MENTOR PROGRAM. The Circle of Wealth System Client Process. (321)

|

|

|

- Bathsheba Wilkins

- 5 years ago

- Views:

Transcription

1 The Circle of Wealth System Client Process MENTOR PROGRAM SESSION 3 Workbook We are in a belief changing business. Two things will differentiate you from other advisors - what you know & what you can communicate. Every agent has product but not every agent has something to say the client wants to hear. We are dedicated to providing you with the tools to effectively communicate financial solutions. (321)

2 Table of Contents Mentor Session 3 Workbook Objective & Study Guide... 3 Tax Master: Compound Interest The Dark Side!... 6 Tax Master: CIT 6 Screens At-A-Glance... 7 Tax Master: CIT Script Outline... 8 Tax Master: CIT Don s Dialog Tax Master: IFR 12 Screens At-A-Glance Tax Master: IFR Script Outline Tax Master: IFR Script Outline Tax Master: IFR Don s Dialog Tax Master: BTID 11 Screens At-A-Glance Tax Master: BTID Script Outline Tax Master: BTID Investment Account Don s Dialog Tax Master: BTID Life Style Account Don s Dialog Qualified Plans 8 Screens At-A-Glance Qualified Plans Script Outline Qualified Plans Don s Dialog Qualified Plan Bombs CD Bombs Step 8: Discuss Client Ideas Step 9: Life Insurance & Other Products Private Reserve Strategy 17 Screens At-A-Glance Private Reserve Strategy Script Outline Private Reserve Strategy Three Legged Stool 9 Screens At-A-Glance Three Legged Stool Script Outline Three Legged Stool Minute Lesson on Life Insurance 1 Screen (34 Reveals) Minute Lesson on Life Insurance Script Outline Understanding Policy Loans 1 Screen Understanding Policy Loans Script Outline Mentor Session 3 Workbook Revision Date:

3 Objectives & Study Guide Objective(s) to be covered during September 16 Group Coaching Call at 11:30 a.m. Eastern Tax Master: CIT be clear on the purpose and use of Tax Master: CIT presentation in Step 7 being able to demonstrate with clients Tax Master: BTID be clear on the purpose and use of Tax Master: BTID presentation in Step 7 being able to demonstrate with clients Study Guide: Complete lesson 7 s Tax Master section videos CIT & BTID in Circle of Wealth 10-Step Client Process o Available on the members website: Memorize the CIT screens and dialog; present to study group Memorize the BTID screens and dialog; present to study group Watch marketing vignette videos listed below. o Available on the members website: o VVCOW12 Standing In the Tax Line Listen to COW Tales: 22 24, 92 o Available on the members website: Objective(s) to be covered during September 30 Group Coaching Call at 11:30 a.m. Eastern Tax Master: IFR be clear on the purpose and use of Tax Master: IFR presentation in Step 7 being able to demonstrate with clients Taxable Account a Different View Study Guide: Complete lesson 7 s Tax Master section video IFR in Circle of Wealth 10-Step Client Process o Available on the members website: Memorize the IFR screens and dialog; present to study group Listen to COW Tales: 33-34, 50-51, 125, 130 o Available on the members website: Review final practice exam questions Mentor Session 3 Workbook Revision Date:

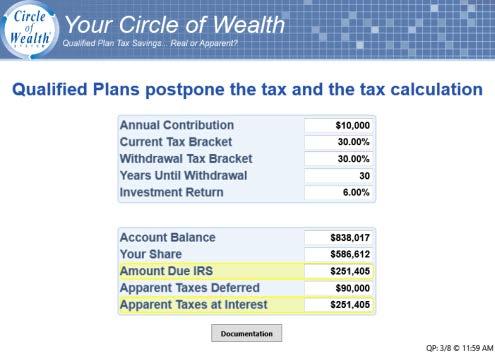

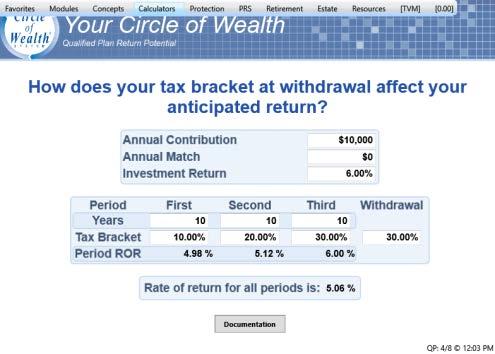

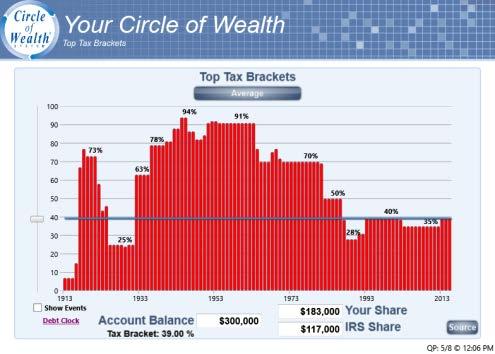

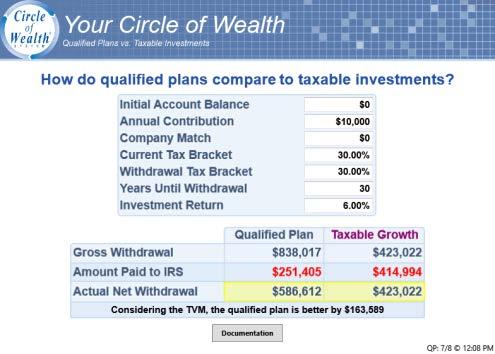

4 Objective(s) to be covered during October 14 Group Coaching Call at 11:30 a.m. Eastern Qualified Plans & Taxes be clear on the purpose and use of Qualified Plans presentation in Step 7 being able to demonstrate with clients Review Final Exam Practice Questions Study Guide: Complete lesson 7 s Tax Master section video Qualified Plans in Circle of Wealth 10- Step Client Process o Available on the members website: On Screen 2 of Qualified Plans, answer the quiz and then explain your rationale behind each answer to your study group. Review all of the applications associated with Qualified Plans: o Pay Off Debt or Contribute to QP? o Qualified Plan Company Match o Qualified Plan Fundamentals o QP Do 2 Things o QP Questions to Ask o QP Return Potential o QP vs. Taxable Investment o Tax Deferred vs. Tax Favored o Types of Qualified Plans Memorize the Qualified Plans screens and dialog; present to study group Watch the on-screen video tutorials for Tax History, Tax Threshold and Government Intervention presentations/screens. Watch marketing vignette videos listed below. o Available on the members website: o VVPEM17 The Tax Filter o VVPEM20 Qualified Plan Contributions o VVCOW05 Qualified Plans Do Two Things o VVCOW10 You May Not Be Saving Taxes o VVCOW18 Average Rate of Return vs. Real Return Listen to COW Tales: 28 30, 48 49, 60, 108, 127 o Available on the members website: Review final practice exam questions Crystal or your group master requests for any areas you need to revisit for next session. Mentor Session 3 Workbook Revision Date:

5 Objective(s) to be covered during October 28 Group Coaching Call at 11:30 a.m. Eastern Self Assessment Review Areas of Need Bases on Survey Response Review Final Exam Practice Questions Study Guide: Review final practice exam questions Objective(s) to be covered during November 4 Group Coaching Call at 11:30 a.m. Eastern High Net Worth Clients and COW Retirement Income Alternatives Review Final Exam Study Guide: Review 10Q, 10 Steps, RRON, CP, CQ, MM, TM, PRS, PEM, QP Mentor Session 3 Workbook Revision Date:

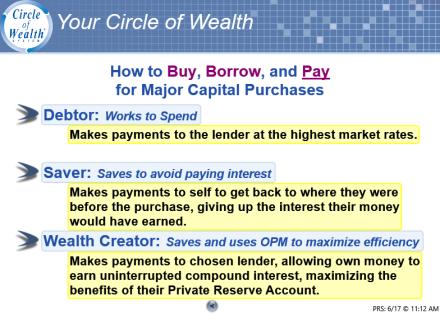

6 Tax Master: Compound Interest The Dark Side! The Tax Master module provides three major discussions regarding compounding investments in a taxable environment. CIT Presentation = Compound Interest Tutorial BTID Presentation = Buy Term Invest the Difference IFR Presentation = Increase, Flatten or Reduce Mentor Session 3 Workbook Revision Date:

7 Tax Master: CIT 6 Screens At-A-Glance Mentor Session 3 Workbook Revision Date:

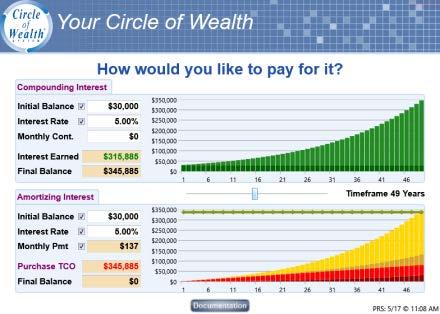

8 Tax Master: CIT Script Outline Intro Comments: o Purpose: CIT Compounding Interest Tutorial. The purpose of this presentation is to show a prospect how much they would need to deposit in a side account upfront to pay all the taxes their taxable investment will create over time. It s a Net Present Value story to grab a prospects attention. o Remember when using this presentation that you are talking about compounding interest in taxable accounts. This should not be used when discussing Qualified Plans since this illustrates taxes that are being paid each year on the interest or earnings growth. You will notice that the presentation builds from one screen to the next. Go slowly and make sure that your prospect is with you every step of the way before moving on to the next point to make sure they fully understand the problem when you are done. 1. Screen 1 a. Let's illustrate the impact that compounding interest can have on your Circle of Wealth. We can use your numbers if you like. b. Advisor notes: This is the initial assumptions input screen. Enter the data and click calculate. You many enter either a lump sum (initial amount), annual contributions, or both. 2. Screen 2 a. Let's go through the years slowly watching the account grow on the left, which represents the money you will have in your account. b. The account on the right represents the taxes, which you must pay in order to maintain the account on the left. c. What is your first reaction to seeing this happening to your account? d. Where are you getting the money to pay the taxes due each year earned on your investment account? (current income or lifestyle) e. If I can show you some opportunities which would allow you to avoid transferring those taxes to the government each year it would have a dramatic impact on your Circle of Wealth. f. This screen is not the whole picture because we have not even considered the opportunity cost. g. Advisor notes: Illustrate the increasing balance of the compounding account along with its associated increasing tax burden. Use the slider to change the displayed values. Often clients focus their attention on the rate of return or amount being earned without any idea of the additional cost to be in these type accounts. Rolling the interest earned each year back into the same account creates an increasing tax liability which can greatly impact the outcome over time. The taxes must be paid each year and usually come from their lifestyle account which can easily be illustrated with the Personal Economic Model. 3. Screen 3 a. This screen is similar to the last screen, but it displays the opportunity cost of the taxes paid. b. Advisor notes: Illustrate that one not only loses the tax, but also everything those tax dollars could have earned if they were not transferred away. If this is the first time you have introduced the concept of Opportunity Cost make sure they get this point. Paying taxes that could be avoided is what we mean by finding money. The tax is Mentor Session 3 Workbook Revision Date:

9 one thing and may not get their full attention but once they understand they are also losing the value of those tax dollars paid they begin to pay closer attention. 4. Screen 4 a. This screen demonstrates the taxes paid, the cumulative taxes paid, and the cumulative taxes paid with opportunity cost. b. Advisor notes: This screen displays the increase in tax liability as the investment grows. Compounding interest in a taxable environment and rolling the interest back in the same account creates an increasing tax liability. The underlying account is not the issue but rather the rolling of the interest earned back in the same account. The more interest the account earns the greater the problem. Unfortunately many are of the misconception that they can make up for the loss with higher returns. This is not true because the taxes paid that could have been avoided must now be calculated at the higher return rate. Since many are paying the taxes due on these accounts from their lifestyle dollars they usually do not even realize there is a problem until their taxes get large enough to impact their lifestyle. By this time they have lost a great deal and those losses can never be recovered. 5. Screen 5 a. This screen calculates the present value of the taxes paid. b. The documentation proves that the lump sum present value of the taxes would be consumed over the time period by the taxes paid. c. Advisor notes: Make sure you client understands that this screen calculates and displays the present value of the taxes paid. That is, it calculates in today s dollars how much you would need to put in a fund which would: 1. Be compounded at the net opportunity investment return. 2. Pay the taxes due at the end of each year. 3. Have a zero balance at the end of the projection. This is a powerful screen which illustrates how much they would have to give to the government on day one of the investment to cover the taxes that they will have to pay from their lifestyle account over the number of years they intend to keep money in this account. Knowing the present value of the future tax stream can bring a different perspective on what is really going on in this account. Remember you have a partner in this investment account which is the government meaning the more interest you earn the greater their cut. Don t forget that you are taking all the risk. 6. Screen 6 a. This screen illustrates graphically the growth of the investment and the consumption of the lump sum (present value of taxes). b. Advisor notes: This screen provides a graphical illustration of the growth of the investment and the decline of the hypothetical present value of tax fund. As the investment grows, it requires more and more taxes be paid from lifestyle. The importance of this screen is to illustrate that the lump sum will be gone by the end of the period. The client would think twice before writing a check like this and give it to the government on the first day they made the investment. The point we want the client to see is that perhaps without even knowing they are going to send the equivalent over time if they continue to compound interest in a taxable account. Mentor Session 3 Workbook Revision Date:

10 Tax Master: CIT Don s Dialog What you should say: Let's illustrate the impact that compounding interest can have on your Circle of Wealth. We can use your numbers if you like. This is the initial assumptions input screen. Enter the data and click calculate. You many enter either a lump sum (initial amount), annual contributions, or both. Transition: Remember when using this tool you are talking about compounding interest in taxable accounts. This should not be used when discussing Qualified Plans since this illustrates taxes that are being paid each year on the interest or earnings growth. You will notice that the presentation builds from one screen to the next. Go slowly and make sure that your prospect is with you every step of the way before moving on to the next point to make sure they fully understand the problem when you are done. Mentor Session 3 Workbook Revision Date:

11 What you should say: Let's go through the years slowly watching the account grow on the left, which represents the money; you have in your account. The account on the right represents the taxes, which you must pay in order to maintain the account on the left. What is your first reaction to seeing this happening to your account? Where are you getting the money to pay the taxes due each year earned on your investment account? (current income or lifestyle) If I can show you some opportunities which would allow you to avoid transferring those taxes to the government each year it would have a dramatic impact on your Circle of Wealth. This screen is not the whole picture because we have not even considered the opportunity cost. Illustrate the increasing balance of the compounding account along with its associated increasing tax burden. Use the slider to change the displayed values. Transition: Often clients focus their attention on the rate of return or amount being earned without any idea of the additional cost to be in these type accounts. Rolling the interest earned each year back into the same account creates an increasing tax liability which can greatly impact the outcome over time. The taxes must be paid each year and usually come from their lifestyle account which can easily be illustrated with the Personal Economic Model. Mentor Session 3 Workbook Revision Date:

12 What you should say: This screen is similar to the last screen, but it displays the opportunity cost of the taxes paid. Illustrate that one not only loses the tax, but also everything those tax dollars could have earned if they were not transferred away. Transition: If this is the first time you have introduced the concept of Opportunity Cost make sure they get this point. Paying taxes that could be avoided is what we mean by finding money. The tax is one thing and may not get their full attention but once they understand they are also losing the value of those tax dollars paid they begin to pay closer attention. Mentor Session 3 Workbook Revision Date:

13 What you should say: This screen demonstrates the taxes paid, the cumulative taxes paid, and the cumulative taxes paid with opportunity cost. This screen displays the increase in tax liability as the investment grows. Transition: Compounding interest in a taxable environment and rolling the interest back in the same account creates an increasing tax liability. The underlying account is not the issue but rather the rolling of the interest earned back in the same account. The more interest the account earns the greater the problem. Unfortunately many are of the misconception that they can make up for the loss with higher returns. This is not true because the taxes paid that could have been avoided must now be calculated at the higher return rate. Since many are paying the taxes due on these accounts from their lifestyle dollars they usually do not even realize there is a problem until their taxes get large enough to impact their lifestyle. By this time they have lost a great deal and those losses can never be recovered. Mentor Session 3 Workbook Revision Date:

14 What you should say: This screen calculates the present value of the taxes paid. The documentation proves that the lump sum present value of the taxes would be consumed over the time period by the taxes paid. This screen calculates and displays the present value of the taxes paid. That is, it calculates in today s dollars how much you would need to put in a fund which would: 1. Be compounded at the net opportunity investment return. 2. Pay the taxes due at the end of each year. 3. Have a zero balance at the end of the projection. Transition: This is a powerful screen which illustrates how much they would have to give to the government on day one of the investment to cover the taxes that they will have to pay from their lifestyle account over the number of years they intend to keep money in this account. Knowing the present value of the future tax stream can bring a different perspective on what is really going on in this account. Remember you have a partner in this investment account which is the government meaning the more interest you earn the greater their cut. Don t forget that you are taking all the risk. Mentor Session 3 Workbook Revision Date:

15 What you should say: This screen illustrates graphically the growth of the investment and the consumption of the lump sum (present value of taxes). This screen provides a graphical illustration of the growth of the investment and the decline of the hypothetical present value of tax fund. As the investment grows, it requires more and more taxes be paid from lifestyle. Transition: The importance of this screen is to illustrate that the lump sum will be gone by the end of the period. The client would think twice before writing a check like this and give it to the government on the first day they made the investment. The point we want the client to see is that perhaps without even knowing they are going to send the equivalent over time if they continue to compound interest in a taxable account. Mentor Session 3 Workbook Revision Date:

16 Tax Master: IFR 12 Screens At-A-Glance Mentor Session 3 Workbook Revision Date:

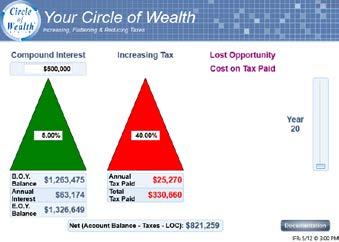

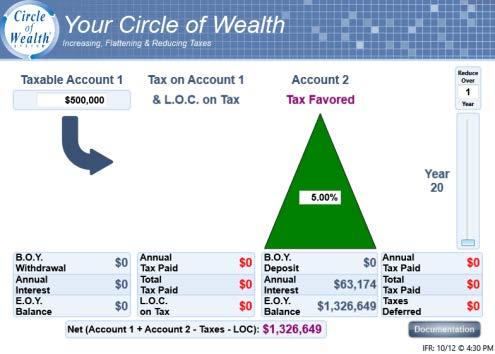

17 Tax Master: IFR Script Outline Intro Comments: o Purpose: IFR it stands for Increase, Flat, Reduce. There are three ways to pay taxes on money that are compounding in a taxable environment. These tools going to give you the chance to illustrate each and every one of those positions to your prospect. o Again, there is no right answer here. It s just helping them understand which would be more efficient than the one they re already doing. 7. Screen 1 a. There are several ways to deal with the taxes due from compounding interest in a taxable investment. b. The first and most obvious would be to move the entire account to a tax favored position. This is not always possible or the most prudent thing to do. c. There are basically three things you can do which we will cover together. d. Advisor notes: You want your client to understand there are three ways to deal with taxes in a taxable investment: 1. Increase taxes (as the investment grows), 2. Flatten taxes, 3. Reduce taxes. Your client is most likely rolling their interest earned each year back in the same account which we call the Increasing Tax position. Once they see the tax issue they will want to explore different alternatives. One would be to move all the money to a tax favored position with the stroke of a pen or over a given period of years which could reduce their taxes. The other option would be to leave the account as is and move only the interest earned which would be the Flat Tax position. Helping your client find the option that best suits their current financial position is the right strategy for the client. None of the options are bad, just some are more tax efficient than others. 8. Screen 2 a. The investment rate of return in Account 1 represents the rate of return you are currently earning on your investment. b. Account 2 is the account, which you may wish to divert some of your dollars to avoid the Compound Interest problem. c. This will become clearer to you as we show you the alternatives available to you. d. Let s put in some assumptions. e. Inputs: current age 60, years of accumulation: 20, initial account balance $500,000, return on taxable account 1: 5%, tax favored account 2: 5% (where the money can grow tax free), opportunity cost: 5%, ordinary tax bracket: 40% and future tax bracket: 40%. Advisor notes: Keep all the percentages the same so you don t get into interest rate conversation. f. Advisor notes: This is an input screen. Since an annual contribution could be diverted directly to another account to solve the tax problems, we will be looking at lump sum contributions from this point on in the program. I like to start this discussion using the same rate of return in the both accounts one and two to avoid getting into risk discussions before the client understands the real issue. Obviously an account with greater returns will outperform another especially if that account is Tax Favored meaning the money in the account grows tax deferred and comes out tax free. 9. Screen 3 a. This is what compounding your money looks like. Mentor Session 3 Workbook Revision Date:

18 b. You start with a lump sum investment and each year your account grows as the interest is paid. c. Most people just roll the interest earned back into the investment account, which continues to add to the compounding effect. d. While the major focus is on the compounding interest, the increasing tax often goes unnoticed. e. Let's look at what I am talking about. f. Advisor notes: Give your client a picture to hang on to of what Compound Interest looks like. No magic here, we are simply showing the future value of the account over time. This is where most focus their attentions with little regard of what we are about to illustrate in the screens to come. Don t forget, you are taking your prospect up the stairs one step at a time and when you are done with your discussion you want them to see things as they really are not what they think they are. 10. Screen 4 a. The government is a silent partner is this account. b. They take no risk but participate in all the profits. c. While you are focusing on the interest, they are counting their returns. d. Your interest is growing but the taxes are growing right along with the growth of your account. e. Advisor notes: The taxes are increasing right along with the compound (increasing) interest. Compound interest creates an increasing tax liability. Taxes do not compound upon themselves. As the account grows so grow the future taxes. Make sure you are using accurate words to describe what is actually going on in these accounts. 11. Screen 5 a. On the left you will notice the account growing at the given interest rate and the taxes growing at the current tax bracket as well. b. The numbers at the bottom of the screen give a year-by-year description of what is happening - illustrating the net account value after the taxes have been paid. c. Remember that most people are paying these tax dollars from their current lifestyle rather than taking the tax due from the investment account. d. Advisor notes: You want your client to understand that they are not only losing money in taxes but they are also losing the money on the tax dollars could have earned had they not had to pay the tax. This is a powerful screen and sets the stage for the rest of your conversation so it is important that you viewer understands first the taxes they will pay from their current lifestyle and then the opportunity cost of what those dollars could be worth to them if they chose another alternative. 12. Screen 6 a. One might say, "What if I just moved it all? Wouldn't that be best?" b. Well, it may or may not be possible or prudent to move the entire lump sum into a tax favored account with the stroke of a pen, but if it was done, it may look something like this. c. Since all the growth is generated within the tax favored account, there would be no annual tax requirement to be paid from lifestyle. d. Instead the tax would be deferred until such time that the growth was actually pulled from the account and used. e. Advisor notes: It is possible, but not always prudent, to immediately move an entire taxable investment into a tax favored account. They have seen the problem and Mentor Session 3 Workbook Revision Date:

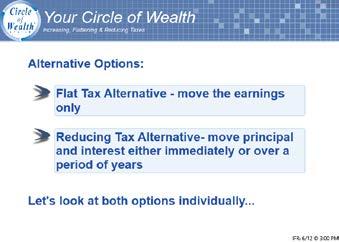

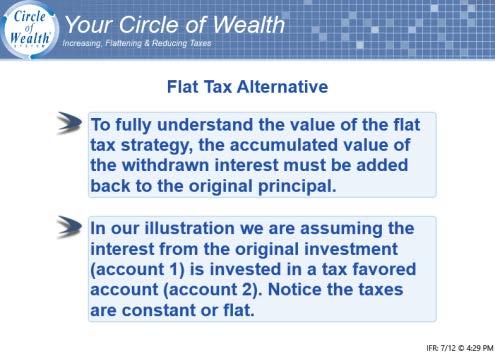

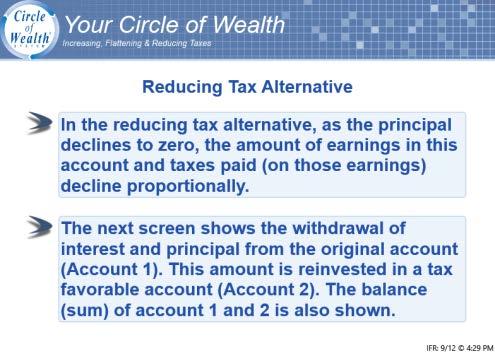

19 now they want to solve it. If they are not moved enough to solve this problem they either do not fully understand what you have been saying or they are not interested in saving taxes. If I could should a few alternatives that are legal which may help you reduce or eliminate the taxes you are currently paying as well as future taxes you will have to pay, would you like to take a look at a few of those options? 13. Screen 7 a. Since you are removing the interest earned each year, you can then put those dollars in an investment account which is tax deferred or tax favored. b. This position assumes that you like the investment you are currently in, but are not in favor of the growing tax liability caused by compounding the interest in the same account. c. Advisor notes: Interest earned each year is removed from the principal investment and invested is a tax favorable position. You must not forget that clients who have a great deal of money in these accounts are usually not interested in moving all their money to a different account even if the risk level is the same or even less. They have worked long and hard to get the money in the account and believe that compound interest is somehow magical. Once they see the tax liability clearly they will be looking for options. Perhaps the easiest to understand is the Flat Tax strategy which leaves their original investment alone and removes only the earnings each year to compound in a tax favored account thus creating a flat tax. 14. Screen 8 a. Account 1 (the taxable account) is level or constant which in turn levels or flattens the taxes due each year. b. The interest earned is then moved to account 2 where it can grow in a tax-favored environment. c. Advisor notes: Illustrate the principal in account 1 remains constant. Illustrate the taxes generated from account 1 remain constant. Illustrate the interest removed from account 1 each year growing in a tax-favored position. Although this screen looks busy it will be up to you to point out exactly what your prospect is seeing. Focus first on the left side. After you get through scrolling through the years illustrating the tax issues then click on account 2 and show what those tax dollars could do first if they were saved and invested in a deferred account. Then click on Deferred and illustrate the outcome if they put the money in a tax favored account. Click on the Net in purple at the bottom of the screen and it will pop up a window to show the differences between each of the strategies. d. Click on the Net (Account 1 + Account 2 Taxes LOC): purple dollar amount. e. This shows the difference between what you are doing currently in compound interest account vs. what may be possible by flattening the taxes and investing those dollars in a tax deferred or tax favored account. f. Advisor notes: There is a considerable difference in taxes between these two positions. Give your prospect an opportunity to ponder this difference and ask for their thoughts. 15. Screen 9 a. Since you are removing principal as well as the interest earned each year, the interest earnings are less and less each year. b. Since the annual interest earned is the taxable portion- the taxes are reduced. c. The next screen will illustrate the effect of repositioning the principal over time. Mentor Session 3 Workbook Revision Date:

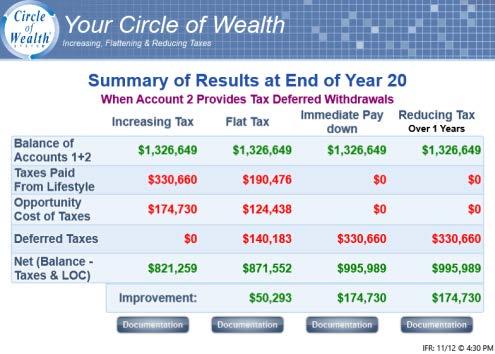

20 d. Advisor notes: Taxes decline as the principal declines because there is less taxable interest earned. Moving all the money to another account in a lump sum is in effect a reducing account but remember that few will wish to move the entire account with the stroke of a pen. More likely you will be able to help your prospect find an amount suitable to their desires. 16. Screen 10 a. Here you can see the results of the reducing tax strategy. b. If we accelerate the amount of the annual withdrawal, we can even further reduce the current tax liability. c. Advisor notes: Illustrate what happens year-by-year as the principal account is reduced. Illustrate the effects of the pay down by accelerating the reduction. Use this to illustrate first what the results would be to move it all at once then move on quickly to the other options they should consider before making a decision. The purpose of the conversation is not to sell them something but rather to help them find what is best in their situation. There is no wrong strategy. Some are more efficient than others but ones present position and personal desires may over ride what you think is best. d. Click OK e. Let s look at the results if you moved all the money to first a tax deferred account and then to a tax favored position. f. Advisor notes: Moving all the money may be the most tax efficient but we want to help them find the strategy that best suits what they want. We are not telling the client what they should do but rather giving them options to consider to determine the best strategy they have available. g. Click on purple text: Tax Deferred to change to a Tax Favored account h. Now let s look at the Tax Favored. i. This is the most tax efficient but there are other things you need to consider. j. The chief concern would be access to capital. k. Advisor notes: Show your prospect that you are concern about them and their interest. If your prospect wants to move it all, stop talking and start talking about where you would suggest them put them money. 17. Screen 11 a. You will notice that all four positions have the same account values on the top. b. The thing to consider is how much it cost to get there. It is obvious that there is a great deal of wealth, which can be recaptured by avoiding the Compound Interest position. Remember compound interest is not the problem, its increasing tax. Since most people try to pay these taxes from their lifestyle, it can have a dramatic effect if these taxes can be avoided. The best thing to note here is that these changes can be made without incurring any additional expense. There are really two things we can do to avoid paying increasing tax on the Compound Interest besides changing the investment altogether. One would be to flatten the tax as we have discussed. Second would be to create a reducing tax position by removing not only the interest but some of the principal as well over time. These two alternatives have a little different philosophy from each other, which should be addressed. c. The flat tax position basically says that I like the investment vehicle I am in currently; I am just not fond of paying taxes. I am satisfied with the amount of risk and the rate of return I am earning and wish not to change my investment. I understand that I do Mentor Session 3 Workbook Revision Date:

21 not want to continue to compound my interest because of tax and wish to remove the interest earned each year, pay the tax, and find another place to park the remaining interest where I can compound my interest in a tax favorable environment. Many are in this position when they retire because they begin living off the interest, which is taxable (unless it is in a Roth IRA or other tax favored account already). Since their account is not getting larger from rolling the interest back over each year, the tax is now flattened. Unfortunately, they may have been able to have more for their retirement had they not compounded their tax burden through their saving years. The reducing tax position varies only slightly. This stance says I am not really that fond of the investment I am in currently, but for several reasons, I am not willing to move the entire lump sum today. I would feel more comfortable moving all the interest earned each year along with some of the principal because of the tax advantages. d. Advisor notes: you want your prospects to see that you are knowledgeable and that you do focus on the process rather than the product. Let your prospect decide which strategy they want. e. Click on documentation f. Anytime you want to see the documentation just let me know. g. Advisor notes: showing the documentation proves there are no smoke and mirrors; however, make sure you understand and have looked at each documentation screen before your prospect asks you to see it and explain. 18. Screen 12 a. What did we learn? b. Compounding interest in a taxable environment creates increasing tax liability c. You can minimize that loss by flattening the taxes simply by moving the earnings from that account to a separate account where the money can grow in a tax favored basis d. Then finally, you can reduce the tax liability overtime by taking principle and interest from the account and moving that to a tax favored position. Mentor Session 3 Workbook Revision Date:

22 Tax Master: IFR Don s Dialog What you should say: There are several ways to deal with the taxes due from compounding interest in a taxable investment. The first and most obvious would be to move the entire account to a tax favored position. This is not always possible or the most prudent thing to do. There are basically three things you can do which we will cover together. There are three ways to deal with taxes in a taxable investment. 1. Increase taxes (as the investment grows) 2. Flatten taxes 3. Reduce taxes Transition: Your client is most likely rolling their interest earned each year back in the same account which we call the Increasing Tax position. Once they see the tax issue they will want to explore different alternatives. One would be to move all the money to a tax favored position with the stroke of a pen or over a given period of years which could reduce their taxes. The other option would be to leave the account as is and move only the interest earned which would be the Flat Tax position. Helping your client find the option that best suits their current financial position is the right strategy for the client. None of the options are bad, just some are more tax efficient than others. Mentor Session 3 Workbook Revision Date:

23 What you should say: The investment rate of return in Account 1 represents the rate of return you are currently earning on your investment. Account 2 is the account, which you may wish to divert some of your dollars to avoid the Compound Interest problem. This will become clearer to you as we show you the alternatives available to you. This is an input screen. Since an annual contribution could be diverted directly to another account to solve the tax problems, we will be looking at lump sum contributions from this point on in the program. Transition: I like to start this discussion using the same rate of return in the both accounts one and two to avoid getting into risk discussions before the client understands the real issue. Obviously an account with greater returns will outperform another especially if that account is Tax Favored meaning the money in the account grows tax deferred and comes out tax free. Mentor Session 3 Workbook Revision Date:

24 What you should say: This is what compounding your money looks like. You start with a lump sum investment and each year your account grows as the interest is paid. Most people just roll the interest earned back into the investment account, which continues to add to the compounding effect. While the major focus is on the compounding interest, the increasing tax often goes unnoticed. Let's look at what I am talking about. Give your client a picture to hang on to of what Compound Interest looks like. Transition: No magic here, we are simply showing the future value of the account over time. This is where most focus their attentions with little regard of what we are about to illustrate in the screens to come. Don t forget, you are taking your prospect up the stairs one step at a time and when you are done with your discussion you want them to see things as they really are not what they think they are. Mentor Session 3 Workbook Revision Date:

interest.")

