Unit 9: Borrowing Money

|

|

|

- Clement Young

- 5 years ago

- Views:

Transcription

1 Unit 9: Borrowing Money 1

2 Financial Vocab Amortization Table A that lists regular payments of a loan and shows how much of each payment goes towards the interest charged and the principal borrowed, as the balance of the loan is reduced to 0. Collateral An asset that is held as security against the repayment of the loan The asset is often the item that you used the loan to purchase In the even that you cannot repay your loan, the item used as collateral, will be taken Compound interest A is the future value, P is the principle amount, i represents the interest rate per compounding period and n represents the number of compounding periods. Increases exponentially NOTE: 3% interest monthly does not mean 3% per month. It means 3% 12 = 0.25% per month Simple Interest A=P(1+rt) or A=P+Prt A is the future value, P is the principal amount, t represents time in years, and r represents the interest rate per annum. Increases linearly (same amount of interest each time) 2

3 Most people will need to take out a loan sometime in their lives (or borrow money in some form.) Few people can afford expensive purchases such as a car or a house without borrowing money from a financial institution. In unit 6 we discussed investments/loans where interest is calculated one of two ways: Simple interest or compound interest. Simple vs. Compound Interest Simple Interest: the amount of interest that you receive (if investing) or pay on a loan is calculated ONLY on the amount of money that you borrow. Usually loans from personal friends, family For simple interest, only the initial principal earns interest. The formula for simple interest is: A= P(1+rt) where A represents the amount present P represents the principal amount r = interest rate divided by 100 t represents the number of years We can calculate the interest only by using the formula: I = Prt 3

4 Example 1 Becca borrowed some money from her sister at 3% simple interest, with the interest calculated annually. If the loan was for 6.5 years and she had to pay back $2360, what was the principal? 4

5 Example 2: Ralph invested his summer earnings of $6000 at 4% simple interest, paid annually. Determine the relation that models this situation and determine when the investment will be worth $

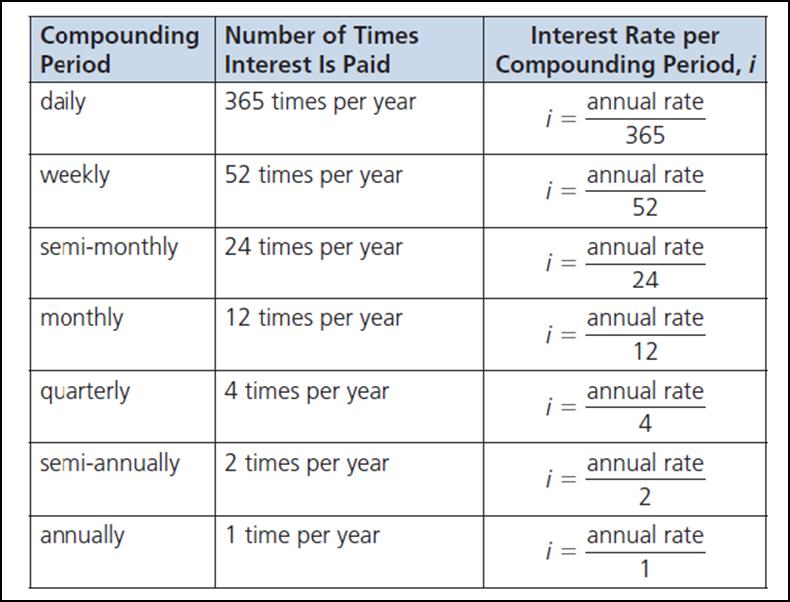

6 Compound Interest: Recall that compound interest is beneficial to the person receiving the interest, as interest gained on interest. But it costs the person paying the interest on a loan/credit card a lot of money, for the same reason. Therefore, the longer it takes to pay back the loan, the more you pay. Most financial institutions charge compound interest. For example; Loan Credit Cards Mortgage Borrowing Investing Savings Accounts Chequing Accounts GIC** Line of Credit Canada Savings Bond ** Student Loan ** GICs and Canada Savings Bonds can have simple or compound interest. Most loans are repaid by making regular payments over the term of the loan. However, some loans can be repaid in a single payment at the end of a term. For compound interest, the initial principal and accumulated interest also gain interest. The formula is where P is the principal amount i is the interest rate per compounding period n is the number of compounding periods Notice that i is the interest rate per compounding period. If interest is compounded x times each year, then the given percentage must be divided by x to come up with i. 6

7 7

8 Ex: A person takes out a $2000 loan, compounded at 10% semi annually. It takes the person 4 years to pay back the loan. How much does he he owe if he pays it back in one lump sum? 8

9 Ex: Which investment would yield a greater return for 10 years Option 1: $1000 at 3.5% annual simple interest Option 2: $1000 at 3% annual compound interest 3% 9

10 Ex: James intends to go to university. His Grandmother would like to invest $2000 in a GIC [Guaranteed Investment Certificate] A) How much will the GIC be worth if it is invested at 3% simple interest for 5 years? B) How much would it be worth if the interest was compounded annually? C) Which option is better for the bank? For James? 10

11 Ex: Annette wants to borrow money to renovate her kitchen. Her bank will charge her 3.6% compounded quarterly. Annette wants to pay back the money with one lump payment after 3 years, and wants this payment to be at most $ Determine the maximum amount of money she can borrow. 11

12 When a financial institution lends money, it will always negotiate the terms of the loan, including the interest rate and how it wants the money paid back. We will consider two cases: Paying Back Loans (Part 1) 1. A loan is paid off using a single payment at the end of the term. 2. A loan is paid off by making regular loan payments (only cases in which payment frequency matches the compounding period). We will start off by looking at loans that are paid off using a single payment at the end of the term. Examples: a farmer making a single lump sum payment on his loan after his crop has been harvested a payday loan offered by certain financial service providers. We have already dealt with these types of problems. Note: Interest Paid = A - P OR I = A - P 12

