Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks

|

|

|

- Josephine Potter

- 5 years ago

- Views:

Transcription

1 Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna Monday - 6:00 pm to 9:00 pm

2 Class introductions J Class admin. Student Detail Slips (please fill out and return to teacher) TAFE Resit Policy and resit dates for Semester 2, 2017 Unit Delivery and Assessment Guide à for all course material Our classroom rules (including your rights & responsibilities at TAFE) Location of some facilities (toilets; library; counselling; careers advisor) What should you do in an emergency? General WHS (Work Health and Safety)

3 Unit Overview Ref. DELIVERY AND ASSESSMENT GUIDE Performance criteria Resources including recommended text Delivery schedule Assessments Unit grading Solutions to even-numbered end-of-chapter questions in the textbook where to find them? Acronym challenge

4 AMEG House Rules Be punctual (teacher included!) Come to every class (if possible) Come to class prepared (students & teacher) Bring textbook (might help a bit) Create and maintain a safe and supportive learning environment (there is no such thing as a silly question!) Eating and drinking in class totally permitted J

5 Lesson 1 TPB Requirements FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks

6 Overview 1. Introduction to activity statements 2. Lodgement of activity statements 3. Interacting with the ATO 4. Providing BAS services

7 Ok let s begin how much do you already know?

8 Which statement do you identify with the most? A: I don t really know anything about BAS. It stands for Bananas, Apples and Strawberries, right? B: I know a little about BAS. I know that the ATO requires this type of statement to be prepared by certain taxpayers. C: I know lots about BAS. I have experience preparing an activity statement in the workplace.

9 Video Clip: Tax basics for small business Activity Statements

10 1. Introduc,on to ac,vity statements

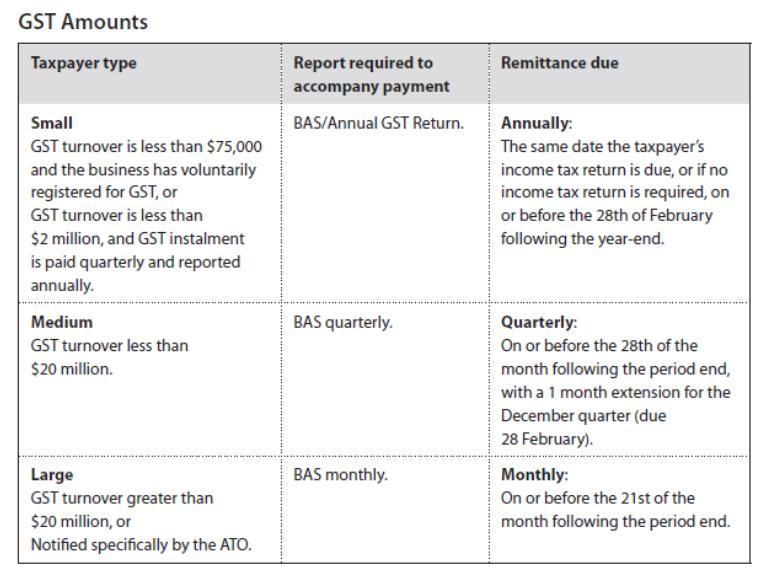

11 Businesses are required to comply with tax legislation. The New Tax System came into effect in 1999 and introduced the Goods and Services Tax (GST). GST replaced indirect taxation with a 10% charge on most sales made by businesses. This effectively shifted the job of tax collection onto businesses. Businesses are required to pay amounts collected to the Australian Taxation Office (ATO) through the use of Activity Statements. Businesses are required to lodge Activity Statements on either a monthly, quarterly or annual basis to the ATO.

12 Types of Ac2vity Statements There are two (2) types of activity statements: The Business Activity Statement (BAS), which must be completed by those taxpayers who are required to report GST in that activity statement period. The Instalment Activity Statement (IAS), which applies to those not registered for GST, taxpayers with investment income and GST-registered businesses who are required to report GST on a quarterly basis but have other monthly reporting obligations.

13 Business Ac2vity Statements All taxpayers who are registered for GST must report their tax obligations on a BAS. A BAS can be used for: GST (lessons 5 and 6) PAYG withholding (lesson 3) PAYG instalments (lesson 4) Luxury Car Tax (LCT) (lesson 7) Wine Equalisation Tax (WET) (lesson 7) Fringe Benefit Tax (FBT) instalments (lesson 7)

14 Business Ac2vity Statements A business that is registered for GST purposes must also apply for an Australian Business Number (ABN). It will then be required to: Complete a BAS. Lodge the BAS. Report and pay tax as required.

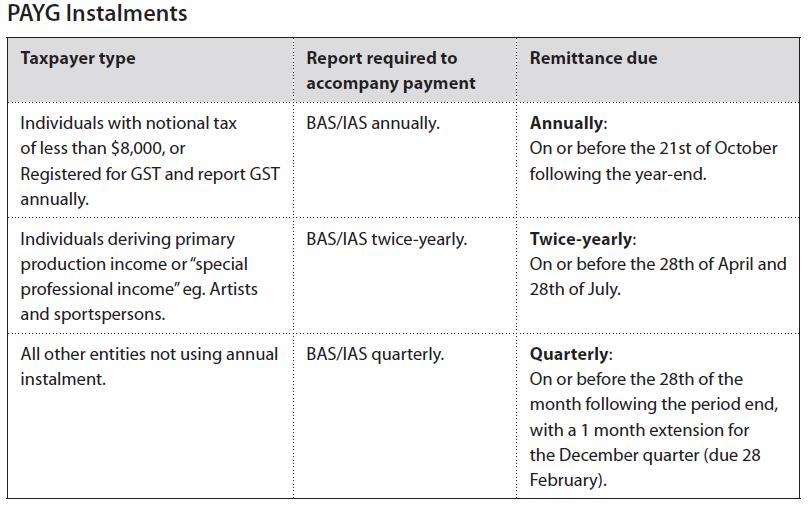

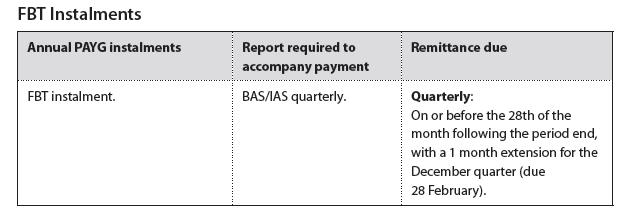

15 Instalment Ac2vity Statements The IAS mainly applies to individual taxpayers with investment income (e.g. rental, interest or dividend income) or who have businesses with an annual turnover below the minimum GST registration threshold of $75,000. In addition, some GST-registered businesses must complete a quarterly BAS and a monthly IAS for the months in between.

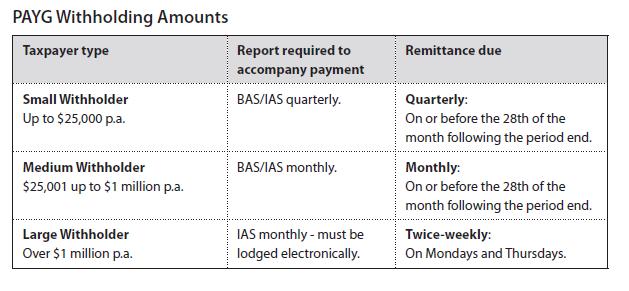

16 Instalment Ac2vity Statements An IAS can be used for the following reporting obligations: PAYG withholding (lesson 3) PAYG instalments (lesson 4) FBT instalments (lesson 7)

17 2. Lodgement of ac,vity statements

18

19

20

21

22 Due dates of instalments Quarterly payments are due 28 days after the end of each quarter, with a one month extension for the December quarter. If a taxpayer s income year starts on 1 July, their instalments will be due: 28 October 28 February 28 April 28 July

23 Due dates of instalments Annual payments are due on 21 October after year-end if the taxpayer s income year starts on 1 July. The ATO will advise taxpayers if they are eligible to make an annual payment. If the taxpayer wishes to pay on this basis, they must complete the form the ATO sends at the time the first instalment is due. The taxpayer is still required to lodge an annual income tax return at the end of the income year. Any amounts of PAYG instalments that have been paid during that year will be credited to the taxpayer s assessment and they can either claim a tax refund or pay the balance of outstanding tax.

