Top 10 Income Tax Planning Ideas for 2013

|

|

|

- Mavis Walters

- 5 years ago

- Views:

Transcription

Ph: (920) 593-1701 E-mail: robert.")

1 Top 10 Income Tax Planning Ideas for 2013 Presented by: Robert S. Keebler, CPA, MST, AEP(Distinguished) Ph: (920)

2 Ideas 1. Bracket Management 2. Real Estate Reorganizations 3. Charitable Lead Trusts 4. Income Shifting 5. Roth IRA Conversions 6. Substantial Sale Charitable Remainder Trust 7. Retirement Charitable Remainder Trust 8. Income Shifting Charitable Remainder Trust 9. IRC 453 Deferred Installment Sale % Surtax on Net Investment Income Bonus: 11. NING Trust

3 Executive Summary The higher rates under American Taxpayer Relief Act (ATRA) and Affordable Care Act (ACA) have necessitated a quantum leap in our approach to tax planning This paradigm shift requires a longer term analysis because of the five-tier system

4 Five Tiers Traditional Income Tax Alternative Minimum Tax 3.8% Tax on Net Investment Income PEP and PEASE limitations The 39.6% and 5% incremental rates

5 Bracket Management

6 Time Frame Shift : 3-5 year horizon : EGTRRA Decade : Time of irresolution 2013-Forward: 5-15 year horizon

7 Recap Flying below the radar $450, % Ordinary Income Tax Rate $300,000 PEP/Pease $250, % Surtax

8 Key Management Issues Capital Gain Rates Income Tax Rates Ordinary Income should at least equal Itemized Deductions plus exemptions Tax liability should equal tax credits available

9 Taxable Income and RMD

10 Amount over 39.6% Tax Bracket

11 Income Tax Rate

12 Capital Gains Tax Rate

13 Taxable Income per Bracket

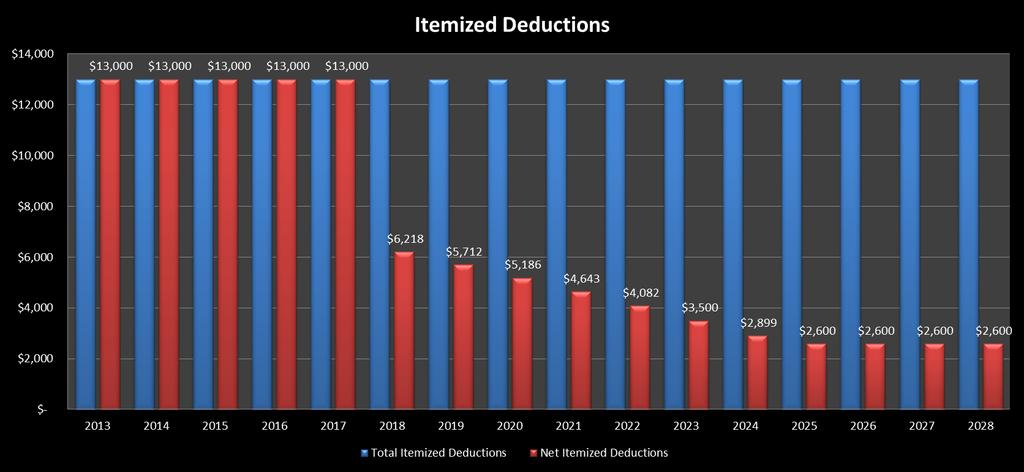

14 Itemized Deductions

15 Real Estate Reorganizations

16 Real Estate Reorganizations The 3.8% Net Investment Income Tax is imposed on Self-Rentals This tax can be avoided with a tax-free restructuring

17 Today s Ownership 50% 50% 50% 50% Operations, LLC Lease Payments Real Estate, LLC Lease is subject to the surtax

18 New Design Holding LLC 100% 100% Operations LLC Lease Payments Real Estate LLC

19 Summary Tax-free transfer of both entities to Holding LLC The lease no longer exists for tax purposes 3.8% Surtax does not apply

20 Income Shifting

21 Key Transactions Outright gifts to children: Advantages Easy Effective Disadvantages No Asset Protection No Spousal Protection No Spend Thrift Protection

22 Key Transactions LLC and partnership gifts: Advantages Effective from a tax perspective Better control Income without cash flow Some asset protection Disadvantages Not the same level of asset protection as a trust

23 Key Transactions Gifts to non-grantor trusts for family EBSTs & QSSTs Distributions from existing trusts Conversion of grantor trusts to non-grantor trusts

24 Income Shifting Steps to Planning Step 1: Develop a 5 to 15 year projection of income and deductions and compare these projections to the various taxes Step 2: Develop an analysis to determine the client s permanent tax bracket. Analysis will test whether an intrabracket transactions increase the 3.8% surtax, the AMT, impact of PEP/Pease, or the 39.6% tax rate

25 Income Shifting Steps to Planning Step 3: Develop a series of bracket-crossing conversions analysis. Each analysis must be measured autonomously standing on its own and take into account the various taxes.