25 What you should say: The government is a silent partner is this account. They take no risk but participate in all the profits. While you are focusing on the interest, they are counting their returns. Your interest is growing but the taxes are growing right along with the growth of your account. The taxes are increasing right along with the compound (increasing) interest. Transition: Compound interest creates an increasing tax liability. Taxes do not compound upon themselves. As the account grows so grow the future taxes. Make sure you are using accurate words to describe what is actually going on in these accounts. Mentor Session 3 Workbook Revision Date:

26 What you should say: On the left you will notice the account growing at the given interest rate and the taxes growing at the current tax bracket as well. The numbers at the bottom of the screen give a year-by-year description of what is happening - illustrating the net account value after the taxes have been paid. Remember that most people are paying these tax dollars from their current lifestyle rather than taking the tax due from the investment account. I am not only losing money in taxes I am also losing the money those tax dollars could have earned me had I not had to pay the tax. Transition: This is a powerful screen and sets the stage for the rest of your conversation so it is important that you viewer understands first the taxes they will pay from their current lifestyle and then the opportunity cost of what those dollars could be worth to them if they chose another alternative. Mentor Session 3 Workbook Revision Date:

27 What you should say: One might say, "What if I just moved it all? Wouldn't that be best?" Well, it may or may not be possible or prudent to move the entire lump sum into a tax favored account with the stroke of a pen, but if it was done, it may look something like this. Since all the growth is generated within the tax favored account, there would be no annual tax requirement to be paid from lifestyle. Instead the tax would be deferred until such time that the growth was actually pulled from the account and used. It is possible, but not always prudent, to immediately move an entire taxable investment into a tax favored account. Transition: They have seen the problem and now they want to solve it. If they are not moved enough to solve this problem they either do not fully understand what you have been saying or they are not interested in saving taxes. If I could should a few alternatives that are legal which may help you reduce or eliminate the taxes you are currently paying as well as future taxes you will have to pay, would you like to take a look at a few of those options? Mentor Session 3 Workbook Revision Date:

28 What you should say: Since you are removing the interest earned each year, you can then put those dollars in an investment account which is tax deferred or tax favored. This position assumes that you like the investment you are currently in, but are not in favor of the growing tax liability caused by compounding the interest in the same account. Interest earned each year is removed from the principal investment and invested is a tax favorable position. Transition: You must not forget that clients who have a great deal of money in these accounts are usually not interested in moving all their money to a different account even if the risk level is the same or even less. They have worked long and hard to get the money in the account and believe that compound interest is somehow magical. Once they see the tax liability clearly they will be looking for options. Perhaps the easiest to understand is the Flat Tax strategy which leaves their original investment alone and removes only the earnings each year to compound in a tax favored account thus creating a flat tax. Mentor Session 3 Workbook Revision Date:

29 What you should say: Account 1 (the taxable account) is level or constant which in turn levels or flattens the taxes due each year. The interest earned is then moved to account 2 where it can grow in a tax-favored environment. Illustrate the principal in account 1 remains constant. Illustrate the taxes generated from account 1 remain constant. Illustrate the interest removed from account 1 each year growing in a taxfavored position. Transition: Although this screen looks busy it will be up to you to point out exactly what your prospect is seeing. Focus first on the left side. After you get through scrolling through the years illustrating the tax issues then click on account 2 and show what those tax dollars could do first if they were saved and invested in a deferred account. Then click on Deferred and illustrate the outcome if they put the money in a tax favored account. Click on the Net in purple at the bottom of the screen and it will pop up a window to show the differences between each of the strategies.. Mentor Session 3 Workbook Revision Date:

30 What you should say: This shows the difference between what you are doing currently in compound interest account vs what may be possible by flattening the taxes and investing those dollars in a tax deferred or tax favored account. There is a considerable difference in taxes between these two positions. Transition: Give your prospect an opportunity to ponder this difference and ask for their thoughts. Mentor Session 3 Workbook Revision Date:

31 What you should say: Since you are removing principal as well as the interest earned each year, the interest earnings are less and less each year. Since the annual interest earned is the taxable portion- the taxes are reduced. The next screen will illustrate the effect of repositioning the principal over time. Taxes decline as the principal declines because there is less taxable interest earned. Transition: Moving all the money to another account in a lump sum is in effect a reducing account but remember that few will wish to move the entire account with the stroke of a pen. More likely you will be able to help your prospect find an amount suitable to their desires. Mentor Session 3 Workbook Revision Date:

32 What you should say: Here you can see the results of the reducing tax strategy. If we accelerate the amount of the annual withdrawal, we can even further reduce the current tax liability. Illustrate what happens year-by-year as the principal account is reduced. Illustrate the effects of the pay down by accelerating the reduction. Transition: Use this to illustrate first what the results would be to move it all at once then move on quickly to the other options they should consider before making a decision. The purpose of the conversation is not to sell them something but rather to help them find what is best in their situation. There is no wrong strategy. Some are more efficient than others but ones present position and personal desires may over ride what you think is best. Mentor Session 3 Workbook Revision Date:

33 What you should say: Let s look at the results if you moved all the money to first a tax deferred account and then to a tax favored position. Moving all the money may be the most tax efficient but we want to help you find the strategy that best suits what you want. Transition: We are not telling the client what they should do but rather giving them options to consider to determine the best strategy they have available. Mentor Session 3 Workbook Revision Date:

34 What you should say: Let s look at the net effect of moving all the money with the stroke of a pen. First the Tax Deferred then the Tax Favored. This is the most tax efficient but there are other things you need to consider. The chief concern would be access to capital. You are concerned about them and their interest. Transition: If your prospect wants to move it all, stop talking and start talking aobut where you would suggest them put them money. Mentor Session 3 Workbook Revision Date:

35 What you should say: You will notice that all four positions have the same account values on the top. The thing to consider is how much it cost to get there. It is obvious that there is a great deal of wealth, which can be recaptured by avoiding the Compound Interest position. Remember compound interest is not the problem, its increasing tax. Since most people try to pay these taxes from their lifestyle, it can have a dramatic effect if these taxes can be avoided. The best thing to note here is that these changes can be made without incurring any additional expense. There are really two things we can do to avoid paying increasing tax on the Compound Interest besides changing the investment altogether. One would be to flatten the tax as we have discussed. Second would be to create a reducing tax position by removing not only the interest but some of the principal as well over time. These two alternatives have a little different philosophy from each other, which should be addressed. The flat tax position basically says that I like the investment vehicle I am in currently; I am just not fond of paying taxes. I am satisfied with the amount of risk and the rate of return I am earning and wish not to change my investment. I understand that I do not want to continue to compound my interest because of tax and wish to remove the interest earned each year, pay the tax, and find another place to park the remaining interest where I can compound my interest in a tax favorable environment. Many are in this position when they retire because they begin living off the interest, which is taxable (unless it is in a Roth IRA or other tax favored account already). Since their account is not getting larger from rolling the interest back over each year, the tax is now flattened. Unfortunately, they may have been able to have more for their retirement had they not compounded their tax burden through their saving years. (continued next page) Mentor Session 3 Workbook Revision Date:

36 The reducing tax position varies only slightly. This stance says I am not really that fond of the investment I am in currently, but for several reasons, I am not willing to move the entire lump sum today. I would feel more comfortable moving all the interest earned each year along with some of the principal because of the tax advantages. You are knowledgeable really do focus on the process rather than product. Transition: Let your prospect decide which strategy they want. Mentor Session 3 Workbook Revision Date:

37 What you should say: Anytime you want to see documentation on any calculation just let me know. No smoke and mirrors Transition: Make sure you understand and have looked at each documentation screen before your prospect asks you to see it and explain. Mentor Session 3 Workbook Revision Date:

38 What you should say: Compound Interest creates the largest wealth transfers. Removing interest from your account each year may reduce your tax liability. Removing interest and principal each year may further reduce your taxes. Transition: Mentor Session 3 Workbook Revision Date:

39 Tax Master: BTID 11 Screens At-A-Glance Mentor Session 3 Workbook Revision Date:

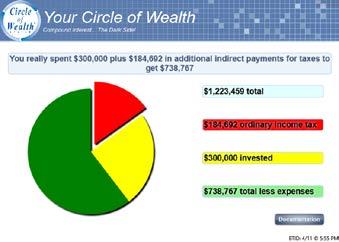

40 Tax Master: BTID Script Outline Intro Comments: Purpose: BTID Buy Term Invest the Difference. Explore (and expose) the often overlooked costs involved with buying term and investing the difference in a taxable scenario. 1. Screen 1: a. Most people are familiar with the rewards of compounding interest, but few are familiar with the tax ramifications associated with interest earned. b. The following discussion is designed to uncover some of these hidden costs. c. Let's enter your data and shine some light on this problem. d. Opportunity Cost may be a term you are not familiar with. e. Basically it represents the interest you could have earned on a given amount had you been able to avoid losing or transferring it away. f. A dollar paid unnecessarily not only cost the dollar but what the dollar could have earned had you not given it away. g. Advisor notes: It is very difficult to calculate the exact results but this tool will give you the opportunity to get in the ballpark and close enough for the client to understand the issues they face trying to win with the buy term and invest the difference strategy. It is important to note that permanent life insurance will not win in every case you illustrate, especially when rates of return are in the double digits in the investment account. Be careful to not get caught up in the rate of return game. There is a place for permanent insurance as well as investments especially if one is planning to leave money to their heirs. When all is said and done the risk involved as well as the fact that term insurance goes away paints a positive picture for have permanent insurance in ones portfolio. 2. Screen 2: a. Over the period of years, in looking at your investment at X interest rate, the results look very impressive. b. At first glance, it looks as if you invested X to get Y. c. Advisor notes: Compound interest can create a sizable account over time. As we begin on this screen this is the amount the client assumes they will have in their account at the end of the period based on a given rate of return. As we move forward we will begin to chip away at that amount with all the expenses due which they have often failed to calculate. They are taxes, opportunity cost on taxes, term cost, opportunity cost on term, and capital gains. 3. Screen 3: a. You really invested X in after tax dollars to get Y. b. Y represents the amount of interest you have earned over the period. c. Advisor notes: Subtract your basis (the contributions) to get the interest earned. A visual picture of the amount of money the client actually put into the account with after tax dollars is an important bench mark. Don t forget that the client had to earn more than the amount the invested to cover the tax due on their earned income. We are not showing that on this screen but it is important to make the point. 4. Screen 4: a. Often we tend to focus on the amount that we actually have in our account as illustrated in screen 4. Mentor Session 3 Workbook Revision Date:

41 b. In order for you to have that amount in your left pocket, you had to reach into your right pocket to cover the taxes due on the interest earned. c. The tax paid over the period is represented in red. d. Advisor notes: In an investment where the interest is compounding in a taxable environment there is a cost. The tax represents a cost to maintain this particular investment. Any tax paid is significant. Compare their tax rate with their return rate. Minimizing, avoiding, or eliminating taxes are strategies your client will be very interested in. Income taxes can t be avoided on earned income however additional tax on those same dollars invested can be avoided or at least minimized. 5. Screen 5: a. What do most people do with the interest they earn in their investment account? Most let it compound through re-investment. b. Very few people pay the taxes due on their investment from the interest earned in the investment. c. They roll the interest back into the account, which gives the appearance of magical growth. d. Where do they get the money to pay the additional taxes due from the investment? e. It usually comes from another source, which we call lifestyle. f. Most likely the taxes due from their investment results are included in their overall tax picture and go unnoticed. g. Unnoticed for a while, which brings us to the next point: h. In what year will the annual tax due be more than your annual contribution? i. Advisor notes: i. Most people roll their investment earnings back into their investment account. They pay the additional taxes due each year from their lifestyle. At some point in the future the tax due will exceed their annual savings. ii. Hint: When you step forward to answer the third question, the program automatically searches for the year in which the tax is equal to or greater than your contribution. This is a very important screen because it illustrates to the client that they may not be able to afford to continue compounding their interest because of the increasing taxes. First let s assume that this particular client can only afford to save $5,000 each year as is represented in the default numbers. Compound interest creates a tax, which is due each year. In year one the client pays little attention to the additional taxes due. Since they are rolling the interest back into the account each year, the tax liability is getting larger each year as well. At some point, their lifestyle may not continue to support the investment contribution and the taxes due, unless they are capable of finding additional funds to pay the tax. They have basically two choices. One would be to pay the taxes out of their lifestyle or secondly they could begin paying taxes by withdrawing the taxes due from the investment account. iii. Either way they are going to have less than they had anticipated. This screen offers a great opportunity for you to discuss other avenues, which can avoid transferring these taxes and incurring the additional cost of the tax. iv. The majority of dollars used to cover the taxes generated in taxable accounts is paid through one s lifestyle account. Once the account gets large enough to generate taxable earnings large enough for it to impact current lifestyle the Mentor Session 3 Workbook Revision Date:

42 client begins to take notice. Your job is to help them see the problem well in advance before the taxes become a serious problem. 6. Screen 6: a. Do people pay more taxes than they have to? b. The obvious answer is yes, but not because they want to. c. Most people would prefer to avoid the tax if they knew of a way to do so. d. If the tax was reduced, they could take less risk and perhaps still have the same or more money, especially if it did not affect their lifestyle. e. Remember if you pay a tax you could have avoided, you not only lose the tax dollar, but what that dollar could have earned for you had you not given it away. f. This is known as Opportunity Cost. g. Advisor notes: Opportunity Cost should be considered when determining the validity of any strategy. The tax lost is one thing and for many they have no problem paying the tax. Opportunity cost on the tax brings the tax loss into the light. This is perhaps the greatest economic principle one needs to understand to better manage their financial decisions. 7. Screen 7: a. Opportunity costs on taxes paid are a cost to be considered when compounding interest in a taxable investment. b. Advisor notes: i. Paying Expenses from Lifestyle: Taxes can be considered the maintenance fee or cost for an investment that yields 1099 income. Opportunity cost is another cost, which must be considered. If you give away a dollar unnecessarily, you have also lost what that dollar could have earned for you had you been able to keep it. ii. Paying Expenses from Investment: Taxes can be considered the maintenance fee or cost for an investment that yields 1099 income. Opportunity cost is another cost, which must be considered. When you take money from your investment account to pay a tax that could have been avoided it not only costs you what you took out but what those dollars would have earned for you had you been able to leave them in your investment. iii. Depending on the rate of return used the opportunity cost can be as high or higher than the actual taxes paid. Notice we break out the tax and the opportunity cost is an additional loss on top of the taxes paid. We do not want the client to miss this serious wealth transfer. 8. Screen 8: a. Let s factor in the term premiums into the equation. b. Advisor notes: Term Insurance has a cost as well. Often the cost of term is so low few people even count it as an expense but as we will see in the next screen with opportunity cost added it can be very costly. The most costly part of term insurance is the fact that you are using money to purchase it which you have less than 1% of ever collecting and when you really need it it become cost prohibitive. 9. Screen 9: a. You can only know the true cost and benefit of owning term insurance at your death. b. At that time you would add up all the premiums paid and compound them at interest to determine the opportunity cost of term. c. The cost would need to be weighed against the benefits received. Mentor Session 3 Workbook Revision Date:

43 d. Advisor notes: The opportunity cost of the term insurance premiums. Term insurance may be the most suitable recommendation for some client's circumstances. Their insurable need may only last the duration of the term, and term insurance may provide the greatest coverage for what they are able to afford. Adding the opportunity cost brings the true cost into focus. We are not saying you should not have term coverage but if you took the risk which we are not telling you to do and you invested the term premiums in your account you would have those dollars as well as the interest they would have earned. Make sure your client is doing all the math in their calculations. e. Click on the purple asterisk * next to opportunity on term f. Now we are looking at all the factors that make up the BTID strategy. g. Advisor notes: You won t your client to feel that you are very through and you have left nothing out. Remember the first screen where the client saw how much money they had in the account and how much they put in to get it. This is hard to argue against when you have broken out each and every expense. Just as there are many more expenses to consider when driving a car than the price of the car, there are expenses in taxable account than they failed to see before they began. 10. Screen 10: a. Finally in our review we would need to include any capital gains to get a true picture of this strategy. b. Advisor notes: Some of the money in their account may be subject to capital gains tax when they liquidate the account. Depending on how you structured the account on the input screen will dictate the effects of capital gains. Some accounts would not be taxed each year on the gain but have taxes deferred until they are sold. Often you will find your client in accounts that have a combination of both ordinary income and capital gains. 11. Screen 11: a. Now that we have accounted for all of the expenses. Let s compare the two positions: compound interest vs. permanent life insurance looking through the eyes of the Lifestyle Account Summary. b. Here on this screen we are going to be able to look at compound interest in a taxable account, buying term and investing the difference, verses permanent insurance and how it compares to the buy term invest the difference strategy. c. Instructor note: Lifestyle Account Summary means they are paying all of the additional expenses (taxes and the term) out of their lifestyle account. It is recommended that you don t put any amount into the permanent life insurance account until you go through each of expense and then come back at the end to talk about the insurance contract. d. Click on each one and explain what they are seeing on the left (compound interest) and on the right (permanent life insurance) e. Instructor Notes: Inputs: Initial Balance: $0, Annual Contributions: $10,000 at beginning of each year, Contribution Years: 30, Accumulation Years: 30, Rate of Return: 10%, % Treated as Ordinary Taxable: 100%, % Treated as Capital Gain: 0%, Ordinary Tax Bracket: 40%, Capital Gain Tax Bracket: 20%, All Term Premiums are set to zero i. Accumulation: Put your mouse pointer on the phrase of Accumulation and click to view the end of the period value calculated from the initial assumptions. A default example of $10,000 invested at 10% for 30 years at a Mentor Session 3 Workbook Revision Date:

44 40% tax bracket will show the figure $1,809,434 on the accumulation line on the left hand side of the screen and zero on the right. The $1,809,434 is the amount the investor is counting on having in their account. At this point we are going to leave the accumulation on the Permanent Insurance side at zero and come back to it at the end of the discussion. When you click on the line items in the middle of the screen; you will not only see the individual values to the left and the right but also at the bottom of the page you will see the difference in the two accounts. The difference arrow will point to the side with the greatest value. As you go through the line items, you will see the net accumulation and the difference change in proportion to each calculation. Using the default assumptions, you will notice at this point that the difference is in favor of the Buy Term & Invest The Difference side by $1,809,434. ii. Less Contributions: The next line item to review is the amount that each contributed to receive the accumulation value shown. You will notice that it is the same on both sides of the ledger and is a negative amount shown in red. iii. Plus Taxes Avoided: The next line illustrates the amount of taxes which must be paid in addition to the regular annual after tax contributions. You will see that the compound interest strategy required $603,774 in taxes on the interest earned. There is a zero in the left-hand column because this person had to pay $603,774 in taxes and at the end of the 30-year period has no claim to any of the dollars sent to the government. The person on the right however had no taxes to pay but still had to reach into their lifestyle and subtract $603,774. The permanent insurance required no additional taxes (under current tax law) so the taxes that were avoided by using permanent insurance could now be invested in a side fund. Let's assume that every time our person on the left wrote a check to the government for taxes due on the interest earned the person on the right put that same amount under their mattress. At the end of the period, our person on the right would have the same dollar amount in cash that the person on the left paid to the government. In order to get the true picture the same out of pocket cost must be accounted for on both sides of the ledger. iv. Plus Opportunity Earnings of Taxes: When clicked, the opportunity cost of the taxes are displayed in the right column. Compound interest created the taxes, which must be paid. Taxes paid cannot then be invested, they are gone and gone forever. The opportunity cost becomes real when those dollars can be redirected and the taxes, which would have been necessary, are avoided. This is a major benefit currently of permanent insurance, the growth inside the policy compounds without being taxed annually. Since the person on the right did not have to pay the taxes they could have not only saved them, but could have invested them. If the person on the right had invested the taxes saved and earned 10%, the default sample investment/opportunity cost rate of return, they would have an additional $832,178. v. Plus Fund Term Premiums Avoided: Now we have to factor in another item which affects the bottom line. The term insurance cost that you entered on the assumptions screen will show up when you click the button. Since our investor on the left wanted to make sure the family had something in case of their premature death they purchased some term insurance. The actual cost of the premiums is shown on this line. The person who purchased the Mentor Session 3 Workbook Revision Date:

45 permanent insurance on the other hand had the same amount of death benefit, which was included in the contract along with their annual $10,000 after tax premium, and it s cost has been factored into the cash value available. In other words, they purchased a policy for the same amount of death benefit as the person on the left for the same dollar amount of premium as the person on the left was investing. ($10,000 a year) In some cases the amount the person on the left is investing will not be enough for the person on the right to purchase a permanent product replacing all the term insurance the person on the left owns. There may also be situations where the annual amount being invested will be more than enough to purchase a permanent policy and you can load the contract with additional cash thus increasing the cash value at the end of the period making the net accumulation even larger. The zero cash value was designed to allow you to use any product you choose so that you can build the permanent life contract to meet the wants and desires of the client. When you factor in these dollars our buy term and invest the difference person on the left had to pay, the picture gets even clearer. Our person on the left paid all those premiums and has zero to show for it today. Yes they had the coverage but they have to cash from this transaction. If they are still alive at the end of the period they may be forced to drop the coverage because now it is getting cost prohibitive or can continue to pay the increasing premiums. Either way the cost is getting greater and greater the longer they live. vi. Plus Opportunity Earnings of Term: Just like the tax paid had an opportunity cost, so does the term premiums. When you click on Opportunity cost on Term you see what the actual premiums would have earned had you invested them at the investment rate of return entered on the assumptions screen. The person on the right was able to recoup the cost of the term premiums so they could also have invested them. Had they done so they would have the opportunity cost in addition to the premiums saved. vii. Plus Capital Gain Tax Avoided: Finally we must factor in any capital gain tax. viii. Total: Now we know that the policy we have been putting this $10,000 a year in has some cash values because there are some illustrated cash values* in the contract. Pull out a ledger from your carrier and circle the illustrated cash value* at the end of the period and type that number in the cell on the top right side of the ledger by accumulation under Permanent Insurance. The net accumulation will now increase on the right by the illustrated* cash value and the difference between the two accounts will also recalculate. Mentor Session 3 Workbook Revision Date:

46 Tax Master: BTID Investment Account Don s Dialog What you should say: Since most people are familiar with the rewards of compounding their interest but are not so familiar with the tax ramifications associated with the growth on the interest earned, the following discussion is designed to uncover some of the hidden costs. Let's enter your data and shine some light on this problem. Opportunity Cost may be a term you are not familiar with. Basically it represents the interest you could have earned on a given amount had you been able to avoid losing or transferring it away. A dollar paid unnecessarily not only cost the dollar but what the dollar could have earned had you not given it away. This is the initial assumptions screen for the main Tax Master presentation. The contributions are always made at the beginning of the year. The program includes an annual contribution at the beginning of the first year. Therefore, if you want a specific amount as the initial contribution, deduct the annual contribution from that initial contribution you desire. For example, if you want to start with exactly $100,000 and add $5,000 each year. Enter an initial balance of $95,000 and annual contributions of $5,000. (continued next page) Mentor Session 3 Workbook Revision Date:

47 Transition: It is very difficult to calculate the exact results but this tool will give you the opportunity to get in the ballpark and close enough for the client to understand the issues they face trying to win with the buy term and invest the difference strategy. It is important to note that permanent life insurance will not win in every case you illustrate, especially when rates of return are in the double digits in the investment account. Be careful to not get caught up in the rate of return game. There is a place for permanent insurance as well as investments especially if one is planning to leave money to their heirs. When all is said and done the risk involved as well as the fact that term insurance goes away paints a positive picture for have permanent insurance in ones portfolio. Mentor Session 3 Workbook Revision Date:

48 What you should say: Over the period of years we are looking at your investment at X interest rate looks very impressive. At first glance, it looks as if you spent X to get Y. Compound interest can create a sizable account over time. Transition: As we begin on this screen this is the amount the client assumes they will have in their account at the end of the period based on a given rate of return. As we move forward we will begin to chip away at that amount with all the expenses due which they have often failed to calculate. They are taxes, opportunity cost on taxes, term cost, opportunity cost on term, and capital gains. Mentor Session 3 Workbook Revision Date:

to get the interest earned.")