24 Due dates of instalments Declaration and Lodgement To finalise the BAS form the declaration box must be signed by an authorised person before lodgement to the ATO.

25 Who can sign an Ac2vity Statement? Once the activity statement is completed and the taxpayer is satisfied that all of the information provided is true and correct, it must be signed and dated. If the activity statement is being lodged electronically by an agent, the agent will need to sign the declaration on the activity statement using their electronic signature. Where an agent lodges a taxpayer s activity statement, the taxpayer must sign a declaration stating that: The taxpayer authorises the agent to give the activity statement to the Commissioner. The information provided to the agent to prepare the activity statement is true and correct.

26 Lodgement of Ac2vity Statements Taxpayers can lodge activity statements online using the ATO s Business Portal or electronic commerce interface (ECI). Registered tax agents and registered BAS agents can help prepare and lodge a taxpayer s activity statement and can lodge them electronically via the electronic lodgement service (ELS). If the taxpayer has no amount to report at any label due to no business activity during the period, lodgement of the BAS/IAS can be made over the telephone. Otherwise, the completed BAS/IAS can be mailed directly to the ATO using the pre-addressed envelope provided.

27 Lodgement of Ac2vity Statements Late Lodgement Penal,es The penalty for lodging an activity statement late is one penalty unit (currently $180) for each 28 day period, or part of a period, that the activity statement is outstanding, up to a maximum of 5 penalty units ($900). For a business with an annual turnover between $1 million but less than $20 million, the penalty is multiplied by two. For a large business with an annual turnover of $20 million or more, the penalty is multiplied by five, resulting in a maximum penalty of $4,500.

28 3. Interac,ng with the ATO

29 Only primary contacts (including public officers), authorised contacts, registered tax agents, registered BAS agents and temporarily appointed tax professionals can contact the ATO on behalf of an entity. What is a primary contact? A primary contact has authority to access all roles on their client s account, and add, remove or update the list of authorised contacts. What is an authorised contact? Primary contacts can authorise contacts to act on their behalf in relation to some or all of the entities tax affairs. They are not able to add, remove or update authorised contacts unless the authorised contact declares they have been given authority to act on behalf of the entity in this capacity.

30 En2ty Types/Primary Contacts

31 4. Providing BAS services

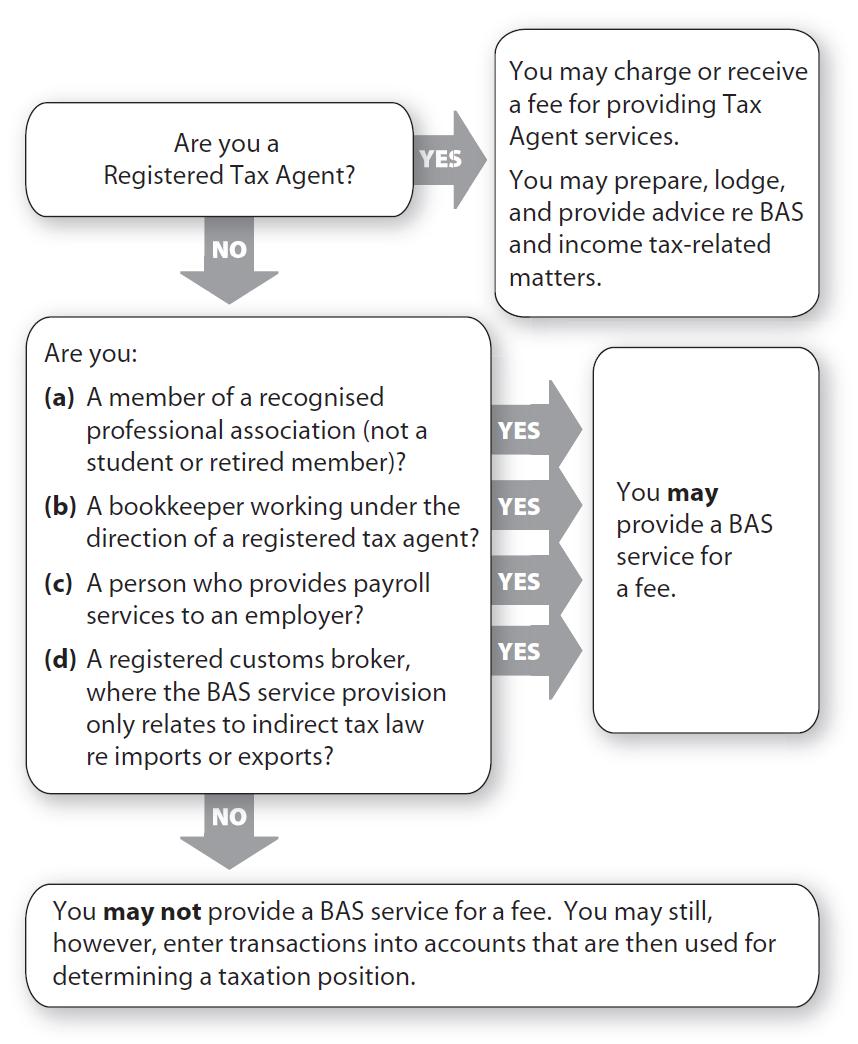

32 After completing this part, you should be able to answer the following questions: 1. Why was the Tax Agent Services Act 2009 introduced? 2. What is the role of the TPB? 3. What does a BAS provision include? 4. What is a BAS service as defined under the Act? 5. Who is allowed to provide a BAS service? 6. Can a BAS agent provide a BAS service for a fee if they are not registered? Are there any consequences for doing so? 7. Can a voting member of a Recognised Professional Associations register as a BAS agent? 8. What do you have to do / what registration criteria do you have to meet before you can become a BAS agent? 9. Do BAS agents have to comply with obligations set out in the Code of Professional Conduct? Are there any consequences for not doing so? 10. Do registered BAS agents need Public Indemnity Insurance? Why?

33 Registered BAS agents can charge a fee for providing BAS services to a taxpayer. A BAS service is defined as: Preparing or lodging an approved form about a taxpayer s liabilities, obligations or entitlements under a BAS provision. Giving advice about the taxpayer s obligations under a BAS provision. Transacting any business with the Commissioner on behalf of a taxpayer in relation to their obligations under a BAS provision.

34 A BAS provision includes/relates to: Goods and Services Tax (GST) law Wine Equalisation Tax (WET) law Luxury Car Tax (LCT) law Fuel Tax law Fringe Benefits Tax (FBT) law relating to collection and recovery only Pay-As-You-Go (PAYG) withholding PAYG instalments

35 Specifically

36 Legisla2on rela2ng to BAS services To ensure appropriate standards of professional and ethical conduct by tax agents and those providing BAS services, the Tax Agent Services Act 2009 was passed in Parliament. The Act became operational in February 2010 after allowing time for the appointment of a national Tax Practitioners Board and the establishment of administrative resources to administer the Act.

37 Tax Agent Services Act 2009 The key features of the Act: The establishment of a national Tax Practitioners Board (TPB), replacing the existing State-based boards. A legislated code of professional conduct that governs the provision of tax agent services. A wider range of disciplinary sanctions available to the new board, including a civil penalty for certain types of serious misconduct by tax practitioners. Registration and regulation of BAS service providers as BAS agents. Protection for taxpayers from tax shortfall penalties for making false or misleading statements, where a taxpayer demonstrates that they have taken reasonable care.

38 BAS Agents BAS agents must be registered with the TPB. A BAS agent may be an individual, partnership or company. If the BAS agent is a partnership or company, a sufficient number of individuals (being registered BAS agents) are required to provide BAS services to a competent standard, and to supervise other employees. A BAS Service Provider (BSP) is either: A registered tax agent. A registered BAS agent. An employee who conducts BAS services for a company or partnership that is a registered BAS agent.

39 Who can provide a BAS service for a fee?

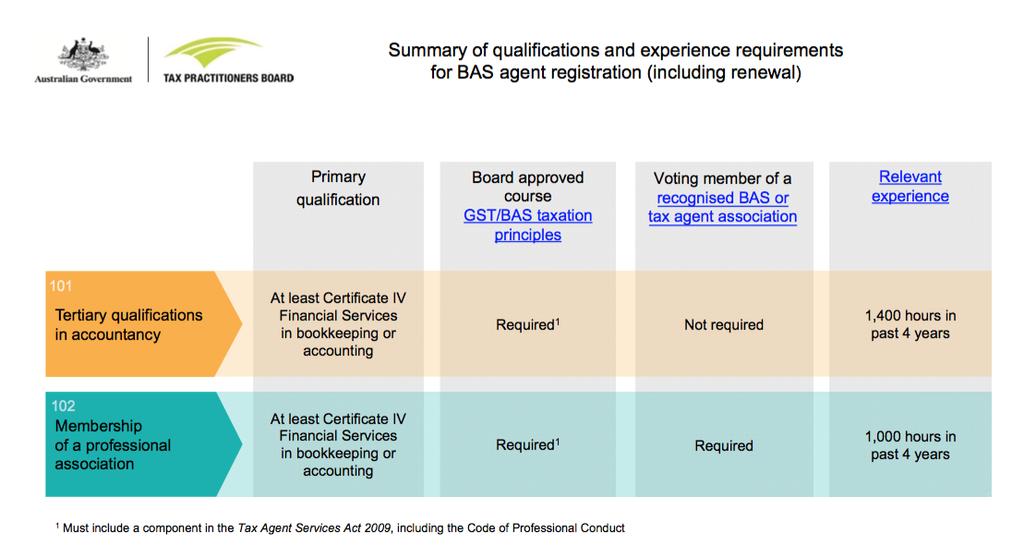

40

41 BAS Agents The requirements and recommendations apply to bookkeepers providing BAS services for a fee and the registered tax agents under whose direction they are working. BAS agents who charge for BAS services are required to be registered with the TPB. To be registered they must hold certain academic qualifications and meet experience requirements.

42 Penal2es Under the Tax Agent Services Act, if a fee for BAS services is charged by a person who is not a registered BAS agent, or a person eligible to do so, they may be prosecuted and fined up to $45,000 for a breach of this law. Conduct prohibited without registration: Providing BAS agent services. Advertising BAS agent services. Representing that you are a BAS agent or BAS service provider. Career as BAS agent à à à

43 Recognised Professional Associa2ons (RPAs) Voting members of the following recognised professional associations are eligible to register as BAS agents: Association of Accounting Technicians. Association of Chartered Certified Accountants. CPA Australia ( CPAs ). Institute of Certified Bookkeepers. Institute of Chartered Accountants in Australia ( CAs ). Institute of Public Accountants.

44 How to Register as a BAS Agent A standard application: The applicant must meet the standard registration requirements. They must be a fit and proper person and meet qualification and experience requirements. The applicant will be registered for three (3) years from the day the TPB decides on the application. The applicant cannot legally provide a BAS service prior to approval of registration. The application fees for BAS agent standard application are: $100 - for registration as a BAS agent who carries on a business. $50 - for registration as a BAS agent who does not carry on a business.

45 Fit and Proper Person Requirement To be eligible for registration, the applicant must satisfy the TPB that they are a fit and proper person. TPB/Subsidiary_content/ 0315_Fit_and_proper_person.aspx

46

or Certificate IV Financial Services (Bookkeeping) from an Australian Registered Training Organisation (RTO) such")

47 Qualifica2ons An individual who wishes to register as a BAS agent must satisfy the TPB they have sufficient qualifications. The individual must hold at least a Certificate IV in Financial Services (Accounting) or Certificate IV Financial Services (Bookkeeping) from an Australian Registered Training Organisation (RTO) such as TAFE. The qualification must include a course in GST/BAS taxation principles. The type of GST/BAS course you need will depend on when the application for registration or renewal is made.

48 Relevant Experience To register as a BAS agent there are two (2) options relating to relevant experience requirements for individuals. Option 1: Experience Based on Accounting Qualifications The individual must have had at least 1,400 hours of relevant experience in the past three years. Option 2: Experience Based on Membership of a Professional Organisation If the individual is a voting member of a recognised professional association the relevant experience requirement for the past three years is 1,000 hours.

49 Other Responsibili2es Not knowingly obstruct the proper administration of the taxation laws. Advise the client of the client s rights and obligations under the taxation laws that are materially related to the BAS agent services provided by the agent. Maintain the professional indemnity insurance that the TPB requires the agent to maintain. Respond to requests and directions from the TPB in a timely, responsible and reasonable manner.

50 Failure to Comply with the Code BAS agents are required to comply with all the obligations set out in the Code of Professional Conduct. If, following an investigation, the TPB is satisfied that a BAS agent failed to comply with the Code; it may impose one or more of the following administrative sanctions: A written caution. An order requiring the agent to take one or more actions including: Ø completing a course of education or training specified by the TPB, Ø providing services (for which the BAS agent is registered) only under the supervision of another BAS agent that has been specified in the order, or Ø providing only those services that are specified in the order. Suspending the agent s registration. Terminating the agent s registration.

51 Professional Indemnity Insurance (PII) Requirements It is possible that clients may suffer financial loss due to the conduct of a BAS agent in the provision of BAS services. Since 1 July 2011, registered BAS agents are typically required to have adequate Professional Indemnity Insurance (PII) cover that meets the TPB s minimum requirements. Adequate Professional Indemnity Insurance will satisfactorily indemnify an agent against civil liability that may arise in the agent s provision of BAS services.

.")

52 This week s homework Get a copy of the recommended text. Download and read a copy of the DELIVERY AND ASSESSMENT GUIDE for this unit (available on ). Complete assigned research activity (started in-class).

53 You are now ready to start the next lesson on: The Business Tax System Income Tax; ABN and TFN Requirements

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday Room H G.09-6:00 pm to 9:00 pm 1 Lesson 3 FNSBKG404 Carry Out Business

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday Room H G.09-6:00 pm to 9:00 pm 1 Lesson 3 FNSBKG404 Carry Out Business

INSTALMENT ACTIVITY STATEMENTS (IAS)

") Chapter 5: BAS & IAS INSTALMENT ACTIVITY STATEMENTS (IAS) What is an Instalment Activity Statement? Individual taxpayers, trustees with business income, and businesses not registered for use the Instalment

Chapter 5: BAS & IAS INSTALMENT ACTIVITY STATEMENTS (IAS) What is an Instalment Activity Statement? Individual taxpayers, trustees with business income, and businesses not registered for use the Instalment

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday Room H G.09-6:00 pm to 9:00 pm Lesson 2 Part 1 TFN and ABN Requirements

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday Room H G.09-6:00 pm to 9:00 pm Lesson 2 Part 1 TFN and ABN Requirements

THE BAS AGENT. The Institute of Certified Bookkeepers. Volume 2: Applying the Code of Conduct. ICB Definitive Guide. August 2012

The Institute of Certified Bookkeepers THE BAS AGENT Volume 2: Applying the Code of Conduct ICB Definitive Guide August 2012 Phone: 1300 85 61 81 email: admin@icb.org.au web: www.icb.org.au Not all bookkeepers

The Institute of Certified Bookkeepers THE BAS AGENT Volume 2: Applying the Code of Conduct ICB Definitive Guide August 2012 Phone: 1300 85 61 81 email: admin@icb.org.au web: www.icb.org.au Not all bookkeepers

CERTIFICATE IV. FNSTPB401 Complete business activity and instalment activity statements USER GUIDE. sample for review

CERTIFICATE IV FNSTPB401 Complete business activity and instalment activity statements USER GUIDE All Rights Reserved Copyright 2018 OfficeLink Learning Version 18.6 Xero No part of the contents of this

CERTIFICATE IV FNSTPB401 Complete business activity and instalment activity statements USER GUIDE All Rights Reserved Copyright 2018 OfficeLink Learning Version 18.6 Xero No part of the contents of this

Sample only. Change of registration details

Change of registration details Use this form to change the following registration details for the entity: entity name or trading name postal, email or business address authorised contact person associates

Change of registration details Use this form to change the following registration details for the entity: entity name or trading name postal, email or business address authorised contact person associates

TASA Code of Professional Conduct and other compliance requirements

TASA Code of Professional Conduct and other compliance requirements March 2014 Once registered you have a legal requirement to comply with the TASA Code of Professional Conduct (s30.5), and other requirements

TASA Code of Professional Conduct and other compliance requirements March 2014 Once registered you have a legal requirement to comply with the TASA Code of Professional Conduct (s30.5), and other requirements

THE GOODS & SERVICES TAX (GST) SYSTEM

SYSTEM") AUSTRALIAN BUSINESS NUMBER (ABN) THE GOODS & SERVICES TAX (GST) SYSTEM The Australian Business Number (ABN) is the identifying number that businesses use when dealing with other businesses. The ABN is

AUSTRALIAN BUSINESS NUMBER (ABN) THE GOODS & SERVICES TAX (GST) SYSTEM The Australian Business Number (ABN) is the identifying number that businesses use when dealing with other businesses. The ABN is

Tax Agent Services Act 2009

Tax Agent Services Act 2009 Act No. 13 of 2009 as amended This compilation was prepared on 21 December 2010 taking into account amendments up to Act No. 145 of 2010 The text of any of those amendments

Tax Agent Services Act 2009 Act No. 13 of 2009 as amended This compilation was prepared on 21 December 2010 taking into account amendments up to Act No. 145 of 2010 The text of any of those amendments

BUSINESS ACTIVITY & INSTALMENT ACTIVITY STATEMENT TASKS

C ARRY OUT BUSINESS ACTIVITY & INSTALMENT ACTIVITY STATEMENT TASKS FOURTH EDITION Disclaimer This book and any related publication are sold and distributed on the basis that the authors, consultants and

C ARRY OUT BUSINESS ACTIVITY & INSTALMENT ACTIVITY STATEMENT TASKS FOURTH EDITION Disclaimer This book and any related publication are sold and distributed on the basis that the authors, consultants and

January 2015 Newsletter

January 2015 Newsletter OUR SERVICES Did you know we can assist you in the following ways: Income Tax Income Tax Preparation Tax Planning Advice GST Business Activity Statements Superannuation Land Tax

January 2015 Newsletter OUR SERVICES Did you know we can assist you in the following ways: Income Tax Income Tax Preparation Tax Planning Advice GST Business Activity Statements Superannuation Land Tax

Change of details for superannuation entities

Change of details for superannuation entities Use this form to change the following details for a superannuation entity: n entity type n Australian Prudential Regulation Authority (APRA) fund type n structure

Change of details for superannuation entities Use this form to change the following details for a superannuation entity: n entity type n Australian Prudential Regulation Authority (APRA) fund type n structure

Change of registration details. Section A: Entity information This section is compulsory. 1 What is the entity s Australian business number (ABN)?

?") SHEET 1 OF 2 Change of registration details Initial sheet here Use this form to change the following registration details for the entity: entity name or trading name postal, email or business address authorised

SHEET 1 OF 2 Change of registration details Initial sheet here Use this form to change the following registration details for the entity: entity name or trading name postal, email or business address authorised

Common BAS errors. General.

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

April The small business $20,000 instant asset write-off. Time to go shopping! The $20,000 instant asset write-off explained

The small business $20,000 instant asset write-off. Time to go shopping! The small business write-off threshold of $20,000 was extended to 30 June 2018 and is available to all small businesses with an

The small business $20,000 instant asset write-off. Time to go shopping! The small business write-off threshold of $20,000 was extended to 30 June 2018 and is available to all small businesses with an

ABN registration for superannuation entities Use this application to register for an Australian business number (ABN).

.") BUSINESS SUPERANNUATION ENTITIES INSTRUCTIONS NAT 2944-06.2005 SEGMENT AUDIENCE FORMAT PRODUCT ID ABN registration for superannuation entities Use this application to register for an Australian business

BUSINESS SUPERANNUATION ENTITIES INSTRUCTIONS NAT 2944-06.2005 SEGMENT AUDIENCE FORMAT PRODUCT ID ABN registration for superannuation entities Use this application to register for an Australian business

Only an entity that is carrying on an enterprise may register. Therefore, it is important that these terms are clearly understood.

2. MANAGING THE GST DO YOU NEED TO REGISTER Whether or not you are in the GST system depends upon whether you are registered or required to be registered. A registration system is necessary for the administration

2. MANAGING THE GST DO YOU NEED TO REGISTER Whether or not you are in the GST system depends upon whether you are registered or required to be registered. A registration system is necessary for the administration

Personal services income schedule 2012

Instructions for companies, partnerships and trusts Personal services income schedule 2012 Schedule and explanatory notes for 1 July 2011 30 June 2012 For more information visit www.ato.gov.au NAT 3421-06.2012

Instructions for companies, partnerships and trusts Personal services income schedule 2012 Schedule and explanatory notes for 1 July 2011 30 June 2012 For more information visit www.ato.gov.au NAT 3421-06.2012

TAXWISE. BUSINESS NEWS September Tax Time 2012 ATO Compliance Program

TAXWISE BUSINESS NEWS September 2012 IN THIS ISSUE Tax Time 2012 ATO Compliance Program; Loss Carry-Back for Small Business; Living-Away-From-Home Allowance Changes; Superannuation Changes; Anti-Avoidance

TAXWISE BUSINESS NEWS September 2012 IN THIS ISSUE Tax Time 2012 ATO Compliance Program; Loss Carry-Back for Small Business; Living-Away-From-Home Allowance Changes; Superannuation Changes; Anti-Avoidance

Tax basics. Tax basics for business operators. The basics:

Main topics - Tax basics - How tax works for different business structures - Summary of business taxes and payments - Claiming deductions for business expenses - Why keep good business records? - Contacts

Main topics - Tax basics - How tax works for different business structures - Summary of business taxes and payments - Claiming deductions for business expenses - Why keep good business records? - Contacts

Your Knowledge March 2018

Simple Creative Solutions Your Knowledge IN THIS ISSUE FBT Some hotspots to look out for. GST on property developments. SINGLE TOUCH PAYROLL When will it apply to me? What Super contributions can be made

Simple Creative Solutions Your Knowledge IN THIS ISSUE FBT Some hotspots to look out for. GST on property developments. SINGLE TOUCH PAYROLL When will it apply to me? What Super contributions can be made

Your super, your service

Issued 1 July 2015 Your super, your service Administration Services Guide AMP SMSF Solutions AMP offers a competitively priced professional administration and compliance service that gives you peace of

Issued 1 July 2015 Your super, your service Administration Services Guide AMP SMSF Solutions AMP offers a competitively priced professional administration and compliance service that gives you peace of

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN. keeping you informed autumn 2018 IN THIS ISSUE YOUR BAS & RECORD KEEPING

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES

2016 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES INCOME TAX RATES AMENDMENT (WORKING HOLIDAY MAKER REFORM) BILL 2016 TREASURY LAWS AMENDMENT (WORKING HOLIDAY MAKER REFORM)

2016 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES INCOME TAX RATES AMENDMENT (WORKING HOLIDAY MAKER REFORM) BILL 2016 TREASURY LAWS AMENDMENT (WORKING HOLIDAY MAKER REFORM)

Tax basics for small business

Guide for small business operators Tax basics for small business Information about your tax obligations and entitlements. For more information visit www.ato.gov.au NAT 1908-08.2010 OUR COMMITMENT TO YOU

Guide for small business operators Tax basics for small business Information about your tax obligations and entitlements. For more information visit www.ato.gov.au NAT 1908-08.2010 OUR COMMITMENT TO YOU

BIZPRAC 12 GUIDE BUSINESS ACTIVITY STATEMENTS

BIZPRAC 12 GUIDE BUSINESS ACTIVITY STATEMENTS BAS EXPLAINED The business activity statement is submitted to the ATO by all businesses to report their tax obligations. They will include: Pay as you go withholding

BIZPRAC 12 GUIDE BUSINESS ACTIVITY STATEMENTS BAS EXPLAINED The business activity statement is submitted to the ATO by all businesses to report their tax obligations. They will include: Pay as you go withholding

Withholding declaration upwards variation

Instructions and form for taxpayers Withholding declaration upwards variation WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the rate or amount withheld

Instructions and form for taxpayers Withholding declaration upwards variation WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the rate or amount withheld

THINGS TO DO BEFORE 30 JUNE

16 June 2017, Volume 7, Page 1 Our Business Website Staff Update Fees Things to do before 30 June Taxation & Accounting Checklists Audit Checklists ATO My Deductions App Office Hours: 8:30am to 5:00pm

16 June 2017, Volume 7, Page 1 Our Business Website Staff Update Fees Things to do before 30 June Taxation & Accounting Checklists Audit Checklists ATO My Deductions App Office Hours: 8:30am to 5:00pm

The Institute of Certified Bookkeepers

The Institute of Certified Bookkeepers News December 14, 2007 A PDF copy of this newsletter is available online, click here. www.icb.org.au Contents The Future Government making it easier for business

The Institute of Certified Bookkeepers News December 14, 2007 A PDF copy of this newsletter is available online, click here. www.icb.org.au Contents The Future Government making it easier for business

TPB Information sheet TPB(I) 18/2013

18/2013") TPB Information sheet TPB(I) 18/2013 Code of Professional Conduct Reasonable care to ensure taxation laws are applied correctly Disclaimer This is a Tax Practitioners Board (TPB) Information sheet (TPB(I)).

TPB Information sheet TPB(I) 18/2013 Code of Professional Conduct Reasonable care to ensure taxation laws are applied correctly Disclaimer This is a Tax Practitioners Board (TPB) Information sheet (TPB(I)).

ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards

ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Title ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Creation

ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Title ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Creation

GST Manual for Schools

GST Manual for Schools Audit Tax Advisory Welcome to the 4 th Edition of the GST Manual for Schools. From the very beginnings of GST in 1999, our office has been integrally involved in the delivery of

GST Manual for Schools Audit Tax Advisory Welcome to the 4 th Edition of the GST Manual for Schools. From the very beginnings of GST in 1999, our office has been integrally involved in the delivery of

Tax Agent Services Regulations

Tax Agent Services Regulations 2009 1 Select Legislative Instrument 2009 No. 314 I, QUENTIN BRYCE, Governor-General of the Commonwealth of Australia, acting with the advice of the Federal Executive Council,

Tax Agent Services Regulations 2009 1 Select Legislative Instrument 2009 No. 314 I, QUENTIN BRYCE, Governor-General of the Commonwealth of Australia, acting with the advice of the Federal Executive Council,

Select Your Service. We re not just another Accounting firm You re not just another client

Our Abacus Angels have made tax season even easier for you this time around with their new and improved EasyPack transforming in to a SIX STEP process! This form contains questions that will help us prepare

Our Abacus Angels have made tax season even easier for you this time around with their new and improved EasyPack transforming in to a SIX STEP process! This form contains questions that will help us prepare

INTRODUCTORY TAXATION

INTRODUCTORY TAXATION SUBJECT OUTLINE A professional accountant is required to possess fundamental tax law knowledge and skills. Introductory Taxation introduces fundamental concepts of income tax law,

INTRODUCTORY TAXATION SUBJECT OUTLINE A professional accountant is required to possess fundamental tax law knowledge and skills. Introductory Taxation introduces fundamental concepts of income tax law,

2001 tax returns: companies and trusts

2001 tax returns: companies and trusts 28 November 2001 Western Australian Division Stuart Third, Winduss & Associates Presented by: Stuart Third Tax ation Institute of Australia 2001 The Tax ation Institute

2001 tax returns: companies and trusts 28 November 2001 Western Australian Division Stuart Third, Winduss & Associates Presented by: Stuart Third Tax ation Institute of Australia 2001 The Tax ation Institute

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN. keeping you informed autumn 2018 IN THIS ISSUE YOUR BAS & RECORD KEEPING

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

The Australia Taxation reflects legislation in place at 1 November Exam questions will be based upon the tax year.

AUSTRALIA TAXATION CPA Program subject outline First edition A professional accountant is required to possess fundamental tax law knowledge and skills. Australia Taxation introduces fundamental concepts

AUSTRALIA TAXATION CPA Program subject outline First edition A professional accountant is required to possess fundamental tax law knowledge and skills. Australia Taxation introduces fundamental concepts

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TAX BASICS FOR NON-PROFIT ORGANISATIONS

NON-PROFIT NON-PROFIT ORGANISATIONS OVERVIEW NAT 7966-06.2005 SEGMENT AUDIENCE FORMAT PRODUCT ID TAX BASICS FOR NON-PROFIT ORGANISATIONS An overview of tax issues relating to non-profit organisations including

NON-PROFIT NON-PROFIT ORGANISATIONS OVERVIEW NAT 7966-06.2005 SEGMENT AUDIENCE FORMAT PRODUCT ID TAX BASICS FOR NON-PROFIT ORGANISATIONS An overview of tax issues relating to non-profit organisations including

Go to question 4. Go to question 2. Only complete this question if the entity applying for an ABN is an APRA regulated superannuation fund.

Application for ABN registration for superannuation entities Complete this application if you need an Australian business number (ABN) for a superannuation entity. The fastest way to get an ABN is to apply

Application for ABN registration for superannuation entities Complete this application if you need an Australian business number (ABN) for a superannuation entity. The fastest way to get an ABN is to apply

NEW SMSF APPLICATION & APPOINTMENT OF TRIPLE A SUPER FOR ADMINISTRATION SERVICES

NEW SMSF APPLICATION & APPOINTMENT OF TRIPLE A SUPER FOR ADMINISTRATION SERVICES Name of Adviser Phone Number Adviser Firm Name Adviser Street Address Adviser Email Address Licensee New Fund Name Type

NEW SMSF APPLICATION & APPOINTMENT OF TRIPLE A SUPER FOR ADMINISTRATION SERVICES Name of Adviser Phone Number Adviser Firm Name Adviser Street Address Adviser Email Address Licensee New Fund Name Type

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

State of the Industry 2010 Bookkeepers who provide BAS services for a fee

State of the Industry 2010 Bookkeepers who provide BAS services for a fee Final Report Prepared for: The Australian Tax Office June 2010 GfK Blue Moon Sydney L2 71-73 Chandos St St Leonards NSW 2065 AUSTRALIA

State of the Industry 2010 Bookkeepers who provide BAS services for a fee Final Report Prepared for: The Australian Tax Office June 2010 GfK Blue Moon Sydney L2 71-73 Chandos St St Leonards NSW 2065 AUSTRALIA

PAYG withholding. Guide for employers and businesses. What employers and businesses need to know to meet their PAYG withholding obligations

Guide for employers and businesses PAYG withholding What employers and businesses need to know to meet their PAYG withholding obligations For more information visit www.ato.gov.au NAT 8075-02.2009 Our

Guide for employers and businesses PAYG withholding What employers and businesses need to know to meet their PAYG withholding obligations For more information visit www.ato.gov.au NAT 8075-02.2009 Our

2018/19 Federal Budget

1. Personal income tax changes 1.1 Personal income tax plan 2018/19 Federal Budget The Government will introduce a seven-year, three-step, Personal Income Tax Plan, as follows: Step 1: Targeted tax relief

1. Personal income tax changes 1.1 Personal income tax plan 2018/19 Federal Budget The Government will introduce a seven-year, three-step, Personal Income Tax Plan, as follows: Step 1: Targeted tax relief

Checklist. 1) Do some background research

Do some background research") Checklist Matters for consideration before you start a charity: Take some time to do some planning before you go ahead and start a charity it will help in achieving your goals, as well as identifying possible

Checklist Matters for consideration before you start a charity: Take some time to do some planning before you go ahead and start a charity it will help in achieving your goals, as well as identifying possible

Individual Tax Time. April Rules against Tax Avoidance. In-house fringe benefits FBT changes

Individual Tax Time April 2013 IN THIS ISSUE Rules against Tax Avoidance Changes to Tax Concessions Provided to Very High Income Earners In-house fringe benefits FBT changes Changes to the Australian Business

Individual Tax Time April 2013 IN THIS ISSUE Rules against Tax Avoidance Changes to Tax Concessions Provided to Very High Income Earners In-house fringe benefits FBT changes Changes to the Australian Business

2018 Tax Transparency Report

ABN 88 000 014 675 CONTENTS CHIEF FINANCIAL OFFICER S INTRODUCTION... 3 PART A... 4 A RECONCILIATION OF THE ACCOUNTING PROFIT TO INCOME TAX EXPENSE... 4 A RECONCILIATION FROM INCOME TAX EXPENSE TO CURRENT

ABN 88 000 014 675 CONTENTS CHIEF FINANCIAL OFFICER S INTRODUCTION... 3 PART A... 4 A RECONCILIATION OF THE ACCOUNTING PROFIT TO INCOME TAX EXPENSE... 4 A RECONCILIATION FROM INCOME TAX EXPENSE TO CURRENT

Taxwise Business News

Taxwise Business News In this Issue... FBT changes: salary packaged meal and other entertainment benefits Other FBT updates Car expense substantiation methods simplified Superannuation rates and thresholds

Taxwise Business News In this Issue... FBT changes: salary packaged meal and other entertainment benefits Other FBT updates Car expense substantiation methods simplified Superannuation rates and thresholds

BUSINESS NEWS. Welcome to the June 2018 Edition Of our PBD Business Newsletter. I trust the following items are informative and interesting.

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

APPLICATION FOR ADMISSION AS FELLOW

APPLICATION FOR ADMISSION AS FELLOW 1. Personal Details (please type or print in block letters) Title: Mr/Mrs/Miss/Ms... Family Name Given Names Firm/Company Name Business Address.... State. Postcode...

APPLICATION FOR ADMISSION AS FELLOW 1. Personal Details (please type or print in block letters) Title: Mr/Mrs/Miss/Ms... Family Name Given Names Firm/Company Name Business Address.... State. Postcode...

Business News June 2018

Business News June 2018 Federal Budget tax measures that may impact your business Small and medium sized businesses received a bit of attention from the Government in this year s 2018-19 Budget. Making

Business News June 2018 Federal Budget tax measures that may impact your business Small and medium sized businesses received a bit of attention from the Government in this year s 2018-19 Budget. Making

ABN and ACNC Registration Policy and Procedures for Private Schools

ABN and ACNC Registration Policy and Procedures for Private Schools Title ABN and ACNC Registration Policy and Procedures for Private Schools Creation Date Version Last Revised Reformatted 31 March 2014

ABN and ACNC Registration Policy and Procedures for Private Schools Title ABN and ACNC Registration Policy and Procedures for Private Schools Creation Date Version Last Revised Reformatted 31 March 2014

Northern Beaches College Business Services Apprentice to Business Owner Program (A to B Program) Structure & Legal s;

Structure & Legal s;") Structure & Legal s; The four main types of business structures commonly used by small businesses are: Sole trader: an individual trading on their own Partnership: an association of people or entities

Structure & Legal s; The four main types of business structures commonly used by small businesses are: Sole trader: an individual trading on their own Partnership: an association of people or entities

Taxwise Individual News

Taxwise Individual News In this Issue... Medicare Levy Surcharge and Private Health Insurance Rebate Superannuation guarantee rate Super contributions caps Changes to superannuation excess concessional

Taxwise Individual News In this Issue... Medicare Levy Surcharge and Private Health Insurance Rebate Superannuation guarantee rate Super contributions caps Changes to superannuation excess concessional

Tax return for individuals July 2011 to 30 June 2012

Use Individual tax return instructions 2012 to fill in this tax return n Print clearly using a black pen only n Use BLOCK LETTERS and print one character per box S M I T H S T Tax return for individuals

Use Individual tax return instructions 2012 to fill in this tax return n Print clearly using a black pen only n Use BLOCK LETTERS and print one character per box S M I T H S T Tax return for individuals

Capital allowances schedule instructions 2012

Instructions for taxpayers Capital allowances schedule instructions 2012 To help you complete your capital allowances schedule for 1 July 2011 30 June 2012 These instructions will help you complete your

Instructions for taxpayers Capital allowances schedule instructions 2012 To help you complete your capital allowances schedule for 1 July 2011 30 June 2012 These instructions will help you complete your

EOY Support Note # 5 Payment Summary Guide

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

Microsoft Dynamics GP. GST and Australian Taxes

Microsoft Dynamics GP GST and Australian Taxes Copyright Copyright 2010 Microsoft. All rights reserved. Limitation of liability This document is provided as-is. Information and views expressed in this

Microsoft Dynamics GP GST and Australian Taxes Copyright Copyright 2010 Microsoft. All rights reserved. Limitation of liability This document is provided as-is. Information and views expressed in this

Tax basics for small business

BUSINESS SMALL BUSINESS GUIDE NAT 1908-06.2006 SEGMENT AUDIENCE FORMAT PRODUCT ID Tax basics for small business Understanding your tax obligations and entitlements when running a small business. For more

BUSINESS SMALL BUSINESS GUIDE NAT 1908-06.2006 SEGMENT AUDIENCE FORMAT PRODUCT ID Tax basics for small business Understanding your tax obligations and entitlements when running a small business. For more

For NDIS Clients or clients with only WPNs and employee between 1-10 staff, do we need to start getting ready for STP?

Will there be a free program/software for STP use? The ATO has released an Expression of Interest (EOI) for providers in the market to create a no or low cost simple STP solution for small, but specifically

Will there be a free program/software for STP use? The ATO has released an Expression of Interest (EOI) for providers in the market to create a no or low cost simple STP solution for small, but specifically

September 2010 IN THIS ISSUE: ATO COMPLIANCE PROGRAM 2010/11 TARGET AREAS

September 2010 IN THIS ISSUE: ATO Compliance Program 20010/11 target areas Employee share schemes Unpaid present entitlements Trusts and Bamford GST Luxottica and refunds Continuing ATO support for businesses

September 2010 IN THIS ISSUE: ATO Compliance Program 20010/11 target areas Employee share schemes Unpaid present entitlements Trusts and Bamford GST Luxottica and refunds Continuing ATO support for businesses

Tax file number declaration

Instructions and form for taxpayers Tax file number declaration Information you provide in this declaration will allow your payer to This is not a TFN application form. ato.gov.au/tfn Terms we use When

Instructions and form for taxpayers Tax file number declaration Information you provide in this declaration will allow your payer to This is not a TFN application form. ato.gov.au/tfn Terms we use When

Fringe Benefits Tax. History

Fringe Benefits Tax Fringe benefits tax is a tax paid on certain benefits employers provide to their employees or their employee s associates (typically family members). FBT is separate from income tax

Fringe Benefits Tax Fringe benefits tax is a tax paid on certain benefits employers provide to their employees or their employee s associates (typically family members). FBT is separate from income tax

TaxWise Business News September 2018

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

FBT for NFPs. A practical guide for your FBT compliance

FBT for NFPs A practical guide for your FBT compliance Presented by Phil Turnour, Risk & Intelligence Manager, Australian Taxation Office / 6 April 2017 Session Overview Session Overview 1. Registering

FBT for NFPs A practical guide for your FBT compliance Presented by Phil Turnour, Risk & Intelligence Manager, Australian Taxation Office / 6 April 2017 Session Overview Session Overview 1. Registering

Taxable payments reporting for government entities

Taxable payments reporting for government entities Presented by Leassa Armstrong, Australian Taxation Office 22July 2016 Objective of today s presentation > The aim of today s session is to provide you

Taxable payments reporting for government entities Presented by Leassa Armstrong, Australian Taxation Office 22July 2016 Objective of today s presentation > The aim of today s session is to provide you

Activity statement and portal changes

Activity statement and portal changes Hosted by Colin Walker, Australian Taxation Office 20 July 2017 Overview Status update Portal activity statement functionality: changes and fixes based on your feedback

Activity statement and portal changes Hosted by Colin Walker, Australian Taxation Office 20 July 2017 Overview Status update Portal activity statement functionality: changes and fixes based on your feedback

TaxWise. Business News February Focus on small business. What the ATO is seeing in the small business market. To do!

TaxWise Business News February 2019 Focus on small business What the ATO is seeing in the small business market On 2 November 2018, the Deputy Commissioner of Small Business, Deborah Jenkins, delivered

TaxWise Business News February 2019 Focus on small business What the ATO is seeing in the small business market On 2 November 2018, the Deputy Commissioner of Small Business, Deborah Jenkins, delivered

STATUTORY DECLARATION BY SMSF TRUSTEE. We, both of

1 STATUTORY DECLARATION BY SMSF TRUSTEE We, both of (Full Name), (Address) make the following declaration under the Statutory Declarations Act 1959. 1. 1 We are the directors of ACN ( SMSF Trustee ) as

1 STATUTORY DECLARATION BY SMSF TRUSTEE We, both of (Full Name), (Address) make the following declaration under the Statutory Declarations Act 1959. 1. 1 We are the directors of ACN ( SMSF Trustee ) as

SMSF ADMINISTRATION SERVICE AGREEMENT

SMSF ADMINISTRATION SERVICE AGREEMENT About our SMSF Service Establishing and operating a self-managed super fund (SMSF) is an exciting and positive step in your lifelong financial journey. SMSFs however

SMSF ADMINISTRATION SERVICE AGREEMENT About our SMSF Service Establishing and operating a self-managed super fund (SMSF) is an exciting and positive step in your lifelong financial journey. SMSFs however

Tax file number declaration

Instructions and form for taxpayers Individuals Tax file number declaration The information you provide in this declaration will enable your payer to work out how much tax to withhold from payments made

Instructions and form for taxpayers Individuals Tax file number declaration The information you provide in this declaration will enable your payer to work out how much tax to withhold from payments made

ABN and ACNC Registration Policy and Procedures for Parish Missions

ABN and ACNC Registration Policy and Procedures for Parish Missions Title ABN and ACNC Registration Policy and Procedures for Parish Missions Creation Date Version Last Revised Reformatted 31 March 2014

ABN and ACNC Registration Policy and Procedures for Parish Missions Title ABN and ACNC Registration Policy and Procedures for Parish Missions Creation Date Version Last Revised Reformatted 31 March 2014

ASSOCIATION OF TAXATION AND MANAGEMENT ACCOUNTANTS CPD Policy what counts as CPD? The ATMA requires that a member undertake a minimum of 40 hours CPD in each calendar year of membership. Excess hours may

ASSOCIATION OF TAXATION AND MANAGEMENT ACCOUNTANTS CPD Policy what counts as CPD? The ATMA requires that a member undertake a minimum of 40 hours CPD in each calendar year of membership. Excess hours may

2016 Client Profile Form

2016 Client Profile Form (All new and existing clients to complete) / / CURRENT INFORMATION Preferred Name Title Given Name(s) Surname E-mail Address 1 E-mail Address 2 Address (physical) P.O. Box not

2016 Client Profile Form (All new and existing clients to complete) / / CURRENT INFORMATION Preferred Name Title Given Name(s) Surname E-mail Address 1 E-mail Address 2 Address (physical) P.O. Box not

keeping you informed winter 2016 IN THIS ISSUE

DFK Australia New Zealand Business & Taxation bulletin IN THIS ISSUE Small Business Benchmarks GIC & SIC Rates Foreign Residents Real Property Withholding Rules Family Assistance Payments Jobactive Subsidies

DFK Australia New Zealand Business & Taxation bulletin IN THIS ISSUE Small Business Benchmarks GIC & SIC Rates Foreign Residents Real Property Withholding Rules Family Assistance Payments Jobactive Subsidies

Medicare levy variation declaration

Instructions and form for taxpayers Medicare levy variation declaration WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the amount withheld from payments

Instructions and form for taxpayers Medicare levy variation declaration WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the amount withheld from payments

FRINGE BENEFITS FOR CHURCHES INDEX

FRINGE BENEFITS FOR CHURCHES Exempt Benefits and Fringe Benefits Tax INDEX 1. The FBT Act 1.1. The Basis for Exempt Benefits 1.2. Churches Responsibility 2. Tax Exempt Benefits 2.1. Remuneration Package

FRINGE BENEFITS FOR CHURCHES Exempt Benefits and Fringe Benefits Tax INDEX 1. The FBT Act 1.1. The Basis for Exempt Benefits 1.2. Churches Responsibility 2. Tax Exempt Benefits 2.1. Remuneration Package

Superannuation changes

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners and small businesses. On Tuesday 3 May,

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners and small businesses. On Tuesday 3 May,

TAX EXPRESS CHECKLIST FOR INDIVIDUAL TAX RETURN TAXEXPRESS 2018 INDIVIDUAL TAX RETURN CHECKLIST

TAXEXPRESS 2018 INDIVIDUAL TAX RETURN CHECKLIST Remember you only have to provide answers to those questions that are relevant to you, and by emailing /mailing/faxing documents to us (e.g. payment summary,

TAXEXPRESS 2018 INDIVIDUAL TAX RETURN CHECKLIST Remember you only have to provide answers to those questions that are relevant to you, and by emailing /mailing/faxing documents to us (e.g. payment summary,

Salary packaging handbook

Salary packaging handbook Exempt toyotafleetmanagement.com.au FLEET MANAGEMENT TRUSTED FIGURES IN FLEET Contents Introduction 3 What is salary packaging? 4 What items can be salary packaged? 5 Why salary

Salary packaging handbook Exempt toyotafleetmanagement.com.au FLEET MANAGEMENT TRUSTED FIGURES IN FLEET Contents Introduction 3 What is salary packaging? 4 What items can be salary packaged? 5 Why salary

Superannuation Contribution Splitting Application

Superannuation Contribution Splitting Application Thank you for your enquiry about splitting contributions in QIEC Super. Please read the information below and return the completed form to QIEC Super if

Superannuation Contribution Splitting Application Thank you for your enquiry about splitting contributions in QIEC Super. Please read the information below and return the completed form to QIEC Super if

Foreign resident capital gains withholding clearance certificate application

Foreign resident capital gains withholding clearance certificate application Completing this form print clearly in BLOCK LETTERS using a black or dark blue pen only fields marked with an asterisk (*) are

Foreign resident capital gains withholding clearance certificate application Completing this form print clearly in BLOCK LETTERS using a black or dark blue pen only fields marked with an asterisk (*) are

Statutory declaration

Statutory declaration MAKING A STATUTORY DECLARATION You can make a declaration if you are an individual person and the declaration relates to your own income tax return n Use a separate declaration for

Statutory declaration MAKING A STATUTORY DECLARATION You can make a declaration if you are an individual person and the declaration relates to your own income tax return n Use a separate declaration for

Personal Income Tax Return Year End Questionnaire 2016

Personal Income Tax Return Year End Questionnaire 2016 Client: Date: To assist us in preparing your income tax return, please use this questionnaire as a checklist when you compile your information. With

Personal Income Tax Return Year End Questionnaire 2016 Client: Date: To assist us in preparing your income tax return, please use this questionnaire as a checklist when you compile your information. With

Tax Brief. 23 March Indirect Tax Sharing Agreements. Limiting joint and several liability. Main effects of an ITSA

Tax Brief 23 March 2010 Indirect Tax Sharing Agreements From 1 July 2010, indirect tax sharing agreements (ITSAs) will become part of the GST landscape. Under the proposed measures, GST group members and

Tax Brief 23 March 2010 Indirect Tax Sharing Agreements From 1 July 2010, indirect tax sharing agreements (ITSAs) will become part of the GST landscape. Under the proposed measures, GST group members and

Self managed superannuation fund annual return instructions 2012

Instructions for superannuation funds Self managed superannuation fund annual return instructions 2012 To help you complete the self managed superannuation fund annual return for 1 July 2011 30 June 2012

Instructions for superannuation funds Self managed superannuation fund annual return instructions 2012 To help you complete the self managed superannuation fund annual return for 1 July 2011 30 June 2012

Completing the Auditor/actuary contravention report

Instructions for SMSF auditors and actuaries Completing the Auditor/actuary contravention report These instructions provide information about the reporting criteria and include examples to help you complete

Instructions for SMSF auditors and actuaries Completing the Auditor/actuary contravention report These instructions provide information about the reporting criteria and include examples to help you complete

Self managed superannuation fund annual return instructions 2011

Instructions for superannuation funds Self managed superannuation fund annual return instructions 211 To help you complete the self managed superannuation fund annual return for 1 July 21 3 June 211 For

Instructions for superannuation funds Self managed superannuation fund annual return instructions 211 To help you complete the self managed superannuation fund annual return for 1 July 21 3 June 211 For

TaxWise Business News September 2018

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

Tax (Financial) Adviser

Adviser") Tax (Financial) Adviser Start today 1300 738 955 5 star education experience Tax Practitioners Board approved courses Qualified trainers with extensive law and tax experience Engaging and carefully structured

Tax (Financial) Adviser Start today 1300 738 955 5 star education experience Tax Practitioners Board approved courses Qualified trainers with extensive law and tax experience Engaging and carefully structured

Rollover request. 1. Your account details. 2. Tax file number (TFN)

") Portfoliofocus - Premium Retirement Service Portfoliofocus - Essentials Super and Pension Service Rollover request Please read the Important information on page 6 before requesting your rollover. For withdrawals

Portfoliofocus - Premium Retirement Service Portfoliofocus - Essentials Super and Pension Service Rollover request Please read the Important information on page 6 before requesting your rollover. For withdrawals

Income Tax Basics 2012 Day 2. Overview...1

Contents Overview...1 1. The self-assessment system...1 1.1 Periods of review...2 2. Preparing the business return...3 2.1 Accounting records vs. tax records...3 2.2 Process for completing the business

Contents Overview...1 1. The self-assessment system...1 1.1 Periods of review...2 2. Preparing the business return...3 2.1 Accounting records vs. tax records...3 2.2 Process for completing the business

Part 5: GLOSSARY OF TERMS

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

AMMA STATEMENT GUIDE A Guide to your Cromwell Property Group (ASX:CMW) 30 June 2018 AMMA Statement

30 June 2018 AMMA Statement") AMMA STATEMENT GUIDE A Guide to your Cromwell Property Group (ASX:CMW) 30 June 2018 AMMA Statement The information in this Guide has been prepared to assist Australian resident individual holders of Cromwell

AMMA STATEMENT GUIDE A Guide to your Cromwell Property Group (ASX:CMW) 30 June 2018 AMMA Statement The information in this Guide has been prepared to assist Australian resident individual holders of Cromwell

We would like to TAX TIME 2018 CORNERSTONE

TAX TIME 2018 We would like to thank you for your continued custom and support over the past year. This has been a particularly difficult year firstly with Marian s radiation treatment over September and

TAX TIME 2018 We would like to thank you for your continued custom and support over the past year. This has been a particularly difficult year firstly with Marian s radiation treatment over September and

Superannuation changes

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners small businesses. On Tuesday 3 May,

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners small businesses. On Tuesday 3 May,