26 2013 Innovative CRT Strategies

27 Charitable Giving Vehicles Direct contributions Donor advised funds Charitable Trusts Charitable Remainder Trusts (CRTs) Charitable Lead Trusts (CLTs)

28 Substantial Sale CRT Substantial Sale CRT (Standard CRT) CRT to eliminate or reduce/defer the 3.8% Surtax and 5% incremental capital gains tax

29 Retirement Charitable Remainder Trust

30 Charitable Remainder Trust (CRT) A Charitable Remainder Trust (CRT) is a split interest trust consisting of an income interest and a remainder interest. During the term of the trust, the income interest is usually paid out to the donor (or some other named beneficiary). At the end of the trust term, the remainder (whatever is left in the trust) is paid to the charity or charities that have been designated in the trust document.

31 Charitable Remainder Trust (CRT) Donor (Income Beneficiary) Donor receives an immediate income tax deduction for present value of the remainder interest (must be at least 10% of the value of the assets originally contributed) Transfer of highlyappreciated assets Annual (or more frequent) payments for life (or a term of years) CRT Charity (Remainder Beneficiary) At the donor s death (or at the end of the trust term), the charity receives the residual assets held in the trust

32 CHARITABLE REMAINDER TRUSTS Charitable remainder trusts can be used to reduce or avoid surtax and incremental capital gains tax by smoothing out income CRTs are particularly useful when a taxpayer has a large capital gain that pushes income above the applicable threshold amount (ATA) Before explaining how the planning works, it will be helpful to look at some background information

33 CRTs Taxation The donor will NOT realize gain or loss when property is transferred to the trust However, the grantor may be required to recognize gain if: Property transferred is subject to indebtedness that exceeds grantor basis Grantor receives property from the trust in exchange for the transfer to the trust. The donor will NOT realize gain or loss if and when the transferred assets are subsequently sold by the trustee of the CRT

34 CRTs Taxation The character of income received by the recipient is subject to and controlled by the tier rules of IRC 664(b) First, distributions are taxed as ordinary income Second, distributions are taxed as capital gains Third, distributions are taxed as tax-exempt income (e.g. municipal bond income) Finally, distributions are assumed to be the non-taxable return of principal CRTs are not subject to the 3.8% surtax CRTs are not subject to the new 5.0% incremental capital gains tax

35 CRTs Taxation STEP 1: Current Ordinary Income STEP 2: Accumulated Ordinary Income STEP 3: Current Capital Gains STEP 4: Accumulated Capital Gains STEP 5: Current Tax- Exempt Income STEP 6: Accumulated Tax-Exempt Income STEP 7: Return of Capital Tier 1 Tier 2 Tier 3 Tier 4

36 Charitable Remainder Trust (CRT) Two Main Types of CRTs Charitable Remainder Annuity Trust (Standard - CRAT) The beneficiaries receive a stated amount of the initial trust assets each year The amount received is established at the beginning of the trust and will not change during the term of the trust regardless of investment performance (unless inadequate investment performance causes the trust to run out of assets) Charitable Remainder Unitrust (Standard - CRUT) Income beneficiaries receive a stated percentage of the trust s assets each year. The distribution will vary from year to year depending on the investment performance of the trust assets and the amount withdrawn

37 FLIP Net Income with Makeup Charitable Remainder Unitrust (FLIP-NIMCRUT) Lesser of (until end of NIMCRUT term): (1) Net Income (2) Annual payout percentage (6.0%) each year (plus any makeup amounts in arrearage during NIMCRUT term) Grantor Charitable deduction when gifted After NIMCRUT term, the payment will be based on the annual payout percentage (6.0%) (any makeup amounts in arrearage are irrevocably lost after conversion) Gift of highly-appreciated asset $1,000,000 FLIP-NIMCRUT Highly-appreciated asset is sold Cash is reinvested without any income tax being imposed Wealth Replacement Trust $1,000,000 At death At death (or end of term) Charity Beneficiaries 37

38 Income Shifting CRT Income Shifting CRT (Standard CRT for children) CRT to eliminate or reduce/defer the 3.8% surtax and 5% incremental capital gains tax while shifting the incidence of taxation to children and grandchildren