49 What you should say: You really spent X amount in after tax dollars to get Y. Y represents the amount of interest you have earned over the period. Subtract your basis (the contributions) to get the interest earned. Transition: A visual picture of the amount of money the client actually put into the account with after tax dollars is an important bench mark. Don t forget that the client had to earn more than the amount the invested to cover the tax due on their earned income. We are not showing that on this screen but it is important to make the point. Mentor Session 3 Workbook Revision Date:

50 What you should say: Often we tend to focus on the amount that we actually have in our account as illustrated in screen 4. In order for you to have that amount in your left pocket, you had to reach into your right pocket to cover the taxes due on the interest earned. The tax paid over the period is represented in red. In an investment where the interest is compounding in a taxable environment there is a cost. The tax represents a cost to maintain this particular investment. Transition: Any tax paid is significant. Compare their tax rate with their return rate. Minimizing, avoiding, or eliminating taxes are strategies your client will be very interested in. Income taxes can t be avoided on earned income however additional tax on those same dollars invested can be avoided or at least minimized. Mentor Session 3 Workbook Revision Date:

51 What you should say: What do most people do with the interest they earn in their investment account? Most let it compound through re-investment. Very few people pay the taxes due on their investment from the interest earned in the investment. They roll the interest back into the account, which gives the appearance of the magical growth. Where do they get the money to pay the additional taxes due from the investment? It usually comes from another source, which we are calling lifestyle. Most likely the taxes due from their investment results are included in their overall tax picture and go unnoticed. Unnoticed for a while, which brings us to the next point: In what year will the annual tax due be more than your annual contribution? Most people roll their investment earnings back into their investment account. They pay the additional taxes due each year from their lifestyle. At some point in the future the tax due will exceed their annual savings. (continued next page) Mentor Session 3 Workbook Revision Date:

52 Hint: When you step forward to answer the third question, the program automatically searches for the year in which the tax is equal to or greater than your contribution. This is a very important screen because it illustrates to the client that they may not be able to afford to continue compounding their interest because of the increasing taxes. First let s assume that this particular client can only afford to save $5,000 each year as is represented in the default numbers. Compound interest creates a tax, which is due each year. In year one the client pays little attention to the additional taxes due. Since they are rolling the interest back into the account each year, the tax liability is getting larger each year as well. At some point, their lifestyle may not continue to support the investment contribution and the taxes due, unless they are capable of finding additional funds to pay the tax. They have basically two choices. One would be to pay the taxes out of their lifestyle or secondly they could begin paying taxes by withdrawing the taxes due from the investment account. Either way they are going to have less than they had anticipated. This screen offers a great opportunity for you to discuss other avenues, which can avoid transferring these taxes and incurring the additional cost of the tax. Transition: The majority of dollars used to cover the taxes generated in taxable accounts is paid through ones lifestyle account. Once the account gets large enough to generate taxable earnings large enough for it to impact current lifestyle the client begins to take notice. Your job is to help them see the problem well in advance before the taxes become a serious problem. Mentor Session 3 Workbook Revision Date:

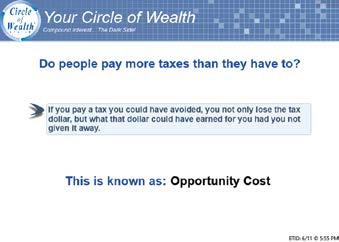

53 What you should say: Do people pay more taxes than they have to? The obvious answer is yes, but not because they want to. Most people would prefer to avoid the tax if they knew of a way to do so which could reduce their risk and at the same time give them more money, especially if it did not affect their lifestyle. Remember if you pay a tax you could have avoided, you not only lose the tax dollar, but what that dollar could have earned for you had you not given it away. This is known as Opportunity Cost. Opportunity Cost should be considered when determining the validity of any strategy. Transition: The tax lost is one thing and for many they have no problem paying the tax. Opportunity cost on the tax brings the tax loss into the light. This is perhaps the greatest economic principle one needs to understand to better manage their financial decisions. Mentor Session 3 Workbook Revision Date:

54 What you should say: Opportunity costs on taxes paid are a cost to be considered when compounding interest in a taxable investment. Paying Expenses from Lifestyle: Taxes can be considered the maintenance fee or cost for an investment that yields 1099 income. Opportunity cost is another cost, which must be considered. If you give away a dollar unnecessarily, you have also lost what that dollar could have earned for you had you been able to keep it. Paying Expenses from Investment: Taxes can be considered the maintenance fee or cost for an investment that yields 1099 income. Opportunity cost is another cost, which must be considered. When you take money from your investment account to pay a tax that could have been avoided it not only costs you what you took out but what those dollars would have earned for you had you been able to leave them in your investment. Transition: Depending on the rate of return used the opportunity cost can be as high or higher than the actual taxes paid. Notice we break out the tax and the opportunity cost is an additional loss on top of the taxes paid. We do not want the client to miss this serious wealth transfer. Mentor Session 3 Workbook Revision Date:

55 What you should say: Let s factor in the term premiums into the equation. Term Insurance has a cost as well. Transition: Often the cost of term is so low few people even count it as an expense but as we will see in the next screen with opportunity cost added it can be very costly. The most costly part of term insurance is the fact that you are using money to purchase it which you have less than 1% of ever collecting and when you really need it it become cost prohibitive. Mentor Session 3 Workbook Revision Date:

56 What you should say: You can only know the true cost and benefit of owning term insurance at your death. At that time you would add up all the premiums paid and compound them at interest to determine the opportunity cost of term. The cost would need to be weighed against the benefits received. The opportunity cost of the term insurance premiums. Term insurance may be the most suitable recommendation for some client's circumstances. Their insurable need may only last the duration of the term, and term insurance may provide the greatest coverage for what they are able to afford. Transition: Adding the opportunity cost brings the true cost into focus. We are not saying you should not have term coverage but if you took the risk which we are not telling you to do and you invested the term premiums in your account you would have those dollars as well as the interest they would have earned. Make sure your client is doing all the math in their calculations. Mentor Session 3 Workbook Revision Date:

57 What you should say: Now we are looking at all the factors that make up the BTID strategy. You are very through and you have left nothing out. Transition: Remember the first screen where the client saw how much money they had in the account and how much they put in to get it. This is hard to argue against when you have broken out each and every expense. Just as there are many more expenses to consider when driving a car than the price of the car, there are expenses in taxable account than they failed to see before they began. Mentor Session 3 Workbook Revision Date:

58 What you should say: Finally in our review we would need to include any capital gains to get a true picture of this strategy. Some of the money in their account may be subject to capital gains tax when they liquidate the account. Transition: Depending on how you structured the account on the input screen will dictate the effects of capital gains. Some accounts would not be taxed each year on the gain but have taxes deferred until they are sold. Often you will find your client in accounts that have a combination of both ordinary income and capital gains. Mentor Session 3 Workbook Revision Date:

59 Tax Master: BTID Life Style Account Don s Dialog What you should say: Disclosures: The rate of return used for the Life Insurance Illustration should have a gross rate of return equal to the rate of return used in the hypothetical account in the Tax Master program. The hypothetical account does not factor investment costs, and if it did, the hypothetical account's results would be less. ANY NUMBER APPEARING IN THE ACCUMULATION CELL UNDER PERMANENT INSURANCE MUST BE DOCUMENTED IN WRITING BY THE PROGRAM USER MAKING THE PRESENTATION. A COPY OF THE INSURANCE PROPOSAL ILLUSTRATING ANY NUMBER OTHER THAN ZERO MUST ACCOMPANY ANY PRINTING OF THIS COMPARISON. Usage Hints: Click the descriptive label for each row to include the value in the account comparison. Click the "Difference" row to quickly display all the information. Enter the cash value of the insurance in the top right box that appears when you click the Account 2's Accumulation ($0). Press tab or enter after you enter the cash value. Click CV to change the display to surrender value. Click SV to toggle the display to death benefit. Click DB to toggle back to cash value. (Each value must be entered individually from a valid policy illustration.) Mentor Session 3 Workbook Revision Date: