMELINE Ohio utilizes the process of judicial foreclosure in connection with the enforcement of both commercial and residential mortgages and liens on real property. 1 In

OHIO FORECLOSURE PROCESS AND TIMELINE Ohio utilizes the process of judicial foreclosure in connection with the enforcement of both commercial and residential mortgages and liens on real property. 1 In

Welcome to your Homeowner s Guide to Success

Welcome to your Homeowner s Guide to Success Hardships create difficult situations and require difficult decisions. If you re experiencing a hardship, you might be wondering what bills to pay and if you

Welcome to your Homeowner s Guide to Success Hardships create difficult situations and require difficult decisions. If you re experiencing a hardship, you might be wondering what bills to pay and if you

FORECLOSURES. I m behind in my mortgage payments, what should I do?

FORECLOSURES This flyer was prepared by Legal Services of Greater Miami, Inc.(LSGMI) with support from the Institute for Foreclosure Legal Assistance. LSGMI represents homeowners in foreclosure and homeowners

FORECLOSURES This flyer was prepared by Legal Services of Greater Miami, Inc.(LSGMI) with support from the Institute for Foreclosure Legal Assistance. LSGMI represents homeowners in foreclosure and homeowners

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU?

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

Early Delinquency Intervention

Early Delinquency Intervention Saving Your Home From Foreclosure There are many reasons homeowners face difficulty in making mortgage payments: unexpected expenses, loss of overtime, unemployment, overspending,

Early Delinquency Intervention Saving Your Home From Foreclosure There are many reasons homeowners face difficulty in making mortgage payments: unexpected expenses, loss of overtime, unemployment, overspending,

Information on Avoiding Foreclosure

Information on Avoiding Foreclosure Learn more About Options to Avoid Foreclosure The variety of options summarized below may help you keep your home. For example, you may be eligible to modify your mortgage,

Information on Avoiding Foreclosure Learn more About Options to Avoid Foreclosure The variety of options summarized below may help you keep your home. For example, you may be eligible to modify your mortgage,

IN RE: MEDIATION MANDATORY MEDIATION CIRCUIT COURT BREVARD COUNTY OWNER OCCUPIED RESIDENTIAL MORTGAGE FORECLOSURE

IN THE CIRCUIT COURT OF THE EIGHTEENTH JUDICIAL CIRCUIT IN AND FOR BREVARD COUNTY, FLORIDA ADMINISTRATIVE ORDER NO: 09-14-B IN RE: MEDIATION MANDATORY MEDIATION CIRCUIT COURT BREVARD COUNTY OWNER OCCUPIED

IN THE CIRCUIT COURT OF THE EIGHTEENTH JUDICIAL CIRCUIT IN AND FOR BREVARD COUNTY, FLORIDA ADMINISTRATIVE ORDER NO: 09-14-B IN RE: MEDIATION MANDATORY MEDIATION CIRCUIT COURT BREVARD COUNTY OWNER OCCUPIED

FORECLOSURE PREVENTION

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

9 Ways To Stop Foreclosure. Don t Let Time RUN OUT!

9 Ways To Stop Foreclosure Don t Let Time RUN OUT! Q.B. Homes - Great Success Realty. Saar (Sam) Elazar, Licensed Real Estate Salesperson CDPE Certified Distress Property Expert 140-21 Queens Blvd. (Ground

9 Ways To Stop Foreclosure Don t Let Time RUN OUT! Q.B. Homes - Great Success Realty. Saar (Sam) Elazar, Licensed Real Estate Salesperson CDPE Certified Distress Property Expert 140-21 Queens Blvd. (Ground

ASSEMBLY, No STATE OF NEW JERSEY. 217th LEGISLATURE INTRODUCED FEBRUARY 22, 2016

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Assemblyman PATRICK J. DIEGNAN, JR. District (Middlesex) Assemblyman JERRY GREEN District (Middlesex, Somerset and

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED FEBRUARY, 0 Sponsored by: Assemblyman PATRICK J. DIEGNAN, JR. District (Middlesex) Assemblyman JERRY GREEN District (Middlesex, Somerset and

Short Sales/Foreclosures/REOs

Short Sales/Foreclosures/REOs In today s economic times the occurrence of Short Sales, Foreclosures and REOs has become common. Below is a description of these property statuses. Short Sale: A short sale

Short Sales/Foreclosures/REOs In today s economic times the occurrence of Short Sales, Foreclosures and REOs has become common. Below is a description of these property statuses. Short Sale: A short sale