39 Income Shifting CRT Shifts ordinary income to family Shift capital gains to family members Benefit charity

40 Charitable Remainder Trust (CRT) for Benefit of Donor s Children Donor s Children and Grandchildren Donor receives an immediate income tax deduction for present value of the remainder interest (must be at least 10% of the value of the assets originally contributed) Transfer of highlyappreciated assets Annual (or more frequent) payments for life (or a term of years) Considerations Income Tax Gift/Estate Tax Generation Skipping Tax Standard - CRT Charity (Remainder Beneficiary) At the donor s death (or at the end of the trust term), the charity receives the residual assets held in the trust

41 IRC 453 Deferred Installment Sale

42 IRC 453 IRC 453 allowed for deferral of taxation on Installment Sales $5,000,000 annual limitation $10,000,000 annual limitation for married couple Gain is generally deferred until payment occurs Depreciation recapture provisions IRC 453(i)

43 Increase in Basis Sale from taxpayer to a non-grantor trust or a child receives a basis increase Basis will equal the purchase price

44 Two-year Rule IRC 453(e)(2) provides a sale by a related party within two years results in realization of the original deferral

45 Two Years and a day? No realization of the original gain if the sale is two years and a day

46 Example Dad sells to Son in exchange for a 20 year note with payments of principal and interest of $250,000 per year Dad flies below the radar

47 Nevada Incomplete Gift Non-Grantor Trust (NING)

48 Payment of Income Tax Gift Tax PLRs Grantor created an irrevocable trust for the benefit of himself and his issue and their issue. A corporate trustee is the sole trustee. During Grantor's lifetime, Trustee must distribute such amounts of net income and principal to Grantor and his issue as directed by the Distribution Committee and/or Grantor. The Distribution Committee is initially composed of Grantor and his sons. The Distribution Committee will cease to exist upon Grantor's death. Trust provides that at all times at least two Eligible Individuals must be members of the Distribution Committee. An Eligible Individual means a member of the class consisting of the adult issue, the parent of a minor issue, and the legal guardian of a minor issue.

49 Payment of Income Tax Gift Tax PLRs , Cont. A vacancy on the Distribution Committee must be filled by the eldest of Grantor's adult issue other than any issue already serving as a member of the Distribution Committee, or if none of Grantor's issue not already serving as a member of the Distribution Committee is an adult, then the legal guardian of the eldest minor issue shall serve, or if such minor issue does not have a legal guardian, then the parent of such minor issue. If at any time fewer than two Eligible Individuals are members of the committee, the Distribution Committee shall be deemed not to exist. Grantor, in a non-fiduciary capacity, may, but shall not be required to, distribute to any one or more of Grantor s issue, such amounts of the principal (including the whole thereof) as Grantor deems advisable to provide for the health, maintenance, support and education of Grantor s issue. Grantor held a testamentary limited power of appointment.

50 Payment of Income Tax Gift Tax PLRs , Cont. Rulings Received: During the period the Distribution Committee is serving, no portion of the items of income, deductions, and credits against tax of Trust shall be included in computing the taxable income, deductions, and credits of Grantor. The contribution of property to Trust by Grantor is not a completed gift subject to federal gift tax. Any distribution of property by the Distribution Committee from Trust to Grantor will not be a completed gift subject to federal gift tax, by any member of the Distribution Committee. Any distribution of property by the Distribution Committee from Trust to any beneficiary of Trust, other than Grantor, will not be a completed gift subject to federal gift tax, by any member of the Distribution Committee. Any distribution of property from Trust to a beneficiary, other than Grantor, will be a completed gift by Grantor. 50

51 Statutory Tax Reduction Opportunities 1. Master Limited Partnerships 2. Qualified Dividends 3. Return of Capital dividends 4. Low-turnover Index funds 5. Buy and Hold blue chip strategies 6. IRC /40 Investments 7. Real Estate & Leveraged Real Estate 8. Real Estate Investment Trusts 9. Life Insurance Strategies 10. Annuity Strategies 51

52 Statutory Tax Reduction Opportunities 11. Charitable Lead Trusts 12. Charitable Remainder Trusts 13. Charitable Remainder Retirement Trusts 14. IRAs, Non-deductible IRAs, Roth IRAs 15. Profit sharing plans 16. Defined Benefit plans 17. Oil & Gas Investments 18. Land investments followed by 1031 exchanges 19. Tax-exempt bonds 20. Wind, biofuel and solar investments 52

53 Required Disclosure Under Circular 230 Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party. For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors.

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Checklist for Individuals Reducing the NIIT

Checklist for Individuals Reducing the NIIT 1. Reducing net investment income (NII) and MAGI General Observations a. Assuming that a taxpayer is subject to the net investment income tax (NIIT) in the first

Checklist for Individuals Reducing the NIIT 1. Reducing net investment income (NII) and MAGI General Observations a. Assuming that a taxpayer is subject to the net investment income tax (NIIT) in the first

Charitable Trusts. Charitable Trusts

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

CHARITABLE GIFTS. A charitable gift has a number of different tax benefits, which benefits differ if the gift is made during life or at death.

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

CHARITABLE GIFTS Charitable Gifts As stated on this website, the current applicable exclusion amount is $5,490,000. This amount will be increased annually for inflation. If an individual dies with an estate

Advanced IRA Planning

Advanced IRA Planning Presented by: Robert S. Keebler, CPA, MST, AEP 420 South Washington Street Green Bay, WI 54301 1 Agenda Tax consequences of large IRAs Roth conversions Life insurance Stretch IRA

Advanced IRA Planning Presented by: Robert S. Keebler, CPA, MST, AEP 420 South Washington Street Green Bay, WI 54301 1 Agenda Tax consequences of large IRAs Roth conversions Life insurance Stretch IRA

Tax-Driven Draw Down Strategies. Presented by Robert S. Keebler, CPA, M.S.T., AEP. 420 South Washington Street Green Bay, WI

Tax-Driven Draw Down Strategies Presented by Robert S. Keebler, CPA, M.S.T., AEP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Bracket Management Overview 2. Taxation of IRA Distributions &

Tax-Driven Draw Down Strategies Presented by Robert S. Keebler, CPA, M.S.T., AEP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Bracket Management Overview 2. Taxation of IRA Distributions &

Understanding CRTs. A Summary of Charitable Remainder Trusts (CRTs) VLC

VLC") Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

Understanding CRTs A Summary of Charitable Remainder Trusts (CRTs) VLC0439-0917 GET READY FOR RETIREMENT If your retirement planning objectives include lifetime income planning, estate tax reduction, 1

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Planning Opportunities in Light of ATRA 2012: What Do We Do Now?

Planning Opportunities in Light of ATRA 2012: What Do We Do Now? Robert S. Keebler, CPA, MST, AEP E-mail: robert.keebler@keeblerandassociates.com Circular 230 Disclosure: To ensure compliance with requirements

Planning Opportunities in Light of ATRA 2012: What Do We Do Now? Robert S. Keebler, CPA, MST, AEP E-mail: robert.keebler@keeblerandassociates.com Circular 230 Disclosure: To ensure compliance with requirements

Charitable remainder trusts and life insurance

Life insurance Allianz Life Insurance Company of North America Charitable remainder trusts and life insurance (R-3/2018) Estate planning with highly appreciated assets When designed properly, a trust can

Life insurance Allianz Life Insurance Company of North America Charitable remainder trusts and life insurance (R-3/2018) Estate planning with highly appreciated assets When designed properly, a trust can

Life Income Gifts 4/19/2016. How a Life Income Gift Works. Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation

Life Income Gifts Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation How a Life Income Gift Works Gift Donor Life Income Gift Remainder to Charity Income tax deduction

Life Income Gifts Rebecca E. Dupras, Esq. Vice President of Development Silicon Valley Community Foundation How a Life Income Gift Works Gift Donor Life Income Gift Remainder to Charity Income tax deduction

Presented by Richard D. Cirincione 677 Broadway Albany, NY Direct: Fax:

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

Presented by Richard D. Cirincione 677 Broadway Albany, NY 12207 Direct: 518-447-3389 Fax: 518-867-4789 646 Plank Road, Suite 206 Clifton Park, New York 12065 518-383-9200 518-867-4789 facsimile cirincione@mltw.com

Planned Giving. For Beginners

Planned Giving For Beginners What is Planned Giving? The integration of personal, financial and estate planning goals using lifetime or testamentary charitable giving with benefits to the donor ANNUAL

Planned Giving For Beginners What is Planned Giving? The integration of personal, financial and estate planning goals using lifetime or testamentary charitable giving with benefits to the donor ANNUAL

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Four Tier Accounting for Charitable Remainder Trust. Richard C. Capasso, CPA, CFP, PFS

Four Tier Accounting for Charitable Remainder Trust Richard C. Capasso, CPA, CFP, PFS Charitable Remainder Trust Provide an option for dealing with appreciated property to philanthropic donors Trust is

Four Tier Accounting for Charitable Remainder Trust Richard C. Capasso, CPA, CFP, PFS Charitable Remainder Trust Provide an option for dealing with appreciated property to philanthropic donors Trust is

A Guide to Planned Giving

A Guide to Planned Giving ~ Boys & Girls Clubs ~ 2 - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable

A Guide to Planned Giving ~ Boys & Girls Clubs ~ 2 - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014)

") THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

Using Your Assets to Promote your Values. Lawrence M. Lehmann, JD, AEP, CAP Lehmann Norman & Marcus LC