13 Ex: Trina s employer loaned her $10000 at a fixed interest rate of 6%, compounded annually, to pay for college tuition and textbooks. The loan is to be repaid in a single payment on the maturity date, which is at the end of 5 years. Determine how much interest Trina will pay on the loan. 13

14 You Try! Ex: Mary borrows $1000 at 10% interest, compounded semi annually. Sean borrows $1000 at 10% interest compounded annually. How much interest will each pay at the end of two years? 14

15 The more frequent the compounding, the more interest will be charged. When making financial decisions, it is important to understand the rate of interest charged, as well as the compounding, as these can create large differences over long periods of time. Ex: Which represents the lowest interest that would be paid? (A) 10% compounded daily (B) 10% compounded monthly (C) 10% compounded annually 15

16 Ex: Which represents the lowest interest that would be paid? (A) 8% compounded daily (B) 12% compounded monthly 16

17 Paying Back Loans Regular/Multiple Loan Payments However, in the majority of loans, the lender wants scheduled payments, not just one lump sum. This is common for mortgages and vehicle loans. There are three common types of regular payment schedules:. Monthly Biweekly Semi Monthly Accelerated Biweekly 17

18 Ex. For a loan that has a $600 per month payment, determine how much will be paid out at the end of 3 years, using each of the 3 payment options. Monthly: Bi weekly: (every 2 weeks) (26 times a year) 1. Find bi weekly payment first. 2. Find the amount paid out in 3 years Accelerated Bi weekly: (monthly payment )2) 26 times a year 1. Find accelerated bi weekly payment first. 2. Find amount paid out in 3 years. 18

19 Ex: 130 biweekly payments are required to pay off a loan. How many years does this represent? Ex: 288 semi monthly payments are required to pay off a loan. How many years does this represent? When people purchase a vehicle, they often link their loan payment schedule to their payroll schedule. Why is this the case? 19

20 The formulas that we learned previously (i.e A = P (1 + rt) and A = P(1 + i) n ) ONLY apply to single loan payments at the end of a term, and thus CANNOT be used in situations in which there is a regular loan payment. What we will do for these types of questions is refer to a table (can be manually created or using software) which shows the payment, interest principal and balance. 20

21 Ex: Mark is buying an ATV for the summer. The bank offers him a loan of $ to pay for his ATV with an interest rate of 4.5% compounding monthly. If Mark makes 36 monthly payments of $223.10, calculate the total interest paid at the end of the loan. (A) Complete the first three rows of the Amortization table... 21

is shown")

22 1. Interest Paid = (interest rate per year )# compounding periods) H Outstanding Balance 2. Principal Paid = Monthly Payment Interest 3. Current Balance = Previous Balance Principal Paid during Current Payment Period The entire table (as created using software) is shown below: 22

23 Determining the Cost of a Loan Using Technology To calculate a loan payment requires a more complicated formula. Usually, we use a TVM Solver (TVM stands for Time Value of Money). The TI 83 has a great TVM Solver in the Apps/Finance menu. Hit "Apps" then "Finance", choose TMV Solver. Hit Enter N is the number of payments I% is the annual interest rate PV is the present value of the loan PMT is the payment. FV is the future value of the loan P/Y is the payments per year. CY is the compounding periods per year. NOTES: if a variable is not being used in a question, or it is being solved for, put in zero for its value. For our purposes we will always leave PMT at END To solve for a variable: Make sure you put in 0 for its' value. Scroll down to the variable you want to solve for and hit "Enter". "FV" is negative when borrowing money 23

How long it will take to pay off at least half of the loan?")

How much interest will Lars have paid by the time the loan is paid off?")

24 Examples: 1. Consider Lars, who borrowed $12000 from a bank at 5% compounded monthly to purchase a new snowmobile. The bank requires him to pay $350 per month until the loan is paid off. A) How long it will take to pay off at least half of the loan? To solve for N, we use the arrow keys to navigate to N and select SOLVE (press ALPHA then ENTER). B) How long it will take to pay off the loan? C) How much interest will Lars have paid by the time the loan is paid off? (Both estimated value and exact value to find exact amount of interest we have to use our Finance App.) Number of Months to Pay off Loan Total Amount Paid = Approximate Interest Paid = Exact amount of interest paid = 24

25 2. When you were born your grandparents deposited $5,000 in a special account for your 21st birthday. The interest was compounded monthly at 5%. A) How much will it be worth on your 21st birthday? B) Suppose they also added $ 10 every month. How much will it be worth on your 21 st birthday? 25

Use a financial application to determine the amount of each monthly payment.")

26 3. Brittany takes out a loan for $ at 6% annual interest. She takes 20 years to repay the loan. A) Use a financial application to determine the amount of each monthly payment. B) How much interest will she have paid at the end of the 20 years? 26

Use TMV solver to determine her monthly payment.")

27 4. A bank offers a mortgage rate of 3.75% compounded semi annually for a 25 year period. Connie purchases a $ house with a 10% down payment. A) Use TMV solver to determine her monthly payment. B) How much interest does she pay? 27

28 5. Which is the better option? Explain. Option 1: Cost of a mortgage is $ , interest rate 2.5%, monthly payments, 25 year amortization. Option 2: Cost of mortgage is $ , interest rate is 3.5%, monthly payments, 20 year amortization. 28

29 A note about accelerated bi weekly payments Another option that banks often offer to the borrower is the option to pay back a loan with accelerated bi weekly payments. Consider a loan of $ in which a person has a $600 per month payment. The interest is compounded annually at 5%. Using our TVM Solver, we see that it takes about 280 months (or years) to pay off the loan, with total interest paid being $ In the span of one year, this person would pay 12 x $600 = $7200. If this person decided to go on a bi weekly payment plan, we would determine his payment per period by dividing $7200 by the 26 periods: Even though this person is paying the exact same money per year, he will save interest charges and lower his amortization date the time taken to pay off a loan because he is saving on interest charges by paying every two weeks instead of waiting until the end of the month. Using our TVM Solver, we see it takes 605 periods, which is equivalent to 1210 weeks (or years). The total interest is $ The person has not saved much time or much money considering the length of time of the loan. An accelerated bi weekly payment combines the two types of payments. The person pays half of the original monthly loan payment (in this case $300) every two weeks. At this rate, the loan will be paid off in 525 periods. This is 1050 weeks or years. This saves over 3 years of paying off a loan. The total interest paid is $ , which is a savings of over $10000! The lesson pay off your loans as quick as possible! 29

30 30

Section10.1.notebook May 24, 2014

Unit 9 Borrowing Money 1 Most people will need to take out a loan sometime in their lives. Few people can afford expensive purchases such as a car or a house without borrowing money from a financial institution.

Unit 9 Borrowing Money 1 Most people will need to take out a loan sometime in their lives. Few people can afford expensive purchases such as a car or a house without borrowing money from a financial institution.

Unit 9 Financial Mathematics: Borrowing Money. Chapter 10 in Text

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Unit 9 Financial Mathematics: Borrowing Money. Chapter 10 in Text

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Section Compound Interest

Section 5.1 - Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we have: Interest: Accumulated

Section 5.1 - Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we have: Interest: Accumulated

SECTION 6.1: Simple and Compound Interest

1 SECTION 6.1: Simple and Compound Interest Chapter 6 focuses on and various financial applications of interest. GOAL: Understand and apply different types of interest. Simple Interest If a sum of money

1 SECTION 6.1: Simple and Compound Interest Chapter 6 focuses on and various financial applications of interest. GOAL: Understand and apply different types of interest. Simple Interest If a sum of money

Name Date. Which option is most beneficial for the bank, and which is most beneficial for Leandro? A B C N = N = N = I% = I% = I% = PV = PV = PV =

F Math 12 2.0 Getting Started p. 78 Name Date Doris works as a personal loan manager at a bank. It is her job to decide whether the bank should lend money to a customer. When she approves a loan, she thinks

F Math 12 2.0 Getting Started p. 78 Name Date Doris works as a personal loan manager at a bank. It is her job to decide whether the bank should lend money to a customer. When she approves a loan, she thinks

Using the Finance Menu of the TI-83/84/Plus calculators

Using the Finance Menu of the TI-83/84/Plus calculators To get to the FINANCE menu On the TI-83 press 2 nd x -1 On the TI-83, TI-83 Plus, TI-84, or TI-84 Plus press APPS and then select 1:FINANCE The FINANCE

Using the Finance Menu of the TI-83/84/Plus calculators To get to the FINANCE menu On the TI-83 press 2 nd x -1 On the TI-83, TI-83 Plus, TI-84, or TI-84 Plus press APPS and then select 1:FINANCE The FINANCE

6.1 Simple and Compound Interest

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

Sections F.1 and F.2- Simple and Compound Interest

Sections F.1 and F.2- Simple and Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we

Sections F.1 and F.2- Simple and Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we

Getting Started Pg. 450 # 1, 2, 4a, 5ace, 6, (7 9)doso. Investigating Interest and Rates of Change Pg. 459 # 1 4, 6-10

doso. Investigating Interest and Rates of Change Pg. 459 # 1 4, 6-10") UNIT 8 FINANCIAL APPLICATIONS Date Lesson Text TOPIC Homework May 24 8.0 Opt Getting Started Pg. 450 # 1, 2, 4a, 5ace, 6, (7 9)doso May 26 8.1 8.1 Investigating Interest and Rates of Change Pg. 459 # 1

UNIT 8 FINANCIAL APPLICATIONS Date Lesson Text TOPIC Homework May 24 8.0 Opt Getting Started Pg. 450 # 1, 2, 4a, 5ace, 6, (7 9)doso May 26 8.1 8.1 Investigating Interest and Rates of Change Pg. 459 # 1

Sample Investment Device CD (Certificate of Deposit) Savings Account Bonds Loans for: Car House Start a business

Savings Account Bonds Loans for: Car House Start a business") Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

KEY CONCEPTS. A shorter amortization period means larger payments but less total interest

KEY CONCEPTS A shorter amortization period means larger payments but less total interest There are a number of strategies for reducing the time needed to pay off a mortgage and for reducing the total interest

KEY CONCEPTS A shorter amortization period means larger payments but less total interest There are a number of strategies for reducing the time needed to pay off a mortgage and for reducing the total interest

Financial institutions pay interest when you deposit your money into one of their accounts.

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

Analyzing Loans. cbalance ~ a Payment ($)

") 2. Analyzing Loans YOU WILL NEED calculator financial application spreadsheet software EXPLORE Which loan option would you choose to borrow $200? Why? A. A bank loan at 5%, compounded quarterly, to be

2. Analyzing Loans YOU WILL NEED calculator financial application spreadsheet software EXPLORE Which loan option would you choose to borrow $200? Why? A. A bank loan at 5%, compounded quarterly, to be

Simple Interest: Interest earned on the original investment amount only. I = Prt

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

The Regular Payment of an Annuity with technology

UNIT 7 Annuities Date Lesson Text TOPIC Homework Dec. 7 7.1 7.1 The Amount of an Annuity with technology Pg. 415 # 1 3, 5 7, 12 **check answers withti-83 Dec. 9 7.2 7.2 The Present Value of an Annuity