7 Things to Know about Mortgages, Foreclosures, and Short Sales

7 Things to Know about Mortgages, Foreclosures, and Short Sales TABLE OF CONTENTS 1. Being in Default is Not Necessarily Being in Foreclosure 2 2. Foreclosure 2 3. Short Sales 3 4. There is No Right to

7 Things to Know about Mortgages, Foreclosures, and Short Sales TABLE OF CONTENTS 1. Being in Default is Not Necessarily Being in Foreclosure 2 2. Foreclosure 2 3. Short Sales 3 4. There is No Right to

Available at:

Available at: http://www.dfs.ny.gov/legal/regulations/emergency/banking/ar419tx.htm Regulations Adopted on an Emergency Basis Part 419. Servicing Mortgage Loans: Business Conduct Rules (Statutory Authority:

Available at: http://www.dfs.ny.gov/legal/regulations/emergency/banking/ar419tx.htm Regulations Adopted on an Emergency Basis Part 419. Servicing Mortgage Loans: Business Conduct Rules (Statutory Authority:

Georgia 2012 Legislative Update. End of Session Update Issued April 13, 2012

Georgia 2012 Legislative Update End of Session Update Issued April 13, 2012 The second session of the 2011-2012 Georgia General Assembly ended Thursday, April 5, 2012. The bills that did not pass during

Georgia 2012 Legislative Update End of Session Update Issued April 13, 2012 The second session of the 2011-2012 Georgia General Assembly ended Thursday, April 5, 2012. The bills that did not pass during

Senate Bill No. 818 CHAPTER 404

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Foreclosure Diversion Program Information Session. Understanding and Preparing for Mediation

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

SB 558 Oregon s New Mandatory Resolution Conference Law Helping Homeowners Facing Foreclosure (2013)

") SB 558 Oregon s New Mandatory Resolution Conference Law Helping Homeowners Facing Foreclosure (2013) By Phillip C. Querin, QUERIN LAW, LLC Website: www.q-law.com Introduction. After a false start in 2012,

SB 558 Oregon s New Mandatory Resolution Conference Law Helping Homeowners Facing Foreclosure (2013) By Phillip C. Querin, QUERIN LAW, LLC Website: www.q-law.com Introduction. After a false start in 2012,

Certified Distressed Property Expert

Certified Distressed Property Expert If we all did the things we are capable of doing we would literally astound ourselves. -Thomas Edison National Delinquency Numbers Mortgage Bankers Association 4.38%

Certified Distressed Property Expert If we all did the things we are capable of doing we would literally astound ourselves. -Thomas Edison National Delinquency Numbers Mortgage Bankers Association 4.38%

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

HOMEOWNER WELCOME PACKAGE. Short Sale Frequently Asked Questions

HOMEOWNER WELCOME PACKAGE Welcome to LA City Short Sales! We understand that this can be a challenging and stressful time in your life and our goal is to make the short sale process as easy as possible

HOMEOWNER WELCOME PACKAGE Welcome to LA City Short Sales! We understand that this can be a challenging and stressful time in your life and our goal is to make the short sale process as easy as possible

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13. Name: Case Number:

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 YOUR TRUSTEE S NAME, ADDRESS, AND TELEPHONE NUMBER: ADAM M. GOODMAN STANDING CHAPTER 13 TRUSTEE 260 PEACHTREE STREET N.W. SUITE 200 ATLANTA, GEORGIA 30303 Telephone:

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 YOUR TRUSTEE S NAME, ADDRESS, AND TELEPHONE NUMBER: ADAM M. GOODMAN STANDING CHAPTER 13 TRUSTEE 260 PEACHTREE STREET N.W. SUITE 200 ATLANTA, GEORGIA 30303 Telephone:

ALTLOAN CREDIT GUIDELINES

ALTLOAN CREDIT GUIDELINES BRIDGE AND FIX & FLIP LOANS PRIMARY RESIDENCE & SECOND HOME TERM LOANS INVESTOR TERM LOANS BRIDGE AND FIX & FLIP Use the lower of two credit scores or middle of three for each

ALTLOAN CREDIT GUIDELINES BRIDGE AND FIX & FLIP LOANS PRIMARY RESIDENCE & SECOND HOME TERM LOANS INVESTOR TERM LOANS BRIDGE AND FIX & FLIP Use the lower of two credit scores or middle of three for each

AKE ONTROL OF OUR ORTGAGE HERE S OPE

AKE ONTROL OF OUR ORTGAGE HERE S OPE A FREE COMMUNITY WORKSHOP FOR HOMEOWNERS STRATEGIES FOR TAKING CONTROL OF YOUR MORTGAGE Hosted by: Presented by Curved poster, PAUL A. BLUCHER OF BLUCHER LAW advertisement,

AKE ONTROL OF OUR ORTGAGE HERE S OPE A FREE COMMUNITY WORKSHOP FOR HOMEOWNERS STRATEGIES FOR TAKING CONTROL OF YOUR MORTGAGE Hosted by: Presented by Curved poster, PAUL A. BLUCHER OF BLUCHER LAW advertisement,

LOAN SERVICING AND EQUITY INTEREST AGREEMENT

LOAN SERVICING AND EQUITY INTEREST AGREEMENT THIS LOAN SERVICING AND EQUITY INTEREST AGREEMENT ( Agreement ) is made as of, 20 by and among Cushman Rexrode Capital Corporation, a California corporation

LOAN SERVICING AND EQUITY INTEREST AGREEMENT THIS LOAN SERVICING AND EQUITY INTEREST AGREEMENT ( Agreement ) is made as of, 20 by and among Cushman Rexrode Capital Corporation, a California corporation

THIS FORM HAS IMPORTANT LEGAL CONSEQUENCES AND THE PARTIES SHOULD CONSULT LEGAL AND TAX OR OTHER COUNSEL BEFORE SIGNING. SHORT SALE ADDENDUM

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 The printed portions of this form, except differentiated additions,

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 The printed portions of this form, except differentiated additions,

FORECLOSURE ALTERNATIVES

FORECLOSURE ALTERNATIVES You may be facing foreclosure, so what are your options? Try to look at the situation more from a financial standpoint rather than an emotional standpoint. This way you can more

FORECLOSURE ALTERNATIVES You may be facing foreclosure, so what are your options? Try to look at the situation more from a financial standpoint rather than an emotional standpoint. This way you can more

OPTIONAL MORTGAGE COVENANTS STANDARD RESIDENTIAL MORTGAGE TERMS AND CONDITIONS TABLE OF CONTENTS

Form 3973 (11-2005) OPTIONAL MORTGAGE COVENANTS STANDARD RESIDENTIAL MORTGAGE TERMS AND CONDITIONS TABLE OF CONTENTS SECTION 1 TERMS YOU NEED TO KNOW...1 SECTION 2 HOW THE MORTGAGE WORKS...3 SECTION 3

Form 3973 (11-2005) OPTIONAL MORTGAGE COVENANTS STANDARD RESIDENTIAL MORTGAGE TERMS AND CONDITIONS TABLE OF CONTENTS SECTION 1 TERMS YOU NEED TO KNOW...1 SECTION 2 HOW THE MORTGAGE WORKS...3 SECTION 3

MANAGING YOUR DEBT. An Informational and Educational Guide for Residents of New York State

MANAGING YOUR DEBT An Informational and Educational Guide for Residents of New York State Designed and Provided by the Rural Law Center of New York, Inc. Rural Law Center of New York, Inc. WHAT TO DO WHEN

MANAGING YOUR DEBT An Informational and Educational Guide for Residents of New York State Designed and Provided by the Rural Law Center of New York, Inc. Rural Law Center of New York, Inc. WHAT TO DO WHEN

Chapter 14 Real Estate Financing: Principles

Chapter 14 Real Estate Financing: Principles OUTLINE: I. Mortgage Law A. A mortgage is a voluntary lien on real estate, given by the mortgagor to secure the payment of a debt or the performance of an obligation

Chapter 14 Real Estate Financing: Principles OUTLINE: I. Mortgage Law A. A mortgage is a voluntary lien on real estate, given by the mortgagor to secure the payment of a debt or the performance of an obligation

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS Compiled by: UNIVERSITY OF SAN FRANCISCO, SCHOOL OF LAW PREDATORY LENDING CLINIC Provided by: COMMUNITY LEGAL SERVICES IN EAST PALO

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS Compiled by: UNIVERSITY OF SAN FRANCISCO, SCHOOL OF LAW PREDATORY LENDING CLINIC Provided by: COMMUNITY LEGAL SERVICES IN EAST PALO

INTRODUCTION TO ILLINOIS MORTGAGE FORECLOSURE PROCESS

INTRODUCTION TO ILLINOIS MORTGAGE FORECLOSURE PROCESS JAMES BRADY, SUPERVISORY ATTORNEY THE FORECLOSURE PROCESS Illinois is a judicial foreclosure state (one of about 22 states) Process is governed by

INTRODUCTION TO ILLINOIS MORTGAGE FORECLOSURE PROCESS JAMES BRADY, SUPERVISORY ATTORNEY THE FORECLOSURE PROCESS Illinois is a judicial foreclosure state (one of about 22 states) Process is governed by

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Fall 2010

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Default and Post-Default Article 9 Remedies I. Default Under Article 9 A. Typical Payment Terms

Secured Transactions Professor Keith A. Rowley William S. Boyd School of Law University of Nevada Las Vegas Default and Post-Default Article 9 Remedies I. Default Under Article 9 A. Typical Payment Terms

florida ARECS Save Your Deal. Save Your Client. Realtor s Distressed Property Guide Revised January 2017

florida TM ARECS Save Your Deal. Save Your Client. Realtor s Distressed Property Guide Revised January 2017 YOUR JOB DESCRIPTION HAS CHANGED DRAMATICALLY... If your deal is in danger of getting pulled

florida TM ARECS Save Your Deal. Save Your Client. Realtor s Distressed Property Guide Revised January 2017 YOUR JOB DESCRIPTION HAS CHANGED DRAMATICALLY... If your deal is in danger of getting pulled

Frequently Asked Questions

Frequently Asked Questions 1. What is the difference between a professional collection service and a creditor collecting on its own behalf? Sometimes consumers confuse third-party collectors with the in-house

Frequently Asked Questions 1. What is the difference between a professional collection service and a creditor collecting on its own behalf? Sometimes consumers confuse third-party collectors with the in-house

session of the legislature, significant changes to New York s judicial residential

2016 Amendments to New York Foreclosure Settlement Conference and Predicate Notice Laws Jacob Inwald Director of Foreclosure Prevention Legal Services NYC As part of a package of legislation enacted in

2016 Amendments to New York Foreclosure Settlement Conference and Predicate Notice Laws Jacob Inwald Director of Foreclosure Prevention Legal Services NYC As part of a package of legislation enacted in

Homeowner Benefits and Responsibilities

Homeowner Benefits and Responsibilities Introduction Homeowner Benefits and Responsibilities Benefits of Homeownership Responsibilities of Homeownership Refinancing and Home Equity Preventing Foreclosure

Homeowner Benefits and Responsibilities Introduction Homeowner Benefits and Responsibilities Benefits of Homeownership Responsibilities of Homeownership Refinancing and Home Equity Preventing Foreclosure

Default Management Servicing Guide

Homeowner Assistance Program I Mortgage Insurance Default Management Servicing Guide January 10, 2014 7566293.0114 Genworth Mortgage Insurance Homeowner Assistance Program Default Management Servicing

Homeowner Assistance Program I Mortgage Insurance Default Management Servicing Guide January 10, 2014 7566293.0114 Genworth Mortgage Insurance Homeowner Assistance Program Default Management Servicing

Florida Foreclosure Law E-Book

Florida Foreclosure Law E-Book Simple Guide to Florida Foreclosure Law by: florida Law Advisers, P.A. 1 Table Of Contents INTRODUCTION.... 3 FIGHTING THE FORECLOSURE OF YOUR HOME.... 3 PREDATORY LENDING.....

Florida Foreclosure Law E-Book Simple Guide to Florida Foreclosure Law by: florida Law Advisers, P.A. 1 Table Of Contents INTRODUCTION.... 3 FIGHTING THE FORECLOSURE OF YOUR HOME.... 3 PREDATORY LENDING.....

Litigation Department: Phase I litigation Phase II Litigation:

The Law Office of: Harvey Rubinchik, PA. Pine Island Professional Center Suite 118 1860 N. Pine Island Road Plantation, Florida 33322 Telephone (954) 475-9995, Facsimile (954) 476-7047 Thank you for selecting

The Law Office of: Harvey Rubinchik, PA. Pine Island Professional Center Suite 118 1860 N. Pine Island Road Plantation, Florida 33322 Telephone (954) 475-9995, Facsimile (954) 476-7047 Thank you for selecting

Financial First Aid 595 Market Street, 16th Floor, San Francisco, CA

Financial First Aid Many circumstances in life can derail even the best money management plan. If you have found yourself in a situation where you can t keep up with your bills, you ll need to take an

Financial First Aid Many circumstances in life can derail even the best money management plan. If you have found yourself in a situation where you can t keep up with your bills, you ll need to take an

THIS FORM HAS IMPORTANT LEGAL CONSEQUENCES AND THE PARTIES SHOULD CONSULT LEGAL AND TAX OR OTHER COUNSEL BEFORE SIGNING. SHORT SALE ADDENDUM

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 The printed portions of this form, except differentiated additions,

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 The printed portions of this form, except differentiated additions,

LOAN SERVICING AND EQUITY INTEREST AGREEMENT

LOAN SERVICING AND EQUITY INTEREST AGREEMENT THIS LOAN SERVICING AND EQUITY INTEREST AGREEMENT ( Agreement ) is made as of, 20 by and among Blackburne & Sons Realty Capital Corporation, a California corporation

LOAN SERVICING AND EQUITY INTEREST AGREEMENT THIS LOAN SERVICING AND EQUITY INTEREST AGREEMENT ( Agreement ) is made as of, 20 by and among Blackburne & Sons Realty Capital Corporation, a California corporation

703: SERVICE MEMBERS CIVIL RELIEF ACT POLICY

703.1. PURPOSE/OVERVIEW 1.1. On loans to military personnel, San Francisco Federal Credit Union (SFFCU) will comply with the Service members Civil Relief Act (SCRA) of 2003 (50 U.S.C.501 et seq.) This

703.1. PURPOSE/OVERVIEW 1.1. On loans to military personnel, San Francisco Federal Credit Union (SFFCU) will comply with the Service members Civil Relief Act (SCRA) of 2003 (50 U.S.C.501 et seq.) This

Waushara County Circuit Court Rules

Waushara County Circuit Court Rules (Sixth Judicial District) Small Claims Rules Facsimile Transmission of Documents to the Court Civil Rule-Mortgage Foreclosure Small Claims Rules I. These rules are made

Waushara County Circuit Court Rules (Sixth Judicial District) Small Claims Rules Facsimile Transmission of Documents to the Court Civil Rule-Mortgage Foreclosure Small Claims Rules I. These rules are made

Marion Superior Court Local Rule on Foreclosure Cases

Marion Superior Court Local Rule on Foreclosure Cases Local Rule 49TR85 Rule 231 Effective March 2, 2009, the Circuit and Superior Courts of Marion County implemented a local rule requiring lenders and

Marion Superior Court Local Rule on Foreclosure Cases Local Rule 49TR85 Rule 231 Effective March 2, 2009, the Circuit and Superior Courts of Marion County implemented a local rule requiring lenders and

Real Estate Finance: 10/17/2017. Why use a mortgage?

Real Estate Finance: McGraw-Hill/Irwin Laws and Contracts Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Fixed rate (Monthly charge is 1/12 of stated annual rate) Adjustable rate

Real Estate Finance: McGraw-Hill/Irwin Laws and Contracts Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Fixed rate (Monthly charge is 1/12 of stated annual rate) Adjustable rate

Exhibit X SECURITY AGREEMENT - CO-OP. Street Address:

Exhibit X SONYMA Exhibit 8/4-99 SONYMA Loan Number Loan No: Apartment No: SECURITY AGREEMENT - CO-OP Street Address: This Security Agreement (the "Agreement") dated the day of, between residing at (collectively,

Exhibit X SONYMA Exhibit 8/4-99 SONYMA Loan Number Loan No: Apartment No: SECURITY AGREEMENT - CO-OP Street Address: This Security Agreement (the "Agreement") dated the day of, between residing at (collectively,

Law for Mortgage on Immovable Property in Banking Transactions

Law for Mortgage on Immovable Property in Banking Transactions Necessity of Creation of Law Article one: Chapter 1 General Principals This Law is created to regulate business and banking transactions that

Law for Mortgage on Immovable Property in Banking Transactions Necessity of Creation of Law Article one: Chapter 1 General Principals This Law is created to regulate business and banking transactions that

[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale

![[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale](/thumbs/90/103076486.jpg "[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale") [Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

[Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

Declaring Personal Bankruptcy

Declaring Personal Bankruptcy DECLARING PERSONAL BANKRUPTCY A declaration of personal bankruptcy doesn t carry the stigma it once did but it is, nonetheless, an admission that one is no longer able to

Declaring Personal Bankruptcy DECLARING PERSONAL BANKRUPTCY A declaration of personal bankruptcy doesn t carry the stigma it once did but it is, nonetheless, an admission that one is no longer able to

TITLE 230 DEPARTMENT OF BUSINESS REGULATION

230-RICR-40-10-4 TITLE 230 DEPARTMENT OF BUSINESS REGULATION CHAPTER 40 BANKING SUBCHAPTER 10 LENDING PART 4 Mortgage Foreclosure Disclosure 4.1 Authority This Part is promulgated pursuant to R.I. Gen.

230-RICR-40-10-4 TITLE 230 DEPARTMENT OF BUSINESS REGULATION CHAPTER 40 BANKING SUBCHAPTER 10 LENDING PART 4 Mortgage Foreclosure Disclosure 4.1 Authority This Part is promulgated pursuant to R.I. Gen.

How to Complete the New SBA 7(a) Litigation 7 Tab Package SOP (Effective Date: March 1, 2013)

Litigation 7 Tab Package SOP (Effective Date: March 1, 2013)") How to Complete the New SBA 7(a) Litigation 7 Tab Package SOP 50 57 (Effective Date: March 1, 2013) The United States Small Business Administration ( SBA ), in SOP 50 57 ( SOP ), recently promulgated Litigation

How to Complete the New SBA 7(a) Litigation 7 Tab Package SOP 50 57 (Effective Date: March 1, 2013) The United States Small Business Administration ( SBA ), in SOP 50 57 ( SOP ), recently promulgated Litigation

Foreclosure Solutions. Know The Facts Get The Help You Need!

Foreclosure Solutions Know The Facts Get The Help You Need! 1 Table of Contents Introduction Know Your Options Chapter 1 Walking Away Will Cost You More Chapter 2 Your 5 Stay In Home Options Chapter 3

Foreclosure Solutions Know The Facts Get The Help You Need! 1 Table of Contents Introduction Know Your Options Chapter 1 Walking Away Will Cost You More Chapter 2 Your 5 Stay In Home Options Chapter 3

LOAN SERVICING AND TENANCY IN COMMON AGREEMENT

LOAN SERVICING AND TENANCY IN COMMON AGREEMENT THIS LOAN SERVICING AND TENANCY IN COMMON AGREEMENT ( Agreement ) is made as of, 2008 by and among Blackburne & Brown Mortgage Company, Inc. ( Servicer ),

LOAN SERVICING AND TENANCY IN COMMON AGREEMENT THIS LOAN SERVICING AND TENANCY IN COMMON AGREEMENT ( Agreement ) is made as of, 2008 by and among Blackburne & Brown Mortgage Company, Inc. ( Servicer ),

CROP LOAN GUARANTEE PROGRAM

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

CROP LOAN GUARANTEE PROGRAM LENDER MANUAL 1 P age Contents ABOUT THIS MANUAL... 3 WHO TO CONTACT... 3 ELIGIBILITY... 4 A. ELIGIBLE LENDERS... 4 B. ELIGIBLE BORROWERS... 5 C. ELIGIBLE LOANS... 6 D. ELIGIBLE

Land Titles Act (Alberta) Set of Standard Form Mortgage Terms - Residential

Set of Standard Form Mortgage Terms - Residential") Variable Rate Land Titles Act (Alberta) Set of Standard Form Mortgage Terms - Residential TABLE OF CONTENTS SECTION 1 TERMS YOU NEED TO KNOW...1 SECTION 2 HOW THE MORTGAGE WORKS...3 SECTION 3 INTEREST...4

Variable Rate Land Titles Act (Alberta) Set of Standard Form Mortgage Terms - Residential TABLE OF CONTENTS SECTION 1 TERMS YOU NEED TO KNOW...1 SECTION 2 HOW THE MORTGAGE WORKS...3 SECTION 3 INTEREST...4

Valuable Secrets to Defending Debt Collection Lawsuits

Valuable Secrets to Defending Debt Collection Lawsuits Creditors will aggressively pursue you. The Terry Law Firm will aggressively defend you. IF YOU HAVE BEEN SUED BY A DEBT COLLECTOR, YOU CAN WIN! David

Valuable Secrets to Defending Debt Collection Lawsuits Creditors will aggressively pursue you. The Terry Law Firm will aggressively defend you. IF YOU HAVE BEEN SUED BY A DEBT COLLECTOR, YOU CAN WIN! David

First wave: Driven by loan terms & home values. Second wave: Driven by unemployment. Various local, state and federal responses

Sustainable Loan Modifications June 2009 J. Michael Collins Introduction Foreclosures at record levels First wave: Driven by loan terms & home values» Concentration in sand states and LMI communities (but

Sustainable Loan Modifications June 2009 J. Michael Collins Introduction Foreclosures at record levels First wave: Driven by loan terms & home values» Concentration in sand states and LMI communities (but

Foreclosure Counseling. A presentation prepared by Neighborhood Housing Services of South Florida

Foreclosure Counseling A presentation prepared by Neighborhood Housing Services of South Florida Are you at risk of foreclosure? Has your financial situation changed due to: Mortgage payment increase?

Foreclosure Counseling A presentation prepared by Neighborhood Housing Services of South Florida Are you at risk of foreclosure? Has your financial situation changed due to: Mortgage payment increase?

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES 1. What is a chapter 7 bankruptcy case and how does it work? A chapter 7 bankruptcy case is a proceeding under federal law

LIQUIDATION UNDER CHAPTER 7 QUESTIONS AND ANSWERS ABOUT CHAPTER 7 BANKRUPTCIES 1. What is a chapter 7 bankruptcy case and how does it work? A chapter 7 bankruptcy case is a proceeding under federal law

SENATE, No STATE OF NEW JERSEY. 218th LEGISLATURE INTRODUCED JANUARY 25, 2018

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED JANUARY, 0 Sponsored by: Senator RONALD L. RICE District (Essex) Senator TROY SINGLETON District (Burlington) SYNOPSIS Codifies the Judiciary's

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED JANUARY, 0 Sponsored by: Senator RONALD L. RICE District (Essex) Senator TROY SINGLETON District (Burlington) SYNOPSIS Codifies the Judiciary's

Whenever Possible, It Is Always Best to Avoid Foreclosure in Favor of Other Alternatives; One Such Alternative Is Called a Short Sale

SHORTSALE VS. FORECLOSURE IN NASSAU COUNTY Whenever Possible, It Is Always Best to Avoid Foreclosure in Favor of Other Alternatives; One Such Alternative Is Called a Short Sale Ronald D. Weiss If you are

SHORTSALE VS. FORECLOSURE IN NASSAU COUNTY Whenever Possible, It Is Always Best to Avoid Foreclosure in Favor of Other Alternatives; One Such Alternative Is Called a Short Sale Ronald D. Weiss If you are

Reverse Mortgage Foreclosure Updates & Methods of Resolution September 19, 2017

Reverse Mortgage Foreclosure Updates & Methods of Resolution September 19, 2017 Presenter: Jennifer N. Levy, Esq. BIOGRAPHY Jennifer is a Senior Staff Attorney at JASA Legal Services for the Elderly in

Reverse Mortgage Foreclosure Updates & Methods of Resolution September 19, 2017 Presenter: Jennifer N. Levy, Esq. BIOGRAPHY Jennifer is a Senior Staff Attorney at JASA Legal Services for the Elderly in

Bankruptcy FAQs - Luongo Bellwoar LLP

Bankruptcy FAQs - Luongo Bellwoar LLP A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot

Bankruptcy FAQs - Luongo Bellwoar LLP A decision to file for bankruptcy should be made only after determining that bankruptcy is the best way to deal with your financial problems. This brochure cannot

Land Registration Reform Act

Page 1 Land Registration Reform Act Set of Standard Charge Terms Variable Rate Page 2 TABLE OF CONTENTS Land Registration Reform Act...1 TABLE OF CONTENTS...2 SECTION 1 TERMS YOU NEED TO KNOW...4 SECTION

Page 1 Land Registration Reform Act Set of Standard Charge Terms Variable Rate Page 2 TABLE OF CONTENTS Land Registration Reform Act...1 TABLE OF CONTENTS...2 SECTION 1 TERMS YOU NEED TO KNOW...4 SECTION

Effective Foreclosure Timeline Management Reference Guide

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing

October 27, 2010 Media Contact: Brad Dwin (202) 589-1938 brad@hopenow.com Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing (WASHINGTON, DC) Faith Schwartz, senior adviser, and former

October 27, 2010 Media Contact: Brad Dwin (202) 589-1938 brad@hopenow.com Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing (WASHINGTON, DC) Faith Schwartz, senior adviser, and former

Lesson 12: Real Estate Financing 311

Real Estate Principles of Georgia 1 of 97 Lesson 12: Real Estate Financing 311 Economics of Real Estate Finance For a lender, a loan is an investment. Interest paid on loan is lender s return. Riskier

Real Estate Principles of Georgia 1 of 97 Lesson 12: Real Estate Financing 311 Economics of Real Estate Finance For a lender, a loan is an investment. Interest paid on loan is lender s return. Riskier

Communicating with Borrowers: Collections and Loss Mitigation Reference Guide

Communicating with Borrowers: Collections and Loss Mitigation Reference Guide It is important to establish trust and confidence in the early stages of communications with borrowers. The more knowledge

Communicating with Borrowers: Collections and Loss Mitigation Reference Guide It is important to establish trust and confidence in the early stages of communications with borrowers. The more knowledge

Preventing or Opposing a Sale in Execution A LEGAL GUIDE MAY 2016

Preventing or Opposing a Sale in Execution A LEGAL GUIDE MAY 2016 ii Preventing or Opposing a Sale in Execution A LEGAL GUIDE Acknowledgements MAY 2016 This guide was produced by the Socio-Economic Rights

Preventing or Opposing a Sale in Execution A LEGAL GUIDE MAY 2016 ii Preventing or Opposing a Sale in Execution A LEGAL GUIDE Acknowledgements MAY 2016 This guide was produced by the Socio-Economic Rights

STANDARD MORTGAGE TERMS. Filed By: PARADIGM QUEST INC. Filing Date: November 30, Filing Number: MT070114

STANDARD MORTGAGE TERMS Filed By: PARADIGM QUEST INC. Filing Date: November 30, 2007 Filing Number: MT070114 These STANDARD MORTGAGE TERMS shall be deemed to be included in every Mortgage which incorporates

STANDARD MORTGAGE TERMS Filed By: PARADIGM QUEST INC. Filing Date: November 30, 2007 Filing Number: MT070114 These STANDARD MORTGAGE TERMS shall be deemed to be included in every Mortgage which incorporates

OWNER-OCCUPIED HOUSING REHABILITATION

Paradise Redevelopment Agency OWNER-OCCUPIED HOUSING REHABILITATION Home Repair/Rehabilitation Program Guidelines January 2008 HOME REPAIR/REHABILITATION PROGRAM GUIDELINES Table of Contents 1.0. GENERAL

Paradise Redevelopment Agency OWNER-OCCUPIED HOUSING REHABILITATION Home Repair/Rehabilitation Program Guidelines January 2008 HOME REPAIR/REHABILITATION PROGRAM GUIDELINES Table of Contents 1.0. GENERAL

DEED OF TRUST AND ASSIGNMENT OF RENTS SAN FRANCISCO POLICE IN THE COMMUNITY LOAN PROGRAM (PIC)

") Free Recording Requested Pursuant to Government Code Section 27383 When recorded, mail to: Mayor's Office of Housing AND Community Development of the City and County of San Francisco One South Van Ness

Free Recording Requested Pursuant to Government Code Section 27383 When recorded, mail to: Mayor's Office of Housing AND Community Development of the City and County of San Francisco One South Van Ness

Foreclosure Hodge Podge. Deanne R. Stodden Managing Partner Castle Meinhold & Stawiarski, LLC

Foreclosure Hodge Podge Deanne R. Stodden Managing Partner Castle Meinhold & Stawiarski, LLC Agenda Title insurance options HAMP and HAFA update The eviction process and PTAFA Amos v. Aspen Alps 123, LLC

Foreclosure Hodge Podge Deanne R. Stodden Managing Partner Castle Meinhold & Stawiarski, LLC Agenda Title insurance options HAMP and HAFA update The eviction process and PTAFA Amos v. Aspen Alps 123, LLC

District of Columbia Amends Rules Regarding the Foreclosure Mediation Program

April 3, 2014 District of Columbia Amends Rules Regarding the Foreclosure Mediation Program By Lee Greenberg The District of Columbia Department of Insurance, Securities and Banking recently amended its

April 3, 2014 District of Columbia Amends Rules Regarding the Foreclosure Mediation Program By Lee Greenberg The District of Columbia Department of Insurance, Securities and Banking recently amended its

AVOIDING BUDGETING FORECLOSURE MADE EASY:

AVOIDING BUDGETING FORECLOSURE MADE EASY: WHAT YOU NEED TO KNOW A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., This complimentary a registered publication charitable

AVOIDING BUDGETING FORECLOSURE MADE EASY: WHAT YOU NEED TO KNOW A free publication provided by Consolidated Credit Counseling Services of Canada, Inc., This complimentary a registered publication charitable