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

Charitable Gifting: Overview and Tax Implications

Charitable Gifting: Overview and Tax Implications Overview The desire to assist a charitable organization must be a primary motive for making a gift; if a charitable inclination does not exist, charitable

Charitable Gifting: Overview and Tax Implications Overview The desire to assist a charitable organization must be a primary motive for making a gift; if a charitable inclination does not exist, charitable

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives. 41st Annual MPGC Conference November 15-16, 2017

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

Issues AND. Tax-Powered Philanthropy: Doing well by doing good

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

2016 Charitable Giving Review

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Charitable Gifting: Overview and Tax Implications. Overview. Tax Implications - Charitable Deduction Rules

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

Charitable Giving Techniques

Life Event Services Estate Planning Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving,

Life Event Services Estate Planning Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving,

Charitable Remainder Trusts

Charitable Remainder Trusts LIFE INCOME GIFTS In the simplest terms, a life income gift is a plan that allows a donor to make a contribution to charity and receive an income in return. Depending upon the

Charitable Remainder Trusts LIFE INCOME GIFTS In the simplest terms, a life income gift is a plan that allows a donor to make a contribution to charity and receive an income in return. Depending upon the

2016 Tax Preparation Checklist. Documentation for Itemized Deductions

Essentials for Taxpayers For 2016 Federal Returns Due in April 2017 2016 Tax Preparation Checklist n Copy of 2015 tax return n Social Security number(s) taxpayers and dependents n W-2 forms from all employers

Essentials for Taxpayers For 2016 Federal Returns Due in April 2017 2016 Tax Preparation Checklist n Copy of 2015 tax return n Social Security number(s) taxpayers and dependents n W-2 forms from all employers

NWPGRT AllianceBernstein

September 2014 Steve S. Schilling, CFA Director Wealth Management Research Bernstein Global Wealth Management 555 California Street San Francisco, CA 94104 Tel: (415) 217-8037 SchillingSS@Bernstein.com

September 2014 Steve S. Schilling, CFA Director Wealth Management Research Bernstein Global Wealth Management 555 California Street San Francisco, CA 94104 Tel: (415) 217-8037 SchillingSS@Bernstein.com

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Estate planning for non-citizens.

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

Kingdom Advisors Charitable Giving Tool Kit

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

Thursday, September WRM# 14-35

Thursday, September 4 2014 WRM# 14-35 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms.

Thursday, September 4 2014 WRM# 14-35 The WRMarketplace is created exclusively for AALU Members by the AALU staff and Greenberg Traurig, one of the nation s leading tax and wealth management law firms.

JMX1059CEPPT 08/17 05/13

This presentation is meant to provide education on the content being presented and is intended for financial industry professionals. It is not intended for use with the general public. Firm and state variations

This presentation is meant to provide education on the content being presented and is intended for financial industry professionals. It is not intended for use with the general public. Firm and state variations

Charitable Giving Techniques

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Charitable Remainder Unitrust. Planned Charitable Giving Using a Split-Interest Trust

Charitable Remainder Unitrust Planned Charitable Giving Using a Split-Interest Trust CRUT Overview Lifetime transfer of cash or property in trust in exchange for unitrust interest payable over (a) Fixed

Charitable Remainder Unitrust Planned Charitable Giving Using a Split-Interest Trust CRUT Overview Lifetime transfer of cash or property in trust in exchange for unitrust interest payable over (a) Fixed

Tax Planning Considerations for 2015

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Charitable Giving Techniques

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

WEALTH STRATEGY REPORT

WEALTH STRATEGY REPORT The 3.8% Surtax on Investment Income - Trusts INTRODUCTION Beginning in 2013, net investment income (NII, as defined in the statute) is subject to an additional 3.8% surtax to the

WEALTH STRATEGY REPORT The 3.8% Surtax on Investment Income - Trusts INTRODUCTION Beginning in 2013, net investment income (NII, as defined in the statute) is subject to an additional 3.8% surtax to the

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

Presenting a live 90-minute webinar with interactive Q&A NING and DING Trusts in Estate Planning: Designing ING Trusts to Avoid State Income Tax and Protect Assets Effective Drafting of Incomplete Gift

Leaving a Legacy. Your Guide to Charitable Giving

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

Individual year-end planning and tax law updates

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

2013 TAX AND FINANCIAL PLANNING TABLES. An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning.

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

2013 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2013 tax planning. WHAT YOU WILL SEE IN THIS BROCHURE 2013 Income Tax Changes Tax Rates

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA Tel: (310) Fax: (310)

Fax: (310)") Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

HELD BUSINESS INTERESTS

PLANNED GIVING WITH CLOSELY HELD BUSINESS INTERESTS Gregory S. Williams, Esq. Carruthers & Roth, P.A. Phone: 336-478-1183 E-mail: gsw@crlaw.com Disclaimer The contents of this presentation have been prepared

PLANNED GIVING WITH CLOSELY HELD BUSINESS INTERESTS Gregory S. Williams, Esq. Carruthers & Roth, P.A. Phone: 336-478-1183 E-mail: gsw@crlaw.com Disclaimer The contents of this presentation have been prepared

Estate Planning for IRAs & Qualified Plans

Estate Planning for IRAs & Qualified Plans Presented by Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP All Rights Reserved 1 Outline Foundation Concepts 401(a)(9) Regulations Estate Planning

Estate Planning for IRAs & Qualified Plans Presented by Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP All Rights Reserved 1 Outline Foundation Concepts 401(a)(9) Regulations Estate Planning

e-pocket TAX TABLES 2014 and 2015 Quick Links:

e-pocket TAX TABLES 2014 and 2015 Quick Links: 2014 Income and Payroll Tax Rates 2015 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2014 and 2015 Quick Links: 2014 Income and Payroll Tax Rates 2015 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

The top federal income tax rate has increased from 35% to 39.6%. All other federal income tax rates are the same as they were in 2012.

Gift Planning and the New Tax Law PG Calc Featured Article, February 2013 http://www.pgcalc.com/about/featured-article-february-2013.htm The American Taxpayer Relief Act (ATRA) passed by Congress on January

Gift Planning and the New Tax Law PG Calc Featured Article, February 2013 http://www.pgcalc.com/about/featured-article-february-2013.htm The American Taxpayer Relief Act (ATRA) passed by Congress on January

Beat the estate tax blow: with deferred annuities and an irrevocable trust

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

2017 INCOME AND PAYROLL TAX RATES

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

Post-Election Proactive Year-End Tax and Financial Planning Opportunities

Post-Election Proactive Year-End Tax and Financial Planning Opportunities Presented by: Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates LLP Robert.Keebler@KeeblerandAssociates.com Earn CPE #AICPApfp

Post-Election Proactive Year-End Tax and Financial Planning Opportunities Presented by: Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates LLP Robert.Keebler@KeeblerandAssociates.com Earn CPE #AICPApfp

THE ESTATE PLANNER S SIX PACK

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Charitable Lead Trusts in the New Tax Landscape

Charitable Lead Trusts in the New Tax Landscape Northern California Planned Giving Planned Giving Conference May 4, 2018 Vivian U. Redsar, Esq. Manatt, Phelps & Phillips, LLP Sarah Copeland Jordan Park

Charitable Lead Trusts in the New Tax Landscape Northern California Planned Giving Planned Giving Conference May 4, 2018 Vivian U. Redsar, Esq. Manatt, Phelps & Phillips, LLP Sarah Copeland Jordan Park

Your Questions Answered: Charitable Tax Planning with Retirement Funds

1/5 Puccini s Madama Butterfly Your Questions Answered: Charitable Tax Planning with Retirement Funds Here are some common questions we get asked when it comes to tax planning with retirement funds: How

1/5 Puccini s Madama Butterfly Your Questions Answered: Charitable Tax Planning with Retirement Funds Here are some common questions we get asked when it comes to tax planning with retirement funds: How

Estate Planning Strategies for the Business Owner

National Life Group is a trade name of of National Life Insurance Company, Montpelier, VT and its affiliates. TC74345(0613)1 Estate Planning Strategies for the Business Owner Presented by: Connie Dello

National Life Group is a trade name of of National Life Insurance Company, Montpelier, VT and its affiliates. TC74345(0613)1 Estate Planning Strategies for the Business Owner Presented by: Connie Dello

ALI-ABA Course of Study Estate Planning for the Family Business Owner

425 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

425 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

Charitable Remainder Annuity Trust. Planned Charitable Giving Using a Split-Interest Trust

Charitable Remainder Annuity Trust Planned Charitable Giving Using a Split-Interest Trust CRAT Overview Lifetime transfer of cash or property in trust in exchange for annuity interest payable over (a)

Charitable Remainder Annuity Trust Planned Charitable Giving Using a Split-Interest Trust CRAT Overview Lifetime transfer of cash or property in trust in exchange for annuity interest payable over (a)

Building Charitable Trusts Into A Client s Estate, Tax And Family Planning

Building Charitable Trusts Into A Client s Estate, Tax And Family Planning Publication: Practising Law Institute Introduction Charitable giving has become a significant consideration in the tax and estate

Building Charitable Trusts Into A Client s Estate, Tax And Family Planning Publication: Practising Law Institute Introduction Charitable giving has become a significant consideration in the tax and estate

How the 3.8% Medicare Surtax Affects Charitable Giving

How the 3.8% Medicare Surtax Affects Charitable Giving September 26, 2013 Jeremiah W. Doyle, IV Senior Vice President jere.doyle@bnymellon.com Agenda Background Net Investment Income (NII) Charitable Remainder

How the 3.8% Medicare Surtax Affects Charitable Giving September 26, 2013 Jeremiah W. Doyle, IV Senior Vice President jere.doyle@bnymellon.com Agenda Background Net Investment Income (NII) Charitable Remainder

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2017 and 2018 Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

DrawDown & Portfolio Strategies

DrawDown & Portfolio Strategies Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Tax Reform Overview for Investors 2 Individual Rates Standard Deduction Personal Exemptions Child/Family Credit

DrawDown & Portfolio Strategies Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Tax Reform Overview for Investors 2 Individual Rates Standard Deduction Personal Exemptions Child/Family Credit

Multigenerational Retirement Distribution Planning. Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs

Multigenerational Retirement Distribution Planning Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs Overview Qualified plans, IRAs and other tax-deferred plans often constitute

Multigenerational Retirement Distribution Planning Maximizing the Family Wealth Planning Benefits of Qualified Plans and IRAs Overview Qualified plans, IRAs and other tax-deferred plans often constitute

Planned Giving. Your Questions Answered: Charitable Tax Planning with Retirement Funds. An Investment in Cape Cod s Future 1/5

1/5 Planned Giving An Investment in Cape Cod s Future Your Questions Answered: Charitable Tax Planning with Retirement Funds Here are some common questions we get asked when it comes to tax planning with

1/5 Planned Giving An Investment in Cape Cod s Future Your Questions Answered: Charitable Tax Planning with Retirement Funds Here are some common questions we get asked when it comes to tax planning with

Double Discounted Transfers

Advanced Markets planning perspective estate planning Double Discounted Transfers The Silver Lining After the Economic Downturn It seems clear that estate taxes are here to stay. For people who are likely

Advanced Markets planning perspective estate planning Double Discounted Transfers The Silver Lining After the Economic Downturn It seems clear that estate taxes are here to stay. For people who are likely

Mastering Complex Giving. Tips & Strategies on Using Charitable Planning for Enhancing your Practice

Mastering Complex Giving Tips & Strategies on Using Charitable Planning for Enhancing your Practice The Leading Independent Donor Advised Fund Choice Since 1993 Table of Contents For many advisors, discussing

Mastering Complex Giving Tips & Strategies on Using Charitable Planning for Enhancing your Practice The Leading Independent Donor Advised Fund Choice Since 1993 Table of Contents For many advisors, discussing

A Guide to Planned Giving

A Guide to Planned Giving 2 Dear Friend, Are you looking for ways to save on your taxes this year through charitable giving? Would you like to avoid capital gains tax on the sale of your appreciated assets?

A Guide to Planned Giving 2 Dear Friend, Are you looking for ways to save on your taxes this year through charitable giving? Would you like to avoid capital gains tax on the sale of your appreciated assets?

2018 TAX AND FINANCIAL PLANNING TABLES

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

Business Interests: Planning Considerations

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

Pointers in Selecting Assets to Fund Charitable Trusts

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

Pointers in Selecting Assets to Fund Charitable Trusts Publication: Estate Planning Magazine Charitable trusts will continue to be an important part of the thoughtful estate planner's repertoire in our

Charitable Remainder Annuity Trust Presentation Input Screen

Charitable Remainder Annuity Trust Presentation Input Screen Annuity Trust Questions Gift Asset Questions Case Name ----- NEW CASE ----- Gift Asset Type Cash Name for Reports Betty Anthropist Value of

Charitable Remainder Annuity Trust Presentation Input Screen Annuity Trust Questions Gift Asset Questions Case Name ----- NEW CASE ----- Gift Asset Type Cash Name for Reports Betty Anthropist Value of

Charitable Planned Giving Strategies

Charitable Planned Giving Strategies Courtesy of: Yellowstone Boys & Girls Ranch Foundation, Inc. This presentation was prepared for educational purposes only. It must not be used as a basis for tax or

Charitable Planned Giving Strategies Courtesy of: Yellowstone Boys & Girls Ranch Foundation, Inc. This presentation was prepared for educational purposes only. It must not be used as a basis for tax or

Planned Giving. A Philanthropist s Guide to Federal Taxes The Most Flexible Tax-Saving Tool: The Charitable Deduction

1/7 Planned Giving An Investment in Cape Cod s Future A Philanthropist s Guide to Federal Taxes 2018 The Most Flexible Tax-Saving Tool: The Charitable Deduction A distinguishing characteristic of American