UNIT 7 Annuities Date Lesson Text TOPIC Homework Dec. 7 7.1 7.1 The Amount of an Annuity with technology Pg. 415 # 1 3, 5 7, 12 **check answers withti-83 Dec. 9 7.2 7.2 The Present Value of an Annuity

Simple Interest. Simple Interest is the money earned (or owed) only on the borrowed. Balance that Interest is Calculated On

only on the borrowed. Balance that Interest is Calculated On") MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

7.7 Technology: Amortization Tables and Spreadsheets

7.7 Technology: Amortization Tables and Spreadsheets Generally, people must borrow money when they purchase a car, house, or condominium, so they arrange a loan or mortgage. Loans and mortgages are agreements

7.7 Technology: Amortization Tables and Spreadsheets Generally, people must borrow money when they purchase a car, house, or condominium, so they arrange a loan or mortgage. Loans and mortgages are agreements

A mortgage is an annuity where the present value is the amount borrowed to purchase a home

KEY CONCEPTS A mortgage is an annuity where the present value is the amount borrowed to purchase a home The amortization period is the length of time needed to eliminate the debt Typical amortization period

KEY CONCEPTS A mortgage is an annuity where the present value is the amount borrowed to purchase a home The amortization period is the length of time needed to eliminate the debt Typical amortization period

Math 166: Topics in Contemporary Mathematics II

Math 166: Topics in Contemporary Mathematics II Xin Ma Texas A&M University October 28, 2017 Xin Ma (TAMU) Math 166 October 28, 2017 1 / 10 TVM Solver on the Calculator Unlike simple interest, it is much

Math 166: Topics in Contemporary Mathematics II Xin Ma Texas A&M University October 28, 2017 Xin Ma (TAMU) Math 166 October 28, 2017 1 / 10 TVM Solver on the Calculator Unlike simple interest, it is much

The principal is P $5000. The annual interest rate is 2.5%, or Since it is compounded monthly, I divided it by 12.

8.4 Compound Interest: Solving Financial Problems GOAL Use the TVM Solver to solve problems involving future value, present value, number of payments, and interest rate. YOU WILL NEED graphing calculator

8.4 Compound Interest: Solving Financial Problems GOAL Use the TVM Solver to solve problems involving future value, present value, number of payments, and interest rate. YOU WILL NEED graphing calculator

9.1 Financial Mathematics: Borrowing Money

Math 3201 9.1 Financial Mathematics: Borrowing Money Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based on the amount of money that you

Math 3201 9.1 Financial Mathematics: Borrowing Money Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based on the amount of money that you

The TVM Solver. When you input four of the first five variables in the list above, the TVM Solver solves for the fifth variable.

1 The TVM Solver The TVM Solver is an application on the TI-83 Plus graphing calculator. It displays the timevalue-of-money (TVM) variables used in solving finance problems. Prior to using the TVM Solver,

1 The TVM Solver The TVM Solver is an application on the TI-83 Plus graphing calculator. It displays the timevalue-of-money (TVM) variables used in solving finance problems. Prior to using the TVM Solver,

Introduction to the Compound Interest Formula

Introduction to the Compound Interest Formula Lesson Objectives: students will be introduced to the formula students will learn how to determine the value of the required variables in order to use the

Introduction to the Compound Interest Formula Lesson Objectives: students will be introduced to the formula students will learn how to determine the value of the required variables in order to use the

Math Week in Review #10

Math 166 Fall 2008 c Heather Ramsey Page 1 Chapter F - Finance Math 166 - Week in Review #10 Simple Interest - interest that is computed on the original principal only Simple Interest Formulas Interest

Math 166 Fall 2008 c Heather Ramsey Page 1 Chapter F - Finance Math 166 - Week in Review #10 Simple Interest - interest that is computed on the original principal only Simple Interest Formulas Interest

The values in the TVM Solver are quantities involved in compound interest and annuities.

Texas Instruments Graphing Calculators have a built in app that may be used to compute quantities involved in compound interest, annuities, and amortization. For the examples below, we ll utilize the screens

Texas Instruments Graphing Calculators have a built in app that may be used to compute quantities involved in compound interest, annuities, and amortization. For the examples below, we ll utilize the screens

1: Finance, then 1: TVM Solver

Wksheet 6-6: TVM Solver A graphing calculat can be used to make calculations using the compound interest fmula: n FV PV ( 1 i). The TVM Solver, the Time-Value-Money Solver, allows you to enter the value

Wksheet 6-6: TVM Solver A graphing calculat can be used to make calculations using the compound interest fmula: n FV PV ( 1 i). The TVM Solver, the Time-Value-Money Solver, allows you to enter the value

3.1 Mathematic of Finance: Simple Interest

3.1 Mathematic of Finance: Simple Interest Introduction Part I This chapter deals with Simple Interest, and teaches students how to calculate simple interest on investments and loans. The Simple Interest

3.1 Mathematic of Finance: Simple Interest Introduction Part I This chapter deals with Simple Interest, and teaches students how to calculate simple interest on investments and loans. The Simple Interest

Lesson 24 Annuities. Minds On

Lesson 24 Annuities Goals To define define and understand how annuities work. To understand how investments, loans and mortgages work. To analyze and solve annuities in real world situations (loans, investments).

Lesson 24 Annuities Goals To define define and understand how annuities work. To understand how investments, loans and mortgages work. To analyze and solve annuities in real world situations (loans, investments).

Activity 1.1 Compound Interest and Accumulated Value

Activity 1.1 Compound Interest and Accumulated Value Remember that time is money. Ben Franklin, 1748 Reprinted by permission: Tribune Media Services Broom Hilda has discovered too late the power of compound

Activity 1.1 Compound Interest and Accumulated Value Remember that time is money. Ben Franklin, 1748 Reprinted by permission: Tribune Media Services Broom Hilda has discovered too late the power of compound

Chapter 4 Real Life Decisions

Chapter 4 Real Life Decisions Chp. 4.1 Owning a vehicle After this section, I'll know how to... Explain the difference between buying, leasing and leasing-to-own a vehicle Calculate the costs of buying,

Chapter 4 Real Life Decisions Chp. 4.1 Owning a vehicle After this section, I'll know how to... Explain the difference between buying, leasing and leasing-to-own a vehicle Calculate the costs of buying,

Name Date. Goal: Solve problems that involve simple interest. 1. term: The contracted duration of an investment or loan.

F Math 12 1.1 Simple Interest p.6 Name Date Goal: Solve problems that involve simple interest. 1. term: The contracted duration of an investment or loan. 2. interest (i): The amount of money earned on

F Math 12 1.1 Simple Interest p.6 Name Date Goal: Solve problems that involve simple interest. 1. term: The contracted duration of an investment or loan. 2. interest (i): The amount of money earned on

TVM Appendix: Using the TI-83/84

Time Value of Money Problems on a Texas Instruments TI-84 Before you start: To calculate problems on a TI-84, you have to go into the applications menu, the lavender APPS key on the calculator. Several

Time Value of Money Problems on a Texas Instruments TI-84 Before you start: To calculate problems on a TI-84, you have to go into the applications menu, the lavender APPS key on the calculator. Several

Learning Goal: What is compound interest? How do we compute the interest on an investment?

Name IB Math Studies Year 1 Date 7-6 Intro to Compound Interest Learning Goal: What is compound interest? How do we compute the interest on an investment? Warm-Up: Let s say that you deposit $100 into

Name IB Math Studies Year 1 Date 7-6 Intro to Compound Interest Learning Goal: What is compound interest? How do we compute the interest on an investment? Warm-Up: Let s say that you deposit $100 into

When changing any conditions of an investment or loan, the amount or principal will also change.

KEY CONCEPTS When changing any conditions of an investment or loan, the amount or principal will also change. Doubling an interest rate or term more than doubles the total interest This is due to the effects

KEY CONCEPTS When changing any conditions of an investment or loan, the amount or principal will also change. Doubling an interest rate or term more than doubles the total interest This is due to the effects

I. Warnings for annuities and

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Section 5.1 Compound Interest

Section 5.1 Compound Interest Simple Interest Formulas: Interest: Accumulated amount: I = P rt A = P (1 + rt) Here P is the principal (money you start out with), r is the interest rate (as a decimal),

Section 5.1 Compound Interest Simple Interest Formulas: Interest: Accumulated amount: I = P rt A = P (1 + rt) Here P is the principal (money you start out with), r is the interest rate (as a decimal),

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

7.5 Amount of an Ordinary Annuity

7.5 Amount of an Ordinary Annuity Nigel is saving $700 each year for a trip. Rashid is saving $200 at the end of each month for university. Jeanine is depositing $875 at the end of each 3 months for 3

7.5 Amount of an Ordinary Annuity Nigel is saving $700 each year for a trip. Rashid is saving $200 at the end of each month for university. Jeanine is depositing $875 at the end of each 3 months for 3

Simple Interest: Interest earned on the original investment amount only

c Kathryn Bollinger, November 30, 2005 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only = I = Prt I = the interest earned, P = the amount

c Kathryn Bollinger, November 30, 2005 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only = I = Prt I = the interest earned, P = the amount

Week in Review #7. Section F.3 and F.4: Annuities, Sinking Funds, and Amortization

WIR Math 166-copyright Joe Kahlig, 10A Page 1 Week in Review #7 Section F.3 and F.4: Annuities, Sinking Funds, and Amortization an annuity is a sequence of payments made at a regular time intervals. For

WIR Math 166-copyright Joe Kahlig, 10A Page 1 Week in Review #7 Section F.3 and F.4: Annuities, Sinking Funds, and Amortization an annuity is a sequence of payments made at a regular time intervals. For

Example. Chapter F Finance Section F.1 Simple Interest and Discount

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Texas Essential Knowledge and Skills (Prerequisite standards)

Texas Essential Knowledge and Skills (Prerequisite standards)") Lesson Description Students learn how to compare various small loans including easy access loans. Through the use of an online calculator, students determine the total repayment as well as the total interest

Lesson Description Students learn how to compare various small loans including easy access loans. Through the use of an online calculator, students determine the total repayment as well as the total interest

And Why. What You ll Learn. Key Words

What You ll Learn To use technology to solve problems involving annuities and mortgages and to gather and interpret information about annuities and mortgages And Why Annuities are used to save and pay

What You ll Learn To use technology to solve problems involving annuities and mortgages and to gather and interpret information about annuities and mortgages And Why Annuities are used to save and pay

Annual = Semi- Annually= Monthly=

F Math 12 1.1 Simple Interest p.6 1. Term: The of an investment or loan 2. Interest (i): the amount of earned on an investment or paid on a loan 3. Fixed interest rate: An interest rate that is guaranteed

F Math 12 1.1 Simple Interest p.6 1. Term: The of an investment or loan 2. Interest (i): the amount of earned on an investment or paid on a loan 3. Fixed interest rate: An interest rate that is guaranteed

The three formulas we use most commonly involving compounding interest n times a year are

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Chapter 15B and 15C - Annuities formula

Chapter 15B and 15C - Annuities formula Finding the amount owing at any time during the term of the loan. A = PR n Q Rn 1 or TVM function on the Graphics Calculator Finding the repayment amount, Q Q =

Chapter 15B and 15C - Annuities formula Finding the amount owing at any time during the term of the loan. A = PR n Q Rn 1 or TVM function on the Graphics Calculator Finding the repayment amount, Q Q =

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

5.3 Amortization and Sinking Funds

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

Chapter 2 :Applying Time Value Concepts

Chapter 2 :Applying Time Value Concepts 2.1 True/False 1) Time value of money is based on the belief that a dollar that will be received at some future date is worth more than a dollar today. Diff: 1 Type:

Chapter 2 :Applying Time Value Concepts 2.1 True/False 1) Time value of money is based on the belief that a dollar that will be received at some future date is worth more than a dollar today. Diff: 1 Type:

Section 5.1 Compound Interest

Section 5.1 Compound Interest Simple Interest Formulas: Interest: Accumulated amount: I = Prt A = P (1 + rt) Here P is the principal (money you start out with), r is the interest rate (as a decimal), and

Section 5.1 Compound Interest Simple Interest Formulas: Interest: Accumulated amount: I = Prt A = P (1 + rt) Here P is the principal (money you start out with), r is the interest rate (as a decimal), and

Chapter 5: Finance. Section 5.1: Basic Budgeting. Chapter 5: Finance

Chapter 5: Finance Most adults have to deal with the financial topics in this chapter regardless of their job or income. Understanding these topics helps us to make wise decisions in our private lives

Chapter 5: Finance Most adults have to deal with the financial topics in this chapter regardless of their job or income. Understanding these topics helps us to make wise decisions in our private lives

Chapter 3 Mathematics of Finance

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Copyright 2015 Pearson Education, Inc. All rights reserved.

Chapter 4 Mathematics of Finance Section 4.1 Simple Interest and Discount A fee that is charged by a lender to a borrower for the right to use the borrowed funds. The funds can be used to purchase a house,

Chapter 4 Mathematics of Finance Section 4.1 Simple Interest and Discount A fee that is charged by a lender to a borrower for the right to use the borrowed funds. The funds can be used to purchase a house,

CHAPTER 2 TIME VALUE OF MONEY

CHAPTER 2 TIME VALUE OF MONEY True/False Easy: (2.2) Compounding Answer: a EASY 1. One potential benefit from starting to invest early for retirement is that the investor can expect greater benefits from

CHAPTER 2 TIME VALUE OF MONEY True/False Easy: (2.2) Compounding Answer: a EASY 1. One potential benefit from starting to invest early for retirement is that the investor can expect greater benefits from

Consumer and Mortgage Loans. Assignments

Financial Plan Assignments Assignments Think through the purpose of any consumer loans you have. Are they necessary? Could you have gotten by without them? If you have consumer loans outstanding, write

Financial Plan Assignments Assignments Think through the purpose of any consumer loans you have. Are they necessary? Could you have gotten by without them? If you have consumer loans outstanding, write

Interest: The money earned from an investment you have or the cost of borrowing money from a lender.

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

1.1. Simple Interest. INVESTIGATE the Math

1.1 Simple Interest YOU WILL NEED calculator graph paper straightedge EXPLORE An amount of money was invested. Interpret the graph below to determine a) how much money was invested, b) the value of the

1.1 Simple Interest YOU WILL NEED calculator graph paper straightedge EXPLORE An amount of money was invested. Interpret the graph below to determine a) how much money was invested, b) the value of the

Finance 197. Simple One-time Interest

Finance 197 Finance We have to work with money every day. While balancing your checkbook or calculating your monthly expenditures on espresso requires only arithmetic, when we start saving, planning for

Finance 197 Finance We have to work with money every day. While balancing your checkbook or calculating your monthly expenditures on espresso requires only arithmetic, when we start saving, planning for

Copyright 2015 by the UBC Real Estate Division

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

Mortgages & Equivalent Interest

Mortgages & Equivalent Interest A mortgage is a loan which you then pay back with equal payments at regular intervals. Thus a mortgage is an annuity! A down payment is a one time payment you make so that

Mortgages & Equivalent Interest A mortgage is a loan which you then pay back with equal payments at regular intervals. Thus a mortgage is an annuity! A down payment is a one time payment you make so that

hp calculators HP 20b Loan Amortizations The time value of money application Amortization Amortization on the HP 20b Practice amortizing loans

The time value of money application Amortization Amortization on the HP 20b Practice amortizing loans The time value of money application The time value of money application built into the HP 20b is used

The time value of money application Amortization Amortization on the HP 20b Practice amortizing loans The time value of money application The time value of money application built into the HP 20b is used

Interest Compounded Annually. Table 3.27 Interest Computed Annually

33 CHAPTER 3 Exponential, Logistic, and Logarithmic Functions 3.6 Mathematics of Finance What you ll learn about Interest Compounded Annually Interest Compounded k Times per Year Interest Compounded Continuously

33 CHAPTER 3 Exponential, Logistic, and Logarithmic Functions 3.6 Mathematics of Finance What you ll learn about Interest Compounded Annually Interest Compounded k Times per Year Interest Compounded Continuously

Alex has a greater rate of return on his portfolio than Jamie does.

The term (in years) is 9 years. The GIC is worth $6299.36. CSB: The principal is $2000. The annual interest rate is 3.1%. times per The term (in years) is 4 years. The CSB is worth $2261.88. Savings account:

The term (in years) is 9 years. The GIC is worth $6299.36. CSB: The principal is $2000. The annual interest rate is 3.1%. times per The term (in years) is 4 years. The CSB is worth $2261.88. Savings account:

Advanced Mathematical Decision Making In Texas, also known as

Advanced Mathematical Decision Making In Texas, also known as Advanced Quantitative Reasoning Unit VI: Decision Making in Finance This course is a project of The Texas Association of Supervisors of Mathematics

Advanced Mathematical Decision Making In Texas, also known as Advanced Quantitative Reasoning Unit VI: Decision Making in Finance This course is a project of The Texas Association of Supervisors of Mathematics

Student Loans. Student Worksheet

Student Loans Student Worksheet Name: Part I: If help from parents, scholarships, grants and work study do not cover the full cost of a student s education, many students get to loans to pay for school.

Student Loans Student Worksheet Name: Part I: If help from parents, scholarships, grants and work study do not cover the full cost of a student s education, many students get to loans to pay for school.

Day 3 Simple vs Compound Interest.notebook April 07, Simple Interest is money paid or earned on the. The Principal is the

LT: I can calculate simple and compound interest. p.11 What is Simple Interest? What is Principal? Simple Interest is money paid or earned on the. The Principal is the What is the Simple Interest Formula?

LT: I can calculate simple and compound interest. p.11 What is Simple Interest? What is Principal? Simple Interest is money paid or earned on the. The Principal is the What is the Simple Interest Formula?

Everyone Wants a Mortgage

Everyone Wants a Mortgage (for a home near the ocean!!) Mortgage Scenario One House cost: $1 290 000 Deposit: $150 000 Minimum Deposit: 10% 1)a) Do you have enough money for the deposit? b) What is the

Everyone Wants a Mortgage (for a home near the ocean!!) Mortgage Scenario One House cost: $1 290 000 Deposit: $150 000 Minimum Deposit: 10% 1)a) Do you have enough money for the deposit? b) What is the

Name Date. Goal: Solve problems that involve credit.

F Math 12 2.3 Solving Problems Involving Credit p. 104 Name Date Goal: Solve problems that involve credit. 1. line of credit: A pre-approved loan that offers immediate access to funds, up to a predefined

F Math 12 2.3 Solving Problems Involving Credit p. 104 Name Date Goal: Solve problems that involve credit. 1. line of credit: A pre-approved loan that offers immediate access to funds, up to a predefined

G r a d e 1 2 A p p l i e d M a t h e m a t i c s ( 4 0 S ) Final Practice Examination Answer Key

Final Practice Examination Answer Key") G r a d e 1 2 A p p l i e d M a t h e m a t i c s ( 4 0 S ) Final Practice Examination Answer Key G r a d e 1 2 A p p l i e d M a t h e m a t i c s Final Practice Examination Answer Key Name: Student

G r a d e 1 2 A p p l i e d M a t h e m a t i c s ( 4 0 S ) Final Practice Examination Answer Key G r a d e 1 2 A p p l i e d M a t h e m a t i c s Final Practice Examination Answer Key Name: Student

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

BUYING YOUR FIRST HOME: THREE STEPS TO SUCCESSFUL MORTGAGE SHOPPING MORTGAGES June 2015 Cat. No.: FC5-22/3-2015E-PDF ISBN: 978-0-660-02848-4 Her Majesty the Queen in Right of Canada (Financial Consumer

2.4 - Exponential Functions

c Kathryn Bollinger, January 21, 2010 1 2.4 - Exponential Functions General Exponential Functions Def: A general exponential function has the form f(x) = a b x where a is a real number constant with a

c Kathryn Bollinger, January 21, 2010 1 2.4 - Exponential Functions General Exponential Functions Def: A general exponential function has the form f(x) = a b x where a is a real number constant with a

Understanding Consumer and Mortgage Loans

Personal Finance: Another Perspective Understanding Consumer and Mortgage Loans Updated 2017-02-07 Note: Graphs on this presentation are from http://www.bankrate.com/funnel/graph/default.aspx? Copied on

Personal Finance: Another Perspective Understanding Consumer and Mortgage Loans Updated 2017-02-07 Note: Graphs on this presentation are from http://www.bankrate.com/funnel/graph/default.aspx? Copied on

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Time Value of Money. Part III. Outline of the Lecture. September Growing Annuities. The Effect of Compounding. Loan Type and Loan Amortization

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

The High Cost of Other People s Money. Hutch Sprunt Appalachian State University NCCTM October 2005

The High Cost of Other People s Money Hutch Sprunt Appalachian State University NCCTM October 2005 A helpful progression for students: Larger loans Credit cards (and debit cards) Various financial sources

The High Cost of Other People s Money Hutch Sprunt Appalachian State University NCCTM October 2005 A helpful progression for students: Larger loans Credit cards (and debit cards) Various financial sources

Texas Instruments 83 Plus and 84 Plus Calculator

Texas Instruments 83 Plus and 84 Plus Calculator For the topics we cover, keystrokes for the TI-83 PLUS and 84 PLUS are identical. Keystrokes are shown for a few topics in which keystrokes are unique.

Texas Instruments 83 Plus and 84 Plus Calculator For the topics we cover, keystrokes for the TI-83 PLUS and 84 PLUS are identical. Keystrokes are shown for a few topics in which keystrokes are unique.

Further Mathematics 2016 Core: RECURSION AND FINANCIAL MODELLING Chapter 7 Loans, investments and asset values

Further Mathematics 2016 Core: RECURSION AND FINANCIAL MODELLING Chapter 7 Loans, investments and asset values Key knowledge (Chapter 7) Amortisation of a reducing balance loan or annuity and amortisation

Further Mathematics 2016 Core: RECURSION AND FINANCIAL MODELLING Chapter 7 Loans, investments and asset values Key knowledge (Chapter 7) Amortisation of a reducing balance loan or annuity and amortisation

Investing & Borrowing Money Practice Test

Investing & Borrowing Money Practice Test Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Determine the interest earned on a simple interest investment

Investing & Borrowing Money Practice Test Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Determine the interest earned on a simple interest investment

Year 10 GENERAL MATHEMATICS

Year 10 GENERAL MATHEMATICS UNIT 2, TOPIC 3 - Part 1 Percentages and Ratios A lot of financial transaction use percentages and/or ratios to calculate the amount owed. When you borrow money for a certain

Year 10 GENERAL MATHEMATICS UNIT 2, TOPIC 3 - Part 1 Percentages and Ratios A lot of financial transaction use percentages and/or ratios to calculate the amount owed. When you borrow money for a certain

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved.

. All rights reserved.") Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Chapter 5 Time Value of Money

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

Introduction to the Hewlett-Packard (HP) 10B Calculator and Review of Mortgage Finance Calculations

10B Calculator and Review of Mortgage Finance Calculations") Introduction to the Hewlett-Packard (HP) 0B Calculator and Review of Mortgage Finance Calculations Real Estate Division Faculty of Commerce and Business Administration University of British Columbia Introduction

Introduction to the Hewlett-Packard (HP) 0B Calculator and Review of Mortgage Finance Calculations Real Estate Division Faculty of Commerce and Business Administration University of British Columbia Introduction

Foundations of Mathematics Simple Interest

1.1 Simple Interest Principal, P, is the amount of money invested or loaned. Interest, I, is the money earned on an investment or paid on a loan. Maturity is the contracted end date of an investment or

1.1 Simple Interest Principal, P, is the amount of money invested or loaned. Interest, I, is the money earned on an investment or paid on a loan. Maturity is the contracted end date of an investment or

13.3. Annual Percentage Rate (APR) and the Rule of 78

and the Rule of 78") 13.3. Annual Percentage Rate (APR) and the Rule of 78 Objectives A. Find the APR of a loan. B. Use the rule of 78 to find the refund and payoff of a loan. C. Find the monthly payment for a loan using an

13.3. Annual Percentage Rate (APR) and the Rule of 78 Objectives A. Find the APR of a loan. B. Use the rule of 78 to find the refund and payoff of a loan. C. Find the monthly payment for a loan using an

Section 5.1 Simple and Compound Interest

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Simple Interest: Interest earned only on the original principal amount invested.

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

F.3 - Annuities and Sinking Funds

F.3 - Annuities and Sinking Funds Math 166-502 Blake Boudreaux Department of Mathematics Texas A&M University March 22, 2018 Blake Boudreaux (TAMU) F.3 - Annuities March 22, 2018 1 / 12 Objectives Know

F.3 - Annuities and Sinking Funds Math 166-502 Blake Boudreaux Department of Mathematics Texas A&M University March 22, 2018 Blake Boudreaux (TAMU) F.3 - Annuities March 22, 2018 1 / 12 Objectives Know

Introduction to Corporate Finance, Fourth Edition. Chapter 5: Time Value of Money

Multiple Choice Questions 11. Section: 5.4 Annuities and Perpetuities B. Chapter 5: Time Value of Money 1 1 n (1 + k) 1 (1.15) PMT $,,(6.5933) $1, 519 k.15 N, I/Y15, PMT,, FV, CPT 1,519 14. Section: 5.7

Multiple Choice Questions 11. Section: 5.4 Annuities and Perpetuities B. Chapter 5: Time Value of Money 1 1 n (1 + k) 1 (1.15) PMT $,,(6.5933) $1, 519 k.15 N, I/Y15, PMT,, FV, CPT 1,519 14. Section: 5.7

5= /

Chapter 6 Finance 6.1 Simple Interest and Sequences Review: I = Prt (Simple Interest) What does Simple mean? Not Simple = Compound I part Interest is calculated once, at the end. Ex: (#10) If you borrow

Chapter 6 Finance 6.1 Simple Interest and Sequences Review: I = Prt (Simple Interest) What does Simple mean? Not Simple = Compound I part Interest is calculated once, at the end. Ex: (#10) If you borrow

6.1 Simple Interest page 243

page 242 6 Students learn about finance as it applies to their daily lives. Two of the most important types of financial decisions for many people involve either buying a house or saving for retirement.

page 242 6 Students learn about finance as it applies to their daily lives. Two of the most important types of financial decisions for many people involve either buying a house or saving for retirement.

Introduction. Once you have completed this chapter, you should be able to do the following:

Introduction This chapter continues the discussion on the time value of money. In this chapter, you will learn how inflation impacts your investments; you will also learn how to calculate real returns

Introduction This chapter continues the discussion on the time value of money. In this chapter, you will learn how inflation impacts your investments; you will also learn how to calculate real returns

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Graphing Calculator Appendix

Appendix GC GC-1 This appendix contains some keystroke suggestions for many graphing calculator operations that are featured in this text. The keystrokes are for the TI-83/ TI-83 Plus calculators. The

Appendix GC GC-1 This appendix contains some keystroke suggestions for many graphing calculator operations that are featured in this text. The keystrokes are for the TI-83/ TI-83 Plus calculators. The

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 1. Basic Interest Theory. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics.

Manual for SOA Exam FM/CAS Exam 2. Chapter 1. Basic Interest Theory. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics.

Section 8.1. I. Percent per hundred

1 Section 8.1 I. Percent per hundred a. Fractions to Percents: 1. Write the fraction as an improper fraction 2. Divide the numerator by the denominator 3. Multiply by 100 (Move the decimal two times Right)

1 Section 8.1 I. Percent per hundred a. Fractions to Percents: 1. Write the fraction as an improper fraction 2. Divide the numerator by the denominator 3. Multiply by 100 (Move the decimal two times Right)

UNIT 6 1 What is a Mortgage?

UNIT 6 1 What is a Mortgage? A mortgage is a legal document that pledges property to the lender as security for payment of a debt. In the case of a home mortgage, the debt is the money that is borrowed

UNIT 6 1 What is a Mortgage? A mortgage is a legal document that pledges property to the lender as security for payment of a debt. In the case of a home mortgage, the debt is the money that is borrowed

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the