1/7 Planned Giving An Investment in Cape Cod s Future A Philanthropist s Guide to Federal Taxes 2018 The Most Flexible Tax-Saving Tool: The Charitable Deduction A distinguishing characteristic of American

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ Fax

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Strategies for Reducing Wealth and Transfer Taxes. By, Pattie S. Christensen, Esq

Strategies for Reducing Wealth and Transfer Taxes By, Pattie S. Christensen, Esq A. Lifetime Gifts The current gift tax program permits a person to transfer up to $13,000 worth of gifts of a present interest

Strategies for Reducing Wealth and Transfer Taxes By, Pattie S. Christensen, Esq A. Lifetime Gifts The current gift tax program permits a person to transfer up to $13,000 worth of gifts of a present interest

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

Understanding TRUSTS. A Summary of Trusts for Estate Planning VLC

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Year-End Tax Planning Summary December 2015

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

Year-End Tax Planning Summary December 2015 Overview Thanks to the continued political gridlock in Washington, 2015 did not see comprehensive tax reform. However, on December 18th, Congress passed the

GIFT AND ESTATE TAX PLANNING GUIDE

I. Tax Free Annual Exclusion Gifts - No Reporting Required, Per Donee Per Donor A. See Reference Chart below which illustrates amounts that can be gifted tax free annually: Number of Grandparents/Parents

I. Tax Free Annual Exclusion Gifts - No Reporting Required, Per Donee Per Donor A. See Reference Chart below which illustrates amounts that can be gifted tax free annually: Number of Grandparents/Parents

e-pocket TAX TABLES Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax

e-pocket TAX TABLES Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security Benefits Personal

e-pocket TAX TABLES Quick Links: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security Benefits Personal

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Personal Trust Services

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

2018 Year-End Tax Reminders

2018 Year-End Tax Reminders Family Office Resources Income Tax Beginning in 2018, the standard deduction for single filers is $12,000 (up from $6,500 in 2017) and $24,000 for married taxpayers who file

2018 Year-End Tax Reminders Family Office Resources Income Tax Beginning in 2018, the standard deduction for single filers is $12,000 (up from $6,500 in 2017) and $24,000 for married taxpayers who file

Tax Planning with Qualified Charitable Distributions

Tax Planning with Qualified Charitable Distributions Understand how to benefit from this tax-saving tool GIVING WITH GREATER BENEFITS Are you age 70 1/2 or higher and subject to required minimum distributions

Tax Planning with Qualified Charitable Distributions Understand how to benefit from this tax-saving tool GIVING WITH GREATER BENEFITS Are you age 70 1/2 or higher and subject to required minimum distributions

Preserving and Transferring IRA Assets

Preserving and Transferring IRA Assets september 2017 The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth potential,

Preserving and Transferring IRA Assets september 2017 The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth potential,

Year-End Tax Moves for Income Tax Rates for 2015

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Tax Bulletin: 2017 Year-End Tax Planning Considerations

Tax Bulletin: 2017 Year-End Tax Planning Considerations PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services On December 2, 2017, the full Senate passed its amended version of the Tax Cuts and

Tax Bulletin: 2017 Year-End Tax Planning Considerations PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services On December 2, 2017, the full Senate passed its amended version of the Tax Cuts and

Giving is a part of life. Charitable Giving With Life Insurance

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

e-pocket TAX TABLES 2016 and 2017 Quick Links: 2016 Income and Payroll Tax Rates 2017 Income and Payroll Tax Rates

e-pocket TAX TABLES 2016 and 2017 Quick Links: 2016 Income and Payroll Tax Rates 2017 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

e-pocket TAX TABLES 2016 and 2017 Quick Links: 2016 Income and Payroll Tax Rates 2017 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum Tax Kiddie Tax Income Taxation of Social Security

Sales to an Employee Stock Ownership Plan

Sales to an Employee Stock Ownership Plan Wealth Planning 2017 General There are a number of ways for a business owner to convert a concentrated, illiquid equity position into a diversified portfolio,

Sales to an Employee Stock Ownership Plan Wealth Planning 2017 General There are a number of ways for a business owner to convert a concentrated, illiquid equity position into a diversified portfolio,

CHARITABLE REMAINDER ANNUITY TRUST VS. UNITRUST. Presented for Valued Client

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 7 The Concept A charitable remainder trust is a split-interest

Presented for Valued Client Presented by John M. Webster HMS Insurance Associates, Inc. johnwebster@financialguide.com 443-632-3436 Page 1 of 7 The Concept A charitable remainder trust is a split-interest

FINANCIAL PROFESSIONAL USE ONLY NOT FOR USE WITH THE PUBLIC

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the